| UNITED STATES SECURITIES AND EXCHANGE COMMISSION • WASHINGTON, D.C. 20549 | ||

FORM 10-K

| Annual Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 | or | Transition Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 | ||||||||||||||||||||||||

| For the fiscal year ended | For the transition period from to | |||||||||||||||||||||||||

Commission file number 001-32887

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||||||||

| , | , | ||||||||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||||||||

Registrant’s telephone number, including area code: (732 ) 528-2600

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. Check one:

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.) ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant at June 30, 2021 was $3,424,586,344 based on the closing price of $14.41 per share.

The number of shares outstanding of the registrant’s common stock as of January 31, 2022 was 254,055,494 .

Documents Incorporated By Reference

Portions of Part III will be incorporated by reference in accordance with Instruction G(3) to Form 10-K no later than 120 days after the end of the Company's fiscal year.

VONAGE HOLDINGS CORP.

FORM 10-K

FOR THE FISCAL YEAR ENDED December 31, 2021

TABLE OF CONTENTS

| Page | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

FORWARD-LOOKING STATEMENTS

VONAGE ANNUAL REPORT 2020

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements and other information which are deemed to be “forward-looking” within the meaning of the Private Securities Litigation Reform Act of 1995, or the Litigation Reform Act. These forward-looking statements and other information are based on our beliefs as well as assumptions made by us using information currently available.

The words "plan," “anticipate,” “believe,” “estimate,” “expect,” “intend,” “will,” “should” and similar expressions, as they relate to us, are intended to identify forward-looking statements. Such statements reflect our current views with respect to future events, are subject to certain risks, uncertainties, and assumptions, and are not a guarantee of future performance. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in such forward-looking statements or information. In light of the significant uncertainties in these forward-looking statements, you should not place undue reliance on these forward-looking statements. The forward-looking statements and information contained in this Annual Report on Form 10-K relate to events and state our beliefs and the assumptions made by us only as to the date of this Annual Report on Form 10-K. We do not intend to update these forward-looking statements, except as required by law.

In accordance with the provisions of the Litigation Reform Act, we are making investors aware that such forward-looking statements, because they relate to future events, are by their very nature subject to many important factors that could cause actual results to differ materially from those contemplated by the forward-looking statements contained in this Annual Report on Form 10-K, any exhibits to this Form 10-K and other public statements we make. Important factors that could cause such differences include, but are not limited to: the competition we face; the expansion of competition in the cloud communications market; incremental business, regulatory, and reputational risks related to the pending Ericsson merger; timing and satisfaction of the closing conditions related to the Ericsson merger; our ability to adapt to rapid changes in the cloud communications market; realizing the expected benefits of our business optimization or other cost-savings plans; risks related to the acquisition or integration of businesses we have acquired; our ability to scale our business and grow efficiently; the nascent state of the cloud communications for business market; our ability to retain customers and attract new customers cost-effectively; developing and maintaining effective distribution channels; risks associated with sales of our services to medium-sized and enterprise customers; the effects of COVID-19 on our business; our reliance on third-party hardware and software; our dependence on third-party vendors; reliance on third parties for our 911 services; the impact of fluctuations in economic conditions, particularly on our small and medium business customers; the effects of significant foreign currency fluctuations; developing and maintaining market awareness and a strong brand; retaining senior executives and other key employees; security breaches and other compromises of information security; system disruptions or flaws in our technology and systems; our ability to comply with data privacy and related regulatory matters; unfavorable litigation or governmental investigations; our ability to obtain or maintain relevant intellectual property licenses or to protect our trademarks and internally developed software; fraudulent use of our name or services; intellectual property and other litigation that have been and may be brought against us; rapid developments in global API regulation and uncertainties relating to regulation of VoIP services; liability under anti-corruption laws or from governmental export controls or economic sanctions; risks associated with the taxation of our business; governmental regulation and taxes in our international operations; our history of net losses and ability to achieve consistent profitability in the future; our ability to fully realize the benefits of our net operating loss carry-forwards if an ownership change occurs; actions of activist shareholders; restrictions in our debt agreements that may limit our operating flexibility; our ability to obtain additional financing if required; risks associated with the settlement and conditional conversion of our Convertible Senior Notes; potential effects the capped call transactions may have on our stock in connection with our Convertible Senior Notes; certain provisions of our charter documents; and other factors that are set forth in the “Risk Factors” section and other sections of this Annual Report on Form 10-K, as well as in our Quarterly Reports on Form 10-Q and amendments to these reports.

FINANCIAL INFORMATION PRESENTATION

For the financial information discussed in this Annual Report on Form 10-K, other than per share and per line amounts, dollar amounts are presented in thousands, except where noted.

1 VONAGE ANNUAL REPORT 2021

GLOSSARY OF TERMS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

| 2018 Credit Facility | $100 million senior secured term loan and $500 million revolving facility due 2023 | |||||||

| Convertible Senior Notes | $345 million aggregate principal amount of 1.75% convertible notes due 2024 | |||||||

| API | Application Program Interfaces | |||||||

| ASC | The FASB Accounting Standards Codification, which the FASB established as the source of authoritative GAAP | |||||||

| ASU | Accounting Standards Updates - updates to the ASC | |||||||

| CCaaS or CC | Contact Center as a Service | |||||||

| Code | Internal Revenue Code of 1986, as amended | |||||||

| CPaaS | Communications Platform as a Service | |||||||

| CRM | Customer Relationship Management | |||||||

| Exchange Act | The Securities Exchange Act of 1934, as amended | |||||||

| ECP | Electronic Check Payments | |||||||

| EPS | Earnings Per Share | |||||||

| FASB | Financial Accounting Standards Board | |||||||

| FCC | Federal Communications Commission | |||||||

| FCPA | Foreign Corrupt Practice Act | |||||||

| GDPR | European Union General Data Protection Regulation | |||||||

| IP | Internet Protocol | |||||||

| IRS | Internal Revenue Service | |||||||

| LIBOR | London Inter-Bank Offered Rate | |||||||

| MPLS | Multi-Protocol Label Switching | |||||||

| NOLs | Net Operating Losses | |||||||

| NVM | NewVoiceMedia Limited | |||||||

| QoS | Quality of Service | |||||||

| SaaS | Software as a Service | |||||||

| SAB | Staff Accounting Bulletins | |||||||

| SD-WAN | Software-Defined Wide Area Network | |||||||

| SEC | U.S. Securities and Exchange Commission | |||||||

| SIP | Session Initiation Protocol | |||||||

| SMB | Small to medium-sized business | |||||||

| SMS | Short Message Service | |||||||

| TokBox | Collectively, Telefonica Digital, Inc., TokBox, Inc., and TokBox Australia Pty Limited | |||||||

| TSR | Total Shareholder Return | |||||||

| UCaaS or UC | Unified Communications as a Service | |||||||

| UI | User Interface | |||||||

| USF | Federal Universal Service Fund | |||||||

| VBC | Vonage Business Communications | |||||||

| VCC | Vonage Contact Center | |||||||

| VCP | Vonage Communications Platform, formerly referred to as Business | |||||||

| VoIP | Voice over Internet Protocol | |||||||

2 VONAGE ANNUAL REPORT 2021

PART I

ITEM 1. Business

OVERVIEW AND STRATEGY

At Vonage, our vision is to accelerate the world's ability to connect. We are observing a secular change in the way business is done, with a fundamental shift in how communications technologies are being leveraged in almost every industry. Through the Vonage Communications Platform, our strategy is to deliver a single leading cloud communications platform that powers our customers' and partners' global engagement solutions using our APIs, Unified Communications, and Contact Center innovations. We believe that the Vonage Communications Platform's products and services are well positioned to take advantage of emerging trends with sizable, growing total addressable markets as companies look to cloud-based communications solutions and API programming architectures as part of their digital transformation.

