UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

For the transition period from ________ to _________

Commission

file number

(Exact name of registrant as specified in charter)

| (State

or jurisdiction of Incorporation or organization) |

I.R.S

Employer Identification No. |

| (Address of principal executive offices) | (Zip code) |

+

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||

| The

|

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate

by check mark whether the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller Reporting Company | ||

| Emerging Growth Company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act) Yes ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

The

aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2022, the last

business day of the registrant’s most recently completed second fiscal quarter, was approximately $

Number of shares of common stock outstanding as of March 31, 2023 was .

Documents

Incorporated by Reference:

Table of Contents

| i |

PART I

In this Annual Report on Form 10-K, unless the context requires otherwise, the terms “we,” “our,” “us,” or “the Company” refer to MySize, Inc., a Delaware corporation, and its subsidiaries, including MySize Israel 2014 Ltd. My Size LLC, Orgad International Marketing Ltd., or Orgad, and Naiz Bespoke Technologies, S.L, or Naiz, taken as a whole.

References to “U.S. dollars” and “$” are to currency of the United States of America, and references to “NIS” are to New Israeli Shekels. Unless otherwise indicated, U.S. dollar translations of NIS amounts presented in this Annual Report on Form 10-K for the year ended on December 31, 2022 are translated using the rate of NIS 3.358 to $1.00.

All information in this Annual Report on Form 10-K relating to shares or price per share reflects the 1-for-25 reverse stock split effected by us on December 8, 2022.

CAUTIONARY NOTE ON FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. Any statements in Annual Report on Form 10-K about our expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as “believe,” “will,” “expect,” “anticipate,” “estimate,” “intend,” “plan” and “would.” For example, statements concerning financial condition, possible or assumed future results of operations, growth opportunities, industry ranking, plans and objectives of management, markets for our common stock and future management and organizational structure are all forward-looking statements. Forward-looking statements are not guarantees of performance. They involve known and unknown risks, uncertainties and assumptions that may cause actual results, levels of activity, performance or achievements to differ materially from any results, levels of activity, performance or achievements expressed or implied by any forward-looking statement.

Any forward-looking statements are qualified in their entirety by reference to the risk factors discussed throughout this Annual Report on Form 10-K. Some of the risks, uncertainties and assumptions that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include but are not limited to:

| ● | our history of losses and needs for additional capital to fund our operations and our inability to obtain additional capital on acceptable terms, or at all; | |

| ● | risks related to our ability to continue as a going concern; | |

| ● | the new and unproven nature of the measurement technology markets; | |

| ● | our ability to achieve customer adoption of our products; | |

| ● | our ability to realize the benefits of our acquisitions of Orgad and Naiz; | |

| ● | our dependence on assets we purchased from a related party; | |

| ● | our ability to enhance our brand and increase market awareness; | |

| ● | our ability to introduce new products and continually enhance our product offerings; | |

| ● | the success of our strategic relationships with third parties; | |

| ● | information technology system failures or breaches of our network security; | |

| ● | competition from competitors; | |

| ● | our reliance on key members of our management team; | |

| ● |

current or future litigation; | |

| ● | current or future unfavorable economic and market conditions and adverse developments with respect to financial institutions and associated liquidity risk; and | |

| ● | the impact of the political and security situation in Israel on our business. |

| 1 |

The foregoing list sets forth some, but not all, of the factors that could affect our ability to achieve results described in any forward-looking statements. You should read this Annual Report on Form 10-K and the documents that we reference herein and have filed as exhibits to the Annual Report on Form 10-K, completely and with the understanding that our actual future results may be materially different from what we expect. You should assume that the information appearing in this Annual Report on Form 10-K is accurate as of the date hereof. Because the risk factors referred to in this Annual Report on Form 10-K, could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by us or on our behalf, you should not place undue reliance on any forward-looking statements.

Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of the information presented in this Annual Report on Form 10-K, and particularly our forward-looking statements, by these cautionary statements.

ITEM 1. BUSINESS

Overview

We are an omnichannel e-commerce platform and provider of AI-driven apparel sizing and digital experience solutions that drive revenue growth and reduce costs for our business clients for online shopping and physical stores.

Our flagship innovative tech products, MySizeID, enables shoppers to generate highly accurate measurements of their body to find the accurate fitting apparel by using our application on their mobile phone or through MySizeID Widget: a simple questionnaire which uses a database collected over the years.

MySizeID syncs the user’s measurement data to a sizing chart integrated through a retailer’s (or a white labeled) mobile application, and only presents items for purchase that match their measurements to ensure a correct fit.

We are positioning ourselves as a consolidator of sizing solutions and new digital experience due to new developments for the fashion industry needs. Our other product offerings include First Look Smart Mirror for physical stores and Smart Catalog to empower brand design teams, which are designed to increase end consumer satisfaction, contributing to a sustainable world and reduce operation costs.

Recent Developments

Orgad Acquisition

On February 7, 2022, My Size Israel 2014 Ltd, or My Size Israel, entered into a Share Purchase Agreement, or the Orgad Agreement, with Amar Guy Shalom and Elad Bretfeld, or the Orgad Sellers, pursuant to which the Orgad Sellers agreed to sell to My Size Israel all of the issued and outstanding equity of Orgad.

Orgad operates an omnichannel e-commerce platform engaged in online retailing in the global market. It operates as a third-party seller on Amazon.com, eBay and others. Orgad currently manages more than 1,000 stock-keeping units, or SKUs, mainly in fashion, apparel and shoes.

The Orgad Sellers are the sole title and beneficial owners of 100% of the shares of Orgad. In consideration of the shares of Orgad, the Orgad Sellers are entitled to receive (i) up to $1,000,000 in cash, or the Orgad Cash Consideration, (ii) an aggregate of 111,602 shares, or the Orgad Equity Consideration, of our common stock, and (iii) earn-out payments of 10% of the operating profit of Orgad for the years 2022 and 2023. The transaction closed on the same day.

The Orgad Cash Consideration is payable to the Orgad Sellers in three installments, according to the following payment schedule: (i) $300,000 which we paid upon closing, (ii) $350,000 payable on the two-year anniversary of the closing, and (iii) $350,000 payable on the three-year anniversary of the closing, provided that in the case of the second and third installments certain revenue targets are met and subject further to certain downward post-closing adjustment.

| 2 |

The Equity Consideration is payable to the Orgad Sellers according to the following payment schedule: (i) 55,801 shares were issued at closing, and (ii) 55,801 shares will be issued in eight equal quarterly installments until the lapse of two years from closing, subject to certain downward post-closing adjustment.

The payment of the second and third cash installments, the equity installments and the earn out are further subject in each case to the Orgad Sellers being actively engaged with Orgad at the date such payment is due (except if the Orgad Sellers resign due to reasons relating to material reduction of salary or adverse change in their position with Orgad or its affiliates).

In connection with the Orgad Agreement, each of the Orgad Sellers entered into employment agreements with Orgad and six-month lock-up agreements with us.

