UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended August 31, 2019

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 000-50298

ORAMED PHARMACEUTICALS INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 98-0376008 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) | |

| 1185 Avenue of the Americas, Suite 228, New York, NY | 10036 | |

| (Address of Principal Executive Offices) | (Zip Code) |

844-967-2633

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $.012 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Date File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Non-accelerated filer ☒ | Smaller reporting company ☒ | |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of the last business day of the registrant’s most recently completed second fiscal quarter was $42,511,402, based on a price of $3.20, being the last price at which the shares of the registrant’s common stock were sold on The Nasdaq Capital Market prior to the end of the most recently completed second fiscal quarter.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date: 17,398,112 shares of common stock issued and outstanding as of November 26, 2019.

ORAMED PHARMACEUTICALS INC.

FORM 10-K

(FOR THE FISCAL YEAR ENDED AUGUST 31, 2019)

TABLE OF CONTENTS

i

As used in this Annual Report on Form 10-K, the terms “we,” “us,” “our,” the “Company,” and “Oramed” mean Oramed Pharmaceuticals Inc. and our wholly-owned Israeli subsidiary, Oramed Ltd., unless otherwise indicated. All dollar amounts refer to U.S. dollars unless otherwise indicated.

On August 31, 2019, the exchange rate between the New Israeli Shekel, or NIS, and the dollar, as quoted by the Bank of Israel, was NIS 3.535 to $1.00. Unless indicated otherwise by the context, statements in this Annual Report on Form 10-K that provide the dollar equivalent of NIS amounts or provide the NIS equivalent of dollar amounts are based on such exchange rate.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

The statements contained in this Annual Report on Form 10-K that are not historical facts are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. Words such as “expects,” “anticipates,” “intends,” “plans,” “planned expenditures,” “believes,” “seeks,” “estimates” and similar expressions or variations of such words are intended to identify forward-looking statements, but are not deemed to represent an all-inclusive means of identifying forward-looking statements as denoted in this Annual Report on Form 10-K. Additionally, statements concerning future matters are forward-looking statements. We remind readers that forward-looking statements are merely predictions and therefore inherently subject to uncertainties and other factors and involve known and unknown risks that could cause the actual results, performance, levels of activity, or our achievements, or industry results, to be materially different from any future results, performance, levels of activity, or our achievements, or industry results, expressed or implied by such forward-looking statements. Such forward-looking statements appear in Item 1 - “Business” and Item 7 - “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” as well as elsewhere in this Annual Report on Form 10-K and include, among other statements, statements regarding the following:

| ● | the expected development and potential benefits from our products in treating diabetes; |

| ● | the prospects of entering into additional license agreements, or other partnerships or forms of cooperation with other companies or medical institutions; |

| ● | future milestones, conditions and royalties under the license agreement with Hefei Tianhui Incubator of Technologies Co., Ltd., or HTIT; |

| ● | our research and development plans, including pre-clinical and clinical trials plans and the timing of enrollment, obtaining results and conclusion of trials, including without limitation, our expectation that we will initiate two six-month Phase III clinical trials, and our expectation to file a New Drug Application thereafter; |

| ● | our belief that our technology has the potential to deliver medications and vaccines orally that today can only be delivered via injection; |

| ● | the competitive ability of our technology based product efficacy, safety, patient convenience, reliability, value and patent position; |

| ● | the potential market demand for our products; |

| ● | our expectation that in the upcoming year our research and development expenses will continue to be our major expenditure; |

| ● | our expectations regarding our short- and long-term capital requirements; |

| ● | our outlook for the coming months and future periods, including but not limited to our expectations regarding future revenue and expenses; and |

| ● | information with respect to any other plans and strategies for our business. |

Although forward-looking statements in this Annual Report on Form 10-K reflect the good faith judgment of our management, such statements can only be based on facts and factors known by us at the time of such statements. Consequently, forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those discussed herein, including those risks described in Item 1A. “Risk Factors”, and expressed from time to time in our other filings with the Securities and Exchange Commission, or SEC. In addition, historic results of scientific research, clinical and preclinical trials do not guarantee that the conclusions of future research or trials would not suggest different conclusions. Also, historic results referred to in this Annual Report on Form 10-K could be interpreted differently in light of additional research, clinical and preclinical trials results. Readers are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report on Form 10-K. Except as required by law, we undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this Annual Report on Form 10-K. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this Annual Report on Form 10-K which attempt to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

ii

DESCRIPTION OF BUSINESS

Research and Development

We are a pharmaceutical company currently engaged in the research and development of innovative pharmaceutical solutions, including an oral insulin capsule to be used for the treatment of individuals with diabetes, and the use of orally ingestible capsules or pills for delivery of other polypeptides. We utilize Clinical Research Organizations, or CROs, to conduct our clinical studies.

Oral insulin: We are seeking to transform the treatment of diabetes through our proprietary flagship product, an orally ingestible insulin capsule, or ORMD-0801. Our technology allows insulin to travel from the gastrointestinal tract via the portal vein to the bloodstream, revolutionizing the manner in which insulin is delivered. It enables the passage in a more physiological manner than current delivery methods of insulin. Our technology is a platform that has the potential to deliver medications and vaccines orally that today can only be delivered via injection.

FDA Guidance: In August 2017, during a call with the U.S. Food and Drug Administration, or FDA, we were advised that the regulatory pathway for the submission of ORMD-0801 would be a Biologics License Application, or BLA. If approved the BLA pathway would grant us 12 years of marketing exclusivity for ORMD-0801, from the approval date, and an additional six months of exclusivity may be granted to us if the product also receives approval for use in pediatric patients. The FDA confirmed that the approach to nonclinical toxicology, chemistry manufacturing controls and qualification of excipients would be driven by their published guidance documents.

Phase IIb Study: In May 2018, we initiated a three-month dose-ranging Phase IIb clinical trial of ORMD-0801. This placebo controlled, randomized, 90-day treatment clinical trial was conducted on 269 type 2 diabetic patients in multiple centers throughout the United States pursuant to an Investigational New Drug application, or IND, with the FDA. The primary endpoints of the trial were to assess the safety and evaluate the effect of ORMD-0801 on HbA1c levels over a 90-day treatment period. Secondary endpoints of the trial included measurements of fasting plasma glucose, or FPG, post-prandial glucose, or PPG levels, during a mixed-meal tolerance test, or MMTT, and weight. In May 2019 we began an extension of this protocol for approximately 75 type 2 diabetic patients, who were dosed using a lower dosage.

