UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21539

(Exact name of registrant as specified in charter)

120 East Liberty Drive

Wheaton, IL 60187

(Address of principal executive offices) (Zip code)

W. Scott Jardine, Esq.

First Trust Portfolios L.P.

120 East Liberty Drive

Wheaton, IL 60187

(Name and address of agent for service)

Registrant's telephone number, including area code: 630-765-8000

Date of fiscal year end: May 31

Date of reporting period: November 30, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

(a) The Report to Shareholders is attached herewith.

|

|

1 |

|

|

2 |

|

|

4 |

|

|

7 |

|

|

17 |

|

|

18 |

|

|

19 |

|

|

20 |

|

|

21 |

|

|

22 |

|

|

29 |

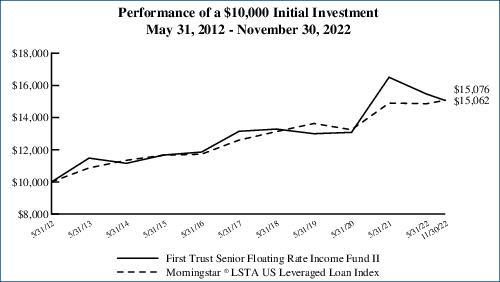

| Performance | |||||

| Average Annual Total Returns | |||||

| 6

Months Ended 11/30/22 |

1

Year Ended 11/30/22 |

5

Years Ended 11/30/22 |

10

Years Ended 11/30/22 |

Inception (5/25/04) to 11/30/22 | |

| Fund Performance(3) | |||||

| NAV | 1.78% | -2.61% | 3.13% | 4.24% | 4.01% |

| Market Value | -2.61% | -8.47% | 3.25% | 3.19% | 3.30% |

| Index Performance | |||||

| Morningstar®

LSTA® US Leveraged Loan Index(4) |

1.44% | -0.41% | 3.30% | 3.70% | 4.39% |

| (1) | Most recent distribution paid or declared through November 30, 2022. Subject to change in the future. |

| (2) | Distribution rates are calculated by annualizing the most recent distribution paid or declared through the report date and then dividing by Common Share Price or NAV, as applicable, as of November 30, 2022. Subject to change in the future. |

| (3) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per share for NAV returns and changes in Common Share Price for market value returns. From inception to October 12, 2010, Four Corners Capital Management, LLC served as the Fund’s sub-advisor. Effective October 12, 2010, the Leveraged Finance Team of First Trust Advisors L.Pon to October 12, 2010, Four Corners Capital Management, LLC served as the Fund’s sub-advisor. Effective October 12, 201. assumed the day-to-day responsibility for management of the Fund’s portfolio. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (4) | Formerly, S&P/LSTA Leveraged Loan Index. |

| (5) | The ratings are by S&P Global Ratings except where otherwise indicated. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations except for those debt obligations that are only privately rated. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest). Investment grade is defined as those issuers that have a long-term credit rating of BBB- or higher. The credit ratings shown relate to the creditworthiness of the issuers of the underlying securities in the Fund, and not to the Fund or its shares. Credit ratings are subject to change. |

| (6) | Percentages are based on long-term positions. Money market funds are excluded. |

| Industry Classification | %

of Total Long-Term Investments(6) |

| Software | 22.1% |

| Insurance | 12.5 |

| Media | 10.7 |

| Health Care Technology | 10.5 |

| Hotels, Restaurants & Leisure | 8.9 |

| Health Care Providers & Services | 7.6 |

| Commercial Services & Supplies | 3.0 |

| Containers & Packaging | 2.9 |

| Wireless Telecommunication Services | 2.1 |

| Electric Utilities | 2.1 |

| Diversified Telecommunication Services | 2.1 |

| Pharmaceuticals | 1.9 |

| Capital Markets | 1.9 |

| Food Products | 1.9 |

| Professional Services | 1.6 |

| Health Care Equipment & Supplies | 1.5 |

| Aerospace & Defense | 1.2 |

| Specialty Retail | 1.1 |

| Diversified Consumer Services | 1.0 |

| Diversified Financial Services | 0.7 |

| Trading Companies & Distributors | 0.7 |

| Electronic Equipment, Instruments & Components | 0.6 |

| Machinery | 0.3 |

| Auto Components | 0.3 |

| Communications Equipment | 0.2 |

| Food & Staples Retailing | 0.2 |

| Household Durables | 0.2 |

| Building Products | 0.1 |

| IT Services | 0.1 |

| Oil, Gas & Consumable Fuels | 0.0* |

| Entertainment | 0.0* |

| Life Sciences Tools & Services | 0.0* |

| Total | 100.0% |

| * | Amount is less than 0.1%. |

| Average Annual Total Returns | |||||

| 6

Months Ended 11/30/22 |

1

Year Ended 11/30/22 |

5

Years Ended 11/30/22 |

10

Years Ended 11/30/22 |

Inception (5/25/04) to 11/30/22 | |

| Fund Performance(1) | |||||

| NAV | 1.78% | -2.61% | 3.13% | 4.24% | 4.01% |

| Market Value | -2.61% | -8.47% | 3.25% | 3.19% | 3.30% |

| Index Performance | |||||

| Morningstar® LSTA® US Leveraged Loan Index* | 1.44% | -0.41% | 3.30% | 3.70% | 4.39% |

Performance figures assume reinvestment of all distributions and do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption or sale of Fund shares. An index is a statistical composite that tracks a specified financial market or sector. Unlike the Fund, the index does not actually hold a portfolio of securities and therefore does not incur the expenses incurred by the Fund. These expenses negatively impact the performance of the Fund. The Fund’s past performance does not predict future performance.

| (1) | Total return is based on the combination of reinvested divided, capital gain, and return of capital distribution, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per Common Share for NAV returns and changes in Common Share price for market value returns. Total returns do not reflect sales load and are not annualized for period of less than one year. |

| * | Formerly, S&P/LSTA Leveraged Loan Index. |

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) – 109.3% | ||||||||

| Aerospace & Defense – 1.4% | ||||||||

| $4,082,724 |

Transdigm, Inc., Tranche G Refinancing TL, 3 Mo. LIBOR + 2.25%, 0.00% Floor |

5.92% | 08/22/24 | $4,062,678 | ||||

| Application Software – 20.5% | ||||||||

| 7,114,966 |

Applied Systems, Inc., 1st Lien Term Loan, 3 Mo. LIBOR + 3.00%, 0.50% Floor |

6.67% | 09/19/24 | 7,086,648 | ||||

| 1,462,693 |

Applied Systems, Inc., 2nd Lien Term Loan, 3 Mo. LIBOR + 5.50%, 0.75% Floor |

9.17% | 09/19/25 | 1,448,066 | ||||

| 1,527,408 |

ConnectWise, LLC, Term Loan B, 3 Mo. LIBOR + 3.50%, 0.50% Floor |

7.17% | 09/30/28 | 1,464,020 | ||||

| 5,118,134 |

Epicor Software Corp., First Lien Term Loan C, 1 Mo. LIBOR + 3.25%, 0.75% Floor |

7.32% | 07/30/27 | 4,936,850 | ||||

| 82,458 |

Flexera Software, LLC, 2020 Term Loan B, 1 Mo. LIBOR + 3.75%, 0.75% Floor |

7.83% | 01/26/28 | 79,297 | ||||

| 4,385,854 |

Gainwell Acquisition Corp. (fka Milano), Term Loan B, 3 Mo. LIBOR + 4.00%, 0.75% Floor |

7.67% | 10/01/27 | 4,271,822 | ||||

| 3,343,529 |

Greeneden U.S. Holdings II, LLC (Genesys Telecommunications Laboratories, Inc.), Initial Dollar Term Loan, 1

Mo. LIBOR + 4.00%, 0.75% Floor |

8.07% | 12/01/27 | 3,241,150 | ||||

| 611,678 |

Hyland Software, Inc., 2nd Lien Term Loan, 1 Mo. LIBOR + 6.25%, 0.75% Floor |

10.32% | 07/10/25 | 576,892 | ||||

| 2,005,649 |

Hyland Software, Inc., Term Loan B, 1 Mo. LIBOR + 3.50%, 0.75% Floor |

7.57% | 07/01/24 | 1,974,320 | ||||

| 4,496,967 |

Internet Brands, Inc. (Web MD/MH Sub I., LLC), 2020 June New Term Loan, 1 Mo. LIBOR + 3.75%, 1.00% Floor |

