United States

Securities and exchange

commission

washington, d.c. 20549

FORM 6-K

report of foreign private

issuer

pursuant to rule 13a-16 or 15d-16 of

the securities exchange act of 1934

For the month of May 2025

Commission File Number 1-15224

Energy Company of Minas Gerais

(Translation of Registrant’s Name into English)

Avenida Barbacena, 1200

30190-131 Belo Horizonte, Minas Gerais, Brazil

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F a Form 40-F ___

Index

| Item | Description of Items |

| 1. | Earnings Release – 4Q2024 |

| 2. | Call Notice to Annual and Extraordinary Shareholders' Meetings |

| 3. | Board of Directors Proposal for the Annual and Extraordinary Shareholders' Meetings |

| 4. | Notice to the Market dated March 27, 2025 – Resignation of Board Member |

| 5. | Notice to the Market dated April 30, 2025 – Filing of Form 20-F |

| 6. | Notice to Shareholders dated April 30, 2025 - Resolutions passed at the AESM – Dividends/IoE |

| 7. | Notice to the Market dated May 5, 2025 – Change in Relevant Shareholding |

| 8. | Earnings Release – 1Q2025 |

Forward-Looking Statements

This report contains statements about expected future events and financial results that are forward-looking and subject to risks and uncertainties. Actual results could differ materially from those predicted in such forward-looking statements. Factors which may cause actual results to differ materially from those discussed herein include those risk factors set forth in our most recent Annual Report on Form 20-F filed with the Securities and Exchange Commission. CEMIG undertakes no obligation to revise these forward-looking statements to reflect events or circumstances after the date hereof, and claims the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

COMPANHIA ENERGÉTICA DE MINAS GERAIS – CEMIG

By: /s/ Andrea Marques de Almeida .

Name: Andrea Marques de Almeida

Title: Vice President of Finance and Investor Relations

Date: May 16, 2025

| 1. | Earnings Release – 4Q2024 |

|

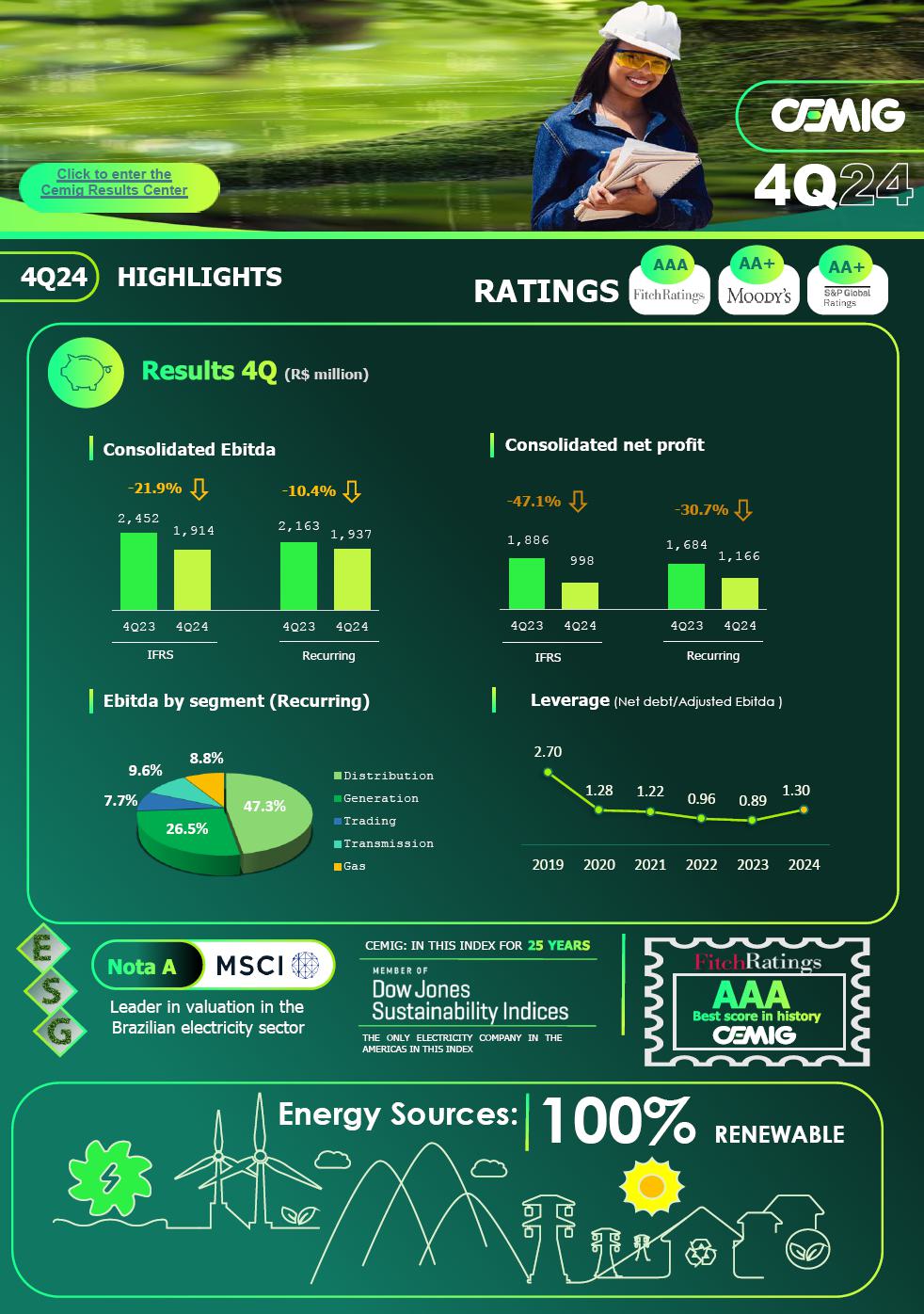

| HIGHLIGHTS – 4Q24 | |

| 4Q24 Ebitda and profit, by company | 6 |

| 4Q24 INCOME STATEMENTS | 7 |

| Results by business segment | 8 |

| CONSOLIDATED ELECTRICITY MARKET | 9 |

| Cemig D | 10 |

| Billed electricity market* | 10 |

| Sources and uses of electricity – MWh | 11 |

| Client base | 11 |

| Performances by sector | 12 |

| The 2024 Annual Tariff Adjustment | 12 |

| Five-year Tariff Reviews compared | 13 |

| Indicators of supply quality: DEC and FEC | 14 |

| Combating default | 14 |

| Energy losses | 15 |

| Cemig GT and the Cemig holding company | 16 |

| Electricity market | 16 |

| Sources and uses of electricity | 16 |

| Gasmig | 17 |

| CONSOLIDATED RESULTS | 18 |

| Net profit | 18 |

| Operational revenue | 19 |

| Operational costs and expenses | 21 |

| Finance income and expenses | 24 |

| Equity income (Gain / loss in non-consolidated investees) | 25 |

| CONSOLIDATED EBITDA (IFRS, and Adjusted) | 26 |

| Ebitda of Cemig D | 28 |

| Cemig GT – Ebitda | 29 |

| Investments | 30 |

| Debt | 31 |

| Cemig’s long-term ratings | 33 |

| ESG – Report on performance | 34 |

| Performance of Cemig’s shares | 37 |

| RAP: July 2024–June 2025 cycle | 40 |

| Regulatory transmission revenue | 41 |

| Complementary information | 41 |

| Cemig D | 41 |

| Cemig GT | 43 |

| Cemig, Consolidated | 44 |

| Disclaimer |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 5  |

| |

4Q24 Ebitda and profit, by company

| 4Q24 | 4Q23 |

Change % |

4Q24 | 4Q23 |

Change % | |

|

Ebitda by company (IFRS) |

Net profit by company (IFRS) | |||||

| (R$ mn) | ||||||

| Cemig D (IFRS) | 958 | 804 | 19.2% | 452 | 400 | 13.0% |

| Cemig GT (IFRS) | 527 | 1,173 | –55.1% | 241 | 844 | –71.4% |

| Gasmig (IFRS) | 179 | 204 | –12.1% | 112 | 139 | –19.2% |

| Consolidated (IFRS) | 1,914 | 2,452 | –21.9% | 998 | 1,886 | –47.1% |

| New replacement value (VNR) | 35 | 22 | 57.4% | |||

|

Equity income (Gain (loss) in non-consolidated investees) |

33 | 139 | –76.4% | |||

|

Consolidated (IFRS) less VNR and equity income |

1,847 | 2,291 | –19.4% | |||

| 4Q24 | 4Q23 |

Change % |

4Q24 | 4Q23 |

Change % | |

|

Adjusted Ebitda, by company |

Adjusted net profit, by company | |||||

| (R$ mn) | ||||||

| Cemig D | 958 | 804 | 19.2% | 452 | 400 | 13.0% |

| Cemig GT | 527 | 884 | –40.4% | 394 | 653 | –39.7% |

| Consolidated – Adjusted | 1,937 | 2,163 | –10.4% | 1,166 | 1,684 | –30.7% |

| New replacement value (NRV) | 35 | 22 | 57.4% | |||

| Gain (loss) in non-consolidated investees | 33 | 139 | –76.4% | |||

|

Adjusted consolidated net profit less VNR and equity income |

1,870 | 2,002 | –6.6% | |||

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 6 |

| |

4Q24 INCOME STATEMENTS

| 4Q24 | 4Q23 | Change, % | |

| IN (R$ ’000) | |||

| NET REVENUE | 11,177 | 9,957 | 12.3% |

| COSTS | |||

| Cost of electricity and gas | –6,178 | –5,242 | 17.9% |

| Infrastructure construction costs | –1,518 | –1,211 | 25.4% |

| Cost of operation | –1,444 | –1,268 | 13.9% |

| Total cost | –9,140 | –7,720 | 18.4% |

| GROSS PROFIT | 2,037 | 2,236 | –8.9% |

| EXPENSES: | |||

| Client default provision | –72 | –102 | –29.4% |

| General and administrative expenses | –214 | –223 | –4.1% |

| Other expenses, net | –234 | –247 | –5.4% |

| Other revenues | 0 | 297 | –100.0% |

| Total expenses | –519 | –275 | 88.8% |

| Share of gain (loss) in non-consolidated investees | 33 | 139 | –76.4% |

| Profit before Finance income (expenses) and taxes on profit | 1,550 | 2,101 | –26.2% |

| Finance income | 284 | 368 | –23.0% |

| Finance expenses | –680 | –466 | 45.8% |

| Net finance income (expense) | –396 | –98 | 304.4% |

| Profit before income and Social Contribution taxes | 1,154 | 2,003 | –42.4% |

| Income tax and Social Contribution tax | –309 | –199 | 55.5% |

| Deferred income tax and Social Contribution tax | 153 | 82 | 86.2% |

| Deferred income tax and Social Contribution tax | –156 | –117 | 33.9% |

| NET PROFIT FOR THE PERIOD | 998 | 1,886 | –47.1% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 7 |

| |

4Q24 Results by business segment

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 8 |

| |

CONSOLIDATED ELECTRICITY MARKET

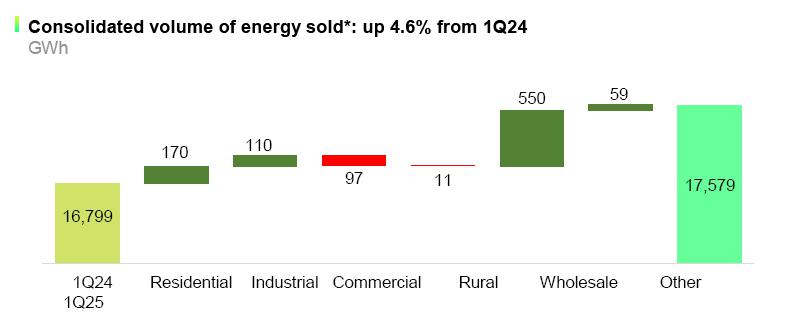

Cemig’s consolidated electricity market

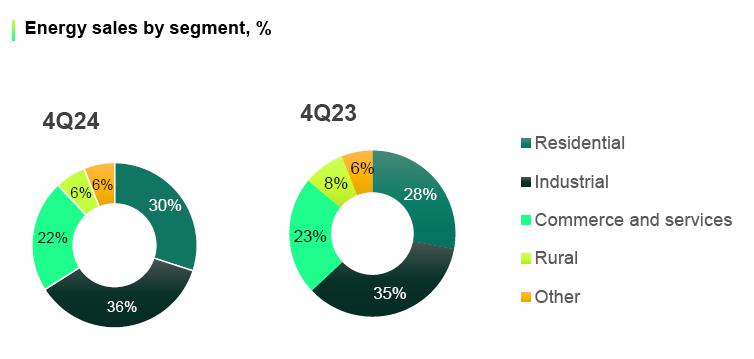

In December 2024 the Cemig Group invoiced 9.41 million clients – an addition of 191,000 clients, or a 2.1% increase in its consumer base, from December 2023. Of this total number of consumers, 9,407,944 were final consumers (including Cemig’s own consumption); and 447 were other agents in the Brazilian power sector.

