UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the Fiscal Year Ended December 31, 2018 | |

| Or | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-35798

HUMANIGEN, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

2834 (Primary Standard Industrial Classification Code Number) |

77-0557236 (I.R.S. Employer Identification No.) |

533 Airport Boulevard, Ste. 400

Burlingame, CA 94005

(Address of Principal Executive Offices) (Zip Code)

(650) 243-3100

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

None.

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller reporting company ☒ | Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s voting stock held by non-affiliates as of June 30, 2018, was approximately $28,444,573 based on the closing price of $0.67 of the Common Stock of the registrant as reported on the OTCQB Venture Market operated by OTC Markets Group, Inc. on such date. As of March 22, 2019, there were 110,112,390 shares of the registrant’s Common Stock, par value $0.001 per share, outstanding.

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☒ No ☐

| 1 |

Humanigen, Inc.

Form 10-K

Index

| 2 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that discuss future events or expectations, projections of results of operations or financial condition, trends in our business, business prospects and strategies and other “forward-looking” information. In some cases, you can identify “forward-looking statements” by words like “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “intends,” “potential” or “continue” or the negative of those words and other comparable words. These statements may relate to, among other things, our expectations regarding the scope, progress, expansion, and costs of researching, developing and commercializing our product candidates; our opportunity to benefit from various regulatory incentives; expectations for our financial results, revenue, operating expenses and other financial measures in future periods; and the adequacy of our sources of liquidity to satisfy our working capital needs, capital expenditures, and other liquidity requirements. Actual events or results may differ materially due to known and unknown risks, uncertainties and other factors such as:

| · | our lack of revenues, history of operating losses, bankruptcy, limited cash reserves and ability to obtain additional capital to develop and commercialize our product candidates, including the additional capital which will be necessary to complete the clinical trials that we have initiated or plan to initiate, and continue as a going concern; |

| · | the effect on our stock price and the significant dilution to the share ownership of our existing stockholders that resulted from conversion of the term loans into equity of the company or that may result in the future upon additional issuances of our equity securities; |

| · | our ability to execute our strategy and business plan focused on developing, alone or in conjunction with a partner, our proprietary monoclonal antibody portfolio; |

| · | our ability to preserve our stock quotation on the OTCQB Venture Market or, in the future, to list our common stock on a national securities exchange, whether through a new listing or by completing a reverse merger or other strategic transaction; |

| · | the success, progress, timing and costs of our efforts to evaluate or consummate various strategic alternatives if in the best interests of our stockholders; |

| · | the success, cost, timing and potential indications of our product development activities and clinical trials; |

| · | the potential timing and outcomes of pre-clinical and clinical studies of lenzilumab, ifabotuzumab, HGEN005 or any other product candidates and the uncertainties inherent in pre-clinical and clinical testing; |

| · | the timing of the initiation, enrollment and completion of planned clinical trials; |

| · | our ability to timely source adequate supply of our development products from third-party manufacturers on which we depend; |

| · | the potential, if any, for future development of any of our present or future products; |

| · | our ability to successfully progress, partner or complete further development of our programs; |

| · | our plans to research, develop and commercialize our product candidates; |

| · | our ability to identify and develop additional uses for our products; |

| · | our ability to attain market exclusivity and/or to protect our intellectual property; |

| · | our ability to reach agreement with a partner to affect successful development and commercialization of any of our product candidates; |

| · | our ability to attract and retain collaborators with development, regulatory and commercialization expertise; |

| · | the outcome of pending or future litigation; |

| · | the ability of our controlling stockholder to exert control over all matters of the Company, including their ability to control elections of directors, amendments of our organizational documents, or approval of any merger, sale of assets, or other major corporate transaction; |

| · | competition; |

| · | our ability to obtain and maintain regulatory approval of our product candidates, and any related restrictions, |

| 3 |

| · | limitations, and/or warnings in the label of an approved product candidate; and |

| · | changes in the regulatory landscape that may prevent us from pursuing or realizing any of the expected benefits from the various regulatory incentives, or the imposition of regulations that affect our products. |

These are only some of the factors that may affect the forward-looking statements contained in this annual report. For a discussion identifying additional important factors that could cause actual results to vary materially from those anticipated in the forward-looking statements, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors” in this Annual Report on Form 10-K. You should review these risk factors for a more complete understanding of the risks associated with an investment in our securities. However, we operate in a competitive and rapidly changing environment and new risks and uncertainties emerge, are identified or become apparent from time to time. It is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this annual report. You should be aware that the forward-looking statements contained in this annual report are based on our current views and assumptions. We undertake no obligation to revise or update any forward-looking statements made in this annual report to reflect events or circumstances after the date hereof or to reflect new information or the occurrence of unanticipated events, except as required by law.

| 4 |

PART I

Overview

During February 2018, we completed the financial restructuring transactions announced in December 2017 and furthered our transformation into a biopharmaceutical company pursuing cutting-edge science to develop our proprietary monoclonal antibodies for various oncology indications and to enhance T-cell therapies, potentially making these treatments safer, more effective and more efficiently administered.

Our primary focus is on preventing the serious and potentially life-threatening side-effects associated with chimeric antigen receptor T-cell, also known as CAR-T, therapy, and in making those therapies more efficacious, efficient and cost-effective. Identifying, treating and managing severe side-effects consumes significant hospital resources and creates additional costs that we believe have impeded the pace of adoption of these promising treatments as the standard of care for certain hematologic cancers. These side-effects may also hamper the expansion of CAR-T to earlier line use beyond the relapsed or refractory setting in hematologic cancers and the utility of CAR-T in solid tumors, both of which represent significant growth drivers for the overall CAR-T marketplace. In addition, not all patients receive clinical benefit from CAR-T therapy and the efficacy profile has room for potential improvement.

Lenzilumab, our lead product candidate, is a novel Humaneered® monoclonal antibody (mAb) that has the potential to both improve the efficacy and safety associated with CAR-T therapy. There are currently no Food and Drug Administration (FDA) approved therapies available for the prevention of the serious side-effects associated with CAR-T cell therapies. Preclinical data generated by the Mayo Clinic in partnership with us indicates that the use of lenzilumab may prevent onset of both CAR-T induced neurologic toxicities and cytokine release syndrome while also enhancing the proliferation and effector functions of the CAR-T therapy itself, thus simultaneously improving the side-effect profile, relapse rates, duration of response and overall efficacy.

We are working to advance the development of lenzilumab through pivotal registration clinical trials in close collaboration with some of the leading and most experienced centers in the CAR-T field. We are also exploring partnerships with established and emerging CAR-T companies. We aim to position lenzilumab as a “must have” companion product to any CAR-T therapy and an essential part of the standard pre-conditioning that all patients administered CAR-T must receive. We believe that lenzilumab’s success in preventing serious, potentially life-threatening side-effects will lead to substantial reductions in intensive care unit (ICU) admissions and duration of ICU stays. Use of lenzilumab alongside CAR-T therapy could result in potential efficacy improvements which could offer significant economic benefits to the healthcare system as a whole, including for hospitals, providers, patients and payers in the United States and abroad. These benefits, coupled with the potential to make CAR-T therapy capable of being administered on an out-patient basis, with follow-up care also monitored and managed in an out-patient setting, may improve access to and reimbursement of CAR-T therapy, which in turn may substantially expand CAR-T uptake and utilization. We also believe we have the opportunity to benefit from various regulatory incentives, such as orphan drug exclusivity, breakthrough therapy designation, fast track designation, priority review and accelerated approval.

