Table of Contents

ANNUAL REPORT FOR THE FISCAL YEAR ENDING DECEMBER 31, 2015

As filed with the Securities and Exchange Commission on March 31, 2016

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the fiscal year ended December 31, 2015

Commission file number 001-32305

CORPBANCA

(Exact name of Registrant as specified in its charter)

(Translation of Registrant’s name into English)

Republic of Chile

(Jurisdiction of incorporation or organization)

Table of Contents

Rosario Norte 660

Las Condes

Santiago, Chile

(Address of principal executive offices)

Investor Relations, Telephone: +(562) 2660-2555, Facsimile: +(562) 2660-2476,

Address: Rosario Norte 660, Las Condes, Santiago, Chile

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class |

Name of each exchange on which registered | |

| American Depositary Shares representing common shares | New York Stock Exchange | |

| Common shares, no par value* | New York Stock Exchange* |

| * | Not for trading purposes, but only in connection with the registration of American Depositary Shares pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities registered for which there is a reporting obligation pursuant Section 15(d) of the Act.

3.125% Senior Notes due January 15, 2018

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

340,358,194,234

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes x No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Table of Contents

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ |

International Financial Reporting Standards as issued by the International Accounting Standards Board x |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. ¨ Yes ¨ No

Table of Contents

CAUTIONARY LANGUAGE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F contains statements that constitute forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements include statements preceded by, followed by or that include “believes,” “expects,” “intends,” “plans,” “projects,” “estimates” or “anticipates” and similar expressions. These statements appear throughout this Annual Report, including, without limitation, under “Item 3. Key Information—D. Risk Factors”, “Item 4. Information on the Company” and “Item 5. Operating and Financial Review and Prospects”, are not based on historical facts but instead represent only our belief regarding future events, many of which, by their nature, are inherently uncertain and outside our control and include statements regarding our current intent, belief or expectations with respect to (1) our asset growth and financing plans, (2) trends affecting our financial condition or results of operations, (3) the impact of competition and regulations, (4) projected capital expenditures, and (5) liquidity. Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those described in such forward-looking statements included in this Annual Report as a result of various factors (including, without limitation, the actions of competitors, future global economic conditions, market conditions, currency exchange rates and operating and financial risks), many of which are beyond our control. The occurrence of any such factors, not currently expected by us, would significantly alter the results set forth in these statements.

Factors that could cause actual results to differ materially and adversely include, but are not limited to:

| • | trends affecting our financial condition or results of operations; |

| • | our dividend policy; |

| • | changes in the participation of our shareholders or any other factor that may result in a change of control; |

| • | the amount of our indebtedness; |

| • | natural disasters; |

| • | changes in general economic, business, regulatory, political or other conditions in the Republic of Chile, or Chile, or the Republic of Colombia, or Colombia, or changes in general economic or business conditions in Latin America; |

| • | changes in capital markets in general that may affect policies or attitudes towards lending to Chile or Colombia, Chilean or Colombian companies or securities issued by Chilean companies; |

| • | the monetary and interest rate policies of the Central Bank of Chile (Banco Central de Chile), or the Central Bank of Colombia (Banco de la República de Colombia); |

| • | inflation or deflation; |

| • | unemployment; |

| • | unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms; |

| • | unanticipated turbulence in interest rates; |

| • | movements in currency exchange rates; |

| • | movements in equity prices or other rates or prices; |

| • | changes in Chilean, Colombian and foreign laws and regulations; |

| • | changes in Chilean or Colombian tax rates or tax regimes; |

| • | competition, changes in competition and pricing environments; |

| • | our inability to hedge certain risks economically; |

| • | the adequacy of our loss allowances, provisions or reserves; |

| • | technological changes; |

| • | changes in consumer spending and saving habits; |

| • | successful implementation of new technologies; |

i

Table of Contents

| • | loss of market share; |

| • | changes in, or failure to comply with, applicable banking, insurance, securities or other regulations; |

| • | difficulties in successfully integrating recent and future acquisitions into our operations; |

| • | our ability to successfully complete the implementation of a new information technology core banking system in Colombia, as part of the integration process in Colombia; |

| • | consequences of the pending acquisition of a controlling interest in us by Itaú Unibanco Holding S.A, or Itaú Unibanco, as well as the merger of Banco Itaú Chile, or Itaú Chile, with and into us and the potential acquisition of Itaú BBA Colombia S.A., Corporación Financiera, or Itaú Colombia by us or the merger of Itaú Colombia with and into Banco CorpBanca Colombia, S.A., or CorpBanca Colombia (the Itaú-CorpBanca Merger); |

| • | the merged bank’s abilities to achieve revenue benefits and cost savings from the integration between CorpBanca’s and Banco Itaú Chile’s businesses and assets; and |

| • | the other factors identified or discussed under “Item 3. Key Information—D. Risk Factors” in this Annual Report |

You should not place undue reliance on such statements, which speak only as of the date that they were made. These cautionary statements should be considered in connection with any written or oral forward-looking statements that we may make in the future. We do not undertake any obligation to release publicly any revisions to such forward-looking statements after the date of this Annual Report to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

Neither CorpBanca nor Banco Itaú Chile, as a matter of course make public projections as to future net revenues, costs, or other results. However, the both banks have prepared prospective financial information for inclusion in this document mainly related to estimated revenue synergies, cost savings, funding costs and capital position to present the estimated impacts of the merge with Banco Itaú Chile. This prospective financial information was not prepared in accordance with the guidelines established by the American Institute of Certified Public Accounts (the “AICPA”) with respect to prospective financial information.

Statements relating to the cost savings that both, CorpBanca and Banco Itaú Chile expect to achieve following the transaction described in this document are based on assumptions which in the view of the bank’s management, were prepared on a reasonable basis, reflect the best currently available estimates and judgments, and present, to the best of such management’s knowledge and belief, the expected course of action and the expected future financial impact on performance of the bank due to the merger with Banco Itaú-Chile. However, the assumptions about these expected cost savings and growth opportunities are inherently uncertain and, though considered reasonable by management as of the date of its preparation, are subject to a wide variety of significant business, economic, and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information. There can be no assurance that the banks will be able to successfully implement the strategic or operational initiatives that are intended.

Neither CorpBanca’s independent auditors, nor any other independent accountants, have complied with, examined, or performed any procedures with respect to the prospective financial information contained herein, nor have they expressed any opinion or any other form of assurance on such information or its achievability, and assume no responsibility for, or disclaim any association with, the prospective financial information.

ii

Table of Contents

ENFORCEMENT OF CIVIL LIABILITIES

We are a banking corporation organized under the laws of Chile. The majority of our directors or executive officers are not residents of the United States and a substantial portion of our assets and the assets of these persons are located outside the United States. As a result, it may not be possible for you to effect service of process within the United States upon us or such persons or to enforce against them or us in the United States or other foreign courts, judgments obtained in the United States predicated upon the civil liability provisions of the federal securities laws of the United States.

No treaty exists between the United States and Chile for the reciprocal enforcement of court judgments. Chilean courts, however, have enforced final judgments rendered in the United States, subject to the review in Chile of the United States judgment in order to ascertain whether certain basic principles of due process and public policy have been respected, without reviewing the merits of the subject matter of the case. If a United States court grants a final judgment in an action based on the civil liability provisions of the federal securities laws of the United States, enforceability of this judgment in Chile will be subject to the obtaining of the relevant “exequatur” (i.e., recognition and enforcement of the foreign judgment) according to Chilean civil procedure law in force at that time, and consequently, subject to the satisfaction of certain factors. Currently, the most important of these factors are the absence of any conflict between the foreign judgment and Chilean laws (excluding for this purpose the laws of civil procedure) and public policies; the absence of a conflicting judgment by a Chilean court relating to the same parties and arising from the same facts and circumstances; the absence of any further means for appeal or review of the judgment in the jurisdiction where judgment was rendered; the Chilean courts’ determination that the United States courts had jurisdiction; that service of process was appropriately served on the defendant and that the defendant was afforded a real opportunity to appear before the court and defend its case; and that enforcement would not violate Chilean public policy.

