Exhibit 99.1

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2022

DATED MARCH 30, 2023

ANNUAL INFORMATION FORM

FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2022

TABLE OF CONTENTS

| PRELIMINARY NOTES |

1 |

| CORPORATE STRUCTURE |

4 |

| GENERAL DEVELOPMENT OF THE BUSINESS |

5 |

| DESCRIPTION OF THE BUSINESS |

11 |

| MINERAL RESERVE AND MINERAL RESOURCE ESTIMATES |

17 |

| MINERAL PROJECTS |

22 |

| MARKET FOR SECURITIES |

64 |

| DIRECTORS AND OFFICERS |

65 |

| CEASE TRADE ORDERS, BANKRUPTCIES, PENALTIES OR SANCTIONS |

71 |

| CONFLICT OF INTEREST |

72 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS |

72 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS |

73 |

| TRANSFER AGENT AND REGISTRAR |

73 |

| MATERIAL CONTRACTS |

73 |

| INTEREST OF EXPERTS |

73 |

| AUDIT COMMITTEE INFORMATION |

74 |

| APPENDIX A DEFINITIONS, TECHNICAL TERMS, ABBREVIATIONS AND CONVERSION |

76 |

| Technical Abbreviations |

76 |

| APPENDIX B AUDIT COMMITTEE CHARTER |

84 |

PRELIMINARY NOTES

Effective Date of

Information

All information in this annual information form

(this “AIF”) of Americas Gold and Silver Corporation (“Americas Gold and Silver” or the “Company”)

is as at December 31, 2022, unless otherwise indicated. This AIF is dated March 30, 2023.

Additional Information

Additional information is provided in the Company’s

audited consolidated financial statements for the years ended December 31, 2022 and 2021 (the “2022 Annual Financial Statements”)

and Management’s Discussion and Analysis dated March 15, 2023 for the year ended December 31, 2022 (the “2022 Annual MD&A”),

each of which has been filed on the Company’s profile on the System for Electronic Document Analysis and Retrieval (“SEDAR”)

(www.sedar.com). Additional information, including directors’ and officers’ remuneration and indebtedness and information

concerning the principal holders of the Company’s securities, and securities authorized for issuance under equity compensation plans,

where applicable, will be contained in the Company’s Management Information Circular to be filed in connection with its upcoming

annual meeting of shareholders for 2023 (the “2023 Circular”). This information, including the 2022 Annual MD&A and the

2022 Annual Financial Statements, and other additional information relating to the Company may be found in the Company’s public filings

with provincial securities regulatory authorities which can be found on the Company’s profile on the SEDAR website at www.sedar.com and

with the U.S. Securities and Exchange Commission (the “SEC”) on the Electronic Data-Gathering, Analysis and Retrieval (“EDGAR”)

website at www.sec.gov/edgar.html or, in the case of the 2023 Circular, will be made available in accordance with the time requirements

of Canadian and U.S. securities laws.

Non-GAAP and Other Financial Measures

The Company has included certain non-GAAP and

other financial measures, which the Company believes, that together with measures determined in accordance with IFRS, provide investors

with an improved ability to evaluate the underlying performance of the Company. Non-GAAP financial measures do not have any standardized

meaning prescribed under IFRS, and therefore they may not be comparable to similar non-GAAP and other financial performance measures employed

by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute

for measures of performance prepared in accordance with IFRS.

Reconciliations and descriptions can be found

under the heading “Non-GAAP and Other Financial Measures” of the 2022 MD&A, which section is incorporated by reference

herein and is available on SEDAR at www.sedar.com.

Interpretation and

Definitions

A glossary of certain technical terms, abbreviations

and measurement conversions is set forth in Appendix A.

***

Currency and Exchange Rate

Unless otherwise indicated, in this AIF all references

to “dollar” or the use of the symbol “$” are to the United States dollar and all references to “C$”

are to the Canadian dollar. The daily average exchange rate for Canadian dollars in terms of the United States dollar on December 31,

2022 and March15, 2023 as reported by the Bank of Canada was 1.3544 and 1.3778, respectively. The daily average exchange rate for Canadian

dollars in terms of the Mexican peso on December 31, 2022 and March 15, 2023 as reported by the Bank of Canada was 0.06949 and 0.07264,

respectively.

United

States Dollars into Canadian Dollars | |

2022 | | |

2021 | | |

2020 | |

| Closing | |

| 1.3544 | | |

| 1.2678 | | |

| 1.2732 | |

| Average | |

| 1.3011 | | |

| 1.2535 | | |

| 1.3415 | |

| High | |

| 1.3856 | | |

| 1.2942 | | |

| 1.4496 | |

| Low | |

| 1.2451 | | |

| 1.2040 | | |

| 1.2718 | |

| Mexican Pesos into Canadian Dollars | |

2022 | | |

2021 | | |

2020 | |

| Closing | |

| 0.06949 | | |

| 0.06209 | | |

| 0.06404 | |

| Average | |

| 0.06471 | | |

| 0.06181 | | |

| 0.06267 | |

| High | |

| 0.07070 | | |

| 0.06477 | | |

| 0.07140 | |

| Low | |

| 0.06021 | | |

| 0.05856 | | |

| 0.05653 | |

Forward-Looking

Statements

Statements contained in this AIF of the Company

that are not current or historical factual statements may constitute “forward-looking information” or “forward-looking

statements” within the meaning of applicable Canadian and United States securities laws (“forward-looking statements”).

These forward-looking statements are presented for the purpose of assisting the Company’s securityholders and prospective investors in

understanding management’s views regarding those future outcomes and may not be appropriate for other purposes. When used in this AIF,

the words “may”, “would”, “could”, “will”, “intend”, “plan”, “anticipate”,

“believe”, “seek”, “propose”, “estimate”, “expect”, and similar expressions, as they

relate to the Company, are intended to identify forward-looking statements. All such forward-looking statements are subject to important

risks, uncertainties and assumptions. These statements are forward-looking because they are based on current expectations, estimates and

assumptions. It is important to know that: (i) unless otherwise indicated, forward-looking statements in this AIF describe expectations

as at the date hereof; and (ii) actual results and events could differ materially from those expressed or implied. Capitalized terms used

but not defined in this “Forward-Looking Statements” section of this AIF shall have the meaning ascribed to such term elsewhere

in this AIF.

Specific forward-looking statements in this AIF

include, but are not limited to: any objectives, expectations, intentions, plans, results, levels of activity, goals or achievements;

estimates of mineral reserves and resources; the realization of mineral reserve estimates; the impairment of mining interests and non-producing

properties; the timing and amount of estimated future production, production guidance, costs of production, capital expenditures, costs

and timing of development; the success of exploration and development activities; the Company’s test work (and receipt of the

results thereof), production, development plans and performance expectations at the Relief Canyon mine and its ability to operate, finance,

develop and operate Relief Canyon, including the timing and conclusions of the technical studies, data compilation and analysis occurring

at Relief Canyon and the potential for reassessment of the remaining carrying value of the Relief Canyon asset; statements regarding the

Galena Complex Recapitalization Plan, including with respect to completion of the Galena hoist project on its expected schedule and updated

budget, and the realization of the anticipated benefits therefrom; Company’s Cosalá Operations, including expected production levels;

the ability of the Company to target higher-grade silver ores at the Cosalá Operations; statements relating to the future financial

condition, assets, liabilities (contingent or otherwise), business, operations or prospects of the Company; material uncertainties that

may impact the Company’s liquidity in the short term; changes in accounting policies not yet in effect; permitting timelines; government

regulation of mining operations; environmental risks; labour relations, employee recruitment and retention, and pension funding and valuation;

the timing and possible outcomes of pending disputes or litigation; negotiations or regulatory investigations; exchange rate fluctuations;

cyclical or seasonal aspects of the Company’s business; the Company’s dividend policy; the liquidity of the Company’s

common shares; and other events or conditions that may occur in the future. Inherent in the forward-looking statements are known and unknown

risks, uncertainties and other factors beyond the Company’s ability to control or predict that may cause the actual results, performance

or achievements of the Company, or developments in the Company’s business or in its industry, to differ materially from the anticipated

results, performance, achievements or developments expressed or implied by such forward-looking statements.

