Item 1. |

Reports to Shareholders. |

| Page | ||||||||

| 2 | ||||||||

| 3 | ||||||||

| 16 | ||||||||

| 18 | ||||||||

| 24 | ||||||||

| 25 | ||||||||

| 26 | ||||||||

| 27 | ||||||||

| 28 | ||||||||

| 30 | ||||||||

| 31 | ||||||||

| 32 | ||||||||

| 72 | ||||||||

| 97 | ||||||||

| 98 | ||||||||

| 99 | ||||||||

| 100 | ||||||||

| 102 | ||||||||

| 105 | ||||||||

| 106 | ||||||||

| 108 | ||||||||

| 109 | ||||||||

| 113 | ||||||||

| 139 | ||||||||

| 140 | ||||||||

| 146 | ||||||||

| 148 | ||||||||

| 149 | ||||||||

| 153 | ||||||||

| Fund | Fund Summary |

Schedule of Investments |

||||||

| 7 | 33 | |||||||

| 8 | 37 | |||||||

| 9 | 41 | |||||||

| 10 | 45 | |||||||

| 11 | 48 | |||||||

| 12 | 51 | |||||||

| 13 | 54 | |||||||

| 14 | 60 | |||||||

| 15 | 66 | |||||||

(1) |

Consolidated Schedule of Investments |

Market Insights |

|

| |

|

| |

Deborah A. DeCotis |

Joshua D. Ratner | |

Chair of the Board of Trustees |

President | |

Total Returns of Certain Asset Classes for the Period Ended December 31, 2023 | ||

Asset Class (as measured by, currency) |

12-Month | |

U.S. large cap equities (S&P 500 Index, USD) |

26.29% | |

Global equities (MSCI World Index, USD) |

23.79% | |

European equities (MSCI Europe Index, EUR) |

15.83% | |

Emerging market equities (MSCI Emerging Markets Index, EUR) |

9.83% | |

Japanese equities (Nikkei 225 Index, JPY) |

30.90% | |

Emerging market local bonds (JPMorgan Government Bond Index-Emerging Markets Global Diversified Index, USD Unhedged) |

12.70% | |

Emerging market external debt (JPMorgan Emerging Markets Bond Index (EMBI) Global, USD Hedged) |

10.45% | |

Below investment grade bonds (ICE BofAML Developed Markets High Yield Constrained Index, USD Hedged) |

13.78% | |

Global investment grade credit bonds (Bloomberg Global Aggregate Credit Index, USD Hedged) |

8.68% | |

Fixed-rate, local currency government debt of investment grade countries (Bloomberg Global Treasury Index, USD Hedged) |

6.72% | |

2 |

PIMCO CLOSED-END FUNDS |

Important Information About the Funds |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 3 |

