UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form | |||||

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended March 31 , 2025

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from __________ to ______________

Commission File Number: 001-37537

(Exact name of registrant as specified in its charter) | ||||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||

(Address of principal executive offices) (Zip Code)

(310 ) 553-8871

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities Registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | ¨ | |||||||||

| Non-accelerated filer | ¨ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of September 30, 2024, the aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $8.43 billion.

As of May 12, 2025, the registrant had 53,789,857 shares of Class A common stock, $0.001 par value per share, and 16,003,904 shares of Class B common stock, $0.001 par value per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Auditor Name: KPMG LLP Auditor Location: Los Angeles, California Auditor Firm ID: 185

HOULIHAN LOKEY, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

| Page | ||||||||

Item 15. | ||||||||

PART I

Unless the context otherwise requires, as used in this Annual Report on Form 10-K (“Form 10-K”), the terms the “Company,” “Houlihan Lokey, Inc.,” “Houlihan Lokey,” “HL,” “our firm,” “we,” “us” and “our” refer to Houlihan Lokey, Inc., a Delaware corporation, and, in each case, unless otherwise stated, all of its subsidiaries. We use the term “HL Holders” to refer to our current and former employees and members of our management who hold our Class B common stock through the Houlihan Lokey Voting Trust (the “HL Voting Trust”). Our fiscal year ends on March 31. Accordingly, references to fiscal 2025, fiscal 2024, and fiscal 2023 are to our fiscal years ended March 31, 2025, 2024, and 2023, respectively. However, references in this Form 10-K to years are to calendar years unless otherwise noted.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements. All statements other than statements of historical fact contained in this Form 10-K may be forward-looking statements. Statements regarding our future results of operations and financial position, business strategy and plans and objectives of management for future operations are forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “may,” “might,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “targets,” “projects,” “contemplates,” “believes,” “estimates,” “intends,” “predicts,” “potential” or “continue,” or the negative of these terms or other similar expressions.

Forward-looking statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. We believe that these factors include, but are not limited to, the following:

•our ability to retain our Managing Directors and our other senior professionals;

•our ability to successfully identify, recruit and develop talent;

•changing market conditions;

•reputational risk;

•the volatility of our revenue and profits on a quarterly basis;

•risks associated with our acquisitions (including integration) and strategic investments;

•the impact of U.S. fiscal, monetary, and/or trade policies on transaction volumes and, consequently, our revenue

•strong competition from other financial advisory and investment banking firms;

•potential impairment of goodwill and other intangible assets, which represent a significant portion of our assets;

•our ability to execute on our growth initiatives, business strategies or operating plans;

•risks associated with the U.S. tax law changes;

•risks associated with our international operations;

•terrorism, political hostilities, war and other civil disturbances or other catastrophic events that reduce business activity;

•fluctuations in foreign currency exchange rates;

•costs of compliance associated with broker-dealer, employment, labor, benefits and tax regulations;

•our potential to offer new products within our existing lines of business or enter into new lines of business, which may result in additional risks and uncertainties in our business;

•operational risks;

•extensive and evolving regulation of our business and the business of our clients;

•substantial litigation risks;

•cybersecurity and other security risks;

•our dependence on fee-paying clients;

•our clients' ability to pay us for our services;

•our ability to generate sufficient cash in the future to service our indebtedness;

•an epidemic or pandemic, and the measures that international, federal, state and local governments, agencies, law enforcement and/or health authorities may implement to address it, which may cause a severe and prolonged disruption and instability in the global financial markets and may precipitate or exacerbate one or more of the above-mentioned factors and/or other risks, and significantly disrupt or prevent us from operating our business in the ordinary course for an extended period; and

•other factors beyond our control.

1

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified, you should not rely on these forward-looking statements as predictions of future events. The events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. For information about other important factors that could adversely affect our future results, see “Risk Factors” in this Form 10-K.

These forward-looking statements speak only as of the date of this filing. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained in this Form 10-K after we file this Form 10-K, whether as a result of any new information, future events or otherwise.

Item 1. Business

Established in 1972, Houlihan Lokey, Inc. is a leading global independent investment bank with expertise in mergers and acquisitions (“M&A”), capital markets, financial restructurings and liability management, and financial and valuation advisory. Through our offices in the Americas, Europe, Asia, Australia, and the Middle East, we serve a diverse set of clients worldwide, including corporations, financial sponsors and government agencies. We provide our financial professionals with an integrated platform that enables them to deliver meaningful and differentiated advice to our clients. We advise our clients on critical strategic and financial decisions, employing a rigorous analytical approach coupled with deep product and industry expertise. We market our services through our product areas, our industry groups and our Financial Sponsors group, serving our clients in three primary business practices: Corporate Finance (“CF”), encompassing M&A and Capital Solutions, Financial Restructuring (“FR”), including restructurings both out-of-court and in formal bankruptcy or insolvency proceedings, and Financial and Valuation Advisory (“FVA”), including financial opinions and a variety of valuation and financial consulting services.

We are committed to a set of principles that serve as the backbone of our success. Independent advice and intellectual rigor, combined with consistent senior-level involvement, are hallmarks of our commitment to client service. Our entrepreneurial culture engenders our flexibility to collaborate across our business practices to provide world-class solutions for our clients. Our broad-based employee ownership serves to align the interests of employees and shareholders and further encourages a collaborative environment where our CF, FR, and FVA professionals work together productively and creatively to solve our clients’ most critical financial issues. We enter into businesses or offer services where we believe we can excel based on our expertise, analytical sophistication, industry focus and competitive dynamics. Finally, we remain independent and specialized, focusing on advisory products and market segments where our expertise is both differentiating and less subject to conflicts of interest arising from non-advisory products and services, and where we believe we can be a market leader in a particular segment. We do not lend or engage in any securities sales and trading operations or research that might conflict with our clients’ interests.

As of March 31, 2025, we had a team of 1,893 financial professionals across 35 offices globally, serving more than 2,000 clients annually over the past several years, ranging from closely held companies to Fortune Global 500 corporations. Information on our segments is set forth in “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Our Advisory Services

We provide our financial professionals with an integrated platform that enables them to deliver meaningful and differentiated advice to our clients. We market our services through our three business practices described below, our industry groups and our Financial Sponsors group, who work collaboratively to deliver comprehensive solutions and seamless execution for our clients. This marketing effort is combined with an extensive network of referral relationships with law firms, consulting firms, accounting firms and other professional services firms that have been developed by our financial professionals who maintain those relationships as potential referral sources and direct clients across all of our business practices.

2

Corporate Finance

As of March 31, 2025, we had 240 CF Managing Directors utilizing a collaborative, interdisciplinary approach to provide our clients with extensive industry and product expertise and global reach in a wide variety of M&A and capital markets transactions. We compete with boutique firms focused on particular industries or geographies as well as other global independent investment banks and bulge-bracket firms. A majority of our engagements relate to mid-cap transactions, which we believe is an attractive segment that is underserved by bulge-bracket investment banks. We believe that our deep sector expertise, significant senior banker involvement and attention, strong financial sponsor relationships and global platform provide a compelling value for our clients, engendering long-term relationships and providing a competitive advantage against our peers in this segment of the market.

