Exhibit 10(d)

/$CurrentDate$/

ACUITY INC. (previously known as Acuity Brands, Inc.)

Amended and Restated 2012 Omnibus Stock Incentive Compensation Plan

Amended and Restated 2012 Omnibus Stock Incentive Compensation Plan

Global Performance Unit Notification and Award Agreement

(rTSR Performance Award)

Grantee: Grant Type: Grant ID: Grant Date: Target Award Amount: Maximum Award Amount: Performance Period Service Period: Grantee Level: Accept by Date: | /$ParticipantName$/ /$GrantType$/ /$GrantID$/ /$GrantDate$/ /$AwardsGranted$/ Up to 200% of the Target Award Amount Three-Year Period Comprised of Fiscal Years 2025, 2026 and 2027 Three-Year Cliff Vest on October 24, 2027 /$UserCode2$/ for Stock Ownership Guidelines (Exhibit A) /$AcceptByDate$/ | ||||

WHEREAS, Acuity Inc. (the “Company”) maintains the Amended and Restated Acuity, Inc. 2012 Omnibus Stock Incentive Compensation Plan (the “Plan”) under which the Compensation Committee of the Company’s Board of Directors (the “Committee”) has authority to grant Performance Units; and

WHEREAS, the Committee has determined that it is in the best interest of the Company and its stockholders to grant this Performance Unit Award to the Grantee identified above, subject to the terms and conditions set forth in the Plan and this Global Performance Unit Notification and Award Agreement, together with its exhibits (the “Agreement”).

NOW, THEREFORE, in consideration of the mutual covenants hereinafter set forth, the parties agree as follows:

1.Incorporation of the Plan. The provisions of the Plan are hereby incorporated by reference. Except as otherwise expressly set forth herein, this Agreement shall be construed in accordance with the provisions of the Plan and any capitalized terms not otherwise defined in this Agreement shall have the definitions set forth in the Plan. In the event of any conflict between the terms of the Plan and the terms of this Agreement, the terms of the Plan shall prevail. The Committee has final authority to interpret and construe the Plan and this Agreement and to make any and all determinations under them, and its decision shall be binding and conclusive upon Grantee and Grantee’s legal representative with respect to any questions arising under the Plan or this Agreement.

2.Grant of Performance Unit Award. The Committee, on behalf of the Company, hereby grants to Grantee, effective as of the Grant Date, Performance Units equal to the Target Award Amount set forth above, on the terms and conditions set forth in this Agreement, including the specific vesting requirements set forth above and the performance goal requirements (the “Performance Goals”) set forth in Exhibit B attached hereto, and as otherwise provided in the Plan. The actual number of Performance Units earned pursuant to the Award will

-1-

Exhibit 10(d)

be determined based on the achievement of the Performance Goals during the Performance Period, as further set forth in Exhibit B.

3.Acceptance of Performance Unit Award. This award of Performance Units is conditioned upon Grantee’s acceptance of the terms of this Agreement, as evidenced by Grantee’s execution of this Agreement or by Grantee’s electronic acceptance of this Agreement in a manner and during the time period allowed by the Company. If the terms of this Agreement are not timely accepted by execution or by such electronic means, the award of Performance Units may be cancelled.

4.Performance Goals. Exhibit B attached hereto sets forth the Performance Goals that must be satisfied in order for the Performance Units to be eligible to vest, subject to Grantee’s satisfaction of the Service Period, except as otherwise set forth in Section 5. The Committee shall certify the extent to which the Performance Goals have been achieved with such certification occurring as soon as practicable following the end of the Performance Period and in any event no later than ninety (90) days following the end of such Performance Period (such certification occurring on the “Certification Date”). Except as set forth in Section 5, any Performance Units for which the Performance Goals have not been achieved shall be automatically forfeited, terminated and cancelled effective as of the applicable Certification Date, without the payment of any consideration by the Company, and Grantee, or Grantee’s beneficiary or personal representative, as the case may be, shall have no further rights with respect to such forfeited Performance Units under the Agreement.

