UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

for the quarterly period ended

for the transition period from to

Commission file number:

SPONSORED BY WORLD GOLD TRUST

SERVICES, LLC

(Exact Name of Registrant as Specified in Its Charter)

| | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices)

(

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) Name | Name of each exchange on which registered | ||

| | | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | ☒ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | |

| Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As of August 4, 2023, the Registrant had

INDEX

| Page | ||

| 1 | ||

| Item 1. |

1 | |

| Statements of Financial Condition at June 30, 2023 (unaudited) and September 30, 2022 |

1 | |

| Schedules of Investment at June 30, 2023 (unaudited) and September 30, 2022 |

2 | |

| Unaudited Statements of Operations for the three and nine months ended June 30, 2023 and 2022 |

3 | |

| Unaudited Statements of Cash Flows for the three and nine months ended June 30, 2023 and 2022 |

4 | |

| 5 | ||

| 6 | ||

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

10 |

| Item 3. |

14 | |

| Item 4. |

14 | |

| 14 | ||

| Item 1. |

14 | |

| Item 1A. |

14 | |

| Item 2. |

15 | |

| Item 3. |

15 | |

| Item 4. |

15 | |

| Item 5. |

15 | |

| Item 6. |

15 | |

| 17 | ||

SPDR® GOLD TRUST

PART I - FINANCIAL INFORMATION:

Item 1. Financial Statements (Unaudited)

Statements of Financial Condition

At June 30, 2023 (unaudited) and September 30, 2022

| (Amounts in 000’s of US$ except for share and per share data) | Jun-30, 2023 | Sep-30, 2022 | ||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Investments in Gold, at fair value (cost $ | $ | $ | ||||||

| Total Assets | $ | $ | ||||||

| LIABILITIES | ||||||||

| Accounts payable to Sponsor | $ | $ | ||||||

| Gold payable | ||||||||

| Total Liabilities | $ | $ | ||||||

| Net Assets | $ | $ | ||||||

| Shares issued and outstanding(1) | ||||||||

| Net asset value per Share | $ | $ | ||||||

(1) Authorized share capital is unlimited and the par value of the Shares is $

See notes to the unaudited financial statements.

SPDR® GOLD TRUST

(Amounts in 000’s except for percentages)

| June 30, 2023 | Ounces of gold | Cost | Fair Value | % of Net Assets | ||||||||||||

| (unaudited) | ||||||||||||||||

| Investment in Gold | $ | $ | % | |||||||||||||

| Total Investment | $ | $ | % | |||||||||||||

| Liabilities in excess of other assets | ( | ) | ( | )% | ||||||||||||

| Net Assets | $ | % | ||||||||||||||

| September 30, 2022 | Ounces of gold | Cost | Fair Value | % of Net Assets | ||||||||||||

| Investment in Gold | $ | $ | % | |||||||||||||

| Total Investment | $ | $ | % | |||||||||||||

| Liabilities in excess of other assets | ( | ) | ( | )% | ||||||||||||

| Net Assets | $ | % | ||||||||||||||

See notes to the unaudited financial statements.

SPDR® GOLD TRUST

Unaudited Statements of Operations

For the three and nine months ended June 30, 2023 and June 30, 2022

| Three Months | Three Months | Nine Months | Nine Months | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| (Amounts in 000’s of US$, except per share data) | Jun-30, 2023 | Jun-30, 2022 | Jun-30, 2023 | Jun-30, 2022 | ||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| EXPENSES | ||||||||||||||||

| Sponsor fees | $ | $ | $ | $ | ||||||||||||

| Total expenses | ||||||||||||||||

| Net investment loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized and change in unrealized gain/(loss) on investment in gold | ||||||||||||||||

| Net realized gain/(loss) from investment in gold sold to pay expenses | ||||||||||||||||

| Net realized gain/(loss) from gold distributed for the redemption of shares | ||||||||||||||||

| Net change in unrealized gain/(loss) on investment in gold | ( | ) | ( | ) | ||||||||||||

| Net realized and change in unrealized gain/(loss) on investment in gold | ( | ) | ( | ) | ||||||||||||

| Net income/(loss) | $ | ( | ) | $ | ( | ) | $ | $ | ||||||||

| Net income/(loss) per share | $ | ( | ) | $ | ( | ) | $ | $ | ||||||||

| Weighted average number of shares (in 000’s) | ||||||||||||||||

See notes to the unaudited financial statements.