In November 2019, we announced positive results from the initial cohort of the Phase IIb trial. Patients randomized in the trial to once-daily ORMD-0801 achieved a reduction in mean HbA1c of 0.60% from baseline, or a reduction of 0.54% adjusted for placebo (p value = 0.036). This 0.54% reduction in HbA1c is considered clinically meaningful, reflecting an improved glucose control that would result in reduced risk of developing diabetes-related complications. Treatment with ORMD-0801 demonstrated an excellent safety profile, with no serious drug-related adverse events and with no increased frequency of hypoglycemic episodes. In addition, during this 90-day trial, no weight gain was observed. In the initial cohort, 269 U.S.-based patients were enrolled and treated with a dose-increasing approach: 16 mg initial dose, titrated to 24 mg per dose, and then titrated to 32 mg per dose. Patients were randomized into three groups to assess dosing frequency: once-daily (32 mg per day), twice-daily (64 mg per day), thrice daily (96 mg per day). There was a corresponding placebo for each treatment arm. Two hundred nine (209) patients completed treatment to the 12-week endpoint and were included in the data analysis (24 subjects did not complete the full 12 weeks of treatment). In addition, due to evidence of treatment-by-center interaction, two sites (36 patients (13.4% of enrolled subjects)) were excluded from the statistical analysis as they showed results opposite from the rest of the statistically significant results. We are still investigating the cause of this discrepancy. The once-daily and twice-daily arms achieved statistically significant (p-value 0.036 and 0.042, respectively) reductions from baseline in A1C of 0.60% (0.54% with placebo adjustment) and 0.59% (0.53% with placebo adjustment), respectively. The thrice-daily arm did not meet statistical significance (p-value 0.093). ORMD-0801 demonstrated an excellent safety profile with no serious drug-related adverse events.

As our Phase IIb three-month dose-ranging clinical trial successfully met its primary endpoints, we anticipate initiating two six-month Phase III clinical trials on both type 1 and type 2 diabetic patients, following which we expect to file a BLA with potential FDA approval by the end of calendar year 2024.

1

Clamp Study: In June 2018, we initiated a glucose clamp study which will quantify insulin absorption in type 1 diabetic patients treated with ORMD-0801. The glucose clamp is a method for quantifying insulin absorption in order to measure a patient’s insulin sensitivity and how well a patient metabolizes glucose. This exploratory, randomized, double-blind glucose clamp study is evaluating exposure-response profiles of type 1 diabetic patients treated with ORMD-0801. Six patients with HbA1c levels of 10% or below, aged 18-50, are enrolled in the study. We expect to receive the results of this study in the first quarter of calendar year 2020.

Food Effect Study: In June 2018, we also initiated a food effect trial in the United States for ORMD-0801. This single-blind, five period, randomized, placebo-controlled crossover trial is evaluating the pharmacokinetics, or PK, and pharmacodynamics of ORMD-0801 taken at different times in relation to meals in healthy volunteers and patients with type 1 diabetes. Forty-eight (48) patients are enrolled, including 24 healthy volunteers and 24 patients with type 1 diabetes. We expect to receive the results of this study in the first quarter of calendar year 2020.

NASH Study: In October 2018, we initiated an exploratory clinical study of ORMD-0801 in patients with nonalcoholic steatohepatitis, or NASH. The three-month treatment study, which was approved by Israel’s Ministry of Health, will assess the effectiveness of ORMD-0801 in reducing liver fat content, inflammation and fibrosis in 30 patients with NASH. As requested by Israel’s Ministry of Health, the first part of the study will be conducted on 10 participants and is expected to be completed during first quarter of calendar year 2020.

Toxicology Study (6 Months): In March 2019, we completed a six-month dosing toxicology study of ORMD-0801, which was initiated in September 2018 following the FDA’s request. We expect to receive the results of this study in the first quarter of calendar year 2020.

Type 1 Study: In November 2019 we initiated a crossover study of type 1 diabetic patients to compare the effects of ORMD-0801 given once daily versus the effects of ORMD-0801 given three times daily. The study is anticipated to include 26 subjects and is expected to be completed in the second quarter of calendar year 2020.

Oral Glucagon-Like Peptide-1: Glucagon-Like Peptide-1, or GLP-1, is an incretin hormone, which is a type of gastrointestinal hormone that stimulates the secretion of insulin from the pancreas. The incretin concept was hypothesized when it was noted that glucose ingested by mouth (oral) stimulated two to three times more insulin release than the same amount of glucose administered intravenously. In addition to stimulating insulin release, GLP-1 was found to suppress glucagon release (a hormone involved in the regulation of glucose) from the pancreas, slow gastric emptying to reduce the rate of absorption of nutrients into the blood stream and increase satiety. Other important beneficial attributes of GLP-1 are its effects of increasing the number of beta cells (cells that manufacture and release insulin) in the pancreas and, possibly, protection of the heart. In addition to our flagship product, the ORMD-0801 insulin capsule, we are using our technology for an orally ingestible GLP-1 capsule, or ORMD-0901.

In February 2019, we completed a Phase I PK trial to evaluate the safety and the pharmacokinetics of ORMD-0901 compared to placebo. We expect to receive the results of this study in the first quarter of calendar year 2020. This study was conducted pursuant to an IND, which we expect to be followed by a Phase II trial on type 2 diabetic patients which will likely be conducted in the United States under an IND.

Diabetes: Diabetes is a disease in which the body does not produce or properly use insulin. Insulin is a hormone that causes sugar to be absorbed into cells, where the sugar is converted into energy needed for daily life. The cause of diabetes is attributed both to genetics (type 1 diabetes) and, most often, to environmental factors such as obesity and lack of exercise (type 2 diabetes). According to the International Diabetes Federation, or IDF, an estimated 425 million adults worldwide suffered from diabetes in 2017 and the IDF projects this number will increase to 629 million by 2045. Also, according to the IDF, in 2017, an estimated 4 million people died from diabetes. According to the American Diabetes Association, or ADA, in the United States there were approximately 30.3 million people with diabetes, or 9.4% of the United States population in 2015. Diabetes is a leading cause of blindness, kidney failure, heart attack, stroke and amputation.

Intellectual property: We own a portfolio of patents and patent applications covering our technologies, and we are aggressively protecting these technology developments on a worldwide basis.

2

Management: We are led by an experienced management team knowledgeable in the treatment of diabetes. Our Chief Scientific Officer, Miriam Kidron, PhD, is a recognized pharmacologist and a biochemist and the innovator primarily responsible for our oral insulin technology development and know-how.

Scientific Advisory Board: Our management team has access to our internationally recognized Scientific Advisory Board whose members are thought-leaders in their respective areas. The Scientific Advisory Board is comprised of Dr. Roy Eldor, Professor Ele Ferrannini, Dr. Robert R. Henry, Professor Avram Hershko, Dr. Harold Jacob and Dr. Jane E. B. Reusch.

Strategy

Short Term Business Strategy

We plan to conduct further research and development on the technology covered by the patent application “Methods and Composition for Oral Administration of Proteins,” which we acquired from Hadasit Medical Research Services and Development Ltd. in 2006, and which is granted in various foreign jurisdictions, as well as the other patents we have filed in various foreign jurisdictions since then, as discussed below under “—Patents and Licenses” and below under “Item 1A. Risk Factors”.

Through our research and development efforts, we have successfully developed an oral dosage form that is intended to withstand the harsh environment of the stomach and intestines and effectively deliver active insulin or other proteins, such as exenatide, for the treatment of diabetes. The excipients that are added to the proteins in the formulation process are not intended to modify the proteins chemically or biologically, and the dosage form is designed to be safe to ingest. We plan to continue to conduct clinical trials to show the effectiveness of our technology.

As our oral insulin (ORMD-0801) Phase IIb three-month dose-ranging clinical trial successfully met its primary endpoints, we anticipate initiating two six-month Phase III clinical trials on both type 1 and type 2 diabetic patients, following which we expect to file a BLA with potential FDA approval by the end of calendar year 2024.