In general, the enforceability in Chile of final judgments of United States courts does not require retrial in Chile.

iii

Table of Contents

| PART I | 1 | |||||

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 1 | ||||

| ITEM 2. | 1 | |||||

| ITEM 3. | 1 | |||||

| ITEM 4. | 28 | |||||

| ITEM 4A. | 113 | |||||

| ITEM 5. | 113 | |||||

| ITEM 6. | 140 | |||||

| THE DIRECTORS COMMITTEE AND AUDIT COMMITTEE | ||||||

| ITEM 7. | 149 | |||||

| ITEM 8. | 152 | |||||

| ITEM 9. | 154 | |||||

| ITEM 10. | 155 | |||||

| ITEM 11. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT FINANCIAL RISK |

191 | ||||

| ITEM 12. | 236 | |||||

| PART II | 237 | |||||

| ITEM 13. | 237 | |||||

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

237 | ||||

| ITEM 15. | 237 | |||||

| ITEM 16. | 240 | |||||

| ITEM 16A. | 240 | |||||

| ITEM 16B. | 240 | |||||

| ITEM 16C. | 240 | |||||

| ITEM 16D. | 241 | |||||

| ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

241 | ||||

| ITEM 16F. | 241 | |||||

| ITEM 16G. | 241 | |||||

| ITEM 16H. | 242 | |||||

| PART III | 243 | |||||

| ITEM 17. | 243 | |||||

| ITEM 18. | 243 | |||||

| ITEM 19. | 243 | |||||

iv

Table of Contents

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Statements

We are a Chilean bank and maintain our financial books and records in Chilean pesos and prepare our consolidated financial statements in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. As required by local regulations, our consolidated financial statements filed with the Chilean Superintendency of Banks and Financial Institutions (Superintendencia de Bancos e Instituciones Financieras), also referred to as the SBIF, have been prepared in accordance with Chilean accounting principles or Chilean Bank GAAP, issued by the SBIF; nevertheless, SBIF’s regulations provide that unless specifically regulated by this agency, our financial statements shall be prepared in accordance with IFRS, as issued by the IASB. Unless otherwise indicated herein, as used hereafter IFRS refers to the standards issued by the IASB. Therefore, our consolidated financial statements filed with the SBIF have been adjusted to IFRS in order to comply with the requirements of the Securities and Exchange Commission, or the SEC. We have included herein certain information in Chilean Bank GAAP with respect to the Chilean financial system and the financial performance of the bank. These disclosures are not considered non-GAAP measures as they are required for regulatory purposes in Chile.

The selected consolidated financial information included herein as of December 31, 2015 and for the year ended December 31, 2015, together with the selected consolidated financial information as of December 31, 2011, 2012, 2013 and 2014 and for the years ended December 31, 2011, 2012, 2013 and 2014, is derived from, and presented on the same basis as, our consolidated financial statements prepared under IFRS and should be read together with such consolidated financial statements. Readers should exercise caution in determining trends based on prior annual reports. See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—The Economy—Critical Accounting Policies and Estimates”.

Our auditors, Deloitte Auditores y Consultores Ltda., or Deloitte, an independent registered public accounting firm, have audited our consolidated financial statements in accordance with IFRS as of December 31, 2015 and 2014 and for the years ended December 31, 2013, 2014 and 2015. See page 238 and F-1 of this report for further details on Deloitte’s opinions.

Foreign Currency Markets

In this Annual Report, references to “$,” “US$,” “U.S. dollars” and “dollars” are to United States dollars, references to “Chilean pesos” or “Ch$” are to Chilean pesos, references to “UF” are to Unidades de Fomento and references to “Colombian pesos” or “COP$” are to Colombian pesos. The UF is an inflation-indexed, Chilean peso-denominated unit that is linked to and adjusted daily to reflect changes in the previous month’s Chilean Consumer Price Index of the Chilean National Statistics Institute (Instituto Nacional de Estadísticas). As of December 31, 2015, one UF equaled US$36.08, Ch$25,629.09 and COP$113,102.78 and as of March 11, 2016, one UF equaled US$37.69, Ch$25,762.22 and COP$117,101. See “Item 5. Operating and Financial Review and Prospects”.

This Annual Report contains translations of certain Chilean peso amounts into U.S. dollars and Colombian pesos at specified rates solely for the convenience of the reader. These translations should not be construed as representations that such Chilean peso amounts actually represent such U.S. dollar or Colombian pesos amounts, were converted from U.S. dollars or Colombian pesos amounts at the rate indicated in preparing our financial statements or could be converted into U.S. dollars or Colombian pesos amounts at the rate indicated or any particular rate at all. Unless otherwise indicated, such U.S. dollar and Colombian pesos amounts have been translated from Chilean pesos based on our own exchange rate of Ch$710.32 and COP$3,135.17, respectively, per US$1.00 as of December 31, 2015.

Specific Loan Information

Unless otherwise specified, all references in this Annual Report to total loans are to loans and financial leases before deduction for allowances for loan losses, and they do not include loans to banks or unfunded loan commitments. In addition, all market share data and financial indicators for the Chilean banking system when compared to CorpBanca’s financial information,

1

Table of Contents

presented in this Annual Report or incorporated by reference into this Annual Report are based on information published periodically by the SBIF, which is published under Chilean Bank GAAP and prepared on a consolidated basis. Non-performing loans include the principal and accrued interest on any loan with one installment more than 90 days overdue. Impaired loans include those loans on which there is objective evidence that customers will not meet some of their contractual payment obligations. Past due loans include all installments and lines of credit more than 90 days overdue, provided that the aggregate principal amount of such loans is not included. Under IFRS, a loan is evaluated on each financial statement reporting date to determine whether objective evidence of impairment exists. A loan will be impaired if and only if, objective evidence of impairment exists as a result of one or more events that occurred after the initial recognition of the loan, and such event or events have an impact on the estimated future cash flows of such loan that can be reliably estimated. It may not be possible to identify a single event that was the individual cause of the impairment. An impairment loss relating to a loan is calculated as the difference between the carrying amount of the loan and the present value of estimated future cash flows discounted at the effective interest rate. Individually significant loans are individually tested for impairment. The remaining financial loans are evaluated collectively in groups with similar credit risk characteristics. The reversal of an impairment loss occurs only if it can be objectively related to an event occurring after the initial impairment loss was recorded. In the case of loans recorded at amortized cost, the reversal is recorded in income. See “Item 4. Information on the Company—Business Overview—Selected Statistical Information —Classification of Banks and Loans; Allowances and Provisions for Loan Losses.”

According to Decree with Force of Law No. 3 of 1997, as amended, the Ley General de Bancos or the Chilean General Banking Act, a bank must have effective net equity (patrimonio efectivo) of at least 8% of its risk weighted assets, net of required allowance for loan losses, and paid in capital and reserves, or basic capital (capital básico), of at least 3% of its total assets, net of required allowance for loan losses.

For these purposes, the effective net equity of a bank is the sum of (1) the bank’s basic capital, (2) subordinated bonds issued by the bank valued at their issue price for an amount of up to 50% of its basic capital; provided that the value of the bonds shall decrease by 20% for each year that elapses during the period commencing six years prior to their maturity and (3) its voluntary allowances for loan losses, for an amount of up to 1.25% of its risk weighted assets to the extent voluntary allowances exceed those that banks are required to maintain by law or regulation; minus (4) certain deductions to be made in accordance with provisions of chapter 12-1 of the regulations of the SBIF (Recopilación Actualizada de Normas), or the Regulations of the SBIF.

Rounding and Other Matters

Certain figures included in this Annual Report and in our audited consolidated financial statements as of and for the year ended December 31, 2015 have been rounded for ease of presentation. Percentage figures included in this Annual Report have in all cases not been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this Annual Report may vary slightly from those obtained by performing the same calculations using the figures in our audited consolidated financial statements as of and for the year ended December 31, 2015. Certain other amounts that appear in this Annual Report may similarly not sum due to rounding.

