UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

For the Fiscal Year Ended

OR

For the Transition Period from to

Commission File Number:

NOVAGOLD RESOURCES INC.

(Exact Name of Registrant as Specified in Its Charter)

| |

N/A |

|||

| (State or Other Jurisdiction of |

(I.R.S. Employer |

|||

|

|

|

|||

| (Address of Principal Executive Offices) |

(Zip Code) |

|||

| (

Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

| |

|

Toronto Stock Exchange |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one)

| |

Accelerated filer ☐ |

Non-accelerated filer ☐ |

| Smaller reporting company |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

Based on the last sale price on the NYSE American of the registrant’s common shares on May 31, 2019 (the last business day of the registrant’s most recently completed second fiscal quarter) of $4.05 per share, the aggregate market value of the voting common shares held by non-affiliates was approximately $

As of January 15, 2020, the registrant had

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than April 1, 2020, in connection with the registrant’s fiscal year 2019 annual meeting of shareholders, are incorporated by reference into Part III of this Annual Report on Form 10-K.

NOVAGOLD RESOURCES INC.

TABLE OF CONTENTS

Unless the context otherwise requires, the words “we,” “us,” “our,” the “Company” and “NOVAGOLD” refer to NOVAGOLD RESOURCES INC., a British Columbia corporation, and its subsidiaries as of November 30, 2019.

CURRENCY

References in this report to $ refer to United States currency and C$ to Canadian currency.

CAUTIONARY NOTE TO U.S. INVESTORS REGARDING ESTIMATES OF MEASURED, INDICATED AND INFERRED RESOURCES AND PROVEN AND PROBABLE RESERVES

We are a mineral exploration company engaged in the exploration and development of mineral properties. As used in this Annual Report on Form 10-K, the terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms as defined in accordance with Canadian National Instrument 43-101—Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (CIM)—CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended (“CIM Definition Standards”). These definitions differ from the definitions in the Securities and Exchange Commission (SEC) Industry Guide 7 (“SEC Industry Guide 7”) under the United States Securities Act of 1933, as amended (the “Securities Act”). Under SEC Industry Guide 7, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves, and the primary environmental analysis or report must be filed with the appropriate governmental authority. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in, and required to be disclosed by, NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that all or any part of a mineral deposit in these categories will ever be converted into reserves. The Company has no reserves, as that term is defined under SEC Industry Guide 7.

“Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable.

Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, SEC Industry Guide 7 normally only permits issuers to report mineralization that does not constitute “reserves” by SEC Industry Guide 7 standards as in place tonnage and grade without reference to unit measures. Accordingly, information contained in this report and the documents incorporated by reference herein contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to SEC Industry Guide 7 reporting and disclosure requirements.

The term “mineralized material” as used in this Annual Report on Form 10-K, although permissible under SEC Industry Guide 7, does not indicate “reserves” by SEC Industry Guide 7 standards. We cannot be certain that any part of the mineralized material will ever be confirmed or converted into SEC Industry Guide 7 compliant “reserves”. Investors are cautioned not to assume that all or any part of the mineralized material will ever be confirmed or converted into reserves or that mineralized material can be economically or legally extracted.

On October 31, 2018, the SEC adopted a final rule (“New Final Rule”) that will replace SEC Industry Guide 7 with new disclosure requirements that are more closely aligned with current industry and global regulatory practices and standards, including NI 43-101. Companies must comply with the New Final Rule for the company’s first fiscal year beginning on or after January 1, 2021, which for NOVAGOLD would be the fiscal year beginning December 1, 2021. While early voluntary compliance with the New Final Rule is permitted, NOVAGOLD has not elected to comply with the New Final Rule at this time.

See the “Glossary of Technical Terms” for more information regarding some of the terms used in this Cautionary Note.

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements or information within the meaning of Canadian securities laws and the United States Private Securities Litigation Reform Act of 1995 concerning anticipated results and developments in our operations in future periods, planned exploration activities, the adequacy of our financial resources and other events or conditions that may occur in the future. These forward-looking statements may include statements regarding perceived merit of properties, exploration results and budgets, mineral reserves and resource estimates, work programs, capital expenditures, operating costs, cash flow estimates, production estimates and similar statements relating to the economic viability of a project, timelines, strategic plans, including our plans and expectations relating to the Donlin Gold project, permitting and the timing thereof, market prices for precious metals, or other statements that are not statements of fact. These statements relate to analyses and other information that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. Statements concerning mineral resource estimates may also be deemed to constitute “forward-looking statements” to the extent that they involve estimates of the mineralization that will be encountered if the property is developed.

Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, assumptions or future events or performance (often, but not always, identified by words or phrases such as “expects”, “is expected”, “anticipates”, “believes”, “plans”, “projects”, “estimates”, “assumes”, “intends”, “strategy”, “goals”, “objectives”, “potential”, “possible” or variations thereof or stating that certain actions, events, conditions or results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved, or the negative of any of these terms and similar expressions) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements are based on a number of material assumptions, including those listed below, which could prove to be significantly incorrect:

| ● |

our ability to achieve production at any of our mineral exploration and development properties; |

| ● |

estimated capital costs, operating costs, production and economic returns; |

| ● |

estimated metal pricing, metallurgy, mineability, marketability and operating and capital costs, together with other assumptions underlying our resource and reserve estimates; |

| ● |

our expected ability to develop adequate infrastructure and that the cost of doing so will be reasonable; |

| ● |

assumptions that all necessary permits and governmental approvals will be obtained and the timing of such approvals; |

| ● |

assumptions made in the interpretation of drill results, the geology, grade and continuity of our mineral deposits; |

| ● |

our expectations regarding demand for equipment, skilled labor and services needed for exploration and development of mineral properties; and |

| ● |

our activities will not be adversely disrupted or impeded by development, operating or regulatory risks. |