For our Consumer customers, we enable users to access and utilize our services and features, via their existing internet connections, including over 3G/4G, LTE, Cable, or DSL broadband networks. This technology enables us to offer our Consumer customers attractively priced voice and messaging services and other features around the world on a variety of devices. Our Consumer strategy is focused on the continued penetration of our core North American markets, which provide value in international long distance and target under-served segments.

EVOLUTION OF VONAGE

Founded in 2001, Vonage was among the first companies to provide Voice over Internet Protocol technology offering feature-rich, low-cost home phone services. Through a series of strategic acquisitions and organic growth, Vonage since has transformed from a VoIP-based residential service provider to a global leader in business cloud communications.

Beginning in November 2013 and continuing through September 2015, Vonage acquired four unified communications-as-a-service companies which began its transformation into a buisness-to-business cloud communications company. In 2016 and 2018, Vonage expanded its offering into the API space with the completion of the acquisition of Nexmo, Inc., a global leader in communications platform as a service and TokBox Inc., an industry leader in WebRTC programmable video that enables developers and enterprises to integrate live video into existing websites, mobile apps and IoT devices with only a few lines of code.

Also in 2018, Vonage completed the acquisition of NewVoiceMedia, an industry-leading cloud contact center-as-a-service provider. This acquisition enabled Vonage to combine its robust Unified Communications and API solutions with NVM's pure-play cloud contact center offerings, culminating in our ability to provide an end-to-end communication experience for an organization's team members and customers.

In 2021, Vonage completed the acquisition of certain assets and liabilities of Jumper AI Ptd. Ltd., a leader in omnichannel conversational commerce solutions. The acquisition expanded Vonage's total addressable market and complemented its robust portfolio of APIs with a packaged AI-enabled conversational commerce offering.

On November 22, 2021, the Company, Telefonaktiebolaget LM Ericsson (publ) ("Ericsson") and Ericsson Muon Holding Inc. entered into an Agreement and Plan of Merger (the "Merger Agreement") providing for the acquisition of the Company by Ericsson for approximately $6.2 billion in cash. The proposed transaction received the required approval of the Company's stockholders on February 9, 2022 and is expected to be consummated during the first half of 2022 following the satisfaction of certain other customary conditions.

3 VONAGE ANNUAL REPORT 2021

OPERATING SEGMENTS

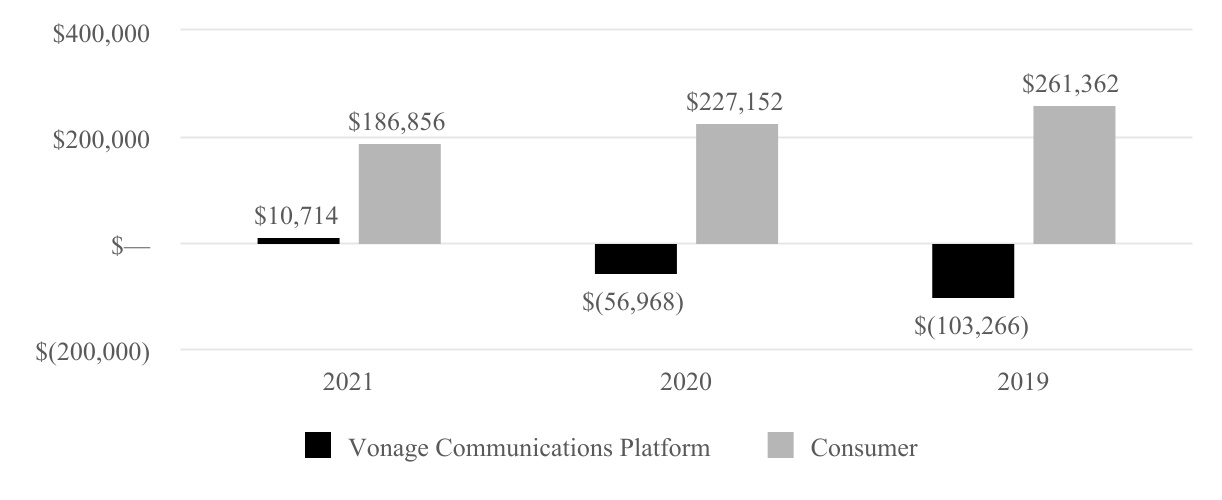

Our business is organized under two reportable operating segments: Vonage Communications Platform and Consumer. The Vonage Communications Platform includes our APIs, Unified Communications, Contact Center service offerings and products. The Vonage Communications Platform represents the Company’s strategic business as the source of future growth. Our Consumer segment includes our communications solutions for residential customers based on the Company's roots in providing VoIP communication services. Additional discussions of our reportable segments is included in Note 16, Industry Segment and Geographical Information to the Consolidated Financial Statements. The following tables summarize our revenues for each of our operating segments for the years ended December 31, 2021, 2020, and 2019:

Vonage Communications Platform

Our strategic business is the Vonage Communications Platform, which delivers a single leading cloud communications platform that powers our customers' and partners' global engagement solutions using our APIs, Unified Communications, and Contact Center innovations. The Vonage Communications Platform brings unique value to businesses by providing multiple communications channels - including video, voice, messaging, email, verification, and artificial intelligence - that integrate into the applications, products and workflows that our customers are already using. We believe this delivers both the power and the flexibility to our customers to address the growing need to transform their communications, connections and experiences for customers and enables the type of business continuity, remote work, and remote delivery of services that are now essential for team members.

The following provides a more detailed description of the products and services within the Vonage Communications Platform:

APIs

Our APIs are fully programmable, embeddable and customizable, enabling software developers to build communications capabilities such as messaging and voice calling within their applications without having to build or maintain communications infrastructure.

Our APIs aim to remove the complexities of the global communications networks and deliver video, voice, chat, messaging, verification, and artificial intelligence capabilities that developers can easily embed into their applications with a low risk, pay-as-you-go business model that fosters innovation. Developers adopt our APIs via a low friction, self service model on our website where they start with a free trial account and pay for additional usage via prepaid accounts. Customers include digital native companies that are looking to disrupt an existing industry, enterprises undergoing digital transformation, and enterprise SaaS companies looking to enhance their products with embedded communications capabilities.

