UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended | |||||

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to . | |||||

Commission file number: 000-50600

| ||||||||

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices, including zip code)

(843 ) 216-6200

(Registrant’s telephone number, including area code)

| Securities Registered Pursuant to Section 12(b) of the Act: | ||||||||

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on which Registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☑ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The number of shares of the registrant’s Common Stock outstanding as of May 1, 2023 was 53,862,559 .

TABLE OF CONTENTS

First Quarter 2023 Form 10-Q |  | 1 | ||||||

Blackbaud, Inc.

| CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | |||||||

This Quarterly Report on Form 10-Q, including the documents incorporated herein by reference, contains forward-looking statements that anticipate results based on our estimates, assumptions and plans that are subject to uncertainty. These "forward-looking statements" are made subject to the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements consist of, among other things, trend analyses, statements regarding future events, future financial performance, our anticipated growth, the effect of general economic and market conditions, our business strategy and our plan to build and grow our business, our operating results, our ability to successfully integrate acquired businesses and technologies, the effect of foreign currency exchange rate and interest rate fluctuations on our financial results, the impact of expensing stock-based compensation, the sufficiency of our capital resources, our ability to meet our ongoing debt and obligations as they become due, cybersecurity and data protection risks and related liabilities, and current or potential legal proceedings involving us, all of which are based on current expectations, estimates, and forecasts, and the beliefs and assumptions of our management. Words such as “believes,” “seeks,” “expects,” “may,” “might,” “should,” “intends,” “could,” “would,” “likely,” “will,” “targets,” “plans,” “anticipates,” “aims,” “projects,” “estimates” or any variations of such words and similar expressions are also intended to identify such forward-looking statements. These forward-looking statements are subject to risks, uncertainties and assumptions that are difficult to predict. Accordingly, they should not be viewed as assurances of future performance, and actual results may differ materially and adversely from those expressed in any forward-looking statements.

Important factors that could cause actual results to differ materially from our expectations expressed in forward-looking statements include, but are not limited to, those summarized under “Part II, Item 1A. Risk factors” and elsewhere in this report, in our Annual Report on Form 10-K for the year ended December 31, 2022 and in our other filings made with the United States Securities & Exchange Commission ("SEC"). Forward-looking statements represent our management's beliefs and assumptions only as of the date of this Quarterly Report on Form 10-Q. We undertake no obligation to update or revise any forward-looking statements, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statement, whether as a result of new information, future events or otherwise.

2 | | First Quarter 2023 Form 10-Q | ||||||

| PART I. FINANCIAL INFORMATION | |||||||

ITEM 1. FINANCIAL STATEMENTS

| Blackbaud, Inc. Condensed Consolidated Balance Sheets (Unaudited) | ||||||||

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | ||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash | ||||||||

Accounts receivable, net of allowance of $ | ||||||||

| Customer funds receivable | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Operating lease right-of-use assets | ||||||||

| Software and content development costs, net | ||||||||

| Goodwill | ||||||||

| Intangible assets, net | ||||||||

| Other assets | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities and stockholders’ equity | ||||||||

| Current liabilities: | ||||||||

| Trade accounts payable | $ | $ | ||||||

| Accrued expenses and other current liabilities | ||||||||

| Due to customers | ||||||||

| Debt, current portion | ||||||||

| Deferred revenue, current portion | ||||||||

| Total current liabilities | ||||||||

| Debt, net of current portion | ||||||||

| Deferred tax liability | ||||||||

| Deferred revenue, net of current portion | ||||||||

| Operating lease liabilities, net of current portion | ||||||||

| Other liabilities | ||||||||

| Total liabilities | ||||||||

| Commitments and contingencies (see Note 8) | ||||||||

| Stockholders’ equity: | ||||||||

Preferred stock; | ||||||||

Common stock, $ | ||||||||

| Additional paid-in capital | ||||||||

Treasury stock, at cost; | ( | ( | ||||||

| Accumulated other comprehensive income | ||||||||

| Retained earnings | ||||||||

| Total stockholders’ equity | ||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||

| The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||

First Quarter 2023 Form 10-Q | | 3 | ||||||

Blackbaud, Inc. Condensed Consolidated Statements of Comprehensive Loss (Unaudited) | ||||||||

| Three months ended March 31, | ||||||||

| (dollars in thousands, except per share amounts) | 2023 | 2022 | ||||||

| Revenue | ||||||||

| Recurring | $ | $ | ||||||

| One-time services and other | ||||||||

| Total revenue | ||||||||

| Cost of revenue | ||||||||

| Cost of recurring | ||||||||

| Cost of one-time services and other | ||||||||

| Total cost of revenue | ||||||||

| Gross profit | ||||||||

| Operating expenses | ||||||||

| Sales, marketing and customer success | ||||||||

| Research and development | ||||||||

| General and administrative | ||||||||

| Amortization | ||||||||

| Total operating expenses | ||||||||

| Loss from operations | ( | ( | ||||||

| Interest expense | ( | ( | ||||||

| Other income, net | ||||||||

| Loss before provision for income taxes | ( | ( | ||||||

| Income tax benefit | ( | ( | ||||||

| Net loss | $ | ( | $ | ( | ||||

| Loss per share | ||||||||

| Basic | $ | ( | $ | ( | ||||

| Diluted | $ | ( | $ | ( | ||||

| Common shares and equivalents outstanding | ||||||||

| Basic weighted average shares | ||||||||

| Diluted weighted average shares | ||||||||

| Other comprehensive (loss) income | ||||||||

| Foreign currency translation adjustment | $ | $ | ( | |||||

| Unrealized (loss) gain on derivative instruments, net of tax | ( | |||||||

| Total other comprehensive (loss) income | ( | |||||||

| Comprehensive loss | $ | ( | $ | ( | ||||

| The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||

4 | | First Quarter 2023 Form 10-Q | ||||||

| Blackbaud, Inc. Condensed Consolidated Statements of Cash Flows (Unaudited) | ||||||||

| Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| Cash flows from operating activities | ||||||||

| Net loss | $ | ( | $ | ( | ||||

| Adjustments to reconcile net loss to net cash provided by operating activities: | ||||||||

| Depreciation and amortization | ||||||||

| Provision for credit losses and sales returns | ||||||||

| Stock-based compensation expense | ||||||||

| Deferred taxes | ( | |||||||

| Amortization of deferred financing costs and discount | ||||||||

| Other non-cash adjustments | ( | ( | ||||||

| Changes in operating assets and liabilities, net of acquisition and disposal of businesses: | ||||||||

| Accounts receivable | ||||||||

| Prepaid expenses and other assets | ( | ( | ||||||

| Trade accounts payable | ||||||||

| Accrued expenses and other liabilities | ( | ( | ||||||

| Deferred revenue | ( | ( | ||||||

| Net cash provided by operating activities | ||||||||

| Cash flows from investing activities | ||||||||

| Purchase of property and equipment | ( | ( | ||||||

| Capitalized software and content development costs | ( | ( | ||||||

| Purchase of net assets of acquired companies, net of cash and restricted cash acquired | ( | |||||||

| Net cash used in investing activities | ( | ( | ||||||

| Cash flows from financing activities | ||||||||

| Proceeds from issuance of debt | ||||||||

| Payments on debt | ( | ( | ||||||

| Employee taxes paid for withheld shares upon equity award settlement | ( | ( | ||||||

| Change in due to customers | ( | ( | ||||||

| Change in customer funds receivable | ( | ( | ||||||

| Net cash used in financing activities | ( | ( | ||||||

| Effect of exchange rate on cash, cash equivalents and restricted cash | ( | |||||||

| Net decrease in cash, cash equivalents and restricted cash | ( | ( | ||||||

| Cash, cash equivalents and restricted cash, beginning of period | ||||||||

| Cash, cash equivalents and restricted cash, end of period | $ | $ | ||||||

The following table provides a reconciliation of cash and cash equivalents and restricted cash reported within the condensed consolidated balance sheets that sum to the total of the same such amounts shown above in the condensed consolidated statements of cash flows:

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | ||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash | ||||||||

| Total cash, cash equivalents and restricted cash in the statement of cash flows | $ | $ | ||||||

| The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||

First Quarter 2023 Form 10-Q | | 5 | ||||||

Blackbaud, Inc.

