Exhibit 10.1

|

|

LOAN AGREEMENT

Dated as of January 22, 2013

Between

RP/HH PARK PLAZA, LIMITED PARTNERSHIP,

as Borrower

and

BANK OF AMERICA, N.A.,

as Lender

|

|

TABLE OF CONTENTS

|

|

|

Page |

|

|

|

|

|

ARTICLE 1 DEFINITIONS; PRINCIPLES OF CONSTRUCTION |

1 | |

|

|

| |

|

SECTION 1.1. |

DEFINITIONS |

1 |

|

SECTION 1.2. |

PRINCIPLES OF CONSTRUCTION |

29 |

|

|

|

|

|

ARTICLE 2 GENERAL TERMS |

29 | |

|

|

| |

|

SECTION 2.1. |

LOAN COMMITMENT; DISBURSEMENT TO BORROWER |

29 |

|

SECTION 2.2. |

INTEREST RATE |

30 |

|

SECTION 2.3. |

LOAN PAYMENTS |

31 |

|

SECTION 2.4. |

PREPAYMENTS |

32 |

|

|

|

|

|

ARTICLE 3 CONDITIONS PRECEDENT |

34 | |

|

|

| |

|

ARTICLE 4 REPRESENTATIONS AND WARRANTIES |

34 | |

|

|

|

|

|

SECTION 4.1. |

ORGANIZATION |

34 |

|

SECTION 4.2. |

STATUS OF BORROWER |

35 |

|

SECTION 4.3. |

VALIDITY OF DOCUMENTS |

35 |

|

SECTION 4.4. |

NO CONFLICTS |

35 |

|

SECTION 4.5. |

LITIGATION |

36 |

|

SECTION 4.6. |

AGREEMENTS |

36 |

|

SECTION 4.7. |

SOLVENCY |

36 |

|

SECTION 4.8. |

FULL AND ACCURATE DISCLOSURE |

37 |

|

SECTION 4.9. |

NO PLAN ASSETS |

37 |

|

SECTION 4.10. |

NOT A FOREIGN PERSON |

37 |

|

SECTION 4.11. |

ENFORCEABILITY |

37 |

|

SECTION 4.12. |

BUSINESS PURPOSES |

38 |

|

SECTION 4.13. |

COMPLIANCE |

38 |

|

SECTION 4.14. |

FINANCIAL INFORMATION |

38 |

|

SECTION 4.15. |

CONDEMNATION |

38 |

|

SECTION 4.16. |

UTILITIES AND PUBLIC ACCESS; PARKING |

39 |

|

SECTION 4.17. |

SEPARATE LOTS |

39 |

|

SECTION 4.18. |

ASSESSMENTS |

39 |

|

SECTION 4.19. |

INSURANCE |

40 |

|

SECTION 4.20. |

USE OF PROPERTY |

40 |

|

SECTION 4.21. |

CERTIFICATE OF OCCUPANCY; LICENSES |

40 |

|

SECTION 4.22. |

FLOOD ZONE |

40 |

|

SECTION 4.23. |

PHYSICAL CONDITION |

40 |

|

SECTION 4.24. |

BOUNDARIES |

41 |

|

SECTION 4.25. |

LEASES AND RENT ROLL |

41 |

|

SECTION 4.26. |

FILING AND RECORDING TAXES |

41 |

|

SECTION 4.27. |

MANAGEMENT AGREEMENT |

41 |

|

SECTION 4.28. |

ILLEGAL ACTIVITY |

41 |

|

SECTION 4.29. |

CONSTRUCTION EXPENSES |

42 |

|

SECTION 4.30. |

PERSONAL PROPERTY |

42 |

|

SECTION 4.31. |

TAXES |

42 |

|

SECTION 4.32. |

TITLE |

42 |

|

SECTION 4.33. |

FEDERAL RESERVE REGULATIONS |

43 |

|

SECTION 4.34. |

INVESTMENT COMPANY ACT |

43 |

|

SECTION 4.35. |

INTENTIONALLY BLANK |

43 |

|

SECTION 4.36. |

INTENTIONALLY BLANK |

43 |

|

SECTION 4.37. |

INTELLECTUAL PROPERTY |

43 |

|

SECTION 4.38. |

COMPLIANCE WITH ANTI-TERRORISM LAWS |

43 |

|

SECTION 4.39. |

PATRIOT ACT |

44 |

|

SECTION 4.40. |

BROKERS AND FINANCIAL ADVISORS |

44 |

|

SECTION 4.41. |

NON-CONSOLIDATION OPINION ASSUMPTIONS |

44 |

|

SECTION 4.42. |

FRANCHISE AGREEMENT |

44 |

|

SECTION 4.43. |

REIMBURSEMENT AND INDEMNITY AGREEMENT |

44 |

|

SECTION 4.44. |

SURVIVAL |

44 |

|

|

|

|

|

ARTICLE 5 BORROWER COVENANTS |

45 | |

|

|

|

|

|

SECTION 5.1. |

EXISTENCE; COMPLIANCE WITH LEGAL REQUIREMENTS |

45 |

|

SECTION 5.2. |

MAINTENANCE AND USE OF PROPERTY |

45 |

|

SECTION 5.3. |

WASTE |

46 |

|

SECTION 5.4. |

TAXES AND OTHER CHARGES |

46 |

|

SECTION 5.5. |

LITIGATION |

47 |

|

SECTION 5.6. |

ACCESS TO PROPERTY |

47 |

|

SECTION 5.7. |

NOTICE OF DEFAULT |

48 |

|

SECTION 5.8. |

COOPERATE IN LEGAL PROCEEDINGS |

48 |

|

SECTION 5.9. |

PERFORMANCE BY BORROWER |

48 |

|

SECTION 5.10. |

AWARDS; INSURANCE PROCEEDS |

48 |

|

SECTION 5.11. |

FINANCIAL REPORTING |

48 |

|

SECTION 5.12. |

ESTOPPEL STATEMENT |

50 |

|

SECTION 5.13. |

LEASING MATTERS |

51 |

|

SECTION 5.14. |

PROPERTY MANAGEMENT |

53 |

|

SECTION 5.15. |

LIENS |

54 |

|

SECTION 5.16. |

DEBT CANCELLATION |

54 |

|

SECTION 5.17. |

ZONING |

54 |

|

SECTION 5.18. |

ERISA |

54 |

|

SECTION 5.19. |

NO JOINT ASSESSMENT |

55 |

|

SECTION 5.20. |

RECIPROCAL EASEMENT AGREEMENTS |

55 |

|

SECTION 5.21. |

ALTERATIONS |

55 |

|

SECTION 5.22. |

FRANCHISE AGREEMENT |

56 |

|

SECTION 5.23. |

INTENTIONALLY BLANK |

56 |

|

SECTION 5.24. |

CONDOMINIUM PROVISIONS |

56 |

|

|

|

|

|

ARTICLE 6 ENTITY COVENANTS |

57 | |

|

|

|

|

|

SECTION 6.1. |

SINGLE PURPOSE ENTITY/SEPARATENESS |

57 |

|

SECTION 6.2. |

CHANGE OF NAME, IDENTITY OR STRUCTURE |

62 |

|

SECTION 6.3. |

BUSINESS AND OPERATIONS |

63 |

|

SECTION 6.4. |

INDEPENDENT MANAGER |

63 |

|

|

|

|

|

ARTICLE 7 NO SALE OR ENCUMBRANCE |

64 | |

|

|

| |

|

SECTION 7.1. |

TRANSFER DEFINITIONS |

64 |

|

SECTION 7.2. |

NO SALE/ENCUMBRANCE |

64 |

|

SECTION 7.3. |

PERMITTED TRANSFERS |

65 |

|

SECTION 7.4. |

LENDER’S RIGHTS |

66 |

|

SECTION 7.5. |

ASSUMPTION |

67 |

|

SECTION 7.6. |

PERMITTED MEZZANINE FINANCING |

70 |

|

SECTION 7.7. |

PERMITTED PREFERRED EQUITY |

71 |

|

SECTION 7.8. |

RETAIL SPACE RELEASE |

72 |

|

SECTION 7.9. |

DEBT |

74 |

|

|

|

|

|

ARTICLE 8 INSURANCE; CASUALTY; CONDEMNATION; RESTORATION |

74 | |

|

|

|

|

|

SECTION 8.1. |

INSURANCE |

74 |

|

SECTION 8.2. |

CASUALTY |

79 |

|

SECTION 8.3. |

CONDEMNATION |

79 |

|

SECTION 8.4. |

RESTORATION |

80 |

|

ARTICLE 9 RESERVE FUNDS |

85 | |

|

|

|

|

|

SECTION 9.1. |

REQUIRED REPAIRS |

85 |

|

SECTION 9.2. |

REPLACEMENTS |

85 |

|

SECTION 9.3. |

INTENTIONALLY BLANK |

86 |

|

SECTION 9.4. |

REQUIRED WORK |

86 |

|

SECTION 9.5. |

RELEASE OF RESERVE FUNDS |

88 |

|

SECTION 9.6. |

TAX AND INSURANCE RESERVE FUNDS |

90 |

|

SECTION 9.7. |

EXCESS CASH; OPERATING EXPENSES; EXTRAORDINARY EXPENSES |

91 |

|

SECTION 9.8. |

RESERVE FUNDS GENERALLY |

92 |

|

SECTION 9.9. |

LETTERS OF CREDIT |

95 |

|

SECTION 9.10. |

SEASONALITY RESERVE |

97 |

|

SECTION 9.11. |

INTENTIONALLY BLANK |

98 |

|

SECTION 9.12. |

ROOM SPLIT RESERVE |

98 |

|

|

|

|

|

ARTICLE 10 CASH MANAGEMENT |

100 | |

|

|

|

|

|

SECTION 10.1. |

LOCKBOX ACCOUNT AND CASH MANAGEMENT ACCOUNT |

100 |

|

