Table of Contents

As filed with the Securities and Exchange Commission on January 16, 2024

Registration No. 333-275640

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Pre-Effective Amendment No. 1 ☒

Post-Effective Amendment No. ☐

(Check appropriate box or boxes)

MidCap Financial Investment Corporation

(Exact Name of Registrant as Specified in Charter)

9 West 57th Street,

New York, NY 10019

(Address of Principal Executive Offices)

(212) 515-3450

(Area Code and Telephone Number)

Kristin Hester

Chief Legal Officer

MidCap Financial Investment Corporation

9 West 57th Street

New York, NY 10019

(Name and Address of Agent for Service)

Copies to:

David W. Blass, Esq.

Jonathan L. Corsico, Esq.

Steven Grigoriou, Esq.

Jonathan Pacheco, Esq.

Simpson Thacher & Bartlett LLP

900 G Street, N.W.

Washington, DC 20001

Telephone: (202) 636-5500

Fax: (202) 636-5502

Approximate Date of Proposed Public Offering: As soon as practicable after this registration statement becomes effective and upon completion of the transactions described in the enclosed document.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the U.S. Securities and Exchange Commission. MidCap Financial Investment Corporation may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This document is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or jurisdiction where such offer or sale is not permitted.

PRELIMINARY—SUBJECT TO COMPLETION—DATED JANUARY 16, 2024

MIDCAP FINANCIAL INVESTMENT CORPORATION

9 West 57th Street

New York, NY 10019

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

[ ], 2024

Dear Stockholder:

You are cordially invited to attend the Special Meeting of Stockholders (the “MFIC Special Meeting”) of MidCap Financial Investment Corporation, a Maryland corporation (“MFIC”), to be held virtually on [ ], 2024, at [ ] a.m., Eastern Time, at the following website: [ ]. Stockholders of record of MFIC (“MFIC Stockholders”) at the close of business on [ ], 2024 are entitled to notice of, and to vote at, the MFIC Special Meeting or any adjournment or postponement thereof.

The notice of special meeting and the joint proxy statement/prospectus accompanying this letter provide an outline of the business to be conducted at the MFIC Special Meeting. At the MFIC Special Meeting, you will be asked to approve the issuance of shares of common stock, par value $0.001 per share, of MFIC (“MFIC Common Stock”) pursuant to the Mergers (as defined below) in accordance with NASDAQ listing rule requirements (“MFIC Share Issuance” and such proposal, the “MFIC Share Issuance Proposal”).

MFIC, Apollo Senior Floating Rate Fund Inc., a Maryland corporation (“AFT”) and Apollo Tactical Income Fund Inc., a Maryland corporation (“AIF”), are proposing a combination of all three companies by mergers and related transactions pursuant to two separate Agreements and Plan of Merger. MFIC is a closed-end, externally managed, diversified management investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Each of AFT and AIF are registered under the 1940 Act as diversified, closed-end management investment companies.

The closing of the AFT Mergers (as defined below) (the “AFT Closing”) is contingent upon:

(a) MFIC Stockholder approval of the MFIC Share Issuance Proposal,

(b) approval of the AFT Mergers by holders of shares of common stock, par value $0.001 per share (“AFT Common Stock”), of AFT, and

(c) satisfaction or waiver of certain other closing conditions.

If the AFT Mergers do not close, then MFIC will not issue shares of MFIC Common Stock to holders of AFT Common Stock (“AFT Stockholders”), even if the MFIC Share Issuance Proposal is approved by the MFIC Stockholders.

The closing of the AIF Mergers (as defined below) (the “AIF Closing”) is contingent upon:

(a) MFIC Stockholder approval of the MFIC Share Issuance Proposal,

(b) approval of the AIF Mergers by holders of shares of common stock, par value $0.001 per share (“AIF Common Stock”), of AIF, and

(c) satisfaction or waiver of certain other closing conditions.

If the AIF Mergers do not close, then MFIC will not issue shares of MFIC Common Stock to holders of AIF Common Stock (“AIF Stockholders”), even if the MFIC Share Issuance Proposal is approved by the MFIC Stockholders.

The AFT Closing is not contingent upon the AIF Closing having occurred, and the AIF Closing is not contingent upon the AFT Closing having occurred.

Table of Contents

As of September 30, 2023, the net asset value (“NAV”) of MFIC Common Stock was $15.28 per share. As of September 30, 2023, the NAV of AFT Common Stock was $15.05 per share. As of September 30, 2023, the NAV of AIF Common Stock was $14.63 per share. Based on the NAVs of MFIC, AFT and AIF as of September 30, 2023, (and adjusted for estimated transaction costs), MFIC would issue approximately 0.9849 and 0.9577 shares of MFIC Common Stock for each share of AFT Common Stock and AIF Common Stock outstanding.

AFT Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AFT, AFT Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AFT Merger Sub”), and, for the limited purposes set forth therein, Apollo Investment Management, L.P., a Delaware limited partnership and the investment adviser to MFIC (“MFIC Adviser”) (as may be amended from time to time, the “AFT Merger Agreement”), subject to the terms and conditions set forth in the AFT Merger Agreement, as of the applicable effective time (the “AFT Effective Time”) AFT Merger Sub would merge with and into AFT (the “AFT First Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT First Merger, AFT would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AFT First Merger, the “AFT Mergers”).

Subject to the terms and conditions of the AFT Merger Agreement, at the AFT Effective Time, each share of AFT Common Stock issued and outstanding immediately prior to the AFT Effective Time (other than shares owned by MFIC or any of its consolidated subsidiaries, including AFT Merger Sub (the “AFT Cancelled Shares”)) will be converted into the right to receive a number of shares of MFIC Common Stock equal to the AFT Exchange Ratio (as defined below) (cash will be paid in lieu of fractional shares). AFT has no preferred stock outstanding, and no preferred stock will be issued by MFIC as a result of the AFT Mergers.

Under the AFT Merger Agreement, as of a mutually agreed date no earlier than 48 hours (excluding Sundays and holidays) prior to the AFT Effective Time (such date, the “AFT Determination Date”), MFIC and AFT will deliver to the other a calculation of its NAV as of such date (such calculation with respect to AFT, the “Closing AFT Net Asset Value” and such calculation with respect to MFIC, the “Closing AFT Merger MFIC Net Asset Value”), in each case using the same set of assumptions, methodologies and adjustments as has been historically used in preparing such calculation. Based on such calculations, the parties will calculate: (1) the “AFT Per Share NAV,” which will be equal to (i) the Closing AFT Net Asset Value divided by (ii) the number of shares of AFT Common Stock issued and outstanding as of the AFT Determination Date (excluding any AFT Cancelled Shares) and (2) the “AFT Merger MFIC Per Share NAV,” which will be equal to (A) the Closing AFT Merger MFIC Net Asset Value divided by (B) the number of shares of MFIC Common Stock issued and outstanding as of the AFT Determination Date. The “AFT Exchange Ratio” will be equal to the quotient (rounded to four decimal places) of (i) the AFT Per Share NAV divided by (ii) the AFT Merger MFIC Per Share NAV.

MFIC and AFT will update and redeliver the Closing AFT Merger Company Net Asset Value or the Closing AFT Net Asset Value, respectively, in the event that the closing of the AFT Mergers is subsequently materially delayed or there is a material change to such calculation between the AFT Determination Date and the closing of the AFT Mergers and as needed to ensure that the calculation is determined within 48 hours (excluding Sundays and holidays) prior to the AFT Effective Time.

Immediately following the AFT Effective Time, MFIC will repay or prepay any amounts outstanding under AFT’s existing credit facility as of the AFT Effective Time, subject to the conditions set forth in MFIC’s senior secured credit facility.

Promptly following closing of the AFT Mergers, MFIC Adviser or one of its affiliates will pay directly to holders of shares of AFT Common Stock that are issued and outstanding immediately prior to the AFT Effective Time a special payment equal to $0.25 per share of AFT Common Stock, subject to deduction for any applicable withholding tax. This payment will not be made by or through AFT. The specific tax characteristics of the $0.25 per share special payment are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

Table of Contents

The AFT Merger Agreement contains certain termination rights, including if the AFT Mergers are not completed on or before November 7, 2024, or if the requisite approvals of MFIC’s and AFT’s stockholders are not obtained. The AFT Merger Agreement provides that, upon the termination of the AFT Merger Agreement under certain circumstances involving entry into a definitive transaction by AFT with a third party, such third party that enters into the definitive transaction with AFT may be required to pay MFIC a termination fee of $7,029,482. The AFT Merger Agreement also provides that, upon the termination of the AFT Merger Agreement under certain circumstances involving entry into a definitive transaction by MFIC with a third party, such third party that enters into the definitive agreement with MFIC may be required to pay to AFT a termination fee of $29,905,339.

