EXHIBIT 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

OPERATIONS AND FINANCIAL CONDITION

FOR THE THREE AND NINE MONTHS ENDED SEPTEMBER 30, 2020

CONTENTS

| Page | ||||||||

| 1: | Highlights and Relevant Updates | |||||||

| 2: | Core Business, Strategy and Outlook | |||||||

| 3: | Review of Financial Results | |||||||

| 4: | Operating Segments Performance | |||||||

| 5: | Construction, Development and Other Initiatives | |||||||

| 6: | Exploration | |||||||

| 7: | Financial Condition and Liquidity | |||||||

| 8: | Economic Trends, Business Risks and Uncertainties | |||||||

| 9: | Contingencies | |||||||

| 10: | Critical Accounting Policies and Estimates | |||||||

| 11: | Non-GAAP Performance Measures | |||||||

| 12: | Disclosure Controls and Procedures | |||||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF OPERATIONS AND FINANCIAL CONDITION

This Management’s Discussion and Analysis of Operations and Financial Condition ("MD&A") should be read in conjunction with Yamana Gold Inc.'s (the "Company" or "Yamana") condensed consolidated interim financial statements for the three and nine months ended September 30, 2020, and the most recently issued annual Consolidated Financial Statements for the year ended December 31, 2019, ("Consolidated Financial Statements"). (All figures are in United States Dollars ("US Dollars") unless otherwise specified and are in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board.

The Company has included certain non-GAAP financial measures, which the Company believes, that together with measures determined in accordance with IFRS, provide investors with an improved ability to evaluate the underlying performance of the Company. Non-GAAP financial measures do not have any standardized meaning prescribed under IFRS, and therefore they may not be comparable to similar measures employed by other companies. The data is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. The non-GAAP financial measures included in this MD&A include:

•Cash costs per gold equivalent ounce ("GEO") sold;

•All-in sustaining costs ("AISC") per GEO sold;

•Net debt;

•Net free cash flow;

•Average realized price per ounce of gold/silver sold; and

•Average realized price per pound of copper sold.

Reconciliations and descriptions associated with the above performance measures can be found in Section 11: Non-GAAP Performance Measures in this MD&A.

Cautionary statements regarding forward-looking information and mineral reserves and mineral resources can be found in Section 11: Disclosure Controls and Procedures in this MD&A.

MANAGING COVID-19

Since the emergence of the global COVID-19 pandemic, the Company’s crisis response team, the members of which are its senior executives and operational leaders, have taken quick and decisive action to respond to the pandemic during a fluid and fast-moving environment. The Company has adjusted and managed its business effectively during this period, mitigating risks and further advancing opportunities, while ensuring the safety of employees, contractors and the communities in which it operates. In the third quarter, the Company saw its costs incurred in association with COVID-19 decrease and despite the ongoing challenges, was able to achieve impressive throughput rates at many of its operations and increase production guidance for 2020.

Although the Company has been able to maintain COVID-19-free mine sites, there have been confirmed employee cases in the communities surrounding the Company's operations. However, with the implementation of monitoring, testing, quarantine and contact tracing protocols, the Company has been able to isolate incidents of infection and limit their spread. Overall, the number of infected persons is not significant and everyone initially infected has recovered. Since early September, the number remaining in quarantine has declined considerably.

The Company will continue to manage its business in a way that respects, and is mindful of, the impact that COVID-19 has had and could have on local communities. The Company has endeavoured to manage its operations with the safeguarding of individuals at site and in local communities in mind. Numerous protocols have been adopted to ensure that the safety and health of employees and persons in local communities is maintained. The Company has had the assistance of a team of International SOS doctors at all South American sites in order to review and validate the Company’s COVID-19 protocols. These reviews found that the Company’s operations were doing extremely well in preventing the contagion and spread of COVID-19 at sites.

The Company has actively responded to the global COVID-19 pandemic through a variety of means, such as:

•Working with local communities to develop and implement local crisis management plans;

•Implementing heightened levels of health screening and where cases are potentially revealed, isolation and support to workers who may have been exposed;

•Donating face masks, hand sanitizer, medical equipment and other critical supplies, and making site medical teams available to support ambulances and local health officials in the communities in which the Company operates;

•Transferring beds and supplies from camps to temporary hospitals, and working alongside local NGOs and small businesses to shift production to manufacturing masks for local community members and employees;

•Building up the capacity of local health clinics to be able to effectively manage community COVID cases, including the purchase of respirators, testing equipment, computers and other critical equipment;

•Donating, and anticipating to donate, hundreds of thousands of dollars in support of communities moving forward.

| 1Yamana commends the remarkable dedication, commitment, professionalism, and compassion of its employees, contractors and suppliers, who have come together in these challenging times to drive success.

For further details on how the Company has actively responded to the global COVID-19 pandemic, please refer to 1. Highlights and Relevant Updates - Health, Safety, Environment and Corporate Responsibility.

1. HIGHLIGHTS AND RELEVANT UPDATES

For the three months ended September 30, 2020, unless otherwise noted

•Above plan gold production of 201,772 ounces, following standout performances from Jacobina, Canadian Malartic, El Peñón and Minera Florida.

•Above plan silver production of 3,040,341 ounces, underpinned by an exceptionally strong performance from El Peñón, which greatly exceeded plan with mine sequencing favouring mining of higher silver grade zones.

•Gold Equivalent Ounce ("GEO") production of 240,466 ounces exceeded plan as a result of strong gold and silver production.

•With overall production, and production at most of the Company’s mines, currently tracking ahead of plan, and in some cases well ahead of plan, the Company increased its 2020 production guidance to 915,000 GEO from the previous guidance of 890,000 GEO, representing an increase of 3%. Gold production and silver production guidance have increased from previous guidance by approximately 1% and 6%, respectively.

•Mine operating earnings of $157.3 million exceeded plan, and increased by $75.5 million or 92%, in relation to the comparative prior year quarter, despite the impact of COVID-19 in the current year. Strong operational performance from Jacobina, El Peñón, and Canadian Malartic and strong precious metal prices contributed to strong mine operating earnings.

•Net earnings of $55.6 million or $0.06 per share basic and diluted, compared to $201.3 million or $0.21 per share basic and diluted for the three months ended September 30, 2019. Adjusting items of $37.3 million, that management believes may not be reflective of current and ongoing operations, and which may be used to adjust or reconcile input models in consensus estimates, reduced earnings for the current period. Adjustments in the current period include $8.6 million of costs incurred in association with COVID-19-related temporary suspensions, standby and other incremental costs at certain operations. Prior year net earnings benefited from a one-time $273.1 million gain from a divestiture. For a complete list of adjustments, refer to Section 3: Review of Financial Results.

•Strong cash flows from operating activities of $215.0 million and cash flows from operating activities before net change in working capital(i) of $199.0 million reflect the impact of strong production, strong precious metal prices and the positive impact of foreign exchange on the costs of the Company. If adjusted for margins associated with the sales of Barnat pre-commercial production of approximately $13.5 million which are disclosed as a credit to expansionary capital and investing cash outflows, and for the $8.6 million of costs incurred in association with COVID-19, normalized cash flows from operating activities and normalized cash flows from operating activities before net change in working capital(i) would have been approximately $237.1 million and $221.1 million, respectively. Cash flows from operating activities are at multi-year highs, which include periods with considerably more production from mines that have since been divested or discontinued.

•The Company generated net free cash flow(i) of $185.5 million, compared to net free cash flow(i) of $89.5 million in the comparative prior year quarter, representing a 107% increase. The change is driven largely by strong gross margins, along with lower interest and other finance expenses in the period associated with lower levels of long term debt.

•To ensure consistency of and prospects for cash flows, the Company compares cash flows in a particular quarter with the average of cash flows in the preceding three quarters. This measure is looked at on a rolling basis quarter over quarter. Continuing with a recent trend, cash flows from operating activities and net free cash flow(i) for the quarter exceeded the averages of such cash flows for the preceding three quarters by 52% and 103% respectively, thereby further demonstrating the strength and resilience of the cash flow generation capacity of the Company.