Inflation figures relating to Chile are those reported by the Chilean National Statistics Institute (Instituto Nacional de Estadísticas) or INE, unless otherwise stated herein or required by the context. Inflation figures relating to Colombia are those reported by the Colombian National Administrative Department of Statistics (Departamento Administrativo Nacional de Estadística) or DANE, unless otherwise stated herein or required by the context. See “—Exchange Rate Information” below.

In this Annual Report, all macroeconomic data related to the Chilean economy is based on information published by the Central Bank of Chile and all macroeconomic data related to the Colombian economy is based on information published by the Central Bank of Colombia. All market share and other data related to the Chilean financial system is based on information published by the SBIF as well as other publicly available information and all market share and other data related to the Colombian financial system is based on information published by the Colombian Superintendency of Finance (Superintendencia Financiera de Colombia) as well as other publicly available information. The SBIF publishes the consolidated risk index (ratio of allowance for loans losses over total loans) of the Chilean financial system on a monthly basis. The Colombian Superintendency of Finance publishes every month the consolidated data required to calculate the risk index of the Colombian banking system (loan loss allowances and total loans).

EXCHANGE RATE INFORMATION

Exchange Rates

Chile has two currency markets, the Formal Exchange Market (Mercado Cambiario Formal) and the Informal Exchange Market (Mercado Cambiario Informal). The Formal Exchange Market is comprised of banks and other entities authorized by the Central Bank of Chile. The Informal Exchange Market is comprised of entities that are not expressly authorized to operate in the Formal Exchange Market, such as certain foreign exchange houses and travel agencies, among others. The Central Bank of Chile is empowered

2

Table of Contents

to require that certain purchases and sales of foreign currencies be carried out on the Formal Exchange Market. Both the Formal and Informal Exchange Markets are driven by free market forces. Current regulations require that the Central Bank of Chile be informed of certain transactions and that they be effected through the Formal Exchange Market.

The U.S. dollar observed exchange rate (dólar observado), or the Observed Exchange Rate, which is reported by the Central Bank of Chile and published daily in the Official Gazette (Diario Oficial) is the weighted average exchange rate of the previous business day’s transactions in the Formal Exchange Market. Nevertheless, the Central Bank of Chile may intervene by buying or selling foreign currency on the Formal Exchange Market to attempt to maintain the Observed Exchange Rate within a desired range. Even though the Central Bank of Chile is authorized to carry out its transactions at the Observed Exchange Rate, it often uses spot rates instead. Many other banks carry out foreign exchange transactions at spot rates as well.

The Informal Exchange Market reflects transactions carried out at an informal exchange rate. There are no limits imposed on the extent to which the rate of exchange in the Informal Exchange Market can fluctuate above or below the Observed Exchange Rate.

The Federal Reserve Bank of New York does not report a noon buying rate for Chilean pesos.

As of December 31, 2015, the U.S. dollar exchange rate used by us was Ch$710.32 per US$1.00 and the Colombian peso exchange rate used by us was Ch$3,135.17 per Cop$1.00.

The following table sets forth the annual low, high, average and period-end Observed Exchange Rate for U.S. dollars for the periods set forth below, as reported by the Central Bank of Chile.

| Daily Observed Exchange Rate (Ch$ per US$)(1) | ||||||||||||||||

| Low (2) | High (2) | Average(3) | Period-End (4) | |||||||||||||

| Year ended December 31, |

||||||||||||||||

| 2011 |

455.91 | 533.74 | 483.36 | 521.46 | ||||||||||||

| 2012 |

469.65 | 519.69 | 486.75 | 478.60 | ||||||||||||

| 2013 |

466.50 | 533.95 | 495.00 | 523.76 | ||||||||||||

| 2014 |

524.61 | 621.41 | 570.01 | 607.38 | ||||||||||||

| 2015 |

597.10 | 715.66 | 654.25 | 707.34 | ||||||||||||

| Quarterly period |

||||||||||||||||

| 2014 1st Quarter |

524.61 | 573.24 | 551.48 | 550.53 | ||||||||||||

| 2014 2nd Quarter |

544.96 | 566.88 | 554.35 | 550.60 | ||||||||||||

| 2014 3rd Quarter |

548.72 | 601.66 | 576.31 | 601.66 | ||||||||||||

| 2014 4th Quarter |

576.50 | 621.41 | 598.18 | 607.38 | ||||||||||||

| 2015 1st Quarter |

606.75 | 642.18 | 624.42 | 626.87 | ||||||||||||

| 2015 2nd Quarter |

597.10 | 637.80 | 617.76 | 634.58 | ||||||||||||

| 2015 3rd Quarter |

636.39 | 706.24 | 676.25 | 704.68 | ||||||||||||

| 2015 4th Quarter |

673.91 | 715.66 | 697.75 | 707.34 | ||||||||||||

| Month ended |

||||||||||||||||

| September 2015 |

676.74 | 705.92 | 691.73 | 704.68 | ||||||||||||

| October 2015 |

673.91 | 698.72 | 685.31 | 690.34 | ||||||||||||

| November 2015 |

688.94 | 715.66 | 704.00 | 712.63 | ||||||||||||

| December 2015 |

693.72 | 711.52 | 704.24 | 707.34 | ||||||||||||

| January 2016 |

710.16 | 730.31 | 721.95 | 711.72 | ||||||||||||

| February 2016 |

689.18 | 715.41 | 704.08 | 689.18 | ||||||||||||

| March 2016(5) |

678.22 | 694.82 | 685.12 | 678.22 | ||||||||||||

Source: Central Bank of Chile

| (1) | Nominal figures. |

| (2) | Exchange rates are the actual low and high, on a day-by-day basis for each period. |

| (3) | The average of the exchange rates on the last day of each month during the period. |

| (4) | Each annual period ends on December 31, and the respective period-end exchange rate is published by the Central Bank of Chile on the first business day following December 31. Each monthly period ends on the last calendar day of such month and the respective period-end exchange rate is published by the Central Bank of Chile on the first business day following the last calendar day of such month. |

| (5) | The information for March 2016 is as of March 11, 2016. |

3

Table of Contents

The following table sets forth the annual low, high, average and period-end exchange rate for U.S. dollars for the periods set forth below under our policy to calculate our own exchange rate:

| Bank’s Exchange Rate Ch$ per US$1 | ||||||||||||||||

| Low (2) | High (2) | Average (3) | Period-End | |||||||||||||

| Year ended December 31, |

||||||||||||||||

| 2011 |

455.87 | 535.03 | 483.49 | 519.08 | ||||||||||||

| 2012 |

469.68 | 518.65 | 486.68 | 479.16 | ||||||||||||

| 2013 |

466.48 | 533.95 | 495.31 | 526.41 | ||||||||||||

| 2014 |

605.46 | 621.56 | 612.85 | 605.46 | ||||||||||||

| 2015 |

593.49 | 714.82 | 654.55 | 710.32 | ||||||||||||

| Quarterly period |

||||||||||||||||

| 2014 1st Quarter |

526.84 | 573.21 | 551.91 | 550.62 | ||||||||||||

| 2014 2nd Quarter |

544.80 | 567.56 | 554.49 | 552.81 | ||||||||||||

| 2014 3rd Quarter |

548.93 | 601.25 | 577.15 | 597.66 | ||||||||||||

| 2014 4th Quarter |

575.31 | 621.56 | 598.21 | 605.46 | ||||||||||||

| 2015 1st Quarter |

612.33 | 642.07 | 624.73 | 623.96 | ||||||||||||

| 2015 2nd Quarter |

593.49 | 638.47 | 618.00 | 638.47 | ||||||||||||

| 2015 3rd Quarter |

635.36 | 704.89 | 676.91 | 696.86 | ||||||||||||

| 2015 4th Quarter |

674.31 | 714.82 | 697.72 | 710.32 | ||||||||||||

| Month ended |

||||||||||||||||

| September 2015 |

678.59 | 704.61 | 691.30 | 696.86 | ||||||||||||

| October 2015 |

674.31 | 695.13 | 684.65 | 691.27 | ||||||||||||

| November 2015 |

689.46 | 714.82 | 704.81 | 710.25 | ||||||||||||

| December 2015 |

690.95 | 712.46 | 703.99 | 710.32 | ||||||||||||

| January 2016 |

710.69 | 731.70 | 721.96 | 710.69 | ||||||||||||

| February 2016 |

691.26 | 713.84 | 703.27 | 694.77 | ||||||||||||

| March 2016(4) |

676.68 | 694.87 | 683.28 | 683.53 | ||||||||||||

Source: CorpBanca

| (1) | Nominal figures. |

| (2) | Exchange rates are the actual low and high, on a day-by-day basis for each period. |