Important Information About the Funds |

(Cont.) |

4 |

PIMCO CLOSED-END FUNDS |

Fund Name |

Inception Date |

Diversification Status | ||||||||

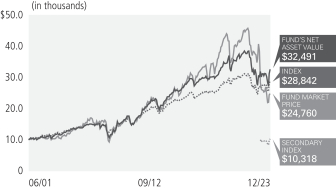

PIMCO Municipal Income Fund |

06/29/01 |

Diversified | ||||||||

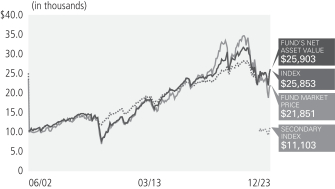

PIMCO Municipal Income Fund II |

06/28/02 |

Diversified | ||||||||

PIMCO Municipal Income Fund III |

10/31/02 |

Diversified | ||||||||

PIMCO California Municipal Income Fund |

06/29/01 |

Diversified | ||||||||

PIMCO California Municipal Income Fund II |

06/28/02 |

Diversified | ||||||||

PIMCO California Municipal Income Fund III |

10/31/02 |

Diversified | ||||||||

PIMCO New York Municipal Income Fund |

06/29/01 |

Non-diversified | ||||||||

PIMCO New York Municipal Income Fund II |

06/28/02 |

Diversified | ||||||||

PIMCO New York Municipal Income Fund III |

10/31/02 |

Non-diversified | ||||||||

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 5 |

Important Information About the Funds |

(Cont.) |

6 |

PIMCO CLOSED-END FUNDS |

Symbol on NYSE - PCQ |

Municipal Bonds & Notes |

||||

Ad Valorem Property Tax |

29.7% |

|||

Health, Hospital & Nursing Home Revenue |

11.2% |

|||

General Fund |

7.2% |

|||

Local or Guaranteed Housing |

7.1% |

|||

College & University Revenue |

7.0% |

|||

Port, Airport & Marina Revenue |

6.1% |

|||

Lease (Abatement) |

4.6% |

|||

Tobacco Settlement Funded |

4.6% |

|||

Sales Tax Revenue |

4.3% |

|||

Natural Gas Revenue |

4.2% |

|||

Electric Power & Light Revenue |

2.6% |

|||

Sewer Revenue |

2.1% |

|||

Water Revenue |

1.8% |

|||

Highway Revenue Tolls |

1.6% |

|||

Lease (Non-Terminable) |

1.5% |

|||

Special Tax |

1.5% |

|||

Other |

2.2% |

|||

Short-Term Instruments |

0.7% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$9.32 |

|||

NAV |

$10.66 |

|||

Premium/(Discount) to NAV |

(12.57)% |

|||

Market Price Distribution Rate (2) |

4.64% |

|||

NAV Distribution Rate (2) |

4.05% |

|||

Total Effective Leverage (3) |

41.65% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 01/25/23* |

Commencement of Operations (06/29/01) |

||||||||||||||||||

|

Market Price |

(35.33)% |

(5.94)% |

2.19% |

(14.27)% |

4.11% |

||||||||||||||||

|

NAV |

7.84% |

1.36% |

4.51% |

1.85% |

5.38% |

||||||||||||||||

|

Bloomberg CA Muni 22+ Year Index |

9.13% |

2.42% |

4.15% |

4.69% |

4.82% |

¨ | |||||||||||||||

|

ICE California Long Duration Municipal Securities Index** |

— |

— |

— |

3.12% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Total return is not annualized for a “since launch” date of less than one year. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to the general obligation segment contributed to performance, as the segment posted positive returns. |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the healthcare sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 7 |

Symbol on NYSE - PCK |

Municipal Bonds & Notes |

||||

Ad Valorem Property Tax |

28.6% | |||

Health, Hospital & Nursing Home Revenue |

10.0% | |||

Local or Guaranteed Housing |

7.4% | |||

General Fund |

6.8% | |||

Tobacco Settlement Funded |

5.7% | |||

College & University Revenue |

5.6% | |||

Natural Gas Revenue |

5.4% | |||

Port, Airport & Marina Revenue |

4.7% | |||

Electric Power & Light Revenue |

4.0% | |||

Sales Tax Revenue |

3.8% | |||

Highway Revenue Tolls |

2.9% | |||

Lease (Abatement) |

2.7% | |||

Sewer Revenue |

2.2% | |||

Special Tax |

1.7% | |||

Lease (Non-Terminable) |

1.4% | |||

Other |

3.9% | |||

Short-Term Instruments |

3.2% | |||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$5.80 |

|||

NAV |

$6.80 |

|||

Premium/(Discount) to NAV |

(14.71)% |

|||

Market Price Distribution Rate (2) |

4.45% |

|||

NAV Distribution Rate (2) |

3.79% |

|||

Total Effective Leverage (3) |

41.29% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 01/25/23* |

Commencement of Operations (06/28/02) |

||||||||||||||||||

|

|

Market Price |

(10.74)% |

(1.04)% |

1.24% |

(6.76)% |

2.16% |

||||||||||||||||

|

|

NAV |

8.34% |

0.94% |

4.81% |

1.91% |

3.49% |

||||||||||||||||

|

|

Bloomberg CA Muni 22+ Year Index |

9.13% |

2.42% |

4.15% |

4.69% |

4.68% |

¨ | |||||||||||||||

|

|

ICE California Long Duration Municipal Securities Index** |

— |

— |

— |

3.12% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Total return is not annualized for a “since launch” date of less than one year. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to the general obligation segment contributed to performance, as the segment posted positive returns. |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the industrial revenue sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

8 |

PIMCO CLOSED-END FUNDS |

Symbol on NYSE - PZC |

Municipal Bonds & Notes |

||||

Ad Valorem Property Tax |

27.5% |

|||

Health, Hospital & Nursing Home Revenue |

13.7% |

|||

Local or Guaranteed Housing |

7.4% |

|||

Tobacco Settlement Funded |

7.1% |

|||

General Fund |

6.1% |

|||

College & University Revenue |

5.5% |

|||

Port, Airport & Marina Revenue |

4.7% |

|||

Sales Tax Revenue |

4.3% |

|||

Lease (Abatement) |

3.6% |

|||

Electric Power & Light Revenue |

3.1% |

|||

Special Tax |

2.8% |

|||

Water Revenue |

2.6% |

|||

Natural Gas Revenue |

2.1% |

|||

Sewer Revenue |

1.8% |

|||

Lease (Non-Terminable) |

1.5% |

|||

Other |

3.8% |

|||

Short-Term Instruments |

2.4% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$7.37 |

|||

NAV |

$7.89 |

|||

Premium/(Discount) to NAV |

(6.59)% |

|||

Market Price Distribution Rate (2) |

4.80% |

|||

NAV Distribution Rate (2) |

4.49% |

|||

Total Effective Leverage (3) |

41.20% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 01/25/23* |

Commencement of Operations (10/31/02) |

||||||||||||||||||

|

|

Market Price |

(7.46)% |

(0.33)% |

3.41% |

(4.83)% |

2.98% |

||||||||||||||||

|

|

NAV |

7.33% |

1.25% |

4.65% |

1.79% |

3.69% |

||||||||||||||||

|

|

Bloomberg CA Muni 22+ Year Index |

9.13% |

2.42% |

4.15% |

4.69% |

4.61% |

||||||||||||||||

|

|

ICE California Long Duration Municipal Securities Index** |

— |

— |

— |

3.12% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Total return is not annualized for a “since launch” date of less than one year. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to the general obligation segment contributed to performance, as the segment posted positive returns. |

| » | Exposure to municipal revenue bonds within the healthcare sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 9 |

