Pioneer Floating Rate Trust

| Annual Report | November 30, 2020 |

| Ticker Symbol: PHD |

Beginning in or after February 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Trust’s shareholder reports like this one will no longer be sent by mail,

unless you specifically request paper copies of the reports from the Trust or from your financial intermediary, such as a broker-dealer, bank or insurance company. Instead, the reports will be made available on the Trust’s website, and you

will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by

this change and you need not take any action. You may elect to receive shareholder reports and other communications electronically by contacting your financial intermediary or, if you invest directly with the Trust, by calling 1-800-710-0935.

You may elect to receive all future reports in paper free of charge. If you invest directly with the Trust, you can inform the Trust that you wish to continue receiving paper copies of your shareholder reports by calling 1-800-710-0935. If you

invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your

account if you invest through your financial intermediary or all funds held within the Pioneer Fund complex if you invest directly.

visit us: www.amundi.com/us

| | |

Pioneer Floating Rate Trust | Annual Report | 11/30/20 1

With a very turbulent 2020 calendar year finally behind us, the U.S. and global economies still face numerous challenges as the

new calendar year dawns. The COVID-19 pandemic has continued to spread, with high numbers of new cases reported in many U.S. states and in other countries. In response, some governments have retightened restrictions on both business and personal

activities. However, as 2021 arrived, deployment of the first approved COVID-19 vaccines had already begun, and expectations are for widespread vaccine distribution by the middle of the year.

While there may

finally be a light visible at the end of the pandemic tunnel, the long-term impact on the global economy from COVID-19, while currently unknown, is likely to be considerable. It is clear that several industries have already felt greater effects than

others, and the markets, which do not thrive on uncertainty, have been volatile, delivering significantly negative performance in the first quarter of 2020, and then recovering most of those losses throughout the following quarters. In fact, the

U.S. stock market, as measured by the Standard & Poor’s 500 Index, returned more than 18% for the full 2020 calendar year, an impressive performance given all of the obstacles market participants faced during those 12 months.

However, despite the market rebound since its March 2020 low point, volatility has remained elevated, with momentum rising and falling on seemingly every bit of positive or negative news about the virus, from

vaccines to spikes in the number of cases as well as rising hospitalization rates in some areas. In addition, the recent U.S. Presidential and Congressional elections have resulted in a power shift in Washington, D.C., and that most likely portends

some changes in fiscal policy. That, too, could lead to increased market volatility as investors analyze the various tax and spending plans, and wait to see what proposed policy alterations actually become law.

With the advent of COVID-19 last winter, we implemented our business continuity plan according to the new COVID-19 guidelines, and most of our employees have been working remotely since March. To date, our operating

environment has faced no interruption. I am proud of the careful planning that has taken place and confident we can maintain this environment for as long as is prudent. History in the making for a company that first opened its doors way back in

1928.

2 Pioneer Floating Rate Trust | Annual Report | 11/30/20

Since 1928, Amundi US’s investment process has been built on a foundation of

fundamental research and active management, principles which have guided our investment decisions for more than 90 years. We believe active management – that is, making active investment decisions – can help mitigate the risks during

periods of market volatility. As 2020 has reminded us, investment risk can arise from a number of factors in today’s global economy, including slower or stagnating growth, changing U.S. Federal Reserve policy, oil price shocks, political and

geopolitical factors and, unfortunately, major public health concerns such as a viral pandemic.

At Amundi US, active management begins with our own fundamental, bottom-up research process. Our team of dedicated

research analysts and portfolio managers analyzes each security under consideration, communicating directly with the management teams of the companies issuing the securities and working together to identify those securities that best meet our

investment criteria for our family of funds. Our risk management approach begins with each and every security, as we strive to carefully understand the potential opportunity, while considering any and all risk factors.

Today, as investors, we have many options. It is our view that active management can serve shareholders well, not only when markets are thriving, but also during periods of market stress.

As you consider your long-term investment goals, we encourage you to work with your financial professional to develop an investment plan that paves the way for you to pursue both your short-term and long-term

goals.

We remain confident that the current crisis, like others in human history, will pass, and we greatly appreciate the trust you have placed in us and look forward to continuing to serve you in the

future.

Sincerely,

Lisa M. Jones

Head of the Americas, President and CEO of US.

Amundi Asset Management US, Inc.

January 2021

Head of the Americas, President and CEO of US.

Amundi Asset Management US, Inc.

January 2021

Any information in this

shareowner report regarding market or economic trends or the factors influencing the Trust’s historical or future performance are statements of opinion as of the date of this report. Past performance is no guarantee of future results.

Pioneer Floating Rate Trust | Annual Report | 11/30/20 3

In the following interview, Jonathan Sharkey discusses the factors that influenced

the performance of Pioneer Floating Rate Trust during the 12-month period ended November 30, 2020. Mr. Sharkey, a senior vice president and a portfolio manager at Amundi Asset Management US, Inc. (Amundi US), is responsible for the day-to-day

management of the Trust.

Q How did the Trust perform during the 12-month period ended November 30, 2020?

A Pioneer Floating Rate Trust returned 1.89% at net asset value (NAV) and 9.96% at market price during the 12-month period ended November

30, 2020. Please note that, during the period, the Trust announced a tender offer that commenced on November 23, 2020 (see note 11). The Trust’s benchmark, the Standard & Poor’s/Loan Syndications & Trading Association Leveraged

Loan Index (the S&P/LSTA Index), returned 3.38% at NAV. Unlike the Trust, the S&P/LSTA Index does not use leverage. While the use of leverage increases investment opportunity, it also increases investment risk.

During the same 12-month period, the average return at NAV of the 52 closed end funds in Morningstar’s Bank Loan Closed End Funds category (which may or may not be leveraged), was 0.65%, and

the average return at market price of the closed end funds in the same Morningstar category was -2.35%.

The shares of the Trust were selling at a 3.9% discount to NAV on November 30, 2020.

Comparatively, the shares of the Trust were selling at a 12.1% discount to NAV on May 31, 2020.

The Trust’s standardized, 30-day SEC yield was 3.76% on November 30, 2020*.

Q How would you describe the investment environment for investing in bank loans during the 12-month period ended November 30, 2020?

A As the period opened in December 2019, the loan market experienced muted demand in an environment of heightened investor risk-aversion

driven by ongoing geopolitical uncertainties, trade war tensions, and concerns about the pace of global economic growth. Mutual funds investing in bank loans continued to experience significant outflows as retail investors responded to the limited

near-term prospect of rising short-term

* The 30-day SEC yield is a standardized formula that is based on the hypothetical annualized earning power (investment

income only) of the Trust’s portfolio securities during the period indicated.

4 Pioneer Floating Rate Trust | Annual Report |

11/30/20

interest rates, given accommodative monetary policy from the

Federal Reserve System (Fed). Lower-quality loans, in particular, experienced a headwind from a technical-demand perspective. Specifically, managers of collateralized loan obligations (CLOs), which have typically absorbed the bulk of new issuance,

had become increasingly wary of deals in the “B-” rating category, due to the risk of downgrades; CLOs are subject to risk guidelines and typically have had quite limited ability to accommodate loans in the “CCC” rating

category. In the early part of the 12-month period, we did see significant refinancing to lower yields among higher-quality loans, given their ratings attractiveness for CLOs.

Beginning in

mid-February 2020, the impact of the COVID-19 virus, which first emerged in China but quickly became a pandemic, began to drive performance in the financial markets. Global economies ground to a near halt during March as public health concerns led

to the rapid implementation by governments and businesses of extreme measures focused on virus containment. Oil prices also plummeted in response to slumping global demand resulting from the spread of COVID-19 as well as a supply shock spurred by a

price war launched on March 8 between Saudi Arabia and Russia.

In the financial markets, uncertainty over the scope and duration of the pandemic crisis as well as investors’ need for

cash drove sell-offs across most asset classes and a flight-to-safety trade that drove U.S. Treasury yields to historic lows. Bank loan and high-yield corporate bond prices declined sharply in price as the outlook shifted from growth to recession

and investors anticipated a spike in defaults. The Trust’s benchmark, the S&P/LSTA Leveraged Loan Index, declined by 12.37% in March, the second-steepest monthly loss in the history of that index. Volatility in the secondary loan market

spiked to all-time highs, with March seeing both the worst and best single-day returns in the history of the loan market. March also saw a record volume of loan ratings downgrades, largely concentrated within lower-quality loans.

The unprecedented shutting down of much of the economy due to COVID-19 spurred extraordinary monetary and fiscal policy responses. First, the Fed jumped into action by dusting off its 2008/2009

policy “playbook” and rapidly rolling out a raft of programs aimed at restoring market liquidity, facilitating credit availability, and boosting investors’ confidence. The measures included reducing the benchmark federal funds

rate’s target range to near zero and committing to making purchases of a broad range of fixed-income assets. On the fiscal side, as March drew to a close, the U.S. government passed a $2.2 trillion stimulus bill, followed

Pioneer Floating Rate Trust | Annual Report | 11/30/20 5

weeks later by another aid package worth nearly $500 billion,

highlighted by support for small businesses. After volatility in the markets subsided, the three-month London Interbank Offered Rate (LIBOR), which is used to reset loan rates, eventually fell more in line with the federal funds rate, declining from

190 basis points (bps) in November 2019 to 22 bps at the end of the 12-month period, thus putting pressure on the dividend yields of loan funds. (A basis point is equal to 1/100th of a percentage point.)