CAR-T Overview and Market Opportunity

Development and implementation of individualized treatments based on T-cell therapies has the potential to revolutionize the fight against cancer. The two CD19 targeted CAR-T therapies that have been approved by the United States Food and Drug Administration, or FDA, Gilead/Kite’s Yescarta® and Novartis’s Kymriah®, are indicated for the treatment of B-cell cancers such as various types of non-Hodgkin’s lymphoma (NHL), including diffuse large B-cell lymphoma (DLBCL), and acute lymphoblastic leukemia (ALL), that are refractory or in second or later stage relapse (r/r). Although patients suffering from these aggressive cancers frequently undergo multiple treatments, including chemotherapy, radiation and targeted therapy of stem cell transplants, the five-year survival rate has been severely limited and patients who do not respond to, or have relapsed following at least two courses of standard treatment, have no other treatment options and a very poor outcome.

| 5 |

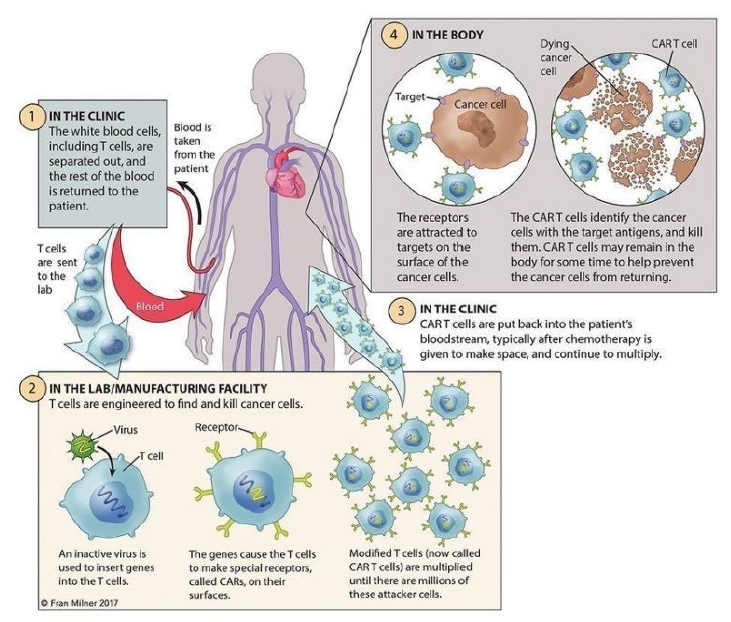

The approved CAR-T therapies have demonstrated effectiveness of using targeted immuno-cellular engineering to cause a patient’s own T-cells to fight certain cancers that have not responded to standard therapies. T-cells are often called the “workhorses” of the immune system because of their role in coordinating the immune response and killing cells infected by pathogens and cancer cells. As depicted below, each of the FDA-approved CAR-T-cell therapies is currently a one-time treatment for most patients that involves multiple steps:

| · | harvesting white blood cells from the patient’s blood; |

| · | engineering T cells within this population to express cancer-specific receptors; |

| · | increasing and purifying the number of genetically re-engineered T cells; and |

| · | infusing the functional cancer-specific T cells back into the patient to allow for expansion and targeting the cancer cells. |

| 6 |

Both Kymriah and Yescarta received FDA approval for adults with r/r DLBCL on the basis of one single-arm Phase II study which served as the pivotal registration trial for each product in this indication, a markedly accelerated process that indicates FDA’s view of the strong potential of these novel CAR-T treatments to address an unmet need and improve patient outcomes. Moreover, Kymriah also received FDA approval for the treatment of pediatrics and adolescents with r/r ALL based on a single phase II study. The Novartis-sponsored Kymriah study in ALL showed that 83% of pediatric and adolescent patients with r/r ALL achieved complete remission or complete remission with incomplete blood count recovery. The Novartis-sponsored Kymriah study in adults with r/r DLBCL showed that 32% of adults achieved a complete response (CR) within three months of infusion.

The single Phase II study that led to the FDA approval of Yescarta in r/r DLBCL showed similarly positive results. The study enrolled 101 patients with large B-cell lymphoma at advanced stages despite having undergone at least two previous treatments, with approximately 20% of patients already having undergone a stem cell transplant. Just over half of the patients in the study achieved a CR with Yescarta.

Since the initial FDA approval was granted to Novartis for Kymriah in r/r ALL, the CAR-T market has seen rapid expansion, with Gilead/Kite launching Yescarta in r/r DLBCL, Novartis expanding its label for Kymriah to include r/r DLBCL and dozens of other biotechnology companies actively working to progress CAR-T therapies as potential treatments for numerous hematologic and solid cancers.

Both Kymriah and Yescarta are autologous individualized CD19 targeted CAR-T cell therapies. Development is also ongoing for both Kymriah and Yescarta for earlier lines of therapy for DLBCL, in other types of NHL and for the treatment of chronic lymphocytic leukemia (CLL). According to the National Cancer Institute Surveillance, Epidemiology, and End Results Program (SEERS) as well as the American Cancer Society's Cancer Statistics Center and World Health Organization Union for International Cancer Control, it is estimated that up to 10,000 patients with r/r B-cell hematologic malignancies (including DLBCL, ALL, CLL) per year may potentially benefit from CD19 targeted CAR-T cell therapies. Should CD19 targeted CAR-T therapies gain approval for earlier second line usage versus stem cell transplantation in DLBCL, an additional 5,000 to 10,000 patients per year may be eligible for treatment. Moreover, there are two BCMA targeted CAR-T cell therapies in phase II development for r/r multiple myeloma and several other novel CAR-T cell therapies targeting various antigens and neo-antigens in development for a number of hematologic and solid cancers. While there may be individual differences between CAR-T products, the overall safety profile is, for the most part, expected to be consistent with that reported with Yescarta and Kymriah. FDA Commissioner Scott Gottlieb and Center for Biologics Evaluation and Research (CBER) Director Peter Marks detailed plans for the agency to keep pace with an expected influx of applications for cell and gene therapies over the coming years. By 2020, Gottlieb and Marks say they expect to be receiving upwards of 200 INDs for cell and gene therapies each year, adding to the 800 active Investigational New Drug Applications (INDs) for such products already filed with the agency. By 2025, they predict the agency will be approving between 10 and 20 cell and gene therapy products annually. The FDA has also issued final guidance to gene therapy and cell therapy developers, whereby under the Regenerative Medicine Advanced Therapy (RMAT) designation, qualified applications will be eligible for priority review and accelerated approval.

The global CAR-T market is projected to grow from approximately $300 million in 2018 to greater than $2 billion in 2021, with continued growth to approximately $8.5 billion in 2028. These market projections do not account for additional growth opportunities including the expansion of CD19 CAR-T therapies for use in various solid tumors, which is currently in early to mid-stage clinical development.

Lenzilumab Overview and Market Opportunity

The two currently approved CAR-T therapies are not without significant limitations. Both Kymriah and Yescarta have black box warnings for cytokine release syndrome (CRS) and neurologic toxicities (NT) and were approved with a risk evaluation and mitigation strategy (REMS) to assist and train certified centers on the management of these serious side effects. This has adversely impacted both market uptake and usage to date. Both CRS and NT are caused by a large-scale release of pro-inflammatory cytokines and chemokines induced by the CAR-T therapy, sometimes referred to as a “cytokine storm”. Up to 94% of patients treated with Yescarta or Kymriah in the clinical trial setting experienced CRS (with up to 49% of cases being severe or grade >3 in nature) and up to 87% experienced NT (with up to 31% of cases being severe or grade >3 in nature). Moreover, approximately 30-60% of patients treated required admission to the intensive care unit (ICU), where ventilator support, vasopressors and other supportive care was provided to attempt to manage these side-effects. Some patients can suffer seizures, coma, brain swelling, heart arrhythmias, organ failure and serious and life-threatening clotting disorders. These can be particularly challenging and concerning issues, especially in younger and pediatric patients. We expect that the CAR-T therapies under development may be hampered by the same significant side effects. If such side-effects can be ameliorated or eradicated, and adequate data is submitted to FDA, the Black Box warning and REMS program could potentially be scaled back or removed.