Forward-looking statements are subject to a variety of known and unknown risks, uncertainties and other factors that could cause actual events or results to differ from those reflected in the forward-looking statements, including, without limitation:

| ● |

uncertainty of whether there will ever be production at our mineral exploration and development properties; |

| ● |

our history of losses and expectation of future losses; |

| ● |

risks related to our ability to finance the development of our mineral properties through external financing, strategic alliances, the sale of property interests or otherwise; |

| ● |

uncertainty of estimates of capital costs, operating costs, production and economic returns; |

| ● |

commodity price fluctuations; |

| ● |

risks related to market events and general economic conditions; |

| ● |

risks related to the third parties on which we depend for our exploration and development activities; |

| ● |

dependence on cooperation of joint venture partners in exploration and development of properties; |

|

| ● | risks related to opposition to our operations at our mineral exploration and development properties from non-governmental organizations or civil society; |

| ● |

the risk that permits and governmental approvals necessary to develop and operate mines on our properties will not be available on a timely basis, subject to reasonable conditions, or at all; |

| ● |

risks and uncertainties relating to the interpretation of drill results, the geology, grade and continuity of our mineral deposits; |

| ● |

uncertainties relating to the assumptions underlying our resource and reserve estimates, such as metal pricing, metallurgy, mineability, marketability and operating and capital costs; |

| ● |

risks related to lack of infrastructure required to develop, construct, and operate our mineral properties; |

| ● |

uncertainty related to title to our mineral properties; |

| ● |

mining and development risks, including risks related to infrastructure, accidents, equipment breakdowns, labor disputes or other unanticipated difficulties with, or interruptions in, development, construction or production; |

| ● |

competition in the mining industry; |

| ● |

risks related to governmental regulation and permits, including environmental regulation; |

| ● |

risks related to our largest shareholder; |

| ● |

risks related to conflicts of interests of some of the directors and officers of the Company; |

| ● |

risks related to the need for reclamation activities on our properties and uncertainty of cost estimates related thereto; |

| ● |

credit, liquidity, interest rate and currency risks; |

| ● |

risks related to increases in demand for equipment, skilled labor and services needed for exploration and development of mineral properties, and related cost increases; |

| ● |

our need to attract and retain qualified management and technical personnel; |

| ● |

uncertainty as to the outcome of potential litigation; |

|

| ● | risks related to information technology systems; | |

| ● | risks related to the Company’s status as a “passive foreign investment company” in the United States; and |

| ● |

risks related to global climate change. |

This list is not exhaustive of the factors that may affect any of our forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and our actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in this Annual Report on Form 10-K under the heading “Risk Factors” and elsewhere.

Our forward-looking statements contained in this Annual Report on Form 10-K are based on the beliefs, expectations and opinions of management as of the date of this report. We do not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change, except as required by law. For the reasons set forth above, investors should not place undue reliance on forward-looking statements.

GLOSSARY OF TECHNICAL TERMS

The following technical terms defined in this section are used throughout this Annual Report on Form 10-K.

| alluvial |

A placer formed by the action of running water, as in a stream channel or alluvial fan; also said of the valuable mineral (e.g. gold or diamond) associated with an alluvial placer. |

|

| arsenopyrite |

An arsenic iron sulfide mineral (FeAsS). |

|

| assay |

A metallurgical analysis used to determine the quantity (or grade) of various metals in a sample. |

|

| concentrate |

A clean product recovered in flotation, which has been upgraded sufficiently for downstream processing or sale. |

|

| cut-off grade |

When determining economically viable mineral reserves, the lowest grade of mineralized material that can be mined and processed at a profit. |

|

| cyanidation |

A metallurgical technique, using a dilute cyanide solution, for extracting gold from ore by dissolving the gold into solution. |

|

| dike |

A tabular igneous intrusion that cuts across the bedding of the host rock. |

|

| doré |

A semi-pure alloy of gold and silver. |

|

| electrowinning |

The deposition of gold from solution to cathodes by passing electric current from anodes through gold-bearing solution. |

|

| flotation |

A process used for the concentration of minerals, especially within base metal systems. |

|

| geotechnical |

Said of tasks or analysis that provide representative data of the geological rock quality in a known volume. |

|

| grade |

Quantity of metal or mineral per unit weight of host rock. |

|

| greywacke |

A variety of sandstone generally characterized by its hardness, dark color, and poorly sorted angular grains of quartz, feldspar, and small rock fragments set in a compact, clay-fine matrix. |

|

| host rock |

A body of rock serving as a host for other rocks or for mineral deposits. |

|

| hydrothermal |

Pertaining to hot aqueous solutions of magmatic origin which may transport metals and minerals in solution. |

|

| intrusive |

Said of igneous rock formed by the consolidation of magma intruded into other rocks. |

|

| mafic |

Igneous rocks composed mostly of dark, iron- and magnesium-rich minerals. |

|

| massive |

Said of a mineral deposit, especially of sulfides, characterized by a great concentration of mineralization in one place, as opposed to a disseminated or vein-like deposit. |

|

| mineral |

A naturally formed chemical element or compound having a definite chemical composition and, usually, a characteristic crystal form. |

|

| mineral deposit |

A mineralized body which has been physically delineated by sufficient drilling, trenching, and/or underground work, and found to contain a sufficient average grade of metal or metals to warrant further exploration and/or development expenditures. |

|

| mineralization |

A natural occurrence in rocks or soil of one or more yielding minerals or metals. |

|

| net present value (NPV) |

The sum of the value on a given date of a series of future cash payments and receipts, discounted to reflect the time value of money and other factors such as investment risk. |

|

| ore |

Rock containing metallic or non-metallic materials that can be mined and processed at a profit. |

|

| placer |

An alluvial deposit of sand and gravel, which may contain valuable metals. |

|

| porphyry |

An igneous rock of any composition that contains conspicuous phenocrysts (large crystals or mineral grains) in a fine-grained groundmass. |

|

| pyrite |

An iron sulfide mineral (FeS2), the most common naturally occurring sulfide mineral. |

|

| pyrrhotite |

An unusual, generally weakly magnetic, iron sulfide mineral with varying iron content (Fe1-x S (x=0 to 0.2)). |

|

| reverse circulation (RC) |

A type of drilling using dual-walled drill pipe in which the material drilled, water and mud are circulated up the center pipe while air is blown down the outside pipe. |

| realgar |

An arsenic sulfide mineral (As4 S4). |

|

| reclamation |

Restoration of mined land to original contour, use, or condition where possible. |

|

| rhyodacite |

A volcanic, high-silica rock composed of mostly quartz and feldspar. |

|

| sedimentary |

Said of rock formed at the Earth’s surface from solid particles, whether mineral or organic, which have been moved from their position of origin and re-deposited, or chemically precipitated. |

|

| shale |

A fine-grained detrital (transported by wind, water, or ice) sedimentary rock, formed by the consolidation of clay, silt, or mud. |

|

| sill |

An intrusive sheet of igneous rock of roughly uniform thickness that has been forced between the bedding planes of existing rock. |

|

| stibnite |

An antimony sulfide mineral (Sb2S3). |

|

| strike |

The direction, or bearing from true north, of a vein or rock formation measured on a horizontal surface. |

|

| sulfide |

A compound of sulfur and some other metallic element. |

|

| syngenetic |

Relating to or denoting a mineral deposit or formation produced at the same time as the host rock. |

|

| tailings |

Uneconomic material produced by a mineral processing plant which is disposed of in a manner meeting government regulation and which may involve a permanent impoundment facility or which may involve the discharge of material to the environment in a manner regulated by the government authority. |

|

| vein |

A thin, sheet-like crosscutting body of hydrothermal mineralization, principally quartz. |

|

| waste rock |

Barren or submarginal rock that has been mined but is not of sufficient value to warrant treatment and is therefore removed ahead of the milling processes. |

Canadian NI 43-101 Definitions:

Terms defined in National Instrument 43-101 – Standards of Disclosure for Mineral Projects. The definitions of the terms “Mineral Reserve”, “Mineral Resource”, “Mining Studies”, and “Qualified Person” also refer to the CIM Definition Standards, where they are further defined.

