SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

| | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended

| | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE EXCHANGE ACT |

For the transition period from __________ to ___________

Commission file number:

GB SCIENCES, INC.

(Exact name of registrant as specified in its charter)

| | |

| (State or other Jurisdiction of | (IRS Employer I.D. No.) |

| Incorporation or Organization) |

Phone: (

(Address and telephone number of

principal executive offices)

Securities registered under Section 12 (b) of the Exchange Act:

| Title of each class | Name of each exchange on which registered | |

| None | None |

Securities registered under Section 12(g) of the Exchange Act:

| | |

| Title of Class |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer", "accelerated filer", "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.).

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| | Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Act). Yes

The aggregate market value of the voting stock held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter, that being September 2022, was approximately $

Total shares outstanding on July 14, 2023, were

Documents Incorporated by Reference

None

GB SCIENCES, INC.

FORM 10-K

DISCLOSURE REGARDING FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K of GB Sciences, Inc., a Nevada corporation and its subsidiaries (the “Company”), contains “forward-looking statements,” as defined in the United States Private Securities Litigation Reform Act of 1995. In some cases, you can identify forward-looking statements by terminology such as “may”, “will”, “should”, “could”, “expects”, “plans”, “intends”, “anticipates”, believes”, “estimates”, “predicts” or “continue”, which list is not meant to be all-inclusive, and other such negative terms and comparable technology. These forward-looking statements, include, without limitation, statements about market opportunity, strategies, competition, expected activities and expenditures as we pursue business our plan, and the adequacy of available cash reserves. Although we believe the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Actual results may differ materially from the predictions discussed in these forward-looking statements. The economic environment within which we operate could materially affect actual results. Additional factors that could materially affect these forward-looking statements and/or predictions include among other things:

(i) product demand, market and customer acceptance of any or all of the Company’s products, equipment and other goods,

(ii) ability to obtain financing to expand its operations,

(iii) ability to attract and retain qualified personnel,

(iv) the results, cost and timing of our preclinical studies and clinical trials, including any delays to such clinical trials relating to enrollment or site initiation, as well as the number of required trials for regulatory approval and the criteria for success in such trials,

(v) our dependence on third parties in the conduct of our preclinical studies and clinical trials,

(vi) legal and regulatory developments in the United States and foreign countries, including any actions or advice that may affect the design, initiation, timing, continuation, progress or outcome of clinical trials or result in the need for additional clinical trials,

(vii) the results of our preclinical studies and earlier clinical trials of our product candidates may not be predictive of future results and we may not have favorable results in our ongoing or planned clinical trials,

(viii) the difficulties and expenses associated with obtaining and maintaining regulatory approval of our product candidates, and the indication and labeling under any such approval,

(ix) our plans and ability to develop and commercialize our product candidates,

(x) successful development of our commercialization capabilities, including sales and marketing capabilities, whether alone or with potential future collaborators,

(xi) the size and growth of the potential markets for our product candidates, the rate and degree of market acceptance of our product candidates and our ability to serve those markets,

(xii) the success of competing therapies and products that are or become available,

(xiii) our ability to limit our exposure under product liability lawsuits, shareholder class action lawsuits or other litigation,

(xiv) our ability to obtain and maintain intellectual property protection for our product candidates,

(xv) our ability to obtain and maintain third-party manufacturing for our product candidates on commercially reasonable terms,

(xvi) delays, interruptions or failures in the manufacture and supply of our product candidates,

(xvii) the performance of third parties upon which we depend, including third-party contract research organizations, or CROs, contract manufacturing organizations, or CMOs, contractor laboratories and independent contractors,

(xviii) the timing and outcome of current and future legal proceedings,

(xix) our ability to maintain proper functionality and security of our internal computer and information systems and prevent or avoid cyberattacks, malicious intrusion, breakdown, destruction, loss of data privacy or other significant disruption,

(xx) the adequacy of capital reserves and liquidity including, but not limited to, access to additional borrowing capacity,

(xxi) the extent to which health epidemics and other outbreaks of communicable diseases, including the ongoing COVID-19 pandemic, could disrupt our operations or materially and adversely affect our business and financial conditions, and

(xxii) general industry and market conditions and growth rates, unexpected natural disasters, and other factors, which we have little or no control: and any other factors discussed in the Company’s filings with the Securities and Exchange Commission (“SEC”).

You should refer to Part I Item 1A. “Risk Factors” of this Annual Report on Form 10-K for a discussion of material factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Annual Report on Form 10-K will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame or at all. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

You should read this Annual Report on Form 10-K and the documents that we reference in this Annual Report on Form 10-K and have filed as exhibits to this Annual Report on Form 10-K completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

ITEM 1. DESCRIPTION OF BUSINESS

Unless the context indicates otherwise, all references to “GB” and “GB Sciences” refers solely to GB Sciences, Inc., a Nevada corporation, and all references to “the Company,” “we”, “us” or “our” in this Annual Report refers to GB Sciences and its consolidated subsidiaries.

Overview

GB Sciences, Inc. (“the Company”, “GB Sciences”, “we”, “us”, or “our”) is a plant-inspired, biopharmaceutical research and development company creating patented, disease-targeted formulations of cannabis- and other plant-inspired therapeutic mixtures for the prescription drug market through its wholly owned Canadian subsidiary, GbS Global Biopharma, Inc. (“GBSGB”).

Through GBSGB, the Company is engaged in the research and development of plant-inspired medicines, with virtual operations in North America and Europe. GBSGB’s assets include a portfolio of intellectual property containing both proprietary plant-inspired formulations and our AI-enabled drug discovery platform, as well as critical research contracts and key supplier arrangements. The Company’s intellectual property portfolio, which is held by GBSGB, contains six U.S. and five foreign patents issued, one US and three foreign patents allowed, as well as 18 U.S. and 55 foreign patent-pending applications.

On February 3, 2023, GB Sciences’ first foreign patent protecting its proprietary cannabinoid-based formulations for Parkinson’s disease was issued in China. China is an increasingly important pharmaceutical market with cultural acceptance of plant-based formulations, which is a good fit for GB Sciences’ drug candidates. The global market for treatments of Parkinson’s disease is projected to grow to $8.8 billion by the year 2026, and new therapies to address Parkinson’s disease symptoms are greatly needed. GB Sciences’ first foreign patent also confirms that the Company’s intellectual property strategy can work globally and validates both our plant-inspired drug discovery process and intellectual property strategy, which involves defining and protecting Minimum Essential Mixtures. GBLX/GBSGB starts its drug discovery process with plant-based therapies that are working anecdotally or in traditional medical systems, then the Company systematically reduces the number of compounds to reveal Minimum Essential Mixtures. The Company’s novel Minimum Essential Mixtures retain the increased efficacy of whole plant medicines, but they are easier to manufacture with precision at scale like single ingredient drugs. These Minimum Essential Mixtures are a viable alternative to standard single ingredient drugs or traditional whole plant medicines. The Chinese Patent was issued for GBSGB’s Cannabinoid-Containing Complex Mixtures for the treatment of Parkinson’s disease.

Several more of GBLX/GBSGB’s foreign patents for plant-based treatments of serious disorders were allowed in different countries, expanding our patent protections as follows. On December 1, 2022, the Israeli (IL) Patent was allowed, protecting our Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). MCAS is a severe immunological condition in which mast cells inappropriately and excessively release inflammatory mediators, resulting in a range of severe chronic hyperinflammatory symptoms and life-threatening anaphylaxis attacks. On December 15, 2022, the Australian (AU) Patent was allowed, protecting the Company’s Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). On February 20, 2023, the Japanese (JP) Patent was allowed, protecting the Company’s Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). Additionally, on March 9, 2023, the Notice of Allowance was received for the Company’s U.S. Patent Application No. 16/878,295. This Notice of Allowance protects the use of the Company’s Myrcene-Containing Complex Mixtures in the treatment of cardiac hypertrophy, overactive bladder, and refractory chronic cough. On April 25, 2023, the Japanese patent was also issued for the use of GBSGB’s Cannabinoid-Containing Complex Mixtures in the treatment of Parkinson’s disease.

GBSGB’s intellectual property covers a range of over 65 medical conditions, from which five drug development programs are in the preclinical stage of drug development including our formulations for Parkinson’s disease ("PD"), chronic pain, COVID-related cytokine release syndrome, depression/anxiety, and cardiovascular therapeutic programs. The Company’s primary focus is on preparing its lead program for the treatment of the motor symptoms of Parkinson's disease for a first-in-human clinical trial. Depending on the results of ongoing preclinical studies, the Company intends to move forward with clinical trials for its chronic pain and COVID-related cytokine release syndrome therapies after PD. The Company’s formulations for chronic pain, anxiety, and depression are currently in preclinical animal studies with researchers at the National Research Council Canada. The Company recently received proof-of-concept data supporting its kava-inspired anxiety formulations. The Company also has positive preclinical proof-of-concept data supporting its complex mixtures for the treatment of Cytokine Release Syndrome, and its lead candidates will be optimized based on late-stage preclinical studies at Michigan State University. Proof-of-concept studies in animals that support our heart disease formulations have been successfully completed at the University of Hawaii. The Company runs a lean drug development program through GBSGB and takes effort to minimize expenses, including personnel, overhead, and fixed capital expenses through strategic partnerships with Universities and Contract Research Organizations (“CROs”). Our productive research and development network includes distinguished universities, hospitals, and Contract Research Organizations.

