UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended: June 30, 2023

Commission File Number: 1-33026

Commvault Systems, Inc.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices, including zip code)

(732 ) 870-4000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, "accelerated filer", "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | |||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange Act. | ☐ | ||||||||||||||||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

As of July 28, 2023, there were 43,874,713 shares of the registrant’s common stock, $0.01 par value, outstanding.

1

COMMVAULT SYSTEMS, INC.

FORM 10-Q

INDEX

| Page | ||||||||

| Part I – FINANCIAL INFORMATION | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

Commvault Systems, Inc.

Consolidated Balance Sheets

(In thousands, except per share data)

(Unaudited)

| June 30, 2023 | March 31, 2023 | |||||||||||||

| ASSETS | ||||||||||||||

| Current assets: | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Trade accounts receivable, net | ||||||||||||||

| Assets held for sale | ||||||||||||||

| Other current assets | ||||||||||||||

| Total current assets | ||||||||||||||

| Property and equipment, net | ||||||||||||||

| Operating lease assets | ||||||||||||||

| Deferred commissions cost | ||||||||||||||

| Intangible asset, net | ||||||||||||||

| Goodwill | ||||||||||||||

| Other assets | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||||||||

| Current liabilities: | ||||||||||||||

| Accounts payable | $ | $ | ||||||||||||

| Accrued liabilities | ||||||||||||||

| Current portion of operating lease liabilities | ||||||||||||||

| Deferred revenue | ||||||||||||||

| Total current liabilities | ||||||||||||||

| Deferred revenue, less current portion | ||||||||||||||

| Deferred tax liabilities, net | ||||||||||||||

| Long-term operating lease liabilities | ||||||||||||||

| Other liabilities | ||||||||||||||

| Commitments and contingencies (Note 6) | ||||||||||||||

| Stockholders’ equity: | ||||||||||||||

Preferred stock, $ | ||||||||||||||

Common stock, $ | ||||||||||||||

| Additional paid-in capital | ||||||||||||||

| Accumulated deficit | ( | ( | ||||||||||||

| Accumulated other comprehensive loss | ( | ( | ||||||||||||

| Total stockholders’ equity | ||||||||||||||

| Total liabilities and stockholders’ equity | $ | $ | ||||||||||||

See accompanying unaudited notes to consolidated financial statements

1

Commvault Systems, Inc.

Consolidated Statements of Operations

(In thousands, except per share data)

(Unaudited)

| Three Months Ended June 30, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Revenues: | ||||||||||||||

| Subscription | $ | $ | ||||||||||||

| Perpetual license | ||||||||||||||

| Customer support | ||||||||||||||

| Other services | ||||||||||||||

| Total revenues | ||||||||||||||

| Cost of revenues: | ||||||||||||||

| Subscription | ||||||||||||||

| Perpetual license | ||||||||||||||

| Customer support | ||||||||||||||

| Other services | ||||||||||||||

| Total cost of revenues | ||||||||||||||

| Gross margin | ||||||||||||||

| Operating expenses: | ||||||||||||||

| Sales and marketing | ||||||||||||||

| Research and development | ||||||||||||||

| General and administrative | ||||||||||||||

| Restructuring | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Total operating expenses | ||||||||||||||

| Income from operations | ||||||||||||||

| Interest income | ||||||||||||||

| Interest expense | ( | ( | ||||||||||||

| Other income (expense), net | ( | |||||||||||||

| Income before income taxes | ||||||||||||||

| Income tax expense | ||||||||||||||

| Net income | $ | $ | ||||||||||||

| Net income per common share: | ||||||||||||||

| Basic | $ | $ | ||||||||||||

| Diluted | $ | $ | ||||||||||||

| Weighted average common shares outstanding: | ||||||||||||||

| Basic | ||||||||||||||

| Diluted | ||||||||||||||

See accompanying unaudited notes to consolidated financial statements

2

Commvault Systems, Inc.

Consolidated Statements of Comprehensive Income

(In thousands)

(Unaudited)

| Three Months Ended June 30, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Net income | $ | $ | ||||||||||||

| Other comprehensive loss: | ||||||||||||||

| Foreign currency translation adjustment | ( | ( | ||||||||||||

| Comprehensive income | $ | $ | ||||||||||||

See accompanying unaudited notes to consolidated financial statements

3

Commvault Systems, Inc.

Consolidated Statements of Stockholders’ Equity

(In thousands)

(Unaudited)

| Common Stock | Additional Paid – In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Total | ||||||||||||||||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||||||||||||||

| Balance as of March 31, 2023 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

| Stock-based compensation | ||||||||||||||||||||||||||||||||||||||

| Share issuances related to stock-based compensation | ||||||||||||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||

| Net income | ||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | ( | ( | ||||||||||||||||||||||||||||||||||||

| Balance as of June 30, 2023 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

| Common Stock | Additional Paid – In Capital | Accumulated Deficit | Accumulated Other Comprehensive Loss | Total | ||||||||||||||||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||||||||||||||

| Balance as of March 31, 2022 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

| Stock-based compensation | ||||||||||||||||||||||||||||||||||||||

| Share issuances related to stock-based compensation | ||||||||||||||||||||||||||||||||||||||

| Repurchase of common stock | ( | ( | ( | ( | ( | |||||||||||||||||||||||||||||||||

| Net income | ||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | ( | ( | ||||||||||||||||||||||||||||||||||||

| Balance as of June 30, 2022 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

See accompanying unaudited notes to consolidated financial statements

4

Commvault Systems, Inc.