SPDR® GOLD TRUST

Unaudited Statements of Cash Flows

For the three and nine months ended June 30, 2023 and June 30, 2022

| Three Months | Three Months | Nine Months | Nine Months | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| (Amounts in 000’s of US$) | Jun-30, 2023 | Jun-30, 2022 | Jun-30, 2023 | Jun-30, 2022 | ||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| INCREASE/DECREASE IN CASH FROM OPERATIONS: | ||||||||||||||||

| Cash proceeds received from sales of gold | $ | $ | $ | $ | ||||||||||||

| Cash expenses paid | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Increase/(Decrease) in cash resulting from operations | ||||||||||||||||

| Cash and cash equivalents at beginning of period | ||||||||||||||||

| Cash and cash equivalents at end of period | $ | $ | $ | $ | ||||||||||||

| SUPPLEMENTAL DISCLOSURE OF NON-CASH FINANCING ACTIVITIES: | ||||||||||||||||

| Value of gold received for creation of shares-net of change in gold receivable | $ | $ | $ | $ | ||||||||||||

| Value of gold distributed for redemption of shares-net of change in gold payable | $ | $ | $ | $ | ||||||||||||

| Three Months | Three Months | Nine Months | Nine Months | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| (Amounts in 000’s of US$) | Jun-30, 2023 | Jun-30, 2022 | Jun-30, 2023 | Jun-30, 2022 | ||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| RECONCILIATION OF NET INCOME/(LOSS) TO NET CASH PROVIDED BY OPERATING ACTIVITIES | ||||||||||||||||

| Net income/(loss) | $ | ( | ) | $ | ( | ) | $ | $ | ||||||||

| Adjustments to reconcile net income/(loss) to net cash provided by operating activities: | ||||||||||||||||

| Proceeds from sales of gold to pay expenses | ||||||||||||||||

| Net realized (gain)/loss from investment in gold sold to pay expenses | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized (gain)/loss from gold distributed for the redemption of shares | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net change in unrealized (gain)/loss on investment in gold | ( | ) | ( | ) | ||||||||||||

| Increase/(Decrease) in accounts payable to Sponsor | ( | ) | ||||||||||||||

| Net cash provided by operating activities | $ | $ | $ | $ | ||||||||||||

See notes to the unaudited financial statements.

SPDR® GOLD TRUST

Unaudited Statements of Changes in Net Assets

For the three and nine months ended June 30, 2023 and June 30, 2022

| Three Months | Three Months | Nine Months | Nine Months | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| (Amounts in 000’s of US$) | Jun-30, 2023 | Jun-30, 2022 | Jun-30, 2023 | Jun-30, 2022 | ||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Net Assets - Opening Balance | $ | $ | $ | $ | ||||||||||||

| Creations | ||||||||||||||||

| Redemptions | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net investment loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net realized gain/(loss) from investment in gold sold to pay expenses | ||||||||||||||||

| Net realized gain/(loss) from gold distributed for the redemption of shares | ||||||||||||||||

| Net change in unrealized gain/(loss) on investment in gold | ( | ) | ( | ) | ||||||||||||

| Net Assets - Closing Balance | $ | $ | $ | $ | ||||||||||||

See notes to the unaudited financial statements.

SPDR® GOLD TRUST

Notes to the Unaudited Financial Statements

| 1. | Organization |

The SPDR® Gold Trust (the “Trust”) is an investment trust formed on

The Shares trade on the NYSE Arca, Inc. (the “NYSE Arca”) under the symbol “GLD”, providing investors with an efficient means to obtain market exposure to the price of gold bullion. The Shares are also listed on the Hong Kong Exchanges and Clearing Limited, the Mexican Stock Exchange (Bolsa Mexicana de Valores), the Singapore Exchange Limited and the Tokyo Stock Exchange.

The Trustee does not actively manage the gold held by the Trust. This means that the Trustee does not sell gold at times when its price is high or acquire gold at low prices in the expectation of future price increases. It also means that the Trustee does not make use of any of the hedging techniques available to professional gold investors to attempt to reduce the risk of losses resulting from price decreases. Any losses sustained by the Trust will adversely affect the value of the Shares.

The Statements of Financial Condition and Schedules of Investment at June 30, 2023 and the Statements of Operations, Cash Flows and Changes in Net Assets for the three and nine months ended June 30, 2023 and 2022 have been prepared on behalf of the Trust without audit. In the opinion of management of the Sponsor of the Trust, all adjustments (which include normal recurring adjustments) necessary to present fairly the financial position, results of operations and cash flows as of and for the three and nine months ended June 30, 2023 and for all periods presented have been made.

These financial statements should be read in conjunction with the financial statements and notes thereto included in the Trust’s Annual Report on Form 10-K for the fiscal year ended September 30, 2022. The results of operations for the three and nine months ended June 30, 2023 are not necessarily indicative of the operating results for the full fiscal year.

| 2. | Significant Accounting Policies |

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) requires those responsible for preparing financial statements to make estimates and assumptions that affect the reported amounts and disclosures. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Trust.

| |

2.1. | Basis of Accounting |

For accounting purposes only, the Trust is an investment company and, therefore, applies the specialized accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services—Investment Companies. The Trust is not registered as an investment company under the Investment Company Act of 1940, as amended.

| |

2.2. | Fair Value Measurement |

FASB Accounting Standards Codification Topic 820, Fair Value Measurements and Disclosures, provides a single definition of fair value, a hierarchy for measuring fair value and expanded disclosures about fair value adjustments.