We were incorporated in the State of Delaware on April 4, 2001, under the name “Flagstick Venture, Inc.” On March 28, 2008, stockholders owning a majority of our outstanding common stock approved changing our then name “Signature Exploration and Production Corp.” as our business model had changed.

On April 4, 2014, we changed our name from Signature Exploration and Production Corporation to Growblox Sciences, Inc. Effective December 12, 2016, the Company amended its Certificate of Corporation pursuant to shareholder approval, and the Company’s name was changed from Growblox Sciences, Inc. to GB Sciences, Inc.

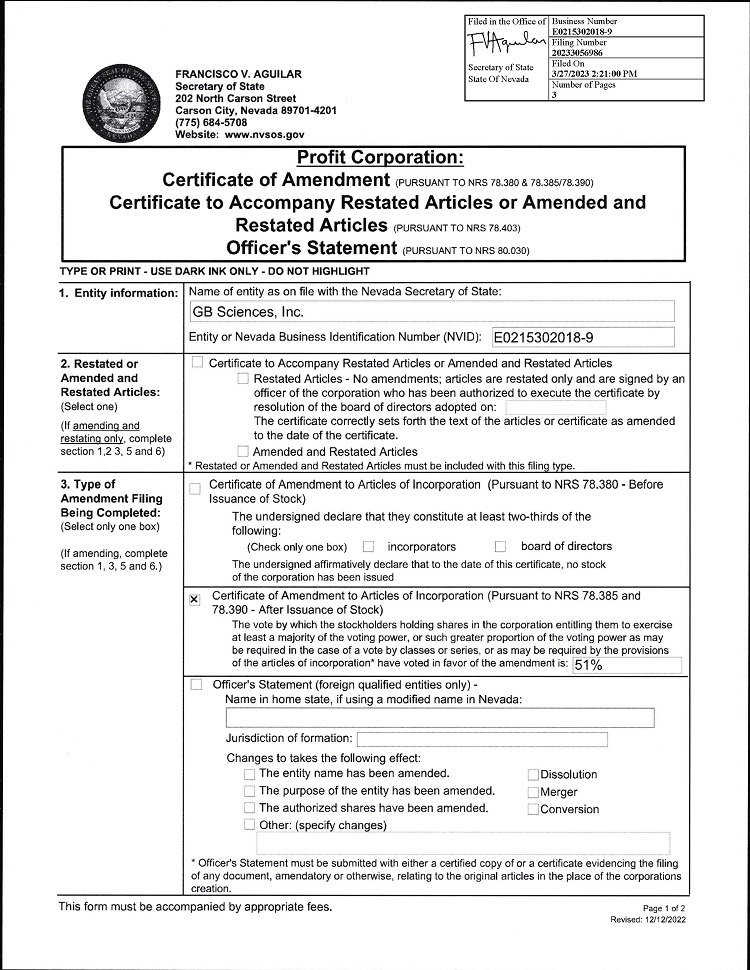

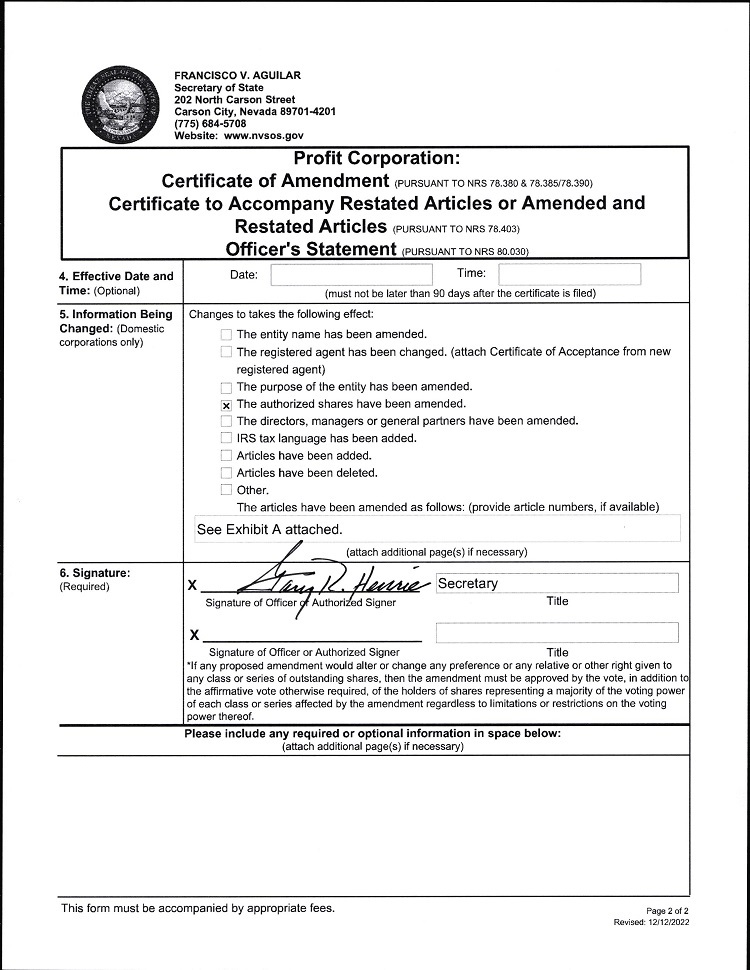

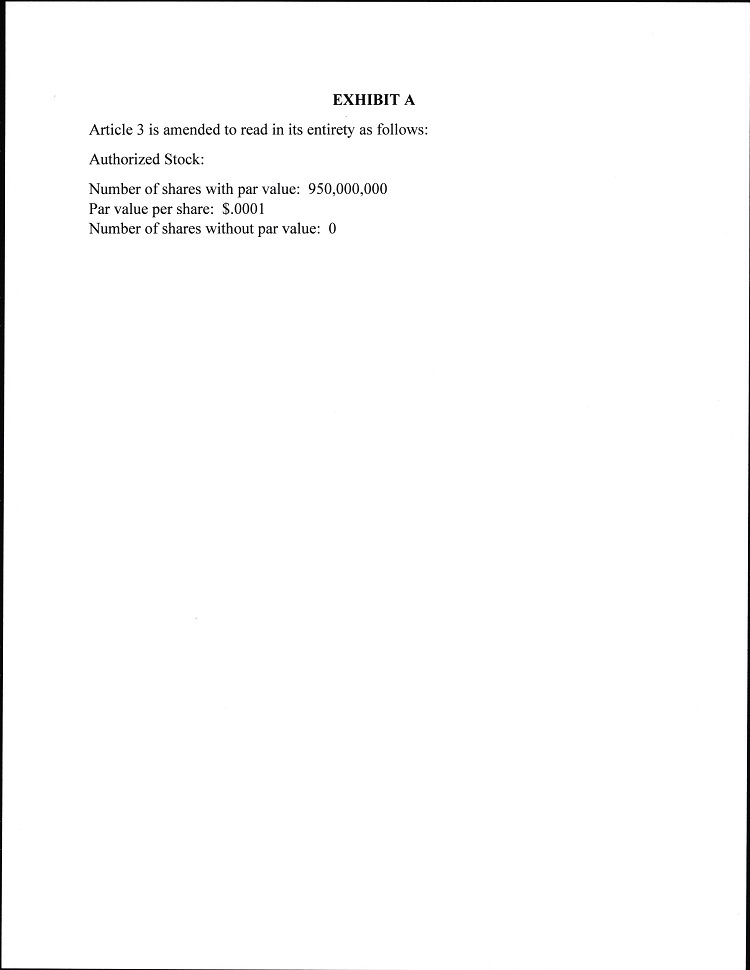

Effective April 8, 2018, Shareholders of the Company approved the change in corporate domicile from the State of Delaware to the State of Nevada and increase in the number of authorized capital shares from 250,000,000 to 400,000,000. Effective August 15, 2019, Shareholders of the Company approved an increase in authorized capital shares from 400,000,000 to 600,000,000. Effective March 09, 2023, Shareholders of the Company approved an increase in authorized capital shares from 600,000,000 to 950,000,000.