The unprecedented scope and rapidity of the response from policy makers allowed the markets for riskier assets to regain the ground lost in the immediate aftermath of the COVID-19 shutdowns. The

leveraged loan secondary market rebounded in April, with the S&P/LSTA Index gaining 4.50%, its best one-month return in more than 10 years. Loans continued to post positive returns through November, although the pace of gains eased as the

12-month period progressed.

Loans finished the 12-month period in comfortably positive territory. Within the loan market, the oil & gas, gaming & leisure, consumer products, and air

transportation segments lagged, while telecommunications, technology, pharmaceuticals, and food products held up relatively well, as those sectors felt fewer negative effects from the COVID-19-related lockdowns and other virus-containment

measures.

Q What factors had the biggest effects on the Trust’s performance relative to the benchmark during the 12-month period ended November

30, 2020?

A The Trust’s allocations across various sectors of the loan market contributed positively overall to relative

performance during the 12-month period; however, negative security selection results more than offset the benefits of sector allocations. In that vein, as conditions deteriorated during the first quarter of 2020, we further emphasized higher-quality

loans within the below-investment-grade loan universe when selecting the portfolio’s positions. The bias towards better quality acted as a constraint on the Trust’s benchmark-relative performance as investors’ appetites for riskier

assets returned in the second quarter of 2020.

In industry terms, selection results within telecommunication services detracted from the Trust’s benchmark-relative performance. Within

the sector, a position in wireline company Windstream was a notable underperformer for the Trust, as Windstream filed for bankruptcy protection. Despite the Trust’s underweight to leisure versus the benchmark, allocations to the sector proved

to be the second-largest

6 Pioneer Floating Rate Trust | Annual Report | 11/30/20

detractor from relative returns for the 12-month period given

the impact of COVID-19 on gym attendance, with portfolio holdings such as 24 Hour Fitness filing for bankruptcy, and large chain LA Fitness requiring additional equity and government support to remain in business. Within energy, the

portfolio’s exposure to oilfield services firms, specifically a bond position in FTS International, which filed for bankruptcy, and midstream holdings such as Summit Midstream, weighed on the Trust’s benchmark-relative results due to the

significant sell-off in the oil market, which began prior to the COVID-19 outbreak. A slight overweight to aerospace/air transport, historically a fundamentally sound industry, also hurt the Trust’s performance as the economic outlook turned

recessionary. Portfolio positions within the segment that were notable laggards during the 12-month period included the bonds of WESCO (aircraft supply chain and components) and Wencor (commercial airline parts manufacturer). Although

technology/electronics exposure was a strong contributor to the Trust’s absolute performance, a modest underweight to the industry detracted from benchmark-relative returns as market sentiment with respect to technology-oriented companies held

up relatively well, supported in part by the work-from-home trend driven by COVID-19.

On the positive side, security selection results within, and an overweight to the health care sector

aided the Trust’s performance, as the portfolio’s holdings were generally able to navigate the pandemic environment successfully and benefited from governmental support. Positive contributions to relative returns within the health care

sector were led by a position in Team Health, a physician outsourcing/staffing company. Selection results within mining & metals also aided the Trust’s performance during the 12-month period. A bond position in iron ore producer Cleveland

Cliffs was a specific positive performance contributor in that sector. A significant portfolio overweight to autos was another positive for the Trust’s performance, as a shutdown in manufacturing coupled with fiscal stimulus provided to

consumers led to a strong rebound in demand. Auto parts restocking also benefited companies such as portfolio holding IXS, while investor sentiment with respect to truck and marine chassis manufacturer Drive Chassis improved along with the recovery

in inter-modal freight shipping during the 12-month period, and aided the Trust’s performance. Other individual portfolio names that made notable positive contributions to the Trust’s performance during the period included West Corp., an

operator of call centers, pharmaceutical company Endo Pharmaceutical, cloud computing company Rackspace, truck and engine manufacturer Navistar International, and outdoor sporting goods company Bass Pro Shops.

Pioneer Floating Rate Trust | Annual Report | 11/30/20 7

With regard to non-benchmark holdings, the Trust’s modest

exposure to high-yield corporate bonds constituted a drag on performance relative to the S&P/LSTA Index during the 12-month period. Within finance, a portfolio position in aircraft lessor Aviation Capital had a negative impact on relative

returns as the pandemic weighed on sentiment with respect to the company’s bonds. Another detractor from performance was Diamond Sports, a regional sports network spun out into Sinclair Broadcasting Group in order to facilitate Disney’s

acquisition of 21st Century Fox. Diamond Sports saw the outlook for its debt deteriorate with the absence of sports-related content for several months, due to COVID-19 containment measures. (The Trust had no exposure to Sinclair, Disney, or 21st

Century Fox as of November 30, 2020.)

With respect to the remainder of the Trust’s off-benchmark exposures, allocations to private label collateralized mortgage obligations and

commercial mortgage-backed securities detracted from relative returns during the 12-month period, while holdings of insurance-linked securities, which are sponsored by property-and-casualty insurers to help mitigate the impact of claims payouts in

the wake of natural disasters, benefited the Trust’s performance.

Finally, the Trust’s exposure to index-based credit-default-swap contracts, which we have utilized to maintain

the portfolio’s exposure to credit, and also to provide liquidity as a buffer to help manage leverage, positively affected the Trust’s performance during the 12-month period.

Q How did the level of leverage in the Trust change over the 12-month period ended November 30, 2020?

A The Trust employs leverage through a revolving credit facility.

As of

November 30, 2020, 27.6% of the Trust’s total managed assets were financed by leverage (or borrowed funds), compared with 32.3% of the Trust’s total managed assets financed by leverage at the start of the period on November 30, 2019.

During the 12-month period, the Trust decreased the absolute amount of funds borrowed by a total of $34 million, to $105 million as of November 30, 2020. The Trust decreased the amount of funds borrowed in connection with a tender offer which

commenced on November 23, 2020 (see Note 11). The percentage of the Trust’s managed assets financed by leverage decreased during the 12-month period due to the decrease in the amount of funds borrowed by the Trust.

8 Pioneer Floating Rate Trust | Annual Report | 11/30/20

Q Did the Trust have any

investments in any derivative securities during the 12-month period ended November 30, 2020? If so, did the derivatives have any material effect on results?

A The Trust had some exposure to high-yield corporate bonds and investment-grade corporate bonds through index-based credit-default-swap securities during the 12-month period, which we employed principally to help

maintain liquidity in the portfolio. The use of these derivatives aided performance by allowing the Trust to gain tactical credit exposure, while maintaining liquidity.

Q Did the Trust’s distributions** to shareholders change during the 12-month period ended November 30, 2020?

A The Trust’s distributions began the 12-month period at $0.0625 per share/per month, declined slightly in the middle of the

period, but had recovered back up to $0.0625 per share/per month by the end of the period on November 30, 2020.

Q What is your investment

outlook?

A The default rate in the loan market for the 12-month period ended November 30, 2020, was 3.89% by loan volume, above the

historical average of slightly over 3%, but below the six-year high of 4.17% that we saw in September. The default rate by number of issuers in the market was 4.27%, also above the long-term average, but representing a decline versus the 10-year

high of 4.64%, also in September. The default rate on loans held in the Trust’s portfolio has remained below that of the market by loan volume and by number of issuers, given our bias toward higher-quality holdings.

Expectations for loan defaults going forward have become less extreme compared with estimates during the pandemic-induced sell-off period. Many companies within the industries that have experienced

the biggest negative effects of the pandemic, such as movie theaters, fitness centers, and cruise lines, have been able to maintain liquidity by issuing bonds. The gaming sector has rebounded strongly, while the airline industry has benefited from a

$25 billion Congressional rescue package.

Our base scenario is that continued support from policymakers in conjunction with the approval and distribution of one or more COVID-19 vaccines

could promote a continued, gradual economic recovery in 2021, which in turn may lead to a decline in loan-default rates back to their long-term averages. Despite the rebound in loan valuations that we saw

**

Distributions are not guaranteed.

Pioneer Floating Rate Trust | Annual Report | 11/30/20 9

over the second quarter of 2020, our view is that loan spreads,

at current levels, more than account for default risk, and that loan prices have the potential to support capital appreciation going forward. (Loan spreads are the interest rates over and above the LIBOR rate charged to borrowers by banks.)

The Fed’s zero-interest-rate policy has put downward pressure on the LIBOR reference rate as well as the Trust’s income generation. While LIBOR troughed during the most recent 12-month

period, we have seen the new-issue loan calendar come with LIBOR floors to help offset the low reference rates.

In this challenging environment, we have continued to maintain a focus on

quality, and on the careful evaluation of the individual loans held in the Trust’s portfolio.

Please refer to the Schedule of Investments on pages 15–35 for a full listing of

Trust securities.

All investments are subject to risk, including the possible loss of principal. In the past several years, financial markets have experienced increased volatility and

heightened uncertainty. The market prices of securities may go up or down, sometimes rapidly or unpredictably, due to general market conditions, such as real or perceived adverse economic, political, or regulatory conditions, recessions, inflation,

changes in interest or currency rates, lack of liquidity in the bond markets, the spread of infectious illness or other public health issues or adverse investor sentiment. These conditions may continue, recur, worsen or spread.

The Trust may invest in derivative securities, which may include futures and options, for a variety of purposes, including: in an attempt to hedge against adverse changes in the marketplace of

securities, interest rates or currency exchange rates; as a substitute for purchasing or selling securities; to attempt to increase the Trust’s return as a non-hedging strategy that may be considered speculative; and to manage portfolio

characteristics. Using derivatives can increase fund losses and reduce opportunities for gains when the market prices, interest rates or the derivative instruments themselves behave in a way not anticipated by the Trust. These types of instruments

can increase price fluctuation.