Naiz Acquisition

On October 7, 2022, we entered into a Share Purchase Agreement, or the Naiz Agreement, with Borja Cembrero Saralegui, or Borja, Aritz Torre Garcia, or Aritz, Whitehole, S.L., or Whitehole, Twinbel, S.L., or Twinbel and EGI Acceleration, S.L., or EGI. Each of Borja, Aritz, Whitehole, Twinbel and EGI shall be referred to as the Naiz Sellers herein. Pursuant to the Naiz Agreement, the Naiz Sellers agreed to sell to My Size all of the issued and outstanding equity of Naiz, a limited liability company incorporated under the laws of Spain. The acquisition of Naiz was completed on October 11, 2022.

In consideration of the purchase of the shares of Naiz, the Naiz Agreement provided that the Naiz Sellers are entitled to receive (i) an aggregate of 240,000 shares, or the Naiz Equity Consideration, of My Size common stock, or the Shares, representing in the aggregate, immediately prior to the issuance of such shares at the closing of the transaction, not more than 19.9% of the issued and outstanding Shares and (ii) up to $2,050,000 in cash, the Naiz Cash Consideration.

The Naiz Equity Consideration was issued to the Naiz Sellers at closing of the transaction of which 94,632 shares of My Size common stock were issued to Whitehole constituting 6.6% of our outstanding shares following such issuance. The Naiz Agreement also provides that, in the event that the actual value of the Naiz Equity Consideration (based on the average closing price of the Shares on the Nasdaq Capital Market over the 10 trading days prior to the closing of the transaction, or the Equity Value Averaging Period) is less than $1,650,000, My Size shall make an additional cash payment, or the Shortfall Value to the Naiz Sellers within 45 days of our receipt of Naiz’s 2025 audited financial statements; provided that certain revenue targets are met. Following the Equity Value Averaging Period, it was determined that the Shortfall Value is $459,240.

The Naiz Cash Consideration is payable to the Naiz Sellers in five installments, according to the following payment schedule: (i) US$500,000 at closing, (ii) up to US$500,000 within 45 days of My Size’s receipt of Naiz’s 2022 audited financial statements, (iii) up to US$350,000 within 45 days of My Size’s receipt of Naiz’s unaudited financial statements for the six months ended June 30, 2023, (iv) up to $350,000 within 45 days of My Size’s receipt of Naiz’s unaudited financial statements for the six months ended December 31, 2023, and (v) up to $350,000 within 45 days of My Size’s receipt of Naiz’s 2024 audited financial statements; provided that in the case of the second, third, fourth and fifth installments certain revenue targets are met.

The payment of the second, third, fourth and fifth cash installments are further subject to the continuing employment or involvement of Borja and Aritz, or the Key Persons, by or with Naiz at the date such payment is due (except if a Key Person is terminated from Naiz due to a Good Reason (as defined in the Naiz Agreement).

The Naiz Agreement contains customary representations, warranties and indemnification provisions. In addition, the Naiz Sellers are subject to non-competition and non-solicitation provisions pursuant to which they agree not to engage in competitive activities with respect to My Size’s business.

In connection with the Naiz Agreement, (i) each of the Naiz Sellers entered into six-months lock-up agreements, or the Lock-Up Agreement, with My Size, (ii) Whitehole, Twinbel and EGI entered into a voting agreement, or the Voting Agreement, with My Size and (iii) each of the Key Persons entered into employment agreements and services agreements with Naiz.

| 3 |

The Lock-Up Agreement provides that each Naiz Seller will not, for the six-months period following the closing of the transaction, (i) offer, pledge, sell, contract to sell, sell any option, warrant or contract to purchase, purchase any option, warrant or contract to sell, grant any option, right or warrant to purchase, or otherwise transfer or dispose of, directly or indirectly, any Shares or any securities convertible into or exercisable or exchangeable for Shares in each case, that are currently or hereafter owned of record or beneficially (including holding as a custodian) by such Naiz Seller, or publicly disclose the intention to make any such offer, sale, pledge, grant, transfer or disposition; or (ii) enter into any swap, short sale, hedge or other agreement that transfers, in whole or in part, any of the economic consequences of ownership of such Naiz Seller’s Shares regardless of whether any such transaction described in clause (i) or this clause (ii) is to be settled by delivery of Shares or such other securities, in cash or otherwise. The Lock-Up Agreement also contains an additional three-months “dribble-out” provision that provides following the expiration of the initial six-months lock-up period, without My Size’s prior written consent (which My Size shall be permitted to withhold at its sole discretion), each Naiz Seller shall not sell, dispose of or otherwise transfer on any given day a number of Shares representing more than the average daily trading volume of the Shares for the rolling 30 day trading period prior to the date on which such Seller executes a trade of the Shares.

The Voting Agreement provides that the voting of any Shares held by each of Whitehole, Twinbel and EGI, or the Naiz Acquisition Stockholders, will be exercised exclusively by a proxy designated by My Size’s board of directors from time to time, or the Proxy, and that each Naiz Acquisition Stockholder will irrevocably designate and appoint the then-current Proxy as its sole and exclusive attorney-in-fact and proxy to vote and exercise all voting right with respect to the Shares held by each Naiz Acquisition Stockholder. The Voting Agreement also provides that, if the voting power held by the Proxy, taking into account the proxies granted by the Naiz Acquisition Stockholders and the Shares owned by the Proxy, represents 20% or more of the voting power of My Size’s stockholders that will vote on an item, or the Voting Power, then the Proxy shall vote such number of Shares in excess of 19.9% of the Voting Power in the same proportion as the Shares that are voted by My Size’s other stockholders. The Voting Agreement will terminate on the earliest to occur of (i) such time that such Naiz Acquisition Stockholder no longer owns the Shares, (ii) the sale of all or substantially all of the assets of My Size or the consolidation or merger of My Size with or into any other business entity pursuant to which stockholders of My Size prior to such consolidation or merger hold less than 50% of the voting equity of the surviving or resulting entity, (iii) the liquidation, dissolution or winding up of the business operations of My Size, and (iv) the filing or consent to filing of any bankruptcy, insolvency or reorganization case or proceeding involving My Size or otherwise seeking any relief under any laws relating to relief from debts or protection of debtors.

Warehouse Fire

On January 2, 2023, Orgad experienced a fire at its warehouse in Israel. we are not aware of any casualties or injuries associated with the fire. We shifted Orgad’s operation to its headquarters. The value of the inventory that was in the warehouse was approximately $450,000. We believe that this incident did not affect the future sales results of Orgad for the year of 2023. The inventory was not insured and it is too early to determine the potential impact of this incident on the other parties that were involved in the incident (lessor and others that leased properties near the warehouse).

January 2023 Financing

On January 10, 2023, we entered into a securities purchase agreement, or the RD Purchase Agreement, pursuant to which we agreed to sell and issue in the RD Offering an aggregate of 162,000 of our shares of common stock, or the RD Shares, and pre-funded warrants, or the Pre-funded Warrants, to purchase up to 279,899 shares of common stock and, in a concurrent private placement, unregistered warrants to purchase up to 883,798 shares of common stock, or the RD Warrants, consisting of Series A warrants, or Series A Warrants, to purchase up to 441,899 shares of common stock and Series B warrants, or Series B Warrants, to purchase up to 441,899 shares of common stock, at an offering price of $3.055 per RD Share and associated Series A and Series B Warrants and an offering price of $3.054 per Pre-funded Warrant and associated Series A and Series B Warrants.

| 4 |

In addition, we entered into a securities purchase agreement, or the PIPE Purchase Agreement, and together with the RD Purchase Agreement, the Purchase Agreements, pursuant to which we agreed to sell and issue in the PIPE Offering an aggregate of up to 540,098 unregistered Pre-funded Warrants and unregistered warrants to purchase up to an aggregate of 1,080,196 shares of common stock, or the PIPE Warrants and together with the RD Warrants, the Warrants, consisting of Series A Warrants to purchase up to 540,098 shares of common stock and Series B Warrants to purchase up to 540,098 shares of common stock at an offering price of $3.054 per Pre-funded Warrant and associated Series A and Series B Warrants.