SECTION 10.2. |

DEPOSITS AND WITHDRAWALS |

102 |

|

SECTION 10.3. |

SECURITY INTEREST |

106 |

|

SECTION 10.4. |

LENDER RELIANCE |

107 |

|

SECTION 10.5. |

BORROWER DISTRIBUTIONS |

108 |

|

|

|

|

|

ARTICLE 11 EVENTS OF DEFAULT; REMEDIES |

108 | |

|

|

|

|

|

SECTION 11.1. |

EVENT OF DEFAULT |

108 |

|

SECTION 11.2. |

REMEDIES |

111 |

|

|

|

|

|

ARTICLE 12 ENVIRONMENTAL PROVISIONS |

112 | |

|

|

|

|

|

SECTION 12.1. |

ENVIRONMENTAL REPRESENTATIONS AND WARRANTIES |

112 |

|

SECTION 12.2. |

ENVIRONMENTAL COVENANTS |

113 |

|

SECTION 12.3. |

LENDER’S RIGHTS |

114 |

|

SECTION 12.4. |

OPERATIONS AND MAINTENANCE |

114 |

|

SECTION 12.5. |

ENVIRONMENTAL DEFINITIONS |

114 |

|

|

|

|

|

ARTICLE 13 SECONDARY MARKET |

115 | |

|

|

|

|

|

SECTION 13.1. |

TRANSFER OF LOAN |

115 |

|

SECTION 13.2. |

DELEGATION OF SERVICING |

115 |

|

SECTION 13.3. |

DISSEMINATION OF INFORMATION |

116 |

|

SECTION 13.4. |

COOPERATION |

116 |

|

SECTION 13.5. |

SECURITIZATION |

119 |

|

SECTION 13.6. |

REGULATION AB INFORMATION |

122 |

|

SECTION 13.7. |

REGISTER |

123 |

|

SECTION 13.8. |

INTENTIONALLY BLANK |

123 |

|

SECTION 13.9. |

INTERCREDITOR AGREEMENT |

123 |

|

|

|

|

|

ARTICLE 14 INDEMNIFICATIONS |

124 | |

|

|

|

|

|

SECTION 14.1. |

GENERAL INDEMNIFICATION |

124 |

|

SECTION 14.2. |

MORTGAGE AND INTANGIBLE TAX INDEMNIFICATION |

124 |

|

SECTION 14.3. |

ERISA INDEMNIFICATION |

124 |

|

SECTION 14.4. |

SURVIVAL |

125 |

|

|

|

|

|

ARTICLE 15 EXCULPATION |

125 | |

|

|

|

|

|

SECTION 15.1. |

EXCULPATION |

125 |

|

|

|

|

|

ARTICLE 16 NOTICES |

128 | |

|

|

|

|

|

SECTION 16.1. |

NOTICES |

128 |

|

|

|

|

|

ARTICLE 17 FURTHER ASSURANCES |

129 | |

|

|

|

|

|

SECTION 17.1. |

REPLACEMENT DOCUMENTS |

129 |

|

SECTION 17.2. |

RECORDING OF MORTGAGE, ETC. |

129 |

|

SECTION 17.3. |

FURTHER ACTS, ETC. |

130 |

|

SECTION 17.4. |

CHANGES IN TAX, DEBT, CREDIT AND DOCUMENTARY STAMP LAWS |

130 |

|

SECTION 17.5. |

EXPENSES |

131 |

|

SECTION 17.6. |

COST OF ENFORCEMENT |

132 |

|

|

|

|

|

ARTICLE 18 WAIVERS |

132 | |

|

|

|

|

|

SECTION 18.1. |

REMEDIES CUMULATIVE; WAIVERS |

132 |

|

SECTION 18.2. |

MODIFICATION, WAIVER IN WRITING |

132 |

|

SECTION 18.3. |

DELAY NOT A WAIVER |

133 |

|

SECTION 18.4. |

TRIAL BY JURY |

133 |

|

SECTION 18.5. |

WAIVER OF NOTICE |

133 |

|

SECTION 18.6. |

REMEDIES OF BORROWER |

133 |

|

SECTION 18.7. |

WAIVER OF MARSHALLING OF ASSETS |

134 |

|

SECTION 18.8. |

WAIVER OF STATUTE OF LIMITATIONS |

134 |

|

SECTION 18.9. |

WAIVER OF COUNTERCLAIM |

134 |

|

|

|

|

|

ARTICLE 19 GOVERNING LAW |

134 | |

|

|

|

|

|

SECTION 19.1. |

CHOICE OF LAW |

134 |

|

SECTION 19.2. |

SEVERABILITY |

136 |

|

SECTION 19.3. |

PREFERENCES |

136 |

|

|

|

|

|

ARTICLE 20 MISCELLANEOUS |

136 | |

|

|

|

|

|

SECTION 20.1. |

SURVIVAL |

136 |

|

SECTION 20.2. |

LENDER’S DISCRETION |

136 |

|

SECTION 20.3. |

HEADINGS |

136 |

|

SECTION 20.4. |

SCHEDULES INCORPORATED |

137 |

|

SECTION 20.5. |

OFFSETS, COUNTERCLAIMS AND DEFENSES |

137 |

|

SECTION 20.6. |

NO JOINT VENTURE OR PARTNERSHIP; NO THIRD PARTY BENEFICIARIES |

137 |

|

SECTION 20.7. |

PUBLICITY |

138 |

|

SECTION 20.8. |

CONFLICT; CONSTRUCTION OF DOCUMENTS; RELIANCE |

138 |

|

SECTION 20.9. |

DUPLICATE ORIGINALS; COUNTERPARTS |

139 |

|

SECTION 20.10. |

ENTIRE AGREEMENT |

139 |

LOAN AGREEMENT

THIS LOAN AGREEMENT, dated as of January 22, 2013 (as amended, restated, replaced, supplemented or otherwise modified from time to time pursuant to the terms hereof, this “Agreement”), between BANK OF AMERICA, N.A., a national banking association, having an address at 214 North Tryon Street, NC1-027-15-01, Charlotte, North Carolina 28255 (together with its successors and/or assigns, “Lender”) and RP/HH PARK PLAZA, LIMITED PARTNERSHIP, a Delaware limited partnership, having an address at c/o Rockpoint Group, L.L.C., Woodlawn at Old Parkland, 3953 Maple Avenues, Suite 300, Dallas, Texas 75219 (together with its successors and/or assigns, “Borrower”).

RECITALS:

Borrower desires to obtain the Loan (defined below) from Lender.

Lender is willing to make the Loan to Borrower, subject to and in accordance with the terms of this Agreement and the other Loan Documents (defined below).

In consideration of the making of the Loan by Lender and the covenants, agreements, representations and warranties set forth in this Agreement, the parties hereto hereby covenant, agree, represent and warrant as follows:

ARTICLE 1

DEFINITIONS; PRINCIPLES OF CONSTRUCTION

Section 1.1. DEFINITIONS

For all purposes of this Agreement, except as otherwise expressly required or unless the context clearly indicates a contrary intent:

“Acceptable Accountant” shall mean (i) PricewaterhouseCoopers LLP (provided that there has been no material adverse change to its financial condition, reputation or ability to conduct its business in the ordinary course), (ii) another “Big Four” accounting firm or (iii) an independent certified public accountant acceptable to Lender.

“Account Maintenance Subaccount” shall have the meaning set forth in Section 10.1(e) hereof.

“Act” shall have the meaning set forth in Section hereof.

“Additional Replacement” shall have the meaning set forth in Section 9.5(g) hereof.

“Additional Required Repair” shall have the meaning set forth in Section 9.5(f) hereof.

“Affiliate” shall mean, as to any Person, any other Person that (i) owns directly or indirectly ten percent (10%) or more of all equity interests in such Person or (ii) is in Control of, is Controlled by or is under common Control with such Person.

“Affiliated Manager” shall mean any manager in which Borrower, Borrower Principal, any SPE Component Entity or any Affiliate of such entities has, directly or indirectly, any legal, beneficial or economic interest.

