Table of Contents

EXHIBIT 99.1

中国人寿保险股佾有限公司

China Life Insurance Company Limited

Interim Report 2019

1949-2019

Stock Code: 2628

Table of Contents

The predecessor of the Company, one of the first batch of enterprises to underwrite insurance business in China, was approved by the Chinese Government for establishment in October 1949, when the People’s Republic of China was founded. In 1996, in compliance with the separate operation regulation, Zhong Bao Life Insurance Company was established to focus on life insurance business. In 1999, Zhong Bao Life Insurance Company was renamed as China Life Insurance Company. On 30 June 2003, China Life Insurance Company was restructured into China Life Insurance (Group) Company, which founded the Company as a sole promoter. With the 70th anniversary of the Company (from 1949 to 2019) as the theme of the cover page, it is intended to mark the long-standing operations of the Company and its predecessor.

Table of Contents

| 4 | ||||

| 11 | ||||

| 14 | ||||

| 41 | ||||

| 48 | ||||

| 61 | ||||

| 68 | ||||

| 71 | ||||

Table of Contents

Table of Contents

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Definitions and Material Risk Alert

In this report, unless the context otherwise requires, the following expressions have the following meanings:

| China Life or the Company1 |

China Life Insurance Company Limited and its subsidiaries | |

| CLIC |

China Life Insurance (Group) Company, the controlling shareholder of the Company | |

| AMC |

China Life Asset Management Company Limited, a non-wholly owned subsidiary of the Company | |

| Pension Company |

China Life Pension Company Limited, a non-wholly owned subsidiary of the Company | |

| AMP |

China Life AMP Asset Management Co., Ltd., an indirect non-wholly owned subsidiary of the Company | |

| CLWM |

China Life Wealth Management Company Limited, an indirect non-wholly owned subsidiary of the Company | |

| CLP&C |

China Life Property and Casualty Insurance Company Limited, a non-wholly owned subsidiary of CLIC | |

| CLI |

China Life Investment Holding Company Limited, a wholly-owned subsidiary of CLIC | |

| China Life Capital |

China Life Capital Investment Company, an indirect wholly-owned subsidiary of CLIC | |

| CBIRC |

China Banking and Insurance Regulatory Commission, the predecessors of which are the former China Insurance Regulatory Commission and the former China Banking Regulatory Commission | |

| CBIRC Beijing Bureau |

Beijing Bureau of the China Banking and Insurance Regulatory Commission | |

| CSRC |

China Securities Regulatory Commission | |

| HKSE |

The Stock Exchange of Hong Kong Limited | |

| SSE |

Shanghai Stock Exchange | |

| Company Law |

Company Law of the People’s Republic of China | |

| Insurance Law |

Insurance Law of the People’s Republic of China | |

| Securities Law |

Securities Law of the People’s Republic of China | |

| Articles of Association |

Articles of Association of China Life Insurance Company Limited | |

| China or PRC |

For the purpose of this report, “China” or “PRC” refers to the People’s Republic of China, excluding the Hong Kong Special Administrative Region, Macau Special Administrative Region and Taiwan region | |

| RMB |

Renminbi Yuan | |

Material Risk Alert:

The Company has stated in this report the details of its existing risks including risks relating to macro trends, risks relating to insurance business, risks relating to investment business and risks relating to network security. Please refer to the analysis of the risks which the Company may face in its future development in the section headed “Management Discussion and Analysis”.

| 1 | Except for “the Company” referred to in the Interim Condensed Consolidated Financial Statements. |

4

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Prelude

The Company is a life insurance company established in Beijing, China on 30 June 2003 according to the Company Law and the Insurance Law. The Company was successfully listed on the New York Stock Exchange, the Hong Kong Stock Exchange and the Shanghai Stock Exchange on 17 and 18 December 2003, and 9 January 2007, respectively. The Company’s registered capital is RMB28,264,705,000.

The Company is a leading life insurance company in China and possesses an extensive distribution network comprising exclusive agents, direct sales representatives, and dedicated and non-dedicated agencies. The Company is one of the largest institutional investors in China, and becomes one of the largest insurance asset management companies in China through its controlling shareholding in China Life Asset Management Company Limited. The Company also has controlling shareholding in China Life Pension Company Limited.

Our products and services include individual life insurance, group life insurance, and accident and health insurance. The Company is a leading provider of individual and group life insurance, annuity products and accident and health insurance in China. As at 30 June 2019, the Company had approximately 297 million long-term individual and group life insurance policies, annuity contracts, and long-term health insurance policies in force. We also provide both individual and group accident and short-term health insurance policies and services.

| I. BASIC INFORMATION | ||

| Registered Name in Chinese |

中國人壽保險股份有限公司(簡稱「中國人壽」) | |

| Registered Name in English |

China Life Insurance Company Limited (“China Life”) | |

| Legal Representative |

Wang Bin | |

| Registered Office Address |

16 Financial Street, Xicheng District, Beijing, P.R. China | |

| Postal Code |

100033 | |

| Current Office Address |

16 Financial Street, Xicheng District, Beijing, P.R. China | |

| Postal Code |

100033 | |

| Telephone |

86-10-63633333 | |

| Fax |

86-10-66575722 | |

| Website |

www.e-chinalife.com | |

| |

ir@e-chinalife.com | |

| Hong Kong Office Address |

16/F, Tower A, China Life Centre, One Harbour Gate, 18 Hung Luen Road, Hung Hom, Kowloon, Hong Kong | |

| Telephone |

852-29192628 | |

| Fax |

852-29192638 | |

II. CONTACT INFORMATION

| Board Secretary | Securities Representative | |||

| Name |

Li Mingguang | Li Yinghui | ||

| Office Address |

16 Financial Street, Xicheng District, Beijing, P.R. China |

16 Financial Street, Xicheng District, Beijing, P.R. China | ||

| Telephone |

86-10-63631241 | 86-10-63631191 | ||

| Fax |

86-10-66575112 | 86-10-66575112 | ||

| |

ir@e-chinalife.com | liyh@e-chinalife.com | ||

| *Ms. Li Yinghui, Securities Representative of the Company, is also the main contact person of the external Company Secretary engaged by the Company |

5

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Prelude

Company Profile (continued)

III. INFORMATION DISCLOSURE AND PLACE FOR OBTAINING THE REPORT

| Media for the Company’s A Share Disclosure |

China Securities Journal, Shanghai Securities News, Securities Times | |

| CSRC’s Designated Website for the Company’s Interim Report Disclosure | www.sse.com.cn | |

| The Company’s H Share Disclosure Websites | HKExnews website of Hong Kong Exchanges and Clearing Limited at www.hkexnews.hk The Company’s website at www.e-chinalife.com | |

| The Company’s Interim Report may be obtained at | 12/F, China Life Plaza, 16 Financial Street, Xicheng District, Beijing, P.R. China | |

IV. STOCK INFORMATION

| Stock Type | Exchanges on which the Stocks are Listed |

Stock Short Name | Stock Code | |||

| A Share |

Shanghai Stock Exchange | China Life | 601628 | |||

| H Share |

The Stock Exchange of Hong Kong Limited | China Life | 2628 | |||

| ADR |

New York Stock Exchange | – | LFC | |||

V. OTHER RELEVANT INFORMATION

| H Share Registrar and Transfer Office |

Computershare Hong Kong Investors Services Limited | Address: Shops 1712-1716, 17th Floor, Hopewell Centre, 183 Queen’s Road East, Wanchai, Hong Kong | ||

| Depositary of ADR |

Deutsche Bank | Address: 60 Wall Street, New York, NY 10005 | ||

| Domestic Legal Adviser |

King & Wood Mallesons | |||

| International Legal Advisers |

Latham & Watkins LLP | Debevoise & Plimpton LLP | ||

| Domestic Auditor | International Auditor | |||

| Ernst & Young Hua Ming LLP | Ernst & Young | |||

| Auditors of the Company |

Address: Level 16, Ernst & Young Tower, Oriental Plaza, No. 1 East Changan Avenue, Dongcheng District, Beijing, P.R. China |