Condensed Consolidated Statements of Stockholders' Equity

(Unaudited)

| (dollars in thousands) | Common stock | Additional paid-in capital | Treasury stock | Accumulated other comprehensive income | Retained earnings | Total stockholders' equity | |||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Net loss | — | — | — | — | — | ( | ( | ||||||||||||||||

| Vesting of restricted stock units | — | — | — | — | |||||||||||||||||||

Employee taxes paid for | — | — | — | ( | — | — | ( | ||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||

| Restricted stock grants | — | — | — | — | |||||||||||||||||||

| Restricted stock cancellations | ( | — | — | — | — | — | — | ||||||||||||||||

| Other comprehensive loss | — | — | — | — | ( | — | ( | ||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| (dollars in thousands) | Common stock | Additional paid-in capital | Treasury stock | Accumulated other comprehensive income | Retained earnings | Total stockholders' equity | |||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||

| Balance at December 31, 2021 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||

| Net loss | — | — | — | — | — | ( | ( | ||||||||||||||||

| Stock issuance costs related to purchase of EVERFI | — | — | ( | — | — | — | ( | ||||||||||||||||

Retirements of common stock(1) | ( | — | ( | — | — | — | ( | ||||||||||||||||

| Vesting of restricted stock units | — | — | — | — | |||||||||||||||||||

Employee taxes paid for | — | — | — | ( | — | — | ( | ||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||

| Restricted stock grants | — | — | — | — | |||||||||||||||||||

| Restricted stock cancellations | ( | — | — | — | — | — | — | ||||||||||||||||

| Other comprehensive income | — | — | — | — | — | ||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||

(1)Represents shares retired after determining certain EVERFI's selling shareholders would be paid in cash, rather than shares of our common stock.

| The accompanying notes are an integral part of these condensed consolidated financial statements. | ||

6 | | First Quarter 2023 Form 10-Q | ||||||

| 1. Organization | ||

We are the leading software provider exclusively dedicated to powering social impact. Serving the nonprofit and education sectors, companies committed to social responsibility and individual change makers, our essential software is built to accelerate impact in fundraising, nonprofit financial management, digital giving, grantmaking, corporate social responsibility and education management. A remote-first company, we have operations in the United States, Australia, Canada, Costa Rica and the United Kingdom, supporting users in 100+ countries.

| 2. Basis of Presentation | ||

Unaudited condensed consolidated interim financial statements

The accompanying condensed consolidated interim financial statements have been prepared pursuant to the rules and regulations of the United States Securities and Exchange Commission ("SEC") for interim financial reporting. These consolidated statements are unaudited and, in the opinion of management, include all adjustments (consisting of normal recurring adjustments and accruals) necessary to state fairly the consolidated balance sheets, consolidated statements of comprehensive income, consolidated statements of cash flows and consolidated statements of stockholders’ equity, for the periods presented in accordance with accounting principles generally accepted in the United States ("U.S.") ("GAAP"). The consolidated balance sheet at December 31, 2022 has been derived from the audited consolidated financial statements at that date. Operating results and cash flows for the three months ended March 31, 2023 are not necessarily indicative of the results that may be expected for the fiscal year ending December 31, 2023, or any other future period. Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with GAAP have been omitted in accordance with the rules and regulations for interim reporting of the SEC. These condensed consolidated interim financial statements should be read in conjunction with the consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2022, and other forms filed with the SEC from time to time.

Basis of consolidation

The condensed consolidated financial statements include the accounts of Blackbaud, Inc. and its wholly owned subsidiaries. All intercompany balances and transactions have been eliminated in consolidation.

Reportable segment

We report our operating results and financial information in one operating and reportable segment. Our chief operating decision maker uses consolidated financial information to make operating decisions, assess financial performance and allocate resources. Our chief operating decision maker is our chief executive officer.

Use of estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during the reporting periods. On an ongoing basis, we reconsider and evaluate our estimates and assumptions, including those that impact revenue recognition, long-lived and intangible assets, income taxes, business combinations, stock-based compensation, capitalization of software and content development costs, our allowances for credit losses and sales returns, costs of obtaining contracts, valuation of derivative instruments, loss contingencies and insurance recoveries, among others. Changes in the facts or circumstances underlying these estimates could result in material changes and actual results could materially differ from these estimates.

First Quarter 2023 Form 10-Q | | 7 | ||||||

Recently issued accounting pronouncements

There are no recently issued accounting pronouncements that we expect to have a material impact on our consolidated financial statements when adopted in the future.

Summary of significant accounting policies

There have been no material changes to our significant accounting policies described in our Annual Report on Form 10-K for the year ended December 31, 2022, filed with the SEC on February 24, 2023.

| 3. Loss Per Share | ||

We compute basic loss per share by dividing net loss available to common stockholders by the weighted average number of common shares outstanding during the period. Diluted loss per share is computed by dividing net loss available to common stockholders by the weighted average number of common shares and dilutive potential common shares outstanding during the period. Diluted loss per share reflects the assumed exercise, settlement and vesting of all dilutive securities using the “treasury stock method” except when the effect is anti-dilutive. Potentially dilutive securities consist of shares issuable upon the exercise of stock options, settlement of stock appreciation rights and vesting of restricted stock awards and units. Diluted loss per share for the three months ended March 31, 2023 and 2022 was the same as basic loss per share as there were net losses in both periods and inclusion of potentially dilutive securities was anti-dilutive.

The following table sets forth the computation of basic and diluted loss per share:

Three months ended March 31, | ||||||||

| (dollars in thousands, except per share amounts) | 2023 | 2022 | ||||||

| Numerator: | ||||||||

| Net loss | $ | ( | $ | ( | ||||

| Denominator: | ||||||||

| Weighted average common shares | ||||||||

| Add effect of dilutive securities: | ||||||||

| Stock-based awards | ||||||||

| Weighted average common shares assuming dilution | ||||||||

| Loss per share | ||||||||

| Basic | $ | ( | $ | ( | ||||

| Diluted | $ | ( | $ | ( | ||||

| Anti-dilutive shares excluded from calculations of diluted loss per share | ||||||||

8 | | First Quarter 2023 Form 10-Q | ||||||

| 4. Fair Value Measurements | ||

We use a three-tier fair value hierarchy to measure fair value. This hierarchy prioritizes the inputs into three broad levels as follows:

•Level 1 - Quoted prices for identical assets or liabilities in active markets;

•Level 2 - Quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets in markets that are not active, and model-derived valuations in which all significant inputs and significant value drivers are observable in active markets; and

•Level 3 - Valuations derived from valuation techniques in which one or more significant inputs are unobservable.

Recurring fair value measurements

Financial assets and liabilities that are measured at fair value on a recurring basis consisted of the following, as of the dates indicated below:

| Fair value measurement using | |||||||||||||||||||||||

| (dollars in thousands) | Quoted Prices in Active Markets for Identical Assets and Liabilities (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | |||||||||||||||||||

| Fair value as of March 31, 2023 | |||||||||||||||||||||||

| Financial assets: | |||||||||||||||||||||||

| Interest rate swaps | $ | $ | $ | $ | |||||||||||||||||||

| Foreign currency forward contracts | |||||||||||||||||||||||

| Total financial assets | $ | $ | $ | $ | |||||||||||||||||||

| Fair value as of March 31, 2023 | |||||||||||||||||||||||

| Financial liabilities: | |||||||||||||||||||||||

| Interest rate swaps | $ | $ | $ | $ | |||||||||||||||||||

| Foreign currency forward contracts | |||||||||||||||||||||||

| Contingent consideration obligations | |||||||||||||||||||||||

| Total financial liabilities | $ | $ | $ | $ | |||||||||||||||||||

| Fair value as of December 31, 2022 | |||||||||||||||||||||||

| Financial assets: | |||||||||||||||||||||||

| Interest rate swaps | $ | $ | $ | $ | |||||||||||||||||||

| Foreign currency forward contracts | |||||||||||||||||||||||

| Total financial assets | $ | $ | $ | $ | |||||||||||||||||||

| Fair value as of December 31, 2022 | |||||||||||||||||||||||

| Financial liabilities: | |||||||||||||||||||||||

| Foreign currency forward contracts | $ | $ | $ | $ | |||||||||||||||||||

| Contingent consideration obligations | |||||||||||||||||||||||

| Total financial liabilities | $ | $ | $ | $ | |||||||||||||||||||

First Quarter 2023 Form 10-Q | | 9 | ||||||

Our derivative instruments within the scope of Accounting Standards Codification ("ASC") 815, Derivatives and Hedging, are required to be recorded at fair value. Our derivative instruments that are recorded at fair value include interest rate swaps and foreign currency forward contracts. See Note 7 to these condensed consolidated financial statements for additional information about our derivative instruments.