7.82% | 09/15/24 | 4,370,513 | ||||

| 1,265,863 |

Internet Brands, Inc. (Web MD/MH Sub I., LLC), 2nd Lien Term Loan, 3 Mo. SOFR + 6.25%, 0.00% Floor |

10.65% | 02/23/29 | 1,134,530 | ||||

| 8,465,748 |

Internet Brands, Inc. (Web MD/MH Sub I., LLC), Initial Term Loan, 1 Mo. LIBOR + 3.75%, 0.00% Floor |

7.82% | 09/13/24 | 8,229,385 | ||||

| 279,886 |

ION Trading Technologies Limited, Term Loan B, 3 Mo. LIBOR + 4.75%, 0.00% Floor |

8.42% | 04/01/28 | 267,291 | ||||

| 4,805,130 |

LogMeIn, Inc. (GoTo Group, Inc.), Term Loan B, 1 Mo. LIBOR + 4.75%, 0.00% Floor |

8.77% | 08/31/27 | 3,073,265 | ||||

| 2,177,572 |

McAfee Corp. (Condor Merger Sub, Inc.), Term Loan B, 1 Mo. SOFR + 3.75%, 0.50% Floor |

7.64% | 02/28/29 | 2,064,621 | ||||

| 361,174 |

N-Able, Inc., Term Loan B, 3 Mo. LIBOR + 3.00%, 0.50% Floor |

7.73% | 07/19/28 | 349,887 | ||||

| 2,092,956 |

Open Text Corporation (GXS), New Term Loan, 1 Mo. SOFR + 3.50%, 0.50% Floor |

7.39% | 12/31/29 | 2,031,046 | ||||

| 2,209,510 |

Open Text Corporation (GXS), Term Loan, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.82% | 05/30/25 | 2,163,663 | ||||

| 912,941 |

RealPage, Inc., Second Lien Term Loan, 1 Mo. LIBOR + 6.50%, 0.75% Floor |

10.57% | 04/22/29 | 873,575 | ||||

| 5,731,488 |

RealPage, Inc., Term Loan B, 1 Mo. LIBOR + 3.00%, 0.50% Floor |

7.07% | 04/24/28 | 5,477,182 | ||||

| 3,073,447 |

SolarWinds Holdings, Inc., Initial Term Loan. 1 Mo. SOFR+ 4.00%, 0.00% Floor |

7.95% | 02/17/27 | 3,017,757 | ||||

| 488,794 |

Solera Holdings, Inc. (Polaris Newco), Term Loan B, 3 Mo. LIBOR + 4.00%, 0.50% Floor |

7.67% | 06/04/28 | 445,565 | ||||

| 232,552 |

Ultimate Kronos Group (UKG, Inc.), 2021 Term Loan, 3 Mo. LIBOR + 3.25%, 0.50% Floor |

7.00% | 05/03/26 | 224,315 | ||||

| 58,801,660 | ||||||||

| Asset Management & Custody Banks – 2.3% | ||||||||

| 3,789,412 |

Edelman Financial Engines Center, LLC, Term Loan B, 1 Mo. LIBOR + 3.50%, 0.75% Floor |

7.57% | 04/07/28 | 3,611,120 | ||||

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) (Continued) | ||||||||

| Asset Management & Custody Banks (Continued) | ||||||||

| $3,248,900 |

Edelman Financial Engines Center, LLC, Term Loan Second Lien, 1 Mo. LIBOR + 6.75%, 0.00% Floor |

10.82% | 07/20/26 | $2,921,996 | ||||

| 6,533,116 | ||||||||

| Auto Parts & Equipment – 0.3% | ||||||||

| 547,253 |

Clarios Global LP (Power Solutions), Term Loan B, 1 Mo. LIBOR + 3.25%, 0.00% Floor |

7.32% | 04/30/26 | 537,791 | ||||

| 519,374 |

Truck Hero, Inc., Term Loan B, 1 Mo. LIBOR + 3.75%, 0.75% Floor |

7.82% | 01/31/28 | 437,832 | ||||

| 975,623 | ||||||||

| Broadcasting – 4.5% | ||||||||

| 329,625 |

E.W. Scripps Company, Tranche B-3 Term Loan, 1 Mo. LIBOR + 2.75%, 0.75% Floor |

6.82% | 01/07/28 | 319,855 | ||||

| 1,519,988 |

Gray Television, Inc., Term Loan B2, 1 Mo. LIBOR + 2.50%, 0.00% Floor |

6.27% | 02/07/24 | 1,516,188 | ||||

| 1,719,808 |

Gray Television, Inc., Term Loan C, 1 Mo. LIBOR + 2.50%, 0.00% Floor |

6.27% | 01/02/26 | 1,669,074 | ||||

| 3,101,009 |

iHeartCommunications, Inc., Second Amendment Incremental Term Loan B, 1 Mo. LIBOR + 3.25%, 0.50% Floor |

7.32% | 05/01/26 | 2,900,405 | ||||

| 1,199,070 |

iHeartCommunications, Inc., Term Loan B, 1 Mo. LIBOR + 3.00%, 0.00% Floor |

7.07% | 05/01/26 | 1,121,777 | ||||

| 5,298,604 |

Nexstar Broadcasting, Inc., Incremental Term Loan B-4, 1 Mo. LIBOR + 2.50%, 0.00% Floor |

6.57% | 09/19/26 | 5,251,128 | ||||

| 21,121 |

Univision Communications, Inc., 2017 Replacement Repriced First Lien Term Loan C-5, 1 Mo. LIBOR + 2.75%, 1.00%

Floor |

6.82% | 03/15/24 | 21,068 | ||||

| 11,616 |

Univision Communications, Inc., 2021 Replacement New First Lien Term Loan, 1 Mo. LIBOR + 3.25%, 0.75% Floor |

7.32% | 03/15/26 | 11,399 | ||||

| 12,810,894 | ||||||||

| Building Products – 0.1% | ||||||||

| 264,822 |

Hunter Douglas, Inc. (Solis), Term Loan B, 3 Mo. SOFR + 3.50%, 0.50% Floor |

7.86% | 02/28/29 | 230,538 | ||||

| Cable & Satellite – 2.8% | ||||||||

| 4,647,746 |

Cablevision (aka CSC Holdings, LLC), March 2017 Term Loan B-1, 1 Mo. LIBOR + 2.25%, 0.00% Floor |

6.12% | 07/17/25 | 4,443,246 | ||||

| 3,537,674 |

Charter Communications Operating, LLC, Term Loan B1, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.83% | 04/30/25 | 3,478,524 | ||||

| 7,921,770 | ||||||||

| Casinos & Gaming – 1.5% | ||||||||

| 4,433,940 |

Golden Nugget, Inc. (Fertitta Entertainment, LLC), Initial Term Loan B, 1 Mo. SOFR + 4.00%, 0.50% Floor |

8.09% | 01/27/29 | 4,222,308 | ||||

| 217,409 |

Scientific Games Holdings LP (Scientific Games Lottery), Initial Dollar Term Loan, 3 Mo. SOFR + 3.50%, 0.50%

Floor |

7.10% | 04/04/29 | 207,354 | ||||

| 4,429,662 | ||||||||

| Coal & Consumable Fuels – 0.0% | ||||||||

| 36,248 |

Arch Coal, Inc., Term Loan B, 1 Mo. LIBOR + 2.75%, 1.00% Floor |

6.82% | 03/07/24 | 35,863 | ||||

| Communications Equipment – 0.3% | ||||||||

| 855,069 |

Commscope, Inc., Term Loan B, 1 Mo. LIBOR + 3.25%, 0.00% Floor |

7.32% | 04/06/26 | 820,601 | ||||

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) (Continued) | ||||||||

| Data Processing & Outsourced Services – 0.1% | ||||||||

| $200,204 |

Paysafe Holdings (US) Corp., Facility B1 Loan, 1 Mo. LIBOR + 2.75%, 0.50% Floor |

6.82% | 06/24/28 | $185,189 | ||||

| Education Services – 0.5% | ||||||||

| 1,471,918 |

Ascensus Holdings, Inc. (Mercury), First Lien Term Loan, 3 Mo. LIBOR + 3.50%, 0.50% Floor |

