UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (D) OF THE SECURITIES AND EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2019

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________ to _______________

Commission File Number: 333-114564

CHINA CARBON GRAPHITE GROUP, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 98-0550699 | |

| (State or other jurisdiction of incorporation of organization) |

(I.R.S. Employer Identification No.) | |

|

20955 Pathfinder Road, Suite 200 Diamond Bar, CA |

91765 | |

| (Address of principal executive offices) | (Zip Code) |

| (909) 843-6518 | ||

| (Registrant’s telephone number, including area code) |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| Emerging growth company | ☐ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ☐ No ☒

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| N/A | N/A |

N/A |

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: As of November 12, 2019, there were 27,502,346 shares of common stock issued and outstanding.

CHINA CARBON GRAPHITE GROUP, INC.

FORM 10-Q

September 30, 2019

TABLE OF CONTENTS

i

PART 1 – FINANCIAL INFORMATION

China Carbon Graphite Group, Inc. and subsidiaries

Consolidated Balance Sheets

| September 30, 2019 | December 31, 2018 | |||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | 7,457 | $ | 9,137 | ||||

| Account Receivable | 3,782 | 5,587 | ||||||

| Inventories | 6,897 | 1,834 | ||||||

| Advance to suppliers | - | 7,517 | ||||||

| Other receivable, net | 55,244 | 29,954 | ||||||

| Total current assets | 73,380 | 54,029 | ||||||

| Right-of-use asset - non current | 20,245 | 27,696 | ||||||

| Property And Equipment, Net | 52,311 | 38,473 | ||||||

| Total Assets | $ | 145,936 | $ | 120,198 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY (DEFICIT) | ||||||||

| Current Liabilities | ||||||||

| Accounts payable and accrued expenses | $ | 137,169 | $ | 91,189 | ||||

| Accrued payroll - related party | 713,849 | 626,662 | ||||||

| Advance from customers | 88,893 | 27,995 | ||||||

| Other payables | 1,531,386 | 1,539,606 | ||||||

| Lease liability - current | 15,427 | 27,696 | ||||||

| Dividends payable | 55,015 | 55,015 | ||||||

| Total current liabilities | 2,541,739 | 2,368,163 | ||||||

| Lease liability - non current | 4,818 | - | ||||||

| Total Liabilities | 2,546,557 | 2,368,163 | ||||||

| Stockholders’ Deficit | ||||||||

| Common stock, $0.001 par value; 100,000,000 shares authorized 27,502,346 and 27,262,346 shares issued and outstanding at September 30, 2019 and December 31, 2018, respectively | 27,502 | 27,262 | ||||||

| Additional paid-in capital | 48,760,711 | 48,753,751 | ||||||

| Accumulated other comprehensive income | 107,516 | 93,271 | ||||||

| Accumulated loss | (51,296,350 | ) | (51,122,249 | ) | ||||

| Total stockholders’ deficit | (2,400,621 | ) | (2,247,965 | ) | ||||

| Total Liabilities and Stockholders’ Deficit | $ | 145,936 | $ | 120,198 | ||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

1

China Carbon Graphite Group, Inc and subsidiaries

Consolidated Statements of Operations and Comprehensive Loss

For the Three And Nine Months Ended September 30, 2019 and 2018

(Unaudited)

| Three Months ended September 30, | Nine Months ended September 30, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| Sales | $ | 200,018 | $ | 302,048 | $ | 258,856 | $ | 1,406,218 | ||||||||

| Cost of Goods Sold | 83,330 | 279,252 | 119,494 | 1,330,535 | ||||||||||||

| Gross Profit | 116,688 | 22,796 | 139,362 | 75,683 | ||||||||||||

| Operating Expenses | ||||||||||||||||

| Selling expenses | 6,575 | 11,364 | 17,689 | 27,149 | ||||||||||||

| General and administrative | 89,402 | 85,025 | 289,262 | 301,121 | ||||||||||||

| Total operating expenses | 95,977 | 96,389 | 306,951 | 328,270 | ||||||||||||

| Loss before other income (expense) and income taxes | 20,711 | (73,593 | ) | (167,589 | ) | (252,587 | ) | |||||||||

| Other Income (Expense) | ||||||||||||||||

| Interest expense | (3,734 | ) | (2,085 | ) | (6,512 | ) | (5,469 | ) | ||||||||

| Other income (expense), net | - | (1 | ) | - | 14 | |||||||||||

| Total other expense (income), net | (3,734 | ) | (2,086 | ) | (6,512 | ) | (5,455 | ) | ||||||||

| Loss before income taxes | 16,977 | (75,679 | ) | (174,101 | ) | (258,042 | ) | |||||||||

| Income Tax Expense | - | - | - | - | ||||||||||||

| Net income (loss) | 16,977 | (75,679 | ) | (174,101 | ) | (258,042 | ) | |||||||||

| Other Comprehensive Income | ||||||||||||||||

| Foreign currency translation gain | 13,622 | 11,121 | 14,245 | 17,406 | ||||||||||||

| Total Comprehensive Income (Loss) | $ | 30,599 | $ | (64,558 | ) | $ | (159,856 | ) | $ | (240,636 | ) | |||||

| Share Data | ||||||||||||||||

| Basic and diluted loss per share | ||||||||||||||||

| Net loss per share – basic and diluted | $ | 0.00 | $ | (0.00 | ) | $ | (0.01 | ) | $ | (0.01 | ) | |||||

| Weighted average common shares outstanding, basic and diluted | 27,502,346 | 27,262,346 | 27,458,390 | 27,221,731 | ||||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

2

China Carbon Graphite Group, Inc and subsidiaries

Consolidated Statements of Changes in Stockholders’ Deficit

For the Quarter Ended September 30, 2019 and 2018

(Unaudited)

| Common Stock | Additional Paid-In | Retained | Other Comprehensive | Total Stockholders’ | ||||||||||||||||||||

| Number | Amount | Capital | Earnings | Income | Deficit | |||||||||||||||||||

| Balance at June 30, 2019 | 27,502,346 | $ | 27,502 | $ | 48,760,711 | $ | (51,313,327 | ) | $ | 93,894 | $ | (2,431,220 | ) | |||||||||||

| Net income | - | - | - | 16,977 | - | 16,977 | ||||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | 13,622 | 13,622 | ||||||||||||||||||

| Balance at September 30, 2019 | 27,502,346 | $ | 27,502 | $ | 48,760,711 | $ | (51,296,350 | ) | $ | 107,516 | $ | (2,400,621 | ) | |||||||||||

| Common Stock | Additional Paid-In | Retained | Other Comprehensive | Total Stockholders’ | ||||||||||||||||||||

| Number | Amount | Capital | Earnings | Income | Deficit | |||||||||||||||||||

| Balance at June 30, 2018 | 27,262,346 | $ | 27,262 | $ | 48,753,751 | $ | (50,958,512 | ) | $ | 82,089 | $ | (2,095,410 | ) | |||||||||||

| Net loss | - | - | - | (75,679 | ) | - | (75,679 | ) | ||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | 11,121 | 11,121 | ||||||||||||||||||

| Balance at September 30, 2018 | 27,262,346 | $ | 27,262 | $ | 48,753,751 | $ | (51,034,191 | ) | $ | 93,210 | $ | (2,159,968 | ) | |||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

