PROSPECTUS SUPPLEMENT

TO THE SHORT FORM BASE SHELF PROSPECTUS DATED December 23, 2022

| New Issue | January 6, 2023 |

Filed

pursuant to General Instruction II.L of Form F-10

File No. 333-268485

PROSPECTUS SUPPLEMENT

(To Prospectus dated December 23, 2022)

SEABRIDGE

GOLD INC.

Up to US$100,000,000

Common Shares

This prospectus supplement (the “Prospectus Supplement”) of Seabridge Gold Inc. (“Seabridge” or the “Company”), together with the accompanying short form base shelf prospectus dated December 23, 2022 (the “Prospectus”), qualifies the distribution (the “Offering”) of common shares (each, an “Offered Share”) of the Company, having an aggregate offering price of up to US$100,000,000 (or C$135,640,000, based on the exchange rate on January 5, 2023 reported by the Bank of Canada). The Company has entered into a Controlled Equity OfferingSM Sales Agreement dated January 6, 2023 (the “Sales Agreement”) with Cantor Fitzgerald & Co. (the “Lead Agent”) and B. Riley Securities, Inc. (together with the Lead Agent, the “Agents”) in respect of the Offering, pursuant to which the Company may distribute Offered Shares from time to time through the Agents, as agent for the distribution of the Offered Shares, in accordance with the terms of the Sales Agreement. The Offering is being made in the United States under the terms of a registration statement on Form F-10 (SEC File No. 333-268485) (the “Registration Statement”) filed and effective with the United States Securities and Exchange Commission (the “SEC”). See “Plan of Distribution”.

The outstanding common shares of the Company (“Common Shares”) are listed for trading on the Toronto Stock Exchange (the “TSX”) under the symbol “SEA” and on the New York Stock Exchange (the “NYSE”) under the symbol “SA”. On January 5, 2023, the last day before the filing of this Prospectus Supplement, the closing trading price of the Common Shares on the TSX was C$18.49 per Common Share and the closing trading price of the Common Shares on the NYSE was US$13.63 per Common Share. The Company has applied to the TSX for the listing of the Offered Shares offered hereunder and such listing is subject to the approval of the TSX in accordance with its applicable listing requirements. NYSE approval is not required for the listing of the Offered Shares offered hereunder.

Sales of Offered Shares, if any, under this Prospectus Supplement and the accompanying Prospectus are anticipated to be made in transactions that are deemed to be “at-the-market distributions” as defined in National Instrument 44-102 - Shelf Distributions (“NI 44-102”), including sales made directly on the NYSE or on any other recognized marketplace outside of Canada upon which the Common Shares are listed, quoted or traded in the United States. No Offered Shares will be offered or sold in Canada on the TSX or other trading markets in Canada. The Offered Shares will be distributed at market prices prevailing at the time of the sale. As a result, prices may vary as between purchasers and during the period of any distribution. There is no minimum amount of funds that must be raised under the Offering. This means that the Company may terminate the Offering after raising only a small portion of the offering amount set out above, or none at all. See “Plan of Distribution”.

The Company will pay the Agents compensation, or allow a discount, for their services in acting as agents in connection with the sale of Offered Shares pursuant to the terms of the Sales Agreement an amount equal to 2.0% of the gross sales price per Offered Share sold.

No underwriter of the at-the-market distribution, and no person or company acting jointly or in concert with an underwriter, may, in connection with the distribution, enter into any transaction that is intended to stabilize or maintain the market price of the securities or securities of the same class as the securities distributed under this Prospectus Supplement, including selling an aggregate number or principal amount of securities that would result in the underwriter creating an over-allocation position in the securities. As sales agents, the Agents will not engage in any transactions to stabilize the price of the Common Shares. See “Plan of Distribution”.

The Agents are not registered as investment dealers in any Canadian jurisdiction and accordingly, the Agents will only sell the Offered Shares in the United States and will not, directly or indirectly, solicit offers to purchase or sell the Offered Shares in Canada.

The purchase and ownership of Offered Shares is subject to certain risks that should be considered carefully by prospective purchasers. Please see “Risk Factors” in this Prospectus Supplement and the accompanying Prospectus and the risk factors in the AIF (as herein defined) and the other documents incorporated herein and therein by reference, for a description of risks involved in an investment in Offered Shares. This Prospectus Supplement should be read in conjunction with and may not be delivered or utilized without the accompanying short form base shelf Prospectus.

The Offering is being made by a Canadian issuer that is permitted, under a multijurisdictional disclosure system adopted by the United States and Canada (“MJDS”) to prepare this Prospectus Supplement in accordance with Canadian disclosure requirements. Prospective investors in the United States should be aware that such requirements are different from those of the United States. Financial statements included or incorporated by reference herein have been prepared in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board, (“IFRS”) and may not be comparable to financial statements of United States companies, which are prepared under United States generally accepted accounting principles, or “US GAAP”. Such financial statements are subject to the standards of the Public Company Accounting Oversight Board (United States) and the United States Securities and Exchange Commission (“SEC”) independence standards.

Prospective investors should be aware that the acquisition and disposition of the Offered Shares described herein may have tax consequences both in the United States and in Canada. Such consequences for investors who are resident in, or citizens of, the United States are not described fully herein. Prospective investors should read the tax discussion contained in this Prospectus Supplement under the headings “Certain United States Federal Income Tax Considerations” and “Certain Canadian Federal Income Tax Considerations” and should consult their own tax advisor with respect to their own particular circumstances.

Some of the directors and officers of the Company and some of the experts named under “Interests of Experts” in the Prospectus are resident outside of Canada. Purchasers are advised that it may not be possible for investors to enforce judgments obtained in Canada against any person or company that is incorporated, continued or otherwise organized under the laws of a foreign jurisdiction or resides outside of Canada, even if the party has appointed an agent for service of process. See “Enforceability of Certain Civil Liabilities”.

The enforcement by investors of civil liabilities under the United States federal securities laws may be affected adversely by the fact that the Company is incorporated or organized under the laws of Canada, that some or all of its officers and directors may be residents outside the United States, that some or all of the underwriters or experts named in the registration statement may be residents of a foreign country, and that all or a substantial portion of the assets of the Registrant and said persons may be located outside the United States. See “Enforceability of Certain Civil Liabilities.”

THESE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND EXCHANGE COMMISSION NOR HAS THE SEC OR THE COMMISSIONS PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROSPECTUS SUPPLEMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The Company’s head office is at 106 Front Street East, Suite 400, Toronto, Ontario, Canada, M5A 1E1 and its registered office is at 10th Floor, 595 Howe Street, Vancouver, British Columbia, Canada, V6C 2T5.

Table of Contents

S-i

IMPORTANT NOTICE ABOUT INFORMATION IN THIS PROSPECTUS SUPPLEMENT AND THE ACCOMPANYING PROSPECTUS

This Prospectus Supplement and the accompanying Prospectus dated December 23, 2022 are part of a registration statement that we filed with the Securities and Exchange Commission, or SEC, utilizing a “shelf” registration process.

This Prospectus Supplement and the accompanying Prospectus relate to the offer by us of our Offered Shares to certain investors. We provide information to you about this offering of Offered Shares in two separate documents: (1) this Prospectus Supplement, which describes the specific details regarding the Offering; and (2) the accompanying Prospectus, which provides general information, some of which may not apply to this Offering. If information in this Prospectus Supplement is inconsistent with the accompanying Prospectus, you should rely on this Prospectus Supplement. However, if any statement in one of these documents is inconsistent with a statement in another document having a later date—for example, a document incorporated by reference in this Prospectus Supplement or the accompanying Prospectus—the statement in the document having the later date modifies or supersedes the earlier statement as our business, financial condition, results of operations and prospects may have changed since the earlier dates. You should read this Prospectus Supplement, the accompanying Prospectus and the documents and information incorporated by reference in this Prospectus Supplement and the accompanying Prospectus when making your investment decision. You should also read and consider the information in the documents we have referred you to under the headings “Additional Information” and “Documents Incorporated by Reference.” These documents contain information you should consider when making your investment decision.