7.19% | 08/02/28 | 1,409,361 | ||||

| Electric Utilities – 2.5% | ||||||||

| 7,175,555 |

PG&E Corp., Term Loan B, 1 Mo. LIBOR + 3.00%, 0.50% Floor |

7.13% | 06/23/25 | 7,057,445 | ||||

| Electronic Equipment & Instruments – 0.7% | ||||||||

| 1,368,043 |

Chamberlain Group, Inc. (Chariot), Term Loan B, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 11/03/28 | 1,278,696 | ||||

| 870,089 |

Verifone Systems, Inc., Term Loan B, 3 Mo. LIBOR + 4.00%, 0.00% Floor |

8.36% | 08/20/25 | 784,307 | ||||

| 2,063,003 | ||||||||

| Environmental & Facilities Services – 2.6% | ||||||||

| 5,725,622 |

GFL Environmental, Inc., Term Loan B, 3 Mo. LIBOR + 3.00%, 0.50% Floor |

7.41% | 05/31/25 | 5,711,308 | ||||

| 2,089,291 |

Packers Holdings, LLC (PSSI), Term Loan B, 1 Mo. LIBOR + 3.25%, 0.75% Floor |

7.13% | 03/15/28 | 1,817,683 | ||||

| 7,528,991 | ||||||||

| Food Distributors – 0.3% | ||||||||

| 778,611 |

US Foods, Inc., Incremental B-2019 Term Loan, 1 Mo. LIBOR + 2.00%, 0.00% Floor |

6.07% | 08/31/26 | 767,041 | ||||

| Health Care Equipment – 0.0% | ||||||||

| 86,399 |

Embecta Corp., Initial Term Loan, 3 Mo. SOFR + 3.00%, 0.50% Floor |

6.55% | 03/31/29 | 82,997 | ||||

| Health Care Facilities – 0.8% | ||||||||

| 495,273 |

Ardent Health Services Inc (AHP Health Partners, Inc.), Term Loan B, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 08/24/28 | 481,445 | ||||

| 2,000,000 |

Select Medical Corporation, Term Loan B, 1 Mo. LIBOR + 2.50%, 0.00% Floor |

6.58% | 03/06/25 | 1,960,620 | ||||

| 2,442,065 | ||||||||

| Health Care Services – 5.6% | ||||||||

| 2,988,859 |

ADMI Corp. (Aspen Dental), 2020 Incremental Term Loan B2, 1 Mo. LIBOR + 3.38%, 0.50% Floor |

7.45% | 12/23/27 | 2,746,014 | ||||

| 2,512,004 |

ADMI Corp. (Aspen Dental), 2021 Incremental Term Loan B3, 1 Mo. LIBOR + 3.75%, 0.50% Floor |

7.82% | 12/23/27 | 2,292,204 | ||||

| 771,968 |

Aveanna Healthcare, LLC, 2021 Term Loan B, 1 Mo. LIBOR + 3.75%, 0.50% Floor |

7.77% | 07/15/28 | 592,485 | ||||

| 315,285 |

Brightspring Health (Phoenix Guarantor, Inc.), Incremental Term Loan B-3, 1 Mo. LIBOR + 3.50%, 0.00% Floor |

7.57% | 03/05/26 | 299,668 | ||||

| 3,289,639 |

CHG Healthcare Services, Inc., Term Loan B, 1 Mo. LIBOR + 3.25%, 0.50% Floor |

7.32% | 09/30/28 | 3,220,919 | ||||

| 2,690,425 |

DaVita, Inc., Term Loan B, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.82% | 08/12/26 | 2,599,623 | ||||

| 2,622,039 |

ExamWorks Group, Inc. (Electron Bidco), Term Loan B, 1 Mo. LIBOR + 3.00%, 0.50% Floor |

7.07% | 10/29/28 | 2,541,516 | ||||

| 1,990,294 |

Global Medical Response, Inc. (fka Air Medical), 2021 Refinancing Term Loan, 1 Mo. LIBOR + 4.25%, 1.00% Floor

|

8.09% | 10/02/25 | 1,573,328 | ||||

| 190,480 |

SCP Health (Onex TSG Intermediate Corp.), Term Loan B, 3 Mo. LIBOR + 4.75%, 0.75% Floor |

9.16% | 02/28/28 | 169,051 | ||||

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) (Continued) | ||||||||

| Health Care Services (Continued) | ||||||||

| $62,686 |

Sevita (National Mentor Holdings, Inc.), Term Loan B, 1 Mo. LIBOR + 3.75%, 0.75% Floor |

7.83% | 03/01/28 | $44,281 | ||||

| 77,454 |

Sevita (National Mentor Holdings, Inc.), Term Loan B, 3 Mo. LIBOR + 3.75%, 0.75% Floor |

7.43% | 03/01/28 | 54,713 | ||||

| 4,102 |

Sevita (National Mentor Holdings, Inc.), Term Loan C, 3 Mo. LIBOR + 3.75%, 0.75% Floor |

7.43% | 03/01/28 | 2,898 | ||||

| 16,136,700 | ||||||||

| Health Care Supplies – 1.7% | ||||||||

| 5,300,957 |

Medline Borrower, LP (Mozart), Initial Dollar Term Loan, 1 Mo. LIBOR + 3.25%, 0.50% Floor |

7.32% | 10/21/28 | 5,028,540 | ||||

| Health Care Technology – 12.0% | ||||||||

| 4,675,565 |

athenahealth, Inc. (Minerva Merger Sub, Inc.), Term Loan B, 1 Mo. SOFR + 3.50%, 0.50% Floor |

7.41% | 02/15/29 | 4,259,440 | ||||

| 3,892,779 |

Ciox Health (Healthport/CT Technologies Intermediate Holdings, Inc.), New Term Loan B, 1 Mo. LIBOR + 4.25%, 0.75%

Floor |

8.32% | 12/16/25 | 3,587,429 | ||||

| 1,808,384 |

Ensemble RCM, LLC (Ensemble Health), Term Loan B, 3 Mo. SOFR + 3.85%, 0.00% Floor |

7.94% | 08/01/26 | 1,752,631 | ||||

| 2,266,541 |

Mediware (Wellsky/Project Ruby Ultimate Parent Corp.), Term Loan B, 1 Mo. LIBOR + 3.25%, 0.75% Floor |

7.32% | 03/10/28 | 2,150,789 | ||||

| 1,209,782 |

Navicure, Inc. (Waystar Technologies, Inc.), Term Loan B, 1 Mo. LIBOR + 4.00%, 0.00% Floor |

8.07% | 10/23/26 | 1,185,587 | ||||

| 1,834,006 |

Press Ganey (Azalea TopCo, Inc.), Term Loan B, 1 Mo. LIBOR + 3.50%, 0.00% Floor |

7.57% | 07/25/26 | 1,694,163 | ||||

| 12,343,896 |

Verscend Technologies, Inc. (Cotiviti), New Term Loan B-1, 1 Mo. LIBOR + 4.00%, 0.00% Floor |

8.07% | 08/27/25 | 12,240,330 | ||||

| 7,647,683 |

Zelis Payments Buyer, Inc., New Term Loan B-1, 1 Mo. LIBOR + 3.50%, 0.00% Floor |

7.57% | 09/30/26 | 7,545,281 | ||||

| 34,415,650 | ||||||||

| Hotels, Resorts & Cruise Lines – 2.4% | ||||||||

| 460,665 |

Alterra Mountain Company, Term Loan B-2, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 08/17/28 | 453,755 | ||||

| 5,926,463 |

Four Seasons Holdings, Inc., Term Loan, 1 Mo. SOFR + 3.25%, 0.50% Floor |

7.44% | 11/30/29 | 5,915,381 | ||||

| 443,489 |

Wyndham Hotels & Resorts, Inc., Term Loan B, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.82% | 05/30/25 | 441,192 | ||||

| 6,810,328 | ||||||||

| Household Appliances – 0.2% | ||||||||

| 677,143 |

Traeger Grills (TGP Holdings III, LLC), Term Loan B, 1 Mo. LIBOR + 3.25%, 0.75% Floor |

7.32% | 06/24/28 | 541,972 | ||||

| Industrial Machinery – 0.4% | ||||||||

| 255,328 |

Filtration Group Corporation, 2021 Incremental Term Loan B, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 10/21/28 | 248,498 | ||||

| 213,229 |

Filtration Group Corporation, Initial Term Loan, 1 Mo. LIBOR + 3.00%, 0.00% Floor |