Address: 22/F, CITIC Tower, 1 Tim Mei Avenue, Central, Hong Kong | ||

| Name of the Signing Auditors: Huang Yuedong, Wu Jun | ||||

6

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Prelude

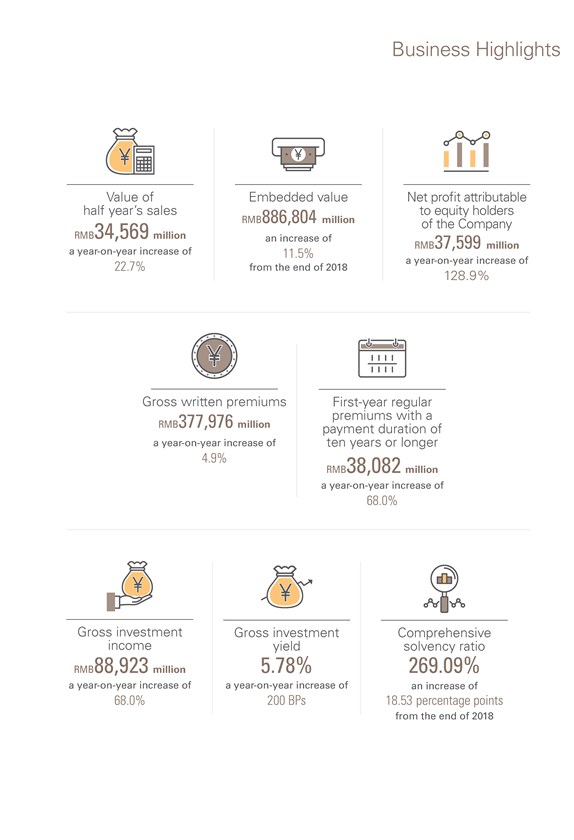

Value of half year’s sales RMB 34,569 million a year-on-year increase of 22.7%

Embedded value RMB886,804 million an increase of 11.5% from the end of 2018

Net profit

attributable to equity holders of the Company RMB37,599 million a year-on-year increase of 128.9%

Gross written premiums RMB377,976 million a year-on-year increase

of 4.9%

First-year regular premiums with a payment duration of ten years or longer RMB38,082 million a year-on-year increase of 68.0%

Gross investment income RMB88,923 million a year-on-year increase of 68.0%

Gross investment

yield 5.78% a year-on-year increase of 200 BPs

Comprehensive solvency ratio 269.09% an increase of 18.53 percentage points from the end of 2018

7

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Prelude

MAJOR FINANCIAL DATA AND INDICATORS

| RMB million | ||||||||||||

| As at 30 June 20191 |

As at 31 December 2018 |

Increase/ Decrease from the end of 2018 |

||||||||||

| Total assets |

3,479,860 | 3,254,403 | 6.9 | % | ||||||||

| Including: Investment assets2 |

3,304,129 | 3,104,014 | 6.4 | % | ||||||||

| Equity holders’ equity |

368,434 | 318,371 | 15.7 | % | ||||||||

| Ordinary share holders’ equity per share3 (RMB per share) |

12.76 | 10.99 | 16.1 | % | ||||||||

| Ratio of assets and liabilities4 (%) |

89.26 | 90.07 | |

A decrease of 0.81 percentage point |

| |||||||

| January to June 20191 |

January to June 2018 |

Increase/ Decrease from the corresponding period in 2018 |

||||||||||

| Total revenues |

448,221 | 401,690 | 11.6 | % | ||||||||

| Including: Net premiums earned |

361,297 | 348,985 | 3.5 | % | ||||||||

| Profit before income tax |

38,893 | 21,447 | 81.3 | % | ||||||||

| Net profit attributable to equity holders of the Company |

37,599 | 16,423 | 128.9 | % | ||||||||

| Net profit attributable to ordinary share holders of the Company |

37,403 | 16,235 | 130.4 | % | ||||||||

| Earnings per share (basic and diluted)3 (RMB per share) |

1.32 | 0.57 | 130.4 | % | ||||||||

| Weighted average ROE (%) |

11.14 | 5.11 | |

An increase of 6.03 percentage points |

| |||||||

| Net cash inflow/(outflow) from operating activities |

150,290 | 44,172 | 240.2 | % | ||||||||

| Net cash inflow/(outflow) from operating activities per share3 (RMB per share) |

5.32 | 1.56 | 240.2 | % | ||||||||

| Notes: |

| 1. | The interim financial results for the Reporting Period are unaudited. | |

| 2. | Investment assets = Cash and cash equivalents + Securities at fair value through profit or loss + Available-for-sale securities + Held-to-maturity securities + Term deposits + Securities purchased under agreements to resell + Loans + Statutory deposits — restricted + Investment properties + Investments in associates and joint ventures | |

| 3. | In calculating the percentage changes of “Ordinary share holders’ equity per share”, “Earnings per share (basic and diluted)” and “Net cash inflow/ (outflow) from operating activities per share”, the tail differences of the basic figures have been taken into account. | |

| 4. | Ratio of assets and liabilities = Total liabilities/Total assets |

8

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Prelude

Financial Summary (continued)

MAJOR ITEMS OF THE CONSOLIDATED FINANCIAL STATEMENTS AND THE REASONS FOR CHANGE

| RMB million | ||||||||||||||

| Major Items of the Consolidated Statement of Financial Position |

As at 30 June 2019 |

As at 31 December 2018 |

Change | Main Reasons for Change | ||||||||||

| Held-to-maturity securities |

874,383 | 806,717 | 8.4 | % | An increase in the allocation of bonds | |||||||||

| Available-for-sale securities |

932,947 | 870,533 | 7.2 | % | An increase in the allocation and fair value of equity investments in available-for-sale securities | |||||||||

| Securities at fair value through profit or loss |

138,366 | 138,717 | -0.3 | % | — | |||||||||

| Securities purchased under agreements to resell |

3,247 | 9,905 | -67.2 | % | The needs for liquidity management | |||||||||

| Cash and cash equivalents |

57,259 | 50,809 | 12.7 | % | The needs for liquidity management | |||||||||

| Loans |

505,669 | 450,251 | 12.3 | % | An increase in the scale of trust schemes and policy loans | |||||||||

| Investment properties |

9,793 | 9,747 | 0.5 | % | — | |||||||||

| Investments in associates and joint ventures |

219,560 | 201,661 | 8.9 | % | New investments in associates and joint ventures | |||||||||

| Deferred tax assets |

57 | 1,257 | -95.5 | % | Affected by an increase in the fair value of available-for-sale securities | |||||||||

| Insurance contracts |

2,457,077 | 2,216,031 | 10.9 | % | The accumulation of insurance liabilities from new policies and renewal business | |||||||||

| Investment contracts |

268,106 | 255,434 | 5.0 | % | An increase in the scale of universal insurance accounts | |||||||||

| Securities sold under agreements to repurchase |

90,496 | 192,141 | -52.9 | % | The needs for liquidity management | |||||||||

| Annuity and other insurance balances payable |

50,931 | 49,465 | 3.0 | % | An increase in maturities payable | |||||||||

| Interest-bearing loans and other borrowingsNote |

20,195 | 20,150 | 0.2 | % | — | |||||||||

| Bonds payable |

34,989 | — | N/A | Issuance of capital supplemental bonds | ||||||||||

| Deferred tax liabilities |

8,312 | — | N/A | Affected by an increase in the fair value of available-for-sale securities | ||||||||||

| Equity holders’ equity |

368,434 | 318,371 | 15.7 | % | Due to the combined impact of total comprehensive income and profit distribution during the Reporting Period | |||||||||

| Note: | Interest-bearing loans and other borrowings include a three-year bank loan of USD970 million with a maturity date on 27 September 2019, a three-year bank loan of USD940 million with a maturity date on 30 September 2019, a three-year bank loan of EUR67 million with a maturity date on 18 January 2021, a five-year bank loan of GBP275 million with a maturity date on 27 June 2024, a six-month bank loan of EUR127 million with a maturity date on 11 July 2019 which is automatically renewed upon maturity pursuant to the terms of the agreement, and a three-month bank loan of USD5 million with a maturity date on 10 September 2019. All the above are fixed rate loans. A three-year loan of EUR400 million with a maturity date on 6 December 2020, which is a floating rate loan. |