Consolidated Statements of Cash Flows

(In thousands)

(Unaudited)

| Three Months Ended June 30, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Cash flows from operating activities | ||||||||||||||

| Net income | $ | $ | ||||||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Noncash stock-based compensation | ||||||||||||||

| Noncash change in fair value of equity securities | ( | |||||||||||||

| Amortization of deferred commissions cost | ||||||||||||||

| Changes in operating assets and liabilities: | ||||||||||||||

| Trade accounts receivable | ||||||||||||||

| Operating lease assets and liabilities, net | ( | |||||||||||||

| Other current assets and Other assets | ( | ( | ||||||||||||

| Deferred commissions cost | ( | ( | ||||||||||||

| Accounts payable | ||||||||||||||

| Accrued liabilities | ( | ( | ||||||||||||

| Deferred revenue | ( | |||||||||||||

| Other liabilities | ||||||||||||||

| Net cash provided by operating activities | ||||||||||||||

| Cash flows from investing activities | ||||||||||||||

| Purchase of property and equipment | ( | ( | ||||||||||||

| Purchase of equity securities | ( | ( | ||||||||||||

| Net cash used in investing activities | ( | ( | ||||||||||||

| Cash flows from financing activities | ||||||||||||||

| Repurchase of common stock | ( | ( | ||||||||||||

| Proceeds from stock-based compensation plans | ||||||||||||||

| Payment of debt issuance costs | ( | |||||||||||||

| Net cash used in financing activities | ( | ( | ||||||||||||

| Effects of exchange rate — changes in cash | ( | ( | ||||||||||||

| Net decrease in cash and cash equivalents | ( | ( | ||||||||||||

| Cash and cash equivalents at beginning of period | ||||||||||||||

| Cash and cash equivalents at end of period | $ | $ | ||||||||||||

See accompanying unaudited notes to consolidated financial statements

5

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited

(In thousands, except per share data)

1. Basis of Presentation

Commvault Systems, Inc. and its subsidiaries ("Commvault," "we," "us," or "our") provides its customers with a data protection platform that helps them secure, defend and recover their most precious asset, their data. We provide these products and services for their data across the following environments: on-premises, hybrid, or multi-cloud. Our data protection offerings are delivered via self-managed software, software-as-a-service (SaaS), integrated appliances, or managed by partners. Customers use our technology to protect themselves from threats like ransomware and recover their data efficiently.

2. Summary of Significant Accounting Policies

Reclassification of Prior Year Balances

Certain prior year amounts have been reclassified for consistency with the current year presentation. These reclassifications have no impact on the amount of total revenue or net income. Beginning in fiscal 2024, the software and services line items on the consolidated statements of operations, related to revenues and cost of revenues, will be presented in the following categories:

Subscription - The amounts on this line include the revenues and costs of recurring time-based arrangements, including the software portion of term-based licenses and SaaS offerings. The software component of term-based licenses is typically recognized when the software is delivered or made available for download. For SaaS offerings, revenue is generally recognized ratably over the contract term beginning on the date that the service is made available to the customer.

Perpetual license - The amounts on this line include the revenues and costs from the sale of perpetual software licenses. Perpetual software license revenue is typically recognized when the software is delivered or made available for download.

Customer support - The amounts on this line include customer support revenues and costs associated with our software products. Customer support includes software updates on a when-and-if-available basis, telephone support, integrated web-based support, and other premium support offerings, for both subscription software and perpetual software license arrangements. Customer support revenue is typically recognized ratably over the term of the customer support agreement.

6

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

Recently Adopted and Recently Issued Accounting Standards

Concentration of Credit Risk

Sales through our distribution agreement with Arrow Enterprise Computing Solutions, Inc. (“Arrow”) totaled 38 % and 36 % of total revenues for the three months ended June 30, 2023 and 2022, respectively. Arrow accounted for approximately 33 % and 34 % of total accounts receivable as of June 30, 2023 and March 31, 2023, respectively.

The following table summarizes the composition of our financial assets measured at fair value at June 30, 2023:

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Cash equivalents | $ | $ | |||||||||||||||||||||

There were no financial assets measured at fair value on a recurring basis as of June 30, 2022.

Equity Securities Accounted for at Net Asset Value

Deferred Commissions Cost

Sales commissions, bonuses, and related payroll taxes earned by our employees are considered incremental and recoverable costs of obtaining a contract with a customer. Our typical contracts include performance obligations related to term-based software licenses, SaaS offerings, perpetual software licenses, software updates, and customer support. In these contracts, incremental costs of obtaining a contract are allocated to the performance obligations based on the relative estimated standalone selling prices and then recognized on a systematic basis that is consistent with the transfer of the goods or services to which the asset relates. We do not pay commissions on annual renewals of customer support contracts for perpetual licenses. The costs allocated to software and products are expensed at the time of sale, when revenue for the functional software license or appliance is recognized. The costs allocated to software updates and customer support for perpetual licenses are amortized ratably over a period of approximately five years , the expected period of benefit of the asset capitalized. We currently estimate a period of five years is appropriate based on consideration of historical average customer

7

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

The incremental costs attributable to professional services are generally amortized over the period the related services are provided and revenue is recognized. Amortization expense related to these costs is included in sales and marketing expenses in the accompanying consolidated statements of operations.

3. Revenue

We derive revenues from various sources, including subscriptions, perpetual software licenses, customer support contracts and other services.

Subscription

Subscription includes the revenues derived from time-based arrangements, including the software portion of term-based licenses and SaaS offerings. The software component of term-based licenses is typically recognized when the software is delivered or made available for download. The term of our subscription arrangements are typically to three years , but can range between and five years . For SaaS offerings, revenue is generally recognized ratably over the contract term beginning on the date that the service is made available to the customer.

Perpetual License

Perpetual license includes the revenue from the sale of perpetual software licenses. Perpetual software license revenue is typically recognized when the software is delivered or made available for download.

Customer Support

Customer support includes revenues associated with support contracts tied to our software products. Customer support includes software updates on a when-and-if-available basis, telephone support, integrated web-based support, and other premium support offerings, for both subscription software and perpetual software license arrangements. We sell our customer support contracts as a percentage of net software purchases. Customer support revenue is recognized ratably over the term of the customer support agreement, which is typically one year on our perpetual licenses and over the term on our term-based licenses.

Other Services

Other services consist primarily of revenues related to professional service offerings, including consultation, assessment and design, installation services, and customer education. Revenues related to other professional services are typically recognized as the services are performed.

We do not customize our software licenses (both perpetual and term-based) and installation services are not required. Software licenses are delivered before related services are provided and are functional without professional services, updates and technical support. We have concluded that our software licenses (both perpetual and term-based) are functional intellectual property that is distinct, as the user can benefit from the software on its own. Revenue for both perpetual and term-based licenses is typically recognized when the software is delivered and/or made available for download as this is the point the user of the software can direct the use of, and obtain substantially all of the remaining benefits from the functional intellectual property. We do not recognize subscription revenue related to the renewal of that subscription earlier than the beginning of the new subscription period.