7.07% | 03/29/25 | 210,218 | ||||

| 618,674 |

TK Elevator Newco GMBH (Vertical U.S. Newco, Inc.), New Term Loan B1 (USD), 6 Mo. LIBOR + 3.50%, 0.50% Floor

|

6.87% | 07/31/27 | 592,380 | ||||

| 1,051,096 | ||||||||

| Insurance Brokers – 14.7% | ||||||||

| 4,509,949 |

Alliant Holdings I, LLC, 2019 New Term Loan, 1 Mo. LIBOR + 3.25%, 0.00% Floor |

7.32% | 05/10/25 | 4,414,112 | ||||

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) (Continued) | ||||||||

| Insurance Brokers (Continued) | ||||||||

| $7,543,348 |

Alliant Holdings I, LLC, Initial Term Loan, 1 Mo. LIBOR + 3.25%, 0.00% Floor |

7.32% | 05/09/25 | $7,391,274 | ||||

| 2,547,300 |

Alliant Holdings I, LLC, TLB-4 New Term Loan, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.44% | 11/06/27 | 2,469,302 | ||||

| 475,455 |

AssuredPartners, Inc., 2021 Term Loan B, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 02/13/27 | 456,080 | ||||

| 108,172 |

AssuredPartners, Inc., 2022 Incremental Term Loan B4, 1 Mo. SOFR + 4.25%, 0.50% Floor |

8.58% | 02/13/27 | 106,077 | ||||

| 1,818,498 |

AssuredPartners, Inc., Incremental Term Loan 2022, 1 Mo. SOFR + 3.50%, 0.50% Floor |

7.59% | 02/13/27 | 1,744,631 | ||||

| 6,445,470 |

AssuredPartners, Inc., Term Loan B, 1 Mo. LIBOR + 3.50%, 0.00% Floor |

7.57% | 02/12/27 | 6,189,005 | ||||

| 2,786,633 |

BroadStreet Partners, Inc., Term Loan B, 1 Mo. LIBOR + 3.00%, 0.00% Floor |

6.75% | 01/27/27 | 2,681,800 | ||||

| 35,901 |

HUB International Limited, Initial Term Loan B, 2 Mo. LIBOR + 2.75%, 0.00% Floor |

6.98% | 04/25/25 | 35,193 | ||||

| 13,714,085 |

HUB International Limited, Initial Term Loan B, 3 Mo. LIBOR + 2.75%, 0.00% Floor |

7.33% | 04/25/25 | 13,443,781 | ||||

| 2,451 |

HUB International Limited, New Term Loan B-3, 2 Mo. LIBOR + 2.75%, 0.75% Floor |

7.23% | 04/25/25 | 2,408 | ||||

| 960,599 |

HUB International Limited, New Term Loan B-3, 3 Mo. LIBOR + 2.75%, 0.75% Floor |

7.53% | 04/25/25 | 944,068 | ||||

| 453,751 |

Ryan Specialty Group, LLC, Term Loan B, 1 Mo. SOFR + 3.00%, 0.75% Floor |

7.19% | 09/01/27 | 450,234 | ||||

| 1,729,760 |

USI, Inc. (fka Compass Investors, Inc.), 2022 New Term Loan, 1 Mo. SOFR + 3.75%, 0.50% Floor |

7.68% | 11/30/29 | 1,699,801 | ||||

| 42,027,766 | ||||||||

| Integrated Telecommunication Services – 2.3% | ||||||||

| 3,378,830 |

Numericable (Altice France SA or SFR), Term Loan B-11, 3 Mo. LIBOR + 2.75%, 0.00% Floor |

7.16% | 07/31/25 | 3,235,230 | ||||

| 751,031 |

Zayo Group Holdings, Inc., Incremental Term Loan B-2, 1 Mo. SOFR + 4.25%, 0.50% Floor |

8.34% | 03/09/27 | 583,506 | ||||

| 3,740,009 |

Zayo Group Holdings, Inc., Initial Dollar Term Loan, 1 Mo. LIBOR + 3.00%, 0.00% Floor |

7.07% | 03/09/27 | 2,810,542 | ||||

| 6,629,278 | ||||||||

| Managed Health Care – 0.7% | ||||||||

| 2,293,123 |

Multiplan, Inc. (MPH), Term Loan B, 3 Mo. LIBOR + 4.25%, 0.50% Floor |

8.98% | 08/31/28 | 1,963,487 | ||||

| Metal & Glass Containers – 0.2% | ||||||||

| 497,673 |

Berry Global, Inc., Term Loan Z, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.63% | 07/01/26 | 491,203 | ||||

| Office Services & Supplies – 0.2% | ||||||||

| 608,895 |

Dun & Bradstreet Corp., Refinancing Term Loan, 1 Mo. LIBOR + 3.25%, 0.00% Floor |

7.29% | 02/08/26 | 600,066 | ||||

| Packaged Foods & Meats – 2.2% | ||||||||

| 16,760 |

Hostess Brands, LLC (HB Holdings), Term Loan B, 1 Mo. LIBOR + 2.25%, 0.75% Floor |

6.32% | 08/03/25 | 16,643 | ||||

| 6,485,964 |

Hostess Brands, LLC (HB Holdings), Term Loan B, 3 Mo. LIBOR + 2.25%, 0.75% Floor |

6.66% | 08/03/25 | 6,440,692 | ||||

| 6,457,335 | ||||||||

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) (Continued) | ||||||||

| Paper Packaging – 3.3% | ||||||||

| $4,669,550 |

Graham Packaging Company, LP, Term Loan B, 1 Mo. LIBOR + 3.00%, 0.75% Floor |

7.07% | 08/04/27 | $4,558,648 | ||||

| 1,598,439 | Pactiv, LLC / Evergreen Packaging, LLC (fka Reynolds Group Holdings), Term Loan B-2, 1 Mo. LIBOR + 3.25%, 0.00% Floor | 7.32% | 02/05/26 | 1,573,600 | ||||

| 3,348,833 |

Pactiv, LLC / Evergreen Packaging, LLC (fka Reynolds Group Holdings), Tranche B-3 U.S. Term Loan, 1 Mo. LIBOR

+ 3.25%, 0.50% Floor |

7.32% | 09/20/28 | 3,295,988 | ||||

| 9,428,236 | ||||||||

| Pharmaceuticals – 2.0% | ||||||||

| 972,491 |

Jazz Pharmaceuticals, Inc., Term Loan B, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 05/05/28 | 963,981 | ||||

| 5,061 |

Mallinckrodt International Finance S.A., Amendment No. 2 Incremental Term Loan, 3 Mo. LIBOR + 5.25%, 0.75% Floor

|

8.73% | 09/30/27 | 3,964 | ||||

| 1,088,938 |

Nestle Skin Health (Sunshine Lux VII SARL/Galderma), 2021 Term Loan B-3, 3 Mo. LIBOR + 3.75%, 0.75% Floor |

7.42% | 10/02/26 | 1,032,793 | ||||

| 3,811,548 |

Parexel International Corp. (Phoenix Newco), First Lien Term Loan, 1 Mo. LIBOR + 3.25%, 0.50% Floor |

7.32% | 11/15/28 | 3,660,534 | ||||

| 5,661,272 | ||||||||

| Research & Consulting Services – 1.9% | ||||||||

| 4,173,518 |

Clarivate Analytics PLC (Camelot), Term Loan B, 1 Mo. LIBOR + 3.00%, 1.00% Floor |

7.07% | 10/31/26 | 4,101,775 | ||||

| 975,807 |

Corelogic, Inc., 2021 Incremental Term Loan B, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.63% | 06/02/28 | 802,602 | ||||

| 386,835 |

J.D. Power (Project Boost Purchaser, LLC), Non-Fungible 1st Lien Term Loan, 1 Mo. LIBOR + 3.50%, 0.50% Floor

|

7.57% | 05/26/26 | 372,329 | ||||

| 334,037 |

Veritext Corporation (VT TopCo, Inc.), Term Loan B-4, 1 Mo. LIBOR + 3.75%, 0.75% Floor |

