UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the fiscal year ended | ||

OR | ||

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||

For the transition period from to

Commission file number:

(Exact Name of Registrant as Specified in its Charter) |

| ||

(State of other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

| |

| ||

(Address of Principal Executive Offices) |

| (Zip Code) |

(

(Registrant’s Telephone Number, including Area Code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of Each Class |

| Trading Symbol(s) |

| Name of Each Exchange on Which Registered |

|

| TBR |

| OTCQB TSX-V |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐

Indicate by check mark whether the Registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 (“Exchange Act”) during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging Growth Company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the Registrant is a shell company, as defined in Rule 12b-2 of the Exchange Act. Yes

As of March 31, 2023, the aggregate market value of the voting and non-voting shares of common stock of the registrant issued and outstanding on such date, excluding shares held by affiliates of the registrant as a group, was $

Number of shares of Common Stock outstanding as of December 29, 2022:

TABLE OF CONTENTS

| 2 |

| Table of Contents |

Unless otherwise indicated, any reference to “Timberline”, or “we”, “us”, “our”, etc. refers to Timberline Resources Corporation and/or all its subsidiaries, including Staccato Gold, BH Minerals, Wolfpack US, Lookout Mountain LLC and Talapoosa Development Corp.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the exhibits attached hereto contain “forward-looking statements” within the meaning of the various provisions of the Securities Act of 1933, as amended (the “Securities Act”), and the Securities Exchange Act of 1934 (the “Exchange Act”). Such forward-looking statements concern the Company’s anticipated results and developments in its operations in future periods, planned exploration and development of its properties, plans related to its business and other matters that may occur in the future. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. These statements include, but are not limited to, comments regarding:

| · | the establishment and estimates of tonnage and grade of mineralization and reserves; |

| · | forecasts of future gold and silver prices, anticipated expenditures and costs in our operations; |

| · | planned exploration activities and the anticipated timing and results of exploration activities; |

| · | planned technical reports, economic assessments and feasibility studies on our properties; |

| · | plans and anticipated timing for obtaining permits and licenses for our properties; |

| · | expected future financing and its anticipated outcome; |

| · | plans and anticipated timing regarding production dates; |

| · | anticipated liquidity to meet expected operating costs and capital requirements; |

| · | our ability to obtain financing to fund our estimated expenditure and capital requirements; and |

| · | factors expected to impact our results of operations. |

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, using words or phrases such as “expects” or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and may be forward-looking statements. Forward-looking statements are subject to a variety of known and unknown risks, uncertainties, and other factors which could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation, risks related to:

| · | our limited operating history; |

| · | our ability to continue as a going concern and to fund our operations; |

| · | a history of losses and our expectation of continued losses; |

| · | the geological risk of mineral exploration; |

| · | properties being in the exploration or, if warranted, development stage; |

| · | bringing our projects into production; |

| · | legislative and administrative changes to mining and environmental laws; |

| · | land reclamation requirements and costs; |

| · | mineral exploration and development activities being inherently hazardous; |

| · | our insurance coverage for operating risks; |

| · | cost increases for our exploration and development projects; |

| · | shortages of skilled personnel, equipment and supplies adversely affecting our ability to operate; |

| · | mineral resource and economic estimates; |

| · | the metallurgical characteristics of current resources and future discoveries; |

| · | fluctuation of prices for precious and base metals, such as gold, silver and copper; |

| · | competition in the mineral exploration industry; |

| · | title and rights in our mineral properties; |

| · | integration issues with acquisitions; |

| · | our shares trading on the Over-the-Counter markets and market conditions generally; |

| · | joint ventures and partnerships; |

| 3 |

| Table of Contents |

| · | potential conflicts of interest of our management; |

| · | dependence on key management; |

| · | our Eureka and other acquired growth projects; |

| · | our business model; |

| · | evolving corporate governance standards for public companies; |

| · | our Canadian regulatory requirements; and |

| · | our shares of common stock or other securities. |

This list is not exhaustive of the factors that may affect our forward-looking statements. Some of the important risks and uncertainties that could affect forward-looking statements are described further under the sections titled “Risk Factors”, “Description of Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, believed, estimated, or expected. We caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. We disclaim any obligation subsequently to revise any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events, except as required by law.

We qualify all the forward-looking statements contained in this Annual Report by the foregoing cautionary statements.

| 4 |

| Table of Contents |

PART I

Note to U.S. Investors Regarding Mineral Reserve and Resource Estimates

Certain of the technical reports referenced in this Annual Report use the terms "mineral resource," "measured mineral resource," "indicated mineral resource" and "inferred mineral resource". We advise investors that these terms are defined in and required to be disclosed in accordance with Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) – CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. As a reporting issuer in Canada, we are required to prepare reports on our mineral properties in accordance with NI 43-101. We reference those technical reports in this Annual Report for informational purposes only, and such reports are not incorporated herein by reference. "Inferred mineral resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Investors are cautioned not to assume that any part or all of mineral deposits in the above categories will ever be converted into reserves.

Effective January 1, 2021, the Securities and Exchange Commission (“SEC”) adopted amendments to modernize the property disclosure requirements for mining registrants and related guidance, which are currently set forth in Item 102 of Regulation S-K Subpart 1300 under the Securities Act of 1933 and the Securities Exchange Act of 1934. The amendments more closely align the SEC’s disclosure requirements and policies for mining properties with current industry and global regulatory practices and standards. This Annual Report on Form 10-K incorporates the disclosures and information required under the guidance of Subpart 1300.

ITEM 1. DESCRIPTION OF BUSINESS

Incorporation and Early History

We were incorporated in the State of Idaho in August 1968 under the name Silver Crystal Mines, Inc., to engage in the business of exploring for precious metal deposits and advancing them toward production. We ceased exploration activities during the 1990’s and became virtually inactive. In December 2003, a group of investors purchased 80-percent of the issued and outstanding common stock from the then-controlling management team. In January 2004, we affected a one-for-four reverse split of our issued and outstanding shares of common stock and increased the number of our authorized shares of common stock to 100,000,000 with a par value of $0.001.

In February 2004, our name was changed to Timberline Resources Corporation. Since the reorganization, we have been in an exploration stage evaluating, acquiring, and exploring mineral prospects with potential for economic deposits of precious and base metals. We define a prospect as a mining property, the value of which has not been determined by exploration. In August 2008, we reincorporated into the State of Delaware pursuant to a merger agreement approved by our shareholders.

In July 2007, we closed our purchase of the Butte Highlands Gold Project. In October 2008, we announced that we had agreed to form a 50/50 joint venture at the Butte Highlands Project. In July 2009, we finalized the joint venture agreement with Highland Mining, LLC (“Highland”) to create Butte Highlands JV, LLC (“BHJV”). Under terms of the joint venture agreement, development began in the summer of 2009, with Highland funding all mine development costs through development. Both Timberline’s and Highland’s 50-percent share of costs were to be paid out of net proceeds from future mine production. On January 29, 2016, we executed a Member Interest Purchase Agreement (the “Purchase Agreement”) with New Jersey Mining Company pursuant to which we sold all of our 50% interest in BHJV.

In June 2010, we closed our acquisition of Staccato Gold Resources Ltd. (“Staccato Gold”), a Canadian-based resource company that was in the business of acquiring, exploring, and developing mineral properties with a focus on gold exploration in the dominant gold producing trends in Nevada. As a result of this acquisition, we obtained Staccato’s flagship gold exploration project (“Lookout Mountain”), and several other projects at various stages of exploration in the Battle Mountain/Eureka gold trend in north-central Nevada, along with Staccato Gold’s wholly owned U.S. subsidiary, BH Minerals USA, Inc. (“BH Minerals”).

In August 2014, we closed our acquisition of Wolfpack Gold (Nevada) Corp. (“Wolfpack US”), a U.S. company and a wholly owned subsidiary of Wolfpack Gold Corp., a Canadian-based resource company (“Wolfpack Gold”), that was in the business of acquiring, exploring, and developing mineral properties with a focus on gold exploration in the dominant gold producing trends in Nevada. As a result of this acquisition, we obtained cash and several projects at various stages of exploration in the gold trends in Nevada.

| 5 |

| Table of Contents |

On March 17, 2015, Timberline signed a definitive option agreement to purchase 100% ownership in the Talapoosa Project in Nevada from Gunpoint Exploration Ltd. (Gunpoint). The Talapoosa Project is located in western Nevada and contains a resource of over 1 million ounces of gold. Under terms of the agreement Timberline paid Gunpoint $300,000 in cash and 2,000,000 shares of common stock on signing the agreement and was required to pay $10,000,000 (“Option Payment”) within 30 months of the agreement date to acquire 100% ownership, subject to significant contingent payments if the price of gold traded above US $1,600 per ounce for extended periods in the five (5) ensuing years. On October 26, 2016, the agreement was amended to extend the option exercise period to March 31, 2019 with the following schedule: payment of $1,000,000 and 1,000,000 common shares of the Company by March 31, 2017, payment of $2,000,000 and 1,000,000 common shares by March 31, 2018, and a final payment of $8,000,000 and 1.5 million common shares by March 31, 2019. Timberline chose to not make the required payment due on March 31, 2018, and, therefore, the Agreement was terminated, resulting in a $3.2 million write off of a loss on abandonment of mineral rights.

In May 2018, we entered into a definitive agreement to acquire ownership interests in two joint venture agreements in Nevada from Americas Gold Exploration, Inc (“AGEI”). The acquisition included a 73.7% interest in the Paiute property joint venture with Nevada Gold Mines LLC (“Nevada Gold”), and the opportunity to earn up to 65% ownership in the Elder Creek joint venture with McEwen Mining, Inc. The acquisition of the two joint venture ownership interests, at Elder Creek with McEwen Mining and at Paiute with Nevada Gold, from AGEI closed on August 14, 2018 for consideration of ten million shares of our common stock and five million warrants to purchase shares of our common stock. An additional five million warrants with the same terms were issued to AGEI contingent upon certain achievements. Upon closing, we became the operator at both of these joint venture projects. Timberline elected to return control and ownership of the Elder Creek property to McEwen Mining in July of 2020.

The ICBM Joint Venture Earn-in Agreement has expired, and Timberline vested its property interest at 74.1%.

