UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to __________

Commission File Number: 333-108715

Joway Health Industries Group Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Nevada | 98-0221494 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

| No. 2, Baowang Road, Baodi Economic Development Zone, Tianjin, P.R.China |

301800 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(86) 022-22533666

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| None | N/A | N/A |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001

(Title of class)

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file Reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☐ No ☒

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a small Reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” or an “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller Reporting company | ☒ |

| Emerging Growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a Report on and attestation to its management’s assessment of the effectiveness of its internal control over financial Reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit Report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☒ No ☐

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the Registrant’s most recently completed year was $385,200. Solely for purposes of this Annual Report, shares of common stock held by executive officers and directors of the Registrant as of such date have been excluded because such persons may be deemed to be affiliates. This determination of executive officers and directors as affiliates is not necessarily a conclusive determination for any other purposes.

Note.—If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstances, provided that the assumptions are set forth in this Form.

20,054,000 shares of common stock were issued and outstanding as of August 5, 2021.

JOWAY HEALTH INDUSTRIES GROUP INC.

Annual Report ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2020

TABLE OF CONTENTS

i

Information Regarding Forward-Looking Statements

In addition to historical information, this Report contains predictions, estimates and other forward-looking statements that relate to future events or our future financial performance. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by the forward-looking statements. These risks and other factors include those listed under “Risk Factors” and elsewhere in this Report. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. We discuss many of these risks in this Report in greater detail under the heading “Risk Factors.” Given these uncertainties, you should not place undue reliance on these forward-looking statements. Also, forward-looking statements represent our management’s beliefs and assumptions only as of March 31, 2021. You should read this Annual Report on Form 10-K and the documents that we have filed as exhibits to this Annual Report completely and with the understanding that our actual future results may be materially different from what we expect.

Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

ii

Overview

We are incorporated in the state of Nevada. Prior to the consummation of the Merger as of December 31, 2020, as more specifically described below, Joway Health Industries Group Inc. (the “Company” or “Joway Health”), through our PRC Operating Entities, were engaged in the manufacture, distribution and sales of tourmaline-related healthcare products. Our principal executive offices were located at No. 19. Baowang Road, Baodi Economic Development Zone, Tianjin City, P.R.China 301800.

As of December 31, 2020, we become a shell company as a result of the Merger described below as we no longer have any business operations.

Recent Developments

Effects of COVID-19

The COVID-19 pandemic and resulting global disruptions have affected our businesses, as well as those of our customers and suppliers. To serve our customers while also providing for the safety of our employees and service providers, we have modified numerous aspects of our logistics, transportation, supply chain, purchasing, and after-sale processes. Beginning in Q1 2020, we made numerous process updates across our operations nationwide, and adapted our fulfillment network, to implement employee and customer safety measures, such as enhanced cleaning and physical distancing, personal protective gear, disinfectant spraying, and temperature checks. We will continue to prioritize employee and customer safety and comply with evolving state and local standards as well as to implement standards or processes that we determine to be in the best interests of our employees, customers, and communities.

Due to the COVID-19 pandemic, our PRC subsidiaries were temporarily shut down from February 1st, 2020 to March 31st, 2020. Our business was negatively impacted and generated lower revenue and net income in 2020. Revenues from our PRC subsidiaries which had been disposed on December 31, 2020 were $225,419 for the year ended December 31, 2020, a decrease of $383,755, or 63%, compared to $609,174 in the same period of last year. The decrease in revenues for the year ended December 31, 2020 was mainly due to the impact of COVID-19 pandemic. The extent of the impact of COVID-19 on the Company’s results of operations and financial condition will depend on the virus’ future developments, including the duration and spread of the outbreak and the impact on the Company’s customers, which are still uncertain and cannot be reasonably estimated at this point of time.

Entry into a Material Definitive Agreement

On November 20, 2020, Joway Health entered into a Merger Agreement (the “Merger Agreement”) with Dynamic Elite International Limited, a British Virgin Islands company and a wholly-owned subsidiary of the Company (“Dynamic Elite”), Crystal Globe Limited, a British Virgin Islands company (“Crystal Globe”) and Joway Merger Subsidiary Limited, a British Virgin Islands company and a wholly-owned subsidiary of Crystal Globe (“Merger Sub”). The Merger Agreement provides that, upon the terms and subject to the satisfaction or waiver of the conditions set forth therein, Merger Sub will be merged with and into Dynamic Elite (the “Merger”), with Dynamic Elite continuing as the surviving corporation as a wholly-owned subsidiary of Crystal Globe. The special committee of the Board of Directors of the Company unanimously approved the Merger Agreement and the transactions contemplated thereby.

Crystal Globe, as the majority shareholder holding approximately 86.81% of the Company, is also the sole shareholder of Dynamic Elite. Mr. Jinghe Zhang, as the President, Chief Executive Officer, Chairman and Director, and the majority beneficial owner of the Company, also serves as sole shareholder and executive director of Crystal Globe. As a result, the Company and Dynamic Elite are under common control of Crystal Globe and Mr. Jinghe Zhang.

Pursuant to the terms of the Merger Agreement, at the effective time of the Merger (the “Effective Time”) and as a result of the Merger, the ordinary shares of common stock of Dynamic Elite issued and outstanding immediately prior to the Effective Time, all of which are held by the Company, were cancelled and extinguished. In accordance with the Merger Agreement, Crystal Globe has offered to pay cash consideration to the Company of $0.045 per share for the outstanding shares of the common stock of the Company (the “Merger Consideration”). At the date of the Merger Agreement, we had 20,054,000 shares of common stock outstanding.

1

The consummation of the Merger was subject to customary closing conditions, including, among others, (i) the Merger having not then been enjoined, made illegal or otherwise prohibited by any applicable law or any order, judgment, decree, injunction or ruling (whether temporary, preliminary or permanent) of any governmental authority (each, a “Governmental Order”) or by any proceeding then pending by a governmental authority seeking any Governmental Order; the truth and accuracy of the other party’s representations and warranties in the Merger Agreement, subject in certain cases to a de minimis, materiality or material adverse effect (each as described in the Merger Agreement) standard; and (ii) the compliance with or performance, in all material respects, of the other party’s covenants and obligations in the Merger Agreement required to be performed at or prior to the consummation of the Merger.

The Merger Agreement contained certain termination rights for the Company and Crystal Globe if the Merger was not consummated on or before December 31, 2020.

Completion of Acquisition or Disposition of Assets

Pursuant to the terms of the Merger Agreement dated November 20, 2020, as of December 31, 2020, the Effective Time of the Merger, the 10,000 ordinary shares of common stock of Dynamic Elite issued and outstanding immediately which were held by the Company, were cancelled for $0.045 per share for the outstanding shares of the common stock of the Company as Merger Consideration.

In January 2021, the Company had received $119,070 from Crystal Globe and distributed proportionately to the Company’s minority shareholders, other than Crystal Globe, which represents 2,646,000 shares of our common stock. Since the remaining 17,408,000 shares of our common stock is owned by Crystal Globe, the $0.045 per share payment for the 17,408,000 shares was offset and Crystal Globe did not receive any cash payment in connection with the Merger.

Change in Shell Company Status

As a result of the consummation of the Merger, the Company became a shell company as of December 31, 2020.

Corporate History

Joway Health Industries Group, Inc.

We were originally formed as a Texas corporation on March 21, 2003. On October 1, 2010, as a result of a transaction with Dynamic Elite (the “Share Exchange”), Dynamic Elite became our wholly-owned subsidiary and we ceased to be a shell company. Dynamic Elite was the holding company of all the equity of Tianjin Junhe Management Consulting Co., Ltd. (“Junhe Consulting”). In December 2010, the Company changed its jurisdiction of incorporation from the State of Texas to the State of Nevada and changed its name to Joway Health Industries Group, Inc. In connection with these changes, the Company adopted new Articles of Incorporation and Bylaws.