7.82% | 08/10/25 | 324,433 | ||||

| 5,601,139 | ||||||||

| Restaurants – 6.4% | ||||||||

| 4,112,297 |

1011778 B.C. Unlimited Liability Company (Restaurant Brands) (aka Burger King/Tim Horton’s), Term Loan

B, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.82% | 11/14/26 | 4,030,051 | ||||

| 1,218,819 |

1011778 B.C. Unlimited Liability Company (Restaurant Brands) (aka Burger King/Tim Horton’s), Term Loan

B, 3 Mo. LIBOR + 1.75%, 0.00% Floor |

6.16% | 11/14/26 | 1,194,443 | ||||

| 7,553,655 |

IRB Holding Corp. (Arby’s/Inspire Brands), New Term Loan B 2022, 1 Mo. LIBOR + 2.75%, 1.00% Floor |

6.82% | 02/05/25 | 7,410,664 | ||||

| 1,965,000 |

IRB Holding Corp. (Arby’s/Inspire Brands), Term Loan B-3, 1 Mo. SOFR + 3.10%, 0.75% Floor |

6.89% | 12/15/27 | 1,888,365 | ||||

| 3,880,000 |

Portillo’s Holdings, LLC, Term Loan B, 1 Mo. LIBOR + 5.50%, 1.00% Floor |

9.57% | 08/30/24 | 3,847,680 | ||||

| 18,371,203 | ||||||||

| Security & Alarm Services – 0.2% | ||||||||

| 549,406 |

Garda World Security Corporation, Second Lien Term Loan B-3, 3 Mo. LIBOR + 4.25%, 0.00% Floor |

8.93% | 10/30/26 | 526,469 | ||||

| Specialized Consumer Services – 0.7% | ||||||||

| 926,400 |

Asurion, LLC, Inc. Amendment No. 6 Term Loan, 1 Mo. LIBOR + 3.25%, 0.00% Floor |

7.32% | 12/23/26 | 809,053 | ||||

| Principal Value |

Description | Rate (a) | Stated Maturity (b) |

Value | ||||

| SENIOR FLOATING-RATE LOAN INTERESTS (c) (Continued) | ||||||||

| Specialized Consumer Services (Continued) | ||||||||

| $1,698,479 |

Asurion, LLC, New B-8 Term Loan, 1 Mo. LIBOR + 5.25%, 0.00% Floor |

9.32% | 01/31/28 | $1,306,130 | ||||

| 2,115,183 | ||||||||

| Specialized Finance – 0.9% | ||||||||

| 850,305 |

Radiate Holdco, LLC (Astound), Term Loan B, 1 Mo. LIBOR + 3.25%, 0.75% Floor |

7.32% | 09/25/26 | 743,881 | ||||

| 731,007 |

WCG Purchaser Corp. (WIRB- Copernicus Group), Initial Term Loan B, 1 Mo. LIBOR + 4.00%, 0.00% Floor |

8.07% | 01/08/27 | 685,319 | ||||

| 1,211,918 |

WCG Purchaser Corp. (WIRB- Copernicus Group), Initial Term Loan B, 3 Mo. LIBOR + 4.00%, 0.00% Floor |

7.67% | 01/08/27 | 1,136,173 | ||||

| 2,565,373 | ||||||||

| Specialty Stores – 1.3% | ||||||||

| 2,770,775 |

Petco Health and Wellness Company, Inc., 2021 Replacement Dollar Term Loan, 3 Mo. LIBOR + 3.25%, 0.75% Floor

|

6.92% | 03/03/28 | 2,681,889 | ||||

| 1,074,628 |

Petsmart, Inc., Initial Term Loan B, 1 Mo. LIBOR + 3.75%, 0.75% Floor |

7.82% | 02/12/28 | 1,031,256 | ||||

| 3,713,145 | ||||||||

| Systems Software – 5.5% | ||||||||

| 2,689,180 |

BMC Software Finance, Inc. (Boxer Parent), Initial Term Loan, 1 Mo. LIBOR + 3.75%, 0.00% Floor |

7.82% | 10/02/25 | 2,575,912 | ||||

| 883,272 |

Idera, Inc., Term Loan B, 3 Mo. LIBOR + 3.75%, 0.75% Floor |

7.50% | 02/15/28 | 835,063 | ||||

| 1,781,852 |

Misys Financial Software Ltd. (Almonde, Inc.) (Finastra), Term Loan B, 3 Mo. LIBOR + 3.50%, 1.00% Floor |

6.87% | 06/13/24 | 1,608,531 | ||||

| 885,870 |

Proofpoint, Inc., Term Loan B, 3 Mo. LIBOR + 3.25%, 0.50% Floor |

7.98% | 08/31/28 | 851,268 | ||||

| 1,962,470 |

Sophos Group PLC (Surf), Term Loan B-5, 3 Mo. LIBOR + 3.50%, 0.00% Floor |

6.67% | 03/05/27 | 1,879,889 | ||||

| 6,804,180 |

SS&C Technologies Holdings, Inc., Facility B1 USD, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.82% | 04/16/25 | 6,671,907 | ||||

| 1,282,564 |

SUSE (Marcel Lux IV SARL), 2021 Refinancing Term Loan, Daily SOFR + 3.25%, 0.00% Floor |

7.16% | 03/15/26 | 1,260,119 | ||||

| 15,682,689 | ||||||||

| Trading Companies & Distributors – 0.8% | ||||||||

| 2,326,073 |

SRS Distribution, Inc., 2022 Refinancing Term Loan, 1 Mo. LIBOR + 3.50%, 0.50% Floor |

7.57% | 06/04/28 | 2,230,122 | ||||

| 113,313 |

SRS Distribution, Inc., Term Loan B, 1 Mo. SOFR + 3.60%, 0.50% Floor |

7.69% | 06/04/28 | 108,249 | ||||

| 2,338,371 | ||||||||

| Wireless Telecommunication Services – 2.5% | ||||||||

| 7,272,834 |

SBA Senior Finance II, LLC, Term Loan B, 1 Mo. LIBOR + 1.75%, 0.00% Floor |

5.83% | 04/11/25 | 7,221,924 | ||||

|

Total Senior Floating-Rate Loan Interests |

313,536,922 | |||||||

| (Cost $324,453,078) | ||||||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (c) – 8.8% | ||||||||