Within thirty days following the closing of the AFT Mergers or the termination of the AFT Merger Agreement pursuant to the terms thereof, as applicable, subject to the closing of the AIF Mergers and applicable law, MFIC shall distribute to the holder of each share of MFIC Common Stock as of a record date to be determined by the MFIC Board an amount in cash equal to $0.20 per share of MFIC Common Stock held by such holder. The specific tax characteristics of the $0.20 per share special distribution are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

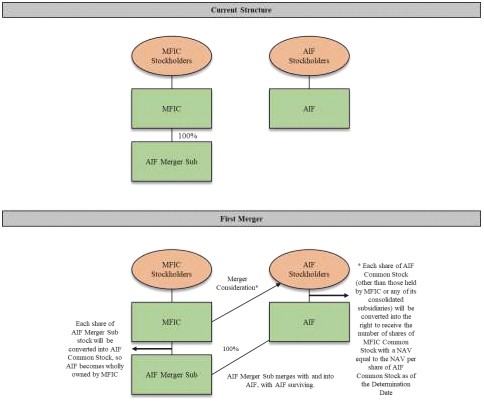

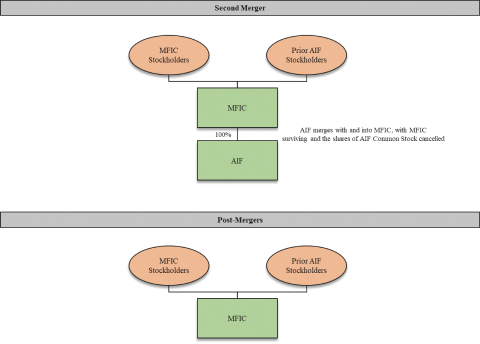

AIF Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AIF, AIF Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AIF Merger Sub”), and, for the limited purposes set forth therein, MFIC Adviser (as may be amended from time to time, the “AIF Merger Agreement” and, together with the AFT Merger Agreement, the “Merger Agreements”), subject to the terms and conditions set forth in the AIF Merger Agreement, as of the applicable effective time (the “AIF Effective Time”) AIF Merger Sub would merge with and into AIF (the “AIF First Merger”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF First Merger, AIF would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AIF First Merger, the “AIF Mergers” and, together with the AFT Mergers, the “Mergers”).

Subject to the terms and conditions of the AIF Merger Agreement, at the AIF Effective Time, each share of common stock, par value $0.001 per share, of AIF (the “AIF Common Stock”) issued and outstanding immediately prior to the AIF Effective Time (other than shares owned by MFIC or any of its consolidated subsidiaries, including AIF Merger Sub (the “AIF Cancelled Shares”)) will be converted into the right to receive a number of shares of MFIC Common Stock equal to the AIF Exchange Ratio (as defined below), plus any cash (without interest) in lieu of fractional shares. AIF has no preferred stock outstanding, and no preferred stock will be issued by MFIC as a result of the AIF Mergers.

Under the AIF Merger Agreement, as of a mutually agreed date no earlier than 48 hours (excluding Sundays and holidays) prior to the AIF Effective Time (such date, the “AIF Determination Date”), each of MFIC and AIF will deliver to the other a calculation of its net asset value as of such date (such calculation with respect to AIF, the “Closing AIF Net Asset Value” and such calculation with respect to MFIC, the “Closing AIF Merger MFIC Net Asset Value”), in each case using the same set of assumptions, methodologies and adjustments as has been historically used in preparing such calculation. Based on such calculations, the parties will calculate: (1) the “AIF Per Share NAV,” which will be equal to (i) the Closing AIF Net Asset Value divided by (ii) the number of shares of AIF Common Stock issued and outstanding as of the AIF Determination Date (excluding any AIF Cancelled Shares) and (2) the “AIF Merger MFIC Per Share NAV,” which will be equal to (i) the Closing AIF Merger MFIC Net Asset Value divided by (ii) the number of shares of MFIC Common Stock issued and outstanding as of the AIF Determination Date. The “AIF Exchange Ratio” will be equal to the quotient (rounded to four decimal places) of (i) the AIF Per Share NAV divided by (ii) the AIF Merger MFIC Per Share NAV.

MFIC and AIF will update and redeliver the Closing AIF Merger MFIC Net Asset Value or the Closing AIF Net Asset Value, respectively, in the event that the closing of the AIF Mergers is subsequently materially delayed or there is a material change to such calculation between the AIF Determination Date and the closing of the AIF Mergers and as needed to ensure that the calculation is determined within 48 hours (excluding Sundays and holidays) prior to the AIF Effective Time.

Table of Contents

Immediately following the AIF Effective Time, MFIC will repay or prepay any amounts outstanding under AIF’s existing credit facility as of the AIF Effective Time, subject to the conditions set forth in MFIC’s senior secured credit facility.

Promptly following closing of the AIF Mergers, MFIC Adviser or one of its affiliates will pay directly to holders of shares of AIF Common Stock that are issued and outstanding immediately prior to the AIF Effective Time a special payment equal to $0.25 per share of AIF Common Stock, subject to deduction for any applicable withholding tax. This payment will not be made by or through AIF. The specific tax characteristics of the $0.25 per share special payment are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

The AIF Merger Agreement contains certain termination rights, including if the AIF Mergers are not completed on or before November 7, 2024, or if the requisite approvals of MFIC’s and AIF’s stockholders are not obtained. The AIF Merger Agreement provides that, upon the termination of the AIF Merger Agreement under certain circumstances involving entry into a definitive transaction by AIF with a third party, such third party that enters into the definitive transaction with AIF may be required to pay MFIC a termination fee of $6,348,267. The AIF Merger Agreement also provides that, upon the termination of the AIF Merger Agreement under certain circumstances involving entry into a definitive transaction by MFIC with a third party, such third party that enters into the definitive agreement with MFIC may be required to pay to AIF a termination fee of $29,905,339.

Within thirty days following the closing of the AIF Mergers or the termination of the AIF Merger Agreement pursuant to the terms thereof, as applicable, subject to the closing of the AFT Mergers and applicable law, MFIC shall distribute to the holder of each share of MFIC Common Stock as of a record date to be determined by the MFIC Board an amount in cash equal to $0.20 per share of MFIC Common Stock held by such holder. The specific tax characteristics of the $0.20 per share special distribution are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

Your vote is extremely important. The presence at the MFIC Special Meeting, virtually or represented by proxy, of MFIC Stockholders entitled to cast a majority of all the votes entitled to be cast at the MFIC Special Meeting will constitute a quorum of MFIC. At the MFIC Special Meeting, MFIC Common Stockholders will be asked to vote on the MFIC Share Issuance Proposal. The affirmative vote of MFIC Stockholders representing a majority of all the votes cast at the MFIC Special Meeting is required to approve the MFIC Share Issuance Proposal.

Abstentions will have no effect on the voting outcome of the MFIC Share Issuance Proposal, although abstentions will be treated as shares present for quorum purposes.

After careful consideration, and on the recommendation of a special committee of the Board of Directors of MFIC (the “MFIC Board”), the MFIC Board unanimously approved the Merger Agreements, declared the Mergers and the transactions contemplated by the Merger Agreements advisable and unanimously recommends that MFIC Stockholders vote “FOR” the MFIC Share Issuance Proposal.

It is important that your shares be represented at the MFIC Special Meeting. Please follow the instructions on the enclosed proxy card and authorize a proxy to vote your shares via the Internet, by telephone or by signing, dating and returning the enclosed proxy card. MFIC encourages you to authorize a proxy to vote your shares via the Internet as it saves MFIC significant time and processing costs. Voting by proxy does not deprive you of your right to participate in the virtual MFIC Special Meeting.