“ALTA” shall mean American Land Title Association, or any successor thereto.

“Alteration Threshold” shall mean $3,500,000.

“Annual Budget” shall mean the operating budget for the applicable fiscal year of Borrower detailing on a monthly basis, consistent with the manner in which Borrower’s operating statements are presented as of the date hereof, projected cash flow for such fiscal year, including all planned capital expenditures, for the Property approved by Lender in accordance with Section 5.11(a)(v) hereof.

“Approved Bank” shall mean Citibank, N.A. or another commercial bank with a long term debt obligation rating of A+ or better (or a comparable long term debt obligation rating) as assigned by the Rating Agencies and otherwise satisfactory to Lender in its reasonable discretion.

“Approved Transferee” shall mean a Transferee who, together with its Affiliates, individually or in the aggregate: (a) have not less than seven (7) years experience in the ownership and/or management of hotels of 350 rooms or greater and of similar quality as the Property and have (or have had during the seven (7) years prior to the proposed assumption) not less than 3,500 rooms under ownership or management), (b) have total assets or assets under management in excess of $500,000,000 and a Net Worth of at least $250,000,000 and (c) have not in the last ten (10) years made an assignment for the benefit of creditors or taken advantage of any Creditors’ Rights Laws.

“Assignment of Management Agreement” shall mean that certain Assignment and Subordination of Management Agreement and Consent of Manager dated the date hereof among Lender, Borrower and Manager, as the same may be amended, restated, replaced, supplemented or otherwise modified from time to time.

“Award” shall mean any compensation paid by any Governmental Authority in connection with a Condemnation in respect of all or any part of the Property.

“Bankruptcy Code” shall mean Title 11 of the United States Code entitled “Bankruptcy”, as amended from time to time, and any successor statute or statutes and all rules and regulations from time to time promulgated thereunder, and any comparable foreign laws relating to bankruptcy, insolvency or creditors’ rights.

“Borrower Adverse Change” shall have the meaning set forth in Section 13.4 hereof.

“Borrower Party” shall mean Borrower and Borrower Principal.

“Borrower Principal” shall mean Rockpoint Real Estate Fund III, L.P.

“Borrower Subaccount” shall have the meaning set forth in Section Section 10.2(c) hereof.

“Borrower’s Account” shall mean that certain operating account with Bank of America in the name of Borrower having account number 4427170014.

“Budget Deemed Approval Requirements” shall mean, with respect to Lender’s approval of (1) the Annual Budget in accordance with Section 5.11(a)(v) hereof or (2) a Budget Variance Request in accordance with Section 5.11(a)(vi) hereof, that (i) no Event of Default shall have occurred and be continuing (either at the date of any notices specified below or as of the effective date of any deemed approval), (ii) Borrower shall have sent Lender a written request for approval with respect to the approval of the Annual Budget or the Budget Variance Request, as applicable, in accordance with the terms and conditions hereof (the “Budget Initial Notice”), which such Budget Initial Notice shall have been (A) accompanied by any and all required information and documentation relating thereto as may be reasonably required in order to approve or disapprove such Annual Budget or Budget Variance Request, as applicable, (the “Budget Approval Information”) and (B) marked in bold lettering with the following language: “LENDER’S RESPONSE IS REQUIRED WITHIN TEN (10) DAYS OF RECEIPT OF THIS NOTICE PURSUANT TO THE TERMS OF A LOAN AGREEMENT BETWEEN THE UNDERSIGNED AND LENDER” and the envelope containing the Budget Initial Notice shall have been marked “PRIORITY-DEEMED APPROVAL MAY APPLY”; (iii) Lender shall have failed to respond to the Budget Initial Notice within the aforesaid time-frame; (iv) Borrower shall have submitted a second request for approval with respect to such Annual Budget or Budget Variance Request, as applicable, in accordance with the terms and conditions hereof (the “Budget Second Notice”), which such Budget Second Notice shall have been (A) accompanied by the Budget Approval Information and (B) marked in bold lettering with the following language: “LENDER’S RESPONSE IS REQUIRED WITHIN TEN (10) DAYS OF RECEIPT OF THIS NOTICE PURSUANT TO THE TERMS OF A LOAN AGREEMENT BETWEEN THE UNDERSIGNED AND LENDER” and the envelope containing the Budget Second Notice shall have been marked “PRIORITY-DEEMED APPROVAL MAY APPLY”; and (v) Lender shall have failed to respond to the Budget Second Notice within the aforesaid time-frame. For purposes of clarification, Lender requesting additional and/or clarified information, in addition to approving or denying any request (in whole or in part), shall be deemed a response by Lender for purposes of the foregoing. Borrower and Lender acknowledge and agree that approval of the foregoing must be obtained (or deemed to have been obtained) by each of Lender and Mezzanine Lender before approval shall be deemed granted for so long as the Mezzanine Loan or Permitted Mezzanine Financing remains outstanding.

“Budget Variance Request” shall have the meaning set forth in Section 5.11(a)(vi) hereof.

“Business Day” shall mean any day other than (i) a Saturday or a Sunday or (ii) a day on which federally insured depository institutions in the States of New York or North

Carolina or the state in which the offices of Servicer are located are authorized or obligated by law, governmental decree or executive order to be closed.

“By-Laws” shall mean those certain by-laws attached to the Declaration providing for the operation of the Condominium, as the same may be amended, supplemented, replaced or otherwise modified from time to time.

“Cash Flow Adjustments” shall mean adjustments proposed by Borrower and reasonably approved by Lender to Borrower’s calculation of Underwritten Net Cash Flow and the components thereof, which adjustments shall be made only for items of a non-recurring nature (it being acknowledged that non-recurring expenses shall be capitalized in accordance with GAAP (or such other method of accounting reasonably acceptable to Lender) in calculating Underwritten Net Cash Flow).

“Cash Management Account” shall have the meaning set forth in Section 10.1(b) hereof.

“Cash Sweep Period” shall mean the period commencing on the date the Debt Yield is less than the Trigger Debt Yield on a trailing twelve (12) month basis as reasonably determined by Lender in accordance with the terms of this Agreement and ending on the date the Debt Yield first equals or exceeds the Termination Debt Yield for the immediately preceding two (2) calendar quarters as reasonably determined by Lender in accordance with the terms of this Agreement.

“Casualty” shall have the meaning set forth in Section 8.2 hereof.

“Cause” shall mean, with respect to an Independent Manager, (i) acts or omissions by such Independent Manager that constitute willful disregard of such Independent Manager’s duties as set forth in Borrower’s organizational documents, (ii) that such Independent Manager has engaged in or has been charged with, or has been convicted of, fraud or other acts constituting a crime under any law applicable to such Independent Manager, (iii) that such Independent Manager is unable to perform his or her duties as Independent Manager due to death, disability or incapacity, or (iv) that such Independent Manager no longer meets the definition of Independent Manager.

“Closing Date” shall mean the date of the funding of the Loan.

“Common Charges” shall mean all common charges and special assessments imposed pursuant to the Condominium Documents.

“Common Elements” shall have the meaning set forth in the Condominium Documents.

“Condemnation” shall mean a temporary or permanent taking by any Governmental Authority as the result, in lieu or in anticipation, of the exercise of the right of condemnation or eminent domain, of all or any part of the Property, or any interest therein or right accruing thereto, including any right of access thereto or any change of grade affecting the Property or any part thereof.

“Condemnation Proceeds” shall have the meaning set forth in Section 8.4(b) hereof.

“Condominium” shall mean The Park Plaza Condominium established pursuant to the Declaration.

“Condominium Act” shall mean the Chapter 183A of the Massachusetts General Laws, Condominiums, as the same may be amended, modified and/or supplemented from time to time.

“Condominium Board” shall mean the “Board”, the “Board of Directors” or the “Condominium Board” (as described in the Declaration) managing the Condominium by virtue of the Condominium Act, and the Condominium Documents, on behalf of all the owners of the Units comprising the Condominium.

“Condominium Board Policy” shall have the meaning set forth in Section 8.1.

“Condominium Documents” shall mean, collectively, the Declaration and the By-Laws.

“Condominium Proxy” shall mean an irrevocable proxy given by Borrower to Lender substantially in the form attached hereto as Exhibit E.

“Constituent Members” shall have the meaning set forth in Section 6.4(a) hereof.

“Control” shall mean, with respect to any Person, the possession, directly or indirectly, of the power to direct or cause the direction of the management and policies of such Person, whether through the ownership of voting securities or other beneficial interests, by contract or otherwise. The terms “Controlled” and “Controlling” shall have correlative meanings.

“Control Parties” shall mean individually and/or collectively, as the context may require, (A) Highgate, (B) Borrower Principal and/or (C) an entity wholly owned and Controlled by either of the foregoing.

“Covered Rating Agency Information” shall have the meaning specified in Section 13.5(f) hereof.