In September 2018, the FDA cleared our IND application for human trials of our oral GLP-1 analog capsule ORMD-0901 and we initiated a Phase I PK trial which will evaluate the safety and the pharmacokinetics of ORMD-0901 compared to placebo. We expect to get the results of this study in the first calendar quarter of 2020.

Clinical trials are planned in order to substantiate our results as well as for purposes of making future filings for drug approval. We also plan to conduct further research and development by deploying our proprietary drug delivery technology for the delivery of other polypeptides in addition to insulin, and to develop other innovative pharmaceutical products.

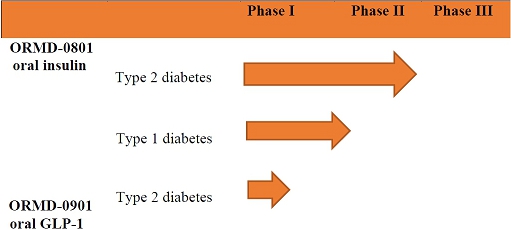

The table below gives an overview of our primary product pipeline:

3

Another component of our business strategy is to partner with other companies or medical institutions in order to further develop our technology and commence pre-commercialization activities. On November 30, 2015, we, our Israeli subsidiary and HTIT entered into a Technology License Agreement, which was further amended, according to which we granted HTIT an exclusive commercialization license in the territory of the People’s Republic of China, Macau and Hong Kong, or the Territory, related to our oral insulin capsule, ORMD-0801. Pursuant to this license agreement, HTIT will conduct, at its own expense, certain pre-commercialization and regulatory activities with respect to our subsidiary’s technology related to the ORMD-0801 capsule, and will pay, upon the meeting of certain conditions, certain royalties and an aggregate of approximately $37.5 million (see “Out-Licensed Technology” below). We plan to seek additional partnerships or forms of cooperation with other companies or medical institutions. While our strategy is to partner with an appropriate party, no assurance can be given that we will in fact be able to reach an agreeable partnership with any third party. Under certain circumstances, we may determine to develop one or more of our oral dosage forms on our own, either world-wide or in select territories.

Long Term Business Strategy

We plan to ultimately seek a strategic commercial partner, or partners, with extensive experience in the development, commercialization, and marketing of insulin applications and/or other orally digestible drugs. We anticipate such partner or partners would be responsible for, or substantially support, late stage clinical trials (Phase III) to increase the likelihood of obtaining regulatory approvals and registrations in the appropriate markets in a timely manner. We further anticipate that such partner, or partners, would also be responsible for sales, marketing and support of our products in these markets. Such planned strategic partnership, or partnerships, may provide a marketing and sales infrastructure for our products as well as financial and operational support for global clinical trials, post marketing studies, label expansions and other regulatory requirements concerning future clinical development in the United States and elsewhere. Any future strategic partner, or partners, may also provide capital and expertise that would enable the partnership to develop new oral dosage forms for other polypeptides. While our strategy is to partner with an appropriate party, no assurance can be given that we will in fact be able to reach an agreeable partnership with any third party. Under certain circumstances, we may determine to develop one or more of our oral dosage forms on our own, either world-wide or in select territories.

Other Planned Strategic Activities

In addition to developing our own oral dosage form drug portfolio, we are, on an on-going basis, considering in-licensing and other means of obtaining additional technologies to complement and/or expand our current product portfolio. Our goal is to create a well-balanced product portfolio that will enhance and complement our existing drug portfolio.

Product Development

Combination Therapy

In June 2012, we presented an abstract, which reported the impact of ORMD-0801 delivered in combination with ORMD-0901. The work assessed the safety and effectiveness of a combination of oral insulin and oral exenatide treatments delivered to pigs prior to food intake. The drug combination resulted in significantly improved blood glucose regulation when compared to administration of each drug separately.

In the near term, we are focusing our efforts on the development of our flagship products, oral insulin and oral exenatide. Once these two products have progressed further in clinical trials, we intend to conduct additional studies with the oral combination therapy.

Other Products

During the first quarter of calendar year 2017, we began developing a new drug candidate, a weight loss treatment in the form of an oral leptin capsule. We anticipate initiating a proof of concept single dose study for our oral leptin drug candidate to evaluate its pharmacokinetic and pharmacodynamics (glucagon reduction) in 10 type 1 adult diabetic patients in the fourth quarter of calendar year 2019. We anticipate receiving the final report of this study in the first quarter of calendar year 2020.

4

Raw Materials

Our oral insulin capsule is currently manufactured by Swiss Caps AG, a member of Aenova Group GmbH .

One of our oral capsule ingredients is being developed and produced by an Indian company.

In July 2010, Oramed Ltd. entered into the Manufacturing and Supply Agreement, or MSA, with Sanofi-Aventis Deutschland GMBH, or Sanofi-Aventis. According to the MSA, Sanofi-Aventis will supply Oramed Ltd. with specified quantities of recombinant human insulin to be used for clinical trials.

We purchase, pursuant to separate agreements with third parties, the raw materials required for the manufacturing of our oral capsule. We generally depend upon a limited number of suppliers for the raw materials. Although alternative sources of supply for these materials are generally available, we could incur significant costs and disruptions if we need to change suppliers. The termination of our relationships with our suppliers or the failure of these suppliers to meet our requirements for raw materials on a timely and cost-effective basis could have a material adverse effect on our business, prospects, financial condition and results of operations.

Patents and Licenses

We maintain a proactive intellectual property strategy, which includes patent filings in multiple jurisdictions, including the United States and other commercially significant markets. We hold 21 patent applications currently pending, with respect to various compositions, methods of production and oral administration of proteins and exenatide. Expiration dates for pending patents, if granted, will fall between 2026 and 2034.

We hold 77 patents, 3 of which were issued during the fiscal year ended August 31, 2019, or fiscal 2019, including patents issued by the United States, Swiss, German, French, U.K., Italian, Netherlands, Swedish, Spanish, Australian, Israeli, Japanese, New Zealand, South African, Russian, Canadian, Hong Kong, Chinese, European and Indian patent offices that cover a part of our technology, which allows for the oral delivery of proteins; patents issued by the Australian, Canadian, European, Austrian, Belgian, French, German, Irish, Italian, Luxembourg, Monaco, Netherlands, Norwegian, Spanish, Swedish, Swiss, U.K., Israeli, New Zealand, South African, Russian and Japanese patent offices that cover part of our technology for the oral delivery of exenatide; and patents issued by the European, Austrian, Belgian, Denmark, French, German, Irish, Italian, Luxembourg, Monaco, Netherlands, Norway, Spanish, Swedish, Swiss, U.K. and Japanese patent offices for treating diabetes.

Consistent with our strategy to seek protection in key markets worldwide, we have been and will continue to pursue the patent applications and corresponding foreign counterparts of such applications. We believe that our success will depend on our ability to obtain patent protection for our intellectual property.

