UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

For the quarterly period ended

For the transition period from ____________ to ____________

Commission File Number:

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (IRS Employer | |

| incorporation or organization) | Identification No.) |

People’s Republic of | ||

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act: None.

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Not Applicable | Not Applicable | Not Applicable |

Indicate by check mark whether the issuer (1)

filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or

for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for

the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of February 13, 2023, there were

TABLE OF CONTENTS

i

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

CHINA HEALTH INDUSTRIES HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

| December 31, 2022 (Unaudited) | June 30, 2022 (Audited) | |||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Accounts receivable, net | ||||||||

| Inventory | ||||||||

| Other receivables, net | ||||||||

| Advances to suppliers | ||||||||

| Prepayments | ||||||||

| Total current assets | $ | $ | ||||||

| Property, plants and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Construction in progress | ||||||||

| Prepayments – Non-Current | ||||||||

| Deferred tax assets | ||||||||

| Total assets | $ | $ | ||||||

| LIABILITIES AND EQUITY | ||||||||

| Current liabilities | ||||||||

| Accounts payable and accrued expenses | $ | $ | ||||||

| Other payables | ||||||||

| Advances from customers | ||||||||

| Related party debts | ||||||||

| Wages payable | ||||||||

| Taxes payable | ||||||||

| Total current liabilities | $ | $ | ||||||

| Equity | ||||||||

| Common stock, ($ | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated other comprehensive (loss) income | ( | ) | ||||||

| Statutory reserves | ||||||||

| Retained earnings | ||||||||

| Total stockholders’ equity | $ | $ | ||||||

| Total liabilities and equity | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

1

CHINA HEALTH INDUSTRIES HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

| For the Three Months Ended | For the Six Months Ended | |||||||||||||||

| December 31, 2022 | December 31, 2021 | December 31, 2022 | December 31, 2021 | |||||||||||||

| REVENUE | $ | $ | $ | $ | ||||||||||||

| COST OF GOODS SOLD | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| GROSS PROFIT | ( | ) | ( | ) | ||||||||||||

| OPERATING EXPENSES | ||||||||||||||||

| Selling, general and administrative expenses | ||||||||||||||||

| Depreciation and amortization expenses | ||||||||||||||||

| Total operating expenses | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| INCOME (LOSS) FROM OPERATIONS | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| OTHER INCOME/(EXPENSES) | ||||||||||||||||

| Interest income | ||||||||||||||||

| Interest expense | ||||||||||||||||

| Other income/(expenses), net | ( | ) | ||||||||||||||

| Bank charges | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Total other income, net | ( | ) | ||||||||||||||

| INCOME/(LOSS) BEFORE INCOME TAXES | ( | ) | ( | ) | ||||||||||||

| Provision for income taxes | ||||||||||||||||

| NET INCOME (LOSS) | ( | ) | ( | ) | ||||||||||||

| Foreign currency translation gain (loss) | ( | ) | ||||||||||||||

| COMPREHENSIVE INCOME (LOSS) | ( | ) | ( | ) | ( | ) | ||||||||||

| $ | $ | ( | ) | $ | $ | ( | ) | |||||||||

| Weighted average shares outstanding: | ||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

2

CHINA HEALTH INDUSTRIES HOLDINGS, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

FOR THE SIX MONTHS ENDED DECEMBER 31, 2022 AND

2021

(Unaudited)

| Common Shares | Additional Paid-in | Retained | Statutory | Accumulated Other Comprehensive Income | Total Stockholders’ | Non- controlling | Total | |||||||||||||||||||||||||||||

| Shares | Amount | Capital | Earnings | Reserve | (loss) | Equity | Interest | Equity | ||||||||||||||||||||||||||||

| Balance, June 30, 2021 | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Other comprehensive loss - Translation adjustment | - | |||||||||||||||||||||||||||||||||||

| Balance, December 31, 2021 | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||

| Balance, June 30, 2022 | ||||||||||||||||||||||||||||||||||||

| Net income | - | |||||||||||||||||||||||||||||||||||

| Other comprehensive loss - Translation adjustment | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | $ | $ | ( | ) | $ | $ | $ | ||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

CHINA HEALTH INDUSTRIES HOLDINGS, INC.

AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

FOR THE THREE MONTHS ENDED DECEMBER 31, 2022

AND 2021

(Unaudited)

| Common Shares | Additional Paid-in | Retained | Statutory | Accumulated Other Comprehensive Income | Total Stockholders’ | Non- controlling | Total | |||||||||||||||||||||||||||||

| Shares | Amount | Capital | Earnings | Reserve | (loss) | Equity | Interest | Equity | ||||||||||||||||||||||||||||

| Balance, September 30, 2021 | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||

| Net loss | - | ( | ) | ( | ) | ( | ) | |||||||||||||||||||||||||||||

| Other comprehensive loss - Translation adjustment | - | |||||||||||||||||||||||||||||||||||

| Balance, December 31, 2021 | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||

| Balance, September 30, 2022 | ( | ) | ||||||||||||||||||||||||||||||||||

| Net income | - | |||||||||||||||||||||||||||||||||||

| Other comprehensive loss - Translation adjustment | - | |||||||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | $ | $ | ( | ) | $ | $ | $ | ||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

CHINA HEALTH INDUSTRIES HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| For the Six Months Ended | ||||||||

| December 31, | December 31, | |||||||

| 2022 | 2021 | |||||||

| Cash Flows from Operating Activities | ||||||||

| Net income (loss) | $ | $ | ( | ) | ||||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | ||||||||

| Depreciation and amortization expenses | ||||||||

| Provisions for doubtful accounts | ( | ) | ||||||

| Deferred taxes loss/(gain) | ||||||||

| Changes in operating assets and liabilities, | ||||||||

| Accounts receivable | ||||||||

| Other receivables | ||||||||

| Inventory | ( | ) | ||||||

| Advances to suppliers and prepaid expenses | ( | ) | ||||||

| Accounts payables and accrued expenses | ( | ) | ( | ) | ||||

| Advances from customers and other payables | ( | ) | ||||||

| Amounts due to related parties | ( | ) | ||||||

| Wages payable | ( | ) | ( | ) | ||||

| Taxes payable | ||||||||

| Net cash provided by operating activities | ||||||||

| Cash Flows from Investing Activities | ||||||||

| Purchases of property, plants and equipment | ||||||||

| Expenditures in construction in progress | ||||||||

| Disposal of property, plant and equipment | ||||||||

| Net cash (used in)/provided by investing activities | ||||||||

| Cash Flows from Financing Activities | ||||||||

| Proceeds from related party debts | ||||||||

| Net cash (used in)/provided by financing activities | ||||||||

| Effect of exchange rate changes on cash and cash equivalents | ( | ) | ( | ) | ||||

| Net increase/(decrease) in cash and cash equivalents | ( | ) | ||||||

| Cash and cash equivalents, beginning balance | ||||||||

| Cash and cash equivalents, closing balance | ||||||||

| Supplemental cash flow information | ||||||||

| Cash paid for income taxes | $ | $ | ||||||

| Cash paid for interest expenses | $ | $ | ||||||

| Non-cash activities: | ||||||||

| Loan from related party for the construction of a facility | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

5

CHINA HEALTH INDUSTRIES HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Note 1 - ORGANIZATION AND BUSINESS BACKGROUND

China Health Industries Holdings, Inc. (“China Health US”) was incorporated in the State of Arizona on July 11, 1996 and was the successor of the business known as Arizona Mist, Inc. which began in 1989. On May 9, 2005, it entered into a stock purchase agreement and share exchange (effecting a reverse merger) with Edmonds 6, Inc. (“Edmonds 6”), a Delaware corporation, and changed its name to Universal Fog, Inc. Pursuant to this agreement, Universal Fog, Inc. (which has been in continuous operation since 1996) became a wholly-owned subsidiary of Edmonds 6.