9

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Prelude

Financial Summary (continued)

| RMB million | ||||||||||||||

| Major Items of the Consolidated Statement of Comprehensive Income |

January to June 2019 |

January to June 2018 |

Change | Main Reasons for Change | ||||||||||

| Net premiums earned |

361,297 | 348,985 | 3.5 | % | — | |||||||||

| Life insurance business |

307,009 | 303,940 | 1.0 | % | — | |||||||||

| Health insurance business |

46,989 | 37,616 | 24.9 | % | The expansion of health insurance business by the Company | |||||||||

| Accident insurance business |

7,299 | 7,429 | -1.7 | % | — | |||||||||

| Investment income |

66,345 | 60,618 | 9.4 | % | An increase in interest income from fixed-income investment assets | |||||||||

| Net realised gains on financial assets |

3,786 | (4,432 | ) | N/A | An increase in spread income of stocks in available-for-sale securities | |||||||||

| Net fair value gains through profit or loss |

13,107 | (7,460 | ) | N/A | An increase in profit or loss in fair value of stocks in securities at fair value through profit or loss | |||||||||

| Share of net profit of associates and joint ventures |

5,665 | 4,136 | 37.0 | % | An increase in the profits of certain associates | |||||||||

| Other income |

3,686 | 3,979 | -7.4 | % | A decrease in commission fees from agency services for CLP&C | |||||||||

| Insurance benefits and claims expenses |

330,049 | 313,319 | 5.3 | % | The growth of insurance business | |||||||||

| Investment contract benefits |

4,617 | 4,829 | -4.4 | % | A decrease in the settlement interest rate of certain universal insurance policies | |||||||||

| Policyholder dividends resulting from participation in profits |

10,836 | 9,312 | 16.4 | % | An increase in investment yield from the participating account | |||||||||

| Underwriting and policy acquisition costs |

45,595 | 35,707 | 27.7 | % | An increase in commissions of regular business due to the Company’s business growth and the optimization of its business structure | |||||||||

| Finance costs |

1,930 | 2,128 | -9.3 | % | A decrease in interest paid for securities sold under agreements to repurchase | |||||||||

| Administrative expenses |

16,958 | 14,924 | 13.6 | % | The growth of business | |||||||||

| Income tax |

964 | 4,744 | -79.7 | % | The impact from the new policy on pre-tax deduction of underwriting and policy acquisition costs | |||||||||

| Net profit attributable to equity holders of the Company |

37,599 | 16,423 | 128.9 | % | An increase in gross investment income and the impact from the new policy on pre-tax deduction of underwriting and policy acquisition costs | |||||||||

10

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

In the first half of 2019, under the guidance of the strategic goal of “China Life Revitalization”, the Chairman’s

Company concentrated on high-quality development, actively served the real economy, prevented and mitigated financial risks, and vigorously pushed Statement forward various reforms, which kicked off a good beginning of “China Life

Revitalization”. I, on behalf of the Company’s board of directors, hereby 11 report to shareholders and the public the Company’s achievements made in the first half of the year, and describe its China journey of “reforming and

restructuring”.

Wang Bin Interim Chairman

11

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Chairman’s Statement

12

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Chairman’s Statement (continued)

13

Table of Contents

MANAGEMENT DISCUSSION AND ANALYSIS

| 15 | ||||

| 18 | ||||

| 28 | ||||

| Technology Empowerment, Operations and Services, Risk Control and Management |

32 | |||

| 35 | ||||

| 38 | ||||

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis

| I. | REVIEW OF BUSINESS OPERATIONS IN THE FIRST HALF OF 2019 |

In the first half of 2019, the Chinese economy generally maintained steady growth, and the situation at home and abroad was intricate and complex. Given that the uncertainties in the external environment brought about pressures and challenges to the insurance market, the insurance industry increasingly deepened transformation and upgrade, and the life insurance industry moved towards high-quality development. During the Reporting Period, the Company firmly concentrated on the strategic goal of “China Life Revitalization” with “Dual Centers and Dual Focuses” as its strategic core and adhered to the operational guideline of “prioritizing business value, strengthening sales force, achieving stable growth, upgrading technology, optimizing customer services and guarding against risks”. By adopting a “customer-oriented” approach and concentrating on local branches and field offices, and sticking to the fundamental requirement of high-quality development, the Company pushed forward various tasks in an active and prudent manner. For the first half of 2019, the core business of the Company developed rapidly and its business structure was optimized consistently, which resulted in a significant growth in its business value. The Company’s sales force was enhanced in both quantity and quality, its investment income increased significantly, and its profitability was improved substantially. In the meanwhile, technology-empowered operation became a new driving force for the Company’s business development. The Company has made a fresh headway in an all-round way.

15

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

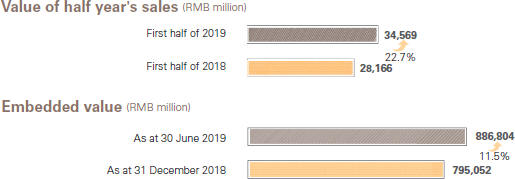

During the Reporting Period, the Company’s gross written premiums amounted to RMB377,976 million, an increase of 4.9% year-on-year. As at 30 June 2019, the embedded value of the Company reached RMB886,804 million, an increase of 11.5% from the end of 2018. The value of half year’s sales was RMB34,569 million, an increase of 22.7% year-on-year. During the Reporting Period, the Company’s gross investment income reached RMB88,923 million, an increase of 68.0% year-on-year. Net profit attributable to equity holders of the Company was RMB37,599 million, an increase of 128.9% year-on-year. As at the end of the Reporting Period, the core solvency ratio and the comprehensive solvency ratio were 258.62% and 269.09%, respectively.

Key Performance Indicators for the First Half of 2019

| RMB million | ||||||||

| January to June 2019 |

January to June 2018 |

|||||||

| Gross written premiums |

377,976 | 360,482 | ||||||

| Premiums from new policies |

127,845 | 125,321 | ||||||

| Including: First-year regular premiums |

83,133 | 81,712 | ||||||

| First-year regular premiums with a payment duration of ten years or longer |

38,082 | 22,669 | ||||||

| Renewal premiums |

250,131 | 235,161 | ||||||

| Gross investment income |

88,923 | 52,937 | ||||||

| Net profit attributable to equity holders of the Company |

37,599 | 16,423 | ||||||

| Value of half year’s sales |

34,569 | 28,166 | ||||||

| Including: Exclusive individual agent channel |

30,378 | 24,077 | ||||||

| Bancassurance channel |

4,039 | 3,887 | ||||||

| Group insurance channel |

152 | 202 | ||||||

| Policy Persistency Rate (14 months)1 (%) |

86.10 | 92.30 | ||||||

| Policy Persistency Rate (26 months)1 (%) |

87.00 | 86.80 | ||||||

| Surrender Rate2 (%) |

1.43 | 4.30 | ||||||

| As at 30 June 2019 |

As at 31 December 2018 |

|||||||

| Embedded value |

886,804 | 795,052 | ||||||

| Number of long-term in-force policies (hundred million) |

2.97 | 2.85 | ||||||

| Notes: | ||||

| 1. The Persistency Rate for long-term individual life insurance policy is an important operating performance indicator for life insurance companies. It measures the ratio of in-force policies in a pool of policies after a certain period of time. It refers to the proportion of policies that are still effective during the designated month in the pool of policies whose issue date was 14 or 26 months ago. 2. Surrender Rate = Surrender payment/(Liability of long-term insurance contracts at the beginning of the period + Premiums of long-term insurance contracts) | ||||

16

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

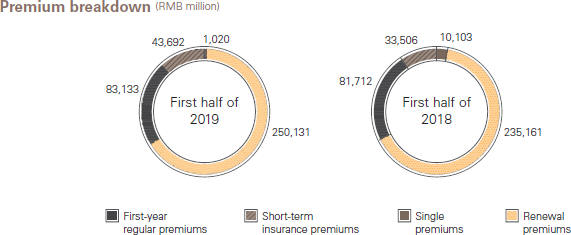

During the Reporting Period, the Company continued to optimize its business structure. First-year regular premiums amounted to RMB83,133 million, which accounted for 98.79% in long-term first-year premiums, increasing by 9.79 percentage points year-on-year. In particular, first-year regular premiums with a payment duration of ten years or longer was RMB38,082 million (a year-on-year increase of 68.0%), which accounted for 45.81% of the first-year regular premiums (a year-on-year increase of 18.07 percentage points). Single premiums were RMB1,020 million, a decrease of 89.9% year-on-year, and the percentage of single premiums in long-term first-year premiums was reduced to 1.21% from 11.00% of the corresponding period in 2018. Renewal premiums amounted to RMB250,131 million (a year-on-year increase of 6.4%), which accounted for 66.18% of the gross written premiums, a slight increase compared to the same period in 2018.