“Credit Card Direction Letter” shall have the meaning set forth in Section 10.2(a)(i) hereof.

“Creditors’ Rights Laws” shall mean with respect to any Person any existing or future law of any jurisdiction, domestic or foreign, relating to bankruptcy, insolvency, reorganization, conservatorship, arrangement, adjustment, winding-up, liquidation, dissolution, composition or other relief with respect to its debts or debtors under the Bankruptcy Code or any other federal or state bankruptcy or insolvency law.

“Custodial Funds” shall mean (i) sales, use and occupancy or other taxes (whether added on to the sales price or included therein) collected from hotel guests or patrons and either remitted, or required to be remitted to appropriate taxing authorities; (ii) the portion of tips, gratuities or service charges with respect to food, beverage, banquet or other guest services to be paid to and retained by employees and to the extent paid in the ordinary course of business and in accordance with industry practice, (iii) the portion of rooms, baggage, handling or service fees to be paid to and retained by employees, (iv) the portion of any movie rental payments to be paid to and retained by the third-party movie service providers; (v) amounts paid out to hotel guests or patrons for checks cashed and (vi) any other funds collected by Borrower on a third party’s behalf that must be paid or remitted to a third party that is not an Affiliate of Borrower or any Borrower Principal pursuant to agreements or other arrangements that are approved by Lender in writing (such approval not to be unreasonably withheld, delayed or conditioned so long as such agreements are consistent with industry practice) and so are not properly considered “revenue” of Borrower including, without limitation, the following: (A) payments or fees received from or on behalf of hotel guests or patrons and paid to any third party service provider, and (B) amounts collected from hotel guests or patrons on behalf of hotel tenants or any other third party that is not an Affiliate of Borrower or any Borrower Principal.

“DBRS” shall mean DBRS, Inc.

“Debt” shall mean the outstanding principal amount set forth in, and evidenced by, this Agreement and the Note together with all interest accrued and unpaid thereon and all other sums due to Lender in respect of the Loan under the Note, this Agreement, the Mortgage or any other Loan Document.

“Debt Service” shall mean, with respect to any particular period of time, scheduled principal and/or interest payments under the Note and this Agreement.

“Debt Service Subaccount” shall have the meaning set forth in Section 10.1(b)(iii) hereof.

“Debt Yield” shall mean, as of any date of calculation, the quotient, expressed as a percentage, obtained by dividing:

(a) Net Operating Income for the applicable trailing period specified in this Agreement and ending on such date of calculation; by

(b) the aggregate principal amount of the Loan and the Mezzanine Loan (less any amounts then on deposit in the Low Debt Yield Reserve Account or similar reserve or holdback accounts established and maintained in connection with the Permitted Mezzanine Financing) then outstanding on such date of calculation.

“Declaration” shall mean that certain Declaration of Trust of The Park Plaza Condominium Trust, Boston, Massachusetts dated as of July 11, 2011 and recorded with the Suffolk County Registry of Deeds in Book 49811, Page 286.

“Deemed Approval Requirements” shall mean, with respect to any matter, that (i) no Event of Default shall have occurred and be continuing (either at the date of any notices

specified below or as of the effective date of any deemed approval), (ii) Borrower shall have sent Lender a written request for approval with respect to such matter in accordance with the applicable terms and conditions hereof (the “Initial Notice”), which such Initial Notice shall have been (A) accompanied by any and all required information and documentation relating thereto as may be reasonably required in order to approve or disapprove such matter (the “Approval Information”) and (B) marked in bold lettering with the following language: “LENDER’S RESPONSE IS REQUIRED WITHIN FIFTEEN (15) BUSINESS DAYS OF RECEIPT OF THIS NOTICE PURSUANT TO THE TERMS OF A LOAN AGREEMENT BETWEEN THE UNDERSIGNED AND LENDER” and the envelope containing the Initial Notice shall have been marked “PRIORITY-DEEMED APPROVAL MAY APPLY”; (iii) Lender shall have failed to respond to the Initial Notice within the aforesaid time-frame; (iv) Borrower shall have submitted a second request for approval with respect to such matter in accordance with the applicable terms and conditions hereof (the “Second Notice”), which such Second Notice shall have been (A) accompanied by the Approval Information and (B) marked in bold lettering with the following language: “LENDER’S RESPONSE IS REQUIRED WITHIN FIFTEEN (15) BUSINESS DAYS OF RECEIPT OF THIS NOTICE PURSUANT TO THE TERMS OF A LOAN AGREEMENT BETWEEN THE UNDERSIGNED AND LENDER” and the envelope containing the Second Notice shall have been marked “PRIORITY-DEEMED APPROVAL MAY APPLY”; and (v) Lender shall have failed to respond to the Second Notice within the aforesaid time-frame. For purposes of clarification, Lender requesting additional and/or clarified information, in addition to approving or denying any request (in whole or in part), shall be deemed a response by Lender for purposes of the foregoing. Borrower and Lender acknowledge and agree that approval of the foregoing must be obtained (or deemed to have been obtained) by each of Lender and Mezzanine Lender before approval shall be deemed granted for so long as the Mezzanine Loan or Permitted Mezzanine Financing remains outstanding.

“Default” shall mean the occurrence of any event hereunder or under any other Loan Document which, but for the giving of notice or passage of time, or both, would be an Event of Default.

“Default Rate” shall mean a rate per annum equal to the lesser of (a) the Maximum Legal Rate and (b) four percent (4%) above the Note Rate.

“Disclosure Document” shall have the meaning set forth in Section 13.5(a) hereof.

“Disregarded Entity” shall mean an entity disregarded from its owner for U.S. federal income tax purposes.

“Eligible Account” shall mean a separate and identifiable account from all other funds held by the holding institution that is either (a) an account or accounts maintained with a federal or state chartered depository institution or trust company acting in its fiduciary capacity which complies with the definition of Eligible Institution, (b) a segregated trust account or accounts maintained with the corporate trust department of a federal or state chartered depository institution or trust company acting in its fiduciary capacity which, in the case of a federally chartered depository institution or trust company acting in its fiduciary capacity is subject to the regulations regarding fiduciary funds on deposit therein under 12 C.F.R. §9.10(b), and in the

case of a state chartered depository institution or trust company, is subject to regulations substantially similar to 12 C.F.R. §9.10(b), having in either case a combined capital surplus of at least $50,000,000 and subject to supervision or examination by federal and state authority or (c) an account otherwise approved by Lender in its sole discretion. An Eligible Account shall not be evidenced by a certificate of deposit, passbook or other instrument.

“Eligible Institution” shall mean Bank of America, N.A., Citibank, N.A. or another depository institution or trust company insured by the Federal Deposit Insurance Corporation (a) the short term unsecured debt obligations, commercial paper or other short term deposits of which are rated at least “A-1” by S&P, “P-1” by Moody’s, “F-1” by Fitch and “R-1 (middle)” by DBRS, in the case of accounts in which funds are held for thirty (30) days or less, or (b) the long term unsecured debt obligations of which are rated at least “AA-” by S&P (or “A-” if the short term unsecured debt obligations are rated at least “A-1” by S&P), “A2” by Moody’s, “AA-” by Fitch (or “A-” if the short term unsecured debt obligations are rated at least “F-1” by Fitch) and “A” by DBRS, in the case of accounts in which funds are held for more than thirty (30) days; provided that after a Securitization only the foregoing ratings requirements of each Rating Agency rating such Securitization shall apply. Notwithstanding the foregoing, prior to a Securitization, Bank of America, N.A. shall be an Eligible Institution regardless of any contrary requirement above.

“Embargoed Person” shall mean any person identified by OFAC or any other Person with whom a Person resident in the United States of America may not conduct business or transactions by prohibition of federal law or Executive Order of the President of the United States of America.

“Environmental Indemnity” shall mean that certain Environmental Indemnity Agreement, dated as of the date hereof, executed by Borrower in connection with the Loan for the benefit of Lender, as the same may be amended, restated, replaced, supplemented or otherwise modified from time to time.

“Environmental Law” shall have the meaning set forth in Section 12.5 hereof.

“Environmental Liens” shall have the meaning set forth in Section 12.5 hereof.

“Environmental Report” shall have the meaning set forth in Section 12.5 hereof.

“ERISA” shall mean the Employee Retirement Income Security Act of 1974, as amended from time to time and any successor statutes thereto and applicable regulations issued pursuant thereto in temporary or final form.

“Event of Default” shall have the meaning set forth in Section 11.1 hereof.

“Excess Cash” shall have the meaning set forth in Section 10.2(c) hereof.

“Excess Cash Reserve Account” shall have the meaning set forth in Section 9.7 hereof.

“Excess Cash Reserve Funds” shall have the meaning set forth in Section 9.7 hereof.

“Excess Cash Subaccount” shall have the meaning set forth in Section 10.1(b)(vii) hereof.

“Exchange Act” shall mean the Securities and Exchange Act of 1934, as amended.