The need for companies to jump between these modes of communication is being driven by today's customer. There is an increased need among businesses to provide their customers with the ability to connect and communicate on their customers' own preferred channels. In an increasingly digital world, this is what customers have come to expect. Our APIs enable businesses to implement these programmable capabilities quickly, with just a few lines of code, and without the need for in-house IT support or expertise.

4 VONAGE ANNUAL REPORT 2021

Our APIs include, but are not limited to, the following:

Communications APIs

•Voice API: Voice API enables companies to deliver better and more flexible voice experiences when communicating with their customers within the context of their existing business workflow, backed by the quality, strength and reliability of the Vonage network in the United States and tier one carriers globally.

•SIP Trunking: Session Initiation Protocol Trunking enables companies to rapidly connect their private branch exchanges to the global telecommunications networks using a pay as you go model and without having to negotiate lengthy carrier contracts.

•SMS API: SMS API enables companies to send and receive SMS messages within the context of their existing business workflows. The direct to carrier approach and patented Adaptive Routing algorithm enables us to deliver messages reliably and with low latency, globally.

•Messages API and Dispatch API: Together they enable brands to engage with their customers wherever they prefer, elevating customer communications by meeting customers on the channels they find most engaging.

•Video API: Programmable video enables developers, independent software vendors, and enterprises to incorporate highly scalable point-to-point and multi-party video into websites, mobile applications and IoT devices with only a few lines of code.

Authentication APIs

•Verify: Verify API enables companies to deploy two-factor-authentication for their applications to help them acquire genuine customers and to protect against fraud. With a single API call, Verify delivers messages via SMS and voice calls if required to ensure high conversion rates. In addition, customers pay only for successful authentications.

•Number Insight: Number Insight API enables companies to get real time intelligence on phone numbers anywhere in the world to ensure numbers are valid and reachable and to discover other insights such as carrier information, roaming status whether a landline or mobile, and caller name.

Use Case APIs and Programmable Numbers

•Audit API: Enables organizations to build security information and event management alerts, and access real-time information on user activities and events within accounts.

•Reports API: Reports API allows applications to access all voice and data in a single location.

•Virtual Phone Numbers: We offer phone numbers that are local all over the world enabling our customers to have a local presence globally. We also offer toll free numbers and short codes in the United States and Canada. Our numbers can be provisioned and de-provisioned programmatically to enable maximum utilization.

Our product offerings combined with the strength of our network, enables us to partner closely with customers to ensure that they are successful through a personalized account management experience, high quality support and consulting services. Our APIs products are supported through our close relationships with tier one carriers across the globe and offer local numbers in more countries along with its private MPLS network with numerous points of presence in the United States allowing us to offer high voice quality, lower costs and increased reliability. Our extensive network of more than one million developers provides customers with the ability to foster rapid innovations, including extensive developer documentation, sample codes, tutorials, libraries and free online support.

Unified Communications

Vonage Business Communications

Vonage Business Communications is our cloud-native, proprietary technology platform which delivers integrated unified communication services. It provides a cost-effective, highly scalable, feature-rich solution, delivered over-the-top of a customer’s broadband. All VBC features and functionality offerings include access to a mobile application, including the ability to update account profiles, manage devices, and contact call logs directly from a mobile device. We also offer virtual extensions, which connects employees to a business phone number through their mobile phones.

5 VONAGE ANNUAL REPORT 2021

VBC integrates with other third-party software applications to improve workflow and enhance productivity via the Vonage App Center ecosystem. Built on a microservices architecture, Vonage App Center creates embedded, UI-level integrations with high-value applications, placing critical functionality at the fingertips of VBC users within a single, familiar interface. Our software uses a combination of open APIs and pre-built integrations to enhance functionality with data from other third-party enterprise applications including Salesforce, Microsoft Dynamics, Microsoft Teams, NetSuite, Zendesk, Oracle Sales Cloud, Hubspot, and others. The investments we have made have enabled scalability to allow Vonage Business Communications to serve a broader customer base.

The launch of VBC was quickly followed by innovations to improve and build upon this service with new features and functionality that we believe transforms the way businesses connect, including:

•VBC Desktop Connect App, which allows employees to start their day in the redesigned Vonage Business Cloud Mobile App and switch to the desktop when they reach the office;

•VonageFlow, a proprietary workstream collaboration solution;

•Business Inbox, which allows customers to reply to messages sent in messaging apps like Facebook Messenger, providing the ability to respond to customers in real-time directly within the app, organizing customer requests in one unified inbox; and

•Vonage Meetings, a programmable video capability which is fully integrated with VBC and leverages Vonage APIs to enable voice, SMS, social, team messaging, and video all within a single interview for a simple, clean user experience.

Vonage Business Enterprise

Vonage Business Enterprise is a purpose-built cloud based platform for existing mid-market and enterprise customers, providing a complete set of enhanced unified communication and collaboration services, including: voice, data, video, mobile and contact center services. We focus on customers for whom guaranteed quality of service and uniformity of services across all locations is critical. We deliver services to this customer base over our private, nationwide, fully redundant, secure IP MPLS network using network points of presence that allow us to deliver dedicated, secure and private bandwidth utilizing all forms of last mile technologies including EoC and Fiber and bandwidth ranging from 1.5Mbps to 1Gbps. Services we deliver include Wide Area Networking, or WAN, Internet Access, MPLS VPN, Managed Firewall, Hosted UCaaS, Hosted Video Conferencing, Web Collaboration, Secure Instant Messaging & Presence, Mobility and Fixed Mobile Convergence.

Vonage Contact Center

Vonage Contact Center provides customers with a robust offering, driving intelligent interactions for customers and agents through emerging technologies such as skills-based routing, real-time sentiment analysis and chatbots. With VCC, we enhance the agent and customer experience by providing a modern contact center with seamless integration into productivity tools and business applications - all on a single, flexible, and unified platform. Our cloud contact center solution can be integrated with the VBC unified communications solution providing an end-to-end communications experience for enhanced customer engagement and conversation. By integrating with today’s leading business applications, productivity tools and CRMs such as Salesforce, ServiceNow, and Microsoft Dynamics, Vonage Contact Center solution delivers better omni-channel interactions and robust analytics, giving businesses the ability to customized agent, employee, and customer connections and workflows to deliver great customer experiences and enhanced productivity - from anywhere.

With the Vonage Contact Center solution, we believe that Vonage is the only cloud communication company that can combine deep CRM integrations with the full range of programmable communications capabilities to enhance the way agents connect with each other and with customers.

