Exhibit

Item 8. Financial Statements and Supplementary Data

Our financial statements as of December 31, 2015 and 2014 and for each of the three years in the period ended December 31, 2015, and the Report of the Registered Independent Public Accounting Firm are included in this report as listed in the index.

|

| |

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Report of Independent Registered Public Accounting Firm

The Board of Directors and Stockholders of

Insulet Corporation

We have audited the accompanying consolidated balance sheets of Insulet Corporation as of December 31, 2015 and 2014, and the related consolidated statements of operations, comprehensive loss, stockholders' equity and cash flows for each of the three years in the period ended December 31, 2015. Our audits also include the financial statement schedule listed in the Index at Item 15(a). These financial statements and schedule are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements and schedule based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the consolidated financial position of Insulet Corporation at December 31, 2015 and 2014, and the consolidated results of its operations and its cash flows for each of the three years in the period ended December 31, 2015, in conformity with U.S. generally accepted accounting principles. Also, in our opinion, the related financial statement schedule, when considered in relation to the basic financial statements taken as a whole, presents fairly in all material respects the information set forth therein.

As discussed in Note 2 to the consolidated financial statements, the Company changed its method for presenting debt issuance costs as a result of the adoption of the amendments to the FASB Accounting Standards Codification resulting from Accounting Standards Update No. 2015-03, ‘‘Simplifying the Presentation of Debt Issuance Costs,’’ effective December 31, 2015.

/s/ Ernst & Young LLP

Boston, Massachusetts

February 29, 2016

(except for the effects of discontinued operations, as discussed in Notes 2 and 18, as

to which the date is September 6, 2016)

INSULET CORPORATION

CONSOLIDATED BALANCE SHEETS

|

| | | | | | | |

| December 31,

2015 | | December 31,

2014 |

(In thousands, except share data) | | | |

ASSETS | | | |

Current Assets | | | |

Cash and cash equivalents | $ | 122,672 |

| | $ | 151,193 |

|

Accounts receivable, net | 42,530 |

| | 35,243 |

|

Inventories, net | 12,024 |

| | 11,450 |

|

Prepaid expenses and other current assets | 4,283 |

| | 2,670 |

|

Current assets of discontinued operations | 9,252 |

| | 7,640 |

|

Total current assets | 190,761 |

| | 208,196 |

|

Property and equipment, net | 41,793 |

| | 36,942 |

|

Intangible assets, net | 933 |

| | — |

|

Goodwill | 39,607 |

| | 37,396 |

|

Other assets | 76 |

| | 294 |

|

Long-term assets of discontinued operations | 1,956 |

| | 14,354 |

|

Total assets | $ | 275,126 |

| | $ | 297,182 |

|

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

Current Liabilities | | | |

Accounts payable | $ | 15,213 |

| | $ | 12,580 |

|

Accrued expenses and other current liabilities | 36,744 |

| | 18,850 |

|

Deferred revenue | 2,361 |

| | 1,554 |

|

Current portion of capital lease obligations | 5,519 |

| | 3,380 |

|

Current liabilities of discontinued operations | 5,319 |

| | 7,932 |

|

Total current liabilities | 65,156 |

| | 44,296 |

|

Capital lease obligations | 269 |

| | 2,263 |

|

Long-term debt, net of discount | 171,698 |

| | 164,020 |

|

Other long-term liabilities | 3,952 |

| | 2,774 |

|

Total liabilities | 241,075 |

| | 213,353 |

|

Commitments and contingencies (Note 13) |

| |

|

Stockholders’ Equity | | | |

Preferred stock, $.001 par value: | | | |

Authorized: 5,000,000 shares at December 31, 2015 and 2014. Issued and outstanding: zero shares at December 31, 2015 and 2014. | — |

| | — |

|

Common stock, $.001 par value: | | | |

Authorized: 100,000,000 shares at December 31, 2015 and 2014.

Issued and outstanding: 56,954,830 and 56,299,022 shares at December 31, 2015 and 2014, respectively. | 57 |

| | 56 |

|

Additional paid-in capital | 686,193 |

| | 661,811 |

|

Accumulated other comprehensive loss | (654 | ) | | (13 | ) |

Accumulated deficit | (651,545 | ) | | (578,025 | ) |

Total stockholders’ equity | 34,051 |

| | 83,829 |

|

Total liabilities and stockholders’ equity | $ | 275,126 |

| | $ | 297,182 |

|

The accompanying notes are an integral part of these consolidated financial statements.

3

INSULET CORPORATION

CONSOLIDATED STATEMENTS OF OPERATIONS

|

| | | | | | | | | | | | |

| | Years Ended December 31, |

(In thousands, except share and per share data) | | 2015 | | 2014 | | 2013 |

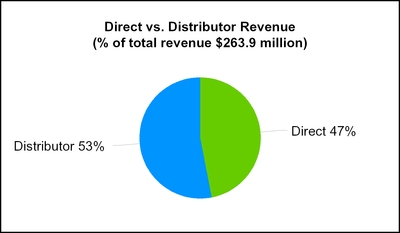

Revenue | | $ | 263,893 |

| | $ | 231,321 |

| | $ | 185,139 |

|

Cost of revenue | | 130,622 |

| | 104,195 |

| | 95,364 |

|

Gross profit | | 133,271 |

| | 127,126 |

| | 89,775 |

|

Operating expenses: | | | | | | |

Research and development | | 43,208 |

| | 27,900 |

| | 21,765 |

|

Sales and marketing | | 78,407 |

| | 50,552 |

| | 45,176 |

|

General and administrative | | 60,392 |

| | 57,548 |

| | 49,509 |

|

Total operating expenses | | 182,007 |

| | 136,000 |

| | 116,450 |

|

Operating loss | | (48,736 | ) | | (8,874 | ) | | (26,675 | ) |

Interest expense | | (12,712 | ) | | (14,578 | ) | | (16,889 | ) |

Other income (expense), net | | 58 |

| | (1,225 | ) | | 1,431 |

|

Loss on extinguishment of long-term debt | | — |

| | (23,203 | ) | | (325 | ) |

Interest and other expense, net | | (12,654 | ) | | (39,006 | ) | | (15,783 | ) |

Loss from continuing operations before income taxes

| | (61,390 | ) | | (47,880 | ) | | (42,458 | ) |

Income tax expense | | (212 | ) | | (60 | ) | | (22 | ) |

Net loss from continuing operations | | (61,602 | ) | | (47,940 | ) | | (42,480 | ) |

Loss from discontinued operations, net of tax ($79, $82 and $78 for years ended December 31, 2015, 2014 and 2013, respectively) | | (11,918 | ) | | (3,560 | ) | | (2,494 | ) |

Net loss | | $ | (73,520 | ) | | $ | (51,500 | ) | | $ | (44,974 | ) |

Net loss per share basic and diluted | | | | | | |

Net loss from continuing operations per share basic and diluted | | $ | (1.08 | ) | | $ | (0.86 | ) | | $ | (0.78 | ) |

Net loss from discontinued operations per share basic and diluted | | $ | (0.21 | ) | | $ | (0.06 | ) | | $ | (0.05 | ) |

Weighted-average number of shares used in calculating net loss per share | | 56,785,646 |

| | 55,628,542 |

| | 54,010,887 |

|

The accompanying notes are an integral part of these consolidated financial statements.

4

INSULET CORPORATION

CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

|

| | | | | | | | | | | | |

| | Years Ended December 31, |

(In thousands) | | 2015 | | 2014 | | 2013 |

Net loss | | $ | (73,520 | ) | | $ | (51,500 | ) | | $ | (44,974 | ) |

Other comprehensive loss, net of tax | | | | | | |

Foreign currency translation adjustment, net of tax | | (641 | ) | | 6 |

| | (19 | ) |

Total other comprehensive (loss) income, net of tax | | (641 | ) | | 6 |

| | (19 | ) |

Total comprehensive loss | | $ | (74,161 | ) | | $ | (51,494 | ) | | $ | (44,993 | ) |

The accompanying notes are an integral part of these consolidated financial statements.

