Exhibit

99.1

ANNUAL

INFORMATION

FORM

FOR

THE YEAR ENDED

DECEMBER

31, 2021

DATED

MARCH 24, 2022

TABLE

OF CONTENTS

Contents

PRELIMINARY

NOTES

Date

of Information

The

information in this Annual Information Form (“AIF”) is presented as of December 31, 2021 unless specified otherwise.

Reporting

Currency

All

dollar amounts are expressed in Canadian dollars unless otherwise indicated. The Issuer’s quarterly and annual financial statements

are presented in Canadian dollars.

Units

of Measure

In

this AIF a combination of Imperial and metric measures are used with respect to the Issuer’s mineral properties. Conversion rates

from Imperial measure to metric and from metric to Imperial are provided below:

| Imperial Measure = Metric Unit |

Metric Measure = Imperial Unit |

| 2.47 acres |

1 hectare (h) |

0.4047 hectares |

1 acre |

| 3.28 feet |

1 meter (m) |

0.3048 meters |

1 foot |

| 0.62 miles |

1 kilometer (km) |

1.609 kilometers |

1 mile |

| 0.032 ounces (troy) (oz) |

1 gram (g) |

31.1035 grams |

1 ounce (troy) |

| 1.102 tons (short) |

1 tonne (t) |

0.907 tonnes |

1 ton |

| 0.029 ounces (troy)/ton |

1 gram/tonne (g/t) |

34.28 grams/tonne |

1 ounce (troy/ton) |

Abbreviations

of unit measures are used in this AIF in addition to those in brackets in the table above as follows:

| Bt

- Billion tonnes |

Ga

– Giga-annum |

kWh

- Kilowatt hours |

Mlb

- Million pounds |

| Mm³

- Million cubic meters |

Moz

- Million ounces |

m/s

- Meters per second |

Mt

- Million tonnes |

| MWh

- Megawatt hours |

ppm

- Parts per million |

tpd

– tonnes per day |

W/m²-

Watt per square meter |

See

“Glossary of Technical Terms” for a description of some important technical terms used in this AIF.

Cautionary

Note to United States Investors Regarding Resource Estimates

This

AIF has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements

of United States securities laws. Mineral resource estimates included in this AIF and in any document incorporated by reference herein

or therein have been prepared in accordance with, and use terms that comply with, the reporting standards in accordance with Canadian

National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed

by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical

information concerning mineral projects. In accordance with NI 43-101, the Issuer uses the terms mineral reserves and resources as they

are defined in accordance with the CIM Definition Standards on mineral reserves and resources (the “CIM Definition Standard”)

adopted by the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”).

The

U.S. Securities and Exchange Commission (the “SEC”) has adopted amendments to its disclosure rules to modernize the

mineral property disclosure requirements for issuers whose securities are registered with the SEC under the Exchange Act. These amendments

became effective February 25, 2019 (the “SEC Modernization Rules”) and have replaced the historical property disclosure

requirements for mining registrants that were included in SEC Industry Guide 7. As a foreign private issuer that files its annual report

on Form 40-F with the SEC pursuant to the multi-jurisdictional disclosure system (“MJDS”), the Issuer is not required

to provide disclosure on its mineral properties under the SEC Modernization Rules and will continue to provide disclosure under NI 43-101

and the CIM Definition Standards. However, if the Issuer either ceases to be a “foreign private issuer” or ceases to be entitled

to file reports under the MJDS, then the Issuer will be required to provide disclosure on its mineral properties under the SEC Modernization

Rules.

Accordingly,

United States investors are cautioned that the disclosure the Issuer provides on its mineral properties in this AIF and under its continuous

disclosure obligations under the Exchange Act may be different from the disclosure that the Issuer would otherwise be required to provide

as a U.S. domestic issuer or a non-MJDS foreign private issuer under the SEC Modernization Rules.

The

SEC Modernization Rules include the adoption of terms describing mineral reserves and mineral resources that are substantially similar

to the corresponding terms under the CIM Definition Standards. As a result of the adoption of the SEC Modernization Rules, the SEC will

now recognize estimates of “measured mineral resources,” “indicated mineral resources” and “inferred mineral

resources.” In addition, the SEC has amended its definitions of “proven mineral reserves” and “probable mineral

reserves” to be substantially similar to the corresponding CIM Definition Standards.

United

States investors are cautioned that while the above terms are substantially similar to CIM Definition Standards, there are differences

in the definitions under the SEC Modernization Rules and the CIM Definition Standards. Accordingly, there is no assurance any mineral

reserves or mineral resources that the Issuer may report as “proven reserves,” “probable reserves,” “measured

mineral resources,” “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would

be the same had the Issuer prepared the reserve or resource estimates under the standards adopted under the SEC Modernization Rules.

United

States investors are also cautioned that while the SEC will now recognize “measured mineral resources,” “indicated

mineral resources” and “inferred mineral resources,” investors should not assume that any part or all of the mineralization

in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. Mineralization described

using these terms has a greater amount of uncertainty as to their existence and feasibility than mineralization that has been characterized

as reserves. Accordingly, investors are cautioned not to assume that any “measured mineral resources,” “indicated mineral

resources,” or “inferred mineral resources” that the Issuer reports are or will be economically or legally mineable.

Further,

“inferred resources” have a greater amount of uncertainty as to their existence and as to whether they can be mined legally

or economically. Therefore, United States investors are also cautioned not to assume that all or any part of the inferred resources exist.

In accordance with Canadian rules, estimates of “inferred mineral resources” cannot form the basis of feasibility or other

economic studies, except in limited circumstances where permitted under NI 43-101.

Accordingly,

information contained in this AIF and the portions of documents incorporated by reference herein contain descriptions of the Issuer’s

mineral deposits that may not be comparable to similar information made public by U.S. companies who prepare their disclosure in accordance

with U.S. federal securities laws and the rules and regulations thereunder.

Seabridge

Gold Inc.

ANNUAL

INFORMATION FORM

| ITEM

1: | CORPORATE

STRUCTURE |

Incorporation

of the Issuer

Seabridge

Gold Inc. (the “Issuer” or “Seabridge”) was incorporated under the Company Act (British

Columbia) on September 14, 1979 under the name of Chopper Mines Ltd., which was subsequently changed to Dragoon Resources Ltd. on November

9, 1984, and then changed again to Seabridge Resources Inc. on May 20, 1998. On June 20, 2002, the Issuer changed its name to “Seabridge

Gold Inc.” and on October 31, 2002, the Issuer was continued under the Canada Business Corporations Act.

The

Issuer’s corporate offices are located at 106 Front Street East, 4th Floor, Toronto, Ontario, Canada M5A 1E1. The Issuer’s

telephone number is (416) 367-9292. The Issuer’s Shares are currently listed for trading on the Toronto Stock Exchange (the “TSX”)

under the symbol “SEA” and on the New York Stock Exchange (the “NYSE”) under the symbol “SA”.

The Issuer’s registered office is located at 10th Floor, 595 Howe Street, Vancouver, British Columbia, Canada V6C 2T5.

Intercorporate

Relationships

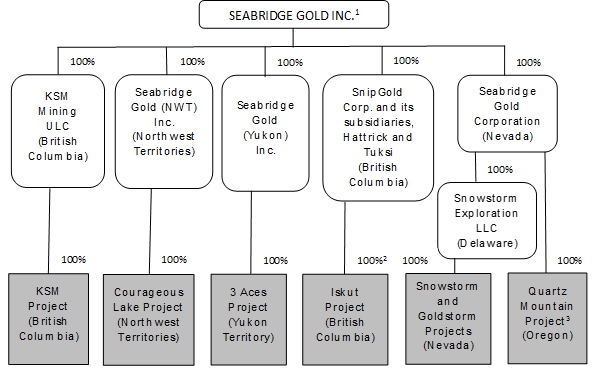

The

Issuer presently has twelve wholly-owned subsidiaries: KSM Mining ULC, Seabridge Gold (KSM) Inc., SnipGold Corp., Hattrick Resources

Corp. (“Hattrick”) and Tuksi Mining & Development Company Ltd. (“Tuksi”), companies incorporated

under the laws of British Columbia, Canada; Seabridge Gold (NWT) Inc., a company incorporated under the laws of the Northwest Territories

of Canada; Seabridge Gold (Yukon) Inc., incorporated under the laws of Yukon; Seabridge Gold Corporation, Pacific Intermountain Gold,

Corporation, 5555 Gold Inc. and 5555 Silver Inc., each Nevada Corporations; and Snowstorm Exploration LLC, a Delaware limited liability

corporation. The following diagram illustrates the inter-corporate relationship between the Issuer, its active subsidiaries and its projects

as of December 31, 2021.

| 1. | Certain

of the Issuer’s subsidiaries have been omitted from the chart as they own no property. |

| 2. | SnipGold,

through Hattrick, owns 95% of 12 of the claims covering an area of approximately 4,339 ha,

which claims are located in the northwest corner of the property and outside of the area

of current exploration activities. |

| 3. | The

Issuer has entered into option agreements under which a 100% interest in the Quartz Mountain

Project may be acquired by a third party. |

| ITEM

2: | GENERAL

DEVELOPMENT OF THE BUSINESS |

Overview

Since

1999, Seabridge has taken steps to achieve its goal of providing strong returns to shareholders by maximizing leverage to the price of

gold. The Issuer’s strategy to achieve this goal is to optimize gold ownership per Common share by increasing gold resources more

rapidly than shares outstanding. This ratio of gold ownership per Common share has provided a simple but effective measure for evaluating

dollars spent on behalf of shareholders.