During the Reporting Period, the Company’s business value was improved significantly. The value of half year’s sales of the Company was RMB34,569 million, rising by 22.7% year-on-year. The new business margin of half year’s sales of the exclusive individual agent channel and the bancassurance channel increased by 4.2 and 7.9 percentage points year-on-year, respectively. As at 30 June 2019, the embedded value of the Company was RMB886,804 million, rising by 11.5% from the end of 2018. The Company accelerated the development of long-term protection-oriented and long-term savings businesses, with its product structure continuously diversified. Out of the top ten insurance products by the first-year regular premiums, six were protection-oriented products. In the first half of 2019, protection-oriented business of the Company developed rapidly, the percentage of which in the first-year regular premiums increased by 5.0 percentage points year-on-year. As at the end of the Reporting Period, the number of long-term in-force policies was 297 million, an increase of 4.2% from the end of 2018.

During the Reporting Period, the Company recorded a gross investment income of RMB88,923 million, an increase of 68.0% year-on-year. Due to an increase in gross investment income and the impact from the new policy on pre-tax deduction of underwriting and policy acquisition costs, net profit attributable to equity holders of the Company was RMB37,599 million, rising by 128.9% year-on-year.

17

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| II. | BUSINESS ANALYSIS |

| (I) | Insurance Business |

| 1. | Gross written premiums categorized by business |

| RMB million | ||||||||||||

| January to June 2019 |

January to June 2018 |

Change | ||||||||||

| Life Insurance Business |

307,461 | 304,341 | 1.0 | % | ||||||||

| First-year business |

78,573 | 87,007 | -9.7 | % | ||||||||

| First-year regular |

77,563 | 76,918 | 0.8 | % | ||||||||

| Single |

1,010 | 10,089 | -90.0 | % | ||||||||

| Renewal business |

228,888 | 217,334 | 5.3 | % | ||||||||

| Health Insurance Business |

62,416 | 48,090 | 29.8 | % | ||||||||

| First-year business |

41,444 | 30,479 | 36.0 | % | ||||||||

| First-year regular |

5,523 | 4,709 | 17.3 | % | ||||||||

| Single |

35,921 | 25,770 | 39.4 | % | ||||||||

| Renewal business |

20,972 | 17,611 | 19.1 | % | ||||||||

| Accident Insurance Business |

8,099 | 8,051 | 0.6 | % | ||||||||

| First-year business |

7,828 | 7,835 | -0.1 | % | ||||||||

| First-year regular |

47 | 85 | -44.7 | % | ||||||||

| Single |

7,781 | 7,750 | 0.4 | % | ||||||||

| Renewal business |

271 | 216 | 25.5 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total |

377,976 | 360,482 | 4.9 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Note: | Single premiums in the above table include premiums from short-term insurance business. |

During the Reporting Period, gross written premiums from the life insurance business of the Company amounted to RMB307,461 million, a year-on-year increase of 1.0%. Gross written premiums from the health insurance business amounted to RMB62,416 million, a year-on-year increase of 29.8%. Gross written premiums from the accident insurance business amounted to RMB8,099 million, a year-on-year increase of 0.6%.

18

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| 2. | Gross written premiums categorized by channel |

| RMB million | ||||||||

| January to June 2019 |

January to June 2018 |

|||||||

| Exclusive Individual Agent Channel |

290,556 | 272,233 | ||||||

| First-year business of long-term insurance |

64,652 | 61,566 | ||||||

| First-year regular |

64,529 | 61,442 | ||||||

| Single |

123 | 124 | ||||||

| Renewal business |

218,023 | 204,781 | ||||||

| Short-term insurance business |

7,881 | 5,886 | ||||||

| Bancassurance Channel |

47,357 | 55,998 | ||||||

| First-year business of long-term insurance |

17,327 | 27,457 | ||||||

| First-year regular |

17,315 | 18,819 | ||||||

| Single |

12 | 8,638 | ||||||

| Renewal business |

29,198 | 27,974 | ||||||

| Short-term insurance business |

832 | 567 | ||||||

| Group Insurance Channel |

16,798 | 14,986 | ||||||

| First-year business of long-term insurance |

1,507 | 2,137 | ||||||

| First-year regular |

622 | 797 | ||||||

| Single |

885 | 1,340 | ||||||

| Renewal business |

1,314 | 1,105 | ||||||

| Short-term insurance business |

13,977 | 11,744 | ||||||

| Other Channels1 |

23,265 | 17,265 | ||||||

| First-year business of long-term insurance |

667 | 655 | ||||||

| First-year regular |

667 | 654 | ||||||

| Single |

– | 1 | ||||||

| Renewal business |

1,596 | 1,301 | ||||||

| Short-term insurance business |

21,002 | 15,309 | ||||||

|

|

|

|

|

|||||

| Total |

377,976 | 360,482 | ||||||

|

|

|

|

|

|||||

Notes:

| 1. | Other channels mainly include supplementary major medical expenses insurance business, tele-sales, online-sales, etc. |

| 2. | The Company’s channel premium breakdown was presented based on the separate groups of sales personnels including exclusive individual agent team, group insurance sales representatives, bancassurance sales team and other distribution channels. |

19

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

In the first half of 2019, the Company recorded a rapid growth in its core business by consistently focusing on its business value growth and pushing forward business restructuring and product diversification. In particular, protection-oriented business saw rapid development and the business structure was continuously optimized. The Company firmly implemented the sales force development strategy of quality improvement and size expansion, and further strengthened its day-to-day management. As a result, the size of the sales force expanded steadily with its quality consistently improved. As at the end of the Reporting Period, the total number of sales force from all channels amounted to about 1.9 million.

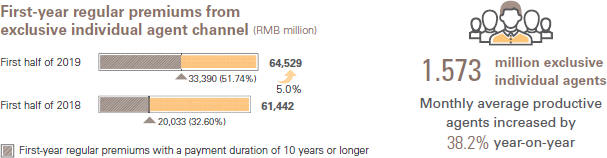

Exclusive Individual Agent Channel. In the first half of 2019, centering on business value growth, the exclusive individual agent channel endeavored to transform and upgrade in its sales management, and strengthened the coordinated development among business, sales force and day-to-day management, so as to achieve continuous growth and its new business margin increased effectively. During the Reporting Period, gross written premiums from the exclusive individual agent channel amounted to RMB290,556 million, an increase of 6.7% year-on-year. First-year regular premiums from the channel were RMB64,529 million, an increase of 5.0% year-on-year, which accounted for 99.81% of long-term first-year premiums. In particular, the percentage of first-year regular premiums with a payment duration of ten years or longer in first-year regular premiums was 51.74%, an increase of 19.14 percentage points year-on-year. New business margin of half year’s sales of the exclusive individual agent channel reached 36.6%, a year-on-year increase of 4.2 percentage points. Renewal premiums amounted to RMB218,023 million, an increase of 6.5% year-on-year. In the first half of 2019, the sales force of the exclusive individual agent channel was improved in both quantity and quality, and the expansion of the sales force vigorously drove the business growth. As at the end of the Reporting Period, the number of exclusive individual agents was 1.573 million, growing by 9.3% from the end of 2018. In the meantime, the quality of the sales force was improved consistently, with its monthly average productive agents increasing by 38.2% year-on-year. Moreover, the monthly average number of agents selling designated protection-oriented products rose substantially, representing an increase of 52.1% year-on-year.