5

INSULET CORPORATION

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(In thousands, except share data)

|

| | | | | | | | | | | | | | | | | | | | | | |

| Common Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Accumulated Other Comprehensive Loss | | Total Stockholders’ Equity |

| Shares | | Amount | |

Balance at December 31, 2012 | 48,359,063 |

| | $ | 48 |

| | $ | 525,679 |

| | $ | (481,551 | ) | | | | $ | 44,176 |

|

Exercise of options to purchase common stock | 872,073 |

| | 1 |

| | 9,479 |

| | — |

| | | | 9,480 |

|

Issuance for employee stock purchase plan | 12,970 |

| | — |

| | 445 |

| | — |

| | | | 445 |

|

Stock-based compensation expense | — |

| | — |

| | 12,616 |

| | — |

| | | | 12,616 |

|

Restricted stock units vested, net of shares withheld for taxes | 217,281 |

| | — |

| | (3,265 | ) | | — |

| | | | (3,265 | ) |

Issuance of common stock, net of offering costs of $5.0 million | 4,715,000 |

| | 5 |

| | 92,807 |

| | — |

| | | | 92,812 |

|

Exercise of warrants to purchase common stock | 47,392 |

| | — |

| | — |

| | — |

| | | | — |

|

Issuance of common stock pursuant to conversion of debt | 646,645 |

| | 1 |

| | 13,325 |

| | — |

| | | | 13,326 |

|

Foreign currency translation adjustment, net of tax | | | | | | | | | (19 | ) | | (19 | ) |

Net loss | — |

| | — |

| | — |

| | (44,974 | ) | | | | (44,974 | ) |

Balance at December 31, 2013 | 54,870,424 |

| | $ | 55 |

| | $ | 651,086 |

| | $ | (526,525 | ) | | $ | (19 | ) | | $ | 124,597 |

|

Exercise of options to purchase common stock | 754,522 |

| | 1 |

| | 11,084 |

| | — |

| | | | 11,085 |

|

Issuance for employee stock purchase plan | 13,620 |

| | — |

| | 583 |

| | — |

| | | | 583 |

|

Stock-based compensation expense | — |

| | — |

| | 22,432 |

| | — |

| | | | 22,432 |

|

Restricted stock units vested, net of shares withheld for taxes | 311,921 |

| | — |

| | (8,665 | ) | | — |

| | | | (8,665 | ) |

Net impact of conversion of 3.75% Notes | — |

| | — |

| | (61,728 | ) | | — |

| | | | (61,728 | ) |

Allocation to equity for conversion feature on 2% Notes, net of issuance costs | — |

| | — |

| | 34,455 |

| | — |

| | | | 34,455 |

|

Issuance of common stock pursuant to conversion of debt | 348,535 |

| | | | 12,564 |

| | — |

| | | | 12,564 |

|

Foreign currency translation adjustment, net of tax | | | | | | | | | 6 |

| | 6 |

|

Net loss | — |

| | — |

| | — |

| | (51,500 | ) | | | | $ | (51,500 | ) |

Balance at December 31, 2014 | 56,299,022 |

| | $ | 56 |

| | $ | 661,811 |

| | $ | (578,025 | ) | | $ | (13 | ) | | $ | 83,829 |

|

Exercise of options to purchase common stock | 449,149 |

| | 1 |

| | 7,198 |

| | | | | | 7,199 |

|

Issuance for employee stock purchase plan | 22,039 |

| | — |

| | 652 |

| | | | | | 652 |

|

Stock-based compensation expense | — |

| | — |

| | 19,178 |

| | | | | | 19,178 |

|

Restricted stock units vested, net of shares withheld for taxes | 184,620 |

| | — |

| | (2,646 | ) | | | | | | (2,646 | ) |

Foreign currency translation adjustment, net of tax | | | | | | | | | (641 | ) | | (641 | ) |

Net loss | — |

| | — |

| | — |

| | (73,520 | ) | | — |

| | (73,520 | ) |

Balance at December 31, 2015 | 56,954,830 |

| | $ | 57 |

| | $ | 686,193 |

| | $ | (651,545 | ) | | $ | (654 | ) | | $ | 34,051 |

|

The accompanying notes are an integral part of these consolidated financial statements.

6

INSULET CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

| | | | | | | | | | | | |

| | Years Ended December 31, |

(In thousands) | | 2015 | | 2014 | | 2013 |

Cash flows from operating activities | | | | | | |

Net loss | | $ | (73,520 | ) | | $ | (51,500 | ) | | $ | (44,974 | ) |

Adjustments to reconcile net loss to net cash used in operating activities | | | | | | |

Depreciation and amortization | | 15,838 |

| | 12,223 |

| | 11,806 |

|

Non-cash interest and other expense | | 7,678 |

| | 10,253 |

| | 9,731 |

|

Stock-based compensation expense | | 19,178 |

| | 22,519 |

| | 12,683 |

|

Loss on extinguishment of debt | | — |

| | 23,203 |

| | 325 |

|

Provision for bad debts | | 1,184 |

| | 3,254 |

| | 4,741 |

|

Impairment and other charges | | 9,086 |

| | — |

| | 2,511 |

|

Changes in operating assets and liabilities: | | | | | | |

Accounts receivable | | (9,793 | ) | | (10,069 | ) | | (4,514 | ) |

Inventories | | (722 | ) | | (3,635 | ) | | 5,403 |

|

Deferred revenue | | 809 |

| | 654 |

| | (4,545 | ) |

Prepaid expenses and other assets | | (1,460 | ) | | 662 |

| | (320 | ) |

Accounts payable, accrued expenses and other current liabilities | | 17,986 |

| | 525 |

| | 10,425 |

|

Other long-term liabilities | | 1,184 |

| | 831 |

| | 76 |

|

Net cash (used in) provided by operating activities (1) | | (12,552 | ) | | 8,920 |

| | 3,348 |

|

Cash flows from investing activities | | | | | | |

Purchases of property and equipment | | (10,608 | ) | | (11,486 | ) | | (7,307 | ) |

Acquisition of Canadian distribution business | | (4,715 | ) | | — |

| | — |

|

Net cash used in investing activities | | (15,323 | ) | | (11,486 | ) | | (7,307 | ) |

Cash flows from financing activities | | | | | | |

Principal payments of capital lease obligations | | (5,576 | ) | | (3,858 | ) | | (994 | ) |

Proceeds from issuance of long-term debt, net of issuance costs | | — |

| | 194,490 |

| | — |

|

Repayment of long-term debt | | — |

| | (189,521 | ) | | (2,000 | ) |

Proceeds from issuance of common stock, net of offering costs | | 7,851 |

| | 11,586 |

| | 102,652 |

|

Payment of withholding taxes in connection with vesting of restricted stock units | | (2,646 | ) | | (8,665 | ) | | (3,265 | ) |

Net cash (used in) provided by financing activities | | (371 | ) | | 4,032 |

| | 96,393 |

|

Effect of exchange rate changes on cash | | (275 | ) | | — |

| | — |

|

Net (decrease) increase in cash and cash equivalents | | (28,521 | ) | | 1,466 |

| | 92,434 |

|

Cash and cash equivalents, beginning of period | | 151,193 |

| | 149,727 |

| | 57,293 |

|

Cash and cash equivalents, end of period | | $ | 122,672 |

| | $ | 151,193 |

| | $ | 149,727 |

|

Supplemental disclosure of cash flow information | | | | | | |

Cash paid for interest | | $ | 4,025 |

| | $ | 4,657 |

| | $ | 5,704 |

|

Cash paid for taxes | | $ | 109 |

| | $ | 124 |

| | $ | 321 |

|

Non-cash investing and financing activities | | | | | | |

Allocation to equity for conversion feature for the 2% Notes | | $ | — |

| | $ | 35,638 |

| | $ | — |

|

Common stock issued in exchange for 3.75% Convertible Senior Notes | | $ | — |

| | $ | 12,564 |

| | $ | 13,000 |

|

Purchases of property and equipment under capital lease | | $ | 5,721 |

| | $ | 1,474 |

| | $ | 9,021 |

|

| |

(1) | Includes activity related to discontinued operations. See note 18 to the consolidated financial statements for discussion of discontinued operations. |

The accompanying notes are an integral part of these consolidated financial statements.

