Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE |

| ACT | OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF |

| 1934 |

For the fiscal year ended 31 March 2013

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF |

| 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE |

| ACT | OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number 1-15240

JAMES HARDIE INDUSTRIES plc

Formerly Known As James Hardie Industries SE

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Ireland

(Jurisdiction of incorporation or organisation)

Europa House, Second Floor

Harcourt Centre

Harcourt Street, Dublin 2, Ireland

(Address of principal executive offices)

Marcin Firek

(Contact name)

353 1411 6924 (Telephone) 353 1479 1128 (Facsimile)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class: |

Name of each exchange on which registered: | |

| Common stock, represented by CHESS Units of Foreign Securities | New York Stock Exchange* | |

| CHESS Units of Foreign Securities | New York Stock Exchange* | |

| American Depositary Shares, each representing five units of CHESS Units of Foreign Securities | New York Stock Exchange |

Table of Contents

| * | Listed, not for trading, but only in connection with the registered American Depositary Shares, pursuant to the |

| requirements | of the Securities and Exchange Commission |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report 441,644,484 shares of common stock at 31 March 2013.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Note — Checking the box will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See the definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP x | International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

Table of Contents

| Page |

||||

| iii | ||||

| 1 | ||||

| 1 | ||||

| 1 | ||||

| 4 | ||||

| 4 | ||||

| 6 | ||||

| 15 | ||||

| 15 | ||||

| 20 | ||||

| 23 | ||||

| 28 | ||||

| 65 | ||||

| 85 | ||||

| 85 | ||||

| 87 | ||||

| 115 | ||||

| 121 | ||||

| Remuneration of Independent Registered Public Accounting Firm |

166 | |||

| 167 | ||||

| 168 | ||||

| 168 | ||||

| 184 | ||||

| 192 | ||||

| 197 | ||||

| 198 | ||||

| 201 | ||||

| 209 | ||||

| 209 | ||||

| 210 | ||||

| 218 | ||||

| 220 | ||||

| 222 | ||||

| 222 | ||||

| 225 | ||||

| 231 | ||||

| 236 | ||||

In this annual report, unless the context otherwise indicates, James Hardie Industries plc, a “public limited company,” or a European company incorporated and existing under the laws of Ireland, is referred to as JHI plc. JHI plc together with its direct and indirect wholly owned subsidiaries as of the time relevant to the applicable reference, are collectively referred to as the James Hardie Group. JHI plc and its current direct and indirect wholly owned subsidiaries are collectively referred to as “we,” “us,” “our,” “JHI plc and its wholly owned subsidiaries”, “James Hardie” or the “Company.”

| James Hardie FY 2013 20-F |

i |

Table of Contents

For certain information about the basis of preparing the financial information in this Annual Report, see Section 2, “Reading this Report.” In addition, this Annual Report contains statements that constitute “forward-looking statements”. For an explanation of forward-looking statements and the risks, uncertainties and assumptions to which they are subject, see Section 2, “Reading this Report.”

A “Glossary of Abbreviations and Definitions” has also been included under Section 4 of this Annual Report.

Information contained in or accessible through the websites mentioned in this Annual Report does not form part of this report unless we specifically state that it is incorporated by reference and forms part of this report. All references in this report to websites are inactive textual references and are for information only.

| James Hardie FY 2013 20-F |

ii |

Table of Contents

FORM 20-F CROSS REFERENCE INDEX

| 20-F Item Number and Description |

Page |

|||

| PART 1 |

||||

| Item 1. Identity of Directors, Senior Management and Advisers |

Not applicable | |||

| Item 2. Offer Statistics and Expected Timetable |

Not applicable | |||

| Item 3. Key Information |

||||

| A. Selected Financial Data |

1-4 |

| B. Capitalisation and Indebtness |

Not applicable | |||

| C. Reasons for the Offer and Use of Proceeds |

Not applicable |

| D. Risk Factors |

168-184 |

| Item 4. Information on the Company |

| A. History and Development of the Company |

4-6; 18-19 |

| B. Business Overview |

6-14 |

| C. Organisational Structure |

5; 15 |

| D. Property, Plants and Equipment |

15-19; 111 |

| Item 4A. Unresolved Staff Comments |

None |

| Item 5. Operating and Financial Review and Prospects |

| A. Operating Results |

94-106 |

| B. Liquidity and Capital Resources |

107-113 |

| C. Research and Development, Patents and Licenses, etc |

13; 114 |

| D. Trend Information |

114 | |||

| E. Off-Balance Sheet Arrangements |

114 | |||

| F. Tabular Disclosure of Contractual Obligations |

113 |

| G. Safe Harbor |

85-86 |

| Item 6. Directors, Senior Management and Employees |

| A. Directors and Senior Management |

20-27 | |||

| B. Compensation |

28-64 |

| C. Board Practices |

23-27; 65-73 |

| D. Employees |

197-198 |

| E. Share Ownership |

49-52; 57-64 |

| Item 7. Major Shareholders and Related Party Transactions |

||||

| A. Major Shareholders |

222-223 |

| B. Related Party Transactions |

68-69 | |||

| C. Interests of Experts and Counsel |

None |

| Item 8. Financial Information |

||||

| A. Consolidated Statements and Other Financial Information |

115-165; 184-192; 205-206 |

| B. Significant Changes |

None |

| Item 9. The Offer and Listing |

| A. Offer and Listing Details |

198-199 |

| B. Plan of Distribution |

Not Applicable |

| C. Markets |

199-200 |

| D. Selling Shareholders |

Not Applicable | |||

| E. Dilution |

Not Applicable | |||

| F. Expenses of the Issue |

Not Applicable |

| Item 10. Additional Information |

| A. Share Capital |

Not Applicable |

| B. Memorandum and Articles of Association |

201-208 | |||

| C. Material Contracts |

209 |

| D. Exchange Controls |

209-210 |

| James Hardie FY 2013 20-F |

iii |

Table of Contents

| 20-F Item Number and Description |

Page |

|||

| E. Taxation |

210-217 | |||

| F. Dividends and paying agents |

Not Applicable | |||

| G. Statement by Experts |

Not Applicable |

| H. Documents on Display |

217 |

| I. Subsidiary Information |

Not Applicable |

| Item 11. Quantitative and Qualitative Disclosures About Market Risk |

218-220 |

| Item 12. Description of Securities Other Than Equity Securities |

||||

| A. Debt Securities |

Not Applicable | |||

| B. Warrants and Rights |

Not Applicable | |||

| C. Other Securities |

Not Applicable |

| D. American Depositary Shares |

220-221 | |||

| PART II |

||||

| Item 13. Defaults, Dividend Arrearages and Delinquencies |

None | |||

| Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds |

None | |||

| Item 15. Controls and Procedures |

78-81 |

| Item 16A. Audit Committee Financial Expert |

71 | |||

| Item 16B. Code of Business Conduct and Ethics |

73 |

| Item 16C. Principal Accountant Fees and Services |

166 |

| Item 16D. Exemptions from the Listing Standards for Audit Committees |

None | |||

| Item 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

None | |||

| Item 16F. Change in Registrant’s Certifying Accountant |

None |

| Item 16G. Corporate Governance |

83-84 |

| Item 16H. Mine Safety Disclosures |

17 | |||

| PART III |

||||

| Item 17. Financial Statements |

Not Applicable |

| Item 18. Financial Statements |

115-165 | |||

| Item 19. Exhibits |

231-235 |

| James Hardie FY 2013 20-F |

iv |

FORM 20-F CROSS REFERENCE INDEX

(Continued)

Table of Contents

The Company is a world leader in manufacturing fibre cement siding and backerboard. Our current primary geographic markets include the United States (“US”), Australia, New Zealand, the Philippines, Europe and Canada.

Our fibre cement products are used in a number of markets, including new residential construction, manufactured housing, repair and remodeling and a variety of commercial and industrial applications.