10 Pioneer Floating Rate Trust | Annual Report | 11/30/20

The Trust is not limited in the percentage of its assets that

may be invested in illiquid securities. Illiquid securities may be difficult to sell at a price reflective of their value at times when the Trust believes it is desirable to do so and the market price of illiquid securities is generally more

volatile than that of more liquid securities. Illiquid securities may be difficult to value, and investment of the Trust’s assets in illiquid securities may restrict the Trust’s ability to take advantage of market opportunities.

The Trust employs leverage through a revolving credit facility. Leverage creates significant risks, including the risk that the Trust’s income or capital appreciation from investments

purchased with the proceeds of leverage will not be sufficient to cover the cost of leverage, which may adversely affect the return for shareowners.

The Trust is required to maintain certain

regulatory and other asset coverage requirements in connection with the Trust’s use of leverage. In order to maintain required asset coverage levels, the Trust may be required to reduce the amount of leverage employed by the Trust, alter the

composition of the Trust’s investment portfolio or take other actions at what might be inopportune times in the market. Such actions could reduce the net earnings or returns to shareowners over time, which is likely to result in a decrease in

the market value of the Trust’s shares.

Investments in high-yield or lower-rated securities are subject to greater-than-average risk. The Trust may invest in securities of issuers that

are in default or that are in bankruptcy.

Investing in foreign and/or emerging markets securities involves risks relating to interest rates, currency exchange rates and economic and political

conditions.

The Trust may invest in insurance-linked securities (ILS). The return of principal and the payment of interest on ILS are contingent on the non-occurrence of a pre-defined

“trigger” event, such as a hurricane or an earthquake of a specific magnitude.

These risks may increase share price volatility.

Any information in this shareowner report regarding market or economic trends or the factors influencing the Trust’s historical or future performance are statements of opinion as of the date

of this report. Past performance is no guarantee of future results.

Pioneer Floating Rate Trust | Annual Report |

11/30/20 11

10 Largest Holdings

(As a percentage of total investments)*

(As a percentage of total investments)*

| 1. |

SPDR Blackstone/GSO Senior Loan ETF |

3.99% |

| 2. |

Invesco Senior Loan ETF (formerly, PowerShares Senior Loan Portfolio) |

2.87 |

| 3. |

Bass Pro Group LLC, Initial Term Loan, 5.75% (LIBOR + 500 bps), 9/25/24 |

1.29 |

| 4. |

Prime Security Services Borrower LLC (aka Protection 1 Security Solutions), |

|

| |

First Lien 2019 Refinancing Term B-1 Loan, 4.25% (LIBOR + 325 bps), 9/23/26 |

1.22 |

| 5. |

Rackspace Technology Global, Inc., First Lien Term B Loan, 4.0% |

|

| |

(LIBOR + 300 bps), 11/3/23 |

1.16 |

| 6. |

U.S. Renal Care, Inc., Initial Term Loan, 5.146% (LIBOR + 500 bps), 6/26/26 |

1.14 |

| 7. |

Endo Luxembourg Finance Co. I S.a.r.l., Initial Term Loan, 5.0% |

|

| |

(LIBOR + 425 bps), 4/29/24 |

1.14 |

| 8. |

Garda World Security Corp., Initial Term Loan, 4.91% (LIBOR + 475 bps), |

|

| |

10/30/26 |

1.11 |

| 9. |

Allied Universal Holdco LLC (f/k/a USAGM Holdco LLC), Initial Term Loan, |

|

| |

4.396% (LIBOR + 425 bps), 7/10/26 |

1.05 |

| 10. |

Team Health Holdings, Inc., Initial Term Loan, 3.75% (LIBOR + 275 bps), 2/6/24 |

1.01 |

* Excludes temporary cash investments and all derivative contracts except for options purchased. The Trust is actively managed, and current holdings may be different. The

holdings listed should not be considered recommendations to buy or sell any securities.

** Investment companies that invest at least 80% of their assets in Senior Loans

(as defined in the Trust’s prospectus).

12 Pioneer Floating Rate Trust | Annual Report | 11/30/20

Market Value per Share^

| |

11/30/20 |

11/30/19 |

| Market Value |

$10.73 |

$10.53 |

| Premium/(Discount) |

(3.94)% |

(10.99)% |

Net Asset Value per Share^

| |

11/30/20 |

11/30/19 |

| Net Asset Value |

$11.17 |

$11.83 |

Distributions per Share*:

| |

Net |

|

|

| |

Investment |

Short-Term |

Long-Term |

| |

Income |

Capital Gains |

Capital Gains |

| 12/1/19–11/30/20 |

$0.7425 |

$ — |

$ — |

Yields

| |

11/30/20 |

11/30/19 |

| 30-day SEC Yield |

3.76% |

5.25% |

The data

shown above represents past performance, which is no guarantee of future results.

^ Net asset value and market value are published in

Barron’s on Saturday, The Wall Street Journal on Monday and The New York Times on Monday and Saturday. Net asset value

and market value are published daily on the Trust’s website at www.amundi.com/us.

* The amount of distributions made to shareowners during the year was in

excess of the net investment income earned by the Trust during the year.

Pioneer Floating Rate Trust | Annual Report |

11/30/20 13

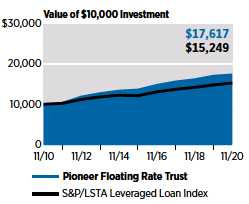

Investment Returns

The mountain chart on the right shows the

change in market value, including reinvestment of dividends and distributions, of a $10,000 investment made in shares of Pioneer Floating Rate Trust during the periods shown, compared with the value of the S&P/LSTA Leveraged Loan Index, which

provides broad and comprehensive total return metrics of the U.S. universe of syndicated term loans.

| Average Annual Total Returns | |||

| (As of November 30, 2020) |

| ||

| |

Net |

|

|

| |

Asset |

|

S&P/LSTA |

| |

Value |

Market |

Leveraged |

| Period |

(NAV) |

Price |

Loan Index |

| 10 Years |

5.84% |

4.89% |

4.31% |

| 5 Years |

4.87 |

6.71 |

4.73 |

| 1 Year |

1.89 |

9.96 |

3.38 |

Call 1-800-225-6292 or visit www.amundi.com/us for the most recent month-end performance results. Current performance may be lower or higher than the performance

data quoted.

Performance data shown represents past performance. Past performance is no guarantee of future results. Investment return and market price will fluctuate, and your shares may

trade below NAV, due to such factors as interest rate changes, and the perceived credit quality of borrowers.

Total investment return does not reflect broker sales charges or commissions. All performance is for

shares of the Trust.

Shares of closed-end funds, unlike open-end funds, are not continuously offered. There is a one-time public offering and, once issued, shares of closed-end funds are bought and sold in the

open market through a stock exchange and frequently trade at prices lower than their NAV. NAV per share is total assets less total liabilities, which include preferred shares, or borrowings, as applicable, divided by the number of shares

outstanding.

When NAV is lower than market price, dividends are assumed to be reinvested at the greater of NAV or 95% of the market price. When NAV is higher, dividends are assumed to be reinvested at prices

obtained through open-market purchases under the Trust’s dividend reinvestment plan.

The performance table and graph do not reflect the deduction of fees and taxes that a shareowner would pay on Trust

distributions or the sale of Trust shares. Had these fees and taxes been reflected, performance would have been lower.

Index returns are calculated monthly, assume reinvestment of dividends and, unlike Trust

returns, do not reflect any fees, expenses or sales charges. The index does not use leverage. You cannot invest directly in an index.

14

Pioneer Floating Rate Trust | Annual Report | 11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