7

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 1. Nature of the Business

Insulet Corporation, the "Company," is primarily engaged in the development, manufacturing and sale of its proprietary OmniPod Insulin Management System (the “OmniPod System”), an innovative, discreet and easy-to-use insulin infusion system for people with insulin-dependent diabetes. The OmniPod System features a unique disposable tubeless OmniPod which is worn on the body for approximately three days at a time and the handheld, wireless Personal Diabetes Manager (“PDM”). Conventional insulin pumps require people with insulin-dependent diabetes to learn to use, manage and wear a number of cumbersome components, including up to 42 inches of tubing. In contrast, the OmniPod System features two discreet, easy-to-use devices that eliminate the need for a bulky pump, tubing and separate blood glucose meter, provides for virtually pain-free automated cannula insertion, communicates wirelessly and integrates a blood glucose meter.

The Company acquired Neighborhood Holdings, Inc. and its wholly-owned subsidiaries (collectively, “Neighborhood Diabetes”) in June 2011. Through Neighborhood Diabetes, the Company provided customers with blood glucose testing supplies, traditional insulin pumps, pump supplies and pharmaceuticals and had the ability to process claims as either durable medical equipment or through pharmacy benefits. In February 2016, the Company sold Neighborhood Diabetes to Liberty Medical LLC ("Liberty Medical"). Additional information regarding the disposition and treatment of the Neighborhood Diabetes business as discontinued operations is provided in note 18 to the consolidated financial statements.

Commercial sales of the OmniPod System began in the United States in 2005. The Company sells the OmniPod System and other diabetes management supplies in the United States through direct sales to customers or through its distribution partners. The OmniPod System is currently available in multiple countries in Europe, Canada and Israel.

On July 7, 2015, the Company executed an asset purchase agreement whereby it acquired the Canadian OmniPod distribution operations from GlaxoSmithKline ("GSK"). With the acquisition, the Company assumed all distribution, sales, marketing, training and support activities for the OmniPod system in Canada. Additional information regarding this acquisition is provided in note 3 to the consolidated financial statements.

Note 2. Summary of Significant Accounting Policies

Use of Estimates in Preparation of Financial Statements

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions in the application of certain of its significant accounting policies that may materially affect the reported amounts of assets, liabilities, equity, revenue and expenses. The most significant estimates used in these financial statements include the valuation of; stock-based compensation expense, acquired businesses, accounts receivable, inventories, goodwill, deferred revenue, equity instruments, the lives of property and equipment and intangible assets, as well as warranty and doubtful accounts allowance reserve calculations. Actual results may differ from those estimates.

Foreign Currency Translation

For foreign operations, asset and liability accounts are translated at exchange rates as of the balance sheet date; income and expenses are translated using weighted average exchange rates for the reporting period. Resulting translation adjustments are reported in accumulated other comprehensive loss, a separate component of stockholders' equity. Gains and losses arising from transactions and translation of period-end balances denominated in currencies other than the functional currency are included in other expense, net, and were not material for fiscal years 2015, 2014 and 2013.

Principles of Consolidation

The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. All material intercompany balances and transactions have been eliminated in consolidation.

Cash and Cash Equivalents

For the purpose of the financial statement classification, the Company considers all highly liquid investment instruments with original maturities of 90 days or less, when purchased, to be cash equivalents. Cash equivalents include money market accounts, which are carried at cost which approximates their fair value. Outstanding letters

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

of credit, related to security deposits for lease obligations, totaled $1.2 million as of December 31, 2015 and December 31, 2014.

Property and Equipment

Property and equipment is stated at cost and depreciated using the straight-line method over the estimated useful life of the respective assets. Leasehold improvements are amortized over their useful life or the life of the lease, whichever is shorter. Assets acquired under capital leases are amortized in accordance with the respective class of owned assets and the amortization is included with depreciation expense. Maintenance and repair costs are expensed as incurred.

Business Combinations

The Company recognizes the assets and liabilities assumed in business combinations on the basis of their fair values at the date of acquisition. The Company assesses the fair value of assets, including intangible assets, using a variety of methods and each asset is measured at fair value from the perspective of a market participant. The method used to estimate the fair values of intangible assets incorporates significant assumptions regarding the estimates a market participant would make in order to evaluate an asset, including a market participant’s use of the asset and the appropriate discount rates for a market participant. Assets recorded from the perspective of a market participant that are determined to not have economic use for the Company are expensed immediately. Any excess purchase price over the fair value of the net tangible and intangible assets acquired is allocated to goodwill. Transaction costs and restructuring costs associated with a business combination are expensed as incurred.

Segment Reporting

Operating segments are defined as components of an enterprise about which separate financial information is available that is evaluated on a regular basis by the chief operating decision-maker ("CODM") in deciding how to allocate resources to an individual segment and in assessing performance of the segment. The Company has concluded that their Chief Executive Officer is the CODM as he is the ultimate decision maker for key operating decisions, determining the allocation of resources and assessing the financial performance of the Company. These decisions, allocations and assessments are performed by the CODM using consolidated financial information. Consolidated financial information is utilized by the CODM as the Company’s current product offering primarily consists of drug delivery and the OmniPod System. The Company’s products are relatively consistent and manufacturing is centralized and consistent across product offerings. Based on these factors, key operating decisions and resource allocations are made by the CODM using consolidated financial data and as such the Company has concluded that they operate as one segment.

Goodwill

Goodwill represents the excess of the cost of acquired businesses over the fair value of identifiable net assets acquired. The Company follows the provisions of Financial Accounting Standards Board ("FASB") ASC 350-20, Intangibles - Goodwill and Other (“ASC 350-20”). The Company performs an assessment of its goodwill for impairment on at least an annual basis or whenever events or changes in circumstances indicate there might be impairment. The Company's annual impairment test date is October 1st.

The majority of the Company's goodwill resulted from the acquisition of Neighborhood Diabetes in June 2011. This goodwill largely reflects operational synergies and expansion of product offerings across markets complementary to the existing core OmniPod offerings.

As the Company operates in one segment, the Company has considered whether that segment contains multiple reporting units. The Company has concluded that there is a single reporting unit as the Company does not have segment managers and discrete financial information below consolidated results is not reviewed on a regular basis. Based on this conclusion, goodwill was tested for impairment at the enterprise level. The Company performs an annual goodwill impairment test unless interim indicators of impairment exist. The Company has the option to first assess the qualitative factors to determine whether it is more likely than not that the fair value of its sole reporting unit is less than its carrying amount. This qualitative analysis is used as a basis for determining whether it is necessary to perform the two-step goodwill impairment analysis. If the Company determines that it is more likely than not that its fair value is less than its carrying amount, then the two-step goodwill impairment test will be performed. The first step compares the carrying value of the reporting unit to its fair value using a discounted cash flow analysis. If the reporting unit’s carrying value exceeds its fair value, the Company would record an impairment loss to the extent that the carrying value of goodwill exceeds its implied fair value. There was no impairment of goodwill during the years ended December 31, 2015, 2014 or 2013. As a result of the sale of Neighborhood Diabetes, goodwill totaling $0.1 million was allocated to the discontinued business on the disposition date using the relative fair value approach.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The following table presents the change in carrying amount of goodwill during the period indicated:

|

| | | | | | | |

| Years Ended December 31, |

| 2015 | | 2014 |

(In thousands) | | | |

Goodwill: | | | |

Beginning balance | $ | 37,396 |

| | $ | 37,396 |

|

Goodwill as a result of acquisition | 2,403 |

| | — |

|

Foreign currency adjustment | (192 | ) | | — |

|

Ending balance | $ | 39,607 |

| | $ | 37,396 |

|

Revenue Recognition

The Company generates the majority of its revenue from sales of its OmniPod System to customers and third-party distributors who resell the products to patients with diabetes.