Advanced Property

A property that has Mineral Reserves or Mineral Resources, the potential economic viability of which is supported by a Preliminary Economic Assessment, a Pre-Feasibility Study or a Feasibility Study.

Disclosure

Any oral statement or written disclosure made by or on behalf of an issuer and intended to be, or reasonably likely to be, made available to the public in a jurisdiction of Canada, whether or not filed under securities legislation, but does not include written disclosure that is made available to the public only by reason of having been filed with a government or agency of government pursuant to a requirement of law other than securities legislation.

Early Stage Exploration Property

A property for which the technical report being filed has no current mineral resources or mineral reserves defined and no drilling or trenching proposed.

Effective Date

With reference to a technical report, the date of the most recent scientific or technical information included in the technical report.

Exploration Information

Geological, geophysical, geochemical, sampling, drilling, trenching, analytical testing, assaying, mineralogical, metallurgical and other similar information concerning a particular property that is derived from activities undertaken to locate, investigate, define or delineate a mineral prospect or mineral deposit.

Mineral Project

Any exploration, development or production activity, including a royalty or similar interest in these activities, in respect of diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial minerals.

Preliminary Economic Assessment

A study, other than a Pre-Feasibility or Feasibility Study, that includes an economic analysis of the potential viability of Mineral Resources.

Professional Association

A self-regulatory organization of engineers, geoscientists, or both engineers and geoscientists that is given authority or recognition by statute in a jurisdiction of Canada or a foreign association that is generally accepted within the international mining community as a reputable professional association; admits individuals on the basis of their academic qualifications, experience, and ethical fitness; requires compliance with the professional standards of competence and ethics established by the organization; requires or encourages continuing professional development; and has and applies disciplinary powers, including the power to suspend or expel a member regardless of where the member practices or resides.

Qualified Person

An individual who is an engineer or geoscientist with a university degree, or equivalent accreditation, in an area of geoscience, or engineering, relating to mineral exploration or mining; has at least five years of experience in mineral exploration, mine development or operation, or mineral project assessment, or any combination of these, that is relevant to his or her professional degree or area of practice; has experience relevant to the subject matter of the mineral project and the technical report; is in good standing with a professional association; and in the case of a professional association in a foreign jurisdiction, has a membership designation that requires attainment of a position of responsibility in their profession that requires the exercise of independent judgement and requires a favourable confidential peer evaluation of the individual’s character, professional judgement, experience, and ethical fitness or requires a recommendation for membership by at least two peers, and demonstrated prominence or expertise in the field of mineral exploration or mining.

Quantity

Either tonnage or volume, depending on which term is the standard in the mining industry for the type of mineral.

SEC Industry Guide 7

The mining industry guide entitled “Description of Property by Issuers Engaged or to be Engaged in Significant Mining Operations” contained in the Securities Act Industry Guides published by the SEC, as amended.

Technical Report

A report prepared and filed in accordance with NI 43-101 and Form 43-101F1 Technical Report that includes, in summary form, all material scientific and technical information in respect of the subject property as of the effective date of the technical report.

Written Disclosure

Includes any writing, picture, map, or other printed representation whether produced, stored or disseminated on paper or electronically, including websites.

Mineral Resource

The terms “Mineral Resource”, “Inferred Mineral Resource”, “Indicated Mineral Resource”, and “Measured Mineral Resource” have the meanings ascribed to those terms by CIM, as the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by CIM Council, as amended.

Mineral Reserve, Probable Mineral Reserve, and Proven Mineral Reserve

The terms “Mineral Reserve”, “Probable Mineral Reserve”, and “Proven Mineral Reserve” have the meanings ascribed to those terms by CIM, as the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by CIM Council, as amended.

Mining Studies

In this Instrument, the terms “Preliminary Feasibility Study”, “Pre-Feasibility Study” and “Feasibility Study” have the meanings ascribed to those terms by CIM, as the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by CIM Council, as amended.

Independence

In this Instrument, a Qualified Person is independent of an issuer if there is no circumstance that, in the opinion of a reasonable person aware of all relevant facts, could interfere with the Qualified Person’s judgement regarding the preparation of the technical report.

CIM Definition Standards for Mineral Resources and Mineral Reserves (“CIM Definition Standards”), adopted by CIM Council on May 10, 2014:

Qualified Person

Mineral Resource and Mineral Reserve estimates and any supporting Technical Reports must be prepared by or under the direction of a Qualified Person, as that term is defined in NI 43-101.

Pre-Feasibility Study (Preliminary Feasibility Study)

A Pre-Feasibility Study is a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the Modifying Factors and the evaluation of any other relevant factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the Mineral Resource may be converted to a Mineral Reserve at the time of reporting. A Pre-Feasibility Study is at a lower confidence level than a Feasibility Study.

Feasibility Study

A Feasibility Study is a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable Modifying Factors together with any other relevant operational factors and detailed financial analysis, that are necessary to demonstrate, at the time of reporting, that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a Pre-Feasibility Study.

Mineral Resource

A Mineral Resource is a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction.

The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

Inferred Mineral Resource

An Inferred Mineral Resource is that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity.

An Inferred Mineral Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of Inferred Mineral Resources could be upgraded to Indicated Mineral Resources with continued exploration.

Indicated Mineral Resource

An Indicated Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics, are estimated with sufficient confidence to allow the application of Modifying Factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit.

Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation.

An Indicated Mineral Resource has a lower level of confidence than that applying to a Measured Mineral Resource and may only be converted to a Probable Mineral Reserve.

Measured Mineral Resource

A Measured Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit.

Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation.

A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated Mineral Resource or an Inferred Mineral Resource. It may be converted to a Proven Mineral Reserve or to a Probable Mineral Reserve.