8

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

We also offer appliances that integrate our software with hardware and address a wide-range of business needs and use cases, ranging from support for remote or branch offices with limited IT staff up to large corporate data centers. Our appliances are almost exclusively sold via a software only model in which we sell software to a third party, which assembles an integrated appliance that is sold to end user customers. As a result, the revenue and costs associated with hardware are usually not included in our financial statements.

Our typical performance obligations include the following:

| Performance Obligation | When Performance Obligation is Typically Satisfied | When Payment is Typically Due | How Standalone Selling Price is Typically Estimated | ||||||||

| Subscription | |||||||||||

| Term-based software licenses | Upon shipment or made available for download (point in time) | Within | Residual approach | ||||||||

| Software-as-a-service (SaaS) | Ratably over the course of the contract (over time) | Annually or at the beginning of the contract period | Observable in transactions without multiple performance obligations | ||||||||

| Perpetual License | |||||||||||

| Perpetual software licenses | Upon shipment or made available for download (point in time) | Within | Residual approach | ||||||||

| Customer Support | |||||||||||

| Software updates | Ratably over the course of the support contract (over time) | At the beginning of the contract period | Observable in renewal transactions | ||||||||

| Customer support | Ratably over the course of the support contract (over time) | At the beginning of the contract period | Observable in renewal transactions | ||||||||

| Other Services | |||||||||||

| Other professional services (except for education services) | As work is performed (over time) | Within | Observable in transactions without multiple performance obligations | ||||||||

| Education services | When the class is taught (point in time) | Within | Observable in transactions without multiple performance obligations | ||||||||

Judgments related to revenue recognition

Most of our contracts contain multiple performance obligations. For these contracts, we evaluate and account for individual performance obligations separately if they are determined to be distinct. The transaction price is allocated to the separate performance obligations on a relative standalone selling price basis. Standalone selling prices of software licenses (both perpetual and term-based) are typically estimated using the residual approach. Standalone selling prices for SaaS, customer support contracts, and other services are typically estimated based on observable transactions when these services are sold on a standalone basis. We recognize revenue net of sales tax.

9

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

Disaggregation of Revenue

We disaggregate revenue from contracts with customers into geographical regions. Our Americas region includes the United States, Canada, and Latin America. Our International region primarily includes Europe, Middle East, Africa, Australia, India, Southeast Asia, and China.

| Three Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Americas | $ | $ | |||||||||

| International | |||||||||||

| Total revenues | $ | $ | |||||||||

Remaining Performance Obligations

Remaining performance obligations represent expected future revenue from existing contracts where performance obligations are unsatisfied or partially unsatisfied at the end of the reporting period. As of June 30, 2023, our remaining performance obligations (inclusive of deferred revenues) were $536,669 of which approximately 64 % is expected to be recognized as revenue over the next 12 months and the remainder recognized thereafter. The vast majority of this revenue consists of customer support, other services and SaaS arrangements. Other services consists primarily of professional services revenue which is contingent upon a number of factors, including customers' needs and scheduling.

The amount of revenue recognized in the period that was included in the opening deferred revenue balance was $107,945 for the three months ended June 30, 2023. The amount of revenue recognized from performance obligations satisfied in prior periods was not significant.

Information about Contract Balances

| Accounts Receivable | Unbilled Receivable (current) | Unbilled Receivable (long-term) | Deferred Revenue (current) | Deferred Revenue (long-term) | |||||||||||||

Opening balance as of March 31, 2023 | $ | $ | $ | $ | $ | ||||||||||||

| Increase (decrease), net | ( | ( | ( | ||||||||||||||

Ending balance as of June 30, 2023 | $ | $ | $ | $ | $ | ||||||||||||

10

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

4. Assets Held for Sale

5. Net Income per Common Share

Basic net income per common share is computed by dividing net income by the weighted average number of common shares during the period. Diluted net income per share is computed using the weighted average number of common shares and, if dilutive, potential common shares outstanding during the period. Potential common shares consist of the incremental common shares issuable upon the vesting of restricted stock units, shares to be purchased under the Employee Stock Purchase Plan ("ESPP"), and the exercise of stock options. The dilutive effect of such potential common shares is reflected in diluted earnings per share by application of the treasury stock method.

The following table sets forth the reconciliation of basic and diluted net income per common share:

| Three Months Ended June 30, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Net income | $ | $ | ||||||||||||

| Basic net income per common share: | ||||||||||||||

| Basic weighted average shares outstanding | ||||||||||||||

| Basic net income per common share | $ | $ | ||||||||||||

| Diluted net income per common share: | ||||||||||||||

| Basic weighted average shares outstanding | ||||||||||||||

| Dilutive effect of stock options and restricted stock units | ||||||||||||||

| Diluted weighted average shares outstanding | ||||||||||||||

| Diluted net income per common share | $ | $ | ||||||||||||

The diluted weighted-average shares outstanding exclude restricted stock units, performance restricted stock units, shares to be purchased under the ESPP and outstanding stock options totaling 514 and 535 for the three months ended June 30, 2023 and 2022, respectively, because the effect would have been anti-dilutive.

6. Commitments and Contingencies

7. Capitalization

11

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

8. Stock Plans

The following table presents the stock-based compensation expense included in cost of revenues, sales and marketing, research and development, general and administrative and restructuring expenses for the three months ended June 30, 2023 and 2022. Stock-based compensation is attributable to restricted stock units, performance-based awards and the ESPP.

| Three Months Ended June 30, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Cost of revenues | $ | $ | ||||||||||||

| Sales and marketing | ||||||||||||||

| Research and development | ||||||||||||||

| General and administrative | ||||||||||||||

| Restructuring | ||||||||||||||

| Stock-based compensation expense | $ | $ | ||||||||||||

As of June 30, 2023, there was $144,453 of unrecognized stock-based compensation expense that is expected to be recognized over a weighted-average period of 1.85 years. We account for forfeitures as they occur. To the extent that awards are forfeited, stock-based compensation will be different from our current estimate.

Stock option activity was not significant for both the three months ended June 30, 2023 and 2022.