Some of the risks and other factors (some of which

are beyond Americas Gold and Silver’s control) that could cause results to differ materially from those expressed in the forward-looking

statements and information contained in this AIF include, but are not limited to: risks associated with market fluctuations in commodity

prices; risks associated with generally elevated inflation; risks related to changing global economic conditions and market volatility,

risks relating to geopolitical instability, political unrest, war, and other global conflicts may result in adverse effects on macroeconomic

conditions, including volatility in financial markets, adverse changes in trade policies, inflation, supply chain disruptions, any or

all of which may affect the Company’s results of operations and financial condition; the Company’s dependence on the success of

its Cosalá Operations, including the San Rafael project, and the Galena Complex, which are exposed to operational risks and other

risks, including certain development and exploration related risks, as applicable; risks related to mineral reserves and mineral resources,

development and production and the Company’s ability to sustain or increase present production; risks related to global financial and

economic conditions; risks related to government regulation and environmental compliance; risks related to mining property claims and

titles, and surface rights and access; risks related to labour relations, disputes and/or disruptions, employee recruitment and retention

and pension funding and valuation; some of the Company’s material properties are located in Mexico and are subject to changes in political

and economic conditions and regulations in that country; risks related to the Company’s relationship with the communities where it operates;

risks related to actions by certain non-governmental organizations; substantially all of the Company’s assets are located outside of Canada,

which could impact the enforcement of civil liabilities obtained in Canadian and U.S. courts; risks related to currency fluctuations that

may adversely affect the financial condition of the Company; the Company may need additional capital in the future and may be unable to

obtain it or to obtain it on favourable terms; risks associated with the Company’s outstanding debt and its ability to make scheduled

payments of interest and principal thereon; risks associated with any hedging activities of the Company; risks associated with the Company’s

business objectives; risks relating to mining and exploration activities and future mining operations; operational risks and hazards inherent

in the mining industry; risks related to competition in the mining industry; risks relating to negative operating cash flows; risks relating

to the possibility that the Company’s working capital requirements may be higher than anticipated and/or its revenue may be lower

than anticipated over relevant periods; and risks relating to climate change and the legislation governing it.

The list above is not exhaustive of the factors

that may affect any of the Company’s forward-looking statements. Investors and others should carefully consider these and other factors

and not place undue reliance on the forward-looking statements. The forward-looking statements contained in this AIF represent the Company’s

views only as of the date such statements were made. Forward-looking statements contained in this AIF are based on management’s plans,

estimates, projections, beliefs and opinions as at the time such statements were made and the assumptions related to these plans, estimates,

projections, beliefs and opinions may change. Although forward-looking statements contained in this AIF are based on what management considers

to be reasonable assumptions based on information currently available to it, there can be no assurances that actual events, performance

or results will be consistent with these forward-looking statements, and management’s assumptions may prove to be incorrect. Some of the

important risks and uncertainties that could affect forward-looking statements are described further in this AIF. The Company cannot guarantee

future results, levels of activity, performance or achievements, should one or more of these risks and uncertainties materialize, or should

underlying assumptions prove incorrect, the actual results or developments may differ materially from those contemplated by the forward-looking

statements. The Company does not undertake to update any forward-looking statements, even if new information becomes available, as a result

of future events or for any other reason, except to the extent required by applicable securities laws.

Cautionary Note to Investors in the United

States Regarding Resources and Reserves

This AIF has been prepared in accordance with

the requirements of the securities laws in effect in Canada, which differ from the requirements of United States securities laws. The

Company’s mineral reserves and mineral resources have been calculated in accordance with National Instrument 43-101 – Standards

of Disclosure for Mineral Projects (“NI 43-101”), as required by Canadian securities regulatory authorities. These standards

differ from the requirements of the SEC that are applicable to domestic United States reporting companies. Accordingly, information in

this AIF that describes the Company’s mineral reserves and mineral resources may not be comparable to information made public by United

States companies subject to the SEC’s reporting and disclosure requirements.

***

CORPORATE STRUCTURE

Name, Address and

Incorporation

Americas Gold and Silver was incorporated as Scorpio

Mining Corporation (“Scorpio Mining”) pursuant to articles of incorporation dated May 12, 1998, under the Canada Business

Corporations Act with authorized share capital of an unlimited number of common shares (the “Common Shares”). On December

23, 2014, a merger of equals transaction between Scorpio Mining and U.S. Silver & Gold Inc. (“U.S. Silver”) was completed

to combine their respective businesses by way of a plan of arrangement of U.S. Silver pursuant to section 182 of the Business Corporations

Act (Ontario). Following the merger of equals, the combined company changed its name to Americas Silver Corporation (“Americas

Silver”) by way of articles of amendment dated May 19, 2015. On April 1, 2019, Americas Silver amended its articles to create a

new class of non-voting preferred shares in the capital of Americas Silver, in connection with its acquisition of Pershing Gold Corporation

(“Pershing Gold”) pursuant to a plan of merger under Nevada law (the “Pershing Gold Transaction”), which was completed

on April 3, 2019. Following the completion of the Pershing Gold Transaction, the Company changed its name to “Americas Gold and

Silver Corporation” pursuant to articles of amendment dated effective September 3, 2019. The Company’s principal and registered

office is located at 145 King Street West, Suite 2870, Toronto, Ontario, Canada M5H 1J8.

The Common Shares trade on the Toronto Stock Exchange

(the “TSX”) under the symbol “USA” and on the NYSE American under the symbol “USAS”.

Inter-Corporate

Relationships

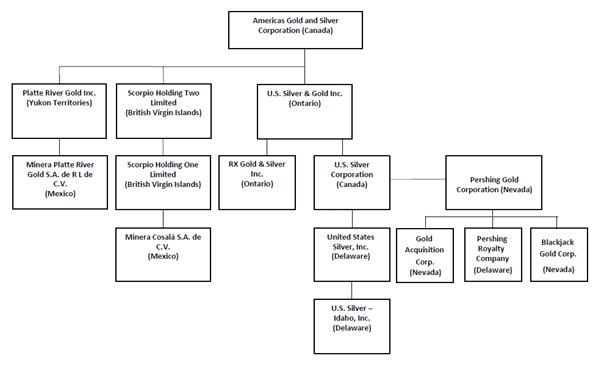

The organizational chart below indicates the inter-corporate relationships between the Company and its material subsidiaries

(and includes their jurisdiction of organization) as of the date hereof. Unless otherwise indicated, all such subsidiaries are wholly

owned.

GENERAL DEVELOPMENT OF THE

BUSINESS

Overview

The Company is a precious metals producer with

two operations in the world’s leading silver mining regions: the Galena Complex in Idaho, USA and the “Cosalá Operations”

in Sinaloa, Mexico. The Company is also advancing technical studies at the Relief Canyon mine (“Relief Canyon”) in Nevada,

USA following a suspension of mining activities in August 2021.

In Idaho, USA, the Company operates the 60% owned

producing Galena Complex (40% owned by Mr. Eric Sprott (“Sprott”)) whose primary assets are the operating Galena mine, the

Coeur mine, and the contiguous Caladay development project in the Coeur d’Alene Mining District of the northern Idaho Silver Valley.

The Galena Complex has recorded production of over 230 million ounces of silver along with associated by-product metals of copper and

lead over a production history of more than sixty years. The Company entered into a joint venture agreement (the “Joint Venture

Agreement”) with Sprott effective October 1, 2019 for a 40% non-controlling interest of the Galena Complex with an initial contribution

of $15 million to fund capital improvements. The goal of the joint venture agreement is to position the Galena Complex to significantly

grow resources, increase production, and reduce operating costs at the mine (the “Recapitalization Plan”).

In Sinaloa, Mexico, the Company operates the 100%-owned

Cosalá Operations, which includes the San Rafael silver-zinc-lead mine (“San Rafael”), after declaring commercial production

in December 2017. Prior to that time, it operated the Nuestra Señora silver-zinc-copper-lead mine after commissioning the Los Braceros

processing facility and declaring commercial production in January 2009. The Cosalá area land holdings also host several other

known precious metals and polymetallic deposits, past-producing mines, and development projects including the Zone 120 silver-copper deposit

and the El Cajón silver-copper deposit. These properties are located in close proximity to the Los Braceros processing plant. The

Company restarted the Cosalá Operations in Q4-2021 following the signing of an accord with the SNM Union and witnessed by the Mexican

Ministries of Economy, Interior and Labour on July 6, 2021. The Company also owns a 100% interest in the San Felipe development project

in Sonora, Mexico, which it acquired on October 8, 2020.