Our patent strategy is as follows:

| ● | Aggressively protect all current and future technological developments to assure strong and broad protection by filing patents and/or continuations in part as appropriate, |

| ● | Protect technological developments at various levels, in a complementary manner, including the base technology, as well as specific applications of the technology, and |

| ● | Establish comprehensive coverage in the United States and in all relevant foreign markets in anticipation of future commercialization opportunities. |

We also rely on trade secrets and unpatentable know-how that we seek to protect, in part, by confidentiality agreements. Our policy is to require our employees, consultants, contractors, manufacturers, outside scientific collaborators and sponsored researchers, our board of directors, or our Board, technical review board and other advisors, to execute confidentiality agreements upon the commencement of employment or consulting relationships with us. These agreements provide that all confidential information developed or made known to the individual during the course of the individual’s relationship with us is to be kept confidential and not disclosed to third parties except in specific limited circumstances. We also require signed confidentiality or material transfer agreements from any company that is to receive our confidential information. In the case of employees, consultants and contractors, the agreements provide that all inventions conceived by the individual while rendering services to us shall be assigned to us as the exclusive property of our Company. There can be no assurance, however, that all persons who we desire to sign such agreements will sign, or if they do, that these agreements will not be breached, that we would have adequate remedies for any breach, or that our trade secrets or unpatentable know-how will not otherwise become known or be independently developed by competitors.

5

Out-Licensed Technology

In June 2010, Oramed Ltd. entered into a joint venture agreement with D.N.A Biomedical Solutions Ltd., or D.N.A, for the establishment of Entera Bio LTD, or Entera.

Under the terms of a license agreement that was entered into between Oramed Ltd. and Entera in August 2010, we out-licensed technology to Entera, on an exclusive basis, for the development of oral delivery drugs for certain indications to be agreed upon between the parties. The out-licensed technology differs from our main delivery technology that is used for oral insulin and GLP-1 analog and is subject to different patent applications. Entera’s initial development effort is for an oral formulation for the treatment of osteoporosis. In March 2011, we entered into a patent transfer agreement, or the Patent Transfer Agreement, to replace the original license agreement pursuant to which Oramed Ltd. assigned to Entera all of its right, title and interest in and to the patent application that it had licensed to Entera in August 2010. Under this agreement, Oramed Ltd. is entitled to receive from Entera royalties of 3% of Entera’s net revenues (as defined in the agreement) and a license back of that patent application for use in respect of diabetes and influenza.

In March 2011, we also consummated a transaction with D.N.A, whereby we sold to D.N.A 47% of Entera’s outstanding share capital on an undiluted basis, retaining a 3% interest as of March 2011. In consideration for the shares sold to D.N.A, we received, among other payments, ordinary shares of D.N.A. The D.N.A ordinary shares are traded on the Tel Aviv Stock Exchange and its quoted price is subject to market fluctuations, and may, at times, have a price below the value on the date we acquired such shares. In addition, the ordinary shares of D.N.A have historically experienced low trading volume; as a result, there is no guarantee that we will be able to resell the ordinary shares of D.N.A at the prevailing market prices. During the years ended August 31, 2019, 2018 and 2017, we did not sell any of the D.N.A ordinary shares. As of August 31, 2019, we held approximately 6.9% of D.N.A’s outstanding ordinary shares.

As of August 31, 2019, Entera had not yet realized any revenues. In July 2018, Entera completed an initial public offering and became listed on The Nasdaq Capital Market, or Nasdaq. In August 2018, Entera announced that it completed the treatment of patients in the first part of the PK/pharmacodynamic study in hypoparathyroidism patients with its oral parathyroid hormone drug, EB612. On December 11, 2018, Entera announced that it had entered into a research collaboration and license agreement, or the Amgen License, with Amgen Inc. related to research of inflammatory disease and other serious illnesses. As reported by Entera, under the terms of the Amgen License, Entera will receive a modest initial technology access fee from Amgen and will be responsible for preclinical development at Amgen’s expense. Entera will be eligible to receive up to $270,000,000 in aggregate payments, as well as tiered royalties up to mid-single digits, upon achievement of various clinical and commercial milestones if Amgen decides to move all of these programs forward. Amgen is responsible for clinical development, manufacturing and commercialization of any of the resulting programs. To the extent the Amgen License results in net revenues as defined in the Patent Transfer Agreement, our Subsidiary will be entitled to the aforementioned royalties.

On November 30, 2015, we, our Israeli subsidiary and HTIT entered into a Technology License Agreement, and on December 21, 2015, these parties entered into an Amended and Restated Technology License Agreement that was further amended by the parties on June 3, 2016 and July 24, 2016, or the License Agreement. According to the License Agreement, we granted HTIT an exclusive commercialization license in the Territory, related to our oral insulin capsule, ORMD-0801, or the Product. Pursuant to the License Agreement, HTIT will conduct, at its own expense, certain pre-commercialization and regulatory activities with respect to our subsidiary’s technology and ORMD-0801 capsule, and will pay (i) royalties of 10% on net sales of the related commercialized products to be sold by HTIT in the Territory, or Royalties, and (ii) an aggregate of $37.5 million, of which $3 million was payable immediately, $8 million will be paid subject to our entry into certain agreements with certain third parties, and $26.5 million will be payable upon achievement of certain milestones and conditions. In the event that we will not meet certain conditions, the Royalties rate may be reduced to a minimum of 8%. Following the final expiration of our patents covering the technology in the Territory in 2033, the Royalties rate may be reduced, under certain circumstances, to 5%. The royalty payment obligation shall apply during the period of time beginning upon the first commercial sale of the Product in the Territory, and ending upon the later of (i) the expiration of the last-to-expire licensed patents in the Territory; and (ii) 15 years after the first commercial sale of the Product in the Territory, or the Royalty Term. The License Agreement shall remain in effect until the expiration of the Royalty Term. The License Agreement contains customary termination provisions. Through August 31, 2019, we received aggregate milestone payments of $20.5 million.

6

We also entered into a separate securities purchase agreement with HTIT, or the SPA, pursuant to which HTIT invested $12 million in us in December 2015 (see – “Liquidity and capital resources” below). In connection with the License Agreement and the SPA, we received a non-refundable payment of $500,000 as a no-shop fee.

Government Regulation

The Drug Development Process

Regulatory requirements for the approval of new drugs vary from one country to another. In order to obtain approval to market our drug portfolio, we need to go through a different regulatory process in each country in which we apply for such approval. In some cases, information gathered during the approval process in one country can be used as supporting information for the approval process in another country. As a strategic decision, we decided to first explore the FDA regulatory pathway. The following is a summary of the FDA’s requirements.

The FDA requires that pharmaceutical and certain other therapeutic products undergo significant clinical experimentation and clinical testing prior to their marketing or introduction to the general public. Clinical testing, known as clinical trials or clinical studies, is either conducted internally by life science, pharmaceutical or biotechnology companies or is conducted on behalf of these companies by CROs.

The process of conducting clinical studies is highly regulated by the FDA, as well as by other governmental and professional bodies. Below we describe the principal framework in which clinical studies are conducted, as well as describe a number of the parties involved in these studies.

Protocols. Before commencing human clinical studies, the sponsor of a new drug or therapeutic product must submit an IND application to the FDA. The application contains, among other documents, what is known in the industry as a protocol. A protocol is the blueprint for each drug study. The protocol sets forth, among other things, the following:

| ● | Who must be recruited as qualified participants, |

| ● | How often to administer the drug or product, |

| ● | What tests to perform on the participants, and |

| ● | What dosage of the drug or amount of the product to give to the participants. |

Institutional Review Board. An institutional review board is an independent committee of professionals and lay persons which reviews clinical research studies involving human beings and is required to adhere to guidelines issued by the FDA. The institutional review board does not report to the FDA, but its records are audited by the FDA. Its members are not appointed by the FDA. All clinical studies must be approved by an institutional review board. The institutional review board’s role is to protect the rights of the participants in the clinical studies. It approves the protocols to be used, the advertisements which the company or CRO conducting the study proposes to use to recruit participants, and the form of consent which the participants will be required to sign prior to their participation in the clinical studies.