Symbol on NYSE - PNF |

Municipal Bonds & Notes |

||||

Water Revenue |

10.2% |

|||

College & University Revenue |

10.1% |

|||

Port, Airport & Marina Revenue |

9.6% |

|||

Tobacco Settlement Funded |

9.3% |

|||

Health, Hospital & Nursing Home Revenue |

9.1% |

|||

Income Tax Revenue |

8.0% |

|||

Electric Power & Light Revenue |

7.2% |

|||

General Fund |

5.4% |

|||

Ad Valorem Property Tax |

4.6% |

|||

Industrial Revenue |

4.0% |

|||

Local or Guaranteed Housing |

3.7% |

|||

Transit Revenue |

3.5% |

|||

Highway Revenue Tolls |

2.5% |

|||

Sales Tax Revenue |

2.2% |

|||

Miscellaneous Revenue |

2.0% |

|||

Appropriations |

1.7% |

|||

Miscellaneous Taxes |

1.1% |

|||

Other |

3.4% |

|||

Short-Term Instruments |

2.4% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$7.86 |

|||

NAV |

$8.98 |

|||

Premium/(Discount) to NAV |

(12.47)% |

|||

Market Price Distribution Rate (2) |

5.11% |

|||

NAV Distribution Rate (2) |

4.48% |

|||

Total Effective Leverage (3) |

32.09% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 01/25/23* |

Commencement of Operations (06/29/01) |

||||||||||||||||||

|

|

Market Price |

(8.59)% |

(3.12)% |

2.76% |

(16.34)% |

3.00% |

||||||||||||||||

|

|

NAV |

8.09% |

0.18% |

3.94% |

1.73% |

3.85% |

||||||||||||||||

|

|

Bloomberg NY Muni 22+ Year Index |

10.66% |

2.04% |

3.66% |

4.98% |

4.52% |

¨ | |||||||||||||||

|

|

ICE New York Long Duration Municipal Securities Index** |

— |

— |

— |

3.79% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Total return is not annualized for a “since launch” date of less than one year. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the transportation sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the education sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

10 |

PIMCO CLOSED-END FUNDS |

Symbol on NYSE - PNI |

Municipal Bonds & Notes |

||||

College & University Revenue |

11.9% |

|||

Tobacco Settlement Funded |

11.8% |

|||

Income Tax Revenue |

10.8% |

|||

Water Revenue |

9.3% |

|||

Port, Airport & Marina Revenue |

9.1% |

|||

Electric Power & Light Revenue |

8.8% |

|||

Health, Hospital & Nursing Home Revenue |

7.1% |

|||

Highway Revenue Tolls |

4.1% |

|||

Sales Tax Revenue |

3.5% |

|||

Miscellaneous Revenue |

3.4% |

|||

Local or Guaranteed Housing |

3.0% |

|||

Ad Valorem Property Tax |

2.8% |

|||

Industrial Revenue |

2.7% |

|||

Lease (Appropriation) |

2.0% |

|||

General Fund |

1.4% |

|||

Appropriations |

1.1% |

|||

Other |

3.7% |

|||

Short-Term Instruments |

3.5% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$7.59 |

|||

NAV |

$8.66 |

|||

Premium/(Discount) to NAV |

(12.36)% |

|||

Market Price Distribution Rate (2) |

4.66% |

|||

NAV Distribution Rate (2) |

4.09% |

|||

Total Effective Leverage (3) |

40.47% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 01/25/23* |

Commencement of Operations (06/28/02) |

||||||||||||||||||

|

|

Market Price |

0.12% |

(1.76)% |

2.51% |

(3.61)% |

3.01% |

||||||||||||||||

|

|

NAV |

8.97% |

0.31% |

4.27% |

1.85% |

3.95% |

||||||||||||||||

|

|

Bloomberg NY Muni 22+ Year Index |

10.66% |

2.04% |

3.66% |

4.98% |

4.43% |

¨ | |||||||||||||||

|

|

ICE New York Long Duration Municipal Securities Index** |

— |

— |

— |

3.79% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The index is not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the transportation sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the industrial revenue sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 11 |

Symbol on NYSE - PYN |

Municipal Bonds & Notes |

||||

Tobacco Settlement Funded |

10.6% |

|||

Water Revenue |

10.6% |

|||

College & University Revenue |

10.3% |

|||

Port, Airport & Marina Revenue |

9.1% |

|||

Income Tax Revenue |

9.1% |

|||

Electric Power & Light Revenue |

7.2% |

|||

Health, Hospital & Nursing Home Revenue |

6.6% |

|||

Industrial Revenue |

6.2% |

|||

Ad Valorem Property Tax |

4.1% |

|||

Local or Guaranteed Housing |

4.1% |

|||

Sales Tax Revenue |

3.2% |

|||

Transit Revenue |

3.2% |

|||

Highway Revenue Tolls |

3.0% |

|||

Lease (Appropriation) |

2.7% |

|||

General Fund |

2.6% |

|||

Miscellaneous Revenue |

2.5% |

|||

Fuel Sales Tax Revenue |

1.3% |

|||

Other |

0.9% |

|||

Short-Term Instruments |

2.7% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$5.96 |

|||

NAV |

$6.88 |

|||

Premium/(Discount) to NAV |

(13.37)% |

|||

Market Price Distribution Rate (2) |

4.99% |

|||

NAV Distribution Rate (2) |

4.33% |

|||

Total Effective Leverage (3) |

39.69% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 01/25/23* |

Commencement of Operations (10/31/02) |

||||||||||||||||||

|

|

Market Price |

(8.35)% |

(2.52)% |

1.81% |

(9.73)% |

1.65% |

||||||||||||||||

|

|

NAV |

8.02% |

0.29% |

3.70% |

1.68% |

2.59% |

||||||||||||||||

|

|

Bloomberg NY Muni 22+ Year Index |

10.66% |

2.04% |

3.66% |

4.98% |

4.31% |

||||||||||||||||

|

|

ICE New York Long Duration Municipal Securities Index** |

— |

— |

— |

3.79% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Total return is not annualized for a “since launch” date of less than one year. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the industrial revenue sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the transportation sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