The fair value of our interest rate swaps and foreign currency forward contracts are based on model-driven valuations using Secured Overnight Financing Rate ("SOFR") rates and foreign currency forward rates, respectively, which are observable at commonly quoted intervals. Accordingly, our interest rate swaps and foreign currency forward contracts are classified within Level 2 of the fair value hierarchy. Our financial contracts that were indexed to LIBOR were modified to reference SOFR during the three months ended September 30, 2022. These modifications did not have a significant financial impact.

Contingent consideration obligations arise from business acquisitions. The fair values are based on discounted cash flow analyses reflecting a probability-weighted assessment approach derived from the likelihood of possible achievement of specified performance measures or events and captures the contractual nature of the contingencies, commercial risk, and the time value of money. As the fair value measurements for our contingent consideration obligations contain significant unobservable inputs, they are classified within Level 3 of the fair value hierarchy.

We believe the carrying amounts of our cash and cash equivalents, restricted cash, accounts receivable, trade accounts payable, accrued expenses and other current liabilities and due to customers approximate their fair values at March 31, 2023 and December 31, 2022, due to the immediate or short-term maturity of these instruments.

We believe the carrying amount of our debt approximates its fair value at March 31, 2023 and December 31, 2022, as the debt bears interest rates that approximate market value. As SOFR rates are observable at commonly quoted intervals, our debt under the 2020 Credit Facility (as defined below) is classified within Level 2 of the fair value hierarchy. Our fixed rate debt is also classified within Level 2 of the fair value hierarchy.

We did not transfer any assets or liabilities among the levels within the fair value hierarchy during the three months ended March 31, 2023.

Non-recurring fair value measurements

Assets and liabilities that are measured at fair value on a non-recurring basis include long-lived assets, intangible assets, goodwill and operating lease right-of-use ("ROU") assets. These assets are recognized at fair value during the period in which an acquisition is completed or at lease commencement, from updated estimates and assumptions during the measurement period, or when they are considered to be impaired. These non-recurring fair value measurements, primarily for long-lived assets, intangible assets acquired and operating lease ROU assets, are based on Level 3 unobservable inputs. In the event of an impairment, we determine the fair value of these assets other than goodwill using a discounted cash flow approach, which contains significant unobservable inputs and, therefore, is considered a Level 3 fair value measurement. The unobservable inputs in the analysis generally include future cash flow projections and a discount rate. For goodwill impairment testing, we estimate fair value using market-based methods including the use of market capitalization and consideration of a control premium.

| 5. Consolidated Financial Statement Details | ||

Restricted cash

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | ||||||

| Restricted cash due to customers | $ | $ | ||||||

Real estate escrow balances and other | ||||||||

| Total restricted cash | $ | $ | ||||||

10 | | First Quarter 2023 Form 10-Q | ||||||

Prepaid expenses and other assets

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | ||||||

Costs of obtaining contracts(1)(2) | $ | $ | ||||||

Prepaid software maintenance and subscriptions(3) | ||||||||

| Derivative instruments | ||||||||

Implementation costs for cloud computing arrangements, net(4)(5) | ||||||||

| Prepaid insurance | ||||||||

| Unbilled accounts receivable | ||||||||

| Taxes, prepaid and receivable | ||||||||

| Deferred tax assets | ||||||||

| Other assets | ||||||||

| Total prepaid expenses and other assets | ||||||||

| Less: Long-term portion | ||||||||

| Prepaid expenses and other current assets | $ | $ | ||||||

(1)Amortization expense from costs of obtaining contracts was $8.3 million and $8.5 million for the three months ended March 31, 2023 and 2022, respectively.

(2)The current portion of costs of obtaining contracts as of March 31, 2023 and December 31, 2022 was $28.5 million and $29.1 million, respectively.

(3)The current portion of prepaid software maintenance and subscriptions as of March 31, 2023 and December 31, 2022 was $32.6 million and $31.7 million, respectively.

(4)These costs primarily relate to the multi-year implementations of our new global enterprise resource planning and customer relationship management systems.

(5)Amortization expense from capitalized cloud computing implementation costs was insignificant for the three months ended March 31, 2023 and 2022, respectively. Accumulated amortization for these costs was $5.7 million and $5.2 million as of March 31, 2023 and December 31, 2022, respectively.

Accrued expenses and other liabilities

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | ||||||

Accrued legal costs(1) | $ | $ | ||||||

| Derivative instruments | ||||||||

| Customer credit balances | ||||||||

| Operating lease liabilities, current portion | ||||||||

| Accrued commissions and salaries | ||||||||

Taxes payable | ||||||||

Contingent consideration liability | ||||||||

| Accrued health care costs | ||||||||

| Accrued vacation costs | ||||||||

| Accrued transaction-based costs related to payments services | ||||||||

| Other liabilities | ||||||||

| Total accrued expenses and other liabilities | ||||||||

| Less: Long-term portion | ||||||||

| Accrued expenses and other current liabilities | $ | $ | ||||||

(1)All accrued legal costs are classified as current.

First Quarter 2023 Form 10-Q | | 11 | ||||||

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| Interest income | $ | $ | ||||||

| Currency revaluation (losses) gains | ( | |||||||

| Other income, net | ||||||||

| Other income, net | $ | $ | ||||||

| 6. Debt | ||

The following table summarizes our debt balances and the related weighted average effective interest rates, which includes the effect of interest rate swap agreements.

| Debt balance at | Weighted average effective interest rate at | ||||||||||||||||

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | March 31, 2023 | December 31, 2022 | |||||||||||||

| Credit facility: | |||||||||||||||||

| Revolving credit loans | $ | $ | % | % | |||||||||||||

| Term loans | % | % | |||||||||||||||

| Real estate loans | % | % | |||||||||||||||

| Other debt | % | % | |||||||||||||||

| Total debt | % | % | |||||||||||||||

| Less: Unamortized discount and debt issuance costs | |||||||||||||||||

| Less: Debt, current portion | % | % | |||||||||||||||

| Debt, net of current portion | $ | $ | % | % | |||||||||||||

2020 credit facility

In October 2020, we entered into a five-year $900.0 million senior credit facility (the "2020 Credit Facility"). At March 31, 2023, we were in compliance with our debt covenants under the 2020 Credit Facility.

Real estate loans

In August 2020, we completed the purchase of our global headquarters facility. As part of the purchase price, we assumed the seller’s obligations under two senior secured notes with a then-aggregate outstanding principal amount of $61.1 million (collectively, the “Real Estate Loans”). At March 31, 2023, we were in compliance with our debt covenants under the Real Estate Loans.

Other debt

From time to time, we enter into third-party financing agreements for purchases of software and related services for our internal use. Generally, the agreements are non-interest-bearing notes requiring annual payments. Interest associated with the notes is imputed at the rate we would incur for amounts borrowed under our then-existing credit facility at the inception of the notes.

