Use these links to rapidly review the document

TABLE OF CONTENTS

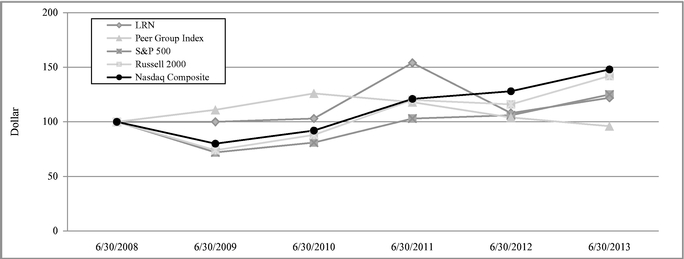

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended June 30, 2013 |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission file number 001-33883

K12 Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

95-4774688 (I.R.S. Employer Identification No.) |

|

2300 Corporate Park Drive Herndon, VA 20171 (Address of principal executive offices) (Zip Code) |

(703) 483-7000 (Registrant's telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, $0.0001 par value | New York Stock Exchange (NYSE) |

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the registrant's voting and non-voting stock held by non-affiliates of the registrant as of December 31, 2012 was approximately $192,429,000. Aggregate market value excludes an aggregate of approximately 27,458,000 shares of common stock held by officers and directors and by each person known by the registrant to own 5% or more of the outstanding common stock on such date. Exclusion of shares held by any of these persons should not be construed to indicate that such person possesses the power, direct or indirect, to direct or cause the direction of the management or policies of the registrant, or that such person is controlled by or under common control with the registrant.

The number of shares of the registrant's common stock outstanding as of August 22, 2013 was 38,033,052.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant's definitive proxy statement for its 2013 annual meeting of stockholders to be filed pursuant to Regulation 14A with the Securities and Exchange Commission not later than 120 days after the registrant's fiscal year ended June 30, 2013, are incorporated by reference into Part III of this Form 10-K.

2

Unless the context requires otherwise, all references in this Annual Report on Form 10-K (the "Annual Report") to "K12," "K12," "Company," "we," "our" and "us" refer to K12 Inc. and its consolidated subsidiaries.

SPECIAL NOTE ON FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 that involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this Annual Report on Form 10-K are forward-looking statements. We have tried, whenever possible, to identify these forward-looking statements using words such as "anticipates," "believes," "estimates," "continues," "likely," "may," "opportunity," "potential," "projects," "will," "expects," "plans," "intends" and similar expressions to identify forward-looking statements, whether in the negative or the affirmative. These statements reflect our current beliefs and are based upon information currently available to us. Accordingly, such forward-looking statements involve known and unknown risks, uncertainties and other factors which could cause our actual results, performance or achievements to differ materially from those expressed in, or implied by, such statements. These risks, uncertainties, factors and contingencies include, but are not limited to:

- •

- the reduction of per pupil funding amounts at the schools we serve;

- •

- failure of the schools we serve or us to comply with regulations resulting in a loss of funding or an obligation to repay

funds previously received;

- •

- reputation harm resulting from poor performance or misconduct by operators or us in any school in our industry and in any

school in which we operate;

- •

- legal and regulatory challenges from opponents of virtual public education or for-profit education companies;

- •

- discrepancies in interpretation of legislation by regulatory agencies that may lead to payment or funding disputes;

- •

- termination of our contracts with schools due to a loss of authorizing charter;

- •

- failure to enter into new contracts or renew existing contracts with schools;

- •

- risks associated with entering into and successfully integrating mergers, acquisitions and joint ventures;

- •

- our potential inability to further develop, maintain and enhance our technology, products, services and brands;

- •

- inability to recruit, train and retain quality teachers and employees;

- •

- infringement of our intellectual property;

- •

- failure to adhere to laws and regulations related to operating schools in a foreign jurisdiction;

- •

- variations in academic performance results as curriculum and testing standards evolve; and

- •

- new market entrants and competitive technologies.

Forward-looking statements reflect our management's expectations or predictions of future conditions, events or results based on various assumptions and management's estimates of trends and economic factors in the markets in which we are active, as well as our business plans. They are not guarantees of future performance. By their nature, forward-looking statements are subject to risks and uncertainties. Our actual results and financial conditions may differ, possibly materially, from the

3

anticipated results and financial conditions indicated in these forward-looking statements. There are a number of factors that could cause actual conditions, events or results to differ materially from those described in the forward-looking statements contained in this Annual Report. A discussion of factors that could cause actual conditions, events or results to differ materially from those expressed in any forward-looking statements appears in "Part 1-Item 1A-Risk Factors."

Readers are cautioned not to place undue reliance on forward-looking statements in this Annual Report or that we make from time to time, and to consider carefully the factors discussed in "Part 1-Item 1A-Risk Factors" of this Annual Report in evaluating these forward-looking statements. These forward-looking statements are representative only as of the date they are made, and we undertake no obligation to update any forward-looking statement as a result of new information, future events or otherwise.

4

Company Overview

We are a technology-based education company. We offer proprietary curriculum, software systems and educational services designed to facilitate individualized learning for students primarily in kindergarten through 12th grade, or K-12. Our mission is to maximize a child's potential by providing access to an engaging and effective education, regardless of geographic location or socio-economic background. Since our inception, we have invested more than $350 million to develop and, to a lesser extent, acquire curriculum and online learning platforms that promote mastery of core concepts and skills for students of all abilities. K12 provides a continuum of technology-based educational products and solutions to public school districts, public schools, public charter schools private schools and families as we strive to transform the educational experience into one that delivers individualized education on a highly scalable basis. In 2013, AdvancED renewed its quality assurance accreditation of the Company.

As an innovator in K-12 online education, we believe we have attained distinctive core competencies that allow us to meet the varied needs of our customers and students. These core competencies include our ability to create engaging curriculum, train teachers to be effective in online instruction, provide turn-key management services to online schools, customize online learning programs for school districts, develop innovative new offerings (such as our Flex schools and National Math Lab) and assist legislators and policy makers in understanding the many benefits of online learning to complement and transform traditional schools. These strengths enable us to provide a unique set of products and services primarily to three lines of business that share many common attributes, including, curriculum, learning systems, management expertise, logistical systems and marketing. These businesses are: Managed Public Schools (turn-key management services sold to public schools), Institutional Sales (educational products and services sold to school districts, public schools and other educational institutions that we do not manage), and International and Private Pay Schools (private schools for which we charge student tuition and make direct consumer sales).