Modifying Factors

Modifying Factors are considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social, and governmental factors.

Mineral Reserve

A Mineral Reserve is the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility level as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified.

The reference point at which Mineral Reserves are defined, usually the point where the ore is delivered to the processing plant, must be stated. It is important that, in all situations where the reference point is different, such as for a saleable product, a clarifying statement is included to ensure that the reader is fully informed as to what is being reported.

The public disclosure of a Mineral Reserve must be demonstrated by a Pre-Feasibility Study or Feasibility Study.

Probable Mineral Reserve

A Probable Mineral Reserve is the economically mineable part of an Indicated, and, in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve.

Proven Mineral Reserve (Proved Mineral Reserve)

A Proven Mineral Reserve is the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the Modifying Factors.

SEC Industry Guide 7 Definitions:

U.S. reporting guidelines that apply to registrants engaged or to be engaged in significant mining operations.

Exploration stage

An Exploration Stage issuer is one engaged in the search for mineral deposit (reserves) which are not in either the development or production stage.

Development stage

A Development Stage issuer is one which is engaged in the preparation of an established commercially mineable deposit (reserves) for its extraction but which is not yet in production. This stage occurs after completion of a feasibility study.

Production stage

A Production Stage issuer is actively engaged in the exploitation of a mineral deposit (reserve).

Mineralized material

Refers to material that is not included in the reserve as it does not meet all of the criteria for adequate demonstration for economic or legal extraction.

Probable (Indicated) reserve

Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven (measured) reserves, is high enough to assume continuity between points of observation.

Proven (Measured) reserve

Reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well-established.

Reserve

That part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. Reserves must be supported by a feasibility study done to bankable standards that demonstrates the economic extraction. (“Bankable standards” implies that the confidence attached to the costs and achievements developed in the study is sufficient for the project to be eligible for external debt financing.) A reserve includes adjustments to the in-situ tonnes and grade to include diluting materials and allowances for losses that might occur when the material is mined.

NOVAGOLD RESOURCES INC.

| Item 1. | Business |

Overview

We operate in the gold mining industry, primarily focused on advancing permitting of the Donlin Gold project in Alaska. The Donlin Gold project is held by Donlin Gold LLC (“Donlin Gold”), a limited liability company owned equally by wholly-owned subsidiaries of NOVAGOLD and Barrick Gold Corporation (“Barrick”).

We do not produce gold or any other minerals, and do not currently generate operating earnings. Funding to explore our mineral properties and to operate the Company was acquired primarily through previous equity financings consisting of public offerings of our common shares and warrants and through debt financing consisting of convertible notes, and the sale of assets. We expect to continue to raise capital through additional equity and/or debt financings, through the exercise of stock options, and otherwise.

We were incorporated by memorandum of association on December 5, 1984, under the Companies Act (Nova Scotia) as 1562756 Nova Scotia Limited. On January 14, 1985, we changed our name to NovaCan Mining Resources (l985) Limited and on March 20, 1987, we changed our name to NOVAGOLD RESOURCES INC. On May 29, 2013, our shareholders approved the continuance of the corporation into British Columbia. Subsequently, we filed the necessary documents in Nova Scotia and British Columbia and we continued under the Business Corporations Act (British Columbia) effective as of June 10, 2013. The current addresses, telephone and facsimile numbers of our offices are:

| Executive office |

Corporate office |

| 201 South Main Street, Suite 400 |

400 Burrard Street, Suite 1860 |

| Salt Lake City, UT, USA 84111 |

Vancouver, BC, Canada V6C 3A6 |

| Telephone (801) 639-0511 |

Toll free (866) 669-6227 |

| Facsimile (801) 649-0509 |

Facsimile (604) 669-6272 |

NOVAGOLD RESOURCES INC.

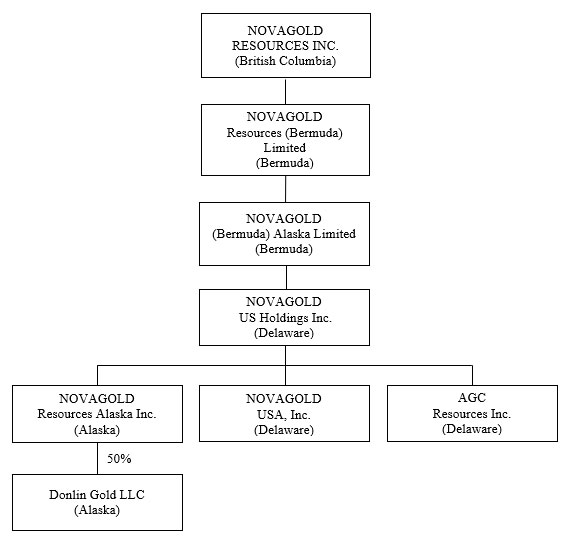

Corporate Structure

As of November 30, 2019, we had the following material, direct and indirect, wholly-owned subsidiaries: NOVAGOLD Resources Alaska, Inc., NOVAGOLD US Holdings Inc., NOVAGOLD USA, Inc., AGC Resources Inc, NOVAGOLD (Bermuda) Alaska Limited and NOVAGOLD Resources (Bermuda) Limited.

The following chart depicts the corporate structure of the Company together with the jurisdiction of incorporation of each of our material subsidiaries and related holding companies. All ownership is 100% unless otherwise indicated.

NOVAGOLD RESOURCES INC.

Employees

On November 30, 2019, we had 12 full-time employees. We also use consultants with specific skills to assist with various aspects of project evaluation, engineering and corporate governance.

Recent Developments

Donlin Gold Project

Donlin Gold LLC continues to support the Alaska Department of Natural Resources (ADNR) to advance permits and certificates for the project.

ADNR’s approval of the Alaska Dam Safety certificates for the tailings storage facility and water retention and diversion structures requires a thorough multi-year stepwise process to deliver a final construction package to ADNR. During July 2019, Donlin Gold commenced a site investigation program in support of advancement of dam engineering from a feasibility level to a final construction package. The site investigation information will support a preliminary design package, detailed design package and ultimately the final construction package, each of which will be submitted to ADNR for final approval and issuance of the dam safety certificates. This program consists of geotechnical core drilling, test pits, overburden drilling, packer tests, hydrogeologic test well installation and pumping tests, and geophysical surveys. Safety training and camp preparations were completed in the third quarter. Due to wildfires that affected the project area, the program was temporarily suspended in July for a period of five weeks, as all personnel were safely moved as a precautionary measure and to accommodate firefighting operations. There was no damage to Donlin Gold structures and equipment and the camp reopened in September.