The chart below itemizes the Cemig Group’s sales to final consumers:

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 9 |

| |

Cemig D

Billed electricity market*

| 4Q24 | 4Q23 | Change, % | |

| Captive clients + Transmission for clients (MWh) | |||

| Residential | 3,269,139 | 3,289,232 | –0.6% |

| Industrial | 5,777,187 | 5,571,405 | 3.7% |

| Captive market | 230,020 | 302,018 | –23.8% |

| Transport of energy | 5,547,167 | 5,269,387 | 5.3% |

| Commercial, services and Others | 1,634,659 | 1,736,739 | –5.9% |

| Captive market | 967,083 | 1,156,259 | –16.4% |

| Transport | 667,576 | 580,480 | 15.0% |

| Rural | 705,045 | 836,885 | –15.8% |

| Captive market | 678,416 | 822,905 | –17.6% |

| Transport | 26,629 | 13,980 | 90.5% |

| Public services | 835,511 | 915,843 | –8.8% |

| Captive market | 659,449 | 797,873 | –17.3% |

| Transport | 176,062 | 117,970 | 49.2% |

| Concession holders | 87,742 | 86,502 | 1.4% |

| Transport | 87,742 | 86,502 | 1.4% |

| Own consumption | 7,678 | 8,005 | –4.1% |

| Total | 12,316,961 | 12,444,612 | –1.0% |

| Total, captive market | 5,811,785 | 6,376,292 | –8.9% |

| Total, energy transported for Free Clients | 6,505,176 | 6,068,320 | 7.2% |

* Excludes supply offset in distributed generation.

Electricity billed to captive clients plus transport of energy for Free Clients and distributors, excluding supply offset in distributed generation, totaled 12,317 GWh in 4Q24. This was 1.0% lower than in 4Q23. The lower total was mainly due to lower consumption in three client categories: consumption by rural consumers was down 15.8% (131.8 GWh) YoY; commercial consumption was down 5.9%, or 102.1 GWh; and public services consumed 8.8% (80.3 GWh) less than in 4Q23. These differences reflect: (i) migration to distributed generation; (ii) milder temperatures; and (iii) higher rainfall – less need for irrigation. On the other hand, consumption by industrial clients was 205.7 GWh (3.7%) higher, reflecting higher industrial production.

The lower total of energy distributed (down 1.0% YoY) reflected: Total consumption by the captive market 8.9% (564.5 GWh) lower, and use of the network by Free Clients 7.2% (436.9 GWh) higher.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 10 |

| |

Sources and uses of electricity – MWh

| 4Q24 | 4Q23 | Change, % | |

| Metered market – MWh | |||

| Transported for distributors | 87,742 | 85,586 | 2.5% |

| Transported for Free Clients | 6,457,709 | 6,000,168 | 7.6% |

| Own load + Distributed generation | 8,773,661 | 9,428,348 | –6.9% |

| Consumption by captive market | 5,924,306 | 6,472,529 | –8.5% |

| Distributed generation market | 1,466,740 | 1,231,100 | 19.1% |

| Losses in distribution network | 1,382,615 | 1,724,719 | –19.8% |

| Total volume carried | 15,319,112 | 15,514,102 | –1.3% |

Client base

In December 2024 Cemig D billed 9.40 million consumers, or 2.1% more than in December 2024.

Of this total, 4,414 were Free Clients using the distribution network of Cemig D.

| Dec. 2024 | Dec. 2023 | Change, % | |

| NUMBER OF CAPTIVE CLIENTS | |||

| Residential | 7,960,300 | 7,725,836 | 3.0% |

| Industrial | 23,807 | 28,437 | –16.3% |

| Commercial, services and Others | 916,307 | 943,831 | –2.9% |

| Rural | 405,953 | 422,829 | –4.0% |

| Public authorities | 72,681 | 69,670 | 4.3% |

| Public lighting | 7,209 | 6,659 | 8.3% |

| Public services | 13,688 | 13,703 | –0.1% |

| Own consumption | 789 | 758 | 4.1% |

| Total, captive clients | 9,400,734 | 9,211,723 | 2.1% |

| NUMBER OF FREE CLIENTS | |||

| Industrial | 1,865 | 1,221 | 52.7% |

| Commercial | 2,377 | 1,714 | 38.7% |

| Rural | 84 | 22 | 281.8% |

| Concession holders | 8 | 8 | 0.0% |

| Others | 80 | 22 | 263.6% |

| Total, Free Clients | 4,414 | 2,987 | 47.8% |

| Total, Captive market + Free Clients | 9,405,148 | 9,214,710 | 2.1% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 11 |

| |

Performances by sector

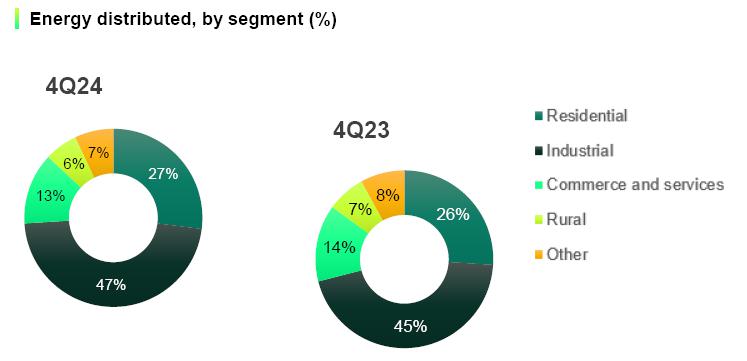

Industrial: Energy distributed to industrial clients was 3.7% higher YoY in 4Q24, on higher physical production by industry, and was 46.9% of Cemig D’s total distribution. The greater part was energy transported for industrial Free Clients (45.0%), which was 5.3% higher by volume than in 4Q23. Energy billed to captive industrial clients was 1.9% of the total distributed, and 23.8% less by volume than in 4Q23 – mainly due to migration of clients to the Free Market. Highlights in industry by sector were: Increased consumption in Ferroalloys (up 13.1% YoY), Cement (up 10.3%), Chemicals (up 8.5%), Food and beverages (up 5.3%), and Extractive industries (up 3.3%) – while consumption by the Non-ferrous metals sector was down 12.6%, YoY.

Residential: Residential consumption was 26.5% of total energy distributed by Cemig D, and 0.6% higher than in 4Q23. Average monthly consumption per consumer in the quarter, at 136.9 kWh/month, was 3.5% lower than in 4Q23, reflecting milder temperatures than in 4Q23. On the other hand, the total number of residential clients was increased by 2.1% year-on-year (234,500 new clients).

Commercial and services: Energy distributed to these consumers was 13.3% of the total distributed by Cemig D in 4Q24, and by volume 5.9% less than in 4Q23. The change is the result of a 16.4% reduction in the volume of energy billed to captive clients, and a 15.0% increase in the volume of energy transported for Free Clients. The lower consumption reflects: (i) milder temperatures, and (ii) migration of clients to distributed generation.

Rural: Consumption by rural clients was 6.8% of the total energy distributed, and was 15.8% lower by volume than in 4Q23. This mainly reflected lower consumption for irrigation, and a reduction of 4.0% in the number of consumer units in this category.

Public services: consumed 6.8% of the energy distributed in 4Q24, and was 8.8% less by volume than in 4Q23.

The 2024 Annual Tariff Adjustment

The tariffs of Cemig D undergo and Annual Tariff Adjustment are adjusted in May each year; and every five years are subjected to a Periodic Tariff Review, also in May. The aim of the Annual Tariff Adjustment is to pass on changes in the costs defined as “non-manageable” in full to the client, and provide inflation adjustment for the costs defined as “manageable”, as specified in the Tariff Review. Manageable costs are adjusted by the IPCA inflation index, less a factor known as the ‘X Factor’, designed to capture productivity, under a system using the price-cap regulatory model.

On May 14, 2024 Aneel ratified Cemig D’s Tariff Adjustment to be effective from May 28, 2024 to May 27, 2025, with an average increase, for consumers, of 7.32%. The average effect for low-voltage clients was an increase of 6.72%, and for residential consumers an increase of 6.70%. The component percentage corresponding to manageable costs (referred to as ‘Portion B’) was 1.27%. The increase relating to non-manageable costs (‘Portion A’ – comprising purchase of energy, transmission, sector charges and non-recoverable revenues) was 0.81%. The increase in the financial components of the tariff contributed 5.23%. The financial-components effect in 2024 comes mainly from absence of the item included in the 2023 adjustment process relating to the repayment to consumers of PIS, Pasep and Cofins taxes totaling R$ 1.27 billion.

| Average effects of the Tariff Adjustment | |

| High voltage – average | 8.63% |

| Low voltage – average | 6.72% |

| Average effect | 7.32% |

See more details at this link:

https://www2.aneel.gov.br/aplicacoes/tarifa/arquivo/Nota%20T%C3%A9cnica%20RTA%202024_CEMIG.pdf

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 12 |

| |

Five-year Tariff Reviews compared

Comparison of the Tariff Reviews made in 2023 and in the previous cycle (2018):

| Five-year Tariff Reviews | 2018 | 2023 |

| Gross Remuneration Base R$ million | 20,490 | 25,587 |

| Net Remuneration Base R$ million | 8,906 | 15,200 |

| Average depreciation rate: | 3.84% | 3.95% |

| WACC (after taxes) | 8.09% | 7.43% |

| Remuneration of ‘Special Obligations’ R$ mn | 149 | 272 |

| CAIMI * R$ mn | 333 | 484 |

| QRR ** (Depreciation calculation) R$ mn | 787 | 1,007 |

* CAIMI: (Cobertura Anual de Instalações Móveis e Imóveis) – Annual support for facilities.

** QRR: ‘Regulatory Reintegration Quota’ – Gross base x annual depreciation rate.

See more details at this link:

https://www2.aneel.gov.br/aplicacoes/tarifa/arquivo/NT%2012%202023%20RTP%20Cemig.pdf

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 13 |

| |

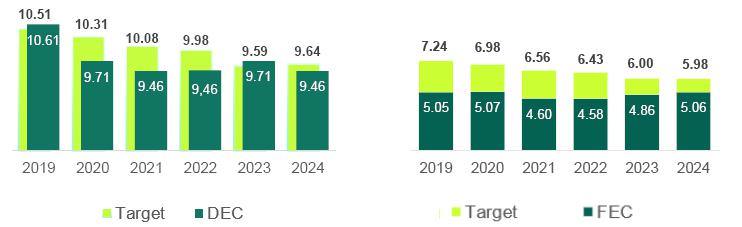

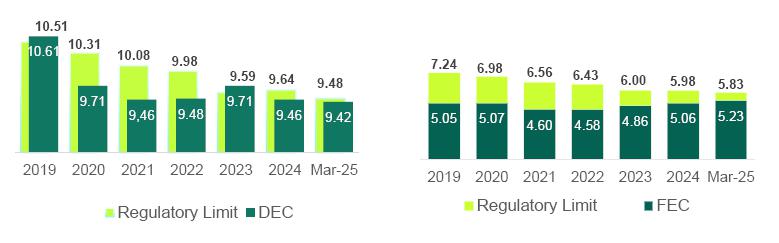

Indicators of supply quality: DEC and FEC

In 2023 the State of Minas Gerais experienced an increase in extreme atmospheric events, which caused a slight increase in electricity outages. In this challenging context Cemig has taken extra steps to reduce outage duration and frequency, and is making major investments in its distribution operation to maximize service quality.

These actions have produced positive results. Cemig’s DEC (average outage Duration per Consumer) is now within the regulatory limit of 9.64 hours: in the 12 months to end-December it was 9.46 hours.

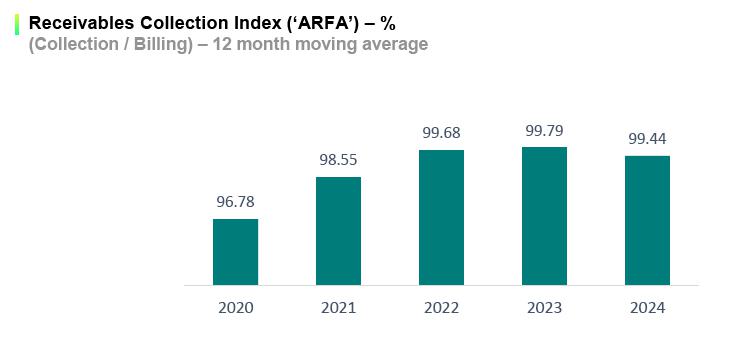

Combating default

The Company has kept collection actions at a high level, helping to keep its Receivables Recovery Index (collection / billing) also high – in December 2024 this index was 99.44%.