Business Strategy

Drug Discovery and Development of Novel Cannabis- and Other Plant-Inspired Therapies

Through its wholly owned Canadian subsidiary, GBS Global Biopharma, Inc. ("GBSGB"), the Company has conducted ground-breaking research embracing the rational design of plant-inspired medicines led by Dr. Andrea Small-Howard, the Company’s President, Chief Science Officer, and Director. In the early days, Small-Howard and Dr. Helen Turner, Vice President of Innovation and Dean of the Natural Sciences and Mathematics Department at Chaminade University, posited that minimum essential mixtures of plant-based ingredients would provide more targeted and effective treatments for specific disease conditions than either single ingredient or whole plant formulations. They started with cannabis-based drug discovery and developed a rapid screening and assaying system that tested thousands of combinations of cannabinoids and terpenes in vitro against cell-based models of disease. This process identified precise mixtures of cannabinoids and terpenes, many of which contained no THC, to treat categories of disease conditions, including neurological disorders, inflammation, heart disease, metabolic syndrome, and chronic neuropathic pain. More recently, a similar approach has been applied to the discovery and validation of therapies informed by plants described in a variety of Traditional Medical Systems. These rich discovery efforts have yielded new preclinical programs; for example, our anxiety and depression formulations that contain minimum essential mixtures of compounds derived from plants in the Piper plant family, such as kava.

Currently, the Company’s drug discovery engine involves both a data analytics/machine learning tool to expedite drug discovery and high throughput screening of cell and animal models of disease. As previously mentioned, the Company initially explored the potential medical uses of specific mixtures derived from cannabis-based raw materials, but our early in silico tools have now been improved, and they are becoming increasingly effective for investigating the medical applications of potential therapeutic mixtures from any plant-derived starting material. In 2014, the Company developed its first rapid screening and assaying system which tested thousands of combinations of cannabinoids and terpenes against cell-based models of diseases. This process has been refined over the years and now has identified precise mixtures of cannabinoids and terpenes, many of which contained no THC, to treat categories of disease conditions, including neurological disorders, inflammation, heart disease, metabolic syndrome, chronic and neuropathic pain. Through GBSGB, the Company has filed for patent protection on these plant-inspired, minimum essential mixtures, and they are validating them in disease-specific animal models in preparation for human trials.

The Company’s drug discovery process combines: 1) PhAROS™: Phytomedical Analytics for Research Optimization at Scale for the prediction of minimum essential mixtures from plant-based materials, and 2) HTS: high throughput screening to refine and validate plant-inspired, minimum essential mixtures in well-established cell and animal models of diseases. This combined approach to drug discovery increases research efficiency and accuracy reducing the time from ideation to patenting from 7 years to 1.5 years. The Company now uses its PhAROS™ Drug Discovery Platform to ‘pre-validate’ therapeutic mixtures. PhAROS can both prioritize and eliminate some potential combinations, which reduces time and resources used in the discovery period. PhAROS™ can also be used to identify and predict the efficacy of plant-inspired, minimum essential mixtures for specific diseases in silico, which are then tested by screening in cell and animal models. Screening of plant-inspired mixtures for drug discovery involves the testing of specific combinations of plant chemicals from many naturally occurring plants and the use of live models for these diseases that have been well established by other researchers. The Company refines the potential therapeutic mixtures pre-validated by PhAROS™ to optimize their effectiveness using cell and animal models. Based on data from disease-specific assays, therapeutic formulations are refined during the HTS screening process by removing compounds that do not act synergistically with the others in the mixtures. The goal is to identify minimum essential mixtures (MEM) that retain the efficacy of the whole plant extracts, but with the manufacturing and quality control advantages of single ingredient pharmaceutical products.

Recently, the Company has received positive preclinical results supporting the efficacy of its proprietary kava-based formulas designed for the treatment of anxiety, which were obtained as a part of its on-going preclinical study of kava-inspired formulations for the treatment of anxiety or depression. The Company is addressing the growing need for anxiety and depression medications with non-psychedelic kava-based formulations. As mental health disorders increasingly impact global populations, Gb Sciences is developing psychotropic but non-psychedelic treatments for anxiety and depression that compete with the emerging billion-dollar psychedelic companies. Gb Sciences’ psychotropic kava-inspired formulas enhance mood, but they do not have potentially unwanted psychedelic side-effects. The National Research Council of Canada (“NRC”) has been testing the Company’s proprietary, psychotropic plant-based formulas for the treatment of depression and anxiety. For these novel psychotropic drug candidates, the Company used their AI-enabled PhAROS™ platform to identify new ingredients to improve upon an initial formulation for anxiety based on traditional medicine. The original plant mixture was derived from the kava plant, but some elements of kava are thought to cause liver toxicity. PhAROS™ identified ingredients from the Piper plant family as a substitute for the functionality of the ingredients in question without the potentially adverse safety profiles of those original ingredients. The Piper plant family includes pepper plants that are used worldwide in traditional medicines. The Company’s novel psychotropic formulations have been tested in preclinical trials at the Zebrafish Toxicology, Genomics and Neurobiology Lab at the NRC, led by Dr. Lee Ellis, Research Officer and Team Lead. The ongoing work between the NRC and the Company has produced strong and applicable data for the evaluation of its therapies, and this trial could provide novel treatment options for patients with depression and anxiety.

The U.S. Patent and Trademark Office allows complex mixtures to be claimed as Active Pharmaceutical Ingredients ("APIs"). Through GBSGB, the Company has six issued patents, plus a series of pending patents containing plant-derived complex mixtures and minimum essential mixtures that act as therapeutic agents for specific disease categories, as described below. The Company’s pending patents are protected whether the individual compounds are derived from the cannabis plant, another plant, synthetically produced, or derived from a combination of sources for the individual chemical compounds in these mixtures.

On February 3, 2023, GB Sciences’ first foreign patent protecting its proprietary cannabinoid-based formulations for Parkinson’s disease was issued in China. China is an increasingly important pharmaceutical market with cultural acceptance of plant-based formulations, which is a good fit for GB Sciences’ drug candidates. The global market for treatments of Parkinson’s disease is projected to grow to $8.8 billion by the year 2026, and new therapies to address Parkinson’s disease symptoms are greatly needed. The Chinese Patent was issued for GBSGB’s Cannabinoid-Containing Complex Mixtures for the treatment of Parkinson’s disease.

Several more of GBLX/GBSGB’s foreign patents for plant-based treatments of serious disorders were allowed in different countries, expanding our patent protections as follows. On December 1, 2022, the Israeli (IL) Patent was allowed, protecting our Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). MCAS is a severe immunological condition in which mast cells inappropriately and excessively release inflammatory mediators, resulting in a range of severe chronic hyperinflammatory symptoms and life-threatening anaphylaxis attacks. On December 15, 2022, the Australian (AU) Patent was allowed, protecting the Company’s Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). On February 20, 2023, the Japanese (JP) Patent was allowed, protecting the Company’s Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). Additionally, on March 9, 2023, the Notice of Allowance was received for the Company’s U.S. Patent Application No. 16/878,295. This Notice of Allowance protects the use of the Company’s Myrcene-Containing Complex Mixtures in the treatment of cardiac hypertrophy, overactive bladder, and refractory chronic cough. On April 25, 2023, the Japanese patent was also issued for the use of GBSGB’s Cannabinoid-Containing Complex Mixtures in the treatment of Parkinson’s disease.

Drug Development Progress

The Company has made significant strides in the past year with respect to both its drug discovery research and product development programs. The Company, through GBSGB, has five preclinical phase product development programs and is aggressively preparing its lead formulations for the treatment of Parkinson’s disease for a first-in-human clinical trial. Our lead program in Parkinson’s disease is being prepared for a first-in-human trial through the following essential steps: a) creating clinical prototypes by combining our proprietary Parkinson’s formulas with a convenient oral delivery system; b) performing a dose response study in rodents to establish the correct range of active ingredients for our first-in-human trial; c) performing necessary ADMET (Absorption, Distribution, Metabolism, Excretion, and Toxicology) tests on the clinical prototypes; and d) selecting a Contract Research Organization (CRO) to prepare an Investigational New Drug (IND) application to the US FDA to begin our first-in-human trial. In addition to our work in preparing the Parkinson’s formulation for a First-in-Human trial, the Company’s chronic pain, anxiety, and depression formulations are currently in preclinical animal studies with Dr. Lee Ellis of the National Research Council ("NRC") Canada in Halifax, Nova Scotia. Based on our positive preclinical, proof-of-concept data supporting our minimum essential mixtures for the treatment of Cytokine Release Syndrome in COVID-19 (COVID-CRS) and other severe hyperinflammatory conditions, the Company’s lead COVID-CRS candidates will be optimized in late-stage preclinical studies with Dr. Norbert Kaminski at Michigan State University.

