UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| (Mark One) | |

| | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the fiscal year ended | |

| or | |

| | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the transition period from to | |

Commission File No.

DOUGLAS DYNAMICS, INC.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

|

Registrant’s telephone number, including area code (

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| | | |

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S‑T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non‑accelerated filer, smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

| | Accelerated filer ☐ | Non‑accelerated filer ☐ | Smaller reporting company Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Exchange Act). Yes

At June 30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting stock of the Registrant held by stockholders who were not affiliates of the Registrant was approximately $

Documents Incorporated by Reference:

Portions of the Proxy Statement for the Registrant’s Annual Meeting of Shareholders to be held on April 25, 2023, which Proxy Statement will be filed with the Securities and Exchange Commission no later than 120 days after the close of the fiscal year ended December 31, 2022, are incorporated into Part III.

Forward Looking Statements

This Annual Report on Form 10‑K contains “forward‑looking statements” made within the meaning of the Private Securities Litigation Reform Act of 1995. Words such as “anticipate,” “believe,” “intend,” “estimate,” “expect,” “continue,” “should,” “could,” “may,” “plan,” “project,” “predict,” “will” and similar expressions are intended to identify forward ‑ looking statements. In addition, statements covering our future sales or financial performance and our plans, performance and other objectives, expectations or intentions are forward‑looking statements, such as statements regarding our liquidity, debt, planned capital expenditures, and adequacy of capital resources and reserves. Factors that could cause our actual results to differ materially from those expressed or implied in such forward‑looking statements include, but are not limited to:

| ● |

Weather conditions, particularly lack of or reduced levels of snowfall and the timing of such snowfall, including as a result of global climate change; |

| ● |

Our inability to maintain good relationships with the original equipment manufacturers (“OEM”) with whom we currently do significant business; |

| ● |

The inability of our suppliers and OEM partners to meet our volume or quality requirements; |

| ● |

Increases in the price of steel or other materials, including as a result of tariffs, necessary for the production of our products that cannot be passed on to our distributors; |

| ● |

Increases in the price of fuel or freight; |

| ● |

The effects of laws and regulations and their interpretations on our business and financial conditions, including policy or regulatory changes related to climate change; |

| ● |

A significant decline in economic conditions, including as a result of the COVID-19 pandemic; |

| ● |

Our inability to maintain good relationships with our distributors; |

| ● |

Lack of available or favorable financing options for our end‑users, distributors or customers; |

| ● |

Inaccuracies in our estimates of future demand for our products; |

| ● |

Our inability to protect or continue to build our intellectual property portfolio; |

| ● |

Our inability to develop new products or improve upon existing products in response to end‑user needs; |

| ● |

Losses due to lawsuits arising out of personal injuries associated with our products; |

| ● |

Factors that could impact the future declaration and payment of dividends or our ability to execute repurchases under our stock repurchase program; |

| ● |

Our inability to compete effectively against our competition; and |

| ● |

Our inability to achieve the projected financial performance with the business of Henderson Enterprises Group, Inc. (“Henderson”), which we acquired in 2014, or with the assets of Dejana Truck & Utility Equipment Company, Inc. (“Dejana”), which we acquired in 2016 and unexpected costs or liabilities related to such acquisitions. |

We undertake no obligation to revise the forward‑looking statements included in this Annual Report on Form 10‑K to reflect any future events or circumstances. Our actual results, performance or achievements could differ materially from the results expressed in, or implied by, these forward‑looking statements. Factors in addition to those listed above that could cause or contribute to such differences are discussed in Item 1A, “Risk Factors” of the Annual Report on Form 10‑K.

Overview

Home to the best-selling brands in the industry, Douglas Dynamics, Inc. (the “Company,” “we,” “us,” “our”) is North America's premier manufacturer and upfitter of commercial work truck attachments and equipment. For more than 75 years, the Company has been innovating products that enable end-users to perform their jobs more efficiently and effectively, providing opportunities for businesses to increase profitability. Our commitment to continuous improvement enables us to consistently produce high quality products and drive shareholder value. The Douglas Dynamics portfolio of products and services is separated into two segments: First, the Work Truck Attachments segment, which includes our operations that manufacture and sell snow and ice control attachments and other products sold under the FISHER®, SNOWEX® and WESTERN® brands, as well as our vertically integrated products. Second, the Work Truck Solutions segment, which includes manufactured municipal snow and ice control products under the HENDERSON® brand and the upfit of market leading attachments and storage solutions under the HENDERSON® brand, and the DEJANA® brand and its related sub-brands. For additional financial information regarding our reportable business segments, see Note 17 of the Notes to Consolidated Financial Statements of this report.

In our Work Truck Attachments segment, we offer a broad product line of snowplows and sand and salt spreaders for light trucks that we believe to be the most complete line offered in the U.S. and Canadian markets. We also provide a full range of related parts and accessories, which generates an ancillary revenue stream throughout the lifecycle of our snow and ice control equipment. For the years ended December 31, 2022, 2021 and 2020, 85%, 84% and 86% of our net sales in our Work Truck Attachments segment were generated from sales of snow and ice control equipment, respectively, and 15%, 16% and 14% of our net sales in our Work Truck Attachments segment were generated from sales of parts and accessories, respectively. While we measure sales of parts and accessories separately from snow and ice control equipment, they are integrated with one another and are not separable.

We sell our Work Truck Attachments products through a distributor network primarily to professional snowplowers who are contracted to remove snow and ice from commercial and residential areas. We have engendered exceptional customer loyalty for our products because of our ability to satisfy the stringent demands of our customers for a high degree of quality, reliability and service. As a result, we believe our installed base is the largest in the light truck market with over 500,000 snowplows and sand and salt spreaders in service. Because sales of snowplows and sand and salt spreaders are primarily driven by the need of our core end‑user base to replace worn existing equipment, we believe our substantial installed base provides us with a high degree of predictable sales over any extended period of time.

We believe that our Work Truck Attachments segment has the snow and ice control industry’s most extensive distribution network worldwide, which consists of approximately 3,100 points of sale. Direct points of shipment are predominantly through North American truck equipment and lawn care equipment distributors. Most of our distributors are located throughout the snow belt regions in North America (primarily the Midwest, East and Northeast regions of the United States as well as all provinces of Canada). We have longstanding relationships with many of our distributors. We continually seek to grow and optimize our network by opportunistically adding high‑quality, well‑capitalized distributors in select geographic areas and by cross‑selling our industry leading brands within our distribution network. We have extended our reach to international markets, establishing distribution relationships in Northern Europe and Asia, where we believe meaningful growth opportunities exist.