| Application Software – 0.1% | ||||||||

| 560,000 |

GoTo Group, Inc. (d) |

5.50% | 09/01/27 | 328,678 | ||||

| Principal Value |

Description | Stated Coupon |

Stated Maturity |

Value | ||||

| CORPORATE BONDS AND NOTES (c) (Continued) | ||||||||

| Broadcasting – 2.7% | ||||||||

| $1,000,000 |

Gray Television, Inc. (d) |

5.88% | 07/15/26 | $922,500 | ||||

| 2,000,000 |

Gray Television, Inc. (d) |

7.00% | 05/15/27 | 1,841,250 | ||||

| 52,000 |

iHeartCommunications, Inc. (d) |

5.25% | 08/15/27 | 46,386 | ||||

| 3,043,000 |

Nexstar Media, Inc. (d) |

5.63% | 07/15/27 | 2,873,307 | ||||

| 2,395,000 |

Sirius XM Radio, Inc. (d) |

3.13% | 09/01/26 | 2,165,176 | ||||

| 7,848,619 | ||||||||

| Cable & Satellite – 2.9% | ||||||||

| 7,000,000 |

CCO Holdings, LLC / CCO Holdings Capital Corp. (d) |

5.13% | 05/01/27 | 6,633,305 | ||||

| 2,000,000 |

CSC Holdings, LLC (d) |

7.50% | 04/01/28 | 1,561,710 | ||||

| 8,195,015 | ||||||||

| Casinos & Gaming – 0.4% | ||||||||

| 572,000 |

Fertitta Entertainment, LLC / Fertitta Entertainment Finance Co., Inc. (d) |

4.63% | 01/15/29 | 505,680 | ||||

| 572,000 |

VICI Properties, L.P. / VICI Note Co., Inc. (d) |

4.25% | 12/01/26 | 532,801 | ||||

| 1,038,481 | ||||||||

| Health Care Facilities – 1.7% | ||||||||

| 2,500,000 |

Tenet Healthcare Corp. (d) |

6.25% | 02/01/27 | 2,398,600 | ||||

| 2,500,000 |

Tenet Healthcare Corp. (d) |

5.13% | 11/01/27 | 2,356,963 | ||||

| 4,755,563 | ||||||||

| Health Care Services – 0.2% | ||||||||

| 376,000 |

DaVita, Inc. (d) |

4.63% | 06/01/30 | 304,930 | ||||

| 226,000 |

DaVita, Inc. (d) |

3.75% | 02/15/31 | 166,453 | ||||

| 324,000 |

Global Medical Response, Inc. (d) |

6.50% | 10/01/25 | 244,392 | ||||

| 715,775 | ||||||||

| Insurance Brokers – 0.3% | ||||||||

| 359,000 |

AmWINS Group, Inc. (d) |

4.88% | 06/30/29 | 310,638 | ||||

| 500,000 |

AssuredPartners, Inc. (d) |

7.00% | 08/15/25 | 480,538 | ||||

| 791,176 | ||||||||

| Integrated Telecommunication Services – 0.2% | ||||||||

| 769,000 |

Zayo Group Holdings, Inc. (d) |

4.00% | 03/01/27 | 552,057 | ||||

| Systems Software – 0.3% | ||||||||

| 1,007,000 |

SS&C Technologies, Inc. (d) |

5.50% | 09/30/27 | 964,008 | ||||

|

Total Corporate Bonds and Notes |

25,189,372 | |||||||

| (Cost $26,351,987) | ||||||||

| FOREIGN CORPORATE BONDS AND NOTES (c) – 0.6% | ||||||||

| Application Software – 0.0% | ||||||||

| 22,000 |

Open Text Corp. (d) |

3.88% | 02/15/28 | 18,585 | ||||

| Environmental & Facilities Services – 0.6% | ||||||||

| 1,554,000 |

GFL Environmental, Inc. (d) |

3.75% | 08/01/25 | 1,456,829 | ||||

| 305,000 |

GFL Environmental, Inc. (d) |

4.00% | 08/01/28 | 262,109 | ||||

| 1,718,938 | ||||||||

|

Total Foreign Corporate Bonds and Notes |

1,737,523 | |||||||

| (Cost $1,766,566) | ||||||||

| Shares | Description | Value | ||

| COMMON STOCKS (c) – 0.3% | ||||

| Pharmaceuticals – 0.3% | ||||

| 150,392 |

Akorn, Inc. (e) (f) |

$977,548 | ||

| (Cost $1,724,086) | ||||

| RIGHTS (c) – 0.1% | ||||

| Electric Utilities – 0.1% | ||||

| 106,607 |

Vistra Energy Corp., no expiration date (f) (g) |

131,500 | ||

| Life Sciences Tools & Services – 0.0% | ||||

| 1 |

New Millennium Holdco, Inc., Corporate Claim Trust, no expiration date (f) (g) (h) (i) |

0 | ||

| 1 |

New Millennium Holdco, Inc., Lender Claim Trust, no expiration date (f) (g) (h) (i) |

0 | ||

| 0 | ||||

|

Total Rights |

131,500 | |||

| (Cost $174,207) | ||||

| WARRANTS (c) – 0.0% | ||||

| Movies & Entertainment – 0.0% | ||||

| 315,514 |

Cineworld Group PLC, expiring 11/23/25 (f) (g) (j) |

19,013 | ||

| (Cost $0) | ||||

|

Total Investments – 119.1% |

341,591,878 | |||

| (Cost $354,469,924) | ||||

|

Outstanding Loans – (18.8)% |

(54,000,000) | |||

|

Net Other Assets and Liabilities – (0.3)% |

(882,337) | |||

|

Net Assets – 100.0% |

$286,709,541 | |||

| (a) | Senior Floating-Rate Loan Interests (“Senior Loans”) in which the Fund invests pay interest at rates which are periodically predetermined by reference to a base lending rate plus a premium. These base lending rates are generally (i) the lending rate offered by one or more major European banks, such as the LIBOR, (ii) the SOFR obtained from the U.S. Department of the Treasury’s Office of Financial Research, (iii) the prime rate offered by one or more United States banks or (iv) the certificate of deposit rate. Certain Senior Loans are subject to a LIBOR or SOFR floor that establishes a minimum LIBOR or SOFR rate. When a range of rates is disclosed, the Fund holds more than one contract within the same tranche with identical LIBOR or SOFR period, spread and floor, but different LIBOR or SOFR reset dates. |

| (b) | Senior Loans generally are subject to mandatory and/or optional prepayment. As a result, the actual remaining maturity of Senior Loans may be substantially less than the stated maturities shown. |

| (c) | All of these securities are available to serve as collateral for the outstanding loans. |

| (d) | This security, sold within the terms of a private placement memorandum, is exempt from registration upon resale under Rule 144A of the Securities Act of 1933, as amended (the “1933 Act”), and may be resold in transactions exempt from registration, normally to qualified institutional buyers. Pursuant to procedures adopted by the Fund’s Board of Trustees, this security has been determined to be liquid by First Trust Advisors L.P. (the “Advisor”). Although market instability can result in periods of increased overall market illiquidity, liquidity for each security is determined based on security specific factors and assumptions, which require subjective judgment. At November 30, 2022, securities noted as such amounted to $26,926,895 or 9.4% of net assets. |

| (e) | Security received in a transaction exempt from registration under the 1933 Act. The security may be resold pursuant to an exemption from registration under the 1933 Act, typically to qualified institutional buyers (see Note 2D - Restricted Securities in the Notes to Financial Statements). |

| (f) | Non-income producing security. |

| (g) | Pursuant to procedures adopted by the Fund’s Board of Trustees, this security has been determined to be illiquid by the Advisor. |

| (h) | This security is fair valued by the Advisor’s Pricing Committee in accordance with procedures approved by the Fund’s Board of Trustees, and in accordance with the provisions of the Investment Company Act of 1940 and rules thereunder, as amended. At November 30, 2022, securities noted as such are valued at $0 or 0.0% of net assets. |

| (i) | This security’s value was determined using significant unobservable inputs (see Note 2A – Portfolio Valuation in the Notes to Financial Statements). |