The Pre-funded Warrants are immediately exercisable at an exercise price of $0.001 per share and will not expire until exercised in full. The Warrants are immediately exercisable upon issuance at an exercise price of $2.805 per share, subject to adjustment as set forth therein. The Series A Warrants have a term of five and one-half years from the date of issuance and the Series B Warrants have a term of 28 months from the date of issuance. The Warrants may be exercised on a cashless basis if there is no effective registration statement registering the shares underlying the warrants.

In connection with the PIPE Purchase Agreement, we entered into a registration rights agreement, or the Registration Rights Agreement. Pursuant to the Registration Rights Agreement, we are required to file a resale registration statement, or the Registration Statement, with the Securities and Exchange Commission, or the SEC, to register for resale the shares issuable upon exercise of the unregistered Pre-funded Warrants and the Series A and Series B Warrants, within 20 days of the signing date of the PIPE Purchase Agreement, or the Signing Date, and to have such Registration Statement declared effective within 60 days after the Signing Date in the event the Registration Statement is not reviewed by the SEC, or 90 days of the Signing Date in the event the Registration Statement is reviewed by the SEC. we will be obligated to pay certain liquidated damages if we fail to maintain the effectiveness of the Registration Statement.

The Purchase Agreements and the Registration Rights Agreements also contain representations, warranties, indemnification and other provisions customary for transactions of this nature. In addition, subject to limited exceptions, the Purchase Agreements provide that for a period of one year following the closing of the Offerings, we will not effect or enter into an agreement to effect a “variable rate transaction” as defined in the Purchase Agreements.

Aggregate gross proceeds to the Company in respect of the Offerings was approximately $3.0 million, before deducting fees payable to the placement agent and other offering expenses payable by the Company.

We also entered into a letter agreement, or the Engagement Agreement, with H.C. Wainwright & Co., LLC, or Wainwright, pursuant to which Wainwright agreed to serve as the exclusive placement agent for the Company in connection with the Offerings. We paid Wainwright a cash placement fee equal to 7% of the aggregate gross proceeds raised in the Offerings, a management fee of 1% of the aggregate gross proceeds raised in the Offerings, a non-accountable expense allowance of $85,000 and clearing fees of $15,950. Wainwright also received placement agent warrants, or the Placement Agent Warrants, with substantially the same terms as the Series A Warrants issued in the Offering in an amount equal to 7% of the aggregate number of Shares and Pre-funded Warrants sold in the Offerings, or 68,740 shares, at an exercise price of $3.8188 per share and a term expiring on January 10, 2028.

Our Solution

Our cloud-based software platform provides highly accurate sizing and measurement with broad applications including the online fashion/apparel industry, logistics and courier services and home DIY. Currently, we are mainly focusing on the e-commerce fashion/apparel industry. This proprietary technology is driven by several patented algorithms which are able to calculate and record measurements in a variety of novel ways. Although specific functionality varies by product, we believe that our core solutions address the need for highly accurate measurements in a variety of consumer friendly, every day uses.

| 5 |

We have developed three products, MySizeID for the fashion/apparel industry, BoxSize for the logistics and courier services market and SizeUp for the home DIY market.

| ● | MySizeID enables shoppers to generate highly accurate measurements of their body to find proper fitting clothes and accessories, through the use of our application on their mobile phone or through a simple questionnaire if the user decides not to download the application. MySizeID syncs the user’s measurement data to a sizing chart and presents items for purchase that match their measurements to ensure a correct fit. MySizeID is available for license by retailers and accessable by consumers through a web page. | |

| ● | BoxSize enables customers to quickly and easily measure the size and volume of a parcel to accurately calculate shipping fees. It also offers shipping companies a variety of precise logistical data for more efficiently managing their supply chain, providing them with an accurate way to compare the physical package with what is in the shipping manifest. BoxSize solution is available for license on both iOS and Android operating systems. BoxSize is available on the Honeywell Marketplace and in August 2019 was approved for Honeywell’s Independent Software Vendor Program, and MySize was granted an independent software vendor (ISV) status on the Zebra Technologies and on DataLogic platforms. | |

| ● | SizeUp is a digital tape measure that allows users to measure length, width and height of a surface by moving their smartphone from point to point of an object or space. SizeUp is a value-add for DIY and home improvement retailers whose customers struggle to find the appropriately sized items (like blinds or curtains) for their homes or projects due to inaccurate measurements. SizeUp also is designed to replace rulers, tape measures and other measuring tools used for DIY projects. SizeUp is available for consumer download on both iOS and Android operating systems. |

The following are some select key features of our solutions:

| ● | Integration Capability. We design our solutions to be flexible and configurable, allowing our clients to match their use of our algorithms and software with their specific business processes and workflows. Our platform has been organically developed from a common code base, data structure and user interface, providing a consistent user experience with powerful features that are easily adaptable to our clients’ needs. The MySizeID widget can be integrated via one-line JavaScript code, or through RESTful API; | |

| ● | Intuitive user experience. Our intuitive, easy-to-use interface is based on current technology, multiple focus groups and automatically adapts to users’ devices, including mobile platforms, thereby significantly increasing accessibility of our solutions; | |

| ● | Big Data Generation. While we supply to the user the information he/she requires, we gather certain vital information such as body measurement and package volume which can be used anonymously to help the retailer acquire predictive size information on stocking, operations and consumers that may be in between sizes. All the information is being gathered and stored on our servers where it can be used by retailers; | |

| ● | Non-Invasive. In taking measurements using our solution, the smartphone camera is not utilized; instead, the measurements are captured by scanning the smartphone over the consumer’s body or package, thus ensuring greater privacy. |

Our Growth Strategy

We aim to drive revenue primarily through penetration of the U.S. and Europe markets through a business to business to consumer (B2B2C) model in the verticals we are targeting. We are pursuing the following growth strategies:

| ● | Sign Additional Commercial Agreements with U.S. Retailers. During 2022, we expanded our commercial agreements with Levi’s, introducing North America (U.S. and Canada) and Latin America regions, and by extension Levis’ native apps in EU and U.S. regions. We also entered into commercial agreements with Baby Fresh, Galax, Punto Blanco, GEF France, Diesel, Gaala, Superdry, Uniontex Industries, and Temperlay London among others. We are in various stages of discussions with U.S. and foreign retailers for the deployment of our size recommendation and measurement technology with a view to entering into additional commercial agreements. |