Share Exchange Transaction

On October 1, 2010, we entered into a Share Exchange Agreement with Crystal Globe, the sole shareholder of Dynamic Elite International Limited, pursuant to which Crystal Globe transferred all of its shares in Dynamic Elite to us in exchange for 15,215,426 shares of our common stock. As a result, Dynamic Elite became our wholly-owned subsidiary and we ceased to be a shell company, and Crystal Globe held a total of 18,515,426 shares (approximately 92.6%) of our issued and outstanding common stock.

The Share Exchange was treated for accounting purposes as a reverse acquisition. Therefore, the Company’s financial statements after the Share Exchange were those of Dynamic Elite and its subsidiaries and controlled companies on a consolidated basis, as if the Share Exchange had been in effect retroactively for all periods presented.

2

Dynamic Elite

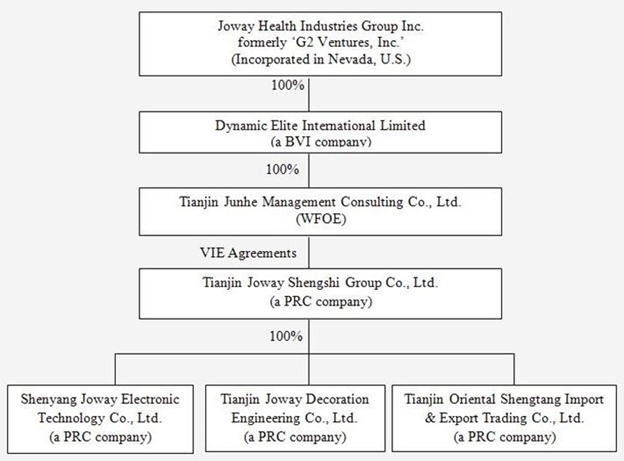

Dynamic Elite was founded on June 2, 2010 under the laws of the British Virgin Islands by Crystal Globe and Evan Liu, the sole shareholder of Crystal Globe, at the request of Mr. Jinghe Zhang. Mr. Liu is a friend of Mr. Jinghe Zhang. On September 15, 2010, Dynamic Elite established a wholly-owned subsidiary — Tianjin Junhe Management Consulting Co., Ltd. (“Junhe Consulting”), as a wholly foreign-owned enterprise (WOFE) under the laws of the PRC for the purposes of acquiring Tianjin Joway Shengshi Group Co., Ltd. and engaging in the manufacture, distribution and sale of tourmaline products in China. Under Article 6 of the Law of the People’s Republic of China on Wholly Foreign-Owned Enterprises, adopted April 12, 1986 at the 4th Sess. of the 6th National People’s Congress and as amended on October 31, 2000 (“PRC WOFE Law”) and Article 7 of the Detailed Rules for the Implementation, any person or entity that intends to establish an enterprise in the PRC with foreign capital is required to submit an application for examination and approval to the appropriate department under the State Council. On September 9, 2010, the local Tianjin City government issued a certificate of approval approving the foreign ownership of Junhe Consulting by Dynamic Elite. Mr. Jinghe Zhang was appointed as the Executive Director of Junhe Consulting.

PRC Operating Entities

All of our business operations were conducted through our PRC Operating Entities. The chart below sets forth our corporate structure prior to the consummation of the Merger as of December 31, 2020. As of January 1, 2021, as a result of the Merger, we no longer have any subsidiaries.

Joway Shengshi

On May 17, 2007, Mr. Jinghe Zhang, Mr. Lijun Si and Mr. Baogang Song founded Tianjin Joway Textile Co., Ltd. as a limited liability company under the PRC law. On November 24, 2009, the company changed its name to Tianjin Joway Shengshi Group Co., Ltd. (“Joway Shengshi”). The registered capital of Joway Shengshi is RMB 50,000,000 and its term of operation will expire on May 16, 2022. Mr. Jinghe Zhang is the Executive Director and General Manager of Joway Shengshi. On July 1, 2010, Mr. Lijun Si transferred 4% of the equity interest in Joway Shengshi to Mr. Jinghe Zhang. As a result, Mr. Zhang owns 99% of the equity interest in Joway Shengshi and Mr. Baogang Song owns the remaining 1% of the equity interest of Joway Shengshi. As of December 31, 2020 and 2019, Joway Shengshi was the sole shareholder of Joway Technology, Joway Decoration, and Shengtang Trading.

3

Joway Technology

Joway Technology was incorporated under PRC law on March 28, 2007, with a registered capital of RMB 1,100,000. It was formed to engage in intelligent engineering design and construction, development and sales of electronics, water filters, and other similar products. Prior to July 25, 2010, Joway Shengshi held 90.91% of Joway Technology. On July 25, 2010 Joway Shengshi acquired the remaining 9.09% of Joway Technology from Mr. Jingyun Chen for RMB 100,000 in cash. As a result of the acquisition, Joway Shengshi became the sole shareholder of Joway Technology.

Joway Decoration

Joway Decoration was cofounded by Joway Shengshi and Mr. Jingyun Chen under PRC law on April 22, 2009, with a registered capital of RMB 2,000,000. It was formed to engage in the business of intelligent electric heating project design and construction, development and sales of electronics technology and water filters, and the manufacture and sales of wood products. Prior to July 9, 2010, Joway Shengshi owned 90% of Joway Decoration. On July 9, 2010, Joway Shengshi entered into a share acquisition agreement with Mr. Jingyun Chen to acquire the remaining 10% of the shares of Joway Decoration for RMB 200,000 in cash. As a result of the acquisition, Joway Shengshi became the sole shareholder of Joway Decoration.

Shengtang Trading

Shengtang Trading was cofounded by Joway Shengshi and Mr. Jingyun Chen under PRC law on September 18, 2009, with a registered capital of RMB 2,000,000. It was formed to engage in the business of importing and exporting merchandise and technology; knitwear, biochemistry (excluding toxic chemicals and drugs), and the wholesale and retail sale of hardware. Prior to July 28, 2010, Joway Shengshi owned 95% of Shengtang Trading. On July 28, 2010, Joway Shengshi entered into a share acquisition agreement with Mr. Aiying Wang to acquire the remaining 5% of the shares of Shengtang Trading for RMB 100,000 in cash. As a result of the acquisition, Joway Shengshi became the sole shareholder of Shengtang Trading.

VIE Agreements

On September 16, 2010, prior to the Share Exchange, Junhe Consulting, Dynamic Elite’s wholly owned subsidiary had entered into a series of control agreements with Joway Shengshi and all of the owners of Joway Shengshi, which agreements allow Junhe Consulting to control Joway Shengshi. Through our ownership of Dynamic Elite, Dynamic Elite’s ownership of Junhe Consulting and Junhe Consulting’s agreements with Joway Shengshi, we believe that Joway Health controls Joway Shengshi and therefore, we consolidate the results of operations of Joway Shengshi and its subsidiaries with ours as variable interest entities.

In connection with the Share Exchange and as consideration for entering into the VIE Agreements, Mr. Jinghe Zhang and Mr. Baogang Song, the shareholders of Joway Shengshi, entered into a Call Option Agreement with the sole shareholder of Crystal Globe, pursuant to which the shareholders of Joway Shengshi have the right to purchase up to 100% of the shares of Crystal Globe at an aggregate price equal to $20,000 over the next three years. The Call Option vested as to 34% of the shares of Crystal Globe on April 2, 2011, and vests as to 33% on April 2 of 2012 and 2013. As a result, the shareholders of Joway Shengshi became the indirect beneficial owners of the shares of the Company held by Crystal Globe.

Under PRC law the acquisition of Joway Shengshi by Junhe Consulting must be structured as a cash transaction with the purchase price based on the appraised value of the equity interest or assets to be sold. Neither Junhe Consulting nor Dynamic Elite had sufficient cash to pay the appraised value of the equity interest or assets of Joway Shengshi. Alternatively, the shareholders of Joway Shengshi entered into a series of contractual agreements (the “VIE Agreements”) which enabled Dynamic Elite to gain control of Joway Shengshi and be entitled to receive 100% of the profits of Joway Shengshi and is obligated for 100% of the losses of Joway Shengshi. As a result of the VIE agreements, we are able to consolidate Joway Shengshi’s financial statements, including the results of operations, assets and liabilities of Joway Shengshi and its subsidiaries without triggering the regulatory requirements of PRC law. Under PRC law the VIE Agreements are considered commercial transactions among legal entities and individuals, and do not trigger the PRC requirements that apply to acquisitions, although the pledge by Joway Shengshi’s equity holders of all their equity in Joway Shengshi to Junhe Consulting pursuant to the Equity Pledge Agreement (the “Equity Pledge”) must be registered with the appropriate governmental agency. The Equity Pledge was registered with local administration department for industry and commerce pursuant to the Section 1 of Article 226 of PRC Property Law passed by National People’s Congress on March 16, 2007.