Restricted Stock Units

Restricted stock unit activity for the three months ended June 30, 2023 was as follows:

| Non-vested Restricted Stock Units | Number of Awards | Weighted- Average Grant Date Fair Value | |||||||||

| Non-vested as of March 31, 2023 | $ | ||||||||||

| Awarded | |||||||||||

| Vested | ( | ||||||||||

| Forfeited | ( | ||||||||||

| Non-vested as of June 30, 2023 | $ | ||||||||||

The weighted-average fair value of restricted stock units awarded was $67.34 per unit during the three months ended June 30, 2023, and $62.60 per unit during the three months ended June 30, 2022. The weighted-average fair value of awards includes the awards with a market condition described below.

12

Commvault Systems, Inc.

Notes to Consolidated Financial Statements - Unaudited (continued)

(In thousands, except per share data)

Performance Based Awards

In the three months ended June 30, 2023, we granted 120 performance restricted stock units ("PSUs") to certain executives. Vesting of these awards is contingent upon i) us meeting certain non-GAAP performance goals (performance-based) in fiscal 2024 and ii) our customary service periods. The awards vest over three years and have the potential to vest between 0 % and 200 % (240 shares) based on actual fiscal 2024 performance. The vesting quantity of these awards may vary based on actual fiscal 2024 performance. The related stock-based compensation expense is determined based on the value of the underlying shares on the date of grant and is recognized over the vesting term using the accelerated method. During the interim financial periods, management estimates the probable number of PSUs that would vest until the ultimate achievement of the performance goals is known. The awards are included in the restricted stock unit table.

Awards with a Market Condition

In the three months ended June 30, 2023, we granted 120 market performance stock units to certain executives. The vesting of these awards is contingent upon us meeting certain total shareholder return ("TSR") levels as compared to the Russell 3000 market index over the next three years . The awards vest in three annual tranches and have the potential to vest between 0 % and 200 % (240 shares) based on TSR performance. The related stock-based compensation expense is determined based on the estimated fair value of the underlying shares on the date of grant and is recognized using the accelerated method over the vesting term. The estimated fair value was calculated using a Monte Carlo simulation model. The fair value of the awards granted during the three months ended June 30, 2023 was $87.90 per unit. The awards are included in the restricted stock unit table.

9. Income Taxes

10. Revolving Credit Facility

13

Item 2 - Management’s Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion and analysis along with our consolidated financial statements and the related notes included elsewhere in this Quarterly Report on Form 10-Q. The statements in this discussion regarding our expectations of our future performance, liquidity and capital resources, and other non-historical statements are forward-looking statements. These forward-looking statements are subject to numerous risks and uncertainties, including, but not limited to, changes in demand as well as the risks and uncertainties described under “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended March 31, 2023. Our actual results may differ materially from those contained in or implied by any forward-looking statements.

Overview

Incorporated in Delaware in 1996, Commvault Systems, Inc. provides its customers with a data protection platform that helps them secure, defend and recover their most precious asset, their data. We provide these products and services for their data across the following environments: on-premises, hybrid, or multi-cloud. Our data protection offerings are delivered via self-managed software, software-as-a-service (SaaS), integrated appliances, or managed by partners. Customers use our technology to protect themselves from threats like ransomware and recover their data efficiently.

Sources of Revenues

We generate revenues through subscription arrangements, perpetual software licenses, customer support contracts and other services. A significant portion of our total revenues comes from subscription arrangements, which include both sales of term-based licenses and SaaS offerings. We are focused on these types of recurring revenue arrangements.

We expect our subscription arrangements will continue to generate revenue from the renewals of term-based licenses and SaaS offerings sold in prior years. Any of our pricing models (capacity, instance based, etc.) can be sold via a subscription arrangement, either through term-based licensing or hosted services. In term-based license arrangements, the customer has the right to use the software over a designated period of time. The capacity of the license is fixed and the customer has made an unconditional commitment to pay. Software revenue in these arrangements is generally recognized when the software is delivered. In SaaS offerings, revenue is recognized ratably over the contract period.

We sell to end-user customers both directly through our sales force and indirectly through our global network of value-added reseller partners, systems integrators, corporate resellers and original equipment manufacturers. Subscription revenue generated through indirect distribution channels accounted for approximately 90% of total subscription revenue in both the three months ended June 30, 2023 and 2022. Subscription revenue generated through direct distribution channels accounted for approximately 10% of total subscription revenue in both the three months ended June 30, 2023 and 2022. Deals initiated by our direct sales force are sometimes transacted through indirect channels based on end-user customer requirements, which are not always in our control and can cause this overall percentage split to vary from period-to-period. As such, there may be fluctuations in the dollars and percentage of subscription revenue generated through our direct distribution channels from time-to-time. We believe that the growth of our subscription revenue, derived from both our indirect channel partners and direct sales force, are key attributes to our long-term growth strategy. We intend to continue to invest in both our channel relationships and direct sales force in the future, but we continue to expect more revenue to be generated through indirect distribution channels over the long term. The failure of our indirect distribution channels or our direct sales force to effectively sell our software applications could have a material adverse effect on our revenues and results of operations.

We have a non-exclusive distribution agreement with Arrow Enterprise Computing Solutions Inc. (“Arrow”) pursuant to which Arrow's primary role is to enable a more efficient and effective distribution channel for our products and services by managing our reseller partners and leveraging their own industry experience. We generated 38% and 36% of our total revenues through Arrow for the three months ended June 30, 2023 and 2022, respectively. If Arrow were to discontinue or reduce the sales of our products or if our agreement with Arrow were terminated, and if we were unable to take back the management of our reseller channel or find another distributor to replace Arrow, there could be a material adverse effect on our future business.

Our customer support revenues include support contracts tied to our software products. Customer support includes software updates on a when-and-if-available basis, telephone support, integrated web-based support, and other premium support offerings, for both subscription software and perpetual software license arrangements. We

14

sell our customer support contracts as a percentage of net software. Customer support revenue is recognized ratably over the term of the customer support agreement.

Our other service revenue consists primarily of professional service offerings, including consultation, assessment and design, installation services, and customer education. Revenues from other services can vary period over period based on the timing services are delivered and are typically recognized as the services are performed.