We believe that, through our industry groups, we have a meaningful presence in every major industry segment, including: business services; consumer; energy; financial services; fintech; healthcare; industrials; real estate, lodging and leisure; and technology. We continue to expand and deepen our specialized industry capabilities through a combination of internal promotion, external hires and acquisitions. While the majority of our engagements are in the United States, we continue to enhance our presence in other geographies, including Europe, Asia, South America, Australia and the Middle East, and we believe there will be continued opportunities to grow in regions outside the United States.

Our CF activities are comprised of two significant categories:

Mergers & Acquisitions: We have extensive expertise in mergers, acquisitions, divestitures, and other related advisory services for a broad range of United States and international clients. Our CF professionals have relationships with thousands of companies and financial sponsors, providing us with valuable insights into a wide variety of relevant markets.

Our M&A business consists primarily of sell-side and buy-side engagements. In particular, we believe we have developed a reputation in the marketplace as one of the most prolific sell-side advisors, consistently selling more companies under $1 billion than any competitor. We provide advice and services to a diverse set of parties, including public and private company executives, boards of directors, special committees and financial sponsors.

We believe our team of experienced and talented financial professionals is well positioned to provide advice across a wide range of M&A advisory services globally, including sell-side, buy-side, joint ventures, asset sales and divestitures that are less subject to conflicts of interest arising from non-advisory services. Our global industry group model with embedded M&A capabilities brings sector-specific knowledge, experience and relationships to our clients, allowing us to provide differentiated expert advice and connect buyers and sellers on a global basis.

Capital Solutions: We provide global financing solutions and capital-raising advisory services for a broad range of corporate and private equity clients across most industry sectors, from large, publicly-held, multinational corporations to financial sponsors to privately-held companies founded and run by entrepreneurs.

Our Capital Solutions professionals leverage a wide array of longstanding, senior-level lender and investor relationships, including with traditional and non-traditional direct capital providers (such as institutional credit funds, commercial finance companies, business development companies, insurance companies, pension funds, mutual funds, global asset managers, special situations investors and structured equity providers). As the traditional syndicated capital markets have become increasingly complex and more regulated, the private capital markets have developed to provide an alternative source of flexible capital that can be tailored to meet clients’ needs.

We believe we excel in providing our clients with sophisticated and thoughtful advice and access to traditional and non-traditional capital providers in the private and public capital markets. Our objective is to help clients create a capital structure that enables them to achieve their strategic priorities on the best terms available in the market, which often involves raising more than one type of capital.

Financial Restructuring

As of March 31, 2025, we had 57 FR Managing Directors working around the globe, which we believe constitutes one of the largest restructuring groups in the investment banking industry. Our FR group has earned a reputation for being the advisor of choice for many of the largest and most complex restructuring and liability management transactions, offering knowledge, experience, and creativity to address challenging situations. We operate in all major worldwide markets as debt issuances have increased around the world. Our FR professionals bring to bear deep expertise and experience in restructurings in the United States, Canada, Europe, Asia, Australia, the Middle East, Latin America and Africa. Given the depth and breadth of the team’s expertise and the high barriers to entry for this expertise and experience, international and multi-jurisdictional restructurings represent an attractive opportunity for our FR group.

3

The group employs an interdisciplinary approach to engagements, calling upon the expertise of our industry groups, Capital Solutions group and Financial Sponsors group, and drawing on the worldwide resources of the FR team as each situation may require. The FR group has deep experience evaluating complex, highly leveraged situations. In addition to comprehensive financial restructuring and liability management transactions, we work with distressed companies on changes of control, asset sales and other M&A and capital markets activities, many times involving the sale of a company or its assets quickly, and in contested or litigious settings on expedited timeframes. We advise companies and creditor constituencies at all levels of the capital structure, in both out-of-court negotiations and in formal bankruptcy or insolvency proceedings. Our experience, geographic diversity and size allow us to provide the immediate attention and staffing required for time-sensitive and mission-critical restructuring and liability management assignments, making us a valued partner for our clients.

Our dedicated team is active throughout business cycles. Our FR practice serves as a countercyclical hedge across macroeconomic cycles, with increasing levels of restructuring opportunities often occurring during periods when demand for M&A and capital markets advisory services may be reduced. In robust macroeconomic environments, demand for the services of our FR team generally continues due to opportunities arising from secular and cyclical disruptions in certain industries. Our geographic diversity and global market leadership allow our FR group to maintain significant levels of activity even when the U.S. capital markets are vibrant.

Our broad base of clients and our extensive experience allow us to understand the dynamics of each restructuring situation and strengthen our negotiating strategies by providing us insight into the needs, attitudes and positions of all parties-in-interest. Our clients include companies, bondholder groups, financial institutions, banks and other secured creditor groups, trade creditors, official Chapter 11 creditors’ committees, equity holders, acquirers, equity sponsors, and other parties-in-interest involved with financially challenged companies.

Our FR professionals work closely with our CF and FVA professionals to provide holistic advice and services.

Financial and Valuation Advisory

As of March 31, 2025, we had 42 Managing Directors in our FVA group, which we believe represents one of the largest and most respected valuation and financial opinion practices in the United States. We have developed a reputation as a thought-leader in the field of valuation, and our professionals produce influential studies and publications, which are recognized and valued throughout the financial industry. We believe our extensive transaction expertise and leadership in the fields of valuation, diligence, tax and financial analytics inspire the confidence of the financial executives, boards of directors, special committees, retained counsel, financial and strategic investors and business owners that we serve. We believe that our reputation for delivering an outstanding analytical product that will withstand legal or regulatory scrutiny coupled with our independent financial, accounting and tax skills makes us the advisor of choice for clients with complex valuation, transaction opinion, transaction accounting, tax and diligence needs.

Our core competencies in our FVA practice are based in our deep technical financial, accounting and tax skills. These capabilities include our ability to analyze and value companies, security interests, and different types of assets, including complex illiquid investments, as well as our ability to analyze, diligence and structure the financial and tax aspects of public and private transactions. We are organized around different service lines as each line has different regulatory or compliance specializations as well as different marketing channels.

Human Capital Resources

Our goal is to attract, develop and retain the best talent in our industry across all levels. We believe our compensation programs are competitive, offering a portion of compensation in deferred cash and a portion in deferred stock awards to provide incentives for our employees to remain with us. In addition, we strive to foster a collaborative environment to attract and retain employees, and we seek individuals who fit our culture of entrepreneurship, integrity, creativity, and commitment to our clients. For over 20 years, we have emphasized broad employee ownership as a way to align the incentives of our employees and shareholders. As of March 31, 2025, we had approximately 1,100 present and former employee shareholders that collectively owned approximately 24% of our equity with no single employee owning more than 2% of our equity. We believe that a strong emphasis on cultural fit during our recruiting process combined with broad employee ownership results in high retention rates.