This joint proxy statement/prospectus describes the MFIC Special Meeting, the Mergers and the documents related to the Mergers (including the Merger Agreements) and other related matters that MFIC Stockholders should review before voting on the MFIC Share Issuance Proposal and should be retained for future reference. Please carefully read this entire document, including “Risk Factors” beginning on page 47 and

Table of Contents

as otherwise incorporated by reference in this joint proxy statement/prospectus, for a discussion of the risks relating to the Mergers, MFIC, AFT and AIF. MFIC files periodic reports, current reports, proxy statements and other information with the U.S. Securities and Exchange Commission (the “SEC”). This information is available free of charge, and stockholder inquiries can be made, by contacting MFIC at 9 West 57th Street, New York, NY, 10019 or by calling MFIC at (212) 515-3450 or on MFIC’s website at https://www.midcapfinancialic.com. The SEC also maintains a website at www.sec.gov that contains such information. Except for the documents incorporated by reference into this joint proxy statement/prospectus, information on MFIC’s website is not incorporated into or a part of this joint proxy statement/prospectus.

No matter how many or few shares of MFIC you own, your vote and participation are very important to us.

| Sincerely yours, |

|

|

| Howard Widra |

| Executive Chairman of the MFIC Board |

Neither the SEC nor any state securities commission has approved or disapproved of the shares of MFIC Common Stock to be issued under this joint proxy statement/prospectus or determined if this joint proxy statement/prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This joint proxy statement/prospectus is dated [ ], 2024 and is first being mailed or otherwise delivered to MFIC Stockholders on or about [ ], 2024.

| MidCap Financial Investment Corporation 9 West 57th Street New York, NY 10019 (212) 515-3450 |

Apollo Senior Floating Rate 9 West 57th Street New York, NY 10019 (212) 515-3200 |

Apollo Tactical Income Fund Inc. 9 West 57th Street New York, NY 10019 (212) 515-3200 |

Table of Contents

MIDCAP FINANCIAL INVESTMENT CORPORATION

9 West 57th Street

New York, NY 10019

NOTICE OF VIRTUAL SPECIAL MEETING OF STOCKHOLDERS

Online Meeting Only—No Physical Meeting Location

[WEBSITE ADDRESS]

[ ], 2024, at [ ] a.m., Eastern Time

Dear Stockholder:

A Special Meeting of Stockholders (the “MFIC Special Meeting”) of MidCap Financial Investment Corporation, a Maryland corporation (“MFIC”), will be conducted online on [ ], 2024, at [ ] a.m., Eastern Time at the following website: [ ].

At the MFIC Special Meeting, the holders of shares of common stock, par value $0.001 per share (“MFIC Common Stock”), of MFIC (“MFIC Stockholders”) will consider and vote on a proposal to approve the issuance of shares of MFIC Common Stock pursuant to the Mergers (as defined below) in accordance with NASDAQ listing rule requirements (“MFIC Share Issuance” and such proposal, the “MFIC Share Issuance Proposal”).

MFIC, Apollo Senior Floating Rate Fund Inc., a Maryland corporation (“AFT”) and Apollo Tactical Income Fund Inc., a Maryland corporation (“AIF”), are proposing a combination of all three companies by mergers and related transactions pursuant to two separate Agreements and Plan of Merger. MFIC is a closed-end, externally managed, diversified management investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Each of AFT and AIF are registered under the 1940 Act as diversified, closed-end management investment companies.

AFT Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AFT, AFT Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AFT Merger Sub”), and, for the limited purposes set forth therein, Apollo Investment Management, L.P., a Delaware limited partnership and the investment adviser to MFIC (“MFIC Adviser”) (as may be amended from time to time, the “AFT Merger Agreement”), subject to the terms and conditions set forth in the AFT Merger Agreement, as of the applicable effective time (the “AFT Effective Time”) AFT Merger Sub would merge with and into AFT (the “AFT First Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT First Merger, AFT would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AFT First Merger, the “AFT Mergers”).

AIF Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AIF, AIF Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AIF Merger Sub”), and, for the limited purposes set forth therein, MFIC Adviser (as may be amended from time to time, the “AIF Merger Agreement” and together with the AFT Merger Agreement, the “Merger Agreements”), subject to the terms and conditions set forth in the AIF Merger Agreement, as of the applicable effective time (the “AIF Effective Time”) AIF Merger Sub would merge with and into AIF (the “AIF First Merger”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF First Merger, AIF would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AIF First Merger, the “AIF Mergers” and, together with the AFT Mergers, the “Mergers”).

Table of Contents

AFTER CAREFUL CONSIDERATION, AND ON THE RECOMMENDATION OF A SPECIAL COMMITTEE OF THE BOARD OF DIRECTORS OF MFIC (THE “MFIC BOARD”), THE MFIC BOARD UNANIMOUSLY APPROVED THE MERGER AGREEMENTS, DECLARED THE MERGERS AND THE TRANSACTIONS CONTEMPLATED BY THE MERGER AGREEMENTS ADVISABLE AND UNANIMOUSLY RECOMMENDS THAT THE MFIC STOCKHOLDERS VOTE “FOR” THE MFIC SHARE ISSUANCE PROPOSAL.

You have the right to receive notice of, and to vote at, the MFIC Special Meeting if you were a stockholder of record of MFIC at the close of business on [ ], 2024. A joint proxy statement/prospectus is attached to this Notice that describes the matters to be voted upon at the MFIC Special Meeting or any adjournment(s) or postponement(s) thereof. The enclosed proxy card will instruct you as to how you may authorize a proxy to vote your shares via the Internet, by telephone or by signing, dating and returning the enclosed proxy card. In addition, information regarding how to find the logistical details of the virtual MFIC Special Meeting (including how to remotely access, participate in and vote during the virtual meeting) is included beginning on page 55 of the attached joint proxy statement/prospectus.

Whether or not you plan to participate in the MFIC Special Meeting, we encourage you to authorize a proxy to vote your shares by following the instructions on the enclosed proxy card. Please note, however, that if you wish to vote during the MFIC Special Meeting and your shares are held of record by a broker or nominee, you must obtain a “legal” proxy issued in your name from that record holder.

We are not aware of any other business that may properly be brought before the MFIC Special Meeting and, pursuant to our bylaws, only the matters set forth in the notice of special meeting may be brought before the MFIC Special Meeting.

Thank you for your continued support of MFIC.

| By order of the Board of Directors, |

|

|

| Kristin Hester |

| Chief Legal Officer and Secretary |

New York, NY

[ ], 2024

To ensure proper representation at the MFIC Special Meeting, please follow the instructions on the enclosed proxy card to authorize a proxy to vote your shares via the Internet or telephone, or by signing, dating and returning the enclosed proxy card. Even if you authorize a proxy to vote your shares prior to the virtual MFIC Special Meeting, you still may participate in the virtual MFIC Special Meeting.

Table of Contents

APOLLO SENIOR FLOATING RATE FUND INC.

9 West 57th Street

New York, NY 10019

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

[ ], 2024

Dear Stockholder:

You are cordially invited to attend the Special Meeting of Stockholders (the “AFT Special Meeting”) of Apollo Senior Floating Rate Fund Inc., a Maryland corporation (“AFT”), to be held virtually on [ ], 2024, at [ ] a.m., Eastern Time, at the following website: [ ]. Stockholders of record of AFT at the close of business on [ ], 2024 are entitled to notice of, and to vote at, the AFT Special Meeting or any adjournment or postponement thereof.

MidCap Financial Investment Corporation, a Maryland corporation (“MFIC”), AFT and Apollo Tactical Income Fund Inc., a Maryland corporation (“AIF”), are proposing a combination of all three companies by mergers and related transactions pursuant to two separate Agreements and Plan of Merger. MFIC is a closed-end, externally managed, diversified management investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Each of AFT and AIF are registered under the 1940 Act as diversified, closed-end management investment companies.

The notice of special meeting and the joint proxy statement/prospectus accompanying this letter provide an outline of the business to be conducted at the AFT Special Meeting. At the AFT Special Meeting, you will be asked to approve the merger of AFT Merger Sub (as defined below) with and into AFT (the “AFT Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC, pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AFT, AFT Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AFT Merger Sub”), and, for the limited purposes set forth therein, Apollo Investment Management, L.P., a Delaware limited partnership and the investment adviser to MFIC (“MFIC Adviser”) (as may be amended from time to time, the “AFT Merger Agreement”), subject to the terms and conditions set forth in the AFT Merger Agreement, AFT Merger Sub would merge with and into AFT (the “AFT Merger”) (such proposal, the “AFT Merger Proposal”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT Mergers, AFT would merge with and into MFIC, with MFIC continuing as the surviving company.