| 7 |

There are currently no FDA-approved products for the prevention or treatment of NT nor for the prevention of CRS associated with CAR-T therapy. Medicines used to manage severe cases of CRS do not universally treat nor necessarily control these side effects and their early prophylactic use is not recommended as it may either interfere with the effectiveness of the CAR-T therapy itself or increase the risk of CAR-T induced NT. Improvements in the ability to prevent or mitigate NT and CRS are needed to remove these major impediments to uptake and utility of CAR-T therapies, reduce healthcare utilization and improve overall patient outcomes. There have been several deaths reported as a result of these side-effects and managing patients with these side-effects can consume a significant amount of in-hospital resources, including extended stays in the ICU. The primary driver of non-drug related costs associated with CAR-T therapy is the length of stay in the hospital, particularly if this includes ICU admission. Non-drug related costs for patients who develop CRS and/or NT are approximately double that of patients who do not develop these serious toxicities. Further, as the potential benefit of CAR-T cell therapies are explored in earlier lines of hematologic cancers (rather than as salvage therapy for patients who have exhausted other options) and in solid tumors, the need to address these serious side-effects, as well as the incremental costs related to serious side-effects, becomes paramount.

In addition to improving patient outcomes, the ability to prevent or treat NT or prevent CRS associated with CAR-T therapy may offer significant benefits in making these treatments more cost-effective to administer in the United States and abroad. Reimbursement for patients who are treated only as out-patients is profoundly different from, and more favorable than that for patients who require inpatient treatment in a hospital. Unfortunately, at present, the need to identify, treat and manage NT and CRS generally has prevented CAR-T therapies from being administered, monitored and managed, on a routine out-patient basis. As a result, having an ICU bed available prior to initiating CAR-T therapy may be required due to the risks associated with CRS and NT, placing pressure on valuable and costly hospital in-patient resources. In certain institutions, the patient is admitted as an in-patient and is required to remain in the hospital for at least a week, with discharge being subject to satisfactory short-term outcomes and no emergence of serious complications. Even in select institutions where the CAR-T infusion is initially administered in an out-patient setting, the patient is closely monitored daily for several weeks and is required to stay within a short distance from the hospital, often requiring additional lodging, food and other costs to be incurred. In some situations these patients are re-admitted to the hospital on an emergency basis as an in-patient if complications ensue. If a patient is admitted or re-admitted to the hospital as an in-patient, the hospital reimbursement dynamics may change in a manner which is negative for the hospital, the payer and the patient. This dynamic also changes typical hospital reimbursement, depending on when in the treatment cycle the patient is admitted or re-admitted.

The reimbursement challenges associated with CAR-T therapies are proving to be an impediment to greater utilization of Kymriah and Yescarta in the United Kingdom (UK), where the National Institute of Clinical Excellence (NICE) initially recommended that the UK National Health Service not reimburse Yescarta based on their assessment of the cost per Quality-Adjusted Life Year (QALY). A key driver of the cost per QALY is in-patient and potential ICU related costs. A positive recommendation for use of Yescarta within the Cancer Drugs Fund (CDF) and in the context of a managed access agreement has subsequently been made by the NICE appraisal committee. When the data collection period finishes (anticipated by February 2022), the process for exiting the CDF will begin and the review of NICE’s guidance for Yescarta will start. While both Kymriah and Yescarta have been approved by the European Medicines Agency (EMA), commercial use has been largely limited to patients in France, Germany and Austria as the companies establish reimbursement arrangements intended to facilitate access to the treatments on a discounted basis consistent with the governmental mandates to curb healthcare spending. These dynamics, and the additional complexity of treating patients with serious and potentially life-threatening side-effects in the hospital and/or ICU, mean that enabling true out-patient administration and follow-up would confer significant benefits to patients, hospitals, payers and the healthcare system.

| 8 |

Our Solution

In our review of results of CAR-T clinical trials, as well as pre-clinical studies that seek to understand the causation of side-effects, we noted that CAR-T infusion leads to an early rise in levels of granulocyte-macrophage colony-stimulating factor (GM-CSF), a cytokine that is well documented to be of critical importance and essential to the initiation of the inflammatory cascade associated with CAR-T-related side- effects. GM-CSF is one of only two cytokines that have been clearly demonstrated to be associated with severe NT, with peak levels of GM-CSF being strongly associated with NT. Moreover, there is an abundance of data demonstrating that GM-CSF is upstream in the cytokine cascade and that the neutralization of GM-CSF is known to inhibit the release of key downstream cytokines known to be associated with CRS.

Lenzilumab, our proprietary Humaneered® monoclonal antibody, targets and neutralizes GM-CSF, and has been shown to be generally safe and well tolerated in more than 110 patients in two Phase I and two Phase II clinical studies, including in chronic myelomonocytic leukemia.

We believe lenzilumab has the potential to improve the efficacy and safety of CAR-T therapy and that the use of lenzilumab may minimize or eradicate the incidence, frequency, duration and/or severity of NT and/or CRS associated with CAR-T therapy while enhancing CAR-T proliferation and effector functions and potentially confer additional benefits in terms of healthcare resource utilization. We also believe lenzilumab may further improve the value proposition of CAR-T therapies and facilitate their use and acceptance throughout the healthcare systems in the United States and abroad.

A strong scientific rationale exists for GM-CSF neutralization with lenzilumab to improve the safety, efficacy and cost-effectiveness of CAR-T therapy. Lenzilumab is in development to significantly reduce the incidence and severity of CAR-T induced NT and CRS, and to improve the overall efficacy and duration of response of CAR-T therapy. Robust scientific rationale and independent scientific research from leading institutions support GM-CSF neutralization as a validated target in this setting. In December 2017, we held a scientific advisory board at the 2018 annual meeting of the American Society of Hematology (ASH) with leading key opinion leaders in the CAR-T field to validate the scientific rationale of lenzilumab prophylactic therapy in combination with CAR-T. Based on feedback received from the advisory board, we created the development plan for lenzilumab. To that end, we initiated preclinical studies using proprietary xenograft models in collaboration with the Mayo Clinic, with final results presented at the oral plenary session of the 2018 ASH annual meeting and a manuscript published and featured on the front cover of Blood, the official journal of ASH. In addition, and following subsequent scientific advisory boards convened at the 2018 American Society of Clinical Oncology and ASH annual meetings, we continued to work with leading key opinion leaders and CAR-T centers to advance lenzilumab into phase Ib/II pivotal trials in combination with the approved, CD19 targeted CAR-T therapies.

Following our outreach to key opinion leaders and innovators in the CAR-T field, we tested the hypothesis of using lenzilumab as a prophylactic approach against these side-effects. The preclinical study conducted in 2018 in collaboration with the Mayo Clinic validated our hypothesis that the use of lenzilumab along with CD19 targeted CAR-T effectively neutralized GM-CSF, significantly reduced NT and prevented CRS. In addition, the Mayo Clinic study showed that the use of lenzilumab enhanced CAR-T proliferation and effector functions, enhanced anti-tumor response and improved the efficacy, duration of response and relapse rates of CAR-T therapy. This was the first time it has been demonstrated that the toxicities associated with CAR-T therapy can be effectively abrogated in-vivo.

Our current clinical and regulatory development plan for lenzilumab contemplates company-sponsored or collaborative phase Ib/II clinical trials in combination with approved CD19 targeted CAR-T therapies. Depending upon FDA feedback, we believe these trials may serve as the basis for registration for lenzilumab.