The Trust does not hold any derivative instruments, and its assets only consist of allocated gold bullion and, from time to time, (i) gold receivable, representing gold covered by contractually binding orders for the creation of Shares where the gold has not yet been transferred to the Trust’s account and (ii) cash, which is used to pay expenses.

U.S. GAAP defines fair value as the price the Trust would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. The Trust’s policy is to value its investments at fair value.

Various inputs are used in determining the fair value of assets and liabilities. Inputs may be based on independent market data (“observable inputs”) or they may be internally developed (“unobservable inputs”). These inputs are categorized into a disclosure hierarchy consisting of three broad levels for financial reporting purposes. The level of a value determined for an asset or liability within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement in its entirety. The three levels of the fair value hierarchy are as follows:

Level 1 – Unadjusted quoted prices in active markets for identical assets or liabilities;

Level 2 – Inputs other than quoted prices included within Level 1 that are observable for the asset or liability either directly or indirectly, including quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not considered to be active, inputs other than quoted prices that are observable for the asset or liability and inputs that are derived principally from or corroborated by observable market data by correlation or other means; and

Level 3 – Inputs that are unobservable for the asset or liability, including the Trust’s assumptions used in determining the fair value of investments.

The following table summarizes the Trust’s investments at fair value:

| (Amounts in 000’s of US$) | ||||||||||||

| June 30, 2023 | Level 1 | Level 2 | Level 3 | |||||||||

| Investment in Gold | $ | $ | $ | |||||||||

| Total | $ | $ | $ | |||||||||

| (Amounts in 000’s of US$) | ||||||||||||

| September 30, 2022 | Level 1 | Level 2 | Level 3 | |||||||||

| Investment in Gold | $ | $ | $ | |||||||||

| Total | $ | $ | $ | |||||||||

There were

The Trustee values the gold held by the Trust on the basis of the price of an ounce of gold as determined by the ICE Benchmark Administration Limited (“IBA”), a benchmark administrator, which provides an independently administered auction process as well as the overall administration and governance for the London Bullion Market Association (“LBMA”). In determining the net asset value (“NAV”) of the Trust, the Trustee values the gold held by the Trust on the basis of the price of an ounce of gold determined by the IBA 3:00 PM auction process (“LBMA Gold Price PM”), which is an electronic auction, with the imbalance calculated, and the price adjusted in rounds (30 seconds in duration). The auction runs twice daily at 10:30 AM and 3:00 PM London time. The Trustee determines the NAV of the Trust on each day the NYSE Arca is open for regular trading, at the earlier of the LBMA Gold Price PM for the day or 12:00 PM New York time. If no LBMA Gold Price is made on a particular evaluation day or if the LBMA Gold Price has not been announced by 12:00 PM New York time on a particular evaluation day, the next most recent LBMA Gold Price (AM or PM) is used in the determination of the NAV of the Trust, unless the Trustee, in consultation with the Sponsor, determines that such a price is inappropriate to use as the basis for such determination.

| 2.3. | Custody of Gold |

Gold is held by the Custodians on behalf of the Trust,

| |

2.4. | Gold Receivable |

Gold receivable represents the quantity of gold covered by contractually binding orders for the creation of Shares where the gold has not yet been transferred to the Trust’s account. Generally, ownership of the gold is transferred within business days of the trade date.

| (Amounts in 000’s of US$) | Jun-30, 2023 | Sep-30, 2022 | ||||||

| Gold receivable | $ | $ | ||||||

| |

2.5. | Gold Payable |

Gold payable represents the quantity of gold covered by contractually binding orders for the redemption of Shares where the gold has not yet been transferred out of the Trust’s account. Generally, ownership of the gold is transferred within business days of the trade date.

| (Amounts in 000’s of US$) | Jun-30, 2023 | Sep-30, 2022 | ||||||

| Gold payable | $ | $ | ||||||

| |

2.6. | Creations and Redemptions of Shares |

The Trust creates and redeems Shares from time to time, but only in one or more Baskets (a Basket equals a block of

As the Shares of the Trust are redeemable in Baskets at the option of the Authorized Participants, the Trust has classified the Shares as Net Assets for financial reporting purposes.