In

1999, management decided that Seabridge’s strategic focus would be on acquiring, exploring and advancing gold deposits. Seabridge

determined it would not build or operate mines, but that it would look to partner or sell assets that were advancing toward production.

In the Issuer’s view, building mines adds considerable technical and financial risks and requires a different set of skills and

resources. Seabridge also decided it would prioritize exploration projects with known gold deposits but exploration upside to reduce

risk in terms of trying to achieve a growing ratio of gold ownership per Common share. The Issuer therefore narrowed the activities it

would undertake to the following three phases, which phases it planned to progress through in the order set forth below and in response

to increases in the price of gold: (i) acquiring known gold deposits, (ii) expanding the deposits, and (iii) advancing its deposits towards

a construction decision by defining the economic parameters of the deposits through engineering studies, upgrading mineral resources

to reserves, securing permits for undertaking mining operations and building relationships with local communities and indigenous groups.

The Issuer believed this was a relatively lower-risk and less capital-intensive strategy consistent with the goal of optimizing gold

ownership per Common share.

In

1999, Seabridge set out to buy gold deposits in North America that were not economic in a low gold price environment. North America was

selected as the preferred jurisdiction because of its established mineral tenure and permitting procedures, political stability and infrastructure

advantages. At that time, many projects were for sale at distressed prices as producers struggled to stay in business. Seabridge decided

it would acquire projects with three main characteristics:

| 1. | Proven

resources with quality work done by reputable companies; |

| 2. | Upside

exploration potential; and |

| 3. | Low

holding costs to conserve cash in the event that a higher gold price was not achieved. |

From

1999 to 2002, Seabridge acquired eight deposits with gold resources in North America, paying less than US$1.00 per ounce of resource

(using aggregate ounces from all resource categories) and has been paying less than US$0.10 per ounce per year in holding costs. Previous

owners had spent an estimated US$300 million exploring and developing these deposits.

By

2002, with the gold price on the rise, the Issuer believed that it was becoming more expensive to acquire existing resources, and the

cost-benefit equation tilted in favor of increasing gold ownership through exploration. Seabridge’s strategy entered its second

phase, which was to expand the Issuer’s resource base by carefully targeted exploration. It has continued exploring even after

it moved to the third phase and these efforts have proved highly successful, with measured and indicated gold resources now totaling

88.2 million ounces with an additional 70.8 million ounces of gold in the inferred resource category (see Mineral Resources Table on

page 11) against a backdrop of only 78.98 million shares outstanding.

By

2008, the gold price had risen sufficiently to make Seabridge think that a number of its projects might be economic. Therefore Seabridge

began work on the third phase of its strategy: defining the economics of its projects through engineering studies, upgrading resources

to reserves, securing permits and building support for the its projects in local communities. This effort focused on the KSM Project,

which, during the exploration phase, had emerged as the Issuer’s most important asset. The permitting process began and the Issuer

undertook substantial infill drilling programs to raise the confidence level in the project’s resources. The Issuer completed its

initial Preliminary Feasibility Study for the KSM Project in March 2010, which was updated in June, 2011. The Issuer then undertook further

optimization work at the KSM Project and revised its project design based on input received from regulatory authorities and local indigenous

groups during a joint harmonized environmental assessment process managed by the Province of British Columbia and Canada, but which also

included an assessment by the Nisga’a Nation and participation of Alaskan State and Federal regulators. This work is reflected

in the third Preliminary Feasibility Study for the KSM Project completed in June 2012. The Issuer submitted its Environmental Impact

Statement/Environmental Assessment Application (the “EA Application and EIS”) in the first quarter of 2013, it was

accepted for formal review by British Columbia in August, 2013 and it was approved by both the federal and provincial authorities in

2014. The provincial EA Certificate was originally approved for a five-year term and was renewed for a further five years on March 21,

2019. A 2-year extension of the EA Certificate was granted in 2021 in recognition of the delays in work at the KSM Project arising from

compliance with restrictions relating to the COVID-19 pandemic and, as a result, the term of the EA Certificate now expires on July 29,

2026. The EA Application and EIS is based on the KSM Project design in the 2012 KSM Preliminary Feasibility Study.

In

conjunction with advancing the EA Application and EIS, the Issuer worked to build its relationships with the Nisga’a Nation,

the Tahltan Nation and other indigenous groups, including pursuing impacts and benefits agreements. In June, 2014, the Issuer and the

Nisga’a Nation entered into a Benefits Agreement. In September, 2013, the Gitxsan Treaty Society, representing the Gitxsan

Hereditary Chiefs, delivered a letter to regulators expressing its support of Seabridge Gold’s KSM Project. In June, 2014, the Issuer

entered into an environmental agreement with the Gitanyow Hereditary Chiefs Office and the wilps represented by Gitanyow Hereditary

Chiefs Office. Although these were important for the Issuer’s success in getting its environmental assessment approvals, work to

maintain and improve these relationships, as well as relationships with the other indigenous groups in the area is ongoing. The Issuer

holds an annual environmental workshop with indigenous groups and regulators to review results of the previous year’s environmental

studies and to communicate planned studies for the upcoming year. The Issuer also observes a process of review of each permit application

with indigenous groups, with an initial phase of review taking place before submission of the application and a second phase with the

relevant regulator and indigenous groups after permit submission. In addition, in 2019, the Issuer entered into an impacts and benefits

agreement with the Tahltan Nation. Alaskan State and US federal regulators also participated in the EA Application and EIS review process,

providing input throughout, and continue to be involved in permitting review associated with the KSM Project due to the location of the

project within a transboundary drainage basin, even though there are no Alaskan regulatory authorizations required. Now that the Issuer

has started site capture work at KSM it is also making significant efforts to hire indigenous businesses as its contractor for as much

of the work as possible.

In

September, 2014, the Issuer received early-stage construction permits for its KSM Project from the Province of British Columbia. The

permits issued include: (1) authority to construct and use roadways along Coulter Creek and Treaty Creek; (2) rights-of-way for the proposed

Mitchell-Treaty tunnels connecting project facilities; (3) permits for constructing and operating numerous camps required to support

constructions activities; and (4) permits authorizing early-stage construction activities at the mine site and tailings management facility.

In

2010 the Issuer also turned its attention to its second-largest asset, the Courageous Lake Project. A preliminary economic assessment

of this project was completed in early 2008 and indicated that the project’s economics were marginal at the then prevailing gold

price. However, with the increase in the gold price by 2010, the Issuer decided to start taking the Courageous Lake Project along a similar

advancement path to the KSM Project, including additional drilling and further engineering work, and completed a preliminary feasibility

study in September, 2012.