•As at September 30, 2020, the Company had cash and cash equivalents of $474.2 million, an increase of $149.4 million from June 30, 2020. The Company has sufficient cash on hand and liquidity through its current balances and incoming cash flows to fully manage its business and fund growth without having to borrow. This includes, but is not limited to obligations related to the Jacobina plant expansions, development of the Odyssey underground project at Canadian Malartic, generative exploration, development of the integrated Agua Rica and Alumbrera project, and further balance sheet improvements, while having excess funds to dedicate to possible other opportunities and dividend increases.

| 2•Net debt(i) decreased by $148.9 million in the quarter to $619.1 million, which advances the Company's objective of achieving a positive net cash(i) position, which is now well ahead of schedule. The Company expects to continue generating strong cash flows, and net free cash flow(i) in particular, in the fourth quarter, with a further reduction to net debt. The Company's next scheduled debt repayment is in 2022 which will be repaid in full rather than refinanced. The Company expects to be in a position by year-end 2020 to achieve its balance sheet management objective of maintaining a leverage ratio of net debt to EBITDA(i) of below 1.0x when assuming a bottom-of-cycle gold price of $1,350 per ounce, underscoring the Company’s significant financial flexibility and best-in-class balance sheets.

•On October 23, 2020, the outstanding $100.0 million of the Company's $750.0 million credit facility was repaid, following strong third quarter operational results, and increased liquidity and financial flexibility. This follows the repayment of the initial $100.0 million in June, of the $200.0 million drawn during the first quarter of 2020 as a precaution due to the uncertainty around COVID-19.

•Combined with modest near to mid-term capital requirements for the Company, the substantive improvement in the balance sheet has provided the flexibility to continue returning capital to shareholders through measured and sustainable dividend increases.

•Subsequent to quarter end, on October 7, 2020, the Company increased its annual dividend by a further 50% to $0.105 per share, for shareholders of record at the close of business on December 31, 2020. At the new rate, the dividend will be 425% higher than the rate just 18 months ago. The Company had previously established a policy of representing the dividend on a per GEO basis, with the objective of maintaining the dividend of between $50 to $100 per GEO, and this increase positions the dividend at the high end of the range, at $100 per ounce. In the quarter, the Company modified its dividend policy such that it will no longer provide a range for its dividend on a per GEO basis, with future dividend increases above the new floor of $100 per GEO based entirely on the cash flow and cash generation capacity of the Company. As its cash flows and cash balances increase, its dividend will rise correspondingly as a percentage of cash flows and commensurate with increasing cash balances from cash flows and sources that supplement cash flows. With current levels of cash on hand, the Company would have sufficient available funds to fund its business and pay the new current dividend for several years independently of gold price. For further information on the Company's approach to maximizing cash returns to shareholders, refer to Section 2: Core Business, Strategy and Outlook.

•The Company balances two additional capital allocation priorities in addition to paying, maintaining and increasing dividends, which are balance sheet management and pursuing and funding growth. In the context of growth, the Company pursues growth that is measured and consistent with the Company’s size, scale and financial resources. Opportunities for growth should meet the Company's minimum requirements that they should be funded through internal resources, meet minimum return levels that well exceed cost of capital and be of a specific size. In terms of size, opportunities should have mineral reserves and resources of at least 1.5 million ounces, which the Company considers large enough to support a mine plan with annual gold production of approximately 150,000 ounces for at least eight years. The Company does not categorize opportunities based on their size alone nor tier assets into various categories. The objective is to deliver robust returns, significant cash flows and accelerated payback. While the Company has a large portfolio of prospective and advancing exploration and development opportunities that will provide it with measured growth, as an extension of the strategy, the Company will consider the acquisition of earlier stage exploration and development opportunities, particularly where the Company can provide added value either through its regional presence, expertise or both. For full details on the Company's investment strategy, please refer to Section 2: Core Business, Strategy, and Outlook.

•Subsequent to quarter end, on October 13, the Company completed its listing and began trading on the Main Market of the London Stock Exchange ("LSE"). This adds another senior exchange for trading of the Company's shares, and will further improve institutional investments and liquidity. For more information, please see the press release issued October 13, 2020, 'Yamana Gold is Admitted to Trading on the London Stock Exchange', available on the Company's website at www.yamana.com.

Strategic developments, construction developments and advanced stage projects:

•Agua Rica Feasibility Study Advancement and Integration Agreement

◦The Company continued to advance the integration of Agua Rica with Minera Alumbrera Limited ("Alumbrera") pursuant to the 2019 integration agreement entered into by the Company, Glencore International AG and Newmont Corporation (collectively the “Parties”), whereby the Agua Rica project would be developed and operated using the existing infrastructure and facilities of Alumbrera. The integration gives the Company 56.25% ownership in the joint Agua Rica and Alumbrera project ("Integrated Project"), which carries significantly less development risk, as certain infrastructure would not need to be constructed.

◦The integration is expected to be completed in the fourth quarter, after which the Integrated Project would be managed as a combined operation. In addition to the considerable infrastructure, tailings system and processing plant available, there is also significant cash in the treasury at Alumbrera.

| 3◦The Parties established a technical committee ("Technical Committee") which is now advancing a full Feasibility Study of the Integrated Project, with updated mineral reserve, production and project cost estimates. COVID-19 introduced uncertainty into the timeline relating to the completion of the Feasibility Study, mainly due to environmental permit approvals and field work, although as the permit process is well advanced, work preparation has begun in anticipation of receiving necessary authorizations in normal course. Nonetheless, the results of the Feasibility Study are expected during 2021.

◦After a strategic review, the Company has concluded that Agua Rica represents an excellent development and growth project which the Company intends to continue to advance through the development process through the Company's controlling interest in the project.

•Jacobina Optimization Project

◦The Phase 1 optimization project, whose objective was to stabilize throughput at a sustainable 6,500 tpd, was completed in June of 2020. The project has exceeded expectations, with a higher than planned steady state of approximately 6,800 tpd achieved in both the second and third quarters. The Company has identified opportunities to further optimize the results and recoveries achieved in Phase 1 with a modest investment. Consequently, works commenced in the third quarter for the expansion of the gravity concentration circuit, with commissioning scheduled for mid-2021 and with an objective to optimize gold recovery at the higher throughput rate.

◦In addition to the incremental optimization of Phase 1, the Company is studying the increase in throughput to 8,500 tpd, referred to as the Phase 2 optimization. A pre-feasibility study for Phase 2 was completed in the second quarter with positive results. The throughput increase is expected to be achieved through the installation of an additional grinding line and incremental upgrades to the crushing and gravity circuits. If implemented, the Phase 2 expansion is expected to increase annual gold production to approximately 230,000 ounces per year, reduce costs, and generate significantly more cash flow and attractive returns.

◦The Company is currently working on the Phase 2 feasibility study, scheduled for completion in mid-2021. However, it is the Company's intention to optimize and stabilize the operation at the new milling rate resulting from the optimization of Phase 1, before proceeding to Phase 2.

◦Separately, Jacobina is studying the installation of a backfill plant to allow up to 2,000 tpd of tailings to be deposited in underground voids. Preliminary results indicate that the project has the potential to improve the way in which the Company manages the environment and environmental impact, extend the life of the existing tailings storage facility, and improve mining recovery, resulting in an increased conversion of mineral resources to mineral reserves. The Company is advancing the backfill project to a feasibility study, to be completed in early 2021.

◦Considerable technical work which supports the viability of the Phase 2 expansion has already been completed, and the Company intends to advance the project following the requisite completion of its Feasibility Study required for the finalization of permitting, which is already underway. Capital costs for the Phase 2 expansion from the May 2020 pre-feasibility study are estimated at $57 million, based on an assumed BRL:USD rate of 4.0. The BRL:USD foreign exchange rates are currently higher than 5.5, and consequently, the Company anticipates that the weaker rates will provide capital cost and operating cost benefits.

•Canadian Malartic Exploration Ramp into Odyssey and East Malartic

◦The Company continues to advance studies related to the underground project at Canadian Malartic, and the main focus of exploration during the third quarter was to provide support for an aggressive infill drill program at East Gouldie, where twelve diamond drill rigs completed 38,000 metres, designed to expand the mineral resource envelope with a 150 metre drill spacing. These twelve drill rigs are employed to define and expand underground mineral resources, with a target to complete 112,000 metres of definition drilling by year end. The drilling has established 44 new pierce points in a mineralized body 1,400 metres long and that extends from 700 metres below surface to 1,900 metres below surface. The pierce points include multiple stacked intercepts in two closely spaced parallel zones, East Gouldie North and South. A thirteenth drill rig is completing a vertical geotechnical drill hole in the area of a proposed shaft to access the mineralized zone. The Company and its partner have started the construction of surface infrastructure and an exploration ramp into Odyssey and East Malartic, with the purpose of eventually mining their respective upper zones and providing further exploration access to allow drilling in tighter spacing to continue studies to a greater detail. The new ramp will also provide the ability to carry out bulk sampling of up to 40,000 tonnes of ore. With governmental approval already in hand, construction of surface infrastructure and the portal in preparation for development of the ramp started in August of 2020, with a budget of C$6.0 million for 2020 on a 50% basis. The objective is to commence development of the ramp in the fourth quarter, which is anticipated to take approximately two years to complete.