4

Through Junhe Consulting, we effectively and substantially controlled Joway Shengshi and its three wholly owned subsidiaries Joway Technology, Shengtang Trading and Joway Decoration.

The VIE Agreements included:

| ● | a Consulting Services Agreement through which Junhe Consulting had the right to advise, consult, manage and operate Joway Shengshi and collected and owned all of the net profits or losses of Joway Shengshi; | |

| ● | an Operating Agreement through which Junhe Consulting had the right to recommend director candidates and appoint the senior executives of Joway Shengshi, approve any transactions that may materially affect the assets, liabilities, rights or operations of Joway Shengshi, and guarantee the contractual performance by Joway Shengshi of any agreements with third parties, in exchange for a pledge by Joway Shengshi of its accounts receivable and assets; | |

| ● | a Proxy Agreement under which the two shareholders of Joway Shengshi had vested their collective voting control over Joway Shengshi to Junhe Consulting and may only transfer their respective equity interests in Joway Shengshi to Junhe Consulting or its designee(s); | |

| ● | an Option Agreement under which the shareholders of Joway Shengshi had granted to Junhe Consulting the irrevocable right and option to acquire all of their equity interests in Joway Shengshi with a consideration equal to the capital paid in by the shareholders in the amount of RMB 50 million (approximately USD $7.52 million). As executive director of Junhe Consulting, Mr. Jinghe Zhang had the power to exercise the option in his sole discretion; and | |

| ● | an Equity Pledge Agreement under which the owners of Joway Shengshi had pledged all of their rights, titles and interests in Joway Shengshi to Junhe Consulting to guarantee Joway Shengshi’s performance of its obligations under the Consulting Services Agreement. |

Terms of the VIE Agreements

Consulting Agreement

Under the Consulting Agreement, Joway Shengshi retained Junhe Consulting to (i) provide general advice and assistance relating to the management and operation of Joway Shengshi’s business; (ii) provide general advice and assistance with respect to employment and staffing issues, including recruiting and training of management personnel, administrative personnel and other staff, establishing an efficient payroll management system, and relocation assistance; (iii) provide business development advice and assistance; and (iv) such other advice and assistance as may be agreed upon by the parties. In return, Joway Shengshi agreed to pay Junhe Consulting quarterly a consulting fee in an amount equal to all of Joway Shengshi’s net income for that quarter within fifteen (15) days after receipt of Joway Shengshi’s quarterly financial statements. Joway Shengshi shall cause the owners of Joway Shengshi to pledge their equity interests in Joway Shengshi to Junhe Consulting to secure the payment of the foregoing consulting fee.

Joway Shengshi was subject to a number of covenants typical for this type of transaction, including the obligation to provide monthly, quarterly and Annual Reports, and other information requested by Junhe Consulting. In addition, Joway Shengshi was subject to a number of negative covenants, including the agreement that it should not (i) issue, purchase or redeem any equity or debt, or equity or debt securities; (ii) create, incur, assume or suffer to exist any liens upon any of its property or assets (except certain enumerated liens); (iii) wind up, liquidate or dissolve its affairs or enter into any transaction of merger or consolidation, or sale of all or substantially all of its assets; (iv) declare or pay any dividends; (v) incur, assume or suffer to exist any indebtedness, (other than certain enumerated exceptions); (vi) lend money or credit or make advances to any Person, or purchase or acquire any stock, obligations or securities of, or any other interest in, or make any capital contribution to, any other Person, except receivables in the ordinary course of business; (vii) enter into any transaction or series of related transactions, whether or not in the ordinary course of business, with any of its affiliates or related parties, other than on terms and conditions substantially as favorable to Joway Shengshi as would be obtainable in a comparable arm’s-length transaction; (viii) make any expenditure for fixed or capital assets (including, without limitation, expenditures for maintenance and repairs which are capitalized in accordance with generally accepted accounting principles in the PRC and capitalized lease obligations) during any quarterly period which exceeds the aggregate the amount contained in the budget; (ix) amend or modify or change its Articles of Association or business license, or any agreement entered into by it, with respect to its capital stock, or enter into any new agreement with respect to its capital stock; or (x) engage (directly or indirectly) in any business other than those types of business prescribed within the business scope of its business license.

5

The Consulting Agreement may be terminated by Junhe Consulting for any reason at any time. In addition, the Consulting Agreement may be terminated by Junhe Consulting by written notice in the event of a material breach by Joway Shengshi which, in the case of breach of a non-financial obligation, has not been remedied within fourteen (14) days following the receipt of such written notice. Either party may terminate the Consulting Agreement by written notice to the other party if (i) the other party becomes bankrupt or insolvent or is the subject of proceedings or arrangements for liquidation or dissolution or ceases to carry on business or becomes unable to pay its debts as they become due; (ii) if the operations of Junhe Consulting are terminated; or (iii) if circumstances arise which materially and adversely affect the performance or the objectives of the Consulting Agreement.

Operating Agreement

Under the Operating Agreement, Junhe Consulting agreed to guarantee Joway Shengshi’s performance of contracts, agreements or transactions with third parties in consideration for the pledge by Joway Shengshi to Junhe Consulting of all of Joway Shengshi’s assets. In addition, Joway Shengshi and its shareholders agreed that Joway Shengshi would not, without the prior written consent of Junhe Consulting, enter into any transactions which may materially affect the assets, obligations, rights or the operations of Joway Shengshi (excluding transactions entered into in the ordinary course of business and the lien obtained by relevant counter parties due to such agreements), including transactions involving (i) the borrowing of money or assumption of any debt; (ii) the sale or purchase from any third party any asset or right, including, but not limited to, any intellectual property rights; (iii) the provision of any guarantees to any third parties using its assets or intellectual property rights; or (iv) the assignment of any business agreements to any third party. Joway Shengshi and its shareholders also agreed to appoint to Joway Shengshi’s board of directors, and Joway Shengshi’s General Manager, Chief Financial Officer, and other senior officers those persons recommended or selected by Junhe Consulting.

Voting Rights Proxy Agreement

Under the Proxy Agreement, the Shareholders irrevocably granted to Junhe Consulting, for the maximum period of time permitted by law, all of their voting rights as shareholders of Joway Shengshi. In addition, the Shareholders agreed not to transfer their equity interest in Joway Shengshi to any third party (other than Junhe Consulting or a designee of Junhe Consulting). The Proxy Agreement may not be terminated without the unanimous consent of all Parties, except Junhe Consulting, which may terminate the Proxy Agreement with or without cause on thirty (30) days prior written notice.

Option Agreement

Under the Option Agreement, the Shareholders irrevocably granted to Junhe Consulting or its designee an exclusive option to purchase at any time, to the extent permitted under PRC Law, all or a portion of the Shareholders’ Equity Interest in Joway Shengshi for a price equal to the capital paid in by the Shareholders on a pro rata basis in accordance with the percentage of the Shareholders’ Equity Interest acquired, subject to applicable PRC laws and regulations.

6

Equity Pledge Agreement

Under the Equity Pledge Agreement, the Shareholders pledged all of their right, title and interest in their equity interests in Joway Shengshi to Junhe Consulting to guarantee Joway Shengshi’s performance of its obligations under the Consulting Services Agreement. The pledge expired two (2) years after the satisfaction by Joway Shengshi of all of its obligations under the Consulting Services Agreement. During the term of the Equity Pledge Agreement, Junhe Consulting was entitled to vote, control, sell, or dispose of the Pledged Collateral in the event the Company did not perform its obligations under the Consulting Services Agreement. In addition, Junhe Consulting was entitled to collect any and all dividends declared or paid in connection with the Pledged Collateral.