6 VONAGE ANNUAL REPORT 2021

Consumer

For our Consumer segment, we enable customers to access and utilize our services and features via their existing internet connections, including over 3G/4G, LTE, Cable, or DSL broadband networks. This technology enables us to offer our Consumer customers attractively priced voice and messaging services and other features around the world on a variety of devices. Our home telephone services are offered to customers through several service plans with different pricing structures. The service plans include basic features such as voicemail, call waiting, and call forwarding as well as unique features such as Simulring, Visual Voicemail, Boomerang and Extensions. We also charge for local and international calling outside of plan limits.

We have two primary Consumer offerings available in the United States: Vonage World and Vonage North America. Each of our Consumer calling plans provides a number of basic features including call waiting, caller ID with name, call forwarding, and voicemail. Vonage plans also include unlimited Vonage Visual Voicemail, which is “readable voicemail” delivered via email or SMS text message, Vonage Extensions, which extends the plan, and inbound calling, to additional phone numbers and devices, and selective call block, which allows users to block unwanted calls. We also offer, in some cases for additional fees, features such as area code selection, virtual phone numbers, and web-enabled voicemail. Additionally, we also provides similar product offerings to customers in both Canada and the United Kingdom.

NETWORK OPERATIONS

Our network uses our customer’s existing or Vonage procured high-speed broadband Internet service to allow calls over the Internet either from a standard telephone through a Vonage-enabled device or through soft phone software or mobile client applications. Our Unified Communications services are not dependent on any specific type or provider of Internet service, and our customers are free to change their Internet service provider in response to a competitive alternative, or because they have moved to a different location. For many of our Business Enterprise customers, our Unified Communications services are delivered over the Company's private, nationwide, fault tolerant, secure IP MPLS network under multi-year contracts to provide the high level of interconnection quality and the ability to offer service level agreements, or SLA, guaranteeing certain levels of voice service performance.

Our network is scalable and geographically distributed for robustness, high availability, and reliability across multiple call processing sites, using regional data interconnection points, where calls to non-Vonage customers are interconnected with the public switched telephone network. We periodically assess the locations of its regional data connection points in connection with efforts to improve the quality of and efficiency in delivering our service. Our interconnections with the public switched telephone network, or IP/SIP networks, are made pursuant to commercial agreements we have with several telecommunications providers. Under these agreements, we transfer calls originated by customers to other carriers who connect the call to the called party or connect peer to peer. We have a varying degree of settlement arrangements with our carrier partners for indirect third party or direct termination of calls. The calls are routed from our network to other carriers’ interconnected circuits at co-location facilities in which the Company leases space. This method of connecting to the public switched telephone or IP/SIP networks allows us to expand capacity quickly, as necessary to meet call volume, and to provide redundancy within the network.

Because Vonage’s system is standards based and not constrained to use any specific broadband service provider to connect to our customers, we can centrally manage and share resources across our customer base to minimize capital investment when entering new markets.

MARKETING

In connection with our transformation from a consumer telecommunications company to a business-focused SaaS provider, beginning in 2020 we introduced a rebranding of the Company and began a focused pivot to drive relevancy in our key business markets. Our marketing objective is to help drive growth, revenue, and relevancy across our business markets. Vonage employs an integrated multi-channel approach to marketing, whereby we evaluate and focus efforts on efficient marketing vehicles to accomplish its goals with the greatest return on investment. To do this, we make use of both broad-reaching and highly-targeted media channels.

For VCP customers, our primary source of lead acquisition is digital marketing in the form of search engine marketing, digital advertising, social media advertising, and affiliate programs. We also utilize database marketing and lead aggregators to source business leads and use direct marketing and account-based marketing to help source leads and create interest in our solutions. For Consumer customers, we have a highly optimized acquisition approach and focus mainly on digital advertising channels.

7 VONAGE ANNUAL REPORT 2021

We make use of marketing research to gain insights into brand, product, and service performance, and utilize those learnings to improve our messaging and media plans. Market research is also leveraged in the areas of testing, retention marketing, and product marketing to ensure we bring compelling products and services to market for our customers.

The Vonage brand is a meaningful factor for customers as they consider business services. We continue to invest in the equity of our brand in order to retain and expand our customer base and to position Vonage as a technology leader that delivers innovative, unified communication services and APIs to help businesses around the world accelerate digital transformation for a fundamentally new way of doing business.

SALES AND DISTRIBUTION

Enterprise Sales

In order to continue to expand in the enterprise sales channel, which we define as businesses larger than 1,000 seats, the enterprise sales organization is positioned to provide high quality business services for Enterprise, through our fully managed solution, which utilizes BroadSoft’s enterprise-grade call processing platform, with a broad portfolio of products delivered over its own private, national MPLS network, with numerous Points-of-Presence, or POPs, across the country and our own team of service delivery project managers using our proprietary provisioning tool Zeus, or with SmartWan, as well as our industry leading CPaaS products. Additionally, Contact Center solutions are commonly integrated into Enterprise solutions

Developer Ecosystem

Our API platform products are principally adopted and consumed by software developers all over the world. Given the nature of the business, we invest significant time and effort to build, recruit, and maintain developers and various software ecosystems. We have a large developer ecosystem worldwide with over one million registered developers.

Field Sales and Inside Sales - SMB and Midmarket

We utilize our team of sales agents (or field sales team), primarily based in geographic territories comprising customers and prospects to market and sell our business services. These field sales agents utilize a consistent, automated, highly-structured sales process to effectively educate prospective customers regarding our services. We have developed a scalable model applicable to both existing and new markets now have a field sales presence in 20 markets within the United States and made significant expansion into new markets globally primarily supporting Vonage APIs. For customers in the SMB segment, we leverage an Inside Sales team to provide solutions across our cloud communications offerings.

Channel Sales

In addition to the inside sales and field sales team, Vonage also has a dedicated team focused on channel sales who work with channel partners to market and sell business services, which helps to broaden sales distribution. Vonage continues to develop and expand this channel program by adding new a new Channel Chief, channel managers, and additional national master agents. Vonage now has a broad and deep coverage of the U.S. market through a network of over 20,000 sub agents and resellers.

Self-Service

Customers can subscribe to consumer services at Vonage websites, http://www.vonageforhome.com, http://www.vonageforhome.ca, http://www.vonageforhome.co.uk. U.S. VCP customers can subscribe to Unified Communications services at www.vonage.com, through our main toll-free number 1-844-365-9460, or through campaign-driven sales lines listed on our www.vonage.com web pages. Additionally, Vonage's API enablement and developer focus lends itself to a self-service model. Developers can register, sign up and test, and scale their businesses easily and quickly without having to engage with anyone at Vonage at www.vonage.com. This allows customers to self-provision their accounts with the aim of improving the customer experience while reducing customer acquisition costs.

INTELLECTUAL PROPERTY

Vonage currently owns over 250 issued U.S. patents as well as a number of foreign patents and pending U.S. and foreign patent applications. The Company routinely reviews technological developments with technology staff and business units to identify the aspects of Vonage technology that provide us with a technological or commercial advantage and seek intellectual property and patent protection as appropriate to protect such key proprietary technology in the United States and internationally, based on our assessment in light of applicable law. The Company's policies require our employees to assign intellectual property rights developed in the scope of or in relation to, company business and to treat proprietary know-how and materials as confidential information.