| 6 |

| ● | Pursue a Two-Pronged Commercialization Strategy. We are seeking to accelerate adoption of our solutions both through direct partnerships with e-commerce websites as well as through third-party platform websites. While we seek to directly enter into partnerships with companies maintaining e-commerce websites in the apparel, courier and DIY markets, we are also seeking to deploy our solutions on third-party platforms. Furthermore, with the expansion of MySizeID through the release of our FirstLook Smart Mirror, which we are offering to brick and mortar stores to digitize the physical stores, MySizeID is now available for online retailers utilizing the WooCoomerce, Shopify, Lightspeed, PrestaShop, Bitrix and Wix platforms and to brick and mortar stores through GK Software POS solution while BoxSize is available on the Honeywell, Zebra Technologies and Datalogic. | |

| ● | Ongoing Investment in our Technology Platform. We continue to invest in building new software capabilities and extending our platform to bring the power of accurate measurement to a broader range of applications. In particular, we seek not only to deliver size recommendations but to provide a robust, end-to-end,artificial intelligence, or AI-driven platform that inspires consumer confidence and drives revenue growth by providing a superior consumer journey to both online and the brick and mortar stores. |

| ● | Grow our database. As the usage of our measurement apps increases, our database of information including user behaviour and body measurements generates valuable statistics. Such data can be used in the big data market for targeted advertising and for blind consumer data mining. | |

| ● | Identify and acquire synergistic businesses. In order to reduce our time to market and obtain complementary technologies, we are seeking to acquire technologies and businesses that are synergistic to our product offering. We recently completed an acquisition of Orgad which operates an omnichannel e-commerce platform and Naiz which provides SaaS technology solutions that solve size and fit issues for fashion ecommerce companies. | |

| ● | Partnerships and cooperation. In order to bring a wider solution for the retail market we are working to partner and integrate our technology with partners that can increase our penetration and offering to the market. |

Market Opportunity

The global e-commerce market was $5.7 trillion in 2022, and the industry is expected to grow significantly in the coming years with no signs of slowing down. Market specialists expect a compound annual growth rate of 27.43% from 2023 to 2028: according to data from Statista, the market is expected to reach $6.5 trillion in 2023. While many sectors have found ways to increase revenue through e-commerce, e-commerce is still plagued by issues that cut into profits and negatively impact the bottom line, such as customer returns, low consumer conversion, and associated restocking and shipping costs.

Fashion/Apparel

Since the onset of the COVID-19 pandemic, an immense shift to digital was recorded, with 85.9% growth vs. pre-pandemic, according to Mastercard, and over 2 billion people worldwide who shop online, according to data from Oberlo. In November 2022, online shoppers broke records with $11.3 billion in spending on Cyber Monday, driving 5.8% year-over-year growth and making the day the biggest online shopping day of all time, according to Adobe Analytics.

In 2021, fashion companies invested between 1.6% and 1.8% of their revenues in technology, according to Mckinsey, and are expected to double the investment by 2030 in order to keep up with digital natives and keep a competitive edge. Personalization in e-commerce and hybrid connectivity in brick-and-mortar retail are two key themes in the future of fashtech, according to Mckinsey’s 2022 State of Fashion Technology.

| 7 |

In the upcoming years, inflation is expected to impact the fashion world. As prices for goods increase, the challenge will be to inspire confidence in consumers, via different smart digital tools. Brands will need to embrace creative digital tools and new channels to deepen customer relationships, and as Mckinsey forecasts in their State of Fashion report for 2023, they will need to execute on priorities such as sustainability and digital acceleration.

The global fashion e-commerce market size is expected to grow from $744.4 billion in 2022 to $821.19 billion in 2023 at a compound annual growth rate of 10.3%. In 2027, the market size is expected to grow to $1,222.32 billion, at a compound annual growth rate of 10.5%, according to BRC.

Based on the importance which shoppers attribute to free shipping - 50% of cart abandonment rate is due to extra shipping costs (Baymard Institute) - the need for fashion retailers to substantiate the optimal size for a customer, thus minimizing returns, has never been more crucial.

As brands move online or significantly expand their online presence, we believe that developing innovative ways to connect with shoppers, both online and offline, has become a top priority.

Shipping/Parcel

According to Pitney Bowes, parcel revenue in 13 major countries around the world increased by 17% year over year from $420 billion in 2020 (reflecting 131 billion parcels) to $491 billion in 2021 (reflecting 159 billion parcels). In the shipping/parcel industry, the dimensions of a package are critical. It is not merely the measurement of a package or box – but rather the amount of space that the package or box will take up on a truck, airplane, or ship that will be transporting the package or box. Far too often, retailers use unfit packaging for their items, adding additional costs in materials and shipping fees.

DIY

Similar to issues in the apparel and fashion market, big box, hardware, furniture, and DIY stores are plagued by returns due to incorrect fit and measurements. In an industry where precise measurement for projects is an absolute necessity, e-commerce has not grown as quickly as in other industries which we believe is due to lack of consumer confidence in measurements at home and buying the correct item online.

MySizeID

We have released the MySizeID app for both iOS and Android which assists consumers to take highly accurate measurement of their own body in order to size clothing in the best way possible without the need to try the clothes on before purchasing. MySizeID is designed to simplify the process of purchasing clothes online and significantly reduce the rate of returns of poor-fitting clothing. During 2022, MySizeID delivered over 23.5 million size recommendations.

The application is the result of a research and development effort that combines:

| ● | anthropometric research – analyses of information pertaining to body measurements derived from a survey and the subsequent determination of correlations between body parts; | |

| ● | body measurement algorithm research – an algorithm created by us to measure body parts; and | |

| ● | retailers size chart analyses – adopting a deep understanding of the size charts of retailers and the corresponding “body to garment size.” |

MySizeID allows consumers to create a secure, online profile of their personal measurements, which can then be utilized, with partnered online retailers, to ensure that no matter the manufacturer or size chart, they will get the right fit. MySizeID operates based on the use of existing sensors in smart phones which enable, through a specific purpose application, the measurement of the body of any consumer by moving the smartphone along his or her body. The MySizeID application does not rely on user photographs or any additional hardware; all a user needs to do is scan their body with their smartphone and the application records their measurements. The measurements can then be saved in our database in the cloud, enabling the user to search for clothes in various retailer websites without worrying about size. When a search is made, the retailer will connect to our cloud database, and then provide results based on the user’s measurements and other parameters as he or she may have defined. This data is also saved for use when a customer enters a brick-and-mortar store to help serve the customer more efficiently and to provide a better shopping experience.

| 8 |

Figure 1: Screenshot of MySizeID on smartphone and e-commerce website

As part of the integration process, we offer to the retailer five main components:

| ● | Mobile App. MySizeID comes in the form of a native app or website. Our native app can be used “as is” integrated into the retailer’s e-commerce website. The website users can build a body profile on the app and receive size recommendations for their profile both in the app and on a widget integrated with their website. |

| 9 |

| ● | Widget. When a consumer enters into the retailer’s website and looks for a specific item, he or she can click on the MySizeID widget which will inform the consumer of his or her recommended size, based on his or her actual measurements, as measured using the app and the item he or she is looking at. |

The widget has two features:

AI Wizard mode - allows the user to obtain size from the following parameters: gender, height, weight, belly shape, hip shape and bra size only. The gender, height and weight questions are mandatory, while the body shape questions are optional and can be added to increase accuracy for specific apparel categories.