Foreign Currency Exchange Rates’ Impact on Results of Operations

Sales outside the United States were 45% of our total revenue for the three months ended June 30, 2023 and 44% of our total revenue for the three months ended June 30, 2022. The income statements of our non-U.S. operations are translated into U.S. dollars at the average exchange rates for each applicable month in a period. To the extent the U.S. dollar weakens against foreign currencies, the translation of these foreign currency denominated transactions generally results in increased revenue, operating expenses and income from operations for our non-U.S. operations. Similarly, our revenue, operating expenses and net income will generally decrease for our non-U.S. operations if the U.S. dollar strengthens against foreign currencies.

Using the average foreign currency exchange rates from the three months ended June 30, 2022, our total revenue would have been higher by $1.2 million, our cost of revenue would have been higher by $0.3 million and our operating expenses would have been higher by $0.9 million from non-U.S. operations for the three months ended June 30, 2023.

In addition, we are exposed to risks of foreign currency fluctuation primarily from cash balances, accounts receivables and intercompany accounts denominated in foreign currencies and are subject to the resulting transaction gains and losses, which are recorded as a component of general and administrative expenses. We recognized insignificant net foreign currency transaction losses for the three months ended June 30, 2023. We recognized net foreign currency transaction gains of approximately $0.5 million for the three months ended June 30, 2022.

Critical Accounting Policies

In presenting our consolidated financial statements in conformity with U.S. generally accepted accounting principles ("U.S. GAAP"), we are required to make estimates and judgments that affect the amounts reported therein. Some of the estimates and assumptions we are required to make relate to matters that are inherently uncertain as they pertain to future events. We base these estimates on historical experience and on various other assumptions that we believe to be reasonable and appropriate. Actual results may differ significantly from these estimates. To the extent that there are material differences between these estimates and actual results, our future financial statement presentation, financial condition, results of operations and cash flows may be affected.

In many cases, the accounting treatment of a particular transaction is specifically dictated by U.S. GAAP and does not require management’s judgment in its application, while in other cases, significant judgment is required in selecting among available alternative accounting standards that allow different accounting treatment for similar transactions. We consider these policies requiring significant management judgment to be critical accounting policies. These critical accounting policies are:

•Revenue Recognition

•Accounting for Income Taxes

•Goodwill

There have been no significant changes in our critical accounting policies during the three months ended June 30, 2023 as compared to the critical accounting policies and estimates disclosed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies” included in our Annual Report on Form 10-K for the year ended March 31, 2023.

15

Results of Operations

Three months ended June 30, 2023 compared to three months ended June 30, 2022

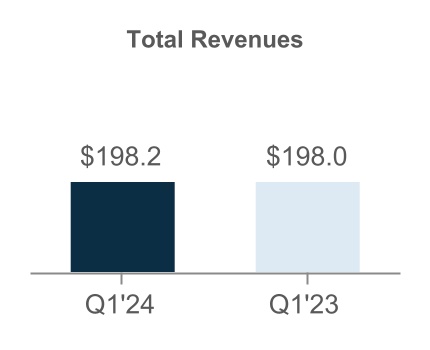

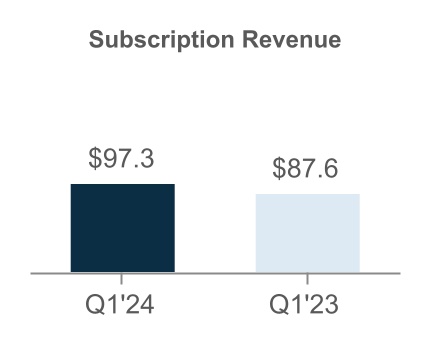

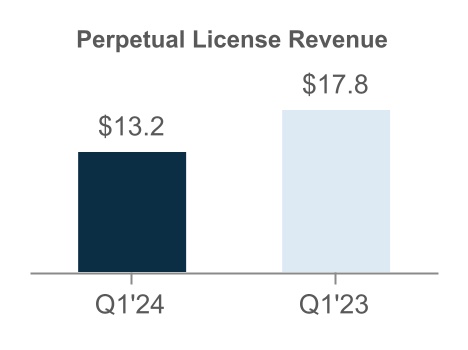

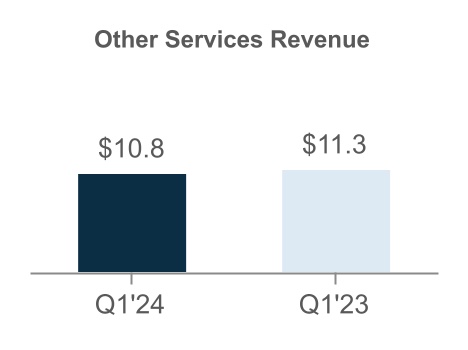

Revenues ($ in millions)

–Total revenues increased $0.2 million, driven primarily by an increase in subscription revenues, offset by decreases in perpetual license and customer support revenues. We remain focused on selling subscription arrangements through both term-based software licenses and SaaS offerings.

–Subscription revenue increased $9.7 million, or 11% year over year, driven by the increase in our SaaS revenue. Our SaaS revenue doubled year over year. This increase was partially offset by a decrease in term-based license revenue. Term-based license revenue declined 4%, due to a decrease in the average selling price on larger term-based license transactions (deals greater than $0.1 million) period over period. Subscription revenue accounted for 49% of total revenues for the three months ended June 30, 2023 compared to 44% for the three months ended June 30, 2022.

–Perpetual license revenue decreased $4.6 million, or 26% year over year as a result of our continued focus on subscription arrangements. Perpetual license revenue accounted for 7% of total revenue for the three months ended June 30, 2023 compared to 9% for the three months ended June 30, 2022.

–Customer support revenue decreased $4.4 million, or 5% year over year, driven by an $11.5 million decrease in customer support revenue attached to perpetual license support renewals, partially offset by a $7.1 million increase in support allocated in term-based license arrangements.

–Other services revenue decreased $0.5 million, primarily due to a decrease in professional services delivered during the period compared to the same period in prior year.