Revenue recognition requires that persuasive evidence of a sales arrangement exists, delivery of goods occurs through transfer of title and risk and rewards of ownership, the selling price is fixed or determinable and collectability is reasonably assured. With respect to these criteria:

| |

• | The evidence of an arrangement generally consists of a physician order form, a patient information form and, if applicable, third-party insurance approval for sales directly to patients or a purchase order for sales to a third-party distributor. |

| |

• | Transfer of title and risk and rewards of ownership are passed to the patient or third-party distributor upon shipment of the products. |

| |

• | The selling prices for all sales are fixed and agreed with the patient or third-party distributor and, if applicable, the patient’s third-party insurance provider(s) prior to shipment and are based on established list prices or, in the case of certain third-party insurers, contractually agreed upon prices. Provisions for discounts, rebates and other adjustments to customers are established as a reduction to revenue in the same period the related sales are recorded. |

The Company offers a 45-day right of return for sales of its OmniPod System in the United States, and a 90-day right of return for sales of its OmniPod System in Canada to new patients and defers revenue to reflect estimated sales returns in the same period that the related product sales are recorded. Returns are estimated through a comparison of the Company’s historical return data to its related sales. Historical rates of return are adjusted for known or expected changes in the marketplace when appropriate. When doubt exists about reasonable assuredness of collectability from specific customers, the Company defers revenue from sales of products to those customers until payment is received.

In June 2011, the Company entered into a development agreement with a U.S. based pharmaceutical company (the "Development Agreement”). Under the Development Agreement, the Company was required to perform design, development, regulatory, and other services to support the pharmaceutical company as it worked to obtain regulatory approval to use the Company’s drug delivery technology as a delivery method for its pharmaceutical. Over the term of the Development Agreement, the Company has invoiced amounts based upon meeting certain deliverable milestones. Revenue on the Development Agreement was recognized using a proportional performance methodology based on efforts incurred and total payments under the agreement. The impact of changes in the expected total effort or contract payments was recognized as a change in estimate using the cumulative catch-up method. The pharmaceutical company received regulatory approval and now purchases product from the Company for use with its pharmaceutical under a supply agreement. Product revenue under this arrangement is recognized at the time that all of the revenue recognition criteria are met, typically upon shipment.

The Company deferred revenue of $2.5 million and $1.6 million as of December 31, 2015 and December 31, 2014, respectively. Deferred revenue as of December 31, 2015 included $0.2 million classified in other long-term liabilities. Deferred revenue primarily relates to undelivered elements on certain arrangements within our developmental arrangements and other instances where we have not yet met the revenue recognition criteria.

International OmniPod revenue accounted for approximately 15%, 22% and 13% in the years ended December 31, 2015, 2014 and 2013, respectively.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Shipping and Handling Costs

The Company does not typically charge its customers for shipping and handling costs associated with shipping its product to its customers. These shipping and handling costs are included in general and administrative expenses.

Concentration of Credit Risk

Financial instruments that subject the Company to credit risk primarily consist of cash and cash equivalents. The Company maintains the majority of its cash with two financial institutions.

The Company purchases OmniPods from Flextronics International Ltd., its single source supplier. As of December 31, 2015 and December 31, 2014, liabilities to this vendor represented approximately 28% and 30% of the combined balance of accounts payable, accrued expenses and other current liabilities, respectively.

In the year ended December 31, 2015, three customers represented 13%, 10% and 12% of total revenue, respectively. In the year ended December 31, 2014, two customers represented 19% and 14% of total revenue, respectively. In the year ended December 31, 2013, two customer represented 17% and 10% of total revenue, respectively.

Reclassification of Prior Period Balance

Certain reclassifications have been made to prior periods amounts to conform to the current period financial statement presentation including adjusting footnotes within to reflect the presentation of discontinued operations as further discussed in Note 18. These reclassifications have no effect on previously reported net loss.

Recent Accounting Pronouncements

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers ("ASU 2014-09"). ASU 2014-09 requires that a company will recognize revenue when it transfers promised goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. Under this guidance, a company may make additional estimates regarding performance conditions and the allocation of variable consideration. The guidance is effective in fiscal years beginning January 1, 2018, with early adoption permitted. The Company is currently evaluating the impact of ASU 2014-09. The Company has not yet selected a transition method nor has it determined the effect of the standard on our consolidated financial position and results of operations.

In June 2014, the FASB issued ASU No. 2014-12, Compensation - Stock Compensation (Topic 718), Accounting for Share-Based Payments when the terms of an award provide that a performance target could be achieved after the requisite service period ("ASU 2014-12"). ASU 2014-12 clarifies the period over which compensation cost would be recognized in awards with a performance target that affects vesting and that could be achieved after the requisite service period. Compensation cost would be recognized over the required service period, if it is probable that the performance condition will be achieved. The guidance is effective in fiscal years beginning after January 1, 2016, with early adoption permitted. Based on the Company's current equity practices, the Company does not anticipate that the adoption will have a material impact.

In August 2014, the FASB issued ASU No. 2014-15, Presentation of Financial Statements- Going Concern ("ASU 2014-15"). ASU No. 2014-15 requires management to evaluate whether there is substantial doubt about the entity’s ability to continue as a going concern within one year after the date that the financial statements are issued. The new standard is effective for fiscal years ending after December 15, 2016. Early adoption is permitted. The Company has concluded, that if this standard had been adopted as of December 31, 2015, substantial doubt about the Company’s ability to continue as a going concern would not exist.

In April 2015, the FASB issued ASU No. 2015-03, Simplifying the Presentation of Debt Issuance Costs ("ASU 2015-03"). ASU 2015-03 amends existing guidance to require the presentation of debt issuance costs in the balance sheet as a deduction from the carrying amount of the related debt liability instead of a deferred charge. The guidance is effective for annual reporting periods beginning after December 15, 2015, and must be applied retrospectively. Early adoption is permitted. The Company has adopted ASU 2015-03, as of December 31, 2015. The Company historically presented deferred debt issuance costs, or fees related to directly issuing debt, as assets on the consolidated balance sheets. As of December 31, 2014, the adoption of this standard resulted in the reclassification of $5.0 million from other assets to long-term debt. These costs will continue to be amortized as interest expense over the term of the corresponding debt issuance.

In July 2015, the FASB issued ASU No. 2015-11, Simplifying the Measurement of Inventory ("ASU 2015-11"). ASU 2015-11 amends existing guidance and requires entities to measure most inventory at the lower of cost and

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

net realizable value. The guidance is effective prospectively for annual reporting periods beginning after December 15, 2016. Early adoption is permitted. Upon adoption, entities must disclose the nature of and reason for the accounting change. The Company is currently evaluating the impact of ASU 2015-11.

In September 2015, the FASB issued ASU No. 2015-16, Simplifying the Accounting for Measurement Period Adjustments ("ASU 2015-16"). ASU 2015-16 eliminates the requirement that an acquirer in a business combination account for measurement-period adjustments retrospectively. Instead, an acquirer will recognize a measurement period adjustment during the period in which it determines the amount of the adjustment, including the effect on earnings of any amounts it would have recorded in previous periods if the accounting had been completed at the acquisition date. Early adoption is permitted. The Company is currently evaluating the impact of ASU 2015-16.

In November 2015, the FASB issued ASU No. 2015-17, Balance Sheet Classification of Deferred Taxes. ASU 2015-17 requires companies to classify all deferred tax assets and liabilities, along with any valuation allowance, as noncurrent on the balance sheet instead of separating deferred taxes into current and noncurrent amounts. The guidance does not change the existing requirement that only permits offsetting within a jurisdiction. The ASU is effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years. Early adoption is permitted. During the fourth quarter of 2015, the Company elected early adoption of this standard as it improved the efficiency of the year end financial reporting process for income taxes and applied the changes retrospectively to all prior periods presented in its consolidated financial statements. Adoption did not have a material impact to the financial statements.

In February 2016, the FASB issued ASU No. 2016-02, Leases ("ASU 2016-02"). ASU 2016-02 requires lessees to recognize the assets and liabilities on their balance sheet for the rights and obligations created by most leases and continue to recognize expenses on their income statements over the lease term. It will also require disclosures designed to give financial statement users information on the amount, timing, and uncertainty of cash flows arising from leases. The guidance is effective for annual reporting periods beginning after December 15, 2018, and interim periods within those years. Early adoption is permitted for all entities. The Company is currently evaluating the impact of ASU 2016-02.