ADNR’s Division of Mining, Land, and Water (DMLW) issued the easement land leases, land use permits, and material site authorizations for the proposed transportation facilities, and easement for the fiber optic cable on State lands on January 2, 2020, following the issuance of the preliminary decisions on January 28, 2019 and the close of the public comment period for these decisions in March 2019. ADNR’s Division of Oil and Gas (DOG), is finalizing the ROW authorizations for the natural gas pipeline, following the issuance of the preliminary decision in March 2019.

In 2018, Earthjustice, on behalf of Orutsararmiut Native Council (ONC), Akiak Native Community IRA Council, Organized Village of Kwethluk, Native Village of Kwigillingok, Chuloonawick Tribal Council, and the Yukon-Kuskokwim River Alliance, requested an informal review of the State of Alaska’s 401 certification (the “Certification”) by the Director of the Division of Water in the Alaska Department of Environmental Conservation (ADEC). In October 2018, the Director responded to the request by deciding to conduct the informal review and reissued the Certification on April 4, 2019. On April 24, 2019, Earthjustice requested a second informal review of the Certification and the request was granted by ADEC on May 4, 2019. A decision on the second informal review of the Certification is expected by the end of the first quarter of 2020.

The final approvals of the Donlin Gold Reclamation and Closure Plan and final Waste Management Permit were issued on January 18, 2019. On February 7, 2019, Earthjustice on behalf of ONC, Akiak Native Community, Chefornak Traditional Council, Chevak Traditional Council, Chuloonawick Native Village, Native Village of Eek, Kasigluk Traditional Council, Kongiganak Traditional Council, Organized Village of Kwethluk, Native Village of Kwigillingok, Native Village of Nightmute, Sleetmute Traditional Council, Tuluksak Native Community, and Native Village of Tununak, filed an administrative appeal of the Reclamation and Closure Plan Approval. ADNR denied the appeal of the Donlin Gold Reclamation and Closure Plan on December 31, 2019 and affirmed DMLW’S original decision. Additionally, Earthjustice, representing the same tribal entities in the appeal of the Reclamation and Closure Plan Approval, requested an informal review of the Waste Management Permit, which was completed by ADEC’s Division of Water on June 25, 2019 with their original decision upheld and with no further appeal.

Donlin Gold LLC, with support from the project owners (NOVAGOLD and Barrick) are committed to growing strong and collaborative working relationships to preserve traditional lifestyles and support economic development for the benefit of Calista and TKC shareholders (owners of the mineral and surface rights, respectively) and the Yukon-Kuskokwim (Y-K) region. Donlin Gold LLC and our Native Corporation partners held more than 200 engagement meetings in 2019 with individual stakeholders and community organizations and remained actively engaged in environmental sustainability projects in the Y-K region.

NOVAGOLD and Barrick continue to study ways to improve the project’s value and to reduce initial capital outlays through enhanced project design and execution, engagement of third-party operators for certain activities, and potential for future financing of some capital-intensive infrastructure. To date, these additional studies have identified key areas that have the potential to add value and maximize the future opportunity and longevity of the project. In 2020, Donlin Gold LLC has envisioned a drilling program in the resource area to follow-up on recent drilling and technical work. NOVAGOLD and Barrick will take all this work into account before reaching a construction decision and will advance the Donlin Gold project in a financially-disciplined manner with a strong focus on environmental stewardship and social responsibility.

NOVAGOLD RESOURCES INC.

The Donlin Gold LLC board must approve a construction program and budget before the Donlin Gold project can be developed. The timing of the required engineering work and the Donlin Gold LLC board’s approval of a construction program and budget, the receipt of all required governmental permits and approvals, and the availability of financing, commodity price fluctuations, risks related to market events and general economic conditions, among other factors, will affect the timing of and whether to develop the Donlin Gold project. Among other reasons, project delays could occur as a result of public opposition, litigation challenging permit decisions, requests for additional information or analysis, limitations in agency staff resources during regulatory review and permitting, or project changes made by Donlin Gold LLC.

For further information, see section Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, below.

Reclamation

We will generally be required to mitigate long-term environmental impacts by stabilizing, contouring, re-sloping and re-vegetating various portions of a site after mining and mineral processing operations are completed. These reclamation efforts will be conducted in accordance with detailed plans, which must be reviewed and approved by the appropriate regulatory agencies. In addition, financial assurance acceptable to the regulatory authority with jurisdiction over reclamation must be provided in an amount that the authority determines to be sufficient to allow the authority to implement the reclamation plan in the event that the project owners fail to complete the work as provided in the plan.

Government and Environmental Regulations

Our exploration and development activities are subject to various national, state, provincial and local laws and regulations in the United States and Canada, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances, disclosure requirements and other matters. We have obtained or have pending applications for those licenses, permits or other authorizations currently required to conduct our exploration and development programs. We believe that we are in compliance in all material respects with applicable mining, health, safety and environmental statutes and regulations in the United States and Canada. There are no current orders or directions relating to us with respect to the foregoing laws and regulations. For a more detailed discussion of the various government laws and regulations applicable to our operations and potential negative effects of these laws and regulations, see section Item 1A, Risk Factors, below.

Competition

We compete with other mineral resource exploration and development companies for financing, technical expertise and the acquisition of mineral properties. Many of the companies with whom we compete have greater financial and technical resources. Accordingly, these competitors may be able to spend greater amounts on the acquisition, exploration and development of mineral properties. This competition could adversely impact our ability to finance further exploration and to obtain the financing necessary for us to develop our mineral properties.

Availability of Raw Materials and Skilled Employees

Most aspects of our business require specialized skills and knowledge. Such skills and knowledge include the areas of geology, drilling, metallurgy, mine planning, logistical planning, preparation of feasibility studies, permitting, construction and operation of a mine, financing, legal and accounting. Historically, we have found that we can locate and retain appropriate employees and consultants and we believe we will continue to be able to do so.

All of the raw materials we require to carry on our business are readily available through normal supply or business contracting channels in the United States and Canada. Historically, we have been able to secure the appropriate equipment and supplies required to conduct our contemplated programs. As a result, we do not believe that we will experience any shortages of required equipment or supplies in the foreseeable future.

Seasonality

Our business is seasonal as our mineral exploration and development activities take place in southwestern Alaska. Due to the northern climate, work on the Donlin Gold project can be limited due to excessive snow cover and cold temperatures. In general, surface work often is limited to late spring through early fall, although work in some locations is more readily and efficiently completed during the winter months when the ground is frozen.

NOVAGOLD RESOURCES INC.

