UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended:

or

For the transition period from __________ to __________

Commission

File Number

(Exact Name of Registrant as Specified in Its Charter)

| (State of Incorporation) | (I.R.S. Employer ID Number) |

P. R. | ||

| (Address of Principal Executive Offices) | (Zip Code) |

(Registrant’s telephone number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name of Each Exchange on Which Registered | ||

| The |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. ☒

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant

to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☐ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.). ☐ Yes

As

of June 30, 2021, the aggregate market value of the common equity held by non-affiliates of the registrant was $

As of April 14, 2022, there were

BIMI INTERNATIONAL MEDICAL INC.

(FORMERLY KNOWN AS “NF ENERGY SAVING CORPORATION” AND “BOQI INTERNATIONAL MEDICAL INC.”)

FORM 10-K

TABLE OF CONTENTS

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this Annual Report on Form 10-K, other than historical facts, may be considered forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. We intend for all such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Securities Act and the Exchange Act, as applicable by law. Such statements include, in particular, statements about our plans, strategies and prospects, and are subject to certain risks and uncertainties, as well as known and unknown risks, which could cause actual results to differ materially from those projected or anticipated. Therefore, such statements are not intended to be a guarantee of our performance in future periods. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as “may,” “will,” “would,” “could,” “should,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” or other similar words.

If one or more of the factors affecting our forward-looking information and statements proves incorrect, then our actual results, performance or achievements could differ materially from those expressed in, or implied by, forward-looking information and statements contained in this Annual Report on Form 10-K and other reports and registration statements filed by us with the U.S. Securities and Exchange Commission (“SEC”). Therefore, we caution you not to place undue reliance on our forward-looking information and statements. We will not update the forward-looking statements to reflect actual results or changes in the factors affecting the forward-looking statements. Forward-looking information and statements should not be viewed as predictions, and should not be the primary basis upon which investors evaluate us. Any investor in our Common Stock should consider all risks and uncertainties disclosed in our filings with the SEC, all of which are accessible on the SEC’s website at http://www.sec.gov. We undertake no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results.

ii

PART I

ITEM 1. BUSINESS

The Company

As used herein the terms “we”, “us”, “our,” “BIMI” and the “Company” means BIMI International Medical Inc., a Delaware corporation, and its subsidiaries, Lasting Wisdom Holdings Limited (“Lasting”), a corporation organized and existing under the laws of BVI, Pukung Limited (“Pukung”), a company organized and existing under the laws of Hong Kong, Beijing Xinrongxin Industrial Development Co., Ltd., (“Xinrongxin”), a company organized and existing under the laws of the PRC, Dalian Boyi Technology Co., Ltd. (“Dalian Boyi”), a company organized and existing under the laws of the PRC, Chongqing Guanzan Technology Co., Ltd. (“Guanzan”), a company organized and existing under the laws of the PRC, Chongqing Lijiantang Pharmaceutical Co. Ltd.(“Lijiantang”), a company organized and existing under the laws of the PRC, Chongqing Shude Pharmaceutical Co., Ltd (“Shude”), a company organized and existing under the laws of the PRC. Boyi (Liaoning) Technology Co., Ltd. (“Liaoning Boyi”), a company organized and existing under the laws of the PRC, Bimai Pharmaceutical (Chongqing) Co., Ltd (“Chongqing Bimai”), a company organized and existing under the laws of the PRC. Chongqing Guoyitang Hospital (“Guoyitang”), a company organized and existing under the laws of the PRC. Chongqing Huzhongtang Healthy Technology Co., Ltd (“Huzhongtang”),a company organized and existing under the laws of the PRC. Chaohu Zhongshan Minimally Invasive Hospital (“Zhongshan”), a company organized and existing under the laws of the PRC. Wuzhou Qiangsheng Hospital (“Qiangsheng”), a company organized and existing under the laws of the PRC. Suzhou Eurasia Hospital(“Eurasia”), a company organized and existing under the laws of the PRC. Yunnan Yuxi MinKang hospital (“Minkang”). a company organized and existing under the laws of the PRC. Chongqing Zhuoda Pharmaceutical Co., Ltd (“Zhuoda”), a company organized and existing under the laws of the PRC. Chongqing Qianmei Medical Devices Co., Ltd (“Qianmei”), a company organized and existing under the laws of the PRC. Pusheng Pharmaceutical Co., Ltd(“Pusheng”) and Bimai Hospital Management (Chongqing) Co. Ltd (“Bimai Hospital”), a company organized and existing under the laws of the PRC.

We were incorporated under the laws of the State of Delaware as Galli Process, Inc. on October 31, 2000. On December 31, 2001, Galli Process, Inc, changed its name to Global Broadcast Group, Inc. On November 12, 2004, Global Broadcast Group, Inc. changed its name to Diagnostic Corporation of America. On March 15, 2007, we changed our name to NF Energy Saving Corporation of America, and on August 24, 2009, we changed our name to NF Energy Saving Corporation. On December 16, 2019, we changed our name to BOQI International Medical Inc. to reflect our new focus on the health care industry and on June 21, 2021, the Company changed its name to BIMI International Medical Inc. Our internet website address is http://www.usbimi.com/index.html. The information on our website is not incorporated by reference into this annual report.

All share and per share information included in this Annual Report has been adjusted to reflect a five share for one share reverse split effective as of February 3, 2022.

Recent History

In January 2019, Mr. Yongquan Bi, a director and a substantial stockholder of the Company, together with a group of investors whose combined holdings constituted a majority of the voting rights in our company, delivered a written consent to the Company’s registered office. The written consent modified the composition of the Board of Directors and Mr. Yongquan Bi was subsequently appointed as the Company’s Chairman of the Board, Chief Executive Officer and President. In October 2019, Mr. Yongquan Bi resigned from the office of the Chief Executive Officer and President and Mr. Tiewei Song succeeded him as Chief Executive Officer and President. On December 14, 2021, Mr. Yongquan Bi resigned as a director and Chairman of the Board of Directors of the Company.

The NF Group disposition

In late 2019, we committed to a plan to dispose of our legacy energy business, NF Investment and its subsidiaries (the “NF Group”), in order to focus on our healthcare business. On March 31, 2020, we entered into an agreement to sell the NF Group for $10 million to be paid in cash at the closing. The transaction closed on June 23, 2020, at which time we received $10 million.

1

The Boqi Zhengji Acquisition and Subsequent Disposition

On October 14, 2019, as the initial step in our shift of focus from the energy sector to the healthcare business, we acquired Boqi Zhengji, the operator of a pharmacy chain business in the PRC, by purchasing 100% of the equity interests of Lasting, Boqi Zhengji’ s parent company. Lasting, through its wholly owned subsidiaries Pukung, and Xinrongxin, owned all the ownership interests in Boqi Zhengji. Lasting, Pukung, Xinrongxin and Boqi Zhengji are hereinafter referenced as the “Boqi Zhengji Group”. The purchase price for the Boqi Zhengji consisted of RMB 40 million (approximately $5,655,709) and 300,000 shares of Common Stock. The 300,000 shares of Common Stock were issued to the sellers in October 2019. The cash consideration, which was subject to post-closing adjustments based on the performance of Boqi Zhengji, measured by its pharmacy club member headcount and gross profit in 2020, was not payable until 2021.

Shortly after the acquisition, the business of Boqi Zhengji was severely impacted by the spread of coronavirus, or COVID-19, and its revenues plummeted. On December 11, 2020, we entered into a Termination and Release Agreement (the “Release Agreement”) with the four individuals who sold Boqi Zhengji to us. We and the sellers confirmed that Boqi Zhengji’s performance targets as stipulated in the Stock Purchase Agreement dated April 11, 2019 (as amended on February 6, 2020, the “Boqi SPA”) would not be met, and therefore the sellers would not be eligible to receive the contingent RMB 40 million cash consideration or any other additional payment.