Managed Public Schools

|

Institutional Sales | International and Private Pay Schools | ||

|---|---|---|---|---|

• Full-time virtual schools |

• K12 curriculum |

• Managed private schools |

||

• Blended schools |

• Aventa curriculum |

—The Keystone School | ||

—Flex schools |

• A+ curriculum |

—George Washington University Online HS | ||

—Passport schools |

• Middlebury joint venture |

—K12 International Academy | ||

—Discovery schools |

• Pre-kindergarten |

—IS Berne | ||

—Other blended schools |

• Post-secondary |

• Independent course sales (Consumer) |

- •

- Managed Public Schools

Virtual Public Schools. The majority of our revenue is derived from long-term service agreements with the governing authorities of the virtual public schools that we serve. In addition to providing our course catalog, course materials and, in certain cases, student computers, we also offer these schools a variety of management, technology and academic support services. In full-time virtual managed schools, students receive online lessons over the Internet and utilize offline learning materials that we supply. The full-time virtual schools we manage are generally associated with different curricula and orientations. K12 managed schools (often named virtual academies) serve K-8 or K-8 and high school students, principally utilize K12 curriculum, and attract both mainstream and academically at-risk students. In addition to these virtual academies, we manage Insight schools, which serve middle school and high school students, typically utilize the Aventa curriculum and tend to focus on academically at-risk students. iQ Academies serve middle school and high school students, primarily utilize the Aventa curriculum, and are generally only

5

- •

- Institutional

Sales. We work closely as partners with a growing number of districts and schools, enabling them to offer their students

an array of online education solutions, including full-time virtual and blended programs, semester courses and supplemental solutions. In addition to curriculum, systems and programs, we also provide

teacher training, teaching services and other support services. These institutions include public schools, school districts, private schools, public charter schools and early childhood learning

centers. Additionally, we operate a joint venture with Middlebury College, known as Middlebury Interactive Languages LLC ("MIL"), to develop and market online foreign language

courses. For the 2012-13 school year, we served school districts or individual schools in all 50 states and the District of Columbia, including those where the regulatory environment restricts or

prohibits state-wide online programs.

- •

- International and Private Pay Schools. We operate three online private schools: The Keystone School, the K12 International Academy and the George Washington University Online High School. We also manage a foreign brick and mortar private school (International School of Berne) and have entered into agreements which enable us to distribute our products and services to over 1,000 school partners throughout the world. We serve students from more than 100 countries around the world. We also are pursuing international opportunities where we believe there is significant demand for a quality online education; our principal customers are expatriate families and foreign students who wish to study in English. Additionally, our curriculum is sold to end user customers who desire to educate their children outside of the traditional school system or to supplement their child's traditional education.

partially managed by K12—typically, the academic program and regulatory compliance for iQ Academies are managed by their host school or school district.

Blended Public Schools. In addition to providing services to full-time virtual programs, we also sell our products and services to blended schools (sometimes referred to as hybrid schools), which are public schools that combine online and face-to-face instruction in many different arrangements with varying amounts of time spent in a physical learning center.

For both virtual and blended managed schools, we generally take responsibility (subject to governing authority oversight) for all aspects of the management of the schools, including monitoring academic achievement, teacher recruitment and training, compensation recommendations for school personnel, financial management, enrollment processing and procurement of curriculum, equipment and other required services. The scope of services we provide varies in accordance with applicable state regulations and each governing authority's policies. Funding is provided primarily by state governments. For the 2013-14 school year, we will provide turn-key management services to Managed Public Schools in 33 states and the District of Columbia.

Given our rapid growth over the past several years, it has been necessary to make significant capital investments in our infrastructure, including a company-wide enterprise resource planning ("ERP") system, a second data center, and an upgrade to our customer relationship management ("CRM") system. As we leverage our core competencies and integrate our acquisitions, we believe we are well positioned to drive and manage the growth we have experienced since our first year as a public company when we achieved revenues of $141 million for the fiscal year ended June 30, 2007. Since fiscal year 2010, our revenues have increased from $384 million to $848 million representing growth of 121% over four years.

6

Our Market

The U.S. market for K-12 education is large and online learning is gaining greater acceptance. For example:

- •

- According to the National Center for Education Statistics ("NCES"), a division of the U.S. Department of Education,

approximately 49.8 million students were expected to attend K-12 public schools in the Fall of 2012, and more than 5 million students were expected to enroll in private schools.

In addition, according to a 2011 report by National Home Education Research Institute, approximately two million students were home schooled. Many of these students will take an online course and a

small percentage will enroll in a full-time online program.

- •

- According to the NCES, the public school system alone encompassed more than 98,800 schools and approximately 13,600

districts during the 2010-11 school year.

- •

- The NCES estimates that total spending in the K-12 market was $686 billion for the 2011-12 school year.

- •

- According to the International Association for K-12 Online Learning ("iNACOL"), in 2012, 48 states had established a significant form of online learning initiative. In addition, according to Ambient Insight, an international market research firm, in 2011, 1.68 million K-12 students participated in a formal online learning program.

Many parents and educators are seeking alternatives to traditional classroom-based education for a variety of reasons. Demand for these alternatives is evident in the expanding number of choices available to parents and students. For example, public charter schools emerged in 1988 to provide an alternative to traditional public schools and, according to the Center for Education Reform, have grown by 245% since 2001. As of 2012, there were over 5,700 public charter schools operating in 40 states and the District of Columbia with an estimated enrollment of over 1.9 million students. Similarly, acceptance of online learning initiatives, including not only virtual and blended public schools, but also online courses, credit recovery, remediation, testing and Internet-based professional development, has continued to grow. Districts are also rapidly adopting online learning to expand course offerings, provide schedule flexibility, increase graduation rates and lower the cost to deliver education.

Demand for Education Alternatives: The Market Opportunity and the K12 Solutions

As evidenced by the varying options being utilized by K-12 students, no single educational model works equally well for all students. Children today utilize technology in all aspects of their lives and we expect them to extend their use of technology to their educational needs and choices. Our business is modeled on the premise that every student has the right to an education that is individualized and available anywhere at any time. We also believe all students can benefit from more rigorous and engaging content.

We believe that full-time virtual schools will meet the needs of a small percentage of the overall K-12 student population, but do represent and will continue to represent a large and growing opportunity in absolute terms. Across our educational programs, families come from a broad range of social, economic and academic backgrounds. They share the desire for individualized instruction to maximize their children's potential. Examples of students for whom this solution fits include, but are not limited to, families with: (i) students seeking to learn at their own pace; (ii) students with safety, social and health concerns about their local school; (iii) students with disabilities who are underserved in traditional classrooms; (iv) students for whom the local public school is not meeting their needs; (v) students who need flexibility, such as student-athletes and performers who are not able to attend regularly-scheduled classes; (vi) college-bound students seeking to bolster their college readiness and application appeal by taking additional Advanced Placement, honors and/or elective courses; (vii) high

7

school dropouts; (viii) students of military families who desire high quality, consistent education across moves; and (ix) students for whom their current school option is otherwise not working. Our individualized learning approach allows students to optimize their educational experience and, therefore, their chances of achieving their goals. The schools we manage, both public and private, which generated the majority of our revenue (approximately 86% in fiscal 2013), serve this demand.