Our Work Truck Solutions segment participates in the manufacture of municipal snow and ice control products and offers a complementary line of upfitting services and products. Our Work Truck Solutions products consist of truck and vehicle upfits where we attach component pieces of equipment, truck bodies, racking, and storage solutions with varying levels of complexity to a vehicle chassis, and which are typically used by end-users for work related purposes. Our Work Truck Solutions segment is a premier upfitter of Class 3 - 8 trucks and other commercial work vehicles. We also provide customized turnkey solutions to governmental agencies such as Departments of Transportation (“DOTs”) and municipalities. Additionally, we believe that our Work Truck Solutions segment is a leading specialized manufacturer of storage solutions for trucks and vans and cable pulling equipment for trucks. We believe we are a regional market leader in the truck and vehicle upfitting market. We believe that our Work Truck Solutions business possesses significant customer relationships comprised of approximately 2,800 customers across the truck equipment industry. We have longstanding relationships with many of our Work Truck Solutions customers. We continually seek to grow and strengthen our customer relationships by providing custom solutions to our customers’ evolving specialty upfit needs. We are able to serve our Work Truck Solutions customers’ needs through our bailment and floor plan agreements with original equipment vehicle manufacturers who supply truck chassis, on which we perform custom upfits for our customers.

We believe we are a leader in operational efficiency in our industries, resulting from our application of lean manufacturing principles, our vertical integration, and a highly variable cost structure We continually seek to use lean principles to reduce costs and increase the efficiency of our manufacturing operations. During the year ended December 31, 2022 we manufactured our products and upfitted vehicles in five facilities that we own in Milwaukee, Wisconsin; Rockland, Maine; Madison Heights, Michigan; Manchester, Iowa; and Huntley, Illinois. We also lease fifteen manufacturing, service and upfit facilities, located in Iowa, Maryland, Missouri, New Jersey, New York, Ohio, Pennsylvania, and Rhode Island. Furthermore, our manufacturing efficiency allows us to deliver desired products quickly to our customers, especially during times of sudden and unpredictable snowfall events when our customers need our products immediately.

Our Industry

Work Truck Attachments Segment

Our Work Truck Attachments Segment participates primarily in the snow and ice control equipment industries in North America. These industries consist predominantly of domestic participants that manufacture their products in North America. The annual demand for snow and ice control equipment is driven primarily by the replacement cycle of the existing installed base, which is predominantly a function of the average life of a snowplow or spreader and is driven by usage and maintenance practices of the end‑user. We believe actively‑used snowplows are typically replaced, on average, every 9 to 12 years.

We believe that sales of both light and heavy duty snow and ice control equipment are driven primarily by the replacement cycle of the existing installed base, which is predominantly a function of the average life of a snowplow or spreader and is driven by usage and maintenance practices of the end‑user. The primary factor influencing the replacement cycle for snow and ice control equipment for light trucks is the level, timing and location of snowfall. Sales of snow and ice control equipment in any given year and region are most heavily influenced by local snowfall levels in the prior snow season. Heavy snowfall during a given winter causes equipment usage to increase, resulting in greater wear and tear and shortened life cycles, thereby creating a need for replacement equipment and additional parts and accessories.

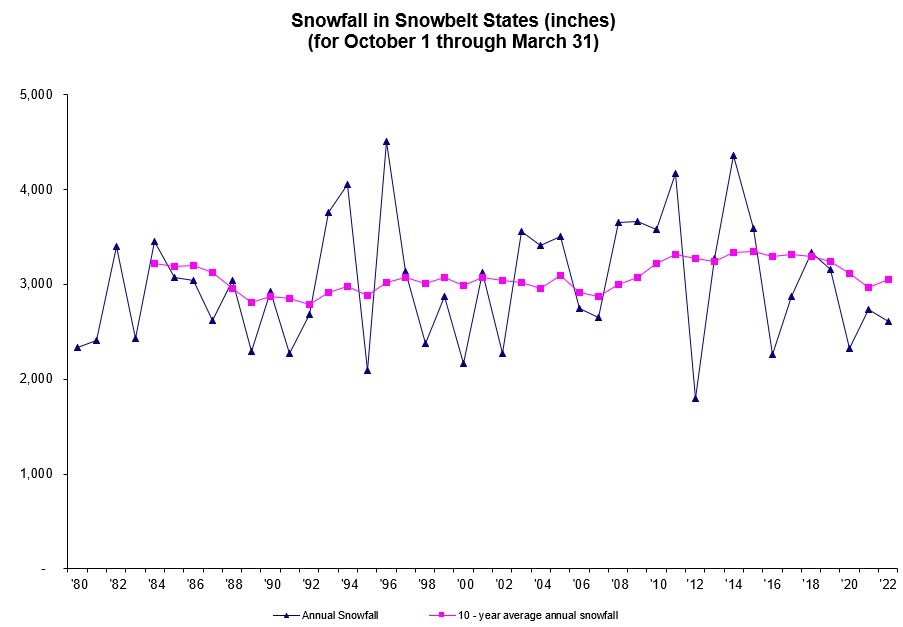

While snowfall levels vary within a given year and from year‑to‑year, snowfall, and the corresponding replacement cycle of snow and ice control equipment, is relatively consistent over multi‑year periods. The following chart depicts aggregate annual and ten‑year (based on the typical life of our snowplows) rolling average of the aggregate snowfall levels in 66 cities in 26 snow belt states across the Northeast, East, Midwest and Western United States where we monitor snowfall levels from 1980 to 2022. As the chart indicates, since 1984, aggregate snowfall levels in any given rolling ten‑year period have been fairly consistent, ranging from 2,782 to 3,345 inches.

| Note: | The 10‑year rolling average snowfall is not presented prior to 1984 for purposes of the calculation due to lack of snowfall data prior to 1975. Snowfall data in this chart is not adjusted for snowfall outside of the 66 cities in the 26 states reflected. |

|

|

|

| Source: | National Oceanic and Atmospheric Administration’s National Weather Service. |

The demand for snow and ice control equipment can also be influenced by general economic conditions in the United States, as well as local economic conditions in the snow‑belt regions in North America. In stronger economic conditions, our end‑users may choose to replace or upgrade existing equipment before its useful life has ended, while in weak economic conditions, our end‑users may seek to extend the useful life of equipment, thereby increasing the sales of parts and accessories. However, since snow and ice control management is a non‑discretionary service necessary to ensure public safety and continued personal and commercial mobility in populated areas that receive snowfall, end‑users cannot extend the useful life of snow and ice control equipment indefinitely and must replace equipment that has become too worn, unsafe or unreliable, regardless of economic conditions. While our parts and accessories yield slightly higher gross margins than our snow and ice control equipment, they yield significantly lower revenue than equipment sales, which adversely affects our results of operations. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Seasonality and Year‑to‑Year Variability.”

Long‑term growth in the overall snow and ice control equipment market also results from geographic expansion of developed areas in the snow belt regions of North America (primarily the Midwest, East and Northeast regions of the United States as well as all provinces of Canada), as well as consumer demand for technological enhancements in snow and ice control equipment and related parts and accessories that improves efficiency and reliability. Continued construction in the snow belt regions in North America increases the aggregate area requiring snow and ice removal, thereby growing the market for snow and ice control equipment. Additionally, there is continued potential for growth within Work Truck Attachments related to the sale of non-truck snow and ice control equipment, including utility terrain vehicle (“UTV”) plows and other such equipment. Additionally, in order to ensure reliable commerce and safe roads, distribution of our ice control equipment continues to expand into states south of the snow belt. The development and sale of more reliable, more efficient and more sophisticated products have contributed to an approximate 2% to 4% average unit price increase in each of 2017 through 2020. In 2021 and 2022, more significant price increases were implemented across both Work Truck Attachments and Work Truck Solutions in response to materials, freight and labor inflation. There were multiple price increases ranging from the mid-single digits to low double-digits and were implemented at various points in 2021 and 2022.