| Nine Months | Nine Months | |||||||

| Ended | Ended | |||||||

| (Amounts are in 000’s) | Jun-30, 2023 | Jun-30, 2022 | ||||||

| Activity in Number of Shares Created and Redeemed: | ||||||||

| Creations | ||||||||

| Redemptions | ( | ) | ( | ) | ||||

| Net Change in Number of Shares Created and Redeemed | ( | ) | ||||||

| Nine Months | Nine Months | |||||||

| Ended | Ended | |||||||

| (Amounts in 000’s of US$) | Jun-30, 2023 | Jun-30, 2022 | ||||||

| Activity in Value of Shares Created and Redeemed: | ||||||||

| Creations | $ | $ | ||||||

| Redemptions | $ | ( | ) | $ | ( | ) | ||

| Net change in Value of Shares Created and Redeemed | $ | ( | ) | $ | ||||

| |

2.7. | Income and Expense (Amounts in 000’s of US$) |

The Trustee will, at the direction of the Sponsor or in its own discretion, sell the Trust’s gold as necessary to pay the Trust’s expenses. When selling gold to pay expenses, the Trustee will endeavor to sell the smallest amount of gold needed to pay expenses in order to minimize the Trust’s holdings of assets other than gold. Unless otherwise directed by the Sponsor, the Trustee will sell gold to the Custodians at the next LBMA Gold Price PM following the sale order. A gain or loss is recognized based on the difference between the selling price and the average cost of the gold sold, and such amounts are reported as net realized gain/(loss) from investment in gold sold to pay expenses on the Statements of Operations.

The Trust’s net realized and change in unrealized gain/(loss) on investment in gold for the nine months ended June 30, 2023 of $

The Trust’s net realized and change in unrealized gain/(loss) on investment in gold for the nine months ended June 30, 2022 of $

| 2.8. | Income Taxes |

The Trust is classified as a “grantor trust” for U.S. federal income tax purposes. As a result, the Trust itself will not be subject to U.S. federal income tax. Instead, the Trust’s income and expenses will “flow through” to the Shareholders, and the Trustee will report the Trust’s proceeds, income, deductions, gains, and losses to the Internal Revenue Service on that basis. The Sponsor of the Trust has evaluated whether or not there are uncertain tax positions that require financial statement recognition and has determined that

The Sponsor evaluates tax positions taken or expected to be taken in the course of its tax treatment, and its tax reporting to its shareholders, of these positions to determine whether the tax positions are “more-likely-than-not” to be sustained by the applicable tax authority. Tax positions not deemed to meet that threshold would be recorded as an expense in the current year. The Trust is required to analyze all open tax years. Open tax years are those years that are open for examination by the relevant income taxing authority. As of June 30, 2023, the 2022, 2021 and 2020 tax years remain open for examination.

| 3. | Related Parties – Sponsor and Trustee |

The Trust’s only recurring fixed expense is the Sponsor’s fee which accrues daily at an annual rate equal to

Affiliates of the Trustee may from time to time act as Authorized Participants or purchase or sell gold or Shares for their own account, as agent for their customers and for accounts over which they exercise investment discretion.

| 4. | Concentration of Risk |

The Trust’s sole business activity is the investment of gold. Various factors could affect the price of gold including: (i) global supply and demand, which is influenced by such factors as gold’s uses in jewelry, technology and industrial applications, purchases made by investors in the form of bars, coins and other gold products, forward selling by gold producers, purchases made by gold producers to unwind gold hedge positions, central bank purchases and sales, and production and cost levels in major gold-producing countries such as China, Australia, and the United States; (ii) investors’ expectations with respect to the rate of inflation; (iii) currency exchange rates; (iv) interest rates; (v) investment and trading activities of hedge funds and commodity funds; (vi) other economic variables such as income growth, economic output, and monetary policies; and (vii) global or regional political, economic or financial events and situations, especially those that are unexpected in nature. In addition, while gold is used to preserve wealth by investors around the world, there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price of gold declines, the Sponsor expects the value of an investment in the Shares to decline proportionately. Each of these events could have a material effect on the Trust’s financial position and results of operations.

| 5. | Indemnification |

The Sponsor, and its shareholders, members, directors, officers, employees, affiliates and subsidiaries, are indemnified by the Trust and held harmless against certain losses, liabilities or expenses incurred in the performance of their duties under the Trust Indenture without gross negligence, bad faith, willful misconduct, willful malfeasance or reckless disregard of the indemnified party’s obligations and duties under the Trust Indenture. Such indemnity includes payment by the Trust of the costs and expenses incurred in defending against any claim or liability under the Trust Indenture. Under the Trust Indenture, the Sponsor may be able to seek indemnification by the Trust for payments it makes in connection with the Sponsor’s activities under the Trust Indenture to the extent its conduct does not disqualify it from receiving such indemnification under the terms of the Trust Indenture. The Sponsor is also indemnified by the Trust and held harmless against any loss, liability or expense arising under the Amended and Restated Marketing Agent Agreement between the Sponsor and the Marketing Agent effective July 17, 2015, as amended, or any agreement entered into with an Authorized Participant which provides the procedures for the creation and redemption of Baskets and for the delivery of gold and any cash required for creations and redemptions insofar as such loss, liability or expense arises from any untrue statement or alleged untrue statement of a material fact contained in any written statement provided to the Sponsor by the Trustee. Any amounts payable to the Sponsor are secured by a lien on the Trust’s assets.