Through these contractual arrangements, we had the ability to substantially influence the daily operations and financial affairs of Joway Shengshi and to receive, through our subsidiaries, all of its profits. As a result, we were considered the primary beneficiary of Joway Shengshi and its operations, and Joway Shengshi and its subsidiaries were deemed to be our variable interest entities. Accordingly, we were able to consolidate into our financial statements the results, assets and liabilities of Joway Shengshi and its subsidiaries.

Call Option Agreement

As part of the reorganization of Joway Shengshi, Mr. Liu and the shareholders of Joway Shengshi entered into a Call Option Agreement, pursuant to which the shareholders of Joway Shengshi had the right to purchase up to 100% of the shares of Crystal Globe at an aggregate price equal of $20,000 over the next three years. In addition, the Option Agreement also provides that Mr. Liu should not dispose any of the shares of Crystal Globe without consent of Mr. Jinghe Zhang and Mr. Baogang Song. Upon the consummation of the Share Exchange Transaction, Crystal Globe became the principal shareholder of Joway Health (f/k/a G2 Ventures, Inc.) and Mr. Zhang and Mr. Song became indirect beneficial owners of the shares in Joway Health held by Crystal Globe pursuant to this Call Option Agreement.

On November 13, 2016, Mr. Jinghe Zhang exercised his Call Option as to 99% of the shares of Crystal Globe and Mr. Baogang Song exercised his Call Option as to 1% of the shares of Crystal Globe. As a result of exercising his Call Option, Mr. Zhang became the controlling shareholder of Crystal Globe and in turn, the controlling shareholder of the Company. On November 20, 2016, Mr. Song transferred his 1% of the shares of Crystal Globe to Mr. Zhang. Mr. Zhang thus controlled 17,408,000 shares, or 86.81%, of the issued and outstanding shares of the Company’s common stock.

As a result of the Merger, we become a shell company on December 31, 2020 and no longer have any subsidiaries.

Business Description

Prior to the consummation of the Merger, we, through our PRC Operating Entities, were engaged in the manufacture and sales of tourmaline-related healthcare products, and had a total of 21 full time employees.

As a result of the consummation of the Merger on December 31, 2020, we became a shell company and as of the date of this Annual Report, we have no full time employees. Starting from January 1, 2021, we have no longer any business operations.

Introduction to Tourmaline

Tourmaline is a crystal silicate mineral compounded with elements such as aluminum, iron, magnesium, sodium, lithium, or potassium. Tourmaline is classified as a semi-precious stone and the gem comes in a wide variety of colors. (Source: http://en.wikipedia.org/wiki/Tourmaline)

Tourmaline has the ability to become its own source of electric charge, as it is both pyroelectric, as well as piezoelectric. When it is put under pressure or when it is dramatically heated or cooled, tourmaline creates an electrical charge capable of emitting far infrared rays (“FIR”) and negative ions. (Source: http://www.globalhealingcenter.com/tourmaline.html)

FIRs are invisible waves of energy capable of penetrating deep into the human body. Negative ions are atoms that have a negative electric charge. FIRs and negative ions are perceived to have certain health benefits. (Source: http://www.globalhealingcenter.com/tourmaline.html)

7

Because it is a permanent source of FIRs and negative ions, tourmaline is perceived to have certain health benefits (Source: Niwa Institute for Immunology, Japan. Int J. Biometeorol 1993 Sep; 37(3) 133-8). In view of its perceived health benefits, tourmaline has been used to manufacture a wide range of healthcare products, including apparel, bedding, water purifiers, sauna rooms, and personal care products.

While tourmaline has perceived health benefits, the actual benefits of tourmaline to human health are unknown. The full efficacy of tourmaline to human health requires further significant clinical study. We are not aware of any formal clinical studies which have validated the health benefits of tourmaline.

We purchased liquid tourmaline from domestic Chinese companies which, in turn, imported it from South Korea. Liquid tourmaline is readily available and its price has remained relatively stable. We had not experienced any shortage in tourmaline but as a precaution, we closely monitored its price and have several back-up suppliers until we become a shell company.

China’s Tourmaline Health-Related Products Market

The use of tourmaline in health-related products in China began in 2001. Although more and more companies are producing tourmaline health-related products every year, the market for these products in China is still in its infancy and highly fragmented. (Source: 2010-2012 China’s tourmaline market and investment prospects research Report, Institute of China Uniway Economics, August, 2010).

Currently, there are numerous kinds of tourmaline health-related products on the market, including tourmaline clothes, tourmaline mattresses, tourmaline water machines, etc. In China, users of tourmaline health-related products are typically middle-aged and elderly people and demand for tourmaline health-related products is still relatively low compared to the size of the Chinese population.

In 2015, New Material is listed in the state development strategies in the State Council Report by Premier Keqiang Li. Tourmaline is defined as New Material and Tourmaline Processing Technology is designated as New Material Application Technology.

We believe that the main challenge for the tourmaline health-related product companies is market development rather than competition. With rising living standards, increasing disposable income, higher health consciousness and the greater awareness of the health benefits of tourmaline, we believe that the tourmaline health products market will grow rapidly in the next few years.

Manufacturing Process

Prior to the consummation of the Merger, we had two manufacturing processes.

One manufacturing process consisted of applying or infusing raw textiles with liquid or granular tourmaline and then producing products from these tourmaline-infused textiles. This process was used to produce Male and Female Underpants, Tourmaline Scarves and Tourmaline Pillowcases.

Our second manufacturing process consisted of applying or infusing already finished products with liquid or granular tourmaline. We purchased finished products, such as clothing, bedding, and mattresses and then, using one or more of the techniques described below, coat and/or infuse the products with liquid or granular tourmaline.

8

We coated or infused liquid or granular tourmaline into our products using one or more of the following methods:

The Spray Method

We used special high-pressure nozzles to spray liquid tourmaline onto the surface of the product. Through this process, the tourmaline particles were attached onto the surface of the product. We then used a high-temperature ironing machine to embed the tourmaline particles into the fibers of the product. This method is generally used in the manufacture of large pieces of textile products, such as mattresses.

The Dip Method

We completely immersed fabrics into liquid tourmaline and then stirred the fabrics in the liquid tourmaline to ensure the tourmaline particles attach to the surface of the fabrics. Finally, we embedded the tourmaline particles into the fibers by applying heat with our special high-temperature ironing machine. This method is used in the manufacture of smaller products, such as underwear, scarves, and shirts.

The Filling Method

We filled the products with tourmaline particles. This method is generally used to make activated water machines and other water treatment products.

The three methods mentioned above were keys to our manufacturing process. We protected our manufacturing methods via confidentiality agreements entered into between us and our employees. Pursuant to the confidentiality agreement, the employees were prohibited from unlawfully revealing and using our confidential technology during his/her term of employment and ten years after the termination of employment.

Our Products and Services

Prior to the consummation of the Merger as of December 31, 2020, we were primarily in the manufacture of the following three series of tourmaline-related healthcare products:

| 1. | Healthcare Knit Goods Series |

For the fiscal years ended December 31, 2020 and 2019, reported as part of loss from operations of our discontinued component, our healthcare knit goods series of products accounted for approximately 15.5% and 11.3% of our annual sales revenue, respectively. This series of products was comprised of tourmaline treated mattresses, bed linen, underwear, and shirts. We used either the spray or dip method to embed tourmaline particles into the fabric of this series of products.