Our Managing Directors (other than our executive officers) are compensated based on their ability to deliver profitable revenues on a consistent basis to our firm, the quality of advice and execution provided to our clients, and their collaboration with their colleagues across industries, products, and regions. We do not compensate on a commission-based pay model. Our compensation structure for junior financial professionals is based on a system of meritocracy whereby bankers are rewarded for past performance and expectation of future development, and compensation levels are tested against prevailing market compensation for bankers at similar levels.

4

The primary sources of recruitment for our junior financial professionals are leading undergraduate and graduate programs around the world. Our consistent hiring practices year after year have created partnerships with these institutions and resulted in a steady and high-quality pipeline of junior financial professionals. To supplement this annual class of new hires, we opportunistically and strategically hire professionals with experience and backgrounds relevant to our various businesses. Regardless of title, we place a high degree of emphasis on cultural fit, technical capability and individual character. When we hire junior financial professionals, we hire them directly into one of our business practices to enable them to begin to develop their relevant skill set from day one.

Across our firm, we devote significant time and resources to training and mentoring our employees to ensure every person achieves their highest possible potential. We strive to identify and cultivate future leaders within our firm and are committed to developing our brightest and most ambitious junior professionals into Managing Directors. This philosophy of investing in our people has been and will continue to be core to our culture and organization. As of March 31, 2025, 2024, and 2023, we employed 2,702, 2,601, and 2,610 people, respectively, worldwide.

Competition

Our competitors are other investment banking and financial advisory firms. We compete on both a global and a regional basis, and on the basis of a number of factors, including industry knowledge, transaction execution skills, strength of client relationships, reputation, and price. We believe our primary competitors vary by product and industry expertise and would include the following: for our CF practice, Jefferies Financial Group Inc., Lazard, Inc., Lincoln International LLC, Moelis & Company, Piper Sandler Companies, Raymond James Financial, Inc., Robert W. Baird & Co. Incorporated, Rothschild & Co SCA, William Blair & Company, LLC, and the bulge-bracket investment banking firms; for our FR practice, Evercore Inc., Lazard, Inc., Moelis & Company, Perella Weinberg Partners, PJT Partners Inc., and Rothschild & Co. SCA; and for our FVA practice, the “big four” accounting firms, Alvarez & Marsal, Kroll, LLC, Lincoln International LLC, and various global financial advisory and accounting firms.

We compete with all of the above as well as with regional and industry-focused boutique firms to attract and retain qualified employees. Our ability to continue to compete effectively in our business will depend upon our ability to attract new employees and retain our existing employees. We may be at a competitive disadvantage in certain situations with regard to certain of our competitors who are able to, and regularly do, provide financing or market making services that are often instrumental in effecting transactions.

Regulation

United States

As a financial services provider, Houlihan Lokey is subject to extensive regulation in the United States and across the globe. As a matter of public policy, regulatory bodies in the United States and the rest of the world are charged with safeguarding the integrity of the securities and other financial markets and with protecting the interests of customers participating in those markets. In the United States, the Securities and Exchange Commission (the “SEC”) is the federal agency responsible for the administration of the federal securities laws. Houlihan Lokey Capital, Inc. (“Houlihan Lokey Capital”), one of our wholly-owned subsidiaries, through which we conduct our CF, FR and transaction opinion businesses in the United States, is registered as a broker-dealer with the SEC and is subject to regulation and oversight by the SEC. In addition, the Financial Industry Regulatory Authority, Inc. (“FINRA”), a self-regulatory organization that is subject to oversight by the SEC, adopts and enforces rules governing the conduct, and examines the activities, of its broker-dealer member firms, including Houlihan Lokey Capital. State securities regulators also have regulatory or oversight authority over Houlihan Lokey Capital in those states in which it does business.

Broker-dealers are subject to regulations that cover all aspects of the securities business, including sales methods, trade practices, the financing of customers’ purchases, capital structure, record-keeping and the conduct and qualifications of directors, officers and employees. In particular, as a registered broker-dealer and member of a self-regulatory organization, we are subject to the SEC’s uniform net capital rule, Rule 15c3-1. Rule 15c3-1 specifies the minimum level of net capital a broker-dealer must maintain and also requires that a significant part of a broker-dealer’s assets be kept in relatively liquid form. The SEC and FINRA impose rules that require notification when net capital falls below certain predefined criteria, limit the ratio of subordinated debt to equity in the regulatory capital composition of a broker-dealer and constrain the ability of a broker-dealer to expand its business under certain circumstances. Additionally, the SEC’s uniform net capital rule imposes certain requirements that may have the effect of prohibiting a broker-dealer from distributing or withdrawing capital and requiring prior notice to the SEC for certain withdrawals of capital.

5

Houlihan Lokey Financial Advisors, Inc. (“HLFA”), our wholly owned subsidiary, provides valuation services and related financial analyses of various businesses and types of assets which are used by clients in connection with mergers and acquisitions, divestitures, recapitalizations, dispute analysis, and estate, gift, and income tax support. In rendering such analyses, HLFA does not: (i) make recommendations or provide advice with respect to the merits of any security or transaction, the suitability of transacting in any security, or any investment decision with respect to any security, or (ii) manage or hold client accounts, securities or funds. In addition to valuation and financial consulting and analytic services, HLFA provides dispute resolution services.

The USA PATRIOT Act of 2001 and the Treasury Department’s implementing federal regulations require us, as a “financial institution,” to establish and maintain an anti-money-laundering program. The Financial Crimes Enforcement Network (“FinCEN’’), a part of the United States Department of the Treasury, is charged with protecting the financial system from illicit use, combating money laundering, and promoting national security through financial intelligence. FinCEN’s customer due diligence rule requires certain financial institutions, including broker-dealers, to obtain, verify, and record certain client information, including, in some cases, beneficial ownership, as well as to maintain adequate internal controls to prevent and detect possible violations of anti-money laundering rules. In addition, in connection with its administration and enforcement of economic and trade sanctions based on United States foreign policy and national security goals, the Treasury Department’s Office of Foreign Assets Control (“OFAC”) publishes a list of individuals and companies owned or controlled by, or acting for or on behalf of, targeted countries. It also lists individuals, groups, and entities, such as terrorists and narcotics traffickers, designated under programs that are not country-specific. Collectively, such individuals and companies are called “Specially Designated Nationals” (“SDNs”). Assets of SDNs are blocked, and we are generally prohibited from dealing with them. In addition, OFAC administers a number of comprehensive sanctions and embargoes that target certain countries, governments and geographic regions. We are generally prohibited from engaging in transactions involving any country, government, entity, or person that is subject to such comprehensive sanctions.

Certain parts of our business are subject to compliance with laws and regulations of United States federal and state governments, non-United States governments, their respective agencies and/or various self-regulatory organizations or exchanges relating to, among other things, the privacy of client information, and any failure to comply with these regulations could expose us to liability and/or reputational damage.

Europe

Our European advisory business is conducted primarily through our subsidiaries and or one of their branches, namely, as regards the provision of regulated investment services:

•in the United Kingdom, Houlihan Lokey UK Limited (“HL UK”), which is organized under the laws of England and Wales; and

•in Germany, Houlihan Lokey (Europe) GmbH (“HLE GmbH”) a private limited company organized under the laws of such jurisdiction with branches in England, France, and Spain in addition to its main office in Germany.