We believe that the majority of students in the United States will continue to be educated in school buildings, although we further believe that the academic benefits for many students and the significant savings for taxpayers will continue to drive states and districts to incorporate online solutions into their school-based programs. One of the challenges the traditional schools continue to face is adoption of technology and innovative new learning modalities. In our Institutional Sales, we offer a complete solution for districts and schools that need a turn-key option and also offer online curriculum and services on a solutions-oriented, individualized basis for those customers who need less than a full-service offering. We believe this range of options creates the opportunity for us to serve the majority of students who will learn within school buildings. Therefore, we have invested significant resources, organically and through acquisitions, in developing product offerings that afford us the flexibility to serve different types of customers with varying value propositions and price points that are adaptable to an institution's capabilities and needs. We have and will continue to pursue selected markets outside the United States where we believe our curricula can address local market needs.

We believe that our core competencies, coupled with the significant investments we have made in our infrastructure and our strategic acquisitions and partnerships, position us to offer educational resources for all types of students. Regardless of whether a student chooses to remain in a classroom or seeks an alternative setting, attends public or private school, lives in the United States or abroad, wants to take online classes on a full or part-time basis or is an advanced or remedial student, our products and services offer students expanded educational opportunities.

Our Business Lines

Managed Public Schools

Virtual Public Schools

The majority of our revenue is derived from long-term service agreements with the governing authorities of the virtual public schools we serve. In addition to a comprehensive course catalog, related books and physical materials and, in certain cases, student computers, we also offer these schools a variety of management, technology and academic support services. In full-time virtual managed schools, students receive online lessons over the Internet and utilize offline learning materials we provide. Students receive assignments, complete lessons, and obtain instruction from certified teachers with whom they interact online, telephonically, in virtual classroom environments, and sometimes face-to-face. For parents who believe their child is not thriving in their current public school or for students and families who require time or location flexibility in their schooling, virtual and blended public schools can provide a compelling choice.

Students are also provided the opportunity to participate in a wide variety of school activities, including outings and clubs. In addition to school-level activities, we sponsor a wide variety of extracurricular activities on a national basis, such as clubs, contests and college and career planning sessions.

The full-time virtual schools we serve are generally associated with different curricula and orientations. K12 managed schools (often named virtual academies) serve K-8 or K-8 and high school students, principally utilize the K12 curriculum and attract both mainstream and academically at-risk students. In addition to these virtual academies, we manage Insight schools, which serve middle school and high school students, typically utilize the Aventa curriculum, and tend to attract mostly

8

academically at-risk students. iQ Academies serve middle school and high school students, primarily utilize the Aventa curriculum, and are generally only partially managed by K12—typically, the academic program and regulatory compliance for iQ Academies are managed by their host school or school district.

Blended Public Schools

In addition to our full-time virtual programs, we also manage and sell our products and services to blended schools (sometimes called hybrid schools), which are public schools that combine online and face-to-face instruction for students in many different arrangements. For the 2013-14 school year, we expect to manage blended schools in California, Hawaii, Illinois, Indiana and New Jersey.

In contrast to a typical brick and mortar public school, blended schools can provide a greater selection of available courses, increased opportunities for self-paced, individualized instruction and greater scheduling flexibility. We manage four types of blended schools, which bring students and teachers physically together more often than a purely online program. In the hybrid schools we manage, students attend a learning center on a part-time basis, where they receive direct instruction.

Additionally, our Flex model is a unique blended school model, where middle and high school students attend a learning center five days a week and access and engage in their individualized online lessons in an open study lab while receiving face-to-face direct instruction in areas of particular need. Flex schools leverage many of the capabilities of a virtual school with the advantages of a physical school environment.

Another type of blended school option is the Passport program which utilizes a similar basic instructional model as a Flex school but is especially designed for academically at-risk students, particularly those who have previously dropped out of high school, and therefore includes more counseling and support services. Due to the reality that many Passport students have work and/or child care responsibilities, most students spend half of each day on-site and complete the remainder of their work online.

We have also piloted select grades and subjects of our curriculum in traditional brick and mortar classrooms in many states through our Discovery programs. These programs utilize an interactive whiteboard with our curriculum and emphasize our math and science courses. For these schools, we also provide intensive professional development for the school's teachers and work closely with the school's principal.

For the 2013-14 school year, we will provide turn-key management services to Managed Public Schools in 33 states and the District of Columbia. For most of these schools, we take responsibility for all aspects of the management of the schools, including monitoring academic achievement, teacher recruitment and training, compensation of school personnel, financial management, enrollment processing and procurement of curriculum, equipment and other required services. Managed Public Schools accounted for approximately 86% of our revenue in fiscal year 2013.

Institutional Sales

Public schools and school districts are increasingly adopting online solutions to cost-effectively expand course offerings, provide schedule flexibility, improve student engagement, increase graduation rates, replace textbooks and retain students. To address these growing needs, we provide curriculum and technology solutions, packaged in a portfolio of flexible learning and delivery models mapped to specific student and/or district needs. This portfolio provides a continuum of delivery models, from full and part-time virtual, to blended learning and other options that can be used in traditional classrooms to differentiate instruction. Our catalog contains solutions to address specific student needs, including Advanced Placement, honors, world languages, remediation, credit recovery, alternative education,

9

career and technology electives and college readiness. In connection with these solutions, we also offer highly qualified state-certified teachers, professional development and other support services as needed by our customers.

In addition to providing a vast array of online learning solutions, we recently launched a system called Personalize, Engage and Achieve with K12 ("PEAK12"), designed to centrally manage multiple online solutions across a school or district through one application. PEAK12 enables teachers and administrators to personalize online learning solutions for their students by leveraging all curricula across all supported solutions. PEAK12 currently supports the majority of the K12 curriculum portfolio and will eventually support not only all K12 content, but also other third-party solutions, open educational resources and district and teacher-created content. For students, teachers and administrators, PEAK12 eliminates the complexity of managing multiple accounts and roles and will provide a consistent online environment for full-time, credit recovery, world languages classes or blended classroom programs. We believe increasing ease-of-use for administrators and teachers is a critical factor in improving student support and therefore, improving student outcomes. PEAK12 addresses this need by serving all of the online instructional needs of a school or district in an integrated, data-driven manner.

We have continued to expand our direct and indirect sales network and have provided nearly all sales representatives the ability to sell all solutions in the K12 portfolio, including the original K12 solutions as well as the Aventa, A+ and MIL product lines. We have also expanded our customer services team to support our growing relationships and employ teachers across the United States to serve students and train school administrators and teachers.