In

2012 the Issuer refocused its exploration activities and began undertaking drilling of new targets at both the KSM Project, in search

of higher grade core zones, and the Courageous Lake Project, in search of deposits of higher grade material, that could improve the economics

of each project. The exploration programs in the 2012 to 2018 seasons were very successful, with the generation of successive resource

estimates for the Kerr deposit and the Iron Cap deposit at the KSM Project and a resource estimate at the Walsh Lake deposit at the Courageous

Lake Project. After its successful drill programs in 2013, 2014 and 2015 that dramatically increased inferred resources below the Kerr

deposit, the Issuer decided to update its 2012 PFS to use current costs and incorporate commitments from the EA Application and EIS and

to include in the report a preliminary economic assessment of the KSM Project presenting an alternative development plan incorporating

the expanded Kerr deposit into a conceptual project design. The updated report was completed in 2016 and showed a modest decline in the

economics of the PFS development plan but improved economics from the alternative development plan that incorporated the new mineral

resources at Kerr. Exploration programs in 2016, 2017 and 2018 have led to a dramatic increase in mineral resources at Iron Cap, which

now total 423 million tonnes in the indicated category and 1.9 billion tonnes in the inferred category. Now the Issuer believes that,

due to the Iron Cap deposit’s proximity to the MTT and its higher grade, Iron Cap could potentially improve KSM’s economics

by mining it before the Kerr deposit.

After

several years of declines in the price of gold, in late 2015 the Issuer decided to look once again for opportunities to acquire gold

properties as they were becoming available at more attractive prices. Since the Issuer had become much larger than it was in the 1999-2002

period when it was first acquiring properties, it has focused on identifying properties with potential for major deposits but accepted

that reasonably priced properties that satisfied its size objective may have limited, or no, mineral resources. In April, 2016, the Issuer

reached an agreement to acquire SnipGold Corp., the owner of the highly prospective Iskut Project, and completed the acquisition in June

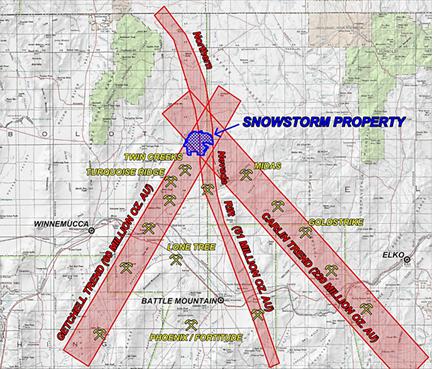

2016. In February, 2017, the Issuer announced that it had entered into a letter of intent to acquire the Snowstorm Project in Northern

Nevada and completed the acquisition in June, 2017. In June, 2019, the Issuer reach an agreement for the acquisition of the Goldstorm

Project, located about 3 km to the east of its Snowstorm Project. At the end of March, 2020 the Issuer announced that it had agreed to

acquire the 3 Aces Project located in the southeastern Yukon and completed the acquisition in May, 2020. The Issuer continues to look

for opportunities to acquire gold properties that meet its criteria.

Each

year from 2017 to 2021 the Issuer undertook exploration programs at its Iskut and Snowstorm Projects. At Iskut, its recent work has found

indications of higher grade copper mineralization and many of the characteristics associated with a large porphyry system below the drilling

to date. Exploration in 2022 will be focused on the area below the previous drilling. At Snowstorm, drilling of newly defined structural

features in favourable stratigraphic host rocks began in the second half of 2020 and is continuing. Drilling in 2020 confirmed the target

stratigraphy and extensions of the Getchell structural setting present at the Turquoise Ridge and Twin Creeks mines, which are located

a few kilometers to the south.

To

date, work on the KSM Project and the Courageous Lake Project has been funded in part by the sale of, or the optioning of, non-core assets,

consistent with the Issuer’s strategy of limiting share dilution. The Issuer has sold the Noche Buena Project and its early-stage

Nevada properties and entered into option agreements in respect of each of the Grassy Mountain, Red Mountain, Quartz Mountain and Castle

Black Rock projects under which the respective optionees could acquire a 100% interest in such properties. The Grassy Mountain project

was sold in February, 2013 upon exercise of the option to acquire a 100% interest in the Grassy Mountain property granted by the Issuer

in 2011. In February, 2017, the option to acquire a 100% interest in the Castle Black Rock Project was exercised and the Project was

sold. In May, 2017, the holder of the option on the Red Mountain Project acquired the Project from the Issuer and in April, 2021 the

Issuer sold its final residual interests in the Red Mountain Project. In addition to the proceeds received on the sale of these Projects,

the Issuer has the potential to receive additional payments in respect of the Grassy Mountain and Quartz Mountain Projects in the form

of a net profits royalty (Grassy Mountain) and an option payment and either $15 million or a net smelter returns royalty (Quartz Mountain).

Seabridge

intends to seek a sale or joint venture of its two core assets, the KSM Project and the Courageous Lake Project, or a sale of the Issuer.

At KSM it is continuing work to improve the economics of the project and advancing with site capture work. As a result of its search

for high grade core zones at the KSM Project from 2013 to 2020, the Issuer has broadened the Project’s economic profile. Before

finding the higher grade mineralized zones below the Kerr deposit and the Iron Cap deposit, KSM was a gold project with a robust copper

credit that would appeal primarily to gold miners as prospective partners. Now, KSM has a much stronger copper profile which opens up

the potential for a joint venture with a large base metal producer. In December, 2020, the Issuer completed the acquisition of the Snowfield

Property which lies adjacent to KSM and has the potential to yield a stronger gold profile for the KSM Project. The Snowfield Property,

which the Issuer has now renamed the East Mitchell Property, includes a large gold resource in close proximity to the Mitchell deposit

at the KSM Project. East Mitchell not only has the potential to improve the economics of the KSM Project but also to permit a much longer

initial phase of open-pit mining before capital will need to be spent to build the infrastructure for block cave mining at the Iron Cap

and Kerr deposits. Realizing value for the Issuer’s shareholders depends on the potential financial return for a prospective purchaser

or partner, success in addressing regulatory issues and indigenous peoples’ concerns, market conditions and gold and copper prices.

The timing of a joint venture, partnership or sales agreements, if any, cannot be determined.

The

continuing success of the Issuer is dependent on (1) the ability to continue to raise capital as needed, (2) strength in the price of

gold and copper, (3) retention of the social license to operate its projects, (4) exploration success on projects, and/or (5) advancement

of its projects through optimization work, success in regulatory reviews and in obtaining and retaining permits.

Three

Year History

In

March, 2019, the Issuer’s environmental assessment certificate (the “EAC”) for its KSM Project was extended

to July 29, 2024 by the British Columbia Environmental Assessment Agency. The EAC was issued for an initial five-year term on July 24,

2014. The 2019 extension of the EAC imposed no new terms and conditions on the KSM Project, reflecting the strong environmental protections

of the proposed development plan for the KSM Project. Under the B.C. Environmental Assessment Act, a project’s EAC is subject to

expiry if the project has not been “substantially started” by the deadline specified in the EAC. Once the ‘substantially

started’ designation is achieved, the EAC is no longer subject to expiry.

In

June, 2019, the Issuer announced that it had reached agreement with the Tahltan Nation on the terms of a Co-operation and Benefits Agreement

in respect of the development and operation of the KSM Project. The more than three year process for reaching agreement culminated in

a vote by the Tahltan Nation that approved the agreement by a majority of 77.8%. The agreement represents another important milestone

for the KSM Project and sets forth a thorough and co-operative framework for the parties to work together on the KSM Project.

At

the Iskut Project, 2019 exploration work included geophysical surveys, geochemical sampling and detailed mapping, which suggested a large

intrusive system at depth and confirmed the presence of gold and copper. An aggressive drill testing program was planned at this target

in 2020. Work continued on the remediation of the former Johnny Mountain mine in 2019 with the continuation of in-situ hydrocarbon remediation

at the former tank farm location; relocation of unapproved landfill waste to the approved landfill location; continued clean-up of the

interior of the former mill building; as well as ongoing water quality sampling. A significant waste rock disposal program was first

implemented at the site in 2021 and will be continued in 2022.

The

Issuer’s first drill program at the Snowstorm Project was undertaken in 2019 to test for an extension of the Getchell Trend and

the distinctive structural and stratigraphic features found at the Twin Creeks and Turquoise Ridge mines. The program encountered technical

difficulties but did identify the favourable stratigraphic host for a Getchell-style deposit as well as structures similar to those which

fed the deposits to the south.

The

Issuer acquired the Goldstorm Project in August, 2019. The Goldstorm Project is in northern Nevada, only about 3 km from the Issuer’s

Snowstorm Project. It consists of 134 mining claims and 1,160 acres of leased land in the Northern Nevada Rift, a geologic feature hosting

many high-grade gold-silver mines. Goldstorm has had limited previous exploration, but surface trenching on a northwest trending vein

yielded 3.0 meters of 9.0 g/t gold and 44.0 g/t silver.