In addition to those entities referenced above, we also provide unregulated corporate finance advisory services through other subsidiaries in Germany, Italy, France, the Netherlands, Sweden, Switzerland, and Spain.

HL UK is authorized and regulated by the United Kingdom’s Financial Conduct Authority (“FCA”). The current U.K. regulatory regime is based upon the Financial Services and Markets Act 2000 (“FSMA”), together with secondary legislation and other rules made under FSMA and other relevant legislation. These rules govern our financial advisory business in the United Kingdom, including regulated activities, record keeping, approval standards for individuals, anti-money laundering and periodic reporting.

HLE GmbH, through which we now conduct our regulated business in the EU, was established in order to mitigate the effects of the United Kingdom ceasing to be a member of the EU (“Brexit”) on our European business, further to the end of the Brexit transitional period and the withdrawal of “passport” rights in favor of other HL entities. HLE GmbH is approved to conduct regulated investment services by the German regulatory authority, Bundesanstalt für Finanzdienstleistungsaufsicht.

HLE GmbH has exercised the appropriate European financial services passport rights to provide cross-border services into all other members of the EEA from Germany and to establish branches in France and Spain. These “passport” rights derive from the pan-European regime established by the EU Markets in Financial Instruments Directive, which regulates the provision of investment services and ancillary activities throughout the EEA.

6

Middle East

Dubai, United Arab Emirates

Houlihan Lokey (MEA Financial Advisory) Ltd. is licensed under Article 48 of the Regulatory Law 2004 by the Dubai Financial Services Authority (“DFSA”) to provide certain regulated financial services from its office in the Dubai International Financial Centre. Such entity is subject to DFSA administered law and regulation (most notably certain applicable modules of the DFSA Rulebook), and individuals within it carrying out “licensed functions” (essentially senior management roles) are required to be approved by DFSA to so act.

Asia Pacific

Australia

Houlihan Lokey (Australia) Pty Limited is licensed and subject to regulation by the Australian Securities & Investments Commission and must also comply with applicable provisions of the Corporations Act 2001 and other Australian legal and regulatory requirements, including capital adequacy rules, customer protection rules, and compliance with other applicable trading and investment banking regulations

Hong Kong SAR

In Hong Kong, the Securities and Futures Commission (the “SFC”) regulates our subsidiary, Houlihan Lokey (China) Limited. The compliance requirements of the SFC include, among other things, various codes of conduct and certain capital requirements. The SFC licenses the activities of the officers, directors, and employees of Houlihan Lokey (China) Limited, and requires the registration of such individuals as licensed representatives.

India

Houlihan Lokey’s Indian corporate finance and financial and valuation advisory businesses are conducted through Houlihan Lokey Advisory (India) Private Limited, which is licensed by the Securities and Exchange Board of India (“SEBI”).

Japan

In Japan, financial advisory services are provided by Houlihan Lokey Corporation, HL Succession Corporation, and BIZIT Inc., none of which conducts regulated activities in Japan.

Singapore

In Singapore, Houlihan Lokey conducts its business through Houlihan Lokey (Singapore) Private Limited, which is registered with the Monetary Authority of Singapore (“MAS”) as an “exempt corporate finance advisor” and is therefore able to provide exempt corporate finance advisory services to accredited investors only, subject to compliance with regulation governing such status as applicable from time to time in Singapore.

South America

Brazil

In Brazil, Houlihan Lokey operates principally a financial restructuring business, which provides unregulated financial advisory services through Houlihan Lokey Assessoria Financeira Ltda.

7

Other

We are also subject to laws and regulations prohibiting corrupt or illegal payments to government officials and other persons, including the US Foreign Corrupt Practices Act and the UK Bribery Act. We maintain policies, procedures and internal controls intended to comply with those regulations.

Organizational Structure

Overview

Houlihan Lokey, Inc. is a holding company that operates our business through its subsidiaries, the primary subsidiaries being Houlihan Lokey Capital, HLFA, HL UK, and HLE GmbH, each of which is described above under “Regulation.”

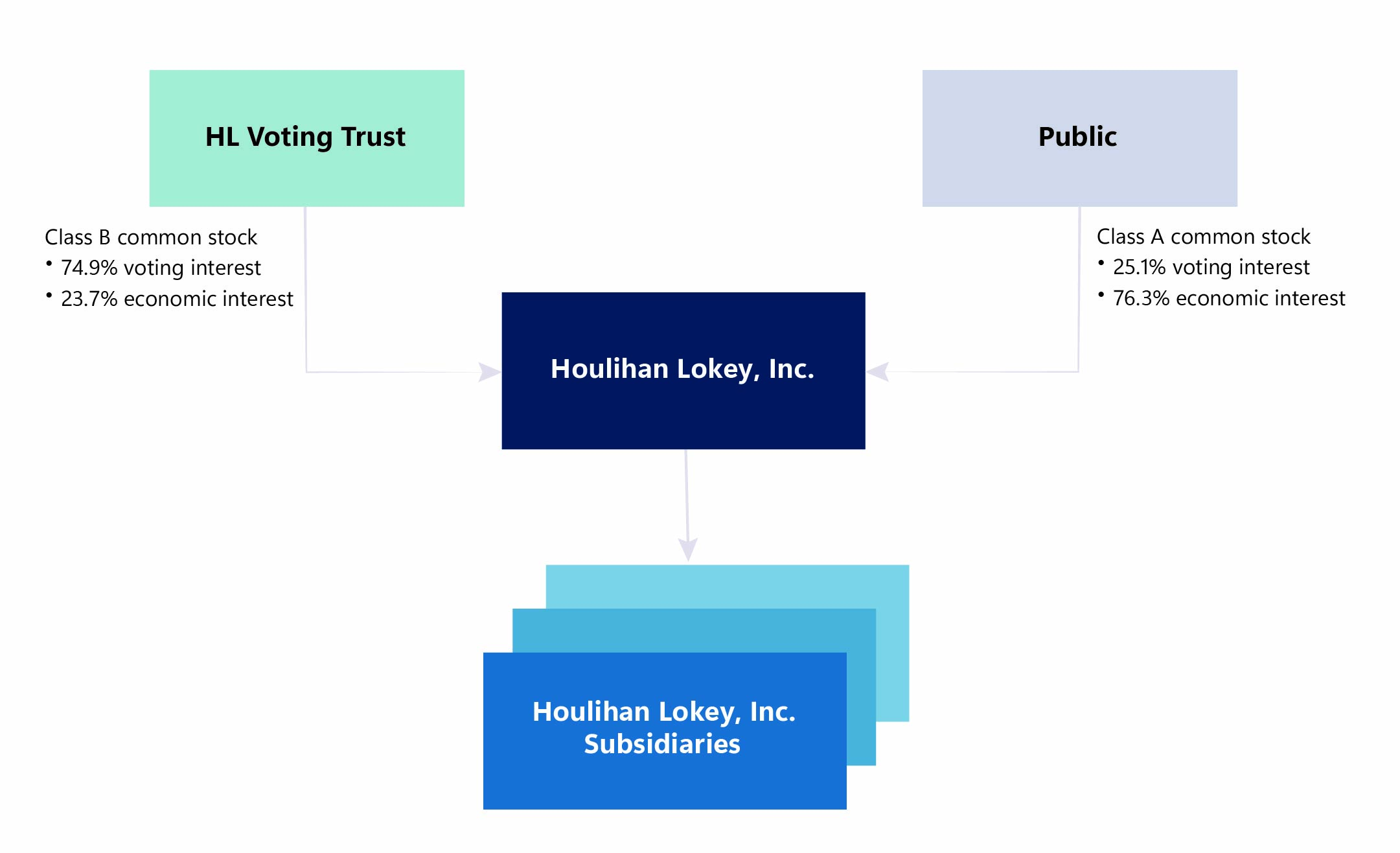

The diagram below depicts our current organizational structure and the percentages are as of March 31, 2025:

HL Voting Trust Agreement

In connection with the successful completion of the initial public offering (“IPO”) of our Class A common stock in August 2015, we entered into the Voting Trust Agreement (the “HL Voting Trust Agreement”), dated as of August 18, 2015, with the HL Holders and the trustees of the HL Voting Trust. Pursuant to the HL Voting Trust Agreement, the trustees have the right to vote the shares of our common stock deposited by any HL Holder, together with any shares of Class B common stock acquired by such HL Holder, in their sole and absolute discretion on any matter, without fiduciary duties of any kind to the HL Holders. As of March 31, 2025, the HL Voting Trust controlled approximately 74.9% of the total voting power of the Company.

8

Controlled Company

The HL Voting Trust controls a majority of the voting power of our outstanding common stock. As a result, we are a “controlled company” under the rules of the New York Stock Exchange. Under these rules, a company of which more than 50% of the voting power is held by an individual, group or another company is a “controlled company” and may elect not to comply with certain corporate governance standards, including the requirements that (i) a majority of our board of directors consist of independent directors and (ii) that our board of directors have compensation and nominating and corporate governance committees composed entirely of independent directors, as independence is defined in Rule 10A-3 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and under the New York Stock Exchange listing standards. We utilize, and intend to continue to utilize, certain of these exemptions. At the present time, the majority of our directors are independent, as required by the New York Stock Exchange, we have a fully independent audit committee, and our compensation and nominating and corporate governance committees are composed entirely of independent directors. See the Risk Factor “We are a ‘controlled company’ within the meaning of the New York Stock Exchange listing standards and, as a result, qualify for, and rely on, exemptions from certain corporate governance requirements. Holders of Class A common stock do not have the same protections afforded to stockholders of companies that are subject to such requirements.” In the event that we cease to be a “controlled company” and our shares continue to be listed on the New York Stock Exchange, we will be required to comply with all of these corporate governance standards by the expiration of the applicable transition periods.

Market and Industry Data

The industry, market and competitive position data referenced throughout this Form 10-K are based on research, industry and general publications, including surveys and studies conducted by third parties. Industry rankings are based on data provided by LSEG unless otherwise noted. Information from LSEG relating to industry rankings are sourced through direct deal submissions from financial institutions coupled with research performed by LSEG analysts. Industry publications, surveys and studies generally state that they have been obtained from sources believed to be reliable. We have not independently verified such third party information. While we are not aware of any misstatements regarding any industry, market or similar data presented herein, such data involve uncertainties and are subject to change based on various factors, including those discussed under the headings “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors” in this Form 10-K.

In this Form 10-K, we use the term “independent investment banks” or “independent advisors” when referring to ourselves and other investment banks or financial advisors that are primarily focused on advisory services and that conduct no or limited commercial banking, lending, or securities sales and trading activities, which we believe are well positioned to provide uncompromised advice that is less subject to conflicts of interest arising from non-advisory services. In this Form 10-K, we use the term “mid-cap” when referring to transactions with a value below $1 billion and the term “large-cap” when referring to transactions with a value equal to or in excess of $1 billion.

Other Information

Our principal executive offices are located at 10250 Constellation Blvd., 5th Floor, Los Angeles, California 90067. Our telephone number is (310) 788-5200. Our website address is www.hl.com. We make available free of charge in the Investor Relations section of our website (http://investors.hl.com) our annual reports on Form 10-K, including this Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed or furnished with the SEC pursuant to Section 13(a) or 15(d) of the Exchange Act. We also make available through our website other reports filed with or furnished to the SEC under the Exchange Act, including our Proxy Statements and reports filed by officers and directors under Section 16(a) of that Act, as well as various governance documents. From time to time, we may use our website as a channel of distribution of material company information. Financial and other material information regarding the Company is routinely posted on and accessible at http://investors.hl.com. We do not intend for information contained in our website to be part of this Form 10-K. The inclusion of our website address in this Form 10-K does not include or incorporate by reference the information on our website into this Form 10-K or any other document into which this Form 10-K is incorporated by reference.

The SEC maintains a website that contains reports, proxy and information statements, and other information regarding registrants that file electronically with the SEC. The address of the site is http://www.sec.gov.

9

Item 1A. Risk Factors

Risks Related to Our Business

Changing market conditions can adversely affect our business in many ways, including by reducing the volume and/or size of the transactions we advise on, which could materially reduce our revenue.