In Nevada, USA, the Company is advancing technical

studies at the 100%-owned, Relief Canyon located in Pershing County. The mine poured its first gold in February 2020 and declared commercial

production in January 2021. Operations were suspended in August 2021 in order to resolve technical challenges related to the metallurgical

characteristics of the deposit. The project includes three historic open-pit mines, a newly constructed crushing and ore conveying

system, leach pads, and a refurbished heap leach processing facility. The landholdings at Relief Canyon and the surrounding area cover

over 11,700 hectares, providing the Company the potential to expand the Relief Canyon deposit and to explore for new discoveries close

to existing processing infrastructure.

The Company’s mission is to profitably expand

its precious metals production through the development of its own projects and consolidation of complementary projects. The Company is

also focused on extending the mine life of its current assets through exploration and charting a path to profitability at the Galena Complex

with the Recapitalization Plan, as well as resolving technical challenges at Relief Canyon. The Company will continue exploring and evaluating

prospective areas accessible from existing infrastructure and the surface at the Galena Complex, and early-stage targets with an emphasis

on the Cosalá District.

The Company’s management and Board of Directors

(the “Board”) are comprised of senior mining executives who have extensive experience identifying, acquiring, developing,

financing, and operating precious metals deposits globally. The Company’s principal and registered office is located at 145 King

Street West, Suite 2870, Toronto, Ontario, Canada, M5H 1J8. The Company is a reporting issuer in each of the provinces of Canada and is

listed on the TSX trading under the symbol “USA” and on the NYSE American trading under the symbol “USAS”.

Three Year History

Fiscal 2020

On January 16, 2020, the Company entered into

a precious metals delivery and purchase agreement with Macquarie Bank Ltd. (“Macquarie”) for working capital purposes at Relief

Canyon. The $5 million advance was to be initially settled through fixed deliveries of gold production from Relief Canyon during the second

half of 2020. On July 31, 2020, the Company and Macquarie amended this agreement and converted the delivery schedule to a $7.2 million

loan to be repaid in equal monthly installments of $1.2 million over a six-month period commencing at the end of October 2020, among other

terms. This obligation was repaid during fiscal 2021.

On February 3, 2020, the Company announced that

a group of individuals had illegally blockaded access to facilities at the Cosalá Operations and because of such illegal blockade

there was a halt in mining and processing operations. The Company filed the applicable legal motions including criminal actions and engaged

with Mexican government officials at the state and federal levels to uphold the rule of law and safely remove the illegal blockade to

ensure the security of the operations.

On February 18, 2020, the Company announced that

first gold production at the Relief Canyon mine had been achieved on February 17, 2020, approximately nine months after the formal commencement

of construction in mid-May 2019.

On February 18, 2020, the Company announced that

it had entered into an at-the-market offering agreement (the “2020 ATM Agreement”), with H.C. Wainwright & Co. LLC, acting

as the lead agent, and Roth Capital Partners, LLC, as agent, pursuant to which the Company established an at-the-market equity program

(the “2020 ATM Offering”). Pursuant to the 2020 ATM Offering, the Company sold, through the lead agent, approximately 9.0

million Common Shares at an average price per share of $1.66, for gross proceeds of approximately $15 million.

On March 31, 2020, the Government of Mexico declared

a national health emergency with extraordinary measures due to the COVID-19 pandemic and instituted a national COVID-19 related decree

for the temporary suspension of all non-essential businesses in the country, including all mining activities, until April 30, 2020 (later

extended to May 31, 2020). The Company’s efforts at resolving the illegal blockade were prolonged by the temporary closure of Mexican

government offices.

On May 11, 2020, the Company received approximately

$4.5 million in loans through the Paycheck Protection Program from the U.S. CARES Act to assist with payroll and other expenses at the

Galena Complex during the COVID-19 pandemic. The Company received confirmation via a letter dated March 31, 2022 from the U.S. Small Business

Administration that $4.3 million of the loans were forgiven. The Company has filed an appeal under the Paycheck Protection Program for

the remaining $0.2 million of loans and is awaiting details on timing of repayment of the amount.

On May 13, 2020, the Company completed a bought

deal public offering of 10,269,500 Common Shares at a price of C$2.80 per share for aggregate gross proceeds of approximately $20.4 million

(C$28.75 million), which included the exercise by the underwriters, in full of the over-allotment option granted by the Company to the

underwriters. The net proceeds were used to advance development at Relief Canyon towards commercial production, care and maintenance at

the Cosalá Operations, debt repayments, and working capital and other general corporate purposes. Strategic investors led by Mr.

Pierre Lassonde and Mr. Eric Sprott subscribed to approximately C$8.75 million of the bought deal public offering.

On July 8, 2020, the Company completed the outstanding

option acquisition agreement for the San Felipe property located in Sonora, Mexico, with Minera Hochschild Mexico S.A. de C.V. (“Hochschild”)

where the Company agreed to issue to Hochschild 1,687,401 Common Shares with a value equal to the outstanding payment of $3.75 million

plus VAT using the 5-day volume-weighted average price on the TSX as of the date of the parties’ agreement (and for which the Company

obtained price protection from the TSX pursuant to its rules), subject to adjustment in certain circumstances. On October 8, 2020, the

Company issued the shares to Hochschild and closed the acquisition of the San Felipe property.

On September 4, 2020, the Company completed a

bought deal public offering of 10,204,510 Common Shares at a price of C$3.86 per share for aggregate gross proceeds of approximately $29.8

million (C$39.39 million), which included the partial exercise by the underwriters of the over-allotment option granted by the Company

to the underwriters. The net proceeds were used to advance development at Relief Canyon towards commercial production, care and maintenance

at the Cosalá Operations, debt repayments, and working capital and other general corporate purposes.

On September 14, 2020, the Company announced a

significant increase to the Galena Complex mineral resource. Based on only 33% of planned Phase 1 exploration drilling as part of the

Recapitalization Plan, measured and indicated silver resources, as of June 30, 2020, increased from 27.4 million ounces to 37.3 million

ounces and inferred silver resources increased from 39.0 million ounces to 78.6 million ounces. This increase represents a 36% and 101%

increase, respectively, from previous reported estimates that will be updated in due course. The Company also provided updates on the

progress of the Recapitalization Plan throughout the year resulting in the rehabilitation of existing infrastructure, a reduction in operating

costs and higher year-over-year production of silver and lead.

Further to the Sandstorm Financing entered into

in 2019, in consideration with the Relief Canyon Project, the Company issued a $5 million promissory note to Sandstorm on December 15,

2020 due June 15, 2022, with interest payable at 7% per annum and repayable at the Company’s option prior to maturity.

Fiscal 2021

On January 11, 2021, the Company announced that

Relief Canyon had declared commercial production effective that day with the sustained operation of the large radial stacker which satisfied

the required stacking rates following first gold pour in February 2020.

On January 29, 2021, the Company completed a bought

deal public offering of 10,253,128 Common Shares at a price of C$3.31 per share for aggregate gross proceeds of approximately $26.7 million

(C$33.94 million), which included the partial exercise by the underwriters of the over-allotment option granted by the Company to the

underwriters for the offering. The net proceeds were used for working capital purposes at Relief Canyon, development and exploration at

the Galena Complex, care and maintenance at the Cosalá Operations, debt repayments, and working capital and other general corporate

purposes.

On February 1, 2021, Sandstorm converted $5 million

of the principal amount of the Company’s $10 million outstanding convertible debenture into an aggregate of 2,336,448 Common Shares

at a conversion price of $2.14. On March 3, 2021, Sandstorm converted the remaining $5 million principal amount of the outstanding convertible

debenture into an aggregate of 2,336,448 Common Shares at the same conversion price.

On April 29, 2021, the Company issued a C$12.5

million secured convertible debenture to Royal Capital Management Corp. (“RoyCap”) due April 28, 2024 (the “2024 Convertible

Debenture”) with interest payable at 8% per annum, repayable at the Company’s option prior to maturity subject to payment

of a redemption premium, and convertible into Common Shares at the holder’s option at a conversion price of C$3.35. The 2024 Convertible

Debenture is secured by the Company’s interest in the Galena Complex and by shares of one of the Company’s Mexican subsidiaries.

The net proceeds raised from the 2024 Convertible Debenture were used in connection with capital requirements relating to the reopening

of the Cosalá Operations, repayment of shorter-term debt obligations, the ramp-up at Relief Canyon and for working capital purposes.

On May 17, 2021, the Company announced that because

of the differences observed between the modelled (planned) and mined (actual) ore tonnage and the carbonaceous material identified in

the early phases of the mine plan, an impairment charge of $55.6 million has been taken in Q1-2021, reducing the carrying value of the

Relief Canyon mineral interest, and property, plant, and equipment. An additional reduction of $23.0 million was taken to inventory in

Q1-2021 because of the decreased recovery expected from gold ounces already placed on the leach pad.