On December 11, 2020, we entered into an agreement to sell all the issued and outstanding equity interests in Boqi Zhengji to a third-party in consideration of $1,700,000 to be paid in cash at the closing. While the cash consideration was received on December 18, 2020, the official recognition of the closing was not received until February 2, 2021.

Strategy

Our strategy is to build a comprehensive healthcare ecosystem, centering on online and offline healthcare products and services, including retail and wholesale sales of medical devices and pharmaceuticals, and hospital services. We intend to expand through both organic growth and acquisitions.

The Guanzan Acquisition

On February 1, 2020, we entered into a stock purchase agreement to acquire Guanzan, a company engaged in the distribution of medical devices and pharmaceuticals, based in Chongqing, the largest city in Southwest region of the PRC. Pursuant to the agreement, we agreed to purchase all the issued and outstanding equity interests in Guanzan and its subsidiary, Shude, (together the “Guanzan Group”), for RMB 100,000,000 (approximately $14,285,714) to be paid by the issuance of 190,000 shares of Common Stock and the cash payment of RMB 80,000,000 (approximately $11,428,571). On March 18, 2020, we closed the Guanzan acquisition by delivering 190,000 shares of Common Stock. The cash consideration, was subject to post-closing adjustments based on the performance of Guanzan in 2020 and 2021.

The rationale for the Guanzan Acquisition was to further expand into the healthcare field by acquiring a medical devices and pharmaceuticals distribution business, in line with our expansion strategy which focuses on deeper penetration of the healthcare market in the Southwest region of China and achieving a wider footprint in the PRC. At the time of the acquisition, Guanzan had strong sales capabilities in Chongqing, the largest city in the Southwest region of the PRC.

On November 20, 2020, the parties to the Guanzan acquisition agreement entered into a Prepayment and Amendment Agreement (the “Prepayment Agreement”) in light of Guanzan’s performance during the period from March 18, 2020 to September 30, 2020, providing for the prepayment of RMB 20,000,000 of the contingent cash consideration in the form of shares of Common Stock. On November 30, 2020, we issued 200,000 shares of Common Stock valued at $3 million as the prepayment. On August 27, 2021, we issued 920,000 shares of Common Stock in full payment of the balance of the post-closing consideration for the acquisition of Guanzan.

The Guoyitang Acquisition

On December 9, 2020, we entered into an agreement to acquire Chongqing Guoyitang Hospital (“Guoyitang”), the owner and operator of a private general hospital in Chongqing City, a city in Southwest China, with 50 hospital beds and 98 employees, including 14 doctors, 28 nurses, 43 other medical staff and 13 non-medical staff. Pursuant to the agreement, we agreed to purchase all the issued and outstanding equity interests in Guoyitang for RMB 100,000,000 (approximately $15,325,905) to be paid by the issuance of 400,000 shares of Common Stock and the payment of RMB 60,000,000 (approximately $9,195,543) in cash. The acquisition closed on February 2, 2021, at which time 4000,000 shares of Common Stock were delivered to the sellers. The cash consideration of RMB 60,000,000 (approximately $9,195,543) was paid in December 2020. The balance of the purchase price of RMB 40,000,000 (approximately $6,097,560) was subject to post-closing adjustments based on the performance of Guoyitang in 2021 and 2022. For the year ended December 31, 2021,there was a performance failure of Guoyitang, accordingly the sellers are not eligible to receive any contingent payments.

2

The Zhongshan Acquisition

On December 15, 2020, we entered into a stock purchase agreement to acquire Chaohu Zhongshan Minimally Invasive Hospital (“Zhongshan”), a private hospital in the Southeast region of China with 160 hospital beds and 95 employees, including 20 doctors, 48 nurses, 10 other medical staff and 17 non-medical staff. Pursuant to the agreement, we agreed to purchase all the issued and outstanding equity interests in Zhongshan for RMB 120,000,000 (approximately $18,348,623), to be paid by the issuance of 400,000 shares of Common Stock and the payment of RMB 80,000,000 in cash. The transaction closed on February 5, 2021 when 100% ownership of Zhongshan was transferred to our company. The cash consideration of RMB 40,000,000 (approximately $6,116,207) was paid to the seller in December 2020. On February 12, 2021, we issued 400,000 shares of Common Stock then valued at RMB 40,000,000 (approximately $6,116,207) to the seller as part of the consideration. The balance of the purchase price in the amount of RMB 40,000,000 (approximately $6,116,207) was subject to post-closing adjustments based on the performance of Zhongshan in 2021 and 2022.

On February 1, 2022, we entered into an amendment to the agreement providing for the reduction of the purchase price, including a retroactive 50% decrease in the closing cash payment, a 50% retroactive decrease in the deferred closing stock payment and a 50% reduction of the 2021 and 2022 performance targets. As a result of such amendment, the Seller agreed to return RMB 40,000,000 in cash to us and 200,000 shares of Common Stock, which were previously delivered to the seller as part of the closing consideration for Zhongshan.

The Qiangsheng, Eurasia And Minkang Hospitals Acquisition

On April 9, 2021, we entered into a stock purchase agreement to acquire Wuzhou Qiangsheng Hospital (“Qiangsheng”),Suzhou Eurasia Hospital(“Eurasia”) and Yunnan Yuxi MinKang hospital (“Minkang”). Qiangsheng, Eurasia and Minkang are private hospitals in the Southern, Northern and Southwest region of China, respectively. Qiangsheng has 20 hospital beds and 63 employees, including 18 doctors, 17 nurses, 8 other medical staff and 20 non-medical staff. Eurasia has 12 hospital beds and 52 employees, including 12 doctors, 15 nurses, 7 other medical staff and 18 non-medical staff. Minkang has 126 hospital beds and 116 employees, including 24 doctors, 58 nurses, 12 other medical staff and 22 non-medical staff. Pursuant to the agreement, we agreed to purchase all the issued and outstanding equity interests in Qiangsheng, Eurasia and Minkang Hospitals for RMB 162,000,000 (approximately $24,827,927), to be paid by the issuance of 800,000 shares of Common Stock and the payment of RMB 84,000,000 in cash. The first payment of the cash consideration was RMB 20,000,000 (approximately $3,097,317). The second and third payments of the Cash Consideration of RMB 64,000,000 (approximately $9,911,416) are subject to post-closing adjustments based on the performance of Qiangsheng, Eurasia and Minkang in 2021 and 2022. The sellers can choose to receive the second and third payments in the form of shares of Common Stock valued at $15.00 per share or in cash. The transaction closed on May 6, 2021, at which time the 800,000 shares of Common Stock were issued. Cash consideration of RMB 20,000,000 was paid on December 1, 2021.

The Zhuoda Acquisition

On September 10, 2021, we entered into a stock purchase agreement to acquire Chongqing Zhuoda Pharmaceutical Co., Ltd. (“Zhuoda”), a company engaged in the distribution of medical devices and pharmaceuticals, based in Chongqing, the largest city in Southwest region of the PRC. Pursuant to the agreement, we agreed to purchase all of the issued and outstanding equity interests in Zhuoda in consideration of $11,617,500 (RMB 75,000,000). Pursuant to the acquisition agreement the entire purchase consideration is payable in shares of Common Stock. At the closing, 440,000 shares of Common Stock valued by the parties at RMB 43,560,000, or $15.00 per share (approximately $6,600,000) were issued as partial consideration for the purchase and the remainder of the purchase price of approximately $5,017,500 (RMB 31,440,000), is subject to post-closing adjustments based on the performance of Zhuoda in 2022 and 2023.