Clinical Trials. Human clinical studies or testing of a potential product are generally done in three stages known as Phase I through Phase III testing. The names of the phases are derived from the regulations of the FDA. Generally, there are multiple studies conducted in each phase.

Phase I. Phase I studies involve testing a drug or product on a limited number of healthy or patient participants, typically 24 to 100 people at a time. Phase I studies determine a product’s basic safety and how the product is absorbed by, and eliminated from, the body. This phase lasts an average of six months to a year.

7

Phase II. Phase II trials involve testing of no more than 300 participants at a time who may suffer from the targeted disease or condition. Phase II testing typically lasts an average of one to two years. In Phase II, the drug is tested to determine its safety and effectiveness for treating a specific illness or condition. Phase II testing also involves determining acceptable dosage levels of the drug. Phase II studies may be split into Phase IIa and Phase IIb sub-studies. Phase IIa studies may be conducted with patient volunteers and are exploratory (non-pivotal) studies, typically designed to evaluate clinical efficacy or biological activity. Phase IIb studies are conducted with patients defined to evaluate definite dose range and evaluate efficacy. If Phase II studies show that a new drug has an acceptable range of safety risks and probable effectiveness, a company will generally continue to review the substance in Phase III studies.

Phase III. Phase III studies involve testing large numbers of participants, typically several hundred to several thousand persons. The purpose is to verify effectiveness and long-term safety on a large scale. These studies generally last two to three years. Phase III studies are conducted at multiple locations or sites. Like the other phases, Phase III requires the site to keep detailed records of data collected and procedures performed.

Biological License Application. The results of the clinical trials for a biological product are submitted to the FDA as part of a BLA. Following the completion of Phase III studies, assuming the sponsor of a potential product in the United States believes it has sufficient information to support the safety and effectiveness of its product, the sponsor will generally submit a BLA to the FDA requesting that the product be approved for marketing. The application is a comprehensive, multi-volume filing that includes the results of all clinical studies, information about the drug’s composition, and the sponsor’s plans for producing, packaging and labeling the product. The FDA’s review of an application can take a few months to many years, with the average review lasting 18 months. Once approved, drugs and other products may be marketed in the United States, subject to any conditions imposed by the FDA. Approval of a BLA provides 12 years of exclusivity in the U.S. market.

Phase IV. The FDA may require that the sponsor conduct additional clinical trials following new drug approval. The purpose of these trials, known as Phase IV studies, is to monitor long-term risks and benefits, study different dosage levels or evaluate safety and effectiveness. In recent years, the FDA has increased its reliance on these trials. Phase IV studies usually involve thousands of participants. Phase IV studies also may be initiated by the company sponsoring the new drug to gain broader market value for an approved drug.

Similar to the U.S., a European sponsor of a biological product may submit a Marketing Approval Application to the EMA for the registration of the product. The approval process in Europe consists of several stages, which together are summed up to 210 days from the time of submission of the application (net, without periods in which the sponsor provides answers to questions raised by the agency) following which, a Marketing Approval may be granted. During the approval process, the sponsor’s manufacturing facilities will be audited in order to assess Good Manufacturing Practice compliance.

The drug approval process is time-consuming, involves substantial expenditures of resources, and depends upon a number of factors, including the severity of the illness in question, the availability of alternative treatments, and the risks and benefits demonstrated in the clinical trials.

Other Regulations

Various federal, state and local laws, regulations, and recommendations relating to safe working conditions, laboratory practices, the experimental use of animals, the environment and the purchase, storage, movement, import, export, use, and disposal of hazardous or potentially hazardous substances, including radioactive compounds and infectious disease agents, used in connection with our research are applicable to our activities. They include, among others, the U.S. Atomic Energy Act, the Clean Air Act, the Clean Water Act, the Occupational Safety and Health Act, the National Environmental Policy Act, the Toxic Substances Control Act, and Resources Conservation and Recovery Act, national restrictions on technology transfer, import, export, and customs regulations, and other present and possible future local, state, or federal regulation. The compliance with these and other laws, regulations and recommendations can be time-consuming and involve substantial costs. In addition, the extent of governmental regulation which might result from future legislation or administrative action cannot be accurately predicted and may have a material adverse effect on our business, financial condition, results of operations and prospects.

8

Competition

Competition in General

Competition in the area of biomedical and pharmaceutical research and development is intense and significantly depends on scientific and technological factors. These factors include the availability of patent and other protection for technology and products, the ability to commercialize technological developments and the ability to obtain regulatory approval for testing, manufacturing and marketing. Our competitors include major pharmaceutical, medical products, chemical and specialized biotechnology companies, many of which have financial, technical and marketing resources significantly greater than ours. In addition, many biotechnology companies have formed collaborations with large, established companies to support research, development and commercialization of products that may be competitive with ours. Academic institutions, governmental agencies and other public and private research organizations are also conducting research activities and seeking patent protection and may commercialize products on their own or through joint ventures. We are aware of certain other products manufactured or under development by competitors that are used for the treatment of the diseases and health conditions that we have targeted for product development. We can provide no assurance that developments by others will not render our technology obsolete or noncompetitive, that we will be able to keep pace with new technological developments or that our technology will be able to supplant established products and methodologies in the therapeutic areas that are targeted by us. The foregoing factors could have a material adverse effect on our business, prospects, financial condition and results of operations. These companies, as well as academic institutions, governmental agencies and private research organizations, also compete with us in recruiting and retaining highly qualified scientific personnel and consultants.

Competition within our sector is increasing, so we will encounter competition from existing firms that offer competitive solutions in diabetes treatment solutions. These competitive companies could develop products that are superior to, or have greater market acceptance, than the products being developed by us. We will have to compete against other biotechnology and pharmaceutical companies with greater market recognition and greater financial, marketing and other resources.

Our competition will be determined in part by the potential indications for which our technology is developed and ultimately approved by regulatory authorities. In addition, the first product to reach the market in a therapeutic or preventive area is often at a significant competitive advantage relative to later entrants to the market. Accordingly, the relative speed with which we, or our potential corporate partners, can develop products, complete the clinical trials and approval processes and supply commercial quantities of the products to the market are expected to be important competitive factors. Our competitive position will also depend on our ability to attract and retain qualified scientific and other personnel, develop effective proprietary products, develop and implement production and marketing plans, obtain and maintain patent protection and secure adequate capital resources. We expect our technology, if approved for sale, to compete primarily on the basis of product efficacy, safety, patient convenience, reliability, value and patent position.

Competition for Our Oral Insulin Capsule

We anticipate the oral insulin capsule to be a competitive diabetes drug because of its anticipated efficacy and safety profile. The following are some of the treatment options for type 1 and type 2 diabetic patients:

| ● | Insulin injections, |

| ● | Insulin pumps, or |

| ● | A combination of diet, exercise and oral medication which improve the body’s response to insulin or cause the body to produce more insulin. |

Scientific Advisory Board

We maintain a Scientific Advisory Board consisting of internationally recognized scientists who advise us on scientific and technical aspects of our business. The Scientific Advisory Board meets periodically to review specific projects and to assess the value of new technologies and developments to us. In addition, individual members of the Scientific Advisory Board meet with us periodically to provide advice in their particular areas of expertise. The Scientific Advisory Board consists of the following members, information with respect to whom is set forth below: Dr. Roy Eldor, Professor Ele Ferrannini, Dr. Robert R. Henry, Professor Avram Hershko, Dr. Harold Jacob and Dr. Jane E. B. Reusch.