During the year ended September 30, 2019, the Company recognized an abandonment expense of $48,500 relating to two patented mining claims at in the New York Canyon area of the Eureka property on which the Company had ceased making advance royalty payments.

On June 28, 2019, we entered into a Limited Liability Company Agreement (the “LLC” and the “LLC Agreement”) with PM & Gold Mines, Inc. (“PM&G”) for the advanced exploration, and if determined feasible, the development of the Lookout Mountain Gold Project, a significant portion of the Company’s broader Eureka property located on the southern end of the Battle Mountain-Eureka Trend near Eureka, Nevada. PM&G was a private firm incorporated in Nevada with an interest to explore and advance gold projects to production. The LLC Agreement called for PM&G to fund exploration and development activities in two stages for earned equity in the project. Timberline was to contribute certain claims that constituted the Lookout Mountain Project and adjacent historical Oswego Mine area to the LLC in exchange for its ownership position.

Concurrent with completion of the LLC Agreement, PM&G also participated in a private placement and acquired 3,367,441 shares, or 4.99%, of our common shares. The placement included the right of PM&G to maintain its position in Timberline by pro-rata participation in future financings. The initial interests in the LLC were 51% PM&G and 49% Timberline, subject to PM&G’s contribution to the LLC in the form of an earn-in. Timberline would manage the project through at least the initial stage of investment, at which time PM&G would have been vested at 51% ownership. PM&G retained the right to manage all subsequent activities with or without Timberline’s participation.

Under terms of the LLC Agreement, PM&G committed to $3,000,000 of work expenditure during each of the first two years following the agreement effective date of June 28, 2019. PM&G committed $755,605 towards the first-year obligation due on June 28, 2020, but failed to deliver sufficient capital to meet the required first year investment. Under the terms of the agreement, after written notice and a 30-day cure period, PM&G did not cure the matter and thereby resigned from the LLC Agreement, giving up all claims and rights to the property.

Overview of Our Mineral Exploration Business

We are a mineral exploration business and, if and when we establish mineral reserves, a development company. Mineral exploration is essentially a research activity that does not produce a product. Successful exploration often results in increased project value that can be realized through the optioning or selling of the claimed site to larger companies. We acquire properties which we believe have potential to host economic concentrations of minerals, particularly gold and silver. These acquisitions have and may take the form of unpatented mining claims on federal land, or leasing claims on private property owned by others. An unpatented mining claim is an interest that can be acquired in the mineral rights on open lands of the federally owned public domain. Claims are staked in accordance with the Mining Law of 1872, recorded with the federal government pursuant to laws and regulations established by the Bureau of Land Management (the Federal agency that administers America’s public lands), that grant the holder of the claim a possessory interest in the mineral rights, subject to the paramount title of the United States.

| 6 |

| Table of Contents |

We perform geological work to identify specific drill targets on the properties, and then collect subsurface samples by drilling to confirm the presence of mineralization (the presence of economic minerals in a specific area or geological formation). We may enter into option and joint venture agreements with other companies to fund further exploration and/or development work. It is our plan to focus on assembling a high-quality group of gold and silver exploration prospects using the experience and contacts of the management group. By such prospects, we mean properties that may have been previously identified by third parties, including prior owners such as exploration companies, as mineral prospects with potential for economic mineralization. Often these properties have been sampled, mapped and sometimes drilled, usually with indefinite results. Accordingly, such acquired projects will either have some prior exploration history or will have strong similarity to a recognized geologic ore deposit model. We place geographic emphasis on the western United States, and Nevada in particular.

The focus of our activity has been to acquire properties that we believe to be undervalued, including those that we believe to hold previously unrecognized mineral potential. Properties have been acquired through the location of unpatented mining claims (which allow the claimholder the right to mine the minerals without holding title to the property), or by negotiating lease/option agreements. Our President and CEO, Patrick Highsmith, our Vice President Exploration, Dr. Steven Osterberg, and our CFO, Ted Sharp, as well as our Directors, have experience in evaluating, staking and filing unpatented mining claims, and in negotiating and preparing transactional agreements in connection with those mining claims, including option and JV or mineral lease agreements.

The geologic potential and ore deposit models have been defined and specific drill targets identified on the majority of our properties. Our property evaluation process involves using geologic fieldwork to perform an initial evaluation of a property. If the evaluation is positive, we seek to acquire it, either by staking unpatented mining claims on open public domain, or by leasing or optioning the property from the owner of private property or the owner of unpatented claims. Once acquired, we then typically make a more detailed evaluation of the property. This detailed evaluation involves expenditures for exploration work which may include rock and soil sampling, geologic mapping, geophysics, trenching, drilling, or other means to determine if economic mineralization is present on the property.

Portions of our mineral properties at September 30, 2023 are owned by third parties and leased to us, or carry a financial commitment from us, as outlined in the following table:

Property Name | Third Party | Number of Claims | Area | Agreements/ Royalties |

Lookout Mountain (Eureka) | Rocky Canyon Mining Company | 373 | 6,368 acres | 3.5% NSR + 1.5% NSR capped at $1.5 million (excludes Trevor and Dave claims); 20-year lease term commencing June 1, 2008; annual advanced royalty payment of $72,000.

|

Silverado | Silver International | 10 | 100 acres | 1% NSR + $10,000 Annual lease payment

|

Seven Troughs | Slash, Inc. | 302 | 4,030 acres | 2% NSR; 50-year lease term commencing December 31, 1975; no annual lease payments;

|

Paiute | Nevada Gold Mines by assignment from LAC Minerals (USA) LLC

| 65 | 1,343 acres | ICBM Joint Venture Earn-in Agreement expired. Timberline vested property interest at 74.1%. |

In the case of properties deemed to be of higher risk due to higher cost exploration or those that host commodities of lesser interest to Timberline (such as base metals), we may choose to present them to larger companies for strategic partnerships. Our strategy is intended to maximize the abilities and skills of the management group, conserve capital, and provide superior leverage for investors.

| 7 |

| Table of Contents |

For our gold and silver prospects where drilling costs are reasonable and the likelihood of success seems favorable, we will undertake our own drilling. The target depths, the tenor of mineralization on the surface, and the general geology of the area are all factors that determine the risk as calculated by us in conducting a drilling operation. Mineral exploration is a research and development activity and is, by definition, a high-risk business that relies on numerous untested assumptions and variables. Accordingly, we make our decisions on a project-by-project basis. We do not have any steadfast formula that we apply in determining the reasonableness of drilling costs in comparison to the likelihood of success, i.e., in determining whether the probability of success seems “favorable.”

Our Competition

The mineral exploration industry is intensely competitive in all phases. In our mineral exploration activities, we compete with many companies possessing greater financial resources and technical facilities than we do for the acquisition of mineral concessions, claims, leases, and other mineral interests as well as for the recruitment and retention of qualified employees, including mining engineers, geologists, and other skilled mining professionals. We use consultants and compete with other mining companies for the man hours of consulting time required to complete our studies. We also compete with other mining companies for exploration and development equipment and services. We must overcome significant barriers to enter into the business of mineral exploration as a result of our limited operating history.

We cannot assure the reader that we will be able to compete in any of our business areas effectively with current or future competitors or that the competitive pressures faced by us will not have a material adverse effect on our business, financial condition, and operating results.

Our Offices and Other Facilities

We currently maintain our administrative office at 9030 North Hess St., Suite 161, Hayden, ID 83835. The telephone number is (866) 513-4859 (toll free) or (208) 664-4859. We also maintain warehouse space in Eureka, NV 89316.

Our Employees

We are an exploration company and currently have three employees. Management engages independent consultants under contract arrangements as necessary to execute on company strategies at the current early exploration stage of our work and expects to hire staff and additional management as necessary for implementation of our business plan.

Regulation

The exploration and mining industries operate in a legal environment that requires permits to conduct virtually all operations. These permits are required by local, state, and federal government agencies. Federal agencies that may be involved include: the U.S. Forest Service (USFS), Bureau of Land Management (BLM), Environmental Protection Agency (EPA), National Institute for Occupational Safety and Health (NIOSH), the Mine Safety and Health Administration (MSHA), and the Fish and Wildlife Service (FWS). Individual states also have various environmental regulatory bodies, such as Departments of Ecology. Local authorities, usually counties, also have control over mining activity. The various permits address such issues as prospecting, development, production, labor standards, taxes, occupational health and safety, toxic substances, air quality, water use, water discharge, water quality, noise, dust, wildlife impacts, as well as other environmental and socioeconomic issues.

Prior to receiving the necessary permits to explore or mine, a mine operator must comply with all regulatory requirements imposed by all governmental authorities having jurisdiction over the project area. Very often, in order to obtain the requisite permits, the operator must have its land reclamation, restoration, or replacement plans pre-approved. Specifically, the operator must present its plan as to how it intends to restore or replace the affected area. Often all or any of these requirements can cause delays or involve costly studies or alterations of the proposed activity or time frame of operations, in order to mitigate impacts. All of these factors make it more difficult and costlier to operate and have a negative and sometimes fatal impact on the viability of the exploration or mining operation. Finally, it is possible that future changes in these laws or regulations could have a significant impact on our business, causing those activities to be economically re-evaluated at that time. For a more detailed discussion of governmental and environmental regulatory requirements applicable to our mineral exploration business see the section titled “Description of Properties - Overview of Regulatory, Economic and Environmental Issues” below.

Reclamation

We generally are required to mitigate long-term environmental impacts of prospecting and drilling activities, which are normally minor but may require contouring, re-sloping and re-vegetating roads and drill sites. Similarly, the greater impacts of mining and mineral processing operations must also be mitigated by stabilizing, contouring, re-sloping and re-vegetating various portions of a site after operations are completed. These reclamation efforts are conducted in accordance with detailed plans, which must be reviewed and approved by the appropriate regulatory agencies and may require us to remit cash to pay for reclamation bonds. Should we cease operations without performing the required reclamation, these bonds would cover the cost of reclamation activities to be performed by the regulatory agency.

| 8 |

| Table of Contents |

The Commodities Market

The prices of gold and silver have fluctuated during the last several years, with the prices of gold and silver falling to their lowest levels in the past several years in 2015 and early 2016, before rebounding. In 2017, gold traded between approximately $1,151 and $1,346 per ounce. In 2018, gold traded between approximately $1,175 and $1,355 per ounce. In 2019, gold traded between approximately $1,270 and $1,547 per ounce. In 2020, gold traded between approximately $1,474 and $2,067 per ounce. In 2021, gold traded between $1,683 and $1,943 per ounce. In 2022, gold traded between approximately $1,634 and $2,039 per ounce. The price of gold was $2,048 per ounce in April 2023, but traded considerably lower during the year, reaching as low as $1,628 per ounce in November 2022, before rising back up to approximately $2,032 at the time of this writing. All of these gold prices are based on the London PM Fix Price per troy ounce of gold in U.S. dollars.