We may pay the outstanding consideration for the Zhuoda acquisitions to the extent payable: (i) in cash from funds to be raised from the sale of equity (to the extent possible) or (ii) through the issuance of shares of Common Stock. If we elect to issue shares of Common Stock in consideration for the balance of the purchase for Zhuoda, we may be required to seek stockholder approval of such issuances prior to issuing such shares.

3

The Mali Hospital Acquisition

On December 20, 2021, we entered into a stock purchase agreement to acquire Bengbu Mali OB-GYN Hospital Co., Ltd. (“Mali Hospital”), a private OB-GYN specialty hospital with 199 beds located in Bengbu city in the southeast region of the People’s Republic of China. We agreed to purchase all the issued and outstanding equity interests in Mali Hospital in consideration of $16,750,000. At the closing, $2,800,000 in cash and 600,000 shares of Common Stock valued at $ 9,000,000, or $15.00 per share will be delivered as partial consideration for the purchase of Mali Hospital. The remainder of the purchase price of 330,000 shares of Common Stock valued at $4,950,000, or $15.00 per share, is subject to post-closing adjustments based on the performance of Mali Hospital in 2022 and 2023, which under certain circumstances may be paid on an earlier date if the 2022 net profit target is met or exceeded In the event an accelerated payment is made, the sellers will not be eligible to receive any additional payments.

The closing of the Mali Hospital acquisition is expected to take place in April 2022, subject to necessary regulatory approvals.

Segments

In 2021 we were engaged in four business segments, wholesale pharmaceuticals, wholesale medical devices, medical services and retail pharmacies. In 2020, we were engaged in three business segments, wholesale pharmaceuticals, wholesale medical devices and retail pharmacies.

Holding Foreign Company Accountable Act

In December 2020, the Holding Foreign Companies Accountable Act, or the HFCAA, was signed into law. The HFCAA amended the Sarbanes Oxley Act to prohibit trading on U.S. exchanges of public reporting companies audited by audit firms located in foreign jurisdictions that the PCAOB has been unable to inspect for three sequential years. Trading in our securities may be prohibited under the HFCAA, if the Public Company Accounting Oversight Board (United States) (the “PCAOB”) determines that it cannot inspect or investigate completely our auditor.

Pursuant to the HFCAA, the PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in (i) the PRC because of a position taken by one or more authorities in the PRC and (ii) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations.

The PCAOB is currently unable to conduct inspections in China without the approval of Chinese government authorities. If it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, investors may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected by the PCAOB, or a lack of PCAOB inspections of audit work undertaken the PRC that prevents the PCAOB from regularly evaluating our auditors’ audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate.

Our auditor, Audit Alliance LLP, is an independent registered public accounting firm with the PCAOB, and as an auditor of publicly traded companies in the U.S., is subject to laws in the U.S. pursuant to which the PCAOB conducts regular inspections to assess its compliance with the applicable professional standards. On December 16, 2021, the PCAOB issued its determination that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, and the PCAOB included in the report of its determination a list of the accounting firms that are headquartered in the PRC or Hong Kong. Audit Alliance LLP is based in Singapore and this list does not include our auditor. Should the PCAOB be unable to fully conduct inspections of our auditor’s work papers in China, it will make it difficult to evaluate the effectiveness of our auditor’s audit procedures or equity control procedures. Investors may consequently lose confidence in our reported financial information and procedures or quality of the financial statements, which would adversely affect us and our securities.

Moreover, if trading in our securities is prohibited under the HFCAA in the future because the PCAOB determines that it cannot inspect or fully investigate our auditor at such future time, our securities will likely be delisted.

4

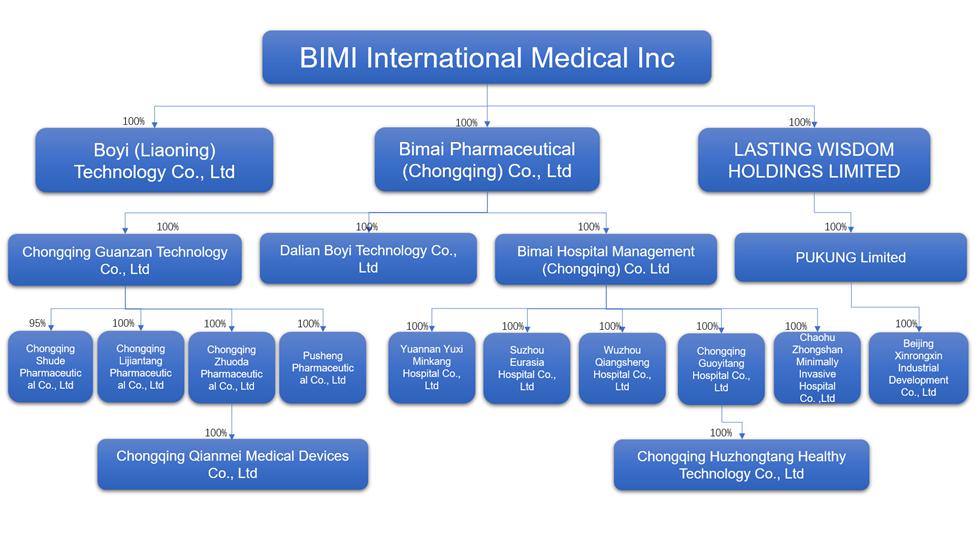

Corporate Organization

The structure of our corporate organization is as follows:

Wholesale Sales of Medical Devices

We acquired Guanzan on March 18, 2020 in an effort to further expand our healthcare operations by acquiring a medical devices and pharmaceuticals distribution business. The acquisition was in line with our expansion strategy, which focuses on deeper penetration of the healthcare market in the Southwest region of the PRC and gaining a wider footprint in the region. On September 22, 2021, we completed the acquisition of Zhuoda. The acquisition was in line with our expansion strategy, which focuses on deeper penetration of the healthcare market in the Southwest region of China and gaining a wider footprint in the PRC.

Our wholesale medical devices and pharmaceuticals business are operated by the Guanzan Group and Zhuoda in Chongqing, the largest city in Southwestern PRC. to drug stores, private clinics, pharmaceutical dealers and hospitals in the Southwest region of China.

Guanzan distribute both domestic and imported advanced medical devices, such as Stryker spinal products, Olympus endoscopes, imported imaging products and diagnostic imaging equipment. Guanzan and to a lesser degree Zhuoda distribute medical devices to drug stores, private clinics, pharmaceutical dealers and hospitals in the Southwest region of the PRC. The majority of our medical device customers are private enterprises in China. Revenues from medical devices for the years ended December 31, 2021 and 2020 was $3,445,107 and $3,059,462 respectively. For the year ended December 31, 2021, our top ten wholesale medical device customers accounted for 72.68% of our wholesale medical devices revenues and two customers accounted for more than 10% of our wholesale medical devices revenues.

We use third party logistics services to transport our medical device products.

5

Wholesale Sales of Pharmaceuticals

Shude primarily distributes pharmaceuticals. Shude currently distributes approximately 300 varieties of products, including raw ingredients for pharmaceutical products, antibiotics, cardiovascular drugs and anti-obesity medicines. The majority of Shude’s customers are private pharmaceutical manufacturers and pharmaceutical wholesale companies in the PRC.

Zhuoda primarily distributes pharmaceuticals. Zhuoda currently distributes approximately 100 products, including antibiotics and their preparations, proprietary Chinese herbal medicine, biochemical drugs and Chinese medicine, etc. The majority of its customers are private pharmaceutical manufacturers and pharmaceutical wholesale companies in the PRC.