For full details on the aforementioned updates, please refer to Section 5: Construction, Development and Other Initiatives.

(i)A cautionary note regarding non-GAAP performance measures is included in Section 11: Non-GAAP Performance Measures.

OPERATING

| 4GEO production was 240,466 ounces and exceeded plan and prior year production of 236,852 ounces. Catalysts included standout gold production performances from Jacobina, Canadian Malartic, El Peñón and Minera Florida and strong silver production performance from El Peñón, which greatly exceeded plan. GEO assumes gold ounces plus the gold equivalent of silver ounces using a ratio of 79.26 for the three months ended September 30, 2020, and 86.79 for the three months ended September 30, 2019. GEO calculations are based on an average realized gold to silver price ratio for the relevant period.

Third quarter unitary total cost of sales and cash costs(iii) were $1,186 and $723 respectively, relatively consistent with $1,148 and $674 in the comparative 2019 period, once production levels are considered. AISC(iii) for the three months ended September 30, 2020 were $1,096 per GEO sold, compared to $1,037 per GEO sold in the comparative period. Total cost of sales, cash costs(iii) and AISC(iii) were in line with those observed in the second quarter.

Third quarter unitary cash costs remained consistent with second quarter costs, as secondary development ramped up in the third quarter commensurate to the increase in production, therefore maintaining a similar cost per ounce structure. For the fourth quarter, the Company anticipates that total secondary development costs will remain relatively constant which, on the expectation that the fourth quarter is usually the strongest production quarter of the year, will decrease the cost per ounce.

With sustaining capital deferrals in the second quarter while certain operations ramped up from temporary suspensions due to COVID-19 restrictions, third quarter sustaining capital increased as expected, and resulted in an increase in AISC(iii) in the quarter over the comparative period. The higher planned capital expenditures per ounce were partially offset by strong performances from Jacobina, El Peñón, and Canadian Malartic. Further, costs were positively impacted by foreign exchange as a result of currencies in all jurisdictions in which the company operates being weaker against the US Dollar during the three months ended September 30, 2020, compared to the same quarter of 2019. Additionally, due to further delays associated with COVID-19, certain capital expenditures and sustaining exploration costs have been deferred and are therefore expected to impact fourth quarter AISC.

| For the three months ended September 30, | For the nine months ended September 30, | |||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||

GEO | ||||||||||||||

Production (i)(ii) | 240,466 | 236,852 | 645,795 | 715,856 | ||||||||||

Sales (i)(ii) | 230,452 | 237,772 | 629,565 | 732,102 | ||||||||||

Per GEO sold data (ii)(iii) | ||||||||||||||

Total cost of sales (iv) | $ | 1,186 | $ | 1,148 | $ | 1,159 | $ | 1,151 | ||||||

Cash costs (iii) | $ | 723 | $ | 674 | $ | 710 | $ | 687 | ||||||

AISC (iii) | $ | 1,096 | $ | 1,037 | $ | 1,082 | $ | 995 | ||||||

Gold and silver production for the quarter was as follows:

| For the three months ended September 30, | For the nine months ended September 30, | |||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||

| Gold | ||||||||||||||

Production (ounces) (i)(ii) | 201,772 | 208,152 | 558,150 | 626,434 | ||||||||||

Sales (ounces) (i)(ii) | 192,578 | 209,542 | 541,531 | 638,537 | ||||||||||

| Per ounce data | ||||||||||||||

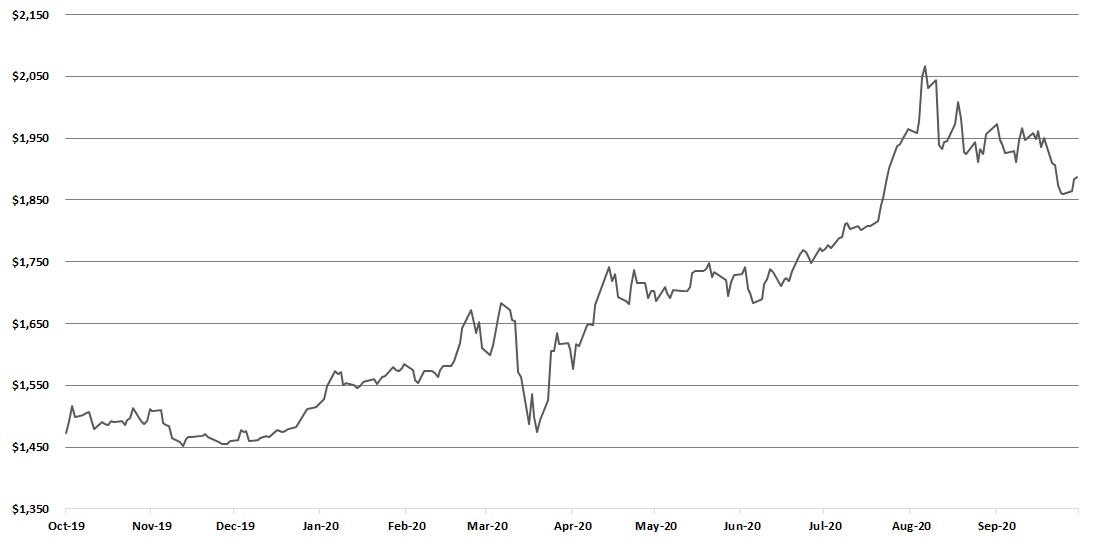

| Revenue | $ | 1,910 | $ | 1,481 | $ | 1,739 | $ | 1,361 | ||||||

Average Realized Price (iii)(v) | $ | 1,910 | $ | 1,473 | $ | 1,739 | $ | 1,356 | ||||||

Average market price (vi) | $ | 1,911 | $ | 1,474 | $ | 1,735 | $ | 1,363 | ||||||

| Silver | ||||||||||||||

Production (ounces) | 3,040,341 | 2,484,155 | 7,779,001 | 7,672,289 | ||||||||||

Sales (ounces) (vii) | 2,907,348 | 2,437,575 | 7,818,919 | 8,073,879 | ||||||||||

| Per ounce data | ||||||||||||||

| Revenue | $ | 24.58 | $ | 17.73 | $ | 20.16 | $ | 15.98 | ||||||

Average Realized Price (iii)(v) | $ | 24.58 | $ | 17.10 | $ | 19.92 | $ | 15.81 | ||||||

Average market price (vi) | $ | 24.39 | $ | 17.02 | $ | 19.22 | $ | 15.83 | ||||||

With production at most of the Company’s mines currently tracking ahead of plan, the Company has increased guidance for the year to 915,000 GEO. The Company provides in this MD&A a discussion on revised guidance in Section 2: Core Business, Strategy and Outlook.

(i)Included in the three and nine months ended September 30, 2020 gold production figures include 13,305 and 18,929, respectively, of pre-commercial production, related to the Company's 50% interest in the Canadian Malartic mine's Barnat deposit. Pre-commercial production ounces are excluded from

| 5sales figures, although pre-commercial production ounces that were sold during their respective period of production had their corresponding revenues and costs of sales capitalized to mineral properties.

(ii)Comparative period GEO and gold figures exclude contributions from the Chapada mine, which was divested in July 2019. Production figures for the three and nine months ended September 30, 2019 exclude 1,771 and 52,311 ounces, respectively. Sales figures for the three and nine months ended September 30, 2019 exclude (335) and 49,738 ounces, respectively, net of quantity adjustments.

(iii)A cautionary note regarding non-GAAP performance measures is included in Section 11: Non-GAAP Performance Measures.

(iv)Cost of sales consists of the sum of 'cost of sales excluding Depletion, Depreciation and Amortization' ("DDA") plus DDA.

(v)Realized prices based on gross sales compared to market prices for metals may vary due to the timing of the sales.

(vi)Source of information: Bloomberg.

(vii)Included in three and nine months ended September 30, 2020 silver sales ounces are 158,591 and 732,514 ounces, respectively, delivered under the silver streaming arrangement (2019: 300,000 and 544,200, respectively).

HEALTH, SAFETY, ENVIRONMENT AND CORPORATE RESPONSIBILITY

Health, safety, environment and community relations ("HSEC") programs are integrated into all our operations. Yamana recognizes the importance of striving to meet and exceed its corporate social responsibility objectives and the role these efforts have in delivering on the overall objective of creating value for all stakeholders.