Work Truck Solutions Segment

Our Work Truck Solutions Segment primarily participates in the manufacture of municipal snow and ice control products, as well as in the truck and vehicle upfitting industry in the United States. This industry consists predominantly of domestic participants that upfit work trucks and vehicles. Specifically, there are regional market leaders that operate in close proximity to the original equipment vehicle manufacturers’ facilities and vehicle ports of entry. In addition to the regional market leaders, there exist smaller upfit businesses. Our Work Truck Solutions segment competes against both the other regional market leaders and the smaller market participants. The annual demand for upfit vehicles is subject to the general macro-economic environment trends and municipal budgets.

We believe our Work Truck Solutions segment is a regional market leader in the Northeast and Mid-Atlantic regions of the United States. We serve a variety of different customers that include dealers who typically sell to light and heavy duty truck end-users and to large national customers who purchase fleets of upfitted vehicles. Heavy duty truck end-users typically are comprised of local governments and municipalities which plan for and execute planned replacement of equipment over time. Approximately half of our revenues are derived from dealer customers, while approximately 40% of our revenues are fleet sales and sales to governmental entities. Our remaining sales are derived from over the counter sales of parts and accessories.

Long term growth in the truck and vehicle upfit market will depend on technological advances in the component products and advances in the original equipment manufacturer’s vehicles, as well customer demand for such products. Along with technological advancements, end-users are demanding more specialized vehicles specifically related to their unique work related needs, which we expect will further increase demand. Along with technological advancements, products become more complex in the marketplace, thus increasing the importance of the role of the truck upfitter in the value chain.

Our Competitive Strengths

We compete solely with other North American manufacturers and upfitters who do not benefit from our manufacturing efficiencies, depth and breadth of products, extensive distributor network and customer relationships. As the market leader in the industries we serve, we enjoy a set of competitive advantages versus smaller competitors, which allows us to generate robust cash flows in all market environments and to support continued investment in our products, distribution capabilities and brand regardless of annual volume fluctuations. We believe these advantages are rooted in the following competitive strengths and reinforce our industry leadership over time.

Exceptional Customer Loyalty and Brand Equity. Our brands enjoy exceptional customer loyalty and brand equity in the snow and ice control equipment and truck upfitting industries with both end‑users and distributors, which have been developed through over 75 years of superior innovation, productivity, reliability and support, consistently delivered year after year. We believe past brand experience, rather than price, is the key factor impacting our products.

Broadest and Most Innovative Product Offering in Work Truck Attachments. In our Work Truck Attachments segment, we provide the industry’s broadest product offering with a full range of snowplows, sand and salt spreaders and related parts and accessories. We believe we maintain the industry’s largest and most advanced in‑house new product development program, historically introducing several new and redesigned products each year. Our broad product offering and commitment to new product development is essential to maintaining and growing our leading market share position as well as continuing to increase the profitability of our business. Meanwhile at our Work Truck Solutions segment, each upfit is customized to the specific needs of our customers.

Extensive North American Distributor Network in Work Truck Attachments. With approximately 3,100 points of sale at our Work Truck Attachments segment, we benefit from having what we believe to be the most extensive distributor network in the light truck and heavy duty snow and ice control equipment industry, providing a significant competitive advantage over our peers. Our distributors function not only as sales and support agents (providing access to parts and service), but also as industry partners providing real‑time end‑user information, such as retail inventory levels, changing consumer preferences or desired functionality enhancements, which we use as the basis for our product development efforts.

Leader in Operational Efficiency. We believe we are a leader in operational efficiency in our industries, resulting from our application of lean manufacturing principles and a highly variable cost structure. By utilizing lean principles, we are able to adjust production levels easily to meet fluctuating demand, while controlling costs in slower periods. This operational efficiency is supplemented by our highly variable cost structure, driven in part by our access to a sizable temporary workforce (comprising approximately 10‑15% of our Work Truck Attachments workforce during average snowfall years), which we can quickly adjust, as needed. These manufacturing efficiencies enable us to respond rapidly to urgent customer demand during times of sudden and unpredictable snowfalls, allowing us to provide exceptional service to our existing customer base and capture new customers from competitors that we believe cannot service their customers’ needs with the same speed and reliability.

Strong Cash Flow Generation. We are able to generate significant cash flow as a result of relatively consistent high profitability, low capital spending requirements and predictable timing of our working capital requirements. Our significant cash flow has allowed us to reinvest in our business, pay down long term debt, pay substantial dividends to our stockholders, and make strategic acquisitions.

Experienced Management Team. We believe our business benefits from an exceptional management team that is responsible for establishing our leadership in the light truck and heavy duty snow and ice control equipment and truck upfitting industries. Our senior management team, consisting of four officers as of December 31, 2022, has an average of approximately sixteen years of weather‑related industry experience and an average of over sixteen years with our company. On January 1, 2019, Robert McCormick became our President and Chief Executive Officer. He has been with us for over 18 years and has served in various roles, including Chief Operating Officer and Chief Financial Officer, among others. Effective December 31, 2022, Keith Hagelin, President, Work Truck Attachments, retired from the Company. Through management’s strategic vision, we have been able to expand our distributor network and grow our market leading position.

Our Business Strategy

Our business strategy is to capitalize on our competitive strengths to maximize cash flow to reinvest in our business, pay dividends, reduce indebtedness, execute repurchases under our stock repurchase program and to create stockholder value. We have also developed a management system called the Douglas Dynamics Management System (“DDMS”) that is intended to assist in value creation and enhanced customer service and includes a collection of tools to solve problems and deliver greater value to our customers by eliminating waste and improving the way we work. DDMS is an integrated system that continues to evolve with our business to deliver on strategic priorities and goals through a culture of continuous improvement, people who embrace change, world-class processes, and practical tools. The building blocks of our strategy are:

Continuous Product Innovation. We believe new product innovation is critical to maintaining and growing our market leading position in the snow and ice control equipment industry. We will continue to focus on developing innovative solutions to increase productivity, ease of use, reliability, durability and serviceability of our products and on incorporating lean manufacturing concepts into our product development process, which has allowed us to reduce the overall cost of development and, more importantly, to reduce our time‑to‑market.

Distributor Network and Customer Optimization. At our Work Truck Attachment segment, we will continually seek opportunities to continue to expand our extensive distribution network by adding high‑quality, well‑capitalized distributors in select geographic areas and by cross‑selling our industry leading brands within our distribution network to ensure we maximize our ability to generate revenue while protecting our industry leading reputation, customer loyalty and brands. We will also focus on optimizing this network by providing in‑depth training, valuable distributor support and attractive promotional and incentive opportunities. As a result of these efforts, we believe a majority of our distributors choose to sell our products exclusively. We believe this sizable high quality network is unique in the industry, providing us with valuable insight into purchasing trends and customer preferences, and would be very difficult to replicate. At our Work Truck Solutions segment, we have well developed customer relationships resulting from being responsive to the needs of our customers. We will seek opportunities to continue to expand our customer group by increasing throughput, allowing us to grow our customer base and continue to be responsive to our customers’ specialized upfit needs.