Set forth below is a list of our major healthcare knit goods products, the trademarks or marks under which they were marketed and the manufacturing method employed prior to the consummation of the Merger as of December 31, 2020:

| No. | Products | Trademark/Mark | Manufacturing Method | |||||

| 1 | Golden Mattress |  |

|

Spray Method | ||||

| 2 | Tourmaline Mattress | |

|

Spray Method | ||||

| 3 | Tourmaline Underwear | |

Dip Method | |||||

| 4 | Tourmaline Bed Linens | |

|

Spray Method | ||||

| 5 | Tourmaline Pillow |  |

Spray Method | |||||

9

| 2. | Daily Healthcare and Personal Care Series |

For the fiscal years ended December 31, 2020 and 2019, reported as part of loss from operations of our discontinued component, our daily healthcare and personal care series of products accounted for approximately 27.9% and 34.7% of our annual sales revenue, respectively. This series was comprised of tourmaline-treated waist protectors, knee protectors, scarves, and shampoo and soap products. We used all three production methods to embed tourmaline particles into these products. We believe these tourmaline-treated daily healthcare products and personal care products produce FIRs and negative ions which have perceived health benefits. This series was also comprised of four edible products without tourmaline treatment, including Xin-Nao-Ling Fish Oil Soft Gel, Zhi-Li-Bao Fish Oil Soft Gel, Glucosamine Chondroitin Sulfate & Calcium Capsule and Vegetable and Fruit Enzyme Juice, which are subject to CFDA regulation.

Set forth below is a list of our major products in the daily healthcare and personal care series, the trademarks or marks under which they were marketed and the manufacturing method employed prior to the consummation of the Merger as of December 31, 2020:

|

No. |

Products | Trademark/Mark | Manufacture Method | |||

| 1 | Tourmaline Waist Protector | |

Spray Method | |||

| 2 | Tourmaline Scarves | |

Dip Method | |||

| 3 | Tourmaline Shampoo |  |

Filling Method | |||

| 4 | Tourmaline Soap | |

Filling Method | |||

| 5 | Tourmaline Toothpaste |  |

Filling Method | |||

| 6 | Xin-Nao-Ling Fish Oil Soft Gel |  |

N/A | |||

| 7 | Zhi-Li-Bao Fish Oil Soft Gel | |

N/A |

| 3. | Wellness House and Activated Water Machine |

For the years ended December 31, 2020 and 2019, reported as part of loss from operations of our discontinued component, our wellness house and activated water machine series of products accounted for approximately 56.7% and 54.0% of our annual sales revenue, respectively. This series of products was comprised mainly of tourmaline wellness houses, foot sauna bucket, tourmaline activated water machines and drinking mugs. Our tourmaline wellness house resembled a regular sauna room in which users experienced heat sessions. However, the inner layer of our wellness house were coated with tourmaline, which emits FIRs and negative ions when heated. Tourmaline is perceived to have certain health benefits. We supplied two types of wellness houses: one for family use, which was designed to be installed in the corner of a room and can contain three people; the other was customized and constructed on site for commercial bathrooms or spas according to their specifications. Our tourmaline activated water machines and drinking mugs were infused tourmaline particles into filters. Our Foot Sauna Bucket was filled with tourmaline particles on the bottom.

Set forth below is a list of our major products in the wellness house and activated water machine series, the trademarks or marks under which they were marketed and the manufacturing method employed prior to the consummation of the Merger as of December 31, 2020:

| No. | Products | Trademark/Mark | Manufacturing Method | |||

| 1 | Wellness House for family use | |

Spray Method | |||

|

||||||

| 2 | Tourmaline Water Mug | |

Filling Method | |||

| 3 | Tap Water Purifier | |

Filling Method | |||

| 4 | Foot Sauna Bucket | |

Filling Method |

10

Return Policy

It was our normal commercial practice to only allow the return of goods that did not conform to the customer’s order due to some occasional error in packaging or shipment. The return should be requested within seven days of purchase. Customers may also request a free repair of defective products within 15 days of purchase. For products purchased more than 15 days previously, we charged a service fee of 110% of the cost of repaired or replaced parts. For the years ended December 31, 2020 and 2019, we did not have sales return occurred.

Services: Wellness House Maintenance

Our wellness house products generally carry a one-year warranty. When the warranty expires, we provide our customers the option to engage us to service and maintain their wellness houses for a fee equal to 200% of the cost of the repaired or replaced parts.

For the years ended December 31, 2020 and 2019, the maintenance fees were $2,052 and $27,119, respectively, accounting for approximately 9% and 23% of sauna sales revenue, respectively.

Manufacturing Facilities

Prior to the consummation of the Merger as of December 31, 2020, our manufacturing facilities were located in Baodi District, Tianjin City, PRC, and occupied an area of approximately 2,500 square meters. We had 1 employee engaged in manufacturing as of December 31, 2020.

After the consummation of the Merger as of December 31, 2020, we no longer had manufacturing facilities and any employees for the manufacturing facilities.

Customers and Suppliers

Customers

Below is a list of our top three customers for the years 2020 and 2019, respectively, prior to the consummation of the Merger as of December 31, 2020.

Top Three Customers in 2020

| No. | Name | Amount (RMB) | Amount (US$) | Products Sold | Percentage of Sales | |||||||||||

| 1 | Xu Xiangyun Store | ¥ | 144,227 | $ | 20,910 | Foot Sauna Bucket, Wellness House,Mobile Health Care Kit, etc. | 9.3 | % | ||||||||

| 2 | Miao Li Store | ¥ | 135,424 | $ | 19,633 | Tap Water Purifier Tourmaline Mattress, Wellness House, etc. | 8.7 | % | ||||||||

| 3 | Wang Xiaojun Store | ¥ | 103,804 | $ | 15,049 | Wellness House,Foot Sauna Bucket, Tap Water Purifier, etc. | 6.7 | % | ||||||||

Top Three Customers in 2019

| No. | Name | Amount (RMB) | Amount (US$) | Products Sold | Percentage of Sales | |||||||||||

| 1 | Tianjin Baicheng Yitong Technology Co., Ltd. | ¥ | 643,938 | $ | 93,345 | Xin-Nao-Ling Fish Oil Soft Gel, Tourmaline Mask, Sanitary Napkins, etc. | 15.3 | % | ||||||||

| 2 | Miao Li Store | ¥ | 587,515 | $ | 85,166 | Foot Sauna Bucket, Tourmaline Mattress, Tap Water Purifier, etc. | 14.0 | % | ||||||||

| 3 | Xu Xiangyun Store | ¥ | 556,624 | $ | 80,688 | Wellness House, Foot Sauna Bucket, Tap Water Purifier, etc. | 13.2 | % | ||||||||

Our main customers were franchisees that were authorized to sell our products exclusively. In 2020, we did not have any customer accounted for more than 10% of our annual sales revenue and in 2019, we had three customers accounted for more than 10% of our annual sales revenue.

11

Suppliers

Below is a list of our top three suppliers in 2020 and 2019, respectively, prior to the consummation of the Merger as of December 31, 2020.

Top Three Suppliers in 2020

| No. | Name | Amount (RMB) | Amount (US$) | Product Purchased | Percentage of Purchase | |||||||||||

| 1 | Xuzhou Hailansauna Equipment Co., Ltd | ¥ | 333,983 | $ | 48,420 | Foot Sauna Bucket、Wellness House | 28.1 | % | ||||||||

| 2 | Penglai Huakang Health Products Co. Ltd. | ¥ | 103,982 | $ | 15,075 | Xin-Nao-Ling Fish Oil Soft Gel and Zhi-Li-Bao Fish Oil Soft Gel | 8.8 | % | ||||||||

| 3 | Zhejiang Taikang Biotechnology Co. Ltd | ¥ | 95,346 | $ | 13,823 | Mattress | 8.0 | % | ||||||||

Top Three Suppliers in 2019

| No. | Name | Amount (RMB) | Amount (US$) | Product Purchased | Percentage of Purchase | |||||||||||

| 1 | Xuchang Baichang Nanotechnology Co., Ltd. | ¥ | 695,000 | $ | 100,747 | Terahertz equipment | 18.5 | % | ||||||||

| 2 | Jiangmen Sangjian Sauna Equipment Co., Ltd. | ¥ | 265,000 | $ | 38,414 | Foot Sauna Bucket | 7.0 | % | ||||||||

| 3 | Cosmaker (Tianjin) Biotechnology Co., Ltd. | ¥ | 174,250 | $ | 25,259 | Tourmaline Mask and Skincare Series | 4.6 | % | ||||||||

In 2020 and 2019, we had one supplier accounted for 28.1% and 18.5% of our annual raw materials purchases, respectively. We do not have long term contracts with any of our suppliers since the raw materials we use are readily available on the market at generally stable prices.