12 |

PIMCO CLOSED-END FUNDS |

Symbol on NYSE - PMF |

Municipal Bonds & Notes |

||||

Health, Hospital & Nursing Home Revenue |

15.2% |

|||

Ad Valorem Property Tax |

10.7% |

|||

Sales Tax Revenue |

5.9% |

|||

Highway Revenue Tolls |

5.3% |

|||

Miscellaneous Revenue |

5.2% |

|||

Tobacco Settlement Funded |

5.0% |

|||

Industrial Revenue |

4.9% |

|||

Water Revenue |

4.9% |

|||

Local or Guaranteed Housing |

4.0% |

|||

Lease (Appropriation) |

4.0% |

|||

Electric Power & Light Revenue |

3.9% |

|||

Natural Gas Revenue |

3.5% |

|||

Sewer Revenue |

3.3% |

|||

College & University Revenue |

3.2% |

|||

Port, Airport & Marina Revenue |

2.7% |

|||

Appropriations |

2.5% |

|||

Income Tax Revenue |

2.4% |

|||

Fuel Sales Tax Revenue |

2.0% |

|||

Nuclear Revenue |

1.6% |

|||

General Fund |

1.5% |

|||

Miscellaneous Taxes |

1.3% |

|||

Resource Recovery Revenue |

1.1% |

|||

Other |

4.4% |

|||

Short-Term Instruments |

0.4% |

|||

Other |

1.1% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$9.33 |

|||

NAV |

$9.73 |

|||

Premium/(Discount) to NAV |

(4.11)% |

|||

Market Price Distribution Rate (2) |

5.40% |

|||

NAV Distribution Rate (2) |

5.18% |

|||

Total Effective Leverage (3) |

41.84% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 12/09/22 |

Commencement of Operations (06/29/01) |

||||||||||||||||||

|

|

Market Price |

(5.62)% |

(0.57)% |

3.22% |

(6.66)% |

4.46% |

||||||||||||||||

|

|

NAV |

7.88% |

0.70% |

4.49% |

4.22% |

5.32% |

||||||||||||||||

|

|

Bloomberg Long Municipal Bond Index |

9.35% |

2.22% |

3.95% |

7.41% |

4.51% |

¨ | |||||||||||||||

|

|

ICE Long Duration National Municipal Securities Index* |

11.03% |

— |

— |

7.60% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the industrial revenue sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the transportation sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 13 |

Symbol on NYSE - PML |

Municipal Bonds & Notes |

||||

Health, Hospital & Nursing Home Revenue |

15.9% |

|||

Ad Valorem Property Tax |

9.2% |

|||

Industrial Revenue |

5.2% |

|||

Tobacco Settlement Funded |

5.2% |

|||

Sales Tax Revenue |

5.2% |

|||

Natural Gas Revenue |

5.1% |

|||

Sewer Revenue |

4.6% |

|||

Lease (Appropriation) |

4.5% |

|||

Electric Power & Light Revenue |

4.1% |

|||

Highway Revenue Tolls |

4.1% |

|||

College & University Revenue |

3.9% |

|||

Water Revenue |

3.8% |

|||

Miscellaneous Revenue |

3.8% |

|||

Local or Guaranteed Housing |

3.3% |

|||

Port, Airport & Marina Revenue |

3.0% |

|||

Appropriations |

2.9% |

|||

Fuel Sales Tax Revenue |

2.2% |

|||

Income Tax Revenue |

2.1% |

|||

General Fund |

1.5% |

|||

Hotel Occupancy Tax |

1.4% |

|||

Miscellaneous Taxes |

1.3% |

|||

Nuclear Revenue |

1.1% |

|||

Resource Recovery Revenue |

1.1% |

|||

Government Fund/Grant Revenue |

1.0% |

|||

Other |

3.4% |

|||

Short-Term Instruments |

0.1% |

|||

Other |

1.0% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$8.30 |

|||

NAV |

$9.01 |

|||

Premium/(Discount) to NAV |

(7.88)% |

|||

Market Price Distribution Rate (2) |

5.71% |

|||

NAV Distribution Rate (2) |

5.26% |

|||

Total Effective Leverage (3) |

38.27% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 12/09/22 |

Commencement of Operations (06/28/02) |

||||||||||||||||||

|

|

Market Price |

(2.97)% |

(3.70)% |

3.58% |

(7.06)% |

3.77% |

||||||||||||||||

|

|

NAV |

8.57% |

1.01% |

4.56% |

4.79% |

4.52% |

||||||||||||||||

|

|

Bloomberg Long Municipal Bond Index |

9.35% |

2.22% |

3.95% |

7.41% |

4.51% |

¨ | |||||||||||||||

|

|

ICE Long Duration National Municipal Securities Index* |

11.03% |

— |

— |

7.60% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to municipal revenue bonds within the industrial revenue sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the healthcare sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