You should rely only on information contained in or incorporated by reference into this Prospectus Supplement and the accompanying Prospectus. We have not, and the Agents have not, authorized anyone to provide you with information that is different. We are offering to sell and seeking offers to buy our Offered Shares only in jurisdictions where offers and sales are permitted. The information contained in this Prospectus Supplement, the accompanying Prospectus and the documents and information that have been filed with the SEC and the securities regulatory authorities in the jurisdictions in Canada in which the Company is a reporting issuer incorporated by reference in this Prospectus Supplement and the accompanying Prospectus are accurate only as of their respective dates, regardless of the time of delivery of this Prospectus Supplement or of any sale of Offered Shares.

This Prospectus Supplement does not constitute, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy, any securities offered by this Prospectus Supplement by any person in any jurisdiction in which it is unlawful for such person to make such an offer or solicitation.

This Prospectus Supplement is deemed to be incorporated by reference into the Prospectus solely for the purposes of the Offering. Other documents are also incorporated or deemed to be incorporated by reference into this Prospectus Supplement and into the Prospectus. See “Documents Incorporated by Reference”.

Unless the context otherwise requires, references in this Prospectus Supplement and the accompanying Prospectus to “Seabridge”, the “Company”, “we”, “us” and “our” includes Seabridge Gold Inc. and each of its material subsidiaries, as the context requires.

S-ii

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION

Unless stated otherwise or as the context otherwise requires, all references to dollar amounts in this Prospectus Supplement and the accompanying Prospectus are references to Canadian dollars. Unless stated otherwise, references to “$” or “C$” are to Canadian dollars and references to “US dollars” or “US$” are to United States dollars. On January 5, 2023, the exchange rate as reported by the Bank of Canada for the conversion of one Canadian dollar into United States dollars was C$1.00 equals US$1.3564.

The high, low, average and closing rates for the United States dollar in terms of Canadian dollars for each of the financial periods of the Company ended September 30, 2022, December 31, 2021 and December 31, 2020, as quoted by the Bank of Canada, were as follows:

| Period from January 1, 2022 to September 30, | Year Ended December 31 | |||||||||||

| 2022 | 2022 | 2021 | ||||||||||

| (expressed in Canadian dollars) | ||||||||||||

| Highest rate during period | 1.3726 | 1.3856 | 1.2942 | |||||||||

| Lowest rate during period | 1.2451 | 1.2451 | 1.2040 | |||||||||

| Average rate during period | 1.2828 | 1.3011 | 1.2535 | |||||||||

| Rate at the end of period | 1.3707 | 1.3544 | 1.2678 | |||||||||

The average exchange rate is calculated using the average of the daily rate on the last business day of each month during the applicable fiscal year or interim period. The Canadian dollar/U.S. dollar exchange rate has varied significantly over the last several years and investors are cautioned not to assume that the exchange rates presented here are necessarily indicative of future exchange rates.

Unless otherwise indicated, all financial information included and incorporated by reference in this Prospectus Supplement and the accompanying Prospectus is determined using IFRS, which differs from United States generally accepted accounting principles and therefore may not be comparable in all material respects to financial information prepared in accordance with United States generally accepted accounting principles.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus Supplement and the accompanying Prospectus, and the documents incorporated by reference herein and therein, contain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of Canadian securities laws concerning future events or future performance with respect to the Company’s projects, business approach and plans, including the completion of the Offering; the use of proceeds and the expected timing of the Offering; the receipt of all necessary regulatory and stock exchange approvals pertaining to the Offering; production, capital, operating and cash flow estimates relating to the existing assets of the Company; business transactions such as the potential sale or joint venture of either or both of the Company’s KSM Project and Courageous Lake Project (each as defined in the 2021 AIF (as defined herein)) and the acquisition of interests in mineral properties; requirements for additional capital; the estimation of mineral resources and reserves; and the timing of completion and success of exploration and advancement activities, community relations, required regulatory and third party consents, permitting and related programs in relation to the KSM Project, Iskut Project, Snowstorm Project, 3 Aces Project or Courageous Lake Project. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives or future events or performance (often, but not always, using words or phrases such as “expects”, “anticipates”, “believes”, “plans”, “projects”, “estimates”, “intends”, “strategy”, “goals”, “objectives” or variations thereof or stating that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements and forward-looking information (collectively referred to in the following information simply as “forward-looking statements”). In addition, statements concerning mineral reserve and mineral resource estimates constitute forward-looking statements to the extent that they involve estimates of the mineralization expected to be encountered if a mineral property is developed and the economics of developing a property and producing minerals.

S-iii

Forward-looking statements are necessarily based on estimates and assumptions made by the Company in light of its experience and perception of historical trends, current conditions and expected future developments. In making the forward-looking statements in this Prospectus Supplement and the accompanying Prospectus, the Company has applied several material assumptions including, but not limited to, the assumption that: (1) market fundamentals will result in sustained demand and prices for gold and copper, and to a much lesser degree, silver and molybdenum; (2) the potential for production at its mineral projects will continue operationally, legally and economically; (3) any additional financing needed will be available on reasonable terms; (4) estimated mineral resources and reserves at the Company’s projects have merit and there is continuity of mineralization as reflected in such estimates; (5) the Company will receive and maintain all required regulatory approvals required in respect of its projects and the Offering; and (6) the Company will receive all required regulatory approvals required in respect of this Prospectus Supplement.

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those expressed or implied by the forward-looking statements, including, without limitation:

| ● | the Company’s history of net losses and negative cash flows from operations and expectation of future losses and negative cash flows from operations; |

| ● | risks related to the Company’s ability to continue its exploration activities and future advancement activities, and to continue to maintain corporate office support of these activities, which are dependent on the Company’s ability to enter into joint ventures, to sell property interests or to obtain suitable financing; |

| ● | the Company’s indebtedness requires payment of quarterly interest and, in certain circumstances, may require repayment of principal and the Company’s principal sources for funds for repayment are capital markets and asset sales; |

| ● | uncertainty of whether the reserves estimated on the Company’s mineral properties will be brought into production; |

| ● | uncertainties relating to the assumptions underlying the Company’s reserve and resource estimates; |

| ● | risks related to obtaining and maintaining all necessary permits and governmental approvals, or extensions or renewals thereof, for exploration and development activities, including in respect of environmental regulation and the risk that the Company’s (Province of British Columbia) Environmental Assessment Certificate might expire before the KSM Project is declared to be “substantially started”; |

| ● | uncertainty of estimates of capital costs, operating costs, production and economic returns and lives of mines; |

| ● | risks relating to the commencement of site access and early site preparation construction activities at the KSM Project; |

| ● | risks related to commercially producing precious metals and copper from the Company’s mineral properties; |

| ● | risks related to fluctuations in the market price of gold, copper and other metals; |

| ● | risks related to fluctuations in foreign exchange rates; |

| ● | mining, exploration and development risks that could result in damage to mineral properties, plant and equipment, personal injury, environmental damage and delays in exploration or mining, which may be uninsurable or not insurable in adequate amounts; |

| ● | uncertainty related to title to the Company’s mineral properties and rights of access over or through lands subject to third party rights, interests and mineral tenures; |

| ● | risks related to unsettled First Nations rights and title and settled Treaty Nations’ rights; |

| ● | risks related to increases in demand for exploration, development and construction services equipment, and related cost increases; |