8 VONAGE ANNUAL REPORT 2021

Vonage has acquired multiple U.S. and foreign patents, and obtained licenses to numerous other patents. The Company owns numerous United States and international trademarks and service marks and have applied for registration of trademarks and service marks in the United States and abroad to establish and protect brand names as part of intellectual property strategy.

COMPETITION

In connection with its cloud communications products, Vonage faces competition from the traditional telephone and cable companies as discussed below, as well as from vendors of premises-based solutions or hosted solutions including the following:

•Independent cloud service providers;

•Premises-based business communication equipment providers;

•Hosted communication services providers;

•Traditional technology companies; and

•Emerging competitors in technology companies.

As the cloud communications market evolves, and the convergence of voice, video, messaging, mobility and data networking technologies accelerates, Vonage may face competition in the future from companies that do not currently compete in the market, including companies that currently compete in other sectors, companies that serve consumers rather than business customers, or companies which expand their market presence to include cloud communications.

Vonage faces strong competition from traditional telephone companies, cable companies, wireless companies, alternative communication providers, direct unified communications providers, legacy consumer VOIP businesses, large technology incumbents, and collaboration providers in the consumer, mobile, SMB and enterprise markets. Because most of the Company's target customers are already purchasing communications services from one or more of these providers, success is dependent upon our ability to attract these customers away from their existing providers. The principal competitive factors affecting our ability to attract and retain customers are price, call quality, brand awareness, customer service, network and system reliability, service features and capabilities, scalability, usability, simplicity, mobile integration and the unique ability to deliver APIs to business customers in addition to our Unified Communications and Contact Center Communications offerings.

There is a continuing trend toward consolidation of competitive companies, including the acquisition of alternative communication providers by Internet product and software companies with significant resources. In addition, certain of our competitors have partnered and may in the future partner with other competitors to offer products and services, leveraging their collective competitive positions. Vonage is also subject to the risk of future disruptive technologies, which could give rise to significant new competition.

HUMAN CAPITAL MANAGEMENT

Successful execution of our strategy is dependent on attracting, developing and retaining key employees and members of our management team. At Vonage, we believe our culture is our human capital competitive advantage that empowers us to win in the marketplace. We believe the substantial skills, experience, and industry knowledge of our employees. These beliefs are built on a core set of values: accountability, collaboration, trust, and excellence. Vonage leaders strive to foster an environment that empowers team members to drive results, delight customers, and inspire teams.

There are several ways in which we attract, develop, and retain highly qualified talent, including:

•Strategic Approach to Work-Life Balance, Diversity, and Inclusion. As part of our strategic plan, we have implemented flexible remote working and parental leave for all employees, have mandatory unconscious bias and culture training for all employees, implement company-sponsored networking events for female employees, and have milestones in place to achieve gender pay parity. Objectives and key results for our senior executives also include metrics on diversity, pay equity, voluntary terminations, and internal mobility. We have also established a Diversity, Equity, and Inclusion Committee that is focused on promoting race, gender, and ethnic diversity throughout the organization.

•Investments in Employee Training and Development. In order to foster internal promotion and development, we continue to implement accelerated leadership development and emerging leadership programs to a diverse set of employees throughout the organization. We also continue to implement development and training programs for all employees including product and sales, Code of Conduct, conflicts of interest, information security and cybersecurity, anti-harassment and anti-bribery, and insider trading prohibitions.

9 VONAGE ANNUAL REPORT 2021

EMPLOYEES

As of December 31, 2021, we had 2,082 employees, none of which are subject to a collective bargaining agreement.

AVAILABLE INFORMATION

Vonage was incorporated in Delaware in May 2000 and changed our name to Vonage Holdings Corp. in February 2001. Vonage maintains a website with the address www.vonage.com. References to our website are provided as a convenience, and the information contained on our website is not included as a part of, or incorporated by reference into, this Annual Report on Form 10-K. Other than an investor’s own Internet access charges, we make available free of charge through our website our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports, as soon as reasonably practicable after we have electronically filed such material with, or furnished such material to, the U.S. Securities and Exchange Commission, or SEC. Copies are also available, without charge, by writing to Vonage’s Investor Relations Department at Vonage Holdings Corp., 23 Main Street, Holmdel, NJ 07733 or calling us at 732.365.1328 or sending an email through the Vonage Investor Relations website at http://ir.vonage.com/. Reports filed with the SEC may be viewed at www.sec.gov or obtained at the SEC Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

10 VONAGE ANNUAL REPORT 2021

ITEM 1A. Risk Factors

You should carefully consider the risks below, as well as all of the other information contained in this Annual Report on Form 10-K and our financial statements and the related notes included elsewhere in this Annual Report on Form 10-K, in evaluating our company and our business. Any of these risks could materially adversely affect our business, financial condition and results of operations and the trading price of our common stock.

Risks Relating to our Business Operations, Strategic Planning and Product Development

If we are unable to compete successfully, we could lose market share and revenue.

The business cloud communications markets and consumer services markets in which we participate are highly competitive. We face intense competition from a broad set of companies, including: software as a service companies, contact center as a service companies, other alternative communication providers, and other providers of cloud communications services; and traditional telephone, wireless service providers, cable companies and alternative communications providers with consumer offerings

Many of these providers are substantially larger and better capitalized than us and have the advantage of greater name and brand name recognition, and have a large existing customer base. These service providers may have the ability to devote greater resources to their communications services and may be able to respond more quickly and effectively than we can to new or changing opportunities. Our competitors' financial resources may allow them to offer services at prices below cost or even for free in order to maintain and gain market share or otherwise improve their competitive positions. Some of our competitors also could use their greater financial resources to develop and market services with more attractive features and more robust customer service. To the extent that these or other companies strengthen their offerings, we may have to reduce our prices, increase promotions, or offer additional features, which may adversely impact our revenues and profitability.

As the cloud communications services market evolves, and the convergence of voice, video, messaging, mobility, artificial intelligence and data networking technologies accelerates, we may face competition in the future from companies that do not currently compete in the cloud communications services market.

As the cloud communications services market evolves, combining voice, video, messaging, mobility, artificial intelligence and data networks, and information technology and communication applications, opportunity is created for new competitors to enter the cloud communications services market and offer competing products, including companies that currently compete in other sectors, companies that serve consumer rather than business customers, or companies which expand their market presence to include business communications. This new competition may take many forms, and may offer products and applications similar to ours. If these new competitors emerge, the cloud communications services market may become increasingly competitive and we may not be able to maintain or improve our market position. Our failure to do so could materially and adversely affect our business and results of operations.

Our pending merger with Telefonaktiebolaget LM Ericsson (publ) (“Ericsson”) creates incremental business, regulatory and reputational risks and failure to close the merger could negatively impact the share price and the future business and financial results of the Company.