On April 21, 2021, we incorporated Pusheng Pharmaceutical Co., Ltd. (“Pusheng”) in the PRC to manage our wholesale distribution of generic drugs.

For the year ended December 31, 2021, our top ten wholesale pharmaceutical customers accounted for 80.82 % of our wholesale pharmaceutical revenues and three customers accounted for more than 10% of our wholesale pharmaceutical revenues.

We use third party logistics services to transport our wholesale pharmaceutical products.

Medical Services

Beginning in 2021, we began to acquire hospitals in an effort to establish a nationwide chain of hospitals specializing in obstetrics and gynecology.

In February 2021, we acquired Guoyitang, the owner and operator of a private general hospital in Chongqing City, a city in Southwest China, with 50 hospital beds and 98 employees, including 14 doctors, 28 nurses, 43 other medical staff and 13 non-medical staff.

In February 2021, we also acquired Zhongshan; a private hospital in the Southeast region of China with 160 hospital beds and 95 employees, including 20 doctors, 48 nurses, 10 other medical staff and 17 non-medical staff.

In May 2021, we acquired the Qiangsheng, Eurasia and Minkang private hospitals in the Southern, Northern and Southwest regions of China, respectively. Qiangsheng has 20 hospital beds and 63 employees, including 18 doctors, 17 nurses, 8 other medical staff and 20 non-medical staff. Eurasia has 12 hospital beds and 52 employees, including 12 doctors, 15 nurses, 7 other medical staff and 18 non-medical staff. Minkang has 126 hospital beds and 116 employees, including 24 doctors, 58 nurses, 12 other medical staff and 22 non-medical staff.

On December 20, 2021, we entered into a stock purchase agreement to acquire Mali Hospital, a private OB-GYN specialty hospital with 199 beds located in Bengbu City in the southeast region of China. Mali Hospital has 148 employees, including 26 doctors, 52 nurses, 11 other medical staff members and 59 non-medical staff members. The closing of the Mali Hospital acquisition is expected to take place in April 2022, subject to necessary regulatory approvals.

Retail Pharmacies

We started to operate in the pharmacy market upon completion of the acquisition of Boqi Zhengji in October 2019. According to the PRC National Bureau of Statistics, in 2020, the per capita consumption expenditure for pharmaceuticals was RMB 1,843 (approximately $283). After deducting the inflation factor, the actual increase in consumption expenditure doubled the growth rate since 2013. In terms of population structure, the aging population continues to grow. The proportion of people aged 65 and over has increased by 6.45 percentage points since 2019. Affected by factors such as expansion and population migration, the urbanization rate in China is over 60%. We believe such urban population expansion means increased demand for healthcare products. We believe that the increasing demand for pharmaceutical products, the aging of the population, the effect of the new “three-child” policy which should promote an increased demand for pediatric medications, and the steady urbanization, will cause the demand for pharmaceutical products to be stable, providing a solid foundation for growth.

6

Our retail pharmacy business sells pharmaceuticals and other healthcare products to customers through directly-owned retail stores. The retail stores offer a wide range of products, including prescription and over-the-counter (“OTC”) drugs, nutritional supplements, traditional Chinese medicines, personal and family care products and medical devices, as well as miscellaneous items. In 2020, we sold the Boqi Pharmacy Group and established a chain of retail pharmacies under the brand name “Lijiantang Pharmacy” in the city of Chongqing, PRC. In September 2021,we closed a pharmacy because of poor performance due to road renovations around the pharmacy. By year-end 2021, we had four pharmacies in Chongqing. Each of our pharmacies employs at least one pharmacist, a store manager and several salespersons. Revenues from retail pharmacy for the years ended December 31, 2021 and 2020 was $316,647 and $84,087 respectively.

The pharmaceutical manufacturers and wholesalers from whom we source our products tend to provide deeper product discounts to companies with both wholesale and retail businesses.

We favor retail locations in well-established residential communities with relatively concentrated consumer purchasing power or are located in close proximity to local hospitals, and evaluate potential store sites to assess consumer traffic, visibility and convenience. Each drugstore has at least one pharmacist on staff, all of whom are properly licensed. The average area of our pharmacy stores is 200 square meters. We only accept prescriptions from licensed health care providers, and verify the validity, accuracy, and completeness of all prescriptions. Most pharmacies also maintain a TCM counter staffed by licensed herbalists. After opening, a location may take up to one year to achieve our projected revenue goals for that particular location Various factors influence individual store revenue including, but not limited to, location, nearby competition, local population demographics, square footage, and government insurance coverage. The first store achieved the expected revenue goal.

At present, we sell prescription drugs, OTC drugs, nutritional supplements, health foods, sundry products and medical devices through our retail pharmacy business. We also distribute medical devices and pharmaceuticals through our wholesale business.

Our retail pharmacy business procures its products from national wholesalers, small regional wholesalers and various pharmaceuticals trading platforms. Our wholesale business primarily sources its products from large state-owned pharmaceutical manufacturers and wholesalers and mid-sized or small private pharmaceutical manufacturers and wholesalers.

Marketing and Promotion

Our current marketing and promotion efforts are focused on our wholesale medical devices, wholesale pharmaceuticals and retail pharmacy operations, and our strategy is to build brand recognition, build strong customer loyalty, and develop incremental revenue opportunities.

For our wholesale business, we promote our products and brand through participation in trade shows and academic seminars and engaging third party professionals in advertisement efforts. We actively pursue direct sales to hospitals, clinics and pharmacies as well government centralized procurement and bidding projects.

In our retail stores, the store managers and staff are encouraged to propose their own advertising and promotional plans, including holiday promotions, posters and billboards. In addition, we periodically offer special discounts and gift promotions for selected merchandise in conjunction with our suppliers’ marketing programs. We intend to invest in advertising in 2022.We also provide ancillary services such as providing free blood pressure readings in our stores.

Many of our promotional programs are designed to encourage manufacturers to invest resources to market their brands within our stores. We charge manufacturers promotional fees in exchange for the right to promote their products during promotional periods. Since manufacturers provide purchasing incentives and information to help customers make informed purchase decisions, we believe that manufacturer led promotions improve our customers’ shopping experience.

Raw Materials and Suppliers

The Company’s medical devices and pharmaceuticals suppliers include national and regional large-scale pharmaceutical and medical device manufacturing companies and wholesale pharmaceutical companies.

7

We believe that competitive sources are readily available for substantially all of the products we require for our retail and wholesale businesses. As such, we believe that we can change suppliers without any material interruption to our business. To date, we have not experienced any significant difficulty in sourcing our suppliers.

In the year ended December 31, 2021, two vendor accounted for more than 10% of our wholesale medical devices purchases and four vendors accounted for more than 10% of our wholesale pharmaceutical purchases.

Quality Control

We strongly emphasize quality control, which starts with procurement. In addition to their market acceptance and costs, we select products based on Good Manufacturing Practice and Good Supply Practices (“GSP”) compliance by our suppliers. We also assess product quality based on the manufacturer’s facilities and capabilities, including technology, packaging and logistics. We conduct random quality inspections of each batch of products we procure and replace any supplier who fails to pass such inspections.

In addition to general quality control measures described above, we also enforce strict quality control measures at our storage and distribution center. All products for our wholesale and retail businesses are screened upon their arrival, and those with evidence of defects or damages are immediately rejected. Products that pass the screening process are recorded and stored strictly according to each manufacturer’s temperature and other requirements. Products (for both our pharmacies and wholesale customers) are verified against the appropriate delivery orders prior to leaving the facility. We use vehicles with cold-temperature storage to make deliveries as necessary.