| (3) | The average of the exchange rates on the last day of each month during the period. |

| (4) | The chart contains information up to March 11, 2016. |

Exchange Controls Considerations

Investments made in our common shares and our ADRs are subject to the following requirements:

| • | any foreign investor acquiring common shares to be deposited into an ADR facility who brought funds into Chile for that purpose must bring those funds through an entity participating in the Formal Exchange Market; |

| • | the entity participating in the Formal Exchange Market through which the funds are brought into Chile must report such investment to the Central Bank of Chile; |

| • | all remittances of funds from Chile to the foreign investor upon the sale of common shares underlying American Depositary Shares, or ADSs, or from dividends or other distributions made in connection therewith must be made through the Formal Exchange Market; and |

| • | all remittances of funds made to the foreign investor must be reported to the Central Bank of Chile. |

When funds are brought into Chile for a purpose other than to acquire common shares to convert them into ADSs and subsequently are used to acquire common shares to be deposited into the ADR facility, such investment must be reported to the Central Bank of Chile by the custodian within ten days following the end of each month within which the custodian is obligated to deliver periodic reports to the Central Bank of Chile.

All payments made within Chile in foreign currency in connection with ADSs through the Formal Exchange Market must be reported to the Central Bank of Chile by the entity participating in the transaction. In the event there are payments made outside of Chile, the foreign investor must provide the relevant information to the Central Bank of Chile directly or through an entity of the Formal Exchange Market within the first ten calendar days of the month following the date on which the payment was made.

4

Table of Contents

We cannot assure you that additional Chilean restrictions applicable to the holders of the ADSs, the disposition of shares underlying ADSs or the conversion or repatriation of the proceeds from such disposition will not be imposed in the future, nor can we assess the duration or impact of such restriction if imposed.

This summary does not purport to be complete and is qualified by reference to Chapter XIV of the Central Bank Foreign Exchange Regulations, a copy of which is available in the original Spanish version at the Central Bank of Chile’s website at www.bcentral.cl.

A. SELECTED FINANCIAL DATA

The following tables present our selected financial data as of the dates and for the periods indicated. You should read the following information together with our audited consolidated financial statements, including the notes thereto, included in this Annual Report and the information set forth in “Item 5. Operating and Financial Review and Prospects”.

| For the fiscal years ended December 31, | ||||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2015 (1) | |||||||||||||||||||

| Ch$ | Ch$ | Ch$ | Ch$ | Ch$ | US$ | |||||||||||||||||||

| (in million of Ch$, in thousand of US$)(2) | ||||||||||||||||||||||||

| Interest income |

528,622 | 762,992 | 1,007,106 | 1,320,124 | 1,299,480 | 1,829,429 | ||||||||||||||||||

| Interest expense |

(335,622 | ) | (506,116 | ) | (549,416 | ) | (689,240 | ) | (678,901 | ) | (955,768 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest income |

193,000 | 256,876 | 457,690 | 630,884 | 620,579 | 873,661 | ||||||||||||||||||

| Net service fee income |

60,362 | 85,644 | 117,977 | 161,590 | 152,847 | 215,181 | ||||||||||||||||||

| Trading and investment, foreign exchange gains and other operating income |

80,469 | 104,398 | 127,039 | 199,225 | 211,153 | 297,265 | ||||||||||||||||||

| Total operating expenses |

(152,706 | ) | (253,644 | ) | (362,145 | ) | (509,672 | ) | (480,789 | ) | (676,861 | ) | ||||||||||||

| Income attributable to investments in other companies |

250 | 367 | 1,241 | 1,799 | 1,300 | 1,830 | ||||||||||||||||||

| Provisions for loan losses |

(40,754 | ) | (51,575 | ) | (102,072 | ) | (127,272 | ) | (169,748 | ) | (238,974 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income before income taxes |

140,621 | 142,066 | 239,730 | 356,554 | 335,342 | 472,703 | ||||||||||||||||||

| Income taxes |

(23,303 | ) | (22,913 | ) | (64,491 | ) | (82,853 | ) | (96,677 | ) | (136,103 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income for the year |

117,318 | 119,153 | 175,239 | 273,701 | 238,665 | 335,999 | ||||||||||||||||||

| Net income per common share (3) |

0.51 | 0.43 | 0.48 | 0.69 | 0.64 | 0.00089 | ||||||||||||||||||

| Dividend per common share (4) |

0.52 | 0.49 | 0.176 | 0.260 | 0.332 | 0.00047 | ||||||||||||||||||

| Dividends per ADS (4) |

787 | 736 | 265 | 390 | 499 | 0.70 | ||||||||||||||||||

| Shares of common stock outstanding (in thousand) |

226,909,290.6 | 250,358,194.2 | 340,358,194.2 | 340,358,194.2 | 340,358,194.2 | |||||||||||||||||||

Source: CorpBanca

| (1) | Amounts stated in U.S. dollars as of December 31, 2015, and for the year ended December 31, 2015 have been translated from Chilean pesos at our exchange rate of Ch$ 710.32 per US$1.00 as of December 31, 2015. |

| (2) | Amounts stated in millions of Chilean pesos and thousands of U.S. dollars except for net income per share, dividends per common share and dividend per ADS expressed in Chilean pesos and in U.S. dollars. |

| (3) | Net income per common share has been calculated on the basis of net income attributable to the equity holders of the Bank divided by the weighted average number of shares outstanding for the period. For further information on basic earnings and diluted earnings please see Note 23 (d) to our financial statements. |

| (4) | Represents dividends paid in respect of net income earned in the prior fiscal year. |

5

Table of Contents

CONSOLIDATED STATEMENTS OF FINANCIAL

POSITION

| As of December 31, | ||||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2015 (1) | |||||||||||||||||||

| Ch$ | Ch$ | Ch$ | Ch$ | US$ | ||||||||||||||||||||

| (in million of Ch$, in thousand of US$) | ||||||||||||||||||||||||

| Cash and deposits in banks |

265,747 | 520,228 | 911,088 | 1,169,178 | 1,004,757 | 1,414,513 | ||||||||||||||||||

| Cash in the process of collection |

96,230 | 123,777 | 112,755 | 212,842 | 176,501 | 248,481 | ||||||||||||||||||

| Trading portfolio financial assets |

166,039 | 159,898 | 431,683 | 685,898 | 323,899 | 455,990 | ||||||||||||||||||

| Investments under agreements to resell |

23,251 | 21,313 | 201,665 | 78,079 | 24,674 | 34,736 | ||||||||||||||||||

| Derivative financial instruments |

248,982 | 268,027 | 376,280 | 766,799 | 1,008,915 | 1,420,367 | ||||||||||||||||||

| Loans and receivables from banks |

304,098 | 482,371 | 217,944 | 814,209 | 451,829 | 636,092 | ||||||||||||||||||

| Loans and receivables from customers |

6,711,945 | 9,993,890 | 12,771,642 | 13,892,270 | 14,454,357 | 20,349,078 | ||||||||||||||||||

| Financial investments available-for-sale |

843,250 | 1,112,435 | 889,087 | 1,156,896 | 1,924,788 | 2,709,748 | ||||||||||||||||||

| Held to maturity investments |

21,962 | 104,977 | 237,522 | 190,677 | 170,191 | 239,598 | ||||||||||||||||||

| Investment in other companies |

3,583 | 5,793 | 13,922 | 15,842 | 14,648 | 20,622 | ||||||||||||||||||

| Intangible assets |

12,239 | 489,306 | 841,370 | 757,777 | 665,264 | 936,569 | ||||||||||||||||||

| Property, plant equipment, net |

57,225 | 65,086 | 98,242 | 92,642 | 91,630 | 128,998 | ||||||||||||||||||

| Current income taxes |

6,278 | — | — | 20,834 | 46,904 | 66,032 | ||||||||||||||||||

| Deferred income taxes |

25,080 | 40,584 | 89,218 | 2,702 | 8,671 | 12,207 | ||||||||||||||||||

| Other assets |

102,775 | 149,903 | 293,118 | 415,267 | 438,323 | 617,077 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| TOTAL ASSETS |