3

China Carbon Graphite Group, Inc and subsidiaries

Consolidated Statements of Changes in Stockholders’ Deficit

For the Three Quarters Ended September 30, 2019 and 2018

(Unaudited)

| Common Stock | Additional Paid-In | Retained | Other Comprehensive | Total Stockholders’ | ||||||||||||||||||||

| Number | Amount | Capital | Earnings | Income | Deficit | |||||||||||||||||||

| Balance at December 31, 2018 | 27,262,346 | $ | 27,262 | $ | 48,753,751 | $ | (51,122,249 | ) | $ | 93,271 | $ | (2,247,965 | ) | |||||||||||

| Issuance of common stock for directors and employees | 240,000 | 240 | 6,960 | - | - | 7,200 | ||||||||||||||||||

| Net loss | - | - | - | (174,101 | ) | - | (174,101 | ) | ||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | 14,245 | 14,245 | ||||||||||||||||||

| Balance at September 30, 2019 | 27,502,346 | $ | 27,502 | $ | 48,760,711 | $ | (51,296,350 | ) | $ | 107,516 | $ | (2,400,621 | ) | |||||||||||

| Common Stock | Additional Paid-In | Retained | Other Comprehensive | Total Stockholders’ | ||||||||||||||||||||

| Number | Amount | Capital | Earnings | Income | Deficit | |||||||||||||||||||

| Balance at December 31, 2017 | 27,010,346 | $ | 27,010 | $ | 48,738,883 | $ | (50,776,149 | ) | $ | 75,804 | $ | (1,934,452 | ) | |||||||||||

| Issuance of common stock for directors and employees | 252,000 | 252 | 14,868 | - | - | 15,120 | ||||||||||||||||||

| Net loss | - | - | - | (258,042 | ) | - | (258,042 | ) | ||||||||||||||||

| Foreign currency translation adjustment | - | - | - | - | 17,406 | 17,406 | ||||||||||||||||||

| Balance at September 30, 2018 | 27,262,346 | $ | 27,262 | $ | 48,753,751 | $ | (51,034,191 | ) | $ | 93,210 | $ | (2,159,968 | ) | |||||||||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

4

China Carbon Graphite Group, Inc and subsidiaries

Consolidated Statements of Cash Flows

(Unaudited)

| Nine Months ended September 30, | ||||||||

| 2019 | 2018 | |||||||

| Cash Flows from Operating Activities | ||||||||

| Net Loss available to common shareholders | $ | (174,101 | ) | $ | (258,042 | ) | ||

| Adjustments to reconcile net cash provided by operating activities | ||||||||

| Depreciation | 6,142 | 11,297 | ||||||

| Stock compensation | 7,200 | 15,120 | ||||||

| Changes in operating assets and liabilities | ||||||||

| Accounts receivable | 1,658 | 3,637 | ||||||

| Other receivables | (27,303 | ) | (2,946 | ) | ||||

| Advance to suppliers | 7,531 | 169,308 | ||||||

| Inventory | (5,346 | ) | (1,048 | ) | ||||

| Right-of-use asset | 6,662 | - | ||||||

| Accounts payable and accrued liabilities | 134,880 | 23,472 | ||||||

| Advance from customers | 64,537 | (92,900 | ) | |||||

| Due to related parties | - | (84,334 | ) | |||||

| Taxes payable | (3,319 | ) | (1,353 | ) | ||||

| Other payables | 8,810 | 297,034 | ||||||

| Lease liability | (6,662 | ) | - | |||||

| Net cash provided by operating activities | 20,689 | 79,245 | ||||||

| Cash flows from investing activities | ||||||||

| Acquisition of plant and equipment | (22,080 | ) | (9,479 | ) | ||||

| Net cash used in investing activities | (22,080 | ) | (9,479 | ) | ||||

| Cash flows from financing activities | ||||||||

| Payments to loan from related parties | - | (124 | ) | |||||

| Net cash used in financing activities | - | (124 | ) | |||||

| Effect of exchange rate fluctuation on cash and cash equivalents | (289 | ) | (3,978 | ) | ||||

| Net increase (decrease) in cash | (1,680 | ) | 65,664 | |||||

| Cash and cash equivalents at beginning of period | 9,137 | 8,106 | ||||||

| Cash and cash equivalents at ending of period | $ | 7,457 | $ | 73,770 | ||||

| Supplemental disclosure of cash flow information | ||||||||

| Interest paid | $ | - | $ | 656 | ||||

| Income taxes paid | $ | - | $ | - | ||||

The accompanying notes are an integral part of these unaudited consolidated financial statements.

5

China Carbon Graphite Group, Inc. and subsidiaries

Notes to Unaudited Consolidated Financial Statements

September 30, 2019

(1) Organization and Business

China Carbon Graphite Group, Inc. (the “Company”), through its subsidiaries, is engaged in the research and development, rework and sales of graphene and graphene oxide and graphite bipolar plates in the People’s Republic of China (“China” or the “PRC”). The Company has developed its own graphene prototype and reworks the products by orders only. The Company outsource the production of large orders to third parties as it has not commercialized its product prototype. We also operate a business-to-business and business-to-consumers Internet portal (www.roycarbon.com) for graphite related products. Vendors can sell raw materials, industrial commodities and consumer (household) commodities to both business and consumers through the website by paying a fee for each transaction conducted through the website.

The Company was incorporated on February 13, 2003 in Nevada under the name Achievers Magazine Inc. In connection with the reverse merger transaction described below, the Company’s corporate name was changed to China Carbon Graphite Group, Inc. on January 30, 2008.

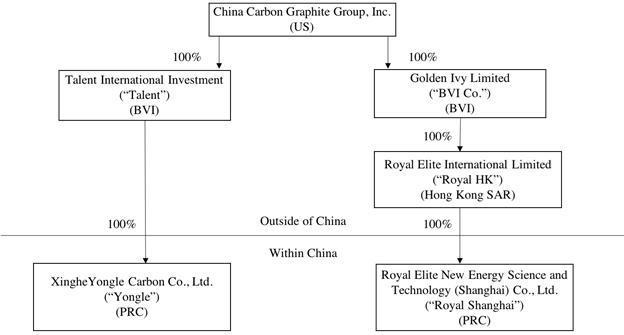

On December 17, 2007, the Company completed a share exchange pursuant to a share exchange agreement with Sincere Investment (PTC), Ltd. (“Sincere”), a British Virgin Islands corporation. Sincere was the sole stockholder of Talent International Investment Limited (“Talent”), a British Virgin Islands corporation., which is the sole stockholder of XingheYongle Carbon Co., Ltd. (“Yongle”), a wholly foreign-owned enterprise company organized under the laws of the PRC. Pursuant to the share exchange agreement, the Company issued 9,388,172 shares of common stock to Sincere in exchange for all of the outstanding on stock of Talent, and Talent became a wholly-owned subsidiary of the Company. Upon completion of the reverse merger, the Company’s business became the business of Talent, its subsidiaries and its affiliated variable interest entities.

Talent owns 100% of the stock of Yongle, which is a wholly foreign-owned enterprise organized under the laws of the PRC.

Acquisition in December 2013

On December 23, 2013, the Company acquired Golden Ivy Limited, a British Virgin Island company (“BVI Co.,”). Pursuant to the terms of the acquisition, we issued an aggregate of 5,000,000 shares of common stock, par value $0.001 per share, to the former shareholders of BVI Co. in exchange for 100% of the issued and outstanding equity of BVI Co. The shares were issued on January 16, 2014. BVI Co. then became a wholly owned subsidiary of the Company.

The Business and the facilities related thereto are all located in the People’s Republic of China (“China”). The Business is conducted by Royal Elite New Energy Science and Technology (Shanghai) Co., Ltd. (“Royal Shanghai”), a wholly foreign owned enterprise under laws of China. Royal Shanghai is wholly owned by Royal Elite International Limited, a Hong Kong company, (“Royal HK”), which is wholly owned by BVI Co.

6

Royal Shanghai was set up in Shanghai on June 9, 2010. Royal HK was set up in Hong Kong on January 8, 2010.