Aggressive Asset Management and Profit Focus. We will continue to aggressively manage our assets in order to maximize our cash flow generation despite seasonal and annual variability in snowfall levels that affect our Work Truck Attachments segment. We believe our ability is unique in our industry and enables us to achieve attractive margins in all snowfall environments. Key elements of our asset management and profit focus strategies include:

| ● |

employment of a highly variable cost structure, which can allow us to quickly adjust costs in response to real‑time changes in demand; |

| ● |

use of enterprise‑wide lean principles, which allow us to easily adjust production levels up or down to meet demand; |

| ● |

implementation of a pre‑season order program, which incentivizes distributors to place orders prior to the retail selling season and thereby enables us to more efficiently utilize our assets; and |

| ● |

development of a vertically integrated business model, which we believe provides us cost advantages over our competition. |

Additionally, although modest, our capital expenditure requirements and operating expenses can be temporarily reduced in response to anticipated or actual lower sales in a particular year to maximize cash flow.

Flexible, Lean Enterprise Platform. We will continue to utilize lean principles to maximize the flexibility, efficiency and productivity of our manufacturing operations while reducing the associated costs, enabling us to increase distributor and end‑user satisfaction. For example, in an environment where shorter lead times and near‑perfect order fulfillment are important to our distributors, we believe our lean processes have helped us to improve our shipping performance and build a reputation for providing industry leading shipping performance.

Our Growth Opportunities

Opportunistically Seek New Products and New Markets. We plan to continue to evaluate other acquisition opportunities within our industry that can help us expand our distribution reach, enhance our technology and as a consequence improve the breadth and depth of our product lines. We also consider diversification and vertical integration opportunities in adjacent markets that complement our business model and could offer us the ability to leverage our core competencies to create stockholder value.

Increase Our Industry Leading Market Share. In our Work Truck Attachments segment, we plan to leverage our industry leading position, distribution network and new product innovation capabilities to capture market share in the North American snow and ice control equipment market, focusing our primary efforts on increasing penetration in those North American markets where we believe our overall market share is less than 50%, including the heavy duty truck market. At our Work Truck Solutions segment, we plan to leverage our regional market leading position and utilize DDMS to further penetrate upfit markets and to grow our customer base.

Order Backlog

We had total backlog of $368.7 million and $315.4 million at December 31, 2022 and 2021, respectively. Backlog information may not be indicative of results of operations for future periods.

Human Capital Management

Our Purpose

Douglas Dynamics is home to the most trusted brands in the industry, Douglas Dynamics is North America’s premier manufacturer and upfitter of work truck attachments and equipment. Our commitment to continuous improvement enables us to consistently produce the highest quality products and drive shareholder value. We serve as trusted partners to our dealers, suppliers and end users, whose businesses benefit from our operational and management expertise.

Our Culture

For more than 75 years, Douglas Dynamics has been manufacturing the best products available on the market. Every day, our employees work hard to meet our customers’ needs, and every day we, as an organization, are focused on fostering a collaborative environment for our employees and offering them the opportunity to have ownership in our company's success. As of December 31, 2022, we employed 1,813 employees, all US based except for 14 employees who work in the Douglas Dynamics Sourcing Office located in Beijing, China. None of our employees are represented by a union and we are not party to any collective bargaining agreements. We believe that our focus on integrity, teamwork and high-performance have enabled us to create an ideal work environment for every one of our employees. Our Board of Directors and our Compensation Committee regularly receive updates from our senior management with respect to our health and safety, diversity and inclusion and our internal talent development initiatives and priorities.

Our commitment to continuous improvement extends well beyond producing the highest quality products or driving shareholder value—we also value the growth, improvement and engagement of our employees.

Creating a culture of excellence is the key to our success, which is why we work hard to give our employees the tools and training to achieve more. We know that when our employees are taken care of, our business partners get the most out of their Douglas Dynamics experience, helping us to remain North America‘s premier manufacturer of vehicle attachments and equipment.

Our Core Values and Winning Behaviors

Our Core Values, Grow, Improve, and Engage, are critical to our individual and organizational success and focus us as an organization to ensure we succeed by executing upon the right things.

Also critical to our success are our Winning Behaviors, a framework of priorities that we expect of each Douglas Dynamics employee to support the success of our company, namely, winning as an organization the right way. Our focus on our Winning Behaviors helps ensure a consistent focus on our Core Values across all employees and in all locations.

| ● |

Be Customer and Results Driven: Consider the customer in everything you do. Focus on meaningful results that benefit both our customers and organization. |

| ● |

Anticipate the Possibilities: See around corners. Envision and embrace new or unique ideas and seek to understand their impact on the future of our business. |

| ● |

Collaborate and Care: Appreciate the value in working together. Work as a team to care for our customers, our business, our communities and most importantly, each other. |

| ● |

Communicate Responsibly: Communicate to build culture and trust. Place an emphasis on listening and speaking in ways that help everyone succeed. |

| ● |

Develop Self and Others: Take active ownership of your development and support others. Continually improve your knowledge, skills and abilities. |

| ● |

Get Better Every Day: Make even the smallest improvement every day. Continuous improvement is at the center of everything we do. Not just what we do, but how we do it, every single day. |

Talent Development

Talent development is a critical component of individual and organizational success. We promote our internal Douglas Dynamics University (DDU) to support all employees' development. DDU is one of the services provided by the Organizational Development Team that supports our company's dedication to the performance, development, and growth of our talented people. To truly develop people, we believe in taking a balanced approach to activity selection within the offerings provided by DDU:

| Instruction |

Interaction |

Application |

| In-Person & Virtual Classes |

Coaching |

Job Rotations |

| Self-Paced eLearning |

Mentoring |

Temporary Assignments |

| Conferences |

Job Shadowing |

Projects |

| Podcasts & Webcasts |

Discussions |

Challenging Projects |

| Books & Articles |

Interest Groups |

Role Playing |

| Websites |

Book Clubs |

Doing |

| Videos |

Online Communities |

We achieve the goals of DDU by:

| ● |

Developing and delivering live and virtual instructor-led training, and eLearning |

| ● |

Managing the Douglas Dynamics Learning Center (DDLC) – an eLearning platform |

| ● |

Supporting projects that require training creation throughout DD |

| ● |

Developing and delivering team building activities upon request |

| ● |

Providing training solutions that can be delivered by other teams or certified trainers |

Our Ethics

Along with our core values and winning behaviors, we act in accordance with our Code of Conduct Policy (Code of Conduct), which creates expectations and provides guidance for all our employees to make the right decisions. Our Code of Conduct covers such topics as anti-corruption, discrimination, harassment, privacy, appropriate use of company assets, protecting confidential information and reporting Code of Conduct violations.