S-iv

| ● | increased competition in the mining industry; |

| ● | ongoing concerns regarding carbon emissions and the impacts of measures taken to induce or mandate lower carbon emissions on the ability to secure permits, finance projects and generate profitability at a project; |

| ● | the Company’s current and proposed operations are subject to risks relating to climate and climate change that may adversely impact its ability to conduct operations, increase operating costs, delay execution or reduce profitability of a future mining operation; |

| ● | the Company’s need to attract and retain qualified management and personnel; |

| ● | risks related to possible conflicts of interest due to some of the Company’s directors’ and officers’ involvement with other natural resource companies; |

| ● | risks associated with failing to maintain an effective system of internal control over financial reporting in the future, including that we may not be able to accurately report our financial condition, results of operations, cash flows or prevent fraud; |

| ● | risks associated with impacts from the reaction to and measures taken to address the spread of the COVID-19 virus; |

| ● | the Company’s classification as a “passive foreign investment company” under the United States tax code; |

| ● | risks associated with the use of information technology systems and cybersecurity; |

| ● | the reassessment by the Canada Revenue Agency of the Company’s refund claim for the 2010 and 2011 financial years in respect of the British Columbia Mining Exploration Tax Credit; |

| ● | uncertainty surrounding an audit by the Canada Revenue Agency of Canadian exploration expenses incurred by the Company during the 2014, 2015 and 2016 financial years which the Company has renounced to subscribers of flow-through share offerings in respect of the 2013 to 2015 tax years; |

| ● | risks related to the dilution of shareholders’ interest; |

| ● | the ability of the Company to raise proceeds under the Offering; |

| ● | risks related to the perception of the significant number of Common Shares in the public market; |

| ● | risks related to the Company’s broad discretion in the use of the net proceeds of the Offering. |

This list is not exhaustive of the factors that may affect any of the Company’s forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in this Prospectus Supplement and the annual information form of the Company dated March 24, 2022 for the year ended December 31, 2021 and filed on SEDAR on March 24, 2022 under National Instrument 51-102 – Continuous Disclosure Obligations (the “2021 AIF”), each under the heading “Risk Factors”, elsewhere in this Prospectus Supplement and the accompanying Prospectus and in documents incorporated by reference herein and therein. In addition, although the Company has attempted to identify important factors that could cause actual achievements, events or conditions to differ materially from those identified in the forward-looking statements, there may be other factors that cause achievements, events or conditions not to be as anticipated, estimated or intended. Many of the foregoing factors are beyond the Company’s ability to control or predict. It is also noted that while the Company engages in exploration and advancement of its properties, including site work in preparation for feasibility study work or site capture construction work, it will not undertake production activities by itself.

These forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made and the Company does not assume any obligation to update forward-looking statements, except as required by applicable securities laws, if circumstances or management’s beliefs, expectations or opinions should change. For the reasons set forth above, forward-looking statements are inherently unreliable, and investors should not place undue reliance on forward-looking statements.

The forward-looking statements contained in this Prospectus Supplement and the documents incorporated by reference herein and therein are qualified by the foregoing cautionary statements.

S-v

CAUTIONARY

NOTE TO UNITED STATES INVESTORS

CONCERNING MINERAL RESERVE AND RESOURCE ESTIMATES

The Company is permitted under a multi-jurisdictional disclosure system adopted by the securities regulatory authorities in Canada and the United States to prepare this Prospectus Supplement, the accompanying Prospectus and the documents incorporated by reference in this Prospectus Supplement and the accompanying Prospectus in accordance with the requirements of Canadian securities laws, which differ from the requirements of U.S. securities laws. National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all scientific and technical information contained or incorporated by reference in this Prospectus Supplement or in the accompanying Prospectus have been prepared in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum Classification System. These standards differ significantly from the requirements of the SEC, and reserve and resource information contained herein, in the accompanying Prospectus and in the documents incorporated by reference herein and in the accompanying Prospectus may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Without limiting the foregoing, this Prospectus Supplement and the accompanying Prospectus, including the documents incorporated by reference in this Prospectus Supplement and the accompanying Prospectus, use the terms “measured”, “indicated” and “inferred” resources. U.S. investors are cautioned that, while such terms are recognized and required by Canadian securities laws, the SEC does not recognize them. Under U.S. standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. U.S. investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into reserves.

For United States reporting purposes, the SEC has adopted amendments to its disclosure rules (the “SEC Modernization Rules”) to modernize the mining property disclosure requirements for issuers whose securities are registered with the SEC under the U.S. Securities Exchange Act of 1934, as amended (the “U.S. Exchange Act”). The SEC Modernization Rules more closely align the SEC’s disclosure requirements and policies for mining properties with current industry and global regulatory practices and standards, including NI 43-101, and replace the historical property disclosure requirements for mining registrants that were included in Industry Guide 7 under the U.S. Securities Act. As a foreign private issuer that is eligible to file reports with the SEC pursuant to the MJDS, the Company is not required to provide disclosure on its mineral properties under the SEC Modernization Rules and provides disclosure under NI 43-101 and the CIM Definition Standards. Accordingly, mineral reserve and mineral resource information contained or incorporated by reference herein may not be comparable to similar information disclosed by United States companies.

As a result of the adoption of the SEC Modernization Rules, the SEC now recognizes estimates of “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources.” In addition, the SEC has amended its definitions of “proven mineral reserves” and “probable mineral reserves” to be “substantially similar” to the corresponding CIM Definition Standards that are required under NI 43-101. While the above terms are “substantially similar” to CIM Definitions, there are differences in the definitions under the SEC Modernization Rules and the CIM Definition Standards. Accordingly, there is no assurance any mineral reserves or mineral resources that the Company may report in this Prospectus Supplement and the accompanying Prospectus, or in the documents incorporated by reference in this Prospectus Supplement and the accompanying Prospectus as “proven mineral reserves”, “probable mineral reserves”, “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would be the same or even would be comparable to the reserve or resource estimates the Company would have prepared under the standards adopted under the SEC Modernization Rules.

S-vi

DOCUMENTS INCORPORATED BY REFERENCE

Under the multi-jurisdictional disclosure system adopted by Canada and the United States, information has been incorporated by reference in this Prospectus Supplement from documents filed by the Company with securities commissions or similar authorities in Ontario, British Columbia, Alberta, Manitoba Saskatchewan, Nova Scotia and the Yukon (the “Commissions”) and filed with the SEC. Copies of the documents incorporated herein by reference may be obtained on request without charge from the Assistant Corporate Secretary of Seabridge at 106 Front Street East, Suite 400, Toronto, Ontario, Canada M5A 1E1, Telephone (416) 367-9292 and are also available electronically on SEDAR, which can be accessed electronically at www.sedar.com, and on EDGAR, which can be accessed electronically at www.sec.gov. This Prospectus Supplement should be read in conjunction with and may not be delivered or utilized without the accompanying short form base shelf Prospectus, including the documents incorporated by reference therein.

Any material change reports (excluding confidential material change reports), any interim and annual consolidated financial statements and related management’s discussion and analysis, proxy circulars (excluding those portions that, pursuant to National Instrument 44-101 – Short Form Prospectus Distributions of the Canadian Securities Administrators, are not required to be incorporated by reference herein), any business acquisition reports, and any other disclosure documents required to be filed pursuant to an undertaking to a provincial or territorial securities regulatory authority that are filed by the Company with various securities commissions or similar authorities in Canada after the date of this Prospectus Supplement and prior to the termination of this offering, shall be deemed to be incorporated by reference in this Prospectus Supplement.