12 | | First Quarter 2023 Form 10-Q | ||||||

The following table summarizes our currently effective supplier financing agreements as of March 31, 2023:

| (dollars in thousands) | Term in Months | Number of Annual Payments | First Annual Payment Due | Original Loan Value | ||||||||||

Effective dates of agreements (1): | ||||||||||||||

| December 2022 | 39 | 3 | January 2023 | $ | ||||||||||

| January 2023 | 36 | 3 | April 2023 | |||||||||||

(1)Represent noncash investing and financing transactions during the periods indicated as we purchased software and services by assuming directly related liabilities.

The changes in supplier financing obligations during the three months ended March 31, 2023, consisted of the following:

| (dollars in thousands) | Total | ||||

| Balance at December 31, 2022 | $ | ||||

Additions | |||||

Settlements | ( | ||||

| Balance at March 31, 2023 | $ | ||||

| 7. Derivative Instruments | ||

We generally use derivative instruments to manage our interest rate and foreign currency exchange risk. We currently have derivatives classified as cash flow hedges and net investment hedges. We do not enter into any derivatives for trading or speculative purposes.

All of our derivative instruments are governed by International Swap Dealers Association, Inc. master agreements with our counterparties. As of March 31, 2023 and December 31, 2022, we have presented the fair value of our derivative instruments at the gross amounts in the condensed consolidated balance sheet as the gross fair values of our derivative instruments equaled their net fair values.

Cash flow hedges

We have entered into interest rate swap agreements, which effectively convert portions of our variable rate debt under the 2020 Credit Facility to a fixed rate for the term of the swap agreements. We designated each of the interest rate swaps as cash flow hedges at the inception of the contracts. As of March 31, 2023 and December 31, 2022, the aggregate notional values of the interest rate swaps were $935.0 million and $435.0 million, respectively. All of the contracts have maturities on or before October 2028.

We have entered into foreign currency forward contracts to hedge revenues denominated in the Canadian Dollar ("CAD") against changes in the exchange rate with the United States Dollar ("USD"). We designated each of the forwards as cash flow hedges at the inception of the contracts. As of March 31, 2023 and December 31, 2022, the aggregate notional values of the foreign currency forward contracts designated as cash flow hedges that we held to buy USD in exchange for Canadian Dollars were $27.7 million CAD and $22.6 million CAD, respectively. All of the contracts have maturities of 12 months or less.

First Quarter 2023 Form 10-Q | | 13 | ||||||

Net investment hedges

We have entered into foreign currency forward contracts to hedge a portion of the foreign currency exposure that arises on translation of our investments denominated in British Pounds ("GBP") into USD. We designated each of these foreign currency forward contracts as net investment hedges at the inception of the contracts. As of March 31, 2023 and December 31, 2022, we had £14.0 million and £11.2 million, respectively, of foreign currency forward contracts designated as net investment hedges to reduce the volatility of the U.S. dollar value of a portion of our GBP-denominated investments.

The fair values of our derivative instruments were as follows as of:

| Asset derivatives | Liability derivatives | ||||||||||||||||||||||

| (dollars in thousands) | Balance sheet location | March 31, 2023 | December 31, 2022 | Balance sheet location | March 31, 2023 | December 31, 2022 | |||||||||||||||||

| Derivative instruments designated as hedging instruments: | |||||||||||||||||||||||

Foreign currency forward contracts, current portion | Prepaid expenses and other current assets | $ | $ | Accrued expenses and other current liabilities | $ | $ | |||||||||||||||||

Interest rate swaps, long-term | Other assets | Other liabilities | |||||||||||||||||||||

| Total derivative instruments designated as hedging instruments | $ | $ | $ | $ | |||||||||||||||||||

The effects of derivative instruments in cash flow and net investment hedging relationships were as follows:

Gain (loss) recognized in accumulated other comprehensive income as of | Location of gain (loss) reclassified from accumulated other comprehensive income into loss | Gain (loss) reclassified from accumulated other comprehensive income into loss | |||||||||

| (dollars in thousands) | March 31, 2023 | Three months ended March 31, 2023 | |||||||||

| Cash Flow Hedges | |||||||||||

| Interest rate swaps | $ | Interest expense | $ | ||||||||

| Foreign currency forward contracts | $ | Revenue | $ | ||||||||

| Net Investment Hedges | |||||||||||

| Foreign currency forward contracts | $ | ( | $ | ||||||||

| March 31, 2022 | Three months ended March 31, 2022 | ||||||||||

| Cash Flow Hedges | |||||||||||

| Interest rate swaps | $ | Interest expense | $ | ( | |||||||

Our policy requires that derivatives used for hedging purposes be designated and effective as a hedge of the identified risk exposure at the inception of the contract. Accumulated other comprehensive income (loss) includes unrealized gains or losses from the change in fair value measurement of our derivative instruments each reporting period and the related income tax expense or benefit. Excluding net investment hedges, changes in the fair value measurements of the derivative instruments and the related income tax expense or benefit are reflected as adjustments to accumulated other comprehensive income (loss) until the actual hedged expense is incurred or until the hedge is terminated at which point the unrealized gain (loss) and related tax effects are reclassified from accumulated other comprehensive income (loss) to current earnings. For net investment hedges, changes in the fair value measurements of the derivative instruments and the related income tax expense or benefit are reflected as adjustments to translation adjustment, a component of accumulated other comprehensive income (loss), and recognized in earnings only when the hedged GBP investment is liquidated. The estimated accumulated other comprehensive income as of March 31, 2023 that is expected to be reclassified into earnings within the next twelve months is

14 | | First Quarter 2023 Form 10-Q | ||||||

| 8. Commitments and Contingencies | ||

Leases

We have operating leases for corporate offices, subleased offices and certain equipment and furniture. As of March 31, 2023, we did not have any operating leases that had not yet commenced.

The following table summarizes the components of our lease expense:

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

Operating lease cost(1) | $ | $ | ||||||

| Variable lease cost | ||||||||

| Sublease income | ( | ( | ||||||

| Net lease cost | $ | $ | ||||||

(1)Includes short-term lease costs, which were immaterial.

Other commitments

The term loans under the 2020 Credit Facility require periodic principal payments. The balance of the term loans and any amounts drawn on the revolving credit loans are due upon maturity of the 2020 Credit Facility in October 2025. The Real Estate Loans also require periodic principal payments and the balance of the Real Estate Loans are due upon maturity in April 2038.

We have contractual obligations for third-party technology used in our solutions and for other services we purchase as part of our normal operations. In certain cases, these arrangements require a minimum annual purchase commitment by us. As of March 31, 2023, the remaining aggregate minimum purchase commitment under these arrangements was approximately $280.7 million through 2027.

Solution and service indemnifications

In the ordinary course of business, we provide certain indemnifications of varying scope to customers against claims of intellectual property infringement made by third parties arising from the use of our solutions or services. We have not identified any losses that might be covered by these indemnifications.

Legal proceedings

We are subject to legal proceedings and claims that arise in the ordinary course of business, as well as certain other non-ordinary course proceedings, claims and investigations, as described below. We make a provision for a loss contingency when it is both probable that a material liability has been incurred and the amount of the loss can be reasonably estimated. If only a range of estimated losses can be determined, we accrue an amount within the range that, in our judgment, reflects the most likely outcome; if none of the estimates within that range is a better estimate than any other amount, we accrue the low end of the range. For proceedings in which an unfavorable outcome is reasonably possible but not probable and an estimate of the loss or range of losses arising from the proceeding can be made, we disclose such an estimate, if material. If such a loss or range of losses is not reasonably estimable, we disclose that fact. We review any such loss contingency provisions at least quarterly and adjust them to reflect the impacts of negotiations, settlements, rulings, advice of legal counsel and other information and events pertaining to a particular case. We recognize insurance recoveries, if any, when they are probable of receipt. All associated costs due to third-party service providers and consultants, including legal fees, are expensed as incurred.

First Quarter 2023 Form 10-Q | | 15 | ||||||

Legal proceedings are inherently unpredictable. However, we believe that we have valid defenses with respect to the legal matters pending or threatened against us and intend to defend ourselves vigorously against all claims asserted. It is possible that our consolidated financial position, results of operations or cash flows could be materially negatively affected in any particular period by an unfavorable resolution of one or more of such legal proceedings.