20

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

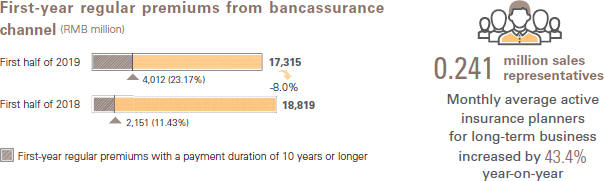

Bancassurance Channel. In the first half of 2019, the bancassurance channel furthered its business restructuring by firmly concentrating on the long-term regular premium business, and the new business margin of half year’s sales of the channel improved constantly. During the Reporting Period, single premiums from the bancassurance channel were significantly reduced to RMB12 million from RMB8,638 million in the corresponding period of 2018, and gross written premiums from the channel were RMB47,357 million, a decrease of 15.4% year-on-year. First-year regular premiums were RMB17,315 million (a year-on-year decrease of 8.0%), which accounted for 99.93% of the long-term first year premiums (a year-on-year increase of 31.39 percentage points). In particular, first-year regular premiums with a payment duration of ten years or longer were RMB4,012 million (a year-on-year increase of 86.5%), which accounted for 23.17% of the first-year regular premiums (a year-on-year increase of 11.74 percentage points). New business margin of half year’s sales of the channel was 21.5%, rising by 7.9 percentage points year-on-year. Renewal premiums amounted to RMB29,198 million (a year-on-year increase of 4.4%), which accounted for 61.66% of the gross written premiums from this channel (a year-on-year increase of 11.70 percentage points). As at the end of the Reporting Period, the number of sales representatives of the bancassurance channel reached 0.241 million and the quality of the sales force of the channel was further improved, with the monthly average active insurance planners for long-term business increasing by 43.4% year-on-year.

21

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| Group Insurance Channel. In the first half of 2019, the group insurance channel consistently pushed forward diversified business development and strengthened business structural optimization, which therefore led to steady growth of various businesses. During the Reporting Period, gross written premiums from the group insurance channel were RMB16,798 million, an increase of 12.1% year-on-year. Short-term insurance premiums from the group insurance channel were RMB13,977 million, an increase of 19.0% year-on-year. The Company actively carried out the pilot program of tax deferred pension insurance business and consistently promoted the tax-advantaged health insurance business. As at the end of the Reporting Period, the number of direct sales representatives reached 0.079 million, among which the number of the high-performance representatives reached 0.051 million. |

|

Other Channels. In the first half of 2019, gross written premiums from other channels reached RMB23,265 million, an increase of 34.8% year-on-year. The Company actively developed the policy-oriented health insurance businesses, including supplementary major medical expenses insurance and long-term care insurance, which consistently led the market. As at the end of the Reporting Period, the Company undertook a total of over 230 supplementary major medical expenses insurance projects, 30 long-term care insurance projects and 38 supplementary medial insurance projects for social security, providing services for nearly 400 million people in 28 provinces. The Company continued to explore the development of online insurance sales and intended to provide more convenient ways of insurance application and diversified financial services to its customers via various measures, such as establishing online malls, streamlining operation procedures and enriching insurance products, etc.

22

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| 3. | Insurance contracts |

| RMB million | ||||||||||||

| As at 30 June 2019 |

As at 31 December 2018 |

Change | ||||||||||

| Life insurance |

2,291,420 | 2,081,822 | 10.1 | % | ||||||||

| Health insurance |

156,614 | 125,743 | 24.6 | % | ||||||||

| Accident insurance |

9,043 | 8,466 | 6.8 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total of insurance contracts |

2,457,077 | 2,216,031 | 10.9 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Including: residual marginNote |

742,177 | 684,082 | 8.5 | % | ||||||||

| Note: | The residual margin is a component of insurance contract reserve, which results in no Day 1 gain at the initial recognition of an insurance contract. The residual margin is set to zero if it is negative. The growth of residual margin arises mainly from new business. |

As at the end of the Reporting Period, the reserves of insurance contracts of the Company increased by 10.9% from the end of 2018, which is primarily due to the accumulation of insurance liabilities from new policies and renewal business. As at the date of the statement of financial position, the reserves of various insurance contracts of the Company passed the adequacy test.

| 4. | Analysis of claims and policyholder benefits |

| RMB million | ||||||||||||

| January to June 2019 |

January to June 2018 |

Change | ||||||||||

| Insurance benefits and claims expenses |

330,049 | 313,319 | 5.3 | % | ||||||||

| Life insurance business |

291,580 | 282,294 | 3.3 | % | ||||||||

| Health insurance business |

35,474 | 27,408 | 29.4 | % | ||||||||

| Accident insurance business |

2,995 | 3,617 | -17.2 | % | ||||||||

| Investment contract benefits |

4,617 | 4,829 | -4.4 | % | ||||||||

| Policyholder dividends resulting from participation in profits |

10,836 | 9,312 | 16.4 | % | ||||||||

During the Reporting Period, insurance benefits and claims expenses rose by 5.3% year-on-year due to the stable development of insurance business. In particular, life insurance business rose by 3.3% year-on-year due to the growth of life insurance business; health insurance business rose by 29.4% year-on-year due to the growth of health insurance business; accident insurance business decreased by 17.2% year-on-year due to the sequential differences in short-term insurance business. Investment contract benefits decreased by 4.4% year-on-year due to a decrease in the settlement interest rate of certain universal insurance policies. Policyholder dividends resulting from participation in profits increased by 16.4% year-on-year due to an increase in investment yield from participating accounts.

23

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| 5. | Analysis of underwriting and policy acquisition costs and other expenses |

| RMB million | ||||||||||||

| January to June 2019 |

January to June 2018 |

Change | ||||||||||

| Underwriting and policy acquisition costs |

45,595 | 35,707 | 27.7 | % | ||||||||

| Finance costs |

1,930 | 2,128 | -9.3 | % | ||||||||

| Administrative expenses |

16,958 | 14,924 | 13.6 | % | ||||||||

| Other expenses |

4,271 | 3,470 | 23.1 | % | ||||||||

| Statutory insurance fund contribution |

737 | 690 | 6.8 | % | ||||||||

During the Reporting Period, underwriting and policy acquisition costs increased by 27.7% year-on-year due to an increase in commissions of regular business as a result of the growth of the Company’s business and the optimization of its business structure. Finance costs decreased by 9.3% year-on-year due to a decrease in interest paid for securities sold under agreements to repurchase. Administrative expenses increased by 13.6% year-on-year as a result of its business growth.

| (II) | Investment Business |

Since 2019, the growth momentum of the global economy has declined gradually, along with the international trade frictions taking place frequently. The domestic economy generally remained stable but still under a downward pressure. In domestic bond market, the interest rate constantly fluctuated at a low level, and in domestic stock market, although it has been pulled back after a surge in the first quarter of 2019, the market saw a notable rise compared to the beginning of 2019. In the first half of 2019, the Company laid emphasis on asset-liability interaction from the perspective of assets and liabilities management. In respect of fixed income investments, the Company increased allocation particularly in bonds with long duration with preemptive actions by seizing allocation opportunities on interest rate trend and market supply. The Company also flexibly allocated to selected bank deposits and non-standard fixed-income investments, and strived to increase investment yields from allocation with stringent credit risk control. In respect of equity investments in the open market, the Company took active actions by capturing any opportunities arising in the equity market effectively and added exposure to long-term core assets at an attractive valuation level while catching short-term trading opportunities. During the pullback period of the market, the Company closely monitored risk exposure with disciplined rebalancing strategy, thus achieving satisfactory investment returns. As at the end of the Reporting Period, the Company’s investment assets reached RMB3,304,129 million, an increase of 6.4% from the end of 2018.