The closing of the AFT Mergers (as defined below) (the “AFT Closing”) is contingent upon:

(a) MFIC Stockholder approval of the issuance of shares of MFIC common stock, par value $0.001 per share (“MFIC Common Stock”) pursuant to the Mergers (as defined below) in accordance with NASDAQ listing rule requirements (“MFIC Share Issuance” and such proposal, the “MFIC Share Issuance Proposal”),

(b) approval of the AFT Mergers by holders of shares of common stock, par value $0.001 per share (“AFT Common Stock”), of AFT, and

(c) satisfaction or waiver of certain other closing conditions.

If the AFT Mergers do not close, then MFIC will not issue shares of MFIC Common Stock to holders of AFT Common Stock (“AFT Stockholders”), even if the MFIC Share Issuance Proposal is approved by the MFIC Stockholders.

The closing of the AIF Mergers (as defined below) (the “AIF Closing”) is contingent upon:

(a) MFIC Stockholder approval of the MFIC Share Issuance Proposal,

Table of Contents

(b) approval of the AIF Mergers by holders of shares of common stock, par value $0.001 per share (“AIF Common Stock”), of AIF, and

(c) satisfaction or waiver of certain other closing conditions.

If the AIF Mergers do not close, then MFIC will not issue shares of MFIC Common Stock to holders of AIF Common Stock (“AIF Stockholders”), even if the MFIC Share Issuance Proposal is approved by the MFIC Stockholders. The AFT Closing is not contingent upon the AIF Closing having occurred, and the AIF Closing is not contingent upon the AFT Closing having occurred.

As of September 30, 2023, the net asset value (“NAV”) of MFIC Common Stock was $15.28 per share. As of September 30, 2023, the NAV of AFT Common Stock was $15.05 per share. As of September 30, 2023, the NAV of AIF Common Stock was $14.63 per share. Based on the NAVs of MFIC, AFT and AIF as of September 30, 2023, (and adjusted for estimated transaction costs), MFIC would issue approximately 0.9849 and 0.9577 shares of MFIC Common Stock for each share of AFT Common Stock and AIF Common Stock outstanding.

AFT Mergers: Pursuant to the AFT Merger Agreement, AFT Merger Sub would merge with and into AFT (the “AFT First Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT First Merger, AFT would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AFT First Merger, the “AFT Mergers”).

Subject to the terms and conditions of the AFT Merger Agreement, at the AFT Effective Time, each share of AFT Common Stock issued and outstanding immediately prior to the AFT Effective Time (other than shares owned by MFIC or any of its consolidated subsidiaries, including AFT Merger Sub (the “AFT Cancelled Shares”)) will be converted into the right to receive a number of shares of MFIC Common Stock equal to the AFT Exchange Ratio (as defined below) (cash will be paid in lieu of fractional shares). AFT has no preferred stock outstanding, and no preferred stock will be issued by MFIC as a result of the AFT Mergers.

Under the AFT Merger Agreement, as of a mutually agreed date no earlier than 48 hours (excluding Sundays and holidays) prior to the AFT Effective Time (such date, the “AFT Determination Date”), MFIC and AFT will deliver to the other a calculation of its NAV as of such date (such calculation with respect to AFT, the “Closing AFT Net Asset Value” and such calculation with respect to MFIC, the “Closing AFT Merger MFIC Net Asset Value”), in each case using the same set of assumptions, methodologies and adjustments as has been historically used in preparing such calculation. Based on such calculations, the parties will calculate: (1) the “AFT Per Share NAV,” which will be equal to (i) the Closing AFT Net Asset Value divided by (ii) the number of shares of AFT Common Stock issued and outstanding as of the AFT Determination Date (excluding any AFT Cancelled Shares) and (2) the “AFT Merger MFIC Per Share NAV,” which will be equal to (A) the Closing AFT Merger MFIC Net Asset Value divided by (B) the number of shares of MFIC Common Stock issued and outstanding as of the AFT Determination Date. The “AFT Exchange Ratio” will be equal to the quotient (rounded to four decimal places) of (i) the AFT Per Share NAV divided by (ii) the AFT Merger MFIC Per Share NAV.

MFIC and AFT will update and redeliver the Closing AFT Merger Company Net Asset Value or the Closing AFT Net Asset Value, respectively, in the event that the closing of the AFT Mergers is subsequently materially delayed or there is a material change to such calculation between the AFT Determination Date and the closing of the AFT Mergers and as needed to ensure that the calculation is determined within 48 hours (excluding Sundays and holidays) prior to the AFT Effective Time.

Immediately following the AFT Effective Time, MFIC will repay or prepay any amounts outstanding under AFT’s existing credit facility as of the AFT Effective Time, subject to the conditions set forth in MFIC’s senior secured credit facility.

Table of Contents

Promptly following closing of the AFT Mergers, MFIC Adviser or one of its affiliates will pay directly to holders of shares of AFT Common Stock that are issued and outstanding immediately prior to the AFT Effective Time a special payment equal to $0.25 per share of AFT Common Stock, subject to deduction for any applicable withholding tax. This payment will not be made by or through AFT. The specific tax characteristics of the $0.25 per share special payment are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

The AFT Merger Agreement contains certain termination rights, including if the AFT Mergers are not completed on or before November 7, 2024, or if the requisite approvals of MFIC’s and AFT’s stockholders are not obtained. The AFT Merger Agreement provides that, upon the termination of the AFT Merger Agreement under certain circumstances involving entry into a definitive transaction by AFT with a third party, such third party that enters into the definitive transaction with AFT may be required to pay MFIC a termination fee of $7,029,482. The AFT Merger Agreement also provides that, upon the termination of the AFT Merger Agreement under certain circumstances involving entry into a definitive transaction by MFIC with a third party, such third party that enters into the definitive agreement with MFIC may be required to pay to AFT a termination fee of $29,905,339.

Within thirty days following the closing of the AFT Mergers or the termination of the AFT Merger Agreement pursuant to the terms thereof, as applicable, subject to the closing of the AIF Mergers and applicable law, MFIC shall distribute to the holder of each share of MFIC Common Stock as of a record date to be determined by the MFIC Board an amount in cash equal to $0.20 per share of MFIC Common Stock held by such holder. The specific tax characteristics of the $0.20 per share special distribution are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

AIF Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AIF, AIF Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AIF Merger Sub”), and, for the limited purposes set forth therein, MFIC Adviser (as may be amended from time to time, the “AIF Merger Agreement” and, together with the AFT Merger Agreement, the “Merger Agreements”), subject to the terms and conditions set forth in the AIF Merger Agreement, as of the applicable effective time (the “AIF Effective Time”) AIF Merger Sub would merge with and into AIF (the “AIF First Merger”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF First Merger, AIF would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AIF First Merger, the “AIF Mergers” and, together with the AFT Mergers, the “Mergers”).

Subject to the terms and conditions of the AIF Merger Agreement, at the AIF Effective Time, each share of common stock, par value $0.001 per share, of AIF (the “AIF Common Stock”) issued and outstanding immediately prior to the AIF Effective Time (other than shares owned by MFIC or any of its consolidated subsidiaries, including AIF Merger Sub (the “AIF Cancelled Shares”)) will be converted into the right to receive a number of shares of MFIC Common Stock equal to the AIF Exchange Ratio (as defined below), plus any cash (without interest) in lieu of fractional shares. AIF has no preferred stock outstanding, and no preferred stock will be issued by MFIC as a result of the AIF Mergers.