Competition

Guanzan, Shude, Zhuoda and Pusheng, our medical devices and pharmaceuticals distributors, have established distribution channels in the city of Chongqing, China. The wholesale medical devices and pharmaceutical distribution industries in China are competitive and highly fragmented. We compete with regional distributors as well as national operators. These competitors have substantially greater logistics capacities and more financial resources, as well as more industry relevant experience, than us.

The pharmacy industry in China is likewise intensely competitive, rapidly evolving and highly fragmented. We compete on the basis of store location, merchandise selection, prices and brand recognition. Many of our competitors include large, national drugstore chains that may have more financial resources, stronger brand strength, and management expertise than us. Other competitors include local and independent drugstores and government operated pharmacies, as well as discount stores, convenience stores, and supermarkets with respect to sundry and other non-medicinal products that we carry.

We plan to focus on on-line initiated sales in the future based on the use of apps and expect to compete against established state-owned pharmacies and internet giants. No assurance can be given that we will succeed in this initiative.

The medical services market in China is highly competitive and fragmented with numerous market participants. Our competitors include major privately-owned multi-site operators in China. We believe the principal competitive factors in this market are price and quality of service, variety of services rendered, convenience and proximity of treatment center location to place of business or residence, brand recognition and reputation, targeted marketing and customized services. We also face intense competition in our general healthcare service business. We compete primarily with other treatment centers in our areas of operation. Key competitive factors include healthcare service quality, reputation, convenience and price. We expect new competitors in the general healthcare service industry will continue to emerge given the state of China healthcare reform and the central and local governments’ supportive policies towards public healthcare reform and private capital investment in the healthcare services industry.

Research and Development

Currently our research and development efforts by our 10-person research and development group are focused on developing mobile APPs (computer programs or software applications designed to run on a mobile device such as a phone, tablet or watch) for our healthcare service platform. We plan to expand the functionality of the current mobile APP used by our customers. In the future, we plan to devote more resources to research and development and plan to acquire businesses with research and development capabilities.

8

Regulatory Compliance

General Regulations

Our operations are subject to regulations imposed by both the PRC and local governments. These include:

Regulations on Annual Inspection. In accordance with relevant PRC laws, all types of enterprises incorporated under PRC laws are required to conduct annual inspections with the State Administration for Industry and Commerce of the PRC or its local branches. In addition, foreign invested enterprises are subject to annual inspections conducted by other applicable PRC governmental authorities. In order to reduce enterprises’ burden of submitting inspection documentation to different governmental authorities, the Measures on Implementing Joint Annual Inspection on Foreign-invested Enterprises issued in 1998 by State Administration of Foreign Exchange (“SAFE”), together with six other ministries, stipulated that foreign-invested enterprises must participate in an annual inspection jointly conducted by all relevant PRC governmental authorities.

Regulations on Foreign Currency Exchange. Pursuant to the Foreign Currency Administration Rules promulgated in 1996 and amended in 2008 and various regulations issued by the State Administration of Industry and Commerce (“SAIC”) and the SAFE and other relevant PRC governmental authorities, Renminbi are freely convertible only to the extent of current account items, such as trade related receipts and payments, interest and dividends. Capital account items, such as direct equity investments, loans and repatriation of investment, require prior approval from SAFE or its local counterpart for conversion of Renminbi into a foreign currency, such as US dollars, and remittance of the foreign currency outside the PRC.

Payments for transactions that take place within the PRC must be made in Renminbi. Unless otherwise approved, PRC companies must repatriate foreign currency payments received from abroad. Foreign-invested enterprises may retain foreign exchange in accounts with designated foreign exchange banks subject to a cap set by SAFE or its local counterpart. Unless otherwise approved, domestic enterprises must convert all of their foreign currency receipts into Renminbi. On August 29, 2008, SAFE promulgated a circular regulating the conversion by a foreign-invested company of its registered capital in foreign currency into Renminbi by restricting how the converted Renminbi may be used. This circular stipulates that the registered capital of a foreign-invested company settled in Renminbi converted from foreign currencies may only be used for purposes within the business scope approved by the applicable governmental authority and may not be used for equity investments within China. Violations of this circular can result in severe penalties, including monetary fines.

In addition, any foreign loans to an operating subsidiary in China that is a foreign invested enterprise, cannot, in the aggregate, exceed the difference between its approved total investment amount and its approved “registered capital amount”.

Regulation of Foreign Exchange in Certain Onshore and Offshore Transactions. In October 2005, SAFE issued Circular 75, which regulates foreign exchange matters in relation to the use of a “special purpose vehicle” by PRC residents to seek offshore equity financing and conduct “return investment” in China. Under Circular 75, a “special purpose vehicle” refers to an offshore entity established or controlled, directly or indirectly, by PRC citizens or PRC entities (collectively, as PRC residents) for the purpose of seeking offshore equity financing using assets or interests owned by such PRC residents or PRC entities in onshore companies, while “round trip investment” refers to the direct investment in China by PRC residents through the use of “special purpose vehicles,” including without limitation, establishing foreign invested enterprises and using such foreign invested enterprises to purchase or control (by way of contractual arrangements) onshore assets. Circular 75 requires that, before establishing or controlling a “special purpose vehicle,” PRC residents are required to complete foreign exchange registration with the competent local counterparts of SAFE for their overseas investments. In addition, such PRC resident is required to amend his or her SAFE registration or to file with SAFE or its competent local branch, with respect to that offshore special purpose vehicle in connection with any increase or decrease of capital, transfer of shares, merger, division, equity investment or creation of any security interest over any assets located in China by the offshore special purpose vehicle. To further clarify the implementation of such amendment or filing procedure, SAFE requires domestic enterprises under Circular 75 to coordinate and supervise such amendment or filings with SAFE or its local counterparts by such PRC residents. If PRC residents fail to comply, the domestic enterprises are required to report to the local SAFE authorities.

Failure to comply with the registration procedures set forth in Circular 75 may result in restrictions being imposed on the foreign exchange activities of the relevant onshore company, including being prohibited from distributing its profits and proceeds from any reduction in capital, share transfer or liquidation to its offshore parent or affiliate, and restrictions on the ability to contribute additional capital from the offshore entity to the PRC entities, and may also subject relevant PRC residents to penalties under PRC foreign exchange administration regulations.

9

Regulation of Overseas Listings. On August 8, 2006, The Ministry of Commerce of the People’s Republic of China (“MOFCOM”), China Securities Regulatory Commission (the “CSRC”), the State-owned Assets Supervision and Administration Commission, State Administration of Taxation (the “SAT”), the SAIC and SAFE jointly promulgated the “Rules on the Mergers and Acquisition of Domestic Enterprises by Foreign Investors,” which became effective on September 8, 2006, and was further amended on June 22, 2009, or the M&A Rules. Among other things, the M&A Rules include provisions that purport to require that an offshore special purpose vehicle, or SPV, formed for listing purposes and controlled directly or indirectly by PRC companies or individuals must obtain the approval of the CSRC prior to the listing and trading of such SPV’s securities on an overseas stock exchange. On September 21, 2006, the CSRC published on its official website procedures specifying documents and materials required to be submitted to it by SPVs seeking CSRC approval of their overseas listings. However, the application of this PRC regulation remains unclear with no consensus currently existing among the leading PRC law firms regarding the scope and applicability of the CSRC approval requirement to various types of transactions, including those which involve the use of variable interest entity agreements.

Regulations of Dividend Distribution. Under current applicable laws and regulations, each of our consolidated PRC entities may pay dividends only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, each of our consolidated PRC entities is required to deposit at least ten percent (10%) of its after-tax profit based on PRC accounting standards each year into its statutory surplus reserve fund until the accumulative amount of such reserve reaches fifty percent (50%) of its registered capital. These reserves are not distributable as cash dividends.