Our Pipeline

We are pursuing several other initiatives with lenzilumab and our two additional novel monoclonal antibodies, ifabotuzumab and HGEN005, in the immune-oncology field. Our monoclonal antibody portfolio was developed using our proprietary, patent-protected Humaneered technology, which consists of methods for converting antibodies (typically murine) into engineered, high-affinity antibodies designed and optimized for human therapeutic use.

| 9 |

These product candidates are in the early stage of development and will require substantial time, resources, research and development, and regulatory approval prior to commercialization. Furthermore, none of these product candidates has advanced into a pivotal registration study and it may be years before such a study is initiated, if at all. Our current pipeline is depicted below:

Pre-clinical research has shown that ifabotuzumab, our first in class anti-EphA3 monoclonal antibody, is an attractive tumor-specific therapy for glioblastoma multiforme (GBM) and other solid tumors, as a naked antibody, as part of an antibody-drug conjugate as well as a backbone for a novel CAR-T construct and a bispecific antibody platform. There has not been a meaningful improvement in overall survival in brain cancer sufferers in decades. Ifabotuzumab crosses the blood-brain barrier (BBB) and accumulates specifically at the tumor site with no observed normal brain tissue uptake. EphA3 is expressed most highly on glioma stem cells (GSCs), where EphA3 has a functional role in survival and self-renewal. In GBM, EphA3 expression has been shown to be significantly elevated in recurrent versus treatment-naïve disease. EphA3 has also been shown to be over-expressed in a number of other solid tumors in humans. EphA3 antibody targeting has been shown to inhibit tumor growth by disrupting newly formed tumor microvasculature (neovasculature). A phase I clinical trial is currently underway using ifabotuzumab in patients with recurrent GBM. This study is in part motivated by reports of the positive results of other ADC therapies in the treatment of GBM. An antibody-drug conjugate (ADC) being developed by Abbvie is in a Phase III clinical study for GBM and utilizes the cytotoxic agent monomethyl auristatin F (MMAF) combined with depatuxizumab. Efficacy has been demonstrated as both a single agent and in combination with temozolomide (TMZ). Ifabotuzumab is being developed by the leading experts in the space, who played a critical role in the discovery and development of the depatuxizumab-based ADC.

HGEN005 is our proprietary Humaneered anti-EMR1 monoclonal antibody in development for various eosinophilic diseases and as a backbone for a novel CAR-T construct for eosinophilic leukemia.

| 10 |

Lenzilumab

Overview and Mechanism of Action

Lenzilumab, previously referred to as KB003, is a novel monoclonal antibody designed to target and neutralize human GM-CSF, which is also known as ‘myeloid inflammation factor’. We used our proprietary and patented-protected Humaneered antibody development platform to develop lenzilumab. There is extensive evidence linking GM-CSF expression to serious and potentially life-threatening side-effects in CAR-T therapy. Our focus for lenzilumab development is investigating its potential to improve efficacy of CAR-T and to prevent or ameliorate CAR-T-related NT and CRS. Following CAR-T administration GM-CSF initiates a signaling cascade of inflammation that results in the trafficking and recruitment of myeloid cells to the tumor site. These myeloid cells then produce key downstream cytokines known to be associated with development of NT and CRS, perpetuating the inflammatory cascade. Peer-reviewed publications in leading journals by well-recognized experts have shown that GM-CSF is a biomarker present in patients who suffer serious NT as a side-effect of CAR-T therapy.

GM-CSF is critical for the initiation of CRS and the inflammatory cascade following CAR-T cell therapy. It is upstream and the precursor to other cytokines involved in the cascade. GM-CSF knock-out (k/o) animals or animals that lack a functional myeloid compartment do not develop CRS and have normal levels of downstream cytokines, including IL-6, IL-1 and MCP-1/CCL2. Animals that are k/o for IL-1, INF-g and IL-6 still develop CRS in models which recapitulate this syndrome. The lack of GM-CSF did not affect T-cell cytotoxicity as GM-CSF k/o animals had equivalent effector to target cell (E:T) ratios and cytotoxic activity against tumour cells. GM-CSF is required for CCR2+ monocytes to initiate and sustain neuro-inflammation. It is postulated that GM-CSF induces CCR2+ inflammatory myeloid derived cells to infiltrate into CNS, activating the microglial cells; the activated microglial cells then increase their expression of CCL2/MCP-1 to further recruit inflammatory myeloid cells in a self-perpetuating manner, forming a positive feedback loop. Research from CAR-T clinical trials demonstrated that fever and elevated MCP-1 levels 36 hours post CAR-T treatment were most predictive of severe CRS and NT across patients with NHL, ALL and CLL.

There are multiple other publications and data that point to the pivotal role of GM-CSF in CRS and NT which have been extensively discussed with leading KOLs. We believe that lenzilumab, used as a companion therapy with CAR-T offers a number of potential benefits, including:

| · | Lower rates of severe/grades >3 CRS and all grades of CRS; |

| · | Lower rates of severe/grades >3 NT and all grades of NT; |

| · | Lower rates of ICU admissions and duration of hospitalization; |

| · | Improved anti-tumor response (e.g. ORR, CR) and overall patient outcomes; |

| · | Improved duration of response and reduced relapse rates; |

| · | Improved cost effectiveness and reduced direct/indirect costs; |

| · | Improved reimbursement, and preferential formulary placement for CAR-T; |

| · | Expansion of CAR-T beyond the relapse/refractory setting to second-line and potential first-line use due to improved benefit-risk profile, increasing utilization to a significantly larger pool of patients; |

| · | Expansion of CAR-T into solid tumor treatments; and |

| · | Scaling back or removal of current CAR-T required REMS programs due to improved benefit-risk profile of CAR-T. |

Preclinical studies conducted at the Mayo Clinic using human ALL blasts, human CD19 CAR-T, and human PBMCs, demonstrate that blockade of GM-CSF with lenzilumab prevents the onset of CRS, reduces neuro-inflammation by 75% (as assessed by quantitative MRI) and maintains the integrity of the BBB compared to CAR-T plus control antibody, where CRS, neuro-inflammation and BBB disruption can be profoundly affected. The administration of lenzilumab in combination with CAR-T therapy led to a significant (5-fold) increase in proliferation of CAR-T cells and improved CAR-T effector function, presumably due to a decrease in MDSC expansion and trafficking which is known to be promulgated by GM-CSF. GM-CSF neutralization in combination with CAR-T therapy reduces relapse, enhances anti-tumor response and improves overall survival compared to CAR-T therapy alone. Moreover, the combination of lenzilumab and CAR-T reduces myeloid cell infiltration into the CNS and results in significantly better leukemic control as quantified by flow cytometry compared to CAR-T and control antibody. Data from CAR-T clinical trials suggests that the only cytokines associated with grade > 3 NT are GM-CSF and IL-2. Moreover, in patients who developed severe NT, there was a 17-fold increase in myeloid cell trafficking into the CNS further establishing the role of GM-CSF in expansion and trafficking of myeloid cells in the toxicities associated with CAR-T therapy.

| 11 |

We are also developing lenzilumab for use in patients with CMML and have completed enrollment of a Phase I study. We are assessing plans to investigate use of lenzilumab in patients with juvenile myelomonocytic leukemia (JMML) where it has been clearly demonstrated that in these pediatric/adolescent patients, there is hypersensitivity to levels of GM-CSF. This could be ameliorated by lenzilumab. Clinical data also shows the potential for lenzilumab as a treatment for certain other conditions, including eosinophilic asthma and rheumatoid arthritis (RA). There is potential for a range of other oncology, immunology and autoimmune conditions and we are actively investigating lifecycle management opportunities for lenzilumab in high value markets with strong unmet medical needs.