The Company has actively responded to the global COVID-19 pandemic. The Company activated its crisis response team in the early phases of the COVID-19 outbreak, the members of which are the senior executives and operational leaders, to ensure it was in a position to take quick and decisive action in what remains a fluid and fast-moving environment. Some of the decisions and actions undertaken include:

•Temporarily restricting all employee travel and shifting to remote work arrangements at corporate and regional offices.

•Restricting visitors to the Company's mines.

•Increased screening procedures, including questionnaires, temperature checks and in some cases rapid testing, for anyone seeking entry into a mine.

•Mandatory social distancing, including staggered meal times and shift changeovers to minimize the flow of people and facilitate rigorous social distancing.

•Increased cleaning and disinfecting procedures at all mines and offices.

•Increased support staff at on-site medical clinics at the Company's mines as a precautionary measure.

•Regular communications with medical experts and government authorities in every country where Yamana operates to ensure it has the proper precautions in place to protect the health and safety of its employees, families, and communities.

•Regular and active discussions with employees and union representatives to ensure they have input into health and safety precautions being implemented and that these measures and the reasons for them are well understood.

•Development of a detailed plan for a phased return to the Corporate and Regional offices.

•Working with local communities to develop and implement local crisis management plans.

Although the Company has been able to maintain COVID-19-free mine sites, there have been confirmed employee cases in the communities surrounding the Company's operations. However, with the implementation of monitoring, testing, quarantine and contact tracing protocols, the Company has been able to isolate incidents of infection and limit their spread. The protocols implemented by the Company included contact tracing which allow each operation to rapidly identify any persons who may have come into contact with an individual who may have been infected, and to isolate and quarantine those persons, thereby limiting the spread of the infection. The individuals and those who have been in contact with the confirmed cases were placed in in self-isolation. If at any point the Company determines that continuing operations poses an increased risk to its workforce or local communities, the Company will reduce operational activities up to and including care and maintenance and management of critical environmental systems. While the number of persons in quarantine has not been significant, representing only a small portion of the workforce as aforementioned, everyone initially infected has recovered. Since early September, the number remaining in quarantine has declined considerably.

Yamana has been deeply committed to supporting its host communities throughout the COVID-19 crisis, with a wide range of initiatives including, but not limited to, the donation of thousands of facemasks, hand sanitizers, medical equipment and other critical supplies. In Chile and Brazil, the Company has made site medical teams and/or ambulances available to support local health officials on the front lines. In Argentina, the Company is working with officials to transfer more than 80 beds and other supplies from the Cerro Moro camp to a temporary hospital, which has been established as a contingency for treating any future local COVID-19 patients. And in Brazil, the Company has worked with local NGOs and small businesses to help shift their production from clothing to production of masks for employees and local community members. In Canada, Yamana has donated $150,000 to St. Joseph’s Hospital for their COVID-19 efforts, as well as $20,000 to each of Foodbanks Canada and Conquer COVID-19 Canada. In addition, Canadian Malartic has donated a sum of $30,000 to various community organizations focusing on food aid and other support services for community members. These are just a few examples of the efforts that the Company's operations are making to support the communities where it operates, with hundreds of thousands of dollars being allocated to the setting up of support funds for communities in the coming weeks and months.

Other recent highlights relating to HSEC are as follows:

•The Company's Total Recordable Injury Frequency Rate was 0.40(i) after the third quarter of 2020.

| 6•The Company’s Social License to Operate Index demonstrated an overall increase of 11% in trust across our operations during the third quarter of 2020. Evidence shows that the mine's COVID-19 response and engagement is a significant contributor to this improvement.

•The Company began a transition to more long term digital engagement with local communities in Q3 2020. This is in response to the challenges raised by more traditional engagement methods in the wake of COVID-19 due to social distancing restrictions. This initiative will help identify and develop appropriate technologies and strategies in order to ensure consistently open lines of communication with communities.

•The Company’s Jacobina mine was named one of the “10 Best Places to Work in Bahia” by The Great Place to Work Institute.

•In September, Canadian Malartic Mine received two awards; The first award, the F.J. O'Connell Trophy in the Surface, transportation and primary metal processing operations category for 2019, from the Quebec Mining Association was a result of improvements in the mine’s Health and Safety record compared to the industry average. The second was the “Sustainable Development and Environment” award from the Val-d’Or Chamber of Commerce.

(i)Calculated on 200,000 hours and includes employees and contractors.

FINANCIAL

For the three months ended September 30, 2020

Net earnings for the three months ended September 30, 2020 were $55.6 million or $0.06 per share basic and diluted, compared to net earnings of $201.3 million or $0.21 per share basic and diluted for the three months ended September 30, 2019. Earnings for the three months ended September 30, 2020 were negatively impacted by $37.3 million of items that management believes may not be reflective of current and ongoing operations and which may be used to adjust or reconcile input models in consensus estimates. Significant and unusual adjusting items in the quarter include:

•A $4.2 million loss on the revaluation of the Company's monetary assets and liabilities, owing to movements in local currencies in multiple jurisdictions where the Company operates;

•A $5.1 million loss on the mark-to-market of the Company's outstanding equity instruments related to share-based payments in association with Performance Share Units and Deferred Share Units, resulting from an increase in share price;

•An $8.6 million expense, representing costs incurred by the Company as a result of COVID-19-related temporary suspensions, standby or reductions at certain operations, and direct incremental costs associated with operating under COVID-19 related restrictions. Costs were incurred predominantly at Cerro Moro due to government imposed restrictions on activity, and also in Chile and Brazil due to health authority regulations for temporary workforce reductions, and/or to promote social distancing;

•$8.7 million of non-cash tax losses on unrealized foreign exchange gains and $12.8 million of tax losses on non-routine transactions and adjustments.

For a full listing of reconciling items between net earnings and adjusted net earnings for the current and comparative period, refer to Section 3: Review of Financial Results.

The aforementioned $8.6 million in COVID-19 related costs can be divided into two major categories:

•Temporary suspension and standby costs, including those associated with placing certain mines in care and maintenance and subsequent ramp-up of those operations, and the underutilization of labour and contractors in relation to the pre-COVID mine plans, and

•Other incremental costs resulting from COVID-19 including community support, additional personal protective equipment acquisitions, higher transportation costs and overtime costs resulting from lower headcount levels on site to accommodate social distancing.

COVID-19 costs are disclosed as part of mine operating earnings as temporary suspension, standby and other incremental COVID-19 costs. The Company anticipates that suspension and standby costs will be minimized prospectively for the balance of the year as the mines return to full production levels anticipated at the beginning of the year. Further, the Company is assessing if any incremental COVID-19 costs are expected to become normal-course in a COVID-19 world. However, those costs are expected to be at levels lower than those experienced this quarter. The Company also anticipates that some of these increases may be offset by efficiencies gained during the period. The breakdown of the expenditures incurred during the quarter are as follows:

| 7For the three months ended September 30, 2020 (In millions of US Dollars; unless otherwise noted) | Temporary suspension and standby costs | Other incremental COVID-19 costs | Total | ||||||||

| Canadian Malartic | $ | — | $ | 0.5 | $ | 0.5 | |||||

| Jacobina | — | 0.4 | 0.4 | ||||||||

| Cerro Moro | 1.7 | 2.4 | 4.1 | ||||||||

| El Peñón | 0.5 | 1.8 | 2.3 | ||||||||

| Minera Florida | 0.7 | 0.6 | 1.3 | ||||||||

| Total | $ | 2.9 | $ | 5.7 | $ | 8.6 | |||||

Despite the aforementioned temporary suspension, standby, and other incremental COVID-19 costs, mine operating earnings increased by $75.5 million or 92% in the three months ended September 30, 2020 compared to the same quarter last year, due to strong precious metal prices and the strong performances from Jacobina, El Peñón and Canadian Malartic. For detailed analysis on individual mines refer to Section 4: Operating Segments Performance.

For the nine months ended September 30, 2020

Net earnings for the nine months ended September 30, 2020 were $100.8 million or $0.11 per share basic and diluted, compared to net earnings of $211.1 million or $0.22 per share basic and diluted for the nine months ended September 30, 2019.