Guest mode - allows a user that does not wish to sign up to MySizeID as a user to obtain size recommendations as well.

| ● | Analytic Pixel. MySizeID analytic pixel allows retailer to track and analyze the widget usage. By adding the pixel to the retailer’s website, MySizeID BI team can track engagement, order, and return data and provide retailers with tools to understand the advantages and benefits of MySizeID. |

Use your own device - using MySizeID instore solution, shoppers can receive size recommendations for all store items, when shopping in the offline stores. The shoppers can build their body profile using an easy to use 3 to 6 questions form, scan an item barcode and receive a size recommendation for the scanned item based on their body profile and the item’s size chart.

Another feature we added is the “in-between sizing” feature. Our system can detect a user that has body dimensions that place the user in-between the clothes sizes being offered and lets the user know that. A user can then choose between the two sizes according to the user’s fit preference (tight/loose/average).

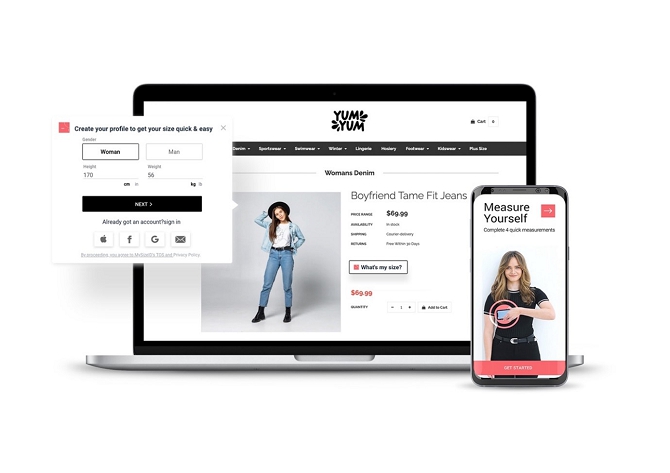

In addition, we have recently released our Instant-App feature which allows shoppers to generate their body measurements directly from our widget, without the need to download our mobile app. Using this technology, the shoppers can create their online profile of their personal measurements and complete a purchase faster and easier with minimum distractions.

The body profile can be created while shoppers are viewing the page from their mobile phone, or by scanning a QR code on desktop that will open the same page on the mobile phone.

Screenshot of Instant-App widget on desktop on yumyumfashion website

| 10 |

| ● | MyDash Platform. The MyDash platform is a smart back-office system where the retailer enters all the information regarding its size charts that correlates to every product in its e-commerce site, and where the retailer can access the information on its users. This system is customizable based on the retailer’s needs. In 2021, we changed the MyDash system to increase the system’s accessibility, added walkthroughs, user guides and changed the user interface and much more for the ease of use. We added the option to use our generic size charts, added the option upload size chart files instead of typing the size charts values manually, added more widget styling options and changed the pairing mechanism between the size chart and the products to be more user-friendly. |

Figure 3: Screenshot of Back-Office System

| ● | FirstLook Smart Mirror. The Smart Mirror provides an interactive, mirror-like touch display that allows brands to provide in-store customers with an enhanced, online shopping experience, contactless checkout and obtains the recommended size. The MySizeID FirstLook Smart Mirror can be placed in numerous locations throughout a retail store, including the fitting rooms (without cameras) or other high-traffic locations of the store. Highlight capabilities of the FirstLook Smart Mirror include a 3D “Try-it-on” interactive avatar experience, personalized and highly accurate size recommendations by MySizeID, third-party point of sale systems integration, styling recommendations and contactless “select and collect” at the register feature. |

Illustration of MySizeID “first look” smart mirror in a fashion store

| 11 |

We are currently offering MySizeID technology to retailers through either a pay-per-use model or a monthly subscription model. In our pay-per-use business model, every time the consumer obtains a recommended size, the retailer is charged for the usage.

BoxSize

BoxSize is a parcel measurement application that can provide real-time logistic data on package volumes and transportation, resulting in improved operational efficiency and reduced operating expenses. In addition, BoxSize allows customers to easily measure the size of their parcel with their smartphone, calculate shipping costs and arrange for a convenient pick-up time for the package. BoxSize is available both on iOS and Android.

In 2020 we released the “One Click” feature on BoxSize that enables the user to measure a package with just one swipe of the handheld device. Previously, measurements through BoxSize would require three separate swipes.

Figure 4: Screenshot of BoxSize

Our BoxSize mobile measurement solution is available on the Honeywell Marketplace. In addition, BoxSize was approved for Honeywell’s Global Vendor Program, and is available to provide highly accurate mobile measurement solutions for thousands of Honeywell clients. We also developed a new dashboard for the courier companies to have all the required data about each package in one place. It includes package dimensions, pictures, scan geo location and more. The dashboard also let the courier use Webhooks, which allows him to get the information from his own system.

| 12 |

In 2020, we announced our partnership with Datalogic, a company focused on the automatic data capture and process automation markets. The partnership makes our BoxSize measurement solution available to thousands of Datalogic customers in the Transportation and Logistics vertical.

Agreement with Delhivery Private Limited, India

We entered into an agreement with Delhivery Private Limited, one of the largest courier pickup, delivery, and online shipping services in India. Delhivery’s reputation as a front-runner in delivery and logistics tech makes its decision to select Boxsize a particularly strong testament to the value the solution provides. BoxSize provides Delhivery’s employees on the B2B side with critical information that will allow them to effortlessly optimize loading efficiency and add even more real-time visibility to operations.

SizeUp

We are working on additional consumer applications, including a DIY application. Our SizeUp application is a smart tape measure for the business to consumer market which allows users to utilize their smartphone as a tape measure. The application provides measurements with an accuracy of within two centimeters. Through the use of SizeUp, users will be able to visualize how an object or a piece of furniture will fit in an existing room in their home or office. It also added Google Vision for image content analysis, object detection, and title suggestions.

Currently the SizeUp app for Android and iOS is available for free for the first 30 days, after which a user will be required to register via e-mail and pay a one-time fee of $1.99 to continue using the application. To date, revenues from downloads have been minimal.

Research and Development

Our research and development team are responsible for the research, algorithm, design, development, and testing of all aspects of our measurement platform technology. We invest in these efforts to continuously improve, innovate, and add new features to our solutions.

We incurred research and development expenses of approximately $1.7 million in 2022 and $4.25 million in 2021, relating to the development of its applications and technologies. The decrease from the corresponding period primarily resulted from share based payment in amount of $2,618,000 attributed to the share issuance to Shoshana Zigdon under the Amendment to Purchase Agreement dated May 26, 2021. We intend to continue to invest in our research and development capabilities to extend our platform and bring our measurement technology to a broader range of applications.

| 13 |

In 2022, the R&D department experienced significant success in their efforts to improve the performance of their size recommendation system. Through a combination of optimized algorithms and the incorporation of cutting-edge technologies, the team was able to achieve a threefold increase in the system’s speed. This breakthrough not only makes the system one of the fastest and most accurate on the market, but also reduced the operation costs, making it more cost-effective for businesses to use. Additionally, the solution is now highly scalable, allowing it to easily adapt to the needs of businesses of any size. The R&D team is now focused on further improving the system and exploring new applications for the technology.

Sales and Marketing

In 2019, we launched a commercialization strategy that directs our sales efforts toward both sales to e-commerce players in specific vertical markets such as fashion/apparel and shipping/delivery as well as to e-commerce third-party platform providers. As of March 15, 2023, our products are being sold in the following countries: US, UK, France, Netherlands, Spain, Portugal Turkey, Germany, Israel and Italy, generating customer leads, building out a sales pipeline, and developing customer relationships.