24

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| 1. | Investment portfolios |

As at the end of the Reporting Period, our investment assets categorized by investment object are set out as below:

| As at 30 June 2019 | RMB million As at 31 December 2018 |

|||||||||||||||

| Investment category |

Amount | Percentage | Amount | Percentage | ||||||||||||

| Fixed-maturity financial assets |

2,505,534 | 75.82 | % | 2,407,236 | 77.55 | % | ||||||||||

| Term deposits |

556,572 | 16.84 | % | 559,341 | 18.02 | % | ||||||||||

| Bonds |

1,352,911 | 40.95 | % | 1,309,831 | 42.20 | % | ||||||||||

| Debt-type financial products1 |

377,681 | 11.43 | % | 351,277 | 11.32 | % | ||||||||||

| Other fixed-maturity investments2 |

218,370 | 6.60 | % | 186,787 | 6.01 | % | ||||||||||

| Equity financial assets |

508,736 | 15.40 | % | 424,656 | 13.68 | % | ||||||||||

| Common stocks |

235,555 | 7.13 | % | 178,710 | 5.76 | % | ||||||||||

| Funds3 |

121,841 | 3.69 | % | 106,271 | 3.42 | % | ||||||||||

| Bank wealth management products |

37,683 | 1.14 | % | 32,854 | 1.06 | % | ||||||||||

| Other equity investments4 |

113,657 | 3.44 | % | 106,821 | 3.44 | % | ||||||||||

| Investment properties |

9,793 | 0.30 | % | 9,747 | 0.31 | % | ||||||||||

| Cash and others5 |

60,506 | 1.83 | % | 60,714 | 1.96 | % | ||||||||||

| Investments in associates and joint ventures |

219,560 | 6.65 | % | 201,661 | 6.50 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

3,304,129 | 100.00 | % | 3,104,014 | 100.00 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Notes:

| 1. | Debt-type financial products include debt investment schemes, equity investment plans, trust schemes, project asset-backed plans, credit asset-backed securities, specialized asset management plans, and asset management products, etc. |

| 2. | Other fixed-maturity investments include policy loans, statutory deposits-restricted, and interbank certificates of deposits, etc. |

| 3. | Funds include equity funds, bond funds and money market funds, etc. In particular, the balances of money market funds as at 30 June 2019 and 31 December 2018 were RMB1,004 million and RMB4,635 million, respectively. |

| 4. | Other equity investments include private equity funds, unlisted equities, preference shares, and equity investment plans, etc. |

| 5. | Cash and others include cash, cash at banks, short-term bank deposits and securities purchased under agreements to resell, etc. |

25

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

As at the end of the Reporting Period, among the major types of investments, the percentage of bonds changed to 40.95% from 42.20% as at the end of 2018, the percentage of term deposits changed to 16.84% from 18.02% as at the end of 2018, the percentage of debt-type financial products increased to 11.43% from 11.32% as at the end of 2018, and the percentage of stocks and funds (excluding money market funds) increased to 10.79% from 9.03% as at the end of 2018.

The Company’s debt-type financial products mainly concentrated on the sectors such as transportation, public utilities and energy, and the financing entities were primarily large central-owned enterprises and state-owned enterprises. As at the end of the Reporting Period, over 98% of the debt-type financial products were rated AAA or above by the external rating institutions. In general, the quality of the Company’s debt-type investment assets was in good condition and the debt risks were well controlled.

| 2. | Investment income |

| RMB million | ||||||||

| January to June 2019 |

January to June 20181 |

|||||||

| Gross investment income2 |

88,923 | 52,937 | ||||||

| Net investment income3 |

72,030 | 64,829 | ||||||

| Net income from fixed-maturity investments |

56,274 | 51,492 | ||||||

| Net income from equity investments |

9,563 | 8,594 | ||||||

| Net income from investment properties |

20 | 75 | ||||||

| Investment income from cash and others |

508 | 532 | ||||||

| Net income from investments in associates and joint ventures |

5,665 | 4,136 | ||||||

| Net realised gains on financial assets |

3,786 | (4,432 | ) | |||||

| Net fair value gains through profit or loss |

13,107 | (7,460 | ) | |||||

| Net investment yield4 |

4.66 | % | 4.66 | % | ||||

| Gross investment yield5 |

5.78 | % | 3.78 | % | ||||

Notes:

| 1. | The figures for the same period of last year were adjusted on the same basis. |

| 2. | Gross investment income = Net investment income + Net realised gains on financial assets + Net fair value gains through profit or loss |

| 3. | Net investment income includes interest income from debt investments, interest income from deposits, dividend and bonus from equity investments, interest income from loans, net income from investment properties, and net income from investments in associates and joint ventures, etc. |

| 4. | Net investment yield = [(Net investment income – Interest paid for securities sold under agreements to repurchase)/((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period)/2)]/181×365 |

| 5. | Gross investment yield = [(Gross investment income – Interest paid for securities sold under agreements to repurchase)/ ((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year – Derivative financial liabilities at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period – Derivative financial liabilities at the end of the period)/2)]/181×365 |

26

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

In the first half of 2019, the Company’s net investment income was RMB72,030 million, an increase of RMB7,201 million from the corresponding period of 2018, rising by 11.1% year-on-year. Given the low interest rate environment, the Company allocated to fixed income products and high-dividend stocks in advance by catching market opportunities and its net investment yield remained stable at 4.66%. In the equity investments, the Company balanced the allocation to long-term core assets and short-term trading. Coupled with the effect of the surge in the domestic stock market in the first half of 2019, the Company’s investment income rose significantly. The gross investment income of the Company reached RMB88,923 million, an increase of RMB35,986 million from the corresponding period of 2018. The gross investment yield was 5.78%, rising by 200 BPs from the corresponding period of 2018. The comprehensive investment yield taking into account the current net fair value changes of available-for-sale securities recognized in other comprehensive income2 was 8.25%, rising by 464 BPs from the corresponding period of 20183.

| 3. | Major investments |

During the Reporting Period, there was no material equity investment or non-equity investment of the Company that was subject to disclosure requirements.

| 2 | Comprehensive investment yield = {[(Gross investment income – Interest paid for securities sold under agreements to repurchase + Current net fair value changes of available-for-sale securities recognized in other comprehensive income)/((Investment assets at the end of the previous year – Securities sold under agreements to repurchase at the end of the previous year – Derivative financial liabilities at the end of the previous year + Investment assets at the end of the period – Securities sold under agreements to repurchase at the end of the period – Derivative financial liabilities at the end of the period)/2)]/181}×365 |

| 3 | The figure of last year was adjusted on the same basis. |

27

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| III. | ANALYSIS OF SPECIFIC ITEMS |

| (I) | Profit before Income Tax |

| RMB million | ||||||||||||

| January to June 2019 |

January to June 2018 |

Change | ||||||||||

| Profit before income tax |

38,893 | 21,447 | 81.3 | % | ||||||||

| Life insurance business |

27,340 | 12,842 | 112.9 | % | ||||||||

| Health insurance business |

4,506 | 4,459 | 1.1 | % | ||||||||

| Accident insurance business |

459 | 85 | 440.0 | % | ||||||||

| Other businesses |

6,588 | 4,061 | 62.2 | % | ||||||||

During the Reporting Period, profit before income tax from the life insurance business increased by 112.9% year-on-year due to an increase in investment income. Profit before income tax from the health insurance business increased by 1.1% year-on-year primarily due to the combined impact from an increase in both investment income and claims expenses. Profit before income tax from the accident insurance business increased by 440.0% year-on-year primarily due to an increase in investment income and a decrease in claims expenses. Profit before income tax from other businesses increased by 62.2% year-on-year primarily due to an increase in the income from investments in associates and joint ventures.

| (II) | Analysis of Cash Flows |

| 1. | Liquidity sources |

Our cash inflows mainly come from insurance premiums, income from non-insurance contracts, interest income, dividend and bonus, and proceeds from sale and maturity of investment assets. The primary liquidity risks with respect to these cash inflows are the risk of surrender by contract holders and policyholders, as well as the risks of default by debtors, interest rate fluctuations and other market volatilities. We closely monitor and manage these risks.

Our cash and bank deposits can provide us with a source of liquidity to meet normal cash outflows. As at the end of the Reporting Period, the balance of cash and cash equivalents was RMB57,259 million. In addition, the vast majority of our term deposits in banks allow us to withdraw funds on deposits, subject to a penalty interest charge. As at the end of the Reporting Period, the amount of term deposits was RMB556,572 million.

Our investment portfolio also provides us with a source of liquidity to meet unexpected cash outflows. We are also subject to market liquidity risk due to the large size of our investments in some of the markets in which we invest. In some circumstances, some of our holdings of investment securities may be large enough to have an influence on the market value. These factors may adversely affect our ability to sell these investments or sell them at a fair price.

28

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| 2. | Liquidity uses |

Our principal cash outflows primarily relate to the payables for the liabilities associated with our various life insurance, annuity, accident insurance and health insurance products, operating expenses, income taxes and dividends that may be declared and paid to our equity holders. Cash outflows arising from our insurance activities primarily relate to benefit payments under these insurance products, as well as payments for policy surrenders, withdrawals and policy loans.