On May 17, 2021, the Company announced it had

entered into an at-the-market offering agreement (the “ATM Agreement”) with H.C. Wainwright & Co. LLC, acting as the lead

agent, and Roth Capital Partners, LLC, as agent, pursuant to which the Company established an at-the-market equity program for aggregate

gross proceeds to the Company of up to $50.0 million (the “ATM Program”). As of February 28, 2023, the date the ATM Program

terminated, approximately 44.1 million Common Shares were sold pursuant to the ATM Program with an average price per share of approximately

$1.01 for gross proceeds of approximately $44.4 million.

On July 7, 2021, the Company announced that it

had signed an agreement with the federal Mexican Ministries of Economy, Interior and Labour committing along with certain union representatives

to a reopening at the Cosalá Operations shut since early 2020 by the illegal blockade.

In July 2021, the Company was served with a statement

of claim filed in the Ontario Superior Court of Justice to commence a proposed class action lawsuit against the Company and its Chief

Executive Officer (the “Securities Action”). Pursuant to the Securities Action, the representative plaintiff sought damages

of C$130 million in relation to the Company’s public disclosure concerning its Relief Canyon mine. The

Company believed that the complaint against it was unfounded and without merit. In November 2022 the Securities Action was fully and finally

dismissed.

On August 13, 2021, the Company and the Board

of Directors temporarily suspended mining operations at Relief Canyon while continuing leaching operations and ongoing technical studies

in order to prioritize capital for the Cosalá Operations re-opening and the Galena hoist replacement.

On September 8, 2021, the Company provided an

updated Mineral Reserve and Resource statement as at June 30, 2021. With Phase 1 drilling of Galena’s Recapitalization Plan complete,

there was a 38% increase in proven and probable silver mineral reserve at the Galena Complex from 12.0 million silver ounces to 16.6 million

silver ounces year-over-year on a 100% basis. On a consolidated and attributable basis, estimated contained metal in the proven and probable

mineral reserve (“P&P”) categories totalled 32.5 million ounces of silver, 139.9 million pounds of zinc, 114.3 million

pounds of lead and 30.2 million pounds of copper. Estimated contained metal in the measured and indicated mineral resource (“M&I”)

categories totalled 72.2 million ounces of silver, 584 thousand ounces of gold, 804.5 million pounds of zinc, 725.4 million pounds of

lead and 34.4 million pounds of copper.

On October 21, 2021, the Company closed a non-brokered

private placement with Sandstorm for gross proceeds of $2.5 million through issuance of approximately 3.3 million of the Common Shares

priced at approximately C$0.94 per share. The proceeds will be used for general corporate purposes including the reopening of the Cosalá

Operations and the Recapitalization Plan.

On November 12, 2021, the Company amended its

existing 2024 Convertible Debenture by increasing the principal balance by C$6.3 million to a total principal balance of C$18.8 million,

in addition to amending its conversion price of C$3.35 to C$1.48 (based on a 35% premium to the 5-day VWAP), and the terms to its Retraction

Option from a retraction of C$0.3 million cumulative per month to a retraction of C$0.45 million cumulative per month. All other material

terms of the 2024 Convertible Debenture remain unchanged. The net proceeds raised will be used for the reopening of the Cosalá

Operations and working capital purposes. During 2021, the 2024 Convertible Debenture was reduced to C$17.9 million through partial retractions

by RoyCap for C$0.9 million settled through issuance of approximately 0.8 million of the Common Shares. As of March 17, 2022, the 2024

Convertible Debenture was further reduced to C$16.8 million through partial retractions by RoyCap for C$1.1 million settled through issuance

of approximately 1.1 million of the Common Shares.

In December 2021 the Cosalá Operations

resumed commercial production following the signing of an accord with a Mexican labour union signed by the Mexican Ministries of Economy,

Interior and Labour in July 2021 and recalling workers in September 2021. The Los Braceros mill ramped up to nameplate production in December

2021. Concentrate shipments resumed with a return to revenue and cash flow generation in Q4-2021.

Fiscal 2022

On January 10, 2022, the Company provided a production

update for the Cosalá Operations following the Q4-2021 re-opening. Initial production was to focus on mining high-grade zinc areas

of the Main Zone which were fully developed prior to the illegal blockade. Over the course of the first six months, the mine continued

development into the Upper Zone, which carries silver grades approximately 5-6 times higher than the Main Zone with an expected increase

in silver production to over 2.5 million ounces of silver on an annualized basis.

On January 24, 2022, the Company hosted the official

opening ceremony for the Cosalá Operations which was attended by the Mexican Minister of Economy, the Governor of the State of

Sinaloa and the Cosalá Mayor.

During fiscal 2022, the Company closed quarterly

non-brokered private placements with Sandstorm Gold Ltd. (“Sandstorm”) for total gross proceeds of $9.9 million through issuance

of approximately 15.2 million of the Company’s common shares priced at approximately C$0.85 per share on average.” The private

placements disclosed here appear to total more than $9.9 million.

On September 13, 2022, the Company provided an

updated Mineral Reserve and Resource statement as at June 30, 2022. At the Galena Complex, mineral reserves were successfully increased

as part of the Phase 2 infill drill program. There was a 26% increase in proven and probable silver mineral reserve at the Galena Complex

to approximately 4.3 million ounces year-over-year on a 100% basis. On a consolidated and attributable basis, estimated contained metal

in the P&P mineral reserve categories totalled 6.5 million ounces of silver, 43.1 million pounds of zinc, 44.0 million pounds of lead

and 1.1 million pounds of copper. Estimated contained metal in the M&I mineral resource categories totalled 15.9 million ounces of

silver, 352 thousand ounces of gold, 83.3 million pounds of zinc, 113.0 million pounds of lead and 4.1 million pounds of copper.

On October 20, 2022, the Company amended the RoyCap

Convertible Debenture by increasing the principal balance by $7.0 million CAD to a total outstanding principal of $25.8 million CAD, in

addition to amending its interest rate of 8% per annum to 9.5% per annum, its conversion price of $1.48 CAD to $1.00 CAD, and the terms

to its Retraction Option retractable at a cumulative $0.45 million CAD per month to a cumulative $0.5 million CAD per month with a beginning

cumulated retraction balance of $1.5 million CAD.

On November 30, 2022, the Company announced that

the Ontario Superior Court of Justice had ruled the putative class action lawsuit brought against the Company and its Chief Executive

Officer in the summer of 2021 cannot proceed. In its decision, the Court dismissed the Plaintiff’s motion for leave to commence

a secondary market claim under the Ontario Securities Act. The Court found that the plaintiff failed to present credible evidence

to establish a reasonable possibility that the action will be resolved in the plaintiff’s favour. As

the plaintiffs agreed not to appeal, the decision brought this proposed class action to an end.

On November 30, 2022, the Company announced that

the Galena Complex and its unionized workers ratified a new 3-year collective bargaining agreement effective November 17, 2022. Unionized

workers at the Cosalá Operations also had recently ratified a collective bargaining agreement effective May 1, 2022. These agreements

support continued stable operations during a period of forecasted production growth.

Sustainability Performance

In March 2021, the Company released its first

sustainability report for the Cosalá Operations, “Working Towards Sustainability.” This report focused on the Company’s

Environmental, Social, and Governance (ESG) strategy, management, policies, and performance at the Cosalá Operations between January

1, 2018, and January 31, 2020, highlighting overall the Company’s commitment to the mining industry in Mexico and to the Cosalá

community in Sinaloa. The Company’s disclosure in this report was centered on the five key pillars of its corporate responsibility

strategy, including governance and business ethics, our people, health and safety, environmental stewardship, and community involvement.

The Company also affirmed its commitment to make annual sustainability reporting a key component of its ongoing sustainability strategy.

In accordance with best business practices, the report accounted for the Company’s fulfillment of its labour commitments, as well

as the environmental, social, safety, and economic impacts in the community where the Cosalá Operations are located.

In June 2022, the second sustainability

report for the Cosalá Operations, “Commitment to Sustainability” was released covering the period from January 1,

2021 to December 31, 2021. The report stated that while there was limited information disclosed due to the illegal blockade which

halted operations until the end of Q4 2022, it included information regarding the restarting of the operations and also highlighted

the support provided by the Mexican and Canadian governments along with the Company’s employees to reopen the operations at

Cosalá. The report also focused on the Company’s ESG strategies and the reaffirmation of its commitment to continue

working within a framework of responsible mining that contributes to the growth of the community through employment and local

procurement.