We manufacture numerous types of fibre cement products with a variety of patterned profiles and surface finishes for a range of applications, including external siding and soffit lining, internal linings, facades and floor and tile underlay.

We employ approximately 2,700 people and generated net sales of US$1.3 billion in fiscal year 2013.

We have included in this annual report the audited consolidated financial statements of the Company, consisting of our consolidated balance sheets as of 31 March 2013 and 2012, and our consolidated statements of operations and comprehensive income (loss), changes in shareholders’ equity (deficit) and cash flows for each of the years ended 31 March 2013, 2012 and 2011, together with the related notes thereto. The consolidated financial statements included in this annual report have been prepared in accordance with accounting principles generally accepted in the US, or “US GAAP.”

The selected consolidated financial information summarised below for the five most recent fiscal years has been derived in part from the Company’s financial statements. You should read the selected consolidated financial information in conjunction with the Company’s financial statements and related notes contained in Section 2, “Consolidated Financial Statements” and with the information provided in Section 2, “Management’s Discussion and Analysis.” Historic financial data is not necessarily indicative of our future results and you should not unduly rely on it.

| James Hardie FY 2013 20-F |

1 |

Table of Contents

| Fiscal Year ended 31 March | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (In millions of US dollars except sales price per unit and per share data) | ||||||||||||||||||||

| Consolidated Statements of Operations Data: | ||||||||||||||||||||

| Net Sales USA and Europe Fibre Cement1 |

$ | 951.4 | $ | 862.0 | $ | 814.0 | $ | 828.1 | $ | 929.3 | ||||||||||

| Asia Pacific Fibre Cement2 |

369.9 | 375.5 | 353.0 | 296.5 | 273.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total net sales |

$ | 1,321.3 | $ | 1,237.5 | $ | 1,167.0 | $ | 1,124.6 | $ | 1,202.6 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (loss)3 |

$ | 29.5 | $ | 155.5 | $ | 104.7 | $ | (21.0 | ) | $ | 173.6 | |||||||||

| Interest expense |

(5.5 | ) | (11.2 | ) | (9.0 | ) | (7.7 | ) | (11.2 | ) | ||||||||||

| Interest income |

7.9 | 3.8 | 4.6 | 3.7 | 8.2 | |||||||||||||||

| Other income (expense)4 |

1.8 | 3.0 | (3.7 | ) | 6.3 | (14.8 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations before income taxes |

33.7 | 151.1 | 96.6 | (18.7 | ) | 155.8 | ||||||||||||||

| Income tax benefit (expense)5 |

11.8 | 453.2 | (443.6 | ) | (66.2 | ) | (19.5 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations |

$ | 45.5 | $ | 604.3 | $ | (347.0 | ) | $ | (84.9 | ) | $ | 136.3 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | 45.5 | $ | 604.3 | $ | (347.0 | ) | $ | (84.9 | ) | $ | 136.3 | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from operations per common share — basic |

$ | 0.10 | $ | 1.39 | $ | (0.80 | ) | $ | (0.20 | ) | $ | 0.32 | ||||||||

| Net income (loss) per common share — basic |

$ | 0.10 | $ | 1.39 | $ | (0.80 | ) | $ | (0.20 | ) | $ | 0.32 | ||||||||

| Income (loss) from operations per common share — diluted |

$ | 0.10 | $ | 1.38 | $ | (0.80 | ) | $ | (0.20 | ) | $ | 0.31 | ||||||||

| Net income (loss) per common share — diluted |

$ | 0.10 | $ | 1.38 | $ | (0.80 | ) | $ | (0.20 | ) | $ | 0.31 | ||||||||

| Dividends paid per share |

$ | 0.43 | $ | 0.04 | $ | — | $ | — | $ | 0.08 | ||||||||||

| Weighted average number of common shares outstanding |

||||||||||||||||||||

| Basic |

439.2 | 436.2 | 435.6 | 433.1 | 432.3 | |||||||||||||||

| Diluted |

440.6 | 437.9 | 435.6 | 433.1 | 434.5 | |||||||||||||||

| Consolidated Cash Flow Information: | ||||||||||||||||||||

| Cash flows provided by (used in) operating activities |

$ | 109.3 | $ | 387.2 | $ | 147.2 | $ | 183.1 | $ | (45.2 | ) | |||||||||

| Cash flows used in investing activities |

$ | (59.7 | ) | $ | (49.9 | ) | $ | (49.6 | ) | $ | (50.5 | ) | $ | (26.1 | ) | |||||

| Cash flows (used in) provided by financing activities |

$ | (158.7 | ) | $ | (84.4 | ) | $ | (89.7 | ) | $ | (159.0 | ) | $ | 25.0 | ||||||

| Other Data: | ||||||||||||||||||||

| Depreciation and amortisation |

$ | 61.2 | $ | 65.2 | $ | 62.9 | $ | 61.7 | $ | 56.4 | ||||||||||

| Adjusted EBITDA6 |

$ | 90.7 | $ | 220.7 | $ | 167.6 | $ | 40.7 | $ | 230.0 | ||||||||||

| Capital expenditures |

$ | 61.1 | $ | 35.8 | $ | 50.3 | $ | 50.5 | $ | 26.1 | ||||||||||

| Volume (million square feet) |

||||||||||||||||||||

| USA and Europe Fibre Cement1 |

1,488.5 | 1,331.8 | 1,248.0 | 1,303.7 | 1,526.6 | |||||||||||||||

| Asia Pacific Fibre Cement2 |

393.7 | 392.3 | 407.8 | 389.6 | 390.6 | |||||||||||||||

| Average sales price per unit (per thousand square feet) |

||||||||||||||||||||

| USA and Europe Fibre Cement1 |

US$ | 639 | US$ | 647 | US$ | 652 | US$ | 635 | US$ | 609 | ||||||||||

| Asia Pacific Fibre Cement2 |

A$ | 911 | A$ | 916 | A$ | 916 | A$ | 894 | A$ | 879 | ||||||||||

| James Hardie FY 2013 20-F |

2 |

Table of Contents

| Fiscal Year ended 31 March | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (Millions of US dollars) | ||||||||||||||||||||

| Consolidated Balance Sheet Data: | ||||||||||||||||||||

| Net current assets7 |

$ | 373.7 | $ | 463.3 | $ | 126.9 | $ | 50.4 | $ | 137.7 | ||||||||||

| Total assets |

$ | 2,107.6 | $ | 2,310.0 | $ | 1,960.6 | $ | 2,178.8 | $ | 1,891.7 | ||||||||||

| Total debt8 |

$ | — | $ | 30.9 | $ | 59.0 | $ | 154.0 | $ | 324.0 | ||||||||||

| Common stock |

$ | 227.3 | $ | 224.0 | $ | 222.5 | $ | 221.1 | $ | 219.2 | ||||||||||

| Shareholders’ equity (deficit) |

$ | 18.2 | $ | 126.4 | $ | (454.5 | ) | $ | (117.9 | ) | $ | (108.7 | ) | |||||||

| 1 | On 1 April 2008, the Company realigned its operating segments by combining the previously reported segments of USA Fibre Cement and Other into one operating segment, USA and Europe Fibre Cement. The USA and Europe Fibre Cement segment manufactures fibre cement interior linings, exterior siding and related accessory products in the United States which are sold in the United States, Canada and Europe. |

| The segment also includes fibre reinforced concrete pipes manufactured and sold in the United States (through May 2008). Our Plant City, Florida Hardie Pipe Plant was closed and the business ceased operations in May 2008. |

| 2 | The Asia Pacific Fibre Cement segment includes all fibre cement manufactured in Australia, New Zealand and the Philippines and sold in Australia, New Zealand, Asia, the Middle East (Israel, Kuwait, Qatar and United Arab Emirates) and various Pacific Islands. |