5.Vesting of Performance Unit Award.

a)In General. Provided that Grantee remains continuously employed by the Company, a Subsidiary or Affiliate through the last day of the Service Period (the “Vesting Date”), this Performance Unit Award shall vest to the extent that the Performance Goals have been achieved, as determined by the Committee on the Certification Date. For purposes of this Agreement, providing active services as an Employee or as a member of the Board shall be considered as employment.

b)Vesting Acceleration Upon Termination due to Death or Disability. Notwithstanding Section 5(a) above, if prior to the Vesting Date, (i) Grantee dies while actively employed by the Company or a Subsidiary or Affiliate, or (ii) Grantee’s employment terminates by reason of Grantee’s Disability, any Performance Units shall become fully vested and non-forfeitable as of the date of Grantee’s death or Disability in an amount equal to the Target Award Amount; provided, however, that if Grantee’s Termination due to Grantee’s death or Disability occurs after the end of the Performance Period, the Performance Units shall become fully vested and non-forfeitable in an amount equal to the number of Performance Units actually earned, as determined by the Committee on the Certification Date.

c)Vesting Following Termination with Tenure. Notwithstanding Section 5(a) above, if Grantee’s employment terminates for a reason other than Cause on or after the date on which the number of completed years of Grantee’s continuous service to the Company or a Subsidiary or Affiliate is at least five (5) (“Tenure”), the Performance Units will remain outstanding and will remain available to vest on a pro rata basis (as described below) at the end of the Service Period set forth above and subject to the terms set forth in this Agreement, including Exhibit B attached hereto, as though Grantee had remained employed, and once vested, will be settled in accordance with Section 7 below; provided, however, that any unvested Performance Units will be forfeited immediately, automatically and without consideration upon Grantee’s breach of the confidentiality, inventions, non-solicitation and non-competition provisions attached hereto as Exhibit D (as determined by the Committee). The pro-rata portion of the Performance Units that will remain outstanding and available to vest following Grantee’s termination with Tenure will be calculated based on the ratio of (x) each full year worked by Grantee from the Grant Date to Grantee’s Date of Termination (as defined below), to (y) the total number of years in the Service Period. The Company, in its sole discretion, will determine whether Grantee has completed five (5) years of continuous service, including the effect of any break-in-service.

-2-

Exhibit 10(d)

d)Termination of Service for Any Other Reason. Except for death, Termination due to Disability or Termination with Tenure, as provided in Sections 5(b) and (c) above, or except as otherwise provided in a duly approved severance agreement with Grantee, if Grantee terminates his or her employment or if the Company or if different, the Subsidiary or Affiliate employing Grantee (the “Employer”) terminates Grantee’s employment prior to the Vesting Date (even in the case of unfair dismissal and whether or not later to be found invalid or in breach of applicable laws in the jurisdiction where Grantee is employed or the terms of Grantee’s employment agreement, if any) Grantee expressly acknowledges that the Performance Units shall cease to vest further and that the Performance Units shall be immediately forfeited as of the Date of Termination. “Date of Termination” means the last day of Grantee’s active employment with the Employer. For greater certainty, Grantee’s Date of Termination shall be deemed to be the date on which the notice of termination of employment provided is stated to be effective (and in the case of alleged constructive dismissal, the date on which the alleged constructive dismissal is alleged to have occurred), and not during or as of the end of any notice or other period following such date during which Grantee is in receipt of, or eligible to receive, statutory, contractual or common law notice of termination or any compensation in lieu of such notice or severance pay. The Company shall have the exclusive discretion to determine when Grantee is no longer actively providing services for purposes of the Performance Unit grant (including whether Grantee may still be considered to be providing services while on a leave of absence).

e)Vesting Acceleration Upon a Change in Control. Notwithstanding the other provisions of this Agreement, in the event of a Change in Control prior to the Vesting Date, all Performance Units shall become fully vested and non-forfeitable as of the date of the Change in Control in an amount equal to the Target Award Amount; provided, however, that if the Change in Control occurs after the end of the Performance Period, the Performance Units shall become fully vested and non-forfeitable in an amount equal to the number of Performance Units actually earned, as determined by the Committee on the Certification Date.