Any statement contained in this Prospectus Supplement or in the accompanying Prospectus or in a document incorporated or deemed to be incorporated by reference herein shall be deemed to be modified or superseded for purposes of this Prospectus Supplement to the extent that a statement contained herein or in any other subsequently filed document which also is, or is deemed to be, incorporated by reference herein, modifies or supersedes such statement. The modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document it modifies or supersedes. The making of a modifying or superseding statement shall not be deemed an admission for any purposes that the modified or superseded statement, when made, constituted a misrepresentation, an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make a statement not misleading in light of the circumstances in which it was made. Any statement so modified or superseded shall not constitute a part of this Prospectus Supplement or accompanying Prospectus, except as so modified or superseded.

References to the Company’s website in any documents that are incorporated by reference into this Prospectus Supplement do not incorporate by reference the information on such website into this Prospectus Supplement, and the Company disclaims any such incorporation by reference.

Upon a new annual information form and the related audited annual financial statements and management’s discussion and analysis being filed by the Company with, and, where required, accepted by, the applicable securities commissions or similar regulatory authorities during the currency of this Prospectus Supplement, the previous annual information form, the previous audited annual financial statements and related management’s discussion and analysis, and all interim financial statements and related management’s discussion and analysis, material change reports and business acquisition reports filed prior to the commencement of the Company’s financial year in which the new annual information form and the related annual financial statements and management’s discussion and analysis are filed shall be deemed no longer to be incorporated into this Prospectus Supplement and accompanying Prospectus for purposes of future offers and sales of securities hereunder. Upon new interim financial statements and related management’s discussion and analysis being filed by us with the applicable securities commissions or similar regulatory authorities during the currency of this Prospectus Supplement, all interim financial statements and related management’s discussion and analysis filed prior to the new interim consolidated financial statements and related management’s discussion and analysis shall be deemed no longer to be incorporated into this Prospectus Supplement and accompanying Prospectus for purposes of future offers and sales of securities hereunder. Upon a new information circular relating to an annual general meeting of holders of Common Shares being filed by us with the applicable securities commissions or similar regulatory authorities during the currency of this Prospectus Supplement, the information circular for the preceding annual general meeting of holders of Common Shares shall be deemed no longer to be incorporated into this Prospectus Supplement and accompanying Prospectus for purposes of future offers and sales of securities hereunder.

DOCUMENTS FILED AS PART OF THE REGISTRATION STATEMENT

The following documents referred to in the accompanying Prospectus or in this Prospectus Supplement have been or will (through post-effective amendment or incorporation by reference) be filed with the SEC as part of the U.S. registration statement on Form F-10 (File No. 333-268485) of which this Prospectus Supplement and the accompanying Prospectus form a part: (i) the documents referred to under the heading “Documents Incorporated by Reference” in this Prospectus Supplement and in the accompanying Prospectus; (ii) powers of attorney from certain of the Company’s officers and directors; and (iii) the Sales Agreement.

S-vii

This summary highlights certain information about the Company, the Offering and selected information contained elsewhere in or incorporated by reference into this Prospectus Supplement or the accompanying Prospectus. This summary is not complete and does not contain all of the information that you should consider before deciding whether to invest in the Offered Shares. For a more complete understanding of the Company and the Offering, we encourage you to read and consider carefully the more detailed information in this Prospectus Supplement and the accompanying Prospectus, including the information incorporated by reference into this Prospectus Supplement and the accompanying Prospectus, and in particular, the information under the heading “Risk Factors” in this Prospectus Supplement and the documents incorporated by reference into this Prospectus Supplement and the accompanying Prospectus. All capitalized terms used in this summary refer to definitions contained elsewhere in this Prospectus Supplement or the accompanying Prospectus, as applicable.

The Company

Seabridge is a gold resource company whose material properties are the KSM project (for Kerr-Sulphurets-Mitchell) located in Northwestern British Columbia, Canada (the “KSM Project”) and the Courageous Lake project located in the Northwest Territories, Canada (the “Courageous Lake Project”). The Company exists under the Canada Business Corporations Act.

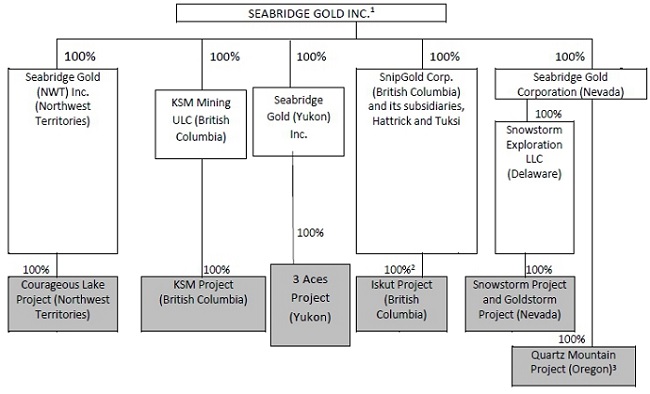

The Company presently has twelve wholly-owned subsidiaries: Seabridge Gold (NWT) Inc., a company incorporated under the laws of the Northwest Territories of Canada; Seabridge Gold (KSM) Inc., KSMCo, SnipGold Corp. (“SnipGold”), Hattrick Resources Corp. (“Hattrick”) and Tuksi Mining & Development Company Ltd. (“Tuksi”), companies incorporated under the laws of British Columbia, Canada; Seabridge Gold (Yukon) Inc., a company incorporated under the laws of Yukon; Seabridge Gold Corporation, Pacific Intermountain Gold Corporation, 5555 Gold Inc. and 555 Silver Inc., each Nevada Corporations; and Snowstorm Exploration LLC, a Delaware limited liability corporation. The following diagram illustrates the inter-corporate relationship between the Company, its active subsidiaries and its projects as of December 31, 2021.

Notes:

| 1. | Certain of the Company’s subsidiaries have been omitted from the chart as they own no mineral property. |

| 2. | SnipGold, through its subsidiary, Hattrick, owns 95% of 12 of the claims included in the Iskut Project covering an area of approximately 4,339 ha, which claims are located in the northwest corner of the property more than 3 km from the area that is the current exploration focus. |

| 3. | The Company has entered into option agreements under which a 100% interest in the Quartz Mountain project, located in Lake County, southern Oregon (the “Quartz Mountain Project”), may be acquired by a third party. |

S-1

The Company owns seven properties, four of which have gold resources, and it has one material property, its KSM Project. The Company holds a 100% interest in each of its properties other than a small portion of the Iskut project located near Stewart, British Columbia, Canada (the “Iskut Project”), in which it owns a 95% interest. The Quartz Mountain Project is subject to an option agreement under which the optionee may acquire a 100% interest in such project. At the date of this Prospectus, approximately 90% of the mineral resources at all of the Company’s projects combined are at the KSM Project. The Company’s principal work in 2022 on the KSM Project has been on early construction works for establishing site access, including building roads, camps and fish habitat compensation sites. Its main exploration efforts in 2022 were focused on the Iskut Project, the 3 Aces project located in southeast Yukon Territory (the “3 Aces Project”) and the Snowstorm project located in the northern Snowstorm Mountains in Nevada (the “Snowstorm Project”). The Company did not carry out significant work at its Courageous Lake Project in 2022, while it focuses on the KSM Project, Iskut Project, 3 Aces Project and Snowstorm Project. The Company considers that each of the Iskut Project, the 3 Aces Project and the Snowstorm Project have good potential for a meaningful discovery. At the Iskut Project, 2022 exploration work focused on drilling targets below the existing resource at Bronson Slope. At the Snowstorm Project, the Company completed drilling in Q2 2022 and has conducted a thorough review of exploration results to date and initiated evaluation of the Goldstorm Property, located about 3 km to the east of the Snowstorm Project. At the 3 Aces Project, due to delays in receiving the required permit, the Company only started work at the 3 Aces Project in September and undertook a program designed to test the Company’s 3-dimensional model of the mineralization at the Hearts zone.