In 2017, silver traded between approximately $15.22 and $18.56 per ounce. In 2018, silver traded between approximately $13.97 and $17.52 per ounce. In 2019, silver traded between approximately $14.38 and $19.42 per ounce. In 2020, silver traded between approximately $12.01 and $28.89 per ounce. In 2021, silver traded between $21.52 and $29.58. In 2022, silver traded between $17.77 and $26.17 per ounce. The price of silver was $18.39 per ounce in October 2022, and continued to rise to a high of $26.02 in April 2023 before settling at approximately $24.19 at the time of this writing. All of these silver prices are based on the London Fix Price per troy ounce of silver in U.S. dollars.

Seasonality

Seasonality in Nevada is not a material factor to our operations. Certain surface exploration work may need to be conducted when there is no snow on the ground, but it is not a material issue.

ITEM 1A. RISK FACTORS

An investment in an exploration stage mining company such as ours involves an unusually high degree of risk, known and unknown, present and potential, including, but not limited to the risks enumerated below.

Failure to successfully address the risks and uncertainties described below could have a material adverse effect on our business, financial condition and/or results of operations, and the trading price of our common stock may decline and investors may lose all or part of their investment. We cannot assure you that we will successfully address these risks or other unknown risks that may affect our business.

Estimates of mineralized material are forward-looking statements inherently subject to error. Although mineralization and reserve estimates require a high degree of assurance in the underlying data when the estimates are made, unforeseen events and uncontrollable factors can have significant adverse or positive impacts on the estimates. Actual results will inherently differ from estimates. The unforeseen events and uncontrollable factors include: geologic uncertainties including inherent sample variability, metal price fluctuations, variations in mining and processing parameters, and adverse changes in environmental or mining laws and regulations. We cannot accurately predict the timing and effects of variances from estimated values.

Risks Related to Our Company

Our ability to operate as a going concern is in doubt.

The audit opinion and notes that accompany our consolidated financial statements for the year ended September 30, 2023, disclose a ‘going concern’ qualification to our ability to continue in business. The accompanying consolidated financial statements have been prepared under the assumption that we will continue as a going concern. We have incurred losses since our inception. We do not have sufficient cash to fund normal operations and meet all of our obligations for the next 12 months. As of September 30, 2023, we have negative working capital of approximately $108,000. We will need to raise funds in the form of equity or debt financings to fund normal operations for the next 12 months.

Full disclosure of the going concern qualification appears in Part II, Item 7 - Financial Condition and Liquidity, and also in the notes to the financial statements (See Note 2 – Summary of Significant Accounting Policies.)

| 9 |

| Table of Contents |

We have a limited operating history on which to base an evaluation of our business and prospects.

Although we have been in the business of exploring mineral properties since our incorporation in 1968, we were inactive for many years prior to our new management in 2004. Since 2004, we have not yet established any mineral reserves. As a result, we have not had any revenues from our exploration activities. While we have had a wholly owned drilling services subsidiary which has generated revenues in past fiscal years, we no longer own that business.In addition, our operating history has been restricted to the acquisition and exploration of our mineral properties, and this does not provide a meaningful basis for an evaluation of our prospects if we ever determine that we have a mineral reserve and commence the construction and operation of a mine.Other than through conventional and typical exploration methods and procedures, we have no additional way to evaluate the likelihood of whether our mineral properties contain any mineral reserves or, if they do that they will be operated successfully.As a result, we are subject to all of the risks associated with developing and establishing new mining operations and business enterprises including:

| · | completion of feasibility studies to verify reserves and commercial viability, including the ability to find sufficient gold reserves to support a commercial mining operation; |

| · | the timing and cost, which can be considerable, of further exploration, preparing feasibility studies, permitting and construction of infrastructure, mining, and processing facilities; |

| · | the availability and costs of drill equipment, exploration personnel, skilled labor, and mining and processing equipment, if required; |

| · | compliance with environmental and other governmental approval and permit requirements; |

| · | the availability of funds to finance exploration, development, and construction activities, as warranted; |

| · | potential opposition from non-governmental organizations, environmental groups, local groups, or local inhabitants which may delay or prevent development activities; |

| · | potential increases in exploration, construction, and operating costs due to changes in the cost of fuel, labor, power, materials, and supplies; and |

| · | potential shortages of mineral processing, construction, and other facilities-related supplies. |

The costs, timing, and complexities of exploration, development, and construction activities may be increased by the location of our properties and demand by other mineral exploration and mining companies. It is common in exploration programs to experience unexpected problems and delays during drill programs and, if warranted, development, construction, and mine start-up. Accordingly, our activities may not result in profitable mining operations and we may not succeed in establishing mining operations or profitably producing metals at any of our properties. There is no history upon which to base any assumption as to the likelihood that we will prove successful, and we can provide investors with no assurance that we will generate any operating revenues or ever achieve profitable operations.

We have a history of losses and expect to continue to incur losses in the future.

We have incurred losses since inception and expect to continue to incur losses in the future. We incurred the following net losses during each of the following periods:

| · | $2,180,344 for the year ended September 30, 2023 |

| · | $5,961,907 for the year ended September 30, 2022; and |

| · | $4,707,815 for the year ended September 30, 2021 |

We had an accumulated deficit of approximately $76.5 million as of September 30, 2023. We expect to continue to incur losses unless and until such time as one of our properties enters into commercial production and generates sufficient revenues to fund continuing operations. We recognize that if we are unable to generate significant revenues from mining operations and dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses, and difficulties frequently encountered by companies at the start-up stage of their business development. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition.

Risks Associated with Mining and Exploration

All of our properties are in the exploration stage. There is no assurance that we can establish the existence of any mineral reserve on any of our properties in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from these properties, and if we do not do so, and are unable to joint venture or sell the properties, we will lose all of the funds that we expend on exploration. If we do not discover any mineral reserve in a commercially exploitable quantity, our business could fail.

We have not established that any of our mineral properties contain any mineral reserves according to recognized reserve guidelines, nor can there be any assurance that we will be able to do so. A mineral reserve is defined by the SEC in its Regulation S-K subpart 1300 as that part of a mineral deposit, which could be economically and legally extracted or produced at the time of the reserve determination. The probability of an individual prospect ever having a "reserve" that meets the requirements of the SEC's Regulation S-K subpart 1300 is remote. Even if we do eventually discover a mineral reserve on one or more of our properties, there can be no assurance that they can be developed into producing mines to extract those minerals. Both mineral exploration and development involve a high degree of risk, and few properties that are explored are ultimately developed into producing mines.

| 10 |

| Table of Contents |

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade, and other attributes of the mineral deposit, the proximity of the mineral deposit to infrastructure such as a smelter, roads, a point for shipping, government regulation, and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral deposit unprofitable.

Mineral operations are subject to applicable law and government regulation. Even if we discover a mineral reserve in a commercially exploitable quantity, these laws and regulations could restrict or prohibit the exploitation of that mineral reserve. If we cannot exploit any mineral reserve that we might discover on our properties, our business may fail.

Both mineral exploration and extraction require permits from various foreign, federal, state, provincial, and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety, and other matters. Regarding our future ground disturbing activity on federal land, we will be required to obtain a permit from the US Forest Service or the Bureau of Land Management prior to commencing exploration. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration of our mineral properties or for the construction and operation of a mine on our properties at economically viable costs. If we cannot accomplish these objectives, our business could face difficulty and/or fail.

We believe that we are in compliance with all material laws and regulations that currently apply to our activities, but there can be no assurance that we can continue to do so. Current laws and regulations could be amended, and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

Environmental hazards unknown to us, which have been caused by previous or existing owners or operators of the properties, may exist on the properties in which we hold an interest. In past years, we have been engaged in exploration in northern Idaho, which is currently the site of a Federal Superfund cleanup project. Although we are no longer involved in this or other areas at present, it is possible that environmental cleanup or other environmental restoration procedures could remain to be completed or mandated by law, causing unpredictable and unexpected liabilities to arise. At the date of this Annual Report, we are not aware of any environmental issues or litigation relating to any of our current or former properties.

Future legislation and administrative changes to the mining laws could prevent us from exploring our properties.

New state and U.S. federal laws and regulations, amendments to existing laws and regulations, administrative interpretation of existing laws and regulations, or more stringent enforcement of existing laws and regulations, could have a material adverse impact on our ability to conduct exploration and mining activities. Any change in the regulatory structure making it more expensive to engage in mining activities could cause us to cease operations.

Regulations and pending legislation governing issues involving climate change could result in increased operating costs, which could have a material adverse effect on our business.

A number of governments or governmental bodies have introduced or are contemplating regulatory changes in response to various climate change interest groups and the potential impact of climate change. Legislation and increased regulation regarding climate change could impose significant costs on us, our venture partners, and our suppliers, including costs related to increased energy requirements, capital equipment, environmental monitoring and reporting, and other costs to comply with such regulations. Any adopted future climate change regulations could also negatively impact our ability to compete with companies situated in areas not subject to such limitations. Given the political significance and uncertainty around the impact of climate change and how it should be dealt with, we cannot predict how legislation and regulation will affect our financial condition, operating performance and ability to compete. Furthermore, even without such regulation, increased awareness and any adverse publicity in the global marketplace about potential impacts on climate change by us or other companies in our industry could harm our reputation. The potential physical impacts of climate change on our operations are highly uncertain and would be particular to the geographic circumstances in areas in which we operate. These may include changes in rainfall and storm patterns and intensities, water shortages, changing sea levels, and changing temperatures. These impacts may adversely impact the cost, production, and financial performance of our operations.

| 11 |

| Table of Contents |

If we establish the existence of a mineral reserve on any of our properties in a commercially exploitable quantity, we will require additional capital in order to develop the property into a producing mine. If we cannot raise this additional capital, we will not be able to exploit the reserve, and our business could fail.