14 |

PIMCO CLOSED-END FUNDS |

Symbol on NYSE - PMX |

Municipal Bonds & Notes |

||||

Health, Hospital & Nursing Home Revenue |

13.1% |

|||

Ad Valorem Property Tax |

10.0% |

|||

Sales Tax Revenue |

6.1% |

|||

Local or Guaranteed Housing |

5.4% |

|||

Electric Power & Light Revenue |

5.2% |

|||

Highway Revenue Tolls |

4.9% |

|||

Industrial Revenue |

4.6% |

|||

Sewer Revenue |

4.5% |

|||

Natural Gas Revenue |

4.4% |

|||

Tobacco Settlement Funded |

4.1% |

|||

Water Revenue |

4.1% |

|||

Port, Airport & Marina Revenue |

4.0% |

|||

Fuel Sales Tax Revenue |

3.6% |

|||

Lease (Appropriation) |

3.5% |

|||

College & University Revenue |

3.1% |

|||

Appropriations |

2.8% |

|||

Income Tax Revenue |

2.6% |

|||

Miscellaneous Revenue |

2.1% |

|||

General Fund |

1.9% |

|||

Nuclear Revenue |

1.4% |

|||

Miscellaneous Taxes |

1.2% |

|||

Resource Recovery Revenue |

1.1% |

|||

Other |

5.3% |

|||

Short-Term Instruments |

0.1% |

|||

Other |

0.9% |

|||

† |

% of Investments, at value. |

§ |

Allocation Breakdown and % of investments exclude securities sold short and financial derivative instruments, if any. |

Market Price |

$ |

|||

NAV |

$ |

|||

Premium/(Discount) to NAV |

( |

|||

Market Price Distribution Rate (2) |

5.36% |

|||

NAV Distribution Rate (2) |

4.77% |

|||

Total Effective Leverage (3) |

40.31% |

|||

Average Annual Total Return (1) for the period ended December 31, 2023 |

||||||||||||||||||||||

1 Year |

5 Year |

10 Year |

Since launch of Secondary Index 12/09/22 |

Commencement of Operations (10/31/02) |

||||||||||||||||||

|

|

Market Price |

(10.64)% |

(2.91)% |

3.02% |

(13.79)% |

3.32% |

||||||||||||||||

|

|

NAV |

8.71% |

0.64% |

4.96% |

4.87% |

4.30% |

||||||||||||||||

|

|

Bloomberg Long Municipal Bond Index |

9.35% |

2.22% |

3.95% |

7.41% |

4.40% |

||||||||||||||||

|

|

ICE Long Duration National Municipal Securities Index* |

11.03% |

— |

— |

7.60% |

— |

||||||||||||||||

(1) |

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the sale of Fund shares. Total return, market price, NAV, market price distribution rate, and NAV distribution rate will fluctuate with changes in market conditions. Performance current to the most recent month-end is available at www.pimco.com or via (844) 33-PIMCO. Performance is calculated assuming all dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. Performance does not reflect any brokerage commissions in connection with the purchase or sale of Fund shares. |

Performance of an index is shown in light of a requirement by the Securities and Exchange Commission that the performance of an appropriate broad-based securities market index be disclosed. However, the Fund is not managed to an index nor should the index be viewed as a “benchmark” for the Fund’s performance. The indexes are not intended to be indicative of the Fund’s investment strategies, portfolio components or past or future performance. Please see Additional Information Regarding the Funds for a description of the Fund’s principal investment strategies. |

(2) |

Distribution rates are not performance and are calculated by annualizing the most recent distribution per share and dividing by the NAV or Market Price, as applicable, as of the reported date. Distributions may be comprised of ordinary income, net capital gains, and/or a return of capital (“ROC”) of your investment in the Fund. Because the distribution rate may include a ROC, it should not be confused with yield or income. If the Fund estimates that a portion of its distribution may be comprised of amounts from sources other than net investment income in accordance with its policies and good accounting practices, the Fund will notify shareholders of the estimated composition of such distribution through a Section 19 Notice. Please refer to the most recent Section 19 Notice, if applicable, for additional information regarding the estimated composition of distributions. Please visit www.pimco.com for most recent Section 19 Notice, if applicable. Final determination of a distribution’s tax character will be provided to shareholders when such information is available. |

(3) |

Represents total effective leverage outstanding, as a percentage of total managed assets. Total effective leverage consists of preferred shares, reverse repurchase agreements and other borrowings, credit default swap notional and floating rate notes issued in tender option bond transactions, as applicable (collectively “Total Effective Leverage”). The Fund may engage in other transactions not included in Total Effective Leverage disclosed above that may give rise to a form of leverage, including certain derivative transactions. For the purpose of calculating Total Effective Leverage outstanding as a percentage of total managed assets, total managed assets refer to total assets (including assets attributable to Total Effective Leverage that may be outstanding) minus accrued liabilities (other than liabilities representing Total Effective Leverage). |

| » | Exposure to municipal revenue bonds within the special tax sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the transportation sector contributed to performance, as the sector posted positive returns. |

| » | Exposure to municipal revenue bonds within the industrial revenue sector contributed to performance, as the sector posted positive returns. |

| » | The costs associated with one or more forms of leverage detracted from performance. The costs of leverage generally will reduce returns to the extent they exceed the rate of return on the additional investments purchased with such leverage. |

| » | There were no other material detractors for this Fund. |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 15 |

Index Descriptions |

Index* |

Index Description | |

Bloomberg Long Municipal Bond Index |

Bloomberg Long Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long-term tax-exempt bond market. | |