As part of the Company’s commitment to make

annual sustainability reporting a key component of its ongoing sustainability strategy, this year’s report is expected to be posted

by the end of May 2023. In addition, the Company plans to document and review the sustainability results at its other operations in the

coming years.

Key highlights of the Company’s ESG performance

at the Cosalá Operations and the full text of the reports are available on the Company’s website. The content of the Company’s

website and information accessible through the website do not form part of this AIF.

***

DESCRIPTION OF THE BUSINESS

Summary

The Company is engaged in the evaluation, acquisition,

exploration, development and operation of precious metals and polymetallic mineral properties, primarily those already producing or with

the potential for near-term production. The Company’s geographic focus is the Western Hemisphere, particularly the United States

and Mexico. The Company owns and operates the Cosalá Operations in Sinaloa, Mexico and manages the 60%-owned

Galena Complex in Idaho, U.S.A. The Company also owns the Relief Canyon mine in Nevada, U.S.A. and the San Felipe property in Sonora,

Mexico.

Principal Product

The Company produces silver-bearing zinc and lead

concentrates. The Company believes that because of the availability of alternate processing and commercialization options for its concentrates,

it is not dependent on a particular purchaser with regard to the sale of its products.

Production

The Company operates the 60% owned Galena Complex

located near the town of Wallace in the State of Idaho, U.S.A., and the 100%-owned Cosalá Operations located near the town of Cosalá

in the State of Sinaloa, Mexico.

The Galena Complex produces a silver-lead concentrate.

Ore mined at the Galena Complex is milled at the Galena mill. The Galena mill has an installed milling capacity of 630 tonnes-per-day.

The 450 tonne-per-day capacity Coeur mill is currently on care and maintenance.

The high grade and “narrow vein” nature

of the underground Galena Complex requires careful application of selective mining techniques such as overhand cut and fill. As well,

the age and expanse of the underground infrastructure demands regular, ongoing maintenance. As such, production and operating costs will

display a degree of variability depending on a number of timing and other factors. Substantial resources exist outside of the defined

reserve, and exploration continues to develop resources and identify new areas of mineralization. A multi-year Recapitalization Plan began

in mid-October 2019 and will conclude with commissioning of the Galena Hoist in mid-2023. Other investments have included mine development,

new equipment purchases and exploration to define and expand silver resources.

Ore at the Cosalá Operations is produced

from the San Rafael mine and treated at the Los Braceros process plant. San Rafael is an underground silver-zinc-lead mine which entered

commercial production in December 2017. The Los Braceros process plant, located 9 kilometers east southeast of the San Rafael mine, produces

silver-bearing zinc and lead concentrates. The facility processes approximately 1,700 tonnes per day.

Commercial production at San Rafael was declared

in 2017. An illegal blockade at the Cosalá Operations caused mining and processing to be suspended from Q1 2020 to Q4 2021 while

the Company worked to resolve the issue. The Cosalá Operations produced continuously through 2022.

***

Consolidated Results and Developments

| Fiscal Year Ended December 31 | |

| 2022 | | |

| 20211,5 | | |

| 20201 | |

| Revenues ($ M) | |

$ | 85.0 | | |

$ | 45.0 | | |

$ | 27.9 | |

| Net Loss ($ M) | |

| (45.2 | ) | |

| (160.6 | ) | |

| (30.1 | ) |

| Comprehensive Loss ($ M) | |

| (38.6 | ) | |

| (159.8 | ) | |

| (33.2 | ) |

| | |

| | | |

| | | |

| | |

| Net Loss per Common Share - Basic and Diluted | |

$ | (0.23 | ) | |

$ | (1.11 | ) | |

$ | (0.24 | ) |

| | |

| | | |

| | | |

| | |

| Silver Produced (oz) | |

| 1,308,201 | | |

| 61,001 | | |

| 39,117 | |

| Zinc Produced (lbs) | |

| 39,319,795 | | |

| 4,164,185 | | |

| 3,221,744 | |

| Lead Produced (lbs) | |

| 24,606,674 | | |

| 1,672,806 | | |

| 1,203,720 | |

| Cost of Sales/Ag Eq Oz Produced ($/oz)2,3,4 | |

$ | 9.89 | | |

$ | 7.47 | | |

$ | 7.19 | |

| Cash Cost/Ag Oz Produced ($/oz)2,3,4 | |

$ | 0.77 | | |

$ | (18.53 | ) | |

$ | (11.32 | ) |

| All-In Sustaining Cost/Ag Oz Produced ($/oz)2,3,4 | |

$ | 9.64 | | |

$ | (14.67 | ) | |

$ | (0.83 | ) |

| | |

| | | |

| | | |

| | |

| Cash ($ M) | |

$ | 2.0 | | |

$ | 2.9 | | |

$ | 4.7 | |

| Receivables ($ M) | |

| 11.6 | | |

| 8.2 | | |

| 5.1 | |

| Inventories ($ M) | |

| 8.8 | | |

| 17.9 | | |

| 9.4 | |

| | |

| | | |

| | | |

| | |

| Property, Plant and Equipment ($ M) | |

$ | 161.3 | | |

$ | 177.9 | | |

$ | 259.3 | |

| | |

| | | |

| | | |

| | |

| Current Assets ($ M) | |

$ | 25.4 | | |

$ | 23.5 | | |

$ | 20.1 | |

| Current Liabilities ($ M) | |

| 42.1 | | |

| 45.6 | | |

| 39.0 | |

| Working Capital ($ M) | |

| (16.7 | ) | |

| (22.1 | ) | |

| (18.9 | ) |

| | |

| | | |

| | | |

| | |

| Total Assets ($ M) | |

$ | 190.8 | | |

$ | 213.4 | | |

$ | 284.8 | |

| Total Liabilities ($ M) | |

| 92.2 | | |

| 109.6 | | |

| 103.6 | |

| Total Equity ($ M) | |

| 98.6 | | |

| 103.8 | | |

| 181.2 | |

| 1 | Consolidated production results exclude the Galena Complex after Q3-2019 due to the Recapitalization Plan,

and are nil from Q2-2020 to Q3-2021 due to the Cosalá Operations being placed under care and maintenance effective February 2020

as a result of the illegal blockade. |

| 2 | Throughout this AIF, consolidated production results and consolidated operating metrics are based on the

attributable ownership percentage of each operating segment (100% Cosalá Operations and 60% Galena Complex). |

| 3 | Cost per ounce measurements during fiscal 2021 were based on operating results starting from December

1, 2021 following return to nameplate production of the Cosalá Operations. Throughout this AIF, all other production results from

the Cosalá Operations during fiscal 2021 were determined based on total production during the year. |

| 4 | This is a supplementary or non-GAAP financial measure or ratio. See “Non-GAAP and Other Financial

Measures” section in the Company’s 2022 Annual MD&A. |

| 5 | Certain fiscal 2021 amounts were adjusted through changes in accounting policies. See “Accounting

Standards and Pronouncements” in the Company’s 2022 Annual MD&A |

Consolidated operating results

from 2022 were significantly improved compared to 2021 due to the restart of mining operations at the Cosalá Operations in Q4-2021

and return to full production thereafter following the removal of the illegal blockade.

Revenue increased by $40.0

million or 89% to $85.0 million in 2022 from $45.0 million during 2021. The increase in revenue was primarily due to the restarted Cosalá

Operations with increased silver, zinc, and lead production, offset by decrease in silver and lead revenue at the Galena Complex from

lower realized metal prices during the year. The average realized silver, zinc, and lead prices1

decreased by 13%, 3%, and 1%, respectively from 2021 to 2022. The average realized silver price of $21.69/oz. for 2022 (2021 – $24.87/oz.)

is comparable to the average London silver spot price of $21.75/oz. for 2022 (2021 – $25.17/oz.).

| 1 | These are supplementary or non-GAAP financial measures or ratios. See “Non-GAAP and

Other Financial Measures” section of the Company’s 2022 Annual MD&A. |

The Company recorded a net

loss of $45.2 million for the year ended December 31, 2022 compared to a net loss of $160.6 million for the year ended December 31, 2021.