UNAFFILIATED ISSUERS — 125.1% |

| |

| |

SENIOR SECURED FLOATING RATE LOAN |

| |

| |

INTERESTS — 96.6% of Net Assets*(a) |

||

| |

Aerospace & Defense — 4.7% |

| |

| 1,217,289 |

American Airlines, Inc., 2017 Class B Term Loan, |

| |

| |

2.141% (LIBOR + 200 bps), 12/15/23 |

$ 1,081,431 | |

| 1,246,875 |

Delta Air Lines, Inc., Term Loan, 5.75% (LIBOR + |

| |

| |

475 bps), 4/29/23 |

1,260,902 | |

| 1,657,065 |

Jazz Acquisition, Inc., First Lien Initial Term Loan, |

| |

| |

4.4% (LIBOR + 425 bps), 6/19/26 |

1,532,786 | |

| 493,750 |

JetBlue Airways Corp., Term Loan, 6.25% (LIBOR + |

| |

| |

525 bps), 6/17/24 |

503,111 | |

| 775,000 |

MAG DS Corp., Initial Term Loan, 6.5% (LIBOR + |

| |

| |

550 bps), 4/1/27 |

742,062 | |

| 1,250,000 |

Mileage Plus Holdings LLC (Mileage Plus Intellectual |

| |

| |

Property Assets, Ltd.), Initial Term Loan, 6.25% |

||

| |

(LIBOR + 525 bps), 6/21/27 |

1,291,812 | |

| 1,223,712 |

MRO Holdings, Inc., Initial Term Loan, 5.22% (LIBOR + |

| |

| |

500 bps), 6/4/26 |

1,036,077 | |

| 1,943,584 |

Peraton Corp. (fka MHVC Acquisition Corp.), First Lien |

| |

| |

Initial Term Loan, 6.25% (LIBOR + |

| |

| |

525 bps), 4/29/24 |

1,943,584 | |

| 700,000 |

Spirit Aerosystems, Inc. (fka Mid-Western Aircraft |

| |

| |

Systems, Inc & Onex Wind Finance LP.), Initial Term |

| |

| |

Loan, 6.0% (LIBOR + 525 bps), 1/15/25 |

708,313 | |

| 2,960,361 |

WP CPP Holdings LLC, First Lien Initial Term Loan, |

| |

| |

4.75% (LIBOR + 375 bps), 4/30/25 |

2,782,739 | |

| |

Total Aerospace & Defense |

$ 12,882,817 | |

| |

Airlines — 1.8% |

| |

| 2,456,250 |

Allegiant Travel Co., Replacement Term Loan, 3.214% |

| |

| |

(LIBOR + 300 bps), 2/5/24 |

$ 2,389,727 | |

| 1,170,000 |

Grupo Aeromexico, Sociedad Anonima Bursatil De |

| |

| |

Capital Variable, Senior Secured Tranche 1, |

||

| |

9.0% (LIBOR + 800 bps), 8/19/22 |

1,191,937 | |

| 950,000 |

Highline Aftermarket Acquisition LLC, First Lien Initial |

| |

| |

Term Loan, 5.25% (LIBOR + 450 bps), 11/9/27 |

945,250 | |

| 340,000 |

SkyMiles IP, Ltd. (Delta Air Lines, Inc.), Initial Term |

| |

| |

Loan, 4.75% (LIBOR + 375 bps), 10/20/27 |

348,394 | |

| |

Total Airlines |

$ 4,875,308 | |

| |

Automobile — 4.1% |

| |

| 2,135,537 |

American Axle & Manufacturing, Inc., Tranche B Term |

| |

| |

Loan, 3.0% (LIBOR + 225 bps), 4/6/24 |

$ 2,100,072 | |

| 1,547,426 |

Commercial Vehicle Group, Inc., Initial Term Loan, |

| |

| |

11.5% (LIBOR + 1,050 bps), 4/12/23 |

1,501,003 | |

| 1,000,000 |

Drive Chassis Holdco LLC, Second Lien Term B Loan, |

| |

| |

9.561% (LIBOR + 825 bps), 4/10/26 |

989,375 | |

| 1,500,249 |

IXS Holdings, Inc., Initial Term Loan, 6.0% (LIBOR + |

| |

| |

500 bps), 3/5/27 |

1,491,498 | |

| 2,361,599 |

Navistar, Inc., Tranche B Term Loan, 3.65% (LIBOR + |

| |

| |

350 bps), 11/6/24 |

2,355,695 |

The

accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Trust | Annual Report |

11/30/20 15

Schedule of Investments | 11/30/20 (continued)

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Automobile — (continued) |

| |

| 1,706,111 |

Thor Industries, Inc., Initial USD Term Loan, 3.938% |

| |

| |

(LIBOR + 375 bps), 2/1/26 |

$ 1,701,846 | |

| 898,483 |

TI Group Automotive Systems LLC, Initial US Term |

| |

| |

Loan, 4.5% (LIBOR + 375 bps), 12/16/24 |

896,236 | |

| 227,868 |

Wabash National Corp., Term B Loan, 4.0% (LIBOR + |

| |

| |

325 bps), 9/28/27 |

227,156 | |

| |

Total Automobile |

$ 11,262,881 | |

| |

Banking — 0.6% |

| |

| 500,000 |

Azalea TopCo, Inc., First Lien 2020 Incremental Term |

| |

| |

Loan, 4.75% (LIBOR + 400 bps), 7/24/26 |

$ 496,250 | |

| 1,190,694 |

Nouryon Finance BV (aka AkzoNobel), Initial Dollar |

| |

| |

Term Loan, 3.141% (LIBOR + 300 bps), 10/1/25 |

1,170,974 | |

| |

Total Banking |

$ 1,667,224 | |

| |

Broadcasting & Entertainment — 0.5% |

| |

| 1,488,750 |

Creative Artists Agency LLC, Closing Date Term Loan, |

| |

| |

3.896% (LIBOR + 375 bps), 11/27/26 |

$ 1,466,419 | |

| |

Total Broadcasting & Entertainment |

$ 1,466,419 | |

| |

Building Materials — 1.0% |

| |

| 1,451,748 |

CPG International LLC (fka CPG International, Inc.), New |

| |

| |

Term Loan, 4.75% (LIBOR + 375 bps), 5/5/24 |

$ 1,453,336 | |

| 1,451,250 |

WKI Holding Co., Inc. (aka World Kitchen), Initial Term |

| |

| |

Loan, 5.0% (LIBOR + 400 bps), 5/1/24 |

1,443,994 | |

| |

Total Building Materials |

$ 2,897,330 | |

| |

Buildings & Real Estate — 1.5% |

| |

| 1,488,579 |

Ply Gem Midco, Inc., Initial Term Loan, 3.88% (LIBOR + |

| |

| |

375 bps), 4/12/25 |

$ 1,481,136 | |

| 2,841,420 |

WireCo WorldGroup, Inc. (WireCo WorldGroup |

| |

| |

Finance LP), First Lien Initial Term Loan, 6.0% (LIBOR + |

| |

| |

500 bps), 9/29/23 |

2,600,342 | |

| |

Total Buildings & Real Estate |

$ 4,081,478 | |

| |

Chemicals — 0.4% |

| |

| 1,000,000 |

Plaze, Inc., 2020-1 Additional Term Loan, 5.25% (LIBOR + |

| |

| |

425 bps), 8/3/26 |

$ 988,125 | |

| |

Total Chemicals |

$ 988,125 | |

| |

Chemicals, Plastics & Rubber — 1.7% |

| |

| 423,981 |

Core & Main LP, Initial Term Loan, 3.75% (LIBOR + |

| |

| |

275 bps), 8/1/24 |

$ 419,741 | |

| 265,000 |

Emerald Performance Materials LLC, Initial Term Loan, |

| |

| |

5.0% (LIBOR + 400 bps), 8/12/25 |

265,332 | |

| 1,037,935 |

Hexion, Inc., USD Term Loan, 3.73% (LIBOR + |

| |

| |

350 bps), 7/1/26 |

1,032,745 |

The

accompanying notes are an integral part of these financial statements.

16 Pioneer Floating Rate Trust | Annual Report |

11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Chemicals, Plastics & Rubber — (continued) |

||

| 2,610,951 |

Tronox Finance LLC, First Lien Initial Dollar Term Loan, |

| |

| |

3.176% (LIBOR + 300 bps), 9/23/24 |

$ 2,583,209 | |

| 436,693 |

Twist Beauty International Holdings SA, Facility B2, 4.0% |

| |

| |

(LIBOR + 300 bps), 4/22/24 |

417,042 | |

| |

Total Chemicals, Plastics & Rubber |

$ 4,718,069 | |

| |

Computers & Electronics — 6.1% |

| |

| 1,135,000 |

Ahead DB Holdings LLC, First Lien Initial Term Loan, |

| |

| |

6.0% (LIBOR + 500 bps), 10/18/27 |

$ 1,098,112 | |

| 234,715 |

Applied Systems, Inc., First Lien Closing Date Term |

| |

| |

Loan, 4.0% (LIBOR + 300 bps), 9/19/24 |

234,379 | |

| 2,750,000 |

Applied Systems, Inc., Second Lien Initial Term Loan, |

| |

| |

8.0% (LIBOR + 700 bps), 9/19/25 |

2,766,041 | |

| 2,211,116 |

Chloe OX Parent LLC, Initial Term Loan, 5.5% (LIBOR + |

| |

| |

450 bps), 12/23/24 |

2,150,311 | |

| 1,708,822 |

CornerStone OnDemand, Inc., Term Loan, 4.396% |

| |

| |

(LIBOR + 425 bps), 4/22/27 |

1,710,157 | |

| 325,000 |

ECi Macola/MAX Holding LLC (ECI Software |

| |

| |

Solution, Inc.), First Lien Initial Term Loan, 4.5% (LIBOR + |

| |

| |

375 bps), 11/9/27 |

322,816 | |

| 1,755,648 |

Energy Acquisition LP (aka Electrical Components |

| |

| |

International), First Lien Initial Term Loan, |

||

| |

4.396% (LIBOR + 425 bps), 6/26/25 |

1,684,690 | |

| 1,250,000 |

LogMeIn, Inc., First Lien Initial Term Loan, 4.888% |

| |

| |

(LIBOR + 475 bps), 8/31/27 |

1,237,695 | |

| 3,120,000 |

Pitney Bowes, Inc., Incremental Tranche B Term Loan, |

| |

| |

5.65% (LIBOR + 550 bps), 1/7/25 |

3,092,700 | |

| 2,651,376 |

Ultra Clean Holdings, Inc., Term B Loan, 4.646% (LIBOR + |

| |

| |

450 bps), 8/27/25 |

2,651,376 | |

| |

Total Computers & Electronics |

$ 16,948,277 | |

| |

Construction & Building — 0.8% |

| |

| 750,000(b) |

CP Atlas Buyer, Inc., Initial Tranche B-1 Term |

| |

| |

Loan, 11/23/27 |

$ 750,187 | |

| 250,000(b) |

CP Atlas Buyer, Inc., Initial Tranche B-2 Term |

| |

| |

Loan, 11/23/27 |

250,063 | |

| 1,255,836 |

Quikrete Holdings, Inc., First Lien Initial Term Loan, |

| |

| |

2.646% (LIBOR + 250 bps), 2/1/27 |

1,239,963 | |

| |

Total Construction & Building |

$ 2,240,213 | |

| |

Consumer Nondurables — 0.5% |

| |

| 1,488,750 |

Sunshine Luxembourg VII S.a.r.l., Facility B1, 5.25% |

| |

| |

(LIBOR + 425 bps), 10/1/26 |

$ 1,488,628 | |

| |

Total Consumer Nondurables |

$ 1,488,628 |

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Trust | Annual Report | 11/30/20 17