Diversity & Inclusion

Douglas Dynamics is deeply committed to increasing diversity and inclusion; however, we continue to have more work to do across our footprint. We are investing in multiple initiatives focused on identifying diverse talent. These include engaging with recruiting firms, utilizing job-posting sites and collaborating with university programs that specialize in connecting companies like Douglas Dynamics with a diverse array of candidates. Moving forward, we will continue to review and refine our initiatives as we seek to further diversify our workforce.

Health & Safety

We are committed to the health and safety of our employees. The environment we provide is based on our vision to create a working environment that places the highest value on the welfare of our employees, to instill a sense of ownership and to embrace excellence in safety, production and quality of work being done.

| ● |

Our goals are simple: to create added value for our customers through best in class performance in environmental, health and safety practices. We pledge to place the safety and well-being of our employees first and to embody honesty and integrity in the pursuit of our vision of creating a world class safety culture. |

| ● |

We are committed to providing world-class products and services that minimize harm to the environment and public health. We are committed not only in regard to our products to our customers but also in the way we conduct internal operations. We look to preserve the environment and will conduct business where feasible in an environmentally, sustainable way. |

Financing Program

We are party to a financing program in which certain distributors may elect to finance their purchases from us through a third party financing company. We provide the third party financing company recourse against us regarding the collectability of the receivable under the program due to the fact that if the third party financing company is unable to collect from the distributor the amounts due in respect of the product financed, we would be obligated to repurchase any remaining inventory related to the product financed and reimburse any legal fees incurred by the financing company. During the years ended December 31, 2022, 2021 and 2020, distributors financed purchases of $15.8 million, $10.5 million and $7.6 million through this financing program, respectively. At both December 31, 2022 and December 31, 2021, there were no uncollectible outstanding receivables related to sales financed under the financing program. The amount owed by our distributors to the third party financing company under this program at December 31, 2022 and 2021 was $16.1 million and $8.3 million, respectively. We were not required to repurchase repossessed inventory for the years ended December 31, 2022, 2021 and 2020.

In the past, minimal losses have been incurred under this agreement. However, an adverse change in distributor retail sales could cause this situation to change and thereby require us to repurchase repossessed units. Any repossessed units are inspected to ensure they are current, unused product and are restocked and resold.

Intellectual Property

We maintain patents relating to snowplow mounts, assemblies, hydraulics, electronics and lighting systems, brooms, sand, salt and fertilizer spreader assemblies, reel handlers and carriers and shelving systems. Patents are valid for the longer period of 17 years from issue date or 20 years from filing date. The duration of the patents we currently possess range between less than one year and 18 years of remaining life. Our patent applications date from 2005 through 2022.

We rely on a combination of patents, trade secrets and trademarks to protect certain of the proprietary aspects of our business and technology. We hold approximately 44 U.S. registered trademarks (including the trademarks WESTERN®, FISHER®, DEJANA®, BLIZZARD®, SNOWEX®, TURFEX®, SWEEPEX®, HENDERSON® and BRINEXTREME®) 13 Canadian registered trademarks, 5 European trademarks, 7 Chinese trademarks, 56 U.S. issued patents, and 4 Canadian patents.

Raw Materials

We have recently experienced increased commodity costs due to market conditions causing the inflation of steel prices. Historically, we have mitigated, and we currently expect to continue to mitigate, commodity cost increases in part by engaging in proactive vendor negotiations, reviewing alternative sourcing options, substituting materials, engaging in internal cost reduction efforts, and increasing prices on some of our products, all as appropriate. See the section titled “–Overview” in Management’s Discussion and Analysis of Financial Condition and Results of Operations below for further discussion.

Most of the components of our products are also affected by commodity cost pressures and are commercially available from a number of sources. In 2022 and 2021, we experienced no significant work stoppages because of shortages of raw materials or commodities, although we did have intermittent shutdowns of various facilities in our Work Truck Solutions segment due to other supply chain disruptions. The highest raw material and component costs are generally for steel, which we purchase from several suppliers.

Government Regulation

Our operations are subject to certain federal, state and local laws and regulations relating to, among other things, climate change, the generation, storage, handling, emission, transportation, disposal and discharge of hazardous and non‑hazardous substances and materials into the environment, the manufacturing of motor vehicle accessories, and employee health and safety. Management believes that the Company’s business is operated in material compliance with all such regulations.

Other Information

We were formed as a Delaware corporation in 2004. We maintain a website with the address www.douglasdynamics.com. We are not including the information contained on our website as part of, or incorporating it by reference into, this report. We make available free of charge (other than an investor’s own Internet access charges) through our website our Annual Report on Form 10‑K, quarterly reports on Form 10‑Q and current reports on Form 8‑K, and amendments to these reports, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the Securities and Exchange Commission (“SEC”). For further information regarding our geographic areas see the Summary of Significant Accounting Policies as discussed in Note 2 to our audited consolidated financial statements included elsewhere in this Annual Report on Form 10‑K.

The Company operates in an environment that involves numerous known and unknown risks and uncertainties. Our business, prospects, financial condition and operating results could be materially adversely affected by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. The risks described below highlight some of the factors that have affected, and in the future could affect our operations.

Risks Related to Weather and Seasonality

Our results of operations for our Work Truck Attachments segment and to a lesser extent our Work Truck Solutions segment depend primarily on the level, timing and location of snowfall. As a result, a decline in snowfall levels in multiple regions for an extended time, including as a result of climate change, could cause our results of operations to decline and adversely affect our ability to generate cash flow.

As a manufacturer through our Work Truck Attachments segment of snow and ice control equipment for light trucks and related parts and accessories, our sales depend primarily on the level, timing and location of snowfall in the regions in which we offer our products. A low level or lack of snowfall in any given year in any of the snow‑belt regions in North America (primarily the Midwest, East and Northeast regions of the United States as well as all provinces of Canada) will likely cause sales of our Work Truck Attachments products and a portion of our Work Truck Solutions products to decline in such year as well as the subsequent year, which in turn may adversely affect our results of operations and ability to generate cash flow. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Seasonality and Year‑to‑Year Variability.” A sustained period of reduced snowfall events in one or more of the geographic regions in which we offer our products could cause our results of operations to decline and adversely affect our ability to generate cash flow. If unfavorable weather conditions are exacerbated by climate change or otherwise, our results of operations may be affected to a greater degree than we have previously experienced.

The year‑to‑year variability of our Work Truck Attachments segment can cause our results of operations and financial condition to be materially different from year‑to‑year and the seasonality of our Work Truck Attachments segment can cause our results of operations and financial condition to be materially different from quarter‑to‑quarter.

Because our Work Truck Attachments segment depends on the level, timing and location of snowfall, our results of operations vary from year‑to‑year. Additionally, because the annual snow season typically only runs from October 1 through March 31, our distributors typically purchase our Work Truck Attachments products during the second and third quarters. As a result, we operate in a seasonal business. We not only experience seasonality in our sales, but also experience seasonality in our working capital needs. Consequently, our results of operations and financial condition of our Work Truck Attachments segment can vary from year‑to‑year, as well as from quarter‑to‑quarter, which could affect our ability to generate cash flow. If we are unable to effectively manage the seasonality and year‑to‑year variability of our Work Truck Attachments segment, our results of operations, financial condition and ability to generate cash flow may be adversely affected.