9

Dr. Roy Eldor, MD, PhD, joined the Oramed Scientific Advisory Board in July 2016. He is an endocrinologist, internist and researcher with over twenty years of clinical and scientific experience. He is currently Director of the Diabetes Unit at the Institute of Endocrinology, Metabolism & Hypertension, Tel-Aviv Sourasky Medical Center. Prior to that, Dr. Eldor served as Principal Scientist at Merck Research Laboratories, Clinical Research - Diabetes & Endocrinology, Rahway, New Jersey. He has previously served as a senior physician in internal medicine at the Diabetes Unit in Hadassah Hebrew University Hospital, Jerusalem, Israel; and the Diabetes Division at the University of Texas Health Science Center in San Antonio, Texas (under the guidance of Dr. R.A. DeFronzo). Dr. Eldor is a recognized expert, with over 35 peer reviewed papers and book chapters, and has been a guest speaker at numerous international forums.

Professor Ele Ferrannini, MD, joined the Oramed Scientific Advisory Board in February 2007. He is a past President to the European Association for the Study of Diabetes, which supports scientists, physicians and students from all over the world who are interested in diabetes and related subjects in Europe, and performs functions similar to that of the ADA in the United States. Professor Ferrannini has worked with various institutions including the Department of Clinical & Experimental Medicine, University of Pisa School of Medicine, and CNR (National Research Council) Institute of Clinical Physiology, Pisa, Italy; and the Diabetes Division, Department of Medicine, University of Texas Health Science Center at San Antonio, Texas. He has also had extensive training in internal medicine and endocrinology, and has specialized in diabetes studies. Professor Ferrannini has received a Certificate of the Educational Council for Foreign Medical Graduates from the University of Bologna, and with cum laude honors completed a subspecialty in Diabetes and Metabolic Diseases at the University of Torino. He has published over 500 original papers and 50 book chapters and he is a “highly cited researcher,” according to the Institute for Scientific Information.

Dr. Robert R. Henry, MD, joined the Oramed Scientific Advisory Board in February 2018 and is a leader in diabetes research. As a past President of the ADA and recipient of its Banting Medal for Scientific Achievement, among other international recognitions, his basic and clinical research funded by the National Institutes of Health, or NIH, has resulted in more than 400 journal articles, chapters and books. Dr. Henry is currently Chief of the Section of Endocrinology, Metabolism & Diabetes, Veterans Affairs Healthcare System in San Diego, California, Professor of Medicine at the University of California, San Diego and Chief of the Center for Metabolic Research in San Diego, California. In addition to studying the metabolic and cardiovascular effects of human skeletal muscle and adipose tissue signaling and interactions, his current clinical research interests involve the study and development of new therapies for type 1 and type 2 diabetes and obesity.

Professor Avram Hershko, MD, PhD, joined the Oramed Scientific Advisory Board in July 2008. He earned his MD degree (1965) and PhD degree (1969) from the Hebrew University-Hadassah Medical School of Jerusalem. Professor Hershko served as a physician in the Israel Defense Forces from 1965 to 1967. After a post-doctoral fellowship with Gordon Tomkins at the University of San Francisco (1969-72), he joined the faculty of the Haifa Technion becoming a professor in 1980. He is now Distinguished Professor in the Unit of Biochemistry in the B. Rappaport Faculty of Medicine of the Technion. Professor Hershko’s main research interests concern the mechanisms by which cellular proteins are degraded, a formerly neglected field of study. Professor Hershko and his colleagues showed that cellular proteins are degraded by a highly selective proteolytic system. This system tags proteins for destruction by linkage to a protein called ubiquitin, which had previously been identified in many tissues, but whose function was previously unknown. Subsequent work by Professor Hershko and many other laboratories has shown that the ubiquitin system has a vital role in controlling a wide range of cellular processes, such as the regulation of cell division, signal transduction and DNA repair. Professor Hershko was awarded the Nobel Prize in Chemistry (2004) jointly with his former PhD student Aaron Ciechanover and their colleague Irwin Rose. His many honors include the Israel Prize for Biochemistry (1994), the Gairdner Award (1999), the Lasker Prize for Basic Medical Research (2000), the Wolf Prize for Medicine (2001) and the Louisa Gross Horwitz Award (2001). Professor Hershko is a member of the Israel Academy of Sciences (2000) and a Foreign Associate of the U.S. Academy of Sciences (2003).

Dr. Harold Jacob, MD, joined the Oramed Scientific Advisory Board in November 2016. Since 1998, Dr. Jacob has served as the president of Medical Instrument Development Inc., a company which provides a range of support and consulting services to start-up and early stage companies as well as patenting its own proprietary medical devices. Since 2011, Dr. Jacob has also served as an attending physician at Hadassah University Medical Center, where he has served as the director of the gastrointestinal endoscopy unit since September 2013. Dr. Jacob has advised a spectrum of companies in the past and he served as a consultant and then as the Director of Medical Affairs at Given Imaging Ltd., from 1997 to 2003, a company that developed the first swallowable wireless pill camera for inspection of the intestine. He has licensed patents to a number of companies including Kimberly-Clark Corporation. Since 2014, Dr. Jacob has served as the Chief Medical Officer and a director of NanoVibronix, Inc., a medical device company using surface acoustics to prevent catheter acquired infection as well as other applications, where he served as Chief Executive Officer from 2004 to 2014. He practiced clinical gastroenterology in New York and served as Chief of Gastroenterology at St. John’s Episcopal Hospital and South Nassau Communities Hospital from 1986 to 1995, and was a Clinical Assistant Professor of Medicine at SUNY from 1983 to 1990. Dr. Jacob founded and served as Editor in Chief of Endoscopy Review and has authored numerous publications in the field of gastroenterology.

10

Dr. Jane E. B. Reusch, MD, joined the Oramed Scientific Advisory Board in February 2018. She is a distinguished academic physician-scientist-diabetologist committed to understanding and treating the vascular complications of diabetes. She is currently Professor of Medicine and Associate Director, Center for Women’s Health, at the University of Colorado at Denver and Director of the Diabetes Care Team at the Veteran’s Administration Medical Center in Denver, Colorado. Dr. Reusch has been awarded numerous NIH Research Project Grant (R01) and VA Merit grants for both basic and clinical research, leading to more than 100 peer-reviewed publications on diabetes and diabetic vascular complications. In a continuation of her life-long service to the diabetes community, Dr. Reusch is a previous ADA President for Medicine and Science.

Employees

We have been successful in retaining experienced personnel involved in our research and development program. In addition, we believe we have successfully recruited the clinical/regulatory, quality assurance and other personnel needed to advance through clinical studies or have engaged the services of experts in the field for these requirements. As of August 31, 2019, we have contracted with thirteen individuals for employment or consulting arrangements. Of our staff, four are senior management, five are engaged in research and development work, and the remaining four are involved in administration work.