| 3 | Operating income (loss) includes the following asbestos adjustments, Asbestos Injuries Compensation Fund (“AICF”) SG&A expenses, Australian Securities and Investments Commission (“ASIC”) related (expenses) recoveries, asset impairment charges, and New Zealand product liability expenses: |

| Fiscal Years Ended 31 March | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (Millions of US dollars) | ||||||||||||||||||||

| (Unfavourable) favourable asbestos adjustments |

$ | (117.1 | ) | $ | (15.8 | ) | $ | (85.8 | ) | $ | (224.2 | ) | $ | 17.4 | ||||||

| AICF SG&A expenses |

$ | (1.7 | ) | $ | (2.8 | ) | $ | (2.2 | ) | $ | (2.1 | ) | $ | (0.7 | ) | |||||

| ASIC related (expenses) recoveries |

$ | (2.6 | ) | $ | (1.1 | ) | $ | 8.7 | $ | (3.4 | ) | $ | (14.0 | ) | ||||||

| Asset impairments |

$ | (16.9 | ) | $ | (14.3 | ) | $ | — | $ | — | $ | — | ||||||||

| New Zealand product liability expenses9 |

$ | (13.2 | ) | $ | (5.4 | ) | $ | — | $ | — | $ | — | ||||||||

| For additional information on the asbestos adjustments, AICF SG&A expenses, ASIC related (expenses) recoveries, asset impairment charges and New Zealand product liability expenses, see Section 2, “Management’s Discussion and Analysis” and Notes 7, 11 and 13 to our consolidated financial statements in Section 2. |

| 4 | Other income (expense) in fiscal years 2013, 2012 and 2011 are due to changes in the fair value of interest rate swap contracts. Other income in fiscal year 2010 primarily includes a realised gain arising from the sale of restricted short-term investments held by AICF. Other expense in fiscal year 2009 consists of an other-than-temporary impairment charge related to restricted short-term investments held by AICF of US$14.8 million. For additional information see Section 2, “Management’s Discussion and Analysis — Results of Operations.” |

| 5 | Income tax benefit in fiscal year 2012 includes a benefit of US$485.2 million recognised upon RCI’s successful appeal of the Australian Taxation Office’s (“ATO”) disputed 1999 amended tax assessment. Income tax expense in fiscal year 2011 includes a charge of US$345.2 million resulting from the dismissal by the Federal Court of Australia of RCI’s appeal of the ATO’s disputed 1999 amended tax assessment. |

| 6 | Adjusted EBITDA represents income from operations before interest income, interest expense, income taxes, other non-operating income (expense), described in footnote four above, and depreciation and amortisation charges. The following table presents a reconciliation of Adjusted EBITDA to net cash provided by (used in) operating activities, as this is the most directly comparable GAAP financial measure to Adjusted EBITDA for each of the periods indicated. Items comprising “Net cash provided by (used in) operating activities,” “Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities” and “Change in operating assets and liabilities, net” for fiscal years ended 31 March 2013, 2012 and 2011 are set forth in the consolidated statements of cash flows in Section 2 of this report. |

| James Hardie FY 2013 20-F |

3 |

Table of Contents

| Fiscal Years Ended 31 March | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| (Millions of US dollars) | ||||||||||||||||||||

| Net cash provided by (used in) operating activities |

$ | 109.3 | $ | 387.2 | $ | 147.2 | $ | 183.1 | $ | (45.2 | ) | |||||||||

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities |

(145.9 | ) | (114.4 | ) | (136.8 | ) | (312.0 | ) | (3.5 | ) | ||||||||||

| Change in operating assets and liabilities, net |

82.1 | 331.5 | (357.4 | ) | 44.0 | 185.0 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

45.5 | 604.3 | (347.0 | ) | (84.9 | ) | 136.3 | |||||||||||||

| Income tax (benefit) expense |

(11.8 | ) | (453.2 | ) | 443.6 | 66.2 | 19.5 | |||||||||||||

| Interest expense |

5.5 | 11.2 | 9.0 | 7.7 | 11.2 | |||||||||||||||

| Interest income |

(7.9 | ) | (3.8 | ) | (4.6 | ) | (3.7 | ) | (8.2 | ) | ||||||||||

| Other (income) expense |

(1.8 | ) | (3.0 | ) | 3.7 | (6.3 | ) | 14.8 | ||||||||||||

| Depreciation and amortisation |

61.2 | 65.2 | 62.9 | 61.7 | 56.4 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 90.7 | $ | 220.7 | $ | 167.6 | $ | 40.7 | $ | 230.0 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA is not a measure of financial performance under US GAAP and should not be considered an alternative to, or more meaningful than, income from operations, net income or net cash provided by (used in) operating activities, as defined by US GAAP, or as a measure of our profitability or liquidity. Not all companies calculate Adjusted EBITDA in the same manner as we have and, accordingly, Adjusted EBITDA may not be comparable with other companies. We have included information concerning Adjusted EBITDA because we believe that this data is commonly used by investors to evaluate the ability of a company’s earnings from its core business operations to satisfy its debt, capital expenditure and working capital requirements. To permit evaluation of this data on a consistent basis from period to period, Adjusted EBITDA has been adjusted for non-cash charges, as well as non-operating income and expense items. |

| 7 | Total current assets less total current liabilities. |

| 8 | Total debt at 31 March 2012 represents the amount owed by AICF under a secured standby loan facility with the government of New South Wales (“Facility”). On 3 April 2012, all amounts outstanding under the AICF loan facility were fully repaid. Because the Company consolidates AICF due to pecuniary and contractual interests in AICF as a result of the funding arrangements outlined in the Amended and Restated Final Funding Agreement (“AFFA”), any drawings, repayments or payments of accrued interest by AICF under the Facility impact the Company’s consolidated financial position, results of operations and cash flows. James Hardie Industries plc and its wholly-owned subsidiaries are not a party to, guarantor of, or security provider in respect of the Facility. |

| 9 | The Company began separately disclosing New Zealand product liability expenses in fiscal year 2013 and did so for fiscal year 2012 for comparative purposes only. |

History and Development of the Company

The Company was established in 1888 as an import business. In 1951, the Company became publicly owned as a listed company on the Australian Stock Exchange. After becoming a listed company, the Company built up a diverse portfolio of building and industrial products including a wide range of asbestos-based products. In the mid-1980s, we pioneered the development of asbestos-free fibre cement technology and began designing and manufacturing a wide range of fibre cement building products that made use of the benefits that came from the products’ durability, versatility and strength. Using the technical and manufacturing expertise developed in Australia, we expanded our operations, in particular to the United States, to become a specialised manufacturer of a wide range of fibre cement building materials.

| James Hardie FY 2013 20-F |

4 |

Table of Contents

Our legal name was changed to James Hardie Industries N.V. from RCI Netherlands Holdings B.V. in July 2001 when our legal form was converted from a “besloten vennootschap met beperkte aansprakelijkheid” (“B.V.”), to a “naamloze vennootschap” ( “N.V.”), or a public limited liability company whose stock, unlike a private limited liability company, may be transferred without executing a notarial deed if such company is listed on a recognised stock exchange. In February 2001, the shareholders of James Hardie Industries Limited (“JHIL”) agreed to exchange their shares for shares in James Hardie Industries N.V., which retained its primary listing on the Australian Securities Exchange (“ASX”). In February 2010, our legal name was changed to James Hardie Industries SE when our legal form was converted from a Dutch N.V. to a Dutch Societas Europaea (“SE”) in connection with the implementation of Stage 1 of a two-stage re-domicile proposal (together, the “re-domicile”) to change our registered corporate domicile from The Netherlands to Ireland. On 17 June 2010, we implemented Stage 2 of the re-domicile and changed our registered corporate domicile to Ireland to become an Irish SE and became an Irish tax resident on 29 June 2010. On 15 October 2012, we converted from an Irish SE into an Irish public limited company (“plc”).