As a financial services firm, we are materially affected by conditions in the global financial markets and economic conditions throughout the world. Financial markets and economic conditions can be negatively impacted by many factors beyond our control, such as the inability to access credit markets, rising interest rates or inflation, terrorism, political uncertainty, supply chain disruptions, uncertainty in the U.S. federal fiscal, monetary, or trade policies and the fiscal, monetary and trade policy of foreign governments, an evolving regulatory environment (and the timing and nature of regulatory reform), climate change, extreme weather events or natural disasters, the emergence or continuation of widespread health emergencies or pandemics, cyberattacks or campaigns, military conflicts around the world, such as ongoing conflicts in Eastern Europe and the Middle East, or other geopolitical events. The current U.S. administration has implemented, and continues to implement, significant and rapid changes in federal government operations and policies, including international trade policies, which may impact economic stability, the financial markets and the financial services industry broadly. Unfavorable market or economic conditions, including reduced expectations for, or further declines in, the U.S. and global economic outlook, may adversely affect our businesses; in particular, where revenue generated is directly related to the volume and size of the transactions in which we are involved. For example, weak market or economic conditions may adversely affect our CF and FVA groups because, in an economic downturn, the volume and size of transactions may decrease, thereby reducing the demand for our M&A, capital raising and opinion advisory services and increasing price competition among financial services companies seeking such engagements. Moreover, in the period following an economic downturn, the volume and size of transactions typically takes time to recover and lags a recovery in market and economic conditions. In particular, our clients engaging in M&A transactions often rely on access to the credit and/or capital markets to finance their transactions. The uncertainty of available credit and interest rates and the volatility of the capital markets and the fact that we do not provide financing or otherwise commit capital to clients can adversely affect the size, volume, timing and ability of such clients to successfully complete M&A transactions and thus can adversely affect our CF and FVA groups. In addition, our profitability would be adversely affected due to our fixed costs and the possibility that we would be unable to reduce our variable costs without reducing revenue or within a timeframe sufficient to offset any decreases in revenue relating to changes in market and economic conditions. On the other hand, strong market or economic conditions may adversely affect our FR group. In a strong environment, the volume and size of recapitalization and restructuring transactions may decrease, thereby reducing the demand for the services provided by our FR business segment and increasing price competition among financial services companies seeking such engagements. Changes in market and economic conditions are expected to impact our businesses in different ways, and we may not be able to benefit from such changes. Further, our business, financial condition and results of operations could be adversely affected by changing market or economic conditions. Our profitability may also be adversely affected by changes in market and economic conditions because we may not be able to reduce certain fixed costs within a time frame sufficient to match any decreases in revenue. Conditions such as an economic recession, stagflation, rising unemployment, the effects of tariffs, trade wars, elevated interest rates, inflationary prices, terrorism or political uncertainty and other factors beyond our control may adversely affect demand for our services and the ability to manage costs associated with employees and vendors. The future market and economic climate may deteriorate because of many factors beyond our control, including tariffs, elevated interest rates or inflation, terrorism or political uncertainty. In addition, the U.S. Federal Reserve changes the federal funds interest rate from time to time, and market interest rates have risen in recent periods. While the timing and impact of rising interest rates are unknown, a continued increase in market interest rates could have an adverse effect on our transaction volumes, results of operations and financial condition. In addition, in recent years, concerns arose with respect to the financial condition of a number of banking organizations in the United States, in particular those with exposure to certain types of depositors and large portfolios of investment securities. We maintain our cash at financial institutions, often with balances that exceed the current FDIC insurance limits. If any such financial institutions enter receivership or become insolvent in the future due to financial conditions affecting the banking system and financial markets, our ability to access our cash, cash equivalents and investments, including transferring funds, making payments or receiving funds, may be threatened and could have a material adverse effect on our business and financial condition. In addition, the operating environment and public trading prices of financial services sector securities can be highly correlated, in particular in times of stress, which may adversely affect the trading price of our Class A common stock and potentially our results of operations.

10

A substantial portion of our revenue is derived from advisory engagements in our CF and FR business segments, where a substantial portion of our fees tend to be contingent on the occurrence of goals, such as the completion of a transaction. As a result, our revenue and profits are highly volatile on a quarterly basis and may cause the price of our Class A common stock to fluctuate and decline.

Revenue and profits derived from our CF and FR business segments can be highly volatile. We derive a substantial portion of our revenue from advisory fees, which are mainly generated at key milestones, such as the closing of a transaction, the timing of which is outside of our control. In many cases, for advisory engagements that do not result in the successful consummation of a transaction, we are not paid a fee other than the reimbursement of certain out-of-pocket expenses and, in some cases, a modest retainer, despite having devoted considerable resources to these transactions. The achievement of these contractually-defined goals is often impacted by factors outside of our control, such as market conditions and the decisions and actions of our clients and interested third parties. For example, a client could delay or terminate an acquisition transaction because of a failure to agree upon final terms with the counterparty, failure to obtain necessary regulatory consents or board or shareholder approvals, failure to secure necessary financing, adverse market conditions or because the target's business is experiencing unexpected financial problems. Anticipated bidders for client assets during a restructuring transaction may not materialize or our client may not be able to restructure its operations or indebtedness due to a failure to reach agreement with its principal creditors. Because fees in such engagements are typically contingent, revenue on such engagements, which is recognized when all revenue recognition criteria are met, is not certain and the timing of receipt is difficult to predict and may not occur evenly throughout the year.

We expect that we will continue to rely on advisory fees, including fees based upon goals, such as the completion of a transaction, for a substantial portion of our revenue for the foreseeable future. Accordingly, a decline in our advisory engagements or the market for advisory services would adversely affect our business. In addition, our financial results will likely fluctuate from quarter to quarter based on when fees are earned, and high levels of revenue in one quarter will not necessarily be predictive of continued high levels of revenue in future periods. Should these contingent fee arrangements represent a greater percentage of our business in the future, we may experience increased volatility in our working capital requirements and greater variations in our quarter-to-quarter results, which could affect the price of our Class A common stock. Because advisory revenue can be volatile and represents a significant portion of our total revenue, we may experience greater variations in our revenue and profits than other larger, more diversified competitors in the financial services industry. Fluctuations in our quarterly financial results could, in turn, lead to large adverse movements in the price of our Class A common stock or increased volatility in our stock price generally.

Our acquisitions and strategic investments may result in additional risks and uncertainties in our businesses.

In addition to recruiting and organic expansion, we have grown, and intend to continue to grow, our core businesses through acquisitions and strategic investments.

We regularly evaluate opportunities to acquire other businesses whose key strategic benefit is the addition of financial professionals. Unless and until acquisitions of other businesses generate meaningful revenues, the purchase prices we pay to acquire such businesses could have a material adverse effect on our business, financial condition and results of operations. If we acquire a business, we may be unable to manage it profitably or successfully integrate its operations with our own. Moreover, we may be unable to realize the financial, operational, and other benefits we anticipate from acquisitions. Competition for future acquisition opportunities in our markets could increase the price we pay for businesses we acquire and could reduce the number of potential acquisition targets. Further, acquisitions may involve a number of special financial and business risks, including expenses related to any potential acquisition from which we may withdraw, diversion of our management's time, attention, and resources, decreased utilization during the integration process, loss of key acquired personnel, difficulties in integrating diverse corporate cultures, increased costs to improve or integrate personnel and financial, accounting, technology and other systems, including compliance with the Sarbanes-Oxley Act, dilutive issuances of equity securities, including convertible debt securities, incurrence of debt, the assumption of legal liabilities, amortization of acquired intangible assets, potential write-offs related to the impairment of goodwill, and additional conflicts of interest. If we are unable to successfully manage these risks, we will not be able to implement our growth strategy, which ultimately could materially adversely affect our business, financial condition and results of operations.

11

Goodwill and other intangible assets represent a significant portion of our assets, and an impairment of these assets could have a material adverse effect on our financial condition and results of operations.

Goodwill and other intangible assets represent a significant portion of our assets, and totaled $1.50 billion as of March 31, 2025. Goodwill is the excess of cost over the fair market value of net assets acquired in business combinations. We review goodwill and intangible assets at least annually for impairment. We may need to perform impairment tests more frequently if events occur or circumstances indicate that the carrying amount of these assets may not be recoverable. These events or circumstances could include a significant change in the business climate, attrition of key personnel, a prolonged decline in our stock price and market capitalization, legal factors, operating performance indicators, competition, sale or disposition of a significant portion of one of our businesses and other factors. Annual impairment reviews of indefinite-lived intangible assets or any future impairment of goodwill or other intangible assets would result in a non-cash charge against earnings, which would adversely affect our results of operations. The valuation of the reporting units requires judgment in estimating future cash flows, discount rates and other factors. In making these judgments, we evaluate the financial health of our reporting units, including such factors as market performance, changes in our client base and projected growth rates. Because these factors are ever changing, due to market and general business conditions, our goodwill and indefinite-lived intangible assets may be impaired in future periods.