We believe an effective method to market our suite of products is for users to actively use and explore its capabilities. We encourage free trials of one or more of our products in order to successfully convert those accounts to paid subscriptions.

Proprietary Rights

We rely on a combination of patent, copyright, trademark and trade secret laws in the United States and other jurisdictions, as well as contractual protections, to protect our proprietary technology.

As of December 31, 2022, we owned 18 issued patents: six in Europe, four in the U.S., three in each of Russia and Japan and one in each of Canada and Israel which expire between January 20, 2033 and August 18, 2036, and we have two additional patent applications in process. As of such date, we do not have any registered trademarks.

We cannot provide any assurance that our proprietary rights with respect to our products will be viable or have value in the future since the validity, enforceability and type of protection of proprietary rights in software-related industries are uncertain and still evolving.

Despite our efforts to protect our proprietary rights, unauthorized parties may attempt to copy aspects of our products or to obtain and use information that we regard as proprietary. Policing unauthorized use of our products is difficult, and while we are unable to determine the extent to which piracy of our software products exists, software piracy can be expected to be a persistent problem. In addition, the laws of some foreign countries do not protect proprietary rights to as great an extent as do the laws of the United States, and effective copyright, trademark, trade secret and patent protection may not be available in those jurisdictions. Our means of protecting our proprietary rights may not be adequate to protect us from the infringement or misappropriation of such rights by others.

Further, in recent years, there has been significant litigation in the United States involving patents and other intellectual property rights, particularly in the software and Internet-related industries. We can become subject to intellectual property infringement claims as the number of our competitors grows and our products and services overlap with competitive offerings. These claims, even if not meritorious, could be expensive to defend and could divert management’s attention from operating our business. If we become liable to third parties for infringing their intellectual property rights, we could be required to pay a substantial award of damages and to develop non-infringing technology, obtain a license or cease selling the products that contain the infringing intellectual property. We may be unable to develop non-infringing technology or obtain a license on commercially reasonable terms, if at all.

| 14 |

Government Regulation

We are subject to a number foreign and domestic laws and regulations that involve matters central to our business. These laws and regulations may involve privacy, data protection, intellectual property, or other subjects. Many of the laws and regulations to which we are subject are still evolving and being tested in courts and could be interpreted in ways that could harm our business. In addition, the application and interpretation of these laws and regulations often are uncertain, particularly in the new and rapidly evolving industry in which we operate. Because global laws and regulations have continued to develop and evolve rapidly, it is possible that we, our products, or our platform may not be, or may not have been, compliant with each such applicable law or regulation.

In particular, we are subject to a variety of federal, state and international laws and regulations governing the processing of personal data. Many U.S. states have passed laws requiring notification to data subjects when there is a security breach of personally identifiable data. There are also a number of legislative proposals pending before the U.S. Congress, various state legislative bodies and foreign governments concerning data protection. In addition, data protection laws in Europe and other jurisdictions outside the United States can be more restrictive than those within the United States, and the interpretation and application of these laws are still uncertain and in flux.

For example, the General Data Protection Regulation, or GDPR, which took effect on May 25, 2018, enhances data protection obligations for entities that process personal data about individuals, including obligations to cooperate with European data protection authorities, implement security measures and keep records of personal data processing activities. Noncompliance with the GDPR can trigger fines equal to the greater of €20 million or 4% of global annual revenue. In addition, the California Consumer Privacy Act of 2018, or CCPA, effective as of January 1, 2020, gives California residents expanded rights to access and require deletion of their personal information, opt out of certain personal information sharing, and receive detailed information about how their personal information is used. The CCPA provides for civil penalties for violations, as well as a private right of action for data breaches, that is expected to increase data breach litigation. Further, failure to comply with the Israeli Privacy Protection Law of 1981, and its regulations, as well as the guidelines of the Israeli Privacy Protection Authority, may expose us to administrative fines, civil claims (including class actions) and in certain cases criminal liability. Current pending legislation may result in a change of the current enforcement measures and sanctions. Given the breadth and depth of changes in data protection obligations, meeting the requirements of GDPR and other applicable laws and regulations has required significant time and resources, including a review of our technology and systems currently in use against the requirements of GDPR and other applicable laws and regulations. We have taken various steps to prepare for complying with GDPR and other applicable laws and regulations however there can be no assurance that these steps are sufficient to assure compliance. Further, additional EU laws and regulations (and member states’ implementations thereof) further govern the protection of individuals and of electronic communications. If our efforts to comply with GDPR or other applicable laws and regulations are not successful, we may be subject to penalties and fines that would adversely impact our business and results of operations, and our ability to use personal data of individuals could be significantly impaired.

Competition

We operate in a highly competitive industry that is characterized by constant change and innovation. Changes in the applications and the programing languages used to develop applications, devices, operating systems, and technology landscape result in evolving customer requirements. Our competitors include True Fit, Fit analytics and 3DLook.

The principal competitive factors in our market include the following:

| ● | High Accuracy Size Recommendations: the highest accuracy and the lowest margin of error by combining patented technology including AI and ML, size chart or spec data, and MySizeID property body data measurement; |

| ● | Integration |

| ○ | Fast 1 week integration including size chart size chart review and product mapping | |

| ○ | Easy 1 line of “all included” script implementation |

| ● | Technical Advantages |

| ○ | Very small library that weighs ±50kb (minimum widget loading time on product page) | |

| ○ | Ultra-Fast loading and size recommendation presenting | |

| ○ | Restful API option (API integration with any website or app) |

| 15 |

| ● | Optimizations |

| ○ | Adjustments of size charts based on performance | |

| ○ | Widget usage analysis by FashTech and BI teams | |

| ○ | Automatic pairing of size charts with products/collections |

| ● | User Experience |

| ○ | Easy to use interface (10-15 seconds to receive size recommendations) | |

| ○ | Option to add/deduct questions to/from widget wizards | |

| ○ | Users automatically receive size recommendations on all products after initial sign up |

| ● | Product and platform features, architecture, reliability, privacy and security, performance, effectiveness, and supported environments; | |

| ● | Product extensibility and ability to integrate with other technology infrastructures; | |

| ● | Digital operations expertise; | |

| ● | Ease of use of products and platform capabilities; | |

| ● | Total cost of ownership; | |

| ● | Adherence to industry standards and certifications; | |

| ● | Strength of sales and marketing efforts; | |

| ● | Brand awareness and reputation; and | |

| ● | Focus on customer success |

We believe we generally compete favorably with our competitors on the basis of these factors. We expect competition to increase as other established and emerging companies enter our markets, as customer requirements evolve, and as new products and technologies are introduced. We expect this to be particularly true as we offer a smartphone-based offering that does not need to utilize the smartphone’s camera, and our competitors may also seek to repurpose their existing offerings to provide similar solutions. Many of our competitors have substantially greater financial, technical, and other resources, greater name recognition, larger sales and marketing budgets, broader distribution, and larger and more mature intellectual property portfolios.

Human Capital Management

As of March 31, 2023, we had a total of 35 employees, of which 30 were full-time employees, including 9 in sales and marketing, 12 in technology and development and 9 in administration and finance.