Other Significant Policies:

The following table identifies the Company's other significant accounting policies and the note and page where a detailed description of each policy can be found.

|

| | | | | |

| Note | 4 |

| Page | |

| | | | |

| Note | 8 |

| Page | |

| | | | |

| Note | 9 |

| Page | |

| | | | |

| Note | 11 |

| Page | |

| | | | |

| Note | 12 |

| Page | |

| | | | |

| Note | 14 |

| Page | |

| | | | |

| Note | 16 |

| Page | |

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Note 3. Business Combinations

On July 7, 2015, the Company executed an asset purchase agreement with GlaxoSmithKline (GSK) whereby the Company acquired GSK's assets associated with the Canadian distribution of the Company's products. With the acquisition, the Company assumed all distribution, sales, marketing, training and support activities for the OmniPod system in Canada through its wholly-owned subsidiary, Insulet Canada Corporation.

The acquisition allows the Company to establish a local presence in Canada that enables it to engage directly with healthcare providers and OmniPod users. The aggregate purchase price of approximately $4.7 million consisted of cash paid at closing, subject to certain adjustments.

The Company has accounted for the acquisition as a business combination. Under business combination accounting, the assets and liabilities were recorded as of the acquisition date, at their respective fair values, and consolidated with the Company. The excess of the purchase price over the fair value of net assets acquired was recorded as goodwill and largely reflects operational synergies complimentary to the existing business. The operating results of GSK Canada have been included in the consolidated financial statements since July 7, 2015, the date the acquisition was completed. These results are not material to our revenues or operating results.

Prior to the acquisition the Company had a pre-existing relationship with GSK. As a result of the acquisition, the pre-existing relationship was settled by Insulet, with Insulet repurchasing the $0.5 million of inventory held by GSK at the date of the asset purchase. The inventory repurchased had been sold to GSK during the second quarter of 2015, however no revenue was recognized by Insulet on these sales given the expectation to repurchase. As the inventory was repurchased at cost, there were no gains or losses associated with this transaction. This transaction was accounted for separately from the business combination.

The table below details the consideration transferred to acquire GSK (in thousands):

|

| | | | |

Cash | | $ | 5,000 |

|

Employment liability transfer fee | | (285 | ) |

Total consideration | | $ | 4,715 |

|

The assets acquired and liabilities assumed were recorded at fair value at date of acquisition as follows:

|

| | | | |

Goodwill | | $ | 2,403 |

|

Contractual relationships | | 2,100 |

|

Inventory step up | | 230 |

|

Assumed liabilities | | (18 | ) |

| | $ | 4,715 |

|

During the year ended December 31, 2015, the Company incurred transaction costs of $0.1 million, consisting primarily of legal fees, which have been recorded as general and administrative expenses. The Company determined that there was no value to the reacquisition of the Canada exclusivity contract due to the contribution charges of the contractual relationships.

Note 4. Fair Value Measurements

The Company adopted the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 820, Fair Value Measurements and Disclosures (“ASC 820”) related to the fair value measurement of certain of its assets and liabilities. ASC 820 defines fair value as the price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. A single estimate of fair value results from a complex series of judgments about future events and uncertainties and relies heavily on estimates and assumptions. When estimating fair value, depending on the nature and complexity of the asset or liability, the Company may use one or all of the following approaches:

| |

• | Market approach, which is based on market prices and other information from market transactions involving identical or comparable assets or liabilities. |

| |

• | Cost approach, which is based on the cost to acquire or construct comparable assets less an allowance for functional and/or economic obsolescence. |

| |

• | Income approach, which is based on the present value of the future stream of net cash flows. |

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

To measure fair value, the Company uses the following fair value hierarchy based on three levels of inputs, as described in ASC 820, of which the first two are considered observable and the last unobservable:

Level 1 — quoted prices in active markets for identical assets or liabilities

Level 2 — observable inputs other than quoted prices in active markets for identical assets or liabilities

Level 3 — unobservable inputs in which there is little or no market data available, which require the reporting entity to develop its own assumptions

Certain of the Company’s financial instruments, including cash and cash equivalents, accounts receivable, accounts payable, accrued expenses and other liabilities are carried at cost, which approximates their fair value because of the short-term maturity of these financial instruments.

The following table provides a summary of assets that are measured at fair value as of December 31, 2015 and 2014, aggregated by the level in the fair value hierarchy within which those measurements fall (in thousands): |

| | | | | | | | | | | | | | | |

| Fair Value Measurements |

| Total | | Level 1 | | Level 2 | | Level 3 |

December 31, 2015 | | | | | | | |

Recurring Fair Value Measurements: | | | | | | | |

Cash Equivalents - Money Market Funds | $ | 98,223 |

| | $ | 98,223 |

| | $ | — |

| | $ | — |

|

Non-Recurring Fair Value Measurements: | | | | | | | |

Long-lived assets from discontinued operations(1) | $ | 1,800 |

| | $ | — |

| | $ | — |

| | $ | 1,800 |

|

December 31, 2014 | | | | | | | |

Recurring Fair Value Measurements: | | | | | | | |

Cash Equivalents - Money Market Funds | $ | 123,141 |

| | $ | 123,141 |

| | $ | — |

| | $ | — |

|

| |

(1) | Long-lived assets from discontinued operations relate to the asset group of the Neighborhood Diabetes business which consists of definite lived intangible assets and property and equipment, presented in long-term assets of discontinued operations on the balance sheet. During the fourth quarter, the Company recognized an impairment charge on this asset group totaling $9.1 million, which represented the difference between the fair value of the asset group and the carrying value and is presented as part of discontinued operations. As a result of the impairment the asset group has been recorded at fair value as of December 31, 2015. The fair value for the asset group was determined using the direct cash flows expected to be received from the disposition of the asset group, which was completed in February 2016 (level 3 input). |

Debt

The estimated fair value of debt is based on the Level 1 quoted market prices for the same or similar issues and included the impact of the conversion features.

The carrying amounts and the estimated fair values of financial instruments as of December 31, 2015 and 2014, are as follows (in thousands):

|

| | | | | | | | | | | | | | | |

| December 31, 2015 | | December 31, 2014 |

| Carrying Value | | Estimated Fair Value | | Carrying

Value | | Estimated Fair

Value |

2% Convertible Senior Notes | $ | 171,698 |

| | $ | 207,882 |

| | $ | 164,020 |

| | $ | 237,475 |

|

The Company issued $201.3 million in principal amount of 2% Notes (as defined below) in June 2014. The carrying value of the 2% Notes at December 31, 2015 includes a debt discount of $25.7 million which is being amortized as non-cash interest expense over the term of the 2% Notes. The decrease in the estimated fair values of these liabilities from December 31, 2014 to 2015 represents the impact of the quoted bond prices at those dates.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Note 5. Debt

The Company had outstanding convertible debt and related deferred financing costs on its consolidated balance sheet as follows (in thousands):

|

| | | | | | | |

| As of |

| December 31,

2015 | | December 31, 2014 |

Principal amount of the 2% Convertible Senior Notes | $ | 201,250 |

| | $ | 201,250 |

|

Unamortized debt discount | (25,704 | ) | | (32,256 | ) |

Deferred financing costs | $ | (3,848 | ) | | $ | (4,974 | ) |

Long-term debt, net of discount | $ | 171,698 |

| | $ | 164,020 |

|

Interest expense related to the 3.75% Notes (as defined below) and the 2% Notes was included in interest and other expense on the consolidated statements of operations as follows (in thousands):

|

| | | | | | | | | | | |

| Years Ended December 31, |

| 2015 | | 2014 | | 2013 |

Contractual coupon interest | $ | 4,025 |

| | $ | 4,657 |

| | $ | 5,704 |

|

Accretion of debt discount | 6,552 |

| | 8,007 |

| | 10,492 |

|

Amortization of debt issuance costs | 1,126 |

| | 895 |

| | 590 |

|

Loss on extinguishment of long-term debt | — |

| | 23,203 |

| | 325 |

|

Total interest and other expense | $ | 11,703 |

| | $ | 36,762 |

| | $ | 17,111 |

|

3.75% Convertible Senior Notes

In June 2011, the Company sold $143.8 million in principal amount of 3.75% Convertible Senior Notes due June 15, 2016 (the "3.75% Notes"). The interest rate on the notes was 3.75% per annum, payable semi-annually in arrears in cash on December 15 and June 15 of each year. The 3.75% Notes were convertible into the Company’s common stock at an initial conversion rate of 38.1749 shares of common stock per $1,000 principal amount of the 3.75% Notes, which was equivalent to a conversion price of approximately $26.20 per share.