Security incident

As previously disclosed, we are subject to risks and uncertainties as a result of a ransomware attack against us in May 2020 in which a cybercriminal removed a copy of a subset of data from our self-hosted environment (the "Security Incident"). Based on the nature of the Security Incident, our research and third party (including law enforcement) investigation, we do not believe that any data went beyond the cybercriminal, has been misused, or has been disseminated or otherwise made available publicly. Our investigation into the Security Incident by our cybersecurity team and third-party forensic advisors remains ongoing.

As a result of the Security Incident, we are currently subject to certain legal proceedings, claims and investigations, as discussed below, and could be the subject of additional legal proceedings, claims, inquiries and investigations in the future that might result in adverse judgments, settlements, fines, penalties or other resolution. To limit our exposure to losses related to claims against us, including data breaches such as the Security Incident, we maintain $50 million of insurance above a $250 thousand deductible payable by us. As noted below, this coverage has reduced our financial exposure related to the Security Incident.

We recorded expenses and offsetting probable insurance recoveries related to the Security Incident as follows:

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| Gross expense | $ | $ | ||||||

| Offsetting probable insurance recoveries | ( | |||||||

| Net expense | $ | $ | ||||||

The following summarizes our cumulative expenses, insurance recoveries recognized and insurance recoveries paid as of:

| (dollars in thousands) | March 31, 2023 | December 31, 2022 | ||||||

| Cumulative gross expense | $ | $ | ||||||

| Cumulative offsetting insurance recoveries recognized | ( | ( | ||||||

| Cumulative net expense | $ | $ | ||||||

| Cumulative offsetting insurance recoveries paid | $ | ( | $ | ( | ||||

Recorded expenses have consisted primarily of payments to third-party service providers and consultants, including legal fees, as well as settlement of the previously disclosed SEC investigation (as discussed below), settlements of customer claims and accruals for certain loss contingencies. Not included in the expenses discussed above were costs associated with enhancements to our cybersecurity program. We present expenses and insurance recoveries related to the Security Incident in general and administrative expense on our consolidated statements of comprehensive loss and as operating activities on our consolidated statements of cash flows. Total costs related to the Security Incident exceeded the limit of our insurance coverage during the first quarter of 2022. We expect to continue to experience significant expenses related to our response to the Security Incident, resolution of legal proceedings, claims and investigations, including those discussed below, and our efforts to further enhance our cybersecurity measures. For the three months ended March 31, 2023, we incurred net pre-tax expense of $17.8 million related to the Security Incident, which included $7.6 million for ongoing legal fees and an additional accrual for loss contingencies of $10.2 million. During the three months ended March 31, 2023, we had net cash outlays of $9.2 million related to the Security Incident, which included ongoing legal fees and the $3.0 million civil penalty paid related to the SEC settlement (as discussed below). In line with our policy, legal fees are expensed as incurred. For full year 2023, we currently expect net pre-tax expense of approximately $20.0 million to $30.0 million and net cash outlays of approximately

16 | | First Quarter 2023 Form 10-Q | ||||||

$25.0 million to $35.0 million for ongoing legal fees related to the Security Incident. Not included in these ranges are our previous settlements or current accruals for loss contingencies related to the matters discussed below.

As of March 31, 2023, we have recorded approximately $30.2 million in aggregate liabilities for loss contingencies based primarily on recent negotiations with certain governmental agencies related to the Security Incident that we believe we can reasonably estimate in accordance with our loss contingency procedures described above. It is reasonably possible that our estimated or actual losses may change in the near term for those matters and be materially in excess of the amounts accrued, but we are unable at this time to reasonably estimate the possible additional loss.

There are other Security Incident-related matters, including customer claims, customer constituent class actions and governmental investigations, for which we have not recorded a liability for a loss contingency as of March 31, 2023 because we are unable at this time to reasonably estimate the possible loss or range of loss. Each of these matters could, separately or in the aggregate, result in an adverse judgment, settlement, fine, penalty or other resolution, the amount, scope and timing of which we are currently unable to predict, but could have a material adverse impact on our results of operations, cash flows or financial condition.

Customer claims. To date, we have received approximately 260 specific requests for reimbursement of expenses, approximately 205 (or 79 %) have been fully resolved and closed. We have also received approximately 400 reservations of the right to seek expense recovery in the future from customers or their attorneys in the U.S., U.K. and Canada related to the Security Incident. We have also received notices of proposed claims on behalf of a number of U.K. data subjects, which we are reviewing. In addition, insurance companies representing various customers’ interests through subrogation claims have contacted us, and certain insurance companies have filed subrogation claims in court. Customer and insurer subrogation claims generally seek reimbursement of their costs and expenses associated with notifying their own customers of the Security Incident and taking steps to assure that personal information has not been compromised as a result of the Security Incident. Our review of customer and subrogation claims includes analyzing individual customer contracts into which we have entered, the specific claims made and applicable law.

Customer constituent class actions. Presently, we are a defendant in 19 putative consumer class action cases [17 in U.S. federal courts (which have been consolidated under multi district litigation to a single federal court) and 2 in Canadian courts] alleging harm from the Security Incident. The plaintiffs in these cases, who purport to represent various classes of individual constituents of our customers, generally claim to have been harmed by alleged actions and/or omissions by us in connection with the Security Incident and assert a variety of common law and statutory claims seeking monetary damages, injunctive relief, costs and attorneys’ fees and other related relief.

Lawsuits that are putative class actions require a plaintiff to satisfy a number of procedural requirements before proceeding to trial. These requirements include, among others, demonstration to a court that the law proscribes in some manner our activities, the making of factual allegations sufficient to suggest that our activities exceeded the limits of the law and a determination by the court—known as class certification—that the law permits a group of individuals to pursue the case together as a class. If these procedural requirements are not met, the lawsuit cannot proceed as a class action and the plaintiff may lose the financial incentive to proceed with the case. We are currently engaged in court proceedings to determine whether this will proceed as a class action. Frequently, a court’s determination as to these procedural requirements is subject to appeal to a higher court. As a result of these uncertainties, we may be unable to determine the probability of loss until, or after, a court has finally determined that a plaintiff has satisfied the applicable class action procedural requirements.

Furthermore, for putative class actions, it is often not possible to reasonably estimate the possible loss or a range of loss amounts, even where we have determined that a loss is reasonably possible. Generally, class actions involve a large number of people and raise complex legal and factual issues that result in uncertainty as to their outcome and, ultimately, making it difficult for us to estimate the amount of damages that a plaintiff might successfully prove. This analysis is further complicated by the fact that the plaintiffs lack contractual privity with us.

First Quarter 2023 Form 10-Q | | 17 | ||||||

Governmental investigations. To date, we have received a consolidated, multi-state Civil Investigative Demand issued on behalf of 49 state Attorneys General and the District of Columbia, a separate Civil Investigative Demand from the office of the Indiana Attorney General and a separate Civil Investigative Demand from the office of the California Attorney General relating to the Security Incident. We have been in discussions, directly with certain Attorneys General or indirectly through an executive committee of the multi-state group of Attorneys General, about potential resolution of issues arising from these investigations. Although we are hopeful that we can resolve these matters on acceptable terms, there is no assurance that we will be able to do so on terms acceptable to us and to any or all such states.

We also are subject to the following pending governmental actions:

•an investigation by the U.S. Federal Trade Commission;

•an investigation by the U.S. Department of Health and Human Services;

•an investigation by the Office of the Australian Information Commissioner; and

•an investigation by the Office of the Privacy Commissioner of Canada.