8,888,684 | 13,537,588 | 17,485,536 | 20,271,912 | 20,805,351 | 29,290,109 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| As of December 31, | ||||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2015 (1) | |||||||||||||||||||

| Ch$ | Ch$ | Ch$ | Ch$ | Ch$ | US$ | |||||||||||||||||||

| (in million of Ch$, in thousand of US$) | ||||||||||||||||||||||||

| Current accounts and demand deposits |

682,720 | 1,112,675 | 3,451,383 | 3,954,948 | 4,431,619 | 6,238,905 | ||||||||||||||||||

| Transaction in the course of payment |

36,948 | 68,883 | 57,352 | 145,771 | 105,441 | 148,442 | ||||||||||||||||||

| Obligations under repurchase agreements |

130,549 | 257,721 | 342,445 | 661,663 | 260,631 | 366,921 | ||||||||||||||||||

| Time deposits and saving accounts |

4,824,378 | 7,682,675 | 7,337,703 | 8,076,966 | 8,495,603 | 11,960,247 | ||||||||||||||||||

| Derivative financial instruments |

166,872 | 193,844 | 281,583 | 607,683 | 731,114 | 1,029,274 | ||||||||||||||||||

| Borrowings from financial institutions |

663,626 | 969,521 | 1,273,840 | 1,431,923 | 1,528,585 | 2,151,967 | ||||||||||||||||||

| Debt issued |

1,522,773 | 1,886,604 | 2,414,557 | 3,079,050 | 3,227,554 | 4,543,803 | ||||||||||||||||||

| Other financial obligations |

20,053 | 18,120 | 16,807 | 15,422 | 14,475 | 20,378 | ||||||||||||||||||

| Current income tax provision |

— | 9,057 | 45,158 | 19,226 | 42,457 | 59,772 | ||||||||||||||||||

| Deferred income taxes |

25,352 | 120,714 | 182,373 | 76,593 | 40,433 | 56,922 | ||||||||||||||||||

| Provisions |

42,030 | 136,240 | 164,932 | 200,289 | 182,707 | 257,218 | ||||||||||||||||||

| Other liabilities |

30,981 | 79,868 | 185,506 | 210,716 | 209,439 | 294,852 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| TOTAL LIABILITIES |

8,146,282 | 12,535,922 | 15,753,639 | 18,480,250 | 19,270,058 | 27,128,700 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Equity Attributable to equity holders of the Bank | 739,793 | 947,296 | 1,426,199 | 1,465,725 | 1,220,552 | 1,718,312 | ||||||||||||||||||

| Non controlling interest |

2,609 | 54,370 | 305,698 | 325,937 | 314,741 | 443,097 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| TOTAL EQUITY |

742,402 | 1,001,666 | 1,731,897 | 1,791,662 | 1,535,293 | 2,161,409 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| TOTAL LIABILITIES AND EQUITY |

8,888,684 | 13,537,588 | 17,485,536 | 20,271,912 | 20,805,351 | 29,290,109 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1) | Amounts stated in U.S. dollars as of December 31, 2015, and for the year ended December 31, 2015 have been translated from Chilean pesos at our exchange rate of Ch$ 710.32 per US$1.00 as of December 31, 2015. |

6

Table of Contents

CONSOLIDATED RATIOS

| As of and for the year ended December 31, | ||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||||||||||||||||

| Profitability and Performance |

||||||||||||||||||||

| Net interest margin(1) |

2.7 | % | 2.3 | % | 3.4 | % | 3.8 | % | 3.6 | % | ||||||||||

| Return on average total assets (2) |

1.5 | % | 0.9 | % | 1.1 | % | 1.4 | % | 1.2 | % | ||||||||||

| Return on average equity (3) |

19.6 | % | 13.1 | % | 12.7 | % | 18.2 | % | 18.0 | % | ||||||||||

| Efficiency ratio (consolidated) (4) |

45.7 | % | 56.8 | % | 51.5 | % | 51.4 | % | 48.8 | % | ||||||||||

| Dividend payout ratio (5) |

100.0 | % | 100.0 | % | 50.0 | % | 57.0 | % | 51.6 | % | ||||||||||

| Capital |

||||||||||||||||||||

| Average equity as a percentage of average total assets |

7.5 | % | 7.2 | % | 8.9 | % | 7.7 | % | 6.4 | % | ||||||||||

| Equity as a percentage of total liabilities |

9.1 | % | 8.0 | % | 11.0 | % | 9.7 | % | 8.0 | % | ||||||||||

| Asset Quality |

||||||||||||||||||||

| Allowances for loan losses as a percentage of overdue loans (6) |

153.8 | % | 101.8 | % | 76.5 | % | 65.3 | % | 77.5 | % | ||||||||||

| Overdue loans as a percentage of total loans (6) |

1.0 | % | 1.1 | % | 1.3 | % | 1.5 | % | 1.5 | % | ||||||||||

| Allowances for loan losses as a percentage of total loans |

1.5 | % | 1.1 | % | 1.0 | % | 1.0 | % | 1.2 | % | ||||||||||

| Past due loans as a percentage of total loans (7) |

0.7 | % | 0.5 | % | 0.5 | % | 0.6 | % | 0.7 | % | ||||||||||

| Other Data |

||||||||||||||||||||

| Inflation rate |

||||||||||||||||||||

| Foreign exchange rate (Ch$/US$) |

11.0 | % | (7.7 | )% | 9.9 | % | 15.0 | % | 17.3 | % | ||||||||||

| Number of employees |

3,461 | 5,163 | 7,298 | 7,456 | 7,545 | |||||||||||||||

| Number of branches and offices |

116 | 209 | 295 | 298 | 304 | |||||||||||||||

| (1) | Net interest margin is defined as net interest income divided by average interest-earning assets. |

| (2) | Return on average total assets is defined as net income divided by average total assets. |

| (3) | Return on average equity is defined as net income divided by average shareholders’ equity. |

| (4) | Efficiency ratio (consolidated) is defined as total operating expenses as a percentage of operating income before loan losses. |

| (5) | Dividend payout ratio represents dividends divided by net income. |

| (6) | Overdue loans consist of all non-current loans (loans to customers). |

| (7) | Past due loans include all installments and lines of credit more than 90 overdue. |

| B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

| C. | REASONS FOR THE OFFER AND USE OF PROCEEDS |

Not applicable.

| D. | RISK FACTORS |

RISKS ASSOCIATED WITH OUR BUSINESS

The growth and composition of our loan portfolio may expose us to increased loan losses.

From December 31, 2012 to December 31, 2015, the compounded annual growth rate of our aggregate gross loan portfolio was 13.4%. Our business strategy is to grow profitably while increasing the size of our loan portfolio.