We track total revenue on a geographic basis. Our Americas region includes the United States, Canada, and Latin America. Our International region primarily includes Europe, Middle East, Africa, Australia, India, Southeast Asia and China. Americas and International represented 62% and 38% of total revenue, respectively, for the three months ended June 30, 2023. Total revenue remained flat year over year in the Americas and increased 1% in International.

▪Total revenue in the Americas was impacted by a 10% increase in subscription revenue, offset by a 30% decrease in perpetual license revenue, driven by the shift from selling perpetual licenses to subscription arrangements. Customer support and other services revenue declined 8% and 9%, respectively.

▪The increase in International total revenue was primarily due to a 14% increase in subscription revenue, offset by a 24% decrease in perpetual license revenue. Customer support revenue declined 2% year over

16

year. Other services revenue increased 5% year over year due to an increase in the delivery of professional services for the region against the comparative period.

Our total revenue in International is subject to changes in foreign exchange rates as further discussed above in the “Foreign Currency Exchange Rates’ Impact on Results of Operations” section.

17

Cost of Revenues and Gross Margin ($ in millions)

| Three Months Ended June 30, | ||||||||||||||||||||

| 2023 | 2022 | |||||||||||||||||||

| Cost of Revenue | Gross Margin | Cost of Revenue | Gross Margin | |||||||||||||||||

| Subscription | $ | 12.4 | 87 | % | $ | 11.0 | 87 | % | ||||||||||||

| Perpetual license | 0.4 | 97 | % | 0.6 | 96 | % | ||||||||||||||

| Customer support | 15.0 | 81 | % | 15.0 | 82 | % | ||||||||||||||

| Other services | 7.8 | 28 | % | 7.2 | 37 | % | ||||||||||||||

| Total | $ | 35.6 | 82 | % | $ | 33.8 | 83 | % | ||||||||||||

–Total cost of revenues increased $1.8 million, and represented 18% and 17% of our total revenues for the three months ended June 30, 2023 and 2022, respectively.

–Cost of subscription revenue represented 13% of our total subscription revenue for both the three months ended June 30, 2023 and 2022. The $1.4 million increase year over year is the result of an increase in the cost of infrastructure related to growth in our SaaS offerings.

–Cost of perpetual license revenue decreased $0.2 million and represented 3% of our total perpetual revenue for the three months ended June 30, 2023 compared to 4% for the three months ended June 30, 2022.

–Cost of customer support revenue was flat relative to the prior year quarter and represented 19% of our total customer support revenue for the three months ended June 30, 2023 compared to 18% for the three months ended June 30, 2022.

–Cost of other services revenue increased $0.6 million, representing 72% of our total other services revenue for the three months ended June 30, 2023 compared to 63% for the three months ended June 30, 2022. The increase in cost of other services revenue was driven by timing of the delivery of certain professional services.

18

Operating Expenses ($ in millions)

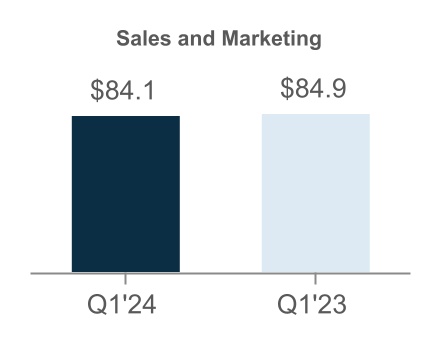

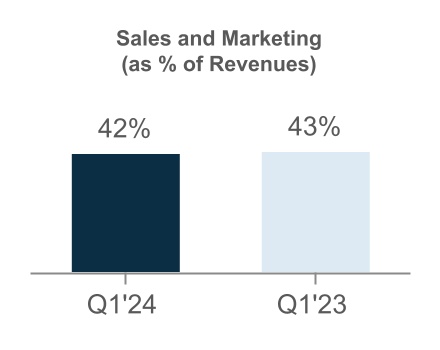

–Sales and marketing expenses decreased $0.8 million, or 1%, primarily due to a decrease in stock-based compensation, partially offset by an increase in travel expenses versus the prior year period.

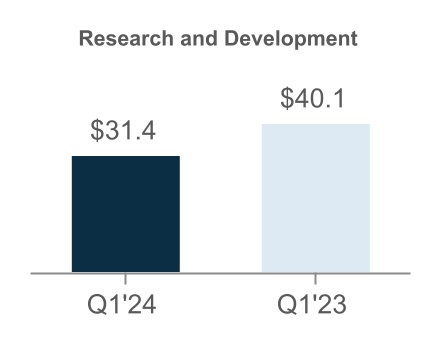

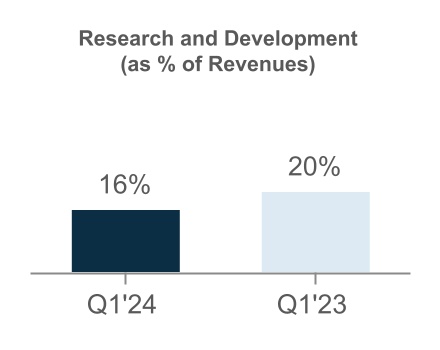

–Research and development expenses decreased $8.7 million, or 22%, driven by decreases in employee compensation and related expenses, including a $3.9 million decrease in stock-based compensation. Investing in research and development remains a priority for Commvault and we anticipate continued responsible spending related to the development of our software applications and hosted services.

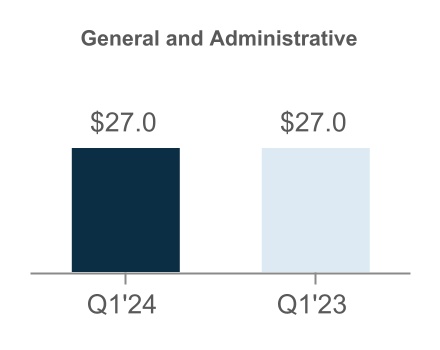

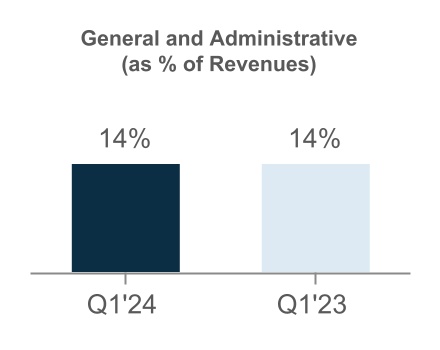

–General and administrative expenses were flat year over year from the prior year quarter. Stock-based compensation decreased $0.9 million year over year.