Development Program

In Combination with CD19 Targeted CAR-T Therapies

We are working to initiate pivotal studies of lenzilumab prophylaxis in combination with CAR-T therapies with a primary objective of reducing the incidence of grade >3 NT and grade >3 CRS. Secondary endpoints of our planned trials include:

| · | the reduction in incidence of all grades NT and all grades CRS; |

| · | reduction in rates and duration of ICU stay; and |

| · | the impact of lenzilumab on the efficacy of CAR-T, including improvement in the objective response rate (ORR), rate of complete response (CR), duration of response (DOR), progression free survival (PFS) and overall survival (OS). |

Currently, we plan to study lenzilumab with both of the FDA-approved CAR-T therapies (Yescarta and Kymriah) utilizing a Phase Ib run-in section, followed by a Phase II section which will enroll a larger number of patients. The trials are expected to begin enrollment in the second half of 2019 and, if outcomes are positive, study completion in 2020 and a biologics license application, or BLA submission in 2021. A pre-IND meeting with the FDA is planned to align on the study design and overall development objectives, including timing and criteria for achieving breakthrough and orphan designation. We have benchmarked the studies undertaken in the CAR-T space and the regulatory strategies employed to secure FDA approval and intend to leverage this knowledge in our clinical development and regulatory plans. We expect this to be a fast-to-recruit and fast to report study with a high probability of technical and regulatory success given the comprehensive body of evidence supporting this approach. The initial phase Ib component of the trial is designed to confirm the dose and dosing frequency of lenzilumab in combination with CAR-T to take forward into the larger phase II portion of the study.

CMML

We believe lenzilumab has potential as a therapy for CMML, a rare form of hematologic cancer with no FDA-approved treatment options and a three-year overall survival rate of 20% and median overall survival of 20 months. We also believe lenzilumab has potential as a therapy for JMML, a rare pediatric form of leukemia with no FDA-approved treatment options. CMML is a clonal stem cell disorder of which monocytosis is a key feature. CMML has features of myelodysplastic syndrome (MDS) including abnormal, dysplastic bone marrow cells, cytopenia, transfusion dependence, and myeloproliferative neoplasms, including overproduction of white blood cells, organomegaly such as splenomegaly and hepatomegaly and extramedullary disease. Approximately 15% to 20% of CMML cases progress to acute myeloid leukemia, or AML. According to the American Cancer Society, approximately 1,100 individuals in the US are newly diagnosed annually with CMML, with the majority of these new patients being age 60 or older. These patients are typically unsuitable for stem cell transplants. Preclinical studies have shown lenzilumab can cause apoptosis in CMML cells by depriving them of GM-CSF.

An IND for a Phase I/II CMML monotherapy study of lenzilumab is in effect. In July 2016, we initiated dosing in a Phase I multicenter, open label, repeat-dose, clinical trial in patients with previously-treated CMML who are no longer responsive to previous treatment, to identify the recommended Phase II dose of lenzilumab and to assess lenzilumab’s safety, pharmacokinetics, and other measures. The study is fully enrolled. The primary endpoint of this study is the safety of lenzilumab, as measured by the number of participants with adverse events, at various doses in order to determine a recommended Phase II dose. Secondary endpoints include changes in spleen size, blood and bone marrow measurements of disease, clinical symptoms and other measures.

| 12 |

We may investigate lenzilumab as a potential treatment for JMML, either alone or with a partner. There are approximately 420 new cases of JMML annually in the US and the disease mostly affects children aged four and younger. We believe that lenzilumab may be eligible for a rare pediatric disease priority review voucher if approved for JMML. We also believe lenzilumab in CMML or JMML could qualify for orphan drug designation and potentially other FDA incentives.

Previous clinical studies of lenzilumab include a repeat-dose, Phase II clinical trial of lenzilumab in RA with the inclusion of a safety run-in portion. On completing the safety run-in portion of this trial, which showed lenzilumab to be well tolerated with no clinically significant adverse events, we reassessed the increasingly competitive RA market and chose to redirect our study of lenzilumab to other areas given the competitive intensity and diminishing levels of unmet need in RA relative to some other medical areas. Results from a subsequent randomized, double-blinded, placebo-controlled, repeat dose, Phase II clinical trial in severe asthma, showed a statistically significant benefit on patients with eosinophilic asthma. As a result of a strategic shift and other corporate activities, we terminated development of lenzilumab in severe asthma. We have generated safety and tolerability data in more than 110 patients in various clinical studies and have demonstrated lenzilumab to be safe and well tolerated in these settings.

Ifabotuzumab

Ifabotuzumab is a Humaneered monoclonal antibody, formerly referred to as KB004, which targets the EphA3 receptor and in which the antibody carbohydrate chains lack fucose, thereby enhancing the targeted cell-killing activity of the antibody. In 2006, we entered into a license agreement with Ludwig Institute for Cancer Research (LICR) pursuant to which LICR granted certain exclusive rights to the ifabotuzumab prototype (referred to as IIIA4) as well as EphA3 intellectual property.

Ifabotuzumab binds to the EphA3 receptor, which plays an important role in cell positioning and tissue organization during fetal development, but is not thought to play a significant role in healthy adults. EphA3 is a receptor tyrosine kinase aberrantly expressed on the tumor cell surface in a number of hematologic malignancies and solid tumors. It is also expressed on the stem cell compartment, which includes malignant stem cells, the vasculature that feeds them, and the stromal cells that protect them. EphA3 expression has been documented in a number of hematologic and solid tumor types, including AML, chronic myelogenous leukemia, chronic lymphocytic leukemia, MDS, myelofibrosis, multiple myeloma, melanoma, breast cancer, non-small cell lung cancer, colorectal cancer, gastric cancer, renal cancer, glioblastoma multiforme (GBM), and prostate cancer, making it an attractive target. Publications related to certain cancers have indicated that EphA3 tumor cell expression correlates with cancer growth and a poor prognosis. EphA3 is overexpressed in GBM and, in particular, in the most aggressive mesenchymal subtype. Importantly, EphA3 is highly expressed on the tumor-initiating cell population in glioma and appears critically involved in maintaining tumor cells in a less differentiated state by modulating mitogen-activated protein kinase signaling. EphA3 knockdown or depletion of EphA3-positive tumor cells may reduce tumorigenic potential to a degree comparable to treatment with a therapeutic radiolabeled EphA3-specific monoclonal antibody. We believe EphA3 is a functional, targetable receptor in GBM as well as certain lymphomas and leukemias. A study published in December 2018 showed that an antibody drug conjugate (ADC) comprising IIIA4 (a predecessor monoclonal antibody and prototype for ifabotuzumab) showed significant survival benefit in mice with GBM.

Anti-EphA3 treatment has shown encouraging preclinical results in multiple experiment types, including patient primary tumor cell assays, colony forming assays, and xenograft mouse models. Upon binding to EphA3, ifabotuzumab causes cell killing to occur either through antibody-dependent, cell-mediated cytotoxicity (ADCC) or through direct apoptosis, and in the case of tumor neovasculature, through cell rounding and blood vessel disruption. Given the expression pattern of EphA3 in multiple tumor types, ifabotuzumab may have the potential to kill cancer cells and the tumor stem cell microenvironment, providing for long-term responses while sparing normal cells.

| 13 |

Further, by developing ifabotuzumab as the backbone for a next generation CAR construct, we may have the ability to target both the tumor and tumor vasculature in a novel manner and build on the experience with current second generation CD19 CAR-T cell therapies. An investigator-sponsored Phase I radiolabeled imaging trial of ifabotuzumab in GBM, a particularly aggressive and deadly form of brain cancer, has begun at the Olivia-Newton John Cancer Institute in Melbourne, Australia and has now expanded to include a site in Brisbane, Australia. On December 5, 2017, the first patient received ifabotuzumab in a trial that will seek to confirm the safety of ifabotuzumab and potentially determine the best dose to effectively penetrate brain tumors. Currently, five patients with recurrent GBM have received ifabotuzumab in this study and the investigators expect approximately 12-18 patients to participate in the trial. Given the interest in EphA3 as a target, the broad range of potential tumors that express EphA3 and our own CAR development, we are now evaluating wider opportunities to partner ifabotuzumab.