We conduct our operations under legislation in various jurisdictions. As an Irish plc we are governed by the Irish Companies Acts. In addition, we operate under the regulatory requirements of numerous jurisdictions and organisations, including the ASX, ASIC, the New York Stock Exchange (“NYSE”), the United States Securities and Exchange Commission (“SEC”), the Irish Takeover Panel and various other rulemaking bodies.

Our corporate domicile is located in Ireland. The address of our registered office in Ireland is Europa House, Second Floor, Harcourt Centre, Harcourt Street, Dublin 2, Ireland. The telephone number there is +353 1411 6924. Our agent in the United States is CT Corporation. Its office is located at 3 Winners Circle, 3rd Floor, Albany, New York 12205.

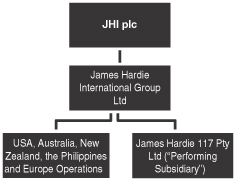

Corporate Restructuring

On 17 May 2011, we announced that we had commenced an internal reorganisation involving the simplification of our corporate structure, including some of the arrangements which were previously part of our Netherlands domicile. This internal reorganisation is being made to facilitate the ability to access and distribute surplus cash flows and earnings of our operating subsidiaries more efficiently, including for the purpose of making periodic contributions to AICF. As part of this restructure, the Company incurred a tax charge of US$32.6 million on undistributed earnings of its US subsidiaries during fiscal year 2011, related to the remittance of US earnings as part of the internal reorganisation.

The following is a simplified diagram of our current corporate structure:

| James Hardie FY 2013 20-F |

5 |

Table of Contents

Consolidation of AICF

In February 2007, our shareholders approved the AFFA entered into on 21 November 2006 to provide long-term funding to AICF. JHI plc owns 100% of James Hardie 117 Pty Ltd (the “Performing Subsidiary”) that funds AICF subject to the provisions of the AFFA. We appoint three of AICF’s directors and the New South Wales (“NSW”) Government appoints two of AICF’s directors.

Under the terms of the AFFA, the Performing Subsidiary has an obligation to make payments to AICF on an annual basis. The amount of these annual payments is dependent on several factors, including our free cash flow (as defined in the AFFA), actuarial estimations, actual claims paid, operating expenses of AICF and the annual cash flow cap. JHI plc guarantees the Performing Subsidiary’s obligation. As a result, for purposes of US GAAP, we consider JHI plc to be the primary beneficiary of AICF.

Although we have no legal ownership in AICF, for financial reporting purposes, our interest in AICF is considered variable and we consolidate AICF due to our pecuniary and contractual interests in AICF as a result of the funding arrangements outlined in the AFFA. Our consolidation of AICF results in a separate recognition of the asbestos liability and certain other asbestos-related assets and liabilities on our consolidated balance sheet. Among other items, we record a deferred tax asset for the anticipated future tax benefit we believe is available to us that arises from amounts contributed to the asbestos fund by the Performing Subsidiary. Since fiscal year 2007, movements in the asbestos liability arising from changes in foreign currency or actuarial adjustments are classified as asbestos adjustments, and the income tax benefit arising from contributions to AICF is included within income tax benefit (expense) on our consolidated statements of operations and comprehensive income (loss) when realised. See Note 2 to our consolidated financial statements in Section 2.

General Overview of our Business

Based on net sales, we believe we are the largest manufacturer of fibre cement products and systems for internal and external building construction applications in the United States, Australia, New Zealand, and the Philippines. We market our fibre cement products and systems under various Hardie brand names, such as HardieBacker® boards, and other brand names such as Artisan® Lap and ArtisanTM Accent Trim by James Hardie, Cemplank® and Prevail® siding (we also formerly marketed siding under the brand name SentryTM siding), and Scyon™ advanced lightweight cement composite products such as Scyon™ Stria™ cladding. We believe that, in certain applications, our fibre cement products and systems provide a combination of distinctive performance, design and cost advantages when compared to other fibre cement products and alternative products and systems that use solid wood, engineered wood, vinyl, brick, stucco or gypsum wallboard. The sale of fibre cement products in the United States accounted for 70%, 67% and 68% of our total net sales in fiscal years 2013, 2012 and 2011, respectively.

Our fibre cement products are used in a number of markets, including new residential construction (single and multi-family housing), manufactured housing (mobile and pre-fabricated homes), repair and remodeling and a variety of commercial and industrial applications (stores, warehouses, offices, hotels, motels, schools, libraries, museums, dormitories, hospitals, detention facilities, religious buildings and gymnasiums). We manufacture numerous types of fibre cement products with a variety of patterned profiles and surface finishes for a range of applications, including external siding and soffit lining, internal linings, facades, and floor and tile underlayments.

| James Hardie FY 2013 20-F |

6 |

Table of Contents

In contrast to some other building materials, fibre cement provides durability attributes, such as strong resistance to moisture, fire, impact and termites, requires relatively little maintenance and can be used as a substrate to create a wide variety of architectural effects with textured and colored finishes.

The breakdown of our net sales by operating segment for each of our last three fiscal years is as follows:

| Fiscal Year Ended 31 March | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Millions of US dollars) | ||||||||||||

| USA and Europe Fibre Cement |

$ | 951.4 | $ | 862.0 | $ | 814.0 | ||||||

| Asia Pacific Fibre Cement |

369.9 | 375.5 | 353.0 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

$ | 1,321.3 | $ | 1,237.5 | $ | 1,167.0 | ||||||

|

|

|

|

|

|

|

|||||||

Industry Overview

US Housing Industry and Fibre Cement Industry

In the United States, fibre cement is principally used in the residential building industry. Such usage fluctuates based on the level of new home construction and the repair and remodeling of existing homes. The level of activity is generally a function of interest rates and the availability of financing to homeowners to purchase a new home or make improvements to their existing homes, inflation, unemployment levels, demographic trends, gross domestic product growth and consumer confidence. Demand for building products is also affected by residential housing starts and existing home sales, the age and size of the housing stock and overall home improvement expenditures. According to the US Census Bureau, single family housing starts, which are one of the key drivers of the Company’s performance, were up 27% to 565,900 for fiscal year 2013, compared to fiscal year 2012.

In the United States, the largest application for fibre cement products is in the external siding industry. Siding is a component of every building and it usually occupies more square footage than any other external building component, such as windows and doors. Selection of siding material is based on installed cost, durability, aesthetic appeal, strength, weather resistance, maintenance requirements and cost, insulating properties and other features. Different regions of the United States show a decided preference amongst siding materials according to economic conditions, weather, materials availability and local preference. The principal siding materials are vinyl, stucco, fibre cement, solid wood and brick. Vinyl has the largest share of the siding market.

International Fibre Cement Industry

In Australia and New Zealand, fibre cement building products are used in both the residential and commercial building industries with applications in external siding, internal walls, ceilings, floors, soffits and fences. The residential building industry represents the principal market for fibre cement products. We believe the level of activity in this industry is generally a function of interest rates, inflation, unemployment levels, demographic trends, gross domestic product growth and consumer confidence. Demand for fibre cement building products is also affected by the level of new housing starts and renovation activity.

Fibre cement products have, across a range of product applications, gained broader acceptance in Australia and New Zealand than in the United States, primarily due to earlier introduction in Australia and New Zealand.

| James Hardie FY 2013 20-F |

7 |

Table of Contents

Australia

According to the Australian Bureau of Statistics total dwelling commencements in Australia increased from 146,500 in calendar year 2011 to 148,000 in calendar year 2012 and detached houses decreased from 91,800 in calendar year 2011 to 89,200 in calendar year 2012. Renovation activity, as measured by the Australian Bureau of Statistics by construction work done, has decreased approximately 10% from calendar year 2011 to calendar year 2012. The Housing Industry Association of Australia expects new housing construction and renovation activity to be up slightly over the short-to-medium term.