For the Company’s lead program in PD therapeutics, the efficacy of our original formulations has been improved and the Company has filed a new patent application family to protect our defined cannabinoid ratio-minimum essential mixtures (DCR-MEMs) for the treatment of Parkinsonian motor symptoms. The Company had announced previously that it has obtained the statistically significant reduction of Parkinson’s-disease like symptoms using proprietary cannabinoid-containing MEMs in an animal model of Parkinson’s disease ("PD"). These important preclinical results will be included in GBS’ Investigational New Drug ("IND") application with the US FDA to enter human clinical trials as soon as possible. New therapies to address Parkinson’s disease symptoms are needed to help those afflicted with this debilitating disease. The combined direct and indirect costs associated with Parkinson’s disease are estimated at $52 billion in the U.S. alone.

This year, we have successfully created clinical prototypes of our top three performing cannabinoid-containing Parkinson’s formulations with Catalent Pharma based on incorporating our proprietary cannabinoid formulations for Parkinson’s disease into Catalent Pharma’s proprietary Zydis® delivery system. Catalent Pharma’s Zydis® delivery system is an Orally Disintegrating Tablet format (“ODT”) that should be ideal for delivering our cannabinoid-ratio controlled formulations to Parkinson’s patients. More than 50% of Parkinson’s patients have trouble swallowing, but the Zydis® format delivers the active ingredients into the mouth by dispersion without needing water or the ability to swallow. To ready the Company’s Parkinson’s disease therapies for a First-in-Human trial, the initial clinical prototypes of our Defined Cannabinoid Ratio (DCR)-MEM have been formulated by Catalent Pharma using Catalent’s Zydis® Orally Disintegrating Tablet technology and they are being evaluated in stability and functional testing. As mentioned above, the ODT format was selected for the PD formulas because it dissolves on the tongues of patients without the need to swallow for ease of use in patients with PD, who often have difficulties with swallowing. Previously, the Company has completed two proof-of-concept studies for its MEM. Now, the Company has completed a Feasibility Study that has produced the clinical prototypes for its DCR-MEM. The Company selected Catalent for the delivery of their PD therapies due to Catalent’s prior experience in working on US FDA-approved, cannabinoid-containing drugs, their Schedule I drug manufacturing facilities, their familiarity with US FDA and international regulatory and manufacturing requirements, their expertise in tackling formulation challenges, and their ability to achieve the stability and dosing necessary for these novel therapeutic mixtures. In addition to its Zydis® technology, Catalent has early drug development services and additional oral drug delivery solutions available for the efficient delivery of the Company's proprietary APIs.

Additionally, the Company has successfully completed our required dose response study in a rodent model of Parkinson’s disease, which will help us to establish the correct dosing for our first-in-human trial. The University of Lethbridge completed this study in February of 2023, and the final report has recently been delivered to us for our usage. Prior to filing our IND application, we must conduct ADMET testing on the clinical prototypes of our Parkinson’s medication being formulated for us by Catalent Pharma. The Company has identified a Contract Research Organization that will perform the ADMET testing. In the IND application for our novel Parkinson’s disease therapy, the ADMET testing data will be combined with the Chemistry Manufacturing and Controls (CMC) data prepared by Catalent Pharma and our proof-of-concept data (National Research Council Canada). In the near future, we expect to announce the selection of the Contract Research Organization that will write the IND-application and run the first-in-human trials for our novel treatment for the motor symptoms of Parkinson’s disease.

For its lead chronic pain program, the Company is testing its MEM for chronic pain both as encapsulated, time-released nanoparticles, as well as in non-encapsulated forms of these therapeutic mixtures in an animal model at the NRC in Halifax, Nova Scotia. In preparation for human clinical trials, our standard MEM and the time-released MEM are currently being compared in an animal model that demonstrates their potential effectiveness at treating chronic pain. The early results from this preclinical research project look very promising.

The Company received positive proof-of-concept data from a human immune cell model supporting the efficacy of their proprietary MEM designed for the suppression of COVID-related, cytokine release syndromes (CRS) while preserving key anti-viral immune responses. Based on this new positive proof-of-concept data, GBSGB converted their provisional patent application entitled, “CANNABINOID-CONTAINING COMPLEX MIXTURES FOR THE TREATMENT OF CYTOKINE RELEASE SYNDROME WHILE PRESERVING KEY ANTI-VIRAL IMMUNE REACTIONS” to a nonprovisional patent application. The best performing MEM will be further developed in preparation for clinical studies to evaluate their anti-inflammatory potential in the treatment of severely ill COVID-19 patients contending with Cytokine Release Syndrome (CRS) and associated hyperinflammatory conditions, such as macrophage activation syndrome (MAS) and acute respiratory distress syndrome (ARDS). CRS, MAS, and ARDS are the leading causes of deaths in COVID-19 patients. The Company’s proof-of-concept study was performed at Michigan State University using a state-of-the-science human immune model. In the Company’s proof-of-concept study, immune cells from human donors were co-cultured together in one of four treatment groups: untreated (no inflammatory stimulus), inflammatory stimulus, control (inflammatory stimulus + vehicle from cannabinoid mixtures), or pre-treatment with the cannabinoid mixture + inflammatory stimulus. Then a panel of cytokines and inflammatory markers was measured from each of these treatment groups from different immune cell types within the co-cultured cells at four time points to determine whether the Company’s MEMs were able to alter the levels of pro-inflammatory cytokines or other inflammatory agents. The Company’s COVID-CRS formulations showed potential for the selective inhibition of pro-inflammatory processes in response to viral- and bacterial-triggered hyperinflammation in a human immune cell model. These positive proof-of-concept results support the potential for some of these mixtures to accomplish our therapeutic goals, but, ultimately, clinical trial results will determine whether they are efficacious. The Company’s plant-based drug discovery platform is advancing biopharmaceutical research at a time when thousands are dying from COVID-19. The next step is to further develop our plant-inspired drugs and eventually bring them to human trials so that the use of well-defined cannabinoid mixtures in clinical practice can become a reality.

As mentioned above, the Company has announced that our kava-inspired formulas for anxiety have achieved statistically significant efficacy in animal proof-of-concept studies. Gb Sciences is now preparing its non-psychedelic, kava-based anxiety formulations to treat the growing global need for anxiety and depression relief. The NRC of Canada has tested our proprietary, psychotropic plant-based formulas for the treatment of depression and anxiety in preclinical animal studies. The Company has leveraged its patent-pending PhAROS™ (Phytomedical Analytics for Research Optimization at Scale) platform to identify these combinations of plant compounds for novel drug candidates to treat depression and anxiety. These are the company’s first non-cannabis formulations to achieve proof-of-concept efficacy in preclinical studies. For these novel psychotropic drug candidates, the Company used the PhAROS™ platform to identify new ingredients to improve upon an initial formulation for anxiety based on traditional medicine. The original plant mixture was derived from the kava plant, but some elements of kava are thought to cause liver toxicity. PhAROS™ identified ingredients from the Piper plant family as a substitute for the functionality of the ingredients in question without the potentially adverse safety profiles of those original ingredients. The Piper plant family includes pepper plants that are used worldwide in traditional medicines. The Global Anxiety Disorder and Depression Treatment Market size is forecast to reach USD 19.81 Billion by 2028 according to Reports & Data.

Favorable Research Updates from our university collaborators reveal the promise in our discovery programs including: 1) Multiple MEM discovery projects using and advancing our proprietary PhAROS™ drug discovery platform in conjunction with Chaminade University, 2) the Company’s Cannabis Metabolomics Project with both Chaminade University of Honolulu, Hawai’i and the University of Athens, Greece, and 3) the Company’s Time-Released Nanoparticles for Delivery of Cannabis-based Ingredients with the University of Seville, Spain and the University of Cadiz, Spain.

In the past year GBLX/GBSGB’s foreign patents for plant-based treatments of serious disorders were allowed in different countries, expanding our patent protections as follows. On February 3, 2023, GB Sciences’ first foreign patent protecting its proprietary cannabinoid-based formulations for Parkinson’s disease was issued in China. China is an increasingly important pharmaceutical market with cultural acceptance of plant-based formulations, which is a good fit for GB Sciences’ drug candidates. The global market for treatments of Parkinson’s disease is projected to grow to $8.8 billion by the year 2026, and new therapies to address Parkinson’s disease symptoms are greatly needed. The Chinese Patent was issued for GBSGB’s Cannabinoid-Containing Complex Mixtures for the treatment of Parkinson’s disease. On December 1, 2022, the Israeli (IL) Patent was allowed, protecting our Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). MCAS is a severe immunological condition in which mast cells inappropriately and excessively release inflammatory mediators, resulting in a range of severe chronic hyperinflammatory symptoms and life-threatening anaphylaxis attacks. On December 15, 2022, the Australian (AU) Patent was allowed, protecting the Company’s Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). On February 20, 2023, the Japanese (JP) Patent was allowed, protecting the Company’s Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). Additionally, on March 9, 2023, the Notice of Allowance was received for the Company’s U.S. Patent Application No. 16/878,295. This Notice of Allowance protects the use of the Company’s Myrcene-Containing Complex Mixtures in the treatment of cardiac hypertrophy, overactive bladder, and refractory chronic cough. On April 25, 2023, the Japanese patent was also issued for the use of GBSGB’s Cannabinoid-Containing Complex Mixtures in the treatment of Parkinson’s disease.