Earnings for the nine months ended September 30, 2020 were negatively impacted by $102.8 million of items that management believes may not be reflective of current and ongoing operations and which may be used to adjust or reconcile input models in consensus estimates. Significant adjusting items in the nine months ended September 30, 2020 include:

•A $21.3 million gain recorded on the discontinuation of the equity method upon the Leagold-Equinox merger;

•A $28.1 million loss on the mark-to-market of the Company's outstanding equity instruments related to share-based payments;

•A $31.3 million expense, representing costs incurred by the Company as a result of COVID-19 related temporary suspension or reductions at certain operations, and direct incremental costs associated with operating under COVID-19 related restrictions. Costs were incurred predominantly at Cerro Moro and Canadian Malartic due to government imposed restrictions on activity, and also in Chile and Brazil due to health authority regulations for temporary workforce reductions, and/or to promote social distancing;

•$51.0 million of non-cash tax losses on unrealized foreign exchange losses and $19.7 million of tax losses on non-routine transactions and adjustments.

For a full listing of reconciling items between net earnings and adjusted net earnings for the current and comparative period, refer to Section 3: Review of Financial Results.

COVID-19 costs are disclosed as part of mine operating earnings as temporary suspension, standby and other incremental COVID-19 costs. The Company anticipates that suspension and standby costs will be minimized prospectively for the balance of the year as the mines return to full production levels anticipated at the beginning of the year. Further, the Company is assessing if any incremental COVID-19 costs are expected to become normal-course in a COVID-19 world. However, those costs are expected to be at levels lower than those experienced this quarter. The Company also anticipates that some of these increases may be offset by efficiencies gained during the period. The breakdown of the expenditures incurred during the nine months ended September 30, 2020 are as follows:

For the nine months ended September 30, 2020 (In millions of US Dollars; unless otherwise noted) | Temporary suspension and standby costs | Other incremental COVID-19 costs | Total | ||||||||

| Canadian Malartic | $ | 1.9 | $ | 1.8 | $ | 3.7 | |||||

| Jacobina | 0.4 | 1.2 | 1.6 | ||||||||

| Cerro Moro | 9.3 | 5.2 | 14.5 | ||||||||

| El Peñón | 1.3 | 3.7 | 5.0 | ||||||||

| Minera Florida | 3.3 | 3.1 | 6.4 | ||||||||

| Other Regional Costs | — | 0.1 | 0.1 | ||||||||

| Total | $ | 16.2 | $ | 15.1 | $ | 31.3 | |||||

Mine operating earnings for the nine months ended September 30, 2020 were $338.1 million, representing an increase of $75.8 million or 29% over the same period in 2019, primarily due to the strong performances from Jacobina, El Peñón and Canadian Malartic, and strong precious metal prices, despite the aforementioned temporary suspension, standby, and other incremental

| 8COVID-19 costs. Additionally the comparative period had a contribution of $103.8 million from Chapada (divested in July 2019). For detailed analysis on individual mines please refer to Section 4: Operating Segments Performance.

| 9Summary of Financial Results

| For the three months ended September 30, | For the nine months ended September 30, | |||||||||||||

(In millions of US Dollars; unless otherwise noted) | 2020 | 2019 | 2020 | 2019 | ||||||||||

Revenue | $ | 439.4 | $ | 357.8 | $ | 1,099.3 | $ | 1,228.4 | ||||||

Cost of sales excluding DDA | (166.6) | (163.4) | (447.3) | (613.4) | ||||||||||

Gross margin excluding DDA | $ | 272.8 | $ | 194.4 | $ | 652.0 | $ | 615.0 | ||||||

Depletion, depreciation and amortization ("DDA") | (106.9) | (112.6) | (282.6) | (352.7) | ||||||||||

Temporary suspension, standby and other incremental COVID-19 costs | (8.6) | — | (31.3) | — | ||||||||||

Mine operating earnings | $ | 157.3 | $ | 81.8 | $ | 338.1 | $ | 262.3 | ||||||

General and administrative | (21.4) | (21.8) | (62.5) | (60.1) | ||||||||||

Exploration and evaluation | (3.6) | (1.8) | (9.1) | (7.0) | ||||||||||

Share of gain (loss) of associates | 3.1 | (16.8) | (1.0) | (16.1) | ||||||||||

Other operating (expenses) income, net | (6.8) | 241.9 | (13.1) | 228.0 | ||||||||||

Operating earnings | $ | 128.6 | $ | 283.3 | $ | 252.4 | $ | 407.1 | ||||||

Finance costs | (17.5) | (58.5) | (57.6) | (122.6) | ||||||||||

Other (costs) income, net | (4.0) | (6.1) | 2.9 | (16.0) | ||||||||||

Net earnings before income taxes | $ | 107.1 | $ | 218.7 | $ | 197.7 | $ | 268.5 | ||||||

Income tax expense, net | (51.5) | (17.4) | (96.9) | (57.4) | ||||||||||

Net earnings | $ | 55.6 | $ | 201.3 | $ | 100.8 | $ | 211.1 | ||||||

Per share data | ||||||||||||||

Earnings per share - basic and diluted | $ | 0.06 | $ | 0.21 | $ | 0.11 | $ | 0.22 | ||||||

Dividends declared per share | $ | 0.0175 | $ | 0.010 | $ | 0.046 | $ | 0.020 | ||||||

Dividends paid per share | $ | 0.0156 | $ | 0.005 | $ | 0.038 | $ | 0.015 | ||||||

Weighted average number of common shares outstanding (thousands) | ||||||||||||||

Basic | 952,479 | 950,413 | 951,611 | 950,210 | ||||||||||

Diluted | 954,526 | 951,944 | 953,427 | 951,564 | ||||||||||

Cash flows (i) | ||||||||||||||

Cash flows from operating activities | $ | 215.0 | $ | 157.4 | $ | 436.5 | $ | 317.5 | ||||||

Cash flows from operating activities before net change in working capital (ii) | $ | 199.0 | $ | 152.4 | $ | 481.5 | $ | 411.5 | ||||||

Cash flows (used in) from investing activities | $ | (47.7) | $ | 731.9 | $ | (84.9) | $ | 528.3 | ||||||

Cash flows used in financing activities | $ | (17.8) | $ | (884.5) | $ | (35.0) | $ | (845.8) | ||||||

| Net free cash flow (ii) | $ | 185.5 | $ | 89.5 | $ | 336.8 | $ | 195.1 | ||||||

(i)For further information on the Company's liquidity and cash flow position, refer to Section 7: Financial Condition and Liquidity.

(ii)A cautionary note regarding non-GAAP performance measures is included in Section 11: Non-GAAP Performance Measures.

Balance Sheet and Liquidity

As at September 30, 2020, the Company had cash and cash equivalents of $474.2 million and available credit of $650.0 million, for total available liquidity of $1,124.2 million.

As at, (In millions of US Dollars) | September 30, 2020 | December 31, 2019 | ||||||

Total assets | $ | 7,300.0 | $ | 7,117.2 | ||||

Total long-term liabilities | $ | 2,491.9 | $ | 2,488.9 | ||||

Total equity | $ | 4,304.7 | $ | 4,219.9 | ||||

Working capital (i) | $ | 222.0 | $ | (6.7) | ||||

Cash and cash equivalents | $ | 474.2 | $ | 158.8 | ||||

Debt (current and long-term) | $ | 1,093.3 | $ | 1,047.9 | ||||

Net debt (ii) | $ | 619.1 | $ | 889.1 | ||||

(i)Working capital is defined as the excess of current assets over current liabilities, which includes assets and liabilities classified as held for sale when applicable.