None of our employees are represented by a collective bargaining agreement, nor have we experienced any work stoppage. We consider our relationship with our employees to be good. Our future success depends on our continuing ability to attract and retain highly qualified engineers, sales and marketing, account management, and senior management personnel.

We also believe we have built a strong sales team focused on expanding into new markets through the acquisition of Naiz and our current team.

We believe that our future success will depend, in part, on our continued ability to attract, hire and retain qualified personnel. In particular, we depend on the skills, experience and performance of our senior management and research personnel. We compete for qualified personnel with other hi-tech companies, as well as universities and non-profit research institutions.

| 16 |

We provide competitive compensation and benefits programs to help meet the needs of our employees. In addition to salaries, these programs (which vary by country/region and employment classification) include incentive compensation plan, pension, and insurance benefits, paid time off, , among others. We also use targeted equity-based grants with vesting conditions to facilitate retention of personnel, particularly for our key employees.

The success of our business is fundamentally connected to the well-being of our people. Accordingly, we implemented an hybrid work policy in which the employees can work from home twice a week.

We consider our employees to be a key factor to our success and we are focused on attracting and retaining the best employees at all levels of our business. Inclusion and diversity is a strategic, business priority. We employ people based on relevant qualifications, demonstrated skills, performance and other job-related factors. We do not tolerate unlawful discrimination related to employment, and strive to ensure that employment decisions related to recruitment, selection, evaluation, compensation, and development, among others, are not influenced by race, color, religion, gender, age, ethnic origin, nationality, sexual orientation, marital status, or disability. Continuous monitoring to ensure pay equity has been a focus in 2022. We have continued to improve gender balance in 2022 with a focus on increasing the representation of women hired as new college graduates. We are committed to creating a trusting environment where all ideas are welcomed and employees feel comfortable and empowered to draw on their unique experiences and backgrounds.

We consider our relations with our employees to be good.

Company Information

Our principal executive offices are located at HaYarden 4 St., POB 1026, Airport City, Israel 7010000, and our telephone number is +972-3-600-9030. Our website address is www.mysizeid.com. Any information contained on, or that can be accessed through, our website is not incorporated by reference into, nor is it in any way a part of, this Annual Report on Form 10-K.

We use our website (www.mysizeid.com) as a channel of distribution of Company information. The information we post through this channel may be deemed material. Accordingly, investors should monitor our website, in addition to following our press releases, SEC filings and public conference calls and webcasts. The contents of our website are not, however, a part of this Annual Report on Form 10-K.

Corporate History

We were incorporated in the State of Delaware on September 20, 1999 under the name Topspin Medical, Inc. In December 2013, we changed our name to Knowledgetree Ventures Inc. Subsequently, in February 2014, we changed our name to MySize, Inc. In 2020, we created a subsidiary in the Russian Federation, My Size LLC.

From inception through 2012, we were engaged in research and development of a medical magnetic resonance imaging, or MRI, technology for interventional cardiology and in the development of MRI technology for use in the diagnosis and treatment of prostate cancer. In January 2012, we acquired Metamorefix Ltd., or Metamorefix. Metamorefix was incorporated in 2007, and was engaged in the development of innovative solutions for the rehabilitation of tissues, particularly skin tissues. By the end of 2012, we ceased operations and in January 2013, we sold our entire ownership interest in Metamorefix.

In September 2013, Ronen Luzon, our Chief Executive Officer, acquired control of the Company from Asher Shmuelevitch, according to which Mr. Luzon purchased 70,238 shares of common stock from Mr. Shmuelevitch, which shares represented approximately 40% of the issued and outstanding capital stock of the Company at such time, thus becoming a controlling shareholder of the Company. In connection with the acquisition, Mr. Luzon reached a settlement with our then creditors pursuant to which the main creditor, Mr. Shmuelevitch, was paid a total sum of approximately $140,000 in consideration for a full and final waiver of any and all his claims that he may have relating to any monetary indebtedness of the Company to the creditors.

| 17 |

In February 2014, My Size Israel, our wholly owned subsidiary, entered into a Purchase Agreement, or the Purchase Agreement, with Shoshana Zigdon, who at the time was a beneficial owner of more than 20% of our outstanding shares, with respect to the acquisition by us of certain rights related to the collection of data for measurement purposes including rights in the venture, the method and a patent application that had been filed by the Seller (PCT/IL2013/050056), or the Assets. In consideration for the sale of the Assets, we agreed to pay to Ms. Zigdon, 18% of our operating profit, directly or indirectly connected with the Assets together with value-added tax in accordance with the law for a period of seven years from the end of the development period of the aforementioned venture. In addition to the foregoing, the Purchase Agreement provided that all developments, improvements, knowledge and know-how developed and/or accumulated by us after the execution of the Purchase Agreement will be owned by us. Further, Ms. Zigdon agreed not to compete, directly or indirectly, with us in any matter relating to the Assets for a period of seven years from the end of the development period of the venture.

On May 26, 2021, we, My Size Israel, and Ms. Zigdon entered into an Amendment to Purchase Agreement, or the Amendment, which made certain amendments to the Purchase Agreement. Pursuant to the Amendment, Ms. Zigdon agreed to irrevocably waive (i) the right to repurchase certain assets related to the collection of data for measurement purposes that My Size Israel acquired from Ms. Zigdon under the Purchase Agreement and upon which our business is substantially dependent, or the Assets, and (ii) all past, present and future rights in any of the intellectual property rights sold, transferred and assigned to My Size Israel under the Purchase Agreement and any modifications, amendments or improvements made thereto, including, without limitation, any compensation, reward or any rights to royalties or to receive any payment or other consideration whatsoever in connection with such intellectual property rights, or the Waiver. In consideration of the Waiver, we issued 100,000 shares of common stock to Ms. Zigdon.

In September 2005, we commenced trading on the Tel Aviv Stock Exchange, or TASE. Between 2007 and 2012 we reported as a public company with the SEC. In August 2012, we suspended our reporting obligations. In mid-2015 we resumed reporting as a public company. On July 25, 2016, our common stock began publicly trading on the Nasdaq Capital Market under the symbol “MYSZ”.

ITEM 1A. RISK FACTORS

An investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors and the other information in this Annual Report on Form 10-K before investing in our common stock. Our business and results of operations could be seriously harmed by any of the following risks. The risks set out below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results. If any of the following events occur, our business, financial condition and results of operations could be materially adversely affected. In such case, the value and trading price of our common stock could decline, and you may lose all or part of your investment.