As previously disclosed, on March 9, 2023, the Company reached a settlement with the SEC in connection with the Security Incident. This settlement fully resolves the previously disclosed SEC investigation of the Security Incident and is further described in an SEC cease-and-desist order (the “SEC Order”). Under the terms of the SEC Order, the Company has agreed to cease-and-desist from committing or causing any violations or any future violations of Sections 17(a)(2) and (3) of the Securities Act of 1933, as amended (the “Securities Act”), and Section 13(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Rules 12b-20, 13a-13 and 13a-15(a) thereunder. No other violations of the securities laws are alleged in the SEC Order. As part of the SEC Order, the Company also agreed to pay, and has paid, a civil penalty in the amount of $3.0 million. The Company consented to the entry of the SEC Order without admitting or denying the findings of the SEC Order, other than with respect to the SEC’s jurisdiction over the Company and the subject matter of the SEC Order. The SEC Order describing the settlement was furnished as Exhibit 99.1 and the SEC’s press release announcing this resolution is furnished as Exhibit 99.2 to the Company’s Current Report on Form 8-K filed with the SEC on March 9, 2023.

On September 28, 2021, the Information Commissioner’s Office in the United Kingdom under the U.K. Data Protection Act 2018 (the "ICO") notified us that it has closed its investigation of the Security Incident. Based on its investigation and having considered our actions before, during and after the Security Incident, the ICO issued our European subsidiary a reprimand in accordance with Article 58(2)(b) of the U.K. General Data Protection Regulation ("U.K. GDPR") due to our non-compliance, in the ICO's view, with the requirements set out in Article 32 of the U.K. GDPR regarding the processing of personal data. The ICO did not impose a penalty related to the Security Incident, nor did it impose any requirements for further action by us.

On September 24, 2021, we received notice from the Spanish Data Protection Authority that it has concluded its investigation of the Security Incident, pursuant to which our European subsidiary paid a penalty of €60,000 in relation to the alleged late notification of two Spanish data controllers regarding the Security Incident.

On January 15, 2021, we were notified by the Data Protection Commission of Ireland that it has concluded its investigation of the Security Incident without taking any action against us.

We continue to cooperate with all ongoing investigations, which include various requests for documents, policies, narratives and communications, as well as requests to interview or depose various Company-related personnel. As noted above, each of these separate governmental investigations could result in adverse judgments, settlements, fines, penalties or other resolution, the amount, scope and timing of which we are currently unable to predict, but could have a material adverse impact on our results of operations, cash flows or financial condition.

18 | | First Quarter 2023 Form 10-Q | ||||||

| 9. Income Taxes | ||

Our income tax benefit and effective income tax rates, including the effects of period-specific events, were:

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| Income tax benefit | $ | ( | $ | ( | ||||

| Effective income tax rate | % | % | ||||||

During the three months ended March 31, 2022, we utilized the discrete effective tax rate method, as allowed by ASC 740-270-30-18, Income Taxes—Interim Reporting, to calculate our interim income tax provision. The discrete method is applied when the application of the estimated annual effective tax rate is impractical because it is not possible to reliably estimate the annual effective tax rate. The discrete method treats the year-to-date period as if it was the annual period and determines the income tax expense or benefit on that basis. We believe that, at this time, the use of this discrete method is no longer more appropriate than the annual effective tax rate method.

The increase in our effective income tax rate for the three months ended March 31, 2023 when compared to the same period in 2022 was primarily attributable to unfavorable impact of non-deductible Security Incident accruals, lower foreign-derived intangible income deduction and an increase to the UK corporate tax rate offset against benefit attributable to valuation allowance reduction.

| 10. Stockholders' Equity | ||

Changes in accumulated other comprehensive income (loss) by component

The changes in accumulated other comprehensive income (loss) by component, consisted of the following:

Three months ended March 31, | ||||||||

| (in thousands) | 2023 | 2022 | ||||||

| Accumulated other comprehensive income, beginning of period | $ | $ | ||||||

| By component: | ||||||||

| Gains and losses on cash flow hedges: | ||||||||

| Accumulated other comprehensive income balance, beginning of period | $ | $ | ||||||

Other comprehensive (loss) income before reclassifications, net of tax effects of $ | ( | |||||||

| Amounts reclassified from accumulated other comprehensive (loss) income | ( | |||||||

| Tax expense (benefit) included in provision for income taxes | ( | |||||||

| Total amounts reclassified from accumulated other comprehensive (loss) income | ( | |||||||

| Net current-period other comprehensive (loss) income | ( | |||||||

| Accumulated other comprehensive income balance, end of period | $ | $ | ||||||

| Foreign currency translation adjustment: | ||||||||

| Accumulated other comprehensive (loss) income balance, beginning of period | $ | ( | $ | |||||

| Translation adjustment | ( | |||||||

| Accumulated other comprehensive loss balance, end of period | ( | ( | ||||||

| Accumulated other comprehensive income, end of period | $ | $ | ||||||

First Quarter 2023 Form 10-Q | | 19 | ||||||

| 11. Revenue Recognition | ||

Transaction price allocated to the remaining performance obligations

As of March 31, 2023, approximately $1.1 billion of revenue is expected to be recognized from remaining performance obligations. We expect to recognize revenue on approximately 60 % of these remaining performance obligations over the next 12 months, with the remainder recognized thereafter.

We applied the practical expedient in ASC 606-10-50-14 and have excluded the value of unsatisfied performance obligations for (i) contracts with an original expected length of one year or less (one-time services); and (ii) contracts for which we recognize revenue at the amount to which we have the right to invoice for services performed (transactional revenue).

Contract balances

Our contract assets as of March 31, 2023 and December 31, 2022 were insignificant. Our closing balances of deferred revenue were as follows:

| (in thousands) | March 31, 2023 | December 31, 2022 | ||||||

| Total deferred revenue | $ | $ | ||||||

The decrease in deferred revenue during the three months ended March 31, 2023 was primarily due to a seasonal decrease in customer contract renewals. Historically, due to the timing of customer budget cycles, we have an increase in customer contract renewals at or near the beginning of our third quarter. Generally, our lowest balance of deferred revenue during the year is at the end of our first quarter. The amount of revenue recognized during the three months ended March 31, 2023 that was included in the deferred revenue balance at the beginning of the period was approximately $162 million. The amount of revenue recognized during the three months ended March 31, 2023 from performance obligations satisfied in prior periods was insignificant.

Disaggregation of revenue

We sell our cloud solutions and related services in three primary geographical markets: to customers in the United States, to customers in the United Kingdom and to customers located in other countries. The following table presents our revenue by geographic area based on the address of our customers:

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| United States | $ | $ | ||||||

| United Kingdom | ||||||||

| Other countries | ||||||||

| Total revenue | $ | $ | ||||||

20 | | First Quarter 2023 Form 10-Q | ||||||

During the third quarter of 2022, we reorganized our market groups. The Social Sector and Corporate Sector market groups comprised our go-to-market organizations as of March 31, 2023. The following is a description of each market group as of that date:

•The Social Sector market group focuses on sales to customers and prospects in the social sector, such as nonprofits, foundations, education institutions, healthcare organizations and other not-for-profit entities globally, and includes JustGiving; and

•The Corporate Sector market group focuses on sales to customers and prospects in the corporate sector globally, and includes EVERFI and YourCause.

The following table presents our revenue by market group:

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022(1) | ||||||

| Social Sector | $ | $ | ||||||

Corporate Sector | ||||||||

| Total revenue | $ | $ | ||||||

(1)Due to the market group change discussed above, we have recast our revenue by market group for the three months ended March 31, 2022 to present them on a consistent basis with the current year.

The following table presents our recurring revenue by type:

Three months ended March 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| Contractual recurring | $ | $ | ||||||

| Transactional recurring | ||||||||

| Total recurring revenue | $ | $ | ||||||

First Quarter 2023 Form 10-Q | | 21 | ||||||

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited, condensed consolidated financial statements and related notes included elsewhere in this Quarterly Report on Form 10-Q. The following discussion and analysis presents financial information denominated in millions of dollars which can lead to differences from rounding when compared to similar information contained in the unaudited, condensed consolidated financial statements and related notes which are primarily denominated in thousands of dollars.

| Executive Summary | ||

We are the leading software provider exclusively dedicated to powering social impact. Serving the nonprofit and education sectors, companies committed to social responsibility and individual change makers, our essential software is built to accelerate impact in fundraising, nonprofit financial management, digital giving, grantmaking, corporate social responsibility and education management. A remote-first company, we have operations in the United States, Australia, Canada, Costa Rica and the United Kingdom, supporting users in 100+ countries.