Under the AIF Merger Agreement, as of a mutually agreed date no earlier than 48 hours (excluding Sundays and holidays) prior to the AIF Effective Time (such date, the “AIF Determination Date”), each of MFIC and AIF will deliver to the other a calculation of its net asset value as of such date (such calculation with respect to AIF, the “Closing AIF Net Asset Value” and such calculation with respect to MFIC, the “Closing AIF Merger MFIC Net Asset Value”), in each case using the same set of assumptions, methodologies and adjustments as has been historically used in preparing such calculation. Based on such calculations, the parties will calculate: (1) the “AIF Per Share NAV,” which will be equal to (i) the Closing AIF Net Asset Value divided by (ii) the number of shares of AIF Common Stock issued and outstanding as of the AIF Determination Date (excluding any AIF Cancelled Shares) and (2) the “AIF Merger MFIC Per Share NAV,” which will be equal to (i) the Closing AIF Merger MFIC Net Asset Value divided by (ii) the number of shares of MFIC Common Stock issued and outstanding as of the AIF Determination Date. The “AIF Exchange Ratio” will be equal to the quotient (rounded to four decimal places) of (i) the AIF Per Share NAV divided by (ii) the AIF Merger MFIC Per Share NAV.

Table of Contents

MFIC and AIF will update and redeliver the Closing AIF Merger MFIC Net Asset Value or the Closing AIF Net Asset Value, respectively, in the event that the closing of the AIF Mergers is subsequently materially delayed or there is a material change to such calculation between the AIF Determination Date and the closing of the AIF Mergers and as needed to ensure that the calculation is determined within 48 hours (excluding Sundays and holidays) prior to the AIF Effective Time.

Immediately following the AIF Effective Time, MFIC will repay or prepay any amounts outstanding under AIF’s existing credit facility as of the AIF Effective Time, subject to the conditions set forth in MFIC’s senior secured credit facility.

Promptly following closing of the AIF Mergers, MFIC Adviser or one of its affiliates will pay directly to holders of shares of AIF Common Stock that are issued and outstanding immediately prior to the AIF Effective Time a special payment equal to $0.25 per share of AIF Common Stock, subject to deduction for any applicable withholding tax. This payment will not be made by or through AIF. The specific tax characteristics of the $0.25 per share special payment are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

The AIF Merger Agreement contains certain termination rights, including if the AIF Mergers are not completed on or before November 7, 2024, or if the requisite approvals of MFIC’s and AIF’s stockholders are not obtained. The AIF Merger Agreement provides that, upon the termination of the AIF Merger Agreement under certain circumstances involving entry into a definitive transaction by AIF with a third party, such third party that enters into the definitive transaction with AIF may be required to pay MFIC a termination fee of $6,348,267. The AIF Merger Agreement also provides that, upon the termination of the AIF Merger Agreement under certain circumstances involving entry into a definitive transaction by MFIC with a third party, such third party that enters into the definitive agreement with MFIC may be required to pay to AIF a termination fee of $29,905,339.

Within thirty days following the closing of the AIF Mergers or the termination of the AIF Merger Agreement pursuant to the terms thereof, as applicable, subject to the closing of the AFT Mergers and applicable law, MFIC shall distribute to the holder of each share of MFIC Common Stock as of a record date to be determined by the MFIC Board an amount in cash equal to $0.20 per share of MFIC Common Stock held by such holder. The specific tax characteristics of the $0.20 per share special distribution are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

Your vote is extremely important. The presence at the AFT Special Meeting, virtually or represented by proxy, of AFT Stockholders entitled to cast a majority of all the votes entitled to be cast at the AFT Special Meeting will constitute a quorum of AFT. At the AFT Special Meeting, you will be asked to vote on the AFT Merger Proposal. The approval of the AFT Merger Proposal requires the affirmative vote of a majority of the securities of AFT entitled to vote on the AFT Merger Proposal.

Abstentions will have the same effect as votes “against” the AFT Merger Proposal.

After careful consideration, and on the recommendation of a special committee of the Board of Directors of AFT (the “AFT Board”), the AFT Board unanimously approved the AFT Merger Agreement, declared the AFT Mergers and the transactions contemplated by the AFT Merger Agreement advisable and unanimously recommends that AFT Stockholders vote “FOR” the AFT Merger Proposal.

It is important that your shares be represented at the AFT Special Meeting. Please follow the instructions on the enclosed proxy card and authorize a proxy to vote your shares via the Internet, by telephone or by signing, dating and returning the enclosed proxy card. AFT encourages you to authorize a proxy to vote your shares via the Internet as it saves AFT significant time and processing costs. Voting by proxy does not deprive you of your right to participate in the virtual AFT Special Meeting.

Table of Contents

This joint proxy statement/prospectus describes the AFT Special Meeting, the Mergers, and the documents related to the Mergers (including the Merger Agreement) that AFT Stockholders should review before voting on the AFT Merger Proposal and should be retained for future reference. Please carefully read this entire document, including “Risk Factors” beginning on page 47 and as otherwise incorporated by reference in this joint proxy statement/prospectus, for a discussion of the risks relating to the Mergers, MFIC, AFT and AFT. AFT files periodic reports, current reports, proxy statements and other information with the U.S. Securities and Exchange Commission (the “SEC”). This information is available free of charge, and stockholder inquiries can be made, by contacting AFT at 9 West 57th Street, New York, NY, 10019 or by calling AFT at (212) 515-3200 or on AFT’s website at https://www.apollofunds.com/apollo-senior-floating-rate-fund. The SEC also maintains a website at www.sec.gov that contains such information. Except for the documents incorporated by reference into this joint proxy statement/prospectus, information on AFT’s website is not incorporated into or a part of this joint proxy statement/prospectus.

No matter how many or few shares of AFT you own, your vote and participation are very important to us.

| Sincerely yours, |

|

|

| Barry Cohen |

| Chairman of the AFT Board |

Neither the SEC nor any state securities commission has approved or disapproved of the shares of MFIC Common Stock to be issued under this joint proxy statement/prospectus or determined if this joint proxy statement/prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This joint proxy statement/prospectus is dated [ ], 2024 and is first being mailed or otherwise delivered to AFT Stockholders on or about [ ], 2024.

| MidCap Financial Investment Corporation 9 West 57th Street New York, NY 10019 (212) 515-3450 |

Apollo Senior Floating Rate 9 West 57th Street New York, NY 10019 (212) 515-3200 |

Apollo Tactical Income Fund Inc. 9 West 57th Street New York, NY 10019 (212) 515-3200 |

Table of Contents

APOLLO SENIOR FLOATING RATE FUND INC.

9 West 57th Street

New York, NY 10019

NOTICE OF VIRTUAL SPECIAL MEETING OF STOCKHOLDERS

Online Meeting Only—No Physical Meeting Location

[WEBSITE ADDRESS]

[ ], 2024, at [ ] a.m., Eastern Time

Dear Stockholder:

A Special Meeting of Stockholders (the “AFT Special Meeting”) of Apollo Senior Floating Rate Fund Inc., a Maryland corporation (“AFT”), will be conducted online on [ ], 2024, at [ ] a.m., Eastern Time at the following website: [ ].

MidCap Financial Investment Corporation, a Maryland corporation (“MFIC”), AFT and Apollo Tactical Income Fund Inc., a Maryland corporation (“AIF”), are proposing a combination of all three companies by mergers and related transactions pursuant to two separate Agreements and Plan of Merger. MFIC is a closed-end, externally managed, diversified management investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Each of AFT and AIF are registered under the 1940 Act as diversified, closed-end management investment companies.

At the AFT Special Meeting, the holders of shares of common stock, par value $0.001 per share (“AFT Common Stock”), of AFT (“AFT Stockholders”) will consider and vote on a proposal to approve the merger of AFT Merger Sub (as defined below) with and into AFT (the “AFT Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC, pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AFT, AFT Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AFT Merger Sub”), and, for the limited purposes set forth therein, Apollo Investment Management, L.P., a Delaware limited partnership and the investment adviser to MFIC (“MFIC Adviser”) (as may be amended from time to time, the “AFT Merger Agreement”), subject to the terms and conditions set forth in the AFT Merger Agreement, AFT Merger Sub would merge with and into AFT (such proposal, the “AIF Merger Proposal”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT Mergers, AFT would merge with and into MFIC, with MFIC continuing as the surviving company.

AFT Mergers: Pursuant to the AFT Merger Agreement, AFT Merger Sub would merge with and into AFT (the “AFT First Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT First Merger, AFT would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AFT First Merger, the “AFT Mergers”).