For the 2012-13 school year, we served school districts or individual schools in all 50 states and the District of Columbia, including those where the legal framework restricts or prohibits state-wide online programs. Based upon school districts' and academic administrators' growing acceptance of online learning and desire for cost efficient, integrated and flexible educational solutions, we believe that the direct-to-district distribution channel offers further significant growth potential.

We provide online services to post-secondary institutions through our Capital Education subsidiary, which offers programs designed for colleges and universities seeking to broaden their reach and build or expand their online offerings. Services include course development and distribution through a proprietary learning management platform, hosting and technical support, student advisory services, marketing and recruitment and program administration. We currently provide services for multiple programs at ten colleges and universities in the United States and will continue to add programs for existing customers and add new customers over the coming years.

International and Private Pay Schools

We operate a variety of private schools that meet the needs of students ranging from simple correspondence courses to challenging college preparatory programs. We also sell individual online courses directly to families. Beyond our business in the United States, we are pursuing international opportunities where we believe there is significant demand for a quality online education. Our international customers are typically expatriate families and foreign students who desire a U.S. diploma and wish to study in English. We maintain a regional presence in Switzerland and Dubai. During fiscal year 2013, we served in excess of 30,000 students in more than 100 countries. In addition, we have entered into agreements which enable us to distribute our products and services to over 1,000 school partners in foreign countries. These institutions use our courses to provide broad elective offerings and dual diploma programs.

We operate the K12 International Academy, an online private school that serves students in both the United States and overseas. Through the K12 International Academy, students may study in an academic program that ultimately leads to an accredited U.S. high school diploma. Students may also

10

enroll in individual courses on a part-time basis. The K12 International Academy utilizes the same curriculum, systems and teaching practices that we provide to the virtual public schools we manage in the United States. In addition, this school provides a unique international community including clubs and events that enrich the student experience by allowing students to interact with peers in other countries. The school is accredited by the Southern Association of Colleges and Schools and AdvancED, and is recognized by the Commonwealth of Virginia as a degree granting institution of secondary learning.

The Keystone School ("Keystone") is a private school that has been an innovator in home education and distance learning for over 35 years. Students attend The Keystone School for middle and high school on a full or part-time basis. Keystone serves students through online courses with teacher support as well as print correspondence course programs. Keystone uses our Aventa curriculum and provides a lower-cost option to families than either of our other two private schools. The Keystone School is accredited by the Northwest Association of Accredited Schools.

The George Washington University Online High School is operated in cooperation with the George Washington University. The program, which launched in 2011-12 school year, offers K12's college preparatory curriculum and is designed for high school students who are seeking a challenging academic experience and aspire to attend top colleges and universities. The school also provides extensive counseling throughout the high school years to help students make academic and extracurricular choices and maximize their future potential.

In April 2011, we acquired the operations of the International School of Berne ("IS Berne"), a traditional school located in Berne, Switzerland, one of the 200 International Baccalaureate ("IB") "World Schools," that provide the full IB curriculum in grades Pre-K through 12. IS Berne has been operating for more than 50 years and had an 78% pass rate on the International Baccalaureate diploma exam among its high school seniors during the 2012-13 school year.

Consumer Sales

Our curriculum is sold directly to customers who desire to educate their children outside of the traditional school system or to supplement their child's existing public school education without the aid of an online teacher. Customers of our consumer product have the option of purchasing a complete grade-level curriculum or individual subjects depending on their child's needs. Typical applications include summer school course work, home schooling and educational supplements.

Our Growth Strategy

Our growth strategy consists of leveraging the investments we have already made in our curriculum and learning systems, as well as the expertise we have developed in online learning and school management, to serve adjacent markets and to diversify our risk profile. This strategy is aligned with the way the education industry is expected to evolve and consists of the following components:

Increase Enrollments at Existing Virtual and Blended Public Schools through Greater Penetration and Removal of Enrollment Restrictions. In the 2013-14 school year, we will manage virtual and blended public schools in 33 states and the District of Columbia. While we plan to increase enrollments at these schools, in a number of states regulations limit or cap student enrollment or enrollment growth. We intend to work with schools, legislators, state departments of education, educators and parents to find solutions that will remove enrollment restrictions and allow access for every child who is interested in attending a virtual or blended public school.

Expand Virtual and Blended Public School Presence into Additional States and Cities. The flexibility and comprehensiveness of our learning systems allows us to efficiently adapt our curriculum to meet the individual educational standards of any state with minimal capital investment. We will continue to

11

work with states to establish virtual and blended public schools and to contract with them to provide our curriculum, online learning platform, management services, and other related offerings.

Accelerate Institutional Sales. We have increased our distribution capacity to schools and school districts by hiring additional sales representatives, acquiring a sales team through our acquisition of KC Distance Learning ("KCDL") and acquiring distributor relationships through our acquisition of The American Education Corporation ("AEC"). We have combined these resources to increase sales to our Institutional Sales customers.

Add Enrollments in Our Private Schools. We currently operate three online private schools that we believe appeal to a broad range of students and families. We look to drive increased enrollments in these schools by increasing awareness, through targeted marketing programs and by solicitation of partnerships with traditional brick and mortar private schools.

Pursue International Opportunities to Offer Our Learning Systems. We believe there is strong worldwide demand for high-quality, online education from U.S. families living abroad and foreign students who seek a U.S.-style of education, and the schools and school systems that serve them in their local market. Our ability to operate virtually is not constrained by the need for a physical classroom or local teachers, which makes our learning systems ideal for use internationally.

Develop Additional Channels through Which to Deliver Our Learning System. We plan to evaluate other delivery channels on a routine basis and to pursue opportunities where we believe there is likely to be significant demand for our offering, such as direct classroom instruction, blended classroom models, supplemental educational offerings and individual products packaged and sold directly to consumers.

Pursue Strategic Partnerships and Acquisitions. As with our joint venture with Middlebury College, we may pursue opportunities with other highly-respected institutions where we can be a valued-added partner or contribute our expertise in curriculum development and educational services to serve more students. We may also pursue selective acquisitions at attractive valuations that complement our existing educational offerings and business capabilities, and that are natural extensions of our core competencies.

Expand Product Line. We intend to continue to expand our product line and offerings, both organically and through strategic acquisitions of product portfolios.

Products and Services

Educational Philosophy

Our focus remains on offering best-in-class solutions for our customers. Our acquisition of several product portfolios during the last few years has allowed us to expand the number and nature of market entry points. As we continue to integrate these portfolios into our content management system, we will augment them so that they embody the relevant aspects of our educational philosophy and guiding principles. We intend to continue to leverage these portfolios across our educational solutions and distribution channels.