New payment channels, and online negotiation, have helped to increase the proportion of collection via digital channels (the PIX instant payment system, automatic debits, payments by card and app, etc.) – which at the end of 2024 reached 67.0% of the total collected, compared to 61.3% in 2023. Of all these, the PIX system stands out – it was used for 31.3% of all collections in December 2024 – and has saved R$ 30.6 million in payment charges/costs since it was implemented. The change in the payments mix has reduced Cemig’s costs of collection/receipt by 15% compared to 2023.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 14 |

| |

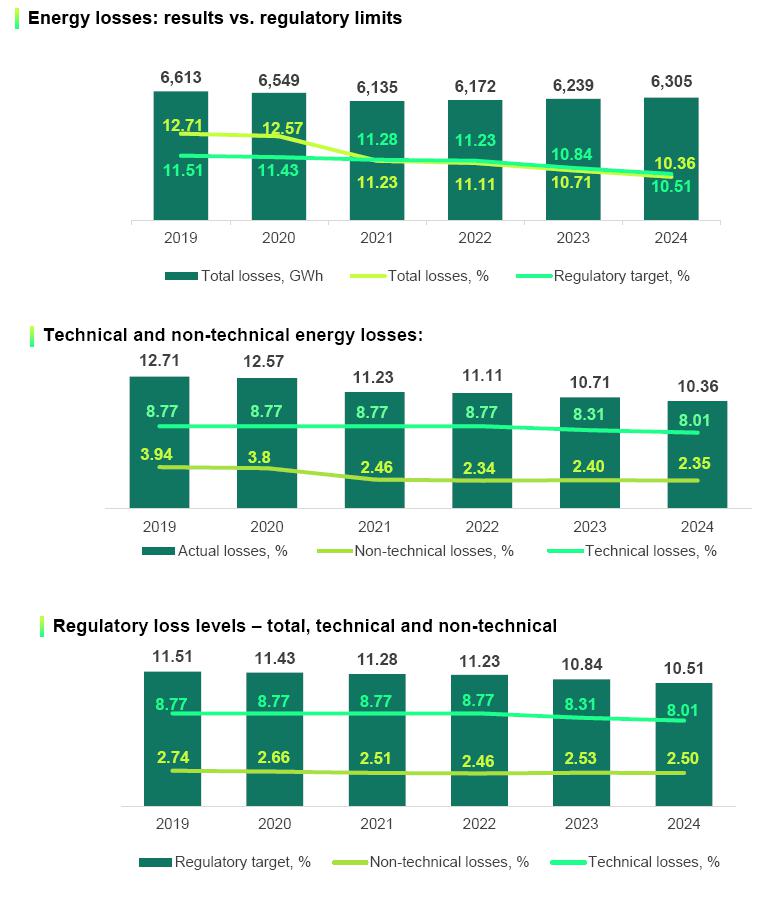

Energy losses

In the 12 months to Dec. 31, 2024, Cemig’s energy losses were 10.36%, below the regulatory target of 10.51%.

Cemig’s success in combating energy losses in 2024 has several components that deserve highlighting: approximately 385,000 inspections; replacement of more than 550,000 obsolete meters; replacement of 57,000 conventional meters by smart meters (bringing the total of smart meters installed since the project began in September 2021 to 370,000); and regularization of 12,200 clandestine connections made by families living in ‘invaded’ and low–income areas, through our Energia Legal program, which uses ‘bulletproofed’ networks (bringing the total of connections regularized since the start of the project in February 2023 to 22,800). Planned for 2025 are: 340,000 inspections; installation of more than 400,000 smart meters; and regularization of 54,000 families in low-income communities (using BT Zero and ‘Bulletproofed Meter Panel’ technologies).

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 15 |

| |

Cemig GT and the Cemig holding company

Electricity market

The total volume of electricity sold by Cemig GT and by the holding company (‘Cemig H’), excluding sales on the wholesale power exchange (CCEE), was 2.5% higher than in 4Q23. Cemig GT billed 5,526 GWh (including quota sales) in 4Q24, 5.8% less than in 4Q23. The lower figure is the result of transfer of sales contracts to Cemig H (the holding company) – which reported sales of 5,108 GWh in 4Q24, 12.7% more than in 4Q23. The migration of purchase contracts from Cemig GT to the holding company began in 3Q21, and has continued gradually since then. It is now around 60%.

| 4Q24 | 4Q23 | Change % | |

| Cemig GT – MWh | |||

| Free Clients | 3,218,766 | 3,204,224 | 0.5% |

| Industrial | 2,128,481 | 2,266,144 | –6.1% |

| Commercial | 874,426 | 932,015 | –6.2% |

| Rural | 5,793 | 6,065 | –4.5% |

| Public authorities | – | – | – |

| ‘Energy retailer’ Free Clients | 210,065 | – | – |

| Free Market – Traders and cooperatives | 1,140,822 | 1,502,666 | –24.1% |

| Quota supply | 574,432 | 574,322 | 0.0% |

| Regulated Market | 559,016 | 551,032 | 1.4% |

| Regulated Market – Cemig D | 33,253 | 33,715 | –1.4% |

| Total, Cemig GT | 5,526,289 | 5,865,959 | –5.8% |

| Cemig H – MWh | |||

| Free Clients | 2,564,269 | 2,370,840 | 8.2% |

| Industrial | 2,067,268 | 1,999,957 | 3.4% |

| Commercial | 458,409 | 352,946 | 29.9% |

| Rural | 38,592 | 17,937 | 115.2% |

| Free Market – Traders and cooperatives | 2,543,342 | 2,161,692 | 17.7% |

| Total Cemig H | 5,107,611 | 4,532,532 | 12.7% |

| Cemig GT + H | 10,633,900 | 10,398,491 | 2.3% |

Sources and uses of electricity

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 16 |

| |

Gasmig

Gasmig is the exclusive distributor of piped natural gas for the whole of the state of Minas Gerais. It supplies industrial, commercial and residential users, compressed natural gas and vehicle natural gas, and gas as fuel for thermoelectric generation plants. Its concession expires in January 2053. Cemig owns 99.57% of Gasmig.

Gasmig’s last Tariff Review was completed in April 2022. Highlights of that Review:

| § | The WACC used (real, after taxes) was reduced from 10.02% p.a. to 8.71% p.a. |

| § | The Net Remuneration Base was increased significantly, to R$ 3.48 billion. |

| § | The regulator recognized the PMSO cost (Personnel, Materials, outsourced Services, Other expenses) in full. |

| Market (Volume in ’000m3) | 2022 | 2023 | 2024 | Change, 2023–24 |

| Automotive | 40,950 | 31,907 | 22,511 | –29.4% |

| Compressed vehicle natural gas | 364 | 541 | 630 | 16.5% |

| Industrial | 870,667 | 830,943 | 786,363 | –5.4% |

| Industrial compressed natural gas | 13,616 | 12,473 | 10,275 | –17.6% |

| Residential | 11,392 | 11,912 | 12,095 | 1.5% |

| Co-generation | 13,137 | 12,075 | 12,164 | 0.7% |

| Commercial | 23,114 | 21,964 | 23,203 | 5.6% |

| Subtotal – conventional gas | 973,240 | 921,815 | 867,241 | –5.9% |

| Thermal plants | 37,991 | – | – | – |

| Subtotal – gas sold | 1,011,231 | 921,815 | 867,241 | –5.9% |

| Industrial – Free Market | 87,133 | 92,362 | 97,302 | 5.3% |

| Industrial compressed natural gas – Free Market | – | – | 10,421 | – |

| Thermal – Free Market | 7,119 | 19,050 | 58,046 | 205% |

| Total (sales + Free Clients) | 1,105,483 | 1,033,227 | 1,033,010 | 0.0% |

| Ebitda (R$ ’000) | 4Q24 | 4Q23 |

| Profit (loss) for the period | 112,101 | 138,803 |

| Net finance income (expenses) | 15,189 | 2,649 |

| Income tax and Social Contribution tax | 28,569 | 40,011 |

| Depreciation and amortization | 23,361 | 22,257 |

| Ebitda per CVM Resolution 156 | 179,150 | 203,720 |

The volume of gas sold in 2024 was 5.9% lower than in 2023, while the volume distributed to industrial Free Clients was 48.8% higher. In 4Q24, total volume sold was 259,900 m3, 1.5% lower than in 4Q23; the captive market diminished by 3.9%, and the free market grew 11.9%.

Gasmig’s Ebitda was 11.3% lower in 4Q24 than 4Q23, reflecting lower volume of gas sold to the captive market.

The number of Gasmig’s clients increased by 8.3% from 4Q23, to a total of 103,885 consumers in December 2024. This reflects expansion of both the commercial and the residential client bases (addition of 8,000 clients).

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 17 |

| |

CONSOLIDATED RESULTS

Net profit

Cemig reports 4Q24 net profit of R$ 998 million, which compares with net profit of R$ 1,886 million in 4Q23. 4Q24 Adjusted net profit is R$ 1,166 million, vs. R$ 1,684 million in 4Q23. Main factors in this result were:

| § | Profit in electricity trading was 61% lower YoY: the 4Q23 comparison base was high, due to a successful strategy in that quarter which achieved a margin significantly above the historical average. |

| § | Equity income (the gain/loss in non-consolidated investees) was R$ 106.4 million lower, due to (i) a weaker result in Belo Monte, and (ii) the absence of Aliança Energia, after Cemig sold its stake in Aliança in 3Q24. |

| § | Cemig D distributed 1.0% less energy in 4Q24 than in 4Q23. |

| § | Net profit of Gasmig was R$ 26.7 million lower, YoY, on lower volume of gas distributed, and worst net financial result. |

| § | Net profit of Cemig D was R$ 52 million higher YoY, mainly reflecting the reduction in energy losses. |

| § | 4Q23 comp: Sales of Baguari and Retiro Baixo provided a gain of R$ 201.9 million in the profit of 4Q23. |

Main non-recurring effects:

| § | Negative: R$ 40.7 million impairment of the entire goodwill carried for the investment in Norte Energia. |

| § | Positive: Reversal, after the successful auction in December of four Small Hydro Plants, of the R$ 11.7 million provision that had been made in 1Q24 for potential impairment of their value. |

| § | Negative: FX variation in 4Q on the US dollar debt, net of the hedge, was R$ 139.5 million negative, compared to R$ 0.5 million positive in 4Q23. The debt was settled in full on December 5. Cemig now has no FX exposure. |

More details of these variations are given below.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 18 |

| |

Operational revenue

| 4Q24 | 4Q23 | Change % | |

| R$ ’000 | |||

| Revenue from supply of electricity | 9,621,909 | 8,917,462 | 7.9% |

| Revenue from use of distribution systems (TUSD charge) | 1,375,131 | 1,192,593 | 15.3% |

| CVA and Other financial components in tariff adjustments | 46,797 | –149,466 | –131.3% |

| Reimbursement to consumers of PIS, Pasep and Cofins tax credits | 0 | 339,403 | –100.0% |

| Transmission – Operation and Maintenance revenue | –20,355 | 93,755 | –121.7% |

| Transmission – Construction revenue | 144,472 | 92,883 | 55.5% |

| Financial remuneration of transmission contractual assets | 219,467 | 123,340 | 77.9% |

| Generation capital reimbursement | 23,232 | 22,783 | 2.0% |

| Distribution construction revenue | 1,402,318 | 1,141,888 | 22.8% |

|

Adjustment to expectation of cash flow from indemnifiable financial assets of the distribution concession |

34,754 | 22,086 | 57.4% |

| Gain on financial updating of Concession Grant Fee | 117,770 | 97,046 | 21.4% |

| Settlements on CCEE | 10,078 | 65,949 | –84.7% |

| Retail supply of gas | 988,396 | 952,998 | 3.7% |

| Fine for continuity indicator shortfall | –45,311 | –46,066 | –1.6% |

| Other revenues | 843,978 | 634,041 | 33.1% |

| Taxes and charges reported as deductions from revenue | –3,585,759 | –3,544,009 | 1.2% |

| Net revenue | 11,176,877 | 9,956,686 | 12.3% |

Revenue from supply of electricity

| 4Q24 | 4Q23 | Change, % | |||||||

| MWh | R$ ’000 |

Average price billed R$/MWh (1) |

MWh | R$ ’000 |

Average price billed R$/MWh (1) |

MWh | R$ ’000 | ||

| Residential | 3,759,818 | 3,654,240 | 971.92 | 3,695,589 | 3,169,467 | 857.64 | 1.7% | 15.3% | |

| Industrial | 4,596,957 | 1,372,739 | 298.62 | 4,642,626 | 1,470,323 | 316.7 | –1.0% | –6.6% | |

| Commercial, services and others | 2,808,877 | 1,752,088 | 623.77 | 3,045,990 | 1,706,210 | 560.15 | –7.8% | 2.7% | |

| Rural | 783,160 | 659,721 | 842.38 | 981,836 | 641,985 | 653.86 | –20.2% | 2.8% | |

| Public authorities | 263,884 | 261,667 | 991.6 | 284,337 | 243,756 | 857.28 | –7.2% | 7.3% | |

| Public lighting | 237,575 | 141,545 | 595.79 | 255,135 | 133,719 | 524.11 | –6.9% | 5.9% | |

| Public services | 203,044 | 184,125 | 906.82 | 268,988 | 208,204 | 774.03 | –24.5% | –11.6% | |

| Subtotal | 12,653,315 | 8,026,125 | 634.31 | 13,174,501 | 7,573,664 | 574.87 | –4.0% | 6.0% | |

| Own consumption | 7,678 | – | – | 8,005 | – | – | –4.1% | – | |

| Retail supply not yet invoiced, net | – | 224,546 | – | – | 108,855 | – | – | – | |

| 12,660,993 | 8,250,671 | 634.31 | 13,182,506 | 7,682,519 | 574.87 | –4.0% | 7.4% | ||

|

Wholesale supply to other concession holders (2) |

4,762,961 | 1,338,863 | 281.1 | 4,742,073 | 1,206,718 | 254.47 | 0.4% | 11.0% | |

|

Wholesale supply not yet invoiced, net |

– | 32,375 | – | – | 28,225 | – | – | 14.7% | |

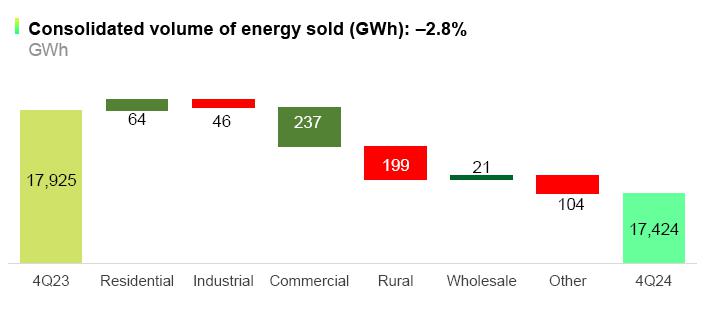

| Total | 17,423,954 | 9,621,909 | 537.71 | 17,924,579 | 8,917,462 | 490.07 | –2.8% | 7.9% | |

| (1) | The calculation of average price does not include revenue from supply not yet billed. |

| (2) | Includes Regulated Market Electricity Sale Contracts (CCEARs) and ‘bilateral’ contracts with other agents. |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 19 |

| |

Energy sold to final consumers

Gross revenue from energy sold to final consumers in 4Q24 was R$ 8,250.7 million, which compares with R$ 7,682.50 million in 4Q23, a year-on-year increase of 7.4%, in spite of the total volume of energy sold to final consumers being 4.0% lower. The variation in revenue is mainly explained by the tariff increase for Distribution which came into effect on May 28, 2024, with average effect of 7.32%.