At the KSM Project, the Company is principally directing in its early construction efforts towards keeping advancement of the KSM Project on track to achieve a ‘substantially started’ designation under its Provincial environmental assessment certificate, including completing construction of the Glacier and Taft Creeks fish habitat offsetting ponds, completing the initial 9 km segment of the Coulter Creek Access Road along with an associated camp, building the initial 17 km of the Treaty Creek Access Road, including the Bell-Irving River Bridge, constructing a camp near the beginning of the Treaty Creek Access Road and further construction of the site for the Mitchell Valley camp. The Company has also entered into an agreement with the British Columbia Hydro and Power Authority (“BC Hydro”) whereby BC Hydro is constructing a switching station that will permit the Company to draw hydro power from the Northwest Transmission Line.

The documents incorporated by reference herein, including the Prospectus, and documents incorporated by reference into the Prospectus, including the 2021 AIF, contain further details regarding the business of Seabridge. See “Documents Incorporated by Reference.”

S-2

| Common Shares offered by us | Common Shares having an aggregate offering price of up to US$100,000,000(or C$135,640,000, based on the exchange rate on January 5, 2023 reported by the Bank of Canada). |

| Plan of Distribution | “At-the-market distributions” as defined in NI 44-102, including sales made directly on the NYSE or on any other existing trading market for the Common Shares in the United States. No Offered Shares will be offered or sold in Canada on the TSX or other trading markets in Canada. The Offered Shares will be distributed at market prices prevailing at the time of the sale of such Offered Shares. See “Plan of Distribution”. |

| Use of Proceeds | The Company intends to use the net proceeds from the Offering to advance the exploration and development of the Company’s projects and for general working capital purposes but may also use it for acquisitions. See “Use of Proceeds”. |

| Risk Factors | See “Risk Factors” in this Prospectus Supplement and the risk factors discussed or referred to in the documents incorporated by reference (including the 2021 AIF) into this Prospectus Supplement and the accompanying Prospectus for a discussion of factors that should be read and considered before investing in the Offered Shares. |

| Tax considerations | Purchasing Offered Shares may have tax consequences. This Prospectus Supplement and the accompanying Prospectus may not describe these consequences fully for all investors. Investors should read the tax discussion in this Prospectus Supplement and the accompanying Prospectus and consult with their tax advisor. See “Certain United States Federal Income Tax Considerations” and “Certain Canadian Federal Income Tax Considerations” in this Prospectus Supplement. |

| Listing symbol | The Common Shares are listed for trading on the TSX under the symbol “SEA” and on the NYSE under the symbol “SA”. |

S-3

Investing in the Common Shares is speculative and involves a high degree of risk. The following risk factors, as well as risks currently unknown to the Company, could materially adversely affect the Company’s future business, operations and financial condition and could cause them to differ materially from the estimates described in this Prospectus Supplement, the accompanying Prospectus or the documents incorporated by reference herein or therein, each of which could cause purchasers of Offered Shares to lose part or all of their investment. Before deciding to invest in the Offered Shares, investors should carefully consider the risk factors set out below, in addition to the other information contained in this Prospectus Supplement, the accompanying Prospectus and the documents incorporated by reference herein and therein.

In addition to the other information contained in this Prospectus Supplement, the accompanying Prospectus and the documents incorporated by reference herein and therein, prospective investors should carefully consider the factors set out under “Risk Factors” in the 2021 AIF and the Company’s annual and interim management’s discussion and analysis for the year ended December 31, 2021 and the nine months ended September 30, 2022 (as well as any future such documents incorporated by reference herein) in evaluating the Company and its business before making an investment in the Offered Shares.

Risks relating to the Offering

Shareholders’ interest may be diluted in the future

The Company likely requires additional funds for exploration and development programs or potential acquisitions. If it raises additional funding by issuing additional equity securities or other securities that are convertible into equity securities, such financings may substantially dilute the interests of existing or future shareholders. Sales or issuances of a substantial number of securities, or the perception that such sales could occur, may adversely affect the prevailing market price for the Common Shares. With any additional sale or issuance of equity securities, investors will suffer immediate dilution in the net tangible book value of their shares. Moreover, the issuance of Offered Shares pursuant to this Offering from time to time will dilute the interests of existing or future shareholders.

There is no certainty regarding the net proceeds to the Company

There is no certainty that US$100,000,000 will be raised under the Offering. The Agents have agreed to use their commercially reasonable efforts to sell the Offered Shares when and to the extent requested by the Company, but the Company is not required to request the sale of the maximum amount offered or any amount and, if the Company requests a sale, the Agents are not obligated to purchase any Offered Shares that are not sold. As a result of the Offering being made on a commercially reasonable efforts basis with no minimum, and only as requested by the Company, the Company may raise substantially less than the maximum total offering amount or nothing at all.

Sales of a significant number of Common Shares in the public markets, or the perception of such sales, could depress the market price of the Common Shares

Sales of a substantial number of Common Shares or other equity-related securities in the public markets by the Company or its significant shareholders could depress the market price of the Common Shares and impair Seabridge’s ability to raise capital through the sale of additional equity securities. Seabridge cannot predict the effect that future sales of the Common Shares or other equity-related securities would have on the market price of the Common Shares. The price of the Common Shares could be affected by possible sales of the Common Shares by hedging or arbitrage trading activity which the Company expects to occur involving the Common Shares.

S-4

The Company has broad discretion in the use of the net proceeds from the Offering and may use them in ways other than as described herein

Management of the Company will have broad discretion with respect to the application of net proceeds received by the Company under the Offering, if any, and may spend such proceeds in ways that do not improve the Company’s results of operations or enhance the value of the Common Shares or its other securities issued and outstanding from time to time. Any failure by management to apply these funds effectively could result in financial losses that could have a material adverse effect on the Company’s business or cause the price of the securities of the Company issued and outstanding from time to time to decline. Because of the number and variability of factors that will determine the Company’s use of such proceeds, if any, the Company’s ultimate use might vary substantially from its planned use. You may not agree with how the Company allocates or spend the proceeds from the Offering, if any.

Risks relating to the Company

The Company has a history of net losses and negative cash flows from operations and expects losses and negative cash flows from operations to continue for the foreseeable future

The Company has a history of net losses and negative cash flows from operations and the Company expects to incur net losses and negative cash flows from operations for the foreseeable future. As of December 31, 2021, the Company’s deficit totaled approximately $150 million. None of the Company’s properties has advanced to the commercial production stage and the Company has no history of earnings or positive cash flow from operations.

The Company expects to continue to incur net losses unless and until such time as one or more of its projects enters into commercial production and generates sufficient revenues to fund continuing operations or until such time as the Company is able to offset its expenses against the sale of one or more of its projects, if applicable. The development of the Company’s projects to achieve production will require the commitment of substantial financial resources. The amount and timing of expenditures will depend on a number of factors, including the progress of ongoing exploration and development, the results of consultant analysis and recommendations, the rate at which operating losses are incurred and the execution of any sale or joint venture agreements with strategic partners, some of which are beyond the Company’s control. There is no assurance that the Company will be profitable in the future.