| (j) | This issuer has filed for protection in bankruptcy court. |

| LIBOR | London Interbank Offered Rate |

| SOFR | Secured Overnight Financing Rate |

| Total Value at 11/30/2022 |

Level

1 Quoted Prices |

Level

2 Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | |

|

Senior Floating-Rate Loan Interests* |

$ 313,536,922 | $ — | $ 313,536,922 | $ — |

|

Corporate Bonds and Notes* |

25,189,372 | — | 25,189,372 | — |

|

Foreign Corporate Bonds and Notes* |

1,737,523 | — | 1,737,523 | — |

|

Common Stocks* |

977,548 | — | 977,548 | — |

| Rights: | ||||

|

Electric Utilities |

131,500 | — | 131,500 | — |

|

Life Sciences Tools & Services |

—** | — | — | —** |

|

Warrants* |

19,013 | — | 19,013 | — |

|

Total Investments |

$ 341,591,878 | $— | $ 341,591,878 | $—** |

| * | See Portfolio of Investments for industry breakout. |

| ** | Investment is valued at $0. |

| ASSETS: | |

|

Investments, at value (Cost $354,469,924) |

$ 341,591,878 |

|

Cash |

8,617,477 |

| Receivables: | |

|

Investment securities sold |

20,522,381 |

|

Interest |

1,419,553 |

|

Prepaid expenses |

4,321 |

|

Total Assets |

372,155,610 |

| LIABILITIES: | |

|

Outstanding loans |

54,000,000 |

| Payables: | |

|

Investment securities purchased |

30,871,664 |

|

Investment advisory fees |

215,248 |

|

Interest and fees on loans |

124,940 |

|

Audit and tax fees |

42,539 |

|

Administrative fees |

28,360 |

|

Custodian fees |

12,340 |

|

Legal fees |

11,485 |

|

Trustees’ fees and expenses |

2,951 |

|

Shareholder reporting fees |

2,724 |

|

Transfer agent fees |

2,470 |

|

Financial reporting fees |

761 |

|

Unrealized depreciation on unfunded loan commitments |

126,559 |

|

Other liabilities |

4,028 |

|

Total Liabilities |

85,446,069 |

|

NET ASSETS |

$286,709,541 |

| NET ASSETS consist of: | |

|

Paid-in capital |

$ 355,520,483 |

|

Par value |

259,834 |

|

Accumulated distributable earnings (loss) |

(69,070,776) |

|

NET ASSETS |

$286,709,541 |

|

NET ASSET VALUE, per Common Share (par value $0.01 per Common Share) |

$11.03 |

|

Number of |

| INVESTMENT INCOME: | ||

|

Interest |

$ 12,570,272 | |

|

Dividends |

32,040 | |

|

Other |

36,248 | |

|

Total investment income |

12,638,560 | |

| EXPENSES: | ||

|

Investment advisory fees |

1,390,610 | |

|

Interest and fees on loans |

1,289,778 | |

|

Administrative fees |

126,787 | |

|

Shareholder reporting fees |

41,834 | |

|

Audit and tax fees |

37,206 | |

|

Legal fees |

26,707 | |

|

Custodian fees |

21,020 | |

|

Listing expense |

18,193 | |

|

Trustees’ fees and expenses |

9,105 | |

|

Transfer agent fees |

7,212 | |

|

Financial reporting fees |

4,616 | |

|

Other |

17,979 | |

|

Total expenses |

2,991,047 | |

|

NET INVESTMENT INCOME (LOSS) |

9,647,513 | |

| NET REALIZED AND UNREALIZED GAIN (LOSS): | ||

|

Net realized gain (loss) on investments |

(16,937,923) | |

| Net change in unrealized appreciation (depreciation) on: | ||

|

Investments |

11,368,149 | |

|

Unfunded loan commitments |

(54,034) | |

|

Net change in unrealized appreciation (depreciation) |

11,314,115 | |

|

NET REALIZED AND UNREALIZED GAIN (LOSS) |

(5,623,808) | |

|

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS |

$ 4,023,705 | |

| Six

Months Ended 11/30/2022 (Unaudited) |

Year Ended 5/31/2022 | ||

| OPERATIONS: | |||

|

Net investment income (loss) |

$ 9,647,513 | $ 14,768,290 | |

|

Net realized gain (loss) |

(16,937,923) | (1,184,588) | |

|

Net change in unrealized appreciation (depreciation) |

11,314,115 | (24,665,993) | |

|

Net increase (decrease) in net assets resulting from operations |

4,023,705 | (11,082,291) | |

| DISTRIBUTIONS TO SHAREHOLDERS FROM: | |||

|

Investment operations |

(11,029,948) | (14,904,773) | |

|

Return of capital |

— | (10,282,054) | |

|

Total distributions to shareholders |

(11,029,948) | (25,186,827) | |

| CAPITAL TRANSACTIONS: | |||

|

Proceeds from Common Shares reinvested |

— | 366,260 | |

|

Repurchase of Common Shares |

— | — | |

|

Net increase (decrease) in net assets resulting from capital transactions |

— | 366,260 | |

|

Total increase (decrease) in net assets |

(7,006,243) | (35,902,858) | |

| NET ASSETS: | |||

|

Beginning of period |

293,715,784 | 329,618,642 | |

|

End of period |

$ 286,709,541 | $ 293,715,784 | |

| CAPITAL TRANSACTIONS were as follows: | |||

|

Common Shares at beginning of period |

25,983,388 | 25,953,421 | |

|

Common Shares issued as reinvestment under the Dividend Reinvestment Plan |

— | 29,967 | |

|

Common Shares at end of period |

25,983,388 | 25,983,388 |

| Cash flows from operating activities: | ||

|

Net increase (decrease) in net assets resulting from operations |

$4,023,705 | |

| Adjustments to reconcile net increase (decrease) in net assets resulting from operations to net cash provided by operating activities: | ||

|

Purchases of investments |

(179,730,082) | |

|

Sales, maturities and paydown of investments |

251,833,263 | |

|

Net amortization/accretion of premiums/discounts on investments |

(845,360) | |

|

Net realized gain/loss on investments |

16,937,923 | |

|

Net change in unrealized appreciation/depreciation on investments and unfunded loan commitments |

(11,314,115) | |

| Changes in assets and liabilities: | ||

|

Increase in interest receivable |

(97,888) | |

|

Decrease in prepaid expenses |

16,916 | |

|

Decrease in interest and fees payable on loans |

(1,662) | |

|

Decrease in investment advisory fees payable |

(49,077) | |

|

Decrease in audit and tax fees payable |

(30,513) | |

|

Increase in legal fees payable |

8,735 | |

|

Decrease in shareholder reporting fees payable |

(17,658) | |

|

Decrease in administrative fees payable |

(1,488) | |

|

Increase in custodian fees payable |

4,534 | |

|

Decrease in transfer agent fees payable |

(8,307) | |

|

Decrease in trustees’ fees and expenses payable |

(152) | |

|

Decrease in financial reporting fees payable |

(10) | |

|

Increase in other liabilities payable |

292 | |

|

Cash provided by operating activities |

$80,729,056 | |

| Cash flows from financing activities: | ||

|

Distributions to Common Shareholders from investment operations |

(11,029,948) | |

|

Repayment of borrowings |

(104,000,000) | |

|

Proceeds from borrowings |

42,000,000 | |

|

Cash used in financing activities |

(73,029,948) | |

|

Increase in cash |

7,699,108 | |

|

Cash at beginning of period |

918,369 | |

|

Cash at end of period |

$8,617,477 | |

| Supplemental disclosure of cash flow information: | ||

|

Cash paid during the period for interest and fees |

$1,291,440 |

| Six

Months Ended 11/30/2022 (Unaudited) |

Year Ended May 31, | |||||||||||

| 2022 | 2021 | 2020 | 2019 | 2018 | ||||||||

|

Net asset value, beginning of period |

$ 11.30 | $ 12.70 | $ 12.46 | $ 13.70 | $ 14.05 | $ 14.28 | ||||||

| Income from investment operations: | ||||||||||||

|

Net investment income (loss) |

0.37 | 0.56 | 0.55 | 0.67 | 0.74 | 0.70 | ||||||

|

Net realized and unrealized gain (loss) |

(0.22) | (0.99) | 0.90 | (0.97) | (0.36) | (0.17) | ||||||

|

Total from investment operations |

0.15 | (0.43) | 1.45 | (0.30) | 0.38 | 0.53 | ||||||

| Distributions paid to shareholders from: | ||||||||||||

|

Net investment income |

(0.42) | (0.57) | (0.56) | (0.69) | (0.73) | (0.70) | ||||||

|

Return of capital |

— | (0.40) | (0.69) | (0.25) | — | (0.06) | ||||||

|

Total distributions paid to Common Shareholders |

(0.42) | (0.97) | (1.25) | (0.94) | (0.73) | (0.76) | ||||||

|

Common Share repurchases |

— | — | 0.04 | — | — | — | ||||||

|

Net asset value, end of period |

$ | $11.30 | $12.70 | $12.46 | $13.70 | $14.05 | ||||||

|

Market value, end of period |

$ | $10.90 | $12.60 | $11.12 | $11.98 | $12.99 | ||||||

|

Total return based on net asset value (a) |

1.78% | (3.64)% | 13.51% | (1.38)% | 3.44% | 4.24% | ||||||

|

Total return based on market value (a) |

(2.61)% | (6.31)% | 26.18% | 0.65% | (2.17)% | 1.05% | ||||||

| Ratios to average net assets/supplemental data: | ||||||||||||

|

Net assets, end of period (in 000’s) |

$ 286,710 | $ 293,716 | $ 329,619 | $ 332,267 | $ 365,804 | $ 375,015 | ||||||

|

Ratio of total expenses to average net assets |

2.08% (b) | 1.67% | 1.70% | 2.35% | 2.53% | 2.17% | ||||||

|

Ratio of total expenses to average net assets excluding interest expense |

1.18% (b) | 1.24% | 1.30% | 1.26% | 1.24% | 1.26% | ||||||

|

Ratio of net investment income (loss) to average net assets |

6.71% (b) | 4.64% | 4.37% | 4.98% | 5.34% | 4.94% | ||||||

|

Portfolio turnover rate |

39% | 45% | 78% | 64% | 58% | 101% | ||||||

| Indebtedness: | ||||||||||||

|

Total loans outstanding (in 000’s) |

$ 54,000 | $ 116,000 | $ 136,000 | $ 119,000 | $ 163,000 | $ 155,000 | ||||||

|

Asset coverage per $1,000 of indebtedness (c) |

$ 6,309 | $ 3,532 | $ 3,424 | $ 3,792 | $ 3,244 | $ 3,419 | ||||||

| (a) | Total return is based on the combination of reinvested dividend, capital gain and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan, and changes in net asset value per share for net asset value returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of future results. |

| (b) | Annualized. |

| (c) | Calculated by subtracting the Fund’s total liabilities (not including the loans outstanding) from the Fund’s total assets, and dividing by the outstanding loans balance in 000’s. |