Transmission

| 4Q24 | 4Q23 | Change % | |

| TRANSMISSION REVENUE (R$ ’000) | |||

| Operation and maintenance | –20,355 | 93,755 | –121.7% |

| Infrastructure construction, updating and enhancement | 144,472 | 92,883 | 55.5% |

| Financial remuneration of transmission contractual assets | 219,467 | 123,340 | 77.9% |

| Total | 343,584 | 309,978 | 10.8% |

Transmission revenues amounted to R$343.6 million in 4Q24, an increase of R$33.6 million over 4Q23. This growth was influenced by the 55.5% increase (+R$51.6 million) in construction revenue, mainly due to the greater volume invested in reinforcements and improvements and the implementation of lot 1 of the 02/2022 auction. Revenue from operation and maintenance plus the remuneration of contract assets totaled R$199.1 million, representing a reduction of 8.3%. (Note that the revenues shown take into account eliminations of transactions between the companies consolidated in the group).

Gas

Gross revenue from supply of gas in 4Q24 totaled R$ 988.4 million, compared to R$ 953.0 million in 4Q23. This higher figure reflects the higher prices charged to consumers than in the prior year – the increase in prices for acquisition of gas were passed through to the consumer.

Revenue from Use of Distribution Systems – the TUSD charge

| 4Q24 | 4Q23 | Change % | |

| TUSD (R$ ’000) | |||

| Use of the Electricity Distribution System | 1,375,131 | 1,192,593 | 15.3% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 20 |

| |

In 4Q24 revenue from the TUSD – charged to Free Consumers for distribution of their energy – was R$ 182.5 million higher than in 4Q23. This mainly reflects: (i) volume of energy transported for Free Clients 7.2% higher; and (ii) the distribution company’s annual tariff adjustment.

| 4Q24 | 4Q23 | Change % | |

| POWER TRANSPORTED – MWh | |||

| Industrial | 5,547,167 | 5,269,387 | 5.3% |

| Commercial | 667,576 | 580,480 | 15.0% |

| Rural | 26,629 | 13,980 | 90.5% |

| Public services | 176,062 | 117,970 | 49.2% |

| Concession holders | 87,742 | 86,502 | 1.4% |

| Total energy transported | 6,505,176 | 6,068,320 | 7.2% |

Operational costs and expenses

| 4Q24 | 4Q23 | Change % | |

| CONSOLIDATED (R$ ’000) | |||

| Electricity bought for resale | 4,922,913 | 3,957,150 | 24.4% |

| Charges for use of national grid | 691,644 | 762,268 | –9.3% |

| Gas purchased for resale | 563,716 | 522,622 | 7.9% |

| Construction cost | 1,518,396 | 1,210,562 | 25.4% |

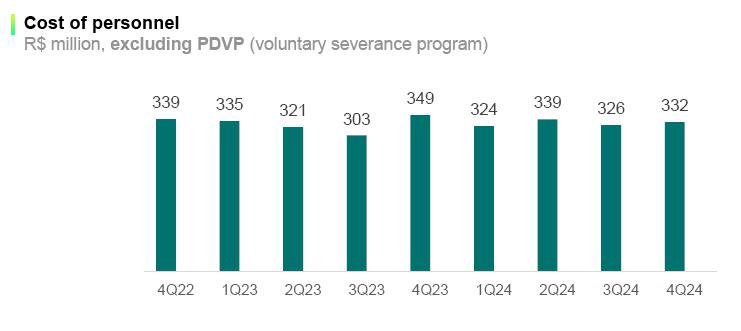

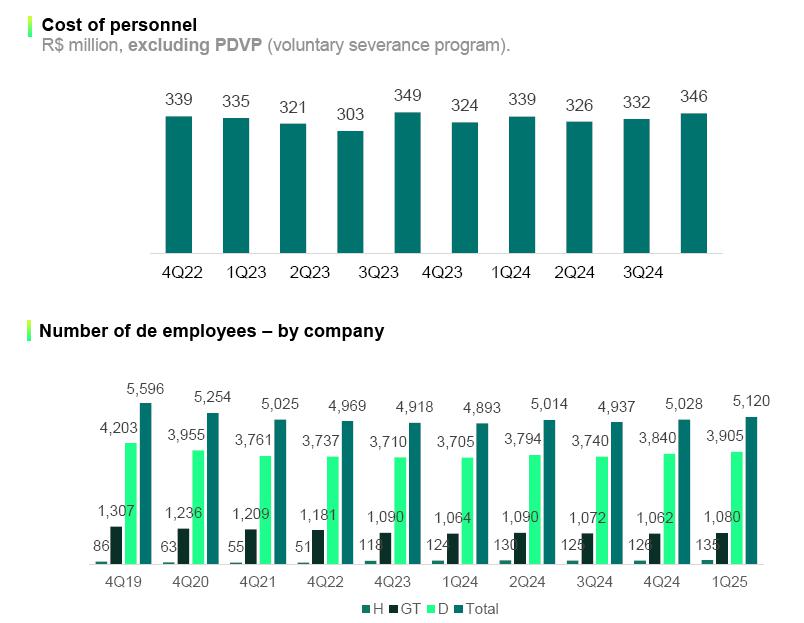

| People | 332,460 | 348,543 | –4.6% |

| Employees’ and managers’ profit shares | 48,902 | 38,746 | 26.2% |

| Post-employment liabilities | 121,809 | 161,347 | –24.5% |

| Materials | 36,933 | 51,276 | –28.0% |

| Outsourced services | 618,024 | 511,225 | 20.9% |

| Depreciation and amortization | 363,995 | 351,452 | 3.6% |

| Provisions (reversals) | 169,850 | 88,390 | 92.2% |

| Impairment | 17,087 | 0 | – |

| Provisions for client default | 72,204 | 102,311 | –29.4% |

| Provision for loss with related party | 0 | 1,250 | – |

| Other operating costs and expenses | 181,519 | 185,091 | –1.9% |

| Other costs and expenses | 9,659,452 | 8,292,233 | 16.5% |

| Gain on disposal of investments | 0 | –288,308 | – |

| Adjustment to fair value of prior holding | 0 | –8,638 | – |

| Total, other revenues (reducing expenses) | 0 | –296,946 | – |

| Total | 9,659,452 | 7,995,287 | 20.8% |

Operational costs and expenses in 4Q24 totaled R$ 9.66 billion, compared to R$ 7.99 billion in 4Q23. The main factors in the higher total were: Cost of energy bought for resale was R$ 965.8 million higher; cost of construction was R$ 307.8 million higher; and outsourced services, R$ 106.8 million higher. Also, in 4Q23, the account Other revenues reducing expenses posted a total of R$ 296.9 million. See more details on costs and expenses in the following pages.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 21 |

| |

Electricity purchased for resale

| 4Q24 | 4Q23 | Change % | |

| CONSOLIDATED (R$ ’000) | |||

| Electricity acquired in Free Market | 1,573,303 | 1,551,187 | 1.4% |

| Electricity acquired in Regulated Market auctions | 1,302,137 | 1,043,326 | 24.8% |

| Distributed generation | 1,038,791 | 669,582 | 55.1% |

| Spot market | 523,810 | 119,014 | 340.1% |

| Supply from Itaipu Binacional | 312,780 | 310,765 | 0.6% |

| Physical guarantee quota contracts | 215,798 | 243,828 | –11.5% |

| Individual (‘bilateral’) contracts | 124,309 | 128,695 | –3.4% |

| Proinfa | 122,333 | 126,923 | –3.6% |

| Quotas for Angra I and II nuclear plants | 92,453 | 91,736 | 0.8% |

| Credits of PIS, Pasep and Cofins taxes | –382,799 | –327,906 | 16.7% |

| 4,922,915 | 3,957,150 | 24.4% |

The consolidated expense on electricity bought for resale in 4Q24 was R$ 4.92 billion, an increase of 24.4% (R$ 965.8 million) from 4Q23. This reflects, mainly:

| § | Regulated Market: Expenses on energy acquired in the Regulated Market were R$ 258.8 million (+24.8%) higher than in 4Q23, reflecting (i) the annual adjustments to contracts, by the IPCA inflation index, and (ii) entry of new contracts. |

| § | Distributed generation: The expense on distributed generation was R$ 369.2 million (+55.1%) higher, reflecting the 20% growth in the number of generation units (from 250,000 in December 2024, to 302,000 in December 2024). The volume of energy injected from distributed generation in 4Q24, at 1,656 GWh, was 15.1% higher than in 4Q23. |

| § | Free Market: The costs of energy acquired in the Free Market (Cemig’s highest cost of purchased energy) totaled R$ 1,573 million, an increase of R$ 22.1 million (+1.4%) in relation to 4Q23. |

| § | Spot market: There was a net increase of R$ 404.8 million in the cost of purchases in the spot market, caused mainly by the impact of the hourly modulation in the spot price, especially in Cemig D, and also by a higher cost of hydrological risk, due to the weaker hydrology in 2024. |

(Note:) For Cemig D, purchased energy is a non-manageable cost: the difference between the amounts used as a reference for calculation of tariffs and the costs actually incurred is compensated for in the next tariff adjustment.

| Energy purchased – Cemig D | 4Q24 | 4Q23 | Change % |

| Cemig D (R$ ’000) | |||

| Supply acquired in auctions on the Regulated Market | 1,313,284 | 1,087,449 | 20.8% |

| Distributed generation | 1,038,791 | 669,582 | 55.1% |

| Spot market – CCEE | 355,623 | 121,212 | 193.4% |

| Supply from Itaipu Binacional | 312,780 | 310,765 | 0.6% |

| Physical guarantee quota contracts | 220,087 | 247,007 | –10.9% |

| Individual (‘bilateral’) contracts | 124,309 | 128,695 | –3.4% |

| Proinfa | 122,333 | 126,923 | –3.6% |

| Quotas for Angra I and II nuclear plants | 92,453 | 91,736 | 0.8% |

| Credits of PIS, Pasep and Cofins taxes | –223,600 | –184,972 | 20.9% |

| 3,356,060 | 2,598,397 | 29.2% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 22 |

| |

Charges for use of the transmission network and other system charges

Charges for use of the transmission network in 4Q24 were R$ 691.6 million, 9.3% lower than in 4Q23.

(This is a non-manageable cost in the distribution business: the difference between the amounts used as a reference for calculation of tariffs and the costs actually incurred is compensated for in the next tariff adjustment.)

Gas purchased for resale

The expense on acquisition of gas in 4Q24 was R$ 563.7 million, or 7.9% higher than in 4Q23. This variation reflects a higher price of gas purchased for resale, but with volume of gas distributed 1.5% lower.

Outsourced services

Expenditure on outsourced services was 20.9% (R$ 106.8 million) higher than in 4Q23, the main factors being: (i) maintenance of electrical facilities and equipment, R$ 22.1 million (10.6%) higher; (ii) the expense on tree pruning, R$ 9.3 million (54.9%) higher; (iii) expense on IT R$ 7.4 million (15.6%) higher; and (iv) cleaning of power line pathways, R$ 7.3 million (21.4%) higher.

Provisions for client default

The expense on provisions for losses due to client default in 4Q24 was R$ 72.2 million, or R$ 30.1 million lower than in 4Q23, reflecting both (i) the Company’s efforts in combating default, and (ii) the revision, in 3Q24 (with positive effect in the subsequent 12 months), of the criteria for accounting overdue client receivables (increasing the threshold for posting a 100% write-off from 12 to 36 months, to provide a more faithful reflection of the actual behavior of Cemig clients in practice).

Provisions

Provisions in 4Q24 totaled R$ 186.9 million, compared to R$ 88.4 million in 4Q23. This included a provision of R$ 40.7 million for impairment of goodwill in Aliança Norte, and higher contingency provisions for employment-law and third-party-liability legal actions.

Post-employment liabilities

The impact of the post-retirement obligations on operational profit in 4Q24 was an expense of R$ 121.8 million, compared to an expense of R$ 161.3 million in 4Q23.