The consumer loans segment represents the single highest level of risk in our loan portfolio. As of December 31, 2015, the risk index (ratio of allowance for loans losses over total loans) of this segment was 1.5% – reflecting a 0.5% decrease in 2015 – while other segments of our loan portfolio such as mortgage loans and commercial loans had lower risk indexes of 0.4% and 1.3%, respectively.

During 2015, our portfolio of consumer loans was negatively impacted by the decline in consumer activity in the country. As of December 31, 2015, consumer loans represented 11.6% of our total loan portfolio compared to 12.2% as of December 31, 2014. While our loan portfolio grew by 4.3%, the composition of our loan portfolio as of December 31, 2015 reflected a greater increase in commercial loans, from Ch$10,090,574 million to Ch$10,696,518 million, this is a 6.0% increase when compared to our portfolio of consumer loans. Our mortgage loan portfolio has remained stable between Ch$2,229,558 million in 2014 and Ch$2,228,619 million in 2015, a 0.04% decrease.

Our consumer loan portfolio may experience loan losses due to the absence of collateral in respect of unsecured loans, insufficient collateral in collateralized loans, and risks relating to the circumstances of individual borrowers, including unemployment or incapacitation of our consumer borrowers.

We believe our total allowances for loan losses is adequate as of the date hereof to cover all known losses in our total loan portfolio. The growth of our loan portfolio (particularly in the lower-middle to middle income consumer segments) may expose us to a higher level of loan losses and require us to establish proportionately higher levels of provisions for loan losses, which would offset the increased income that we can expect to receive as our loan portfolio grows.

7

Table of Contents

Our loan portfolio may not continue to grow at the same or similar rate.

Past performance of our loan portfolio may not be indicative of future performance. Our loan portfolio may not continue to grow at the same or similar rates as the growth rate that we historically experienced, particularly in light of the growth in recent years attributable to the acquisitions of CorpBanca Colombia in May 2012 (the CorpBanca Colombia Aqcuisition) and Helm Bank in August 2013 (the Helm Bank Aqcuisition). Additionally, changes in the Chilean or Colombian economy, a slowdown in the growth of customer demand, an increase in market competition or changes in governmental regulations could also adversely affect the rate of growth of our loan portfolio and our risk index.

Our allowances for loan losses may not be adequate to cover the future actual losses to our loan portfolio.

As of December 31, 2015, our allowance for loan losses was Ch$173,939 (excluding allowances for loan losses on loans and receivable to banks) and the risk index was 1.2%. The amount of allowance for loan losses is based on our current assessment and expectations concerning various factors affecting the quality of our loan portfolio. These factors include, among others, our customers’ financial condition, repayment abilities and repayment intentions, the realizable value of any collateral, the prospects for support from any guarantor, Chilean and Colombian economies, government macroeconomic policies, interest rates and the legal and regulatory environment. Many of these factors are beyond our control. In addition, as these factors evolve, the models we use to determine the appropriate level of allowance for loan losses require recalibration, which may lead to increased provision for loan losses. If our assessment of and expectations concerning the above mentioned factors differ from actual developments, if the quality of our loan portfolio deteriorates or if the future actual losses exceed our estimates, our allowance for loan losses may not be adequate to cover actual losses and we may need to make additional allowances for loan losses, which may materially and adversely affect our results of operations and financial condition.

If we are unable to maintain the quality of our loan portfolio, our financial condition and results of operations may be materially and adversely affected.

As of December 31, 2015, our past due loans were Ch$104,897, which resulted in a past due loans to total loans ratio of 0.7%. As of December 31, 2015, our non-performing loans were Ch$196,806, which resulted in a non-performing to total loans ratio of 1.3%. We seek to continue to improve our credit risk management policies and procedures. However, we cannot assure you that our credit risk management policies, procedures and systems are free from any deficiency. Failure of credit risk management policies may result in an increase in the level of non-performing loans and adversely affect the quality of our loan portfolio. In addition, the quality of our loan portfolio may also deteriorate due to various other reasons, including factors beyond our control, such as the macroeconomic factors affecting the Chilean or Colombian economies. If such deterioration were to occur, it could materially and adversely affect our financial conditions and results of operations.

Additionally, due to limitations in the availability of information and the developing information infrastructure in Chile and Colombia, our assessment of the credit risks associated with a particular customer may not be based on complete, accurate or reliable information. In addition, although we have been improving our credit scoring systems to better assess borrowers’ credit risk profiles, we cannot assure you that our credit scoring systems collect complete or accurate information reflecting the actual behavior of customers or that their credit risk can be assessed correctly.

Furthermore, a substantial number of our customers consist of individuals and small-to-medium-sized enterprises, or SMEs. Our business results relating to our lower-income individual and SME customers are, however, more likely to be adversely affected by downturns in the Chilean and Colombian economies, including increases in unemployment, than our business from large corporations and high-income individuals. For example, unemployment directly affects the capacity of individuals to obtain and repay consumer loans. Consequently, this could materially and adversely affect the liquidity, business and financial condition of our customers, which may in turn cause us to experience higher levels of past due loans, and result in higher allowances for loan losses, which could in turn materially affect our asset quality, results of operations and financial conditions.

The value of any collateral securing our loans may not be sufficient, and we may be unable to realize the full value of the collateral securing our loan portfolio.

From time to time, we require our borrowers to collateralize their loans with guarantees, pledges of particular assets or other security. The value of any collateral securing our loan portfolio may significantly fluctuate or decline due to factors beyond our

8

Table of Contents

control. Such factors include market factors, environmental risks, natural disasters, macroeconomic factors and political events affecting the Chilean or Colombian economies. Any decline in the value of the collateral securing our loans may result in a reduction in the recovery from collateral realization and may have an adverse impact on our results of operations and financial condition.

In addition, the Bank may face difficulties in perfecting its liens and enforcing its rights as a secured creditor. In particular, timing delays and procedural problems in enforcing against collateral and local protectionism in the markets in which we operate may make foreclosures on collateral and enforcement of judgments difficult, and may result in losses that could materially and adversely affect the our results of operations and financial condition.

We may be unable to meet requirements relating to capital adequacy.

Chilean banks are required by the Chilean General Banking Act to maintain regulatory capital of at least 8% of risk-weighted assets, net of required allowance for loan losses and deductions, and basic capital of at least 3% of total assets, net of required allowance for loan losses. For the purposes of maintaining a high solvency classification from the SBIF and continued compliance with the SBIF’s capital requirements on us, our intention is to have the highest classification from the SBIF. As of December 31, 2015, the ratio of our Bank for International Settlements, or BIS, capital-weighted assets ratio was 9.5%. Nevertheless our capital ratios levels decreased from 12.4% to 9.5% between 2014 and 2015, following the approval of the merger with Banco Itaú Chile, considering that our shareholders, together with approving the merger, approved a special dividend distribution in the amount of Ch$239.86 billion that was paid on July 1, 2015.

Additionally, Colombian financial institutions are subject to capital adequacy requirements (as set forth in Decree 1771 of 2012, as amended) that are based on applicable Basel Committee standards. The regulations establish four categories of assets, which are each assigned different risk weights, and require that a credit institution’s Technical Capital (as defined below) be at least 9% of that institution’s total risk-weighted assets, and that its ordinary basic capital be at least 4.5% of that institution’s total risk-weighted assets. Technical Capital for the purposes of the Colombian regulations consists of the sum of Tier One Capital (ordinary basic capital) and Tier Two Capital (additional basic capital plus additional capital), collectively, Technical Capital. As of December 31, 2015, the consolidated ratio for our Colombian operations (calculated as BIS capital to risk-weighted assets) was 12.9%.