On November 22, 2021, the Company entered into an Agreement and Plan of Merger (the "Merger Agreement") with Ericsson and Ericsson Muon Holding Inc.. The proposed transaction with Ericsson entails important risks, including, among others: the occurrence of any event, change or other circumstances that could give rise to the termination of the Merger Agreement; the inability to complete the proposed merger due to the failure to satisfy conditions to completion of the proposed merger, including obtaining the requisite Committee on Foreign Investment in the U.S. clearance; risks related to disruption of management’s attention from the Company’s ongoing business operations due to the proposed merger; the risk that we will not be able to attract, retain, and motivate qualified personnel; the effect of the announcement of the proposed merger on the Company’s relationships with its customers, operating results and business generally; the risk that litigation associated with the proposed merger affects the merger or the business otherwise; and the risk that the proposed merger will not be consummated in a timely manner.

11 VONAGE ANNUAL REPORT 2021

If we fail to adapt to rapid changes in the market for cloud communications services, then our products and services could become obsolete.

The market for our products and services is constantly and rapidly evolving as we and our competitors introduce new and enhanced products and services and react to changes in the cloud communications services industry and customer demands. We may not be able to develop or acquire new products and plans or product and plan enhancements that compete effectively with present or emerging cloud communications services technologies or differentiate our products and plans based on functionality and performance. In addition, we may not be able to establish or maintain strategic alliances that will permit enhancement opportunities or innovative distribution methods for our products and plans.

To address these issues, we are targeting revenue growth in large, existing markets, which require us to enhance our current products and plans, and develop new products and plans on a timely basis to keep pace with market needs and satisfy the increasingly sophisticated requirements of customers. If we are unable to attract users of these services our net revenues may fail to grow as we expect.

Cloud communications services are complex, and new products and plans and enhancements to existing products and plans can require long development and testing periods. Any delays in developing and releasing new or enhanced products and plans could cause us to lose revenue opportunities and customers. Any technical flaws in products we release could diminish the innovative impact of the products and have a negative effect on customer adoption and our reputation.

We also are subject to the risk of future disruptive technologies. New products based on new technologies or new industry standards could render our existing products obsolete and unmarketable. If new technologies develop that are able to deliver competing voice and messaging services at lower prices, better or more conveniently, it could have a material adverse effect on us.

The market for our API products and platform is relatively nascent and may not experience the growth that we anticipate.

The utilization of APIs to embed contextual, programmable real time communications into mobile apps, websites and business systems workflows, remains a relatively new market, and developers and organizations may not yet recognize the need for, or benefits of, our products and platform. It is important that we are able to educate developers, organizational leaders, and other potential customers regarding our products and platform in order to help grow the market and to realize our market share. If we fail to achieve the foregoing, the market for our products and platform or our share of that market could fail to grow significantly. If the API market, or our share of that market, does not experience significant growth, then our business, results of operations and financial condition could be adversely affected.

We may not fully realize the expected benefits of our business optimization plans or other cost-saving initiatives, which may negatively impact our results of operations and financial condition.

Since the third quarter of 2020, the Company has been implementing a business optimization and alignment project to focus the use of Company resources and drive operational execution. The Company may pursue similar cost-saving initiatives in the future. We may not achieve the operational improvements and efficiencies that we have targeted in this project.

Implementing any restructuring, optimization, or cost-savings plan presents significant potential risks that may impair our ability to achieve anticipated operating improvements and/or cost reductions. These risks include (but are not limited to) higher than anticipated costs in implementing these plans, management distraction from ongoing business activities, failure to maintain adequate controls and procedures while executing these plans, damage to our reputation, brand image, and workforce attrition beyond our planned reductions, and our ability to provide optimal service to our customers. Any of these risks could have a negative impact on our profitability and on our results of operations and financial condition.

We may face difficulties related to the acquisition or integration of businesses, which could harm our growth or operating results.

In August 2018, we acquired TokBox with the intention of integrating and adding video to our VCP offerings in voice, SMS, and IP messaging. In October 2018, we completed the acquisition of NewVoiceMedia as a contact center provider, with the intention of combining our UC, CC and API solutions to provide an end-to-end communications experience for a company's employees and customers. In August 2019, we acquired intellectual property assets from Over.ai in order to integrate conversational artificial intelligence into our VCP product offerings. In October 2021, we acquired Jumper.ai to integrate omnichannel conversational commerce solutions into our VCP product offerings. In addition, we have made several acquisitions over the past several years to build our business services and continue to periodically review acquisition opportunities.

12 VONAGE ANNUAL REPORT 2021

Acquisition and integration activities require substantial management time and resources. Acquisitions of existing businesses involve substantial risks, including the risk that we may not be able to integrate the operations, personnel, services, or technologies, the potential disruption of our ongoing businesses, the diversion of management attention, the maximization of financial and strategic opportunities, the difficulty in developing or maintaining controls and procedures, and the dilution to our existing stockholders from the issuance of additional shares of common stock. We may elect to acquire additional businesses or assets in the future. However, we cannot predict or guarantee that we will be able to identify suitable acquisition candidates or consummate any acquisition. As a result of these and other risks, we may not produce anticipated revenue, profitability, or synergies.

Acquisitions may require us to issue debt or equity securities, use our cash resources, incur debt or contingent liabilities, amortize intangibles, or write-off acquisition-related expenses. If we are unable to successfully integrate any acquired businesses or assets we may not receive the intended benefits of such acquisition. In addition, we cannot predict market reactions to any acquisitions we may make or to any failure to announce any future acquisitions.

Further, there may be risks or liabilities that such due diligence efforts fail to discover, are not disclosed to us, or that we inadequately assess. The discovery of material liabilities associated with acquisitions or joint venture opportunities, economic risks faced by joint venture partners, or any failure of joint venture partners to perform their obligations could adversely affect our business, results of operations, and financial condition.

Our Vonage Communications Platform segment is growing rapidly, and any inability to scale our business and grow efficiently could materially and adversely harm our business and results of operations.

As our VCP segment expands, we will need to continue to improve our application architecture, integrate our products and applications across our technology platforms, integrate with third-party systems, and maintain infrastructure performance. We expect the number of users, the amount of data transferred and processed, the number of locations where our service is being used, and the volume of communications over our networks to continue to expand. To address this growth, we will need to scale our systems and customer services organization. Our ability to execute on these initiatives may impact system and network performance, customer satisfaction, and ultimately, sales and revenue. These efforts may also divert management resources. These factors may materially and adversely harm our business and results of operations.

Risks Relating to Customer Attraction and Sales

If we are unsuccessful at retaining customers or attracting new customers, we may experience a reduction in revenue or may be required to spend more money or alter our marketing approaches to grow our customer base.