The Sponsor has agreed to indemnify certain parties against certain liabilities and to contribute to payments that such parties may be required to make in respect of those liabilities. The Trustee has agreed to reimburse such parties, solely from and to the extent of the Trust’s assets, for indemnification and contribution amounts due from the Sponsor in respect of such liabilities to the extent the Sponsor has not paid such amounts when due. The Sponsor has agreed that, to the extent the Trustee pays any amount in respect of the reimbursement obligations described in the preceding sentence, the Trustee, for the benefit of the Trust, will be subrogated to and will succeed to the rights of the party so reimbursed against the Sponsor.

| 6. | Financial Highlights |

The Trust is presenting the following financial highlights related to investment performance and operations of a Share outstanding for the three and nine months ended June 30, 2023 and 2022, respectively. The total return at net asset value is based on the change in net asset value of a Share during the period and the total return at market value is based on the change in market value of a Share on the NYSE Arca during the period. An individual investor’s return and ratios may vary based on the timing of capital transactions.

Financial Highlights (Unaudited)

For the three and nine months ended June 30, 2023 and 2022

| Three Months | Three Months | Nine Months | Nine Months | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| Jun-30, 2023 | Jun-30, 2022 | Jun-30, 2023 | Jun-30, 2022 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Net Asset Value | ||||||||||||||||

| Net asset value per Share, beginning of period | $ | $ | $ | $ | ||||||||||||

| Net investment income/(loss) | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net Realized and Change in Unrealized Gain/(Loss) | ( | ) | ( | ) | ||||||||||||

| Net Income/(Loss) | ( | ) | ( | ) | ||||||||||||

| Net asset value per Share, end of period | $ | $ | $ | $ | ||||||||||||

| Market value per Share, beginning of period | $ | $ | $ | $ | ||||||||||||

| Market value per Share, end of period | $ | $ | $ | $ | ||||||||||||

| Ratio to average net assets | ||||||||||||||||

| Net investment loss(1) | ( | )% | ( | )% | ( | )% | ( | )% | ||||||||

| Gross expenses(1) | % | % | % | % | ||||||||||||

| Net expenses(1) | % | % | % | % | ||||||||||||

| Total Return, at net asset value(2) | ( | )% | ( | )% | % | % | ||||||||||

| Total Return, at market value(2) | ( | )% | ( | )% | % | % | ||||||||||

(1) Percentages are annualized.

(2) Percentages are not annualized.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

This information should be read in conjunction with the financial statements and notes included in Item 1 of Part I of this Quarterly Report. The discussion and analysis which follows may contain trend analysis and other forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, which reflect our current views with respect to future events and financial results. Words such as “anticipate,” “expect,” “intend,” “plan,” “believe,” “seek,” “outlook” and “estimate” as well as similar words and phrases signify forward-looking statements. SPDR® Gold Trust’s forward-looking statements are not guarantees of future results and conditions and important factors, risks and uncertainties may cause our actual results to differ materially from those expressed in our forward-looking statements.

Trust Overview

SPDR® Gold Trust (the “Trust”) is an investment trust that was formed on November 12, 2004 (the “Date of Inception”). The Trust issues baskets of Shares (“Baskets”) in exchange for deposits of gold and distributes gold in connection with the redemption of Baskets. The investment objective of the Trust is for the Shares to reflect the performance of the price of gold bullion, less the expenses of the Trust’s operations. The Shares are designed to provide investors with a cost effective and convenient way to invest in gold.

Gold is held by HSBC Bank plc ("HSBC") and JPMorgan Chase Bank, N.A. ("JPMorgan" and each of HSBC and JPMorgan, a "Custodian" and together, the “Custodians”) on behalf of the Trust.

As of the date of this quarterly report, Credit Suisse Securities (USA) LLC, Goldman, Sachs & Co., Goldman Sachs Execution & Clearing, L.P., HSBC Securities (USA) Inc., J.P. Morgan Securities LLC, Merrill Lynch Professional Clearing Corp., Morgan Stanley & Co. LLC, RBC Capital Markets LLC, UBS Securities LLC and Virtu Americas LLC are the only Authorized Participants. An updated list of Authorized Participants can be obtained from the Trustee or the Sponsor.

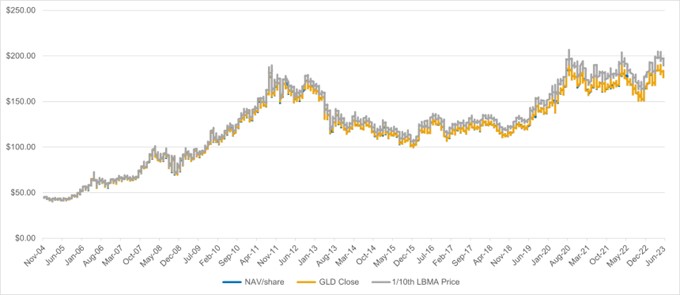

Investing in the Shares does not insulate the investor from certain risks, including price volatility. The following chart illustrates the movement in the price of the Shares and NAV of the Shares against the corresponding gold price (per 1/10 of an oz. of gold) since the day the Shares first began trading on the NYSE and subsequent transfer to NYSE Arca:

Share price & NAV v. gold price – November 18, 2004 to June 30, 2023

The divergence of the price of the Shares and NAV of the Shares from the gold price over time reflects the cumulative effect of the Trust expenses that arise if an investment had been held since inception.