Regulations Relating to Taxation. The PRC Enterprise Income Tax Law applies a 25% enterprise income tax rate to both foreign-invested enterprises and domestic enterprises, except to the extent tax incentives are granted to special industries and projects. Under the PRC Enterprise Income Tax Law and its implementation regulations, dividends generated from the business of a PRC subsidiary after January 1, 2008 and payable to its foreign investor may be subject to a withholding tax rate of 10% if the PRC tax authorities determine that the foreign investor is a non-resident enterprise, unless there is a tax treaty with China that provides for a preferential withholding tax rate. Distributions of earnings generated before January 1, 2008 are exempt from PRC withholding tax.

Under the PRC Enterprise Income Tax Law, an enterprise established outside China with “de facto management bodies” within China is considered a “resident enterprise” for PRC enterprise income tax purposes and is generally subject to a uniform 25% enterprise income tax rate on its worldwide income. A circular issued by the State Administration of Taxation in April 2009 regarding the standards used to classify certain Chinese-invested enterprises controlled by Chinese enterprises or Chinese enterprise groups and established outside of China as “resident enterprises” clarified that dividends and other income paid by such PRC “resident enterprises” will be considered PRC-source income and subject to PRC withholding tax, currently at a rate of 10%, when paid to non-PRC enterprise shareholders. This circular also subjects such PRC “resident enterprises” to various reporting requirements with the PRC tax authorities.

Under the implementation regulations to the PRC Enterprise Income Tax Law, a “de facto management body” is defined as a body that has material and overall management and control over the manufacturing and business operations, personnel and human resources, finances and properties of an enterprise. In addition, the tax circular mentioned above specifies that certain PRC invested overseas enterprises controlled by a Chinese enterprise or a Chinese enterprise group in the PRC will be classified as PRC resident enterprises if the following are located or resident in the PRC: senior management personnel and departments that are responsible for daily production, operation and management; financial and personnel decision making bodies; key properties, accounting books, the company seal, and minutes of board meetings and shareholders’ meetings; and 50% or more of the senior management or directors having voting rights.

Pharmaceutical and Ancillary Regulation

According to the “Administrative Measures for Pharmaceutical Business Licenses” and other relevant regulations in China, we need to obtain qualification certificates the operations of our Company, including all of our subsidiaries and pharmacy stores in China. The qualification certificates mainly include the “Quality Management Certificate for Pharmaceutical Administration” (GSP Certificate) and the “Pharmaceutical Business License”. “Food Business License”, “Medical Device Business License”, “Medical Agency Practice License”, etc.

All of our pharmacies have obtained Pharmaceutical Business Licenses and Pharmaceutical Management Quality Management Certificates In addition, all of our pharmacies have obtained Internet Drug Information Service Qualification Certificates and Medical Device Network Sales Records These business qualifications, which are necessary for operating pharmacies in China, are subject to annual renewal.

10

A distributor of pharmaceutical products must obtain a distribution permit from the relevant provincial or designated municipal or county level Food and Drug Administration. The grant of such permit is subject to an inspection of the distributor’s facilities, warehouses, hygienic environment, quality control systems, personnel, and equipment. The distribution permit is valid for five (5) years, and the holder must apply for renewal of the permit within six (6) months prior to its expiration. In addition, a pharmaceutical product distributor needs to obtain a business license from the relevant administration for industry and commerce prior to commencing its business. All of our retail pharmacies s have obtained necessary pharmaceutical distribution permits, and we do not expect to face any difficulties in renewing these permits and/or certifications.

In addition, under the Supervision and Administration Rules on Pharmaceutical Product Distribution, promulgated by the SFDA, a pharmaceutical product distributor is responsible for its procurement and sales activities and is liable for the actions of its employees or agents in connection with their conduct of distribution on behalf of the distributor. A retail distributor of pharmaceutical products is not allowed to sell prescription pharmaceutical products or Tier A OTC pharmaceutical products listed in the national or provincial medical insurance catalogs without a valid prescription or the presence of a certified in-store pharmacist. See “Reimbursement under the National Medical Insurance Program.”

A distributor of nutritional supplements and other food products must obtain a food circulation permit from its local Administration of Industry and Commerce. The grant of such permit is subject to an inspection of the distributor’s facilities, warehouses, hygienic environment, quality control systems, personnel, and equipment. The food circulation permit is valid for three (3) years, and the holder must apply for renewal of the certificate within thirty (30) days prior to its expiration. The Guanzan Group has received this permit for its operation.

GSP standards regulate wholesale and retail pharmaceutical product distributors to ensure the quality of distribution of pharmaceutical products in China. All wholesale and retail pharmaceutical product distributors are required to apply for GSP certification within thirty (30) days after obtaining drug distribution permits. The current applicable GSP standards require pharmaceutical product distributors to implement strict controls on the distribution of pharmaceutical products, including standards regarding staff qualifications, distribution premises, warehouses, inspection equipment and facilities, management, and quality control. Specifically, the warehouse must be able to store the pharmaceutical products at various required temperatures and humidity, and handle transport, warehouse entries, delivery, and billing by computerized logistics management systems. The GSP certificate is usually valid for five (5) years. Currently, Guanzan Group is a GSP certified company.

Under the Rules on Administration of Prescriptions promulgated by the SFDA, doctors are required to include the chemical ingredients of the medicine they prescribe in their prescription and are not allowed to include brand names in their prescription. This regulation is designed to provide consumers with choices among different pharmaceutical products that contain the same chemical ingredients.

Eligible participants in the national medical insurance program, consisting primarily of urban residents, are entitled to purchase medicine when presenting their medical insurance cards in an authorized pharmacy, provided that the medicine they purchase has been included in the national or provincial medical insurance catalogs. Depending on relevant local regulations, authorized pharmacies can either (i) sell medicine on credit and obtain reimbursement from relevant government social security bureaus on a monthly basis, or (ii) receive payments from the participants at the time of their purchases, and the participants in turn obtain reimbursement from relevant government social security bureaus.

Medications included in the national and provincial medical insurance catalogs are divided into two (2) tiers. Purchases of Tier A pharmaceutical products are generally fully reimbursable. Purchasers of Tier B pharmaceutical products, which are generally more expensive than those in Tier A, are required to make a certain percentage of co-payments, with the remaining amount being reimbursable. The percentage of reimbursement for Tier B OTC products varies in different regions in the PRC. Factors that affect the inclusion of medicine in the medical insurance catalogs include whether the medicine is consumed in large volumes and commonly prescribed for clinical use in China and whether it is considered to be important in meeting the basic healthcare needs of the general public.

China’s Ministry of Labor and Social Security, together with other government authorities, have the power to determine which medicines are included in the national medical insurance catalog every two (2) years, under which of the two (2) tiers the included medicine falls, and whether an included medicine should be removed from the catalog.

11

Under the Advertising Law of the PRC, the contents of an advertisement must be true, lawful, without falsehood, and must neither deceive nor mislead consumers. Accordingly, advertisements must be examined by the competent authority prior to its publication or broadcast through any form of media. In addition, advertisements of pharmaceutical products may only be based on a drug’s approved indication of use statement, and may not contain any assurance of a product’s efficiency, treatment efficiency, curative rate, or any other information prohibited by law. Advertisement for certain drugs should include an admonishment to seek a doctor’s advice before purchasing and application. Advertising is prohibited for certain drugs such as anesthetics and psychotropic drugs.