We are in discussions with separate and various parties and may initiate partnerships to pursue some of the following activities:

| · | Initiate and complete pre-clinical studies with a CAR product; |

| · | Complete the on-going clinical study and pre-clinical studies with various ADCs that are based on ifabotuzumab (in partnership with leading centers in Australia); |

| · | Develop bi-specific antibodies based on ifabotuzumab; and |

| · | Develop a radiopharmaceutical therapeutic. |

We have conducted a Phase I/II trial for ifabotuzumab in multiple hematologic malignancies. The most common adverse event attributed to ifabotuzumab in this trial was infusion reactions (chills, fever, nausea, hypertension, and rapid heart rate) which is an expected safety finding based on the mechanism of action. The majority of infusion reactions were mild-to-moderate in severity and resolved with temporary stoppage of infusion and/or use of medications to treat symptoms. In 2014, we completed the Phase I dose escalation portion of our study, primarily treating patients with AML as well as patients with MDS and myelofibrosis. We suspended enrollment in that study due to the bankruptcy filing in December 2015.

Centers in Australia continued to work independently on IIIA4, the murine antibody parent of ifabotuzumab, as an ADC in mice and a December 2018 publication in the journal ‘Cancers’ showed that in mice engrafted with GBM, treatment with an ADC based on IIIA4 showed significantly improved survival. The authors pointed out the similarities between this approach and that taken by AbbVie with their ADC (depatuxizumab mafodotin) currently in Phase III for GBM. We have developed, with a collaborator in a leading center, ifabotuzumab mafodotin and initiated pre-clinical animal testing. The aim is to develop this ADC for the treatment of GBM, similar to what AbbVie have done, and explore use in other solid tumors that express EphA3.

HGEN005

HGEN005 is a pre-clinical stage Humaneered monoclonal antibody that is being evaluated as a novel treatment for disorders caused by eosinophils. Eosinophils are multi-functional white blood cells implicated in the pathogenesis of a wide variety of disorders including: eosinophilic leukemia, eosinophilic esophagitis, eosinophilic/allergic asthma, helminth (intestinal worm) infections, hematologic malignancies and hypereosinophilic syndromes (HES). The target for HGEN005 is EMR1 (human epidermal growth factor-like module containing mucin-like hormone receptor) a G-protein coupled receptor of unknown function. An analysis of human blood and bone marrow confirmed that EMR1 expression is high and restricted to eosinophils. In vivo studies have demonstrated that blood eosinophils are efficiently and selectively depleted by targeting EMR1 with a chimeric antibody precursor to HGEN005 and this work was published in J. Allergy Clin. Immunol. Importantly, HGEN005 does not to appear to impact mast cells, while selectively and effectively depleting eosinophils.

HGEN005 may offer utility as part of a CAR-T approach in serious eosinophilic disorders. We are collaborating with a top US center to develop an HGEN005-based CAR, potentially as a treatment for eosinophilic leukemia, an orphan disease with high unmet medical need and also exploring partnering opportunities.

| 14 |

Our Humaneered Technology

Our proprietary and patented Humaneered technology platform is a method for converting existing antibodies (typically murine) into engineered, high-affinity human antibodies designed for therapeutic use, particularly for chronic conditions. We have developed or in-licensed targets or research (mouse) antibodies, typically from academic institutions, and then applied our Humaneered technology to them. Lenzilumab, ifabotuzumab and HGEN005 are Humaneered antibodies. In aggregate, our Humaneered antibodies have been tested clinically in more than 200 patients with no evidence of serious immunogenicity. We believe our Humaneered antibodies are closer to human antibodies than chimeric or conventionally humanized antibodies, that they are prone to being rejected less and may bind better to their target. Specifically, our Humaneered technology generates an antibody from an existing antibody with the required specificity as a starting point and, we believe, provides the following advantages:

| · | retention of identical target epitope specificity of the starting antibody and frequent generation of higher affinity antibodies; |

| · | very-near-to-human germ line sequence, which we believe means our Humaneered antibodies are less likely to induce an inappropriate immune response in broad patient populations when used chronically than chimeric or conventionally humanized antibodies, which has proven to be the case in clinical studies; |

| · | antibodies with physiochemical properties that facilitate process development and formulation (lack of aggregation at high concentration); |

| · | high solubility; |

| · | high antibody expression yields; |

| · | an optimized antibody processing time of three to six months; and |

| · | potential cost-of-goods benefits. |

As we are focused on progressing our current portfolio of antibodies through clinical development and out-licensing, we are not currently dedicating additional resources to the research or development of additional Humaneered antibodies other than our existing portfolio of lenzilumab, ifabotuzumab and HGEN005.

Intellectual Property

Licensing and Collaborations

The Ludwig Institute for Cancer Research

In May 2004, we entered into a license agreement with the Ludwig Institute for Cancer Research (LICR) pursuant to which LICR granted to us an exclusive license for intellectual property rights and materials related to chimeric anti-GM-CSF antibodies that formed the basis for lenzilumab. Under the agreement, we were granted an exclusive license to develop antibodies related to LICR’s antibodies against GM-CSF. We are responsible for using commercially reasonable efforts to research, develop, and sell lenzilumab. We pay LICR a quarterly license fee and are obligated to pay to LICR a royalty from 1.5% to 3% of net sales of licensed products, subject to certain potential offsets and deductions. Our royalty obligation applies on a country-by-country and licensed product-by-licensed product basis, and will begin on the first commercial sale of a licensed product in a given country and end on the later of the expiration of the last to expire patent covering a licensed product in a given country (which in the United States, is currently expected in 2029 for the composition of matter and 2038 for methods of use in CAR-T) or 10 years from first commercial sale of such licensed product in the country. We must also pay to LICR a certain percentage of sublicensing revenue received by us. Payments made to LICR under this license for the twelve months ended December 31, 2018 and 2017 were $0.1 million and $0.1 million, respectively.

| 15 |

Other Material License Agreements

LICR and ifabotuzumab

In 2006, we entered into a license agreement with LICR pursuant to which LICR granted to us certain exclusive rights to the ifabotuzumab prototype (IIIA4) which targets the EphA3 receptor and EphA3-related intellectual property. Under the agreement, we obtained rights to develop and commercialize products made through use of licensed patents and any improvements thereto, including human or Humaneered antibodies that bind to or modulate EphA3. We paid LICR an upfront option fee of $0.05 million and a further $0.05 million upon our exercise of the option for the exclusive license outlined above. We are responsible for contingent milestone payments of less than $2.5 million and royalties of 3% of net sales subject to certain potential offsets and deductions. In addition, we are obligated to pay to LICR a percentage of certain payments we receive from any sublicensee in consideration for a sublicense. Our royalty obligation exists on a country-by-country and licensed product-by-licensed product basis, which will begin on the first commercial sale and end on the later of the expiration of the last to expire patent covering such licensed product in such country, which in the United States is currently expected in 2031, or 10 years from first commercial sale of such licensed product in such country.

BioWa and Lonza

In October 2010, we entered into a license agreement with BioWa, Inc. (BioWa) and Lonza Sales AG (Lonza) pursuant to which BioWa and Lonza granted us a non-exclusive, royalty-bearing, sub-licensable license under certain know-how and patents related to antibody expression and antibody-dependent cellular cytotoxicity enhancing technology using BioWa and Lonza’s Potelligent® CHOK1SV technology. This technology is used to enhance the cell killing capabilities of antibodies and is currently used by us in connection with our development of ifabotuzumab. Under this agreement, we owe annual license fees, milestone payments in connection with certain regulatory and sales milestones and royalties in the low single digits on net sales of products developed under the agreement. The agreement expires upon the expiration of royalty payment obligations under the agreement, is terminable at will by us upon written notice, is terminable by BioWa and Lonza if we challenge or otherwise oppose any licensed patents under the agreement, and is terminable by either party upon the occurrence of an uncured material breach or insolvency. Payments made to BioWa under this license for the twelve months ended December 31, 2018 and 2017 were $0.1 million and $0.1 million, respectively.