The design, development and delivery of our products and services are grounded in the following set of guiding principles:

- •

- Apply "Tried and True" Educational Approaches for Instruction through Technology; Employ Technology Appropriately to Deliver and Enhance Those Approaches. Our learning systems are designed to utilize both "tried and true" methods to drive academic success. "Tried" methodologies are those that have been experientially tested and proven to be effective. "True" methodologies are those based on more recent cognitive research regarding the way in which

12

- •

- Employ Technology Appropriately for Learning. All of our

courses are delivered primarily through an online platform and generally include a significant amount of online content. We employ technology where we feel it is appropriate and can enhance the

learning process, with the offline:online ratio changing appropriately for advancing developmental levels in students. In addition to online content, our curriculum includes a rich mix of course

materials, including engaging textbooks and hands-on materials such as instructional kits, scientific and musical instruments, art supplies and science specimens. Furthermore, our teachers utilize

telephonic contact as well as email and virtual electronic classrooms. We believe our balanced use of technology and more traditional approaches helps to maximize the effectiveness of our learning

systems.

- •

- Base Learning Objectives on "Big Ideas". We use the

expression "big ideas" for the key, subconscious frameworks that serve as the foundation to a student's future understanding of a subject matter. For example, an understanding of waves is fundamental

to a physicist's understanding of quantum mechanics; for that reason, we teach 1st graders the fundamentals of waves in an age-appropriate form. We use "big ideas" in every subject area to

organize the explicit learning objectives for each course we develop.

- •

- Assess Every Objective to Ensure Mastery. Ongoing

assessments are the most effective way to evaluate a student's mastery of a lesson or concept. To facilitate effective assessment, our curriculum states clear objectives for each lesson. Throughout a

course, every student's progress is assessed at a point when each objective is expected to be mastered, providing direction for appropriate pacing. These periodic and well-timed assessments reinforce

learning and promote mastery of a topic before a student moves to the next lesson or course.

- •

- Individualized Learning. We create engaging curriculum

content with the purpose of capturing the student's attention to make learning more interesting and effective. It is our fundamental belief that each student learns in a highly individualized manner.

Our instructional system allows students to learn from a curriculum that caters to their unique learning style and offers a high degree of program flexibility.

- •

- Prioritize Important, Complex Objectives. Our content

experts have developed a clear understanding of those subjects and concepts that are difficult for students, from both historical and cognitive points of view (that is, from both the "tried" and the

"true" perspective described earlier). Greater instructional effort is focused on the most important concepts (the biggest ideas) and on the most challenging concepts and skills (as revealed by

experience and research). We use existing research, feedback from parents and students, and experienced teacher judgments to determine these priorities, and to modify our learning systems to guide the

allocation of each student's time and effort.

- •

- Facilitate Flexibility to Accommodate Variations in Ability. We believe that each student should be challenged appropriately, where "challenge" is both a matter of the difficulty inherent in the subject matter, and also the pace at which the subject matter is presented. Generally, adequate progress for most students is to complete one academic year's curriculum within a nine-month school year. Each individual student may take greater or fewer instructional hours and make more or less effort than the average student to achieve this progress. Our learning systems are designed to facilitate this flexibility in order to ensure that the appropriate amount of time and effort is allocated to each lesson.

individuals learn. "Tried" methodologies employed by K12 must also pass through the "true" litmus test; the two criteria are not antagonistic. This "tried and true" philosophy allows us to benefit from both decades of research about learning and over a century of published analysis of effective methods of teaching.

13

- •

- Ensure Fundamental Content Soundness. Our highly

credentialed subject matter experts ("SMEs") or "Content Specialists" bring their own scholarly and teaching backgrounds to course design and development and are required to maintain relationships

with and awareness of guidelines from nearly 40 national and international subject-area associations.

- •

- Integrate Curriculum, Teachers and Technology to Maximize Student Learning. We believe students learn better not just with great curriculum, but also great teachers and technology that allows them to access the content and teachers in a way that makes learning more engaging and effective.

Academic Performance

Our fundamental goal for every child who enrolls in an online public or private school managed by the Company, or program offered through a school district, is to improve his or her academic performance. The challenge we face, however, is that the 33 states in which we manage public schools each measure academic performance using different methods. Some states set proficiency standards, which measure minimum levels of comprehension by grade level for certain subjects (e.g., typically math and reading) that are discerned through year-end testing. These static proficiency measures are generally used to assess Adequate Yearly Progress ("AYP") under the No Child Left Behind Act ("NCLB"). According to a November 2012 report by the Center for Education Policy, nearly half of the nation's public schools (48%) did not achieve AYP in 2011, with some states exceeding that AYP failure rate and others falling below. Similarly, for the virtual public schools we manage, some achieved AYP proficiency standards while the majority did not.

Recognizing the limitations in the NCLB approach for measuring academic performance, as of August 2013, a total of 39 states and the District of Columbia have obtained NCLB waivers and are using alternative accountability measures, including various "growth models". While these growth models can have different assumptions, methodologies and analytics from state-to-state, their purpose is to determine how much a student learns over the course of a school year, and therefore measure actual learning gains. A student that enrolls two years behind grade level in math, for example, could realize a full year of improvement but still fall below a static proficiency model used with AYP measures.

While recognizing that the virtual public schools we manage in each state are evaluated under each state's respective academic performance framework, we share the view taken by the many states granted AYP waivers that assessing a student's academic performance by his or her learning growth is a more accurate measure of a school's effectiveness. When applied to the statewide virtual public schools we serve, academic success defined by using grade-level, static proficiency tests is even more problematic given high enrollment growth rates, high student mobility and a high percentage of students who enter behind grade level. For these reasons, we measure academic performance in the virtual schools we manage with a growth model that uses a nationally normed computer adaptive test provided by Scantron, an independent provider of web-based K-12 assessments which are taken by virtual school students from their home at the beginning and end of the school year. Nearly 90% of the students enrolled in the managed public schools we served during the 2012-13 school year completed the Scantron tests at the beginning and the end of the school year. As we reported in our 2013 Annual Academic Report, found online at http://www.k12.com/sites/default/files/pdf/2013-K12-Academic-Report-Feb6-2013.pdf, pre and post test data from the Scantron Performance Series adaptive assessment system showed that, in aggregate, students in the managed public schools we serve scored at the national average in math and above the national average for gains in language arts. We also recognize that as state-specific growth models using different assessments emerge in the coming years, the virtual schools we manage in those states will be measured for academic performance against those standards, which may yield different results than the Scantron nationally normed tests.

14

While measuring academic performance is necessary, taking meaningful steps to improve student outcomes is imperative. Accordingly, we continually strive to achieve that objective by undertaking new initiatives and piloting new programs, such as our National Math Lab and our Mark 12 remedial reading program. To monitor student learning progress during the school year, we are adding multiple equivalent assessments at the lesson, unit and semester level to ensure that our measurement of mastery is reliable and valid. We are also piloting a diagnostic assessment tool to be able to develop individualized learning plans for new students who often start school before their academic records are provided to us from their previous school.