Risks Related to Economic Conditions

If economic conditions in the United States deteriorate, or if spending by governmental agencies is limited or reduced, our results of operations, financial condition and ability to generate cash flow may be adversely affected.

Historically, demand for snow and ice control equipment for light and heavy duty trucks as well as upfitted vehicles has been influenced by general economic conditions in the United States, as well as local economic conditions in the snow-belt regions in North America.

The global outbreak of COVID-19 in 2020 severely restricted the level of economic activity in North America. In response to this outbreak, the governments of many countries, states, cities and other geographic regions took preventative or protective actions, such as imposing restrictions on travel and business operations. These measures have and are expected to continue to have significant adverse impacts on domestic and foreign economies of uncertain severity and duration. It is likely that the continued spread of COVID-19 and its lingering impact may cause a further economic slowdown, and it is possible that it could cause a global recession.

Weakened economic conditions and limited or reduced government spending (including as a result of the COVID-19 pandemic) may cause both our Work Truck Attachments and Work Truck Solutions end-users to delay purchases of replacement snow and ice control equipment and upfit vehicles and instead repair their existing equipment and vehicles, leading to a decrease in our sales of new equipment and upfitted vehicles. Weakened economic conditions and limited or reduced governmental spending may also cause our end-users to delay their purchases of new light and heavy duty trucks. Because our end-users tend to purchase new snow and ice control equipment concurrent with their purchase of new light or heavy duty trucks, their delay in purchasing new light or heavy duty trucks can also result in the deferral of their purchases of new snow and ice control equipment. The deferral of new equipment purchases during periods of weak economic conditions or limited or reduced government spending may negatively affect our results of operations, financial condition and ability to generate cash flow.

Weakened economic conditions or limited or reduced government spending may also cause both our Work Truck Attachments and Work Truck Solutions end-users to consider price more carefully in selecting new snow and ice control equipment and upfit vehicles, respectively. Historically, considerations of quality and service have outweighed considerations of price, but in a weak economy, or an environment of constrained government spending, price may become a more important factor. Any refocus away from quality in favor of cheaper equipment could cause end-users to shift away from our products to less expensive competitor products, or to shift away from our more profitable products to our less profitable products, which in turn would adversely affect our results of operations and our ability to generate cash flow.

Weakened economic conditions may lead to significant inflation in raw materials and components, labor, benefits, freight, and other areas, which would adversely affect our results of operations and our ability to generate cash flow.

The COVID-19 pandemic could continue to have an adverse effect on our business, financial condition, results of operations and cash flows

As a result of the COVID-19 pandemic, and the market volatility and other economic implications associated with it, our business, financial condition, results of operations and cash flows have been adversely impacted in the years ended December 31, 2022, 2021, and 2020, and may be significantly impacted in future years. It may be more difficult to collect from customers as a result of customer bankruptcy or other hardships. Supply chains may continue to be disrupted which could raise prices and impact our ability to obtain inventory timely. During the years ended December 31, 2022, 2021 and 2020, we faced supply chain disruptions and additional difficulty obtaining chassis and other inventory, which we attribute in part to the impacts of the COVID-19 pandemic, and supply chains may continue to be disrupted which could adversely affect our results. We preventatively and voluntarily closed our facilities on March 18, 2020, suspending production and shipments at all of our locations, which negatively impacted sales volumes and profitability during the shutdown period. Throughout the second quarter of 2020, we slowly ramped up production at various facilities as appropriate and have since returned to full production levels. We incurred certain overhead and other costs during the shutdown period that were not capitalized into inventory.

The COVID-19 pandemic has impacted, and may continue to impact, our office locations and our manufacturing and servicing facilities, as well as those of our third party vendors, including the effects of facility closures, reductions in operating hours and other social distancing efforts. For example, we enacted temporary shutdown of certain of our facilities in the first and second quarters of 2020 to protect the health and safety of our employees, customers, partners and the surrounding communities. We slowly ramped up production during the second quarter, and are currently at full production levels. Although our operations are generally viewed as essential services in the geographies in which we operate, we can give no assurance that our operations will continue to be classified as essential in each of the jurisdictions in which we operate.

We may have challenges in short-term liquidity which could impact our ability to fund working capital needs. If our access to capital were to become significantly constrained or if costs of capital increased significantly due the impact of COVID-19, including volatility in the capital markets, a reduction in our credit ratings or other factors, results of operations and cash flows could be adversely affected.

We are not able to predict the full impact of the pandemic on our future financial results as the situation remains unpredictable. The extent to which the COVID-19 pandemic impacts our financial condition will depend on future developments that are highly uncertain and cannot be predicted, including new information that may emerge concerning the severity of COVID-19, the longevity of COVID-19, the impact of COVID-19 on economic activity, and the actions to contain its impacts on public health and the global economy.

The price of steel, a commodity necessary to manufacture our products, is highly variable. If the price of steel increases, our gross margins could decline.

Steel is a significant raw material used to manufacture our products. During 2022, our raw steel purchases were in amounts equivalent to approximately 13% of our revenue. During 2021, our raw steel purchases were in amounts equivalent to approximately 12% of our revenue. During 2020, our raw steel purchases were in amounts equivalent to approximately 10% of our revenue. The steel industry is highly cyclical in nature, and steel prices have been volatile in recent years and may remain volatile in the future. Steel prices are influenced by numerous factors beyond our control, including general economic conditions domestically and internationally as a result of the lingering impacts of the COVID-19 pandemic and otherwise, the availability of raw materials, competition, labor costs, freight and transportation costs, production costs, tariffs and other trade restrictions. For example, in March 2018, the United States imposed an additional 25% tariff under Section 232 of the Trade Expansion Act of 1962, as amended, on steel products imported into the Unites States. Steel prices are volatile and may also increase as a result of increased demand from the automobile and consumer durable sectors. If the price of steel increases, our variable costs may increase. We may not be able to mitigate these increased costs through the implementation of permanent price increases or temporary invoice surcharges, especially if economic conditions are weak and our distributors and end‑users become more price sensitive. If we are unable to successfully mitigate such cost increases in the future, our gross margins could decline.

If petroleum prices increase, then our results of operations could be adversely affected.

Petroleum prices have fluctuated significantly in recent years. Prices and availability of petroleum products are subject to political, economic and market factors that are outside of our control. Political events in petroleum‑producing regions, including the conflict in Ukraine, as well as hurricanes and other weather‑related events may cause the price of fuel to increase. If the price of fuel increases, the demand for our products may decline and transportation and freight costs may increase, which would adversely affect our financial condition and results of operations.

Global climate change and related emphasis on ESG matters by various stakeholders could negatively affect our business.