“Exchange Act Filing” shall have the meaning set forth in Section 13.6(a) hereof.

“Excluded Taxes” shall mean any of the following Taxes imposed on or with respect to any Recipient or required to be withheld or deducted from a payment to a Recipient, (a) Taxes imposed on (or measured by) its net income (however denominated), franchise Taxes, and branch profits Taxes, in each case, (i) imposed by the jurisdiction (or any political subdivision thereof) under the laws of which such Recipient is organized or in which its principal office is located or, in the case of any Lender, in which its applicable lending office is located, or (ii) imposed as a result of a present or former connection between such Recipient and the jurisdiction imposing such Tax (other than connections arising solely from such Recipient having executed, delivered, become a party to, or performed its obligations under any Loan Document), (b) any withholding Taxes (including backup withholding) imposed on amounts payable to or for the account of any such Recipient pursuant to a law in effect on the date on which such Recipient acquires such interest in the Loan or becomes a Servicer of this Loan (or, in each case, designates a new lending office), (c) Taxes attributable to such Recipient’s failure or inability to comply with Section 2.4(b) hereof, (d) any Taxes imposed under FATCA, and (e) any liabilities, penalties, interest and additions to tax with respect to any of the foregoing.

“Exculpated Parties” shall have the meaning set forth in Section 15.1(a) hereof.

“Extraordinary Expense” shall mean an operating expense or capital expenditure with respect to the Property that (i) is not set forth on the Annual Budget approved by Lender (subject to the Permitted Variances), (ii) is not an Operating Expense that has been approved by Lender or a Non-Discretionary Expense, and (iii) is not subject to payment by withdrawals from the Required Repair Account, the Room Split Reserve Account, or the Replacement Reserve Account.

“Extraordinary Expense Subaccount” shall have the meaning set forth in Section 10.1(b)(vi) hereof.

“FATCA” shall mean Sections 1471 through 1474 of the Internal Revenue Code, as of the date of this Agreement, any current or future regulations or official interpretations thereof, and any agreements entered into pursuant to Section 1471(b)(1) of the Code (or any amended or successor versions of any of the foregoing).

“FF&E” shall mean, all fixtures, furnishings, equipment (including operating equipment, operating supplies and fixtures attached to and forming part of the Improvements), apparatus and other tangible personal property owned by Borrower and used in, or held in storage for use in (or if the context so dictates, required in connection with), or required for the

operation of that portion of the Property to be used as a hotel in accordance with this Agreement, including without limitation, (i) office furnishings and equipment, (ii) specialized hotel equipment necessary for the operation of the Property, including equipment for kitchens, laundries, dry cleaning facilities, bars, restaurants, public rooms, guest rooms, guest bathrooms, corridors, commercial and parking space, spa and recreational facilities, (iii) flooring, floor coverings, wall coverings, paint, window treatments, (iv) design and project fees, shipping costs, taxes, warehousing and installation, and (v) all other furniture, fixtures and equipment as Borrower reasonably deems necessary for the operation of that portion of the Property to be used as a hotel in accordance with this Agreement, provided the same is comparable to furniture, fixtures and equipment at similarly situated hotels in a comparable market segment.

“Fitch” shall mean Fitch, Inc.

“Franchise Agreement” shall mean any franchise agreement or similar agreement, between Borrower and a franchisor, as the same may be amended or modified from time to time.

“GAAP” shall mean generally accepted accounting principles in the United States of America as of the date of the applicable financial report.

“Governmental Authority” shall mean any court, board, agency, department, commission, office or other authority of any nature whatsoever for any governmental unit (federal, state, county, municipal, city, town, special district or otherwise) whether now or hereafter in existence.

“Guaranty” shall mean that certain Guaranty of Recourse Obligations of Borrower, dated as of the date hereof, from Borrower Principal to Lender, as the same may be amended, restated, replaced, supplemented or otherwise modified from time to time.

“Hazardous Materials” shall have the meaning set forth in Section 12.5 hereof.

“Highgate” shall mean (a) Mahmood Khimji, an individual, (b) Mehdi Khimji, an individual, (c) Mahmood Khimji and Mehdi Khimji, or (d) any Person Controlled by any combination of any of the foregoing.

“Improvements” shall have the meaning set forth in the granting clause of the Mortgage.

“Indemnified Liabilities” shall have the meaning set forth in Section 14.1 hereof.

“Indemnified Parties” shall mean (a) Lender, (b) any prior owner or holder of the Loan or any portion thereof or interest therein, (c) any servicer or prior servicer of the Loan, (d) any Investor or any prior Investor in any Securities, (e) any trustees, custodians or other fiduciaries who hold or who have held a full or partial interest in the Loan for the benefit of any Investor or other third party, (f) any receiver or other fiduciary appointed by Lender in a foreclosure or other Creditors’ Rights Laws proceeding, (g) any officers, directors, shareholders, partners, members, employees, agents, servants, representatives, contractors, subcontractors, affiliates or subsidiaries of any and all of the foregoing, and (h) the heirs, legal representatives,

successors and assigns of any and all of the foregoing (including, without limitation, any successors by merger, consolidation or acquisition of all or a substantial portion of the Indemnified Parties’ assets and business), in all cases whether during the term of the Loan or as part of or following a foreclosure of the Mortgage.

“Independent Manager” of any corporation or limited liability company shall mean an individual with at least three (3) years of employment experience servicing as an independent director at the time of appointment who is provided by, and is in good standing with, CT Corporation, Corporation Service Company, National Registered Agents, Inc., Wilmington Trust Company, Stewart Management Company, Lord Securities Corporation or, if none of those companies is then providing professional independent directors or managers or is not acceptable to the Rating Agencies, another nationally-recognized company reasonably approved by Lender and if required by Lender following the Securitization of the Loan, the Rating Agencies, in each case that is not an Affiliate of such corporation or limited liability company and that provides professional independent directors or managers and other corporate services in the ordinary course of its business, and which individual is duly appointed as a member of the board of directors or board of managers of such corporation or limited liability company and is not, and has never been, and will not while serving as independent director or manager be:

(i) a member (other than an independent, non-economic “springing” member), partner, equityholder, manager, director, officer or employee of such corporation or limited liability company or any of its equityholders or Affiliates (other than as an independent director or manager of an Affiliate of such corporation or limited liability company that is not in the direct chain of ownership of such corporation or limited liability company and that is required by a creditor to be a single purpose bankruptcy remote entity, provided that such independent director or manager is employed by a company that routinely provides professional independent directors or managers in the ordinary course of business);

(ii) a customer, creditor, supplier or service provider (including provider of professional services) to such corporation or limited liability company or any of its equityholders or Affiliates (other than a nationally-recognized company that routinely provides professional independent directors or managers and other corporate services to such corporation or limited liability company or any of its respective equityholders or Affiliates in the ordinary course of business);

(iii) a family member of any such member, partner, equityholder, manager, director, officer, employee, creditor, supplier or service provider; or

(iv) a Person that Controls or is under common Control with (whether directly, indirectly or otherwise) any of (i), (ii) or (iii) above.

A natural person who otherwise satisfies the foregoing definition other than subparagraph (i) by reason of being the independent director or manager of a single purpose bankruptcy remote

entity in the direct chain of ownership of such corporation or limited liability company shall not be disqualified from serving as an independent director or manager of such corporation or limited liability company, provided that the fees that such individual earns from serving as independent directors or managers of such Affiliates in any given year constitute in the aggregate less than five percent (5%) of such individual’s annual income for that year. For purposes of this paragraph, a “special purpose entity” is an entity whose organizational documents contain restrictions on its activities and impose requirements intended to preserve such entity’s separateness that are substantially similar to those contained in Section 6.1 hereof.

“Independent Manager Event” shall mean, with respect to an Independent Manager, (i) any acts or omissions by such Independent Manager that constitute willful disregard of such Independent Managers duties under the applicable organizational documents, (ii) such Independent Manager engaging in or being charged with, or being convicted of, fraud or other acts constituting a crime under any law applicable to such Independent Manager, (iii) such Independent Manager is unable to perform his or her duties as Independent Manager due to death, disability or incapacity, or (iv) such Independent Manager no longer meeting the definition of Independent Manager.

“Insurance Premiums” shall have the meaning set forth in Section 8.1(b) hereof.

“Insurance Proceeds” shall have the meaning set forth in Section 8.4(b) hereof.

“Intercreditor Agreement” shall have the meaning set forth in Section 13.9 hereof.

“Interest Accrual Period” shall mean (i) prior to the first Payment Date, the Interim Interest Accrual Period, and (ii) commencing on the first Payment Date and continuing on each Payment Date thereafter, the calendar month immediately preceding such Payment Date.

“Interim Interest Accrual Period” shall mean the period from and including the Closing Date through and including the last day of the calendar month in which the Closing Date occurs, provided, however, there shall be no “Interim Interest Accrual Period” in the event the Closing Date is the first day of a calendar month.