Additional Information

Additional information about us is contained on our Internet website at www.oramed.com. Information on our website is not incorporated by reference into this report. On our website, under “Investors”, “SEC Filings”, we make available free of charge our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Reports filed with the SEC are made available on its website at www.sec.gov. The following Corporate Governance documents are also posted on our website: Code of Ethics, Whistleblowing Policy and the Charters for each of the Audit Committee, Compensation Committee and Nominating Committee of our Board.

An investment in our securities involves a high degree of risk. You should consider carefully the following information about these risks, together with the other information contained in this Annual Report on Form 10-K before making an investment decision. Our business, prospects, financial condition and results of operations may be materially and adversely affected as a result of any of the following risks. The value of our securities could decline as a result of any of these risks. You could lose all or part of your investment in our securities. Some of the statements in “Item 1A. Risk Factors” are forward-looking statements. The following risk factors are not the only risk factors facing our Company. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also affect our business, prospects, financial condition and results of operations.

Risks Related to Our Business

We continue, and in the future expect, to incur losses.

Successful completion of our development programs and our transition to normal operations are dependent upon obtaining necessary regulatory approvals from the FDA prior to selling our products within the United States, and foreign regulatory approvals must be obtained to sell our products internationally. There can be no assurance that we will receive regulatory approval of any of our product candidates, and a substantial amount of time may pass before we achieve a level of revenues adequate to support our operations. We also expect to incur substantial expenditures in connection with the regulatory approval process for each of our product candidates during their respective developmental periods. Obtaining marketing approval will be directly dependent on our ability to implement the necessary regulatory steps required to obtain marketing approval in the United States and in other countries. We cannot predict the outcome of these activities.

11

Based on our current cash resources and commitments, we believe we will be able to maintain our current planned development activities and the corresponding level of expenditures for at least the next 12 months, although no assurance can be given that we will not need additional funds prior to such time. If there are unexpected increases in our operating expenses, we may need to seek additional financing during the next 12 months.

We will need substantial additional capital in order to satisfy our business objectives.

To date, we have financed our operations principally through offerings of securities and we will require substantial additional financing at various intervals in order to continue our research and development programs, including significant requirements for operating expenses including intellectual property protection and enforcement, for pursuit of regulatory approvals, and for commercialization of our products. We can provide no assurance that additional funding will be available on a timely basis, on terms acceptable to us, or at all. In the event that we are unable to obtain such financing, we will not be able to fully develop and commercialize our technology. Our future capital requirements will depend upon many factors, including:

| ● | Continued scientific progress in our research and development programs, |

| ● | Costs and timing of conducting clinical trials and seeking regulatory approvals and patent prosecutions, |

| ● | Competing technological and market developments, |

| ● | Our ability to establish additional collaborative relationships, and |

| ● | Effects of commercialization activities and facility expansions if and as required. |

If we cannot secure adequate financing when needed, we may be required to delay, scale back or eliminate one or more of our research and development programs or to enter into license or other arrangements with third parties to commercialize products or technologies that we would otherwise seek to develop ourselves and commercialize ourselves. In such event, our business, prospects, financial condition and results of operations may be adversely affected as we may be required to scale-back, eliminate, or delay development efforts or product introductions or enter into royalty, sales or other agreements with third parties in order to commercialize our products.

We have a history of losses and can provide no assurance as to our future operating results.

We do not have sufficient revenues from our research and development activities to fully support our operations. Consequently, we have incurred net losses and negative cash flows since inception. We currently have only licensing revenues and no product revenues, and may not succeed in developing or commercializing any products which could generate product revenues. We do not expect to have any products on the market for several years. In addition, development of our product candidates requires a process of pre-clinical and clinical testing, during which our products could fail. We may not be able to enter into agreements with one or more companies experienced in the manufacturing and marketing of therapeutic drugs and, to the extent that we are unable to do so, we will not be able to market our product candidates. Eventual profitability will depend on our success in developing, manufacturing, and marketing our product candidates. As of August 31, 2019, August 31, 2018 and August 31, 2017, we had working capital of $28,016,000, $26,484,000 and $15,132,000, respectively, and stockholders’ equity of $19,393,000, $31,112,000 and $19,238,000, respectively. During fiscal 2019 and the fiscal years ended August 31, 2018, or fiscal 2018, and 2017, we generated revenues of $2,703,000, $2,449,000 and $2,456,000, respectively. For the period from our inception on April 12, 2002 through August 31, 2019, and for fiscal 2019, fiscal 2018 and fiscal 2017, we incurred net losses of $83,578,000, $14,355,000, $12,727,000 and $10,480,000, respectively. We may never achieve profitability and expect to incur net losses in the foreseeable future. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

We rely upon patents to protect our technology.

The patent position of biopharmaceutical and biotechnology firms is generally uncertain and involves complex legal and factual questions. We do not know whether any of our current or future patent applications will result in the issuance of any patents. Even issued patents may be challenged, invalidated or circumvented. Patents may not provide a competitive advantage or afford protection against competitors with similar technology. Competitors or potential competitors may have filed applications for, or may have received patents and may obtain additional and proprietary rights to compounds or processes used by or competitive with ours. In addition, laws of certain foreign countries do not protect intellectual property rights to the same extent as do the laws of the United States.

12

Patent litigation is becoming widespread in the biopharmaceutical and biotechnology industry and we cannot predict how this will affect our efforts to form strategic alliances, conduct clinical testing or manufacture and market any products under development. If challenged, our patents may not be held valid. We could also become involved in interference proceedings in connection with one or more of our patents or patent applications to determine priority of invention. If we become involved in any litigation, interference or other administrative proceedings, we will likely incur substantial expenses and the efforts of our technical and management personnel will be significantly diverted. In addition, an adverse determination could subject us to significant liabilities or require us to seek licenses that may not be available on favorable terms, if at all. We may be restricted or prevented from manufacturing and selling our products in the event of an adverse determination in a judicial or administrative proceeding or if we fail to obtain necessary licenses.

We may be unable to protect our intellectual property rights and we may be liable for infringing the intellectual property rights of others.

Our ability to compete effectively will depend on our ability to maintain the proprietary nature of our technologies. We currently hold several pending patent applications in the United States, Canada, Brazil, Europe, India, Hong Kong, Japan and China for our technologies covering oral administration of insulin and other proteins and oral administration of exenatide and proteins and 77 patents issued by the United States, Australian, Canadian, Chinese, Israeli, Japanese, New Zealand, South African, Russian, European, Hong Kong, Swiss, German, Spanish, French, United Kingdom, Italian, Indian, Austrian, Belgian, Irish, Swedish, Denmark, Luxembourg, Monaco, Norway and Netherlands patent offices for our technologies covering oral administration of insulin and other proteins, or for our technologies covering oral administration of exenatide, or for methods and compositions for treating diabetes. Further, we intend to rely on a combination of trade secrets and non-disclosure and other contractual agreements and technical measures to protect our rights in our technology. We intend to depend upon confidentiality agreements with our officers, directors, employees, consultants, and subcontractors, as well as collaborative partners, to maintain the proprietary nature of our technology. These measures may not afford us sufficient or complete protection, and others may independently develop technology similar to ours, otherwise avoid our confidentiality agreements, or produce patents that would materially and adversely affect our business, prospects, financial condition and results of operations. We believe that our technology is not subject to any infringement actions based upon the patents of any third parties; however, our technology may in the future be found to infringe upon the rights of others. Others may assert infringement claims against us or against companies to which we have licensed our technology, and if we should be found to infringe upon their patents, or otherwise impermissibly utilize their intellectual property, our ability to continue to use our technology could be materially restricted or prohibited. If this event occurs, we may be required to obtain licenses from the holders of this intellectual property, enter into royalty agreements, or redesign our products so as not to utilize this intellectual property, each of which may prove to be uneconomical or otherwise impossible. Licenses or royalty agreements required in order for us to use this technology may not be available on terms acceptable to us, or at all. These claims could result in litigation, which could materially adversely affect our business, prospects, financial condition and results of operations. Further, we may need to indemnify companies to which we licensed our technology in the event that such technology is found to infringe upon the rights of others.