Bloomberg CA Muni 22+ Year Index |

The Bloomberg CA Muni 22+ Year Index is the long maturity California component of the Bloomberg Municipal Bond Index, which consists of a broad selection of investment grade general obligation and revenue bonds. It is an unmanaged index representative of the tax-exempt bond market. | |

Bloomberg NY Muni 22+ Year Index |

The Bloomberg NY Muni 22+ Year Index is the long maturity New York component of the Bloomberg Municipal Bond Index, which consists of a broad selection of investment grade general obligation and revenue bonds. It is an unmanaged index representative of the tax-exempt bond market. | |

ICE California Long Duration Municipal Securities Index |

ICE California Long Duration Municipal Securities Index is a subset of the ICE Long Duration National Municipal Securities Index including only securities issued within the State of California. The ICE Long Duration National Municipal Securities Index tracks the performance of long duration rated and unrated US dollar denominated tax-exempt debt publicly issued by US states and territories, and their political subdivisions, in the US domestic market. | |

ICE Long Duration National Municipal Securities Index |

ICE Long Duration National Municipal Securities Index tracks the performance of long duration rated and unrated US dollar denominated tax-exempt debt publicly issued by US states and territories, and their political subdivisions, in the US domestic market. | |

ICE New York Long Duration Municipal Securities Index |

ICE New York Long Duration Municipal Securities Index is a subset of the ICE Long Duration National Municipal Securities Index including only securities issued within the State of New York. The ICE Long Duration National Municipal Securities Index tracks the performance of long duration rated and unrated US dollar denominated tax-exempt debt publicly issued by US states and territories, and their political subdivisions, in the US domestic market. | |

16 |

PIMCO CLOSED-END FUNDS |

ANNUAL REPORT |

| | DECEMBER 31, 2023 | 17 |

Financial Highlights |

Investment Operations |

Less Distributions to Preferred Shareholders (c) |

Less Distributions to Common Shareholders (d) |

||||||||||||||||||||||||||||||||||||||||||||||||||

Selected Per Share Data for the Year Ended^: |

Net Asset Value Beginning of Year (a) |

Net Investment Income (Loss) (b) |

Net Realized/ Unrealized Gain (Loss) |

From Net Investment Income |

From Net Realized Capital Gains |

Net Increase (Decrease) in Net Assets Applicable to Common Shareholders Resulting from Operations |

From Net Investment Income |

From Net Realized Capital Gains |

Tax Basis Return of Capital |

Total |

Increase Resulting from Tender of ARPS (c) |

Increase Resulting from Common Share Offering |

Offering Cost Charged to Paid in Capital |

|||||||||||||||||||||||||||||||||||||||

PIMCO California Municipal Income Fund |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 10.31 | $ | 0.55 | $ | 0.57 | $ | (0.37 | ) | $ | 0.00 | $ | 0.75 | $ | (0.24 | ) | $ | 0.00 | $ | (0.19 | ) | $ | (0.43 | ) | $ | 0.03 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

14.08 | 0.65 | (3.48 | ) | (0.14 | ) | 0.00 | (2.97 | ) | (0.59 | ) | (0.02 | ) | (0.19 | ) | (0.80 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||

12/31/2021 |

14.28 | 0.71 | (0.12 | ) | (0.01 | ) | 0.00 | 0.58 | (0.78 | ) | 0.00 | 0.00 | (0.78 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

12/31/2020 |

14.20 | 0.74 | 0.20 | (0.07 | ) | 0.00 | 0.87 | (0.78 | ) | (0.01 | ) | 0.00 | (0.79 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

12/31/2019 |

13.32 | 0.80 | 1.16 | (0.16 | ) | 0.00 | 1.80 | (0.92 | ) | 0.00 | 0.00 | (0.92 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

PIMCO California Municipal Income Fund II |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 6.53 | $ | 0.33 | $ | 0.38 | $ | (0.22 | ) | $ | 0.00 | $ | 0.49 | $ | (0.16 | ) | $ | 0.00 | $ | (0.10 | ) | $ | (0.26 | ) | $ | 0.05 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

9.11 | 0.39 | (2.50 | ) | (0.09 | ) | 0.00 | (2.20 | ) | (0.36 | ) | 0.00 | (0.02 | ) | (0.38 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||

12/31/2021 |

9.13 | 0.40 | (0.04 | ) | 0.00 | 0.00 | 0.36 | (0.38 | ) | 0.00 | 0.00 | (0.38 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

12/31/2020 |

8.98 | 0.41 | 0.17 | (0.04 | ) | 0.00 | 0.54 | (0.38 | ) | (0.01 | ) | 0.00 | (0.39 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

12/31/2019 |

8.29 | 0.50 | 0.87 | (0.10 | ) | 0.00 | 1.27 | (0.42 | ) | (0.16 | ) | 0.00 | (0.58 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

PIMCO California Municipal Income Fund III |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 7.70 | $ | 0.39 | $ | 0.37 | $ | (0.25 | ) | $ | 0.00 | $ | 0.51 | $ | (0.27 | ) | $ | 0.00 | $ | (0.08 | ) | $ | (0.35 | ) | $ | 0.03 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

10.20 | 0.48 | (2.43 | ) | (0.09 | ) | 0.00 | (2.04 | ) | (0.46 | ) | 0.00 | 0.00 | (0.46 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||