Former subsidiaries of ABN 60 Pty Limited (“ABN 60”) developed fibre cement in Australia as a replacement for asbestos cement in the early 1980s. Asbestos cement sheet production ceased in the early 1980s and asbestos cement pipe production ceased in 1987. Competition has intensified over the past decade in Australia. In addition to competition from solid wood, engineered wood, wallboard, masonry and brick, two Australian competitors have established fibre cement manufacturing facilities in Australia and fibre cement imports are also growing.

New Zealand

According to Statistics New Zealand, new dwellings consents in New Zealand increased from approximately 14,600 for the year ended March 2012 to 17,400 for the year ended March 2013. Residential renovation activity in New Zealand has increased from the year ended March 2012 to the year ended March 2013 for a total increase over this period of approximately 8%. InfoMetrics New Zealand expects new housing construction and renovation activity to increase further during calendar year 2013, consistent with the growth during calendar year 2012.

Competition continues to intensify in New Zealand as fibre cement imports have become more cost competitive and overseas manufacturers struggling with the global recession look for additional markets to add to their existing ones.

Philippines

In the Philippines and other Asian and Middle Eastern (Israel, Kuwait, Qatar and the United Arab Emirates) markets, fibre cement building products are used in both the residential and commercial building industries with applications in ceilings, internal walls and external siding, facades and soffits. The residential building industry represents the principal market for fibre cement products. In general, fibre cement products have, across a range of product applications, gained broader acceptance in these regions over the last decade. In the Philippines, additional imported fibre cement products have entered the market. However, in some of the developing markets, gypsum usage has increased and penetrated into fibre cement applications. Fibre cement and asbestos cement production facilities are located throughout Asia and exporting between countries is common practice. Unlike some of our competitors in the Asian market, we do not manufacture fibre cement products containing asbestos. We believe that fibre cement has good long-term growth potential because of the benefits of light-weight and framed construction compared to traditional masonry construction. In addition, we believe the opportunity to replace wood-based products, such as plywood, with more durable fibre cement will be attractive to some consumers in some of these markets.

Europe

In Europe, fibre cement building products are used in both residential and commercial building applications in external siding, internal walls, floors, soffits and roofing. We compete in most segments except roofing and promote the use of fibre cement products against traditional masonry, gypsum-based products and wood-based products. Since we commenced selling our products in Europe in

| James Hardie FY 2013 20-F |

8 |

Table of Contents

fiscal year 2004, we have continued to work to grow demand for our products by building awareness among distributors, builders and contractors. Management believes that the growth outlook for fibre cement in Europe is favourable in light of stricter insulation requirements driving demand for advanced exterior cladding systems as well as better building practices increasing the use of fibre cement in interior applications.

Products

We manufacture fibre cement products in the United States, Australia, New Zealand and the Philippines. In fiscal year 2004, we commenced our European fibre cement business by distributing our fibre cement products in the United Kingdom and France. We also manufacture fibre cement pipes in Australia and previously manufactured fibre cement pipes and roofing products in the United States. In May 2008 and April 2006, we ceased operation of our pipes and roofing businesses, respectively, in the United States. Our total product offering is aimed at the building and construction markets, including new residential construction, manufactured housing, repair and remodeling and a variety of commercial and industrial building applications.

We offer a wide range of fibre cement products for both exterior and interior applications. In the United States and elsewhere, our products are typically sold as planks or flat sheets with a variety of patterned profiles and finishes. Planks are used for external siding while flat sheets are used for internal and external wall linings and floor and tile underlayments. Outside the United States, we also manufacture fibre cement products for use in other applications such as building facades, lattice, fencing, decorative columns, flooring, soffit lining and ceiling applications, some of which have not yet been introduced into the United States.

We developed a proprietary technology platform that enables us to produce thicker yet lighter-weight fibre cement products that are generally lighter and easier to handle than traditional building products. The first application of this technology in the United States has been our HardieTrim® board. HardieTrim board is a fibre cement trim product that is used on the exterior of residential and commercial construction to replace traditional wood and engineered wood trim. HardieTrim board was launched in fiscal year 1999, with the introduction of HardieTrim HLD board.

We believe that our products provide certain performance, design and cost advantages. The principal fibre cement attributes in exterior applications are durability and low maintenance, particularly when compared to competing wood and wood-based products, while offering comparable aesthetics. Our fibre cement products exhibit resistance to the damaging effects of moisture, fire, impact and termites compared to wood and wood-based products, which we believe has enabled us to gain a competitive advantage over competing products. Vinyl siding products generally have better durability characteristics than wood-based products, but typically cannot duplicate fibre cement’s aesthetics and the characteristics necessary for effectively accepting paint applications.

Our fibre cement products provide strength and the ability to imprint patterns that closely resemble patterns and profiles of traditional materials such as wood and stucco. The surface properties provide an effective paint-holding finish, compared to wood and engineered wood products, such that the periods between necessary maintenance and repainting are generally longer. Compared to masonry construction, fibre cement is lightweight, physically flexible and can be cut using readily available tools. This makes fibre cement suitable for lightweight construction across a range of architectural styles. Fibre cement is well suited to both timber and steel-framed construction.

In our interior product range, we believe our ceramic tile underlayment products exhibit better handling and installation characteristics compared to fibreglass mesh cement boards. Compared to wood and wood-based products, our products provide the same general advantages that apply to external

| James Hardie FY 2013 20-F |

9 |

Table of Contents

applications. In addition, our fibre cement products exhibit less movement in response to exposure to moisture than many alternative competing products, providing a more consistent and durable substrate on which to install tiles. In internal lining applications where exposure to moisture and impact damage are significant concerns, our products provide superior moisture resistance and impact resistance than traditional gypsum wet area wallboard and other competing products.

In the United States, the following new products were released over the last five years:

| — | During fiscal year 2009, we introduced two new siding profiles, HardieSoffit® Beaded Porch Panel and HardieShingle® Shingle Plank. |

| — | During fiscal year 2010, we introduced HardieZone® System siding products. |

| — | During fiscal year 2011, we introduced new HardieShingle® siding, HardieTrim® NT3® Boards, two new lap siding products, 12’ Artisan® Accent Trim and HardieBacker® ProGrid™ cement board. |

| — | During fiscal year 2012, we introduced new profile HZ5® HardiePlank® siding, additional HardieShingle® siding profiles, new Improved Smooth HardieTrim® boards, new HardieTrim® Crown Mouldings and three new colors to the palette for James Hardie® products using ColorPlus® technology. |

| — | During fiscal year 2013, we introduced a new profile HZ10® HardiePlank® siding. |

In Australia and New Zealand, new products released over the past five years in the Scyon™ lightweight advanced cement composite range include Axon™ cladding, Stria™ cladding, Secura™ Interior Flooring, and Secura™ Exterior Flooring and Axent™ trim, and Horizon™ Lining in the James Hardie product range; in Australia only, new products include: Matrix™ cladding; and additionally, in New Zealand only, the following new products were released: in the James Hardie product range ShingleSide™ panel, Linea™ Oblique™ cladding, CLD™ Cavity Battens, RAB™ PreClad™ Lining and homeRAB™ board (Rigid Air Barrier products), Horizon™ Lining, and RawForm™ Lining. In both countries, new product launches have been supported by the launch of energy efficiency related accessories such as HardieBreak™ thermal break tape as well as web based initiatives such as the ACCEL™ suite of online product information, calculator and application tools, the LookHome™ and LightHome™ e-zines as well as the SmarterGreen™, SmarterPartner™, SmarterDesign™ and The Smarter Small Home™ initiatives. In New Zealand, The Drawing Board™ online design tool provides an aid to smart design using James Hardie products.

In the Philippines, new products released over the past five years include Hardieplank™ Siding, Hardiefloor™ Systems and Hardiepattern™ Boards. The established Hardieflex™ board range has been extended to include Hardieflex™ Wet Area lining boards. In November 2012, Hardieflex™ Pro was launched which is primarily for wet area application.