China Health Industries Holdings Limited (“China Health HK”) was incorporated on July 20, 2007 in Hong Kong under the Companies Ordinance as a limited liability company. China Health HK was formed for the purpose of seeking and consummating a merger or acquisition with a business entity organized as a private corporation, partnership, or sole proprietorship as defined by FASB ACS Topic 915 (“Development Stage Entities”).

Harbin Humankind Biology Technology Co., Limited (“Humankind”) was incorporated in Harbin City, Heilongjiang Province, the People’s Republic of China (the “PRC”) on December 14, 2003, as a limited liability company under the Company Law of the PRC. Humankind is engaged in the manufacturing and sale of health products.

On August 20, 2007, the sole shareholder of China

Health HK entered into a share purchase agreement (the “Share Purchase Agreement”) with the owners of Humankind. Pursuant

to the Share Purchase Agreement, China Health HK purchased

On October 14, 2008, Humankind set up a

On December 31, 2008, China Health HK entered

into a reverse merger with Universal Fog, Inc., a U.S. publicly traded shell company (the “Transaction”). China Health HK

is the acquirer in the Transaction, and the Transaction has been treated as a recapitalization of China Health US.

On November 22, 2013, Humankind completed the

acquisition of Heilongjiang Huimeijia Pharmaceutical Co., Ltd. (“HLJ Huimeijia”) for a total purchase price of $

On December 24, 2014, Humankind entered into a

stock transfer agreement (the “Original Agreement”) with Xiuzheng Pharmaceutical Group Co., Ltd. a company incorporated under

the laws of the PRC and located in Jilin province (“Xiuzheng Pharmacy” or the “Buyer”), Mr. Xin Sun, the CEO of

the Company, and Huimeijia,

6

On February 9, 2015, the four parties to the Original

Agreement entered into a supplementary agreement (the “Supplementary Agreement”) to modify the terms of the Original Agreement,

pursuant to which the Equity Holders and Huimeijia (collectively the “Asset Transferors”) would sell only the 19 drug approval

numbers (including the tablet, capsule, powder, mixture, oral liquid, syrup and oral solution under the 19 approval numbers; licenses

including the original copies of Business License, Organization Code Certificate, Tax Registration Certificate, Drug Production Permit

and GMP Certificate, and other documents and original copies related to the production and operation of the 19 drugs) (the “Assets”)

to Xiuzheng Pharmacy. The Equity Holders would have retained their equity interests in Huimeijia, but would have pledged such equity interests

to Xiuzheng Pharmacy until the Assets were transferred, at which time the cash consideration would have been paid by the Buyer. Total

cash consideration would have been the same as under the Original Agreement, i.e., RMB

On October 12, 2016, the same four parties agreed

to rescind the Supplementary Agreement and entered into a new supplementary agreement (the “New Supplementary Agreement”),

pursuant to which the four parties agreed to execute the transfer of the equity interests based on the Original Agreement and the Equity

Holders agreed to sell their respective equity interests in Huimeijia to Xiuzheng Pharmacy. The transfer of

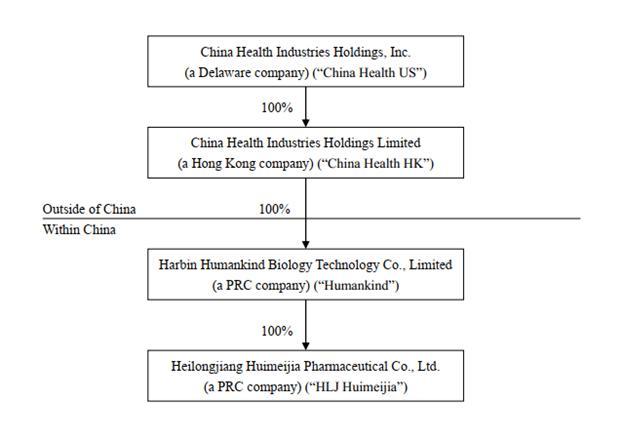

China Health US, China Health HK, Humankind and HLJ Huimeijia are collectively referred herein to as the “Company.”

As of December 31, 2022, the Company’s corporate structure was as follows:

7

Note 2 - SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

This summary of the Company’s significant accounting policies is presented to assist in understanding the Company’s financial statements. The financial statements and notes are representations of the Company’s management (“Management”), which is responsible for the integrity and objectivity of the financial statements and notes. These accounting policies conform to generally accepted accounting principles in the United States (“US GAAP”) and have been consistently applied in the preparation of the unaudited condensed consolidated financial statements.

The accompanying unaudited condensed consolidated

financial statements have been prepared by the Company without audit pursuant to the rules and regulations of the U.S. Securities and

Exchange Commission (“SEC”). Certain information and disclosures normally included in financial statements prepared in accordance

with US GAAP have been condensed or omitted as allowed by such rules and regulations, and Management believes that the disclosures are

sufficient so that the information presented is not misleading.

Principles of Consolidation

The accompanying unaudited condensed consolidated financial statements include China Health US and its three subsidiary companies, namely China Health HK, Humankind, and HLJ Huimeijia. All significant intercompany balances and transactions have been eliminated in consolidation and combination.

On November 22, 2013, China Health US, through its wholly owned subsidiary Humankind, completed the acquisition of HLJ Huimeijia. HLJ Huimeijia and Humankind were and are under the common control of Mr. Xin Sun, the CEO of China Health US, before and after the date of transfer. Humankind’s accounting policy adopted the guidance in ASC 805-50-05-5 for the transfer of net assets between entities under common control to apply an accounting method similar to the pooling-of-interests method. Under this method, the financial statements of Humankind shall report results of operations for the period in which the transfer occurs as though the transfer of net assets had occurred at the beginning of the period. Results of operations for that period will thus comprise both those of the previously separate entities combined from the beginning of the period to the date the transfer is completed and those of the combined operations from that date to the end of the period. Similarly, Humankind shall present statements of financial position and other financial information as of the beginning of the period as though the assets and liabilities had been transferred at that date. Financial statements and financial information of Humankind presented for prior years shall also be retrospectively adjusted to furnish comparative information.

Segment Reporting

FASB ASC Topic 280, “Segment Reporting,” established standards for reporting information about operating segments on a basis consistent with the Company’s internal organizational structure as well as information about geographical areas, business segments and major customers in financial statements for details on the Company’s business segments. The Company has three reportable operating segments: Humankind, HLJ Huimeijia and Others. The segments are grouped based on the types of products provided.

Fair Value of Financial Instruments

The provisions of accounting guidance, FASB ASC Topic 820 that applies to the Company requires all entities to disclose the fair value of financial instruments, both assets and liabilities recognized and not recognized on the balance sheet, for which it is practicable to estimate fair value, and defines fair value of a financial instrument as the amount at which the instrument could be exchanged in a current transaction between willing parties.

Fair Value Measurements

FASB ASC Topic 820, “Fair Value Measurements and Disclosures”, clarifies the definition of fair value for financial reporting, establishes a framework for measuring fair value, and requires additional disclosures about the use of fair value measurements.

Various inputs are considered when determining the fair value of the Company’s debt. The inputs or methodologies used for valuing securities are not necessarily an indication of the risk associated with investing in these securities. These inputs are summarized in the three broad levels listed below:

Level 1 – observable market inputs that are unadjusted quoted prices for identical assets or liabilities in active markets.

8

Level 2 – other significant observable inputs, including quoted prices for similar securities, interest rates, credit risk, etc.

Level 3 – significant unobservable inputs, including the Company’s own assumptions in determining the fair value of investments.

The carrying value of financial assets and liabilities recorded at fair value is measured on a recurring or a nonrecurring basis. Financial assets and liabilities measured on a non-recurring basis are those that are adjusted to fair value when a significant event occurs. The Company had no financial assets or liabilities carried and measured on a nonrecurring basis during the reporting periods. Financial assets and liabilities measured on a recurring basis are those that are adjusted to fair value each time a financial statement is prepared. The Company had no financial assets or liabilities carried and measured on a recurring basis during the reporting periods.