12/31/2021 |

10.29 | 0.52 | (0.15 | ) | 0.00 | 0.00 | 0.37 | (0.46 | ) | 0.00 | 0.00 | (0.46 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

12/31/2020 |

10.20 | 0.52 | 0.09 | (0.05 | ) | 0.00 | 0.56 | (0.46 | ) | (0.01 | ) | 0.00 | (0.47 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

12/31/2019 |

9.46 | 0.56 | 0.80 | (0.11 | ) | 0.00 | 1.25 | (0.51 | ) | 0.00 | 0.00 | (0.51 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

PIMCO New York Municipal Income Fund |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 8.70 | $ | 0.45 | $ | 0.47 | $ | (0.29 | ) | $ | 0.00 | $ | 0.63 | $ | (0.15 | ) | $ | 0.00 | $ | (0.25 | ) | $ | (0.40 | ) | $ | 0.05 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

12.13 | 0.48 | (3.30 | ) | (0.11 | ) | 0.00 | (2.93 | ) | (0.40 | ) | 0.00 | (0.10 | ) | (0.50 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||

12/31/2021 |

12.01 | 0.54 | 0.09 | (0.01 | ) | 0.00 | 0.62 | (0.50 | ) | 0.00 | 0.00 | (0.50 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

12/31/2020 |

12.15 | 0.60 | (0.17 | ) | (0.06 | ) | 0.00 | 0.37 | (0.50 | ) | (0.01 | ) | 0.00 | (0.51 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||

12/31/2019 |

11.29 | 0.68 | 0.96 | (0.13 | ) | 0.00 | 1.51 | (0.65 | ) | 0.00 | 0.00 | (0.65 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

PIMCO New York Municipal Income Fund II |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 8.29 | $ | 0.44 | $ | 0.55 | $ | (0.30 | ) | $ | 0.00 | $ | 0.69 | $ | (0.23 | ) | $ | 0.00 | $ | (0.12 | ) | $ | (0.35 | ) | $ | 0.03 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

11.66 | 0.47 | (3.25 | ) | (0.11 | ) | 0.00 | (2.89 | ) | (0.48 | ) | 0.00 | 0.00 | (0.48 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||

12/31/2021 |

11.50 | 0.48 | 0.17 | (0.01 | ) | 0.00 | 0.64 | (0.48 | ) | 0.00 | 0.00 | (0.48 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

12/31/2020 |

11.59 | 0.56 | (0.12 | ) | (0.05 | ) | 0.00 | 0.39 | (0.48 | ) | 0.00 | 0.00 | (0.48 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

12/31/2019 |

10.67 | 0.63 | 0.93 | (0.13 | ) | 0.00 | 1.43 | (0.51 | ) | 0.00 | 0.00 | (0.51 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

PIMCO New York Municipal Income Fund III |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 6.66 | $ | 0.39 | $ | 0.40 | $ | (0.30 | ) | $ | 0.00 | $ | 0.49 | $ | (0.10 | ) | $ | 0.00 | $ | (0.20 | ) | $ | (0.30 | ) | $ | 0.03 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

9.20 | 0.42 | (2.42 | ) | (0.11 | ) | 0.00 | (2.11 | ) | (0.33 | ) | 0.00 | (0.10 | ) | (0.43 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||

12/31/2021 |

9.15 | 0.44 | 0.05 | (0.01 | ) | 0.00 | 0.48 | (0.43 | ) | 0.00 | 0.00 | (0.43 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

12/31/2020 |

9.29 | 0.48 | (0.14 | ) | (0.05 | ) | 0.00 | 0.29 | (0.42 | ) | 0.00 | (0.01 | ) | (0.43 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||

12/31/2019 |

8.66 | 0.55 | 0.66 | (0.13 | ) | 0.00 | 1.08 | (0.41 | ) | 0.00 | (0.04 | ) | (0.45 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

PIMCO Municipal Income Fund (Consolidated) |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 9.51 | $ | 0.61 | $ | 0.43 | $ | (0.37 | ) | $ | 0.00 | $ | 0.67 | $ | (0.37 | ) | $ | 0.00 | $ | (0.13 | ) | $ | (0.50 | ) | $ | 0.05 | $ | N/A | $ | N/A | ||||||||||||||||||||||

12/31/2022 |

13.33 | 0.68 | (3.71 | ) | (0.14 | ) | 0.00 | (3.17 | ) | (0.65 | ) | 0.00 | 0.00 | (0.65 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||

12/31/2021 |

13.22 | 0.71 | 0.06 | (0.01 | ) | 0.00 | 0.76 | (0.65 | ) | 0.00 | 0.00 | (0.65 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

12/31/2020 |

13.35 | 0.74 | (0.07 | ) | (0.07 | ) | 0.00 | 0.60 | (0.65 | ) | (0.08 | ) | 0.00 | (0.73 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||

12/31/2019 |

12.36 | 0.81 | 1.07 | (0.16 | ) | 0.00 | 1.72 | (0.72 | ) | (0.01 | ) | 0.00 | (0.73 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

PIMCO Municipal Income Fund II (Consolidated) |

||||||||||||||||||||||||||||||||||||||||||||||||||||

12/31/2023 |

$ | 8.76 | $ | 0.52 | $ | 0.40 | $ | (0.25 | ) | $ | 0.00 | $ | 0.67 | $ | (0.30 | ) | $ | 0.00 | $ | (0.17 | ) | $ | (0.47 | ) | $ | 0.05 | $ | 0.00 | $ | 0.00 | ||||||||||||||||||||||