Certain developments could affect our ability to continue to satisfy the current capital adequacy requirements applicable to us, including:

| • | the increase of risk-weighted assets as a result of the expansion of our business; |

| • | the failure to increase our capital correspondingly; |

| • | losses resulting from a deterioration in our asset quality; |

| • | declines in the value of our available-for-sale investment portfolio; |

| • | goodwill and minority interest; |

| • | changes in accounting rules; and |

| • | changes in the guidelines regarding the calculation of the capital adequacy ratios of banks in the countries we operate. |

| • | fluctuations in exchange rates that could impact our loan portfolio, valuation adjustments due to the translation effects in equity or hedging strategies. |

As provided in article 68 of the Chilean General Banking Act, if we fail at any time to meet the legal requirements relating to the maintenance of regulatory capital (which is comprised of effective net worth and basic capital, as both concepts are defined in article 66 of the Chilean General Banking Act and Chapter 12-1 of the Regulations of the SBIF), we would have to comply with such legal requirements within a period of sixty days. For each day we fail to comply with such legal requirements, we would be subject to a daily penalty equal to one thousandth of the deficit of the effective net worth or basic capital, as the case may be.

If our Colombian operations fail to comply with the capital adequacy requirements applicable to Colombian financial institutions, we may be subject to certain penalties and sanctions that are graduated depending on the level of compliance failure, and which may include an administrative take-over by the government with the purpose of administration or liquidation. As a result, our business, results of operations and financial condition may be materially and adversely affected.

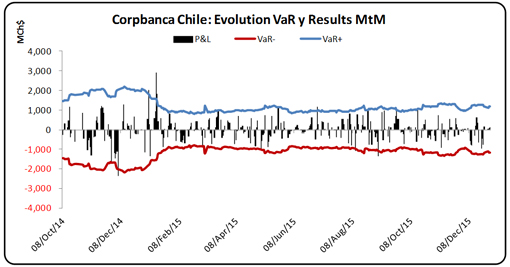

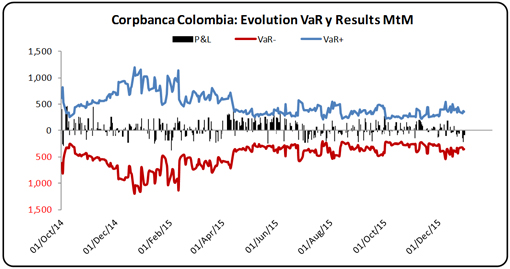

We are subject to market risk.

We are directly and indirectly affected by changes in local and international market conditions. Market risk, or the risk of losses in positions arising from movements in market prices, is inherent in the products and instruments associated with our operations, including loans, deposits, securities, bonds, long-term debt, short-term borrowings, proprietary trading in assets and liabilities and derivatives. Changes in market conditions that may affect our financial condition and results of operations include fluctuations in interest and currency exchange rates, securities prices, changes in the implied volatility of interest rates and foreign exchange rates, among others.

9

Table of Contents

Our results of operations are affected by interest rate volatility and inflation rate volatility.

Our results of operations depend to a great extent on our net interest income. In 2013, 2014 and 2015, our ratio of net interest income to total operating income was 65.1%, 63.6%, and 63.0% respectively. Changes in market interest rates in Chile or Colombia could affect the interest rates earned on our interest-earning assets differently from the interest rates paid on our interest-bearing liabilities leading to a reduction in our net interest income. Interest rates are highly sensitive to many factors beyond our control, including the monetary policies of the Central Bank of Chile and Colombia, changes in regulation of the financial sector in Chile and Colombia, domestic and international economic and political conditions and other factors. Yields on the Chilean government’s 90-day benchmark rate reached a high of 5.1% and a low of 4.8% in 2013, a high of 4.5% and a low of 3.7% in 2014, and a high of 3.1% and a low of 1.5% in 2015. On the other hand, the Colombian government does not issue short-term bonds of 30, 60 or 90 days as the Chilean government does. Instead, every month a committee of the Central Bank of Colombia determines the benchmark rate in order to achieve a specific goal of inflation. Yields on the Colombian benchmark rate reached a high of 4.0% and a low of 3.25% for 2013, a high of 4.5% and a low of 3.25% for 2014, and a high of 5.8% and a low of 4.5% for 2015. As of December 31, 2013, 2014, and 2015, we had Ch$889,087 million, Ch$1,156,896 million, and Ch$1,924,788 million, respectively, in financial investments available-for-sale. In the current global economic climate, there is a greater degree of uncertainty and unpredictability in the policy decisions and the setting of interest rates by the Central Bank of Chile and Central Bank of Colombia and, as a result, any volatility in interest rates could adversely affect us, including our future financial performance and the market value of our securities. In addition, inflation rate volatility could adversely affect our net interest income due to fluctuations in the gap between assets and liabilities that are indexed to the UF.

Increased competition and industry consolidation may adversely affect the results of our operations.

The Chilean and Colombian markets for financial services are highly competitive and competition is likely to increase.

In Chile, we face competition from banking and non-banking institutions with respect to the different products we offer. In the consumer and other loans businesses, we compete with other banks, credit unions and public social security funds (cajas de compensación). In some of our credit products, we face competition from department stores, large supermarket chains and leasing, factoring and automobile finance companies and in the saving products and mortgage loans businesses we compete with mutual funds, pension funds, insurance companies and with residential mortgage loan managers (Administradoras de Mutuos Hipotecarios). Furthermore, under the Chilean General Banking Act, representative offices of non-Chilean banks are now allowed to promote the credit products and services of their headquarters, which has increased, and may further increase, competition in our industry and, thus, have an adverse effect on our results of operation and financial condition.

In Colombia, we operate in a highly competitive environment and increased competitive conditions are to be expected in the jurisdictions where we operate. Intensified merger activity in the financial services industry produces larger, better capitalized and more geographically diverse firms that are capable of offering a wider array of financial products and services at more competitive prices. Our ability to maintain our competitive position in Colombia depends mainly on our ability to fulfill new customers’ needs through the development of new products and services and offer adequate services and strengthen our customer bases through cross-selling. Our Colombian operations will be adversely affected if we are not able to maintain efficient service strategies, or overcome certain delays or difficulties in the transition of the integration of the operational services and activities of CorpBanca Colombia and Helm Bank. In addition, our efforts to offer new services and products may not succeed if product or market opportunities develop more slowly than expected or if the profitability of opportunities is undermined by competitive pressures.

Our risk management system may not be sufficient to avoid losses that could have a material adverse effect on our business, financial condition and results of operations.

In addition to granting loans, part of our financial portfolio consists of trading transactions by our treasury division. Our financial success depends on, among other factors, our ability to accurately balance the risks we take and the returns we gain from our transactions. We use various processes to identify, analyze, manage and control our risk exposure, both in favorable and adverse market conditions. However, these processes involve subjective and complex judgments and assumptions, including projections of economic conditions and assumptions on the ability of our borrowers to repay their loans. Because of the nature of these risks, we cannot guarantee that our risk management efforts will prevent us from experiencing material losses. In particular, we may experience losses that could have a material adverse effect on our business, financial condition and results of operations if, among other factors:

| • | we are not capable of identifying all of the risks that may affect our portfolio; |

| • | our risk analysis or our measures taken in response to such risks are inadequate or inaccurate; |

| • | the markets move in an unexpected and adverse way with respect to speed, direction, strength or other aspects and our ability to manage risks in such a scenario is restricted; |

10

Table of Contents

| • | our clients are affected by unforeseen events resulting in their default or losses in an amount higher than those considered in our risk analyses; or |

| • | collateral pledged in our favor is insufficient to cover our clients’ obligations to us if they default. |

Our reliance on short-term deposits as our principal source of funds exposes us to sudden increases in our costs of funding which could have a material adverse effect on our revenues.

Time deposits and other term deposits are our primary sources of funding, which represented 44.1% of our liabilities as of December 31, 2015. If a substantial number of our depositors withdraw their demand deposits or do not roll over their time deposits upon maturity, our liquidity position, results of operations and financial condition may be materially and adversely affected. We cannot assure you that in the event of a sudden or unexpected shortage of funds, any money markets in which we operate will be able to maintain levels of funding without incurring higher funding costs or the liquidation of certain assets. If this were to happen, our business, results of operations and financial condition may be materially and adversely affected.