The availability of inputs observable in the market varies from instrument to instrument and depends on a variety of factors, including the type of instrument, whether the instrument is actively traded, and other characteristics particular to the transaction. For some financial instruments, pricing inputs are readily observable in the market, the valuation methodology used is widely accepted by market participants, and the valuation does not require significant discretion of Management. For other financial instruments, pricing inputs are less observable in the market and may require judgment of Management.

Translation of Foreign Currencies

Humankind, Huimeijia and HLJ Huimeijia maintain their books and accounting records in PRC currency “Renminbi” (“RMB”), which has been determined as the functional currency. The functional currency of China Health HK is the Hong Kong Dollar (“HKD”).

Transactions denominated in currencies other than the functional currencies are recorded at the exchange rates prevailing on the date of the transactions, as quoted by the Federal Reserve Board. Foreign currency exchange gains and losses resulting from these transactions are included in operations.

Humankind, Huimeijia, HLJ Huimeijia and China Health Hong Kong’s financial statements are translated into the reporting currency, the United States Dollar (“USD”). Assets and liabilities of the above entities are translated at the prevailing exchange rate at each reporting period end date. Contributed capital accounts are translated using the historical rate of exchange when capital is injected. Income and expense accounts are translated at the average rate of exchange during the reporting period. Translation adjustments resulting from the translation of these financial statements are reflected as accumulated other comprehensive income in shareholders’ equity and non-controlling interests.

Statement of Cash Flows

In accordance with Statement FASB ASC Topic 230, “Statement of Cash Flows”, cash flow from the Company’s operations is calculated based upon the local currencies and translated to the reporting currency using an average foreign exchange rate for the reporting period. As a result, amounts related to assets and liabilities reported in the statement of cash flows will not necessarily be the same as the corresponding balances on the balance sheets.

Use of Estimates and Assumptions

The preparation of financial statements in conformity with US GAAP requires Management to make estimates and judgments that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities on the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Management bases its estimates and judgments on historical experience and on various other assumptions and information that are believed to be reasonable under the circumstances. Estimates and assumptions of future events and their effects cannot be perceived with certainty and, accordingly, these estimates may change as new events occur, as more experience is acquired, as additional information is obtained, and as the Company’s operating environment changes. Significant estimates and assumptions by Management include, among others, useful life of long-lived assets and intangible assets, valuation of inventory, accounts receivable and notes receivable, impairment analysis of long-lived assets, construction in progress, intangible assets, and deferred taxes. While Management believes that the estimates and assumptions used in the preparation of the financial statements are appropriate, actual results could differ from those estimates. Estimates and assumptions are periodically reviewed and the effects of revisions are reflected in the financial statements in the period they are determined to be necessary.

9

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand, deposits in banks with maturities of three months or less, and all highly liquid investments which are unrestricted as to withdrawal or use and which have original maturities of three months or less at the time of purchase.

As of December 31, 2022 and June 30, 2022, the

Company’s uninsured bank balances were mainly maintained at financial institutions located in the PRC and Hong Kong. The uninsured

bank balances were $

Accounts Receivable

Accounts receivable is recorded at the invoiced

amount and do not bear interest. The Company extends unsecured credit to its customers in the ordinary course of business, but mitigates

the associated risks by performing credit checks and actively pursuing past due accounts. An allowance for doubtful accounts is established

and determined based on Management’s assessment of known requirements, aging of receivables, payment and bad debt history, the customer’s

current credit worthiness, changes in customer payment patterns and the economic environment. From November 1, 2013, the Company changed

its credit policy by offering ninety (90) day payment terms for sales agents. As of December 31, 2022 and June 30, 2022, the balances

of accounts receivable were $

Advances to Suppliers

The Company periodically makes advances to certain

vendors for purchases of raw materials or to service providers for services relating to construction plans for its plants, equipment and

production lines for Good Manufacturing Practice (“GMP”) upgrading, and records these payments as advances to suppliers. As

of December 31, 2022 and June 30, 2022, advances to suppliers amounted to $

Inventory

Inventory consists of raw materials, work in progress, and finished goods or manufactured products.

Inventory is stated at the lower of either cost or market value and consists of materials, labor and overhead. HLJ Huimeijia uses the weighted average method for inventory valuation. Other subsidiaries of the Company use the first-in, first-out (“FIFO”) method for inventory valuation. Overhead costs included in finished goods include direct labor costs and other costs directly applicable to the manufacturing process. The Company evaluates inventory for excess, slow moving, and obsolete inventory, as well as inventory the value of which is in excess of its net realizable value. This evaluation includes analysis of sales levels by product and projections of future demand. If future demand or market conditions are less favorable than the Company’s projections, a write-down of inventory may be required, and would be reflected in cost of goods sold in the period the revision is made. The inventory allowance in the amounts of $ and $ were provided for as of December 31, 2022 and June 30, 2022, respectively.

Impairment of Long-Lived Assets

The Company’s long-lived assets and other assets are reviewed for impairment in accordance with the guidance of the FASB ASC Topic 360-10, “Property, Plant, and Equipment”, and FASB ASC Topic 205, “Presentation of Financial Statements”. The Company tests for impairment losses on long-lived assets used in operations whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable. Recoverability of an asset to be held and used is measured by a comparison of the carrying amount of the asset to the future undiscounted cash flows expected to be generated by the asset. If such asset is considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the asset exceeds its fair value. Impairment evaluations involve Management’s estimates on asset useful life and future cash flows. Actual useful life and cash flows could be different from those estimated by Management, which could have a material effect on the Company’s reporting results and financial position. Fair value is determined through various valuation techniques including discounted cash flow models, quoted market values, and third-party independent appraisals, as considered necessary. As of December 31, 2022 and June 30, 2022, the Company had not experienced impairment losses on its long-lived assets. However, there can be no assurances that demand for the Company’s products or services will continue, which could result in an impairment of long-lived assets in the future.

10

Property, Plants and Equipment

Property, plants and equipment are carried at the lower of either cost or fair value. Maintenance, repairs and minor renewals are expensed as incurred, and major renewals and improvements that extend the life or increase the capacity of plant assets are capitalized.

When assets are retired or disposed of, the cost and accumulated depreciation are removed from the accounts and any resulting gains or losses are included in the results of operations in the reporting period of disposition.

Depreciation is calculated on a straight-line basis over the estimated useful life of the assets. The depreciable lives applied are:

| Buildings, Warehouses and Improvements | ||

| Office Equipment | ||

| Vehicles | ||

| Machinery and Equipment |

Intangible Assets

The Company evaluates intangible assets in accordance with FASB ASC Topic 350, “Intangibles — Goodwill and Other”. Intangible assets deemed to have indefinite life are not amortized, but are subject to annual impairment tests. If the assumptions and estimates used to allocate the purchase price are not correct, or if business conditions change, purchase price adjustments or future asset impairment charges could be required. The value of the Company’s intangible assets could be impacted by future adverse changes such as: (i) any future declines in the Company’s operating results, (ii) a decline in the valuation of technology, including the valuation of the Company’s common stock, (iii) a significant slowdown in the worldwide economy, or (iv) any failure to meet the performance projections included in the Company’s forecasts of future operating results. In accordance with FASB ASC Topic 350, the Company tests intangible assets for impairment on an annual basis or more frequently if the Company believes indicators of impairment exist. Impairment evaluations involve Management’s estimates of asset useful life and future cash flows. Significant judgment of Management is required in the forecasts of future operating results that are used in the evaluations. It is possible, however, that the plans and estimates used may be incorrect. If the Company’s actual results, or the plans and estimates used in future impairment analysis, are lower than the original estimates used to assess the recoverability of these assets, the Company could incur additional impairment charges in a future period. Based on such evaluations, there was no impairment recorded for intangible assets, for the six months ended December 31, 2022 and 2021, respectively.