Our rate of customer terminations for our UC and CC services could increase in the future if customers are not satisfied with the quality and reliability of our network, the value proposition of our products, and the ability of our customer service to meet the needs and expectations of our customers. For our API customers, our ability to grow revenue depends, in part, on our ability to maintain and grow usage of our platform by new and existing customers. If we are not able to increase customer usage of our products, our revenue may decline which would adversely impact our business, results of operations and financial condition. Our API customers are charged based on their usage of our products and generally our customers do not have long-term contractual financial commitments to us, therefore, usage rates may fluctuate at any time. In addition, our agreements with business customers typically provide for service level commitments. If we are unable to meet these commitments or if we suffer extended periods of downtime for our products or platform, our business, results of operations and financial condition could be adversely affected. Our ability to attract and retain customers for our consumer services are impacted by our pricing, brand awareness, customer service, network and system reliability and service features and capabilities. A material decline in the usage of our business and consumer products could cause us to spend significantly more on sales and marketing than we currently budget in order to maintain or increase revenue from customers, which could adversely affect our business, results of operations and financial condition.

Our success in the cloud communications market for our business services depends in part on developing and maintaining effective distribution channels. The failure to develop and maintain these channels could materially and adversely affect our business.

A portion of our business revenue is generated through our direct sales, or “field sales,” team. This channel consists of sales agents that market and sell our business services products to customers to customers through direct, commonly face-to-face interaction. Our continued success requires that we continue developing and maintaining a successful sales organization. If we fail to do so, or if our sales agents are not successful in their sales efforts, our sales may decrease and our operating results would suffer.

13 VONAGE ANNUAL REPORT 2021

A portion of our business revenue is generated through indirect channel sales. These channels consist of third-party resellers and value-added distributors that market and sell our business services products to customers. These channels may generate an increasing portion of our business revenue in the future. Generally, we do not have long-term contracts with these third-party resellers and value-added distributors, and the loss of or reduction in sales through these third parties could materially reduce our revenues. We also compete for preference amongst our current or potential resellers with our competitors. Our continued success requires that we continue developing and maintaining successful relationships with these third-party resellers and value-added distributors. If we fail to do so, or if our resellers are not successful in their sales efforts, our sales may decrease and our operating results would suffer.

Sales of our UC and CC business services to medium-sized and enterprise customers involve significant risks which, if not managed effectively, could materially and adversely affect our business and results of operations.

As we continue to expand our sales efforts to medium-sized and larger businesses, we may incur higher selling expense and longer, more complex, sales cycles. Customers in this market segment may also require bespoke features and integration services, increasing the complexity and expense related to the sales and delivery process, and requiring highly skilled sales and support personnel. As a result, we may devote greater sales and support to these customers, which may result in increased costs and a strain on our support resources. In addition, the rollout of our products with medium-sized and enterprise customers can take longer periods of time compared to smaller customers, which can result in longer lead times in realizing revenues. These factors could materially and adversely affect our results of operations and our overall ability to grow our customer base.

Risks Relating to External Factors and Third Parties

The recent coronavirus (COVID-19) pandemic and the global attempt to contain it has impacted and may continue to impact our business and results of operations.

The global spread of the novel coronavirus (COVID-19) and the various measures to contain its effects have created significant volatility, uncertainty, and economic disruption worldwide. COVID-19 has impacted some of our customers more than others, including customers in the travel, hospitality, retail, and other industries where physical interaction is critical. We have experienced and expect that we will continue to experience slowdowns in bookings and customer payments; increased customer churn and reduced usage; and issuance of customer credits to distressed customers served by certain product lines, including SMS API, Vonage Business Cloud, and Vonage Business Enterprise. Moreover, as businesses and educational institutions have pivoted to cloud-based communications in light of social distancing, we are experiencing and expect to experience intense competition from our existing competitors, and also emerging competitors seeking to capitalize on the growing industry.

In addition to COVID-19, our operations, and the operations of our vendors and customers, may also suffer interruptions caused by other pandemic diseases, natural disasters, acts of terrorism, acts of war, military conflict (including escalating military tension between Russia and Ukraine), economic sanctions, and such operations may be further affected by government reactions due to such incidents. Such uncertainties could have a material adverse effect on the continuity of our business and our results of operations and financial condition.

Our ability to provide our telephony service and manage related customer accounts is dependent upon third-party facilities, equipment, and systems, the failure of which could cause delays of or interruptions to our service, damage our reputation, cause us to lose customers, limit our growth, and affect our financial condition.

Our success depends on our ability to provide quality and reliable telephony service, which is in part dependent upon the proper functioning of facilities and equipment owned and operated by third parties and is, therefore, beyond our control. Unlike traditional wireline telephone service or wireless service, our telephony service typically requires our customers to have an operative broadband Internet connection and an electrical power supply, which are provided by the customer's Internet service provider and electric utility company, respectively, and not by us. The quality of some broadband Internet connections may be too poor for customers to use our telephony services properly. In addition, if there is any interruption to a customer's broadband Internet service or electrical power supply, that customer will be unable to make or receive calls, including emergency calls, using our telephony service.

We outsource several of our network functions to third-party providers. For example, we outsource the maintenance of our regional data connection points, which are the facilities at which our network interconnects with the public switched telephone network. If our third-party service providers fail to maintain these facilities properly, or fail to respond quickly to problems, our customers may experience service interruptions. Interruptions in our service caused by third-party facilities have in the past caused and may in the future cause us to lose customers or cause us to offer substantial customer credits, which could adversely affect our revenue and profitability. If interruptions adversely affect the perceived reliability of our service, we may have difficulty attracting new customers, and our brand, reputation, and growth will be negatively impacted.

14 VONAGE ANNUAL REPORT 2021

There can be no guarantee that these third party providers will be able or willing to supply services to us in the future on commercially reasonable terms, or that we will be able to engage alternative or additional providers. Our ability to provide our services may be impacted during any transition, which could have an adverse effect on our business, financial condition or results of operations.

We rely on third-party vendors that may be difficult to replace or may not perform adequately.

It is vital to our customers that there be a minimum of disruption to the performance of our API, UC and CC services. We are therefore vulnerable to service interruptions of our third-party data center providers, such as IBM Softlayer and Amazon Web Services, or AWS; and of third-party hosted services. We also rely on third-party vendors that support our internal operations, including Genpact, which provides certain accounting transaction-processing activities. We may experience interruptions, delays and outages in third-party service and availability due to a variety of factors, including infrastructure changes, human or software errors, website hosting disruptions and capacity constraints caused by technical failures, natural disasters, fraud or security attacks. To the extent that we do not effectively address interruptions, delays and outages in our data center providers’ and other hosted providers’ service and availability or capacity constraints, our business, results of operations and financial condition may be adversely affected.

In some cases we rely on purchased or leased hardware and software licensed from third parties in order to provide our services. For example, Broadsoft, Inc. provides us with infrastructure, call termination and origination services, and other hardware and software in connection with certain of our Enterprise offerings. We also integrate third-party licensed software components into our platform. This hardware and software may not continue to be available on commercially reasonable terms or pricing or may fail to continue to be updated to remain competitive. The loss of the right to use this third party hardware or software may increase our expenses or impact the provisioning of our services. The failure of this third party hardware or software could materially impact the performance of our services and may cause material harm to our business or results of operations.