Seasonality

Our earnings are seasonal and typically follow activity levels in the building and construction industry. In the United States, the calendar quarters ending in December and March generally reflect reduced levels of building activity depending on weather conditions. In Australia and New Zealand, the calendar quarter ending in March is usually affected by a slowdown due to summer holidays. In the Philippines, construction activity diminishes during the wet season from June through September and during the last half of December due to the slowdown in business activity over the holiday period. Also, general industry patterns can be affected by weather, economic conditions, industrial disputes and other factors. See Section 3, “Risk Factors.”

| James Hardie FY 2013 20-F |

10 |

Table of Contents

Raw Materials

The principal raw materials used in the manufacture of fibre cement are cellulose fibre (wood-based pulp), silica (sand), portland cement and water.

Cellulose Fibre. Reliable access to specialised, consistent quality, low cost pulp is critical to the production of fibre cement building materials. Cellulose fibre is sourced from New Zealand, the United States, Canada, and Chile and is processed to our specifications. It is further processed using our proprietary technology to provide the reinforcing material in the cement matrix of fibre cement. We have developed a high level of internal expertise in the production and use of wood-based pulps. This expertise is shared with our pulp producers, which have access to appropriate raw wood stocks, in order to formulate superior reinforcing pulps. The resulting pulp formulas are typically proprietary and are the subject of confidentiality agreements between the pulp producers and us. Moreover, we have obtained patents in the United States and in certain other countries covering certain unique aspects of our pulping formulas and processes that we believe cannot adequately be protected through confidentiality agreements. However, we cannot assure you that our intellectual property and other proprietary information will be protected in all cases. See Section 3, “Risk Factors.” We have entered into contracts that provide discounted pulp prices relative to various pulp indices and we purchase our pulp from several qualified suppliers in an attempt to mitigate price increases and supply interruptions.

Pulp has historically demonstrated more price sensitivity than other raw materials that we use in our manufacturing process. In fiscal year 2013, the average Northern Bleached Softwood Kraft (“NBSK”) pulp price relative to our US business was US$878 per ton, an 8% decrease compared to fiscal year 2012.

Silica. High purity silica is sourced locally by the various production plants. In the majority of locations, we use silica sand as a silica source. In certain other locations, however, we process quartz rock and beneficiate silica sand to ensure the quality and consistency of this key raw material.

Cement. Cement is acquired in bulk from local suppliers and is supplied on a just-in-time basis to our manufacturing facilities. The silos at each fibre cement plant hold between one and three days of our cement requirements. We continue to evaluate options on agreements with suppliers for the purchase of cement that can fix our cement prices over longer periods of time.

Water. We use local water supplies and seek to process all wastewater to comply with environmental requirements.

Sales, Marketing and Distribution

The principal markets for our fibre cement products are the United States, Australia, New Zealand, the Philippines, Canada, and in parts of Europe, including the United Kingdom and France. In addition, we sell fibre cement products in many other countries, including Belgium, China, Denmark, France, French Caribbean, Germany, Hong Kong, Hungary, India, Indonesia, Ireland, Italy, Malta, Mexico, the Middle East (Israel, Kuwait, Qatar and the United Arab Emirates), The Netherlands, Norway, various Pacific Islands, South Africa, South Korea, Spain, Sri Lanka, Switzerland, Taiwan, Turkey and Vietnam. Our brand name, customer education in comparative product advantages, differentiated product range and customer service, including technical advice and assistance, provide the basis for our marketing strategy. We offer our customers support through a specialised fibre cement sales force and customer service infrastructure in the United States, Australia, New Zealand, the Philippines and Europe (which is based out of The Netherlands). The customer service infrastructure includes inbound customer service support coordinated nationally in each country (customer service support for Canada is based out of the United States and customer service support for Europe is based out of The Netherlands),

| James Hardie FY 2013 20-F |

11 |

Table of Contents

and is complemented by outbound telemarketing capability. Within each regional market, we provide sales and marketing support to building products dealers and lumber yards and also provide support directly to the customers of these distribution channels, principally homebuilders and building contractors.

In the United States, we sell fibre cement products for new residential construction predominantly to distributors, which then sell these products to dealers or lumber yards. This two-step distribution process is supplemented with direct sales to dealers and lumber yards as a means of accelerating product penetration and sales. Repair and remodel products in the United States are typically sold through the large home center retailers and specialist distributors. Our top five US customers accounted for approximately 54% of our total USA and Europe Fibre Cement gross sales in fiscal year 2013. In Australia and New Zealand, both new construction and repair and remodel products are generally sold directly to distributor/hardware stores and lumber yards rather than through the two-step distribution process. In the Philippines, a network of thousands of small to medium size dealer outlets sells our fibre cement products to consumers, builders and real estate developers, although in recent years, do-it-yourself type stores have started to enter the Philippines market. Physical distribution of product in each country is primarily by road or sea transport, except in the United States where transportation is primarily by road and, to a lesser extent, by rail. Fibre cement products manufactured in Australia, New Zealand and the Philippines are exported to a number of markets in Asia, the Pacific, and the Middle East (Israel, Kuwait, Qatar and the United Arab Emirates) by sea transport.

We maintain dedicated regional sales management teams in our major sales territories. As of 31 May 2013, the sales teams (including telemarketing staff) consisted of approximately 298 people in the United States and Canada, 77 people in Australia, 22 people in New Zealand, 39 people in the Philippines, and 27 people in Europe. We also employ one person based in Hong Kong who functions as a regional export salesperson, and who covers markets such as South Korea, Hong Kong, Macau, China and the Middle East (Israel, Kuwait, Qatar and the United Arab Emirates). Our national sales managers and national account managers, together with the regional sales managers and sales representatives, maintain relationships with national and other major accounts. Our sales force includes skilled trades people who provide on-site technical advice and assistance. In some cases, sales forces manage specific product categories.

Despite the fact that distributors and dealers are generally our direct customers, we also aim to increase primary demand for our products by marketing our products directly to homeowners, architects and builders. We encourage them to specify and install James Hardie® products because of the quality and craftsmanship of our products. This “pull through” strategy, in turn, assists us in expanding sales for our distribution network as distributors benefit from the increasing demand for our products.

Geographic expansion of our fibre cement business has occurred in markets where framed construction is prevalent for residential applications or where there are opportunities to change building practices from masonry to framed construction. Expansion is also possible where there are direct substitution opportunities irrespective of the methods of construction. Our entry into the Philippines is an example of the ability to substitute fibre cement for an alternative product (in this case plywood). With the exception of our current major markets, as well as Japan and certain rural areas in Asia, Scandinavia, and Eastern Europe, most markets in the world principally utilise masonry construction for external walls in residential construction. Accordingly, further geographic expansion depends substantially on our ability to provide alternative construction solutions and for those solutions to be accepted in those markets.

Because fibre cement products were relatively new to the Philippines, the launch of our fibre cement products in the Philippines in fiscal year 1999 was accompanied by strategies to address the particular

| James Hardie FY 2013 20-F |

12 |

Table of Contents

needs of local customers and the building trade. For example, we established a carpenter training and accreditation program whereby Filipino carpenters who are unfamiliar with our products are taught installation techniques. Our training programs for counterclerks and carpenters are geared not only to educate them but also to develop them as brand advocates. We have also put greater emphasis on building our relationships with new home developers and builders in order to educate the market on the benefits of our products in this particular sector.

Dependence on Trade Secrets and Research and Development

We pioneered the successful development of cellulose reinforced fibre cement and, since the 1980s, have progressively introduced products developed as a result of our proprietary product formulation and process technology. The introduction of differentiated products is one of the core components of our global business strategy. This product differentiation strategy is supported by our significant investment in research and development activities.