Construction in Progress

Construction in progress represents the costs incurred in connection with the construction of buildings or new additions to the Company’s plant facilities. Costs classified as construction in progress include all costs of obtaining the asset and bringing it to the location and condition necessary for its intended use. No depreciation is provided for construction in progress until such time as the assets are completed and are placed into service.

The Company reviews the carrying value of construction in progress for impairment whenever events and circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value of the assets, an impairment loss is recognized equal to an amount by which the carrying value exceeds the fair value of the assets. The factors considered by Management in performing this assessment include current operating results, trends and prospects, the manner in which the property is used, and the effects of obsolescence, demand, competition, and other economic factors. Based on this assessment, there was no impairment recorded for construction in progress, for the six months ended December 31, 2022 and 2021, respectively. However, there can be no assurances that demand for the Company’s products or services will continue, which could result in an impairment of long-lived assets in the future.

11

Revenue Recognition

The Company recognizes revenue in the amount to which it expects to be entitled when control of the products or services is transferred to its customers based on any contract. Control is generally transferred when the Company has a present right to payment and title and the significant risks and rewards of ownership of products or services are transferred to its customers while performance obligation are completed. For most of the Company’s products net sales, control transfers when products are shipped and transaction price are determined. The majority of the Company’s revenue relates to the sale of inventory to customers, and revenue is recognized when control of the products or services is transferred to its customers that reflects the performance obligations are properly allocated and satisfied with transaction price. Given the nature of the Company’s business and the applicable rules guiding revenue recognition, the Company’s revenue recognition practices do not contain estimates that materially affect the results of operations. The Company records revenue at the discounted selling price and allows its customers to return products for exchange or credit subject to certain limitations. A provision for such returns is recorded based upon historical experience. There has been no provision recorded for returns based upon historical experience for the six months ended December 31, 2022 and 2021, respectively.

Cost of Goods Sold

Cost of goods sold consists primarily of the costs of raw materials, freight charges, direct labor, depreciation of plants and machinery, warehousing and overhead costs associated with the manufacturing process, and commission expenses.

Income Taxes

The Company adopts FASB ASC Topic 740 (“ASC 740”), “Income Taxes,” which requires the recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the financial statements or tax returns. Under this method, deferred income taxes are recognized for the tax consequences in future years of differences between the tax bases of assets and liabilities and their financial reporting amounts at each period end based on enacted tax laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. A valuation allowance is established for deferred tax assets if it is more likely than not that these items will either expire before the Company is able to realize the benefits or that future deductibility is uncertain.

Under ASC 740, a tax position is recognized as a benefit only if it is “more likely than not” that the tax position would be sustained in a tax examination, with a tax examination being presumed to occur. The evaluation of a tax position is a two-step process. The first step is to determine whether it is more-likely-than-not that a tax position will be sustained upon examination, including the resolution of any related appeals or litigations based on the technical merits of that position. The second step is to measure a tax position that meets the more-likely-than-not threshold to determine the amount of benefit to be recognized in the financial statements. A tax position is measured at the largest amount of benefit that is greater than 50 percent likely of being realized upon ultimate settlement. Tax positions that previously failed to meet the more-likely-than-not recognition threshold should be recognized in the first subsequent period in which the threshold is met. Previously recognized tax positions that no longer meet the more-likely-than-not criteria should be de-recognized in the first subsequent financial reporting period in which the threshold is no longer met. Penalties and interest incurred related to underpayment of income tax are classified as income tax expense in the year incurred. GAAP also provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods, disclosures and transition.

As a result of the implementation of FIN 48 (ASC 740-10), the Company undertook a comprehensive review of its portfolio of tax positions in accordance with recognition standards established by FIN 48 (ASC 740-10). The Company recognized no material adjustments to liabilities or stockholders’ equity as a result of the implementation. The adoption of FIN 48 did not have a material impact on the Company’s financial statements.

The application of tax laws and regulations is subject to legal and factual interpretation, judgment and uncertainty. Tax laws and regulations themselves are subject to changes as a result of changes in fiscal policy, changes in legislation, the evolution of regulations and court rulings. Therefore, the actual liability may be materially different from the Company’s estimates, which could result in the need to record additional tax liabilities or potentially reverse previously recorded tax liabilities or deferred tax asset valuation allowance.

12

Enterprise Income Tax

Under the PRC Enterprise Income Tax Law, (the

“EIT Law”), income tax is payable by enterprises at a rate of

Value Added Tax

The Provisional Regulations of the PRC Concerning Value Added Tax promulgated by the State Council came into effect on January 1, 1994, and revised on January 1, 2009. Under the regulations and the Implementing Rules of the PRC Concerning Value Added Tax, value added tax (“VAT”) is imposed on goods sold in, or imported into, the PRC and on processing, repair and replacement services provided within the PRC.

VAT payable in the PRC is charged on an aggregated

basis at a rate of

Sales-Related Taxes

Pursuant to the tax law and regulations of the

PRC, the Company is obligated to pay

Concentrations of Business and Credit Risks

All of the Company’s manufacturing is located in the PRC. There can be no assurance that the Company will be able to successfully continue to manufacture its products and failure to do so would have a material adverse effect on the Company’s financial position, results of operations and cash flows. Moreover, the success of the Company’s operations is subject to numerous contingencies, some of which are beyond management’s control. These contingencies include general economic conditions, prices of raw materials, competition, governmental and political conditions, and changes in regulations. Since the Company is dependent on trade in the PRC, the Company is subject to various additional political, economic and other uncertainties. Among other risks, the Company’s operations will be subject to the risks of restrictions on transfer of funds, domestic customs, changing taxation policies, foreign exchange restrictions, and political and governmental regulations. The Company operates in China, which may give rise to significant foreign currency risks from fluctuations and the degree of volatility of foreign exchange rates between USD and the Chinese currency RMB. The results of operations denominated in foreign currency are translated at the average rate of exchange during the reporting periods.

Earnings Per Share

Basic earnings per common share are computed by dividing net earnings applicable to common shareholders by the weighted-average number of common shares outstanding during the period. When applicable, diluted earnings per common share is determined using the weighted-average number of common shares outstanding during the period, adjusted for the dilutive effect of common stock equivalents, consisting of shares that might be issued upon exercise of common stock options and warrants. For the six months ended December 31, 2022 and 2021, the Company had no potential dilutive common stock equivalents outstanding.

Potential common shares issued are calculated using the treasury stock method, which recognizes the use of proceeds that could be obtained upon the exercise of options and warrants in computing diluted earnings per share. It assumes that any proceeds would be used to purchase common stock at the average market price of the common stock during the period.

FASB ASC Topic 260, “Earnings Per Share”, requires a reconciliation of the numerator and denominator of the basic and diluted earnings per share (EPS) computations.

13

Recent Accounting Pronouncements

In June 2016, the FASB issued ASU 2016-13, Financial Instruments-Credit Losses (Topic 326) – Measurement of Credit Losses on Financial Instruments (ASU 2016-13). The main objective of the standard is to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. In issuing this standard, the FASB is responding to criticism that today’s guidance delays recognition of credit losses. The standard will replace today’s “incurred loss” approach with an “expected loss” model. The new model, referred to as the current expected credit loss (“CECL”) model, will apply to: (1) financial assets subject to credit losses and measured at amortized cost, and (2) certain off-balance sheet credit exposures. The standard is applicable to loans, accounts receivable, trade receivables, and other financial assets measured at amortized cost, loan commitments and certain other off-balance sheet credit exposures, debt securities (including those held-to-maturity) and other financial assets measured at fair value through other comprehensive income, and beneficial interests in securitized financial assets. The CECL model does not apply to available-for-sale debt securities. For available-for-sale debt securities with unrealized losses, entities will measure credit losses in a manner similar to what they do today, except that the credit losses will be recognized as allowances rather than reductions in the amortized cost of the securities. Accordingly, the new methodology will be utilized when assessing the Company’s financial instruments for impairment. As a result, entities will recognize improvements to estimated credit losses immediately in earnings rather than as interest income over time, as they do today. The ASU also simplifies the accounting model for purchased credit-impaired debt securities and loans. ASU 2016-13 also expands the disclosure requirements regarding an entity’s assumptions, models, and methods for estimating the allowance for loan and lease losses. ASU 2016-13 is effective for years beginning after December 15, 2019, including interim periods within those fiscal years under a modified retrospective approach. Early adoption is permitted for the periods beginning after December 15, 2018. The Company adopted the guidance from July 1, 2020. The Company finalized its analysis and determined that the adoption of this guidance has no material impact on the Company’s consolidated financial statements and its internal controls over financial reporting.