Schedule of Investments | 11/30/20 (continued)

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Consumer Services — 1.5% |

| |

| 4,236,389 |

Prime Security Services Borrower LLC (aka Protection 1 |

| |

| |

Security Solutions), First Lien 2019 Refinancing |

||

| |

Term B-1 Loan, 4.25% (LIBOR + 325 bps), 9/23/26 |

$ 4,220,020 | |

| |

Total Consumer Services |

$ 4,220,020 | |

| |

Containers, Packaging & Glass — 1.6% |

| |

| 725,000 |

Graham Packaging Co., Inc., Initial Term Loan, 4.5% |

||

| (LIBOR + 375 bps), 8/4/27 |

$ 725,050 | ||

| 1,575,000 |

Pactiv Evergreen, Inc., Tranche B-1 US Term Loan, 2.896% |

| |

| (LIBOR + 275 bps/PRIME + 175 bps), 2/5/23 |

739,436 | ||

| 747,494 |

Pactiv Evergreen, Inc., Tranche B-2 US Term Loan, 3.396% |

| |

| (LIBOR + 325 bps), 2/5/26 |

1,551,572 | ||

| 1,488,750 |

Pregis TopCo LLC, First Lien Initial Term Loan, 3.896% |

| |

| |

(LIBOR + 375 bps), 7/31/26 |

1,471,692 | |

| |

Total Containers, Packaging & Glass |

$ 4,487,750 | |

| |

Diversified & Conglomerate Manufacturing — 2.1% |

| |

| 864,112 |

ExamWorks Group, Inc. (fka Gold Merger Co., Inc.), |

| |

| |

Term B-1 Loan, 4.25% (LIBOR + 325 bps), 7/27/23 |

$ 860,440 | |

| 3,854,092 |

Garda World Security Corp., Initial Term Loan, 4.91% |

| |

| |

(LIBOR + 475 bps), 10/30/26 |

3,852,485 | |

| 1,002,613 |

Pelican Products, Inc., First Lien Term Loan, 4.5% |

| |

| |

(LIBOR + 350 bps), 5/1/25 |

975,668 | |

| |

Total Diversified & Conglomerate Manufacturing |

$ 5,688,593 | |

| |

Diversified & Conglomerate Service — 9.6% |

||

| 1,955,623 |

Albany Molecular Research, Inc., First Lien Initial Term |

| |

| |

Loan, 4.25% (LIBOR + 325 bps), 8/30/24 |

$ 1,952,690 | |

| 2,168,709 |

Alion Science & Technology Corp., First Line |

| |

| |

Replacement Term Loan, 4.75% (LIBOR + |

| |

| |

375 bps), 7/23/24 |

2,182,264 | |

| 3,640,006 |

Allied Universal Holdco LLC (f/k/a USAGM Holdco LLC), |

| |

| |

Initial Term Loan, 4.396% (LIBOR + 425 bps), 7/10/26 |

3,621,581 | |

| 1,000,000 |

Camelot U.S. Acquisition 1 Co. (aka Thomson Reuters |

| |

| |

Intellectual Property & Science), Amendment No. 2 |

| |

| |

Incremental Term Loan, 4.0% (LIBOR + |

| |

| |

300 bps), 10/30/26 |

997,812 | |

| 1,996,467 |

CB Poly Investments LLC, First Lien Closing Date Term |

| |

| |

Loan, 5.5% (LIBOR + 450 bps), 8/16/23 |

1,846,732 | |

| 999,792 |

DG Investment Intermediate Holdings 2, Inc. (aka |

| |

| |

Convergint Technologies Holdings LLC), First Lien Initial |

| |

| |

Term Loan, 3.75% (LIBOR + 300 bps), 2/3/25 |

979,484 | |

| 2,422,427 |

DTI Holdco, Inc., Replacement B-1 Term Loan, 5.75% |

| |

| |

(LIBOR + 475 bps), 9/29/23 |

2,194,026 | |

| 1,532,082 |

First Brands Group LLC, First Lien Tranche B-3 Term |

| |

| |

Loan, 8.5% (LIBOR + 750 bps), 2/2/24 |

1,532,082 | |

| 1,407,892 |

Gates Global LLC, Initial B-2 Dollar Term Loan, 3.75% |

| |

| |

(LIBOR + 275 bps), 4/1/24 |

1,398,017 | |

| 1,324,237 |

Intrado Corp., Incremental Term B-1 Loan, 4.5% (LIBOR + |

| |

| |

350 bps), 10/10/24 |

1,257,198 | |

| 2,391,521 |

Intrado Corp., Initial Term B Loan, 5.0% (LIBOR + |

| |

| |

400 bps), 10/10/24 |

2,281,767 | |

| |

|

| |

| |

|

|

The

accompanying notes are an integral part of these financial statements.

18 Pioneer Floating Rate Trust | Annual Report |

11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Diversified & Conglomerate Service — (continued) |

| |

| 1,974,797 |

Mitchell International, Inc., First Lien Initial Term Loan, |

||

| 3.396% (LIBOR + 325 bps), 11/29/24 |

$ 1,913,496 | ||

| 807,655 |

Sound Inpatient Physicians, Inc., Second Lien Initial |

| |

| |

Term Loan, 6.896% (LIBOR + 675 bps), 6/26/26 |

799,578 | |

| 3,955,508 |

Team Health Holdings, Inc., Initial Term Loan, 3.75% |

| |

| |

(LIBOR + 275 bps), 2/6/24 |

3,480,847 | |

| |

Total Diversified & Conglomerate Service |

$ 26,437,574 | |

| |

Electric & Electrical — 1.4% |

| |

| 4,020,625 |

Rackspace Technology Global, Inc., First Lien Term B |

| |

| |

Loan, 4.0% (LIBOR + 300 bps), 11/3/23 |

$ 3,998,287 | |

| |

Total Electric & Electrical |

$ 3,998,287 | |

| |

Electronics — 1.9% |

| |

| 2,351,820 |

Natel Engineering Co., Inc., Initial Term Loan, 6.0% |

| |

| |

(LIBOR + 500 bps), 4/30/26 |

$ 2,075,481 | |

| 3,260,417 |

Scientific Games International, Inc., Initial Term B-5 |

| |

| |

Loan, 2.896% (LIBOR + 275 bps), 8/14/24 |

3,149,019 | |

| |

Total Electronics |

$ 5,224,500 | |

| |

Financial Services — 1.8% |

| |

| 2,372,116 |

Blackhawk Network Holdings, Inc., First Lien Term |

| |

| |

Loan, 3.146% (LIBOR + 300 bps), 6/15/25 |

$ 2,269,523 | |

| 656,721 |

Cardtronics USA, Inc., Initial Term Loan, 5.0% (LIBOR + |

| |

| |

400 bps), 6/29/27 |

658,691 | |

| 1,905,288 |

Everi Payments, Inc., Term B loan, 3.75% (LIBOR + |

| |

| |

275 bps), 5/9/24 |

1,866,189 | |

| 99,750 |

Everi Payments, Inc., Term Loan, 11.5% (LIBOR + |

| |

| |

1,050 bps), 5/9/24 |

103,989 | |

| |

Total Financial Services |

$ 4,898,392 | |

| |

Forest Products — 1.1% |

| |

| 1,750,000 |

Chobani LLC, 2020 New Term Loan, 4.5% (LIBOR + |

| |

| |

350 bps), 10/25/27 |

$ 1,745,312 | |

| 1,310,814 |

ProAmpac PG Borrower LLC, First Lien 2020-1 Term |

| |

| |

Loan, 5.0% (LIBOR + 400 bps), 11/3/25 |

1,297,706 | |

| |

Total Forest Products |

$ 3,043,018 | |

| |

Gaming and Hotels — 0.2% |

| |

| 439,135 |

PCI Gaming Authority, Term B Facility Loan, 2.646% |

| |

| |

(LIBOR + 250 bps), 5/29/26 |

$ 431,274 | |

| |

Total Gaming and Hotels |

$ 431,274 | |

| |

Healthcare — 2.1% |

| |

| 525,000 |

CNT Holdings I Corp, First Lien Initial Term Loan, 4.5% |

| |

| |

(LIBOR + 375 bps), 11/8/27 |

$ 521,842 | |

| 629,118 |

Milano Acquisition Corp., First Lien Term B Loan, 4.75% |

| |

| |

(LIBOR + 400 bps), 10/1/27 |

624,923 | |

| 3,225,625 |

Option Care Health, Inc., Term B Loan, 4.396% (LIBOR + |

| |

| |

425 bps), 8/6/26 |

3,217,561 |

The

accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Trust | Annual Report |

11/30/20 19

Schedule of Investments | 11/30/20 (continued)