Increased public awareness and concern regarding global climate change may result in more regional and/or federal requirements to reduce or mitigate the effects of greenhouse gas emissions. There continues to be a lack of consistent climate legislation, which creates economic and regulatory uncertainty. Such regulatory uncertainty extends to our product portfolio and overall costs of compliance, which may impact the demand for our products and/ or require us to make increased capital expenditures to meet new standards and regulations. Further, our customers and the markets we serve may impose emissions or other environmental standards upon us through regulation, market-based emissions policies or consumer preference that we may not be able to timely meet, or which may not be economically feasible for us, due to the required level of capital investment or technological advancement.

There is a growing consensus that greenhouse gas emissions are linked to global climate changes. Climate changes, such as extreme weather conditions, create financial risk to our business. For example, the demand for our products and services may be affected by unseasonable weather conditions. Climate changes could also disrupt our operations by impacting the availability and cost of materials needed for manufacturing and could increase insurance and other operating costs. We could also face indirect financial risks passed through the supply chain, and process disruptions due to climate changes could result in price modifications for our products and the resources needed to produce them.

Furthermore, customer, investor, and employee expectations in areas such as the environment, social matters and corporate governance (ESG) have been rapidly evolving and increasing. Specifically, certain customers are requiring information on our environmental sustainability plans and commitments, which we have not yet released publicly as of the date of this filing. There can be no assurance of the extent to which any of our future plans or commitments will be achieved, or that any investments we make in furtherance of achieving any such plans, targets, goals or other commitments will meet customer, investor, employee or other stakeholder expectations and desires or any legal standards regarding sustainability performance.

Additionally, the enhanced stakeholder focus on ESG issues requires the continuous monitoring of various and evolving standards and the associated reporting requirements. A failure to adequately meet stakeholder expectations may result in the loss of business, diluted market valuation, an inability to attract and retain customers or an inability to attract and retain top talent.

Risks Related to our Business and Operations

We depend on outside suppliers and original equipment manufacturers who may be unable to meet our volume and quality requirements, and we may be unable to obtain alternative sources.

We purchase certain components essential to our snowplows and sand and salt spreaders from outside suppliers, including off‑shore sources. We also have OEM partners that supply truck chassis used in our truck upfitting operations across both segments. Most of our key supply arrangements can be discontinued at any time. A supplier may encounter delays in the production and delivery of such products and components or may supply us with products and components that do not meet our quality, quantity or cost requirements. In addition, as was the case in 2022, 2021, and 2020, an OEM may encounter difficulties and may be unable to deliver truck chassis according to our production needs, as a result of computer chip shortages or otherwise, which may result in the deferral of sales to future periods. Additionally, a supplier may be forced to discontinue operations. Any discontinuation or interruption in the availability of quality products, components or truck chassis from one or more of our suppliers may result in increased production costs, delays in the delivery of our products and lost end‑user sales, which could have an adverse effect on our business and financial condition.

We have continued to increase the number of our off‑shore suppliers. Our increased reliance on off‑shore sourcing may cause our business to be more susceptible to the impact of natural disasters, global health epidemics, war and other geopolitical conflict, and other factors that may disrupt the transportation systems or shipping lines used by our suppliers, a weakening of the dollar over an extended period of time and other uncontrollable factors such as changes in foreign regulation, tariffs or economic conditions. In addition, reliance on off‑shore suppliers may make it more difficult for us to respond to sudden changes in demand because of the longer lead time to obtain components from off‑shore sources. We may be unable to mitigate this risk by stocking sufficient materials to satisfy any sudden or prolonged surges in demand for our products. If we cannot satisfy demand for our products in a timely manner, our sales could suffer as distributors can cancel purchase orders without penalty until shipment.

Security breaches and other disruptions could compromise our information and expose us to liability, which would cause our business and reputation to suffer.

In the ordinary course of our business, we collect and store sensitive data, including our proprietary business information and that of our customers, suppliers and business partners, as well as personally identifiable information of our customers and employees, in our data centers and on our networks. The secure processing, maintenance and transmission of this information is critical to our operations and business strategy. Despite our security measures, our information technology and infrastructure may be vulnerable to malicious attacks or breached due to employee error, malfeasance or other disruptions, including as a result of rollouts of new systems. In addition, we currently have portions of our workforce working remotely, which may heighten these risks. Any such breach could compromise our networks and the information stored there could be accessed, publicly disclosed, lost or stolen. Any such access, disclosure or other loss of information could result in legal claims or proceedings and/or regulatory penalties, disrupt our operations, damage our reputation, and/or cause a loss of confidence in our products and services, which could adversely affect our business.

We are heavily dependent on our senior management team. If we are unable to retain, attract, and motivate qualified employees, it may adversely affect our business.

Our continued success depends on the retention, recruitment and continued contributions of key management, finance, sales and marketing personnel, some of whom could be difficult to replace. Our success is largely dependent upon our senior management team. The loss of any one or more of such persons could have an adverse effect on our business and financial condition. Our ability to implement our business plan is dependent on our retaining, hiring, and training a large number of qualified employees every year. Our results of operations could be adversely affected by increased costs due to higher competition for employees, higher employee turnover, or increased employee benefit costs.

Our failure to maintain good relationships with our customers and distributors, the loss or consolidation of our distributor base or the actions or inactions of our distributors could have an adverse effect on our results of operations and our ability to generate cash flow.

We depend on a network of truck equipment distributors to sell, install and service our products and upfitted vehicles. Nearly all of these sales and service relationships are at will, so almost all of our distributors could discontinue the sale and service of our products and upfitted vehicles at any time, and those distributors that primarily sell our products and upfitted vehicles may choose to sell competing products or vehicles at any time. Further, difficult economic or other circumstances could cause any of our distributors to discontinue their businesses. Moreover, if our distributor base were to consolidate or if any of our distributors were to discontinue their business, competition for the business of fewer distributors would intensify. If we do not maintain good relationships with our distributors and customers, or if we do not provide product or upfit offerings and pricing that meet the needs of our distributors and customers, we could lose a substantial amount of our distributor and customer base. A loss of a substantial portion of our distributor and customer base could cause our sales to decline significantly, which would have an adverse effect on our results of operations and ability to generate cash flow.

In addition, our distributors may not provide timely or adequate service to our end‑users. If this occurs, our brand identity and reputation may be damaged, which would have an adverse effect on our results of operations and ability to generate cash flow.

Lack of available financing options for our end‑users or distributors may adversely affect our sales volumes.

Our end‑user base in our Work Truck Attachments segment is highly concentrated among professional snowplowers who comprise over 50% of our end‑users, many of whom are individual landscapers who remove snow during the winter and landscape during the rest of the year, rather than large, well‑capitalized corporations. These end‑users often depend upon credit to purchase our Work Truck Attachments products. If credit is unavailable on favorable terms or at all, then these end‑users may not be able to purchase our Work Truck Attachments products from our distributors, which would in turn reduce sales and adversely affect our results of operations and ability to generate cash flow.

In addition, because our distributors, like our end‑users, rely on credit to purchase our products, if our distributors are not able to obtain credit, or access credit on favorable terms, we may experience delays in payment or nonpayment for delivered products. Further, if our distributors are unable to obtain credit or access credit on favorable terms, they could experience financial difficulties or bankruptcy and cease purchases of our products altogether. Thus, if financing is unavailable on favorable terms or at all, our results of operations and ability to generate cash flow would be adversely affected.