If we do discover mineral reserves in commercially exploitable quantities on any of our properties, we will be required to expend substantial sums of money to establish the extent of the reserve, develop processes to extract it, and develop extraction and processing facilities and infrastructure. There can be no assurance that a mineral reserve will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis. If we cannot raise the necessary capital or complete the necessary facilities and infrastructure, our business may fail.

Land reclamation requirements for our properties may be burdensome and expensive.

Although variable depending on location and the governing authority, land reclamation requirements are generally imposed on mineral exploration companies (as well as companies with mining operations) in order to minimize long-term effects of land disturbance. Reclamation may include requirements to control dispersion of potentially deleterious effluents and re-establish pre-disturbance landforms and vegetation.

In order to carry out reclamation obligations imposed on us in connection with our potential development activities, we must allocate financial resources that might otherwise be spent on further exploration and development programs. We plan to set up a provision for our reclamation obligations on our properties, as appropriate, but this provision may not be adequate. If we are required to carry out unanticipated reclamation work, our financial position could be adversely affected.

Mining exploration and development are inherently hazardous and subject to conditions or events beyond our control, which could have a material adverse effect on our business and plans.

Mining and mineral exploration involves various types of risks and hazards, including:

| · | environmental hazards; |

| · | power outages; |

| · | metallurgical and other processing problems; |

| · | unusual or unexpected geological formations; |

| · | personal injury, flooding, fire, explosions, cave-ins, landslides, and rock-bursts; |

| · | inability to obtain suitable or adequate machinery, equipment, or labor; |

| · | metals losses; |

| · | fluctuations in exploration, development, and production costs; |

| · | labor disputes; |

| · | unanticipated variations in grade; |

| · | mechanical equipment failure; and |

| · | periodic interruptions due to inclement or hazardous weather conditions. |

These risks could result in damage to, or destruction of, mineral properties, production facilities, or other properties, personal injury, environmental damage, delays in mining, increased production costs, monetary losses, and possible legal liability.

Mineral exploration and development is subject to extraordinary operating risks. We do not currently insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which would have an adverse impact on our Company.

Mineral exploration, development, and production involve many risks, which even a combination of experience, knowledge, and careful evaluation may not be able to overcome. Our operations will be subject to all the hazards and risks inherent in the exploration, development and production of minerals, including liability for pollution, cave-ins or similar hazards against which we cannot insure or against which we may elect not to insure. Any such event could result in work stoppages and damage to property, including damage to the environment. We do not currently maintain any insurance coverage against these operating hazards. The payment of any liabilities that arise from any such occurrence could have a material adverse impact on our Company.

| 12 |

| Table of Contents |

Increased costs could affect our financial condition.

We anticipate that costs at our projects that we may explore or develop will frequently be subject to variation from one year to the next due to a number of factors, such as changing ore grade, metallurgy, and revisions to mine plans, if any, in response to the physical shape and location of the ore body. In addition, costs are affected by the price of commodities such as fuel, rubber, and electricity. Such commodities are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in costs at any significant location could have a significant effect on our profitability.

A shortage of equipment and supplies could adversely affect our ability to operate our business.

We are dependent on various supplies and equipment to carry out our mining exploration and, if warranted, development operations. Any shortage of such supplies, equipment, and parts could have a material adverse effect on our ability to carry out our operations and, therefore, limit or increase the cost of production.

Estimates of mineralized material are subject to evaluation uncertainties that could result in project failure.

Our exploration and future mining operations, if any, are and would be faced with risks associated with being able to accurately predict the quantity and quality of mineralized material within the earth using statistical sampling techniques. Estimates of any mineralized material on any of our properties would be made using samples obtained from appropriately placed trenches, test pits, and underground workings and intelligently designed drilling. There is an inherent variability of assays between check and duplicate samples taken adjacent to each other and between sampling points that cannot be reasonably eliminated. Additionally, there also may be unknown geologic details that have not been identified or correctly appreciated at the current level of accumulated knowledge about our properties. This could result in uncertainties that cannot be reasonably eliminated from the process of estimating mineralized material. If these estimates were to prove to be unreliable, we could implement an exploitation plan that may not lead to commercially viable operations in the future.

Mineral prices are subject to dramatic and unpredictable fluctuations.

We expect to derive revenues, if any, from the eventual extraction and sale of precious metals such as gold and silver. The price of those commodities has fluctuated widely in recent years, and is affected by numerous factors beyond our control, including international, economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities and increased production due to new extraction developments, and improved extraction and production methods. The effect of these factors on the price of precious metals, and, therefore, the economic viability of any of our exploration projects, cannot accurately be predicted.

The mining industry is highly competitive and there is no assurance that we will continue to be successful in acquiring mineral claims. If we cannot continue to acquire properties to explore for mineralized material, we may be required to reduce or cease exploration activity and/or operations.

The mineral exploration, development, and production industry is largely fragmented. We compete with other exploration companies looking for mineral properties and the minerals that can be produced from them. While we compete with other exploration companies in the effort to locate and license mineral properties, we do not compete with them for the removal or sales of mineral products from our properties if we should eventually discover the presence of them in quantities sufficient to make production economically feasible. Readily available markets exist worldwide for the sale of gold and other mineral products. Therefore, we will likely be able to sell any gold or mineral products that we identify and produce.

There are hundreds of public and private companies that are actively engaged in mineral exploration. A representative sample of exploration companies that are similar to us in size, financial resources, and primary objective include such publicly traded mineral exploration companies as Allegiant Gold Ltd. (AUAU.V), NuLegacy Gold Corp (NUG.V), Comstock Mining Inc. (LODE), Viva Gold Corp (VAUCF), Nevgold Corp (NAUFF), Ridgeline Minerals Corp (RDGMF) and Summa Silver Corp (SSVR).

Many of our competitors have greater financial resources and technical facilities. Accordingly, we will attempt to compete primarily through the knowledge and experience of our management. This competition could adversely affect our ability to acquire suitable prospects for exploration in the future. Accordingly, there can be no assurance that we will acquire any interest in additional mineral properties that might yield reserves or result in commercial mining operations.

| 13 |

| Table of Contents |

Third parties may challenge our rights to our mineral properties, or the agreements that permit us to explore our properties may expire, if we fail to timely renew them and pay the required fees.

In connection with the acquisition of our mineral properties, we sometimes conduct only limited reviews of title and related matters and obtain certain representations regarding ownership. These limited reviews do not necessarily preclude third parties from challenging our title and, furthermore, our title may be challenged as defective. Consequently, there can be no assurance that we hold good and marketable title to all of our mining concessions and mining claims. If any of our concessions or claims were challenged, we could incur significant costs and lose valuable time in defending such a challenge. These costs or an adverse ruling with regards to any challenge of our titles could have a material adverse effect on our financial position or results of operations. There can be no assurance that any such disputes or challenges will be resolved in our favor.

We are not aware of challenges to the location or area of any of our mining claims. There is, however, no guarantee that title to the claims will not be challenged or impugned in the future.

Acquisitions and integration issues may expose us to risks.

Our business strategy includes making targeted acquisitions. Any acquisition that we make may be of a significant size, may change the scale of our business and operations, and may expose us to new geographic, political, operating, financial, and geological risks. Our success in our acquisition activities depends on our ability to identify suitable acquisition candidates, negotiate acceptable terms for any such acquisition and integrate the acquired operations successfully with our own. Any acquisitions would be accompanied by risks. For example, there may be significant decreases in commodity prices after we have committed to complete the transaction and have established the purchase price or exchange ratio; a potential mineralized property may prove to be below expectations; we may have difficulty integrating and assimilating the operations and personnel of any acquired companies, realizing anticipated synergies and maximizing the financial and strategic position of the combined enterprise and maintaining uniform standards, policies and controls across the organization; the integration of the acquired business or assets may disrupt our ongoing business and our relationships with employees, customers, suppliers, and contractors; and the acquired business or assets may have unknown liabilities which may be significant. If we choose to use equity securities as consideration for such an acquisition, existing shareholders may suffer dilution. Alternatively, we may choose to finance any such acquisition with our existing resources. There can be no assurance that we would be successful in overcoming these risks or any other problems encountered in connection with such acquisitions.

Joint ventures and other partnerships in relation to our properties may expose us to risks.

We have in the past, and may in the future, entered into joint ventures or other partnership arrangements with other parties in relation to the exploration, development, and production of certain of the properties in which we have an interest. Joint ventures can often require unanimous approval of the parties to the joint venture or their representatives for certain fundamental decisions such as an increase or reduction of registered capital, merger, division, dissolution, amendments of constating documents, and the pledge of joint venture assets, which means that each joint venture party may have a veto right with respect to such decisions which could lead to a deadlock in the operations of the joint venture or partnership. Further, we may be unable to exert control over strategic decisions made in respect of such properties. Any failure of such other companies to meet their obligations to us or to third parties, or any disputes with respect to the parties' respective rights and obligations, could have a material adverse effect on the joint ventures or their properties and, therefore, could have a material adverse effect on our results of operations, financial performance, cash flows, and the price of our common stock.

Risks Related to Our Company

Minimal staffing may be reasonably likely to materially affect the Company’s internal control over financial reporting

With a very limited staff, it is difficult to maintain appropriate segregation of duties in the initiating and recording of transactions, thereby creating a segregation of duties weakness. Due to the significance of segregation of duties to the preparation of reliable financial statements, this weakness may result in more than a remote likelihood that a material misstatement or lack of disclosure within the annual or interim financial statements not be prevented or detected.