In connection with the issuance of the 3.75% Notes, the Company repurchased $70 million in principal amount of its 5.375% Convertible Senior Notes due June 15, 2013 (the "5.375% Notes") for $85.1 million, a 21.5% premium on the principal amount. The investors that held the $70 million in principal amount of repurchased 5.375% Notes purchased $59.5 million in principal amount of the 3.75% Notes and retained approximately $13.5 million in principal amount of the remaining 5.375% Notes. These investors’ combined $73.0 million in principal amount of convertible debt ($13.5 million of 5.375% Notes and $59.5 million of 3.75% Notes) was considered to be a modification of a portion of the 5.375% Notes and was accounted for separately from the issuance of the remainder of the 3.75% Notes.

The Company recorded a total debt discount of $25.8 million related to the modified debt. This discount consisted of $10.5 million related to the remaining debt discount on the $70 million in principal amount of 5.375% Notes repurchased, $15.1 million related to the premium payment in connection with the repurchase and $0.2 million related to the increase in the value of the conversion feature. The total debt discount was being amortized as non-cash interest expense at the effective rate of 16.5% over the five year term of the modified debt. Additionally, the Company paid transaction fees of approximately $2.0 million related to the modification, which were recorded as interest and other expense at the time of the modification.

As of December 31, 2013, the 5.375% Notes were repaid in full and no amounts remained on the Company's balance sheet related to these notes.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Of the $143.8 million in principal amount of 3.75% Notes issued in June 2011, $84.3 million in principal amount was considered to be an issuance of new debt. The Company recorded a debt discount of $26.6 million related to the $84.3 million in principal amount of 3.75% Notes. The debt discount was recorded as additional paid-in capital to reflect the value of its nonconvertible debt borrowing rate of 12.4% per annum and was being amortized as non-cash interest expense over the five year term of the 3.75% Notes. The Company incurred deferred financing costs related to this offering of approximately $2.8 million, of which $0.9 million has been reclassified as an offset to the value of the amount allocated to equity. The remainder was recorded as other assets in the consolidated balance sheet and was being amortized as non-cash interest expense over the five year term of the 3.75% Notes.

In June 2014, in connection with the issuance of $201.3 million in principal amount of 2% Convertible Senior Notes due June 15, 2019 (the “2% Notes”), the Company repurchased approximately $114.9 million in principal amount of the 3.75% Notes for $160.7 million, a premium of $45.8 million over the principal amount. Investors that held approximately $80.0 million of 3.75% Notes purchased approximately $98.2 million in principal amount of the 2% Notes. The repurchase of the 3.75% Notes was treated as an extinguishment of debt since the fair value of the conversion feature changed by more than 10%. The extinguishment of the 3.75% Notes was accounted for separately from the issuance of the 2% Notes. The $160.7 million paid to extinguish the debt was allocated to debt and equity based on their respective fair values immediately prior to the transaction. The Company allocated $112.4 million of the payment to the debt and $48.3 million to equity.

The 3.75% Notes were convertible at the option of the holder during the quarter ended June 30, 2014 since the last reported sales price per share of the Company's common stock was equal to or greater than 130% of the conversion price for at least 20 of the 30 trading days ended on March 31, 2014. The 3.75% Notes and any unpaid interest were convertible at the Company’s option for cash, shares of the Company’s common stock or a combination of cash and shares of the Company’s common stock.

Beginning on June 20, 2014, the Company had the right to redeem the 3.75% Notes, at its option, in whole or in part, if the last reported sale price per share of the Company’s common stock was at least 130% of the conversion price then in effect for at least 20 trading days during a period of 30 consecutive trading days. In June 2014, the Company met the redemption requirements and notified holders of its intent to redeem the outstanding $28.8 million in principal amount of 3.75% Notes in July 2014. Prior to the redemption date, holders of $28.5 million in principal amount of 3.75% Notes exercised their right to convert their outstanding 3.75% Notes. The Company settled this conversion of the 3.75% Notes in July 2014 by providing cash of $28.5 million for the principal amount of the outstanding 3.75% Notes converted and issuing 348,535 shares of common stock for the conversion premium totaling $12.6 million, for a total consideration paid of $41.1 million. The Company settled the redemption of the remaining $0.3 million in principal amount in exchange for a cash payment of $0.3 million representing principal and accrued and unpaid interest. The Company allocated $27.9 million of the total consideration paid to the debt and $13.5 million to equity.

The Company recorded a loss on extinguishment of debt of $23.2 million in connection with the repurchase and redemption of the 3.75% Notes during the year ended December 31, 2014, representing the excess of the $140.3 million allocated to the debt over its carrying value, net of deferred financing costs.

Certain features related to a portion of the 3.75% Notes, including the holders’ ability to require the Company to repurchase their notes and the higher interest payments required in an event of default, were considered embedded derivatives and were required to be bifurcated and accounted for at fair value. The Company assessed the value of these embedded derivatives at each balance sheet date.

No cash interest expense was recorded related to the 3.75% Notes in the year ended December 31, 2015. Cash interest expense related to the 3.75% Notes outstanding was $2.4 million and $5.4 million in the years ended December 31, 2014 and 2013, respectively. There was no non-cash interest expense recorded in the year ended December 31, 2015 related to the 3.75% Notes, compared to $4.9 million and $10.8 million in years ended December 31, 2014 and 2013, respectively.

As of December 31, 2014, no amounts remain outstanding related to the 3.75% Notes.

2% Convertible Senior Notes

In June 2014, the Company sold $201.3 million in principal amount of the 2% Notes due June 15, 2019. The interest rate on the notes is 2% per annum, payable semi-annually in arrears in cash on June 15 and December 15 of each year. The 2% Notes are convertible into the Company’s common stock at an initial conversion rate of 21.5019 shares of common stock per $1,000 principal amount of the 2% Notes, which is equivalent to a conversion price of approximately $46.51 per share, subject to adjustment under certain circumstances.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The Company recorded a debt discount of $35.6 million related to the 2% Notes. The debt discount was recorded as additional paid-in capital to reflect the value of the Company’s nonconvertible debt borrowing rate of 6.2% per annum. This debt discount is being amortized as non-cash interest expense over the five year term of the 2% Notes. The Company incurred deferred financing costs related to this offering of approximately $6.7 million, of which $1.2 million has been reclassified as an offset to the value of the amount allocated to equity. The remainder is recorded as a reduction to debt in the consolidated balance sheet and is being amortized as non-cash interest expense over the five year term of the 2% Notes.

The 2% Notes contain provisions that allow for additional interest to the holders of the Notes upon the failure to timely file documents or reports that the Company is required to file with the SEC. The additional interest is at a rate of 0.25% per annum of the principal amount of the notes outstanding for the first 180 days and 0.50% per annum of the principal amount of the notes outstanding for a period up to 360 days.

If the Company is purchased by a company outside of the US, then additional taxes may be required to be paid by the Company under the terms of the 2% Notes.

The Company determined that the higher interest and tax payments required in certain circumstances are considered embedded derivatives and should be bifurcated and accounted for at fair value. The Company assesses the value of the embedded derivatives at each balance sheet date. The derivatives had de minimis value at the balance sheet date.

Cash interest expense related to the 2% Notes was $4.0 million and $2.3 million in the years ended December 31, 2015 and 2014, respectively. Non-cash interest expense related to the 2% Notes was $7.7 million and $4.0 million in the years ended December 31, 2015 and 2014, respectively.