We do not sell our products under long‑term purchase contracts, and sales of our products are significantly impacted by factors outside of our control; therefore, our ability to estimate demand is limited.

We do not enter into long‑term purchase contracts with our distributors and the purchase orders we receive may be cancelled without penalty until shipment. Therefore, our ability to accurately predict future demand for our products is limited. Nonetheless, we attempt to estimate demand for our products for purposes of planning our annual production levels and our long‑term product development and new product introductions. We base our estimates of demand on our own market assessment, snowfall figures, quarterly field inventory surveys and regular communications with our distributors. Because wide fluctuations in the level, timing and location of snowfall, economic conditions and other factors may occur, each of which is out of our control, our estimates of demand may not be accurate. Underestimating demand could result in procuring an insufficient amount of materials necessary for the production of our products, which may result in increased production costs, delays in product delivery, missed sale opportunities and a decrease in customer satisfaction. Overestimating demand could result in the procurement of excessive supplies, which could result in increased inventory and associated carrying costs.

We face competition from other companies in our industry, and if we are unable to compete effectively with these companies, it could have an adverse effect on our sales and profitability. Price competition among our distributors and customers could negatively affect our market share.

In our Work Truck Attachments segment, we primarily compete with regional manufacturers of snow and ice control equipment for light trucks. While we are the most geographically diverse company in our industry, we may face increasing competition in the markets in which we operate. Additionally, in our Work Truck Solutions segment, we compete with other market leaders in the municipal snow and ice manufacturing and truck upfit industries. In saturated markets, price competition may lead to a decrease in our market share or a compression of our margins, both of which would affect our profitability. Moreover, current or future competitors may grow their market share and develop superior service and may have or may develop greater financial resources, lower costs, superior technology or more favorable operating conditions than we maintain. As a result, competitive pressures we face may cause price reductions for our products, which would affect our profitability or result in decreased sales and operating income. Additionally, saturation of the markets in which we compete or channel conflicts among our brands and shifts in consumer preferences may increase these competitive pressures or may result in increased competition among our distributors and affect our sales and profitability. In addition, price competition among the distributors that sell our products could lead to significant margin erosion among our distributors, which could in turn result in compressed margins or loss of market share for us. Management believes that, after ourselves, the next largest competitors in the market for snow and ice control equipment for light trucks are The Toro Company (the manufacturer of the Boss brand of snow and ice control equipment) and Buyers Products Company, and that these companies represent our primary competitors for light truck market share for our Work Truck Attachments segment. Management believes that, after ourselves, the next largest competitors in the market for snow and ice control equipment for heavy trucks are Monroe and Viking, and that these companies represent our primary competitors for heavy truck market share for our Work Truck Solutions segment. Management believes that, other regional market leaders in the truck upfitting industry are Knapheide, Reading, Palfleet and Autotruck, and that these companies represent our primary competitors for the upfit market share for our Work Truck Solutions segment.

The statements regarding our industry, market positions and market share in this filing are based on our management’s estimates and assumptions. While we believe such statements are reasonable, such statements have not been independently verified.

Information contained in this Annual Report on Form 10‑K concerning the snow and ice control equipment and truck upfitting industries, our general expectations concerning these industries and our market positions and other market share data regarding the industries are based on estimates our management prepared using end‑user surveys, anecdotal data from our distributors and distributors that carry our competitors’ products, our results of operations and management’s past experience, and on assumptions made, based on our management’s knowledge of this industry, all of which we believe to be reasonable. These estimates and assumptions are inherently subject to uncertainties, especially given the year‑to‑year variability of snowfall and the difficulty of obtaining precise information about our competitors, and may prove to be inaccurate. In addition, we have not independently verified the information from any third‑party source and thus cannot guarantee its accuracy or completeness, although management also believes such information to be reasonable. Our actual operating results may vary significantly if our estimates and outlook concerning the industry, snowfall patterns, our market positions or our market shares turn out to be incorrect.

We are subject to product liability claims, product quality issues, and other litigation from time to time that could adversely affect our operating results or financial condition.

The manufacture, sale and usage of our products expose us to a risk of product liability claims. If our products are defective or used incorrectly by our end‑users, then injury may result, giving rise to product liability claims against us. If a product liability claim or series of claims is brought against us for uninsured liabilities or in excess of our insurance coverage, and it is ultimately determined that we are liable, our business and financial condition could suffer. Any losses that we may suffer from any liability claims, and the effect that any product liability litigation may have upon the reputation and marketability of our products, may divert management’s attention from other matters and may have a negative impact on our business and operating results. Additionally, we could experience a material design or manufacturing failure in our products, a quality system failure or other safety issues, or heightened regulatory scrutiny that could warrant a recall of some of our products. A recall of some of our products could also result in increased product liability claims. Any of these issues could also result in loss of market share, reduced sales, and higher warranty expense.

Risks Related to Execution of Strategy

We may be unable to identify, complete or benefit from strategic transactions.

Our long‑term growth strategy includes building value for our company through a variety of methods. These methods may include acquisition of, investment in, or joint ventures involving, complementary businesses. We cannot assure that we will be able to identify suitable parties for these transactions. If we are unable to identify suitable parties for strategic transactions we may not be able to capitalize on market opportunities with existing and new customers, which could inhibit our ability to gain market share. Even if we identify suitable parties to participate in these transactions, we cannot assure that we will be able to make them on commercially acceptable terms, if at all.

In July 2016, we acquired Dejana. In December 2014, we acquired Henderson. We may not be able to achieve the projected financial performance or incur unexpected costs or liabilities as a result of these transactions. In addition, if in the future we acquire another company or its assets, it may be difficult to assimilate the acquired businesses, products, services, technologies and personnel into our operations. These difficulties could disrupt our ongoing business, distract our management and workforce, increase our expenses and adversely affect our operating results and ability to compete and gain market share. Mergers and acquisitions are inherently risky and are subject to many factors outside our control. No assurance can be given that any future acquisitions will be successful and will not materially adversely affect our business, operating results, or financial condition. In addition, we may incur debt or be required to issue equity securities to pay for future acquisitions or investments. The issuance of any equity securities could be dilutive to our stockholders. We also may need to make further investments to support any acquired company and may have difficulty identifying and acquiring appropriate resources. If we divest or otherwise exit certain portions of our business in connection with a strategic transaction, we may be required to record additional expenses, and our estimates with respect to the useful life and ultimate recoverability of our carrying basis of assets, including goodwill and purchased intangible assets, could change.

If we are unable to enforce, maintain or continue to build our intellectual property portfolio, or if others invalidate our intellectual property rights, our competitive position may be harmed.

Our patents relate to snowplow mounts, assemblies, hydraulics, electronics and lighting systems, brooms, sand, salt and fertilizer spreader assemblies, reel handlers and carriers and shelving systems. Patents are valid for the longer period of 17 years from issue date or 20 years from filing date. The duration of the patents we currently possess range between less than one year and 18 years of remaining life. Our patent applications date from 2005 through 2022.