–Depreciation and amortization expense decreased $1.0 million, driven by the reclassification of our owned corporate headquarters as assets held for sale in the fourth quarter of fiscal 2023.

19

Income Tax Expense

Income tax expense was $6.9 million in the three months ended June 30, 2023 compared to expense of $3.7 million in the three months ended June 30, 2022. The increase in income tax expense relative to the prior year relates primarily to current federal and state taxes driven by the increase of pre-tax income relative to the prior year quarter.

Liquidity and Capital Resources

In recent fiscal years, our principal source of liquidity has been cash provided by operations. As of June 30, 2023, our cash and cash equivalents balance was $274.6 million, of which approximately $194.1 million was held outside of the United States by our foreign legal entities. These balances are dispersed across approximately 35 international locations around the world. We believe that such dispersion meets the current and anticipated future liquidity needs of our foreign legal entities. In the event we need to repatriate funds from outside of the United States, such repatriation would likely be subject to restrictions by local laws and/or tax consequences, including foreign withholding taxes.

On December 13, 2021, we entered into a five-year $100 million senior secured revolving credit facility (the “Credit Facility”) with JPMorgan Chase Bank, N.A. The Credit Facility is available for share repurchases, general corporate purposes, and letters of credit. The Credit Facility contains financial maintenance covenants including a leverage ratio and interest coverage ratio. The Credit Facility also contains certain customary events of default which would permit the lender to, among other things, declare all loans then outstanding to be immediately due and payable if such default is not cured within applicable grace periods. The Credit Facility also limits our ability to incur certain additional indebtedness, create or permit liens on assets, make acquisitions, make investments, loans or advances, sell or transfer assets, pay dividends or distributions, and engage in certain transactions with foreign affiliates. Outstanding borrowings under the Credit Facility accrue interest at an annual rate equal to the Secured Overnight Financing Rate plus 1.25% subject to increases based on our actual leverage. The unused balance on the Credit Facility is also subject to a 0.25% annual interest charge subject to increases based on our actual leverage. As of June 30, 2023, there were no borrowings under the Credit Facility and we were in compliance with all covenants.

On April 20, 2023, the Board of Directors approved an increase of the existing share repurchase program so that $250.0 million was available. The Board's authorization has no expiration date. For the three months ended June 30, 2023, we have repurchased $51.0 million of our common stock. The remaining amount available under the current authorization is $204.9 million.

Our summarized cash flow information is as follows (in thousands):

| Three Months Ended June 30, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

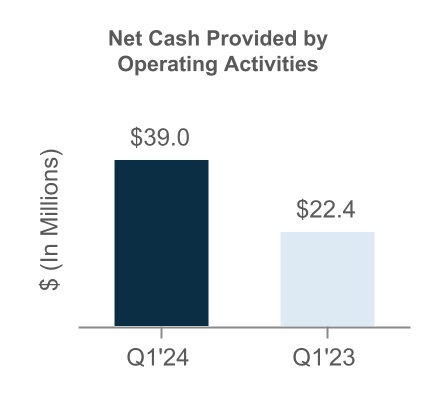

| Net cash provided by operating activities | $ | 39,037 | $ | 22,433 | ||||||||||

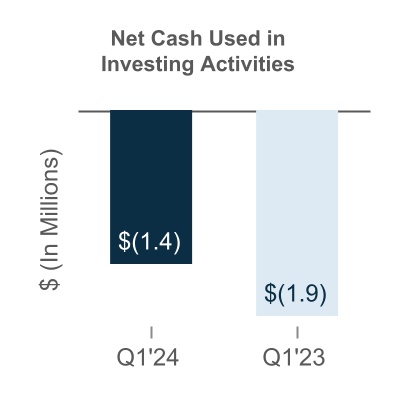

| Net cash used in investing activities | (1,459) | (1,882) | ||||||||||||

| Net cash used in financing activities | (49,829) | (18,299) | ||||||||||||

| Effects of exchange rate - changes in cash | (938) | (11,046) | ||||||||||||

| Net decrease in cash and cash equivalents | $ | (13,189) | $ | (8,794) | ||||||||||

20

–Net cash provided by operating activities was impacted by net income adjusted for the impact of non-cash charges, and decreases in accounts receivable and accrued liabilities.

–Net cash used in investing activities was related to $0.3 million for the purchase of equity securities and $1.1 million of capital expenditures.

–Net cash used in financing activities was the result of $51.0 million of repurchases of common shares, partially offset by $1.2 million of proceeds from the exercise of stock options.

Working capital decreased $18.1 million from $140.8 million as of March 31, 2023 to $122.7 million as of June 30, 2023. The net decrease in working capital was primarily driven by decreases in accounts receivable and accrued liabilities.

We believe that our existing cash, cash equivalents and our cash from operations will be sufficient to meet our anticipated cash needs for working capital, income taxes, capital expenditures and potential stock repurchases for at least the next twelve months. We may seek additional funding through public or private financings or other arrangements during this period. Adequate funds may not be available when needed or may not be available on terms favorable to us, or at all. If additional funds are raised by issuing equity securities, dilution to existing stockholders will result. If we raise additional funds by obtaining loans from third parties, the terms of those financing arrangements may include negative covenants or other restrictions on our business that could impair our operational flexibility, and would also require us to fund additional interest expense. If funding is insufficient at any time in the future, we may be unable to develop or enhance our products or services, take advantage of business opportunities or respond to competitive pressures, any of which could have a material adverse effect on our business, financial condition and results of operations.

Off-Balance Sheet Arrangements

As of June 30, 2023, we did not have off-balance sheet financing arrangements, including any relationships with unconsolidated entities or financial partnerships, such as entities often referred to as structured finance or special purpose entities.

Impact of Recently Issued Accounting Standards

There were no recently issued accounting standards that had a material effect on our condensed consolidated financial statements and accompanying disclosures, and no recently issued accounting standards that are expected to have a material impact on our condensed consolidated financial statements and accompanying disclosures.