The consolidated financial statements presented herein consolidate the financial statements of China Carbon Graphite, Inc. with the financial statements of its subsidiaries in the following structure chart.

Organizational Structure Chart

The following chart sets forth our organizational structure:

Liquidity and Working Capital Deficit

As of September 30, 2019 and as of December 31, 2018, the Company managed to operate its business with a negative working capital.

The Company Law of the PRC applicable to Chinese companies provides that net after tax income should be allocated by the following rules:

| 1. | 10% of after tax income to be allocated to a statutory surplus reserve until the reserve amounts to 50% of the company’s registered capital. |

| 2. | If the cumulative balance of statutory surplus reserve is not enough to make up the Company’s cumulative prior years’ losses, the current year’s after tax income should be first used to make up the losses before the statutory surplus reverse is drawn. |

| 3. | Allocation can be made to the discretionary surplus reserve, if such a reserve is approved at the meeting of the equity owners. |

Therefore, the Company is required to maintain a statutory reserve in China that limits any equity distributions to its shareholders. The maximum amount of the shareholders has not been reached. The Company has never distributed earnings to shareholders and has no intentions to do so.

7

(2) Going Concern

The Company’s consolidated financial statements are prepared using generally accepted accounting principles in the United States of America applicable to a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As of and for the period ended September 30, 2019, the Company has incurred operating losses of $51,296,350 and working capital deficit of $2,468,359. The ability of the Company to continue as a going concern is dependent on the Company obtaining adequate capital to fund operating losses until it becomes profitable. If the Company is unable to obtain adequate capital, it could be forced to cease operations. The accompanying consolidated financial statements do not include any adjustments that might be necessary if the Company is unable to continue as a going concern.

Management’s Plan to Continue as a Going Concern

In order to continue as a going concern, the Company will need, among other things, additional capital resources. Management’s plans to obtain such resources for the Company include (1) obtaining capital from the sale of its equity securities, (2) sales of its products, and (3) short-term or long-term borrowings from banks, stockholders or other party(ies) when needed. However, management cannot provide any assurance that the Company will be successful in accomplishing any of its plans. The Company plans to look for opportunities to merge with other companies in the graphite industry.

The ability of the Company to continue as a going concern is dependent upon its ability to successfully accomplish the plans described in the preceding paragraph and eventually to secure other sources of financing and attain profitable operations.

(3) Basis for Preparation of the Consolidated Financial Statements

Management acknowledges its responsibility for the preparation of the accompanying interim consolidated financial statements which reflect all adjustments, consisting of normal recurring adjustments, considered necessary in its opinion for a fair statement of its consolidated financial position and the results of its operations for the interim period presented. These consolidated financial statements should be read in conjunction with the summary of significant accounting policies and notes to consolidated financial statements included in the Company’s Form 10-K annual report for the year ended December 31, 2018. The consolidated balance sheet as of December 31, 2018 has been derived from the audited financial statements. The results of the nine months ended September 30, 2019 are not necessarily indicative of the results to be expected for the full fiscal year ending December 31, 2019.

8

The accompanying unaudited consolidated financial statements for China Carbon Graphite Group, Inc. and its subsidiaries and variable interest entity, have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X.

The Company maintains its books and accounting records in Renminbi (“RMB”), but its reporting currency is U.S. dollars.

The financial statements have been prepared in order to present the financial position and results of operations of the Company and its subsidiaries whose financial condition consolidated with the Company pursuant to ASC Topic 810-10, Consolidation, in accordance with U.S. GAAP. All significant intercompany accounts and transactions have been eliminated.

(4) Summary of Significant Accounting Policies

The accompanying unaudited consolidated financial statements reflect the application of certain significant accounting policies as described in this note and elsewhere in the accompanying consolidated financial statements and notes.

Use of estimates

The preparation of these financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that may affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the financial statements and the reported amounts of net sales and expenses during the reporting period. Some of the significant estimates include values and lives assigned to acquired property and equipment, reserves for customer returns and allowances, uncollectible accounts receivable, slow moving, obsolete and/or damaged inventory. Actual results may differ from these estimates.

Cash and cash equivalents

The Company considers all highly liquid debt instruments purchased with maturity periods of six months or less to be cash equivalents. The carrying amounts reported in the accompanying balance sheet for cash and cash equivalents approximate their fair value. Substantially all of the Company’s cash is held in bank accounts in the PRC and is not protected by FDIC insurance or any other similar insurance. The Company’s bank account in the United States is protected by FDIC insurance.

Accounts receivable

Trade receivables are recognized and carried at the original invoice amount less allowance for any uncollectible amounts. An allowance for doubtful accounts is made when collection of the full amount is no longer probable. Bad debts are written off as incurred. Accounts receivable are recorded at the invoiced amount and do not bear interest. Management reviews the adequacy of the allowance for doubtful accounts on an ongoing basis, using historical collection trends and aging of receivables. Management also periodically evaluates individual customer’s financial condition, credit history, and the current economic conditions to make adjustments in the allowance when it is considered necessary.

9

Inventory

Inventory is stated at the lower of cost and net realizable value. The cost of inventories comprises all costs of purchases, and other costs incurred in bringing the inventories to their present location and condition. Cost is determined using the weighted average method. Net realizable value represents the estimated selling price in the ordinary course of business less the estimated costs necessary to complete the sale. The Company periodically reviews historical sales activity to determine excess, slow moving items and potentially obsolete items and also evaluates the impact of any anticipated changes in future demand. The Company provides inventory allowances based on excess and obsolete inventories determined principally by customer demand. Impairment of inventories is recorded in cost of goods sold.

For the nine months ended September 30, 2019 and 2018, the Company has not made provision for inventory in regards to slow moving or obsolete items.

Lease

The Company used comparative method and adopted ASU 2018-20, Leases (Topic 842) to recognize leases assets and lease liabilities on the balance sheet and disclosing key information about lease transactions. All existing leases since January 1, 2018 are reported under this rule. After the adoption, $27,696 of operating lease right-of-use asset and $27,696 of operating lease liabilities were retroactively reflected to December 31, 2018 financial statements.

Property and equipment

Property and equipment is stated at the historical cost, less accumulated depreciation. Depreciation on property and equipment is provided using the straight-line method over the estimated useful lives of the assets for both financial and income tax reporting purposes as follows:

| Machinery and equipment | 5 years | |

| Motor vehicle | 5 years |

Expenditures for renewals and betterments are capitalized while repairs and maintenance costs are normally charged to the statement of operations in the year in which they are incurred. In situations where it can be clearly demonstrated that the expenditure has resulted in an increase in the future economic benefits expected to be obtained from the use of the asset, the expenditure is capitalized as an additional cost of the asset.

10

Upon sale or disposal of an asset, the historical cost and related accumulated depreciation or amortization of such asset were removed from their respective accounts and any gain or loss is recorded in the statements of income.

The Company reviews the carrying value of property, plant, and equipment for impairment whenever events and circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value, an impairment loss is recognized equal to an amount by which the carrying value exceeds the fair value of assets. The factors considered by management in performing this assessment include current operating results, trends and prospects, the manner in which the property is used, and the effects of obsolescence, demand, competition and other economic factors. Based on this assessment, no impairment expenses for property, plant, and equipment was recorded in operating expenses during the nine months ended September 30, 2019 and 2018.

Stock-based compensation

Stock-based compensation includes (i) common stock awards granted to employees and directors for services which are accounted for under FASB ASC 718, Compensation–Stock Compensation” and (ii) common stock awards granted to consultants which are accounted for under FASB ASC 505-50, Equity–Equity-Based Payments to Non-Employees.