Other steps taken in fiscal year 2013 to improve student education include the hiring of a Chief Academic Officer and formation of a new K12 Educational Advisory Committee ("EAC"). The EAC will assist us in focusing on academic achievement and growth goals as well as advising us on specific tactics to be successful in these areas. The members of our EAC are:

- •

- Dr. Andrew Porter, Dean of the Graduate School of Education, University of Pennsylvania

- •

- Dr. Elanna Yalow, CEO of Knowledge Universe Early Learning programs

- •

- Dr. Susan Patrick, CEO of iNACOL

- •

- Dr. Beverly Hutton, Executive Director of the National Association of Secondary School Principals

- •

- Dr. Mary Futrell, Professor (and former Dean of Education), George Washington University

- •

- Dr. David Driscoll, former Commissioner of Education, Commonwealth of Massachusetts

- •

- Dr. Craig Barrett, former CEO and Chairman of the Board of Intel Corporation

- •

- Dr. Richard Wenning, former Deputy Superintendent, Colorado Department of Education

Our Products

Our mission remains to invest in systems and technology to educate students more effectively and efficiently. To date, we have invested more than $350 million in our curriculum and learning systems. It is our expectation that these investments will help states, districts and schools improve the education of their students.

Much of this investment has been in the development of K-12 online courses and management systems. Most recently, we have begun to develop specialized courses and programs designed to remediate the rapidly increasing number of students who are enrolling in schools behind grade level. Specifically, we are creating even more individualized learning programs for students using adaptive learning technology, which requires a significant investment to develop a specialized curriculum and a complex database.

As school districts confront the same issues that we are experiencing in the Managed Public Schools, we believe that our solutions could gain widespread acceptance. During the past few fiscal years, we built a new K-6 math curriculum and a remedial reading course, both based on the latest educational research and pedagogical methods. In addition, our PEAK12 system provides school districts and administrators a better way to manage their online education programs and content.

Just as we pioneered the development of virtual schools, we are resolved to address the most challenging educational needs facing schools and districts. Our goal is to assist teachers, schools and districts in implementing individualized education programs to better serve their students. This can take a variety of forms including turn-key solutions, partnerships, vendor relationships, enterprise licenses, and purchases of curriculum and services.

15

Our investment strategy is not limited, however, to curriculum and systems. We are also making substantial investments in our service offerings to improve student outcomes. For the 2013-14 school year, we are conducting a randomized control trial for two innovative supplemental mathematics programs and we are comparing how students perform compared with our own National Math Lab. This research will examine the differential effects of technology tools compared with effective teacher-led synchronous sessions. Additionally, we continue to invest in improving the quality of our teachers and school leaders through professional development efforts.

Curriculum

K12 has one of the largest digital curriculum portfolio for the K-12 online education industry. The K12 curriculum consists of online lessons, offline instructional kits and materials and lesson guides. We offer an extensive catalog of proprietary courses designed to teach concepts to students from pre-kindergarten through 12th grade, as well as curriculum for use in post-secondary online programs. A single year-long K12 course generally consists of 120 to 180 unique instructional lessons. Each lesson is designed to last approximately 45 to 60 minutes, although students are able to work at their own pace. We have more than 700 courses across kindergarten, elementary, middle and high school, including world languages. This combined portfolio contains over 107,000 hours of instructional content and over one million visual, audio and interactive instructional elements in our asset repository.

Online Lessons. Our K12 online lessons or curricula are accessed through a proprietary learning management platform, which we call our Online School ("OLS") for K-8 students and the eCollege platform for high school students, as well as a number of other common industry platforms for students who access Aventa and A+ curricula. Each online lesson provides the roadmap for the entire lesson, including direction to specific online and offline materials, summaries of major objectives for the lesson and the actual lesson content with assessments. Digital versions of documents, readings, labs and other activities may also be included. Lessons utilize a combination of innovative technologies, including animations, demonstrations, audio, video and other graphic/digital interactivity, educational games and individualized feedback, all coordinated with offline textbooks and hands-on materials, to create an engaging, responsive and highly-effective curriculum. The formative, and periodic summative, online assessments ensure that students have mastered the material and are ready to proceed to the next lesson, allowing them to work at their own pace. Pronunciation guides for key words and references to suggested additional resources, specific to each lesson and each student's assignments and assessments, are also included.

Learning Kits. Many of our courses utilize learning kits in conjunction with the online lessons to maximize the effectiveness of our learning systems. In addition to receiving access to our online lessons through the Internet, each K-8 student receives a shipment of materials, including award-winning textbooks, art supplies, laboratory supplies (e.g., microscopes, scales, science specimens) and other reference materials which are referred to and incorporated in instruction throughout our curriculum. This approach is consistent with our guiding principle to utilize technology where appropriate for our learning systems, and combine it with other effective instructional methods. Most of the textbooks we use are proprietary, written by K12 to be verbally engaging and visually appealing to students, with careful control of reading levels, and to complement the online experience. Through fiscal year 2013, we also converted 54 K12 books used across 61 courses into an electronic format, enabling us to offer options to enhance the student experience without physical books. We believe that our ability to effectively combine online lessons and materials—to develop, deliver and implement them together for instruction—is a competitive advantage.

Lesson Guides. Our courses are generally paired with a lesson guide. Lesson guides work in coordination with the online lessons and include the following: overview information for learning

16

coaches, lesson objectives, lesson outlines and activities, answer keys to student exercises and suggestions for explaining difficult concepts to students.

Pre-K and K-8 Courses

From pre-kindergarten through 8th grade, our courses are generally categorized into seven major subject areas: English and language arts, mathematics, science, history, art, music and world languages. Our proprietary curriculum includes all of the courses that students need to complete their core kindergarten through 8th grade education; a new pre-K offering, which we refer to as EmbarK12, introduces students to core subjects through cross-curricular thematic units, building initial and fundamental relationships among concepts. Courses focus on developing fundamental skills and teaching the key knowledge building blocks or schemas-the "big ideas"-that each student will need to master the major subject areas, meet state standards-including those formulated as the Common Core State Standards ("CCSS")-and complete more advanced coursework. Unlike a traditional classroom education, our learning systems offer the flexibility for each student to take courses at different grade levels in a single academic year, providing flexibility for students to progress at their own level and pace within each subject area.