We believe that our sources of liquidity are sufficient to meet our current cash requirements.

| 3. | Consolidated cash flows |

The Company has established a cash flow testing system, and conducts regular tests to monitor the cash inflows and outflows under various scenarios and adjusts the asset portfolio accordingly to ensure sufficient sources of liquidity.

| RMB million | ||||||||||||||

| January to June 2019 |

January to June 2018 |

Change | Main Reasons for Change | |||||||||||

| Net cash inflow/(outflow) from operating activities |

150,290 | 44,172 | 240.2 | % | A decrease in surrender payments and maturity payments | |||||||||

| Net cash inflow/(outflow) from investing activities |

(75,908 | ) | (40,269 | ) | 88.5 | % | The needs for investment management | |||||||

| Net cash inflow/(outflow) from financing activities |

(67,937 | ) | 5,462 | N/A | The needs for liquidity management | |||||||||

| Foreign exchange gains/(losses) on cash and cash equivalents |

5 | 22 | -77.3 | % | — | |||||||||

| Net increase/(decrease) in cash and cash equivalents |

6,450 | 9,387 | -31.3 | % | — | |||||||||

29

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| (III) | Solvency Ratio |

An insurance company shall have the capital commensurate with its risks and business scale. According to the nature and capacity of loss absorption by capital, the capital of an insurance company is classified into the core capital and the supplementary capital. The core solvency ratio is the ratio of core capital to minimum capital, which reflects the adequacy of the core capital of an insurance company. The comprehensive solvency ratio is the ratio of the sum of core capital and supplementary capital to minimum capital, which reflects the overall capital adequacy of an insurance company. The following table shows the Company’s solvency ratios as at the end of the Reporting Period.

| RMB million | ||||||||

| As at 30 June 2019 (unaudited) |

As at 31 December 2018 |

|||||||

| Core capital |

864,484 | 761,353 | ||||||

| Actual capital |

899,487 | 761,367 | ||||||

| Minimum capital |

334,270 | 303,872 | ||||||

| Core solvency ratio |

258.62 | % | 250.55 | % | ||||

| Comprehensive solvency ratio |

269.09 | % | 250.56 | % | ||||

| Note: | The China Risk Oriented Solvency System was formally implemented on 1 January 2016. This table is compiled according to the rules of the system. |

As at the end of the Reporting Period, the Company’s comprehensive solvency ratio increased by 18.53 percentage points from the end of 2018, which was mainly due to a significant increase in investment income, the consistent improvement in business structure and the issuance of capital supplemental bonds.

| (IV) | Sale of Material Assets and Equity |

During the Reporting Period, there was no sale of material assets and equity of the Company.

30

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| (V) | Business Operations of Our Main Subsidiaries and Affiliates |

| RMB million | ||||||||||||||||||

| Company Name |

Major Business Scope |

Registered Capital |

Shareholding |

Total Assets | Net Assets | Net Profit | ||||||||||||

| China Life Asset Management Company Limited |

Management and utilization of proprietary funds; acting as agent or trustee for asset management business; consulting business relevant to the above businesses; other asset management business permitted by applicable PRC laws and regulations | 4,000 | 60% | 10,765 | 9,605 | 596 | ||||||||||||

| China Life Pension Company Limited |

Group pension insurance and annuity; individual pension insurance and annuity; short-term health insurance; accident insurance; reinsurance of the above insurance businesses; business for the use of insurance funds that are permitted by applicable PRC laws and regulations; pension insurance asset management product business; management of funds in RMB or foreign currency as entrusted by entrusting parties for the retirement benefit purpose; other businesses permitted by the CBIRC | 3,400 | 70.74% is held by the Company, and 3.53% is held by AMC | 5,158 | 3,716 | 264 | ||||||||||||

| China Life Property and Casualty Insurance Company Limited |

Property loss insurance; liability insurance; credit insurance and bond insurance; short-term health insurance and accident insurance; reinsurance of the above insurance businesses; business for the use of insurance funds that are permitted by applicable PRC laws and regulations; other business permitted by the CBIRC | 18,800 | 40% | 91,001 | 22,791 | 1,608 | ||||||||||||

| China Guangfa Bank Co., Ltd. |

The businesses approved by the CBIRC include commercial banking businesses such as public and private deposits, loans, payment and settlement, and capital business | 19,687 | 43.686% | 2,480,962 | 158,971 | 7,191 | ||||||||||||

Note: For details, please refer to Note 19 in the Notes to the Interim Condensed Consolidated Financial Statements in this report.

| (VI) | Structured Entities Controlled by the Company |

The details of structured entities controlled by the Company are set out in Note 19 in the Notes to the Interim Condensed Consolidated Financial Statements in this report.

| (VII) | Changes in Accounting Estimates |

The changes in accounting estimates of the Company during the Reporting Period are set out in Note 3 in the Notes to the Interim Condensed Consolidated Financial Statements in this report.

| (VIII) | Core Competitiveness |

During the Reporting Period, there was no material change in the Company’s core competitiveness.

31

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| IV. | TECHNOLOGY EMPOWERMENT, OPERATIONS AND SERVICES, RISK CONTROL AND MANAGEMENT |

| (I) | Technology Empowerment |

During the first half of 2019, the Company kicked off its 3-year action plan for the “Technology-driven China Life” initiative in all aspects by applying technology empowerment in insurance whole value chain, with a view to supporting the high-quality development.

Technology-empowered Sales Team. Through the application of technologies such as Mobile Internet and Big Data, the Company optimized and upgraded digital applications for its sales team that supported the agents in their independent marketing and real-time management of sales teams, thus contributing to the transformation and upgrade of the Company’s sales model. For the first half of 2019, the online customer acquisition grew by 18% from the corresponding period of last year, the percentage of online sales force recruitment exceeded 55.6%, and the online sales team management recorded a three-fold increase from the corresponding period of last year. With 44.57 million customers being recommended to the sales team via the intelligent platform, 30% of them purchased long-term insurance policies.

Technology-empowered Field Offices. The application of “Internet of Things” technology promoted the expansion of Internet network, addition of intelligent electronic equipment and enrichment of information services for the Company’s field offices, which accelerated the real-time interconnection between different field offices and intelligent upgrade of daily office operations. In the first half of 2019, the total capacity of network bandwidth surged by 156% from the corresponding period of last year and the number of additional intelligent equipment was 85,000 sets. With a digitalized real-time interconnected platform featured with flat structure and visualization, communications and performance tracking between departments of the Company at all levels and frontline field offices were conducted through mobile means for 24 hours. The digitalized platform also provided field offices with real-time and cross-regional day-to-day operations, such as training, morning meetings, broadcast of activities, mobile office operations, and agency services for remote operations. All these would turn the field offices across China into the digital bases of the Company for further services expansion.

Technology-empowered Operation. The application of artificial intelligence technology facilitated the intelligent upgrade of whole-chain and whole-process operation, and a new driving force was derived from technological empowerment. To date, the Company offered 21 intelligent capabilities on its artificial intelligence platform to support 32 application scenarios. In the first half of 2019, the Company constantly optimized application scenarios, including intelligent underwriting, intelligent policy administration and intelligent claims settlement, and launched a financial robot using robotic process automation (RPA), which improved operating efficiency. The Company upgraded and optimized an artificial intelligence model for risk assessment of critical illness insurance, and the accuracy rate of fraudulent claims detection through investigation increased by 32.2% from the corresponding period of last year. The Company also launched an intelligent risk control system for anti-money laundering, with which the accuracy rate of high-risk identification rose by 52.3% as compared to the corresponding period of last year.

32

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

Construction of Digital Ecosystem. With the support of a digital platform, the Company deepened internal and external cooperation to create an open and “win-win” digital ecosystem. On the one hand, the Company consistently enriched the internal ecosystem. For the first half of 2019, the Company created more than 70 innovative applications; 1,076 applications were launched on the platform cumulatively and over 280 application and data services were made available for use on the platform, thus consistently enhancing the technology-empowered ecosystem. On the other hand, the Company actively integrated with the external ecosystem. By launching the application named “Shanghu Bao” on the digital platform, the Company has currently cooperated with 4,180 business partners in the way that the Company provided insurance products and platforms, whereas its business partners provided sales scenarios and customers.

| (II) | Operations and Services |

By adhering to the “customer-oriented” approach and concentrating on local branches and field offices, the Company focused on strengthening service quality and technology-driven development, and improved efficiency of operations and services as well as customer experience, with a view to vigorously driving the Company towards high-quality development.