All grants of common stock awards and stock options to employees and directors are recognized in the financial statements based on their grant date fair values. The Company has elected to recognize compensation expense using the straight-line method for all common stock awards and stock options granted with service conditions that have a graded vesting schedule, with a corresponding charge to additional paid-in capital.

Common stock awards are granted to directors for services provided. The vested portions of common stock awards granted but not yet issued are recorded in common stock to be issued.

Common stock awards issued to consultants represent common stock granted to non-employees in exchange for services at fair value. The measurement dates for such awards are set at the dates that the contracts are entered into as the awards are non-forfeitable and vest immediately. The measurement date fair value is then recognized over the service period as if the Company has paid cash for such service.

The Company estimates fair value of common stock awards based on the number of shares granted and the quoted price of the Company’s common stock on the date of grant.

11

Foreign currency translation

The reporting currency of the Company is U.S. dollars. The Company uses RMB as its functional currency. The results of operations and cash flows are translated at average exchange rates during the period, and assets and liabilities are translated at the unified exchange rates at the balance sheet dates, and equity is translated at the historical exchange rates. As a result, amounts related to assets and liabilities reported on the statements of cash flows will not necessarily agree with changes in the corresponding accounts on the balance sheets. Translation adjustments resulting from this process are included in accumulated other comprehensive income in the statements of stockholders’ equity. Translation adjustments for the three months ended September 30, 2019 and 2018 were $13,622 and $11,121, respectively. Translation adjustments for the nine months ended September 30, 2019 and 2018 were $14,245 and $17,406, respectively. The cumulative translation adjustment and effect of exchange rate changes on cash for the nine months ended September 30, 2019 and 2018 were $(289) and $(3,978), respectively. Transaction gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency are included in the results of operations as incurred.

Assets and liabilities were translated at 7.15 RMB and 6.88 RMB to $1.00 at September 30, 2019 and December 31, 2018, respectively. The equity accounts were stated at their historical rates. The average translation rates applied to income statements for the nine months ended September 30, 2019 and 2018 were 6.86 RMB and 6.51 RMB to $1.00, respectively. Cash flows are also translated at average translation rates for the period; therefore, amounts reported on the statement of cash flows will not necessarily agree with changes in the corresponding balances on the balance sheet.

Revenue recognition

The Company derives revenues from distribution of graphite-based products. We recognize revenue in accordance with ASC 606, Revenue is recognized upon transfer of control of promised products to customers in an amount that reflects the consideration we expect to receive in exchange for those products. We enter into contracts that can include products, which are generally capable of being distinct and accounted for as separate performance obligations. Revenue is recognized net of allowances for returns and any taxes collected from customers, which are subsequently remitted to governmental authorities. Sales represent the invoiced value of goods, net of value added tax (“VAT”), if any, and are recognized upon delivery of goods and passage of title according to shipping terms.

The Company is subject to VAT, which is levied on a majority of the products, at a rate ranging from 13% to 17% on the invoiced value of sales. Output VAT is borne by customers in addition to the invoiced value of sales and input VAT is borne by the Company in addition to the invoiced value of purchases to the extent not refunded for export sales.

The Company recognizes revenue upon transfer of control of promised products to customers according to shipping terms. The Company does not provide chargeback or price protection rights to the customers. The customer only places purchase orders with the Company once it has confirmed the sale with a third party because this is a specialized business, which dictates that the Company will not sell the products until the purchase order is received. The Company allows its customers to return products only if its products are later determined by the Company to be defective. Based on the Company’s historical experience, product returns have been insignificant throughout all of its product lines. Therefore, the Company does not record an allowance for sales returns. If sales returns occur, they are taken against revenue when products are returned from customers. Sales are presented net of any discounts given to customers. Interest income is recognized when earned. The Company experienced no returns for the nine months ended September 30, 2019 and 2018.

12

In May 2014, the FASB issued Accounting Standards Update (“ASU”) 2014-09, Revenue from Contracts with Customers (Topic 606), amending revenue recognition guidance and requiring more detailed disclosures to enable users of financial statements to understand the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. We adopted this ASU on January 1, 2018 for all revenue contracts with our customers using the modified retrospective approach.

There is no impact of applying this ASU.

Cost of goods sold

Cost of goods sold consists primarily of the purchase costs of products.

Shipping and handling costs

The Company follows ASC 606, as amended and clarified by ASU 2016-10, to record shipping and handling cost. The Company classifies shipping and handling costs paid on behalf of its customers in selling expenses. For the three months ended September 30, 2019 and 2018, shipping and handling costs were $561 and $$4,398, respectively. For the nine months ended September 30, 2019 and 2018, shipping and handling costs were $1,519 and $11,459, respectively.

Taxation

Taxation on profits earned in the PRC has been calculated based on the estimated assessable profits for the year at the rates of taxation prevailing in the PRC after taking into account the benefits from any special tax credits or “tax holidays” allowed in the county of operations.

The Company does not accrue U.S. income tax since it has no operations in the United States. Its operating subsidiaries are organized and located in the PRC and do not conduct any business in the United States.

In 2006, the Financial Accounting Standards Board (“FASB”) issued ASC, 740 Income Tax, formerly known as FIN 48, which clarifies the application of SFAS 109 by defining a criterion that an individual income tax position must meet for any part of the benefit of that position to be recognized in an enterprise’s financial statements and provides guidance on measurement, recognition, classification, accounting for interest and penalties, accounting in interim periods, disclosure and transition. In accordance with the transition provisions, the Company adopted FIN 48 effective January 1, 2007.

13

The Company recognizes that virtually all tax positions in the PRC are not free from some degree of uncertainty due to tax law and policy changes by the state. The Company cannot reasonably quantify political risk factors and thus must depend on guidance issued by current government officials.

Based on all known facts and circumstances and current tax law, the Company believes that the total amount of unrecognized tax benefits as of September 30, 2019 is not material to its results of operations, financial condition or cash flows. The Company also believes that the total amount of unrecognized tax benefits as of September 30, 2019, if recognized, would not have a material effect on its effective tax rate. The Company further believes that there are no tax positions for which it is reasonably possible, based on current Chinese tax law and policy, that the unrecognized tax benefits will significantly increase or decrease over the next twelve months producing, individually or in the aggregate, a material effect on the Company’s results of operations, financial condition or cash flows.

Enterprise income tax

The enterprise income tax is calculated on the basis of the statutory profit as defined in the PRC tax laws. This statutory profit is computed differently than the Company’s net income under U.S. GAAP.

Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax basis. Deferred tax assets, including tax loss and credit carry forwards, and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect of deferred tax assets and liabilities from a change in tax rates is recognized in income in the period that includes the enactment date. Deferred income tax expense represents the change during the period in the deferred tax assets and deferred tax liabilities. The components of the deferred tax assets and liabilities are individually classified as current and non-current based on their characteristics. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all of the deferred tax assets will not be realized.

Value added tax

The Provisional Regulations of the PRC Concerning Value Added Tax promulgated by the State Council came into effect on January 1, 1994. Under these regulations and the Implementing Rules of the Provisional Regulations of the PRC Concerning Value Added Tax, value added tax (“VAT”) is imposed on goods sold in or imported into the PRC and on processing, repair and replacement services provided within the PRC.

VAT payable in the PRC is charged on an aggregated basis at a rate of 13% or 17% (depending on the type of goods involved) on the full price collected for the goods sold or, in the case of taxable services provided, at a rate of 17% on the charges for the taxable services provided, but excluding, in respect of both goods and services, any amount paid in respect of VAT included in the price or charges, and less any deductible value added tax already paid by the taxpayer on purchases of goods and services in the same financial year.