Conflicts of Interest

Certain of our officers and directors may be or become associated with other businesses, including natural resource companies that acquire interests in mineral properties. Such associations may give rise to conflicts of interest from time to time. Our directors are required by Delaware’s General Corporation Law to act honestly and in good faith with a view to our best interests and to disclose any interest which they may have in any of our projects or opportunities. In general, if a conflict of interest arises at a meeting of the board of directors, any director in a conflict will disclose his interest and abstain from voting on such matter or, if he does vote, his vote will not be counted.

| 14 |

| Table of Contents |

We have not adopted any separate formal corporate policy regarding conflicts of interest; however, other corporate governance measures have been adopted, such as creating a directors’ audit committee requiring independent directors. Additionally, our Code of Ethics does address areas of possible conflicts of interest. As of the date of filing of this report, we had two independent directors on our board of directors (Leigh Freeman and Pamela Saxton). We have formed three committees to ensure our legal compliance. We established an independent audit committee consisting of two independent directors, both of whom were determined to be “financially literate” and one of whom was designated as the “financial expert.” We also formed a compensation committee comprised entirely of independent directors and a corporate governance and nominating committee, the majority of which is comprised of independent directors. At this time, we feel that these committees and our Code of Ethics provide sufficient corporate governance for our purposes.

Dependence on Key Management Employees and Contractors

Our ability to continue our exploration and development activities and to develop a competitive edge in the marketplace depends, in large part, on our ability to attract and maintain qualified key management personnel. Competition for such personnel is intense, and there can be no assurance that we will be able to attract and retain such personnel. Our development now and in the future will depend on the efforts of key management figures such as Patrick Highsmith, Steven Osterberg, and Ted Sharp. The loss of any of these key people could have a material adverse effect on our business. In this regard, we have attempted to reduce the risk associated with the loss of key personnel and have obtained directors and officers insurance coverage. In addition, our shareholders have approved our 2015 Stock and Incentive Plan and 2018 Incentive Plan so that we can provide incentives for our key personnel.

We may not realize the benefits of Eureka, Paiute, Seven Troughs and other acquired growth projects.

As part of our strategy, we will continue existing efforts and initiate new efforts to develop gold and other mineral properties. We have three such project areas, including Eureka, Paiute and Seven Troughs. A number of risks and uncertainties are associated with the development of these types of projects, including political, regulatory, design, construction, labor, operating, technical and technological risks, and uncertainties relating to capital and other costs and financing risks. The failure to successfully develop any of these initiatives could have a material adverse effect on our financial position and results of operations.

As part of our business model, we pursue a strategy that may cause us to expend significant resources exploring properties that may not become revenue-producing sites.

Part of our business model is to pursue a strategy which includes significant exploration activities, such as proposed exploration and, if warranted, development at the Eureka, Paiute, and the Seven Troughs Projects. Because of the nature of exploration for precious metals, a property’s exploration potential is not known until a significant amount of geologic information has been generated. We may spend significant resources exploring and developing the projects and gathering certain geologic information only to determine that the project is not capable of being a revenue-producing property for us.

Our business is subject to evolving corporate governance and public disclosure regulations that have increased both our compliance costs and the risk of noncompliance, which could have an adverse effect on our stock price.

We are subject to changing rules and regulations promulgated by a number of governmental and self-regulated organizations, including the SEC, the Public Company Accounting Oversight Board (“PCAOB”) and the Financial Accounting Standards Board. These rules and regulations continue to evolve in scope and complexity, and many new requirements have been created in response to laws enacted by Congress, making compliance more difficult and uncertain. For example, on July 21, 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) with increased disclosure obligations for public companies and mining companies in the United States. Our efforts to comply with the Dodd-Frank Act and other new regulations have resulted in, and are likely to continue to result in, increased general and administrative expenses and a diversion of our management’s time and attention from operating activities to compliance activities.

We are required to comply with Canadian securities regulations and are subject to additional regulatory scrutiny in Canada.

We are a “reporting issuer” in the Canadian provinces of British Columbia and Alberta. As a result, our disclosure outside the United States differs from the disclosure contained in our SEC filings. Our reserve and resource estimates disseminated outside the United States are not directly comparable to those made in filings subject to SEC reporting and disclosure requirements, as we generally report reserves and resources in accordance with Canadian practices. These practices are different from the practices used to report reserve and resource estimates in reports and other materials filed with the SEC. It is Canadian practice to report measured, indicated, and inferred resources, which are generally not permitted in disclosures filed with the SEC. In the United States, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. United States investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves. Further, “inferred resources” have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. Disclosure of “contained ounces” is permitted disclosure under Canadian regulations; however, the SEC only permits issuers to report “resources” as in-place tonnage and grade without reference to unit measures. Accordingly, information concerning descriptions of mineralization, reserves, and resources contained in disclosures released outside the United States may not be comparable to information made public by other United States companies subject to the reporting and disclosure requirements of the SEC.

| 15 |

| Table of Contents |

We are also subject to increased regulatory scrutiny and costs associated with complying with securities legislation in Canada. For example, we are subject to civil liability for misrepresentations in written disclosure and oral statements. Legislation has been enacted in these provinces which creates a right of action for damages against a reporting issuer, its directors and certain of its officers in the event that the reporting issuer or a person with actual, implied, or apparent authority to act or speak on behalf of the reporting issuer releases a document or makes a public oral statement that contains a misrepresentation or the reporting issuer fails to make timely disclosure of a material change. We do not anticipate any particular regulation that would be difficult to comply with. However, failure to comply with regulations may result in civil awards, fines, penalties, and orders that could have an adverse effect on us.

Risks Associated with Our Common Stock

Our stock price has been volatile and your investment in our common stock could suffer a decline in value.

Our common stock is quoted on the OTCQB Market (“OTCQB”) and traded on the TSX Venture Exchange (“TSX-V”). The market price of our common stock may fluctuate significantly in response to a number of factors, some of which are beyond our control. These factors include price fluctuations of precious metals, government regulations, disputes regarding mining claims, broad stock market fluctuations, and general economic conditions in the United States and Canada.

We do not intend to pay any dividends on shares of our common stock in the near future.

We do not currently anticipate declaring and paying dividends to our shareholders in the near future, and any future decision as to the payment of dividends will be at the discretion of our board of directors and will depend upon our earnings, financial position, capital requirements, plans for expansion, and such other factors as our board of directors deems relevant. It is our current intention to apply net earnings, if any, in the foreseeable future to finance the growth and development of our business.

Investors’ interests in our Company will be diluted and investors may suffer dilution in their net book value per share, if we issue additional employee/director/consultant options or if we sell additional shares and/or warrants to finance our operations.

We have not generated material revenue from exploration since the commencement of our exploration stage in January 2004. In order to further expand our company and meet our objectives, any additional growth and/or expanded exploration activity may need to be financed through sale and issuance of additional shares, including, but not limited to, raising finances to explore our properties. Furthermore, to finance any acquisition activity, should that activity be properly approved, and depending on the outcome of our exploration programs, we may also need to issue additional shares to finance future acquisitions, growth and/or additional exploration programs at any or all of our projects or to acquire additional properties. We may also in the future grant to some or all of our directors, officers, insiders, and key employees options to purchase our common shares and stock unit awards as non-cash incentives. The issuance of any equity securities could, and the issuance of any additional shares will, cause our existing shareholders to experience dilution of their ownership interests.

If we issue additional shares or decide to enter into joint ventures with other parties in order to raise financing through the sale of equity securities, investors' interests in our Company will be diluted and investors may suffer dilution in their net book value per share depending on the price at which such securities are sold. As of September 30, 2023, there are also outstanding options and warrants granted that are exercisable into 17,898,522 common shares. If all of these options and warrants were exercised, the underlying shares would represent approximately 9.32% of our issued and outstanding shares. If all of these options and warrants are exercised and the underlying shares are issued, such issuance will cause a reduction in the proportionate ownership and voting power of all other shareholders. The dilution may result in a decline in the market price of our shares.

| 16 |

| Table of Contents |

We are subject to the continued listing criteria of the TSX-V and our failure to satisfy these criteria may result in delisting of our shares of common stock.

Our shares of common stock are currently listed on the TSX-V. In order to maintain the listing, we must maintain certain share prices, financial, and share distribution targets, including maintaining a minimum amount of shareholders’ equity and a minimum number of public shareholders. In addition to objective standards, the TSX-V may delist our securities if, in their discretionary opinion: (i) our financial condition and/or operating results appear unsatisfactory; (ii) it appears that the extent of public distribution or the aggregate market value of the security has become so reduced as to make continued listing on TSX-V inadvisable; (iii) we sell or dispose of principal operating assets or cease to be an operating company; (iv) we fail to comply with the listing requirements of the TSX-V; (v) our shares of common stock sell at what the TSX-V considers a “low selling price” and if we fail to correct this via a reverse split of shares after notification by the TSX-V; or (vi) any other event occurs or any condition exists which makes continued listing on the TSX-V, in their opinion, inadvisable.

If the TSX-V delists our shares of common stock, investors may face material adverse consequences, including, but not limited to, a lack of trading market for our securities, reduced liquidity, decreased analyst coverage of our securities, and an inability for us to obtain additional financing to fund our operations.

ITEM 1B. UNRESOLVED STAFF COMMENTS

All staff comments have been addressed as of the date of filing of this report.

ITEM 2. DESCRIPTION OF PROPERTIES

We have acquired mineral prospects for exploration in Nevada mainly for target commodities of gold and silver, and formerly copper. The prospects are held by both patented and unpatented mining claims owned directly by us or through legal agreements conveying exploration and development rights to us. Most of our prospects have had a prior exploration history, which is typical in the mineral exploration industry. Most mineral prospects go through several rounds of exploration before an economic ore body is discovered, and prior work often eliminates targets or points to new ones. Also, prior operators may have explored under a completely different commodity price structure or technological regime. Mineralization which was uneconomic in the past may be ore grade at current market prices when extracted and processed with modern technology.