“Internal Revenue Code” shall mean the Internal Revenue Code of 1986, as amended.

“Investor” shall have the meaning set forth in Section 13.3 hereof.

“Issuer Group” shall have the meaning set forth in Section 13.5(b) hereof.

“Issuer Person” shall have the meaning set forth in Section 13.5(b) hereof.

“Kroll” shall mean Kroll Bond Rating Agency, Inc., and its successor-in-interest.

“Lease” shall have the meaning set forth in the Mortgage.

“Legal Requirements” shall mean all statutes, laws, rules, orders, regulations, ordinances, judgments, decrees and injunctions of Governmental Authorities affecting the Property or any part thereof, or the construction, use, alteration, ownership or operation thereof, whether now or hereafter enacted and in force, and all permits, licenses, authorizations and regulations relating thereto, and all covenants, agreements, restrictions and encumbrances contained in any instruments, either of record or known to Borrower, at any time in force affecting the Property or any part thereof, including, without limitation, any which may (a) require repairs, modifications or alterations in or to the Property or any part thereof, or (b) in any way limit the use and enjoyment thereof.

“Letter of Credit” or “Letters of Credit” shall mean one or more irrevocable, unconditional, transferable, clean sight draft letters of credit, in favor of Lender, for the ratable benefit of Lender, and entitling Lender to draw thereon in New York, New York, or anywhere within the United States inside or outside of New York, New York if it is capable of being drawn upon by facsimile presentation, based solely on a statement executed by an officer or authorized signatory of Lender and issued by an Approved Bank. If at any time (a) the institution issuing any such Letter of Credit shall cease to be an Approved Bank or (b) the Letter of Credit is due to expire prior to the ninety-first (91st) day after the Maturity Date, Lender shall have the right immediately to draw down the same in full and hold the proceeds thereof in accordance with the provisions of this Agreement, unless Borrower shall deliver a replacement Letter of Credit from an Approved Bank within (i) as to clause (a) above, twenty (20) days after Lender delivers written notice to Borrower that the institution issuing the Letter of Credit has ceased to be an Approved Bank or (ii) as to clause (b) above, at least thirty (30) days prior to the expiration date of such Letter of Credit. Borrower shall not have or be permitted to have any liability or other obligations under any reimbursement agreement with respect to any Letter of Credit or otherwise in connection with reimbursement to the Approved Bank for draws on such Letter of Credit.

“Lien” shall mean any mortgage, deed of trust, lien, pledge, hypothecation, assignment, security interest, or any other encumbrance, charge or transfer of, on or affecting Borrower, the Property, any portion thereof or any interest therein, including, without limitation, any conditional sale or other title retention agreement, any financing lease having substantially the same economic effect as any of the foregoing, the filing of any financing statement, and mechanic’s, materialmen’s and other similar liens and encumbrances.

“LLC Agreement” shall have the meaning set forth in Section 6.1(c) hereof.

“Loan” shall mean the loan made by Lender to Borrower pursuant to this Agreement.

“Loan Bifurcation” shall have the meaning set forth in Section 13.4(f) hereof.

“Loan Documents” shall mean, collectively, this Agreement, the Note, the Mortgage, the Guaranty, the Environmental Indemnity, the Assignment of Management Agreement, the Lockbox Agreement and any and all other documents, agreements and certificates executed and/or delivered in connection with the Loan, as the same may be amended, restated, replaced, supplemented or otherwise modified from time to time.

“Lockbox Account” shall have the meaning set forth in Section 10.1(a) hereof.

“Lockbox Agreement” shall mean that certain agreement relating to deposit account control services by and among Borrower, Lender and Lockbox Bank, as the same may be amended, restated, replaced, supplemented or otherwise modified from time to time, relating to the operation and maintenance of, and application of funds in, the Lockbox Account.

“Lockbox Bank” shall mean any Eligible Institution acting as Lockbox Bank under the Lockbox Agreement.

“Losses” shall mean any and all actual claims, suits, liabilities (including, without limitation, strict liabilities), actions, proceedings, obligations, debts, damages, losses, out of pocket costs and expenses, fines, penalties, charges, fees, judgments, awards, amounts paid in settlement of whatever kind or nature (including but not limited to reasonable legal fees and other actual out of pocket costs of defense) and shall in no event include any special, punitive or consequential damages.

“Low Debt Yield Reserve Account” shall have the meaning set forth in the Mezzanine Loan Agreement.

“LTV Ratio” shall have the meaning set forth in Section 8.4(c) hereof.

“Major Lease” shall mean as to the Property (i) any Lease which, individually or when aggregated with all other leases at the Property with the same Tenant or its Affiliate, demises 5,000 square feet or more of the Property’s leasable area with (A) a term of ten (10) years or more (excluding renewal options at then fair market rents), or (B) an annual triple net base rental that is less than $45 per square foot, (ii) any Lease which contains any option, offer, right of first refusal or other similar entitlement to acquire all or any portion of the Property, or (iii) any instrument guaranteeing or providing credit support for any Lease meeting the requirements of (i) or (ii) above.

“Management Agreement” shall mean the management agreement entered into by and between Borrower and Manager, pursuant to which Manager is to provide management and other services with respect to the Property, as the same may be amended, restated, replaced, supplemented or otherwise modified in accordance with the terms of this Agreement.

“Manager” shall mean Highgate Hotels, L.P., a Delaware limited partnership, or such other entity selected as the manager of the Property in accordance with the terms of this Agreement.

“Material Action” shall mean, as to Borrower or the SPE Component Entity (if any), to file any insolvency, or reorganization case or proceeding, to institute proceedings to have such Person be adjudicated bankrupt or insolvent, to institute proceedings under any applicable insolvency law, to seek any relief under any law relating to relief from debts or the protection of debtors, to consent to the filing or institution of bankruptcy or insolvency proceedings against such Person, to file a voluntary petition seeking, or consent to, reorganization or relief with respect to such Person under any applicable federal or state law relating to bankruptcy or insolvency, to seek or consent to the appointment of a receiver,

liquidator, assignee, trustee, sequestrator, custodian, or any similar official of or for such Person or a substantial part of its property, to make any assignment for the benefit of creditors of such Person, or to take action in furtherance of any of the foregoing.

“Material Adverse Effect” shall mean, with respect to any event, condition, act or omission to act, a material adverse effect on the value, current use or operation of the Property, the business, operations or condition (financial or otherwise) of Borrower or Borrower Principal or the priority of Lender’s lien pursuant to the Mortgage, Borrower’s ability to pay its obligations under the Loan Documents when due, or Borrower’s ability to perform its obligations under the Loan Documents.

“Maturity Date” shall mean the Payment Date occurring in February, 2018.

“Maximum Legal Rate” shall mean the maximum nonusurious interest rate, if any, that at any time or from time to time may be contracted for, taken, reserved, charged or received on the indebtedness evidenced by the Note and as provided for herein or the other Loan Documents, under the laws of such state or states whose laws are held by any court of competent jurisdiction to govern the interest rate provisions of the Loan.

“Member” shall have the meaning set forth in Section 6.1(c) hereof.

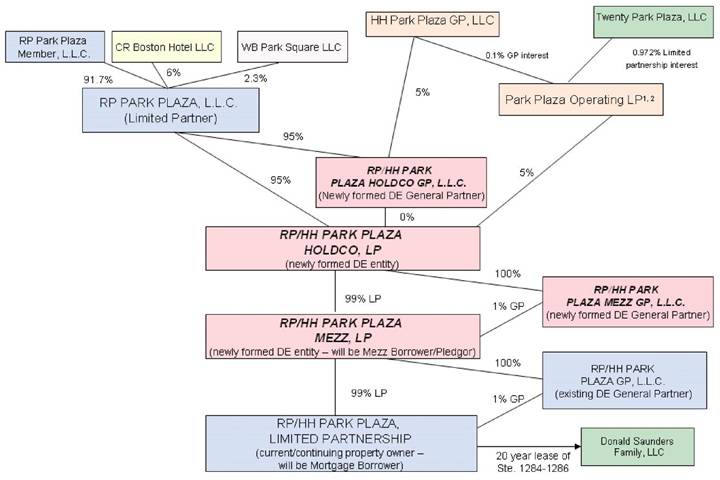

“Mezzanine Borrower” shall mean, collectively, RP/HH Park Plaza Mezz, LP, a Delaware limited partnership.

“Mezzanine Default” shall have the meaning ascribed to the term “Default” in the Mezzanine Loan Agreement.

“Mezzanine Lender” shall mean the owner and holder of the Mezzanine Loan.

“Mezzanine Loan” shall mean that certain loan made by Mezzanine Lender to Mezzanine Borrower on the date hereof pursuant to the Mezzanine Loan Agreement, as the same may be amended or split pursuant to the terms of the Mezzanine Loan Documents or the Permitted Mezzanine Financing, as applicable.

“Mezzanine Loan Account” shall have the meaning set forth in Section 10.1(b) hereof.