In 2021, our growing intellectual property portfolio was augmented with additional patent-protections for our PhAROS™ drug discovery platform that were filed in July of 2021 and in October of 2021. The Company, through GBSGB, also filed for protection of new PhAROS™ discovered, non-cannabis formulations in July of 2021. In September of 2021, the Company filed a patent application for the Company’s improved DCR-MEM formulations for our PD therapeutic program. These new patent applications expanded upon the solid foundation of intellectual property developed over the past six years. In 2020, the three patents which protect formulations for the Company’s lead therapeutic programs were issued by the USPTO. The issuance of U.S. Patent No. 10,653,640 entitled "Cannabinoid-Containing Complex Mixtures for the Treatment of Neurodegenerative Diseases" on May 19, 2020 protects methods of using GBSGB’s proprietary cannabinoid-containing complex mixtures (CCCM™) for treating Parkinson’s Disease. This was an important milestone in the development of these vitally important therapies and validates GBSGB’s drug discovery platform. In the US alone, the combined direct and indirect costs associated with Parkinson’s disease are estimated at $52 billion, and new therapies to address Parkinson’s disease symptoms are greatly needed. This was also the first time that a US patent has been awarded for a cannabis-based complex mixture defined using this type of drug discovery method. The first US patent for PD therapies validated our drug discovery platform and strengthened our intellectual property portfolio of unique CCCM’s™, each targeting one of up to 60 specific clinical applications.

The issuance of the Company’s second and third US patents for active pharmaceutical ingredients that are complex mixtures identified by our biotech platform further confirmed that the Company’s pharmaceutical compositions can be patent protected for use as biopharmaceutical and nutraceutical products. The US Patent entitled “Myrcene-Containing Complex Mixtures Targeting TRPV1” protects methods of using our proprietary MEMs for the treatment of pain disorders related to arthritis, shingles, irritable bowel syndrome, sickle cell disease, and endometriosis. In the US alone, chronic pain represents an estimated health burden of between $560 and $650 billion dollars, and an estimated 20.4% of U.S. adults suffer from chronic pain that significantly decreases their quality of life. Despite the widespread rates of addiction and death, opioids remain the standard of care treatment for most people with chronic pain. The Company believes that it is important to create safer, less addictive alternatives to opioids for the treatment of chronic pain disorders, like GBSGB’s myrcene-containing MEMs.

The Company's third issued US Patent entitled "Cannabinoid-Containing Complex Mixtures for the Treatment of Mast-Cell-Associated or Basophil-Mediated Inflammatory Disorders" protects methods of using the Company’s proprietary MEMs for treating Mast Cell Activation Syndrome (MCAS). MCAS is a severe immunological condition in which mast cells inappropriately and excessively release inflammatory mediators, resulting in a range of severe chronic hyperinflammatory symptoms and life-threatening anaphylaxis attacks. Receiving this patent for the treatment of MCAS using our MEMs is an important milestone in the development of this urgently needed medicine. There is no single recommended treatment for MCAS patients. Instead, they attempt to manage MCAS symptoms primarily by avoiding ‘triggers’ and using rescue medicines for their severe hyperinflammatory attacks. Therefore, MCAS patients need new therapeutic options to control their mast cell related symptoms, and our MEMs were designed to simultaneously control multiple inflammatory pathways within mast cells as a comprehensive treatment option. The Company is strategically targeting MCAS for two additional reasons. By focusing on a rare disease with no known cure, our company can apply for the U.S. Food and Drug Administration’s expedited approval process, which allows clinically successful treatments to get to market both quicker and more cost effectively. Gaining approval from the US FDA for the entire anti-inflammatory market would be extremely time consuming and cost prohibitive. Demonstrating that our MEMs are safe for the treatment of MCAS would favorably position our Company for clinical testing of these MEMs as potential treatments for other related inflammatory disorders, such as inflammatory bowel disease, thereby widening the target market and drastically shortening the development cycle and costs.

The Company’s fourth US Patent was issued on March 1, 2022 for a cannabinoid-containing mixture designed to treat cardiac hypertrophy, often present in advanced heart disease. Gb Sciences’ newly issued patent also covers the use of these receptor-targeted formulations for the treatment of TRPV1-receptor associated hearing loss and urinary cystitis. Despite multiple categories of prescription heart medications on the market, heart disease remains the leading cause of death in the United States for people of most racial and ethnic groups. Alternative therapeutic approaches are still needed, especially for the treatment of advanced heart disease. The market for prescription heart disease medications is predicted to rise to $64 billion dollars in the US by 2026, with future market growth fueled by innovative new therapeutic approaches.

Intellectual Property

GBSGB retained Fenwick & West, a Silicon Valley based law firm focusing on life sciences and high technology companies with a nationally top-ranked intellectual property practice, to develop strategies for the protection of the Company's intellectual property. The status of the intellectual property portfolio is as follows. Unless otherwise indicated, all patents listed below are assigned to the Company's wholly-owned subsidiary, GBS Global Biopharma, Inc.

Six USPTO & Five International Patents Issued; One USPTO & Three International Patents Allowed*

*Notice of Allowances received which confirms patent protection on claim set

Title: CANNABINOID-CONTAINING COMPLEX MIXTURES FOR THE TREATMENT OF NEURODEGENERATIVE DISEASES (002 Patent Family)

| U.S. Patent Number: US10653640B2 | Issued: May 19, 2020 |

| Expiration date: October 10, 2037 | Inventors: Andrea Small-Howard et al. |

| Chinese Patent Number: CN109963595B | Issued: Feb 3, 2023 |

| Expiration date: October 10, 2037 | Inventors: Andrea Small-Howard et al. |

| Japanese Patent Number: JP7225103B2 | Issued: April 25, 2023 |

| Expiration date: October 10, 2037 | Inventors: Andrea Small-Howard et al. |

On May 19, 2020, U.S. Patent protection was granted for GbS’ Cannabinoid-Containing Complex Mixtures for the treatment of Parkinson’s disease. On February 3, 2023, the Chinese Patent was issued for GbS’ Cannabinoid-Containing Complex Mixtures for the treatment of Parkinson’s disease. On April 25, 2023, the Japanese patent was issued for the use of GbS’ Cannabinoid-Containing Complex Mixtures in the treatment of Parkinson’s disease. These patents claim benefit of U.S. Patent Application No. 62/406,764 that was originally filed October 11, 2016.

Title: MYRCENE-CONTAINING COMPLEX MIXTURES TARGETING TRPV1 (005 Patent Family)

| U.S. Patent Number US10709670B2 | Issued: July 14, 2020 |

| Expiration date: May 22, 2038 | Inventors: Andrea Small-Howard, et al. |

| US Patent Application: US20200390721A1 | Allowed: March 9, 2023 |

| Expiration date: May 22, 2038 | Inventors: Andrea Small-Howard et al. |

As of July 14, 2020, GbS’ Myrcene-Containing Complex Mixtures (MCCM) are protected in the US for use in the treatment of pain related to arthritis, shingles, irritable bowel syndrome, sickle cell disease, and endometriosis. On March 9, 2023, the Notice of Allowance was received for GbS’ U.S. Patent Application No. 16/878,295, which was filed as a Continuation of Review of US Patent Application No. 15/986,316 (originally filed on May 22, 2018). The Notice of Allowance on the Continued Review Application protects the use of GbS’ MCCM in the treatment of cardiac hypertrophy, overactive bladder, and refractory chronic cough. These patents claim benefit of U.S. Patent Application No. 62/509,546 that was originally filed May 22, 2017.

Title: CANNABINOID-CONTAINING COMPLEX MIXTURES FOR THE TREATMENT OF MAST CELL-ASSOCIATED OR BASOPHIL-MEDIATED INFLAMMATORY DISORDERS (003 Patent Family)

| U.S. Patent Number US10,857,107B2 | Issued: December 8, 2020 |

| Expiration date: January 31, 2038 | Inventors: Andrea Small-Howard et al. |

| IL Patent Number: IL268211B | Allowed: December 1, 2022 |

| Expiration date: January 31, 2038 | Inventors: Andrea Small-Howard et al. |

| AU Patent Number: AU2018215200B2 | Allowed: December 15, 2022 |

| Expiration date: January 31, 2038 | Inventors: Andrea Small-Howard et al. |

| JP Patent Number: JP7225104B2 | Allowed: February 20, 2023 |

| Expiration date: January 31, 2038 | Inventors: Andrea Small-Howard et al. |

On December 8, 2020, U.S. Patent protection was granted for GbS’ Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). On December 1, 2022, the Israeli (IL) Patent was allowed, protecting GbS’ Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). On December 15, 2022, the Australian (AU) Patent was allowed, protecting GbS’ Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). On February 20, 2023, the Japanese (JP) Patent was allowed, protecting GbS’ Cannabinoid-Containing Complex Mixtures for the treatment of Mast Cell Activation Syndrome (MCAS). These patents claim benefit of U.S. Patent Application No. 62/453,161 originally filed February 1, 2017.