We depend on third-party vendors to supply, configure and deliver the phones that we sell. Any delays in delivery, or failure to operate effectively with our own servers and systems, may result in delay or failure of our services, which could harm our business, financial condition and results of operations.

We rely on Yealink Inc. and Polycom, Inc. to provide, and a single fulfillment agent to configure and deliver, the phones that we offer for sale to our customers that use our UC and CC services. If these third parties are unable to deliver phones of acceptable quality or quantity, or in a timely manner, we may be forced to offer replacements at a higher cost than what is currently contracted. In addition, these phones must interoperate with our servers and systems. If either of our providers changes the operation of their phones, we may be required to engage in development efforts to ensure that the new phones interoperate with our system. The failure of our vendor-supplied phones to operate effectively with our system could impact our customers’ ability to use our services and could cause customers to cancel our services, which may cause material harm to our business or results of operations.

We rely on third parties to provide a portion of our customer service representatives, provide aspects of our E-911 service, which differs from traditional 911 service, and initiate local number portability for our customers. If these third parties do not provide our customers with reliable, high-quality service, our reputation will be harmed and we may lose customers.

We offer our customers support 24 hours a day, seven days a week through both our comprehensive online account management website and our toll free number. Our customer support is currently provided via United States based employees as well as third party partners located in various global locations. Our third-party providers generally represent us without identifying themselves as independent parties. The ability to support our customers may be disrupted by natural disasters, inclement weather conditions, civil unrest, and other adverse events in the locations where our customer support is provided.

We also contract for services required to provide E-911 services including assistance in routing emergency calls, terminating E-911 calls, operating a national call center that is available 24 hours a day, seven days a week to receive certain emergency calls, and maintaining PSAP databases for the purpose of deploying and operating E-911 services. Interruptions in service from our vendor could cause failures in our customers’ access to E-911 services and expose us to liability and damage our reputation. We also have agreements with companies that initiate our local number portability, which allow new customers to retain their existing telephone numbers when subscribing to our services.

If any of these third parties do not provide reliable, high-quality service, our reputation and our business will be harmed. In addition, industry consolidation among providers of services to us may impact our ability to obtain these services or increase our expense for these services.

15 VONAGE ANNUAL REPORT 2021

We market our products and services to small and medium-sized businesses, which may be disproportionately impacted by fluctuations in economic conditions.

We market our products to small and medium-sized businesses. Customers in this market may be affected by economic downturns to a greater extent, and may have more limited financial resources, than larger or more established businesses. If customers in our VCP markets experience financial hardship as a result of a weak economy, the demand for our services could be materially and adversely affected.

Significant foreign currency exchange rate fluctuations could adversely affect our financial results.

Because our consolidated financial statements are presented in U.S. dollars, increases or decreases in the value of the U.S. dollar relative to other currencies in which we transact business could materially adversely affect our financial results. For example, our API business collects revenues in Euros, and accordingly the strengthening of the U.S. dollar relative to the Euro adversely affects our revenue and operating results presented in U.S. dollars. In addition, Following the departure of the U.K. from the EU and the EEA on January 31, 2020 (commonly referred to as “Brexit”) and the expiration of a transition period on December 31, 2020, there continues to be uncertainty over the practical consequences of Brexit including the potential for Brexit to contribute to long-term instability in financial, stock and currency exchange markets, greater restrictions on the supply and availability of goods and services between the U.K. and EEA region, and a general deterioration in consumer sentiment and credit conditions leading to overall negative economic growth and increased risk of merchant default. Brexit has continued to cause significant volatility in global stock markets and currency exchange rate fluctuations that resulted in the fluctuation of the U.S. dollar against foreign currencies in which we conduct business, such as the British Pound, Euro and other currencies. Such fluctuations of the U.S. dollar relative to other currencies may adversely affect our revenue and operating results. In addition, Brexit may affect our ability to negotiate future customer and vendor contracts, and changes to U.K. border and immigration policy could likewise occur as a result of Brexit, affecting our U.K. operation's ability to recruit and retain employees from outside the U.K.

Risks Relating to Marketing and Talent Management

Growth of our business will depend on market awareness and a strong brand, and any failure to develop, maintain, protect and enhance our brand would hurt our ability to retain or attract subscribers.

Beginning in 2020, we introduced a rebranding of the Company and began implementing a new marketing campaign. Building and maintaining market awareness, brand recognition and goodwill in a cost-effective manner is important to our overall success in achieving widespread acceptance of our existing and future solutions and products and is an important element in attracting new customers. While we may choose to engage in a broader marketing campaign to further promote our brand, this effort may not be successful, or our marketing techniques or content may be challenged. The success of our business also relies on our ability to attract new customers in a cost-effective manner by using a variety of marketing channels. Our efforts in developing our brand may be hindered by the marketing efforts of our competitors and our reliance on any strategic partners to promote our brand. If we are unable to cost-effectively maintain and increase awareness of our brand, our business, financial condition, cash flows and results of operations could be harmed.

We depend on the continued services of our senior management and other key employees, the loss of any of whom could adversely affect our business, results of operations and financial condition.

Our future performance depends on the continued services and contributions of our senior management and other key employees to execute on our business plan, and to identify and pursue opportunities and services innovations. The loss of services of senior management or other key employees could significantly delay or prevent the achievement of our development and strategic objectives. None of our executive officers or other senior management personnel is bound by a written employment agreement and any of them may therefore terminate employment with us at any time with no advance notice. The replacement of any of these senior management personnel would likely involve significant time and costs, and such loss could significantly delay or prevent the achievement of our business objectives and acquisition integrations. The loss of the services of our senior management or other key employees for any reason could adversely affect our business, financial condition, or results of operations.

16 VONAGE ANNUAL REPORT 2021

Risks Relating to Cybersecurity, IT Systems, Data Privacy and Fraud

Security breaches and other cybersecurity or technological risks could compromise our information systems and network and expose us to liability, which could cause our business and reputation to suffer and which could have a material adverse effect on our business, financial condition, and operating results.

There are several inherent risks to engaging in a technology business, including our reliance on our data centers and networks, and the use and interconnectivity of those networks. A significant portion of our operations relies heavily on our ability to provide secure processing, storage and transmission of confidential and other sensitive data, including intellectual property, proprietary business information, and personally identifiable information of our customers and employees, in our data centers and on our networks. The secure processing, storage, and transmission of this information is critical to our operations and business strategy. As seen in our industry and others, these activities have been, and will continue to be, subject to continually evolving cybersecurity and other technological risks. Targeted attacks, such as advanced persistent threat is prevalent throughout the Internet and associated with the theft of intellectual property and state-sponsored espionage. Due to the nature of our business and reliance on the Internet, we are susceptible to this type of attack. In addition, physical security of devices located within our offices, and/or remote devices, pose cybersecurity and other technological risks that could negatively impact our business and reputation.