(ii)A cautionary note regarding non-GAAP performance measures is included in Section 11: Non-GAAP Performance Measures.

| 10Capital Expenditures

| For the three months ended September 30, | 2020 | 2019 | 2020 | 2019 | 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||

| (In millions of US Dollars) | Sustaining and other | Expansionary | Exploration | Total | ||||||||||||||||||||||

Canadian Malartic (i) | $ | 13.5 | $ | 14.4 | $ | (2.3) | $ | 10.1 | $ | 0.4 | $ | 0.1 | $ | 11.6 | $ | 24.6 | ||||||||||

Jacobina | 4.8 | 6.7 | 3.0 | 8.7 | 1.3 | 1.5 | $ | 9.1 | $ | 16.9 | ||||||||||||||||

Cerro Moro | 9.2 | 5.9 | 2.1 | 0.1 | 4.0 | 5.1 | $ | 15.3 | $ | 11.1 | ||||||||||||||||

El Peñón | 7.3 | 8.5 | — | 0.3 | 4.8 | 5.7 | $ | 12.1 | $ | 14.5 | ||||||||||||||||

Minera Florida | 2.9 | 3.1 | 4.2 | 3.4 | 2.1 | 2.1 | $ | 9.2 | $ | 8.6 | ||||||||||||||||

Other (ii) | 0.4 | — | 3.0 | 3.7 | 1.2 | 3.3 | $ | 4.6 | $ | 7.0 | ||||||||||||||||

| Total | $ | 38.1 | $ | 38.6 | $ | 10.1 | $ | 26.3 | $ | 13.7 | $ | 17.8 | $ | 61.9 | $ | 82.7 | ||||||||||

| For the nine months ended September 30, | 2020 | 2019 | 2020 | 2019 | 2020 | 2019 | 2020 | 2019 | ||||||||||||||||||

| (In millions of US Dollars) | Sustaining and other | Expansionary | Exploration | Total | ||||||||||||||||||||||

Canadian Malartic (i) | $ | 33.9 | $ | 31.7 | $ | 7.1 | $ | 26.7 | $ | 3.1 | $ | 0.7 | $ | 44.1 | $ | 59.1 | ||||||||||

Jacobina | 16.2 | 16.4 | 11.0 | 23.8 | 4.0 | 3.6 | $ | 31.2 | $ | 43.8 | ||||||||||||||||

Cerro Moro | 20.5 | 11.7 | 2.4 | 1.1 | 9.1 | 12.3 | $ | 32.0 | $ | 25.1 | ||||||||||||||||

El Peñón | 21.5 | 23.2 | — | 0.5 | 11.2 | 15.3 | $ | 32.7 | $ | 39.0 | ||||||||||||||||

Minera Florida | 8.2 | 9.5 | 10.8 | 8.8 | 5.2 | 7.1 | $ | 24.2 | $ | 25.4 | ||||||||||||||||

Other (ii) | 1.1 | 28.0 | 9.1 | 18.4 | 4.2 | 7.3 | $ | 14.4 | $ | 53.7 | ||||||||||||||||

| $ | 101.5 | $ | 120.5 | $ | 40.4 | $ | 79.3 | $ | 36.8 | $ | 46.3 | $ | 178.6 | $ | 246.1 | |||||||||||

(i)Canadian Malartic's Barnat pit had pre-commercial production ounce revenues and costs of sales capitalized to mineral properties against expansionary capital expenditures for the 2020 and 2019 periods.

(ii)Included in Other for the comparative period are capital expenditures relating to Chapada, which was disclosed separately in the comparative period.

2. CORE BUSINESS, STRATEGY AND OUTLOOK

Yamana Gold Inc. (“Yamana” or the “Company”) is a Canadian-based precious metals producer with significant gold and silver production, development stage properties, exploration properties, and land positions throughout the Americas, including Canada, Brazil, Chile and Argentina. Yamana plans to continue to build on this base through expansion and optimization initiatives at existing operating mines, development of new mines, the advancement of its exploration properties and, at times, by targeting other consolidation opportunities with a primary focus in the Americas. The Company is listed on the Toronto Stock Exchange (trading symbol "YRI"), the New York Stock Exchange (trading symbol "AUY"), and the London Stock Exchange (trading symbol "AUY").

The Company’s principal mining properties comprise the Cerro Moro mine in Argentina, the Canadian Malartic mine (50% interest) in Canada, the El Peñón and Minera Florida mines in Chile and the Jacobina mine in Brazil. Upon finalization of the integration agreement, the Company will also own a 56.25% interest in the integrated Agua Rica-Alumbrera project, a large-scale copper, gold, silver and molybdenum project located in the province of Catamarca, Argentina. For full details on the Agua Rica integration agreement, please refer to Section 5: Construction, Development and Other Initiatives.

Over the years, the Company has grown and generated value through strategic acquisitions and portfolio optimizations, and by pursuing organic growth to increase cash flows and unlock value at existing mines and development assets. Looking ahead, the Company’s primary objectives include the following:

•Continued focus on the Company’s operational excellence program, advancing near-term and ongoing optimizations related to production, operating costs, and key performance objectives in Health, Safety, Environment and Corporate Responsibility. This includes the "One Team, One Goal: Zero" vision for Social Responsibility, which reflects the Company's commitment to zero harm to employees, the environment and communities near its operations.

•Increasing mine life at the Company’s existing operating mines through exploration targeted on the most prospective properties. The Company does not rely exclusively on proven and probable mineral reserves at any point to determine mine life as that would undervalue and misrepresent the potential of its operations. Similarly, the Company does not rely solely on a reserve life index to the exclusion of other measures to determine mine life, as the Company believes there are other factors that determine mine life. Where possible, the Company endeavours to increase mineral reserves early on, although the Company recognizes that often it is more cost effective and technically efficient to progressively extend mine life as, and when, mine development is advancing. This is particularly true for underground mines and prospects. The Company believes that to rely exclusively at any given point on proven and probable mineral reserves does not

| 11give sufficient allowance for discovery of new mineral resources, history of conversion of mineral resources to mineral reserves and exploration potential. This is particularly true for El Peñón and Minera Florida for which the Company gives considerable allowance for mine life that is well in excess of mineral reserves, given the aforementioned factors of new discovery of mineral resources, historical conversion of mineral resources to mineral reserves and significant exploration potential. This will likely to be true for the underground at Canadian Malartic, which today carries substantial mineral resources and not mineral reserves. Additionally, the underground at Canadian Malartic has significant potential as a long-life operation.

•Maximizing the overall value of the Company as an enterprise, cash flows and free cash flows, and cash returns on invested capital, first on producing and then non-producing assets:

◦Within the producing portfolio, attention remains focused on per share measures related to the growth and quality of mineral reserves and mineral resources for mine life extensions and scope for throughput increases, metal grade and recovery improvements, and cost reductions that are expected to improve margins and cash flows.

•Maximizing cash returns to shareholders through sustainable dividends, which will also be reported as dividends per GEO produced, resulting from disciplined management of financial resources and capital allocation:

◦The Company has employed a gradual and progressive approach to dividend increases as the Company’s cash balances continue to increase from free cash flow, and successful and continuing initiatives to monetize its portfolio of non-producing assets and financial instruments;

◦The Company modified its dividend policy such that it will no longer provide a range for its dividend on a per GEO basis, with future dividend increases above the new floor of $100 per GEO based entirely on the cash flow and cash generation capacity of the Company. As its cash flows and cash balances increase, its dividend will rise correspondingly as a percentage of cash flows and commensurate with increasing cash balances from cash flows and sources that supplement cash flows;

◦Consistent with its dividend policy and sustainability objectives, the Company has sufficient cash reserves on hand to support payment of the dividend at the increased level for three years. The cash reserve fund provides the Company with the flexibility to pay the dividend at the new floor for an extended period even in a bottom of cycle gold price environment;

◦The Company will continue to engage regularly with investors to ensure it is maintaining an optimal balance between the amount payable and dividend sustainability;

◦Following the Company's initial capital spending and development phase from 2003 to 2006, the Company has consistently paid dividends since 2007. As of the date of this MD&A, dividends have aggregated to over $972.6 million paid over 13 years.

•Consistently optimize the Company's financial position to create financial flexibility, allowing the Company to execute on its business plan and increase shareholder value. The Company successfully improved its financial flexibility with the repayment of:

◦2020: $56.0 million in senior notes issued in March 2012, $200.0 million of indebtedness under the revolving credit facility was repaid in June and October 2020 ($200.0 million drawn in March 2020 as a prudent and conservative measure given global pandemic). As of the date of this MD&A, the Company has no outstanding balance on its revolving credit facility;

◦2019: $415.0 million in senior notes issued in March 2012 and June 2013 on a pro rata basis and indebtedness under the Company’s senior notes issued in June 2014 and December 2017; and

◦2019: $385.0 million of indebtedness under the revolving credit facility.

•Advancing the Company’s generative exploration program for the next generation of Yamana Mines:

◦Advance the Company’s most advanced exploration projects;

◦Pursue exploration and drilling programs at highly-prospective, early stage projects in the Company’s existing portfolio.

◦Expand the Company’s exploration portfolio through evaluations and targeted land acquisition

•For strategic assets in the portfolio, the focus is to assess the best path for creation of value for shareholders, including advancing the projects through exploration, technical/financial reviews, studies and optimizations, permitting and community engagement, and/or considering strategic alternatives to realize returns from the these strategic assets. This may include developing the assets through a joint venture or other strategic arrangements, or through monetization such as the recently accomplished successful sale of the royalty portfolio, the sale of Equinox shares, and the JV for its Suyai Project in Argentina.

•Advancement of Agua Rica, and along with our partners, determining the merits of the advancement of the Suyai Project.