Our revenue is primarily generated from the following sources: (i) charging for the use of our software solutions in cloud and hosted environments; (ii) providing payment and transactional services; (iii) providing software maintenance and support services; (iv) providing Impact-as-a-Service™ digital educational content; and (v) providing professional services, including implementation, consulting, training, analytic and other services.

Update on Five Key Operational Initiatives

| 1 | Product Innovation | |||||||||||||

| 2 | Bookings Growth and Acceleration | |||||||||||||

| 3 | Transactional Revenue Optimization | |||||||||||||

| 4 | Modernized Approach to Pricing and Multi-Year Customer Contracts | |||||||||||||

| 5 | Keen Attention to Cost Management | |||||||||||||

1.Product Innovation

We support our customers by replacing their aging, mission-critical systems of record and adding advanced digital services. We continuously seek ways to add substantial value for our customers and their constituents by investing in both organic innovation and ecosystem enablement through partnerships and acquisitions. These new capabilities and partnerships strengthen our offers and create new opportunities for our customers to deliver on their missions. For example, with the availability of SKY API endpoints for Blackbaud CRM and Blackbaud Altru, we are enabling customers to leverage applications in the Blackbaud Marketplace to integrate complementary point solutions with our partners.

We have expanded strategic partnerships to unlock even more value for our customers with partners like Almabase and SwipeTrack's XTrulink. We recently announced an expanded partnership with Almabase to provide a modern solution for advancement teams to unlock higher education and K-12 school alumni engagement and better fundraising by creating integrations that enable secure movement of constituent, gift and event data between systems, without friction. Additionally, we have partnered with SwipeTrack Solutions to create an integration between Blackbaud Altru and Blackbaud Merchant Services to modernize the patron digital experience and back office operations at arts and cultural organizations.

We also recently announced a new feature for general availability with Blackbaud TeamRaiser, Good Move. Good Move leverages Kilter, which we acquired last year, and helps charitable organizations raise more with mobile-first, gamified activity tracking and peer-to-peer fundraising.

22 | | First Quarter 2023 Form 10-Q | ||||||

2.Bookings Growth and Acceleration

We drove strong bookings performance in the first quarter, up significantly versus last year, led by our corporate sector (YourCause and EVERFI solutions) which more than doubled its bookings over the first quarter of 2022. We signed several notable large enterprise contracts during the first quarter, which speaks to the resilience of the end markets we serve and the focus we have placed on driving further improvements in sales productivity. Productivity per sales representative (defined as new sales bookings for the period divided by the number of sales representatives) has improved over 30% versus last year. There can be volatility quarter-to-quarter on bookings. However, the strong start in the first quarter with the most in-year revenue impact positions us well.

3.Transactional Revenue Optimization and Expansion

Transactional revenue, which is about one-third of total revenue, has proven to be resilient so far in 2023 following the lower average donation sizes we experienced during the fourth quarter of 2022. The rate changes that we announced on Blackbaud Merchant Services in the U.S. in late 2022 began to take effect during the first quarter. Our Blackbaud Tuition Management and JustGiving platforms continue to perform well against plan. And as we look ahead, our teams are hard at work to drive innovation across our payments solutions that are a win-win for both our customers and Blackbaud. We have already introduced our two fee cover models, and we are also looking at ways to optimize our payments solutions to drive a better donor experience.

4.Modernized Approach to Pricing and Multi-Year Contracts

We deeply value the relationships we have with our customers, many of whom have been with us for decades. Our solutions add considerable value for our customers and raise billions of dollars annually to fuel social impact, and we continue to innovate on our suite of products to generate incremental value. Last summer, we put in place an updated pricing policy primarily for our social sector customers that directly reflects the value we provide to them, is in-line with the broader market and reflects the inflationary pressures that all businesses are facing. In November 2022, we started notifying customers with a March 2023 contract renewal that we would be making two important contract changes. First, we are offering 3-year contract renewal terms as our standard, replacing one-year renewal terms. This process was already being implemented outside of the pricing changes. Second, we are implementing a more significant rate increase on the 1-year renewal option versus the 3-year renewal option. And third, the 3-year renewal option includes annual rate increases that will compound. Our 3-year renewal options did not historically include annual compounding rate increases.

Through April 2023, we have renewed over 25% of the customers that are up for renewal in our 2023 cohort. The close day-to-day management of renewals, the mix of 3-year and 1-year contracts, and the impact of pricing are progressing very well, and we expect more impact from the compounding effect of these rate increases over time as we layer in future year contract renewals and annual rate increases. For example, over 50% of our planned 2023 revenue will renew in a little over 3 years and approximately 35% of that renewable base is expected to renew this year. These contracts are renewing every day and create revenue growth that we expect to accelerate with each successive quarter this year. We expect that to lead to an even greater impact in 2024, 2025 and beyond as we begin to see the full-year impact of the rate increases compound annually. Approximately 30% of the renewable base is up for renewal in 2024 and more than 20% in 2025. The adoption of 3-year renewals as a standard are expected to have an added benefit of higher retention which provides greater revenue assurance and predictability. Looking even further ahead, the cycle starts fresh in 2026 as the 2023 signed contracts will begin to renew. We expect that this will be a sustainable and meaningful revenue growth stream for us.

5.Keen Attention to Cost Management

We closed four legacy data centers during 2022, and we plan to close more this year. We renegotiated key vendor contracts including Microsoft Azure and AWS and made the difficult decision to further reduce our staff in the first quarter. Because we have organized to achieve much better scale efficiencies, we now have reduced our headcount by approximately 14% since the third quarter of 2022. Our goal is to run the business at about this headcount level for the foreseeable future, such that our revenue growth will better drive margin acceleration.