Summary Risk Factors

The principal factors and uncertainties that make investing in our ordinary shares risky, include, among others:

Risks Related to Our Financial Position and Capital Requirements

| ● | We have historically incurred significant losses and there can be no assurance when, or if, we will achieve or maintain profitability. | |

| ● | Our limited operating history makes it difficult to evaluate our business and prospects. | |

| ● | We will need to raise additional capital to meet our business requirements in the future, which is likely to be challenging, could be highly dilutive and may cause the market price of our common stock to decline. | |

| ● | The report of our independent registered public accounting firm contains an explanatory paragraph regarding substantial doubt about our ability to continue as a going concern. |

Risks Related to Our Company and Our Business

| ● | The market for our measurement technology is new and unproven, may experience limited growth and is highly dependent on U.S. retailers and online third-party resellers adopting our flagship product, MySizeID. |

| 18 |

| ● | Failure to effectively develop and expand our sales and marketing capabilities could harm our ability to grow our business and achieve broader market acceptance of our products. | |

| ● | We expect our sales cycle to be long and unpredictable and require considerable time and expense before executing a customer agreement, which may make it difficult to project when, if at all, we will obtain new customers and when we will generate revenue from those customers. | |

| ● | We recently acquired Orgad and Naiz and may in the future engage in additional acquisitions, joint ventures or collaborations which may increase our capital requirements, dilute our shareholders, cause us to incur debt or assume contingent liabilities, and subject us to other risks. We may not realize the benefits of these acquisitions, joint ventures or collaborations. | |

| ● | If we are not able to enhance our brand and increase market awareness of our company and products, then our business, results of operations and financial condition may be adversely affected. | |

| ● | If we do not develop enhancements to our products and introduce new products that achieve market acceptance, our business, results of operations and financial condition could be adversely affected. | |

| ● | The mobile technology industry is subject to rapid technological change and, to compete, we must continually enhance our mobile device applications and custom development services. | |

| ● | Our growth depends, in part, on the success of our strategic relationships with third parties. | |

| ● | Changes in economic conditions could materially affect our business, financial condition and results of operations. | |

| ● | We rely upon third parties to provide distribution for our applications, and disruption in these services could harm our business. | |

| ● | We rely on third-party hosting and cloud computing providers to operate certain aspects of our business. Any failure, disruption or significant interruption in our network or hosting and cloud services could adversely impact our operations and harm our business. | |

| ● | Real or perceived errors, failures, or bugs in our products could adversely affect our operating results and growth prospects. | |

| ● | We could be harmed by improper disclosure or loss of sensitive or confidential company, employee, or customer data, including personal data. | |

| ● | A material breach in security relating to our information systems and regulation related to such breaches could adversely affect us. | |

| ● | Our products and our business are subject to a variety of U.S. and international laws and regulations, including those regarding privacy, data protection and information security, and our customers may be subject to regulations related to the handling and transfer of certain types of sensitive and confidential information. Any failure of our products to comply with or enable our customers to comply with applicable laws and regulations would harm our business, results of operations and financial condition. | |

| ● | We may not be able to adequately protect our intellectual property, which, in turn, could harm the value of our brands and adversely affect our business. | |

| ● | We may face intense competition and expect competition to increase in the future, which could limit us in developing a customer base and generating revenue. | |

| ● | Our business operations and future development could be significantly disrupted if we lose key members of our management team. |

| 19 |

| ● | If we are able to expand our operations, we may be unable to successfully manage our future growth. |

Risks Related to Our Operations in Israel and Russia

| ● | Our headquarters and most of our operations are located in Israel, and therefore, political conditions in Israel may affect our operations and results. | |

| ● | Russia’s invasion of Ukraine and sanctions brought against Russia could disrupt our operations in Russia. |

Risks Related to Our Common Stock

| ● | A more active, liquid trading market for our common stock may not develop, and the price of our common stock may fluctuate significantly. | |

| ● | Our business, operating results and growth rates may be adversely affected by current or future unfavorable economic and market conditions and adverse developments with respect to financial institutions and associated liquidity risk; | |

| ● | Sales by our stockholders of a substantial number of shares of our common stock in the public market could adversely affect the market price of our common stock. | |

| ● | Our securities are traded on more than one market which may result in price variations. | |

| ● | We are a former “shell company” and as such are subject to certain limitations not generally applicable to other public companies. |

Risks Related to Our Financial Position and Capital Requirements

We have historically incurred significant losses and there can be no assurance when, or if, we will achieve or maintain profitability.

We realized a net loss of approximately $8.3 million and $10.5 million for the years ended December 31, 2022 and 2021 and had an accumulated deficit of $53.5 million as at December 31, 2022. Because of the numerous risks and uncertainties associated with the development and commercialization of our products and business, we are unable to predict the extent of any future losses or when we will become profitable, if at all. Expected future operating losses will have an adverse effect on our cash resources, shareholders’ equity and working capital. Our failure to become and remain profitable could depress the value of our stock and impair our ability to raise capital, expand our business, maintain our development efforts, or continue our operations. A decline in our value could also cause you to lose all or part of your investment in us.

Our limited operating history makes it difficult to evaluate our business and prospects.

We have only been developing our measurement technology since 2014. Since then, our operating history has been primarily limited to research and development, pilot studies, raising capital, and more recently acquisitions and sales and marketing efforts. Therefore, it may be difficult to evaluate our business and prospects. We have not yet demonstrated an ability to commercialize our products. Consequently, any predictions about our future performance may not be accurate, and you may not be able to fully assess our ability to complete development and/or commercialize our products, and any future products.

We will need to raise additional capital to meet our business requirements in the future, which is likely to be challenging, could be highly dilutive and may cause the market price of our common stock to decline.

Based on our projected cash flows and the cash balances as of the date of this Annual Report on Form 10-K, our existing cash is insufficient to fund operations for a period of more than 12 months. As a result, there is substantial doubt about our ability to continue as a going concern. In order to meet our business objectives in the future, we will need to raise additional capital, which may not be available on reasonable terms or at all. Additional capital would be used to accomplish the following:

| ● | finance our current operating expenses; | |

| ● | pursue growth opportunities; | |

| ● | hire and retain qualified management and key employees; |

| 20 |

| ● | respond to competitive pressure; | |

| ● | comply with regulatory requirements; and | |

| ● | maintain compliance with applicable laws. |

Current conditions in the capital markets are such that traditional sources of capital may not be available to us when needed or may be available only on unfavorable terms. Our ability to raise additional capital, if needed, will depend on conditions in the capital markets, economic conditions, and a number of other factors, many of which are outside our control, and on our financial performance. Accordingly, we cannot assure you that we will be able to successfully raise additional capital at all or on terms that are acceptable to us. If we cannot raise additional capital when needed, it may have a material adverse effect on our business, results of operations and financial condition.

To the extent that we raise additional capital through the sale of equity or convertible debt securities, the issuance of such securities could result in substantial dilution for our current stockholders. The terms of any securities issued by us in future capital transactions may be more favorable to new investors, and may include preferences, superior voting rights and the issuance of warrants or other derivative securities, which may have a further dilutive effect on the holders of any of our securities then-outstanding. We may issue additional shares of our common stock or securities convertible into or exchangeable or exercisable for our common stock in connection with hiring or retaining personnel, option or warrant exercises, future acquisitions or future placements of our securities for capital-raising or other business purposes. The issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of our common stock to decline and existing stockholders may not agree with our financing plans or the terms of such financings. In addition, we may incur substantial costs in pursuing future capital financing, including investment banking fees, legal fees, accounting fees, securities law compliance fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we issue, such as convertible notes and warrants, which may adversely impact our financial condition. Furthermore, any additional debt or equity financing that we may need may not be available on terms favorable to us, or at all. If we are unable to obtain such additional financing on a timely basis, we may have to curtail our development activities and growth plans and/or be forced to sell assets, perhaps on unfavorable terms, or we may have to cease our operations, which would have a material adverse effect on our business, results of operations and financial condition.

Management has concluded that there is substantial doubt about our ability to continue as a going concern which could prevent us from obtaining new financing on reasonable terms or at all.