AIF Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AIF, AIF Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AIF Merger Sub”), and, for the limited purposes set forth therein, MFIC Adviser (as may be amended from time to time, the “AIF Merger Agreement” and together with the AFT Merger Agreement, the “Merger Agreements”), subject to the terms and conditions set forth in the AIF Merger Agreement, as of the applicable effective time (the “AIF Effective Time”) AIF Merger Sub would merge with and into AIF (the “AIF First Merger”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF First Merger, AIF would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AIF First Merger, the “AIF Mergers” and, together with the AFT Mergers, the “Mergers”).

Table of Contents

AFTER CAREFUL CONSIDERATION, AND ON THE RECOMMENDATION OF A SPECIAL COMMITTEE OF THE BOARD OF DIRECTORS OF AFT (THE “AFT BOARD”), THE AFT BOARD UNANIMOUSLY APPROVED THE AFT MERGER AGREEMENT, DECLARED THE AFT MERGERS AND THE TRANSACTIONS CONTEMPLATED BY THE AFT MERGER AGREEMENT ADVISABLE, AND UNANIMOUSLY RECOMMENDS THAT AFT STOCKHOLDERS VOTE “FOR” THE AFT MERGER PROPOSAL.

You have the right to receive notice of, and to vote at, the AFT Special Meeting if you were a stockholder of record of AFT at the close of business on [ ], 2024. A joint proxy statement/prospectus is attached to this Notice that describes the matters to be voted upon at the AFT Special Meeting or any adjournment(s) or postponement(s) thereof. The enclosed proxy card will instruct you as to how you may authorize a proxy to vote your shares via the Internet, by telephone or by signing, dating and returning the enclosed proxy card. In addition, information regarding how to find the logistical details of the virtual AFT Special Meeting (including how to remotely access, participate in and vote during the virtual meeting) is included beginning on page 58 of the attached joint proxy statement/prospectus.

Whether or not you plan to participate in the AFT Special Meeting, we encourage you to authorize a proxy to vote your shares by following the instructions on the enclosed proxy card. Please note, however, that if you wish to vote during the AFT Special Meeting and your shares are held of record by a broker or nominee, you must obtain a “legal” proxy issued in your name from that record holder.

We are not aware of any other business that may properly be brought before the AFT Special Meeting, and, pursuant to our bylaws, only the matters set forth in the notice of special meeting may be brought before the AFT Special Meeting.

Thank you for your continued support of AFT.

| By order of the Board of Directors, |

|

|

| Kristin Hester |

| Chief Legal Officer and Secretary |

New York, NY

[ ], 2024

To ensure proper representation at the AFT Special Meeting, please follow the instructions on the enclosed proxy card to authorize a proxy to vote your shares via the Internet or telephone, or by signing, dating and returning the enclosed proxy card. Even if you authorize a proxy to vote your shares prior to the virtual AFT Special Meeting, you still may participate in the virtual AFT Special Meeting.

Table of Contents

APOLLO TACTICAL INCOME FUND INC.

9 West 57th Street

New York, NY 10019

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

[ ], 2024

Dear Stockholder:

You are cordially invited to attend the Special Meeting of Stockholders (the “AIF Special Meeting”) of Apollo Tactical Income Fund Inc., a Maryland corporation (“AIF”), to be held virtually on [ ], 2024, at [ ] a.m., Eastern Time, at the following website: [ ]. Stockholders of record of AIF at the close of business on [ ], 2024 are entitled to notice of, and to vote at, the AIF Special Meeting or any adjournment or postponement thereof.

MidCap Financial Investment Corporation, a Maryland corporation (“MFIC”), AIF and Apollo Senior Floating Rate Fund Inc., a Maryland corporation (“AFT”), are proposing a combination of all three companies by mergers and related transactions pursuant to two separate Agreements and Plan of Merger. MFIC is a closed-end, externally managed, diversified management investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Each of AFT and AIF are registered under the 1940 Act as diversified, closed-end management investment companies.

The notice of special meeting and the joint proxy statement/prospectus accompanying this letter provide an outline of the business to be conducted at the AIF Special Meeting. At the AIF Special Meeting, you will be asked to approve the merger of AIF Merger Sub (as defined below) with and into AIF (the “AIF Mergers”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC, pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AIF, AIF Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AIF Merger Sub”), and, for the limited purposes set forth therein, Apollo Investment Management, L.P., a Delaware limited partnership and the investment adviser to MFIC (“MFIC Adviser”) (as may be amended from time to time, the “AIF Merger Agreement”), subject to the terms and conditions set forth in the AIF Merger Agreement, AIF Merger Sub would merge with and into AIF (the “AIF Mergers”) (such proposal, the “AIF Merger Proposal”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF Mergers, AIF would merge with and into MFIC, with MFIC continuing as the surviving company.

The closing of the AIF Mergers (as defined below) (the “AIF Closing”) is contingent upon:

(a) MFIC Stockholder approval of the issuance of shares of MFIC common stock, par value $0.001 per share (“MFIC Common Stock”) pursuant to the Mergers (as defined below) in accordance with NASDAQ listing rule requirements (“MFIC Share Issuance” and such proposal, the “MFIC Share Issuance Proposal”),

(b) approval of the AIF Mergers by holders of shares of common stock, par value $0.001 per share (“AIF Common Stock”), of AIF, and

(c) satisfaction or waiver of certain other closing conditions.

If the AIF Mergers do not close, then MFIC will not issue shares of MFIC Common Stock to holders of AIF Common Stock (“AIF Stockholders”), even if the MFIC Share Issuance Proposal is approved by the MFIC Stockholders.

The closing of the AFT Mergers (as defined below) (the “AFT Closing”) is contingent upon:

(a) MFIC Stockholder approval of the MFIC Share Issuance Proposal,

Table of Contents

(b) approval of the AFT Mergers by holders of shares of common stock, par value $0.001 per share (“AFT Common Stock”), of AFT, and

(c) satisfaction or waiver of certain other closing conditions.

If the AFT Mergers do not close, then MFIC will not issue shares of MFIC Common Stock to holders of AFT Common Stock (“AFT Stockholders”), even if the MFIC Share Issuance Proposal is approved by the MFIC Stockholders. The AIF Closing is not contingent upon the AFT Closing having occurred, and the AFT Closing is not contingent upon the AIF Closing having occurred.

As of September 30, 2023, the net asset value (“NAV”) of MFIC Common Stock was $15.28 per share. As of September 30, 2023, the NAV of AFT Common Stock was $15.05 per share. As of September 30, 2023, the NAV of AIF Common Stock was $14.63 per share. Based on the NAVs of MFIC, AFT and AIF as of September 30, 2023, (and adjusted for estimated transaction costs), MFIC would issue approximately 0.9849 and 0.9577 shares of MFIC Common Stock for each share of AFT Common Stock and AIF Common Stock outstanding.

AIF Mergers: Pursuant to the AIF Merger Agreement, AIF Merger Sub would merge with and into AIF (the “AIF First Merger”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF First Merger, AIF would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AIF First Merger, the “AIF Mergers”).

Subject to the terms and conditions of the AIF Merger Agreement, at the AIF Effective Time, each share of AIF Common Stock issued and outstanding immediately prior to the AIF Effective Time (other than shares owned by MFIC or any of its consolidated subsidiaries, including AIF Merger Sub (the “AIF Cancelled Shares”)) will be converted into the right to receive a number of shares of MFIC Common Stock equal to the AIF Exchange Ratio (as defined below) (cash will be paid in lieu of fractional shares). AIF has no preferred stock outstanding, and no preferred stock will be issued by MFIC as a result of the AIF Mergers.

Under the AIF Merger Agreement, as of a mutually agreed date no earlier than 48 hours (excluding Sundays and holidays) prior to the AIF Effective Time (such date, the “AIF Determination Date”), MFIC and AIF will deliver to the other a calculation of its NAV as of such date (such calculation with respect to AIF, the “Closing AIF Net Asset Value” and such calculation with respect to MFIC, the “Closing AIF Merger MFIC Net Asset Value”), in each case using the same set of assumptions, methodologies and adjustments as has been historically used in preparing such calculation. Based on such calculations, the parties will calculate: (1) the “AIF Per Share NAV,” which will be equal to (i) the Closing AIF Net Asset Value divided by (ii) the number of shares of AIF Common Stock issued and outstanding as of the AIF Determination Date (excluding any AIF Cancelled Shares) and (2) the “AIF Merger MFIC Per Share NAV,” which will be equal to (A) the Closing AIF Merger MFIC Net Asset Value divided by (B) the number of shares of MFIC Common Stock issued and outstanding as of the AIF Determination Date. The “AIF Exchange Ratio” will be equal to the quotient (rounded to four decimal places) of (i) the AIF Per Share NAV divided by (ii) the AIF Merger MFIC Per Share NAV.