Critical Accounting Policy

Valuation of Gold, Definition of NAV

The Trustee values the gold held by the Trust and determines the NAV of the Trust as of the LBMA Gold Price PM on each day that the NYSE Arca is open for regular trading, at the earlier of the LBMA Gold Price PM for the day or 12:00 PM New York time. If no LBMA Gold Price PM is announced on a particular evaluation day or if the LBMA Gold Price PM has not been announced by 12:00 PM New York time on a particular evaluation day, the next most recent LBMA Gold Price (AM or PM) is used in the determination of the NAV of the Trust, unless the Trustee, in consultation with the Sponsor, determines that such price is inappropriate to use as the basis for such determination. In the event the Trustee and the Sponsor determine that such price is not an appropriate basis for valuation of the Trust’s gold, they will identify an alternative basis for such valuation to be employed by the Trustee. While we believe that the LBMA Gold Price is an appropriate indicator of the value of gold, there are other indicators that are available that could be different than the LBMA Gold Price. The use of such an alternative indicator could result in materially different fair value pricing of the gold in the Trust which could result in different market adjustments or redemption value adjustments of our outstanding redeemable Shares.

Once the value of the gold has been determined, the Trustee subtracts all estimated accrued fees, expenses and other liabilities of the Trust from the total value of the gold and all other assets of the Trust (other than any amounts credited to the Trust’s reserve account, if established). The resulting figure is the NAV of the Trust. The Trustee determines the NAV per Share by dividing the NAV of the Trust by the number of Shares outstanding as of the close of trading on NYSE Arca.

Inspectorate International Limited (“Inspectorate”) conducts two counts each year of the gold bullion held on behalf of the Trust at the vaults of the Custodians. A complete bar count is conducted once per year and coincides with the Trust’s financial year end at September 30th. On October 3, 2022, Inspectorate concluded the annual full count of the Trust’s gold bullion held by HSBC. The second count is a random sample count and is conducted at a date which falls within the same financial year and was conducted most recently at JPMorgan's vault on March 24, 2023, and at HSBC's vault on April 5, 2023. The results can be found on www.spdrgoldshares.com. The Sponsor generally visits the vaults of the Custodians twice a year as part of its due diligence procedures.

Results of Operations

In the three months ended June 30, 2023, an additional 21,500,000 Shares (215 Baskets) were created in exchange for 1,997,516.6 ounces of gold, 23,300,000 Shares (233 Baskets) were redeemed in exchange for 2,164,492.9 ounces of gold, and 29,669.9 ounces of gold were sold to pay expenses.

At June 30, 2023, the amount of gold owned by the Trust and held by the Custodians was 29,797,492.7 ounces, 100% of which is allocated gold in the form of London Good Delivery gold bars with a market value of $56,980,255,365 based on the LBMA Gold Price PM on June 30, 2023 (cost— $49,807,017,551).

At September 30, 2022, the amount of gold owned by the Trust and held by the Custodians was 30,323,468 ounces, 100% of which is allocated gold in the form of London Good Delivery gold bars with a market value of $50,693,257,111 based on the LBMA Gold Price PM on September 30, 2022 (cost— $49,274,427,022).

Cash Resources and Liquidity

At June 30, 2023, the Trust did not have any cash balances. When selling gold to pay expenses, the Trustee endeavors to sell the exact amount of gold needed to pay expenses in order to minimize the Trust’s holdings of assets other than gold. As a consequence, we expect that the Trust will not record any net cash flow from its operations and that its cash balance will be zero at the end of each reporting period.

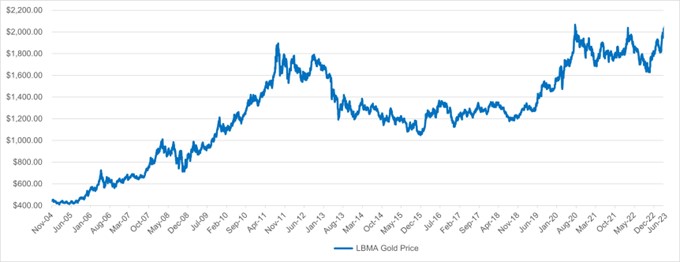

Movements in the Price of Gold

As movements in the price of gold are expected to directly affect the price of the Trust’s Shares, investors should understand what the recent movements in the price of gold have been. Investors, however, should also be aware that past movements in the gold price are not indicators of future movements.

The following chart provides historical background on the price of gold. The chart illustrates movements in the price of gold in US dollars per ounce over the period from November 12, 2004 to June 30, 2023 and is based on the LBMA Gold Price PM when available.