Franchise Stores

Prior to the consummation of the Merger as of December 31, 2020, approximately 88% and 78% of our annual sales in 2020 and 2019, respectively, were made to our franchisees.

As of December 31, 2020, there were approximately 49 franchise stores across the PRC that were authorized to sell our products exclusively. Set forth below is a geographical breakdown of the franchise stores:

| Region | Number of Franchise Stores | |||

| Northeastern China (Liaoning, Jilin, Heilongjiang) | 2 | |||

| Northern China (Beijing, Tianjin, Hebei, Shanxi, Inner Mongolia) | 38 | |||

| Central China (Henan, Hubei, Hunan, Jiangxi) | 8 | |||

| Southwestern China (Chongqing, Sichuan, Guizhou, Yunnan, Tibet) | 1 | |||

| Total | 49 | |||

We used multiple criteria to select our franchisees, including financial condition, sales network, sales personnel, and facilities.

12

We typically entered into a standard franchising agreement with the applicant. Pursuant to the agreement, the franchisee was authorized to sell our products exclusively at a predetermined retail price. In exchange, we provided them with products at a discounted price, geographical exclusivity, and marketing, training and technological support. The franchisee was also required to adhere to certain standards of product merchandising, promotion and presentment. No initial franchise fees were required from the franchisee, nor was the franchisee required to pay any continuing royalties. The agreement was generally for a term of three years and was renewable on the mutual agreement of both parties.

After the consummation of the Merger as of December 31, 2020, we have no franchise stores across the PRC.

Marketing and Sales

Prior to the consummation of the Merger as of December 31, 2020, our primary marketing strategies were directed towards both our franchisees and end users, and the marketing efforts of our franchisees were directed towards end users. We assisted franchisees on monthly product introduction seminars, which were open to both our franchisees and to the general public.

The franchise stores were responsible for the cost of organizing the monthly product introduction seminars and meetings and we were responsible for the travel expenses of our employees who attended these meetings and seminars to explain and promote our various product lines. There were on average 3 such seminars and meetings each month nationwide in 2019. Generally, we chose the venue for the product seminars and meetings based on market prospects, sales volume and the extent of meeting preparation. During the year ended December 31, 2020, we did not hold a product seminar and meeting due to the COVID-19.

Below is a breakdown of our marketing expenses in the fiscal years 2020 and 2019.

| 2019 | 2020 | |||||||||||||||

| Expenses | RMB | US$ | RMB | US$ | ||||||||||||

| Promotion | ¥ | 19,396 | $ | 2,812 | ¥ | 6,810 | $ | 987 | ||||||||

| Printing | 2,313 | 335 | - | - | ||||||||||||

| Travelling | 289,640 | 41,986 | 35,737 | 5,181 | ||||||||||||

| Salaries | 655,443 | 95,012 | 163,496 | 23,703 | ||||||||||||

| Total | ¥ | 966,792 | $ | 140,145 | ¥ | 206,043 | $ | 29,871 | ||||||||

After the consummation of the Merger as of December 31, 2020, we no longer have a marketing and sales budget for sales personnel, and the remainder for travel, training and other expenses of our sales and marketing department.

Seasonality

Because our products were for daily use, seasonal variations do not have meaningful impact on the market demand for our products.

13

Competition

Competitive Environment

China’s tourmaline health products market is highly segmented and is in the stage with great demand.

However, given the highly segmented nature of the market, we are unable to locate any information on the size of the tourmaline healthcare-related market in China. Currently, Japanese and Korean companies are leaders in tourmaline technology. However, they have not yet developed a sizeable market share for their products in the PRC (Source: 2010-2012 China’s tourmaline market and investment prospects research Report, Institute of China Uniway Economics, August 2010). Therefore, we believe that there is a great opportunity for us to create demand and market share and establish ourselves as a leader in the tourmaline-related healthcare products field.

Our Competitors

Our major competitors in the PRC were as follows prior to the consummation of the Merger, effective as of December 31, 2020:

| ● | Hanya Nano Technology Co., Ltd. operates in Changsha, Hunan province, PRC. They mainly focus on manufacturing tourmaline sauna rooms and tourmaline health products. | |

| ● | Harbin Handu Tourmaline Nano Technology Development Co., Ltd. operates in PRC. They mainly focus on manufacturing tourmaline sauna rooms and tourmaline health products. |

Our Competitive Advantages

We believe that by leveraging the following strengths, we can effectively compete and enhance our market position:

| ● | Brand Advantage: We are one of the first companies to manufacture, distribute and sell tourmaline health-related products in the PRC and we believe that our trademark, “Joway”, is the most established and well-known brand in the market. | |

| ● | Technology Advantage: We possess several patents for tourmaline health-related products. We also invest a significant amount of time and expense in new product research and development. In 2016, we applied for a new patent on tourmaline after researching with Tianjin University of Technology. In addition, we have 3 types of products put on record of the Class 1 Medical devices in Tianjin Market and Quality Supervision and Administration Commission which lay a foundation of making health care products listed in Tianjin catalogue of medical system. | |

| ● | Product Diversification Advantage: Most of our competitors concentrate on the one of the tourmaline segments. On the contrary, our products cover diversified tourmaline related catalogue such as tourmaline daily health-related products, water treatment products and tourmaline home accessories. |

| ● | Sales Channels Advantage: As of December 31, 2020, we had approximately 49 franchise stores in most of the big cities in the PRC and we continue to expand our franchise network. We believe our extensive franchisee network will assure that our sales continue to grow. | |

| ● | Talent Advantage: We have recruited additional employees in the fields of marketing, franchise and training, who have several years of relevant experience in their previous careers. We plan to focus the efforts of these individuals to enhance our marketing and sales. | |

| ● | Public Relation Advantage: We enjoy the benefits of a membership at China Health Care Association and China Home Textile Association. For example, as a member, we are entitled to obtain the fist-hand technology related to tourmaline and apply such technology to our business when necessary. |

14

Business Strategy

As a result of the consummation of the Merger on December 31, 2020, we became a shell company.

As of the date of this Annual Report, we intend to seek, investigate and, if such investigation warrants, engage in a business combination with a private entity whose business presents an opportunity for our shareholders. Our objectives discussed below are extremely general and are not intended to restrict discretion of our Board of Directors to search for and enter into potential business opportunities or to reject any such opportunities. We have no particular business combination in mind and have not entered into any negotiations regarding such a combination. Neither our officers nor any of our affiliates has engaged in any negotiations with any representative of any company regarding the possibility of an acquisition or combination between our company and such other company. We have not yet entered into any agreement, nor do we have any commitment or understanding to enter into or become engaged in a transaction.

Research and Development

Prior to the consummation of the Merger, our research and development focused on developing new products in the daily health-related, tourmaline products, including tourmaline undergarment, tourmaline scarf and shawl, wellness room for family use. Prior to the consummation of the Merger as of December 31, 2020, we had no employee engaged in research and development activities.

During 2020 and 2019, we spent $405 (RMB 2,793) and $33,048 (RMB 227,984), respectively, on research and development activities which were reported as part of our discontinued operations in our financial statements. The following is a breakdown of our research and development expenses for 2020 and 2019.

| 2019 | 2020 | |||||||||||||||

| Item | RMB | US$ | RMB | US$ | ||||||||||||

| Equipment | ¥ | 6,690 | $ | 970 | ¥ | - | $ | - | ||||||||

| Samples | 130,619 | 18,934 | 121 | 18 | ||||||||||||

| Travel Expense | 5,038 | 730 | - | - | ||||||||||||

| Salary | 60,902 | 8,828 | - | - | ||||||||||||

| Inspection Fee | 24,735 | 3,586 | 2,672 | 387 | ||||||||||||

| Total | ¥ | 227,984 | $ | 33,048 | ¥ | 2,793 | $ | 405 | ||||||||

After the consummation of the Merger as of December 31, 2020, we no longer have any employees engaged in research and development activities.