14

Contingent liabilities and contingent assets

A contingent liability is a possible obligation that arises from past events and whose existence will only be confirmed by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the Company. It can also be a present obligation arising from past events that is not recognized because it is not probable that the Company will incur a liability or obligations as a result. A contingent liability, which might occur but is not probable, is not recorded but is disclosed in the notes to the financial statements. The Company will recognize a liability or obligation when it is probable that the Company will incur such liability or obligation.

A contingent asset is an asset, which could possibly arise from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain events not wholly within the control of the Company. Contingent assets are not recorded but are disclosed in the notes to the financial statements when it is likely that the Company will recognize an economic benefit. When the benefit is virtually certain, the asset is recognized.

Fair value of financial instruments

The Company has adopted ASC Topic 820, Fair Value Measurement and Disclosure, which defines fair value, establishes a framework for measuring fair value in U.S. GAAP, and expands disclosures about fair value measurements. It does not require any new fair value measurements, but provides guidance on how to measure fair value by providing a fair value hierarchy used to classify the source of the information. It establishes a three-level valuation hierarchy of valuation techniques based on observable and unobservable inputs, which may be used to measure fair value and include the following:

| ● | Level 1 inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| ● | Level 2 inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the assets or liability, either directly or indirectly, for substantially the full term of the financial instruments. |

| ● | Level 3 inputs to the valuation methodology are unobservable and significant to the fair value. |

The carrying amount of other receivables, advance to vendors, advances from customers, other payables, accrued liabilities are reasonable estimates of their fair value because of the short-term nature of these items.

15

Loss per share

Basic loss per share is computed by dividing net income available to common shareholders by the weighted average number of shares of common stock outstanding during the period. Diluted loss per share is computed by dividing net income available to common shareholders by the weighted average number of shares of common stock, common stock equivalents and potentially dilutive securities outstanding during each period. Potentially dilutive shares of common stock consist of the common stock issuable upon the conversion of convertible debt, preferred stock and warrants. The Company uses if-converted method to calculate the dilutive preferred stock and treasury stock method to calculate the dilutive shares issuable upon exercise of warrants.

The following table sets forth the computation of the number of net loss per share for the nine months ended September 30, 2019 and 2018:

| September 30, 2019 | September 30, 2018 | |||||||

| Weighted average shares of common stock outstanding (basic) | 27,458,390 | 27,221,731 | ||||||

| Shares issuable upon conversion of Series B Preferred Stock | - | - | ||||||

| Weighted average shares of common stock outstanding (diluted) | 27,458,390 | 27,221,731 | ||||||

| Net loss available to common shareholders | $ | (174,101 | ) | $ | (258,042 | ) | ||

| Net loss per shares of common stock (basic) | $ | (0.01 | ) | $ | (0.01 | ) | ||

| Net loss per shares of common stock (diluted) | $ | (0.01 | ) | $ | (0.01 | ) | ||

The following table sets forth the computation of the number of net loss per share for the three months ended September 30, 2019 and 2018:

| September 30, 2019 | September 30, 2018 | |||||||

| Weighted average shares of common stock outstanding (basic) | 27,502,346 | 27,262,346 | ||||||

| Shares issuable upon conversion of Series B Preferred Stock | - | - | ||||||

| Weighted average shares of common stock outstanding (diluted) | 27,502,346 | 27,262,346 | ||||||

| Net loss available to common shareholders | $ | 16,977 | $ | (75,679 | ) | |||

| Net loss per shares of common stock (basic) | $ | 0.00 | $ | (0.00 | ) | |||

| Net loss per shares of common stock (diluted) | $ | 0.00 | $ | (0.00 | ) | |||

Accumulated other comprehensive income

The Company follows ASC 220, Comprehensive Income, formerly known as SFAS No. 130, Reporting Comprehensive Income, to recognize the elements of comprehensive income. Comprehensive income is comprised of net income and all changes to the statements of stockholders’ equity, except those due to investments by stockholders, changes in paid-in capital and distributions to stockholders. For the Company, comprehensive income for the nine months ended September 30, 2019 and 2018 included net income and foreign currency translation adjustments.

16

Related parties

Parties are considered to be related to the Company if the parties that, directly or indirectly, through one or more intermediaries, control, are controlled by, or are under common control with the Company. Related parties also include principal owners of the Company, its management, members of the immediate families of principal owners of the Company and its management and other parties with which the Company may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests. Transactions with related parties are disclosed in the financial statements.

Recent accounting pronouncements

The Company has reviewed all recently issued, but not yet effective, accounting pronouncements and does not believe the future adoption of any such pronouncements will have a material impact on its financial condition or the results of its operations.

In February 2016, the FASB issued ASU No. 2016-02, “Leases (Topic 842)”, to increase the transparency and comparability about leases among entities. The new guidance requires lessees to recognize a lease liability and a corresponding lease asset for virtually all lease contracts. It also requires additional disclosures about leasing arrangements. ASU 2016-02 is effective for interim and annual periods beginning after December 15, 2018, and requires a modified retrospective approach to adoption. The Company adopted the policy on January 1,2019 and the impact of the adoption of this guidance is listed in Note 14.

In October 2016, the FASB issued ASU 2016-16, “Income Taxes (Topic 740): Intra-Entity Transfer of Assets Other than Inventory”, which requires the recognition of the income tax consequences of an intra-entity transfer of an asset, other than inventory, when the transfer occurs. ASU 2016-06 will be effective for the Company in its first quarter of 2019. The Company does not expect that the adoption of this guidance will have a material impact on its consolidated financial statements.

Management does not believe that any recently issued, but not yet effective accounting pronouncements, when adopted, will have a material effect on the accompanying financial statements.

(5) Concentration of Business and Credit Risk

Most of the Company’s bank accounts are in banks located in the PRC and are not covered by any type of protection similar to that provided by the Federal Deposit Insurance Corporation (“FDIC”) on funds held in U.S. banks. The Company’s bank account in the United States is covered by FDIC insurance.

Because the Company’s operations are located in the PRC, this may give rise to significant foreign currency risks due to fluctuations in and the volatility of foreign exchange rates between U.S. dollars and RMB.

17

Financial instruments that potentially subject the Company to concentration of credit risk consist principally of cash, trade accounts receivables and inventories, the balances of which are stated on the balance sheet. The Company places its cash in banks located in China. Concentration of credit risk with respect to trade accounts receivables is limited due to the diversity of the Company’s customers who are located in different regions of China. The Company does not require collateral or other security to support financial instruments subject to credit risk.

Sales to certain customers generated over 10% of the Company’s total net sales. Sales to one Company for the nine months ended September 30, 2019 were approximately 46% of the Company’s net sales. Sales to other Company for the nine months ended September 30, 2019 were approximately 29% of the Company’s net sales.

Sales to certain customers generated over 10% of the Company’s total net sales. Sales to one Company for the nine months ended September 30, 2018 were approximately 95% of the Company’s net sales.

For the nine months ended September 30, 2019, three suppliers accounted for approximately 93% of total purchases.

For the nine months ended September 30, 2018, one supplier accounted for approximately 96% of total purchases.

(6) Accounts Receivable

The Company establishes an individualized credit and collection policy based on each individual customer’s credit history. The Company does not have a uniform policy that applies equally to all customers. The collection period usually ranges from three months to twelve months. The Company grants extended payment terms only when the Company believes that the payment will be collectible at the end of the term. The Company grants extended payment terms to customers if based on the following factors: (a) whether or not the Company views a real need, from the customer’s perspective, for the extension and (b) how critical the Company’s relationship with the customer and is the customer the Company’s long-term business. The Company grants extended payment terms only when the Company believes that the payment will be collectible at the end of the term. This meets the criteria of revenue recognition under U.S. GAAP, which requires that collection of the resulting receivable be reasonably assured.