To further prevent misleading advertising of pharmaceutical products, the SAIC and the SFDA jointly promulgated the Standards for Examination and Publication of Advertisements of Pharmaceutical Products and Measures for Examination of Advertisement of Pharmaceutical Products in March 2007. Under these regulations, an approval must be obtained from the provincial level of food and drug administration before a pharmaceutical product may be advertised. In addition, once approved, an advertisement’s content may not be altered without further approval. Such approval, once obtained, is valid for one (1) year.

Regulation of Medical Institutions

We started to operate in and have been subject to regulations relating to the management of medical institutions upon completion of the acquisition of Guoyitang in January 2021.

The Administrative Measures on Medical Institutions, as amended, provides that the establishment of a medical institution by any entity or individual must be reviewed and approved by health administrative departments at or above the county level and obtain a Medical Institution Practicing Certificate.

The Administrative Measures for Verification of Medical Institutions (For Trial Implementation) provides that the Medical Institution Practicing Certificate is subject to periodic examinations and verifications by registration authorities. The verification period is 3 years for general hospitals, hospitals of traditional Chinese medicine, hospitals of western medicine, hospitals of ethnic minority medicine and specialized hospitals, as well as sanitariums, rehabilitation hospitals, maternity and children’s health care centers, emergency centers, clinical laboratories and specialized disease prevention institutions equipped with more than 100 beds, while the verification period is 1 year for other medical institutions. In the event that a medical institution fails to apply for verification as required and post re-verification procedures or unsuccessful in its re-verification application, the registration authorities may cancel its Medical Institution Practicing Certificate.

According to the Interim Provisions of Management of Physical Examination, the registration authority is required to examine and assess the medical institutions.

According to the Regulations on the Control of Narcotic Drugs and Psychotropic Drugs, as amended, any medical institution that uses narcotic drugs and certain psychotropic drugs is subject to the approval of the relevant authority, and must obtain authority to purchase such drugs.

According to the Administrative Regulations on Sanitation of Public Places and its implementing rules hospitals equipped with waiting rooms must apply to the sanitary administrative authorities for a sanitary license in a timely manner.

According to the Drug Administration Law of PRC, as amended, the Regulations for the Implementation of the Drug Administration Law and the Measures for Supervision and Administration of Drugs of Medical Institutions (For Trial Implementation), medical institutions must purchase drugs from enterprises qualified to produce and deal in drugs. Drugs used by medical institutions must be purchased uniformly by special departments in accordance with the provisions, and other departments and medical staff members of medical institutions are forbidden to purchase drugs on their own.

Seasonality

Our management believes that our operations are not currently subject to seasonal influences.

12

Employees

We consider our employees the most valuable asset of our company. We offer competitive compensation and comprehensive benefits to attract and retain our employees. We believe that an engaged workforce is key to maintaining our ability to innovate. We invest in our employees’ career growth and development is an important focus for us. We are committed to providing a safe work environment for our employees in compliance with applicable regulations. We have taken necessary precautions in response to the recent COVID-19 outbreak, including offering employees flexibility to work from home and mandatory social distancing requirements in the workplace.

As of December 31, 2021, we had a total of 524 full-time employees working in the PRC, including 216 employees working in hospitals, of which 62 are engaged in information technology, 16 employees working in retail pharmacies and 50 employees are engaged in distribution of medical devices and pharmaceuticals. As of December 31, 2021 the number of employees employed in the retail pharmacy, wholesale medical devices wholesale pharmaceuticals. medical service and other were 30, 49, 72, 360 and 13, respectively. We believe we have a good relationship with our employees.

13

ITEM 1A. RISK FACTORS

Investing in our shares of Common Stock involves a high degree of risk and uncertainty. You should carefully consider the risks and uncertainties described below before investing. Our business, prospects, financial condition and results of operations could be adversely affected due to any of the following risks. In that case, the value of our ordinary shares could decline, and you could lose all or part of your investment. These risk factors include, but are not limited to:

| ● | There are doubts about our company’s ability to continue as a going concern. |

| ● | We have had a history of losses and our ability to grow sales and achieve profitability are unpredictable. |

| ● | We have a substantial amount of existing debt, which may restrict our financing and operating flexibility and have other adverse consequences; defaults could have a material adverse effect on our business, financial condition, results of operations and cash flows. |

| ● | We failed to realize any financial benefits from our recent acquisition and may be unable to realize any benefits from any other future transactions. |

| ● | The impairment of intangible assets and goodwill arising from our acquisitions could continue to negatively impact affect our net income and shareholders’ equity. |

| ● | Raising additional capital will be difficult and may cause dilution to our shareholders and restrict our operations. |

| ● | The recent COVID-19 pandemic had a material adverse effect on our business operations, results of operations, cash flows and financial position during 2021. |

| ● | The markets in which we now operate are very competitive and further increases in competition could adversely affect us. |

| ● | Breaches of network or information technology security could have an adverse effect on our business. |

| ● | If we fail to implement effective internal controls required by the Sarbanes-Oxley Act of 2002, or remedy any material weaknesses in our internal controls that we may identify, such failure could result in material misstatements in our financial statements, cause investors to lose confidence in our reported financial information and have a negative effect on the trading price of our Common Stock. |

| ● | Violations of anti-bribery, anti-corruption and/or international trade laws to which we are subject could have a material adverse effect on our business operations, financial position, and results of operations. |

| ● | Increasing scrutiny and changing expectations from investors, lenders, customers and other market participants with respect to our Environmental, Social and Governance, or ESG, policies may impose additional costs on us or expose us to additional risks. |

| ● | We may be subject to fines and penalties if we fail to comply with the applicable PRC laws and regulations governing sales of medicines under China’s National Medical Insurance Program. |

| ● | Certain risks are inherent in providing pharmacy services; our insurance may not be adequate to cover any claims against us. |

| ● | Our newly acquired hospitals derive a significant portion of revenue by providing healthcare services to patients with public medical insurance coverage; any delayed payment under China’s public medical insurance programs could affect our results of operations. |

| ● | Our hospitals could become the subject of patient complaints, claims and legal proceedings in the course of their operations, which could result in costs and materially and adversely affect our brand image, reputation and results of operations. | |

| ● | If we fail to properly manage the employment of the physicians and other medical professionals of our hospitals, we may be subject to penalties against these hospitals, which could materially and adversely affect our business and results of operations. | |

| ● | We have limited or no control over the quality of pharmaceuticals, medical consumables and other medical equipment used in the operations of our hospitals. If such quality does not meet the required standards, we could be exposed to liabilities and our reputation, business, results of operations, financial condition and prospects could be adversely affected. | |

| ● | As a provider of medical services, we are exposed to inherent risks relating to malpractice claims. |

14

| ● | Our retail, wholesale operations and newly acquired hospitals require a number of permits and licenses in order to carry on their business. |

| ● | If we do not maintain the privacy and security of sensitive customer and business information, we could damage our reputation, incur substantial additional costs and become subject to litigation. |

| ● | The impact of China’s regulatory reforms is unpredictable. |

| ● | We may be unable to attract, hire, and retain a highly qualified workforce, including key management. |

| ● | We substantially depend on a few key personnel who, if not retained, could cause declines in productivity and operational results and loss of our strategic guidance, all of which would diminish our business prospects and value to investors. |

| ● | We are responsible for the indemnification of our officers and directors. |

| ● | Adverse changes in economic and political policies of the PRC government could have a material adverse effect on the overall economic growth of China, which could adversely affect our business. |

| ● | Substantial uncertainties exist with respect to the interpretation and implementation of new PRC laws, rules and regulations relating to foreign investment and how they may impact the viability of our current corporate structure, corporate governance and business operations. |