The decrease in net loss was primarily attributable to the Relief Canyon impairment charges in fiscal 2021, higher net revenue from restart

of the Cosalá Operations, lower cost of sales, lower care and maintenance costs, lower interest and financing expense, lower loss

on fair value of metals contract liability, and gain on government loan forgiveness, offset in part by higher depletion and amortization,

higher foreign exchange loss, lower gain on derivatives, and higher income tax expense. The Company significantly reduced the consolidated

monthly spend with the Relief Canyon mining suspension that contributed to the prior year’s net loss. These variances are further

discussed in the following sections.

Cosalá Operations

| | |

Fiscal

Year Ended

December 31, | |

| | |

2022 | | |

20214 | |

| Tonnes Milled | |

| 585,270 | | |

| 59,191 | |

| Silver Grade (g/t) | |

| 56 | | |

| 56 | |

| Zinc Grade (%) | |

| 3.86 | | |

| 4.09 | |

| Lead

Grade (%) | |

| 1.63 | | |

| 1.88 | |

| Silver Recovery (%) | |

| 60.9 | | |

| 57.7 | |

| Zinc Recovery (%) | |

| 78.9 | | |

| 78.1 | |

| Lead

Recovery (%) | |

| 72.8 | | |

| 68.3 | |

| Silver Produced (oz) | |

| 636,246 | | |

| 61,001 | |

| Zinc Produced (lb) | |

| 39,319,795 | | |

| 4,164,185 | |

| Lead Produced (lb) | |

| 15,318,779 | | |

| 1,672,806 | |

| Total

Silver Equivalent Produced ($/oz)1,2 | |

| 4,167,449 | | |

| 433,456 | |

| Silver Sold (oz) | |

| 607,498 | | |

| 59,897 | |

| Zinc Sold (lb) | |

| 38,063,861 | | |

| 3,721,943 | |

| Lead

Sold (lb) | |

| 15,071,390 | | |

| 1,683,233 | |

| Cost of Sales/Ag Eq Oz Produced

($/oz)2,3 | |

$ | 8.01 | | |

$ | 7.47 | |

| Cash Costs/Ag Oz Produced ($/oz)2,3 | |

$ | (19.03 | ) | |

$ | (18.53 | ) |

| All-In Sustaining Costs/Ag

Oz Produced ($/oz)2,3 | |

$ | (11.26 | ) | |

$ | (14.67 | ) |

| 1 | Throughout this AIF, silver equivalent production was calculated based on all metals production at average

realized silver, zinc, and lead prices during each respective period. |

| 2 | This is a supplementary or non-GAAP financial measure or ratio. See “Non-GAAP and Other Financial

Measures” section of the Company’s 2022 Annual MD&A. |

| 3 | Cost per ounce measurements during fiscal 2021 were based on operating results starting from December

1, 2021 following return to nameplate production of the Cosalá Operations. Throughout this AIF, all other production results from

the Cosalá Operations during fiscal 2021 were determined based on total production during the year. |

| 4 | Production results are nil for the Cosalá Operations from Q2-2020 to Q3-2021 due to it being placed

under care and maintenance effective February 2020 as a result of the illegal blockade. |

The Cosalá Operations

had a successful year in fiscal 2022 as production increased significantly following the resolution of the illegal blockade. The operations

reopened in September 2021 with commercial production re-established in December 2021. The Cosalá Operations produced approximately

636,000 ounces of silver, 39.3 million pounds of zinc and 15.3 million pounds of lead in 2022. The Los Braceros processing plant treated

585,270 tonnes with the milling rate averaging approximately 1,600 tonnes per day during 2022. Cash costs and all-in sustaining costs

were negative $19.03 per silver ounce and negative $11.26 per silver ounce, respectively, benefitting from strong zinc and lead production

and base metal prices.

Production during 2022 initially

focused on maximizing near-term free cash flow by mining high-grade zinc areas of the Main Zone which were fully developed prior to the

illegal blockade. The Company continued to focus on mining the higher-grade zinc and lower-grade silver areas of the Main Zone to maximize

revenue generated from the Cosalá Operations during the year. As a result, base metal production exceeded the upper end of the

2022 guidance range while silver production was slightly below the bottom end of the range. The second half of the fourth quarter saw

higher silver production as the mining rate increased in the higher-grade silver Upper Zone. The Company expects to see higher average

silver grades throughout fiscal 2023 as the ore from the high-grade Upper Zone is blended more consistently with Main Zone ore.

Galena Complex

| | |

Fiscal

Year Ended

December 31, | |

| | |

2022 | | |

20213 | |

| Tonnes Milled | |

| 109,246 | | |

| 119,975 | |

| Silver Grade (g/t) | |

| 328 | | |

| 271 | |

| Lead

Grade (%) | |

| 6.75 | | |

| 7.59 | |

| Silver Recovery (%) | |

| 97.3 | | |

| 96.8 | |

| Lead

Recovery (%) | |

| 95.2 | | |

| 93.3 | |

| Silver Produced (oz) | |

| 1,119,925 | | |

| 1,012,582 | |

| Lead Produced (lb) | |

| 15,479,825 | | |

| 18,724,139 | |

| Total

Silver Equivalent Produced ($/oz)1,2 | |

| 1,810,664 | | |

| 1,751,676 | |

| Silver Sold (oz) | |

| 1,107,812 | | |

| 1,029,030 | |

| Lead

Sold (lb) | |

| 15,563,193 | | |

| 19,172,490 | |

| Cost of Sales/Ag Eq Oz Produced

($/oz)2 | |

$ | 17.10 | | |

| - | |

| Cash Costs/Ag Oz Produced ($/oz)2 | |

$ | 19.51 | | |

| - | |

| All-In Sustaining Costs/Ag

Oz Produced ($/oz)2 | |

$ | 29.42 | | |

| - | |

| All-In Sustaining

Costs with Galena Recapitalization Plan/Ag Oz Produced ($/oz)2 | |

$ | 35.32 | | |

| - | |

| 1 | Throughout this AIF, silver equivalent production was calculated based on all metals production at average

realized silver, zinc, and lead prices during each respective period. |

| 2 | This is a supplementary or non-GAAP financial measure or ratio. See “Non-GAAP and Other Financial

Measures” section of the Company’s 2022 Annual MD&A. |

| 3 | Disclosure of certain operating metrics were suspended during the Galena Recapitalization Plan implementation. |

The Company announced the

strategic Joint Venture Agreement with Sprott in September 2019 to recapitalize the mining operations at the Galena Complex. The goal

of the joint venture is to position the Galena Complex to significantly grow resources, increase production, and reduce operating costs

at the mine. The strategic 60/40 joint venture has allowed the Company to take positive action: to advance development, modernize infrastructure,

purchase new mining equipment, and define and expand silver resources.

Lead production for the year

was within guidance while silver production was slightly below the lower end of the guidance range due to weaker than expected production

in late Q3-2022 due to poor quality of cemented backfill which required remedial work in the effected stopes and areas. Silver production

in December 2022 was the highest of any month during the calendar year as the operation began accessing higher grade silver stopes including

a new area on the 3700 Level which is expected to continue in 2023.

As previously noted, the Company

successfully installed the major components of the Galena hoist prior to year-end. Shaft repair will start following completion of electrical

work and commissioning. Once it becomes fully operational, the Galena hoist will increase hoisting capacity at the Galena Complex, support

plans to increase production and improve operational flexibility. Cash costs per ounce at the Galena Complex are also anticipated to decrease

with the completion of the Galena replacement hoist as the benefits of scaling economies on the existing cost base with higher grade silver

ore are realized.

Employees

As at December 31, 2022, the Company had the following

number of employees:

| | |

Galena

Complex | | |

Cosalá

Operations | | |

Relief

Canyon | | |

Corporate | | |

Total | |

| Salary | |

| 43 | | |

| 113 | | |

| 3 | | |

| 12 | | |

| 171 | |

| Hourly | |

| 194 | | |

| 228 | | |

| 12 | | |

| 0 | | |

| 434 | |

| Total | |

| 237 | | |

| 341 | | |

| 15 | | |

| 12 | | |

| 605 | |

| * | Some workers at the Galena Complex and Cosalá Operations are covered by collective

bargaining agreements. See “Changes to Contracts and Economic Dependence” also see “Risk Factors –

Labour Relations, Employee Recruitment, Retention and Pension Funding”. |

In addition, the Company, from time to time, employs

outside contractors on a fee-for-service

basis.

Specialized Skill

and Knowledge

Various aspects of the Company’s business

require specialized skills and knowledge. Such skills and knowledge include the areas of geology, drilling, metallurgy, engineering, logistical

planning and implementation of programs as well as finance and accounting and legal/regulatory compliance. While competitive conditions

exist in the industry, the Company has been able to locate and retain employees and consultants with such skills and believes it will

continue to be able to do so in the foreseeable future. See “Risk Factors – Labour Relations, Employee Recruitment, Retention

and Pension Funding”.