The following table sets forth our research and development expenditures for the three preceding fiscal years:

| Fiscal Years Ended 31 March | ||||||||||||

| (Millions of US dollars) | 2013 | 2012 | 2011 | |||||||||

| Research and Development Expenditures1 |

$ | 39.6 | $ | 32.4 | $ | 31.2 | ||||||

| Research and Development Expenditures as a percentage of total net sales |

3.0% | 2.6% | 2.7% | |||||||||

| 1 | Included within research and development expenditures for fiscal years 2013, 2012 and 2011 is US$2.4 million, US$2.0 million and US$3.2 million, respectively, classified as selling, general and administrative expenses. |

Our current patent portfolio is based mainly on fibre cement compositions, associated manufacturing processes and the resulting products. Our non-patented technical intellectual property consists primarily of our operating and manufacturing know-how, which is maintained as trade secret information. We have enhanced our abilities to effectively create, manage and utilise our intellectual property and have implemented a strategy that increasingly uses patenting, licensing, trade secret protection and joint development to protect and increase our competitive advantage. However, we cannot assure you that our intellectual property and other proprietary information will be protected in all cases. In addition, if our research and development efforts fail to generate new, innovative products or processes, our overall profit margins may decrease and demand for our products may fall.

In addition, the Company owns a variety of patents and licenses; industrial, commercial and financial contracts; and manufacturing processes. While the Company is dependent on the competitive advantage that these items provide as a whole, the Company is not dependent on any one of them individually and does not consider any one of them individually to be material. We do not materially rely on intellectual property licensed from any outside third parties. See Section 3, “Risk Factors.”

Governmental Regulation

As noted above, on 15 October 2012, we converted into an Irish plc from an Irish SE and are now governed by the Irish Companies Acts. Previously, as an Irish SE company, we were governed by the Irish Companies Acts and the SE Regulation, European Union Council Regulations and relevant European Union Directives. We also continue to operate under the regulatory requirements of numerous jurisdictions and organisations, including the ASX, ASIC, the NYSE, the SEC, the Irish

| James Hardie FY 2013 20-F |

13 |

Table of Contents

Takeovers Panel and various other rulemaking bodies. See Section 3, “Memorandum and Articles of Association” for information regarding Irish Companies Acts and regulations to which we are subject.

Environmental Regulation

Our operations and properties are subject to extensive federal, state and local and foreign environmental protection and health and safety laws, regulations and ordinances. These environmental laws, among other matters, govern activities and operations that may have adverse environmental effects, such as discharges to air, soil and water, and establish standards for the handling of hazardous and toxic substances and the handling and disposal of solid and hazardous wastes. In the United States, these environmental laws include, but are not limited to the:

| — | Resource Conservation and Recovery Act; |

| — | Comprehensive Environmental Response, Compensation and Liability Act; |

| — | Clean Air Act; |

| — | Occupational Safety and Health Act; |

| — | Mine Safety and Health Act; |

| — | Emergency Planning and Community Right to Know Act; |

| — | Clean Water Act; |

| — | Safe Drinking Water Act; |

| — | Surface Mining Control and Reclamation Act; |

| — | Toxic Substances Control Act; |

| — | National Environmental Policy Act; and |

| — | Endangered Species Act, |

as well as analogous state, regional and local regulations. Other countries also have statutory schemes relating to the protection of the environment.

Some environmental laws provide that a current or previous owner or operator of real property may be liable for the costs of removal or remediation of environmental contamination on, under, or in that property or other impacted properties. In addition, persons who arrange, or are deemed to have arranged, for the disposal or treatment of hazardous substances may also be liable for the costs of removal or remediation of environmental contamination at the disposal or treatment site, regardless of whether the affected site is owned or operated by such person. Environmental laws often impose liability whether or not the owner, operator or arranger knew of, or was responsible for, the presence of such environmental contamination. Also, third parties may make claims against owners or operators of properties for personal injuries, property damage and/or for clean-up associated with releases of hazardous or toxic substances pursuant to applicable environmental laws and common law tort theories, including strict liability.

Environmental compliance costs in the future will depend, in part, on continued oversight of operations, expansion of operations and manufacturing activities, regulatory developments and future requirements that cannot presently be predicted.

| James Hardie FY 2013 20-F |

14 |

Table of Contents

JHI plc is incorporated and domiciled in Ireland.

The table below sets forth our significant subsidiaries, all of which are wholly-owned by JHI plc, either directly or indirectly, as of 31 May 2013.

| Name of Company |

Jurisdiction of | |

| James Hardie 117 Pty Ltd. |

Australia | |

| James Hardie Aust Holdings Pty Ltd. |

Australia | |

| James Hardie Austgroup Pty Ltd. |

Australia | |

| James Hardie Australia Management Pty Ltd. |

Australia | |

| James Hardie Australia Pty Ltd. |

Australia | |

| James Hardie Building Products Inc. |

United States | |

| James Hardie Europe B.V. |

Netherlands | |

| James Hardie Finance Holdings 3 Limited |

Bermuda | |

| James Hardie Holdings Limited |

Ireland | |

| James Hardie International Finance Limited |

Ireland | |

| James Hardie International Group Limited |

Ireland | |

| James Hardie International Holdings Limited |

Ireland | |

| James Hardie New Zealand |

New Zealand | |

| James Hardie NZ Holdings |

New Zealand | |

| James Hardie Philippines Inc. |

Philippines | |

| James Hardie Technology Limited. |

Bermuda | |

| James Hardie U.S. Investments Sierra LLC |

United States | |

| N.V. Technology Holdings, A Limited Partnership |

Australia | |

| RCI Holdings Pty Ltd. |

Australia |

Property, Plants and Equipment

We estimate that our manufacturing plants are among the largest and lowest cost fibre cement manufacturing plants in the United States. We believe that the location of our plants positions us near attractive markets in the United States while minimising our transportation costs for product distribution and raw material sourcing.

Our manufacturing plants use significant amounts of water which, after internal recycling and reuse, are eventually discharged to publicly owned treatment works (with the exception of our Reno, Nevada facility and Summerville, South Carolina facility at which production was suspended in November 2008, which maintain closed loop systems). The discharge of process water is monitored by us, as well as by regulators. In addition, we are subject to regulations that govern the air quality and emissions from our plants. In the past, from time to time, we have received notices of discharges in excess of our water and air permit limits. In each case, we have addressed the concerns raised in those notices, including the payment of any associated minor fines and capital expenditures associated with preventing future discharges in excess of permitted levels.

Plants and Process

Fibre Cement Building Products

We manufacture fibre cement building products in the United States and Asia Pacific. Annual design capacity is based on management’s historical experience with our production process and is calculated assuming continuous operation, 24 hours per day, seven days per week, producing 5/16” medium

| James Hardie FY 2013 20-F |

15 |

Table of Contents

density product at a targeted operating speed. Annual design capacity is not necessarily reflective of our actual capacity utilisation rates for our fibre cement plants by region. Annual capacity utilisation is affected by factors such as demand, product mix, batch size, plant availability and production speeds and is usually less than annual design capacity. We manufacture products of varying thicknesses and density.

We currently have an annual flat sheet design capacity of 3,390 mmsf and 520 mmsf in the United States and Asia Pacific, respectively, for our fibre cement building products. Fiscal year 2013 capacity utilisation, based on this annual flat sheet design capacity, for our fibre cement building products plants was an average of 42% and 68% in the United States and Asia Pacific, respectively. As indicated above, annual flat sheet design capacity is based on management’s estimates. No accepted industry standard exists for the calculation of our fibre cement manufacturing facility design and utilisation capacities.

We are expanding production capacity in anticipation of the continued improvement of the operating environment and we expect to incur significant capital expenditures in fiscal year 2014 and beyond to meet anticipated demand increases in major markets. Once the Fontana, California and Carole Park, Queensland capacity expansions are complete, our annual flat sheet design capacity will increase by 2% to 3,460 mmsf and 9% to 570 mmsf in the United States and Asia Pacific, respectively. See “Capital Expenditures” below.