In

2020 and 2021, the Issuer continued to advance its KSM Project and further exploration at its other projects, but the scale of work programs

at the KSM site was reduced on account of the COVID-19 pandemic and related restrictions and the pace of advancement has slowed, in part

due to a slowdown in permitting timelines. All of the Issuer’s active projects are located in remote areas of northern Canada,

except for its Snowstorm Project and nearby Goldstorm Project in Nevada. Canadian provinces and territories adopted restrictive operating

regulations for exploration camps to address COVID-19 concerns and travel restrictions not only upon entering Canada but also certain

internal travel restrictions and bans on entering certain provinces or territories. Indigenous communities were particularly vulnerable

to COVID-19 risks for various reasons, including housing shortages resulting in close living conditions as well as the absence of close

access to the healthcare facilities needed to treat more serious COVID-19 illness. Accordingly, the Issuer was very careful in how it

conducted its programs with the goal of not permitting any spread of COVID-19 at its operations, and this goal was achieved in both years.

The

Issuer completed a geotechnical drill program at its KSM project in 2020 along the proposed Mitchell-Treaty tunnels route to confirm

rock composition. The other work on the KSM Project in 2020 involved advancing towards commencement of building onsite infrastructure

to facilitate data collection for a feasibility study in anticipation of securing a partner for the Project.

The

Issuer’s search for large new porphyry targets within the KSM Project continued in 2020 and identified four prospects which can

be tested from the surface but are likely to be evaluated as bulk underground opportunities. In addition, 6,121 m of drilling was completed

in 26 holes within the proposed Sulphurets pit limits at the margins of the deposit. Of the 26 holes drilled, 24 intersected over 1.0

g/t gold material in areas not captured in the existing deposit resource model and the intersections are being evaluated for inclusion

in the resource model.

At

its Iskut Project in 2020, the Issuer completed almost 9,000 m of drilling in 11 holes. Drilling found intervals of higher grade copper

mineralization (e.g. 0.62% copper over 31.8 m) and longer intervals of lower grade copper/gold. The results were consistent with encountering

the outer portions of the alteration halo from a large porphyry system. The results continue to be analysed to plan programs with the

objective of vectoring towards the heart of the system. Work on the reclamation and closure of the Johnny Mountain Mine was scaled back

for 2020 due to COVID-19 related limitations on housing work crews, with work being limited to collection of data and completion of studies.

In

May, 2020, the Issuer acquired the 3 Aces Project, a district scale, orogenic-gold project covering approximately 350 km² and located

in a readily accessible part of southeastern Yukon. The target concept for this project is consistent with some of the biggest and richest

gold deposits in the world, including the California Mother Lode Belt, Juneau Gold Belt, Murentau in Uzbekistan and Obuasi in Ghana.

Historical work has identified a broad area of gold-in-soil extending more than 20 km along strike and recent drilling in the Central

Core Area has progressed to a point where, with additional exploration drilling, the property could potentially advance to an initial

resource with exceptional grade. The Issuer’s work in 2020 on the 3 Aces Project involved assembling the historic data into a 3-dimensional

model and identifying targets to drill in 2021.

In

August, 2020, the Issuer commenced a drill program at its Snowstorm Project to follow-up on the permissive stratigraphic host rocks identified

in its 2019 program. The program is targeting the intersection of these host rocks by fault structures that may have transported gold-bearing

solutions. The program encountered some challenges with drilling conditions and progress was slow, however the program was completed

in the first quarter of 2021 after drilling a total of 4,495 m. In April, 2021, the Issuer reported that its drilling had encountered

a gold-bearing system hosted within similar rocks and structural setting as the Turquoise Ridge Mine and would be evaluating how to use

the results to find higher concentrations of gold.

In

December of 2020, the Issuer completed the acquisition of the East Mitchell Property, which lies immediately to the east of its Mitchell

deposit at its KSM project. The East Mitchell Property hosts a large gold resource and enables new development opportunities for the

KSM Project. The 1.37 billion tonne measured and indicated resource on the East Mitchell Property provides the Issuer with an opportunity,

after detailed analysis of the integration of East Mitchell into the KSM Project, to significantly increase the KSM Project’s proven

and probable reserves. In addition, the resource is near the surface, making it amenable to open pit mining, presenting the opportunity

to defer the more capital-intensive block cave mining considered for the Iron Cap and Kerr deposits with possible improvements to the

KSM Project’s net present value and internal rate of return.

At

the KSM Project, the work for 2021 involved:

| ● | advancing

development of the Project on site-capture construction for achieving ‘substantially started’; |

| ● | completing

data collection in respect of the East Mitchell Property and commencing work on a study of

the integration of the East Mitchell Property into the KSM Project; and |

| ● | continuing

work to meet the Issuer’s obligation under the EAC and collect additional data required

for a feasibility study on the KSM Project. |

| ● | working

with the BC government to secure a further extension to the EA Certificate due to the impacts

of the COVID-19 pandemic |

Work

towards achieving the ‘substantially started’ designation included building construction camps at the beginning of the Coulter

Creek Access Road (the “CCAR”) and beside Highway 37 (Hodder Camp) near the beginning of the Treaty Creek access Road,

preparing the site for construction of its camp facilities in the Mitchell Valley, starting an initial 9 km segment of the CCAR and beginning

construction of the Glacier Creek fish habitat offsetting program. The Issuer reached an agreement with Eskay Mining Corp. under which

Eskay Mining Corp. will fund half the cost of the initial segment of the CCAR up to a maximum of $6.25 million.

In

November, 2021, the Issuer received a two-year extension to its EAC in recognition of the impact of COVID-19 measures it adopted in 2020

and 2021 for the protection of the people and communities of northwestern BC on its schedule for completing work to achieve the ‘substantially

started’ designation. The deadline for achieving ‘substantially started’ is now July 29, 2026. In addition, the Issuer

was issued authorizations from the Department of Fisheries and Oceans for the Glacier, Taft and Treaty Creek fish habitat offsetting

programs.

In

connection with its commencement of these early construction activities at KSM the Issuer has increased its personnel. It is building

a construction management team, expanding its permitting team and brought in human resources professionals. Over the course of 2021,

the Issuer has grown from 7 officers and 28 employees to 10 officers and 41 employees.

The

Issuer drilled 3,484 m on the East Mitchell Property in 2021 and the results have confirmed the East Mitchell geological model and block

grades. The Company now foresees the integration of the East Mitchell deposit into the KSM Project which could enhance gold reserves,

projected annual gold production and payback while extending the period of open pit mining and thereby also deferring and reducing major

capital expenditures associated with blockcave development. The results have also confirmed that the East Mitchell deposit is the upper

part of the Mitchell deposit and has decided to rename it the “East Mitchell deposit” to reflect Mitchell’s continuity.

In

April, 2021, the Issuer announced that it had sold its residual interests in the Red Mountain Project for US$18 million. The interests

sold were the right to a $1.5 million payment due upon achievement of commercial production and a gold stream interest entitling it to

purchase, at US$1,000/oz, 10% of annual gold production up to a maximum of 50,000 ounces.

At

the Iskut Project, the Issuer’s 2021 program focused on the corridor of porphyritic intrusive rock endowed with gold and copper

identified in 2020 drilling and started with a magnetotelluric survey. Drilling began in August on the target emerging from its analysis

of collected data which points to a coherent zone for the gold-copper porphyry source below the Quartz Rise Lithocap. The Company encountered

difficulties in its drilling program, with poor weather impacting drilling productivity. Results from the drill hole continue to be evaluated

to refine the target concept. The Issuer also continued its reclamation work at the old Johnny Mountain Mine site on its Iskut Project.

The

2021 exploration program at 3Aces commenced with line cutting to support a geophysical survey. A CSAMT geophysical program was also completed.

This work was designed to allow the Issuer to build a 3-D earth image to integrate with historical drilling. The aim of this initial

work is to expand high-grade gold targets previously identified and detect new targets for initial drill testing. Drill testing was planned

for later in the year but permitting delays resulted in the Issuer not being able to start its planned drill program.

The

2021 exploration program at Snowstorm commenced in August, 2021 and followed-up on the gold bearing structures identified in 2020 and

was designed to off-set these previous intersections toward a structure with a topographic expression which is projected into the Paleozoic

section using magnetotelluric (MT) geophysical readings. The surface expression of this structure has produced a significant arsenic

in soil anomaly. As of the date of this AIF this drill program is not yet complete and the Company has experienced delays in receiving

results from assay labs.