Daily Gold Price – November 12, 2004 – June 30, 2023

LBMA Gold Price PM USD

The average, high, low and end-of-period gold prices for the three and twelve-month periods over the prior three years and for the period from the Date of Inception through June 30, 2023, based on the LBMA Gold Price PM when available from March 20, 2015 and previously the London Fix, were:

| Last |

||||||||||||||||||||

| End of |

business |

|||||||||||||||||||

| Period |

Average |

High |

Date |

Low |

Date |

period |

day (1) |

|||||||||||||

| Three months to September 30, 2020 |

$ | 1,908.56 | $ | 2,067.15 | Aug 6, 2020 |

$ | 1,771.05 | July 1, 2020 |

$ | 1,886.90 | Sep 30, 2020 |

|||||||||

| Three months to December 31, 2020 |

$ | 1,874.23 | $ | 1,940.80 | Nov 6, 2020 |

$ | 1,762.55 | Nov 30, 2020 |

$ | 1,891.10 | Dec 31, 2020 |

(2) |

||||||||

| Three months to March 31, 2021 |

$ | 1,794.01 | $ | 1,943.20 | Jan 4, 2021 |

$ | 1,683.95 | Mar 30, 2021 |

$ | 1,691.05 | Mar 31, 2021 |

|||||||||

| Three months to June 30, 2021 |

$ | 1,816.48 | $ | 1,902.75 | Jun 2, 2021 |

$ | 1,726.05 | Apr 1, 2021 |

$ | 1,763.15 | Jun 30, 2021 |

|||||||||

| Three months to September 30, 2021 |

$ | 1,789.52 | $ | 1,829.30 | Jul 29, 2021 |

$ | 1,723.35 | Aug 10, 2021 |

$ | 1,742.80 | Sept 30, 2021 |

|||||||||

| Three months to December 31, 2021 |

$ | 1,795.25 | $ | 1,864.90 | Nov 17, 2021 |

$ | 1,753.20 | Oct 5, 2021 |

$ | 1,820.10 | Dec 31, 2021 |

(2) |

||||||||

| Three months to March 31, 2022 |

$ | 1,877.16 | $ | 2,039.05 | Mar 08, 2022 |

$ | 1,788.15 | Jan 28, 2022 |

$ | 1,820.10 | Mar 31, 2022 |

|||||||||

| Three months to June 30, 2022 |

$ | 1,870.58 | $ | 1,976.75 | Apr 13, 2022 |

$ | 1,809.50 | May 16, 2022 |

$ | 1,817.00 | June 30, 2022 |

|||||||||

| Three months to September 30, 2022 |

$ | 1,728.91 | $ | 1,808.40 | Jul 4, 2022 |

$ | 1,634.30 | Sep 27, 2022 |

$ | 1,671.75 | Sep 30, 2022 |

|||||||||

| Three months to December 31, 2022 |

$ | 1,725.85 | $ | 1,823.55 | Dec 13, 2022 |

$ | 1,628.75 | Nov 3, 2022 |

$ | 1,812.35 | Dec 30, 2022 |

(2) |

||||||||

| Three months ended March 31, 2023 |

$ | 1,889.92 | $ | 1,993.80 | Mar 24, 2023 |

$ | 1,810.95 | Feb 24, 2023 |

$ | 1,979.70 | Mar 31, 2023 |

|||||||||

| Three months ended June 30, 2023 |

$ | 1,975.93 | $ | 2,048.45 | Apr 13, 2023 |

$ | 1,899.60 | Jun 29, 2023 |

$ | 1,912.25 | Jun 30, 2023 |

|||||||||

| Twelve months ended June 30, 2021 |

$ | 1,848.95 | $ | 2,067.15 | Aug 6, 2020 |

$ | 1,683.95 | Mar 30, 2021 |

$ | 1,763.15 | Jun 30, 2021 |

|||||||||

| Twelve months ended June 30, 2022 |

$ | 1,832.48 | $ | 2,039.05 | Mar 8, 2022 |

$ | 1,723.35 | Aug 10, 2021 |

$ | 1,817.00 | Jun 30, 2022 |

|||||||||

| Twelve months ended June 30, 2023 |

$ | 1,829.07 | $ | 2,048.45 | Apr 13, 2023 |

$ | 1,628.75 | Nov 3, 2022 |

$ | 1,912.25 | Jun 30, 2023 |

|||||||||

| November 12, 2004 to June 30, 2023 |

$ | 1,258.46 | $ | 2,067.15 | Aug 6, 2020 |

$ | 411.10 | Feb 8, 2005 |

$ | 1,912.25 | Jun 30, 2023 |

|||||||||

| (1) | The end of period gold price is the LBMA Gold Price PM on the last business day of the period. This is in accordance with the Trust Indenture and the basis used for calculating the Net Asset Value of the Trust. |

| (2) | There was no LBMA Gold Price PM on the last business day of December 2022, 2021 or 2020. The LBMA Gold Price AM on the last business day of December 2022, 2021 and 2020 was $1,812.35, $1,820.10 and $1,891.10, respectively. The Net Asset Value of the Trust on December 31, 2022, 2021 and 2020 was calculated using the LBMA Gold Price AM, in accordance with the Trust Indenture. |

Item 3. Quantitative and Qualitative Disclosures About Market Risk

The Trust Indenture does not authorize the Trustee to borrow for payment of the Trust’s ordinary expenses. The Trust does not engage in transactions in foreign currencies which could expose the Trust or holders of Shares to any foreign currency related market risk. The Trust does not invest in any derivative financial instruments or long-term debt instruments. Fluctuations in the value of gold bullion will affect the value of Shares which are designed to reflect the performance of the price of gold bullion, less the Trust’s expenses.