Insurance product supply was constantly enriched. In the first half of 2019, for satisfying the demands of its customers, the Company developed a total of 46 new insurance products, including 11 life insurance products, 18 health insurance products, 14 accident insurance products and 3 annuity insurance products. Out of these new products, 42 were protection-oriented products and 4 were long-term savings products.

Customer experience was continuously improved with efficiency of operations enhanced significantly. In the first half of 2019, the Company further upgraded its operations and services by constantly promoting intensive, intelligent and ecological operations and services. Services became more accessible. Through the multi-media Customer Contact Center or a portal of China Life Insurance APP, customers could easily access to a variety of services provided by CLP&C, Pension Company, China Guangfa Bank Co., Ltd. and AMP. The number of online registered users of China Life Insurance APP was over 67 million, with the monthly average number of active users increasing by 52%. The Company also launched a new one-stop enquiry service in relation to 14 types of customers’ rights and interests and a new one-click sales appointment. Services were more convenient and efficient. The Company constantly improved online services, with the utilization rate of paperless insurance application in the exclusive individual agent channel reaching 96%. The rate of automatic claims settlement rose by more than 30 percentage points as compared to that of 2018, and time required for making claims payment was shortened by 37% year-on-year. The Company also launched the service of “Claims Settlement for Critical Illness within One Day”. It consistently developed the service of 5-waiver direct claims payment which allowed the settlement of insurance benefits immediately following the discharge from hospitals, and the number of cooperating medical institutions was over 10,000. Services became smarter. The Company consistently improved differentiated underwriting policies and enhanced the application of artificial intelligence technology, with the rate of intelligent underwriting increasing by 8.7 percentage points year-on-year. The Company upgraded services provided by the “Intelligent Customer Service Robot” by launching voice services, with the number of intelligent customer services performed amounting to 23.4371 million. The Company also upgraded the service of “Intelligent Protection Estimate” to customize insurance protection plans for customers on family basis. Services were more caring. The Company further improved its VIP service system, widely promoted the “Five Exclusive VIP Services”, continuously expanded and upgraded the ecological services such as “Insurance + Sports”, “Insurance + Health”, and “Insurance + Rescue”, and continuously organized activities including “Little Painters of China Life”, “China Life 700 Running”, and “Health Hiking”, with the number of offline activities amounting to 2,371 and the number of customers actively participating such activities reaching 2.28 million. The Company further launched a number of featured VIP services, including domestic medical care advice, critical illness fast-track and global emergency assistance, etc.

33

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

In addition, the Company continuously promoted the implementation of the “Inclusive Healthcare Service” and “Integrated Aged-care” strategy, actively consolidated the resources of healthcare and medical services that covered all life cycles, accelerated the construction of an online platform for healthcare management services, and continuously pushed forward the development of an offline medical and healthcare resources network, so as to satisfy customers’ diversified needs for healthcare services. The Company also actively created an innovative model for the cooperation between medical care and insurance protection, and promoted application of the claims settlement model that integrated government and businesses in the form of “basic medical insurance + supplemental major medical expenses insurance + commercial insurance”. The Company will constantly promote the development and operation of the “Integrated Aged-care” projects, and actively explore pension investment models and investment layout to facilitate the integration of medical care and aged care services and to enhance the quality of aged care services.

| (III) | Risk Control and Management |

The Company consistently strengthened its efforts on internal control and risk management in strict compliance with the laws and regulations of its listed jurisdictions, as well as regulatory provisions and requirements, for the purpose of consolidating the line of defense against risks. Actively adapting to the new development of regulatory environment, the Company organized and carried out various risk investigations and rectification exercises. It consistently improved the risk management system of “China Risk Oriented Solvency System” (C-ROSS) and continuously updated the relevant work mechanisms, with its integrated risk rating maintaining at a satisfactory level. Benefiting from applicable theories and experiences in or outside China and taking into account the characteristics of the insurance industry, the Company explored new models for risk prevention and control in relation to unlawful funds raising and put more efforts on promotion and risk investigations, which enhanced the effects of risk management and control. The Company also optimized its ex-ante, halfway and ex-post system of sales risk management and promoted the application of the pre-warning system of sales risks. It constantly pushed forward the establishment of the internal control system and the assessment on and inspection of internal control for the purpose of enhancing the effectiveness of the internal control mechanism. The Company strengthened internal control and operation policies for anti-money laundering, launched a pilot program of the application of the anti-money laundering intelligent verification platform, and innovatively created the models of intelligent identification and intelligent verification with respect to insurance business, so that its ability to prevent and control the risk of money laundering was enhanced. The Company also strengthened compliance management, improved the compliance management system and its efficiency, with a view to promoting its standardized management and compliant operation. The Company further strengthened the organization and management of the internal audit, actively exerted the supervision and services functions of internal audit, carried out the tasks such as economic responsibility audit and the audit on assets and liabilities management system. With a focus on its strategic objectives, the Company conducted special audits to support its in-depth reforms. The Company continuously stepped up its efforts on the application of audit results and strengthened rectification exercises, thus further contributing to the healthy development of the Company.

34

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| V. | PERFORMANCE OF THE CORPORATE SOCIAL RESPONSIBILITY |

The Company adhered to its culture philosophy of “Success for You, Success by You”, and attached great importance to fulfilling its social responsibility. It actively probed into a business mode that balanced the development of itself and the society, and strived to improve people’s livelihood and promote social equity in aspects of aged care, medical services, social assistance and education, with a view to making contributions to the national economy and social development while achieving high-quality development of its own.

| (I) | Leveraging the advantage of insurance business to protect people’s livelihood. |

The Company gave priority to the people’s livelihood, and took various measures to strengthen people’s livelihood protection network. Through participating in micro-insurance business, insurance for the aged, maternity insurance, supplementary major medical expenses insurance, etc, the Company provided effective support to the development for a moderately prosperous society in all respects. In the first half of 2019, the Company provided micro-insurance protection for over 70 million people, the elderly accident injury insurance protection for over 34 million aged people and the risk coverage for nearly 15 million families with childbirth plans. The Company also provided the supplementary major medical insurance protection for nearly 400 million urban and rural residents, the long-term care insurance protection for more than 10 million people, and the supplementary medical insurance protection for social security for nearly 20 million people. It undertook over 500 medical insurance administration projects, covering nearly 100 million people.

| (II) | Carrying out public welfare programs consistently and shouldering its due social responsibilities. |

The Company kept “supporting public benefit, promoting social harmony and development” as its tenet, actively shouldered its social responsibilities, and strove to repay the society. In the first half of 2019, the Company donated RMB37,459,700 through China Life Foundation for targeted poverty alleviation. The Company also rolled out the “Green Life” project and the “Blessing for Growth” project to provide major illness relief for the juveniles living in poverty. The Company continually supported orphans from Wenchuan, Ludian and Yushu earthquakes as well as those from Zhouqu mudslide.

| (III) | Adhering to green culture in operations and advocating green environmental protection. |

Being a non-manufacturing insurance company with low energy consumption and light pollution, the Company greatly promoted green building and green offices in its daily operations. Committed to the development and application of new technologies, the Company continuously developed intelligent and mobile service networks, expanded online service channels and vigorously carried out electronic and paperless office operations to reduce resources consumption and carbon emissions during its operations. The Company exerted great efforts to reducing the waste of paper generated from the traditional operation process in insurance industry. As at 30 June 2019, the Company processed 22.27 million policy administration services through online channels, accounting for 62.11% of the total business volume. Through developing online services, the Company reduced the paper used at service counters which saved approximately 178 tons of paper. In addition, the Company consistently promoted green environmental protection, encouraging its employees and customers to participate in the “Earth Hour” activity to increase the awareness of energy conservation and emission reduction.

35

Table of Contents

China Life Insurance Company Limited ● 2019 Interim Report

Management Discussion and Analysis (continued)

| (IV) | Targeted poverty alleviation |

| 1. | Targeted poverty alleviation plan |