Our commercial success will also depend significantly on our ability to operate without infringing the patents and other proprietary rights of third parties. Patent applications are, in many cases, maintained in secrecy until patents are issued. The publication of discoveries in the scientific or patent literature frequently occurs substantially later than the date on which the underlying discoveries were made and patent applications are filed. In the event of infringement or violation of another party’s patent, we may be prevented from pursuing product development or commercialization. See “Item 1. Business—Description of Business—Patents and Licenses.”

13

At present, our success depends primarily on the successful commercialization of our oral insulin capsule.

The successful commercialization of our oral insulin capsule is crucial for our success. At present, our principal product is the oral insulin capsule. Our oral insulin capsule is in a clinical development stage and faces a variety of risks and uncertainties. Principally, these risks include the following:

| ● | Future clinical trial results may show that the oral insulin capsule is not well tolerated by recipients at its effective doses or is not efficacious as compared to placebo, |

| ● | Future clinical trial results may be inconsistent with previous preliminary testing results and data from our earlier studies may be inconsistent with clinical data; similarly, we may encounter discrepancies due to evidence of treatment-by-center interaction which could cause us to exclude certain results, as happened with the results of two sites in the initial cohort of our Phase IIb trial, |

| ● | Even if our oral insulin capsule is shown to be safe and effective for its intended purposes, we may face significant or unforeseen difficulties in obtaining or manufacturing sufficient quantities or at reasonable prices, |

| ● | Our ability to complete the development and commercialization of the oral insulin capsule for our intended use is significantly dependent upon our ability to obtain and maintain experienced and committed partners to assist us with obtaining clinical and regulatory approvals for, and the manufacturing, marketing and distribution of, the oral insulin capsule on a worldwide basis, |

| ● | Even if our oral insulin capsule is successfully developed, commercially produced and receives all necessary regulatory approvals, there is no guarantee that there will be market acceptance of our product, and |

| ● | Our competitors may develop therapeutics or other treatments which are superior or less costly than our own with the result that our products, even if they are successfully developed, manufactured and approved, may not generate significant revenues. |

If we are unsuccessful in dealing with any of these risks, or if we are unable to successfully commercialize our oral insulin capsule for some other reason, it would likely seriously harm our business.

We have limited experience in conducting clinical trials.

Clinical trials must meet FDA and foreign regulatory requirements. We have limited experience in designing, conducting and managing the preclinical studies and clinical trials necessary to obtain regulatory approval for our product candidates in any country. We have entered into agreements with Integrium LLC to assist us in designing, conducting and managing our various clinical trials in the United States. Any failure of Integrium LLC or any other consultant to fulfill their obligations could result in significant additional costs as well as delays in designing, consulting and completing clinical trials on our products.

Our clinical trials may encounter delays, suspensions or other problems.

We may encounter problems in clinical trials that may cause us or the FDA or foreign regulatory agencies to delay, suspend or terminate our clinical trials at any phase. These problems could include the possibility that we may not be able to conduct clinical trials at our preferred sites, enroll a sufficient number of patients for our clinical trials at one or more sites or begin or successfully complete clinical trials in a timely fashion, if at all. Furthermore, we, the FDA or foreign regulatory agencies may suspend clinical trials at any time if we or they believe the subjects participating in the trials are being exposed to unacceptable health risks or if we or they find deficiencies in the clinical trial process or conduct of the investigation. If clinical trials of any of the product candidates fail, we will not be able to market the product candidate which is the subject of the failed clinical trials. The FDA and foreign regulatory agencies could also require additional clinical trials, which would result in increased costs and significant development delays. Our failure to adequately demonstrate the safety and effectiveness of a pharmaceutical product candidate under development could delay or prevent regulatory approval of the product candidate and could have a material adverse effect on our business, prospects, financial condition and results of operations.

14

Clinical trials of our products conducted by third parties may encounter delays, suspensions or other problems and are outside of our control.

Third parties who conduct clinical trials of our products may encounter problems that may cause delays, suspensions or other problems at any phase. These problems could include the possibility that they may not be able to conduct clinical trials at their preferred sites, enroll a sufficient number of patients for their clinical trials at one or more sites or begin or successfully complete clinical trials in a timely fashion, if at all. In addition, these third parties are not controlled by us and may conduct these trials in a manner in which we disagree or which may prove to be unsuccessful. Furthermore, domestic or foreign regulatory agencies may suspend clinical trials at any time if they believe the subjects participating in the trials are being exposed to unacceptable health risks or if they find deficiencies in the clinical trial process or conduct of the investigation. If such clinical trials conducted by third parties fail, it could have a material adverse effect on our business, prospects, financial condition and results of operations.

We can provide no assurance that our products will obtain regulatory approval or that the results of clinical studies will be favorable.

The testing, marketing and manufacturing of any of our products will require the approval of the FDA or regulatory agencies of other countries. We have completed certain non-FDA clinical trials and pre-clinical trials for our products. In addition, we have completed a Phase IIb clinical trial in patients with type 2 diabetes under an IND with the FDA and we have completed Phase IIa clinical trials of ORMD-0801 in patients with type 1 diabetes under an IND with the FDA. However, success in pre-clinical testing and early clinical trials does not ensure that later clinical trials will be successful. Even within a clinical trial there might be discrepancies from statistically significant data, as occurred at two of the sites in the initial cohort of our Phase IIb trial, which we excluded while we investigate such discrepancies. Further, a number of companies in the pharmaceutical industry have suffered significant setbacks in advanced clinical trials.

We cannot predict with any certainty the amount of time necessary to obtain regulatory approvals, including from the FDA or other foreign regulatory authorities, and whether any such approvals will ultimately be granted. In any event, review and approval by the regulatory bodies is anticipated to take a number of years. Preclinical and clinical trials may reveal that one or more of our products are ineffective or unsafe, in which event further development of such products could be seriously delayed or terminated. Moreover, obtaining approval for certain products may require the testing on human subjects of substances whose effects on humans are not fully understood or documented. Delays in obtaining necessary regulatory approvals of any proposed product and failure to receive such approvals would have an adverse effect on the product’s potential commercial success and on our business, prospects, financial condition and results of operations. In addition, it is possible that a product may be found to be ineffective or unsafe due to conditions or facts which arise after development has been completed and regulatory approvals have been obtained. In this event we may be required to withdraw such product from the market. See “Item 1. Business—Description of Business—Government Regulation.”

We are dependent upon third party suppliers of our raw materials.