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Healthcare — (continued) |

| |

| 1,382,553 |

Phoenix Guarantor, Inc. (aka Brightspring), First Lien |

| |

| |

Tranche B-1 Term Loan, 3.4% (LIBOR + |

| |

| |

325 bps), 3/5/26 |

$ 1,366,135 | |

| |

Total Healthcare |

$ 5,730,461 | |

| |

Healthcare & Pharmaceuticals — 6.2% |

| |

| 3,212,002 |

Alphabet Holding Co., Inc. (aka Nature’s Bounty), First |

| |

| |

Lien Initial Term Loan, 3.646% (LIBOR + |

| |

| |

350 bps), 9/26/24 |

$ 3,150,916 | |

| 1,500,000 |

Alphabet Holding Co., Inc. (aka Nature’s Bounty), |

| |

| |

Second Lien Initial Term Loan, 7.896% (LIBOR + |

||

| |

775 bps), 9/26/25 |

1,461,875 | |

| 4,037,182 |

Endo Luxembourg Finance Co. I S.a.r.l., Initial Term |

| |

| |

Loan, 5.0% (LIBOR + 425 bps), 4/29/24 |

3,931,206 | |

| 1,488,750 |

FC Compassus LLC, Initial Term Loan, 6.0% (LIBOR + |

| |

| |

500 bps), 12/31/26 |

1,477,584 | |

| 1,571,038 |

Kindred Healthcare LLC, Closing Date Term Loan, |

| |

| |

5.188% (LIBOR + 500 bps), 7/2/25 |

1,573,002 | |

| 1,265,427 |

NMN Holdings III Corp., First Lien Closing Date Term |

| |

| |

Loan, 3.679% (LIBOR + 350 bps), 11/13/25 |

1,230,627 | |

| 218,576 |

NMN Holdings III Corp., First Lien Delayed Draw Term |

| |

| |

Loan, 4.011% (LIBOR + 375 bps/PRIME + |

| |

| |

275 bps), 11/13/25 |

212,565 | |

| 750,000 |

Parexel International Corp., Initial Term Loan, 2.896% |

| |

| |

(LIBOR + 275 bps), 9/27/24 |

735,234 | |

| 1,872,669 |

Sotera Health Holdings LLC, First Lien Initial Term Loan, |

| |

| |

5.5% (LIBOR + 450 bps), 12/11/26 |

1,875,478 | |

| 1,485,000 |

Upstream Newco, Inc., First Lien Initial Term Loan, |

| |

| |

4.646% (LIBOR + 450 bps), 11/20/26 |

1,447,875 | |

| |

Total Healthcare & Pharmaceuticals |

$ 17,096,362 | |

| |

Healthcare, Education & Childcare — 5.0% |

||

| 1,512,917 |

Alliance HealthCare Services, Inc., Second Lien Initial |

| |

| |

Term Loan, 12.0% (LIBOR + 1,100 bps), 4/24/24 |

$ 707,289 | |

| 2,887,237 |

ATI Holdings Acquisition, Inc., First Lien Initial Term |

| |

| |

Loan, 4.5% (LIBOR + 350 bps), 5/10/23 |

2,778,965 | |

| 2,704,225 |

KUEHG Corp. (fka KC MergerSub, Inc.) (aka KinderCare), |

| |

| |

Term B-3 Loan, 4.75% (LIBOR + 375 bps), 2/21/25 |

2,585,240 | |

| 1,413,103 |

LifePoint Health, Inc. (fka Regionalcare Hospital |

| |

| |

Partners Holdings, Inc.), First Lien Term B Loan, 3.896% |

| |

| |

(LIBOR + 375 bps), 11/16/25 |

1,395,665 | |

| 1,809,736 |

Quorum Health Corp., Exit Term Loan, 9.25% (LIBOR + |

| |

| |

825 bps), 4/29/25 |

1,757,706 | |

| 537,300 |

Surgery Center Holdings, Inc., 2020 Incremental Term |

| |

| |

Loan, 9.0% (LIBOR + 800 bps), 9/3/24 |

550,665 | |

| 3,967,456 |

U.S. Renal Care, Inc., Initial Term Loan, 5.146% (LIBOR + |

| |

| |

500 bps), 6/26/26 |

3,941,005 | |

| |

Total Healthcare, Education & Childcare |

$ 13,716,535 |

The accompanying notes are an integral part of these financial statements.

20 Pioneer Floating

Rate Trust | Annual Report | 11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Hotel, Gaming & Leisure — 2.8% |

| |

| 2,218,947 |

Caesars Resort Collection LLC, Term B Loan, 2.896% |

| |

| |

(LIBOR + 275 bps), 12/23/24 |

$ 2,151,129 | |

| 1,100,000 |

Caesars Resort Collection LLC, Term B-1 Loan, 4.646% |

| |

| |

(LIBOR + 450 bps), 7/21/25 |

1,091,652 | |

| 215,169 |

Flutter Entertainment plc, USD Term Loan, 3.72% |

| |

| |

(LIBOR + 350 bps), 7/10/25 |

215,853 | |

| 231,125 |

Golden Nugget Online Gaming, Inc., 2020 Buyback Term |

| |

| |

Loan, 13.0% (LIBOR + 1,200 bps), 10/4/23 |

266,949 | |

| 18,875 |

Golden Nugget Online Gaming, Inc., 2020 Initial Term |

| |

| |

Loan, 13.0% (LIBOR + 1,200 bps), 10/4/23 |

21,801 | |

| 2,986,004 |

Golden Nugget, Inc. (aka Landry’s, Inc.), Initial Term B |

| |

| |

Loan, 3.25% (LIBOR + 250 bps), 10/4/23 |

2,847,901 | |

| 1,290,306 |

Penn National Gaming, Inc., Term B-1 Facility Loan, 3.0% |

| |

| |

(LIBOR + 225 bps), 10/15/25 |

1,269,631 | |

| |

Total Hotel, Gaming & Leisure |

$ 7,864,916 | |

| |

Insurance — 3.7% |

| |

| 992,462 |

Alliant Holdings Intermediate LLC, 2019 New Term Loan, |

| |

| |

3.393% (LIBOR + 325 bps), 5/9/25 |

$ 970,364 | |

| 523,688 |

AqGen Ascensus, Inc., First Lien Seventh Amendment |

| |

| |

Replacement Term Loan, 5.0% (LIBOR + |

| |

| |

400 bps), 12/3/26 |

521,069 | |

| 1,590,930 |

Confie Seguros Holding II Co., Term B Loan, 5.75% |

| |

| |

(LIBOR + 475 bps), 4/19/22 |

1,570,713 | |

| 1,247,791 |

Integro Parent, Inc., First Lien Initial Term Loan, 6.75% |

| |

| |

(LIBOR + 575 bps), 10/31/22 |

1,210,357 | |

| 1,196,605 |

MPH Acquisition Holdings LLC, Initial Term Loan, 3.75% |

| |

| |

(LIBOR + 275 bps), 6/7/23 |

1,182,097 | |

| 1,250,000 |

Navicure, Inc., First Lien 2020 Incremental Term Loan, |

| |

| |

4.75% (LIBOR + 400 bps), 10/22/26 |

1,248,437 | |

| 1,728,125 |

Sedgwick Claims Management Services, Inc. (Lightning |

| |

| |

Cayman Merger Sub, Ltd.), 2019 Term Loan, 4.146% |

| |

| |

(LIBOR + 400 bps), 9/3/26 |

1,711,805 | |

| 249,375 |

Sedgwick Claims Management Services, Inc. (Lightning |

| |

| |

Cayman Merger Sub, Ltd.), 2020 Term Loan, 5.25% |

| |

| |

(LIBOR + 425 bps), 9/3/26 |

250,622 | |

| 1,619,900 |

USI, Inc. (fka Compass Investors, Inc.), 2017 New Term |

| |

| |

Loan, 3.22% (LIBOR + 300 bps), 5/16/24 |

1,588,514 | |

| |

Total Insurance |

$ 10,253,978 | |

| |

Leasing — 0.5% |

| |

| 1,550,000 |

Fly Funding II S.a.r.l., Term B Loan, 7.0% (LIBOR + |

| |

| |

600 bps), 10/15/25 |

$ 1,499,625 | |

| |

Total Leasing |

$ 1,499,625 |

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Trust | Annual Report | 11/30/20 21

Schedule of Investments | 11/30/20 (continued)

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Leisure & Entertainment — 1.5% |