First Quarter 2023 Form 10-Q | | 23 | ||||||

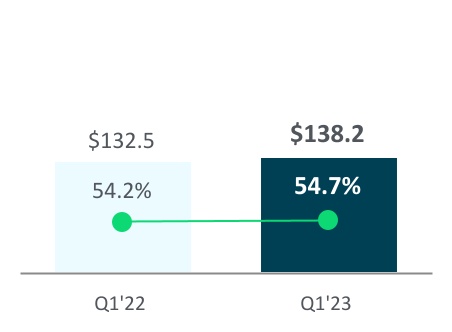

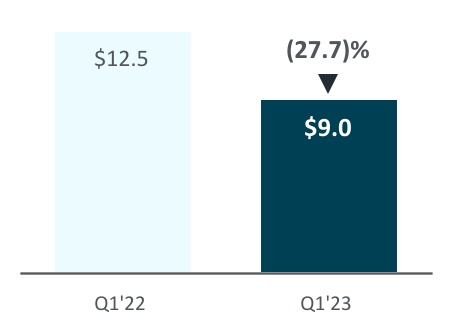

Financial Summary

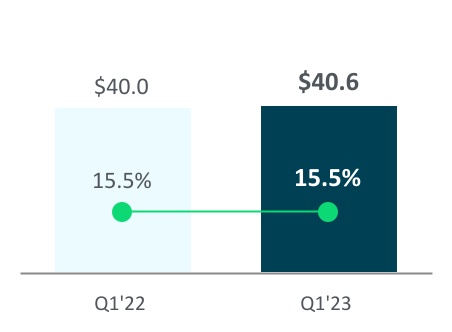

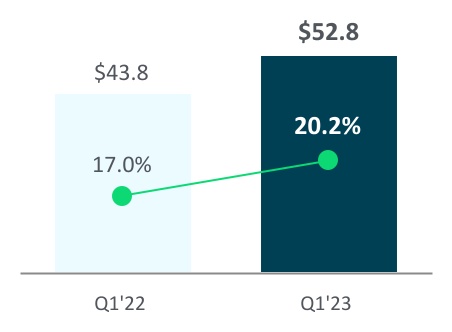

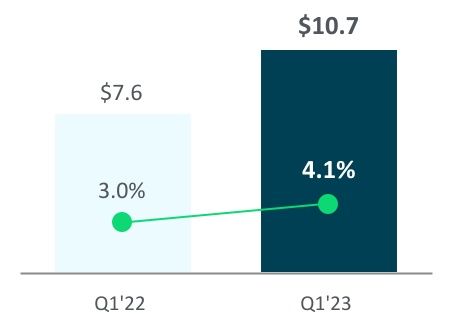

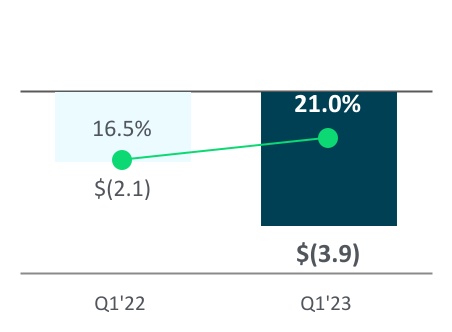

| Total revenue ($M) | Loss from operations ($M) | |||||||

| YoY Growth (%) | YoY Growth (%) | |||||||

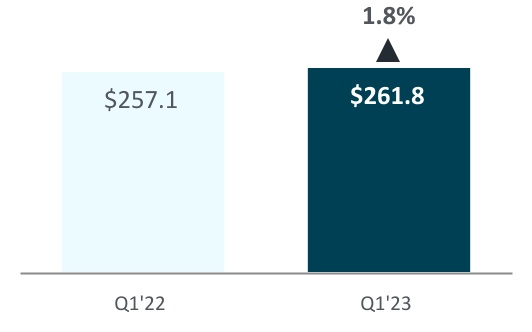

Total revenue increased by $4.6 million during the three months ended March 31, 2023, when compared to the same period in 2022, driven largely by the following:

| + | Growth in recurring revenue primarily related to: •increase in transactional recurring revenue of $5.0 million primarily due to increases in volume for our Blackbaud Tuition Management and JustGiving solutions and positive results related to a pricing initiative we implemented at the beginning of 2023; the increase in transactional recurring revenue was partially offset by a decrease related to fluctuations in foreign currency exchange rates of $1.7 million, respectively •increase in contractual recurring revenue of $3.1 million related to the performance of our cloud solutions; partially offset by a decrease in maintenance revenue as customers migrate to our cloud solutions and a decrease related to fluctuations in foreign currency exchange rates of $0.8 million | ||||||||||

| - | Decreases in one-time service and other revenue primarily related to: •decrease in one-time consulting revenue due primarily due to less revenue from implementation and customization services, in line with our multi-year strategic shift from a license-based and one-time services business model to a cloud subscription business model. Our cloud subscription offerings generally require less implementation and customization services •decreases in one-time analytics revenue as analytics are generally integrated in our cloud solutions | ||||||||||

For additional information on the impact of foreign currency fluctuations on our financial results, see Foreign Currency Exchange Rates below on page 41.

We have a number of multi-year pricing initiatives underway, some to bring our pricing in line with the market while others are model changes that are expected to drive greater revenue for both us and our customers. As a result, we expect to see an acceleration in growth in the second half of 2023 when compared to the first half of the year as we begin to see the full-year effect of some of these pricing initiatives.

We expect that the one-time services and other revenue will continue to significantly decrease during 2023 compared to 2022 driven by our continued migration to the cloud in our core business.

24 | | First Quarter 2023 Form 10-Q | ||||||

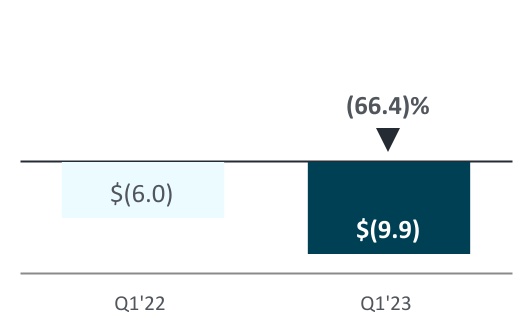

Income from operations decreased by $4.0 million during the three months ended March 31, 2023, when compared to the same period in 2022, driven largely by the following:

| - | Increase in Security Incident-related expenses of $10.6 million. See "Security Incident update" below. | ||||||||||

| - | Increase in stock-based compensation expense of $2.1 million primarily due to 2022 performance-based equity award adjustments, partially offset by the targeted workforce reductions during the fourth quarter of 2022 and first quarter of 2023 | ||||||||||

| - | Increase in transaction-based costs of $2.1 million related to the increase in the volume of transactions for which we process payments and, to a lesser extent, increases in vendor rates | ||||||||||

| - | Increase in third-party software costs of $1.9 million primarily related to a higher number of licenses needed and also price increases | ||||||||||

| - | Net decrease of $0.9 million due to an increase in amortization of capitalized software and content development costs, partially offset by an increase in software and content development costs that were required to be capitalized under the internal-use software guidance | ||||||||||

| + | Decrease in compensation costs other than stock-based compensation of $7.7 million, partially offset by a corresponding increase in severance costs of $4.3 million due to our targeted workforce reductions discussed above | ||||||||||

| + | Increase in total revenue, as described above | ||||||||||

| + | Decrease in hosting and data center costs of $2.1 million as we continue to migrate our cloud infrastructure to leading public cloud service providers and make investments in security; currently, we expect our cloud infrastructure migration efforts and increased level of cybersecurity investments to continue for the foreseeable future | ||||||||||

| + | Decrease in third-party contractor costs of $1.9 million primarily due to a decrease in our use of third-party software developers | ||||||||||

| + | Decrease in advertising costs of $0.9 million | ||||||||||

We are continuing to make critical investments in the business in areas such as digital marketing, innovation, cybersecurity, customer success and our continued shift of cloud infrastructure to leading public cloud service providers. Our profitability during the first quarter reflects some of these incremental investments. In 2023, we expect our financial performance to improve with each successive quarter, starting with meaningful improvement in the second quarter as our pricing and cost initiatives take hold.

We continuously seek opportunities to optimize our portfolio of solutions to focus time and resources on innovation that will have the greatest impact for our customers and the markets we serve, and drive the highest return on investment. To that end, we will continue to simplify and rationalize our portfolio through product sunsets and divestitures of non-core businesses and technologies.

| Gross dollar retention | ||||||||

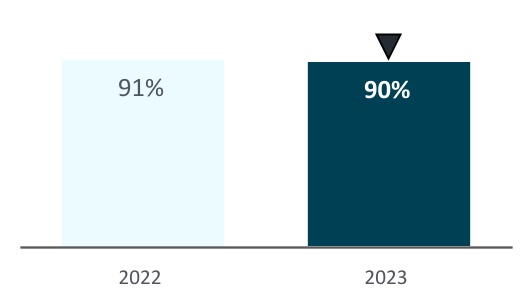

A key factor to our overall success is the renewal and expansion of our existing subscription agreements with our customers. Management uses gross dollar retention in analyzing our success at delighting our customers with innovative and cloud solutions. Gross dollar retention is defined as contracted annual recurring revenue ("CARR") divided by beginning CARR with a measurement period of twelve months. For the twelve months ended March 31, 2023, our gross dollar retention was approximately 90%. This gross dollar retention rate is relatively unchanged from our rate for the full year ended December 31, 2022. We are continually investing in innovation, which we believe will increase gross dollar retention over the long-term.

First Quarter 2023 Form 10-Q | | 25 | ||||||

Although some customer attrition is normal, our new contract pricing and renewal model (as described above on page 24) does not appear to have impacted customer attrition to date.

Balance sheet and cash flow

At March 31, 2023, our cash and cash equivalents were $24.1 million and the carrying amount of our debt under the 2020 Credit Facility was $817.1 million. Our net leverage ratio was 2.99 to 1.00.

During the three months ended March 31, 2023, we generated $21.8 million in cash from operations, had a net increase in borrowings of $17.2 million, and had aggregate cash outlays of $15.3 million for purchases of property and equipment and capitalized software and content development costs.

Security Incident update