As of September 30, 2019 and December 31, 2018, accounts receivable consisted of the following:

| September 30, 2019 | December 31, 2018 | |||||||

| Amount outstanding | $ | 3,782 | $ | 5,587 | ||||

| Less: Allowance for doubtful accounts | - | - | ||||||

| Net amount | $ | 3,782 | $ | 5,587 | ||||

18

(7) Advances to Suppliers

As of September 30, 2019 and December 31, 2018, advances to suppliers are advances for finished goods and amounted to $0 and $7,517, respectively.

Advances to suppliers represent interest-free cash paid in advance to suppliers for purchases of inventory.

(8) Inventories

As of September 30, 2019 and December 31, 2018, inventories consisted of the following:

| September 30, 2019 | December 31, 2018 | |||||||

| Inventory in transit | $ | 6,897 | $ | 1,834 | ||||

| Reserve for slow moving and obsolete inventory | - | - | ||||||

| Inventory, net | $ | 6,897 | $ | 1,834 | ||||

For the nine months ended September 30, 2019 and 2018, the Company has not made provision for inventory in regards to slow moving or obsolete items. As of September 30, 2019 and December 31, 2018, the Company did not record any provision for inventory in regards to slow moving or obsolete items.

(9) Other Receivables

Other receivables amounted $55,244 and $29,954 as of September 30, 2019 and December 31, 2018, respectively. Other receivables are mainly export tax rebates.

(10) Property and Equipment, net

As of September 30, 2019 and December 31, 2018, property, plant and equipment consisted of the following:

| September 30, 2019 | December 31, 2018 | |||||||

| Machinery and equipment | $ | 55,545 | $ | 35,705 | ||||

| Office equipment | 10,677 | 11,100 | ||||||

| Motor vehicles | 39,084 | 40,630 | ||||||

| Total | 105,306 | 87,435 | ||||||

| Less: accumulated depreciation | (52,995 | ) | (48,962 | ) | ||||

| Plant and Equipment, net | $ | 52,311 | $ | 38,473 | ||||

19

For the three months ended September 30, 2019 and 2018, depreciation expenses amounted to $2,019 and $3,991, respectively. For the nine months ended September 30, 2019 and 2018, depreciation expenses amounted to $6,142 and $7,671, respectively.

The Company purchased approximately $22,080 and $9,479 property and equipment during the nine months ended September 30, 2019 and 2018, respectively.

The Company reviews the carrying value of property and equipment for impairment whenever events and circumstances indicate that the carrying value of an asset may not be recoverable from the estimated future cash flows expected to result from its use and eventual disposition. In cases where undiscounted expected future cash flows are less than the carrying value, an impairment loss is recognized equal to an amount by which the carrying value exceeds the fair value of assets. The factors considered by management in performing this assessment include current operating results, trends and prospects, the manner in which the property is used, and the effects of obsolescence, demand, competition and other economic factors. Based on this assessment, no impairment expenses for property, plant, and equipment was recorded in operating expenses during the nine months ended September 30, 2019 and 2018.

(11) Stockholders’ deficit

Restated Articles of Incorporation

On January 22, 2008, the Company changed its authorized capital stock to 120,000,000 shares of capital stock, of which 20,000,000 shares are shares of preferred stock, par value $0.001 per share, and 100,000,000 shares are shares of common stock, par value $0.001 per share. The restated articles of incorporation authorizes the board of directors of the Company to issue one or more series of preferred stock and to designate the rights, preferences, privileges and limitation of the holders of such preferred stock. The board of directors has authorized the issuance of two series of preferred stock, Series A Convertible Preferred Stock (“Series A Preferred Stock”) and Series B Convertible Preferred Stock (“Series B Preferred Stock”).

Issuance of Common Stock

The Company has total outstanding shares of common stock of 27,502,346 and 27,262,346 as of September 30, 2019 and December 31, 2018, respectively.

(a) Stock Issuances For Compensation

On February 20, 2019, the Company issued an aggregate of 200,000 shares of common stock to four directors as compensation for services provided in 2018. The issuance of these shares was recorded at grant date fair market value at $0.03 per share.

20

On February 20, 2019, the Company issued 40,000 shares of common stock to the CFO. The issuance of these shares was recorded at grant date fair market value of $0.03.

(b) Shares Held in Escrow

In a private placement that closed on December 22, 2009 and January 13, 2010, the Company sold an aggregate of 2,480,500 shares of Series B Preferred Stock and five-year warrants to purchase 992,000 shares of common stock at an exercise price of $1.30 per share, for an aggregate purchase price of $2,976,600. The Company also paid the private placement agent an aggregate of $298,000 and issued five-year warrants to purchase 124,025 shares of common stock at an exercise price of $1.32 per share. In connection with the private placement and pursuant to the transaction agreements, the Company deposited into escrow an aggregate of 1,240,250 shares of common stock, which are to be held in escrow to be returned to the Company or delivered to the investors, depending on whether the Company meets certain financial performance targets for the years ending December 31, 2010 and 2011.

The Company did not meet the financial targets. The number of Escrow Shares payable to each Investor shall be equal to a fraction of the total number of Escrow Shares potentially issuable pursuant to the terms hereof, the numerator of which shall be the amount by which (i) the number of Conversion Shares issued or issuable upon Preferred Shares which was initially issued to the Investor exceeds (ii) the sum of (x) the number of Conversion Shares sold or otherwise transferred by the Investor plus (y) the number of shares of Conversion Shares issued or issuable sold or otherwise transferred by the Investor, and the denominator of which is the number of Conversion Shares issued or issuable by the Company in the Offering. Any Escrow Shares for either Fiscal Year 2011 or Fiscal Year 2010 which are not transferred to the Investors pursuant to this paragraph shall be returned to the Company for cancellation. As of September 30, 2019, no Escrow Shares have been transferred to investors or returned to the Company.

(12) Related Parties

As of September 30, 2019 and December 31, 2018, $668,849 and $581,662 are the salary owed to Mr. Donghai Yu, who is CEO of the Company. As of September 30, 2019 and December 31, 2018, $45,000 and $45,000 are the salary owed to Ms. Grace King, who is VP finance of the Company. Ms. Grace King has resigned from the Company in 2018.

(13) Other Payable

Other payable amounted $1,531,386 and $1,539,606 as of September 30, 2019 and December 31, 2018, respectively. Other payables are mainly money borrowed from unrelated parties for operating purpose. These payable are without collateral, interest free, and due on demand.

(14) Lease Commitment

Our principal executive office is located in US. The Company leased its corporate address month to month for a monthly fee of $365. The lease is month to month.

Royal Shanghai has operating leases for corporate offices. Our leases have remaining lease terms of 6 months to 24 months.

21

Royal Shanghai leases an office in Shanghai China. The lease term of the office space is from March 16, 2019 to March 15, 2021. The current monthly rent including monthly management fee is approximately $1,052 (RMB 7,063).

Royal Shanghai leases another office in Shanghai China. The lease term of the office space is from August 29, 2018 to November 30, 2019. The current monthly rent including monthly management fee is approximately $2,513 (RMB 16,866).