Competitive Conditions

Competition in the mineral exploration industry

is intense. The Company competes with other mining companies, many of which have significant financial resources and technical facilities

for the acquisition and development of, and production from, mineral interests, as well as for the recruitment and retention of qualified

employees and consultants. The ability of the Company to acquire viable mineral properties in the future will depend not only on its ability

to develop its present properties, but also on its ability to select and acquire suitable producing properties or prospects for development

or mineral exploration.

Business Cycles

The mining business is highly cyclical. The marketability

of minerals and mineral concentrates is also affected by global economic cycles. The ultimate economic viability of the Company’s

projects is related and sensitive to the market price of gold and silver as well the market price of by-products

such as zinc, lead and copper. Metal prices fluctuate widely and are affected by numerous factors such as global supply, demand, inflation,

exchange rates, interest rates, forward selling by producers, central bank sales and purchases, production, global or regional political,

economic or financial situations and other factors beyond the control of the Company.

Changes to Contracts

and Economic Dependence

The Company’s cash flow is dependent on

delivery of its ore concentrate to market. The Company’s contracts with the concentrate purchasers provide for provisional payments

based on periodic deliveries. The Company may sell its concentrate to a metal trader while it is at the smelter in order to help manage

its cash flow. The Company has not had any problems collecting payments from concentrate purchasers in a reliable and timely manner and

expects no such difficulties in the foreseeable future. However, this cash flow is dependent on continued mine production which can be

subject to interruption for various reasons including fluctuations in metal prices and concentrate shipment difficulties. Additionally,

unforeseen cessation in smelter provider capabilities could severely impact the Company’s capital resources. Although the Company

sells its concentrate to a limited number of customers, it is not economically dependent upon any one customer as there are other markets

throughout the world for the Company’s concentrate.

Environmental Protection

The Company’s mining, exploration and development

activities are subject to various federal, state and municipal laws and regulations relating to the protection of the environment, including

requirements for closure and reclamation of mining properties. In all jurisdictions where the Company operates, specific statutory and

regulatory requirements and standards must be met throughout the exploration, development and operations stages of a mining property with

regard to matters including water quality, air quality, wildlife protection, solid and hazardous waste management and disposal, noise,

land use and reclamation. Changes in any applicable governmental regulations to which the Company is subject may adversely affect its

operations. Failure to comply with any condition set out in any required permit or with applicable regulatory requirements may result

in the Company being unable to continue to carry out its activities. The impact of these requirements cannot accurately be predicted.

Management estimates costs associated with reclamation

of mining properties as well as remediation costs for inactive properties. The Company uses assumptions about future costs, including

inflation, prices, mineral processing recovery rates, production levels and capital and reclamation costs. Such assumptions are based

on the Company’s current mining plan and the best available information for making such estimates. Details and quantification of

the Company’s reclamation and closure costs are discussed in the 2022 Annual Financial Statements (see “Note 3 –

Decommissioning Provision”) and the 2022 Annual MD&A (see “Significant Accounting Estimates and Judgements –

Decommissioning Provision”). See also “Risk Factors – Government Regulation and Environmental Compliance”.

The Company is focused on strengthening monitoring,

controls and disclosure of environmental issues that affect employees and the surrounding communities. Through proactive public engagement,

the Company continues to gain a better understanding of the concerns of area-wide citizens and regulators and continues to work collaboratively

to identify the most reasonable and cost-effective measures to address the most pressing concerns.

Foreign Operations

As of the date hereof, substantially all of the

Company’s long-term assets, comprising its mineral properties, are located in Mexico and the United States.

Tax Considerations

With current operations in the United States and

Mexico, the Company is subject to the tax considerations of those jurisdictions. Certain changes to United States and Mexican tax laws

affect the Company. See “Risk Factors – Tax Considerations” and “Note 24 – Income Taxes”

of the Company’s 2022 Annual Financial Statements

The corporate income tax rate is 21% and the corporate

alternative minimum tax was repealed effective January 1, 2018. On March 27, 2020, President Trump signed into law the Coronavirus Aid,

Relief, and Economic Security Act, which included certain changes in tax law intended to stimulate the U.S. economy in light of the COVID-19

coronavirus outbreak, including temporary beneficial changes to the treatment of net operating losses, interest deductibility limitations

and payroll tax matters.

It cannot be predicted whether, when, in what

form, or with what effective dates, new tax laws may be enacted, or regulations and rulings may be enacted, promulgated or issued under

existing or new tax laws, which could result in an increase in the Company’s or investors’ tax liability or require changes

in the manner in which the Company operates in order to minimize or mitigate any adverse effects of changes in tax law or in the interpretation

thereof.

***

MINERAL RESERVE AND MINERAL

RESOURCE ESTIMATES

Americas Gold and Silver’s Mineral Reserves

and Mineral Resources have been estimated as at June 30, 2022 in accordance with definitions adopted by the Canadian Institute of Mining,

Metallurgy and Petroleum and incorporated into NI 43-101. See “Glossary of Technical Terms”.

2022 production details are provided under “Description

of the Business – Production” and in the 2022 Annual Financial Statements and the 2022 Annual MD&A.

For further detail regarding the extent to which

estimates of Mineral Reserves and Mineral Resources may be materially affected by external factors, including metallurgical, environmental,

permitting, title and other risks and relevant issues, please refer to “Risk Factors – Mineral Reserves and Resources,

Development and Production”.

***

Attributable proven and probable Mineral Reserves - June 30,2022

Silver Mineral Reservess

| | |

Proven | | |

Probable | | |

Proven and Probable | |

| Property | |

Tonnes

(kt) | | |

Grade

(g/t) | | |

Ounces (koz) | | |

Tonnes

(kt) | | |

Grade

(g/t) | | |

Ounces (koz) | | |

Tonnes

(kt) | | |

Grade

(g/t) | | |

Ounces (koz) | |

| Galena - Ag-Pb (60%) | |

| 162 | | |

| 241 | | |

| 1,261 | | |

| 465 | | |

| 252 | | |

| 3,774 | | |

| 628 | | |

| 249 | | |

| 5,034 | |

| Galena - Ag-Cu (60%) | |

| 83 | | |

| 589 | | |

| 1,575 | | |

| 269 | | |

| 681 | | |

| 5,902 | | |

| 353 | | |

| 660 | | |

| 7,477 | |

| Galena Subtotal (60%) | |

| 246 | | |

| 359 | | |

| 2,836 | | |

| 735 | | |

| 410 | | |

| 9,676 | | |

| 980 | | |

| 397 | | |

| 12,511 | |

| San Rafael | |

| 708 | | |

| 163 | | |

| 3,715 | | |

| 957 | | |

| 117 | | |

| 3,589 | | |

| 1,665 | | |

| 136 | | |

| 7,304 | |

| El Cajón | |

| - | | |

| - | | |

| - | | |

| 788 | | |

| 157 | | |

| 3,983 | | |

| 788 | | |

| 157 | | |

| 3,983 | |

| Zone 120 | |

| - | | |

| - | | |

| - | | |

| 2,052 | | |

| 165 | | |

| 10,914 | | |

| 2,052 | | |

| 165 | | |

| 10,914 | |

| Cosalá Subtotal | |

| 708 | | |

| 163 | | |

| 3,715 | | |

| 3,797 | | |

| 151 | | |

| 18,486 | | |

| 4,505 | | |

| 153 | | |

| 22,201 | |

| Total Silver | |

| 954 | | |

| 214 | | |

| 6,550 | | |

| 4,532 | | |

| 193 | | |

| 28,162 | | |

| 5,486 | | |

| 197 | | |

| 34,712 | |

Zinc Mineral Reserves

| | |

Proven | | |

Probable | | |

Proven and Probable | |

| Property | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds (Mlbs) | | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | |

| San Rafael Subtotal | |

| 708 | | |

| 2.76 | | |

| 43.1 | | |

| 957 | | |

| 3.03 | | |

| 64.0 | | |

| 1,665 | | |

| 2.92 | | |

| 107.0 | |

| Total Zinc | |

| 708 | | |

| 2.76 | | |

| 43.1 | | |

| 957 | | |

| 3.03 | | |

| 64.0 | | |

| 1,665 | | |

| 2.92 | | |

| 107.0 | |

Lead Mineral Reserves

| | |

Proven | | |

Probable | | |

Proven and Probable | |

| Property | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds (Mlbs) | | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | |

| Galena Subtotal (60%) | |

| 162 | | |

| 7.72 | | |

| 27.7 | | |

| 465 | | |

| 6.74 | | |

| 69.2 | | |

| 628 | | |

| 7.00 | | |

| 96.8 | |

| San Rafael Subtotal | |

| 708 | | |

| 1.04 | | |

| 163.3 | | |

| 957 | | |

| 1.07 | | |

| 22.6 | | |

| 1,665 | | |

| 1.06 | | |

| 38.9 | |

| Total Lead | |

| 871 | | |

| 2.29 | | |

| 44.0 | | |

| 1,422 | | |

| 2.93 | | |

| 91.8 | | |

| 2,293 | | |

| 2.69 | | |

| 135.7 | |

Copper Mineral Reserves

| | |

Proven | | |

Probable | | |

Proven and Probable | |

| Property | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | | |

Tonnes

(kt) | | |

Grade

(%) | | |

Pounds

(Mlbs) | |

| Galena Subtotal (60%) | |

| 83 | | |

| 0.61 | | |

| 1.1 | | |

| 269 | | |

| 0.73 | | |

| 4.3 | | |

| 353 | | |

| 0.70 | | |

| 5.4 | |

| El Cajón | |

| - | | |

| - | | |

| - | | |

| 788 | | |

| 0.49 | | |

| 8.5 | | |

| 788 | | |

| 0.49 | | |

| 8.5 | |

| Zone 120 | |

| - | | |

| - | | |

| - | | |

| 2,052 | | |

| 0.41 | | |

| 18.7 | | |

| 2.052 | | |

| 0.41 | | |

| 18.7 | |

| Cosalá Subtotal | |

| - | | |

| - | | |

| - | | |

| 2,840 | | |

| 0.43 | | |

| 27.2 | | |

| 2,840 | | |

| 0.43 | | |

| 27.2 | |

| Total Copper | |

| 83 | | |

| 0.61 | | |

| 1.1 | | |

| 3,109 | | |

| 0.46 | | |

| 31.5 | | |

| 3,192 | | |

| 0.46 | | |

| 32.6 | |

Attributable Measured

and Indicated Mineral Resources - June 30, 2022

Gold

Mineral Resources - Exclusive of Mineral Reserves

| | |

Measured | | |

Indicated | | |

Measured and Indicated | |

| | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | |

| Property | |

(kt) | | |

(g/t) | | |

(koz) | | |

(kt) | | |

(g/t) | | |

(koz) | | |

(kt) | | |

(g/t) | | |

(koz) | |

| Relief Canyon Subtotal | |

| 12,177 | | |

| 0.90 | | |

| 352 | | |

| 10,431 | | |

| 0.66 | | |

| 220 | | |

| 22,608 | | |

| 0.79 | | |

| 572 | |

| Total Gold | |

| 12,177 | | |

| 0.90 | | |

| 352 | | |

| 10,431 | | |

| 0.66 | | |

| 220 | | |

| 22,608 | | |

| 0.79 | | |

| 572 | |

Silver

Mineral Resources - Exclusive of Mineral Reserves

| | |

Measured | | |

Indicated | | |

Measured and Indicated | |

| | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | |

| Property | |

(kt) | | |

(g/t) | | |

(koz) | | |

(kt) | | |

(g/t) | | |

(koz) | | |

(kt) | | |

(g/t) | | |

(koz) | |

| Relief Canyon Subtotal | |

| 12,177 | | |

| 3.4 | | |

| 1,346 | | |

| 10,431 | | |

| 0.6 | | |

| 210 | | |

| 22,608 | | |

| 2.1 | | |

| 1,556 | |

| Galena - Ag-Pb (60%) | |

| 441 | | |

| 324 | | |

| 4,594 | | |

| 2,042 | | |

| 327 | | |

| 21,500 | | |

| 2,483 | | |

| 327 | | |

| 26,094 | |

| Galena - Ag-Cu (60%) | |

| 250 | | |

| 647 | | |

| 5,204 | | |

| 761 | | |

| 616 | | |

| 15,078 | | |

| 1,011 | | |

| 624 | | |

| 20,282 | |

| Galena Subtotal (60%) | |

| 691 | | |

| 441 | | |

| 9,799 | | |

| 2,803 | | |

| 406 | | |

| 36,578 | | |

| 3,494 | | |

| 413 | | |

| 46,377 | |

| San Rafael | |

| 1,508 | | |

| 85 | | |

| 4,139 | | |

| 2,277 | | |

| 67 | | |

| 4,909 | | |

| 3,785 | | |

| 74 | | |

| 9,048 | |

| Nuestra Señora | |

| 257 | | |

| 85 | | |

| 700 | | |

| 1,879 | | |

| 89 | | |

| 5,379 | | |

| 2,136 | | |

| 89 | | |

| 6,079 | |

| El Cajón | |

| - | | |

| - | | |

| - | | |

| 299 | | |

| 131 | | |

| 1,263 | | |

| 299 | | |

| 131 | | |

| 1,263 | |

| Zone 120 | |

| - | | |

| - | | |

| - | | |

| 1,470 | | |

| 114 | | |

| 5,395 | | |

| 1,470 | | |

| 114 | | |

| 5,395 | |

| Cosalá Subtotal | |

| 1,764 | | |

| 85 | | |

| 4,839 | | |

| 5,926 | | |

| 89 | | |

| 16,946 | | |

| 7,690 | | |

| 88 | | |

| 21,785 | |

| San Felipe Subtotal | |

| - | | |

| - | | |

| - | | |

| 4,677 | | |

| 61 | | |

| 9,115 | | |

| 4,677 | | |

| 61 | | |

| 9,115 | |

| Total Silver | |

| 14,632 | | |

| 34 | | |

| 15,984 | | |

| 23,837 | | |

| 82 | | |

| 62,849 | | |

| 38,469 | | |

| 64 | | |

| 78,834 | |

Zinc

Mineral Resources - Exclusive of Mineral Reserves

| | |

Measured | | |

Indicated | | |

Measured and Indicated | |

| | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | |

| Property | |

(kt) | | |

(%) | | |

(Mlbs) | | |

(kt) | | |

(%) | | |

(Mlbs) | | |

(kt) | | |

(%) | | |

(Mlbs) | |

| San Rafael | |

| 1,508 | | |

| 2.20 | | |

| 73.3 | | |

| 2,277 | | |

| 1.99 | | |

| 99.7 | | |

| 3,785 | | |

| 2.07 | | |

| 173.0 | |

| Nuestra Señora | |

| 257 | | |

| 1.76 | | |

| 10.0 | | |

| 1,879 | | |

| 1.74 | | |

| 71.9 | | |

| 2,136 | | |

| 1.74 | | |

| 81.9 | |

| Cosalá Subtotal | |

| 1,764 | | |

| 2.14 | | |

| 83.3 | | |

| 4,157 | | |

| 1.87 | | |

| 171.7 | | |

| 5,921 | | |

| 1.95 | | |

| 254.9 | |

| San Felipe Subtotal | |

| - | | |

| - | | |

| - | | |

| 4,677 | | |

| 5.43 | | |

| 560.1 | | |

| 4,677 | | |

| 5.43 | | |

| 560.1 | |

| Total Zinc | |

| 1,764 | | |

| 2.14 | | |

| 83.3 | | |

| 8,834 | | |

| 3.76 | | |

| 731.8 | | |

| 10,598 | | |

| 3.49 | | |

| 815.0 | |

Lead

Mineral Resources - Exclusive of Mineral Reserves

| | |

Measured | | |

Indicated | | |

Measured and Indicated | |

| | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | | |

Tonnes | | |

Grade | | |

Ounces | |

| Property | |

(kt) | | |

(%) | | |

(Mlbs) | | |

(kt) | | |

(%) | | |

(Mlbs) | | |

(kt) | | |

(%) | | |

(Mlbs) | |

| Galena Subtotal (60%) | |

| 441 | | |

| 7.87 | | |

| 76.4 | | |

| 2,042 | | |

| 7.75 | | |

| 349.0 | | |

| 2,483 | | |

| 7.77 | | |

| 425.5 | |

| San Rafael | |

| 1,508 | | |

| 0.96 | | |

| 31.8 | | |

| 2,277 | | |

| 0.90 | | |

| 44.9 | | |

| 3,785 | | |

| 0.92 | | |

| 76.8 | |