If we fail to maintain an effective system of internal control over financial reporting in the future, we may not be able to accurately report our financial condition, results of operations, cash flows or prevent fraud.

We are subject to National Instrument 52-109 – Certification of Disclosure in Issuers’ Annual and Interim Filings of the Canadian Securities Administrators and Section 404 of the Sarbanes-Oxley Act (collectively the “ICOFR Requirements”) requiring that effective internal controls for financial reporting and disclosure controls and procedures be maintained. We are required to furnish a report by management on, among other things, the effectiveness of internal control over financial reporting. This report will include disclosure of any material weaknesses identified by management in our internal control over financial reporting. A material weakness is a deficiency, or combination of deficiencies, in internal control over financial reporting that results in more than a reasonable possibility that a material misstatement of annual or interim financial statements will not be prevented or detected on a timely basis. Any testing by us conducted in connection with the ICOFR Requirements, or any subsequent testing by our independent registered public accounting firm, may reveal deficiencies in our internal controls over financial reporting that are deemed to be material weaknesses or that may require prospective or retroactive changes to our financial statements or identify other areas for further attention or improvement. In addition, undetected material weaknesses in our internal controls over financial reporting could lead to restatements of our financial statements and require us to incur the expense of remediation. Failure to remedy any material weakness in our internal control over financial reporting, or to implement or maintain other effective control systems required of public companies, could also undermine investor confidence in the accuracy and completeness of our financial reports and adversely impact our share price and future access to the capital markets.

S-5

Since the date of the unaudited condensed interim consolidated financial statements of the Company for the three and nine months ended September 30, 2022 which are incorporated by reference in this Prospectus Supplement, there have been no material changes to the share and loan capital of the Company on a consolidated basis, except for the issuance of securities set forth under “Prior Sales”.

Assuming the entire Offering is sold, total equity capitalization will increase by approximately US$97,750,000 being the aggregate proceeds of US$100,000,000, less commissions of US$2,000,000 and estimated total offering expenses of US$250,000. The number of Offered Shares issued will depend upon the at-the-market prices at which they are sold.

The net proceeds from the Offering are not determinable in light of the nature of the distribution. The net proceeds of any given distribution of Offered Shares through the Agents in an “at-the-market distribution” will be the gross proceeds after deducting the applicable compensation payable to the Agents under the Sales Agreement and the expenses of the distribution.

The Company expects to use the net proceeds from the Offering, to advance the exploration and advancement of the Company’s projects and for general working capital purposes but may also use net proceeds to fund all or a portion of the price of an acquisition. None of the proceeds have been allocated to a specific capital expenditure or future acquisition. The Company reserves the right, for sound business reasons and at the sole discretion of the Company’s management, to reallocate the proceeds of this offering in response to developments in the Company’s business and other factors.

Business Objectives

A description of the Company’s objectives appears in the accompanying Prospectus under the heading “Use of Proceeds, Business Objectives and Milestones”. It indicates that proceeds from this Prospectus Supplement are likely to be spent on the objectives relating to exploration at the Snowstorm project and reclamation and closure of the Johnny Mountain Mine (expected to be in the range of $4-$6 million each in 2023). In addition, the proceeds could be used to fund the Company’s own early construction activities, the costs to meet the Company’s obligations under the Facilities Agreement with British Columbia Power and Hydro Authority or the costs of other objectives established by the Company for 2023 and 2024.

The Company has entered into the Sales Agreement with the Agents under which it may issue and sell from time to time Offered Shares through the Agents having an aggregate sales amount of up to US$100,000,000 (or C$135,640,000, based on the exchange rate on January 5, 2023 reported by the Bank of Canada). Sales of Offered Shares, if any, will be made in transactions that are deemed to be “at-the-market distributions” as defined in NI 44-102, including sales made directly on the NYSE or other existing trading markets for the Common Shares in the United States. No Offered Shares will be offered or sold in Canada through the TSX or any other trading market in Canada.

The Agents will offer the Offered Shares subject to the terms and conditions of the Sales Agreement on a daily basis or as otherwise agreed upon by the Company and the Agents. The Company will designate the maximum amount of Offered Shares to be sold pursuant to any single placement instruction to the Agents.

S-6

Subject to the terms and conditions of the Sales Agreement, the Agents will use its commercially reasonable efforts to sell on the Company’s behalf, all of the Offered Shares requested to be sold by the Company. The Company may instruct the Agents not to sell the Offered Shares if the sales cannot be effected at or above the price designated by the Company in any such instruction.

Either the Company or the Agents may suspend the Offering of the Offered Shares being made through the Agents under the Sales Agreement upon proper notice to the other party. The Company and the Agents each have the right, by giving written notice as specified in the Sales Agreement, to terminate the Sales Agreement in each party’s sole discretion at any time.

The Company will pay the Agents compensation, or allow a discount, for its services in acting as agents or in the sale of the Offered Shares pursuant to the terms of the Sales Agreement an amount equal to 2.0% of the gross sales price per Offered Share sold. The Company has also agreed to reimburse the Agents for certain specified expenses, including the fees and disbursements of its legal counsel, in an amount not to exceed US$50,000, plus applicable taxes. The remaining sales proceeds, after deducting any expenses payable by the Company and any transaction, listing or filing fees imposed by any governmental, regulatory or self-regulatory organization in connection with the sales, will equal the net proceeds to the Company for the sale of such Offered Shares.

The Agents will provide written confirmation to the Company following the close of trading on the NYSE on each day in which Offered Shares are sold through them as agent under the Sales Agreement. Each confirmation will include the number of Offered Shares sold on that day, the average price realized from the sale of the Offered Shares on the NYSE, the compensation payable to the Agents and the net proceeds to the Company.

Settlement for the sales of the Offered Shares will occur, unless the parties agree otherwise, on the second trading day following the date on which any sales were made in return for payment of the net proceeds to the Company. There is no agreement for funds to be received in an escrow, trust or similar arrangement. Sales of Offered Shares as contemplated in this Prospectus Supplement will be settled through the facilities of The Depository Trust Company in the United States, or by such other means as the Company and the Agents may agree upon.

Cantor Fitzgerald & Co. and B. Riley Securities, Inc. are not registered as investment dealers in any Canadian jurisdiction and, accordingly, will only sell the Offered Shares in the United States, and will not, directly or indirectly, solicit offers to purchase or sell the Offered Shares in Canada. Subject to applicable laws, the Agents may offer the Offered Shares outside of Canada and the United States.

In connection with the sales of the Offered Shares on the Company’s behalf, each of the Agents will be deemed to be an “underwriter” within the meaning of the U.S. Securities Act, and the compensation paid to the Agents will be deemed to be underwriting commissions or discounts. The Company has agreed in the Sales Agreement to provide indemnification and contribution to the Agent against certain liabilities, including liabilities under the U.S. Securities Act. In addition, the Company has agreed, under certain circumstances, to reimburse the reasonable fees and disbursements of the Agents’ legal counsel and the Agents’ other advisors in connection with this Offering. The expenses of the Offering, excluding commissions payable to the Agents under the Sales Agreement, are estimated to be approximately US$250,000.

The Agents will not engage in any transactions that stabilize the price of the Common Shares. No underwriter or dealer involved in the distribution, no affiliate of such an underwriter or dealer and no person or company acting jointly or in concert with such an underwriter or dealer has over-allotted, or will over allot, securities in connection with the distribution or has effected, or will effect, any other transactions that are intended to stabilize or maintain the market price of the Common Shares.