Gold Price History

The price of gold is volatile and is affected by numerous factors, all of which are beyond our control, such as the sale or purchase of gold by various central banks and financial institutions, inflation, recession, fluctuation in the relative values of the U.S. dollar and foreign currencies, changes in global and regional gold demand, in addition to international and national political and economic conditions.

The following table presents the high, low and average afternoon fixed prices in U.S. dollars for an ounce of gold on the London Bullion Market over the past five calendar years:

| Year |

High |

Low |

Average |

|||||||||

| 2015 |

$ | 1,296 | $ | 1,049 | $ | 1,160 | ||||||

| 2016 |

$ | 1,366 | $ | 1,077 | $ | 1,251 | ||||||

| 2017 |

$ | 1,346 | $ | 1,151 | $ | 1,257 | ||||||

| 2018 |

$ | 1,355 | $ | 1,178 | $ | 1,269 | ||||||

| 2019 |

$ | 1,546 | $ | 1,271 | $ | 1,392 | ||||||

| 2020 (to January 15) |

$ | 1,573 | $ | 1,527 | $ | 1,554 | ||||||

| Data Source: www.kitco.com | ||||||||||||

Available Information

We make available, free of charge, on or through our website at www.novagold.com, our Annual Report on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”). These reports are also available at the SEC website at www.sec.gov. Our website and the information contained therein or connected thereto are not intended to be, and are not incorporated into this Annual Report on Form 10-K.

| Risk Factors |

You should carefully consider the following risk factors in addition to the other information included in this Annual Report on Form 10-K. Each of these risk factors could adversely affect our business, operating results and financial condition, as well as adversely affect the value of an investment in our common shares. The risks described below are not the only ones facing the Company. Additional risks that we are not presently aware of, or that we currently believe are immaterial, may also adversely affect our business, operating results and financial condition. We cannot assure you that we will successfully address these risks and caution that other unknown risks may exist or may arise that may affect our business.

An investment in our securities is speculative and involves a high degree of risk due to the nature of our business and the present stage of exploration and development of our mineral properties. The following risk factors, as well as risks not currently known to us, could materially adversely affect our future business, operations and financial condition and could cause them to differ materially from the estimates described in the forward-looking statements relating to us.

Risks Related to Our Business

We have no history of commercially producing precious metals from our mineral exploration properties and there can be no assurance that we will successfully establish mining operations or profitably produce precious metals.

None of our mineral properties are in production, we have no history of commercially producing precious metals from our current portfolio of mineral properties, and we have no ongoing mining operations or revenue from mining operations. Mineral exploration and development has a high degree of risk and few properties that are explored are ultimately developed into producing mines. None of our mineral properties are currently under construction. The future development of any mineral properties found to be economically feasible will require obtaining permits and financing and the construction and operation of mines, processing plants and related infrastructure. As a result, we are subject to all of the risks associated with establishing new mining operations and business enterprises, including:

| ● |

the need to obtain necessary environmental and other governmental approvals and permits, and the timing and conditions of those approvals and permits; |

| ● |

the availability and cost of funds to finance construction and development activities; |

| ● |

the timing and cost, which can be considerable, of the construction of mining and processing facilities as well as related infrastructure; |

| ● |

potential opposition from non-governmental organizations, environmental groups or local groups which may delay or prevent development activities; |

NOVAGOLD RESOURCES INC.

| ● |

potential increases in construction and operating costs due to changes in the cost of labor, fuel, power, materials and supplies, services, and foreign exchange rates; |

| ● |

the availability and cost of skilled labor and mining equipment; and |

| ● |

the availability and cost of appropriate smelting and/or refining arrangements. |

The costs, timing and complexities of mine construction and development are increased by the remote location of our mineral properties, with additional challenges related thereto, including access, water and power supply, and other support infrastructure. Cost estimates may increase significantly as more detailed engineering work and studies are completed on a project. New mining operations commonly experience unexpected costs, problems and delays during development, construction, and mine start-up. In addition, delays in the commencement of mineral production often occur. Accordingly, there are no assurances that our activities will result in profitable mining operations, or that we will successfully establish mining operations, or profitably produce precious metals at any of our mineral properties.

In addition, there is no assurance that our mineral exploration activities will result in any discoveries of new ore bodies. If further mineralization is discovered there is also no assurance that the mineralized material would be economical for commercial production. Discovery of mineral deposits is dependent upon a number of factors and significantly influenced by the technical skill of the exploration personnel involved. The commercial viability of a mineral deposit is also dependent upon a number of factors which are beyond our control, including the attributes of the deposit, commodity prices, government policies and regulation, and environmental protection requirements.

We have a history of net losses and expect losses to continue for the foreseeable future.

We have a history of net losses and we expect to incur net losses for the foreseeable future. None of our mineral properties have advanced to the commercial production stage and we have no history of earnings or cash flow from operations. We expect to continue to incur net losses unless and until such time the Donlin Gold project enters into commercial production and generates sufficient revenues to fund continuing operations. The development of our mineral properties to achieve production will require the commitment of substantial financial resources. The amount and timing of expenditures will depend on a number of factors, including the progress of ongoing exploration and development, the results of consultants’ analyses and recommendations, the rate at which operating losses are incurred, the process of obtaining required government permits and approvals, the availability and cost of financing, the participation of our partners, and the execution of any sale or joint venture agreements with strategic partners. These factors, and others, are beyond our control. There is no assurance that we will be profitable in the future.

We have a limited property portfolio.

At present, our only material mineral property is the interest that we hold in the Donlin Gold project. Unless we acquire or develop additional mineral properties, we will be solely dependent upon this property. If no additional mineral properties are acquired by us, any adverse development affecting our operations and further development at the Donlin Gold project may have a material adverse effect on our financial condition and results of operations.

Our ability to continue the exploration, permitting, development, and construction of the Donlin Gold project, and to continue as a going concern, will depend in part on our ability to obtain suitable financing.

We have limited financial resources. We will need external financing to develop and construct the Donlin Gold project. On December 5, 2011, we announced the total capital cost estimate for the Donlin Gold project was approximately $6.7 billion including costs related to the natural gas pipeline (100% basis). Our failure to obtain sufficient financing could result in the delay or indefinite postponement of exploration, development, construction, or production at the Donlin Gold project. The cost and terms of such financing may significantly reduce the expected benefits from development of the Donlin Gold project and/or render such development uneconomic. There can be no assurance that additional capital or other types of financing will be available when needed or that, if available, the terms of such financing will be favorable. Our failure to obtain financing could have a material adverse effect on our growth strategy and results of operations and financial condition.