MFIC and AIF will update and redeliver the Closing AIF Merger Company Net Asset Value or the Closing AIF Net Asset Value, respectively, in the event that the closing of the AIF Mergers is subsequently materially delayed or there is a material change to such calculation between the AIF Determination Date and the closing of the AIF Mergers and as needed to ensure that the calculation is determined within 48 hours (excluding Sundays and holidays) prior to the AIF Effective Time.

Immediately following the AIF Effective Time, MFIC will repay or prepay any amounts outstanding under AIF’s existing credit facility as of the AIF Effective Time, subject to the conditions set forth in MFIC’s senior secured credit facility.

Promptly following closing of the AIF Mergers, MFIC Adviser or one of its affiliates will pay directly to holders of shares of AIF Common Stock that are issued and outstanding immediately prior to the AIF Effective Time a special payment equal to $0.25 per share of AIF Common Stock, subject to deduction for any applicable

Table of Contents

withholding tax. This payment will not be made by or through AIF. The specific tax characteristics of the $0.25 per share special payment are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

The AIF Merger Agreement contains certain termination rights, including if the AIF Mergers are not completed on or before November 7, 2024, or if the requisite approvals of MFIC’s and AIF’s stockholders are not obtained. The AIF Merger Agreement provides that, upon the termination of the AIF Merger Agreement under certain circumstances involving entry into a definitive transaction by AIF with a third party, such third party that enters into the definitive transaction with AIF may be required to pay MFIC a termination fee of $6,348,267. The AIF Merger Agreement also provides that, upon the termination of the AIF Merger Agreement under certain circumstances involving entry into a definitive transaction by MFIC with a third party, such third party that enters into the definitive agreement with MFIC may be required to pay to AIF a termination fee of $29,905,339.

Within thirty days following the closing of the AIF Mergers or the termination of the AIF Merger Agreement pursuant to the terms thereof, as applicable, subject to the closing of the AFT Mergers and applicable law, MFIC shall distribute to the holder of each share of MFIC Common Stock as of a record date to be determined by the MFIC Board an amount in cash equal to $0.20 per share of MFIC Common Stock held by such holder. The specific tax characteristics of the $0.20 per share special distribution are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

AFT Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AFT, AFT Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AFT Merger Sub”), and, for the limited purposes set forth therein, MFIC Adviser (as may be amended from time to time, the “AFT Merger Agreement” and, together with the AIF Merger Agreement, the “Merger Agreements”), subject to the terms and conditions set forth in the AFT Merger Agreement, as of the applicable effective time (the “AFT Effective Time”) AFT Merger Sub would merge with and into AFT (the “AFT First Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT First Merger, AFT would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AFT First Merger, the “AFT Mergers” and, together with the AIF Mergers, the “Mergers”).

Subject to the terms and conditions of the AFT Merger Agreement, at the AFT Effective Time, each share of common stock, par value $0.001 per share, of AFT (the “AFT Common Stock”) issued and outstanding immediately prior to the AFT Effective Time (other than shares owned by MFIC or any of its consolidated subsidiaries, including AFT Merger Sub (the “AFT Cancelled Shares”)) will be converted into the right to receive a number of shares of MFIC Common Stock equal to the AFT Exchange Ratio (as defined below), plus any cash (without interest) in lieu of fractional shares. AFT has no preferred stock outstanding, and no preferred stock will be issued by MFIC as a result of the AFT Mergers.

Under the AFT Merger Agreement, as of a mutually agreed date no earlier than 48 hours (excluding Sundays and holidays) prior to the AFT Effective Time (such date, the “AFT Determination Date”), each of MFIC and AFT will deliver to the other a calculation of its net asset value as of such date (such calculation with respect to AFT, the “Closing AFT Net Asset Value” and such calculation with respect to MFIC, the “Closing AFT Merger MFIC Net Asset Value”), in each case using the same set of assumptions, methodologies and adjustments as has been historically used in preparing such calculation. Based on such calculations, the parties will calculate: (1) the “AFT Per Share NAV,” which will be equal to (i) the Closing AFT Net Asset Value divided by (ii) the number of shares of AFT Common Stock issued and outstanding as of the AFT Determination Date (excluding any AFT Cancelled Shares) and (2) the “AFT Merger MFIC Per Share NAV,” which will be equal to (i) the Closing AFT Merger MFIC Net Asset Value divided by (ii) the number of shares of MFIC Common Stock issued and outstanding as of the AFT Determination Date. The “AFT Exchange Ratio” will be equal to the quotient (rounded to four decimal places) of (i) the AFT Per Share NAV divided by (ii) the AFT Merger MFIC Per Share NAV.

Table of Contents

MFIC and AFT will update and redeliver the Closing AFT Merger MFIC Net Asset Value or the Closing AFT Net Asset Value, respectively, in the event that the closing of the AFT Mergers is subsequently materially delayed or there is a material change to such calculation between the AFT Determination Date and the closing of the AFT Mergers and as needed to ensure that the calculation is determined within 48 hours (excluding Sundays and holidays) prior to the AFT Effective Time.

Immediately following the AFT Effective Time, MFIC will repay or prepay any amounts outstanding under AFT’s existing credit facility as of the AFT Effective Time, subject to the conditions set forth in MFIC’s senior secured credit facility.

Promptly following closing of the AFT Mergers, MFIC Adviser or one of its affiliates will pay directly to holders of shares of AFT Common Stock that are issued and outstanding immediately prior to the AFT Effective Time a special payment equal to $0.25 per share of AFT Common Stock, subject to deduction for any applicable withholding tax. This payment will not be made by or through AFT. The specific tax characteristics of the $0.25 per share special payment are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

The AFT Merger Agreement contains certain termination rights, including if the AFT Mergers are not completed on or before November 7, 2024, or if the requisite approvals of MFIC’s and AFT’s stockholders are not obtained. The AFT Merger Agreement provides that, upon the termination of the AFT Merger Agreement under certain circumstances involving entry into a definitive transaction by AFT with a third party, such third party that enters into the definitive transaction with AFT may be required to pay MFIC a termination fee of $7,029,482. The AFT Merger Agreement also provides that, upon the termination of the AFT Merger Agreement under certain circumstances involving entry into a definitive transaction by MFIC with a third party, such third party that enters into the definitive agreement with MFIC may be required to pay to AFT a termination fee of $29,905,339.

Within thirty days following the closing of the AFT Mergers or the termination of the AFT Merger Agreement pursuant to the terms thereof, as applicable, subject to the closing of the AIF Mergers and applicable law, MFIC shall distribute to the holder of each share of MFIC Common Stock as of a record date to be determined by the MFIC Board an amount in cash equal to $0.20 per share of MFIC Common Stock held by such holder. The specific tax characteristics of the $0.20 per share special distribution are described in “Certain Material U.S. Federal Income Tax Considerations—Tax Consequences if the Merger Qualifies as a Reorganization.”

Your vote is extremely important. The presence at the AIF Special Meeting, virtually or represented by proxy, of AIF Stockholders entitled to cast a majority of all the votes entitled to be cast at the AIF Special Meeting will constitute a quorum of AIF. At the AIF Special Meeting, you will be asked to vote on the AIF Merger Proposal. The approval of the AIF Merger Proposal requires the affirmative vote of a majority of the securities of AIF entitled to vote on the AIF Merger Proposal.

Abstentions will have the same effect as votes “against” the AIF Merger Proposal.

After careful consideration, and on the recommendation of a special committee of the Board of Directors of AIF (the “AIF Board”), the AIF Board unanimously approved the AIF Merger Agreement, declared the AIF Mergers and the transactions contemplated by the AIF Merger Agreement advisable and unanimously recommends that AIF Stockholders vote “FOR” the AIF Merger Proposal.

It is important that your shares be represented at the AIF Special Meeting. Please follow the instructions on the enclosed proxy card and authorize a proxy to vote your shares via the Internet, by telephone or by signing, dating and returning the enclosed proxy card. AIF encourages you to authorize a proxy to vote your shares via the Internet as it saves AIF significant time and processing costs. Voting by proxy does not deprive you of your right to participate in the virtual AIF Special Meeting.