Fibre Reinforced Concrete Pipes

We manufacture fibre reinforced concrete pipes in Australia. Our current annual design capacity for our fibre reinforced concrete pipes plant is 50 thousand tons.

Plant Locations

The location of each of our fibre cement plants is set forth below:

| Fibre Cement Building Products |

||

| Cleburne, Texas |

||

| Peru, Illinois |

||

| Plant City, Florida Pulaski, Virginia |

||

| Reno, Nevada Tacoma, Washington Waxahachie, Texas |

||

| United States – Plants Suspended |

||

| Blandon, Pennsylvania1 Fontana, California2 |

||

| Summerville, South Carolina2 |

||

| Asia Pacific |

||

| Australia |

||

| Sydney, New South Wales (Rosehill) |

||

| Brisbane, Queensland (Carole Park)3 |

||

| New Zealand |

||

| Auckland |

||

| The Philippines |

||

| Manila |

||

| Fibre Reinforced Concrete Pipes |

||

| Australia |

||

| Brisbane, Queensland (Meeandah)3 |

||

| James Hardie FY 2013 20-F |

16 |

Table of Contents

| 1 | We suspended production at our Blandon, Pennsylvania plant in November 2007 and in the fourth quarter of fiscal year 2013 we announced that we will not re-open the plant. |

| 2 | We suspended production at our Fontana, California and Summerville, South Carolina plants in December 2008 and November 2008, respectively. In fiscal year 2013, we announced that we were spending US$34 million to refurbish and reconfigure the Fontana plant, which is scheduled to reopen early calendar year 2014. |

| 3 | There are two manufacturing plants in Brisbane. Carole Park produces only flat sheets and Meeandah produces only pipes and columns. As announced in May 2013, we have purchased the land and buildings at the Carole Park facility and are expanding production capacity at this plant. |

While the same basic process is used to manufacture fibre cement building products at each facility, plants are designed to produce the appropriate mix of products to meet each geographic market’s specific, projected needs. The facilities were constructed and are operated so production can be efficiently adjusted in response to increased consumer demand by increasing production capacity utilisation, enhancing the economies of scale or adding additional lines to existing facilities, or making corresponding reductions in production capacity in response to weaker demand.

Except for the Waxahachie, Texas facility, we own all of our fibre cement manufacturing facilities located in the United States. The lease for the Waxahachie, Texas facility expires on 31 March 2020, at which time we have an option to purchase the facility.

Two of our three Australian fibre cement manufacturing facilities (Rosehill, Sydney and Meeandah, Brisbane) are leased by us. The Rosehill lease expires on 23 March 2016, with an option to renew the lease for two further terms of 10 years expiring in March 2036. The Meeandah lease expires on 23 March 2019, and contains options to renew for two further terms of 10 years expiring in March 2039. As previously announced, in May 2013 we entered into an agreement to purchase the remaining Australian fibre cement manufacturing facility (Carole Park, Brisbane) as part of our Australian manufacturing capacity expansion. Our one New Zealand fibre cement manufacturing facility is leased by us. The lease for our New Zealand facility expires on 22 March 2016, at which time we have an option to renew the lease for two further terms of 10 years expiring in March 2036. There is no purchase option available under our leases related to our Australian and New Zealand facilities.

The land on which our Philippines fibre cement plant is located is owned by Ajempa Holding inc (“Ajempa”), a related party. Ajempa is 40% owned by James Hardie Philippines operating entity and 60% owned by the James Hardie Philippines Retirement fund. The James Hardie operating entity owns 100% of the fixed assets on the land owned by Ajempa.

Mines

We lease silica quartz mine sites in Tacoma, Washington, Reno, Nevada and Victorville, California. The lease for our quartz mine in Tacoma, Washington expires in February 2014 (with options to renew). The lease for our silica quartz mine site in Reno, Nevada expires in January 2014 (with options to renew or purchase). The lease for our silica mine site in Victorville, California expires in June, 2015. Further, we own rights to an additional property in Victorville, California, however, as of 31 May 2013, we have not begun to mine this site.

As a mine operator, we are required by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), and rules promulgated by the Securities and Exchange Commission implementing that section of the Dodd-Frank Act, to provide certain information concerning mine safety violations and other regulatory matters concerning the operation of our mines. During fiscal year 2013, we did not receive any notices, citations, orders, legal action or other communication from the US Department of Labor’s Mine Safety and Health Administration that would necessitate additional disclosure under Section 1503(a) of the Dodd-Frank Act.

| James Hardie FY 2013 20-F |

17 |

Table of Contents

Capital Expenditures

The following table sets forth our capital expenditures for each year in the three-year period ended 31 March 2013.

| Fiscal Years Ended 31 March | ||||||||||||

| 2013 | 2012 | 2011 | ||||||||||

| (Millions of US dollars) | ||||||||||||

| USA and Europe Fibre Cement |

$ | 43.2 | $ | 26.7 | $ | 39.5 | ||||||

| Asia Pacific Fibre Cement |

10.7 | 6.7 | 9.9 | |||||||||

| Research and Development and Corporate |

7.2 | 2.4 | 0.9 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Capital Expenditures |

$ | 61.1 | $ | 35.8 | $ | 50.3 | ||||||

|

|

|

|

|

|

|

|||||||

The Company did not have any material divestitures in the fiscal years ended 31 March 2013, 2012 and 2011.

The significant capital expenditure projects over the past three fiscal years in our USA and Europe Fibre Cement segment include:

| — | enhancement of trim capability at our Peru, Illinois plant for US$3.6 million in fiscal year 2011; |

| — | commencement of a new finishing capability on an existing product line in fiscal year 2009. As of 31 March 2013, we have incurred US$23.9 million related to this project; |

| — | commencement of expenditures to enhance environmental compliance at our plants in fiscal year 2011. As of 31 March 2013, we have incurred US$13.3 million related to this project; |

| — | an upgrade of our supply chain management IT systems for US$4.3 million through fiscal year 2013; |

| — | a new finishing line at our Cleburne plant for US$6.1 million which was primarily incurred in fiscal year 2011; |

| — | commencement of reconfiguration and re-commissioning of our Fontana, California plant in fiscal year 2013. As of 31 March 2013, we have incurred US$4.1 million related to this project; |

| — | re-commissioning and upgrade of our Waxahachie, Texas plant for US$5.0 million in fiscal year 2013; |

| — | expansion of a warehouse facility at our Pulaski, Virginia plant. As of March 2013, we have incurred US$3.3 million related to this project; |

| — | installation of new packaging technology at our Pulaski, Virginia plant. As of 31 March 2013, we have incurred US$2.8 million related to this project; |

| — | recommissioning and upgrade of a proprietary raw material manufacturing plant in Fontana, California for US$1.8 million in fiscal year 2013; and |

| — | construction of a new warehouse facility at our Cleburne, Texas plant. As of 31 March 2013, we have incurred US$2.8 million related to this project. |

| James Hardie FY 2013 20-F |

18 |

Table of Contents

In our Asia Pacific Fibre Cement segment, significant capital expenditures in the last three years include the installation of a new ball mill at our Carole Park plant in Australia in fiscal year 2013. As of 31 March 2013, we have incurred US$2.5 million related to this project.

In our Research and Development segment, we purchased and fitted out a building for our new research and development facility in Naperville, Illinois for US$4.8 million in fiscal year 2013.

We currently expect to spend approximately US$150.0 million in fiscal year 2014 for capital expenditures, including facility upgrades and expansions, equipment to enhance environmental compliance, and the implementation of new fibre cement technologies. Part of the expected amount of spending in fiscal year 2014 includes additional capital expenditures on projects that were in progress during fiscal year 2013, including US$29.9 million related to the reconfiguring and re-commissioning of our Fontana, California plant, which is expected to reopen in calendar year 2014; and the recommissioning of idled production assets at a number of our other US plants.