Item 3 - Quantitative and Qualitative Disclosures about Market Risk

Interest Rate Risk

None.

21

Foreign Currency Risk

Economic Exposure

As a global company, we face exposure to adverse movements in foreign currency exchange rates. Our international sales are generally denominated in foreign currencies and this revenue could be materially affected by currency fluctuations. Approximately 45% of our revenues were from outside the United States for the three months ended June 30, 2023. Our primary exposures are to fluctuations in exchange rates for the U.S. dollar versus the Euro, and to a lesser extent, the Australian dollar, British pound sterling, Canadian dollar, Chinese yuan, Indian rupee, Korean won and Singapore dollar. Changes in currency exchange rates could adversely affect our reported revenues and require us to reduce our prices to remain competitive in foreign markets, which could also have a material adverse effect on our results of operations. Historically, we have periodically reviewed and revised the pricing of our products available to our customers in foreign countries and we have not maintained excess cash balances in foreign accounts.

Transaction Exposure

Our exposure to foreign currency transaction gains and losses is primarily the result of certain net receivables due from our foreign subsidiaries and customers being denominated in currencies other than the functional currency of the subsidiary. Our foreign subsidiaries conduct their businesses in local currency and we generally do not maintain excess U.S. dollar cash balances in foreign accounts.

Foreign currency transaction gains and losses are recorded in general and administrative expenses in the consolidated statements of operations. We recognized insignificant net foreign currency transaction losses for the three months ended June 30, 2023. We recognized net foreign currency transaction gains of approximately $0.5 million for the three months ended June 30, 2022.

Item 4 - Controls and Procedures

Evaluation of Disclosure Controls and Procedures

Our management, with the participation of the Chief Executive Officer and Chief Financial Officer, has evaluated the effectiveness of our disclosure controls and procedures, as defined in Rules 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934, as amended, as of June 30, 2023. Based on that evaluation, the Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were effective as of June 30, 2023.

Changes in Internal Control over Financial Reporting

There was no change in our internal control over financial reporting that occurred during the first quarter of fiscal 2024 that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

Inherent Limitations on Internal Controls

Our management, including our Chief Executive Officer and Chief Financial Officer, do not expect that our disclosure controls and procedures or our internal control over financial reporting will prevent or detect all error and all fraud. A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within the company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of a simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by management override of the controls. The design of any system of controls also is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Over time, controls may become inadequate because of changes in conditions, or the degree of compliance with the policies or procedures may deteriorate. Because of inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected.

22

PART II. OTHER INFORMATION

Item 1. Legal Proceedings

From time to time, we are subject to claims in legal proceedings arising in the normal course of business. We do not believe that we are currently party to any pending legal action that could reasonably be expected to have a material adverse effect on our business or operating results. Please refer to Part I, “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended March 31, 2023 for additional information.

Item 1A. Risk Factors

In addition to the other information set forth in this report, you should carefully consider the factors discussed in Part I, “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended March 31, 2023, which are incorporated herein by reference, and could materially affect our business, financial condition or future results. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may materially adversely affect our business, financial condition and/or operating results. If any of the risks actually occur, our business, financial conditions or results of operations could be negatively affected. In that case, the trading price of our stock could decline, and our stockholders may lose part or all of their investment. There have been no material changes from the risk factors set forth in Part I, “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended March 31, 2023.

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

Purchases of Equity Securities by the Issuer

On April 20, 2023, the Board of Directors approved an increase of the existing share repurchase program so that $250.0 million was available. The Board's authorization has no expiration date. During the three months ended June 30, 2023, we repurchased $51.0 million of common stock, or approximately 0.8 million shares, under our share repurchase program. As of June 30, 2023, the remaining amount available under the current authorization is $204.9 million. A summary of our repurchases of common stock is as follows:

| Period | Total number of shares purchased | Average price paid per share | Total number of shares purchased as part of publicly announced programs | Approximate dollar value of shares that may yet be purchased under the program (in thousands) | ||||||||||||||||||||||

| April 1-30, 2023 | 160,700 | $ | 58.81 | 160,700 | $246,514 | |||||||||||||||||||||

| May 1-31, 2023 | 363,600 | $ | 64.60 | 363,600 | $223,024 | |||||||||||||||||||||

| June 1-30, 2023 | 254,300 | $ | 71.13 | 254,300 | $204,936 | |||||||||||||||||||||

| Three Months Ended June 30, 2023 | 778,600 | $ | 65.54 | 778,600 | ||||||||||||||||||||||

Item 3. Defaults upon Senior Securities

None.

Item 4. Mine Safety Disclosures

Not Applicable.

Item 5. Other Information

23

Item 6. Exhibits

| Exhibit No. | Description | ||||

| Certification of Chief Executive Officer Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 | |||||

| Certification of Chief Financial Officer Pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 | |||||

| Certification of Chief Executive Officer Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 | |||||

| Certification of Chief Financial Officer Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 | |||||

| 101.INS | XBRL Instance Document - the instance document does not appear in the Interactive Data File because its XBRL tags are embedded within the Inline XBRL document | ||||

| 101.SCH | XBRL Taxonomy Extension Schema Document | ||||

| 101.CAL | XBRL Taxonomy Extension Calculation Linkbase Document | ||||

| 101.DEF | XBRL Taxonomy Extension Definition Linkbase Document | ||||

| 101.LAB | XBRL Taxonomy Extension Label Linkbase Document | ||||

| 101.PRE | XBRL Taxonomy Extension Presentation Linkbase Document | ||||

| 104 | Cover Page Interactive Data File (formatted as Inline XBRL and contained in Exhibit 101) | ||||

| * Furnished herewith | |||||

24

Signatures

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

| Commvault Systems, Inc. | ||||||||||||||

| Dated: | August 1, 2023 | By: | /s/ Sanjay Mirchandani | |||||||||||

| Sanjay Mirchandani | ||||||||||||||

| Director, President and Chief Executive Officer | ||||||||||||||

| (Principal Executive Officer) | ||||||||||||||

| Dated: | August 1, 2023 | By: | /s/ Gary Merrill | |||||||||||

| Gary Merrill | ||||||||||||||

| Chief Financial Officer | ||||||||||||||

| (Principal Financial Officer) | ||||||||||||||

25