Investment and Exploration Strategy

A further primary objective of the Company, although one with an intermediate to longer-term time horizon, is the advancement of its generative exploration program. The Company has an extensive exploration portfolio with well-defined exploration prospects

| 12and organic growth opportunities in all jurisdictions, with more advanced opportunities in Canada and Brazil. The objective of the generative exploration program is to advance at least one project to achieve mineral reserve and mineral resource inventories of at least 1.5 million ounces which the Company considers large enough to support a mine plan with annual gold production of approximately 150,000 ounces for at least eight years.

The Company is continuously reviewing its capital allocation strategy, and exploring options for funding such projects that do not draw on free cash flows. Funding strategies include, but are not limited to, proceeds from the monetization of non-cash producing assets or non-core assets that do not meet the Company's precious metal and scale requirements and, where applicable, flow-through funding arrangements. Funds are allocated to develop promising internal opportunities for organic growth through exploration and provide long term growth.

To assess these opportunities, the Company relies on an experienced local exploration team that operates in its established jurisdictions and other favourable districts in North and South America.

Every project in the generative exploration program has had some drilling, with some projects more advanced than others. At Lavra Velha in Brazil and Monument Bay in Canada, the Company has identified mineral resources in various categories. In the case of Monument Bay, the Company is further advancing the project with internal technical and economic assessments considering the project as an underground mine rather than an open pit mine. While resources would be reduced from current levels, this would be an economically attractive alternative with lower required capital investment (due to the higher investment required to develop a large tonnage, low grade, open pit mine), a reduced environmental footprint and significant exploration potential for increases in mineral resources down plunge and in satellite surface areas. A new high- grade geological model is being evaluated while several well-defined high-grade zones along a 4 kilometre strike length of the deposit have been identified. An expansion drill program on these targets is planned to begin this year and extend into next year. For more details, please refer to Section 6: Exploration.

The Company will also, from time to time, make investments in prospective advancing exploration and more advanced prospects where it can provide value-added guidance either from the Company's exploration or technical services groups. Recently, the Company made an investment in Monarch Gold, an emerging Canadian gold mining company that aims to be a 100,000-200,000 ounce per year gold producer through the development of its portfolio of high-quality projects in the Abitibi mining camp in Quebec, Canada.

As a complement to the advancement of the internal exploration opportunities, the Company will consider the acquisition of earlier stage development assets or companies that align with Yamana's objectives for capital allocation and financial results, jurisdiction, geology and operational expertise. Such opportunities should be funded through internal resources, meet minimum return levels that well exceed cost of capital and would meet the Company's minimum requirements to achieve mineral reserve and mineral resource inventories, mine life and per year production rate. Furthermore, preference would be given to geological and operational characteristics where the Company has an identified expertise and excellent opportunities for value enhancement. Such opportunities would also extend an existing regional presence or lead to that longer-term objective. Although the Company has an established portfolio of early-to-later-stage organic growth projects, the Company also considers it prudent to consider opportunities to extend regional presences in quality jurisdictions that offer geological and operational synergies and similarities to its current portfolio of assets.

2020 Revised Guidance

Jacobina, El Peñón and Canadian Malartic all enjoyed standout quarters. With overall production, and production at most of the Company’s mines, currently tracking ahead of plan, and in some cases well ahead of plan, the Company increased its 2020 production guidance from the previous guidance of 890,000 GEO to 915,000 GEO, representing an increase of 3%. Gold production and silver production guidance have increased from previous guidance by approximately 1% and 6%, respectively.

3. REVIEW OF FINANCIAL RESULTS

| 13FOR THE THREE MONTHS ENDED SEPTEMBER 30, 2020

Net earnings

Net earnings for the three months ended September 30, 2020, were $55.6 million or $0.06 per share basic and diluted, compared to net earnings of $201.3 million or $0.21 per share basic and diluted for the three months ended September 30, 2019. Net earnings and earnings per share for the three months ended September 30, 2020 and 2019 were affected by the following non-cash and other items that management believes are not reflective of current and ongoing operations, and which may be used to adjust or reconcile input models in consensus estimates:

| For the three months ended September 30, | ||||||||

| (In millions of US Dollars; except per share amounts) | 2020 | 2019 | ||||||

| Non-cash unrealized foreign exchange losses | $ | 4.2 | $ | 17.1 | ||||

| Share-based payments/mark-to-market of deferred share units | 5.1 | 9.0 | ||||||

| Mark-to-market (gains) losses on derivative contracts, investments and other assets and liabilities | (1.5) | 1.6 | ||||||

| Gain on sale of subsidiaries and other assets | (1.8) | (284.6) | ||||||

| Temporary suspension and standby costs | 2.9 | — | ||||||

| Other incremental COVID-19 costs | 5.7 | — | ||||||

| Share of one-off provision recorded against deferred income tax assets of associate | — | 13.0 | ||||||

| Financing costs paid on early note redemption | — | 35.0 | ||||||

| Other provisions, write-downs and adjustments (i) | 6.1 | 28.8 | ||||||

| Non-cash tax on unrealized foreign exchange gains | 8.7 | 36.7 | ||||||

| Income tax effect of adjustments | (4.9) | (0.8) | ||||||

| One-time tax adjustments | 12.8 | (7.6) | ||||||

Total adjustments - increase (decrease) to earnings | $ | 37.3 | $ | (151.8) | ||||

Total adjustments - increase (decrease) to earnings per share | $ | 0.04 | $ | (0.16) | ||||

(i)This balance includes, among other things, revisions in estimates and write-downs & provisions, or reversals of provisions, for items such as tax credits and legal contingencies.

Revenue

In the three months ended September 30, 2020, revenue was $439.4 million compared to $357.8 million in the same period in 2019. The 23% increase was primarily attributable to higher realized prices for gold and silver in the current period, and to increases in sales volumes at the Jacobina, El Peñón and Minera Florida mines, partially offset by lower sales volumes from the Canadian Malartic and Cerro Moro mines.

For a cautionary note on non-GAAP performance measures and a reconciliation to average realized prices, refer to Section 11: Non-GAAP Performance Measures.

Cost of Sales excluding DDA

Cost of sales excluding DDA was consistent with the same quarter in prior year, increasing only $3.2 million or 2%, with insignificant changes across all mine operations.

Depletion, Depreciation and Amortization (DDA)

Total DDA expense decreased $5.7 million or 5% for the three months ended September 30, 2020 when compared to the same period in 2019, primarily due to lower DDA at El Peñón. The decrease at El Peñón resulted from reduced rates of depletion in the current period due to additions to mineral reserves and resources announced at December 31, 2019.

General and administrative

General and administrative ("G&A") expenses include expenses related to management of the business that are not part of direct mine operating costs. In the three months ended September 30, 2020, G&A expenses were consistent with the comparative quarter in 2019, decreasing $0.4 million or 2%. The Company's cash G&A expenses were $17.2 million for the three months ended September 30, 2020, which was in line with plan and guided cash G&A expenses.

Exploration and evaluation

Exploration and evaluation expenses of $3.6 million for the three months ended September 30, 2020 were higher than in 2019 due to increased expenditures resulting from the generative exploration program. The program is focused on advancing projects

| 14in Yamana’s portfolio, while continuing drilling activity at a number of the Company’s highly prospective earlier stage projects. For more information please refer to Section 6: Exploration.

Share of earnings/loss of investments in associates

The Company's investments in associates at September 30, 2020 comprised of investments in Nomad Royalty Company and Monarch Gold, with the Company's share of earnings of associates in the three months ended September 30, 2020 of $3.1 million reflecting the net equity pick up from these two investments. For the same period in 2019, the Company recorded a share of loss of associate of $16.8 million, which represented Yamana's share of its then associate Leagold's loss for the period. The loss was primarily due to the Company recognizing its share of a $63.5 million provision recorded against Leagold's deferred income tax assets. On March 10, 2020, Leagold merged with Equinox and as a result of its reduced shareholding in the combined entity Yamana ceased to have significant influence in the investee, and therefore, discontinued equity accounting for the investment using the equity method from this date.

Other operating expenses/income

In the three months ended September 30, 2020, the Company recorded other operating expenses of $6.8 million compared to other operating income of $241.9 million for the same period in 2019. Operating expenses in the current period are comprised primarily of contributions to social and infrastructure development causes in jurisdictions where the Company is active, business and professional transaction costs, changes in provisions, and mark-to-market adjustments on financial assets and liabilities. Other operating income recorded in the prior period was primarily comprised of a $273.1 million gain recognized upon the divestment of the Chapada mine.