Nevada Gold Properties

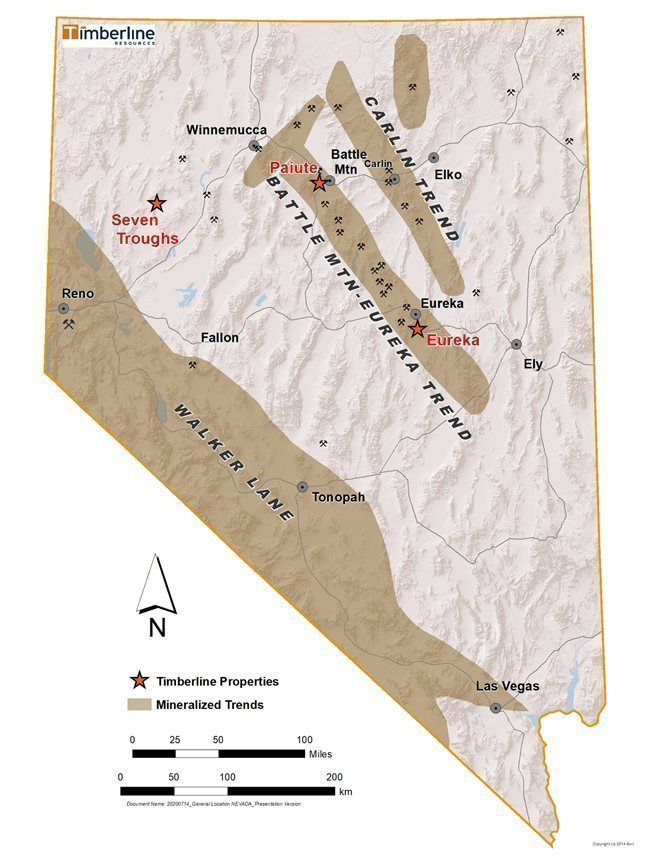

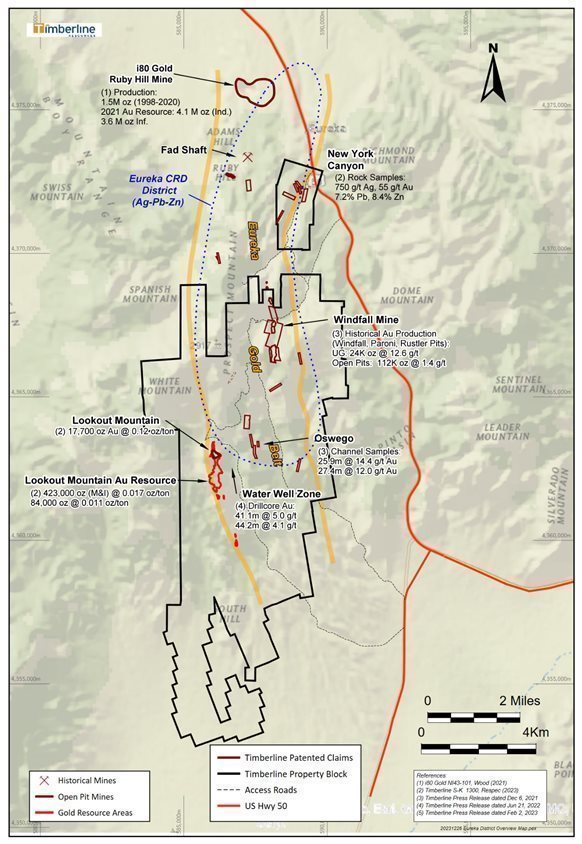

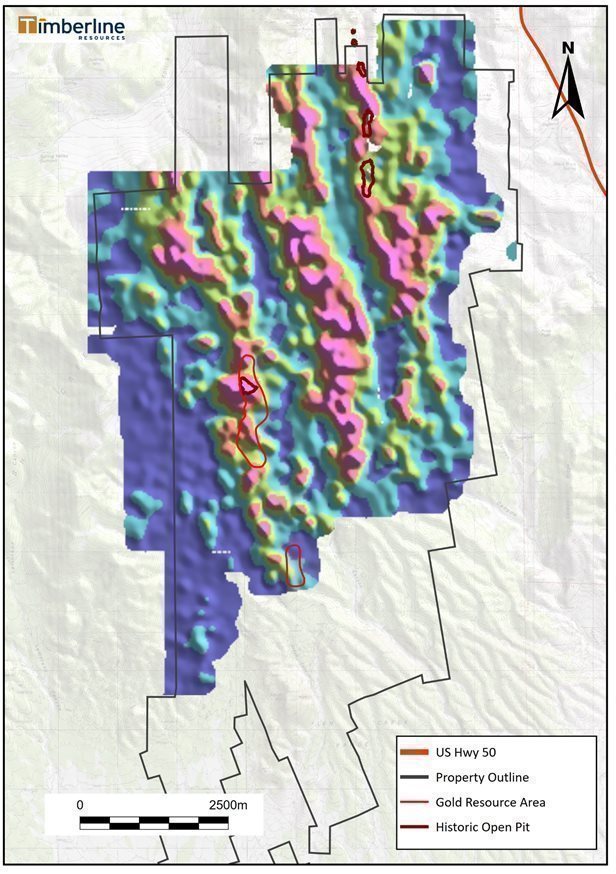

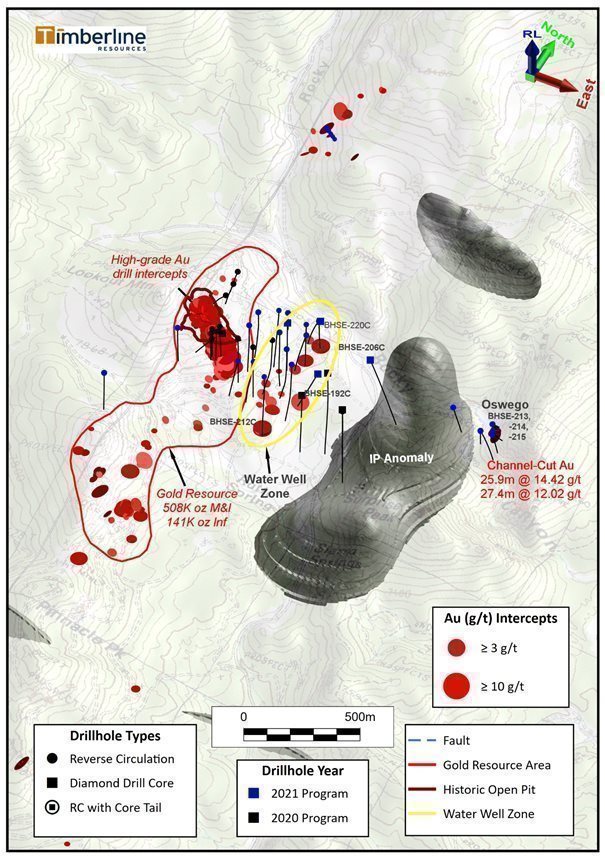

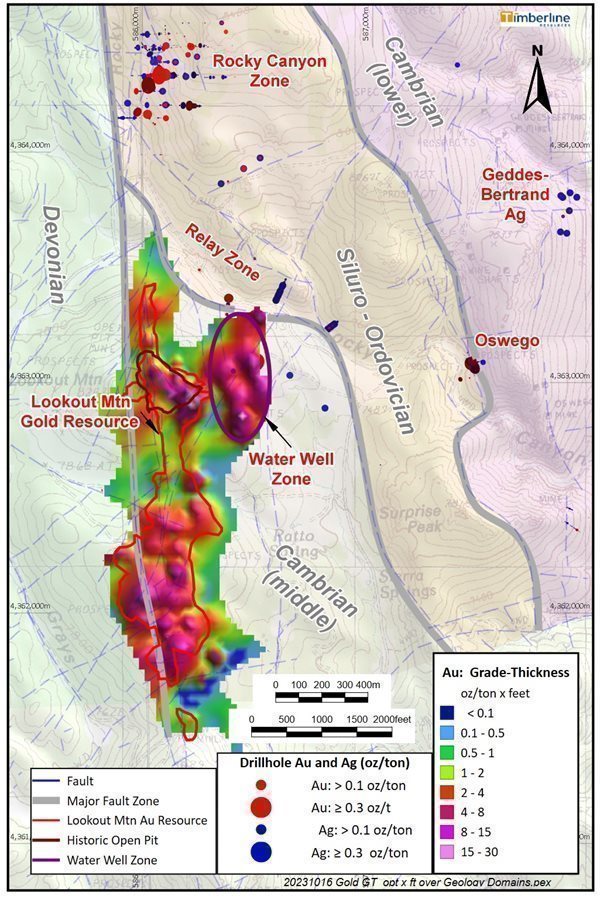

The Company currently controls three mineral properties in Nevada including Eureka, Paiute, and Seven Troughs (Figure 1).