As of December 31, 2015, the Company included $171.7 million on its balance sheet in long-term debt related to the 2% Notes.

Note 6. Capital Lease Obligations

As of December 31, 2015 and 2014, the Company has approximately $13.7 million and $8.0 million of manufacturing equipment acquired under capital leases, included in property and equipment, respectively. The obligations under the capital leases are being repaid in equal monthly installments over 24 to 36 month terms and include principal and interest payments with an effective interest rate of 13% to 17%.

The assets acquired under capital leases are being amortized on a straight-line basis over 5 years in accordance with the Company's policy for depreciation of manufacturing equipment. Amortization expense on assets acquired under capital leases is included with depreciation expense. Amortization expense related to these capital leased assets was $2.5 million, $1.3 million and $0.6 million in the years ended December 31, 2015, 2014 and 2013, respectively.

Assets held under capital leases consist of the following (in thousands):

|

| | | | | | | |

| As of |

| December 31, 2015 | | December 31, 2014 |

Manufacturing equipment | $ | 13,705 |

| | $ | 7,984 |

|

Less: Accumulated amortization | (4,346 | ) | | (1,885 | ) |

Total | $ | 9,359 |

| | $ | 6,099 |

|

The aggregate future minimum lease payments related to these capital leases as of December 31, 2015, are as follows (in thousands): |

| | | |

Years Ending December 31, | Minimum Lease Payments |

2016 | $ | 5,874 |

|

2017 | 269 |

|

Total future minimum lease payments | $ | 6,143 |

|

Interest expense | (355 | ) |

Total capital lease obligations | $ | 5,788 |

|

The Company recorded $1.2 million of interest expense on capital leases in the years ended December 31, 2015 and 2014, and $0.4 million of interest expense on capital leases in 2013.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Note 7. Net Loss Per Share

Basic net loss per share is computed by dividing net loss by the weighted average number of common shares outstanding for the period, excluding unvested restricted common shares. Diluted net loss per share is computed using the weighted average number of common shares outstanding and, when dilutive, potential common share equivalents from options, restricted stock units and warrants (using the treasury-stock method), and potential common shares from convertible securities (using the if-converted method). Because the Company reported a net loss from both continuing and discontinued operations for the years ended December 31, 2015, 2014 and 2013, all potential dilutive common shares have been excluded from the computation of the diluted net loss per share for all periods presented, as the effect would have been anti-dilutive.

Potential dilutive common share equivalents consist of the following: |

| | | | | | | |

| Years Ended December 31, |

| 2015 | | 2014 | 2013 |

3.75% Convertible Senior Notes | — |

| | — |

| 5,487,642 |

|

2.00% Convertible Senior Notes | 4,327,257 |

| | 4,327,257 |

| — |

|

Unvested restricted stock units | 811,965 |

| | 746,612 |

| 1,011,893 |

|

Outstanding options | 2,999,199 |

| | 1,847,669 |

| 1,828,613 |

|

Total dilutive common shares | 8,138,421 |

| | 6,921,538 |

| 8,328,148 |

|

Note 8. Accounts Receivable

Accounts receivable consist of amounts due from third-party payors, patients, third-party distributors and government agencies. The Company records an allowance for doubtful accounts at the time potential collection risk is identified. The Company estimates its allowance based on historical experience, assessment of specific risk, discussions with individual customers or various assumptions and estimates that are believed to be reasonable under the circumstances. The Company believes the reserve is adequate to mitigate current collection risk.

Accounts receivable from two customers represented approximately 22% and 19% of gross accounts receivable as of December 31, 2015, respectively. As of December 31, 2014 accounts receivable from two customers represented approximately 22% and 12% of gross accounts receivable, respectively.

The components of accounts receivable related to continuing operations are as follows (in thousands): |

| | | | | | | |

| As of |

December 31,

2015 | | December 31, 2014 |

Trade receivables | $ | 46,668 |

| | $ | 40,121 |

|

Allowance for doubtful accounts | (4,138 | ) | | (4,878 | ) |

Total accounts receivable | $ | 42,530 |

| | $ | 35,243 |

|

Refer to footnote 18 for accounts receivable related to discontinued operations.

Note 9. Inventories

Inventories are held at the lower of cost or market, determined under the first-in, first-out method. Inventory has been recorded at cost as of December 31, 2015 and 2014. Work in process is calculated based upon a buildup in the stage of completion using estimated labor inputs for each stage in production. The Company periodically reviews inventories for net realizable value based on quantities on hand and expectations of future use.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Inventories related to continuing operations consist of the following (in thousands): |

| | | | | | | |

| As of |

December 31,

2015 | | December 31, 2014 |

Raw materials | $ | 632 |

| | $ | 853 |

|

Work-in-process | 1,960 |

| | 254 |

|

Finished goods, net | 9,432 |

| | 10,343 |

|

Total inventories | $ | 12,024 |

| | $ | 11,450 |

|

Refer to footnote 18 for inventories related to discontinued operations, which are fully comprised of finished goods.

Note 10. Property and Equipment

Property and equipment related to continuing operations consist of the following (in thousands):

|

| | | | | | | | | |

| Estimated Useful Life (Years) | | As of December 31, |

| 2015 | | 2014 |

Machinery and equipment | 2-5 | | $ | 49,059 |

| | $ | 35,690 |

|

Lab equipment | 2-3 | | 1,615 |

| | 1,585 |

|

Computers | 3 | | 2,067 |

| | 3,937 |

|

Software | 3 | | 2,566 |

| | 5,399 |

|

Office furniture and fixtures | 3-5 | | 1,468 |

| | 1,140 |

|

Leasehold improvement | * | | 927 |

| | 810 |

|

Construction in process | — | | 12,275 |

| | 10,502 |

|

Total property and equipment | | | $ | 69,977 |

| | $ | 59,063 |

|

Less: accumulated depreciation | | | (28,184 | ) | | (22,121 | ) |

Total property and equipment | | | $ | 41,793 |

| | $ | 36,942 |

|

* Lesser of lease term or useful life of asset

Property and equipment by geographic location consist of the following (in thousands):

|

| | | | | | | |

| As of December 31, |

| 2015 | | 2014 |

Property and equipment: | | | |

U.S. property and equipment | $ | 19,267 |

| | $ | 21,892 |

|

Non-U.S. property and equipment | 50,710 |

| | 37,171 |

|

Less: accumulated depreciation | (28,184 | ) | | (22,121 | ) |

Total property and equipment | $ | 41,793 |

| | $ | 36,942 |

|

Property and equipment related to discontinued operations were not significant as of December 31, 2015 and 2014.

Depreciation expense related to property and equipment from continuing operations was $11.4 million, $7.7 million, and $6.4 million for the years ended December 31, 2015, 2014 and 2013, respectively. Depreciation expense from discontinued operations was not significant during those same periods. The Company recorded $0.2 million of capitalized interest in the years ended December 31, 2015 and 2014 and $0.3 million of capitalized interest in 2013.

Construction in process mainly consists of infrastructure improvements and internal use software. Depreciation on software does not begin until the assets are integrated into the current systems.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

During the years ended December 31, 2015 and 2014, the Company wrote-off $5.4 million and $19.0 million, respectively, of fully depreciated assets, as the assets were no longer in use. No gain or loss was recognized in the year ended December 31, 2014 related to the write-off of these assets.

Note 11. Other Intangible Assets

The Company’s finite-lived intangible assets are stated at cost less accumulated amortization. The Company assesses its intangible and other long-lived assets for impairment whenever events or changes in circumstances suggest that the carrying value of an asset may not be recoverable. The Company recognizes an impairment loss for intangibles and other finite-lived assets if the carrying amount of a long-lived asset is not recoverable based on its undiscounted future cash flows. Any such impairment loss is measured as the difference between the carrying amount and the fair value of the asset. The estimation of useful lives and expected cash flows requires the Company to make significant judgments regarding future periods that are subject to some factors outside its control. Changes in these estimates can result in significant revisions to the carrying value of these assets and may result in material charges to the results of operations.