In

December, 2021, the Issuer also filed its first comprehensive Sustainability Report detailing the Company’s approach and progress

towards integrating sustainability into its business. The report was prepared with select disclosures and guidance from the Sustainability

Standards Accounting Board (SASB) Metals and Mining Industry Standards and the Global Reporting Initiative (GRI) Standards, as well as

other metrics developed for its purposes. The Sustainability Report is posted on the Company’s website.

At

the date of this AIF, the Issuer plans exploration work at each of its Iskut, 3 Aces and Snowstorm Projects in 2022. At the Iskut Project,

the 2022 exploration work will focus on drilling the porphyry target further below the Quartz Rise lithocap as well as drilling in the

area of the existing resource at Bronson Slope. The Issuer will also continue with the next year of its planned reclamation and closure

plan for the Johnny Mountain Mine. At 3 Aces, contingent on receipt of permits, the Issuer plans to undertake its first drilling program

on the exploration targets developed from its work to date. At Snowstorm, the Issuer plans a thorough review of exploration results to

date and expansion of the MT surveys before selecting targets for further drilling and to initiate evaluation of the Goldstorm Property.

At

the KSM Project, the Issuer is principally directing in its efforts towards achieving ‘substantially started’, including

completing construction of the Glacier and Taft Creeks fish habitat offsetting ponds, completing the initial 9 km segment of the CCAR,

building the initial 17 km of the Treaty Creek Access Road, including the Bell-Irving River Bridge, construction of a camp near the beginning

of the Treaty Creek Access Road and further construction of the Mitchell Valley camp. In addition, in February, 2022, KSMCo entered into

a Facilities Agreement with British Columbia Hydro and Power Authority (“BC Hydro”) covering the design and construction

of the Treaty Creek Switching Station (the “TCT”) by BC Hydro to supply construction phase hydro-sourced electricity

to the KSM Project. The TCT, located where KSM’s Treaty Creek Access Road meets Highway 37, south of Bell 2, is scheduled to be

completed before the end of 2024. KSMCo has completed its design for a 30 km long 287 KV transmission line to interconnect the TCT and

the KSM plant site. This KSM transmission line is scheduled to be constructed in 2023 with completion and commissioning planned for late

2024 to be ready for connection to the TCT. The cost of the TCT consists of $28.9 million in cash payments for facilities directly required

by the KSM Project and $54.2 million in security (or cash in lieu) for BC Hydro system reinforcement as required to make the power available.

The system reinforcement security will be forgiven annually, typically over a period of less than 8 years, based on project power consumption.

In March, 2022, KSM Mining ULC (“KSMCo”),

a wholly-owned subsidiary of the Issuer, sold a US$225,000,000 secured note that is to be exchanged at maturity for a silver royalty on

the KSM Project and Seabridge sold concurrently a Contingent Right, to Sprott Private Resource Streaming and Royalty (B) Corp. and Ontario

Teachers’ Pension Plan for US$225 million (approximately C$285 million at the current exchange rate). The proceeds of this sale

will be used to fund the works the Issuer is planning to advance the KSM Project towards the designation of ‘substantially started’.

The terms of the agreements relating to this financing are described below under “Material Contracts”.

Impacts

of COVID-19 Pandemic

On

March 11, 2020, the COVID-19 outbreak was declared a pandemic by the World Health Organization, which has caused significant financial

market and social dislocation. In response, the Issuer has implemented measures to safeguard the health and well-being of its employees,

contractors, consultants and community members to ensure their safety. Many of the Issuer’s employees worked from home before the

pandemic, but its employees that worked in its offices have worked from home during periods of lockdown. The Issuer reduced the scope

of the work programs at its KSM and Iskut projects originally planned for 2020 in order to observe social distancing and implement preventative

actions at its camps and cancelled work programs at 3 Aces. The measures in British Columbia limited the number of personnel accommodated

at remote camps and, therefore, the amount of work that can be completed. Management’s plans for 2021 work were prepared assuming

COVID-19 restrictions will remain in place for its field season, which proved to be the case. The Issuer continued to move forward with

some of its development work at the KSM Project and progressed with its planned exploration programs at the Iskut Project and Snowstorm

Project, however its reclamation work at the old Johnny Mountain mine within its Iskut Project was deferred in 2020 due to lack of camp

space. In addition, the Issuer’s engagement with potential joint venture partners or potential acquirors for the KSM Project or

the Courageous Lake Project has slowed as major mining companies have focused on addressing the needs of their existing operations as

a result of the pandemic and travel restrictions, particularly quarantine requirements, have made site visits too difficult.

The

Issuer continues to have full access to its properties in Canada and the United States and has managed to adequately staff its remote

camps for planned programs. The Issuer has not experienced problems with obtaining the supplies needed for its work programs. The Issuer

has instituted and will continue to implement operational and monitoring protocols to ensure the health and safety of its employees and

stakeholders, which follow the advice of local governments and health authorities where it operates. The Issuer plans work programs on

an annual basis and adjusts its plans to the conditions it faces for funding and executing programs as it operates. It expects to be

able to continue operating on this basis going forward, although it may need to expand its camp capacity in order to advance development

at its KSM Project in a timely manner.

While

at this point the Issuer cannot reasonably estimate the impact of COVID-19 on potential operations, to date, the COVID-19 crisis has

not materially impacted the Issuer’s operations, but it has reduced the scale of the work it undertook in advancing the KSM Project

and the reclamation of the Johnny Mountain Mine. With the increase in the price of gold since the start of the pandemic, the Issuer has

enjoyed favourable capital markets and has continued to raise funds under its at-the-market offering of common shares and its financial

condition has not been adversely impacted by the pandemic. As a company without revenue from operations, its financial performance has

not been impacted by the pandemic. The Issuer will continue to monitor developments of the pandemic and continuously assess the pandemic’s

potential further impact on the Issuer’s operations and business.

See

“Risk Factors” for additional details on the impacts of the COVID-19 pandemic on the Issuer.

| ITEM

3: | DESCRIPTION

OF THE ISSUER’S BUSINESS |

General

The

Issuer owns 7 properties, 4 of which have gold resources, and it has one material property, its KSM Project. The Issuer holds a 100%

interest in each of its properties other than a small portion of the Iskut Project, in which it owns a 95% interest. The Quartz Mountain

project is subject to an option agreement under which the optionee may acquire a 100% interest in such project. At the date of this AIF,

the estimated gold resources at the Issuer’s properties are set forth in the following table and are broken down by project and

resource category.

Mineral

Resources (Gold and Copper)

| PROJECT |

Cut-Off

Grade

(g/t) |

Measured |

Indicated |

Inferred |

Tonnes

(000’s) |

Gold

Grade

(g/t) |

Gold

(000’s ozs) |

Copper

Grade

(%) |

Copper

(million

lbs) |

Tonnes

(000’s) |

Gold

Grade

(g/t) |

Gold

(000’s ozs) |

Copper

Grade

(%) |

Copper

(million

lbs) |

Tonnes

(000’s) |

Gold

Grade

(g/t) |

Gold

(000’s ozs) |

Copper

Grade

(%) |

Copper

(million

lbs) |

| KSM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Mitchell |

See

Note 1 |

750,000 |

0.63 |

15,125 |

0.17 |

2,844 |

1,045,000 |

0.57 |

19,191 |

0.16 |

3,795 |

478,000 |

0.42 |

6,406 |

0.12 |

1,230 |

| Iron

Cap |

See

Note 1 |

-- |

-- |

-- |

-- |

-- |

423,000 |

0.41 |

5,576 |

0.22 |

2,051 |

1,899,000 |

0.45 |

27,474 |

0.30 |

12,556 |

| Sulphurets |

See

Note 1 |

-- |

-- |

-- |

-- |

-- |

446,000 |

0.55 |

7,887 |

0.21 |

2,064 |

223,000 |

0.44 |

3,155 |

0.13 |

639 |

| Kerr |

See

Note 1 |

-- |

-- |

-- |

-- |

-- |

374,000 |

0.22 |

2,660 |

0.41 |

3,405 |

1,999,000 |

0.31 |

19,823 |

0.40 |

17,720 |

| KSM

Total² |

-- |

750,000 |

0.63 |

15,125 |

0.17 |

2,844 |

2,288,000 |

0.48 |

35,314 |

0.22 |

11,315 |

4,599,000 |

0.38 |

56,858 |

0.32 |

32,145 |

| East Mitchell (East Mitchell) |

0.30 |

189,800 |

0.82 |

4,983 |

0.09 |

380 |

1,180,300 |

0.55 |

20,934 |

0.10 |

2,600 |

833,200 |

0.34 |

9,029 |

0.06 |

1,100 |

Courageous

Lake:

Fat

Deposit²

Walsh

Lake² |

0.83

0.60

|

13,401

--

|

2.53

--

|

1,090

--

|

--

--

|

--

--

|

93,914

--

|

2.28

--

|

6,884

--

|

--

--

|

--

--

|

48,963

4,624

|

2.18

3.24

|

3,432

482

|

--

--

|

--

--

|

| Quartz

Mountain3 |

0.34 |

3,480 |

0.98 |

110 |

-- |

-- |

54,330 |

0.91 |

1,591 |

-- |

-- |

44,800 |

0.72 |

1,043 |

-- |

-- |

| Iskut

(Bronson Slope) |

See

Note 4 |

84,150 |

0.42 |

1,140 |

0.15 |

280 |

102,740 |

0.31 |

1,020 |

0.10 |

222 |

-- |

-- |

-- |

-- |

-- |

| Note: | The

resource estimates have been prepared in accordance with the standards and guidance referenced

in NI 43-101. See “Cautionary Note to United States Investors Regarding Resource Estimates”

in the Preliminary Notes. |

| | | |

| 1. | The

cut-off grade for KSM is CDN$9 in net smelter return (NSR) for the open pits and CDN$16 in

NSR for the underground mining. |

| 2. | The

effective dates of the KSM and Courageous Lake resource estimates above are as follows: KSM,

December 31, 2019; Courageous Lake (Fat), September 2012; and Courageous Lake (Walsh Lake),

March, 2014. |

| 3. | Seabridge

has entered into an option agreement under which a 100% interest in the Quartz Mountain project

may be acquired. |

| 4. | The

cut-off grade for the Iskut Project resource is CDN$9.00 in NSR. |

The

measured and indicated mineral resources at the KSM Project and Courageous Lake Project are inclusive of mineral reserves. Mineral resources

which are not mineral reserves do not have demonstrated economic viability.

The

Issuer will provide updated estimates for mineral reserves and mineral resources at its KSM Project as part of a new Technical Report

expected to be completed in June 2022.

Cautionary

Note Regarding Forward-Looking Statements

This

AIF contains forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and

forward-looking information within the meaning of Canadian securities laws concerning future events or future performance with respect

to the Issuer’s projects, business approach and plans, including production, capital, operating and cash flow estimates; business

transactions such as the potential sale or joint venture of the Issuer’s KSM Project and Courageous Lake Project (each as defined

herein) and the acquisition of interests in mineral properties; requirements for additional capital; the estimation of mineral resources

and reserves; and the timing of completion and success of exploration and advancement activities, community relations, required regulatory

and third party consents, permitting and related programs in relation to the KSM Project, East Mitchell Property, Courageous Lake Project,

Iskut Project, Snowstorm Project or 3 Aces Project. Any statements that express or involve discussions with respect to predictions, expectations,

beliefs, plans, projections, objectives or future events or performance (often, but not always, using words or phrases such as “expects”,

“anticipates”, “believes”, “plans”, “projects”, “estimates”, “intends”,

“strategy”, “goals”, “objectives” or variations thereof or stating that certain actions, events or

results “may”, “could”, “would”, “might”, or “will” be taken, occur or be

achieved, or statements of “potential” or something “possible”, or the negative of any of these terms and similar

expressions) are not statements of historical fact and may be forward-looking statements and forward-looking information (collectively

referred to in the following information simply as “forward-looking statements”). In addition, statements concerning

mineral reserve and mineral resource estimates constitute forward-looking statements to the extent that they involve estimates of the

mineralization expected to be encountered if a mineral property is developed and, in the case of reserves, the economics of developing

a property and producing minerals.

Forward-looking

statements are necessarily based on estimates and assumptions made by the Issuer in light of its experience and perception of historical

trends, current conditions and expected future developments. In making the forward-looking statements in this AIF the Issuer has applied

several material assumptions including, but not limited to, the assumption that: (1) market fundamentals will result in sustained demand

and prices for gold and copper, and to a much lesser degree, silver and molybdenum; (2) the potential for production at its mineral projects

will continue operationally, legally and economically; (3) any additional financing needed will be available on reasonable terms; and

(4) estimated reserves and resources at the Issuer’s projects have merit and there is continuity of mineralization as reflected

in such estimates.

Forward-looking

statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results

to differ from those expressed or implied by the forward-looking statements, including, without limitation:

| ● | the

Issuer’s history of net losses and negative cash flows from operations and expectation of future losses and negative cash flows

from operations; |

| ● | risks

related to the Issuer’s ability to continue its exploration activities and future advancement

activities, and to continue to maintain corporate office support of these activities, which

are dependent on the Issuer’s ability to enter into joint ventures, to sell property

interests or to obtain suitable financing; |

| ● | the

Issuer’s indebtedness requires payment of quarterly interest and, in certain circumstances, may require repayment of principal

and the Issuer’s principal sources for funds for repayment are capital markets and asset sales; |

| ● | uncertainty

of whether the reserves estimated on the Issuer’s mineral properties will be brought

into production; |

| ● | uncertainties

relating to the assumptions underlying the Issuer’s reserve and resource estimates; |

| ● | risks

related to obtaining and maintaining all necessary permits and governmental approvals, or

extensions/renewals thereof, for exploration and development activities, including in respect

of environmental regulation, and the risk that the Issuer’s EAC might expire before

the KSM Project is declared to be substantially started; |

| ● | uncertainty

of estimates of capital costs, operating costs, production and economic returns; |

| ● | risks relating to the commencement of site access and early

site preparation construction activities at the KSM Project; |

| ● | risks

related to commercially producing precious metals and copper from the Issuer’s mineral

properties; |

| ● | risks

related to fluctuations in the market price of gold, copper and other metals; |

| ● | risks

related to fluctuations in foreign exchange rates; |

| ● | mining,

exploration and development risks that could result in damage to mineral properties, plant

and equipment, personal injury, environmental damage and delays in mining, which may be uninsurable

or not insurable in adequate amounts; |

| ● | uncertainty

related to title to the Issuer’s mineral properties and rights of access over or through

lands subject to third party rights, interests and mineral tenures; |

| ● | risks

related to unsettled First Nations rights and title and settled Treaty Nations’ rights

and uncertainties relating to the application of the United Nations Declaration on the

Rights of Indigenous Peoples to the laws in Canadian jurisdictions; |

| ● | the

integration of the East Mitchell Property into the KSM Project may not yield the benefits

to development, profitability or rate of return of the KSM Project that were anticipated; |

| ● | risks

related to increases in demand for exploration and development services equipment, and related

cost increases; |

| ● | increased

competition in the mining industry; |

| ● | ongoing

concerns regarding carbon emissions and the impacts of measures taken to induce or mandate

lower carbon emissions on the ability to secure permits, finance projects and generate profitability

at a project; |

| ● | the

Issuer’s current and proposed operations are subject to risks relating to climate and

climate change that may adversely impact its ability to conduct operations, increase operating

costs, delay execution or reduce the profitability of a future mining operation; |

| ● | the

Issuer’s need to attract and retain qualified management and personnel; |

| ● | risks

related to some of the Issuer’s directors’ and officers’ involvement with

other natural resource companies; |

| ● | risks

associated with impacts from the reaction to and measures taken to address the spread of

the COVID-19 virus; |

| ● | the

Issuer’s classification as a “passive foreign investment company” under the

United States tax code; |

| ● | risks

associated with the use of information technology systems and cybersecurity; |

| ● | uncertainty

surrounding an audit by the Canada Revenue Agency (“CRA”) of Canadian

exploration expenses incurred by the Issuer during the 2014, 2015 and 2016 financial years

which the Issuer has renounced to subscribers of flow-through share offerings and the CRA’s

decision to reduce such renunciations to such subscribers; and |

| ● | the

reassessment by the CRA of the Issuer’s refund claim for the 2010 and 2011 financial years

in respect of the British Columbia Mining Exploration Tax Credit. |

This

list is not exhaustive of the factors that may affect any of the Issuer’s forward-looking statements. Forward-looking statements

are statements about the future and are inherently uncertain, and actual achievements of the Issuer or other future events or conditions

may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors,

including, without limitation, those referred to in this AIF under the heading “Risk Factors” and elsewhere in this

AIF. In addition, although the Issuer has attempted to identify important factors that could cause actual achievements, events or conditions

to differ materially from those identified in the forward-looking statements, there may be other factors that cause achievements, events

or conditions not to be as anticipated, estimated or intended. Many of the foregoing factors are beyond the Issuer’s ability to

control or predict. It is also noted that while Seabridge engages in exploration and advancement of its properties, including site work

in preparation for feasibility study work or site capture construction work, it will not undertake production activities by itself.