Title: TRPV1 ACTIVATION-MODULATING COMPLEX MIXTURES OF CANNABINOIDS AND/OR TERPENES (006 Patent Family)

| U.S. Patent Number US11260044B2 | Issued: May 1, 2022 |

| Expiration date: May 22, 2039 | Inventors: Andrea Small-Howard, et al. |

U.S. Patent coverage was granted for CBGA-containing mixtures used for the treatment of TRPV1-associated heart disease, renal cystitis, and hearing loss. This patent claims benefit of U.S. Patent Application Nos. 62/674,843 filed May 22, 2018; 62/769,743 filed November 20, 2018; and 62/849,719 filed May 17, 2019.

Title: METHODS AND COMPOSITIONS FOR PREVENTION AND TREATMENT OF CARDIAC HYPERTROPHY (050 Patent Family)

| U.S. Patent Number: US9084786B2 | Issued: July 21, 2015 |

| U.S. Patent Number: US10137123B2 | Issued: November 27, 2018 |

| European Union Patent Number: EP2635281B1 | Issued: March 14, 2018 |

| Hong Kong Patent Number: HK14102182.8B1 | Issued: March 14, 2018 |

| Inventor: Alexander Stokes | Assignee: University of Hawai’i |

GbS has sublicensed these two issued USPTO patents and two issued international patents for the prevention and treatment of heart failure due to cardiac hypertrophy through therapeutic regulation of TRPV1 from Makai Biotechnology, LLC.

Title: METHOD FOR PRODUCING A PHARMACEUTICAL COMPOSITION OF POLYMERIC NANOPARTICLES FOR TREATING NEUROPATHIC PAIN CAUSED BY PERIPHERAL NERVE COMPRESSION (008 Patent Family)

Spanish Patent: ES2582287 Issued: September 29, 2017

Expiration: February 9, 2035

Inventors: Martin Banderas, Lucia; Fernandez Arevalo, Mercedes; Berrocoso, Dominguez, Esther; and Mico Segura, Juan Antonio

Assignees: Universidad de Sevilla, Universidad de Cadiz, and Centro de Investigacion Biomedica En Red

Exclusive worldwide license held by GbS Global Biopharma, Inc. Claims benefit of Spanish Patent Application no. P201500129 (Pub. No. ES 2582287).

GbS holds the exclusive worldwide rights to commercialize the issued Spanish patent-protected, cannabinoid-containing, time-released, oral nanoparticles for the treatment of neuropathic pain.

Issued Patents

In addition to the issued patents listed above, GBSGB's intellectual property portfolio includes a total of ten USPTO and thirty-five international patents pending:

| Title |

Jurisdiction |

Application Number |

Other International Applications Filed |

Continuation of |

||||

| CANNABINOID-CONTAINING COMPLEX MIXTURES FOR THE TREATMENT OF NEURODEGENERATIVE DISEASES |

US |

USPTO 16/844,713 |

AU, CA, CN, EP, HK, IL, JP |

US15/729,565 CN202310039015.8A JP2023058599A |

||||

| MYRCENE-CONTAINING COMPLEX MIXTURES TARGETING TRPV1 |

US |

USPTO 16/878,295 |

AU, CA, CN, EP, HK, IL, JP |

US15/986,316 US16/878,295 |

||||

| CANNABINOID-CONTAINING COMPLEX MIXTURES FOR THE TREATMENT OF MAST CELL-ASSOCIATED OR BASOPHIL-MEDIATED INFLAMMATORY DISORDERS |

US |

USPTO 17/065,400 |

AU, CA, CN, EP, HK, IL, JP |

US15/885,620 |

||||

| TRPV1 ACTIVATION-MODULATING COMPLEX MIXTURES OF CANNABINOIDS AND/OR TERPENES |

US |

USPTO 16/420,004 PCT/US2019/033618 |

AU, CA, CN, EP, HK, IL, JP |

US17/576,485 |

||||

| THERAPEUTIC NANOPARTICLES ENCAPSULATING TERPENOIDS AND/OR CANNABINOIDS |

US |

USPTO 16/686,069 |

AU, CA, CN, EP, HK, IL, JP |

|||||

| TREATMENT OF PAIN USING ALLOSTERIC MODULATOR OF TRPV1 |

US |

USPTO 16/914,205 |

AU, CA, CN, EP, HK, IL, JP |

|||||

| CANNABINOID-CONTAINING COMPLEX MIXTURES FOR THE TREATMENT OF CYTOKINE RELEASE SYNDROME WHILE PRESERVING KEY ANTI-VIRAL IMMUNE REACTIONS |

US |

USPTO 17/406,035 |

AU, CA, CN, EP, HK, IL, JP |

|||||

| IN SILICO META-PHARMACOPEIA ASSEMBLY FROM NON-WESTERN MEDICAL SYSTEMS USING ADVANCED DATA ANALYTIC TECHNIQUES TO IDENTIFY AND DESIGN PHYTOTHERAPEUTIC STRATEGIES |

US |

USPTO 17/501,498 |

CA, EP, HK, KR |

| METHODS AND COMPOSITIONS FOR PREVENTION AND TREATMENT OF CARDIAC HYPERTROPHY |

US/EU |

EPO 3,348,267 |

IN, CN |

|||||

| METHOD FOR PRODUCING A PHARMACEUTICAL COMPOSITION OF POLYMERIC NANOPARTICLES FOR TREATING NEUROPATHIC PAIN CAUSED BY PERIPHERAL NERVE COMPRESSION |

WIPO/PCT |

WIPO 2016/128591 |

US, EU, CA |

|||||

| CANNABINOID-CONTAINING FORMULATIONS FOR PARKINSONIAN MOVEMENT DISORDERS |

US |

USPTO 17/501,498 PCT/US2021/055056 |

||||||

| METHODS AND COMPOSITIONS FOR THE IDENTIFICATION OF NOVEL THERAPEUTIC APPROACHES TO MIGRAINE USING THE PHAROS IN SILICO DRUG DISCOVERY PLATFORM |

US |

USPTO 63/221,334 |

||||||

| METHOD AND COMPOSITIONS FOR THE PHYTOMEDICAL COMPONENT SUPPLY CHAIN DECISION SUPPORT USING THE PHAROS IN SILICO DRUG DISCOVERY PLATFORM |

US |

Incorporated into USPTO 17/501,498 |

||||||

| METHODS AND COMPOSITIONS FOR NOVEL PAIN THERAPIES INCLUDING OPIOID-ALTERNATIVE STRATEGIES IDENTIFIED USING THE PHAROS IN SILICO DRUG DISCOVERY PLATFORM |

US |

Incorporated into USPTO 17/501,498 |

||||||

| METHODS AND COMPOSITIONS FOR NOVEL PAIN THERAPIES TARGETED TO SPECIFIC PAIN SUBTYPES IDENTIFIED USING THE PHAROS IN SILICO DRUG DISCOVERY PLATFORM |

US |

Incorporated into USPTO 17/501,498 |

||||||

| METHODS AND COMPOSITIONS DEVELOPMENT OF NOVEL THERAPEUTICS BASED ON PIPER SPECIE-CONTAINING PHYTOMEDICINES FOR ANXIETY AND ASSOCIATED DISORDERS USING THE PHAROS IN SILICO DRUG DISCOVERY PLATFORM |

US |

Incorporated into USPTO 17/501,498 |

||||||

| METHODS AND COMPOSITIONS FOR DECONVOLUTION OF COMPLEX PHYTOMEDICAL FORMULAE FOR CANCER TO IDENTIFY TARGETED STRATEGIES FOR CANCER PAIN AND CYTOTOXIC THERAPEUTIC CANDIDATES USING THE PHAROS IN SILICO DRUG DISCOVERY PLATFORM |

US |

Incorporated into USPTO 17/501,498 |

||||||

| NANOPARTICLE FORMULATIONS FOR TREATING PAIN |

US |

63/374,581 (provisional) |

||||||

| FORMULATIONS FOR TREATING CYTOKINE RELEASE SYNDROME |

US |

63/374,583 (provisional) |

||||||

| FORMULATIONS FOR TREATING ANXIETY |

US |

63/374,584 (provisional) |

Partnering Strategy

The Company runs a lean drug development program and minimizes expenses, including personnel, overhead, and fixed capital expenses (such as lab and diagnostic equipment), through strategic partnerships with universities, hospitals, suppliers, Contract Research Organizations (“CROs”), and Contract Manufacturing Organizations (“CMOs”). Through these research and development agreements, the Company has created a virtual pipeline for the further development of novel medicines based on ingredients originally derived from the cannabis plant and other plant-based traditional medicines. The partners bring both expertise and infrastructure at a reasonable cost to the life sciences program. In most instances, the Company has also negotiated with these partners to keep 100% of the ownership of the IP within GBSGB for original patent filings.