People

The expense on personnel in 4Q24 was R$ 332.5 million, compared to R$ 348.5 million in 4Q23. The figure was 4.6% lower in spite of the 4.6% increase in salaries from November 2024, under the Collective Work Agreement.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 23 |

| |

Finance income and expenses

| 4Q24 | 4Q23 | Change % | |

| (R$ ’000) | |||

| Finance income | 283,578 | 368,351 | –23.0% |

| Finance expenses | –679,958 | –466,361 | 45.8% |

| Net finance income (expenses) | –396,380 | –98,010 | 304.4% |

For 4Q24 the Company posted consolidated net financial expenses of R$ 396.4 million, compared to net financial expenses of R$ 98 million in 4Q23. Main factors:

| § | FX variation: Net negative effect, of R$ 211.4 million, in 4Q24, from foreign exchange variation on the debt in US dollars and the related hedge. This effect in 4Q24 reflects 11.2% appreciation in the US dollar exchange rate up to December 5 (the date when the debt was settled) – whereas in 4Q23, this effect had been positive, at R$ 0.8 million, as the dollar depreciated (3.3%) against the Real in that quarter. |

| § | Monetary updating of loans: The financial expense posted for monetary updating of loans was R$ 71.4 million higher, and borrowing costs were R$ 35.4 million higher – reflecting (i) gross debt R$ 2.4 billion higher, and (ii) higher IPCA inflation in the quarter (1.47%) than in 4Q23 (1.08%). |

| § | Revenue from cash investments, on the other hand, at R$ 148.9 million, was R$ 20.9 million higher than in 4Q23 – mainly on a higher volume of cash available for investment in 4Q24. |

Eurobonds: Effects in fourth quarter R$ ’000

| 4Q24 | 4Q23 | |

| Effect of FX variation on the debt | –232,629 | 117,828 |

| Effect on the hedge | 21,242 | –117,019 |

| Net effect in Finance income (expenses) | –211,387 | 809 |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 24 |

| |

Equity income (Gain / loss in non-consolidated investees)

| R$ ’000 | 4Q24 | 4Q23 | Change R$ ’000 |

| Gain/loss in non-consolidated investees | |||

| Taesa | 110,989 | 97,880 | 13,109 |

| Aliança Geração | – | 37,780 | –37,780 |

| Paracambi | 7,877 | 4,177 | 3,700 |

| Hidrelétrica Pipoca | 2,957 | 2,668 | 289 |

| Hidrelétrica Cachoeirão | 1,448 | 1,851 | –403 |

| Guanhães Energia | 5,595 | 17,977 | –12,382 |

| Cemig Sim (Equity holdings) | 5,488 | 8,037 | –2,549 |

| Baguari Energia | – | – | 0 |

| Retiro Baixo | – | – | 0 |

| Belo Monte (Aliança Norte and Amazônia Energia) | –101,509 | –31,115 | –70,394 |

| Itaocara | – | – | 0 |

| Total | 32,845 | 139,255 | –106,410 |

The gain in equity value of the Company’s holdings in non-consolidated investees in 4Q24 was R$ 106.4 million lower than in 4Q23. The main factors were:

(i) a weaker result in Belo Monte, on higher finance expenses, due to the higher TJLP (long-term interest rate) in 4Q24 and higher cost of purchasing energy to cover exposure to the MRE (Surpluses Reallocation Mechanism); and

(ii) the fact that Cemig no longer has an interest in Aliança Geração, after that asset was sold in 3Q24.

| (iii) | On the other hand the contribution of Taesa in 4Q24, was R$ 13.1 million higher YoY, at R$ 111.0 million. |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 25 |

| |

CONSOLIDATED EBITDA (IFRS, and Adjusted)

Ebitda is a non-accounting metric, prepared by the Company, reconciled with its consolidated financial statements in accordance with the specifications in CVM Circular SNC/SEP 01/2007 and CVM Resolution 156 of June 23, 2022. It comprises: Net profit adjusted for the effects of: (i) Net finance income (expenses); (ii) Depreciation and amortization; and (iii) Income tax and the Social Contribution tax. Ebitda is not a metric recognized by Brazilian GAAP nor by IFRS; it does not have a standard meaning; and it may be non-comparable with metrics with similar titles provided by other companies. Cemig publishes Ebitda because it uses it to measure its own performance. Ebitda should not be considered in isolation or as a substitute for net profit or operational profit, nor as an indicator of operational performance or cash flow, nor to measure liquidity, nor capacity for payment of debt. In accordance with CVM Instruction 156/2022, the Company adjusts Ebitda to exclude extraordinary items which, by their nature, do not contribute to information on the potential for gross cash flow generation.

| Consolidated Ebitda 2024 | |||||||

| Ebitda - 2024 - R$ mn | Generation | Transmission | Trading | Distribution | Gas | Holding co. and equity interests | Total |

| Profit (loss) for the period | 1,281 | 1,560 | 517 | 2,206 | 498 | 1,057 | 7,119 |

| Income tax and Social Contribution tax | 334 | 557 | 136 | 662 | 213 | 336 | 2,238 |

| Net finance income (expenses) | 180 | 108 | -24 | 17 | 52 | 188 | 521 |

| Depreciation and amortization | 325 | 9 | - | 922 | 98 | 22 | 1,376 |

| Ebitda per CVM Resolution 156 | 2,120 | 2,234 | 629 | 3,807 | 861 | 1,603 | 11,254 |

| Non-recurring and non-cash effects | |||||||

| Net profit attributed to non–controlling stockholders | - | - | - | - | -2 | - | -2 |

| Gain on disposal of investments (SHPs) | -43 | - | - | - | - | - | -43 |

| Asset impairment | - | - | 5 | - | - | 41 | 46 |

| Provision for civil action on an energy sale | - | - | 53 | - | - | - | 53 |

| Reversal of tax provision – Social security contributions on profit sharing |

-31 | -33 | -5 | -513 | - | -3 | -585 |

| Voluntary retirement program | 9 | 10 | 2 | 56 | - | 1 | 78 |

| Gain on disposal of investments (Aliança) | - | - | - | - | - | -1,617 | -1,617 |

| Result of the Transmission Periodic Tariff Review |

- | -1,521 | - | - | - | - | -1,521 |

| Reversal of provision with related party (Aliança) | - | - | - | - | - | -58 | -58 |

| Adjusted Ebitda | 2,055 | 690 | 684 | 3,350 | 859 | -33 | 7,605 |

| Consolidated 4Q24 Ebitda | |||||||

| R$ mn | Generation | Transmission | Trading | Distribution | Gas | Holding co. and equity interests | Total |

| Profit (loss) for the period | 327 | 118 | 129 | 452 | 112 | –141 | 998 |

|

Income tax and Social Contribution tax |

50 | 7 | 32 | 117 | 27 | –76 | 156 |

| Net finance income (expenses) | 79 | 68 | –7 | 138 | 15 | 103 | 397 |

| Depreciation and amortization | 79 | 3 | 0 | 252 | 25 | 5 | 364 |

| Ebitda per CVM Resolution 156 | 536 | 196 | 155 | 958 | 179 | –110 | 1,914 |

|

Reversal of impairment (Small Hydro Plants) |

–18 | – | – | – | – | – | –18 |

| Impairment (goodwill) | – | – | – | – | – | 41 | 41 |

| Adjusted Ebitda: | 518 | 196 | 155 | 958 | 179 | –69 | 1,937 |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 26 |

| |

| Consolidated Ebitda 2023 | |||||||

| Ebitda - 2023 - R$ mn | Generation | Transmission | Trading | Distribution | Gas | Holding co. and equity interests | Total |

| Profit (loss) for the period | 1,387 | 465 | 959 | 1,611 | 596 | 749 | 5,767 |

| Income tax and Social Contribution tax | 326 | 114 | 428 | 405 | 248 | -437 | 1,084 |

| Net finance income (expenses) | 12 | 47 | -82 | 253 | 9 | 140 | 379 |

| Depreciation and amortization | 327 | 1 | - | 834 | 94 | 18 | 1,274 |

| Ebitda per CVM Resolution 156 | 2,052 | 627 | 1,305 | 3,103 | 947 | 470 | 8,504 |

| Non-recurring and non-cash effects | |||||||

| Net profit attributed to non–controlling stockholders | - | - | - | - | -3 | - | -3 |

| Gain on disposal of investments | - | - | - | - | - | -344 | -344 |

| Remeasurement of post-employment liabilities | -11 | -7 | -1 | -34 | - | -4 | -57 |

| Others | - | - | -22 | - | - | - | -22 |

| Adjusted Ebitda | 2,041 | 620 | 1,282 | 3,069 | 944 | 122 | 8,078 |

| Consolidated 4Q23 Ebitda | |||||||

| R$ mn | Generation | Transmission | Trading | Distribution | Gas | Holding co. and equity interests | Total |

| Profit (loss) for the period | 337 | 123 | 335 | 401 | 139 | 552 | 1,886 |

|

Income tax and Social Contribution tax |

51 | 27 | 121 | 94 | 38 | –214 | 117 |

| Net finance income (expenses) | 5 | 9 | –28 | 73 | 3 | 36 | 98 |

| Depreciation and amortization | 85 | 1 | 0 | 237 | 24 | 3 | 351 |

| Ebitda per CVM Resolution 156 | 478 | 160 | 428 | 805 | 204 | 378 | 2,452 |

| Gain on sale of investment | – | – | – | – | – | –289 | –289 |

| Adjusted Ebitda | 478 | 160 | 428 | 805 | 203 | 89 | 2,163 |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 27 |

| |

Ebitda of Cemig D

| R$ ’000 | 4Q24 | 4Q23 | Change % |

| Cemig D Ebitda – R$ mn | |||

| Net profit for the period | 452 | 400 | 13.0% |

| Income tax and Social Contribution tax | 117 | 93 | 24.8% |

| Net finance income (expense) | 138 | 73 | 89.7% |

| Amortization | 252 | 238 | 5.9% |

| Ebitda per CVM Resolution 156 | 958 | 804 | 19.2% |

| New replacement value (VNR) | 35 | 22 | 57.4% |

| Ebitda less VNR | 924 | 782 | 18.1% |

Cemig D posted Ebitda of R$ 958 million, 19.2% more than the Ebitda of 4Q23.

Main effects in Ebitda in the quarter:

| § | Lower energy losses: Positive impact of the significant reduction in energy losses to 10.31% in the 12 months to December 2024 (from 10.76% in the 12 months to September 2024) – once again within the required regulatory limit. |

| § | New Replacement Value (VNR) of R$34.7 in 4Q24 and R$ 22.1 million in 4Q23. |

| § | Allowance for client default losses R$ 12.4 million lower than in 4Q23. |

| § | Total energy volume distributed was 1.0% lower than in 4Q23 (8.9% lower in the captive market, and 7.2% higher in the Free Market). This reflected milder temperatures and higher rainfall than in 4Q23 – resulting in lower consumption by the rural, commercial and residential categories (respectively down 15.8%, 5.9%, and 0.6%) – though consumption by the industrial segment, on the other hand, was up 3.7% YoY. |

| § | PMSO (Personnel, Materials, outsourced Services, Other) expenses were up 3.1% YoY – less than the inflation of 2024, which was 4.83%. |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 28 |

| |

Cemig GT – Ebitda

| Cemig GT: 4Q24 Ebitda | |||||

| R$ mn | Generation | Transmission | Trading | Equity interests | Total |

| Profit (loss) for the period | 333 | 111 | –20 | –183 | 241 |

| Income tax and Social Contribution tax | 50 | 6 | –33 | –40 | –17 |

| Net finance income (expenses) | 79 | 69 | –7 | 80 | 221 |

| Depreciation and amortization | 73 | 9 | 0 | 0 | 82 |

| Ebitda per CVM Resolution 156 | 536 | 194 | –60 | –143 | 527 |

| Impairments (reversals) | –18 | 0 | 0 | 41 | 23 |

| Adjusted Ebitda | 518 | 194 | –60 | –102 | 550 |

| Cemig GT 4Q23 Ebitda | |||||

| R$ mn | Generation | Transmission | Trading | Equity interests | Total |

| Profit (loss) for the period | 344 | 120 | 201 | 180 | 844 |

| Income tax and Social Contribution tax | 50 | 25 | 52 | 106 | 233 |

| Net finance income (expenses) | 5 | 9 | –27 | 23 | 9 |

| Depreciation and amortization | 86 | 1 | 0 | 0 | 87 |

| Ebitda per CVM Resolution 156 | 484 | 155 | 225 | 309 | 1,173 |

| Gain on sale of investment | 0 | 0 | 0 | –289 | –289 |

| Adjusted Ebitda | 484 | 155 | 225 | 20 | 884 |

4Q24 Ebitda of Cemig GT was R$ 550 million, 37.8% lower than in 4Q23.