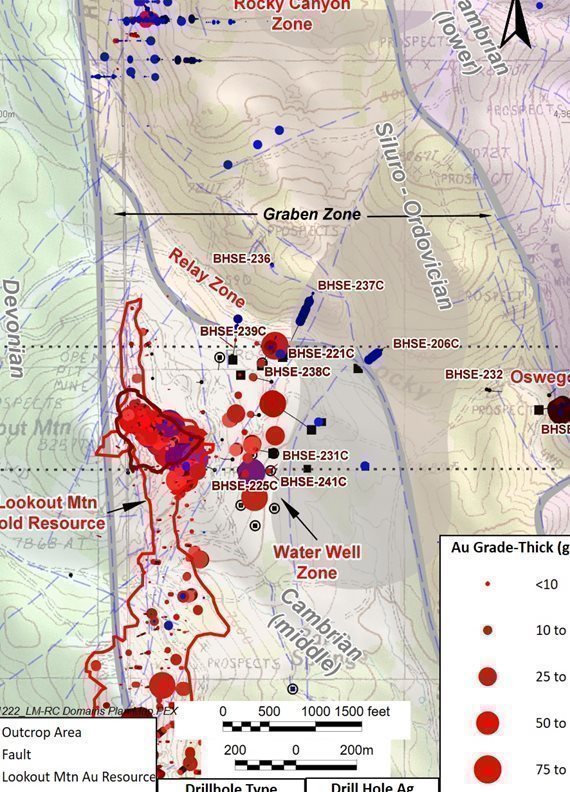

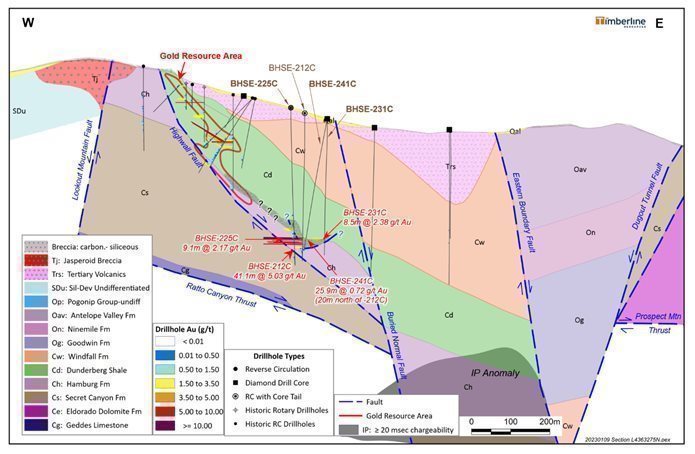

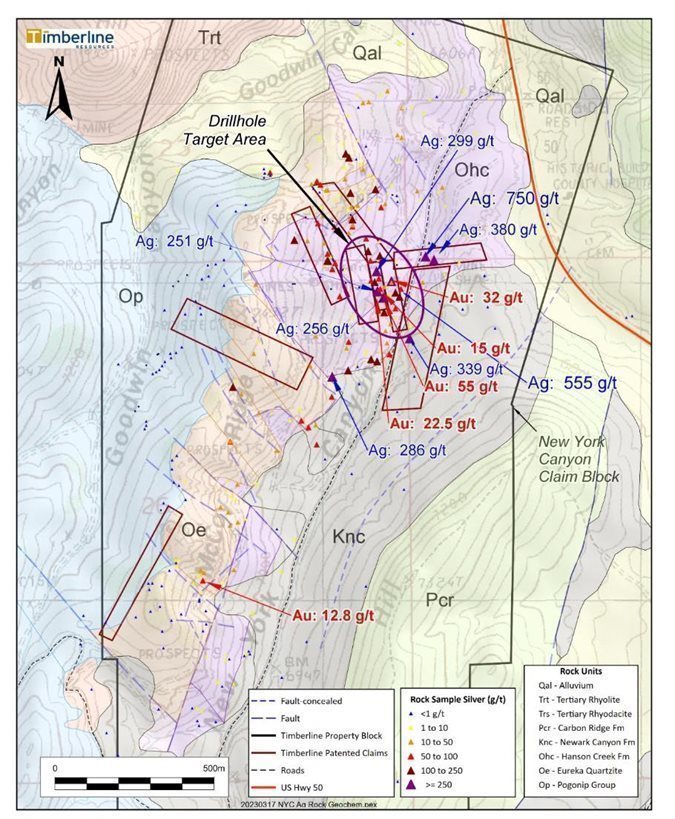

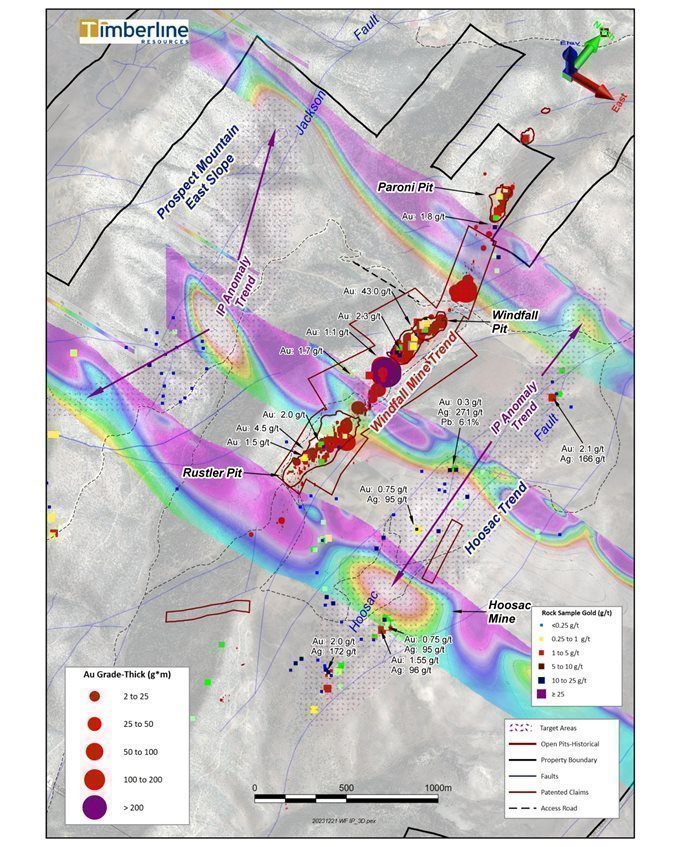

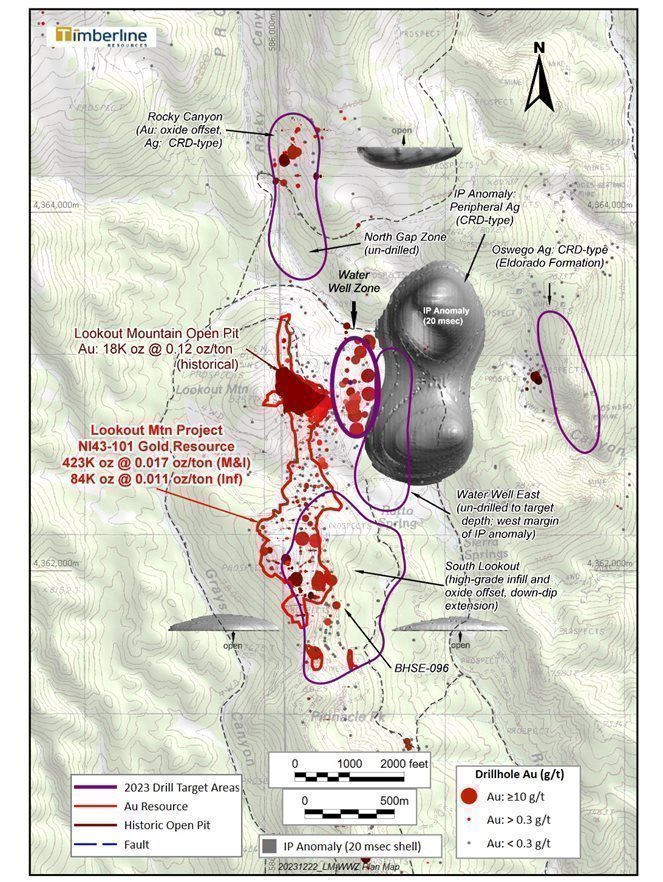

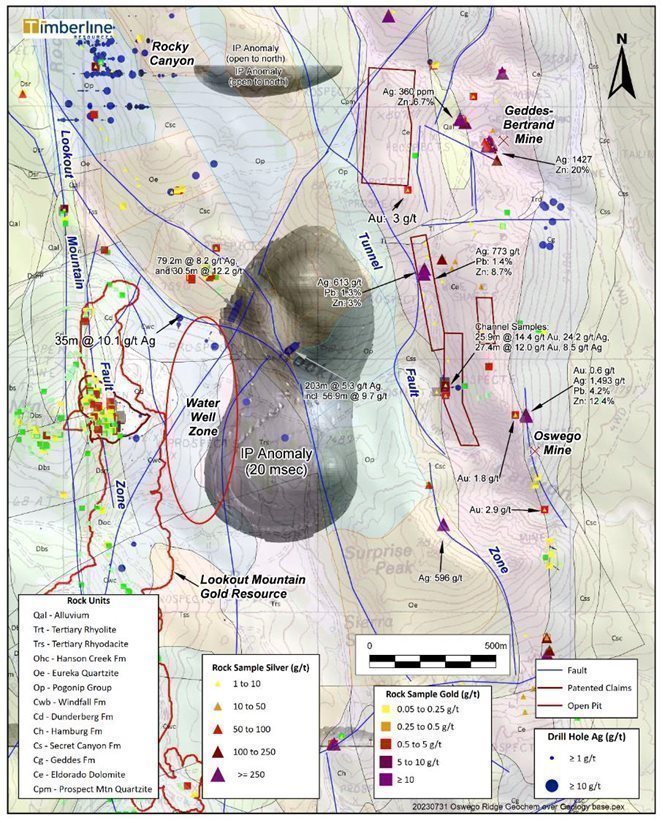

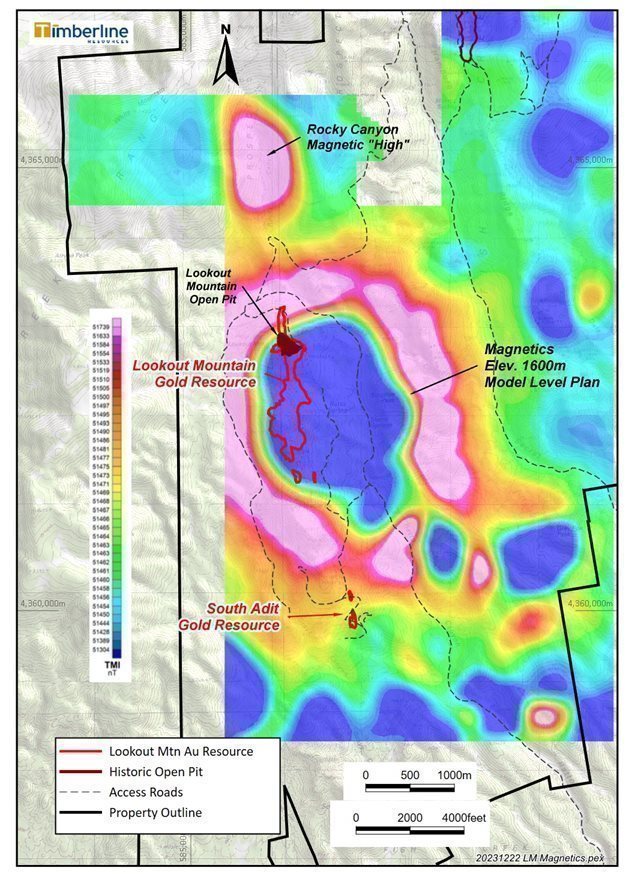

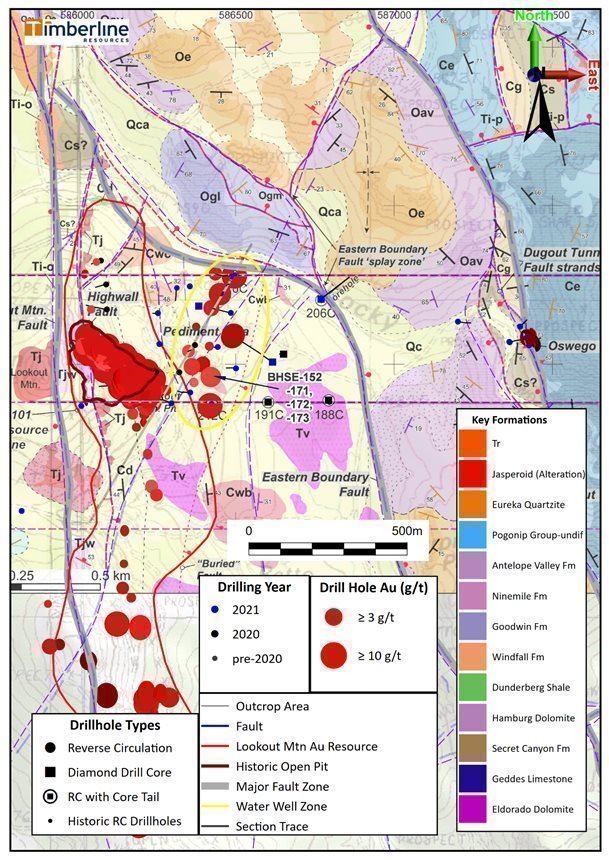

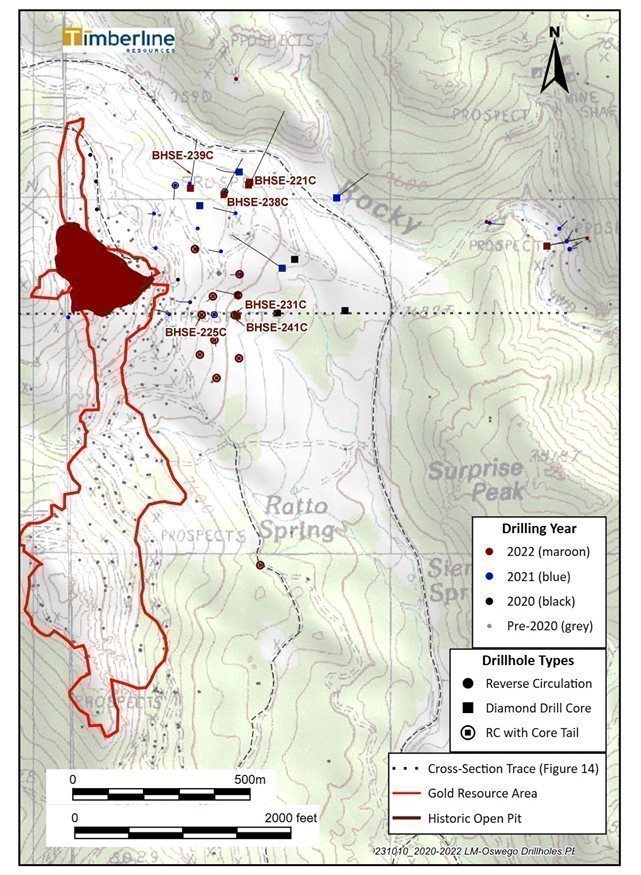

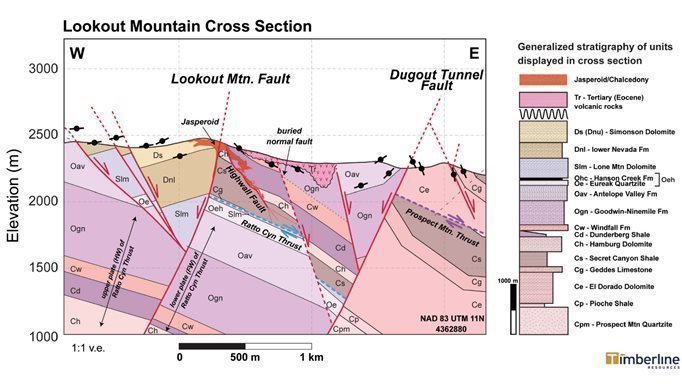

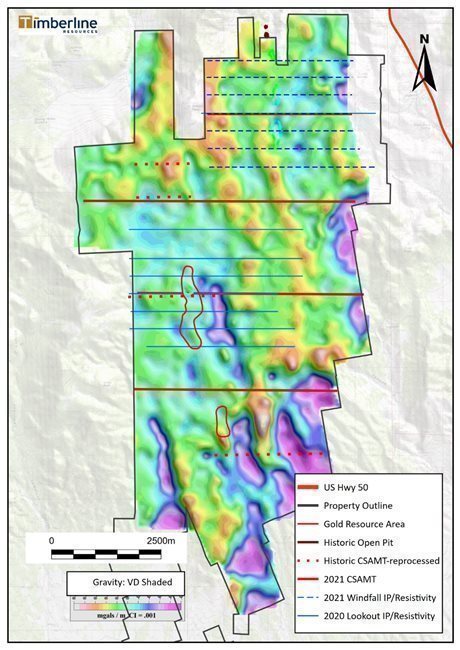

Eureka Project (Battle Mountain/Eureka Trend)

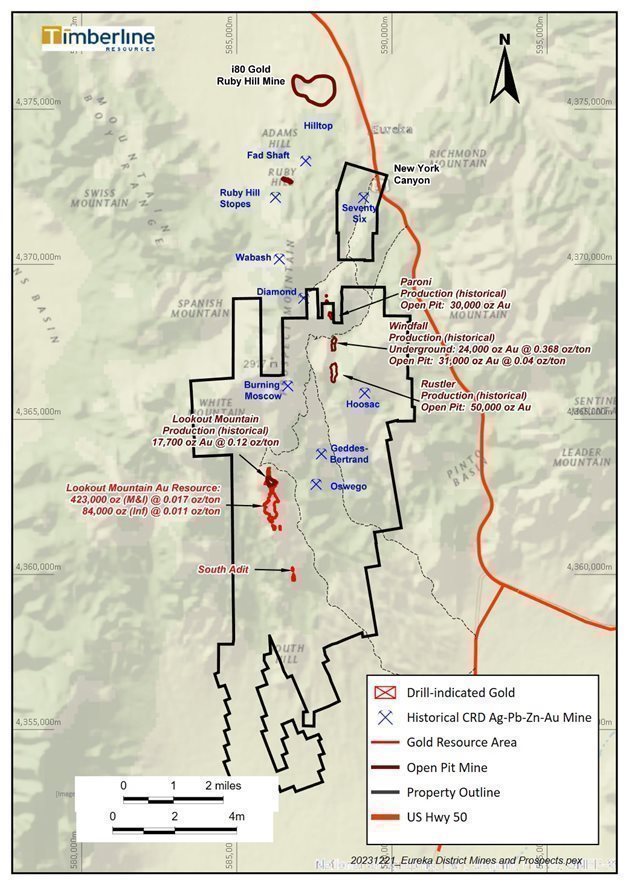

We acquired the Eureka Project as part of our acquisition of Staccato Gold Resources Ltd. (“Staccato Gold”) and its wholly owned subsidiary, BH Minerals USA, Inc. (“BH Minerals”), in June 2010. Eureka comprises an area of 18,464 acres (~29 square miles) within the Battle Mountain – Eureka Mineral Trend. The property’s northern boundary is located approximately 1 mile south of the town of Eureka, Nevada, in Eureka County (Figure 2).

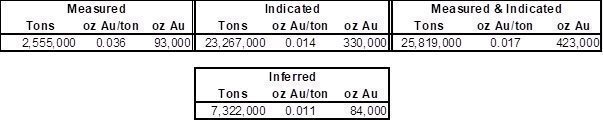

Historical production of gold in the project area included approximately 112,000 oz at the Windfall Mine, which began operation in 1975 (Russell, 2005). An additional 17,700 oz of gold was produced from the Lookout Mountain Pit which operated in 1987 (Cargill, 1988, Jonson, 1991).

Property Description

The Eureka Project is situated in the southern part of the Eureka mining district, within T19N, R53E and unsurveyed T17N and T18N, and R53E (Figure 2). The property is also within the bounds of the United States Geological Survey (USGS) 1:24,000-scale 7.5-minute topographic series maps of the Pinto Summit and Spring Valley Summit quadrangles.