The components of lease expense were as follows:

| Nine months Ended September 30, | ||||||||

| 2019 | 2018 | |||||||

| Operating lease cost | $ | 31,332 | $ | 25,410 | ||||

Supplemental cash flow information related to leases was as follows:

| Nine months Ended September 30, | ||||||||

| 2019 | 2018 | |||||||

| Cash paid for amounts included in the measurement of lease liabilities: | ||||||||

| Operating cash flows from operating leases | $ | 6,662 | $ | - | ||||

| Right-of-use assets obtained in exchange for lease obligations: | ||||||||

| Operating leases | 6,662 | - | ||||||

Supplemental balance sheet information related to leases was as follows:

| September 30, 2019 | December 31, 2018 | |||||||

| Operating Leases | ||||||||

| Operating lease right-of-use assets-non current | $ | 20,245 | $ | 27,696 | ||||

| Total operating lease right-of-use assets | 20,245 | 27,696 | ||||||

| Operating lease liability-current | $ | 15,427 | $ | 27,696 | ||||

| Operating lease liability-non current | 4,818 | - | ||||||

| Total operating lease liabilities | $ | 20,245 | $ | 27,696 | ||||

Maturities of lease liabilities were as follows:

| Year Ending September 30, | Operating Leases | |||

| 2020 | $ | 15,427 | ||

| 2021 | 4,818 | |||

| Total lease payments | 20,245 | |||

| Less imputed interest | - | |||

| Total | $ | 20,245 | ||

22

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion of the results of our operations and financial condition should be read in conjunction with our financial statements and the related notes, which appear elsewhere in this report. The following discussion includes forward-looking statements. For a discussion of important factors that could cause actual results to differ from our forward-looking statements, see the section entitled “Cautionary Note Regarding Forward Looking Statements” above.

In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, undue reliance should not be placed on these forward-looking statements. Also, forward-looking statements represent our estimates and assumptions only as of the date of this report. This Quarterly Report should be read in its entirety and with the understanding that our actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

Overview

We engage in the research and development, small production and sales of graphene and graphene oxide and graphite bipolar plates in the People’s Republic of China. We have developed our own graphene prototype and produces the products by orders only, for which we sell domestically and export internationally. We outsource the production of large orders to third parties as we have not commercialized our product prototype. Starting in the second quarter of 2018, we have started producing our graphene products on a regular basis and standardized the packaging for our customers’ commercial use. We also operate a business-to-business and business-to-consumers Internet portal (www.roycarbon.com) for graphite related products.

For the nine months ended September 30, 2019, the Company has incurred operating losses. The ability of the Company to continue as a going concern is dependent on the Company obtaining adequate capital to fund operating losses until it becomes profitable. If the Company is unable to obtain adequate capital, it could be forced to cease operations. In order to continue as a going concern, the Company will need, among other things, additional capital resources. Management’s plans to obtain such resources for the Company include (1) obtaining capital from the sale of its equity securities, (2) sales of its products, and (3) short-term or long-term borrowings from banks, stockholders or other party(ies) when needed. However, management cannot provide any assurance that the Company will be successful in accomplishing any of its plans. The Company plans to look for opportunities to merge with or acquire other graphite companies.

PRC regulations grant broad powers to the government to adjust the price of raw materials and manufactured products. Although the government has not imposed price controls on our raw materials or our products, it is possible that price controls may be implemented in the future, thereby affecting our results of operations and financial condition.

Results of Operations

Comparison of Results of Operation for the Three Months Ended September 30, 2019 and 2018

Sales

During the three months ended September 30, 2019, we had sales of $200,018, compared to sales of $302,048 for the three months ended September 30, 2018, a decrease of $102,030, or approximately 33.78%. The sales decrease was mainly because we focused on the development of core products such as graphite felt and graphene application.

23

Cost of goods sold

Our cost of goods sold consists of the purchase cost. During the three months ended September 30, 2019, our cost of goods sold was $83,330, compared to $279,252 for the cost of goods sold for the three months ended September 30, 2018, a decrease of $195,922 or approximately 70.16%. The significant decrease in the cost of sales was primarily attributable to the corresponding decreasing in sales.

Gross profit

Our gross profit increase from $22,796 for the three months ended September 30, 2018 to $116,688 for the three months ended September 30, 2019. The increase of the gross profit is mainly because our core products were sold at a higher price and profit margin.

Gross profit Margin

Our gross profit margin increased from 7.5% for the three months ended September 30, 2018 to 58.3% for the three months ended September 30, 2019 because our core products were sold at a higher price and profit margin.

Operating expenses

Operating expenses totaled $95,977 for the three months ended September 30, 2019, compared to $96,389 for the three months ended September 30, 2018, a decrease of $412, or approximately 0.43%.

Selling, general and administrative expenses

Selling expenses decreased from $11,364 for the three months ended September 30, 2018 to $6,575 for the three months ended September 30, 2019, a decrease of $4,789, or approximately 42.14%. The decrease is mainly the corresponding decrease in sales.

Our general and administrative expenses consist of salaries, office expenses, utilities, business travel, amortization expenses, public company expenses (including legal expenses, accounting expenses and investor relations expenses) and stock compensation. General and administrative expenses were $89,402 for the three months ended September 30, 2019, compared to $85,025 for the three months ended September 30, 2018, an increase of $4,377 or 5.15%. The increase of general and administrative expenses is mainly because we dedicated more resources to improve the business.

Loss from operations

As a result of the factors described above, operating loss was $73,593 for the three months ended September 30, 2019, compared to operating income of $20,711 for the three months ended September 30, 2018, an increase of approximately $94,304.

Other income and expenses

Our interest expense was $3,734 for the three months ended September 30, 2019, compared to interest expense of $2,085 for the three months ended September 30, 2018. The reason is due to the change in interest rate.

Other expenses of $0 and other expense of $(1) were recorded as other income for the three months ended September 30, 2019 and 2018, respectively.

Income tax

During the three months ended September 30, 2019 and 2018, we did not incur any income tax due for these periods.

24

Net loss

As a result of the factors described above, our net income for the three months ended September 30, 2019 was $16,977, compared to net loss of $(75,679) for the three months ended September 30, 2018, an increase of $92,656.

Foreign currency translation

Our consolidated financial statements are expressed in U.S. dollars but the functional currency of our operating subsidiary is RMB. Results of operations and cash flows are translated at average exchange rates during the period, assets and liabilities are translated at the unified exchange rate at the end of the period and equity is translated at historical exchange rates. Translation adjustments resulting from the process of translating the financial statements denominated in RMB into U.S. dollars are included in determining comprehensive income. Our foreign currency translation gain for the three months ended September 30, 2019 was $13,622, compared a translation gain of $11,121 for the three months ended September 30, 2018, an increase of $2,501.

Net loss available to common stockholders

Net gain available to our common stockholders was $0.00, or $0.00 per share (basic and diluted), for the three months ended September 30, 2019, compared to net loss of $0.00, or net loss of $0.00 per share (basic and diluted), for the three months ended September 30, 2018.

Comparison of Results of Operation for the Nine months ended September 30, 2019 and 2018

Sales

During the nine months ended September 30, 2019, we had sales of $258,856, compared to sales of $1,406,218 for the nine months ended September 30, 2018, a decrease of $1,147,362, or approximately 81.59%. The significant sales decrease was mainly because we focused on the development of core products, and innovation.

Cost of goods sold

Our cost of goods sold consists of the purchase cost. During the nine months ended September 30, 2019, our cost of goods sold was $119,494, compared to $1,330,535 for the cost of goods sold for the nine months ended September 30, 2018, a decrease of $1,211,041 or approximately 91.02%. The significant decrease in the cost of sales was primarily attributable to the corresponding decreasing in sales.

Gross profit

Our gross profit increased from $75,683 for the nine months ended September 30, 2018 to $139,362 for the nine months ended September 30, 2019. The increase of the gross profit is mainly attributed to because our core products were sold at a higher price and profit margin.

Gross profit Margin

Our gross profit margin increased from 5.4% for the nine months ended September 30, 2018 to 53.8% for the nine months ended September 30, 2019 due to because our core products are were at a higher price and profit margin.

Operating expenses

Operating expenses totaled $306,951 for the nine months ended September 30, 2019, compared to $328,270 for the nine months ended September 30, 2018, a decrease of $21,319, or approximately 6.49%.

