Our business model is the result of the combination of the local banks’ strengths and local knowledge, which will allow us to reach more clients, with an extended range of products and financial solutions.

By consolidating operations in Chile and Colombia, the new bank became one of Chile’s largest private financial institutions, ranking fifth in the Chilean banking industry with a market share by loans of 9.8% in Chile as of December 31, 2021. The Merger and combination of the strengths of both banks has translated into an expansion in the offer of products and services for our clients, with a large branch platform in Chile. Indeed, we operate 187 branch offices in Chile, one branch in New York, 103 branches in Colombia and one office in Panama.

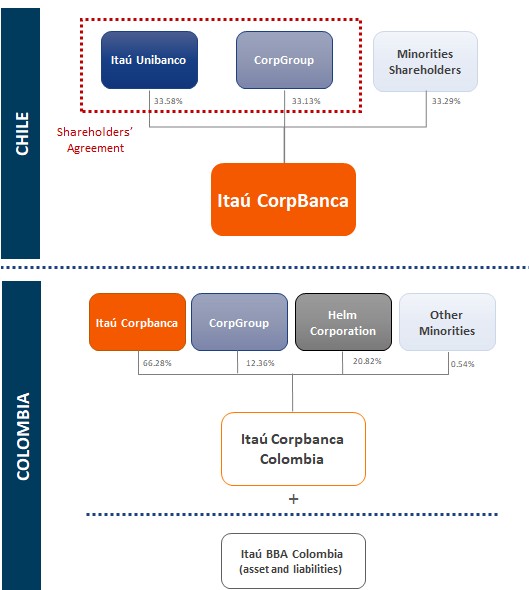

As of the date of this report, Itaú Unibanco Holding and CorpGroup beneficially owned 55.96% and 14.00% of our outstanding common shares, respectively. Itaú Unibanco Holding and CorpGroup also entered into the Itaú CorpGroup Shareholders’ Agreement. Upon the consummation of the Merger, as previously mentioned, Itaú Unibanco Holding became the sole controlling shareholder of the merged bank. For a description of the Itaú CorpGroup Shareholders’ Agreement and the Transaction Agreement, see “Item 10. Additional Information—C. Material Contracts.”

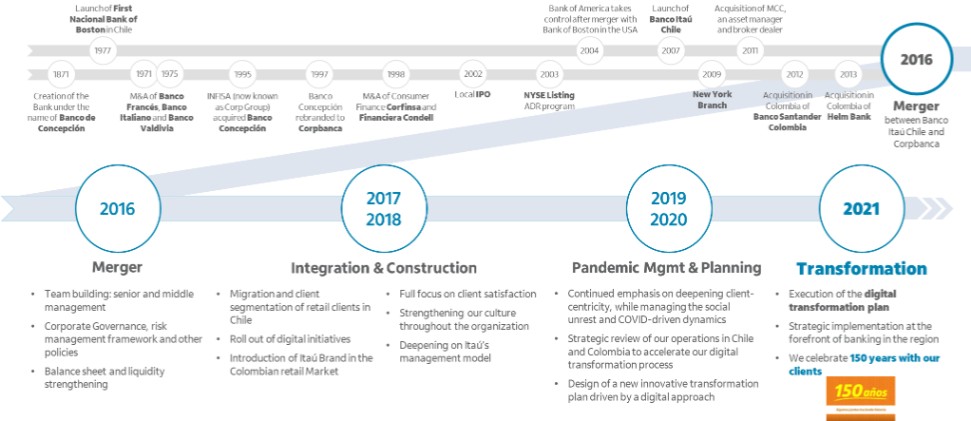

A summary of the main milestones in the history of the Bank is set forth in the following chart:

The Itaú Colombia Acquisition

The obligation of the parties to the Transaction Agreement to cause Itaú Corpbanca to acquire all of the outstanding shares of Itaú BBA Colombia or to carry out a merger of Itaú Corpbanca Colombia, formerly Banco Corpbanca Colombia, with Itaú BBA Colombia was amended on January 20, 2017 and replaced with the obligation of the parties to cause Itaú Corpbanca Colombia to acquire the assets and liabilities of Itaú BBA Colombia at their book value in accordance with the terms and conditions agreed by Itaú Corpbanca Colombia and Itaú BBA Colombia on November 1, 2016 (the “Itaú Colombian Asset & Liabilities Acquisition”). The Itaú Colombian Asset & Liabilities Acquisition was approved by the shareholders of Itaú Corpbanca Colombia and the Colombian Financial Superintendency and completed on June 16, 2017, as established in the agreement signed on June 1, 2017 between Itaú Corpbanca Colombia, as assignee, and Itaú BBA Colombia S.A. Corporación Financiera, as assignor. Pursuant to the Itaú Colombian Asset & Liabilities Acquisition transaction, Itaú Corpbanca Colombia paid to Itaú BBA Colombia S.A. Corporación Financiera Ch$33,205 million. This agreement also contemplated the rendering of certain services by Itaú Corpbanca Colombia in favor of Itaú BBA Colombia and the hiring of the senior management of Itaú BBA Colombia by Itaú Corpbanca Colombia.

On February 22, 2022, following receipt of regulatory approvals from the banking regulators in Chile, Colombia and Brazil, and in compliance with the Transaction Agreement, the Bank completed the acquisition – directly and

49