The Company currently has on-going research agreements with the following institutions covering the indicated areas of research:

Chaminade University: Broad-based research program to support the drug discovery platform that has yielded many of the Company’s original patents to date in the areas of neurodegenerative diseases, heart disease, inflammatory diseases, neuropathic and chronic pain. They have also performed the bioassay portion of the Cannabis Metabolomics study performed with the University of Athens, Greece and the Company. Our collaborations with Chaminade also led to the development of our PhAROS™ drug discovery platform.

University of Athens: Broad-based metabolomics analysis of over 100 cannabis genotypes including both hemp and THC-producing cannabis varieties, in combination with the Company’s bioassay data linking genotypes and potential disease-remediations. This project has the potential to define active ingredients from plant-derived mixtures beyond the standard cannabinoids and terpenoids. The discovery potential is huge, and novel agents have recently been discovered. Novel ligands have been identified and are being validated. This project will ultimately yield novel patent-protected therapies.

Michigan State University: Preclinical work using a cutting-edge, multi-cellular model of the human immune system and a multi-cell model of the brain to validate our MEMs for use in the treatment of COVID-19-related cytokine release syndromes (COVID-CRS). MSU has performed experiments using their novel model of the human-immune system that have allowed GBSGB to prepare cannabis-based formulas for the potential treatment of virally-induced hyperinflammation/cytokine storm syndrome that has led to the majority of COVID-19 deaths. Positive proof-of-concept results have guided the development of these selectively anti-inflammatory MEM.

The University of Lethbridge: Our research partners bring expertise in studying neurodegenerative diseases using animal models and “Home Cage Small World” assessments using cameras and Artificial Intelligence-to assess efficacy of our proprietary Minimum Essential Mixtures for the treatment of Parkinson’s disease symptoms. Our colleagues at the University of Lethbridge have recently finished the dose-response study for our Company’s cannabinoid-containing Parkinson’s disease therapies.

The University of Seville: Bringing their novel expertise to the development and functional testing of time-released and disease-targeted nanoparticles of cannabis-based minimum essential mixtures for oral administration. These specialized nanoparticles are being used for the precise and time-released delivery of several of our therapies, including the Company’s chronic pain MEMs used in the preclinical animal testing performed at the NRC Canada. The University of Seville has completed functional testing on nanoparticles containing myrcene, nerolidol, and beta-caryophyllene for our chronic pain MEMs. In cell-based assays, the effectiveness and kinetics of the nanoparticle-forms of these terpenes were compared with the “naked” terpenes both individually and in mixtures. In all cases, the effectiveness of the nanoparticles was superior to the naked terpenes, however, the mixtures were dramatically more effective than the individuals. Recently, our partners at the University of Seville have completed the formulation of new cannabis-based ingredients for inclusion into the oral, time-released nanoparticle format for the completion of our maximally effective MEMs for chronic pain. The results from Seville are very promising, and these nanoparticles have entered the animal testing phase at the NRC of Canada in Halifax.

The National Research Center (NRC) of Canada, Halifax, Nova Scotia: Three animal-phase studies are being performed by Dr. Lee Ellis’ group at the NRC of Canada. 1) Chronic Pain: The Company has re-started a safety and efficacy study in animals for our Chronic Pain (CP) formulas. The midterm results for these preclinical pain studies were promising, but the study was significantly delayed by the COVID pandemic. 2) Anxiety: We recently announced the positive performance of our plant-inspired formulas in an animal model of anxiety. 3) Depression: Minimum essential mixtures of plant-based ingredients from kava and the related Piper plant family are being evaluated now.

The University of Cadiz: Testing the safety and efficacy of the above-mentioned time-released nanoparticles in rodent models of chronic pain. Proof of concept complete for one formulation.

University of Hawaii: Validating the efficacy of a complex cannabis-based mixture for the treatment of cardiac hypertrophy and cardiac disease in a rodent model. Proof of concept work is complete in rodents, and we are seeking commercialization partners.

Path to Market: Drug Development Stages and Proposed Clinical Trials

The Company has plant-based therapeutic products in the following stages of drug development: Discovery, Pre-Clinical, and entering the Clinical Phase. It has also licensed therapeutic products that the Company intends to develop through partners, labeled Partner Programs.

The completion of discovery, preclinical studies, clinical trials, and the required regulatory submissions required for obtaining US FDA pre-market approvals for pharmaceutical products (and equivalent approvals from other corresponding agencies worldwide) is traditionally a long and expensive process. However, the Company asserts that its proprietary, PhAROS™, AI-enabled, drug discovery engine; plant-inspired formulations; lean development program; novel regulatory strategy; experienced development partners; and aggressive licensing of these products at early clinical stages can mitigate some of the risks. The Company uses a combination of in silico discovery methods and automated screening of cellular and animal models of disease to decrease the time in Discovery prior to filing novel patent applications for disease-specific therapeutics. Through GBSGB, the Company’s original patent applications cover new chemical entities (“NCE”) based on discovery and validation of minimum essential mixtures derived from complex, plant-based therapeutics. The Company plans to use an Exploratory IND/Phase 0 Program that gets the Company to First-in-Human sooner than traditional programs, which reduces translational risks, and includes preliminary efficacy measures for responsible development decisions. In contrast, a traditional phased-development path would not provide any efficacy measures until Phase II. After the completion of our Phase 0 study for PD, which compares the efficacies of multiple related cannabinoid-based formulations, the Company plans to advance the lead PD drug candidate using an adaptive trial design that is more efficient than the traditional phased-development pathway. Through GBSGB, the Company has entered into research contracts, partnerships, and/or joint ventures with several respected, independent contract research organizations, medical schools, universities, and with other scientific consultants to increase developmental efficiencies. If and when one or more of the Company’s drugs, therapies or treatments are approved by the US FDA, the Company will seek to market them under licensing arrangements with major biotechnology or pharmaceutical companies.

There can be no assurance that we will ever be able to enter into any joint ventures or other arrangements with third parties to finance our drug development program or that if we are able to do so, that any of our projected therapies will ever be approved by the US FDA. Even if we obtain US FDA approval to market one of our therapies, there can be no assurance that it could be successfully marketed or would not be superseded by another plant-based therapy produced by one or more of our competitors. It also may be anticipated that even if we enter into a joint venture development with a financially stable pharmaceutical or institutional partner, we will still be required to raise significant additional capital in the future to achieve the strategic goals of the Company. There can be no assurance that we will be able to obtain such additional capital on reasonable terms, if at all. If the Company fails to achieve its goal of producing one or more plant-inspired pharmaceuticals or therapies, it would have a material adverse effect on our future financial condition and business prospects.

Other Operations

On March 24, 2020, the Company entered into the Membership Interest Purchase Agreement ("Teco MIPA") with AJE Management, LLC. Pursuant to the Teco MIPA, the Company agreed to sell 100% of its membership interests in GB Sciences Nevada, LLC, and GB Sciences Las Vegas, LLC (the "Teco Subsidiaries") for approximately $8 million, which amount includes a cash payment at closing, the extinguishment of certain liabilities owed to the purchaser and affiliates of the purchaser, and an 8% promissory note.

On August 10, 2020, the Company entered into the Membership Interest Purchase Agreement ("Nopah MIPA") and Promissory Note Modification Agreement with 483 Management, LLC. Pursuant to the Nopah MIPA, the Company agreed to sell its 100% membership interest in GB Sciences Nopah, LLC ("Nopah"), which holds a Nevada medical marijuana cultivation certificate. As consideration, the Company would receive $300,000 as a reduction to the balance of the 0% Note payable dated October 23, 2017 and accounts payable of $74,647, which were owed to an affiliate of the purchaser.

The closing of the Teco and Nopah sales was contingent upon the successful transfer of the Nevada cultivation and production licenses. On December 14, 2021, the Company received approval from the Nevada Cannabis Compliance Board for the transfer of cannabis cultivation and extraction licenses held by its subsidiaries GB Sciences Nevada, LLC, GB Sciences Las Vegas, LLC, and GB Sciences Nopah, LLC (the "Nevada Subsidiaries"). Consequently, all conditions to closing the sales of the 100% membership interests in the Nevada Subsidiaries were satisfied, and the transactions formally closed on December 31, 2021. After the closing date, the Company retains no ownership interest in the Nevada Subsidiaries.