We intend to fund our business plan from working capital, the proceeds of financings, and the proceeds received from the sale of our interest in the Galore Creek project. In the future, our ability to continue our exploration, permitting, development, and construction activities, if any, will depend in part on our ability to obtain suitable financing. If we raise additional funding by issuing additional equity securities or other securities that are convertible into equity securities, such financings may substantially dilute the interest of existing or future shareholders. Sales or issuances of a substantial number of securities, or the perception that such sales could occur, may adversely affect the prevailing market price for our common shares. With any additional sale or issuance of equity securities, investors will suffer dilution of their voting power and may experience dilution in earnings per share.

NOVAGOLD RESOURCES INC.

There can be no assurance that we will commence production at any of our mineral properties or generate sufficient revenues to meet our obligations as they become due or obtain necessary financing on acceptable terms, if at all. Our failure to meet our ongoing obligations on a timely basis could result in the loss or substantial dilution of our interests (as existing or as proposed to be acquired) in our mineral properties. In addition, should we incur significant losses in future periods, we may be unable to continue as a going concern, and realization of assets and settlement of liabilities in other than the normal course of business may be at amounts materially different than our estimates.

Actual capital costs, operating costs, production and economic returns may differ significantly from those we have anticipated and there are no assurances that any future development activities will result in profitable mining operations.

The capital costs to take our projects into production may be significantly higher than anticipated. On December 5, 2011, we announced the total capital cost estimate for the Donlin Gold project of approximately $6.7 billion, including costs related to the natural gas pipeline (100% basis). The previous capital cost estimate for the project released in April 2009 was $4.5 billion, which did not include the cost of a natural gas pipeline. Conditions may have changed since the Donlin Gold FS (as defined below) was completed and the results of that study may no longer reflect an accurate economic assessment of the Donlin Gold project.

None of our mineral properties have an operating history upon which we can base estimates of future operating costs. Decisions about the development of these and other mineral properties will ultimately be based upon feasibility studies. Feasibility studies derive estimates of cash operating costs based upon, among other things:

| ● |

anticipated tonnage, grades and metallurgical characteristics of the ore to be mined and processed; |

| ● |

anticipated recovery rates of gold and other precious metals from the ore; |

| ● |

cash operating costs of comparable facilities and equipment; and |

| ● |

anticipated climatic conditions. |

Capital costs, operating costs, production and economic returns, and other estimates contained in studies or estimates prepared by or for us may differ significantly from those anticipated by our current studies and estimates, and there can be no assurance that the capital costs incurred to construct and the operating costs incurred in operating the Donlin Gold project will not be higher than currently anticipated.

Changes in the market price of gold, which in the past has fluctuated widely, affect our financial condition.

Our profitability and long-term viability will depend, in large part, upon the market price of gold that may be produced from our Donlin Gold project. The market price of gold is volatile and is impacted by numerous factors beyond our control, including:

| ● |

global or regional consumption patterns; |

| ● |

expectations with respect to the rate of inflation; |

| ● |

the relative strength of the U.S. dollar and certain other currencies; |

| ● |

interest rates; |

| ● |

global or regional political or economic conditions, including interest rates and currency values; |

| ● |

supply and demand for jewelry and industrial products containing gold; and |

| ● |

sales or purchases by central banks and other holders, speculators and producers of gold in response to any of the above factors. |

We cannot predict the effect of these factors on gold prices. A decrease in the market price of gold could affect our ability to finance the development of the Donlin Gold project, which would have a material adverse effect on our financial condition and results of operations. There can be no assurance that the market price of gold will remain at current levels or that such prices will improve. In particular, an increase in worldwide supply, and consequent downward pressure on prices, may result over the longer term from increased production from the development of new or expansion of existing mines. There is no assurance that if commercial quantities of gold are discovered, that a profitable market may exist or continue to exist for a production decision to be made or for the ultimate sale of gold.

General economic conditions may adversely affect our growth, future profitability and ability to finance.

Some key impacts which can contribute to financial market turmoil potentially impacting the mining industry include contraction in credit markets resulting in a widening of credit risk, imposition of trade tariffs among various countries, devaluations, high volatility in global equity, commodity, foreign exchange and precious metal markets and a lack of market liquidity. The prices of gold and gold mining company equities have experienced significant volatility over the past few years.

NOVAGOLD RESOURCES INC.

A worsening of gold prices or tightening of credit in the financial markets or other economic conditions, including but not limited to, consumer spending, employment rates, business conditions, inflation, fuel and energy costs, consumer debt levels, lack of available credit, the state of the financial markets, interest rates and tax rates, may adversely affect our ability to finance development and construction of the Donlin Gold project. Specifically:

| ● |

global economic conditions could make other investment sectors more attractive, thereby affecting the cost and availability of financing to us and our ability to achieve our business plan; |

| ● |

the imposition of protectionist or retaliatory trade tariffs by countries may impact our ability to import materials needed to construct our projects or conduct our operations, or to export our products, at prices that are economically feasible for our operations, or at all; |

| ● |

the volatility of metal prices would impact the economic viability of our mineral properties and any future revenues, profits, losses and cash flow; |

| ● |

negative economic pressures could adversely impact demand for future production from our mineral properties; |

| ● |

construction related costs could increase and adversely affect the economics of our projects; |

| ● |

volatile energy, commodity and consumables prices and currency exchange rates would impact our future production costs; and |

| ● |

the devaluation and volatility of global stock markets would impact the valuation of our equity and other securities. |

We are dependent on a third party that participates in exploration and development of our Donlin Gold project.

Our success with respect to the Donlin Gold project depends on the efforts and expertise of a third party with whom we have contracted; we hold a 50% interest and the remaining 50% interest is held by a third party that is not under our control or direction. We are dependent on that third party for the progress and development of the Donlin Gold project. The third party may also have different priorities which could impact the timing and cost of development of the Donlin Gold project. The third party may also be in default of its agreement with us, without our knowledge, which may put the mineral property and related assets at risk. The existence or occurrence of one or more of the following circumstances and events could have a material adverse impact on our ability to achieve our business plan, profitability, or the viability of our interests held with the third party, which could have a material adverse impact on our business, future cash flows, earnings, results of operations and financial condition: (i) disagreement with our business partner on how to develop and operate the Donlin Gold project efficiently; (ii) inability to exert influence over certain strategic decisions made in respect of the jointly-held Donlin Gold project; (iii) inability of our business partner to meet its obligations to the joint business or third parties; and (iv) litigation with our business partner regarding joint business matters.