Selling, general and administrative expenses

Selling expenses decreased from $27,149 for the nine months ended September 30, 2018 to $17,689 for the nine months ended September 30, 2019, a decrease of $9,460, or approximately 34.84%. The decrease is mainly attributed to the corresponding decreasing in sales.

Our general and administrative expenses consist of salaries, office expenses, utilities, business travel, amortization expenses, public company expenses (including legal expenses, accounting expenses and investor relations expenses) and stock compensation. General and administrative expenses were $289,262 for the nine months ended September 30, 2019, compared to $301,121 for the nine months ended September 30, 2018, a decrease of $11,859 or 3.94%. The decrease of general and administrative expenses is mainly because we focused on the development of innovation.

25

Loss from operations

As a result of the factors described above, operating loss was $(167,589) for the nine months ended September 30, 2019, compared to operating loss of $(252,587) for the nine months ended September 30, 2018, a decrease in loss of approximately $84,998, or 33.65%.

Other income and expenses

Our interest expense was $(6,512) for the nine months ended September 30, 2019, compared to interest expense of $(5,469) for the nine months ended September 30, 2018. The reason is due to the change in interest rate.

Other income of $0 and other expense of $14 were recorded as other income for the nine months ended September 30, 2019 and 2018, respectively.

Income tax

During the nine months ended September 30, 2019 and 2018, we did not incur any income tax due for these periods.

Net loss

As a result of the factors described above, our net loss for the nine months ended September 30, 2019 was $(174,101), compared to net loss of $(258,042) for the nine months ended September 30, 2018, a decrease in loss of $83,941, or approximately 32.53%.

Foreign currency translation

Our consolidated financial statements are expressed in U.S. dollars but the functional currency of our operating subsidiary is RMB. Results of operations and cash flows are translated at average exchange rates during the period, assets and liabilities are translated at the unified exchange rate at the end of the period and equity is translated at historical exchange rates. Translation adjustments resulting from the process of translating the financial statements denominated in RMB into U.S. dollars are included in determining comprehensive income. Our foreign currency translation gain for the nine months ended September 30, 2019 was $14,245, compared a translation gain of $17,406 for the nine months ended September 30, 2018, a decrease of $3,161.

Net loss available to common stockholders

Net loss available to our common stockholders was $0.01, or $0.01 per share (basic and diluted), for the nine months ended September 30, 2019, compared to net loss of $0.01, or net loss of $0.01 per share (basic and diluted), for the nine months ended September 30, 2018.

Liquidity and Capital Resources

All of our business operations are carried out by Royal Shanghai, and all of the cash generated by our operations has been held by that entity. In order to transfer such cash to our parent entity, China Carbon Graphite Group, Inc., which is a Nevada corporation, we would need to rely on dividends, loans or advances made by our PRC subsidiaries. Such transfers may be subject to certain regulations or risks. To date, our parent entity has paid its expenses by raising capital through private placement transactions. In the future, in the event that our parent entity is unable to raise needed funds from private investors, Royal Shanghai would have to transfer funds to our parent entity through our wholly-owned subsidiaries, Royal Hongkong and BVI. Co.

26

PRC regulations relating to statutory reserves and currency conversion would impact our ability to transfer cash within our corporate structure. The Company Law of the PRC applicable to Chinese companies provides that net after tax income should be allocated by the following rules:

| 1. | 10% of after tax income to be allocated to a statutory surplus reserve until the reserve amounts to 50% of the company’s registered capital. |

| 2. | If the accumulate balance of statutory surplus reserve is not enough to make up the Company’s cumulative prior years’ losses, the current year’s after tax income should be first used to make up the losses before the statutory surplus reverse is drawn. |

| 3. | Allocation can be made to the discretionary surplus reserve, if such a reserve is approved at the meeting of the equity owners. |

Therefore, the Company is required to maintain a statutory reserve in China that limits any equity distributions to its shareholders. The maximum amount of the shareholders has not been reached. The company has never distributed earnings to shareholders and has consistently stated in the Company’s filings it has no intentions to do so.

The RMB cannot be freely exchanged into the Dollars. The State Administration of Foreign Exchange (“SAFE”) administers foreign exchange dealings and requires that they be conducted though designated financial institutions. Foreign Investment Enterprises, such as Royal Shanghai, may purchase foreign currency from designated financial institutions in connection with current account transactions, including profit repatriation.

These factors will limit the amount of funds that we can transfer from Royal Shanghai to our parent entity and may delay any such transfer. In addition, upon repatriation of earnings of Royal Shanghai to the United States, those earnings may become subject to United States federal and state income taxes. We have not accrued any U.S. federal or state tax liability on the undistributed earnings of our foreign subsidiary because those funds are intended to be indefinitely reinvested in our international operations. Accordingly, taxes imposed upon repatriation of those earnings to the U.S. would reduce the net worth of the Company.

Our primary capital needs have been to fund our working capital requirements. Our primary sources of financing will be cash generated from loans from banks, equity investment from investors, and borrowings from unrelated parties.

The Company’s consolidated financial statements are prepared using generally accepted accounting principles in the United States of America applicable to a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As of and for the period ended September 30, 2019, the Company has incurred operating losses and working capital deficit from operating activities. The Company’s sales revenue is not sufficient to cover the company’s expenses for the nine months ended September 30, 2019.

The ability of the Company to continue as a going concern is dependent on the Company obtaining adequate capital to fund operating losses until it becomes profitable. If the Company is unable to obtain adequate capital, it could be forced to cease operations. At this point, there can be no assurance that the Company is able to obtain such funding.

27

Our long-term goal is to develop our Royal Shanghai business. During the interim, we expect that anticipated cash flows from future operations, loans and equity investment from unrelated or related parties, provided that:

| ● | we generate sufficient business so that we are able to generate substantial profits, which cannot be assured; |

| ● | we are able to generate savings by improving the efficiency of our operations. |

We may require additional equity, debt or bank funding to finance acquisitions or to allow us to develop our Royal Shanghai business, which is one of our primary growth strategies. We can provide no assurances that we will be able to enter into any additional financing agreements on terms favorable to us, if at all, especially considering the current global instability of the capital markets.

At September 30, 2019, cash and cash equivalents were $7,457, compared to $9,137 at December 31, 2018, an increase of $1,680. Our working capital deficit increased by $154,225 to a deficit of $2,468,359 at September 30, 2019 from $2,314,134 at December 31, 2018.

Accounts receivable, net of allowance, were $3,782 and $5,587 as of September 30, 2019 and December 31, 2018, respectively. The decrease was mainly due to decreased sales during the nine months ended September 30, 2019. Accounts receivable are recorded at the invoiced amount and do not bear interest. Our management reviews the adequacy of our allowance for doubtful accounts on an ongoing basis, using historical collection trends and the aging of receivables. Management also periodically evaluates individual customer’s financial condition, credit history, and the current economic conditions to make adjustments in the allowance when it is considered necessary.

As of September 30, 2019, inventories were $6,897, compared to $1,834 at December 31, 2018, an increase of $ 5,063, or 276.06%. As of September 30, 2019 and December 31, 2018, the Company has not made provision for inventory in regards to slow moving or obsolete items.

Advances to suppliers decreased from $7,517 at December 31, 2018 to $0 at September 30, 2019. The decrease of advances to suppliers is mainly because the Company made less advanced payments to suppliers during the nine months ended September 30, 2019. No allowance for doubtful accounts for the balance of advances to suppliers was reserved as of September 30, 2019 and December 31, 2018, respectively.

The following table sets forth information about our net cash flow for the three months indicated:

| For the Nine months ended September 30, | ||||||||

| 2019 | 2018 | |||||||

| Net cash flows provided by operating activities | $ | 20,689 | $ | 79,245 | ||||