In August 2018, the FASB issued ASU 2018-13, Fair Value Measurement (Topic 820) – Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement (ASU 2018-13), which modifies the disclosure requirements on fair value measurements, including removing the requirement to disclose (1) the amount of and reasons for transfers between Level 1 and Level 2 of the fair value hierarchy, (2) the policy for timing of transfers between levels and (3) the valuation processes for Level 3 fair value measurements. ASU 2018-13 also added new disclosures including the requirement to disclose (a) the changes in unrealized gains and losses for the period included in other comprehensive income for recurring Level 3 fair value measurements held at the end of the reporting period and (b) the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements. ASU 2018-13 is effective for fiscal years (and interim reporting periods within those years) beginning after December 15, 2019 and early adoption is permitted. This standard will only impact the disclosures pertaining to fair value measurements. The Company adopted the guidance from July 1, 2020. The Company finalized its analysis and determined that the adoption of this guidance has no material impact on the Company’s consolidated financial statements and its internal controls over financial reporting.

NOTE 3 - ACCOUNTS RECEIVABLE

The Company’s accounts receivable were $

NOTE 4 - INVENTORY

Inventory consisted of following:

| December 31, | June 30, | |||||||

| 2022 | 2022 | |||||||

| Raw Materials | $ | $ | ||||||

| Supplies and Packing Materials | ||||||||

| Work-in-Progress | ||||||||

| Finished Goods | ||||||||

| Total | $ | $ | ||||||

The inventory allowance in the amounts of $ and $ was provided for as of December 31, 2022 and June 30, 2022, respectively.

14

NOTE 5 - CONSTRUCTION IN PROGRESS

Construction in progress from the continuing operations of the Company consisted of the following:

| December 31, | June 30, | |||||||

| 2022 | 2022 | |||||||

| Plant - HLJ Huimeijia | $ | $ | ||||||

| Total | $ | $ | ||||||

On April 6, 2012, HLJ Huimeijia entered into an agreement with a contractor

for construction of the HLJ Huimeijia plant. The estimated total cost of construction was approximately $

NOTE 6 - PROPERTY, PLANTS AND EQUIPMENT

Property, plants and equipment consisted of the following:

| December 31, | June 30, | |||||||

| 2022 | 2022 | |||||||

| Building, Warehouses and Improvements | $ | $ | ||||||

| Machinery and Equipment | ||||||||

| Office Equipment | ||||||||

| Vehicles | ||||||||

| Others | ||||||||

| Less: Accumulated Depreciation | ( | ) | ( | ) | ||||

| Total | $ | $ | ||||||

Depreciation expenses were $

NOTE 7 - INTANGIBLE ASSETS

The following is a summary of intangible assets from the continuing operations of the Company:

| December 31, 2022 | June 30, 2022 | |||||||

| Land Use Rights – Humankind | $ | $ | ||||||

| Health Supplement Product Patents – Humankind | ||||||||

| Pharmaceutical Patents - HLJ Huimeijia | ||||||||

| Land Use Rights - HLJ Huimeijia | ||||||||

| Less: Accumulated Amortization | ( | ) | ( | ) | ||||

| Total | $ | $ | ||||||

All land in the PRC belongs to the government

of the PRC. Enterprises and individuals can pay the PRC government a fee to obtain the right to use a piece of land for commercial purposes

or residential purposes for an initial period of

Amortization expenses were $

15

NOTE 8 - RELATED PARTY DEBTS

Related party debts, which represent temporary short-term loans from Mr. Xin Sun and Mr. Kai Sun, consisted of the following:

| December 31, 2022 | June 30, 2022 | |||||||

| Mr. Xin Sun | $ | $ | ||||||

| Mr. Kai Sun | ||||||||

| Total | $ | $ | ||||||

These loans are unsecured, non-interest bearing, and have no fixed terms of repayment; therefore, they are deemed payable on demand. Mr. Kai Sun is a PRC citizen and a family member of Mr. Xin Sun, the CEO of the Company.

NOTE 9 - INCOME TAXES

(a) Corporate income taxes

United States

China Health US was organized in the United States.

China Health US had no taxable income for US income tax purposes for the six months ended December 31, 2022 and 2021. As of December 31,

2022, China Health US had a

Hong Kong

China Health HK was incorporated in Hong Kong and is subject to Hong Kong taxation on its activities conducted in Hong Kong and income arising in or derived from Hong Kong. No provision for income taxes have been made because China Health HK has no taxable income in Hong Kong.

People’s Republic of China

Under the EIT Law, the standard EIT rate is

The provision for income taxes of the Company consisted of the following for the six months ended December 31, 2022 and 2021:

| For the Three Months Ended | For the Six Months Ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||

| Current provision: | ||||||||||||||||

| USA | $ | $ | $ | $ | ||||||||||||

| PRC | ( | ) | ||||||||||||||

| Total current provision | ( | ) | ||||||||||||||

| Deferred provision: | - | - | - | - | ||||||||||||

| USA | ||||||||||||||||

| PRC | ||||||||||||||||

| Total deferred provision | ||||||||||||||||

| Total provision for income taxes | $ | $ | ( | ) | $ | $ | ||||||||||

16

Significant components of deferred tax assets of the Company were as follows:

| December 31, | June 30, | |||||||

| 2022 | 2022 | |||||||

| Deferred tax assets | ||||||||

| Net operating loss carry forward | $ | $ | ||||||

| Allowances for doubtful accounts | ( | ) | ( | ) | ||||

| Valuation allowance | ( | ) | ( | ) | ||||

| Total | $ | $ | ||||||

(b) Uncertain tax positions

There were no unrecognized tax benefits as of December 31, 2022 and June 30, 2022. Management does not anticipate any potential future adjustments in the next twelve months which would result in a material change to its tax positions. For the six months ended December 31, 2022 and 2021, the Company did not incur any interest or penalties arising from its tax payments.

NOTE 10 – EARNINGS (LOSS) PER SHARE

Basic earnings (loss) per common share are computed by dividing net earnings applicable to common shareholders by the weighted-average number of common shares outstanding during the period. When applicable, diluted earnings (loss) per common share is determined using the weighted-average number of common shares outstanding during the period, adjusted for the dilutive effect of common stock equivalents, consisting of shares that might be issued upon exercise of common stock options and warrants. For the six months ended December 31, 2022 and 2021, the Company had no potential dilutive common stock equivalents outstanding.

Potential common shares issued are calculated using the treasury stock method, which recognizes the use of proceeds that could be obtained upon the exercise of options and warrants in computing dilutive earnings per share. It assumes that any proceeds would be used to purchase common stock at the average of the market price of the common stock during the period.

FASB ASC Topic 260, Earnings Per Share, requires a reconciliation of the numerator and denominator of the basic and diluted earnings per share (EPS) computations.