Finance costs

Finance costs decreased $41.0 million or 70% in the three months ended September 30, 2020 compared to the same period in 2019. Finance costs in the prior period included a $35.0 million expense relating to the early redemption of certain of the Company's senior notes in connection with the sale of the Chapada mine. The Company repaid $800.0 million of debt in total during the third quarter of 2019, and as a result, interest expense associated with long term debt has decreased in 2020.

Other income/costs

Other costs were $4.0 million in the three months ended September 30, 2020, compared to other costs of $6.1 million in the comparative period. Other income/costs is comprised primarily of unrealized gains and losses on derivatives and foreign exchange and, given the nature of these items, is expected to fluctuate from period to period. The loss in the current period was primarily due to unrealized foreign exchange losses.

Income tax expense

The Company recorded an income tax expense of $51.5 million for the three months ended September 30, 2020, as a result of higher profitability at the Company's operations, in relation to the comparative quarter's income tax expense of $17.4 million. The income tax provision further reflects a current income tax expense of $29.6 million and a deferred income tax expense of $21.9 million, compared to a current income tax expense of $18.9 million and a deferred income tax recovery of $1.5 million for the three months ended September 30, 2019.

Included in the income tax expense are withholding taxes of $10.4 million for the three months ended September 30, 2020 compared to an income tax expense of $1.5 million for the same period in 2019. The income tax expense also includes mining taxes of $10.3 million for the three months ended September 30, 2020, compared to mining taxes of $1.7 million in the three months ended September 30, 2019. An expense of $6.8 million relating to non-taxable items is included in the income tax expense for the three months ended September 30, 2020 compared to a recovery of $57.0 million for the three months ended September 30, 2019.

FOR THE NINE MONTHS ENDED SEPTEMBER 30, 2020

Net earnings

Net earnings for the nine months ended September 30, 2020, were $100.8 million or $0.11 per share basic and diluted, compared to net earnings of $211.1 million or $0.22 per share basic and diluted for the nine months ended September 30, 2019.

Net earnings and earnings per share for the nine months ended September 30, 2020 and 2019 were affected by the following non-cash and other items that management believes are not be reflective of current and ongoing operations, and which may be used to adjust or reconcile input models in consensus estimates:

| 15| For the nine months ended September 30, | ||||||||

| (In millions of US Dollars; except per share amounts) | 2020 | 2019 | ||||||

Non-cash unrealized foreign exchange (gains) losses | $ | (0.3) | $ | 28.3 | ||||

Share-based payments/mark-to-market of deferred share units | 28.1 | 11.8 | ||||||

Mark-to-market (gains) losses on derivative contracts, investments and other assets and liabilities | (1.1) | 1.0 | ||||||

Gain on sale of subsidiaries and other assets | (1.8) | (284.6) | ||||||

| Gain on discontinuation of the equity method of accounting | (21.3) | — | ||||||

| Temporary suspension and standby costs | 16.2 | — | ||||||

| Other incremental COVID-19 costs | 15.1 | — | ||||||

| Share of one-off provision recorded against deferred income tax assets of associate | — | 13.0 | ||||||

Financing costs paid on early note redemption | — | 35.0 | ||||||

| Other provisions, write-downs and adjustments (i) | 14.5 | 34.6 | ||||||

Non-cash tax on unrealized foreign exchange losses | 51.0 | 21.8 | ||||||

| Income tax effect of adjustments | (17.3) | (0.2) | ||||||

One-time tax adjustments | 19.7 | 21.1 | ||||||

Total adjustments - increase (decrease) to earnings | $ | 102.8 | $ | (118.2) | ||||

Total adjustments - increase (decrease) to earnings per share | $ | 0.11 | $ | (0.12) | ||||

(i)This balance includes, among other things, revisions in estimates and write-downs & provisions, or reversals of provisions, for items such as tax credits and legal contingencies.

Revenue

For the nine months ended September 30, 2020, revenue was $1,099.3 million compared to $1,228.4 million in the same period in 2019. The difference was primarily attributable to the absence of contributions from the Chapada mine (divested July 5, 2019), which contributed $226.8 million to revenue in the comparative period, as well as lower sales volumes from the Canadian Malartic and Cerro Moro mines, which were impacted by their respective temporary demobilization and suspension of operations as a result of the COVID-19 pandemic, and subsequent ramp up periods. The decreases in sales volumes were partially offset by higher realized prices for gold and silver in the current period, and by increases in sales volumes at the Jacobina, El Peñón and Minera Florida mines.

For a cautionary note on non-GAAP performance measures and a reconciliation to average realized prices, refer to Section 11: Non-GAAP Performance Measures.

Cost of sales excluding DDA

Cost of sales excluding DDA decreased $166.1 million or 27% for the nine months ended September 30, 2020 compared to the same period in 2019, primarily due to lower sales volumes from Canadian Malartic and Cerro Moro as discussed above, and the absence of cost of sales excluding DDA from Chapada ($110.9 million in the comparative period). Cost of sales excluding DDA was also positively impacted by ongoing operational efficiencies at Jacobina and El Peñón, improving per unit costs at these mines, and the depreciation of certain local currencies against the US Dollar.

Depletion, depreciation and amortization (DDA)

Total DDA expense decreased $70.1 million or 20% for the nine months ended September 30, 2020 compared to the same period in 2019, primarily due to lower sales volumes from Canadian Malartic and Cerro Moro as discussed above, as well as lower DDA at El Peñón and Jacobina resulting from reduced rates of depletion in the current period due to additions to mineral reserves and resources at these mines announced at December 31, 2019. The comparative period also included $12.1 million of DDA related to Chapada.

General and administrative

G&A expenses include costs related to the overall management of the business that are not part of direct mine operating costs. In the nine months ended September 30, 2020, G&A expenses increased $2.4 million or 4% compared to the same period in 2019, attributable to a $5.4 million increase in stock-based compensation expense, in particular in performance share units, due to the increase in the Company's share price in 2020. This was partially offset by cash reductions that have resulted from the Company's evaluation of its G&A expenses in the second quarter of 2019 to align its cost structure to the portfolio of assets that remained after the sale of the Chapada mine. The guided cash G&A rate for 2020 was $63.0 million, and the Company's cash G&A expenses of $47.2 million in the nine months to September 30, 2020 were in line with this target.

| 16Exploration and evaluation

Exploration and evaluation expenses of $9.1 million for the nine months ended September 30, 2020 were higher than the same period in 2019 due to increased expenditures relating to the ongoing generative exploration program. The program is focused on advancing projects in Yamana’s portfolio, while continuing drilling activity at a number of the Company’s highly prospective earlier stage projects. For more information please refer to Section 6: Exploration.

Share of earnings/loss of associates

The Company's share of net loss related to its associates totalled $1.0 million for the nine months ended September 30, 2020, and was comprised of the Company's share of losses of Leagold, prior to Yamana ceasing to have significant influence in Leagold in March 2020. This was partially offset by the Company's share of net earnings in Nomad Royalty Company and Monarch Gold, both of which were acquired in the latter half of the second quarter. In the comparative period in 2019, the Company recorded losses of $16.1 million, being the Company's share of Leagold's losses for the nine month period, which included the Company recognizing its share of a $63.5 million provision recorded against Leagold's deferred income tax assets during the period.

Other operating expenses/income

In the nine months to September 30, 2020, the Company recorded other operating expenses of $13.1 million. In the same period in 2019, the Company recorded other operating income of $228.0 million. Other operating expenses recorded in the current period include a $12.4 million mark to market loss on deferred share compensation due to the increase in the Company's share price, contributions to social and infrastructure development causes in jurisdictions where the Company is active, and various other individually insignificant operating expenses. These expenses were partially offset by a $21.3 million gain recognized upon the discontinuation of the equity method on the Company's investment in Leagold (now Equinox). Other operating income recorded in the prior period was primarily comprised of the $273.1 million gain recognized upon the sale of Chapada, partially offset by various other operating expenses.

Finance costs

Finance costs decreased $65.0 million or 53% in the nine months ended September 30, 2020 compared to the same period in 2019, primarily attributable to the lower interest expense in the current period, following the repayment of $800.0 million of debt during the third quarter of 2019. The reduction in the carrying amount of debt has significantly reduced the carrying cost of interest on debt, freeing up cash for other uses and for the Company to further improve its net debt position. Further, finance costs in the prior period included a $35.0 million expense relating to the early redemption of certain of the Company's senior notes in connection with the above mentioned repayment of debt in the third quarter of 2019.

Other income/costs