The Company recorded $32.9 million of other intangible assets as a result of the acquisition of Neighborhood Diabetes in 2011. In December 2015, the Company completed a long-lived asset impairment test for Neighborhood Diabetes and determined that the carrying value of the long-lived asset group, which included intangible assets, exceeded the undiscounted cash flows expected to be generated from the asset group. The Company compared the fair value of the intangible assets and the related asset group, which was estimated based on the subsequent sales price of the asset group as of February 2016. As a result, an impairment charge of $9.0 million was recorded within discontinued operations for the year ended December 31, 2015. The impairment charge was allocated on pro-rata basis based on the carrying value of the assets within the asset group. As a result, impairment charges of approximately $7.4 million and $1.6 million, respectively, were recorded on the customer relationship and trade name intangible assets which are included within long-term assets of discontinued operations on the balance sheet.

The Company recorded $2.1 million of other intangible assets in the year ended December 31, 2015 as a result of the July 2015 acquisition of its Canadian distribution business (see Footnote 3 for further description). The Company determined that the estimated useful life of the contractual relationship asset is 5 years and is amortizing the asset over the estimated lives, based on the expected cash flows of the assets, accordingly. The amortization expense of other intangible assets was approximately $1.0 million for the year ended December 31, 2015, which was recorded in general and administration expenses on the statement of operations.

Intangible assets on the balance sheet consist of the following (in thousands): |

| | | | | | | | | | | | | | | | | | | | | | | |

| | As of | | | | |

December 31, 2015 | | December 31, 2014 |

| Gross Carrying Amount | | Accumulated Amortization | | Net Book Value | | Gross Carrying Amount | | Accumulated Amortization | | Net Book Value |

Customer and contractual relationships, net(1) (2) | $ | 3,399 |

| | $ | (1,000 | ) | | $ | 2,399 |

| | $ | 30,100 |

| | $ | (18,167 | ) | | $ | 11,933 |

|

Tradename (3) | 322 |

| | — |

| | 322 |

| | 2,800 |

| | (669 | ) | | 2,131 |

|

Total intangible assets (4) | $ | 3,721 |

| | $ | (1,000 | ) | | $ | 2,721 |

| | $ | 32,900 |

| | $ | (18,836 | ) | | $ | 14,064 |

|

| |

(1) | Includes foreign currency translation loss of approximately $0.2 million. |

| |

(2) | The customer relationships asset includes $1.5 million of both the gross carrying amount and net book value, respectively that are included in long-term assets from discontinued operations on the balance sheet as of December 31, 2015. The full customer relationships balance as of December 31, 2014 is included in long-term assets from discontinued operations on the balance sheet. |

| |

(3) | The tradename asset is included in long-term assets from discontinued operations on the balance sheet as of December 31, 2015 and 2014. |

| |

(4) | As a result of the impairment recorded on the Neighborhood Diabetes asset group, the Company recorded an impairment charge of approximately $9.0 million on the related Neighborhood Diabetes intangible assets, which was recorded through discontinued operations. This resulted in the gross carrying value and accumulated amortization of the Neighborhood Diabetes intangibles being reduced by $31.1 million and $22.1 million respectively at December 31, 2015. |

Amortization expense was approximately $1.0 million from continuing operations and $3.3 million from discontinued operations for the year ended December 31, 2015. Amortization expense from discontinued operations was approximately $4.0 million and $4.9 million for the years ended December 31, 2014 and 2013,

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

respectively. There was no amortization expense from continuing operations in the years ended December 31, 2014 and 2013, respectively.

Amortization expense expected for the next five years and thereafter from continuing operations is as follows (in thousands):

|

| | | |

| Amortization Expense |

Years Ending December 31, | Customer and Contractual Relationships |

2016 | $ | 421 |

|

2017 | 175 |

|

2018 | 150 |

|

2019 | 125 |

|

2020 | 62 |

|

Thereafter | — |

|

Total | $ | 933 |

|

As of December 31, 2015, the weighted average amortization period of the Company’s intangible assets from continuing operations is approximately 5.0 years.

Note 12. Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities related to continuing operations consist of the following (in thousands):

|

| | | | | | | |

| Years Ended December 31, |

| 2015 | | 2014 |

Employee compensation and related items | $ | 16,856 |

| | $ | 9,521 |

|

Professional and consulting services | 5,654 |

| | 3,650 |

|

Sales and use tax | 1,163 |

| | 268 |

|

Supplier charges | 4,981 |

| | 1,201 |

|

Warranty | 1,592 |

| | 981 |

|

Other | 6,498 |

| | 3,229 |

|

Total accrued expenses and other current liabilities | $ | 36,744 |

| | $ | 18,850 |

|

Product Warranty Costs

The Company provides a four-year warranty on its PDMs sold in the United States and a five-year warranty on its PDMs sold in Canada and may replace any OmniPods that do not function in accordance with product specifications. The Company estimates its warranty at the time the product is shipped based on historical experience and the estimated cost to service the claims. Warranty expense is recorded in cost of goods sold on the statement of operations. Cost to service the claims reflects the current product cost which has been decreasing over time. As these estimates are based on historical experience, and the Company continues to introduce new products and versions, the Company also considers the anticipated performance of the product over its warranty period in estimating warranty reserves.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

A reconciliation of the changes in the Company’s product warranty liability is as follows (in thousands):

|

| | | | | | | |

| Years Ended December 31, |

| 2015 | | 2014 |

Balance at the beginning of the period | $ | 2,614 |

| | $ | 3,090 |

|

Warranty expense | 4,964 |

| | 1,665 |

|

Warranty claims settled | (3,426 | ) | | (2,141 | ) |

Balance at the end of the period | $ | 4,152 |

| | $ | 2,614 |

|

|

| | | | | | | |

| As of |

| December 31,

2015 | | December 31,

2014 |

Composition of balance: | | | |

Short-term | $ | 1,592 |

| | $ | 981 |

|

Long-term | 2,560 |

| | 1,633 |

|

| $ | 4,152 |

| | $ | 2,614 |

|

Note 13. Commitments and Contingencies

Operating Leases

The Company leases its facilities in Massachusetts, New York, Florida, Canada and Singapore. The Company’s leases are accounted for as operating leases. The leases generally provide for a base rent plus real estate taxes and certain operating expenses related to the leases.

In 2013, the Company entered into a new lease agreement for approximately 90,000 square feet of laboratory and office space for its corporate headquarters in Billerica, Massachusetts. The lease term began in August 2014 and expires in November 2022 and contains escalating payments over the life of the lease. In 2015, the Company extended its Singapore lease which now expires in July 2016. In 2014, the Company amended its existing lease for warehouse space in Billerica, Massachusetts which extended the term and increased the approximate square footage under the lease. The lease now expires in September 2019. In the second quarter of 2015, the Company entered into a new lease agreement of office space in Ontario, Canada. The lease term began in June 2015 and expires in May 2018.

Certain of the Company’s operating lease agreements contain scheduled rent increases. Rent expense is recorded using the straight-line method and deferred rent is included in other liabilities in the accompanying balance sheets. The Company has considered FASB ASC 840-20, Leases in accounting for these lease provisions.

The aggregate future minimum lease payments related to these leases from continuing operations as of December 31, 2015, are as follows (in thousands):

|

| | | |

Years Ending December 31, | Minimum Lease Payments |

2016 | $ | 2,141 |

|

2017 | 2,178 |

|

2018 | 2,160 |

|

2019 | 2,169 |

|

2020 | 2,146 |

|

Thereafter | 3,934 |

|

Total | $ | 14,728 |

|

Minimum future lease payments for discontinued operations are not significant.

Legal Proceedings

The Company is in the process of responding to a revised audit report received in December 2015 on behalf of the Centers for Medicare and Medicaid Services and the State of New York alleging overpayment of certain Medicaid claims to Neighborhood Diabetes.

INSULET CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The Company is in the process of responding to a draft audit report received in June 2015 from the Connecticut Department of Social Services Office of Quality Assurance alleging overpayment of certain Medicaid claims to Neighborhood Diabetes.