Table of Contents

This joint proxy statement/prospectus describes the AIF Special Meeting, the Mergers, and the documents related to the Mergers (including the Merger Agreement) that AIF Stockholders should review before voting on the AIF Merger Proposal and should be retained for future reference. Please carefully read this entire document, including “Risk Factors” beginning on page 47 and as otherwise incorporated by reference in this joint proxy statement/prospectus, for a discussion of the risks relating to the Mergers, MFIC, AIF and AFT. AIF files periodic reports, current reports, proxy statements and other information with the U.S. Securities and Exchange Commission (the “SEC”). This information is available free of charge, and stockholder inquiries can be made, by contacting AIF at 9 West 57th Street, New York, NY, 10019 or by calling AIF at (212) 515-3200 or on AIF’s website at https://www.apollofunds.com/apollo-tactical-income-fund. The SEC also maintains a website at www.sec.gov that contains such information. Except for the documents incorporated by reference into this joint proxy statement/prospectus, information on AIF’s website is not incorporated into or a part of this joint proxy statement/prospectus.

No matter how many or few shares of AIF you own, your vote and participation are very important to us.

| Sincerely yours, |

|

|

| Barry Cohen |

| Chairman of the AIF Board |

Neither the SEC nor any state securities commission has approved or disapproved of the shares of MFIC Common Stock to be issued under this joint proxy statement/prospectus or determined if this joint proxy statement/prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This joint proxy statement/prospectus is dated [ ], 2024 and is first being mailed or otherwise delivered to AIF Stockholders on or about [ ], 2024.

| MidCap Financial Investment Corporation 9 West 57th Street New York, NY 10019 (212) 515-3450 |

Apollo Senior Floating Rate 9 West 57th Street New York, NY 10019 (212) 515-3200 |

Apollo Tactical Income Fund Inc. 9 West 57th Street New York, NY 10019 (212) 515-3200 |

Table of Contents

APOLLO TACTICAL INCOME FUND INC.

9 West 57th Street

New York, NY 10019

NOTICE OF VIRTUAL SPECIAL MEETING OF STOCKHOLDERS

Online Meeting Only—No Physical Meeting Location

[WEBSITE ADDRESS]

[ ], 2024, at [ ] a.m., Eastern Time

Dear Stockholder:

A Special Meeting of Stockholders (the “AIF Special Meeting”) of Apollo Tactical Income Fund Inc., a Maryland corporation (“AIF”), will be conducted online on [ ], 2024, at [ ] a.m., Eastern Time at the following website: [ ].

MidCap Financial Investment Corporation, a Maryland corporation (“MFIC”), AIF and Apollo Senior Floating Rate Fund Inc., a Maryland corporation (“AFT”), are proposing a combination of all three companies by mergers and related transactions pursuant to two separate Agreements and Plan of Merger. MFIC is a closed-end, externally managed, diversified management investment company that has elected to be treated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). Each of AFT and AIF are registered under the 1940 Act as diversified, closed-end management investment companies.

At the AIF Special Meeting, the holders of shares of common stock, par value $0.001 per share (“AIF Common Stock”), of AIF (“AIF Stockholders”) will consider and vote on a proposal to approve the merger of AIF Merger Sub (as defined below) with and into AIF (the “AIF Mergers”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC, pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AIF, AIF Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AIF Merger Sub”), and, for the limited purposes set forth therein, Apollo Investment Management, L.P., a Delaware limited partnership and the investment adviser to MFIC (“MFIC Adviser”) (as may be amended from time to time, the “AIF Merger Agreement”), subject to the terms and conditions set forth in the AIF Merger Agreement, AIF Merger Sub would merge with and into AIF (such proposal, the “AIF Merger Proposal”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF Mergers, AIF would merge with and into MFIC, with MFIC continuing as the surviving company.

AIF Mergers: Pursuant to the AIF Merger Agreement, AIF Merger Sub would merge with and into AIF (the “AIF First Merger”), with AIF continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AIF First Merger, AIF would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AIF First Merger, the “AIF Mergers”).

AFT Mergers: Pursuant to the Agreement and Plan of Merger, dated as of November 7, 2023, by and among MFIC, AFT, AFT Merger Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of MFIC (“AFT Merger Sub”), and, for the limited purposes set forth therein, MFIC Adviser (as may be amended from time to time, the “AFT Merger Agreement” and together with the AIF Merger Agreement, the “Merger Agreements”), subject to the terms and conditions set forth in the AFT Merger Agreement, as of the applicable effective time (the “AFT Effective Time”) AFT Merger Sub would merge with and into AFT (the “AFT First Merger”), with AFT continuing as the surviving company and as a wholly-owned subsidiary of MFIC. Immediately after the effectiveness of the AFT First Merger, AFT would merge with and into MFIC, with MFIC continuing as the surviving company (together with the AFT First Merger, the “AFT Mergers” and, together with the AIF Mergers, the “Mergers”).

Table of Contents

AFTER CAREFUL CONSIDERATION, AND ON THE RECOMMENDATION OF A SPECIAL COMMITTEE OF THE BOARD OF DIRECTORS OF AIF (THE “AIF BOARD”), THE AIF BOARD UNANIMOUSLY APPROVED THE AIF MERGER AGREEMENT, DECLARED THE AIF MERGERS AND THE TRANSACTIONS CONTEMPLATED BY THE AIF MERGER AGREEMENT ADVISABLE, AND UNANIMOUSLY RECOMMENDS THAT AIF STOCKHOLDERS VOTE “FOR” THE AIF MERGER PROPOSAL.

You have the right to receive notice of, and to vote at, the AIF Special Meeting if you were a stockholder of record of AIF at the close of business on [ ], 2024. A joint proxy statement/prospectus is attached to this Notice that describes the matters to be voted upon at the AIF Special Meeting or any adjournment(s) or postponement(s) thereof. The enclosed proxy card will instruct you as to how you may authorize a proxy to vote your shares via the Internet, by telephone or by signing, dating and returning the enclosed proxy card. In addition, information regarding how to find the logistical details of the virtual AIF Special Meeting (including how to remotely access, participate in and vote during the virtual meeting) is included beginning on page 61 of the attached joint proxy statement/prospectus.

Whether or not you plan to participate in the AIF Special Meeting, we encourage you to authorize a proxy to vote your shares by following the instructions on the enclosed proxy card. Please note, however, that if you wish to vote during the AIF Special Meeting and your shares are held of record by a broker or nominee, you must obtain a “legal” proxy issued in your name from that record holder.

We are not aware of any other business that may properly be brought before the AIF Special Meeting, and, pursuant to our bylaws, only the matters set forth in the notice of special meeting may be brought before the AIF Special Meeting.

Thank you for your continued support of AIF.

| By order of the Board of Directors, |

|

|

| Kristin Hester |

| Chief Legal Officer and Secretary |

New York, NY

[ ], 2024

To ensure proper representation at the AIF Special Meeting, please follow the instructions on the enclosed proxy card to authorize a proxy to vote your shares via the Internet or telephone, or by signing, dating and returning the enclosed proxy card. Even if you authorize a proxy to vote your shares prior to the virtual AIF Special Meeting, you still may participate in the virtual AIF Special Meeting.

Table of Contents

| Page | ||||

| 1 | ||||

| QUESTIONS AND ANSWERS ABOUT THE STOCKHOLDER MEETINGS AND THE MERGERS |

4 | |||

| 28 | ||||

| 47 | ||||

| 59 | ||||

| 65 | ||||

| 67 | ||||

| 69 | ||||

| 72 | ||||

| 75 | ||||

| 78 | ||||

| 134 | ||||

| 155 | ||||

| 176 | ||||

| 177 | ||||

| 178 | ||||

| 179 | ||||

| 180 | ||||

| 195 | ||||

| 196 | ||||

| 197 | ||||

| 198 | ||||

| 202 | ||||

| 203 | ||||

| 207 | ||||

| CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS OF MFIC |

211 | |||

| 212 | ||||

| 213 | ||||

| 214 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF MFIC |

216 | |||

| 217 | ||||

| 220 | ||||

| 238 | ||||