Patents and Trade Secrets

We use a combination of patent, trade secret and other intellectual property protections to protect our product candidates. We will be able to protect our product candidates from unauthorized use by third parties only to the extent they are covered by valid and enforceable patents or to the extent our technology is effectively maintained as trade secrets. Patent and trade secrets are an important element of our business. Our success will depend in part on our ability to obtain, maintain, defend and enforce patent rights for and to extend the life of patents covering lenzilumab, ifabotuzumab, HGEN005 and our Humaneered technology, to preserve trade secrets and proprietary know how, and to operate without infringing the patents and proprietary rights of third parties. We actively seek patent protection, if available, in the United States and select foreign countries for the technology we develop. We have 74 registered patents, including 17 registered in the U.S. and 57 registered in foreign countries. Of the 74 registered patents, 50 are owned by us, nine are owned jointly with a third party, and 15 are exclusively licensed from a third party. We also have 15 patent applications pending globally.

Using our Humaneered technology, we developed and own a composition of matter patent covering lenzilumab and related anti-GM-CSF antibodies that provide patent protection through April 2029 and have additional pending patents in the United States and a number of foreign countries covering various methods of treatment, including in the CAR-T space covering a broad and comprehensive range of approaches to neutralizing GM-CSF, which, if granted, is expected to confer protection to at least October 2038. We also have current and pending patent applications in the United States and selected foreign countries for anti-EphA3 antibodies and their use, and we developed and own an issued U.S. composition of matter patent covering ifabotuzumab and related anti-EphA3 antibodies, which is currently expected to expire in 2031. The patents to our Humaneered technology cover methods of producing human antibodies that are very specific for target antigens using only a small region from mouse antibodies.

| 16 |

We cannot be certain that any of our pending patent applications, or those of our licensors, will result in issued patents. In addition, because the patent positions of biopharmaceutical companies are highly uncertain and involve complex legal and factual questions, the patents we own and license, or any further patents we may own or license, may not prevent other companies from developing similar or therapeutically equivalent products, even though we may be able to prevent their commercial use without our permission if our intellectual property allows for such limitations. Patents also will not protect our products if competitors devise ways of making or using these products without legally infringing our patents. We cannot be assured that our patents will not be challenged by third parties or that we will be successful in any defense we undertake.

In addition, changes in patent laws, rules or regulations or in their interpretations by the courts may materially diminish the value of our intellectual property or narrow the scope of our patent protection, which could have a material adverse effect on our business and financial condition. However, prospective partners may have to license or otherwise come to an agreement with us if they wish to use our products and those products and methods of use of such products have issued patents in those territories.

We also rely on trade secrets, technical know-how and continuing innovation to develop and maintain our competitive position. We seek to protect our proprietary information by requiring our employees, consultants, contractors, outside scientific collaborators and other advisors to execute non-disclosure and confidentiality agreements and our employees to execute assignment of invention agreements to us on commencement of their employment. Agreements with our employees also prevent them from bringing any proprietary rights of third parties to us. We also require confidentiality or material transfer agreements from third parties that receive our confidential data or materials.

Manufacturing

We outsource basic development activities, including the development of formulation prototypes, and have adopted a manufacturing strategy of contracting with third parties for the manufacture of drug substance and product. Additional contract manufacturers are used to fill, label, package, and distribute investigational drug products. This allows us to maintain a more flexible infrastructure while focusing our expertise on developing our products. It does however mean that we have to carefully plan the availability of manufacturing ‘slots’ and the availability of drug for investigation in preclinical and clinical trials. The use of contract manufacturers can be expensive, complicated and time consuming and could delay clinical trials, drug approval and potential product launch.

Sales and Marketing

We do not currently have the sales and marketing infrastructure in place that would be necessary to market and sell our products, if approved. The establishment of a sales and marketing operation can be expensive, complicated and time consuming and could delay any potential product launch. As our drug candidates progress, while we may build or contract with expert commercial vendors the type of infrastructure that would be needed to successfully market and sell any successful drug candidate on our own, we may also seek strategic alliances and partnerships with third parties including those with existing infrastructure.

Competition

We compete in an industry characterized by rapidly advancing technologies, intense competition, a changing regulatory and legislative landscape and a strong emphasis on the benefits of intellectual property protection and regulatory exclusivities. Our competitors include pharmaceutical companies, other biotechnology companies, academic institutions, government agencies and other private and public research organizations. We compete with these parties for therapies for neglected and rare diseases and in recruiting highly qualified personnel. Our product candidates, if successfully developed and approved, may compete with established therapies, with new treatments that may be introduced by our competitors, including competitors relying to a large extent on our drug approvals or on our biologics approvals, or with generic copies of our product approved by FDA, as bio-similars, referencing our drug products. Many of our potential competitors have substantially greater scientific, research, and product development capabilities, as well as greater financial, marketing, sales and human resources capabilities than we do.

| 17 |

In addition, many specialized biotechnology firms have formed collaborations with large, established companies to support the research, development and commercialization of products that may be competitive with ours. Accordingly, our competitors may be more successful with respect to their products than we may be in developing, commercializing, and achieving widespread market acceptance for our products. In addition, our competitors’ products may be more effective or more effectively marketed and sold than any treatment we or our development partners may commercialize and may render our product candidates obsolete or non-competitive before we can recover the expenses related to developing and supporting the commercialization of any of our product candidates. Developments by competitors may render our product candidates obsolete or noncompetitive. After one of our product candidates is approved, FDA may also approve a generic version with the same or similar dosage form, safety, strength, route of administration, quality, performance characteristics and intended use as our product. These bio-similar equivalents would be less costly to bring to market and could generally be offered at lower prices, thereby limiting our ability to gain or retain market share. However, our product candidates are all biologics and, as such, would benefit from 12 years market exclusivity from launch in the United States.

The acquisition or licensing of pharmaceutical products is also very competitive, and a number of more established companies, which have acknowledged strategies to in-license or acquire products, may have competitive advantages as may other emerging companies taking similar or different approaches to product acquisitions. The more established companies may have a competitive advantage over us due to their size, cash flows, institutional experience and historical corporate reputation.

Lenzilumab and CAR-T-related toxicities competition

Significant ongoing concerns for clinicians, care-givers, patients and FDA regarding CAR-T therapy are current levels of efficacy, duration of response, relapse, long-term outcomes and serious and potentially life-threatening side-effects, namely NT and CRS. Both Kymriah and Yescarta carry black box warnings in their labels for NT and CRS and are subject to a REMS program, such that on-going data has to be provide to FDA and the CAR-T products can only be administered in strictly controlled situations at trained centers.

There are no FDA-approved therapies for the prevention of CAR-T-induced NT and CRS or for the treatment of CAR-T induced NT. The CAR-T-cell-therapy-associated TOXicity (CARTOX) Working Group currently recommends intensive monitoring, accurate grading and aggressive supportive care with the anti-IL-6 receptor blocker tocilizumab (Genentech’s Actemra®) and/or high-dose corticosteroids. These treatments are reserved only for the treatment of severe cases of CRS and are not approved for prevention. Since corticosteroids suppress T-cell function and/or induce T-cell apoptosis, they may limit the effectiveness of CAR-T cell therapy; thus use of corticosteroids is generally limited to moderate-to-severe cases of CRS refractory to tocilizumab and severe cases of NT. Sometimes high-dose corticosteroids are used alongside tocilizumab, although there is no evidence for either intervention impacting morbidity or mortality. Tocilizumab has not been found to be effective in the prevention or management of CAR-T-induced NT. In fact its early use has been shown to increase rates of NT in a cohort of patients evaluated in clinical trial setting. Serum IL-6 levels have been shown to increase shortly after administration of tocilizumab which may increase passive diffusion of IL-6 into the CNS and increase the risk of NT. A similar concern may apply in terms of increasing the levels of GM-CSF if a GM-CSF receptor blocker is utilized. Lenzilumab neutralizes GM-CSF without interfering with the GM-CSF receptor.