Effects on Ebitda, in this YoY comparison:

| § | Volume of energy sold, excluding settlements on the CCEE, was 5.8% lower, reflecting transfer of contracts to the Holding company. |

| § | Trading in the fourth quarter of 2023 had returned a robust performance, due to a successful strategy that produced a margin higher than the prior average, and higher than that achieved in 4Q24. |

| § | Spot market: There was a negative effect in 4Q24, due to higher exposure to the spot market, and in particular to differences in the spot price by sub-market (many purchases are made in the Northeast, and a major part of this energy is sold in other sub-markets). |

| § | Equity income: A weaker result – negative by R$ 83 million in 4Q24, compared to positive by R$ 34 million in 4Q23. The main factors were: (i) the weaker result of Belo Monte, on higher finance expenses, due to the higher TJLP (long-term interest rate) in 4Q24; (ii) higher cost of purchasing energy to cover exposure to the MRE (Surpluses Reallocation Mechanism); and (iii) the fact that we no longer have a stake in Aliança Geração, after the sale of that asset in 3Q24. |

| § | Reversal of an impairment – of R$ 17.7 million – that had been posted for potential loss on the sale of 4 Small Hydro Plants, after the 4 plants were successfully sold for a significant premium. |

| § | Recognition of impairment – of R$ 40.7 million – to the goodwill of Aliança Norte. |

| § | Comparison base: In 4Q23 there was a gain of R$ 289 million on the sales of Baguari and Retiro Baixo. |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 29 |

| |

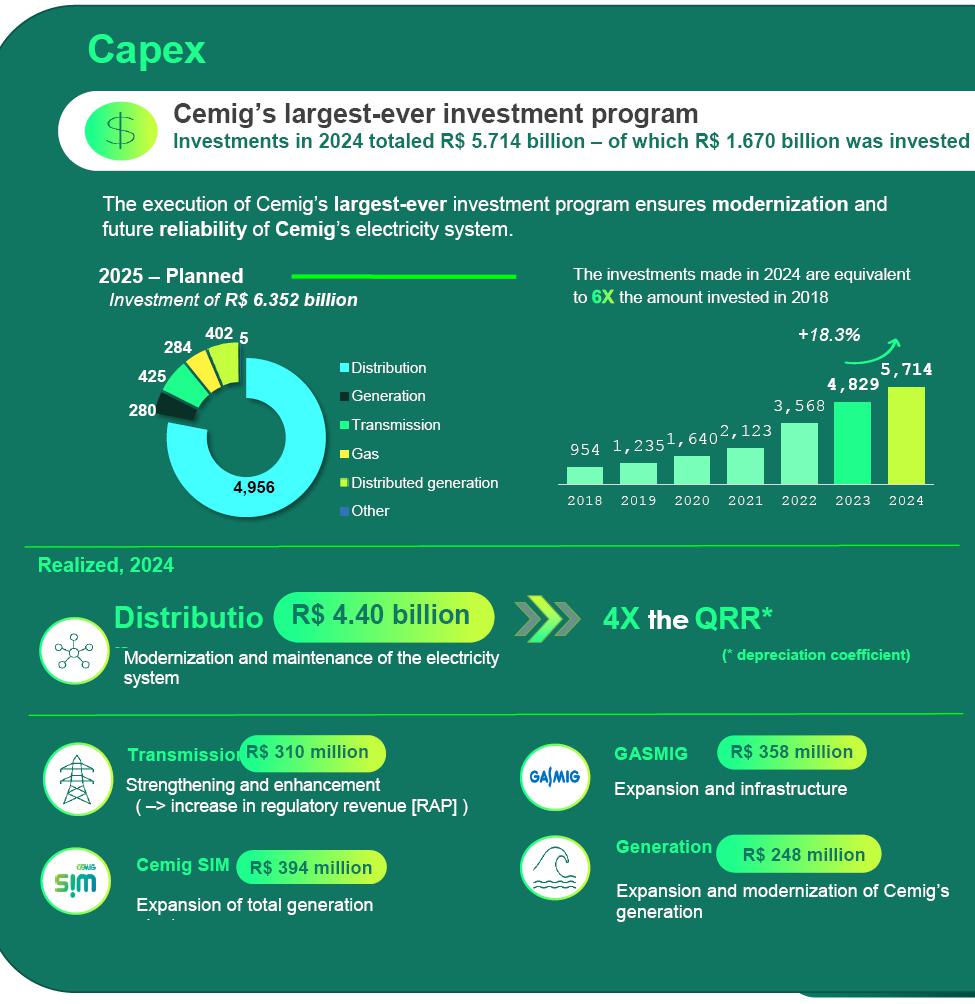

Investments

The total invested in 2024 was R$ 5.71 billion, 18.3% more than in 2023 – led by the R$ 4.40 billion investment made by Cemig D (distribution) in the year.

As well as further highlights in the year were: connection of more than 190,000 new customers; addition of 5,000 km of network; expansion of 155 MW in centralized solar generation capacity; and construction of 211 km of gas pipelines.

Execution of the largest investment program in Cemig’s history will modernize Cemig’s electricity system, ensuring reliability, in line with its strategic plan of focusing on Minas Gerais and its core businesses, providing ever-better service to the client. Investment totaling R$ 39.20 billion is planned for 2025–2029, of which R$ 6.35 billion is being invested in 2025.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 30 |

| |

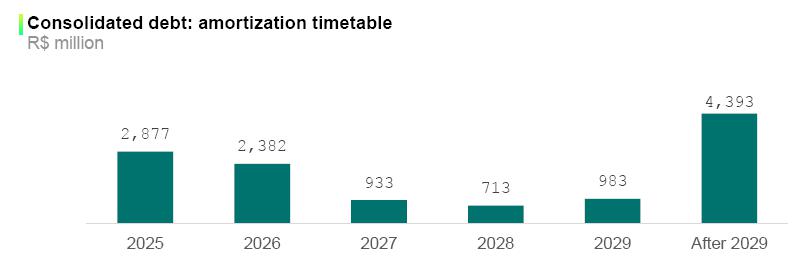

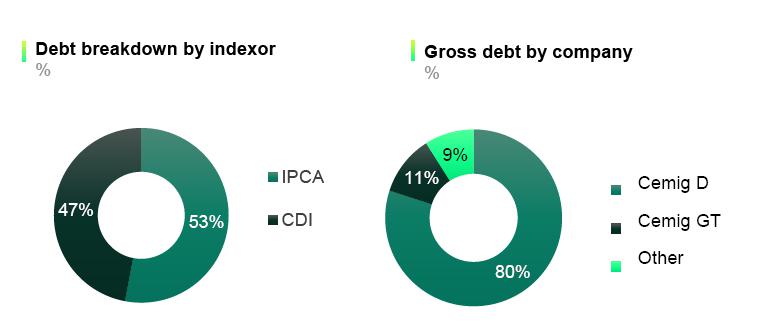

Debt

| CONSOLIDATED (R$ ’000) | 2024 | 2023 | Change, % |

| Gross debt | 12,279,300 | 9,831,139 | 24.9% |

| Cash and equivalents + Securities | 2,390,743 | 2,311,464 | 3.4% |

| Net debt | 9,888,557 | 7,519,675 | 31.5% |

| Debt in foreign currency | – | 1,854,093 | – |

| CEMIG GT (R$ ’000) | 2024 | 2023 | Change, % |

| Gross debt | 1,031,924 | 2,868,093 | –64.0% |

| Cash and equivalents + Securities | 542,566 | 937,518 | –42.1% |

| Net debt | 489,358 | 1,930,575 | –74.7% |

| Debt in foreign currency | – | 1,854,093 | – |

| CEMIG D (R$ ’000) | 2024 | 2023 | Change, % |

| Gross debt | 10,037,621 | 5,887,622 | 70.5% |

| Cash and equivalents + Securities | 1,114,866 | 450,748 | 147.3% |

| Net debt | 8,922,755 | 5,436,874 | 64.1% |

| Debt in foreign currency | – | – | – |

Cemig GT settled its Eurobonds in full in 4Q24 – an amortization totaling R$ 2,309 million. The net effect on the Company’s cash position was R$ 1,866 million (US$381 million, at the exchange rate of US$1=R$ 6.0585, less an effect of R$ 443 million under the hedge transaction). Following this settlement, Cemig now has no debt in non-Brazilian currency.

Gasmig debentures – In December 2024, Gasmig completed its 9th issue of non-convertible debentures: for a total of R$ 200 million, remunerated at the CDI rate plus 0.47% p.a., with maturity at five years and partial amortization in the third and fourth years.

Cemig D made two debenture issues in 2024, raising R$ 2.0 billion in March and R$ 2.5 billion in September.

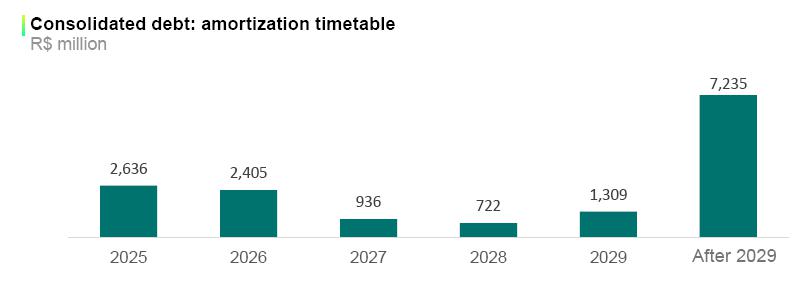

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 31 |

| |

| 4Q24 | 2024 | |

| DEBT AMORTIZED – R$ ’000 | ||

| Cemig GT | 2,308,955 | 2,308,955 |

| Cemig D | 0 | 575,916 |

| Others | 2 | 90,000 |

| Total | 2,308,957 | 2,974,871 |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 32 |

| |

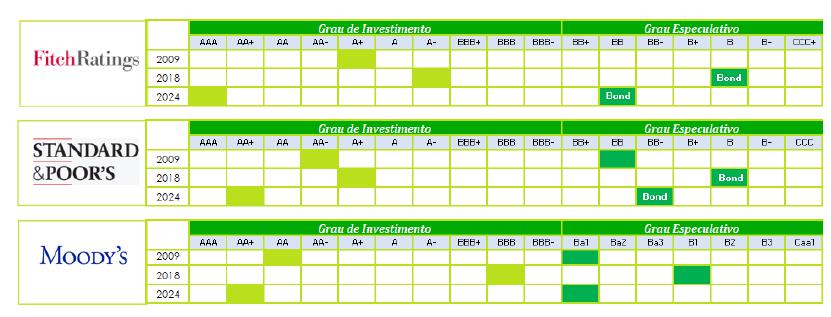

Cemig’s long-term ratings

Cemig’s ratings have improved significantly in recent years, and are currently at their highest ever.

In 2021 the three principal rating agencies upgraded their ratings for Cemig.

In April 2022, Moody’s again upgraded its rating for Cemig, this time by one notch.

In May 2024, Moody’s raised its rating to AA+.

In October 2024 Fitch raised its rating to AAA, the highest of all ratings on the Brazilian scale.

According to their note, this recognized:

(i) consistent results and cash generation,

(ii) a diversified asset base, and

(iii) discipline in capital allocation.

This table illustrates these changes:

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 33 |

| |

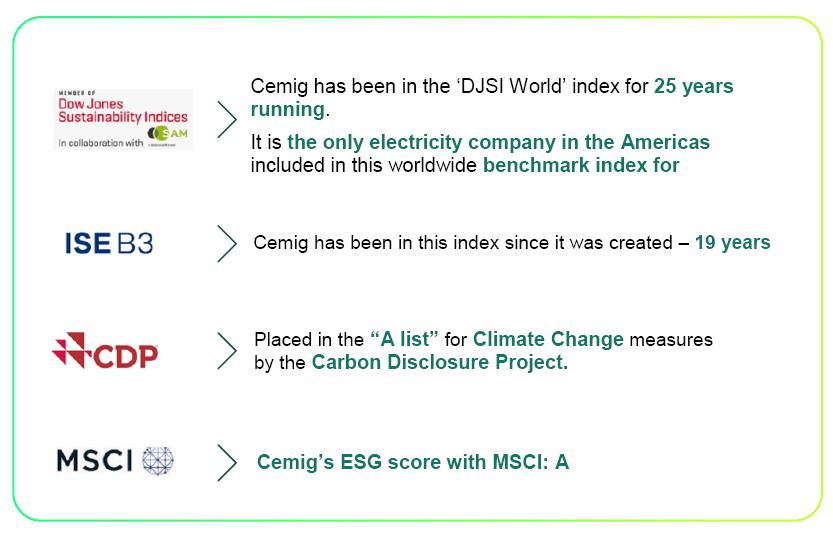

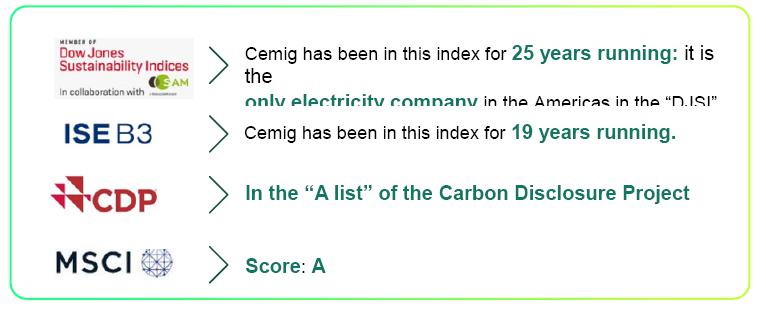

ESG – Report on performance

Cemig Highlights

| § | The Company received the highest credit risk rating in its history: Fitch Ratings increased its corporate rating from “AA+” to “AAA”, with outlook stable. |

| § | Thus, Cemig now has the highest credit risk rating on the Brazilian scale. |

| § | In 2024 Cemig was included in the Dow Jones Sustainability Index (the ‘DJSI World’) for the 25th year running. Cemig’s overall score increased by 6 points from the previous year, with leadership positions in three segments: Transparency and Reporting, Renewable Generation, and Human Rights – consolidating its position as a benchmark for sustainability in the electricity sector worldwide. |

| § | An unprecedented partnership between the Government of Minas Gerais State and Cemig attracted investments totaling R$ 265 million, expected to generate 215 jobs for the state. The SupriMinas Project resulted in attraction of a new Nansen plant, which will provide low- and medium-voltage transformers for execution of the Company’s investment program. |

| § | A work of major impact for the energy sector and the Jequitinhonha Valley region was completed: Construction of a 34.5 kV feeder serving Companhia Brasileira de Lítio (Brazilian Lithium Company). This 50-km network connects the Pedra Azul Substation to the town of Divisa Alegre, on the border with Bahia, with benefits ranging from improvement in power supply quality to economic development for the region. |

| § | Client outage time was reduced by 13% in 2024: On Cemig’s part, this reduction was made possible by its investment of more than R$ 4.4 billion in energy distribution in the year to increase resilience of the distribution system. In 2024, the total annual outage duration experienced by the Company’s consumers was reduced by approximately 2.5 hours: the average number of outages per consumer was down by 14%, and the time taken to re-establish supply was reduced by 13%. |

| § | Cemig is the first Brazilian electricity utility to have 4 GW of distributed generation connected to its concession – the equivalent of four large hydroelectric plants – enough to serve approximately 4 million people. This rapid growth reflects Cemig’s dedicated work in a robust and efficient process, which it developed to meet requests for distributed generation connections. |