The property consists of 1,036 claims totaling 18,249 acres most of which are US Bureau of Land Management (BLM) unpatented claims with the remainder being patented (Table 1). Timberline pays federal and county claim maintenance fees on the Eureka Project. The federal claim fees are due to the BLM before September 1 of each year, and the county fees are due to Eureka County on November 1 of each year. All unpatented mining claims on the Eureka property have been located under the General Mining Laws of the United States on BLM managed lands.

| 17 |

| Table of Contents |

Figure 1. Timberline Project Locations

| 18 |

| Table of Contents |

Figure 2. Timberline’s Eureka Project Area

| 19 |

| Table of Contents |

The following table summarizes the claims and royalties for the Eureka Project:

Table 1 - Eureka Project Claim and Royalty Summary

Property Name & Agreements/Royalties | Type of Claim | Number of Claims | Area |

Lookout Mountain Mining lease and agreement dated August 22, 2003, and amended on June 1, 2008, between Timberline and Rocky Canyon Mining Company; 3.5% Net Smelter Return (NSR) royalty + 1.5% NSR royalty capped at $1.5 million (excludes Trevor and Dave claims); 20-year lease term commencing June 1, 2008; annual advanced royalty payment of $72,000. | Unpatented

| 373 | 6,368 acres |

Trail Timberline holds title | Unpatented | 30 | 620 acres |

South Ratto Timberline holds title; 4% NSR | Unpatented | 108 | 1,850 acres |

Hoosac North Amselco 4% NSR | Unpatented | 192 | 3,100 acres

|

Little Rosa (Hoosac royalty applies) | Patented | 1 | 7 acres |

Rambler (North Amselco royalty applies) | Patented | 1 | 7 acres |