For the six months ended December 31, 2022 and 2021, the Company did not have potential dilutive shares. The following table sets forth the computation of basic and diluted net income per share:

| For the Three Months Ended | For the Six Months Ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| 2022 | 2021 | 2022 | 2021 | |||||||||||||

| Net income/(loss) attributable to China Health Industries Holdings | $ | $ | ( | ) | $ | $ | ( | ) | ||||||||

| Net income/(loss) per share: | ||||||||||||||||

| $ | $ | ( | ) | $ | ( | ) | ||||||||||

| Weighted average shares outstanding: | ||||||||||||||||

17

NOTE 11 - COMMITMENTS AND CONTINGENCIES

The Company’s assets are located in the PRC and revenues are derived from operations in the PRC.

In terms of industry regulations and policies, the economy of the PRC has been transitioning from a planned economy to market-oriented economy. Although in recent years the Chinese government has implemented measures emphasizing the utilization of market forces for economic reforms, the reduction of state ownership of productive assets and the establishment of sound corporate governance in business enterprises, a substantial portion of productive assets in the PRC is still owned by the Chinese government. For example, all land is state owned and leased to business entities or individuals through the government’s granting of land use rights. The granting process is typically based on government policies at the time of granting and can be lengthy and complex. This process may adversely affect the Company’s future manufacturing expansions. The Chinese government also exercises significant control over the PRC’s economic growth through the allocation of resources and provides preferential treatment to particular industries or companies. Uncertainties may arise with changing governmental policies and measures.

The Company faces a number of risks and challenges not typically associated with companies in North America and Western Europe, since its assets are located solely in the PRC, and its revenues are derived from its operations therein. The PRC is a developing country with an early stage market economic system, overshadowed by the state. Its political and economic systems are very different from the more developed countries and are in transition. The PRC also faces many social, economic and political challenges that may lead to major shocks, instabilities and even crises, in both its domestic arena and in its relationships with other countries, including the United States. Such shocks, instabilities and crises may in turn significantly and negatively affect the Company’s performance.

The Company had no rental commitment as of December 31, 2022.

NOTE 12 - MAJOR SUPPLIERS AND CUSTOMERS

For the six months ended December 31, 2022,

the Company had only

For the six months ended December 31, 2022, the

Company had only

18

NOTE 13 - SEGMENT REPORTING

The Company is organized into the following

The following tables present summary information by segment for the three and six months ended December 31, 2022 and 2021, respectively:

| For the Three Months Ended December 31, 2022 | For the Three Months Ended December 31, 2021 | |||||||||||||||||||||||||||||||

| HLJ | HLJ | |||||||||||||||||||||||||||||||

| Huimeijia | Humankind | Others | Consolidated | Huimeijia | Humankind | Others | Consolidated | |||||||||||||||||||||||||

| Revenues | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||

| Cost of revenues | ||||||||||||||||||||||||||||||||

| Gross profit (loss) | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| Interest income(expense) | ||||||||||||||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||||||||||||||

| Income tax | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| Net income (loss) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||||||||||

| Total capital expenditures | ||||||||||||||||||||||||||||||||

| Total assets | $ | $ | $ | $ | $ | $ | $ | ( | ) | $ | ||||||||||||||||||||||

| For the Six Months Ended December 31, 2022 | For the Six Months Ended December 31, 2021 | |||||||||||||||||||||||||||||||

| HLJ | HLJ | |||||||||||||||||||||||||||||||

| Huimeijia | Humankind | Others | Consolidated | Huimeijia | Humankind | Others | Consolidated | |||||||||||||||||||||||||

| Revenues | $ | $ | $ | $ | $ | |||||||||||||||||||||||||||

| Cost of revenues | ||||||||||||||||||||||||||||||||

| Gross profit (loss) | ( | ) | ( | ) | ||||||||||||||||||||||||||||

| Interest income | ||||||||||||||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||||||||||||||

| Income tax | ||||||||||||||||||||||||||||||||

| Net income (loss) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||||||||||||||

| Total capital expenditures | ||||||||||||||||||||||||||||||||

| Total assets | $ | $ | $ | $ | ( | ) | $ | |||||||||||||||||||||||||

NOTE 14 - SUBSEQUENT EVENTS

The Company has evaluated subsequent events from the balance sheet date through the date the financial statements were issued and determined that there are no additional items to disclose.

19

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

FORWARD LOOKING STATEMENTS

We make certain forward-looking statements in this report. Statements concerning our future operations, prospects, strategies, financial condition, future economic performance (including growth and earnings), demand for our services, and other statements of our plans, beliefs, or expectations, including the statements contained under this caption as well as under captions elsewhere in this document, are forward-looking statements. In some cases, these statements are identifiable through the use of words such as “anticipate”, “believe”, “estimate”, “expect”, “intend”, “plan”, “project”, “target”, “can”, “could”, “may”, “should”, “will”, “would”, and similar expressions. The forward-looking statements we make are not guarantees of future performance and are subject to various assumptions, risks, and other factors that could cause actual results to differ materially from those suggested by these forward-looking statements. These risks and uncertainties, together with the other risks described from time to time in reports and documents that we file with the SEC should be considered in evaluating forward-looking statements. Because such statements are subject to risks and uncertainties, actual results may differ materially from those expressed or implied by the forward-looking statements. Indeed, it is likely that some of our assumptions will prove to be incorrect. Our actual results and financial position will vary from those projected or implied in the forward-looking statements and the variances may be material. You are cautioned not to place undue reliance on such forward-looking statements, which reflect our view only as of the date of this report.

Important factors that could cause actual results to differ from those in the forward-looking statements include, without limitation, the following:

| ● | the effect of political conditions, economic conditions, market conditions, and geopolitical events; | |

| ● | legislative and regulatory changes that affect our business; | |

| ● | the availability of funds and working capital; and | |

| ● | the actions and initiatives of current and potential competitors. |

Except as required by applicable laws, regulations, or rules, we do not undertake any responsibility to publicly release any revisions to these forward-looking statements to take into account events or circumstances that occur after the date of this report. Additionally, we do not undertake any responsibility to update you on the occurrence of any unanticipated events which may cause actual results to differ from those expressed or implied by any forward-looking statements.

The following discussion and analysis should be read in conjunction with our unaudited condensed consolidated financial statements and the related notes thereto as filed with the SEC and other financial information contained elsewhere in this report.

Except as otherwise indicated by the context, references in this report to “we”, “us”, “our”, “the Registrant”, “our Company”, or “the Company” are to China Health Industries Holdings, Inc., a Delaware corporation, China Health Industries Holdings Limited, a limited liability company incorporated under the laws of Hong Kong, its wholly owned subsidiary in China, Harbin Humankind Biology Technology Co. Limited (“Humankind”), and indirect wholly owned subsidiary, Heilongjiang Huimeijia Pharmaceutical Co., Ltd. (“HLJ Huimeijia”). Unless the context otherwise requires, all references to (i) the “PRC” and “China” are to the People’s Republic of China; (ii) “U.S. dollar,” “$” and “US$” are to United States dollars; (iii) “RMB” are to Renminbi Yuan of China; (iv) “Securities Act” are to the Securities Act of 1933, as amended; and (v) “Exchange Act” are to the Securities Exchange Act of 1934, as amended.

20

Business Overview

Our principal business operations are conducted through our wholly-owned subsidiaries, Humankind and HLJ Huimeijia.

The Company owns a GMP-certified plant and production facilities and has the capacity to produce 21 different NMPA-approved medicines, 14 NMPA-approved health supplement products and 8 hemp derivative products in soft capsule, hard capsule, tablet, granule, and oral liquid forms. These products address the needs of some key sectors in China, including the feminine, geriatric, and children’s markets.

HLJ Huimeijia was founded on October 30, 2003 and its latest GMP certificate is effective until April 24, 2023. HLJ Huimeijia engages in the manufacture and distribution of tincture, ointments, rubber paste, including hormones, topical solution, suppositories, enemas, oral liquids, and liniment, including traditional Chinese medicine extractions. HLJ Huimeijia’s predecessor was Heilongjiang Xue Du Pharmaceutical Co., Ltd., which established brand recognition in the market through its supply of high-quality drug products. HLJ Huimeijia is a “high and new technology” enterprise that provides the most comprehensive types of topical medical products in Heilongjiang Province, a northeastern province of China.