Competition

The biotech industry is subject to intense and increasing competition. We face potential competition from many different sources, including large pharmaceutical and biotechnology companies, specialty pharmaceutical and generic drug companies, and medical technology companies. Any product candidates that we successfully develop and commercialize will compete with existing therapies and new therapies that may become available in the future. Some of our competitors may have substantially greater capital resources, facilities and infrastructure then we have, which may enable them to compete more effectively in this market. These competitors include Cara Therapeutics Inc., Corbus Pharmaceuticals Holdings Inc., Zynerba Pharmaceuticals Inc., Tetra Bio-Pharma, Inc., Revive Therapeutics, Inc., Axim Biotechnologies, Inc., and Emerald BioScience, Inc., among others.

There are several organizations that may be developing or marketing therapies for the indications that we are pursuing. Many of our competitors, including many of the organizations named above, have substantially greater financial, technical and human resources than we do and significantly greater experience in the development of product candidates, obtaining FDA and other regulatory approvals of products and the commercialization of those products. Mergers and acquisitions in the pharmaceutical and biotechnology industries may result in even more resources being concentrated among a smaller number of competitors.

We believe the key competitive factors that will affect the development and commercial success of our product candidates, if approved for marketing, are likely to be their safety, efficacy and tolerability profile, reliability, convenience of dosing, price and reimbursement from government and third-party payers. Our commercial opportunity could be reduced or eliminated if our competitors develop and commercialize products that are safer, more effective, have fewer or less severe side effects, are more convenient or are less expensive than any products that we may develop. Our competitors also may obtain FDA or other regulatory approval for their products more rapidly than we may obtain approval for ours, which could result in our competitors establishing a strong market position before we are able to enter the market. In addition, our ability to compete may be affected in many cases by insurers or other third-party payers seeking to encourage the use of generic products. Generic products that broadly address these indications are currently on the market for the indications that we are pursuing, and additional products are expected to become available on a generic basis over the coming years. If our product candidates achieve marketing approval, we expect that they will be priced at a significant premium over competitive generic products.

Government Regulation and Federal Policy

Government authorities in the U.S. (including federal, state and local authorities) and in other countries extensively regulate, among other things, the manufacturing, research and clinical development, marketing, labeling and packaging, storage, distribution, post-approval monitoring and reporting, advertising and promotion, export and import of pharmaceutical products, such as those we are developing. The process of obtaining regulatory approvals and the subsequent compliance with appropriate federal, state, local and foreign statutes and regulations require the expenditure of substantial time and financial resources. Moreover, failure to comply with applicable regulatory requirements may result in, among other things, warning letters, clinical holds, civil or criminal penalties, recall or seizure of products, injunction, disbarment, partial or total suspension of production or withdrawal of the product from the market. Any agency or judicial enforcement action could have a material adverse effect on us.

FDA Regulation

In the U.S., the FDA regulates drugs under the Federal Food, Drug, and Cosmetic Act (“FDCA”) and its implementing regulations. Drugs are also subject to other federal, state and local statutes and regulations. The process required by the FDA before product candidates may be marketed in the U.S. generally involves the following:

●completion of extensive preclinical laboratory tests and preclinical animal studies, all performed in accordance with the FDA’s Good Laboratory Practice (“GLP”) regulations. Preclinical testing generally includes evaluation of our product candidates in the laboratory or in animals to characterize the product and determine safety and efficacy;

●submission to the FDA of an Investigational New Drug application ("IND"), which must become effective before human clinical trials may begin and must be updated annually;

●performance of adequate and well-controlled human clinical trials to establish the safety and efficacy of the product candidate for each proposed indication;

●submission to the FDA of a New Drug Application ("NDA") after completion of all pivotal clinical trials;

●a determination by the FDA within 60 days of its receipt of an NDA to file the NDA for review;

●satisfactory completion of an FDA pre-approval inspection of the manufacturing facilities at which the active pharmaceutical ingredient (“API”) and finished drug product are produced and tested to assess compliance with cGMP regulations;

●satisfactory completion of an FDA pre-approval inspection of one or more of the clinical sites at which the clinical trials were conducted;

●at the discretion of the FDA, a public Advisory Committee Meeting where the data is reviewed by experts who discuss the data and give their opinion (which the FDA is not obliged to follow) of the adequacy of the data to support an approval; and

●FDA review and approval of an NDA prior to any commercial marketing or sale of the drug in the U.S.

We rely and expect to continue to rely on third parties for the production, distribution, shipping and storage of clinical and commercial quantities of our product candidates. Future FDA and state inspections may identify compliance issues at the facilities of our contract manufacturers that may disrupt production or distribution or require substantial resources to correct. In addition, discovery of previously unknown problems with a product or the failure to comply with applicable requirements may result in restrictions on a product, manufacturer or holder of an approved NDA, including withdrawal or recall of the product from the market or other voluntary, FDA-initiated or judicial action that could delay or prohibit further marketing. Newly discovered or developed safety or effectiveness data may require changes to a product’s approved labeling, including the addition of new warnings and contraindications, and also may require the implementation of other risk management measures. Also, new government requirements, including those resulting from new legislation, may be established, or the FDA’s policies may change, which could delay or prevent regulatory approval of our product candidates under development.

In addition to regulations in the U.S., we will be subject to a variety of regulations in other jurisdictions governing, among other things, clinical trials and any commercial sales and distribution of our products. Whether or not we obtain FDA approval for a product, we must obtain the requisite approvals from regulatory authorities in foreign countries prior to the commencement of clinical trials or marketing of the product in those countries. Certain countries outside of the U.S. have a similar process that requires the submission of a clinical trial application much like the IND prior to the commencement of human clinical trials. In Europe, for example, a clinical trial application (“CTA”) must be submitted to each country’s national health authority and an independent ethics committee, much like the FDA and IRB, respectively. Once the CTA is approved in accordance with a country’s requirements, clinical trial development may proceed.

The requirements and process governing the conduct of clinical trials, product licensing, pricing and reimbursement vary from country to country. In all cases, the clinical trials are conducted in accordance with GCP and the applicable regulatory requirements and the ethical principles that have their origin in the Declaration of Helsinki.

To obtain regulatory approval of an investigational drug under European Union regulatory systems, we must submit a marketing authorization application. The application used to file the NDA in the U.S. is similar to that required in Europe, with the exception of, among other things, country-specific document requirements. For other countries outside of the European Union, such as countries in Eastern Europe, Latin America or Asia, the requirements governing the conduct of clinical trials, product licensing, pricing and reimbursement vary from country to country. In all cases, again, the clinical trials are conducted in accordance with GCP and the applicable regulatory requirements and the ethical principles that have their origin in the Declaration of Helsinki.

If we fail to comply with applicable foreign regulatory requirements, we may be subject to, among other things, fines, suspension or withdrawal of regulatory approvals, product recalls, seizure of products, operating restrictions and criminal prosecution.

Cannabis Regulation

Although the Company has completely divested of its cannabis cultivation and production facilities effective December 31, 2021, the Company has owned and operated subsidiaries that were involved in the manufacturing and distribution of cannabis products under State law. These operations were subject to prohibition under United States federal law.

Under the Controlled Substances Act (“CSA”), the policies and regulations of the Federal government and its agencies are that cannabis (marijuana) is a Schedule 1 narcotic that is addictive and has no medical benefit. Accordingly, and a range of activities including cultivation and the personal use of cannabis is prohibited and subject to prosecution and criminal penalties. Unless and until Congress amends the CSA with respect to medical cannabis, there is a risk that the federal authorities may enforce current federal law, and we may be deemed to have engaged in producing, cultivating, or dispensing cannabis in violation of federal law, or we may be deemed to have facilitated the sale or distribution of drug paraphernalia in violation of federal law with respect to our Company’s divested business operations. Active enforcement of the current federal regulatory position on cannabis may thus indirectly and adversely affect our strategic goals, revenues and profits. The risk of strict enforcement of the CSA in light of Congressional activity, judicial holdings, and stated federal policy remains uncertain. See “Risk Factors” below. The U.S. Supreme Court declined to hear a case brought by San Diego County, California that sought to establish federal preemption over state medical cannabis laws. The preemption claim was rejected by every court that reviewed the case. The California 4th District Court of Appeals wrote in its unanimous ruling, “Congress does not have the authority to compel the states to direct their law enforcement personnel to enforce federal laws.” However, in another case, the U.S. Supreme Court held that, as long as the CSA contains prohibitions against cannabis, under the Commerce Clause of the United States Constitution, the United States may criminalize the production and use of cannabis even where states approve its use for medical purposes.