These

forward-looking statements are based on the beliefs, expectations and opinions of management on the date the statements are made and

the Issuer does not assume any obligation to update forward-looking statements, except as required by applicable securities laws, if

circumstances or management’s beliefs, expectations or opinions should change. For the reasons set forth above, investors should

not place undue reliance on forward-looking statements.

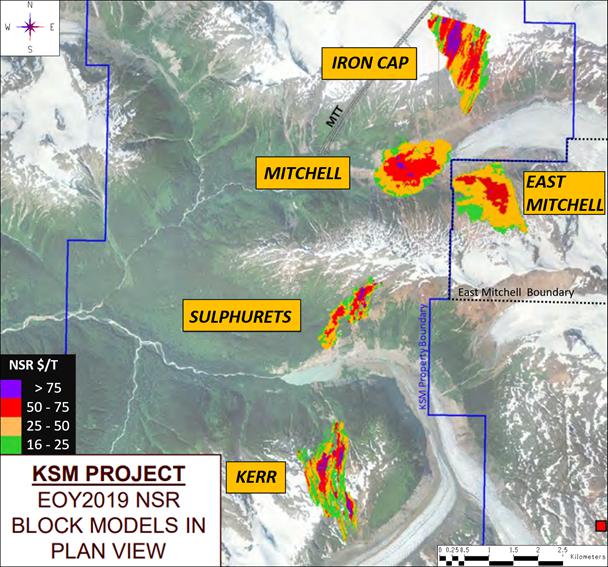

KSM

Project

Overview

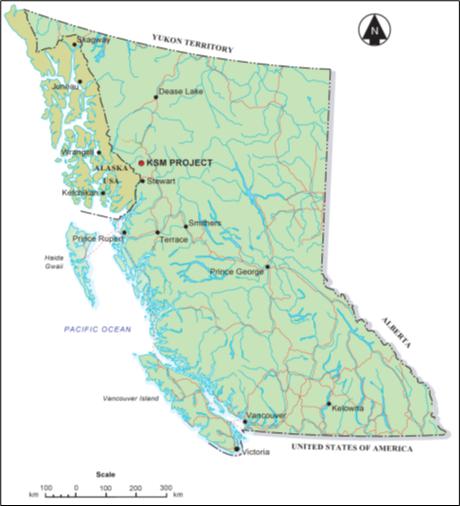

The

KSM Project is located within the Iskut-Stikine region of British Columbia, approximately 21 kilometers south-southeast of the former

Eskay Creek Mine and approximately 65 kilometers north-northwest of Stewart, British Columbia. (See Figure 1.) The provincial government

has recognized the significance of historical mining activity in this area, which includes the past producing Eskay Creek, Snip, Granduc,

and Premier mines. More recently the Red Chris Mine and the Brucejack Mine commenced mining operations.

Access

to the property is by helicopter from Bell II Crossing on the Stewart Cassiar Highway or Stewart, British Columbia. Mobilization of equipment

and personnel is staged from kilometer 54 on the private Eskay Creek Mine Road (about 25 km from the Project) and from Bell II Crossing

on the Stewart Cassiar Highway (about 40 km from the Project).

At

the time the Issuer acquired the KSM Project in 2001, the project consisted of two distinct zones (Kerr and Sulphurets) which had been

modeled separately by Placer Dome (CLA) Limited (“Placer Dome”). Subsequent drilling and engineering work by the Issuer

has defined two new very large zones, the Mitchell Zone and the Iron Cap Zone, as well as dramatically expanding the mineralized zone

beneath the Kerr zone.

From

2008 to 2012 Seabridge focused on further exploration and advancement of the four known deposits at the KSM Project and generated successive

resource estimates and three preliminary feasibility studies, the last of which being the 2012 KSM PFS Report (as defined herein) with

an effective date of June 22, 2012. In 2012 Seabridge continued advancement efforts, including work required for the submission of its

EA Application and EIS, but changed its exploration focus at KSM to a search for higher temperature core zones that typically concentrate

high-grade metals within very large porphyry systems such as KSM. Exploration since 2011 has resulted in the discovery of two core zones,

Deep Kerr (a down dip continuation of Kerr deposit mineralization) and Iron Cap Lower Zone (a down dip continuation of Iron Cap deposit

mineralization), an extension of the Mitchell zone and other promising core targets.

After

completing drilling in 2021 the resource drill hole database for the KSM Project now includes 1,030 drill holes totaling approximately

404,606 meters. More than 95% of the holes at Mitchell and 95% of the holes at Iron Cap were drilled by Seabridge between 2006 and 2021.

Figure

1 - KSM Project Location Map

In

July, 2014, the Issuer’s provincial EA Application for the KSM Project under the British Columbia Environmental Assessment Act

was approved. The Canadian Environmental Assessment Agency (CEAA) issued its Comprehensive Study Report in July 2014, as required

by the Canadian Environmental Assessment Act, which concluded that the KSM Project would not have significant impacts to the environment.

The EA Application and EIS review process involved Alaskan regulators throughout and the CEAA Study Report also concluded that the KSM

Project would not have significant impacts to the environment situated downstream of the Alaska border. In December 2014 the Federal

Minister of the Environment issued a positive project decision which endorsed the conclusions of the Comprehensive Study Report. The

provincial EA approval was for a term of five years, it was extended for a further five year term in March, 2019 and for another two

years in November, 2021, and now expires on July 29, 2026. The EAC can be extended indefinitely if the province declares the Issuer has

‘substantially started” construction of the Project. The federal approval is for an indefinite term. The Issuer believes

that the EA Application and EIS materials and subsequent approvals demonstrate that the KSM project, as designed, is an environmentally

responsible and a generally socially accepted Project.

The

Project received a license under the International Rivers Improvement Act (Canada) on October 21, 2016, authorizing the construction,

operation and maintenance of the Water Storage Facility (WSF) and ancillary water works for the KSM Project within the Unuk River watershed

in northwestern British Columbia.

In

June, 2017, the Issuer also announced it had been given a regulatory amendment to Schedule 2 of the Metal Mining Effluent Regulations

under the Fisheries Act (Canada) which authorizes the use of North Treaty Creek for the discharge from the KSM tailings management

facility, subject to strict bonding and fishery habitat offsets.

After

completion of the 2015 exploration season the Issuer announced a resource estimate for the Kerr/Deep Kerr zone that exceeded 1 billion

tonnes and at higher grade than much of the material in the mine plan used for the 2012 KSM PFS Report. This new deposit presented great

potential for improving Project economics if it was incorporated into the Issuer’s development plan at the Project. In addition,

in the course of the EA Application and EIS review process, the Issuer made commitments to enhance the environmental mitigation and protection

offered by the Project, which the Issuer knew would increase the cost of building KSM Project infrastructure. Since the 2012 KSM PFS

Report did not incorporate the Deep Kerr deposit or these increased infrastructure costs and given the change in the market prices used

in the 2012 KSM PFS Report, the Issuer decided in early 2016 to update the 2012 KSM PFS Report. In November, 2016, the Issuer completed

a new pre-feasibility study report which reflected more current market conditions and included the costs associated with the Issuer’s

EA Application and EIS commitments, but otherwise used essentially the same construction plan and mine plan as in the 2012 KSM PFS Report.

The report also presented an alternative development plan for the Project, at a preliminary economic assessment level, that incorporated

material from the Deep Kerr deposit. Overall, this new report showed that the projected economics of the original development plan had

declined since 2012, but that the projected economics of the development plan that incorporated the Kerr deposit in its entirety showed

meaningful improvement for the Project as a whole.