| |

| 1,082,266(b)(c) |

24 Hour Fitness Worldwide, Inc., Term Loan (LIBOR + |

| |

| |

350 bps), 5/30/25 |

$ 27,902 | |

| 1,989,899 |

AMC Entertainment Holdings, Inc. (fka AMC |

| |

| |

Entertainment, Inc.), Term B-1 Loan, 3.23% (LIBOR + |

| |

| |

300 bps/PRIME + 200 bps), 4/22/26 |

1,518,169 | |

| 1,645,875 |

Carnival Corp., Initial Advance, 8.5% (LIBOR + |

| |

| |

750 bps), 6/30/25 |

1,705,538 | |

| 928,057 |

Fitness International LLC, Term B Loan, 4.25% (LIBOR + |

| |

| |

325 bps), 4/18/25 |

781,888 | |

| |

Total Leisure & Entertainment |

$ 4,033,497 | |

| |

Machinery — 1.8% |

| |

| 1,421,164 |

Blount International, Inc., New Refinancing Term Loan, |

| |

| |

4.75% (LIBOR + 375 bps), 4/12/23 |

$ 1,424,717 | |

| 851,429 |

CTC AcquiCo GmbH, Facility B2, 2.897% (LIBOR + |

| |

| |

275 bps), 3/7/25 |

808,857 | |

| 1,240,625 |

MHI Holdings LLC, Initial Term Loan, 5.146% (LIBOR + |

| |

| |

500 bps), 9/21/26 |

1,234,422 | |

| 97,196 |

NN, Inc., Tranche B Term Loan, 6.5% (LIBOR + |

| |

| |

575 bps), 10/19/22 |

96,791 | |

| 384,755 |

Shape Technologies Group, Inc., Initial Term Loan, |

| |

| |

3.146% (LIBOR + 300 bps), 4/21/25 |

311,651 | |

| 1,035,865 |

Welbilt, Inc. (fka Manitowoc Foodservice, Inc.), Term B |

| |

| |

Loan, 2.647% (LIBOR + 250 bps), 10/23/25 |

982,130 | |

| |

Total Machinery |

$ 4,858,568 | |

| |

Media — 0.7% |

| |

| 1,977,196 |

Altice France SA, USD TLB-13 Incremental Term Loan, |

| |

| |

4.237% (LIBOR + 400 bps), 8/14/26 |

$ 1,962,367 | |

| |

Total Media |

$ 1,962,367 | |

| |

Metals & Mining — 2.1% |

| |

| 930,511 |

Atkore International, Inc., First Lien Initial Incremental |

| |

| |

Term Loan, 3.75% (LIBOR + 275 bps), 12/22/23 |

$ 929,445 | |

| 1,508,411 |

BWay Holding Co., Initial Term Loan, 3.48% (LIBOR + |

| |

| |

325 bps), 4/3/24 |

1,440,399 | |

| 2,887,704 |

Phoenix Services International LLC, Term B Loan, 4.75% |

| |

| |

(LIBOR + 375 bps), 3/1/25 |

2,828,145 | |

| 746,142 |

TMS International Corp. (aka Tube City IMS Corp.), |

| |

| |

Term B-2 Loan, 3.75% (LIBOR + 275 bps), 8/14/24 |

740,546 | |

| |

Total Metals & Mining |

$ 5,938,535 | |

| |

Oil & Gas — 1.8% |

| |

| 540,375 |

Centurion Pipeline Co. LLC (fka Lotus Midstream LLC), |

| |

| |

Initial Term Loan, 3.396% (LIBOR + |

| |

| |

325 bps), 9/29/25 |

$ 534,634 | |

| 612,500 |

NorthRiver Midstream Finance LP, Initial Term B Loan, |

| |

| |

3.475% (LIBOR + 325 bps), 10/1/25 |

591,971 | |

| 1,609,222(b) |

Summit Midstream Partners Holdings LLC, Term Loan |

| |

| |

Credit Facility (LIBOR + 600 bps), 5/13/22 |

362,075 |

The

accompanying notes are an integral part of these financial statements.

22 Pioneer Floating Rate Trust | Annual Report |

11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Oil & Gas — (continued) |

| |

| 3,562,000 |

Traverse Midstream Partners LLC, Advance, 6.5% |

| |

| |

(LIBOR + 550 bps), 9/27/24 |

$ 3,379,447 | |

| |

Total Oil & Gas |

$ 4,868,127 | |

| |

Personal, Food & Miscellaneous Services — 1.6% |

| |

| 2,513,592 |

IRB Holding Corp. (aka Arby’s/Buffalo Wild Wings), |

| |

| |

2020 Replacement Term B Loan, 3.75% (LIBOR + |

| |

| |

275 bps), 2/5/25 |

$ 2,474,666 | |

| 992,031 |

Knowlton Development Corp., Inc., Initial Term Loan, |

| |

| |

3.896% (LIBOR + 375 bps), 12/22/25 |

982,111 | |

| 1,000,000 |

Parfums Holding Co., Inc., Second Lien Initial Term Loan, |

| |

| |

9.977% (LIBOR + 875 bps/PRIME + 775 bps), 6/30/25 |

957,500 | |

| |

Total Personal, Food & Miscellaneous Services |

$ 4,414,277 | |

| |

Printing & Publishing — 0.7% |

| |

| 1,393,000 |

Nielsen Finance LLC, Dollar Term B-5 Loan, 4.75% |

| |

| |

(LIBOR + 375 bps), 6/4/25 |

$ 1,398,920 | |

| 454,779 |

Trader Corp., First Lien 2017 Refinancing Term Loan, |

| |

| |

4.0% (LIBOR + 300 bps), 9/28/23 |

451,369 | |

| |

Total Printing & Publishing |

$ 1,850,289 | |

| |

Professional & Business Services — 7.2% |

| |

| 995,000 |

AI Convoy (Luxembourg) S.a.r.l., Facility B, 4.5% |

| |

| |

(LIBOR + 350 bps), 1/18/27 |

$ 993,756 | |

| 1,800,000(b) |

Amentum Government Services Holdings LLC, |

| |

| |

Incremental Term Loan, 1/29/27 |

1,789,875 | |

| 1,492,500 |

APX Group, Inc., Initial Loan, 5.146% (LIBOR + 500 bps/ |

| |

| |

PRIME + 400 bps), 12/31/25 |

1,482,862 | |

| 2,969,924 |

athenahealth, Inc., First Lien Term B Loan, 4.75% |

| |

| |

(LIBOR + 450 bps), 2/11/26 |

2,958,787 | |

| 987,500 |

Blackstone CQP Holdco LP, Initial Term Loan, 3.725% |

| |

| |

(LIBOR + 350 bps), 9/30/24 |

978,242 | |

| 2,107,462 |

Clear Channel Outdoor Holdings, Inc., Term B Loan, |

| |

| |

3.714% (LIBOR + 350 bps), 8/21/26 |

1,982,770 | |

| 1,485,000 |

Ensemble RCM LLC, Closing Date Term Loan, 3.964% |

| |

| |

(LIBOR + 375 bps), 8/3/26 |

1,480,359 | |

| 1,481,250 |

MYOB US Borrower LLC, First Lien Initial US Term Loan, |

| |

| |

4.146% (LIBOR + 400 bps), 5/6/26 |

1,451,625 | |

| 1,050,000 |

PAE Incorporated, First Lien Initial Term Loan, 5.25% |

| |

| |

(LIBOR + 450 bps), 10/19/27 |

1,048,031 | |

| 2,005,630 |

Pre-Paid Legal Services, Inc. (aka LegalShield), First Lien |

| |

| |

Initial Term Loan, 3.396% (LIBOR + |

| |

| |

325 bps), 5/1/25 |

1,956,743 | |

| 1,136,822 |

SIWF Holdings, Inc. (aka Spring Window Fashions), |

| |

| |

First Lien Initial Term Loan, 4.396% (LIBOR + |

||

| |

425 bps), 6/15/25 |

1,119,060 | |

| 735,000 |

Tosca Services LLC, First Lien Term Loan, 5.25% |

| |

| |

(LIBOR + 425 bps), 8/18/27 |

738,675 |

The

accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Trust | Annual Report |

11/30/20 23

Schedule of Investments | 11/30/20 (continued)

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Professional & Business Services — (continued) |

| |

| 1,920,295 |

Verscend Holding Corp., Term B Loan, 4.646% |

| |

| |

(LIBOR + 450 bps), 8/27/25 |

$ 1,919,494 | |

| |

Total Professional & Business Services |

$ 19,900,279 | |

| |

Retail — 5.9% |

| |

| 4,441,887 |

Bass Pro Group LLC, Initial Term Loan, 5.75% (LIBOR + |

| |

| |

500 bps), 9/25/24 |

$ 4,448,980 | |

| 2,228,138 |

Dealer Tire LLC, Term B-1 Loan, 4.396% (LIBOR + |

| |

| |

425 bps), 12/12/25 |

2,204,464 | |

| 975,000 |

Harbor Freight Tools USA, Inc., Initial Term Loan, 4.0% |

| |

| |

(LIBOR + 325 bps), 10/19/27 |

970,038 | |

| 2,208,969 |

Michaels Stores, Inc., 2020 Refinancing Term B Loan, |

| |

| |

4.25% (LIBOR + 350 bps), 10/1/27 |

2,182,737 | |

| 1,958,481 |

PetSmart, Inc., Amended Term Loan, 4.5% (LIBOR + |

| |

| |

350 bps), 3/11/22 |

1,951,343 | |

| 3,193,745 |

Staples, Inc., 2019 Refinancing New Term B-2 Loan, |

| |

| |

4.714% (LIBOR + 450 bps), 9/12/24 |

3,111,241 | |

| 650,000 |

TruGreen LP, First Lien Second Refinancing Term Loan, |

| |

| |

4.75% (LIBOR + 400 bps), 11/2/27 |

649,188 | |

| 856,540 |

United Natural Foods, Inc., Initial Term Loan, 4.396% |

| |

| |

(LIBOR + 425 bps), 10/22/25 |

852,257 | |

| |

Total Retail |

$ 16,370,248 | |

| |

Securities & Trusts — 1.2% |

| |

| 1,514,553 |

KSBR Holding Corp., Initial Term Loan, 3.393% (LIBOR + |

| |

| |

325 bps), 4/15/26 |

$ 1,507,609 | |

| 1,861,776 |

Spectacle Gary Holdings LLC, Closing Date Term Loan, |

| |

| |

11.0% (LIBOR + 900 bps), 12/23/25 |

1,829,195 | |

| |

Total Securities & Trusts |

$ 3,336,804 | |

| |

Telecommunications — 2.3% |

| |

| 1,765,001 |

Commscope, Inc., Initial Term Loan, 3.396% (LIBOR + |

| |

| |

325 bps), 4/6/26 |

$ 1,739,786 | |

| 800,000 |

Consolidated Communications, Inc., Initial Term Loan, |

| |

| |

5.75% (LIBOR + 475 bps), 10/2/27 |

801,834 | |

| 675,000 |

Frontier Communications Corp., Initial Term Loan, |

| |

| |

5.75% (LIBOR + 475 bps), 10/8/21 |

677,531 | |

| 500,000(b) |

Virgin Media Bristol LLC, Term Q Loan, 1/31/29 |

497,125 | |

| 798,000 |

Windstream Services II LLC, Initial Term Loan, 7.25% |

| |

| |

(LIBOR + 625 bps), 9/21/27 |

768,740 | |

| 1,998,475 |

Xplornet Communications, Inc., Initial Term Loan, |

| |

| |

4.898% (LIBOR + 475 bps), 6/10/27 |

1,980,676 | |

| |

Total Telecommunications |

$ 6,465,692 | |

| |

Textile & Apparel — 1.0% |

| |

| 2,476,212 |

Adient US LLC, Initial Term Loan, 4.413% (LIBOR + |

| |

| |

425 bps), 5/6/24 |

$ 2,408,116 | |

| 350,000 |

Canada Goose, Inc., 2020 Refinancing Term Loan, 5.0% |

| |

| |

(LIBOR + 425 bps), 10/7/27 |

350,219 | |

| |

Total Textile & Apparel |

$ 2,758,335 |

The accompanying notes are an integral part of these financial statements.