There are no prospective, randomized clinical trials evaluating the safety and efficacy of tocilizumab for the treatment of CAR-T induced CRS. FDA approval of tocilizumab with or without high-dose corticosteroids, for the management of severe cases of CRS was announced in conjunction with approval of Kymriah solely as part of its REMS program based on a retrospective analysis of 45 patients across CAR-T clinical trials despite the lack of an IND, NDA or conduct of a prospective trial of tocilizumab in this setting. Tocilizumab is not approved for the prevention of CRS nor for the prevention or treatment of NT. Tocilizumab is also not approved for the treatment of mild or moderate cases of CRS.

| 18 |

There are several experimental approaches in early stage development in an effort to bring forward next-generation, CAR-T constructs, including introducing suicide genes into CAR-T cells using herpes simplex virus thymidine kinase (HSV-TK) or inducible caspase-9 (iCasp9) genes with “on / off” switches, RNA-guided DNA targeting technology such as CRISPR/Cas9 system or other epitope-based / gene-editing technology. It is possible that these approaches could prevent CAR-T induced NT and/or CRS. However, these are all in early stages of development and may never progress into the clinic or to approval. Even if they do enter development, they would likely take many years to progress through to approval, if at all. There are several other anti-GM-CSF compounds that are in various stages of development, however the focus of all of these compounds appears to be in chronic autoimmune disorders such as rheumatoid arthritis, axial spondyloarthritis, giant cell arteritis and related disorders.

Government Regulation

Drug Development and Approval in the U.S.

As a biopharmaceutical company operating in the United States, we are subject to extensive regulation by FDA and by other federal, state, and local regulatory agencies. FDA regulates biological products such as our product candidates under the United States Federal Food and Cosmetic Act (FDCA) the Public Health Service Act (PHSA) and their implementing regulations. Under the PHSA, an FDA-approved biologics license application (BLA) is required to market a biological product, or biologic, in the United States. These laws and regulations set forth, among other things, requirements for preclinical and clinical testing, development, approval, labeling, manufacture, storage, record keeping, reporting, distribution, import, export, advertising, and promotion of our products and product candidates. Biologics receive 12 years market exclusivity from approval and launch.

Applications Relying on the Applicant’s Clinical Data

The approval process for a BLA under the PHSA requires the conduct of extensive studies and the submission of large amounts of data by the applicant. The biologic development process for these applications will generally include the following phases:

Preclinical Testing. Before testing any new biologic in human subjects in the United States, a company must generate extensive preclinical data. Preclinical testing generally includes laboratory evaluation of product chemistry and formulation, as well as toxicological and pharmacological studies in several animal species to assess the quality and safety of the product. Animal studies must be performed in compliance with FDA’s Good Laboratory Practice (GLP) regulations and the United States Department of Agriculture’s Animal Welfare Act.

IND Application. Human clinical trials in the United States cannot commence until an Investigational New Drug (IND) application is submitted and becomes effective. A company must submit preclinical testing results to FDA as part of the IND, and FDA must evaluate whether there is an adequate basis for testing the product in initial clinical studies in human volunteers. Unless FDA raises concerns, the IND becomes effective 30 days following its receipt by FDA. Once human clinical trials have commenced, FDA may stop the clinical trials by placing them on “clinical hold” because of concerns about the safety of the product being tested, or for other reasons.

Clinical Trials. Clinical trials involve the administration of the product to healthy human volunteers or to patients, under the supervision of a qualified investigator. The conduct of clinical trials is subject to extensive regulation, including compliance with FDA’s bioresearch monitoring regulations and Good Clinical Practice (GCP) requirements, which establish standards for conducting, recording data from, and reporting the results of clinical trials. GCP requirements are intended to assure that the data and reported results are credible and accurate, and that the rights, safety, and well-being of study participants are protected.

| 19 |

Clinical trials must be conducted under protocols that detail the study objectives, parameters for monitoring safety, and the efficacy criteria, if any, to be evaluated. Each protocol is submitted to FDA as part of the IND. In addition, each clinical trial must be reviewed, approved, and conducted under the auspices of an Institutional Review Board (IRB), at the institution conducting the clinical trial. Companies sponsoring the clinical trials, investigators, and IRBs also must comply with regulations and guidelines for obtaining informed consent from the study subjects, complying with the protocol and investigational plan, adequately monitoring the clinical trial, and timely reporting of adverse events. Foreign studies conducted under an IND must meet the same requirements that apply to studies being conducted in the United States. Data from a foreign study not conducted under an IND may be submitted in support of a BLA if the study was conducted in accordance with GCP and FDA is able to validate the data. A study sponsor is required to publicly post certain details about active clinical trials and clinical trial results on the government website clinicaltrials.gov.

Human clinical trials are typically conducted in three sequential phases, although the phases may overlap with one another and, notably, in the CAR-T setting, FDA has granted approval to both currently marketed CAR-Ts based on Phase II data and to tocilizumab without any prospective data in the CAR-T setting:

| · | Phase I clinical trials include the initial administration of the investigational product to humans, typically to a small group of healthy human subjects, but occasionally to a group of patients with the targeted disease or disorder. Phase I clinical trials generally are intended to determine the metabolism and pharmacologic actions of the product, the side effects associated with increasing doses, and, if possible, to gain early evidence of effectiveness. |

| · | Phase II clinical trials generally are controlled studies that involve a relatively small sample of the intended patient population, and are designed to develop data regarding the product’s effectiveness, to determine dose response and the optimal dose range, and to gather additional information relating to safety and potential adverse effects. |

| · | Phase III clinical trials are conducted after preliminary evidence of effectiveness has been obtained and are intended to gather additional information about safety and effectiveness necessary to evaluate the product’s overall risk-benefit profile, and to provide a basis for physician labeling. Generally, Phase III clinical development programs consist of expanded, large-scale studies of patients with the target disease or disorder to obtain statistical evidence of the efficacy and safety of the drug at the proposed dosing regimen, or with the safety, purity, and potency of a biological product. |

| · | The FDA does not always require every approved therapy to complete Phase I through III studies to secure approval. Approval through expedited routes is at the discretion of FDA. |

The sponsoring company, FDA, or the IRB may suspend or terminate a clinical trial at any time on various grounds, including a finding that the subjects are being exposed to an unacceptable health risk. Further, success in early-stage clinical trials does not assure success in later-stage clinical trials. Data obtained from clinical activities are not always conclusive and may be subject to alternative interpretations that could delay, limit, or prevent regulatory approval.

| 20 |

BLA Submission and Review

After completing clinical testing of an investigational biologic product, a sponsor must prepare and submit a BLA for review and approval by FDA. A BLA is a comprehensive, multi-volume application that must include, among other things, sufficient data establishing the safety, purity and potency of the proposed biological product for its intended indication. The application includes all relevant data available from pertinent preclinical and clinical trials, including negative or ambiguous results as well as positive findings, together with detailed information relating to the product’s chemistry, manufacturing, controls and proposed labeling. When a BLA is submitted, FDA conducts a preliminary review to determine whether the application is sufficiently complete to be accepted for filing. If it is not, FDA may refuse to file the application and may request additional information, in which case the application must be resubmitted with the supplemental information and review of the application is delayed.