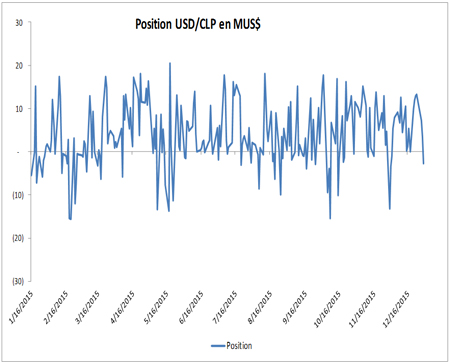

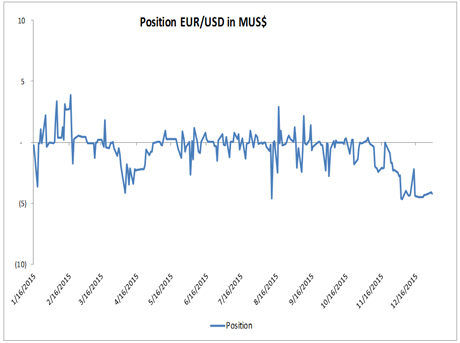

Currency fluctuations could adversely affect our financial condition and results of operations and the value of our securities.

Economic policies and any future changes in the value of the Chilean peso or the Colombian peso against the U.S. dollar could affect the dollar value of our securities, since the equity value of CorpBanca is hedged against our base currency Chilean peso. The Chilean peso and the Colombian peso have been subject to significant fluctuations in their value against the U.S. Dollar in the past and could be subject to similar fluctuations in the future. As of December 31, 2014, the Chilean peso depreciated against the U.S. dollar by 15.0% and the Colombian peso depreciated against the U.S. dollar by 24.3%, each as compared to December 31, 2013. As of December 31, 2015, the Chilean peso depreciated against the U.S. dollar by 17.3% and the Colombian peso depreciated against the U.S. dollar by 31.1%, each as compared to December 31, 2014.

Our results of operations may be affected by fluctuations in exchange rates between and among the Chilean peso, the Colombian peso and the U.S. dollar despite our internal policy and Chilean and Colombian regulations relating to the general avoidance of material exchange rate gaps. As of December 31, 2011, 2012, 2013, 2014 and 2015, the gap between foreign currency denominated assets and foreign currency denominated liabilities, excluding derivatives, was Ch$(23,560), Ch$241,832 million, Ch$434,942 million, Ch$(26,191) million and Ch$(497,644) million, respectively.

We may decide to change our policy regarding exchange rate gaps. Regulations that limit such gaps may also be amended or eliminated. Greater exchange rate gaps could increase our exposure to the devaluation of the Chilean peso and/or the Colombian peso, and any such devaluation may impair our capacity to service our foreign-currency obligations and may, therefore, materially and adversely affect our financial condition and results of operations.

Our business is highly dependent on proper functioning and improvement of information technology systems.

Our business is highly dependent on the ability of our information technology systems to accurately process a large number of transactions across numerous and diverse markets and products in a timely manner. The proper functioning of our financial control, risk management, accounting, customer service and other data processing systems is critical to our business and our ability to compete effectively. We have backup data for our key data processing systems that could be used in the event of a catastrophe or a failure of our primary systems, and have established alternative communication networks where available. However, we cannot assure you that our business activities would not be materially disrupted if there were a partial or complete failure of any of these primary information technology systems or communication networks. Such failures could be caused by, among other things, software bugs, computer virus attacks, cyber attacks or conversion errors due to system upgrading. In addition, any security breach caused by unauthorized access to information or systems, intentional malfunctions or loss or corruption of data, software, hardware or other computer equipment, could have a material adverse effect on our business, results of operations and financial condition.

Our ability to remain competitive and achieve further growth will depend in part on our ability to upgrade our information technology systems and increase our capacity on a timely and cost effective basis. Any substantial failure to improve or upgrade information technology systems effectively or on a timely basis could materially and adversely affect our business, financial condition and results of operations.

Our business in Colombia is dependent on a technology service agreement with Banco Santander, S.A.

Our business in Colombia is dependent on the service and support of a subsidiary of Banco Santander S.A., provided to us pursuant to a technology service agreement. This technology service agreement was extended and expires at the end of December

11

Table of Contents

2016 unless we exercise our option to extend its term through June 2017. If Banco Santander, S.A. is unable to service and support our business in Colombia or if we are unable to integrate our information technology systems into our business in Colombia after the expiration of the technology service agreement, then such failure could materially and adversely affect our business, financial condition and results of operations.

A worsening of labor relations in Chile or Colombia could impact our business.

As of December 31, 2015, on a consolidated basis we had 3,838 employees in Chile (including 27 at our New York Branch), of which 54.2% were unionized and 3,707 employees in Colombia, of which 20.2% were unionized. We are parties to collective bargaining agreements with unions representing our employees in Chile and Colombia. CorpBanca Colombia’s current labor agreement with eigthteen unions in Colombia was subscribed on August 26, 2015 and expires on August 31, 2017. We generally apply the relevant terms of our collective bargaining agreement to unionized and non-unionized employees in each of the markets in which we operate. We have traditionally enjoyed good relations with our employees and their unions. However, a strengthening of cross-industry labor movements may result in increased employee or labor costs that could materially and adversely affect our business, financial condition or results of operations.

On December 29, 2014, the Chilean government proposed a labor reform bill to the Chilean Congress, or the Labor Reform, which intends to substantially modify rules applicable to collective bargaining, including our unionized Chilean employees. The principal proposals included in this bill are to (1) prohibit employers, including us, from hiring replacement employees in the event of a worker strike affecting the business, and (2) ensure a minimum level of benefits. Additionally, the bill prohibits the workers from negotiating and entering into collective bargaining agreements directly with employers outside of established unions. Instead, workers will be required to organize collective bargaining efforts through established union. The bill is expected to be enacted as law during the first half of 2016, in which case it will become effective a year after its publication in the Official Gazette. If this bill becomes law, the effects of any strike or collective bargaining efforts by our employees in Chile could have a negative impact on our business, financial condition or results of operations.

We rely on third parties for important products and services

Third party vendors provide key components of our business infrastructure such as different loan servicing systems, internet connections and network access. Any problems caused by these third parties, including as a result of their not providing us their services for any reason or their performing their services poorly, could adversely affect our ability to deliver products and services to customers and otherwise to conduct business. Replacing these third party vendors could also entail significant delays and expense and could negatively impact our business.

We may experience operational problems, errors or fraud.

We are exposed to many types of operational risks, including the risk of fraud by employees and outsiders, failure to obtain proper authorizations, failure to properly document transactions, equipment failures and errors by employees. Although we maintain a system of operational controls, there can be no assurances that operational problems or errors will not occur and that their occurrence will not have a material adverse effect on our business, financial condition and results of operations.

Our anti-money laundering and anti-terrorist financing measures may not prevent third parties from using us as a conduit for those activities, which could have a material adverse effect on our business, financial condition and results of operations.

We are required to comply with applicable anti-money laundering and anti-terrorist financing laws and regulations and we have adopted various policies and procedures, including internal controls and “know-your customer” procedures, aimed at preventing money laundering and terrorist financing. In addition, because we also rely on our correspondent banks having their own appropriate anti-money laundering and anti-terrorist financing procedures, we use what we believe are commercially reasonable procedures for monitoring our correspondent banks. However, these measures, procedures and compliance may not be entirely effective in preventing third parties from using us (and our correspondent banks) as a conduit for money laundering (including illegal cash operations) or terrorist financing without our (and our correspondent banks’) knowledge or consent. If we were to be associated with money laundering (including illegal cash operations) or terrorist financing, our reputation could be harmed and we could become subject to fines, sanctions or legal enforcement (including being added to any “blacklists” that would prohibit certain parties from engaging in transactions with us), which could have a material adverse effect on our business, financial condition and results of operation.

Banking regulations may restrict our operations and thereby adversely affect our financial condition and results of operations.