24 Pioneer Floating

Rate Trust | Annual Report | 11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Transport — 0.4% |

| |

| 1,117,994 |

Patriot Container Corp. (aka Wastequip), First Lien |

| |

| |

Closing Date Term Loan, 4.5% (LIBOR + |

| |

| |

350 bps), 3/20/25 |

$ 1,094,237 | |

| |

Total Transport |

$ 1,094,237 | |

| |

Transportation — 0.7% |

| |

| 2,200,949 |

Envision Healthcare Corp., Initial Term Loan, 3.896% |

| |

| |

(LIBOR + 375 bps), 10/10/25 |

$ 1,810,967 | |

| 257,522 |

Syncreon Group BV, Second Out Term Loan, 7.0% |

| |

| |

(LIBOR + 600 bps), 4/1/25 |

247,543 | |

| |

Total Transportation |

$ 2,058,510 | |

| |

Utilities — 2.5% |

| |

| 671,522 |

Compass Power Generation LLC, Tranche B-1 Term |

| |

| |

Loan, 4.5% (LIBOR + 350 bps), 12/20/24 |

$ 667,325 | |

| 1,929,719 |

Eastern Power LLC (Eastern Covert Midco LLC) |

| |

| |

(aka TPF II LC LLC), Term Loan, 4.75% (LIBOR + |

||

| |

375 bps), 10/2/25 |

1,928,245 | |

| 1,968,022 |

Edgewater Generation LLC, Term Loan, 3.896% |

| |

| |

(LIBOR + 375 bps), 12/13/25 |

1,930,968 | |

| 997,500 |

Hamilton Projects Acquiror LLC, Term Loan, 5.75% |

| |

| |

(LIBOR + 475 bps), 6/17/27 |

998,539 | |

| 1,451,363 |

PG&E Corp., Term Loan, 5.5% (LIBOR + 450 bps), 6/23/25 |

1,464,969 | |

| |

Total Utilities |

$ 6,990,046 | |

| |

TOTAL SENIOR SECURED FLOATING RATE LOAN INTERESTS |

| |

| |

(Cost $269,372,239) |

$267,007,865 | |

| | |||

| Shares |

|

| |

| |

COMMON STOCKS — 0.5% of Net Assets |

||

| |

Energy Equipment & Services — 0.5% |

| |

| 72,091(d) |

FTS International, Inc. |

$ 1,347,381 | |

| |

Total Energy Equipment & Services |

$ 1,347,381 | |

| |

Specialty Retail — 0.0%† |

| |

| 91,346+^(d) |

Targus Cayman SubCo., Ltd. |

$ 120,576 | |

| |

Total Specialty Retail |

$ 120,576 | |

| |

TOTAL COMMON STOCKS |

| |

| |

(Cost $2,065,469) |

$ 1,467,957 | |

The accompanying notes are an integral part of these financial statements.

Pioneer Floating Rate Trust | Annual Report | 11/30/20 25

Schedule of Investments | 11/30/20 (continued)

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

ASSET BACKED SECURITIES — 1.4% of Net Assets |

| |

| 1,000,000(a) |

522 Funding Clo, Ltd., Series 2019-4A, Class E, 7.218% |

| |

| |

(3 Month USD LIBOR + 700 bps), 4/20/30 (144A) |

$ 937,476 | |

| 1,000,000(a) |

Goldentree Loan Management US CLO 2, Ltd., Series |

| |

| |

2017-2A, Class E, 4.918% (3 Month USD LIBOR + |

| |

| |

470 bps), 11/28/30 (144A) |

879,237 | |

| 1,000,000(a) |

Madison Park Funding XXII, Ltd., Series 2016-22A, |

| |

| |

Class ER, 6.937% (3 Month USD LIBOR + |

| |

| |

670 bps), 1/15/33 (144A) |

959,585 | |

| 1,000,000(a) |

Octagon Investment Partners XXI, Ltd., Series 2014-1A, |

| |

| |

Class DRR, 7.221% (3 Month USD LIBOR + |

||

| |

700 bps), 2/14/31 (144A) |

967,133 | |

| |

TOTAL ASSET BACKED SECURITIES |

| |

| |

(Cost $3,935,369) |

$ 3,743,431 | |

| |

COLLATERALIZED MORTGAGE OBLIGATIONS — |

| |

| |

1.5% of Net Assets |

| |

| 4,100,000(a) |

Connecticut Avenue Securities Trust, Series 2019-HRP1, |

| |

| |

Class B1, 9.4% (1 Month USD LIBOR + 925 bps), |

||

| |

11/25/39 (144A) |

$ 3,363,731 | |

| 760,000(a) |

Freddie Mac Stacr Trust, Series 2019-HQA1, Class B2, |

| |

| |

12.4% (1 Month USD LIBOR + 1,225 bps), |

| |

| |

2/25/49 (144A) |

802,950 | |

| |

TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS |

| |

| |

(Cost $4,860,000) |

$ 4,166,681 | |

| |

COMMERCIAL MORTGAGE-BACKED |

||

| |

SECURITIES — 0.5% of Net Assets |

| |

| 235,938(a) |

FREMF Mortgage Trust, Series 2020-KF74, Class C, 6.37% |

| |

| |

(1 Month USD LIBOR + 623 bps), 1/25/27 (144A) |

$ 227,299 | |

| 625,000(a) |

Morgan Stanley Capital I Trust, Series 2019-BPR, |

| |

| |

Class D, 4.141% (1 Month USD LIBOR + |

| |

| |

400 bps), 5/15/36 (144A) |

474,024 | |

| 1,000,000 |

Wells Fargo Commercial Mortgage Trust, Series |

| |

| |

2015-C28, Class E, 3.0%, 5/15/48 (144A) |

574,741 | |

| |

TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES |

| |

| |

(Cost $1,630,858) |

$ 1,276,064 | |

| |

CORPORATE BONDS — 15.2% of Net Assets |

| |

| |

Advertising — 0.5% |

| |

| 1,250,000 |

MDC Partners, Inc., 6.5%, 5/1/24 (144A) |

$ 1,231,250 | |

| |

Total Advertising |

$ 1,231,250 | |

| |

Banks — 0.6% |

| |

| 1,000,000(e)(f) |

Citigroup, Inc., 4.7% (SOFRRATE + 323 bps) |

$ 1,021,550 | |

| 700,000(e)(f) |

Credit Suisse Group AG, 7.5% (5 Year USD Swap |

| |

| |

Rate + 460 bps) (144A) |

762,090 | |

| |

Total Banks |

$ 1,783,640 |

The accompanying notes are an integral part of these financial statements.

26 Pioneer Floating

Rate Trust | Annual Report | 11/30/20

| Principal |

|

| |

| Amount |

|

| |

| USD ($) |

|

Value | |

| |

Building Materials — 0.4% |

| |

| 996,000 |

Patrick Industries, Inc., 7.5%, 10/15/27 (144A) |

$ 1,080,660 | |

| |

Total Building Materials |

$ 1,080,660 | |

| |

Chemicals — 0.6% |

| |

| 1,000,000 |

Hexion, Inc., 7.875%, 7/15/27 (144A) |

$ 1,072,500 | |

| 500,000 |

OCI NV, 4.625%, 10/15/25 (144A) |

521,250 | |

| |

Total Chemicals |

$ 1,593,750 | |

| |

Coal — 0.7% |

| |

| 2,000,000 |

SunCoke Energy Partners LP/SunCoke Energy Partners |

| |

| |

Finance Corp., 7.5%, 6/15/25 (144A) |

$ 1,970,000 | |

| |

Total Coal |

$ 1,970,000 | |

| |

Commercial Services — 1.1% |

| |

| 1,380,000 |

Allied Universal Holdco LLC/Allied Universal Finance |

| |

| |

Corp., 9.75%, 7/15/27 (144A) |

$ 1,530,448 | |

| 1,000,000 |

APX Group, Inc., 6.75%, 2/15/27 (144A) |

1,080,000 | |

| 495,000 |

Garda World Security Corp., 4.625%, 2/15/27 (144A) |

496,237 | |

| |

Total Commercial Services |

$ 3,106,685 | |

| |

Computers — 0.0%† |

| |

| 100,000 |

Diebold Nixdorf, Inc., 9.375%, 7/15/25 (144A) |

$ 109,750 | |

| |

Total Computers |

$ 109,750 | |

| |