| (1) | The terms “security” and “securities” used throughout the Notes to Financial Statements include Senior Loans. |

| 1) | the most recent price provided by a pricing service; |

| 2) | the fundamental business data relating to the borrower; |

| 3) | an evaluation of the forces which influence the market in which these securities are purchased and sold; |

| 4) | the type, size and cost of the security; |

| 5) | the financial statements of the borrower, or the financial condition of the country of issue; |

| 6) | the credit quality and cash flow of the borrower, or country of issue, based on the Pricing Committee’s, sub-advisor’s or portfolio manager’s analysis, as applicable, or external analysis; |

| 7) | the information as to any transactions in or offers for the security; |

| 8) | the price and extent of public trading in similar securities (or equity securities) of the borrower, or comparable companies; |

| 9) | the coupon payments; |

| 10) | the quality, value and salability of collateral, if any, securing the security; |

| 11) | the business prospects of the borrower, including any ability to obtain money or resources from a parent or affiliate and an assessment of the borrower’s management; |

| 12) | the prospects for the borrower’s industry, and multiples (of earnings and/or cash flows) being paid for similar businesses in that industry; |

| 13) | the borrower’s competitive position within the industry; |

| 14) | the borrower’s ability to access additional liquidity through public and/or private markets; and |

| 15) | other relevant factors. |

| 1) | benchmark yields; |

| 2) | reported trades; |

| 3) | broker/dealer quotes; |

| 4) | issuer spreads; |

| 5) | benchmark securities; |

| 6) | bids and offers; and |

| 7) | reference data including market research publications. |

| 1) | the last sale price on the exchange on which they are principally traded or, for Nasdaq and AIM securities, the official closing price; |

| 2) | the type of security; |

| 3) | the size of the holding; |

| 4) | the initial cost of the security; |

| 5) | transactions in comparable securities; |

| 6) | price quotes from dealers and/or third-party pricing services; |

| 7) | relationships among various securities; |

| 8) | information obtained by contacting the issuer, analysts, or the appropriate stock exchange; |

| 9) | an analysis of the issuer’s financial statements; |

| 10) | the existence of merger proposals or tender offers that might affect the value of the security; and |

| 11) | other relevant factors. |

| • | Level 1 – Level 1 inputs are quoted prices in active markets for identical investments. An active market is a market in which transactions for the investment occur with sufficient frequency and volume to provide pricing information on an ongoing basis. |

| • | Level 2 – Level 2 inputs are observable inputs, either directly or indirectly, and include the following: |

| o | Quoted prices for similar investments in active markets. |

| o | Quoted prices for identical or similar investments in markets that are non-active. A non-active market is a market where there are few transactions for the investment, the prices are not current, or price quotations vary substantially either over time or among market makers, or in which little information is released publicly. |

| o | Inputs other than quoted prices that are observable for the investment (for example, interest rates and yield curves observable at commonly quoted intervals, volatilities, prepayment speeds, loss severities, credit risks, and default rates). |

| o | Inputs that are derived principally from or corroborated by observable market data by correlation or other means. |

| • | Level 3 – Level 3 inputs are unobservable inputs. Unobservable inputs may reflect the reporting entity’s own assumptions about the assumptions that market participants would use in pricing the investment. |

| Borrower | Principal Value |

Commitment Amount |

Value | Unrealized Appreciation (Depreciation) | ||||

| athenahealth, Inc. (Minerva Merger Sub, Inc.), Term Loan | $ 794,455 | $ 791,140 | $ 723,748 | $ (67,392) | ||||

| Aveanna Healthcare LLC, Term Loan | 181,205 | 180,135 | 139,075 | (41,060) | ||||

| Traeger Grills (TGP Holdings III LLC), Term Loan | 89,286 | 88,929 | 71,463 | (17,466) | ||||

| Veritext Corporation (VT TopCo, Inc.), Term Loan | 22,309 | 22,309 | 21,668 | (641) | ||||

| $1,082,513 | $955,954 | $(126,559) |

| Security | Acquisition Date |

Shares | Current Price | Carrying Cost |

Value | %

of Net Assets |

| Akorn, Inc. | 10/15/2020 | 150,392 | $6.50 | $1,724,086 | $977,548 | 0.34% |

| Distributions paid from: | |

|

Ordinary income |

$14,904,773 |

|

Return of capital |

10,282,054 |

|

Undistributed ordinary income |

$— |

|

Undistributed capital gains |

— |

|

Total undistributed earnings |

— |

|

Accumulated capital and other losses |

(37,881,083) |

|

Net unrealized appreciation (depreciation) |

(24,183,450) |

|

Total accumulated earnings (losses) |

(62,064,533) |

|

Other |

— |

|

Paid-in capital |

355,780,317 |

|

Total net assets |

$293,715,784 |

| Tax Cost | Gross Unrealized Appreciation |

Gross Unrealized (Depreciation) |

Net

Unrealized Appreciation (Depreciation) | |||

| $354,469,924 | $600,911 | $(13,478,957) | $(12,878,046) |

| (1) | If Common Shares are trading at or above net asset value (“NAV”) at the time of valuation, the Fund will issue new shares at a price equal to the greater of (i) NAV per Common Share on that date or (ii) 95% of the market price on that date. |

| (2) | If Common Shares are trading below NAV at the time of valuation, the Plan Agent will receive the dividend or distribution in cash and will purchase Common Shares in the open market, on the NYSE or elsewhere, for the participants’ accounts. It is possible that the market price for the Common Shares may increase before the Plan Agent has completed its purchases. Therefore, the average purchase price per share paid by the Plan Agent may exceed the market price at the time of valuation, resulting in the purchase of fewer shares than if the dividend or distribution had been paid in Common Shares issued by the Fund. The Plan Agent will use all dividends and distributions received in cash to purchase Common Shares in the open market within 30 days of the valuation date except where temporary curtailment or suspension of purchases is necessary to comply with federal securities laws. Interest will not be paid on any uninvested cash payments. |

FUND ACCOUNTANT, AND

CUSTODIAN

PUBLIC ACCOUNTING FIRM

| (b) | Not applicable. |

Item 2. Code of Ethics.

Not applicable.

Item 3. Audit Committee Financial Expert.

Not applicable.

Item 4. Principal Accountant Fees and Services.

Not applicable.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

| (a) | Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to shareholders filed under Item 1 of this form. |

| (b) | Not applicable. |

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

| (a) | Not applicable. |

| (b) | There have been no changes, as of the date of filing, in any of the Portfolio Managers identified in response to paragraph (a)(1) of this item in the registrant’s most recent annual report on Form N-CSR. |

Item 9. Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no material changes to the procedures by which the shareholders may recommend nominees to the registrant’s board of directors, where those changes were implemented after the registrant last provided disclosure in response to the requirements of Item 407(c)(2)(iv) of Regulation S-K (17 CFR 229.407) (as required by Item 22(b)(15) of Schedule 14A (17 CFR 240.14a-101)), or this Item.

Item 11. Controls and Procedures.

| (a) | The registrant’s principal executive and principal financial officers, or persons performing similar functions, have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)). |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) that occurred during the period covered by this report that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting. |

Item 12. Disclosure of Securities Lending Activities for Closed-End Management Investment Companies.

| (a) | Not applicable. |

| (b) | Not applicable. |

Item 13. Exhibits.

| (a)(1) | Not applicable. |

| (a)(2) | Certifications pursuant to Rule 30a-2(a) under the 1940 Act and Section 302 of the Sarbanes-Oxley Act of 2002 are attached hereto. |

| (a)(3) | Not applicable. |

| (a)(4) | Not applicable. |

| (b) | Certifications pursuant to Rule 30a-2(b) under the 1940 Act and Section 906 of the Sarbanes-Oxley Act of 2002 are attached hereto. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| (Registrant) | First Trust Senior Floating Rate Income Fund II |

| By (Signature and Title)* | /s/ James M. Dykas | |

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

| Date: | February 2, 2023 |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By (Signature and Title)* | /s/ James M. Dykas | |

| James M. Dykas, President and Chief Executive Officer (principal executive officer) |

| Date: | February 2, 2023 |

| By (Signature and Title)* | /s/ Donald P. Swade | |

| Donald P. Swade, Treasurer, Chief Financial Officer and Chief Accounting Officer (principal financial officer) |

| Date: | February 2, 2023 |

* Print the name and title of each signing officer under his or her signature.