| ● | Our shares may be delisted under the Holding Foreign Companies Accountable Act (“HFCCA”) if the PCAOB is unable to inspect our auditors for three consecutive years beginning in 2021. If the bill passed by the U.S. Senate on June 22, 2021 is passed by the U.S. House of Representatives and signed into law, this would reduce the number of consecutive non-inspection years required for triggering the prohibitions under the HFCAA from three years to two. The delisting of our shares, or the threat of their being delisted, may materially and adversely affect the value of your investment. |

| ● | We have limited business insurance coverage in China. |

| ● | Because our funds are held in banks in the PRC that do not provide insurance, the failure of any bank in which we deposit our funds could affect our ability to continue in business. |

| ● | We may suffer currency exchange losses if the RMB depreciates relative to the US Dollar. |

| ● | The Chinese government has strengthened the regulation of investments made by Chinese residents in offshore companies and reinvestments in China made by these offshore companies. Our business may be adversely affected by these restrictions. |

| ● | The PRC legal system embodies uncertainties which could limit the legal protections available to us and you, or could lead to penalties on us. | |

| ● | It may be difficult to enforce any civil judgments against us or our board of directors or officers, because all of our operating and/or fixed assets are located outside of the United States. | |

| ● | Because our assets are located overseas, shareholders may not receive distributions that they would otherwise be entitled to if we were declared bankrupt or insolvent. | |

| ● | A recurrence of Severe Acute Respiratory Syndrome (SARS), Avian Flu, or another widespread public health problem, such as the spread of H1N1 (“Swine”) Flu, or COVID-19 in the PRC could adversely affect our operations. | |

| ● | The PRC may establish complex procedures for some acquisitions of Chinese companies by foreign investors, which could make it more difficult for us to pursue growth through acquisitions in China. | |

| ● | We will need to raise additional capital that will likely cause dilution to our shareholders. | |

| ● | The trading volume of our Common Stock has fluctuated from time to time, which may make it difficult for investors to sell their shares at times and prices that investors feel are appropriate. | |

| ● | The Nasdaq Capital Market imposes listing standards on our Common Stock that we may not be able to fulfill, thereby leading to a possible delisting of our Common Stock. |

15

Risks Related to Our Business

There are doubts about our company’s ability to continue as a going concern.

Our company’s independent auditors have raised doubts about our ability to continue as a going concern. There can be no assurance that sufficient funds required during the next year or thereafter will be generated from operations or that funds will be available from external sources, such as securities, debt or equity financing or other potential sources. We intend to overcome the circumstances that impact our ability to remain a going concern through a combination of new sources of revenues, with interim cash flow deficiencies being addressed through additional financing. We anticipate raising additional funds through public or private financing, securities financing and/or strategic relationships or other arrangements in the near future to support our business operations; however, we may not have commitments from third parties for a sufficient amount of additional capital. We cannot be certain that any such financing will be available to us on acceptable terms, or at all, and our failure to raise capital when needed could limit our ability to continue our operations. Our ability to obtain additional funding will determine if we can continue as a going concern. Failure to secure additional financing in a timely manner and on favorable terms would have a material adverse effect on our financial performance, results of operations and share price and require us to curtail or cease operations, sell off assets, seek protection from creditors through bankruptcy proceedings, or otherwise. Furthermore, additional equity financing may be dilutive to the holders of our shares, and debt financing, if available, may have onerous terms. including restrictive covenants. Any additional financing could have a negative effect on our shareholders.

We have had a history of losses and our ability to grow sales and achieve profitability are unpredictable.

As of December 31, 2021, we had an accumulated deficit of $47.90 million and incurred net losses of $34,921,745 and $1,877,925, in the years ended December 31, 2021 and 2020, respectively. Our ability to maintain and improve future levels of sales and profitability depends on many factors, which include:

| ● | successfully implementing our business strategy; | |

| ● | increasing revenues; and | |

| ● | controlling costs. |

There can be no assurance that we will be able to successfully implement our business plan, meet our challenges and become profitable in the future.

16

We have a substantial amount of existing debt, which may restrict our financing and operating flexibility and have other adverse consequences; defaults could have a material adverse effect on our business, financial condition, results of operations and cash flows.

In order to fund our operations and recent acquisitions we have incurred a substantial amount of indebtedness. Our significant level of debt could have important consequences, including, but not limited to, the following:

| ● | making it more difficult for us to service our debt obligations and liabilities; | |

| ● | making us vulnerable to, and reducing our flexibility to respond to, general adverse economic and industry conditions; | |

| ● | requiring that a substantial portion of our cash flows from operations be dedicated to servicing debt, thereby reducing the funds available to us to fund working capital, or other general corporate purposes; | |

| ● | impeding our ability to obtain additional debt or equity financing and increasing the cost of any such borrowing, particularly due to the financial and other restrictive covenants contained in the agreements governing our debt; and | |

| ● | adversely affecting public perception of us. |

Although we believe we will be able to continue to service and repay our debt, there is no assurance that we will be able to do so. If our plans for future operations do not generate sufficient cash flows and earnings, our ability to make required payments on our debt would be impaired. If we fail to pay our indebtedness when due, it could have a material adverse effect on us and may require us to curtail or cease operations, sell off assets, seek protection from creditors through bankruptcy proceedings, or otherwise.

We failed to realize any financial benefits from our recent acquisition and may be unable to realize any benefits from any other future transactions.

Mergers and acquisitions of companies are inherently risky and subject to many factors outside of our control and no assurance can be given that acquisition of companies in the future will be successful and will not adversely affect our business, operating results, or financial condition. In 2021 we recorded impairment losses totaling approximately $26.13 million with respect to the goodwill relating to our acquisitions of the Guanzan Group, Guoyitang, Zhongshan, Minkang, Qiangsheng, Eurasia and Zhuoda.

If we acquire other businesses, we may face difficulties, including:

| ● | Difficulties in integrating the operations, systems, technologies, products, and personnel of the acquired businesses or enterprises; | |

| ● | Diversion of management’s attention from normal daily operations of the business and the challenges of managing larger and more widespread operations resulting from acquisitions; | |

| ● | Integrating financial forecasting and controls, procedures and reporting cycles; | |

| ● | Difficulties in entering markets in which we have no or limited direct prior experience and where competitors in such markets have stronger market positions; | |

| ● | The uncertainties in the operations of the target acquisitions caused by the COVID-19 that may prevent such companies from achieving their performance projections. | |

| ● | Insufficient revenue to offset increased expenses associated with acquisitions; and | |

| ● | The potential loss of key employees, customers, distributors, vendors and other business partners of the companies we acquire following and continuing after announcement of acquisition plans. |

17

The impairment of intangible assets and goodwill arising from our acquisitions could continue to negatively impact affect our net income and shareholders’ equity

When we acquire a business, a substantial portion of the purchase price of the acquisition may be allocated to goodwill and other identifiable intangible assets. The amount of the purchase price which is allocated to goodwill and other intangible assets is determined by the excess of the purchase price over the net identifiable assets acquired. The current accounting standards require that goodwill and intangible assets should be deemed to have indefinite lives, which should be tested for impairment at least annually (or more frequently if impairment indicators arise). Other intangible assets are amortized over their useful lives. For the year ended December 31, 2021, we recorded impairment losses on goodwill of $26.13 million.

Future declines in the results of our acquisitions and other factors could cause us to record an impairment of all or a portion of the relevant goodwill in the future. We may not be able to achieve our business targets for businesses we previously acquired or will acquire in the future, which could result in our incurring additional goodwill and other intangible assets impairment charges. Further declines in our market capitalization increase the risk that we may be required to perform another goodwill impairment analysis, which could result in an impairment of up to the entire balance of our goodwill based on the quantitative assessment performed.

Raising additional capital will be difficult and may cause dilution to our shareholders and restrict our operations.