Environment

| § | Net Zero Alliance – UNEZA: Cemig is the first Brazilian electricity company to join UNEZA – the Utilities for Net Zero Alliance, a global association bringing utilities together to drive the energy transition and decarbonization. Cemig’s president Reynaldo Passanezi Filho made this announcement at COP 29 in Azerbaijan. With 100% of its generation from renewable sources, Cemig has reduced its emissions by more than 50% since formally accepting the challenge of Net Zero in 2022. The decision underlines its commitment to sustainable practices aligned with the global targets for reduction of emissions by 2040. |

Social

| § | Wheelchair basketball athletes from the city of Uberaba, Minas Gerais, received a gift of 10 wheelchairs especially constructed for practice of this sport. This project is run by the Minas Gerais Wheelchair Basketball League (LMBC), which works in a partnership with the Uberaba Handicapped People's Association (ADEFU). Cemig sponsors the project, under the federal Sports Incentive Law, together with Vale. |

| § | Cemig’s Energy Efficiency Program has been awarded the CIER Energy Efficiency Certificate. This is given by the Regional Energy Integration Committee (Comisión de Integración Energética Regional – CIER). The company was recognized as a leader in the “Government, Trade and Services” category. Initiatives that helped Cemig win this award include Minas LED, Cemig in Schools (Cemig nas Escolas) and Cemig in Hospitals (Cemig nos Hospitais). |

Governance

| § | We have received ISO 37001 Anti-bribery Management System certification, under the NBR ABNT seal for this international standard, which has about 6,000 valid certificates issued worldwide. ISO 37001 specifies measures that an organization should take to prevent, detect and address bribery: Adoption of an Anti-bribery Policy; appointment of a person responsible for overseeing compliance with the policy; training of all employees; due diligence risk assessments in relation to both individuals and transaction partners; and implementation of financial and non-financial controls, and/or strengthening of existing controls. |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 34 |

| |

Cemig in the main sustainability indices

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 35 |

| |

Indicators

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 36 |

| |

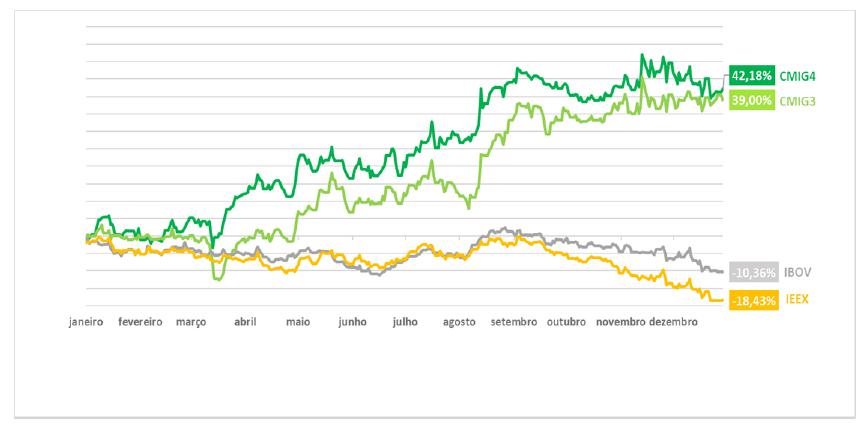

Performance of Cemig’s shares

| Security | 2024 | 2023 | Change, % |

| Prices (2) | |||

| CMIG4 (PN) at the close (R$/share) | 11.11 | 7.81 | 42.18% |

| CMIG3 (ON) at the close (R$/share) | 14.63 | 10.52 | 39.00% |

| CIG (ADR for PN shares), at close (US$/share) | 1.79 | 1.57 | 14.05% |

| CIG.C (ADR for ON shares) at close (US$/share) | 2.32 | 3.12 | –25.62% |

| XCMIG (Cemig PN shares on Latibex), close (€/share) | 1.71 | 1.88 | –9.04% |

| Average daily trading | |||

| CMIG4 (PN) (R$ mn) | 143.11 | 131.35 | 8.95% |

| CMIG3 (ON) (R$ mn) | 3.75 | 7.82 | –52.05% |

| CIG (ADR for PN shares) (US$ mn) | 4.3 | 8.98 | –52.12% |

| CIG.C (ADR for ON shares) (US$ mn) | 0.33 | 0.17 | 94.12% |

| Indices | |||

| IEE | 77,455 | 94,957 | –18.43% |

| IBOV | 120,283 | 134,185 | –10.36% |

| DJIA | 8,978 | 8,097 | 10.88% |

| Indicators | |||

| Market valuation at end of period, R$ mn | 35,149 | 27,948 | 25.77% |

| Enterprise value (EV), R$ mn (1) | 42,668 | 35,892 | 18.88% |

| Dividend yield of CMIG4 (PN) (%) (3) | 11.96 | 11.24 | 0.72 pp |

| Dividend yield of CMIG3 (ON) (%) (3) | 9.08 | 8.53 | 0.55 pp |

| (1) EV = { Market valuation [= R$/share x number of shares]} + { consolidated Net debt }. | |

| (2) Share prices adjusted for corporate action payments, including dividends. | |

| (3) (Dividends distributed in last 4 quarters) / (Share price at end of the period). | |

Cemig’s shares, by volume (aggregate of common (ON) and preferred (PN) shares), were the fourth most liquid in Brazil’s electricity sector, and among the most traded in the Brazilian equity market, in the quarter. On the NYSE, Cemig’s preferred ADRs (CIG) traded US$1.086 billion in 2024 – reflecting investors’ continued recognition of Cemig as a global investment option. In São Paulo, the benchmark Ibovespa index of the B3 Stock Exchange fell 10.36% in 2024, while Cemig’s PN (preferred) shares rose 42.18% and its ON shares rose 39.00%. These were the highest rises of any Brazilian power sector stock in the period. In New York the ADRs for Cemig’s preferred shares rose 14.05% in 2024, and the ADRs for the common shares fell 25.62%.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 37 |

| |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 38 |

| |

Cemig generation plants

| Plant | Company | Cemig power (MW) | Cemig physical guarantee (MW) | Concession ends: | Type |

Cemig interest |

||

| Emborcação | Cemig GT | 1,192 | 475 | May 2027 | Hydro | 100.0% | ||

| Nova Ponte | Cemig GT | 510 | 257 | Aug. 2027 | Hydro | 100.0% | ||

| Irapé | Cemig GT | 399 | 198 | Sep. 2037 | Hydro | 100.0% | ||

| Três Marias | Cemig GT | 396 | 227 | Jan. 2053 | Hydro | 100.0% | ||

| Salto Grande | Cemig GT | 102 | 74 | Jan. 2053 | Hydro | 100.0% | ||

| Boa Esperança | Cemig GT | 85 | 25 | Aug. 2057 | Solar | 100.0% | ||

| Sá Carvalho | Sá Carvalho S.A. | 78 | 54 | Aug. 2026 | Hydro | 100.0% | ||

| Três Marias Jusante | Cemig GT | 70 | 20 | Feb. 2058 | Solar | 100.0% | ||

| Rosal | Rosal Energia S.A. | 55 | 28 | Dec. 2035 | Hydro | 100.0% | ||

| Itutinga | Cemig Ger. Itutinga | 52 | 27 | Jan. 2053 | Hydro | 100.0% | ||

| Camargos | Cemig Ger. Camargos | 46 | 22 | Jan. 2053 | Hydro | 100.0% | ||

| Volta do Rio | Cemig GT | 42 | 18 | Dec. 2031 | Wind | 100.0% | ||

| Poço Fundo | Cemig GT | 30 | 17 | May 2052 | Small Hydro | 100.0% | ||

| Praias do Parajuru | Cemig GT | 29 | 8 | Sep. 2032 | Wind | 100.0% | ||

| Pai Joaquim | Cemig PCH S.A. | 23 | 14 | Oct. 2033 | Small Hydro | 100.0% | ||

| Piau | Cemig Ger. Sul | 18 | 14 | Jan. 2053 | Hydro | 100.0% | ||

| Gafanhoto | Cemig Ger. Oeste | 14 | 7 | Jan. 2053 | Hydro | 100.0% | ||

| Peti | Cemig Ger. Leste | 9 | 6 | Jan. 2053 | Hydro | 100.0% | ||

| Tronqueiras | Cemig Ger. Leste | 9 | 3 | Dec. 2046 | Hydro | 100.0% | ||

| Joasal | Cemig Ger. Sul | 8 | 5 | Jan. 2053 | Hydro | 100.0% | ||

| Queimado | Cemig GT | 87 | 65 | July 2034 | Hydro | 82.5% | ||

| Belo Monte | Norte Energia | 1,313 | 534 | Jul. 2046 | Hydro | 11.7% | ||

| Cachoeirão | Cachoeirão | 13 | 8 | Sep. 2033 | Small Hydro | 49.0% | ||

| Paracambi | LightGer | 12 | 10 | Jan. 2034 | Hydro | 49.0% | ||

| Pipoca | Hidrelétrica Pipoca | 10 | 6 | Dec. 2034 | Small Hydro | 49.0% | ||

| Others | 76 | 37 | ||||||

| Subtotal | 4,678 | 2,158 | ||||||

| Cemig Sim (MWp) | Via equity interests | 29 | 5.5 | Solar | 49.00% | |||

| Cemig Sim (MWp) | Owned | 36 | 7.1 | Solar | 100.00% | |||

| Total | 4,743 | 2,170 |

Note: The physical guarantee of Boa Esperança and Jusante is the value certified by a certifying company. It has not been approved by Aneel. For the plants of Cemig Sim, the estimated generation was considered to be the physical guarantee.

There are more details of Cemig Sim's expansion projects on the following page.

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 39 |

| |

Expansion of solar generation

| Project | Company | Installed capacity (MWac) | Capacity (MWp) | Expected generation (MWaverage) |

Planned operational start date |

| Ouro Solar Project | Cemig Sim | 40.5 | 57.5 | 11.4 | Aug. 2025 – Apr. 2026 |

| Bloco Azul project | Cemig Sim | 23.0 | 32.6 | 12.0 | Apr 26 |

| Solar do Cerrado Project | Cemig Sim | 50.0 | 70.0 | 13.1 | Dec. 2025 – May 2026 |

| Total | 113.5 | 160.1 | 36.5 |

RAP: July 2024–June 2025 cycle

The RAP (Permitted Annual Revenue – Receita Annual Permitida) of Cemig GT, including the Adjustment Component, received an increase of 18.8% as from July, reflecting: (i) inflation in the period; (ii) strengthening and enhancements of the network; and (iii) flow from reprofiling of the ‘RBSE’ National Grid component.

| ANEEL RATIFYING RESOLUTION (ReH) 3348/2024 (2024–2025 cycle) | ||||

| R$ ’000 | RAP | Adjustment component | Total | Expiration |

| Cemig | 1,243,011 | 115,284 | 1,358,295 | |

| Cemig GT | 1,161,990 | 117,855 | 1,279,845 | Dec. 2042 |

| Cemig Itajubá | 43,096 | –1,524 | 41,572 | Oct. 2030 |

| Centroeste | 26,008 | –1,284 | 24,724 | Mar. 2035 |

| Sete Lagoas | 11,917 | 237 | 12,154 | Jun. 2041 |

| Taesa (Cemig stake: 21.68%) | 625,278 | –32,793 | 592,485 | |

| TOTAL RAP | 1,950,780 | |||

| REIMBURSEMENT FOR NATIONAL GRID ASSETS** | |||||||

|

R$ ’000 – by cycle |

2020–2021 | 2021–2022 | 2022–2023 | 2023–2024 |

2024–2025 (1) |

From 2025–2026, to 2027–2028 |

From 2028–2029, to 2032–2033 |

| Economic | 144,547 | 144,547 | 144,547 | 144,375 | 21,662 | 83,019 | 26,039 |

| Financial | 332,489 | 88,662 | 129,953 | 275,556 | 275,556 | 275,556 | – |

| TOTAL | 477,036 | 233,209 | 274,500 | 419,931 | 297,218 | 358,575 | 26,039 |

* The figures for indemnity of RBSE National Grid components are included in the RAP of Cemig (first table).

1) 2024–2025 includes the Adjustment Component for postponement of the 2023 Review.