Intellectual Property

Prior to the consummation of the Merger, we regard our trademarks, trade secrets, patents and similar intellectual property as critical factors to our success. We rely on patent, trademark and trade secret law, as well as confidentiality and license agreements with certain of our employees, customers and others to protect our proprietary rights.

The trademarks we currently use include the “Joway” trademark, which is owned by our President, Chief Executive Officer and director, Mr. Jinghe Zhang. We are permitted to use the “Joway” trademark pursuant to a license agreement with Mr. Jinghe Zhang dated December 1, 2009 for a term of ten years. The agreement was renewed at the end of its respective term. There is no license fee to Mr. Jinghe Zhang for the use of the trademark.

15

Set forth below is a detailed description of the trademarks we used in our business prior to the Merger.

| Mark | Registration /Application No. |

Class | Effective Date | Expiration Date |

Owner/Applicant | |||||

|

4794111 |

Class 24: Fabrics. Textiles and textile goods, not included in other classes; bed and table covers. |

February 21, 2009 | February 20, 2029 | Jinghe Zhang | |||||

|

6104256 |

Class 3: Cosmetics and Cleaning Preparations. Bleaching preparations and other substances for laundry use; cleaning, polishing, scouring and abrasive preparations; soaps; perfumery, essential oils, cosmetics, hair lotions; dentifrices. |

March 21, 2010 | March 20, 2030 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

6104253 |

Class 11: Environmental control apparatus. Apparatus for lighting, heating, steam generating, cooking, refrigerating, drying, ventilating, water supply and sanitary purposes. |

February 14, 2010 | February 13, 2030 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

8467175 |

Class 30: Staple foods. Coffee, tea, cocoa, sugar, rice, tapioca, sago, artificial coffee; flour and preparations made from cereals, bread, pastry and confectionery, ices; honey, treacle; yeast, baking-powder; salt, mustard; vinegar, sauces (condiments); spices; ice. |

July 21, 2011 | July 20, 2021 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

8236524 |

Class 24: Fabrics. Textiles and textile goods, not included in other classes; bed and table covers. |

April 28, 2011 | April 27, 2021 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

8029052 | Class 5: Pharmaceuticals. Pharmaceutical, veterinary and sanitary preparations; dietetic substances adapted for medical use, food for babies; plasters, materials for dressings; material for stopping teeth, dental wax; disinfectants; preparations for destroying vermin; fungicides, herbicides. | April 14, 2011 | April 13, 2021 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

8029009 |

CLASS 2: Paints Paints, varnishes, lacquers; preservatives against rust and against deterioration of wood; colorants; mordents; raw natural resins; metals in foil and powder form for painters, decorators, printers and artists. |

April 14, 2011 | April 13, 2021 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

16

| Mark | Registration /Application No. |

Class | Effective Date | Expiration Date |

Owner/Applicant | |||||

|

8236733 |

Class 30: Staple foods. Coffee, tea, cocoa, sugar, rice, tapioca, sago, artificial coffee; flour and preparations made from cereals, bread, pastry and confectionery, ices; honey, treacle; yeast, baking-powder; salt, mustard; vinegar, sauces (condiments); spices; ice. |

December 14, 2011 | December 13, 2021 | Tianjin Joway Shengshi Group Co., Ltd | |||||

|

8236538 |

Class 24: Fabrics. Textiles and textile goods, not included in other classes; bed and table covers. |

June 7, 2011 | June 6, 2021 | Tianjin Joway Shengshi Group Co., Ltd | |||||

|

8236684 |

Class 11: Environmental control apparatus. Apparatus for lighting, heating, steam generating, cooking, refrigerating, drying, ventilating, water supply and sanitary purposes |

June 21, 2011 | June 20, 2021 | Tianjin Joway Shengshi Group Co., Ltd | |||||

|

8236641 |

Class 3: Cosmetics and Cleaning Preparations. Bleaching preparations and other substances for laundry use; cleaning, polishing, scouring and abrasive preparations; soaps; perfumery, essential oils, cosmetics, hair lotions; dentifrices. |

May 28, 2011 | May 27, 2021 | Tianjin Joway Shengshi Group Co., Ltd | |||||

|

11275200 |

Class 30: Staple foods. Coffee, tea, cocoa, sugar, rice, tapioca, sago, artificial coffee; flour and preparations made from cereals, bread, pastry and confectionery, ices; honey, treacle; yeast, baking-powder; salt, mustard; vinegar, sauces (condiments); spices; ice. |

December 28, 2013 | December 27, 2023 | Tianjin Joway Shengshi Group Co., Ltd | |||||

|

11232054 |

Class 33: Alcoholic beverages. Fruit extracts [alcoholic], aperitifs, distilled beverages, cider, digesters [liqueurs and spirits], wine, clear wine, alcoholic beverages [except beer] and sake. |

December 14, 2013 | December 13, 2023 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

11203446 |

Class 5: Pharmaceuticals. Glue ball, Reducing tea, air purifying preparations, mosquito-repellent incense, sanitary pads, sanitary towels, antisepsis paper and babies’ diapers. |

December 7, 2013 | December 6, 2023 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

17

| Mark | Registration /Application No. |

Class | Effective Date | Expiration Date |

Owner/Applicant | |||||

|

16579737 |

Class 3: Cosmetics and Cleaning Preparations. Bleaching preparations and other substances for laundry use; cleaning, polishing, scouring and abrasive preparations; soaps; perfumery, essential oils, cosmetics, hair lotions; dentifrices. |

June 7, 2016 | June 6, 2026 | TianjinJoway Shengshi Group Co., Ltd. | |||||

|

16579738 |

Class 3: Cosmetics and Cleaning Preparations. Cleansing lotion, cleanser, facial mask, cosmetics, complexion cream, wrinkle cream. |

June 7, 2016 | June 6, 2026 | Tianjin Joway Shengshi Group Co., Ltd. | |||||

|

16966456 |

Class 3: Cosmetics and Cleaning Preparations. Cleansing lotion, cleanser, facial mask, cosmetics, complexion cream, wrinkle cream. |

July 21, 2016 | July 20, 2026 | Tianjin Joway Shengshi Group Co., Ltd. |

The patents that we used during the year ended December 31, 2020 are owned by our Chief Executive Officer, Mr. Jinghe Zhang. Pursuant to a license agreement with our President, Chief Executive Officer and director, Mr. Jinghe Zhang, we are permitted to use the following two patents for free from the effective date to the expiration date of each patent.

| No. | Product | Type | Patent No. | Application Date | Effective Date | Term |

Owner & Inventor | |||||||

| 1 | Water Purifier |

Utility Model |

ZL201620164704.7 | March 3, 2016 | July 6, 2016 | Ten years | Jinghe Zhang | |||||||

| 2 | Tourmaline Wellness House | Utility Model | ZL201620839876.X | August 3, 2016 | April 26, 2017 | Ten years | Jinghe Zhang |

Insurance

We do not carry property insurance on our buildings, facilities, and major operating assets, but on our vehicles, and we do not have any business interruption insurance due to the limited availability of this type of coverage in the PRC. During 2020 and 2019, we had no product liability claims.

Employees

Prior to the consummation of the Merger as of December 31, 2020, we had a total of 21 full time employees. After the consummation of the Merger, we have no full time employees.

There are no collective bargaining contracts covering any of our employees. We believe our relationship with our employees is satisfactory.

We are required to contribute a portion of our employees’ total salaries to the PRC government’s social insurance funds, including pension insurance, medical insurance, unemployment insurance, work-related injury insurance, and maternity insurance, in accordance with relevant regulations. We have purchased work injury insurance and medical insurance for all our employees.

Effective January 1, 2008, the PRC introduced a new labor contract law that enhances rights for the nation’s workers, including open-ended work contracts and severance pay. The legislation requires employers to provide written contracts to their workers, restricts the use of temporary laborers and makes it harder to lay off employees. It also requires that employees with fixed-term contracts be entitled to an indefinite-term contract after a fixed-term contract is renewed twice. Although the new labor contract law will increase our labor costs, we do not anticipate there will be any significantly effects on our overall profitability in the near future since such amount was historically not material to our operating cost. Management anticipates this may be a step toward improving candidate retention for skilled workers.