We have developed the following products that are derived from hemp and obtained business license to manufacture and sell these products. We began to sell these products since May 2018. Hemp Oil, Hemp Protein Powder, Hemp Polypeptide and Collagen Peptide are sold through Humankind, other cosmetics are sold through HLJ Huimeijia. The revenue of the Hemp Seed Beer accounted for 100.00% and 0.00% for the six-month periods ended December 31, 2022 and 2021, respectively.

| Serial No. | Name | |

| 1 | Hemp Oil | |

| 2 | Hemp Protein Powder | |

| 3 | Hemp Polypeptide | |

| 4 | Collagen Peptide | |

| 5 | Natural Hemp Essence Repair Lotion | |

| 6 | Natural Hemp Revitalizing Essence | |

| 7 | Natural Hemp Anti-aging Brightening Eye Cream | |

| 8 | Natural Hemp Frozen Age Nourishing Cream | |

| 9 | Hemp Seed Beer |

Our business model is to sell our products directly to end customers through our own sales personnel as well as our sales agents, operating primarily in Anhui, Zhejiang, Shanghai, Jiangsu, Beijing and Gansu, where most of our revenues are used to be generated. Because of the “Transformation of the Company”, we sold a little of our product to sales agents for the six months ended December 31, 2022. Humankind is using existing materials to research and develop hemp related products. Humankind decided to transform the primary business to Cannabidiol (“CBD”) extractive project, following the government’s guidance in expanding the use of hemps into cosmetics, food, or daily uses. The Company will also receive the government’s sponsorship in R&D expenses to support the company research in CBD aspect. However, by the end of fiscal year 2022, the support guidelines had not been published. As the Chinese government has officially stopped the zero-case policy, we expect the CBD extractive project to start generating revenue and finally balance our investment in the hemp related products by 2024 (“Transformation”).

21

Results of Operations

Three months ended December 31, 2022 compared to the three months ended December 31, 2021

The following table summarizes the top lines of the results of our operations for the three months ended December 31, 2022 and 2021, respectively:

| December 31, | December 31, | |||||||||||||||

| 2022 | 2021 | Variance | % | |||||||||||||

| Revenues | $ | 32,650 | $ | 2 | $ | 32,648 | 100.00 | % | ||||||||

| Humankind | 32,650 | - | 32,650 | 100.00 | % | |||||||||||

| HLJ Huimeijia | - | 2 | (2 | ) | (100.00 | )% | ||||||||||

| Cost of Goods Sold | $ | 29,645 | $ | 11 | $ | 29,634 | 100.00 | % | ||||||||

| Humankind | 29,645 | - | 29,645 | 100.00 | % | |||||||||||

| HLJ Huimeijia | - | 11 | (11 | ) | (100.00 | )% | ||||||||||

| Gross Profit | $ | 3,005 | $ | (9 | ) | $ | 3,014 | 100.00 | % | |||||||

| Humankind | 3,005 | - | 3,005 | 100.00 | % | |||||||||||

| HLJ Huimeijia | - | (9 | ) | 9 | (100.00 | )% | ||||||||||

Revenue

Total revenues increased by $32,648 or 100.00% for the three months ended December 31, 2022, as compared to the same period in 2021. The increase in revenues was primarily due to an increase of $32,650 in Humankind’s revenues for the three months ended December 31, 2022 as compared to the same period in 2021. The increase in Humankind’s sales revenues was primarily derived from selling a new product, Hemp Seed Beer, in the three months ended December 31, 2022.

Our total cost of goods sold increased by $29,634 or 100.00% for the three months ended December 31, 2022 as compared to the same period in 2021. The increase in Humankind’s cost of goods sold was primarily derived from cost on selling a new product, Hemp Seed Beer, in the three months ended December 31, 2022.

Our gross margin increased by $3,014 for the three months ended December 31, 2022 as compared to the same period in 2021. This change was consistent with the change of sales and costs in HLJ Huimeijia and Humankind. The increase is mainly derived from selling a new product Hemp Seed Beer, in the three months ended December 31, 2022.

Sales by Product Line

The following table summarizes a breakdown of our sales by major product lines for the three months ended December 31, 2022 and 2021 respectively:

| December 31, 2022 | December 31, 2021 | |||||||||||||||||||||||

| Quantity | % of | Quantity | % of | |||||||||||||||||||||

| (Unit) | Sales US $ | Sales | (Unit) | Sales US $ | Sales | |||||||||||||||||||

| Humankind | ||||||||||||||||||||||||

| Hemp Oil | - | - | -% | - | - | - | % | |||||||||||||||||

| Collagen Peptide | - | - | -% | - | - | - | % | |||||||||||||||||

| Hemp Polypeptide | - | - | -% | - | - | - | % | |||||||||||||||||

| Hemp Protein Powder | - | - | -% | - | - | - | % | |||||||||||||||||

| Hemp Seed Beer | 6,456 | 32,650 | 100.00 | % | - | - | - | % | ||||||||||||||||

| HLJ Huimeijia | ||||||||||||||||||||||||

| Muskiness Bone Strengthener Paste | - | - | -% | - | - | - | % | |||||||||||||||||

| Dampness dispelling pain ointment | - | - | -% | - | - | - | % | |||||||||||||||||

| Refining Cream dogskin | - | - | -% | - | - | - | % | |||||||||||||||||

| Indometacin and Furazolidone Suppositories | - | - | -% | - | - | - | % | |||||||||||||||||

| ShangBiTongDing | - | - | -% | - | - | - | % | |||||||||||||||||

| Total | 6,456 | 32,650 | 100.00 | % | - | $ | - | - | % | |||||||||||||||

22

Operating Expenses

The following table summarizes our operating expenses for the three months ended December 31, 2022 and 2021, respectively:

December 31, | December 31, | Variance | % | |||||||||||||

| Operating Expenses | ||||||||||||||||

| Selling, general and administrative | $ | 223,473 | $ | 92,586 | $ | 130,887 | 141.37 | % | ||||||||

| Depreciation and amortization | 192,365 | 180,012 | 12,353 | 6.86 | % | |||||||||||

| Total Operating Expenses | $ | 415,838 | $ | 272,598 | $ | 143,240 | 52.55 | % | ||||||||

Total operating expenses for the three months ended December 31, 2022 were $143,240 or 52.55% higher than those in the corresponding period in 2021. The increase in operating expenses was primarily attributable to an increase of $130,887 or 141.37% in selling, general and administrative expenses. The increase in selling, general and administrative expenses was mainly due to the expired destruction of inventory.

Interest Income and Interest Expense

Interest income was $26,046 for the three months ended December 31, 2022, as compared to $40,598 for the three months ended December 31, 2021. This decrease of $14,552, or 36%, was mainly due to the decreased average balance of bank deposits compared with the same period of 2021. This decline in bank balances was mainly due to the effects of currency translation difference from RMB to USD during the periods and normal daily operating expenses payment.

Interest expense was $nil for the three months ended December 31, 2022 and $nil for the three months ended December 31, 2021.

Income Taxes

Income taxes was $nil for the three months ended December 31, 2022 as compared to $107,057 tax credit for the three months ended December 31, 2021. The decrease of tax credit was primarily due to the increase of net profits before income taxes.

23

Net Income (loss) and Net Income (loss) Per Share

Net Income was $929,303 for the three months ended December 31, 2022, as compared to $573,524 net loss for the three months ended December 31, 2021. This increase of $1,502,827 in net income was primarily due to the transfer of one of Huimeijia’s production technique. Such transfer would not affect future production.

Net income per share was $0.0142 for the three months ended December 31, 2022 and $0.0088 net loss per share for the three months ended December 31, 2021, respectively. This increase was primarily a result of the aforementioned increase in net profit.