Cemig currently has state environmental (REA) approval for additional large-scale works of strengthening and enhancement, for total capex of R$ 1,238 million, and investments of R$ 220 million related to Lot 1 of Auction 02/2022 (with completion planned for 2028). Note: The amounts stated for 2024 include investments that were made, but not in Ratifying Resolution 3348/2024, which approved the RAP for July 2024–June 2025.

| Planned operational startup date | Capex (R$ ’000) | RAP (R$ ’000) |

| 2024 | 232,197 | 35,176 |

| 2025 | 307,845 | 49,239 |

| 2026 | 259,678 | 41,480 |

| 2027 | 414,707 | 68,840 |

| 2028 | 243,910 | 22,396 |

| Total | 1,458,337 | 217,131 |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 40 |

| |

Regulatory transmission revenue

| Regulatory Transmission revenue – 4Q24 | |||

| R$ ’000 | GT | Centroeste | Sete Lagoas |

| REVENUE | 433.482 | 6.219 | 2.777 |

| Transmission operations revenue | 433.482 | 6.219 | 2.777 |

| Taxes on revenue | -39.663 | -228 | -257 |

| PIS and Pasep taxes | -7.075 | -41 | -46 |

| Cofins tax | -32.588 | -187 | -211 |

| ISS tax | - | - | - |

| Sector charges | -74.541 | -235 | -120 |

| Research and Development (R&D) | -3.120 | -57 | -24 |

| Global Reversion Reserve (RGR) | - | -155 | -84 |

| Energy Development Account (CDE) | -56.706 | - | - |

| Electricity Services Inspection Charge (TFSEE) | -1.321 | -23 | -12 |

| Other charges | -13.394 | - | - |

| Net revenue | 319.278 | 5.756 | 2.400 |

Complementary information

Cemig D

| MARKET OF CEMIG D (GWh) | ||||

| QUARTER | CAPTIVE | TUSD – ENERGY (1) | E.T.D (2) | TUSD – DEMAND (3) |

| 1Q22 | 5,738 | 5,397 | 11,136 | 36.2 |

| 2Q22 | 6,050 | 5,853 | 11,904 | 36.7 |

| 3Q22 | 5,942 | 5,790 | 11,733 | 34.7 |

| 4Q22 | 6,047 | 5,755 | 11,802 | 40.5 |

| 1Q23 | 5,723 | 5,566 | 11,289 | 38.0 |

| 2Q23 | 5,949 | 6,058 | 12,007 | 38.5 |

| 3Q23 | 5,812 | 6,028 | 11,840 | 39.2 |

| 4Q23 | 6,376 | 6,068 | 12,445 | 39.9 |

| 1Q24 | 5,930 | 6,097 | 12,027 | 40.4 |

| 2Q24 | 5,924 | 6,301 | 12,225 | 42.4 |

| 3Q24 | 5,821 | 6,557 | 12,378 | 43.6 |

| 4Q24 | 5,812 | 6,505 | 12,317 | 42.5 |

(1) This refers to the ‘energy’ portion for calculation of the regulatory charges to Free Clients (‘Portion A’).

(2) Total energy distributed

(3) Sum of TUSD billed, according to demand contracted (‘Portion B’).

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 41 |

| |

| Cemig D | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| Operating Revenues (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Revenue from supply of energy | 6,964 | 6,021 | 6,241 | 15.7% | 11.6% |

| Reimbursement of PIS/Pasep and Cofins credits to customers | 0 | 0 | 339 | - | - |

| Revenue from Use of Distribution Systems (the TUSD charge) | 1,386 | 1,344 | 1,200 | 3.1% | 15.4% |

| CVA and Other financial components in tariff adjustment | 47 | 357 | -149 | - | - |

| Construction revenue | 1,290 | 1,151 | 1,053 | 12.1% | 22.5% |

| Adjustment to expectation of cash flow from indemnifiable financial assets of distribution concession (VNR) | 35 | 16 | 22 | 117.2% | 57.4% |

| Others | 667 | 609 | 505 | 9.6% | 32.1% |

| Subtotal | 10,389 | 9,498 | 9,212 | 9.38% | 12.8% |

| Deductions | -2,827 | -2,740 | -2,784 | 3.2% | 1.5% |

| Net Revenues | 7,562 | 6,758 | 6,427 | 11.9% | 17.6% |

| 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % | |

| Cemig D - Expenses | 4Q/3Q | 4Q/4Q | |||

| Personnel | 256 | 223 | 229 | 14.7% | 11.8% |

| Employees' and managers' profit sharing | 21 | 24 | 24 | -11.2% | -10.8% |

| Forluz – Post-retirement obligations | 81 | 81 | 109 | 0.2% | -25.2% |

| Materials | 28 | 26 | 43 | 6.5% | -35.4% |

| Outsourced services | 508 | 409 | 446 | 24.1% | 13.9% |

| Amortization | 252 | 231 | 237 | 8.9% | 5.9% |

| Operating provisions | 162 | 22 | 173 | 636.1% | -6.4% |

| Charges for Use of Basic Transmission Network | 762 | 869 | 796 | -12.3% | -4.3% |

| Energy purchased for resale | 3,356 | 3,078 | 2,598 | 9.0% | 29.2% |

| Construction Cost | 1,290 | 1,151 | 1,053 | 12.1% | 22.5% |

| Other Expenses | 141 | 101 | 153 | 39.3% | -8.3% |

| Total | 6,855 | 6,215 | 5,860 | 10.3% | 17.0% |

| Cemig D | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| Statement of Results (R$ mn) | 4Q/3Q | 4Q/4Q | |||

| Net Revenue | 7,562 | 6,758 | 6,427 | 11.9% | 17.6% |

| Operating Expenses | 6,855 | 6,215 | 5,860 | 10.3% | 17.0% |

| Operational profit | 706 | 543 | 567 | 30.1% | 24.5% |

| EBITDA | 958 | 774 | 805 | 23.7% | 19.0% |

| Financial Result | -138 | -75 | -73 | 83.9% | 89.1% |

| Provision for Income Taxes, Social Cont & Deferred Income Tax | -117 | -96 | -94 | 21.5% | 24.5% |

| Net Income | 452 | 372 | 401 | 21.4% | 12.8% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 42 |

| |

Cemig GT

| Cemig GT - Operating Revenues | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Sales to end consumers | 848 | 899 | 912 | -5.7% | -7.1% |

| Supply | 542 | 501 | 641 | 8.3% | -15.4% |

| Revenues from Trans. Network | 129 | 198 | 186 | -34.8% | -30.5% |

| Construction revenue | 144 | 118 | 84 | 22.4% | 72.1% |

| Financial remuneration of transmission contractual assets | 198 | 111 | 121 | 78.7% | 64.4% |

| Gain on monetary updating of Concession Grant Fee | 118 | 94 | 97 | 25.3% | 21.4% |

| Transactions in the CCEE | 10 | -2 | 37 | -599.3% | -73.0% |

| Generation indemnity revenue | 23 | 21 | 23 | 10.6% | 2.0% |

| Others | 62 | 31 | 45 | 101.1% | 38.5% |

| Subtotal | 2,075 | 1,971 | 2,146 | 5.3% | -3.3% |

| Deductions | -380 | -378 | -394 | 0.4% | -3.7% |

| Net Revenues | 1,696 | 1,593 | 1,752 | 6.5% | -3.2% |

| Cemig GT - Operating Expenses | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Personnel | 73 | 78 | 87 | -6.5% | -16.0% |

| Employees' and managers' profit sharing | 9 | 9 | 9 | -0.1% | 1.5% |

| Forluz – Post-retirement obligations | 25 | 25 | 34 | 0.9% | -24.9% |

| Materials | 8 | 7 | 7 | 9.7% | 4.1% |

| Outsourced services | 72 | 63 | 47 | 14.5% | 52.1% |

| Depreciation and Amortization | 82 | 84 | 87 | -2.0% | -5.0% |

| Operating provisions | 35 | 9 | 18 | 288.9% | 94.4% |

| Charges for Use of Basic Transmission Network | 71 | 73 | 67 | -2.4% | 5.7% |

| Energy purchased for resale | 642 | 587 | 549 | 9.3% | 16.8% |

| Construction Cost | 116 | 74 | 63 | 56.8% | 84.6% |

| Impairment | 17 | 2 | 0 | 754.4% | - |

| Reversal of provision with related party | 0 | -58 | 0 | - | - |

| Other Expenses | 17 | 33 | 20 | -48.0% | -13.6% |

| Total | 1,167 | 986 | 988 | 18.4% | 18.1% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 43 |

| |

| Cemig GT - Statement of Results | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Net Revenue | 1,696 | 1,593 | 1,752 | 6.5% | -3.2% |

| Operating Expenses | 1,167 | -2,152 | 700 | -154.2% | 66.7% |

| Operational profit | 529 | 3,745 | 1,052 | -85.9% | -49.8% |

| Equity gain in subsidiaries | -83 | -30 | 34 | 176.7% | -344.4% |

| EBITDA | 528 | 3,798 | 1,173 | -86.1% | -55.0% |

| Financial Result | -222 | 37 | -9 | - | - |

| Provision for Income Taxes, Social Cont & Deferred Income Tax | 18 | -1,121 | -233 | - | -107.6% |

| Net Income | 242 | 2,630 | 844 | -90.8% | -71.4% |

Cemig, Consolidated

| Energy Sales | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (in GWh) | 4Q/3Q | 4Q/4Q | |||

| Residential | 3,760 | 3,450 | 3,696 | 9.0% | 1.7% |

| Industrial | 4,597 | 4,581 | 4,643 | 0.3% | -1.0% |

| Commercial | 2,809 | 2,848 | 3,046 | -1.4% | -7.8% |

| Rural | 783 | 1,117 | 982 | -29.9% | -20.2% |

| Others | 705 | 709 | 808 | -0.6% | -12.7% |

| Subtotal | 12,654 | 12,705 | 13,174 | -0.4% | -3.9% |

| Own Consumption | 8 | 7 | 8 | 14.3% | 0.0% |

| Supply | 4,763 | 4,200 | 4,742 | 13.4% | 0.4% |

| TOTAL | 17,425 | 16,912 | 17,924 | 3.0% | -2.8% |

| Revenue from supply of electricity | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Residential | 3,654 | 3,124 | 3,169 | 17.0% | 15.3% |

| Industrial | 1,373 | 1,379 | 1,470 | -0.5% | -6.6% |

| Commercial | 1,752 | 1,577 | 1,706 | 11.1% | 2.7% |

| Rural | 660 | 735 | 642 | -10.2% | 2.8% |

| Others | 587 | 544 | 586 | 7.9% | 0.2% |

| Subtotal | 8,026 | 7,359 | 7,574 | 9.1% | 6.0% |

| Unbilled supply | 225 | -46 | 109 | -588.1% | 106.3% |

| Supply | 1,371 | 1,243 | 1,235 | 10.3% | 11.0% |

| TOTAL | 9,621 | 8,556 | 8,918 | 12.5% | 7.9% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 44 |

| |

| Operating Revenues - consolidated | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Sales to end consumers | 8,250 | 7,313 | 7,683 | 12.8% | 7.4% |

| Supply | 1,371 | 1,243 | 1,235 | 10.3% | 11.0% |

| TUSD | 1,375 | 1,338 | 1,193 | 2.8% | 15.3% |

| CVA and Other financial components in tariff adjustment | 47 | 357 | -149 | -86.9% | - |

| Reimbursement of PIS/Pasep and Cofins over ICMS credits to customers | 0 | 0 | 339 | - | - |

| Transmission revenue plus RTP | -20 | 145 | 93 | -113.8% | -121.5% |

| Financial remuneration of transmission contractual assets | 219 | 40 | 123 | 448.7% | 77.9% |

| Transactions in the CCEE | 10 | 27 | 66 | -62.7% | -84.7% |

| Gas supply | 988 | 1,038 | 953 | -4.8% | 3.7% |

| Construction revenue | 1,547 | 1,375 | 1,235 | 12.5% | 25.3% |

| Others | 974 | 764 | 730 | 27.5% | 33.5% |

| Subtotal | 14,763 | 13,640 | 13,501 | 8.2% | 9.3% |

| Deductions | -3,586 | -3,491 | -3,544 | 2.7% | 1.2% |

| Net Revenues | 11,177 | 10,149 | 9,957 | 10.1% | 12.3% |

| Operating Expenses - consolidated | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| Personnel | 332 | 326 | 349 | 2.0% | -4.6% |

| Employees’ and managers’ profit sharing | 49 | 41 | 39 | 19.3% | 26.2% |

| Forluz – Post-Retirement Employee Benefits | 122 | 122 | 161 | - | -24.5% |

| Materials | 37 | 35 | 51 | 5.5% | -28.0% |

| Outsourced services | 618 | 497 | 511 | 24.4% | 20.9% |

| Energy purchased for resale | 4,923 | 4,567 | 3,957 | 7.8% | 24.4% |

| Charges for use of the national grid | 692 | 805 | 762 | -14.1% | -9.3% |

| Gas bought for resale | 564 | 544 | 523 | 3.6% | 7.9% |

| Depreciation and Amortization | 364 | 346 | 351 | 5.2% | 3.6% |

| Operating Provisions | 187 | 94 | 88 | 98.9% | 112.5% |

| Construction costs | 1,518 | 1,336 | 1,211 | 13.7% | 25.4% |

| Expected credit losses of accounts receivable | 72 | -51 | 102 | - | -29.4% |

| Other Expenses | 182 | 88 | 186 | 106.3% | -2.4% |

| Total | 9,660 | 8,750 | 8,292 | 10.39% | 16.50% |

COMPANHIA ENERGÉTICA DE MINAS GERAIS S.A. | 45 |

| |

| Financial Result Breakdown | 4Q24 | 3Q24 | 4Q23 | chg. % | chg. % |

| (R$ million) | 4Q/3Q | 4Q/4Q | |||

| FINANCE INCOME | |||||

| Income from cash investments | 148 | 105 | 128 | 41.4% | 16.4% |

| Arrears fees on sale of energy | 78 | 72 | 71 | 8.6% | 10.9% |

| Monetary variations | |||||

| Monetary variations – CVA | 12 | 5 | -5 | 138.4% | -336.7% |

| Monetary updating on Court escrow deposits | 18 | 18 | 21 | -1.6% | -13.8% |