“Mezzanine Loan Agreement” shall mean that certain Loan Agreement dated as of the date hereof between Mezzanine Borrower and Mezzanine Lender.

“Mezzanine Loan Documents” shall mean all documents or instruments evidencing, securing or guaranteeing the Mezzanine Loan, including without limitation, the Mezzanine Loan Agreement.

“Mezzanine Note” shall mean that certain Promissory Note dated as of the date hereof given by Mezzanine Borrower to Mezzanine Lender in the original principal amount of $30,000,000.

“Mold” shall have the meaning set forth in Section 12.5 hereof.

“Monthly Mezzanine Debt Service Payment Amount” shall mean the monthly amount of interest and scheduled amortization payments due and payable pursuant to the Mezzanine Loan Agreement and the Mezzanine Note.

“Monthly Payment Amount” shall mean, with respect to each Payment Date, a constant monthly payment of $601,054.87, which is computed on the basis of an amortization schedule for a loan having (a) a principal amount equal to the original principal amount of the Note, (b) an amortization period of thirty (30) years, and (c) an annual interest rate equal to the Note Rate.

“Moody’s” shall mean Moody’s Investors Service, Inc.

“Morningstar” shall mean Morningstar Credit Ratings, LLC.

“Mortgage” shall mean that Mortgage, Assignment of Leases and Rents, Security Agreement and Fixture Filing of even date herewith, executed and delivered by Borrower as security for the Loan and encumbering the Property, as the same may be amended, restated, replaced, supplemented or otherwise modified from time to time.

“Negative Monthly Budget Variance” shall mean the amount, if any, by which the aggregate amount disbursed to Borrower pursuant to Section 10.1(c)(ii) hereof during the month in which the calculation is being made, exceeds the aggregate amount of budgeted operating expenses actually spent by Borrower during such month.

“Net Liquidation Proceeds After Debt Service” shall have the meaning set forth in the Mezzanine Loan Agreement.

“Net Operating Income” shall mean, with respect to any period of time, the amount obtained by subtracting Operating Expenses (based on annualized amounts for any recurring expenses not paid monthly divided by twelve and multiplied by the number of months in the applicable time period for which Net Operating Income is being calculated) from Operating Income.

“Net Proceeds” shall have the meaning set forth in Section 8.4(b) hereof.

“Net Proceeds Deficiency” shall have the meaning set forth in Section 8.4(b)(vi) hereof.

“Net Sales Proceeds” shall mean for the sale of the Retail Space, the cash proceeds (including any cash received by way of deferred payment pursuant to a promissory note, receivable or otherwise) received from such sale, net of (i) customary expenses of sale in the jurisdiction where the Retail Space is located (including, without limitation, brokerage fees, if any, transfer taxes, and legal fees), (ii) any payments (other than payments of principal and interest) required to be made to Lender in connection with a release of such Retail Space from the Loan and the Mezzanine Loan as a result of such asset sale as provided herein and (iii) all third party out-of-pocket costs incurred by Borrower, Mezzanine Borrower or any of their

Affiliates in connection with the release of the Retail Space in accordance with the terms hereof and the Mezzanine Loan Documents.

“Net Worth” shall mean, as of a given date, the value of a Person’s tangible assets calculated in conformance with GAAP less total liabilities excluding unrealized contingent liabilities from non-recourse or other guaranties.

“New Non-Consolidation Opinion” shall mean a bankruptcy non-consolidation opinion from the counsel to Borrower that delivered the Non-Consolidation Opinion or other outside counsel to Borrower reasonably acceptable to Lender, in form and substance satisfactory to Lender and, following the Securitization of the Loan, the Rating Agencies, and which is required to be delivered subsequent to the Closing Date pursuant to, and in connection with, this Agreement, it being understood and agreed that, notwithstanding the foregoing, a New Non-Consolidation Opinion in form and substance substantially identical to the Non-Consolidation Opinion shall be acceptable in all respects.

“Non-Consolidation Opinion” shall mean that certain bankruptcy non-consolidation opinion dated as of the Closing Date delivered to Lender in connection with the Loan.

“Non-Discretionary Expenses” shall mean any non-discretionary expense required for the Property which is not expressly provided for in the Annual Budget and which were not known (or would not have been known by a prudent owner of hospitality properties similar in size and scope as the Property) at the time the Annual Budget was approved by Lender and is necessary to (a) comply with then-existing service contracts or other agreements (e.g., service contract fee escalations pursuant to the existing terms thereof, union costs, reimbursable payrolls), encumbrances or other instruments affecting the Property existing on the date hereof or otherwise entered into in accordance with the terms of this Agreement, (b) comply in all material respects with Legal Requirements, all zoning laws and/or entitlements affecting the Property, (c) comply with any final orders, judgments or decrees in favor of any governmental authority or (d) to prevent any imminent threat to the health, safety or welfare of any person or any property in, on, under, within, upon, around or about the Property, or material damage or loss to the Property.

“Note” shall mean, individually and collectively as the context may require, Note A-1 and Note A-2.

“Note A-1” shall mean that certain promissory note of even date herewith in the principal amount of $95,000,000, made by Borrower in favor of Lender, as the same may be amended, restated, replaced, severed, supplemented or otherwise modified from time to time.

“Note A-2” shall mean that certain promissory note of even date herewith in the principal amount of $25,000,000, made by Borrower in favor of Lender, as the same may be amended, restated, replaced, severed, supplemented or otherwise modified from time to time.

“Note Rate” shall mean a rate per annum equal to four and four hundred and two thousandths percent (4.402%).

“OFAC” shall have the meaning set forth in Section 4.38 hereof.

“Officer’s Certificate” shall mean a certificate delivered to Lender by Borrower which is signed by an authorized officer of Borrower or the general partner, managing member or sole member of Borrower, as applicable.

“Operating Expenses” shall mean, with respect to any period of time, the total of all expenses actually paid or payable, computed in accordance with GAAP and the Uniform System of Accounts (or such other method of accounting reasonably acceptable to Lender), of whatever kind relating to the operation, maintenance and management of the Property, including without limitation, as applicable, utilities, ordinary repairs and maintenance, Insurance Premiums, license fees, Taxes and Other Charges, advertising expenses, payroll and related taxes, computer processing charges, management fees equal to the greater of 3% of the Operating Income and the management fees actually paid under the Management Agreement, operational equipment or other lease payments as approved by Lender, normalized FF&E equal to 4% of the Operating Income (unless any then applicable Management Agreement requires a higher FF&E expenditure; provided, however, normalized FF&E shall be set at 4% of the Operating Income for years one and two of the Loan irrespective of any requirements for a higher FF&E expenditure under the Management Agreement), marketing fees equal the marketing fees actually paid, franchise fees equal to any franchise fees actually paid under any Franchise Agreement, but specifically excluding depreciation and amortization, income taxes, Debt Service, debt service due on the Mezzanine Loan, any incentive fees due under the Management Agreement, any item of expense that in accordance with GAAP should be capitalized, any item of expense for which reimbursement would be covered under any insurance policy to be paid by a third party, and any item of expenses that in accordance with GAAP should be capitalized but only to the extent the same would otherwise be covered by the provisions hereof but which is paid by any Tenant under such Tenant’s Lease or other agreement (other than real estate taxes paid directly to any taxing authority by such Tenant), and deposits into the Reserve Accounts.

“Operating Expense Subaccount” shall have the meaning set forth in Section 10.1(b)(v) hereof.

“Operating Income” shall mean, with respect to any period of time, all income, computed in accordance with GAAP and the Uniform System of Accounts (or such other method of accounting acceptable to Lender), derived from the ownership and operation of the Property from whatever source, including, but not limited to, rental income from rental of rooms, rental income from all tenants (if any) paying rent and in actual physical occupancy (by the tenant, its Affiliate or a sublessee) of their demised premises pursuant to Leases in full force and effect (whether base rent, additional rent or escalations), utility, real estate tax or other miscellaneous expense recoveries, all income and proceeds received from food and beverage operations, bookings, or any other use of the Property consistent with the terms of this Agreement and from catering services conducted from the Property regardless of whether rendered inside or outside of the Property, all income and proceeds received from the spa and/or gift shop(s) operated at the Property and from related ancillary facilities and/or activities, common area maintenance, service fees or charges, license fees, parking fees, rent concessions or credits, and other required pass-throughs, business interruption or rent loss insurance; but excluding sales, use and occupancy or other taxes on receipts required to be accounted for by Borrower to any Governmental Authority, tax rebates, refunds and uncollectible accounts, proceeds from the sale of furniture, fixtures and

equipment or any other sale, transfer or exchange, proceeds from any financing, capital contributions, interest income from any source other than the escrow accounts, Reserve Accounts or other accounts required pursuant to the Loan Documents, Insurance Proceeds (other than business interruption or rent loss insurance), Awards, unforfeited tenant security, utility and other similar deposits, any other extraordinary, non-recurring revenues, income from tenants not paying rent, income from tenants in the form of a lease termination payment, income from tenants in bankruptcy under Leases not assumed in the bankruptcy proceeding, non-recurring or extraordinary income, including, without limitation lease termination payments, and any disbursements to Borrower from the Reserve Accounts.