Our international operations are subject to certain risks, which may affect our revenue.

In fiscal 2025, we earned approximately 28.8% of our revenue from our international operations. We intend to grow our non-United States business, including growth into new regions with which we have less familiarity and experience, and this growth is important to our overall success. Many of our larger clients are non-United States entities. Our international operations carry special financial and business risks, which could include the following:

•greater difficulties in managing and staffing foreign operations;

•fluctuations in foreign currency exchange rates that could adversely affect our results;

•unexpected and costly changes in trading policies, regulatory requirements, tariffs and other barriers;

•cultural and language barriers and the need to adopt different business practices in different geographic areas;

•longer transaction cycles;

•higher operating costs;

•local labor conditions and regulations;

•adverse consequences or restrictions on the repatriation of earnings;

•potentially adverse tax consequences, such as trapped foreign losses;

•potentially less stable political and economic environments;

•terrorism, political hostilities, war and other civil disturbances or other catastrophic events, such as the conflicts in Ukraine and Israel, that reduce business activity; and

•difficulty collecting fees.

As part of our day-to-day operations outside the United States, we are required to create compensation programs, employment policies, compliance policies and procedures and other administrative programs that comply with the laws of multiple countries. We also must communicate and monitor standards and directives across our global operations. Our failure to successfully manage and grow our geographically diverse operations could impair our ability to react quickly to changing business and market conditions and to enforce compliance with non-United States standards and procedures.

Any payment of distributions, loans or advances to and from our subsidiaries could be subject to restrictions on, or taxation of, dividends or repatriation of earnings under applicable local law, monetary transfer restrictions, foreign currency exchange regulations in the jurisdictions in which our subsidiaries operate or other restrictions imposed by current or future agreements, including debt instruments, to which our non-United States subsidiaries may be a party. Our business, financial condition and/or results of operations could be adversely impacted, possibly materially, if we are unable to successfully manage these and other risks of international operations in a volatile environment. If our international business increases relative to our total business, these factors could have a more pronounced effect on our operating results or growth prospects.

12

Although the current U.S. Presidential administration has signed an executive order to pause, subject to certain exceptions, the initiation of new investigations and enforcement actions under the FCPA, the United States Department of Justice and the SEC have historically devoted significant resources to enforcement of the FCPA. In addition, the United Kingdom has significantly expanded the reach of its anti-bribery laws. While we have developed and implemented policies and procedures designed to ensure strict compliance by us and our personnel with the FCPA and other anti-corruption laws, such policies and procedures may not be effective in all instances to prevent violations. Any determination that we have violated the FCPA (notwithstanding the current pause on FCPA investigations and enforcement action) or other applicable anti-corruption laws could subject us to, among other things, civil and criminal penalties, material fines, profit disgorgement, injunctions on future conduct, securities litigation and a general loss of investor confidence, any one of which could adversely affect our business prospects, financial condition, results of operations or the market value of our Class A common stock.

Fluctuations in foreign currency exchange rates could adversely affect our results.

Because our financial statements are denominated in United States Dollars and we receive a portion of our net revenue in other currencies, we are exposed to fluctuations in foreign currencies. In addition, we pay certain of our expenses in such currencies. Fluctuations in foreign currency exchange rates led to a net loss in cash of $(0.8) million for fiscal 2025, compared to a net loss in cash of $(0.4) million for fiscal 2024. In particular, we are exposed to the Euro, the Yen, and the Pound Sterling, and fluctuations in these and other currencies relative to the United States Dollar have had, and may continue to have, an adverse effect on our revenue. From time to time, we have entered into transactions to hedge our exposure to certain foreign currency fluctuations through the use of derivative instruments or other methods. Notwithstanding our entry into such hedge transactions, a depreciation of any of the currencies to which we are exposed relative to the United States Dollar could result in an adverse impact to our business, financial condition, results of operations and/or cash flows.

The cost of compliance with broker-dealer, employment, labor, benefits, and tax regulations may adversely affect our business and hamper our ability to expand internationally.

Because we operate our business both in the United States and internationally, we are subject to many distinct securities, employment, labor, benefits and tax laws in each country in which we operate, including regulations affecting our employment practices and our relations with our employees and service providers. If we are required to comply with new regulations or new interpretations of existing regulations, or if we are unable to comply with these regulations or interpretations, our business could be adversely affected or the cost of compliance may make it difficult to expand into new international markets. Additionally, our competitiveness in international markets may be adversely affected by regulations requiring, among other things, the awarding of contracts to local contractors, the employment of local citizens and/or the purchase of services from local businesses or favoring or requiring local ownership.

Our ability to retain our Managing Directors and our other senior professionals, as well as our ability to successfully identify, recruit and develop talent, is critical to the success of our business.

We depend on the efforts and reputations of our senior management and financial professionals. Our Managing Directors’ and other senior professionals’ reputations and relationships with clients and potential clients are critical elements in the success of our business. Our future success depends to a substantial degree on our ability to retain qualified management and financial professionals within our organization, including our Managing Directors. In addition, our future growth will depend on, among other things, our ability to successfully identify and recruit individuals and teams to join our firm. It typically takes time for these financial professionals to become profitable and effective. During that time, we may incur significant expenses and expend significant time and resources toward training, integration and business development aimed at developing this new talent. However, we may not be successful in our efforts to identify, recruit, train and retain the required personnel as the market for qualified investment bankers is extremely competitive. Our financial professionals possess substantial experience and expertise and have strong relationships with our advisory clients. As a result, the loss of these financial professionals could jeopardize our relationships with clients and result in the loss of client engagements. For example, if our Managing Directors or other senior professionals, including our executive officers, or groups of professionals, were to join or form a competing firm, some of our current clients could choose to use the services of that competitor rather than our services. Managing Directors and other senior professionals have left Houlihan Lokey in the past and others may do so in the future, and the departure of any of these senior professionals may have an adverse impact on our business. Our compensation arrangements and post-employment restriction agreements with our Managing Directors and other professionals may not provide sufficient incentives or protections to prevent these professionals from resigning to pursue other employment opportunities. In addition, recent initiatives at state and federal levels have sought to restrict or limit the enforceability of restrictive covenants, with several states having enacted such legislation, including California. In addition, some of our competitors have more resources than we do, which may allow them to attract some of our existing employees by offering superior compensation and benefits or otherwise. The departure of a number of Managing Directors or groups of senior professionals could have a material adverse effect on our business, financial condition and results of operations.

13

We are subject to reputational and legal risk arising from, among other things, actual or alleged employee misconduct, conflicts of interest, failure to meet client expectations or other operational failures.

As a professional services firm, our ability to secure new engagements is substantially dependent on our reputation and the individual reputations of our financial professionals. Any factor that diminishes our reputation or that of our financial professionals, including not meeting client expectations or actual or alleged misconduct by our financial professionals, including misuse of confidential information, could make it substantially more difficult for us to attract new engagements and clients.