The Offering pursuant to the Sales Agreement will terminate on the earlier of: (i) the termination of the Sales Agreement; (ii) the issuance and sale of all the Offered Shares subject to the Sales Agreement; or (iii) the date the receipt for the Prospectus ceases to be effective. The Company and the Agents may each terminate the Sales Agreement at any time upon ten days’ prior notice or by either Agent at any time in certain circumstances, including the occurrence of a material and adverse change in the Company’s business or financial condition that makes it impractical or inadvisable to market the Company’s common shares or to enforce contracts for the sale of the Company’s common shares.

S-7

This Prospectus Supplement and the Prospectus may be made available in electronic format on the websites maintained by the Agents or their U.S. affiliates participating in the Offering. Other than the Prospectus Supplement and Prospectus in electronic format, the information on these websites is not part of this Prospectus Supplement or the Registration Statement of which this Prospectus Supplement forms a part, has not been approved or endorsed by the Company or the Agents in their capacity as agents, and should not be relied upon by investors.

Certain of the Agents and its affiliates have provided in the past to the Company and its affiliates, and may provide from time to time in the future, various investment banking, commercial banking, financial advisory and other financial services for the Company and its affiliates, for which services they have received, and may continue to receive in the future, customary fees and commissions. To the extent required by Regulation M, the Agents will not engage in any market making activities involving the Common Shares, while the Offering is ongoing under this Prospectus Supplement. However, from time to time, the Agents and its U.S. affiliates may have effected transactions for their own account or the account of customers, and hold on behalf of themselves or their customers, long or short positions in the Company’s equity securities, and may do so in the future.

The Company has applied to the TSX to conditionally approve the listing of the Offered Shares offered by this Prospectus Supplement. Listing is subject to us fulfilling all of the requirements of the TSX, which cannot be assured. NYSE approval is not required for the listing of the Offered Shares offered hereunder.

DESCRIPTION OF SECURITIES BEING DISTRIBUTED

The Company is authorized to issue an unlimited number of Common Shares without par value and an unlimited number of preferred shares, issuable in series, of which at January 5, 2023, 81,330,012 Common Shares were issued and outstanding and no preferred shares were issued and outstanding.

The holders of the Common Shares are entitled to receive notice of and to attend all meetings of the shareholders of the Company and each Common Share confers the right to one vote in person or by proxy at all meetings of the shareholders of the Company. The holders of the Common Shares, subject to the prior rights, if any, of the holders of any other class of shares of the Company, are entitled to receive such dividends in any financial year as the board of directors of the Company may by resolution determine. In the event of the liquidation, dissolution or winding-up of the Company, whether voluntary or involuntary, the holders of the Common Shares are entitled to receive, subject to the prior rights, if any, of the holders of any other class of shares of the Company, the remaining property and assets of the Company.

The directors of the Company are authorized to create series of preferred shares in such number and having such rights and restrictions with respect to dividends, rights of redemption, conversion or repurchase and voting rights as may be determined by the directors and shall have priority over the Common Shares to the property and assets of the Company in the event of liquidation, dissolution or winding-up of the Company.

S-8

Common Shares

During the 12-month period before the date of this Prospectus Supplement, the Company issued the following Common Shares:

| DATE OF ISSUE | TYPE OF SECURITY | NUMBER OF SECURITIES | ISSUE OR EXERCISE PRICE PER SECURITY | NATURE OF ISSUE | ||||||||

| January 3, 2022 | Common Shares | 10,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| March 2, 2022 | Common Shares | 10,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| March 3, 2022 | Common Shares | 10,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| March 4, 2022 | Common Shares | 10,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| March 7, 2022 | Common Shares | 20,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| March 8, 2022 | Common Shares | 25,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| March 8, 2022 | Common Shares | 12,500 | $ | 15.46 | Exercise of Stock Options | |||||||

| March 15, 2022 | Common Shares | 20,000 | $ | 15.46 | Exercise of Stock Options | |||||||

| March 15, 2022 | Common Shares | 800 | $ | 23.05 | Conversion of Restricted Share Units | |||||||

| April 1, 2022 | Common Shares | 50,000 | $ | 15.46 | Exercise of Stock Options | |||||||

| April 5, 2022 | Common Shares | 3,334 | $ | 13.14 | Exercise of Stock Options | |||||||

| April 13, 2022 | Common Shares | 5,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| April 18, 2022 | Common Shares | 10,000 | $ | 15.46 | Exercise of Stock Options | |||||||

| April 21, 2022 | Common Shares | 123,000 | $ | 26.08 | Conversion of Restricted Share Units | |||||||

| April 22, 2022 | Common Shares | 173 | $ | 13.14 | Exercise of Stock Options | |||||||

| June 23, 2022 | Common Shares | 5,000 | $ | 17.36 | Conversion of Restricted Share Units | |||||||

| August 31, 2022 | Common Shares | 10,000 | $ | 16.95 | Conversion of Restricted Share Units | |||||||

| September 6, 2022 | Common Shares | 5,000 | $ | 15.79 | Conversion of Restricted Share Units | |||||||

| October 14, 2022 | Common Shares | 100,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| October 21, 2022 | Common Shares | 5,000 | $ | 15.19 | Conversion of Restricted Share Units | |||||||

| November 22, 2022 | Common Shares | 5,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| November 24, 2022 | Common Shares | 5,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 1, 2022 | Common Shares | 7,800 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 2, 2022 | Common Shares | 2,300 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 6, 2022 | Common Shares | 10,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 8, 2022 | Common Shares | 90,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 9, 2022 | Common Shares | 57,291 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 12, 2022 | Common Shares | 37,436 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 13, 2022 | Common Shares | 25,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 14, 2022 | Common Shares | 15,000 | $ | 13.14 | Exercise of Stock Options | |||||||

| December 21, 2022 | Common Shares | 146,300 | $ | 21.97 | Private placement of British Columbia super flow-through Common Shares | |||||||

| December 21, 2022 | Common Shares | 196,900 | $ | 24.39 | Private placement of British Columbia critical mineral exploration flow-through Common Shares | |||||||

| December 21, 2022 | Common Shares | 332,200 | $ | 21.09 | Private placement of Canadian federal flow-through Common Shares | |||||||

| January 1, 2022 to Present | Common Shares | 998,629 | (1) | $ | 22.82 | (1) | At-The-Market Distributions(1) | |||||

| (1) | During the twelve months ended December 31, 2022, the Company issued 998,629 Common Shares, at an average selling price of $22.82 per share, for net proceeds of $22.3 million under Company’s At-The-Market offering. |

S-9

Stock Options

During the 12-month period before the date of this Prospectus Supplement, the Company has not granted any stock options.

As of the date hereof, there are options outstanding to purchase 477,500 Common Shares at exercise prices ranging from C$15.46 to C$17.72 with expiry dates ranging from October 2023 to June 2024.

Restricted Share Units (“RSUs”)

During the 12-month period before the date of this Prospectus Supplement, the Company granted 310,266 RSUs with varying terms and vesting criteria as follows:

| a. | 37,500 RSUs granted to non-executive directors vesting on the earlier of December 12, 2025 and the date the director ceases to serve as a director; |

| b. | 58,066 RSUs granted to executives which vest on the Company submitting its application to the EAO seeking a determination that construction of the KSM Project has been “substantially started”, all of which expire on December 12, 2025 if they have not vested by such date; |

| c. | 174,200 RSUs granted to executives of which 116,133 RSUs vest on the Company announcing a joint venture agreement or other transformative transaction affecting the ownership and control of the KSM Project and 58,067 RSUs vest on the Company receiving a decision from the EAO that construction of the KSM Project has been “substantially started”, all of which expire on December 12, 2027 if they have not vested by such date; |

| d. | 40,500 RSUs granted to employees vesting as to 1/3rd on each of the December 12, 2023, December 12, 2024 and December 12, 2025. |

25,000 RSUs that were granted in 2021 remain outstanding and vest between June and October of 2023. As of the date hereof, there are 335,266 RSUs outstanding.