“Other Charges” shall mean all ground rents, maintenance charges, impositions other than Taxes, and any other charges, including, without limitation, vault charges and license fees for the use of vaults, chutes and similar areas adjoining the Property, now or hereafter levied or assessed or imposed against the Property or any part thereof, including Borrower’s proportionate share of all Common Charges payable with respect to the Property pursuant to the Condominium Documents.

“Partial Release Event” shall mean the prepayment of the Loan relating to only the Retail Space in accordance with the terms hereof.

“Participations” shall have the meaning set forth in Section 13.1 hereof.

“Patriot Act” shall have the meaning set forth in Section 4.38 hereof.

“Payment Date” shall mean the first (1st) day of each month beginning on March, 2013.

“Permitted Encumbrances” shall mean collectively, (a) the Lien and security interests created by the Loan Documents, (b) all Liens, encumbrances and other matters disclosed in the Title Insurance Policy, (c) any encumbrances necessary to enable Borrower to comply with any conditions to maintain any existing entitlements, (d) Liens, if any, for Taxes, Other Charges or other assessments or governmental charges (whether or not imposed by any Governmental Authority) or for any other matter not yet due or delinquent or which are being contested in good faith by appropriate proceedings in accordance with the terms of this Agreement so long as, in the case of a Lien with respect to any portion of the Property, such proceedings operate to stay the sale of any portion of the Property on account of such lien, (e) such de minimis other encumbrances arising from Borrower’s ownership and operation of the Property in the ordinary course of Borrower’s business consistent with the terms of the Loan Documents and which do not, in the aggregate, result in a Material Adverse Effect, (f) trade payables and equipment leases in the ordinary course of Borrower’s business and which are permitted pursuant to the terms of this Agreement, (g) any zoning or similar law reserved to or vested in any Government Authority to control or regulate the use of any real property, (h) the Mezzanine Loan and the Liens created thereby, (i) Permitted Mezzanine Financing and the pledge of the indirect equity interests in Borrower and any SPE Component Entity, (j) the Permitted Preferred Equity and (k) such other title and survey exceptions as Lender has approved or may approve in writing in Lender’s sole discretion.

“Permitted Investments” shall mean to the extent available from Lender or Lender’s servicer for deposits in the Reserve Accounts and the Cash Management Account, any one or more of the following obligations or securities acquired at a purchase price of not greater than par, including those issued by a servicer of the Loan, the trustee under any securitization or any of their respective Affiliates, payable on demand or having a maturity date not later than the Business Day immediately prior to the date on which the funds used to acquire such investment are required to be used under this Agreement and meeting one of the appropriate standards set forth below:

(a) obligations of, or obligations fully guaranteed as to payment of principal and interest by, the United States or any agency or instrumentality thereof provided such obligations are backed by the full faith and credit of the United States of America including, without limitation, obligations of: the U.S. Treasury (all direct or fully guaranteed obligations), the Farmers Home Administration (certificates of beneficial ownership), the General Services Administration (participation certificates), the U.S. Maritime Administration (guaranteed Title XI financing), the Small Business Administration (guaranteed participation certificates and guaranteed pool certificates), the U.S. Department of Housing and Urban Development (local authority bonds) and the Washington Metropolitan Area Transit Authority (guaranteed transit bonds); provided, however, that the investments described in this clause must (i) have a predetermined fixed dollar of principal due at maturity that cannot vary or change, (ii) be rated “AAA” or the equivalent by each of the Rating Agencies, (iii) if rated by S&P, must not have an “r” highlighter affixed to their rating, (iv) if such investments have a variable rate of interest, such interest rate must be tied to a single interest rate index plus a fixed spread (if any) and must move proportionately with that index, and (v) such investments must not be subject to liquidation prior to their maturity;

(b) Federal Housing Administration debentures;

(c) obligations of the following United States government sponsored agencies: Federal Home Loan Mortgage Corp. (debt obligations), the Farm Credit System (consolidated systemwide bonds and notes), the Federal Home Loan Banks (consolidated debt obligations), the Federal National Mortgage Association (debt obligations), the Financing Corp. (debt obligations), and the Resolution Funding Corp. (debt obligations); provided, however, that the investments described in this clause must (i) have a predetermined fixed dollar of principal due at maturity that cannot vary or change, (ii) if rated by S&P, must not have an “r” highlighter affixed to their rating, (iii) if such investments have a variable rate of interest, such interest rate must be tied to a single interest rate index plus a fixed spread (if any) and must move proportionately with that index, and (iv) such investments must not be subject to liquidation prior to their maturity;

(d) federal funds, unsecured certificates of deposit, time deposits, bankers’ acceptances and repurchase agreements with maturities of not more than 365 days of any bank, the short term obligations of which at all times are rated in the highest short term rating category by each Rating Agency (or, if not rated by all Rating Agencies, rated by at least one Rating Agency in the highest short term rating category and otherwise acceptable to each other Rating Agency, as confirmed in writing that such investment would not, in and of itself, result in a downgrade, qualification or withdrawal of the initial, or, if higher, then current ratings assigned

to the Securities); provided, however, that the investments described in this clause must (i) have a predetermined fixed dollar of principal due at maturity that cannot vary or change, (ii) if rated by S&P, must not have an “r” highlighter affixed to their rating, (iii) if such investments have a variable rate of interest, such interest rate must be tied to a single interest rate index plus a fixed spread (if any) and must move proportionately with that index, and (iv) such investments must not be subject to liquidation prior to their maturity;

(e) fully Federal Deposit Insurance Corporation-insured demand and time deposits in, or certificates of deposit of, or bankers’ acceptances with maturities of not more than 365 days and issued by, any bank or trust company, savings and loan association or savings bank, the short term obligations of which at all times are rated in the highest short term rating category by each Rating Agency (or, if not rated by all Rating Agencies, rated by at least one Rating Agency in the highest short term rating category and otherwise acceptable to each other Rating Agency, as confirmed in writing that such investment would not, in and of itself, result in a downgrade, qualification or withdrawal of the initial, or, if higher, then current ratings assigned to the Securities); provided, however, that the investments described in this clause must (i) have a predetermined fixed dollar of principal due at maturity that cannot vary or change, (ii) if rated by S&P, must not have an “r” highlighter affixed to their rating, (iii) if such investments have a variable rate of interest, such interest rate must be tied to a single interest rate index plus a fixed spread (if any) and must move proportionately with that index, and (iv) such investments must not be subject to liquidation prior to their maturity;

(f) debt obligations with maturities of not more than 365 days and at all times rated by each Rating Agency (or, if not rated by all Rating Agencies, rated by at least one Rating Agency and otherwise acceptable to each other Rating Agency, as confirmed in writing that such investment would not, in and of itself, result in a downgrade, qualification or withdrawal of the initial, or, if higher, then current ratings assigned to the Securities) in its highest long-term unsecured rating category; provided, however, that the investments described in this clause must (i) have a predetermined fixed dollar of principal due at maturity that cannot vary or change, (ii) if rated by S&P, must not have an “r” highlighter affixed to their rating, (iii) if such investments have a variable rate of interest, such interest rate must be tied to a single interest rate index plus a fixed spread (if any) and must move proportionately with that index, and (iv) such investments must not be subject to liquidation prior to their maturity;

(g) commercial paper (including both non-interest-bearing discount obligations and interest-bearing obligations payable on demand or on a specified date not more than one year after the date of issuance thereof) with maturities of not more than 365 days and that at all times is rated by each Rating Agency (or, if not rated by all Rating Agencies, rated by at least one Rating Agency and otherwise acceptable to each other Rating Agency, as confirmed in writing that such investment would not, in and of itself, result in a downgrade, qualification or withdrawal of the initial, or, if higher, then current ratings assigned to the Securities) in its highest short-term unsecured debt rating; provided, however, that the investments described in this clause must (i) have a predetermined fixed dollar of principal due at maturity that cannot vary or change, (ii) if rated by S&P, must not have an “r” highlighter affixed to their rating, (iii) if such investments have a variable rate of interest, such interest rate must be tied to a single interest rate index plus a fixed spread (if any) and must move proportionately with that index, and (iv) such investments must not be subject to liquidation prior to their maturity;

(h) units of taxable money market funds, with maturities of not more than 365 days and which funds are regulated investment companies, seek to maintain a constant net asset value per share and invest solely in obligations backed by the full faith and credit of the United States, which funds have the highest rating available from each Rating Agency (or, if not rated by all Rating Agencies, rated by at least one Rating Agency and otherwise acceptable to each other Rating Agency, as confirmed in writing that such investment would not, in and of itself, result in a downgrade, qualification or withdrawal of the initial, or, if higher, then current ratings assigned to the Securities) for money market funds; and