Additional drilling was completed at the Iron

Cap deposit in 2017 and 2018 with great success. In March, 2019, an updated resource estimate was completed for the Iron Cap deposit which

increased inferred resources at the deposit by more than four times the number of tonnes in the inferred resource estimate used in the

2016 update to the 2012 KSM PFS Report.

In 2020 the Issuer acquired the East Mitchell

Property (formerly known as the Snowfield Property), a single mineral claim covering 1,267 Ha adjacent to the Mitchell deposit, from Pretium

Resources Inc. for US$100 million, a 1.5% net smelter returns (“NSR”) royalty on East Mitchell Property production

and a future contingent payment of US$20 million of which US$15 million can be credited against future royalty payments. The East Mitchell

Property hosts a large gold/copper mineral resource and was acquired with a view to incorporating it into the Issuer’s KSM Project.

The Issuer has commenced a study looking at incorporating the East Mitchell Property into the KSM Project development plan which is expected

to be completed in the second quarter of 2022. In May, 2020, the Issuer also paid $350,000 to acquire the 2.5% NSR on claims originally

known as the BJ and Tina claims, which NSR applied to the northwest portion of the Iron Cap deposit.

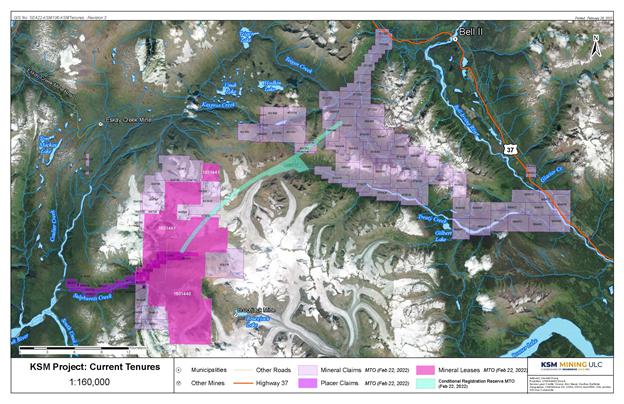

Land Status

The KSM property is comprised of four discrete

claim blocks (see Figure 2) and a group of placer claims. Claim blocks of the KSM Property include mineral leases and both cell and legacy

claims. The claim blocks are referred to as:

| (a) | the KSM tenures containing 20 mineral claims totaling 6,097.42 Ha and 2 mining leases of 11,247.00 Ha

(the westernmost block in Figure 2); |

| (b) | the Seabee claims covering 18,674.30 Ha within 46 mineral claims (the large block in the east of the Project

lying mainly to the west of Highway 37 in Figure 2); |

| (c) | the Tina claims composed of 11 mineral claims covering 3,052.44 Ha (the block between the KSM tenures

and the Seabee claims in Figure 2); and |

| (d) | the Treaty Creek Switching Station claims with 2 claims totalling 160.25 Ha (the small block lying to

the east of Highway 37 in Figure 2). |

The four claim blocks include 79 mineral claims

(cell and legacy) and 2 mining leases with a combined area of 40,785 ha. The mineral resources are positioned within the KSM Claims and

include the original claims purchased from Placer Dome and the BJ claims. The East Mitchell Property lies immediately to the east of KSM

mining leases. If it was grouped with the KSM claims it would increase that claim block to 21 mineral claims totaling 7,364.85 Ha and

the two mining leases. This claim is shown in Figure 2 for clarity.

Figure 2 - KSM Project Claim Map

The Seabee and Tina claim blocks are located about

19 km northeast of the Kerr-Sulphurets-Mitchell-Iron Cap mineralized zones. These claim blocks are currently being considered for

proposed infrastructure siting. The Treaty Creek Switching Station claims, adjacent to the NTL and to the east of the Seabee claims, are

being used for power infrastructure siting.

Placer claims only cover areas on part of the

westernmost KSM Claims covering an area of 1,554 hectares. The Issuer’s placer claims lie along Sulphurets Creek and Mitchell Creek

in areas where certain of the Project’s proposed infrastructure will be located.

These claims are 100% owned by the Issuer through

its wholly-owned subsidiary, KSM Mining ULC. Newmont Corporation retains a 1% net smelter returns (“NSR”) royalty

that is capped at $4.5 million. Two of the pre-converted claims (Xray 2 and Xray 6), the areas of which have now been converted into

part of mining lease 1031440, and one pre-converted claim (Xray 8), the area of which is now within the East Mitchell Property (mineral

claim 509216) are also subject to an effective 1% NSR royalty capped at US$650,000. In addition, the Issuer has granted two options to

a subsidiary of Royal Gold, Inc. under which such subsidiary can acquire a 1.25% NSR Royalty and a 0.75% NSR Royalty on gold and silver

produced from the KSM Property for $100 million and $60 million, respectively, subject to certain conditions. KSMCo sold to Sprott Private Resource

Streaming and Royalty (B) Corp. a secured note under which Sprott has agreed it will use all of the principal amount repaid on maturity

of such Note to purchase a 60% gross silver royalty on the KSM Project (or, in certain circumstances, a 75% gross silver royalty on the

KSM Project), subject to certain rights of Sprott to redeem the Secured Note and be repaid the principal instead of purchasing the royalty.

A more detailed description of the terms of the Secured Note, as well as the Issuer’s right to buy back 50% of such royalty, appear

below under “Material Contracts”. The Treaty

Creek Switching Station Claims and certain fractional claims within the Seabee claims are subject to royalties, however none of the mineral

resources at the KSM Project are located on the claims subject to these royalties and they are intended for infrastructure siting.

Under the Benefits Agreement with the Nisga’a

Nation and the Co-operation and Benefits Agreement with the Tahltan Nation, the Issuer has agreed to pay each Nation annual payments.

The combined annual payments to these Nations are payable in two forms; payments that are a percentage of the tax payable (the “Mineral

Tax”) under the Mineral Tax Act (British Columbia) (the “Mineral Tax Act”), which is a tax on net

operating profit of the KSM Project, and payments that are based on net smelter returns of the KSM Project. The combined payments payable

to both Nations are as follows:

| (a) | with respect to years 1-7 of mining operations, a 0.1% NSR royalty and either (i) 5% of the amount of

Mineral Tax payable in respect of any Capital Recovery Year (defined below), or (ii) 11% of the amount of Mineral Tax payable in respect

of any Post-Capital Recovery Year (defined below); |

| (b) | with respect to years 8-20 of mining operations, a 0.4% NSR royalty and either (i) 7.75% of the amount

of Mineral Tax payable in respect of any Capital Recovery Year, or (ii) 13.75% of the amount of Mineral Tax payable in respect of any

Post-Capital Recovery Year; and |

| (c) | with respect to period after 20 years of mining operations, a 0.5% NSR royalty and either (i) 7.75% of

the amount of Mineral Tax payable in respect of any Capital Recovery Year, or (ii) 13.75% of the amount of Mineral Tax payable in respect

of any Post-Capital Recovery Year. |

For the purposes of the description above, a “Capital

Recovery Year” is a year in which the Issuer is able to apply sufficient amounts in the KSM Capital Account (as determined under

the Mineral Tax Act) to fully offset operating profit, and a “Post-Capital Recovery Year” is a year in which the Issuer

is unable to apply sufficient amounts in the KSM Capital Account (as determined under the Mineral Tax Act) to fully offset operating profit.

In addition, a sale of the original claims that

were purchased in 2001 is subject to a right of first refusal held by Glencore Canada Corporation.

The property is located on Crown land; therefore,

all surface and access rights are granted under, and subject to, the Land Act (British Columbia) and the Mineral Tenure Act

(British Columbia). Approximately 13 km of the proposed 23 km Mitchell-Treaty tunnels (the “MTT”) pass under Crown

Land subject to mineral claims held by third parties. The Issuer has been granted a licence of occupation, a form of land tenure that

grants it rights to occupy the area through which the proposed MTT will pass, subject to the rights of the third party mineral claims

holders. In the Issuer’s opinion, these rights are addressed by the Issuer’s obligations, under the management plan associated

with the licence of occupation, to segregate and deliver to such claims holders all earth and rock material removed from the third party

claims during construction of the MTT.

The four gold-copper deposits, and the proposed

waste rock storage areas, lie within the Unuk River drainage in the area covered by the Cassiar-Iskut-Stikine Land and Resource Management

Plan approved by the British Columbia Government in 2000. A part of the proposed ore transport tunnel lies within the boundaries of the