The Common Shares are listed on the TSX under the symbol “SEA” and the NYSE under the symbol “SA”. The following table sets forth, for the 12 month period prior to the date of this Prospectus Supplement, details of the trading prices and volume on a monthly basis of the Common Shares on the TSX and NYSE, respectively:

| Toronto Stock Exchange | NYSE | |||||||||||||||||||||||

| Period | Volume | High (CDN$) | Low (CDN$) | Volume | High (US$) | Low (US$) | ||||||||||||||||||

| 2022 | ||||||||||||||||||||||||

| January | 1,152,642 | 21.85 | 18.85 | 6,175,186 | 17.45 | 14.85 | ||||||||||||||||||

| February | 1,347,587 | 22.43 | 19.17 | 5,937,587 | 17.42 | 15.08 | ||||||||||||||||||

| March | 2,449,262 | 25.00 | 21.76 | 10,685,723 | 19.90 | 17.04 | ||||||||||||||||||

| April | 1,445,726 | 28.00 | 22.00 | 7,435,618 | 22.22 | 17.21 | ||||||||||||||||||

| May | 1,833,107 | 23.62 | 17.49 | 7,197,946 | 18.39 | 13.42 | ||||||||||||||||||

| June | 1,439,429 | 19.62 | 15.90 | 5,939,425 | 15.60 | 12.32 | ||||||||||||||||||

| July | 1,628,226 | 17.79 | 14.28 | 7,637,461 | 13.89 | 10.94 | ||||||||||||||||||

| August | 1,134,908 | 18.49 | 15.79 | 4,705,135 | 14.38 | 12.03 | ||||||||||||||||||

| September | 1,504,505 | 17.32 | 14.25 | 7,358,644 | 13.37 | 10.35 | ||||||||||||||||||

| October | 929,671 | 18.01 | 14.50 | 5,266,287 | 13.22 | 10.63 | ||||||||||||||||||

| November | 1,359,547 | 17.27 | 13.83 | 5,974,423 | 12.78 | 10.03 | ||||||||||||||||||

| December | 1,610,521 | 17.59 | 14.99 | 7,106,118 | 13.12 | 10.97 | ||||||||||||||||||

| 2023 | ||||||||||||||||||||||||

| January 1 to January 5 | 292,222 | 18.65 | 17.19 | 925,474 | 13.85 | 12.58 | ||||||||||||||||||

On January 5, 2023 the last trading day of the Common Shares prior to the date of this Prospectus Supplement, the closing price of the Common Shares on the TSX was C$18.49 and on the NYSE was US$13.63.

S-10

CERTAIN UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS

The following is a general summary of the U.S. federal income tax considerations applicable to a U.S. Holder (as defined below) arising from the acquisition of Common Shares pursuant to the Offering and the ownership and disposition of the Common Shares. This summary applies only to U.S. Holders who hold Common Shares as capital assets (generally, property held for investment) and who acquire Common Shares at their original issuance pursuant to the Offering and does not apply to any subsequent U.S. Holder of a Common Share.

This summary is for general information purposes only. It is not a complete analysis or description of all potential U.S. federal income tax considerations that may apply to a U.S. Holder as a result of the ownership and disposition of Common Shares. In addition, this summary does not take into account the individual facts and circumstances of any particular U.S. Holder that may affect the U.S. federal income tax consequences to such U.S. Holder, including specific tax consequences to a U.S. Holder under an applicable tax treaty. Accordingly, this summary is not intended to be, and should not be construed as, legal or U.S. federal income tax advice with respect to any particular U.S. Holder. In addition, this summary does not address the U.S. federal alternative minimum, U.S. federal estate and gift, U.S. state and local, or non-U.S. tax consequences of the acquisition, ownership, or disposition of Common Shares. Except as specifically set forth below, this summary does not discuss applicable tax reporting requirements. Each U.S. Holder should consult its own tax advisor regarding all U.S. federal, U.S. state and local and non-U.S. tax consequences of the acquisition, ownership, or disposition of Common Shares.

No opinion from U.S. legal counsel or ruling from the Internal Revenue Service (the “IRS”) has been requested, or will be obtained, regarding the U.S. federal income tax consequences of the acquisition, ownership, or disposition of Common Shares. This summary is not binding on the IRS, and the IRS is not precluded from taking a position that is different from, and contrary to, any position taken in this summary. In addition, because the authorities upon which this summary is based are subject to various interpretations, the IRS and the U.S. courts could disagree with one or more of the positions taken in this summary.

Scope of This Disclosure

Authorities

This summary is based on the Internal Revenue Code of 1986, as amended (the “Code”), Treasury Regulations (whether final, temporary, or proposed), published rulings of the IRS, published administrative positions of the IRS, the Convention Between Canada and the United States of America with Respect to Taxes on Income and on Capital, signed September 26, 1980, as amended (the “Canada- U.S. Tax Convention”), and U.S. court decisions that are applicable and, in each case, as in effect and available, as of the date hereof. Any of the authorities on which this summary is based could be changed in a material and adverse manner at any time, and any such change could be applied on a retroactive or prospective basis which could affect the U.S. federal income tax considerations described in this summary. This summary does not discuss the potential effects, whether adverse or beneficial, of any proposed legislation that, if enacted, could be applied on a retroactive or prospective basis.

U.S. Holders

For purposes of this summary, the term “U.S. Holder” means a beneficial owner of Common Shares that is for U.S. federal income tax purposes:

| ● | An individual who is a citizen or resident of the United States; |

| ● | A corporation (or other entity taxable as a corporation for U.S. federal income tax purposes) created or organized in or under the laws of the United States, any state thereof or the District of Columbia; |

| ● | An estate the income of which is subject to U.S. federal income taxation regardless of its source; or |

| ● | A trust that (a) is subject to the primary supervision of a court within the United States and the control of one or more U.S. persons for all substantial decisions or (b) has a valid election in effect under applicable Treasury Regulations to be treated as a U.S. person. |

S-11

Non-U.S. Holders

For purposes of this summary, a “non-U.S. Holder” is a beneficial owner of Common Shares that is not a partnership (or other “pass-through” entity) for U.S. federal income tax purposes and is not a U.S. Holder. This summary does not address the U.S. federal income tax considerations applicable to non-U.S. Holders arising from the acquisition, ownership, or disposition of Common Shares.

Accordingly, a non-U.S. Holder should consult its own tax advisor regarding all U.S. federal, U.S. state and local, and non-U.S. tax consequences (including the potential application of and operation of any income tax treaties) relating to the purchase of the Common Shares pursuant to the Offering and the acquisition, ownership, or disposition of Common Shares.

Transactions Not Addressed

This summary does not address the tax consequences of transactions effected prior or subsequent to, or concurrently with, any purchase of the Offered Shares (whether or not any such transactions are undertaken in connection with the purchase of the Offered Shares), other than the U.S. federal income tax considerations to U.S. Holders of the acquisition of Offered Shares and the ownership and disposition of such Offered Shares.

U.S. Holders Subject to Special U.S. Federal Income Tax Rules Not Addressed