In addition, we face the possibility of an actual, potential or perceived conflict of interest where we represent a client on a transaction in which an existing client is a party. We may be asked by two potential clients to act on their behalf on the same transaction, including by two clients as potential buyers in the same acquisition transaction. In each of these situations, we face the risk that our current policies, controls and procedures may not timely identify or appropriately manage such conflicts of interest. Conflicts may also arise from investments or activities of employees outside their business activities on behalf of the Company. It is possible that actual, potential or perceived conflicts could give rise to client dissatisfaction, litigation or regulatory enforcement actions. Appropriately identifying and managing actual or perceived conflicts of interest is complex and difficult, and our reputation could be damaged if we fail, or appear to fail, to deal appropriately with one or more potential or actual conflicts of interest. Regulatory scrutiny of, or litigation in connection with, conflicts of interest could have a material adverse effect on our reputation which could materially adversely affect our business in a number of ways, including a reluctance of some potential clients and counterparties to do business with us.

Further, because we provide our services primarily in connection with significant or complex transactions, disputes or other matters that usually involve confidential and sensitive information or are adversarial, and because our work is the product of myriad judgments of our financial professionals and other staff operating under significant time and other pressures, we may not always perform to the standards expected by our clients. In addition, we may face reputational damage from, among other things, litigation against us, our failure to protect confidential information. There is also a risk that our employees could engage in misconduct that could adversely affect our business. If our employees were to improperly use or disclose confidential information provided by our clients, we could be subject to regulatory sanctions and legal liability and suffer serious harm to our reputation, financial position, current client relationships and ability to attract future clients. It is not always possible to deter employee misconduct, and the precautions we take to detect and prevent misconduct may not be effective in all cases. In addition, our financial professionals and other employees are responsible for the security of the information in our systems or under our control and for ensuring that non-public information is kept confidential. Should any employee not follow appropriate security measures, the improper release or use of confidential information could result. If our employees engage in misconduct or fail to follow appropriate security measures, we could be subject to legal liability and reputational harm, which could impair our ability to attract and retain clients and in turn materially adversely affect our business.

We may be unable to execute on our growth initiatives, business strategies, or operating plans.

We are executing on a number of growth initiatives, strategies and operating plans designed to enhance our business. For example, we intend to continue to expand our platform into new industry and product sectors, both organically and through additional hires or acquisitions, and to expand our existing expertise into new geographies. The anticipated benefits from these efforts are based on several assumptions that may prove to be inaccurate. Moreover, we may not be able to complete successfully these growth initiatives, strategies and operating plans and realize all of the benefits, including growth targets and cost savings, we expect to achieve or it may be more costly to do so than we anticipate. A variety of factors could cause us not to realize some or all of the expected benefits. These factors include, among others: delays in the anticipated timing of activities related to such growth initiatives, strategies and operating plans; difficulty in competing in certain industries, product areas and geographies in which we have less experience than others; negative attention from any failed initiatives; and increased or unexpected costs in implementing these efforts.

In addition, sustaining growth will require us to commit additional management, operational and financial resources and to maintain appropriate operational and financial systems to adequately support expansion, especially in instances where we open new offices that may require additional resources before they become profitable. We may not be able to recruit and develop talent and manage our expanding operations effectively, and any failure to do so could materially adversely affect our ability to grow revenue and control our expenses.

Moreover, our continued implementation of these programs may disrupt our operations and performance. As a result, we may not realize the expected benefits from these plans. If, for any reason, the benefits we realize are less than our estimates or the implementation of these growth initiatives, strategies and operating plans adversely affect our operations or cost more or take longer to effectuate than we expect, or if our assumptions prove inaccurate, we will not be able to implement our growth strategy, which ultimately could materially adversely affect our business, financial condition and results of operations.

14

We are subject to risks relating to our operations, including our information and technology, which could harm our business.

We operate a business that is highly dependent on information systems and technology to securely process, transmit and store such information and to communicate among our locations around the world and with our employees, clients and vendors. Any failure to keep accurate books and records can render us liable to disciplinary action by governmental and self-regulatory authorities, as well as to claims by our clients. We rely on third-party service providers for certain aspects of our business. Any interruption or deterioration in the performance of these third parties or failures of their information systems and technology could impair our operations, affect our reputation and adversely affect our business.

Our clients typically provide us with sensitive and confidential information. We have been subject to attempted security breaches and cyber-attacks and, a successful breach could lead to shutdowns or disruptions of our systems or third-party systems on which we rely and potential unauthorized disclosure of sensitive or confidential information. Breaches of our security systems or third-party network security systems on which we rely could involve attacks that are intended to obtain unauthorized access to our proprietary information, client and third party information, destroy data or disable, degrade or sabotage our systems, often through the introduction of computer viruses, cyber-attacks and other means and could originate from a wide variety of sources, including unknown third parties outside the Company. As cyber-attack techniques evolve in response to enhanced detection and protection measures, cyber-attacks/threats/incidents could persist for an extended period of time before detection or escalation. There can be no assurance that the cybersecurity protections and controls utilized by us, or by our third parties on whom we rely, will be effective within this cyber threat landscape. For example, phishing and email spoofing attacks often seek to obtain information to impersonate employees or clients in order to, among other things, direct fraudulent bank transfers or obtain valuable information via social engineering. The proliferation of deepfake technology adds to these risks. Fraudulent transfers resulting from phishing attacks or email spoofing of our employees could result in a material loss of assets, reputational harm or legal liability and in turn materially adversely affect our business. In addition, our employees are responsible for following proper measures to maintain the confidentiality of information we hold. If our systems or third-party systems on which we rely are compromised or perceived to be compromised, do not operate properly or are disabled, or if an employee fails to follow proper measures resulting in the release of confidential information, we could suffer a disruption of our business, financial losses, liability to clients, regulatory sanctions and damage to our reputation.

We are exploring the integration of artificial intelligence technologies (“AI”) into our operations. The deployment of AI, which relies on substantial data volumes, introduces risks such as potential leakage of confidential or proprietary information, unauthorized access, misuse, or theft of sensitive data, and the possibility of competitors adopting AI more effectively, which could materially impact our business, financial condition, results of operations, or market share. Additionally, third-party service providers may independently implement AI solutions, which could further complicate our risk landscape.

In addition, a disaster or other business continuity problem, such as a pandemic, other man-made or natural disaster or disruption involving electronic communications or other services used by us or third parties with whom we conduct business, could lead us to experience operational challenges. The incidence and severity of catastrophes and other disasters are inherently unpredictable, and our inability to timely and successfully recover could materially disrupt our business and cause material financial loss, regulatory actions, reputational harm or legal liability.

Our revenue in any given period is dependent on the number of fee-paying clients in such period and the size of transactions on which we are advising, so a significant reduction in the number of fee-paying clients or the size of transactions in any given period could reduce our revenue and adversely affect our operating results in such period.

Our revenue in any given period is dependent on the number of fee-paying clients in such period and the size of transactions on which we are advising that close during such period. We may lose clients as a result of the sale or merger of a client, a change in a client's senior management, competition from other financial advisors and financial institutions and other causes. A significant reduction in the number of fee-paying clients and/or the size of transactions on which we are advising that close in any given period could reduce our revenue and adversely affect our operating results in such period.

15

Our clients may be unable to pay us for our services.