The first phase of our K12 second generation elementary language arts program is designed to deliver increased interactivity and make instruction even more engaging while integrating rewards, interactive practice and a virtual world. Our Fundamentals of Geometry and Algebra course completes our proprietary K-8 math offering. These courses support students at various skill levels via targeted, timely remediation, embody CCSS and include significant media integration. In addition, the flexibility of our learning systems allows us to tailor our curriculum to state specific requirements. For example, we have developed almost 70 courses specifically created for the public school standards in 13 states. In addition to the ongoing evolution of our K-5 Math+ program, we have also created over 80 custom Math+ sequences to serve specific state needs. We continue to migrate K12 K-8 courses from our legacy content management system ("CMS") to our new CMS.

High School Courses

The curriculum available to high school students is much broader and varies from student to student, largely as a result of the increased flexibility in course selection available to high school students. Students also are able to select from a wide range of electives. We have augmented our lab program for lab science courses with the creation of alternate kit-free science labs as an augmentation or alternative for our formerly kit-based high school science labs in order to provide a more flexible and robust lab program across our physical science, earth science, biology, chemistry and physics courses. Our overall lab program now includes traditional kit-based labs based on either shipped-in or household materials, virtual labs, video-based labs, data-collection and data-manipulation labs, and field studies. This array provides schools with additional materials flexibility, and integrates diverse modalities directly into our science curriculum to promote conceptual mastery. Across all subject areas, the K12 proprietary core curriculum accounts for approximately 90% of our high school course enrollments.

Aventa Learning by K12 Curriculum. We also offer curriculum to schools and school districts marketed as our Aventa Learning by K12 product line. Aventa courses are written to national academic standards and each of Aventa's 22 AP courses has been reviewed and approved by The College Board, as are all the AP courses that we offer. Aventa's online courses are developed by subject matter experts, designed by multimedia teams and delivered by highly qualified high school instructors. Aventa classes are primarily delivered over the Internet and use a variety of interactive elements to keep students engaged throughout. A deep understanding of K-12 pedagogy, as well as the human factors associated with online technology, is integrated into Aventa's curriculum.

17

A+. Our A+ courseware is currently in use in over 5,000 public and private K-12 schools, public charter schools, colleges, correctional institutions, centers of adult literacy, military education programs and after-school learning centers. The A+nyWhere Learning System provides an integrated offering of instructional software and assessment for reading, mathematics, language arts, science, writing, history, government, economics and geography for grade levels K-12. In addition, we also provide assessment testing and instructional content for the General Educational Development ("GED") test. These products are designed to provide for LAN, WAN and Internet delivery in schools and support Windows and Macintosh platforms. Spanish-language versions are available for mathematics and language arts in grade levels 1-6.

Middlebury Interactive Languages. We offer digital world language courses and residential summer language academies through our MIL joint venture. This venture offers immersive language courses for K-12 students based on Middlebury College's pedagogy to help students gain a stronger base of comprehension and accelerate language acquisition. The age-appropriate language courses, which can be implemented fully online, in a blended learning environment or as supplemental material, use instructional tools such as animation, music, videos and other authentic materials to immerse students in the language and culture of study. Chinese, French, German, Latin and Spanish courses for elementary, middle and high school students are now available, and additional courses are in development to create a comprehensive suite of world language offerings. The joint venture also operates summer residential language academies, an immersive program for middle and high school students. Academy students live in language by taking the Language Pledge®, a promise to communicate solely in their language of study for four weeks. Instruction is offered in Arabic, Chinese, French, German and Spanish at multiple college campuses in the United States and in Beijing, China.

Innovative Learning Applications

In order to continue to enhance the user experience and instructional methods of our learning systems, we strive to develop new technologies and learning applications and adapt our curriculum to new technology devices and platforms.

- •

- Mobile Learning: We have created a limited number of

mobile tools and applications. Eight new mobile applications were delivered in fiscal year 2013 for a total of 21 applications now available for download. Three of our new apps were created in HTML5.

As of June 30, 2013, these apps have been downloaded over 740,000 times since 2010. We continue to deploy innovative educational tools for the mobile environment. With the increase in the use

of mobile devices, our mobile applications will create the ability for a student to learn "on-the-go," allowing for more continuous learning, engagement and mastery of content. We offer certain

applications for both phones and tablets available via Apple, Google Play and the Amazon marketplace, adapting many of our award-winning curriculum features for the mobile application space. We are

continuing to work on solutions that facilitate the deployment of our curriculum on mobile devices.

- •

- Interactive Games: An active educational games initiative

is delivering new methods for engagement, practice and review of K-12 concepts, including: narrative/immersive styles, rewards, persistent data, complex algorithms, etc. These games make use of

extensive research and educational best practices and address targeted learning objectives. We have delivered a total of nine interactive games and an innovative review and practice portal called

Noodleverse. As of June 30, 2013, Noodleverse included approximately 3,000 activities, an increase of 1,300 over fiscal 2012. Noodleverse is designed for K-3 students in conjunction with a new

language arts program.

- •

- Virtual Labs: We have delivered alternatives for our educational partners who desire materials-free curriculum. This includes converting over 59 existing materials-based high school

18

- •

- eBook and Digital Book Distribution: Through fiscal year

2013, we have converted 54 K12 textbooks used across 61 courses into an electronic format, including textbooks, reference guides, literature readers and lab manuals. This digital

delivery ability enables us to offer options to our customers via interactive online books that enhance the student's reading experience, reinforce the student's learning approach and create a new

method for delivering book and print materials. Each offline book is converted into an electronic book format with a custom user interface to be viewed via a standard web browser or a commercially

available electronic reader (Kindle, Nook, etc.).

- •

- Adaptive Learning: We have learning management systems and

can now build courses that are adaptive, which enable individualized learning experiences as the course "adapts" at key points to student behavior and input. Based on assessment results or individual

activity, these courses can automatically route students to an alternate explanation, additional practice or remediation on a prerequisite skill or crucial concept. In addition to remediation, the

capability allows students to accelerate past previously mastered concepts, giving skillful students time for more challenging work. Our MARK12 reading remediation product captures

individual students' successes and challenges as they practice phonemic awareness, alphabetic principles, accuracy and fluency, vocabulary and comprehension. The program serves the individual student

more exercises, practice and review in areas of difficulty. Adaptation in this way tailors the instruction automatically for each student, making learning experiences more efficient and effective by

building right into the course the logic an expert teacher or tutor uses to differentiate instruction.

- •

- National Math Lab: The National Math Lab program has been

designed to address students' math needs and to help them develop the necessary skills to succeed in math. The program works with students in grades 5 through 10 across all of the K12 network schools,

who experience challenges in math and need supplemental support. National Math Lab provides nearly twice the usual amount of math instruction to students and in addition to their regular online math

coursework, students attend targeted synchronous mathematical instruction sessions provided by highly-trained math teachers four days per week.