18

Government Regulations and Compliance with Applicable Laws

Below is a list of agencies which may have jurisdiction over our business prior to the consummation of the Merger as of December 31, 2020:

| Agency | Functions | |

| State Food and Drug Administration (“CFDA”)(1) | Supervise the entire process from research and development, manufacturing, and distribution to utilization of drugs; supervise and coordinate the safety management of food, health food and cosmetics and organize investigations of serious accidents. | |

| National Development and Reform Commission (“NDRC”) | Make strategic and mid- to long-term plans for the PRC healthcare industry; regulate drug prices; manage disaster relief funds and carry out healthcare development projects sponsored by the government. | |

| Ministry of Commerce (“MOFCOM”) | Formulate regulations and policies on foreign trade, foreign direct investments, consumer protection, and market competition; negotiate bilateral and multilateral trade agreements. | |

| Ministry of Science and Technology (“MST”) | Lay out science and technology development plans and policies; draft relevant regulations and rules and guarantee implementation of regulations and rules | |

| General Administration of Quality Supervision, Inspection and Quarantine (“AQSIQ”) | Manage national quality, metrology, entry-exit commodity inspection, entry-exit health quarantine, entry-exit animal and plant quarantine, import-export food safety, certification, accreditation, and standardization, as well as enforce administrative laws | |

| State Administration of Taxation (“SAT”) | Draft tax regulations and implementation rules and propose tax policies. | |

| State Administration of Foreign Exchange (“SAFE”) | Make regulations and policies governing foreign exchange market activities and manage state foreign exchange reserves. |

| (1) | The PRC State Food and Drug Administration is responsible for (i) regulating the research and development, manufacturing, distribution and utilization of drugs; (ii) supervising and coordinating the safety management of food, health food and cosmetics; and (iii) investigating serious accidents with respect to the foregoing. The products we manufacture are not regulated by the CFDA as they are not drugs, diet supplements or food consumed by humans. There are no existing laws or regulations in China governing the manufacture and sale of tourmaline health care products such as those sold by the Company nor are there any inspection requirements applicable to our products. |

We acted as a distributor for four edible products including Xin-Nao-Ling Fish Oil Soft Gel, Zhi-Li-Bao Fish Oil Soft Gel, Glucosamine Chondroitin Sulfate& Calcium Capsule and Vegetable and Fruit Enzyme Juice, which are subject to CFDA regulation. These products were manufactured by Penglai Huakang Healthcare Industries, Ltd., Wuhan Senlan Biotechnology Co., Ltd. and Weihai Biohigh Biotechnology Co., Ltd., which had obtained the necessary manufacturing licenses and certifications from the CFDA.

19

Environmental Regulations

Prior to the consummation of the Merger as of December 31, 2020, the major environmental regulations applicable to us included the PRC Environmental Protection Law, the PRC Law on the Prevention and Control of Water Pollution and its Implementation Rules, the PRC Law on the Prevention and Control of Air Pollution and its Implementation Rules, the PRC Law on the Prevention and Control of Solid Waste Pollution, and the PRC Law on the Prevention and Control of Noise Pollution.

According to Article 32 of the PRC Environmental Protection Law, a project that may cause pollution to the environment cannot be undertaken until an environmental impact statement has been approved by the applicable department of environmental protection administration.

In March 2008, Joway Shengshi submitted an environmental impact statement with respect to the manufacturing of 300,000 sets of knitwear annually to the Tianjin Baodi Environmental Protection Bureau. The environmental impact statement assesses the pollution that the manufacturing is likely to produce and its impact on the environment. In addition, the Report stipulates the preventive and curative measures the company will undertake. Tianjin Baodi Environmental Protection Bureau approved the environmental impact statement on March 12, 2008 and on April 22, 2009. The Tianjin Baodi Environmental Protection Bureau approved the manufacture of 300,000 sets of knitwear annually.

The Company’s production process does not produce industrial waste water or waste gas emissions of a type that is regulated by current PRC laws and regulations. The Company’s other emissions, including noise, waste water, solid waste and atmospheric pollutants meet regulatory standards. According to the Letter regarding Environment Protection of Tianjin Joway Shengshi Group Co, Ltd. issued by Tianjin Baodi Environmental Protection Bureau dated August 6, 2014, Joway Shengshi complies with applicable environmental protection laws and regulations and its discharge of pollutants meets with the standards of the state and Tianjin City.

In addition, Joway Shengshi obtained ISO 140001 International Environmental Management System Certification on January 15, 2009. ISO 140001 was first published as a standard in 1996 and specifies the requirements for an organization’s environmental management system. It applies to those environmental aspects over which an organization has control and where it can be expected to have an influence. Joway Shengshi passed each annual inspection of the ISO 140001. Such Certification covers the production and service of tourmaline health-related products such as underwear, bras, scarves, hats, knee-protectors, waist-protectors, socks, bedding and daily commodities.

We have not been named as a defendant in any legal proceedings alleging violation of environmental laws and have no reasonable basis to believe that there is any threatened claim, action or legal proceedings against us that would have a material adverse effect on our business, financial condition or results of operations due to any non-compliance with environmental laws.

During the year ended December 31, 2020, we did not incur any significant costs in connection with complying with PRC national or local environmental laws.

AS A SMALLER REPORTING COMPANY, WE ARE NOT REQUIRED TO PROVIDE A STATEMENT OF RISK FACTORS. NONETHELESS, WE ARE VOLUNTARILY PROVIDING RISK FACTORS HEREIN. THIS ANNUAL REPORT CONTAINS CERTAIN STATEMENTS RELATING TO FUTURE EVENTS OR THE FUTURE FINANCIAL PERFORMANCE OF OUR COMPANY. YOU ARE CAUTIONED THAT SUCH STATEMENTS ARE ONLY PREDICTIONS AND INVOLVE RISKS AND UNCERTAINTIES, AND THAT ACTUAL EVENTS OR RESULTS MAY DIFFER MATERIALLY. IN EVALUATING SUCH STATEMENTS, YOU SHOULD SPECIFICALLY CONSIDER THE VARIOUS FACTORS IDENTIFIED IN THIS ANNUAL REPORT, INCLUDING THE MATTERS SET FORTH BELOW, WHICH COULD CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE INDICATED BY SUCH FORWARD-LOOKING STATEMENTS.

An investment in our common stock involves a number of very significant risks. You should carefully consider the following risks and uncertainties in addition to other information in this Annual Report in evaluating our company and its business before purchasing shares of our common stock. Our business, operating results and financial condition could be seriously harmed due to any of the following risks. You could lose all or part of your investment due to any of these risks.

20

Risks Related To Our Business

Because we are currently considered a “shell company” within the meaning of Rule 12b-2 under the Exchange Act, the ability of holders of our common stock to re-sell their shares may be limited by applicable regulations.

We are currently considered a “shell company” within the meaning of Rule 12b-2 under the Exchange Act and Rule 405 of the Securities Act of 1933, as a result of the consummation of the Merger on December 31, 2020. Accordingly, the ability of holders of our common stock to re-sell their shares may be limited by applicable regulations. Specifically, shares of common stock which are considered “restricted securities” may not be sold except through a qualified registration statement under the Securities Act, pursuant to Section 4(1) of the Securities Act, or by meeting the conditions of Rule 144(i) under the Securities Act.

We have a history of losses, which raise substantial doubt about our ability to continue as a going concern.

As of December 31, 2020, we had an accumulated deficit of approximately $7.2 million and a working capital deficit of approximately $0.7 million. In addition, reported as part of loss from operations of discontinued component, our revenues decreased by $383,755 to $225,419 in 2020 compared with 2019, mainly due to the slowdown in the growth of the health product industry in China. Our cash as of December 31, 2020, was $0.

On December 31, 2020, we became a shell company. We can offer no assurance that we will ever operate profitably or that we will generate positive cash flow in the future. In addition, our operating results in the future may be subject to significant fluctuations due to many factors not within our control, such as the unpredictability of customers’ expectations and demands, the level of competition and general economic conditions.

We are a shell company and may never be able to effectuate our business plan.