Opposition to our operations from local stakeholders or non-governmental organizations could have a material adverse effect on us.

There is an increasing level of public concern relating to the effect of mining production on its surroundings, communities and environment. Local communities and non-governmental organizations (NGOs), some of which oppose resource development, are often vocal critics of the mining industry. While we seek to operate in a socially responsible manner, opposition to extractive industries or our operations specifically or adverse publicity generated by local communities or NGOs related to extractive industries, or our operations specifically, could have an adverse effect on our reputation and financial condition or our relationships with the communities in which we operate. As a result of such opposition or adverse publicity, we may be unable to obtain permits necessary for our operations or to continue our operations as planned or at all. See “Recent Developments – Donlin Gold Project” above.

We require various permits to conduct our current and anticipated future operations, and delays or a failure to obtain such permits, or a failure to comply with the terms of any such permits that we have obtained, could have a material adverse impact on us.

Our current and anticipated future operations, including further exploration and development activities and commencement of production on our mineral properties, require permits from various United States federal, state and local governmental authorities. There can be no assurance that all permits that we require for the construction of mining facilities and to conduct mining operations will be obtainable on reasonable terms, or at all. Delays or a failure to obtain such permits, or a failure to comply with the terms of any such permits that we have obtained, could have a material adverse impact on us.

The duration and success of efforts to obtain and renew permits are contingent upon many variables not within our control. Shortage of qualified and experienced personnel in the various levels of government could result in delays or inefficiencies. Backlog within the permitting agencies could affect the permitting timeline of the various projects. Other factors that could affect the permitting timeline include (i) the number of other large-scale projects currently in a more advanced stage of development which could slow down the review process and (ii) significant public response regarding a specific project. As well, it can be difficult to assess what specific permitting requirements will ultimately apply to our projects.

NOVAGOLD RESOURCES INC.

The figures for our mineral resources and mineral reserves are estimates based on interpretation and assumptions and may yield less mineral production under actual conditions than is currently estimated.

Unless otherwise indicated, mineralization figures presented in this Annual Report on Form 10-K and in our other filings with securities regulatory authorities, press releases and other public statements that may be made from time to time are based upon estimates made by our personnel and independent professionals. These estimates use mining terms as defined in accordance with Canadian NI 43-101 and CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in the SEC Industry Guide 7. For further information, see Cautionary Note to U.S. Investors Regarding Estimates of Measured, Indicated and Inferred Resources and Proven and Probable Reserves above. In addition, these estimates are imprecise and depend upon geologic interpretation and statistical inferences drawn from drilling and sampling analysis, which may prove to be unreliable. There can be no assurance that:

| ● |

these estimates will be accurate; |

| ● |

mineral reserve, mineral resource or other mineralization figures will be accurate; or |

| ● |

this mineralization could be mined, processed, or sold profitably. |

Because we have not commenced commercial production at any of our mineral properties, mineralization estimates for our properties may require adjustments, including potential downward revisions based upon further exploration or development work, actual production experience, or changes in the price of gold. In addition, the grade of ore ultimately mined, if any, may differ from that indicated by drilling results. There can be no assurance that the percentage of minerals recovered in small-scale tests will be duplicated in large-scale tests under on-site conditions or at production scale.

Mineral resource estimates for mineral properties that have not commenced production are based, in many instances, on limited and widely spaced drill hole information, which is not necessarily indicative of the conditions between and around drill holes. Accordingly, such mineral resource estimates may require revision as more drilling information becomes available or as actual production experience is gained. No assurance can be given that any part or all of our mineral resources constitute or will be converted into reserves.

The estimating of mineral reserves and mineral resources is a subjective process that relies on the judgment and experience of the persons preparing the estimates. The process relies on the quantity and quality of available data and is based on knowledge, mining experience, analysis of drilling results and industry practices. Valid estimates made at a given time may significantly change when new information becomes available. By their nature, mineral resource and reserve estimates are imprecise and depend, to a certain extent, upon analysis of drilling results and statistical inferences that may ultimately prove to be inaccurate. There can be no assurances that actual results will meet the estimates contained in studies.

Estimated mineral reserves or mineral resources may have to be recalculated based on changes in metal prices, further exploration or development activity, or actual production experience. In addition, if production costs increase, recovery rates decrease, if applicable laws and regulations are adversely changed, there is no assurance that the anticipated level of recovery will be realized or that mineral reserves or mineral resources as currently reported can be mined or processed profitably. This could materially and adversely affect estimates of the volume or grade of mineralization, estimated recovery rates or other important factors that influence mineral reserve or mineral resource estimates. The extent to which mineral resources may ultimately be reclassified as mineral reserves is dependent upon the demonstration of their profitable recovery. Any material changes in mineral resource estimates and grades of mineralization will affect the economic viability of placing a mineral property into production and a mineral property’s return on capital. We cannot provide assurance that mineralization identified at our mineral properties can or will be mined or processed profitably.

The resource and reserve estimates contained in this Annual Report on Form 10-K have been determined and valued based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for gold may render portions of our mineralization uneconomic and result in reduced reported mineralization. Any material reductions in estimates of mineralization, or of our ability to extract this mineralization, could have a material adverse effect on our ability to implement our business strategy, the results of operations or our financial condition.

We have established the presence of proven and probable reserves at our Donlin Gold project under Canadian standards. There can be no assurance that any resource estimates for our mineral projects will ultimately be reclassified as mineral reserves. There can be no assurance that subsequent testing or future studies will establish proven and probable mineral reserves at our other mineral properties, if any. The failure to establish proven and probable mineral reserves could restrict our ability to successfully implement our strategies for long-term growth and could impact future cash flows, earnings, results of operation and financial condition.

NOVAGOLD RESOURCES INC.

Lack of infrastructure could delay or prevent us from developing advanced projects.

Completion of the development of the Donlin Gold project is subject to various requirements, including the availability and timing of acceptable arrangements for power, water, transportation, access and facilities. The lack of availability on acceptable terms or the delay in the availability of any one or more of these items could prevent or delay development of the project. There can be no assurance that adequate infrastructure, including access and power supply, will be built, that it will be built in a timely manner or that the cost of such infrastructure will be reasonable or that it will be sufficient to satisfy the requirements of the project. If adequate infrastructure is not available in a timely manner, there can be no assurance that:

| ● |

the development of the Donlin Gold project will be commenced or completed on a timely basis, if at all; |

| ● |

the resulting operations will achieve the anticipated production volume; or |

| ● |

the construction costs and ongoing operating costs associated with the development of the Donlin Gold project will not be higher than anticipated. |