- •

- Engaging Videos: We continue to explore opportunities to enhance student engagement through strategic use of relevant multimedia. Multimedia is specifically used as appropriate for the subject matter. For example, our video on photosynthesis for high school biology allows students to witness the setup, procedure and data in a classic experiment in which an aquatic plant is exposed to light and produces oxygen bubbles. The high definition video and the presentation to the student of real data (which they then use in their analysis) makes this video lab a multimedia experience that is coupled with a scientific method.

Science labs into highly interactive virtual labs and video lab simulations that meet state standards and still maintain teaching the original learning objectives. For example, in high school chemistry we have developed a virtual laboratory on chromatography, in which students separate a number of inks into their component pigments. This laboratory is performed at a virtual lab bench with all the materials and with the same procedures high school students would use in a physical chemistry laboratory.

Online School Platform-Learning Management System

For our K12 curriculum users in grades K-8, we provide a proprietary learning management system, our OLS platform. The OLS is a significant part of our ongoing effort to provide the most engaging and productive learning experience for students. The OLS platform is an adaptive, intuitive, web-based software platform that provides access to our online lessons, our lesson planning and scheduling tools, and our progress tracking tool which serves a key role in assisting parents and teachers in managing

19

each student's progress. The OLS is also the central structure through which students, parents, teachers and administrators interact using Kmail and Class Connect (our integrated synchronous session scheduler). Because the OLS is a web-based platform, students, parents and teachers can access our online tools and lessons through the OLS from anywhere with an Internet connection. During fiscal year 2013, we completed several major releases of our platform intended to enhance the capabilities available to our learning coaches, increase teacher efficiency and drive overall academic achievement. We license a third-party learning management system for use in our high school program.

- •

- Lesson Planning and Scheduling Tools. In a school year, a

typical student will complete between 800 and 1,200 lessons across six or more subject areas. Our lesson planning and scheduling tools enable teachers and parents to establish an individualized plan

for each student to complete his or her lessons. These tools are designed to dynamically update the lesson plan as a student progresses through each lesson and course, allowing flexibility to increase

or decrease the pace at which the student advances through the curriculum while ensuring that the student progresses towards completion in the desired time frame. For example, the schedule can easily

be adapted to accommodate a student who desires to attend school six days a week, a student who is interested in studying during the winter holidays to take time off during the spring, or a student

who chooses to complete two math lessons a day for the first month of the school year and delay art lessons until the second month of the school year. Moreover, changes can be made to the schedule at

any point during the school year and the remainder of the student's schedule will automatically be adjusted in the OLS. Unlike a traditional classroom education, our learning systems offer the

flexibility for each student to take courses at different grade levels in a single academic year, providing flexibility for students to progress at their own level and pace within each subject area.

The curriculum includes assessments built into every lesson to guide and tailor the pace of progress to each child's needs.

- •

- Progress Tracking Tools. Once a schedule has been

established, the OLS delivers lessons based upon the specified parameters of the school and the teacher. Each day, a student is initially directed to a home page listing the schedule for that

particular day and begins the school day by selecting one of the listed lessons. As each lesson is completed, the student returns to the day's schedule to proceed to the next subject. If a student

does not complete a lesson by the end of the day on which it was originally scheduled, the lesson will be rescheduled to the next day and will resume at the point where the student left off. Our

progress tracking tool allows students, parents, learning coaches and teachers to monitor student progress. In addition, information collected by our progress tracking tool regarding student

performance, attendance and other data are transferred to our proprietary Student Administration Management System ("SAMS") for use in providing administrative support services. This instructional

program includes several processes and educational techniques that embrace proactive intervention. As a result, we can provide high quality instruction and intervention equal to student needs.

- •

- Assessment Tracking Tools: Meaningful assessments and feedback are critical to efficient and successful learning. Assessments embedded into our lessons help the parent, teacher, and student verify that the student is achieving important learning objectives. A student does not progress to the next lesson in a course until he has mastered the assessment at the end of the previous lesson. Teachers can easily view assessment data for their students in the OLS so that they can proactively provide additional instruction to students when needed. Our assessment tools also help us improve the program by providing information on the effectiveness of specific instructional activities and the curriculum.

Our program makes use of a variety of formative and summative assessment instruments:

- •

- Lesson assessments are used to verify mastery of the objectives for that lesson and to determine whether further study of the lesson is necessary.

20

- •

- Unit assessments show whether or not the student has retained key learning objectives for the unit, and identify specific

objectives students may need to review before moving on.

- •

- Semester assessments verify student mastery of key learning objectives for the semester.

Independent third-party assessments are used in most of our managed schools to pinpoint specific individual student strengths and weaknesses relative to state standards. These results enable the teacher to develop a highly individualized learning plan for each student. Students are tested via an online, adaptive test at the beginning and end of the school year to provide a measure of individual student growth demonstrating the value-added gains of the school program.

School Management Systems

SAMS is our proprietary student information system. SAMS is integrated with the OLS and several other proprietary systems including our online enrollment system that allows parents to complete school enrollment forms online and our Order Management System that generates orders for learning kits and computers to be delivered to students. SAMS stores student-specific data and is used for a variety of functions, including enrolling students in courses, assigning progress marks and grades, tracking student demographic data, and generating student transcripts. Our systems also include TotalView, a suite of online applications that provides administrators, teachers, parents and students a unified view of student progress, attendance, communications, and learning kit shipment tracking. TotalView includes a sophisticated means of documenting student engagement in required classroom activities, identification of those students struggling with grade level state content standards, and previous year's performance on state tests. TotalView also includes Kmail, our internal communications system. Through Kmail, administrators and teachers can communicate electronically with learning coaches and students. TotalView also includes an enrollment processing and tracking tool that allows us to closely monitor and manage the enrollment process for new students. Over the past several years, we have enhanced TotalView with additional functionality to better support the operation of the virtual and blended public schools.

PEAK12

In fiscal year 2012, we launched an innovative online learning solution called PEAK12. This solution simplifies a district's management of online learning by consolidating multiple solutions on a single platform. It allows administrators and teachers to manage enrollments, programs and performance tracking, alerts and reporting across multiple online solutions from a single solution. In addition, through the PEAK12 library, districts can quickly and easily search, build, provision and publish content or course modifications or new course solutions using various online learning assets. In the near future, it will integrate with a variety of third-party platforms to allow districts more flexibility and control over how they launch and manage their online learning programs. Since its launch, PEAK12 has served nearly 750 school districts and school partners and more than 110,000 students. As more districts adopt online learning, they are demanding more control and flexibility in running their programs. PEAK12 provides unparalleled capabilities for districts wanting to operate multiple solutions or catalogs from a single place and offers rich personalization features that can be managed at the district, school or teacher level.

Our Services

We offer a comprehensive suite of services to students and their families as well as directly to virtual and blended public schools, traditional schools and school districts. Our services can be categorized broadly into academic support services and management and technology services.

21

Academic Support Services