Six months ended December 31, 2022 compared to the six months ended December 31, 2021

The following table summarizes the top lines of the results of our operations for the six months ended December 31, 2022 and 2021, respectively:

| December 31, | December 31, | |||||||||||||||

| 2022 | 2021 | Variance | % | |||||||||||||

| Revenues | $ | 32,650 | $ | 268 | $ | 32,382 | 100.00 | % | ||||||||

| Humankind | 32,650 | - | 32,650 | 100.00 | % | |||||||||||

| HLJ Huimeijia | - | 268 | (268 | ) | (100.00 | )% | ||||||||||

| Cost of Goods Sold | $ | 29,645 | $ | 1,755 | $ | 27,890 | 100.00 | % | ||||||||

| Humankind | 29,645 | - | 29,645 | 100.00 | % | |||||||||||

| HLJ Huimeijia | - | 1,755 | (1,755 | ) | (100.00 | )% | ||||||||||

| Gross Profit | $ | 3,005 | $ | (1,487 | ) | $ | 4,492 | (100.00 | )% | |||||||

| Humankind | 3,005 | - | 3,005 | 100.00 | % | |||||||||||

| HLJ Huimeijia | - | (1,487 | ) | (1,487 | ) | 100.00 | % | |||||||||

Revenue

Total revenues increased by $32,382 or 100.00% for the six months ended December 31, 2022, as compared to the same period in 2021. The increase in revenues was primarily caused by an increase of $32,650 in Humankind’s revenues for the six months ended December 31, 2022 as compared to the same period in 2021. The increase in Humankind’s sales revenues was primarily derived from selling a new product, Hemp Seed Beer, in the six months ended December 31, 2022.

Our total cost of goods sold increased by $27,890 or 100.00% for the six months ended December 31, 2022 as compared to the same period in 2021. This increase was mainly derived from cost on selling a new product, Hemp Seed Beer, in the six months ended December 31, 2022.

Our gross margin increased by $4,492 or 100.00% for the six months ended December 31, 2022 as compared to the same period in 2021. This change was consistent with the change of sales and costs in Humankind. The increase in gross profit was primarily derived from selling a new product, Hemp Seed Beer, in the six months ended December 31, 2022.

24

Sales by Product Line

The following table summarizes the breakdown of our sales by major product lines for the six months ended December 31, 2022 and 2021 respectively:

| December 31, 2022 | December 31, 2021 | |||||||||||||||||||||||

| Quantity | % of | Quantity | % of | |||||||||||||||||||||

| (Unit) | Sales US$ | Sales | (Unit) | Sales US$ | Sales | |||||||||||||||||||

| Humankind | ||||||||||||||||||||||||

| Hemp Oil | - | - | - | % | - | - | - | % | ||||||||||||||||

| Collagen Peptide | - | - | - | % | - | - | - | % | ||||||||||||||||

| Hemp Polypeptide | - | - | - | % | - | - | - | % | ||||||||||||||||

| Hemp Protein Powder | - | - | - | % | - | - | - | % | ||||||||||||||||

| Hemp Seed Beer | 6,456 | 32,650 | 100.00 | % | - | - | - | % | ||||||||||||||||

| HLJ Huimeijia | ||||||||||||||||||||||||

| Muskiness Bone Strengthener Paste | - | - | - | % | 223 | 18 | 6.87 | % | ||||||||||||||||

| Dampness dispelling pain ointment | - | - | - | % | 1,852 | 153 | 57.05 | % | ||||||||||||||||

| Refining Cream dogskin | - | - | - | % | 788 | 65 | 24.28 | % | ||||||||||||||||

| Indometacin and Furazolidone Suppositories | - | - | - | % | 383 | 32 | 11.80 | % | ||||||||||||||||

| ShangBiTongDing | - | - | - | - | - | - | % | |||||||||||||||||

| Enema Glycerini and Essence repair liquid | - | - | - | - | - | - | % | |||||||||||||||||

| Total | 6,456 | 32,650 | 100.00 | % | 3,246 | $ | 268 | 100.00 | % | |||||||||||||||

Operating Expenses

The following table summarizes our operating expenses for the six months ended December 31, 2022 and 2021, respectively:

December 31, | December 31, | Variance | % | |||||||||||||

| Operating Expenses | ||||||||||||||||

| Selling, general and administrative | $ | 558,319 | $ | 347,659 | $ | 210,660 | 60.59 | % | ||||||||

| Depreciation and amortization | 348,242 | 359,962 | (11,720 | ) | (3.26 | )% | ||||||||||

| Total Operating Expenses | $ | 906,561 | $ | 707,621 | $ | 198,940 | 28.11 | % | ||||||||

Total operating expenses for the six months ended December 31, 2022 were $198,940 or 28.11% higher than those in the same period in 2021. The increase in operating expenses was primarily attributable to increase of $210,660 or 60.59% in selling, general and administrative expenses. The increase in selling, general and administrative expenses was mainly due to the expired destruction of inventory.

Interest Income and Interest Expense

Interest income was $60,529 for the six months ended December 31, 2022, as compared to $81,632 for the six months ended December 31, 2021. This decrease of $21,103, or 26%, was mainly due to the decreased average balance of bank deposits compared with the same period of 2021. This decline in bank balances was mainly due to the effects of currency translation difference from RMB to USD during the periods and normal daily operating expenses payment.

Interest expense was $nil and $nil for the six months ended December 31, 2022 and for the six months ended December 31, 2021.

Income Taxes

Income taxes was $nil for the six months ended December 31, 2022 and $nil for the six months ended December 31, 2021.

25

Net Income and Net Income Per Share

Net income was $472,858 for the six months ended December 31, 2022, as compared to $594,911 net loss for the six months ended December 31, 2021. This increase of $1,067,769 in net income was primarily attributable to the transfer of one of Huimeijia’s production technique. Such transfer would not affect future production.

Net income per share was $0.0072 for the six months ended December 31, 2022 and net loss per share was $0.0091 for the six months ended December 31, 2021, respectively. This increase was primarily a result of the aforementioned increase in net profit.

Liquidity and Capital Resources

We believe our current working capital position, together with our expected future cash flows from operations and loans from our major shareholder, will be adequate to fund our operations in the ordinary course of business, anticipated capital expenditures, debt payment requirements, and other contractual obligations for at least the next twelve months. However, this belief is based upon many assumptions and is subject to numerous risks, and there can be no assurance that we will not require additional funding in the future.

The following table summarizes our cash and cash equivalents positions, our working capital, and our cash flow activities as of December 31, 2022 and June 30, 2022 and for the six months ended December 31, 2022 and 2021:

| December 31, 2022 | June 30, 2022 | |||||||

| Cash and cash equivalents | $ | 43,169,488 | $ | 44,789,999 | ||||

| Working capital | $ | 37,372,363 | $ | 37,652,693 | ||||

| Inventories | $ | 419,437 | $ | 521,229 | ||||

| For the Six Months ended December 31, | ||||||||

| 2022 | 2021 | |||||||

| Cash provided by (used in): | ||||||||

| Operating activities | $ | 512,196 | $ | 2,799,172 | ||||

| Investing activities | $ | - | $ | - | ||||

| Financing activities | $ | - | $ | - | ||||

For the six months ended December 31, 2022, our net decrease in cash and cash equivalents totaled $ 1,620,511, which total was comprised of net cash provided by operating activities in the amount of $512,196 and the negative effect of prevailing exchange rates on our cash position of $2,132,707.

Our working capital as of December 31, 2022 was $37,372,363, compared to working capital of $37,652,693 as of June 30, 2022. This decrease of $280,330 or 1% was primarily attributable to the decrease of cash and cash equivalents in the amount of $1,620,511, decrease of inventory in the amount of $101,792, which offset by the decrease of advance from customers in the amount of $298,071 and a decrease of amount due to related parties in the amount of $ 1,089,149.

26