Item 4. Controls and Procedures

Disclosure Controls and Procedures

The duly authorized officers of the Sponsor, performing functions equivalent to those a principal executive officer and principal financial officer of the Trust would perform if the Trust had any officers, have evaluated the effectiveness of the Trust’s disclosure controls and procedures, and have concluded that the disclosure controls and procedures of the Trust were effective as of the end of the period covered by this report. Such disclosure controls and procedures are designed to provide reasonable assurance that information required to be disclosed in the reports that the Trust files or submits under the Securities Exchange Act of 1934, as amended, are recorded, processed, summarized and reported, within the time period specified in the applicable rules and forms, and that such information is accumulated and communicated to the duly authorized officers of the Sponsor performing functions equivalent to those a principal executive officer and principal financial officer of the Trust would perform if the Trust had any officers, and to the Audit Committee of the Sponsor, as appropriate, to allow timely decisions regarding required disclosure.

Internal Control Over Financial Reporting

There has been no change in the internal control over financial reporting that occurred during our most recent fiscal quarter that has materially affected, or is reasonably likely to materially affect, the Trust’s internal control over financial reporting.

None.

You should carefully consider the factors discussed in Part I, Item 1A. “Risk Factors” in our Annual Report on Form 10-K for the year ended September 30, 2022, which could materially affect our business, financial condition or future results. There have been no material changes in our risk factors from those disclosed in our Annual Report on Form 10-K.

The risks described in our Annual Report on Form 10-K are not the only risks facing the Trust. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

| a) |

None. |

| b) |

Not applicable. |

| c) |

Although the Trust does not purchase shares directly from its shareholders, in connection with its redemption of Baskets, the Trust redeemed 233 Baskets (23,300,000 Shares) during the quarter ended June 30, 2023 |

| Period |

Total Number of Shares Redeemed |

Average Ounces of Gold Per Share |

||||||

| 4/1/23 to 4/30/23 |

7,000,000 | 0.09293 | ||||||

| 5/1/23 to 5/31/23 |

6,500,000 | 0.09290 | ||||||

| 6/1/23 to 6/30/23 |

9,800,000 | 0.09287 | ||||||

| Total |

23,300,000 | 0.09290 | ||||||

Item 3. Defaults Upon Senior Securities

None.

Item 4. Mine Safety Disclosures.

Not Applicable.

|

a) |

None. |

|

b) |

Not applicable. |

|

c) |

Not applicable. |

The exhibits listed on the accompanying Exhibit Index, and such Exhibit Index, are filed or incorporated by reference as a part of this report.

EXHIBIT INDEX

Pursuant to Item 601 of Regulation S-K

| Exhibit No. |

Description of Exhibit |

|

| 31.1 |

||

| 31.2 |

||

| 32.1 |

||

| 32.2 |

||

| 101.INS* |

Inline XBRL Instance Document |

|

| 101.SCH* |

Inline XBRL Taxonomy Extension Schema Document |

|

| 101.CAL* |

Inline XBRL Taxonomy Extension Calculation Linkbase Document |

|

| 101.LAB* |

Inline XBRL Taxonomy Extension Label Linkbase Document |

|

| 101.PRE* |

Inline XBRL Taxonomy Extension Presentation Linkbase Document |

|

| 101.DEF* |

Inline XBRL Taxonomy Extension Definition Linkbase Document |

|

| 104.1 |

Cover Page Interactive Data File—The cover page interactive data file does not appear in the interactive data file because its XBRL tags are embedded within the inline XBRL document. |

| * | Pursuant to Rule 406T of Regulation S-T, these interactive data files are deemed not filed or part of a registration statement or prospectus for purposes of Sections 11 or 12 of the Securities Act of 1933, as amended, are deemed not filed for the purposes of Section 18 of the Securities and Exchange Act of 1934, as amended, and otherwise are not subject to liability under those sections. |

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned in the capacities* indicated thereunto duly authorized.

| WORLD GOLD TRUST SERVICES, LLC |

|

| Sponsor of the SPDR® Gold Trust (Registrant) |

|

| /s/ Joseph R. Cavatoni |

|

| Joseph R. Cavatoni |

|

| Principal Executive Officer* |

|

| /s/ Amanda Krichman |

|

| Amanda Krichman | |

| Principal Financial and Accounting Officer* | |

Date: August 7, 2023

* The Registrant is a trust and the persons are signing in their capacities as officers of World Gold Trust Services, LLC, the Sponsor of the Registrant.