12/31/2022 |

12.37 | 0.60 | (3.43 | ) | (0.10 | ) | 0.00 | (2.93 | ) | (0.60 | ) | 0.00 | (0.11 | ) | (0.71 | ) | 0.00 | 0.03 | 0.00 | |||||||||||||||||||||||||||||||||

12/31/2021 |

12.42 | 0.66 | 0.00 | 0.00 | 0.00 | 0.66 | (0.71 | ) | 0.00 | 0.00 | (0.71 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||||

12/31/2020 |

12.50 | 0.69 | (0.01 | ) | (0.05 | ) | 0.00 | 0.63 | (0.71 | ) | 0.00 | 0.00 | (0.71 | ) | 0.00 | N/A | N/A | |||||||||||||||||||||||||||||||||||

12/31/2019 |

11.62 | 0.77 | 1.01 | (0.12 | ) | 0.00 | 1.66 | (0.78 | ) | 0.00 | 0.00 | (0.78 | ) | 0.00 | N/A | N/A | ||||||||||||||||||||||||||||||||||||

18 |

PIMCO CLOSED-END FUNDS |

See Accompanying Notes |

Common Share |

Ratios/Supplemental Data |

|||||||||||||||||||||||||||||||||||||

Ratios to Average Net Assets Applicable to Common Shareholders |

||||||||||||||||||||||||||||||||||||||

Net Asset Value End of Year (a) |

Market Price End of Year |

Total Investment Return (e) |

Net Assets Applicable to Common Shareholders End of Year (000s) |

Expenses (f)(g) |

Expenses Excluding Waivers (f)(g) |

Expenses Excluding Interest Expense (f) |

Expenses Excluding Interest Expense and Waivers (f) |

Net Investment Income (Loss) (f) |

Portfolio Turnover Rate |

|||||||||||||||||||||||||||||

| |

|

|

||||||||||||||||||||||||||||||||||||

| $ | 10.66 | $ | 9.32 | (35.33 | )% | $ | 202,306 | 2.16 | % | 2.16 | % | 1.34 | % | 1.34 | % | 5.43 | % | 28 | % | |||||||||||||||||||

| 10.31 | 15.07 | (14.34 | ) | 195,462 | 1.78 | 1.78 | 1.26 | 1.26 | 5.73 | 28 | ||||||||||||||||||||||||||||

| 14.08 | 18.58 | 7.99 | 266,321 | 1.44 | 1.44 | 1.20 | 1.20 | 5.05 | 11 | |||||||||||||||||||||||||||||

| 14.28 | 17.98 | (4.94 | ) | 269,561 | 1.67 | 1.67 | 1.22 | 1.22 | 5.28 | 15 | ||||||||||||||||||||||||||||

| 14.20 | 19.86 | 29.47 | 267,390 | 2.09 | 2.09 | 1.18 | 1.18 | 5.75 | 16 | |||||||||||||||||||||||||||||

| |

|

|

||||||||||||||||||||||||||||||||||||

| $ | 6.81 | $ | 5.80 | (10.74 | )% | $ | 219,490 | 2.29 | % | 2.29 | % | 1.37 | % | 1.37 | % | 5.12 | % | 25 | % | |||||||||||||||||||

| 6.53 | 6.79 | (23.32 | ) | 210,581 | 1.77 | 1.77 | 1.29 | 1.29 | 5.49 | 27 | ||||||||||||||||||||||||||||

| 9.11 | 9.35 | 7.99 | 293,165 | 1.41 | 1.41 | 1.21 | 1.21 | 4.44 | 11 | |||||||||||||||||||||||||||||

| 9.13 | 9.03 | (5.58 | ) | 293,591 | 1.62 | 1.62 | 1.23 | 1.23 | 4.68 | 19 | ||||||||||||||||||||||||||||

| 8.98 | 10.00 | 36.01 | 288,138 | 1.99 | 1.99 | 1.18 | 1.18 | 5.61 | 16 | |||||||||||||||||||||||||||||

| |

|

|

||||||||||||||||||||||||||||||||||||

| $ | 7.89 | $ | 7.37 | (7.46 | )% | $ | 177,348 | 2.33 | % | 2.33 | % | 1.36 | % | 1.36 | % | 5.20 | % | 30 | % | |||||||||||||||||||

| 7.70 | 8.35 | (20.55 | ) | 172,972 | 1.80 | 1.80 | 1.27 | 1.27 | 5.71 | 28 | ||||||||||||||||||||||||||||

| 10.20 | 11.10 | 13.11 | 228,733 | 1.45 | 1.45 | 1.21 | 1.21 | 5.06 | 13 | |||||||||||||||||||||||||||||

| 10.29 | 10.25 | (5.89 | ) | 230,271 | 1.68 | 1.68 | 1.23 | 1.23 | 5.13 | 13 | ||||||||||||||||||||||||||||

| 10.20 | 11.41 | 25.66 | 227,745 | 2.12 | 2.12 | 1.20 | 1.20 | 5.59 | 16 | |||||||||||||||||||||||||||||

| |

|

|

||||||||||||||||||||||||||||||||||||

| $ | 8.98 | $ | 7.86 | (8.59 | )% | $ | 70,675 | 1.48 | % | 1.48 | % | 1.39 | % | 1.39 | % | 5.16 | % | 45 | % | |||||||||||||||||||