6.Dividend Equivalents. During the period that Grantee holds Performance Units granted pursuant to this Agreement, on each date that the Company pays a cash dividend to holders of its Common Stock, the Company shall credit to a non-interest bearing account on its books for Grantee an unvested amount equal to the United States (“U.S.”) Dollar amount paid per share of Common Stock for each Performance Unit initially granted pursuant to this Agreement (the “Dividend Equivalents”). The Dividend Equivalents credited to Grantee’s non-interest bearing account shall vest only to the extent that the Performance Units vest and, except as otherwise provided in Section 5, only with respect to the number of Performance Units actually earned, based on achievement of the Performance Goals. Any such vested Dividend Equivalents shall be paid in accordance with Section 7 below. The Dividend Equivalents shall be forfeited in the event that the Performance Units are forfeited.

7.Issuance of Shares upon Vesting. No Shares shall be issued to Grantee prior to the date that the Performance Units vest pursuant to this Agreement. As soon as practical and in any event within sixty (60) days after the date that the Performance Units vest pursuant to Section 5 (or within such longer period as may be permitted under Section 409A upon Grantee’s death), and subject to the Company’s Incentive-Based Compensation Recoupment Policy (described in Section 11 below) and the applicable terms of Exhibit D attached hereto, the Company will cause Shares to be issued to an unrestricted account in Grantee’s name in payment of such vested Performance Units and will cause any Dividend Equivalents attributed to such vested Performance Units to be paid in cash to Grantee or, in the event of death, to Grantee’s heirs, subject to the applicable laws of descent and distribution. Notwithstanding the foregoing, (a) in the event of vesting of the Performance Units upon a Change in Control, the Performance Units and any Dividend Equivalents shall be paid in accordance with Section 14.2 of the Plan, and (b) to the extent that (i) the Performance Units constitute “nonqualified deferred compensation” subject to Section 409A, (ii) Grantee is subject to U.S. federal taxation and (iii) the aforementioned sixty (60) day period spans two calendar years, the Performance Units and any Dividend Equivalents will be paid in the second of such calendar years.

-3-

Exhibit 10(d)

8.Transfer Restrictions. The Performance Units may not be sold, assigned, transferred, pledged, or otherwise encumbered in any manner other than by will or the laws of descent and distribution, unless and until the shares of Common Stock underlying the vested Performance Units have been issued.

9.Stockholder Rights. The Performance Units granted pursuant to this Agreement do not and shall not entitle Grantee to any rights of a stockholder of the Company’s Common Stock. Grantee’s rights with respect to the Performance Units shall remain forfeitable at all times prior to the Vesting Date (or, if later, the Certification Date) or such other date on which the Performance Units vest pursuant to Section 5.

10.Adjustments Upon Specified Events. In the event of a Share Change (as defined in the Plan), the number and class of Shares or other securities that Grantee shall be entitled to, and shall hold, pursuant to this Agreement shall be appropriately adjusted or changed to reflect the Share Change, provided that any such additional Shares or additional or different Shares or securities shall remain subject to the restrictions in this Agreement.

11.Recoupment. All Awards of Performance Units, whether unvested or vested, and any Shares issued or Dividend Equivalents paid on vesting of the Performance Units, shall be subject to the Company’s Incentive-Based Compensation Recoupment Policy, as it may be amended from time to time (the “Recoupment Policy”), such that any Award that was made to a Grantee who is subject to the Recoupment Policy, and any Shares or Dividend Equivalents acquired pursuant to such Award, shall be subject to deduction, clawback or forfeiture, as provided under the Recoupment Policy. Further, the Performance Units, whether unvested or vested, and any Shares issued or Dividend Equivalents paid on vesting of the Performance Units, shall be subject to deduction, clawback or forfeiture to the extent required to comply with any recoupment requirement imposed under applicable laws, rules, regulations or stock exchange listing standards. In order to satisfy any recoupment obligation arising under the Recoupment Policy or otherwise under applicable laws, rules, regulations or stock exchange listing standards, among other things, Grantee expressly and explicitly authorizes the Company to issue instructions, on Grantee’s behalf, to any brokerage firm or stock plan service provider engaged by the Company to hold any Shares, Dividend Equivalents or other amounts acquired pursuant to the Performance Units to re-convey, transfer or otherwise return such Shares, Dividend Equivalents and/or other amounts to the Company upon the Company’s enforcement of the Recoupment Policy. To the extent that this Agreement and the Recoupment Policy conflict, the terms of the Recoupment Policy shall prevail.

12.Compliance with Section 409A of the Code for U.S. Taxpayers. The parties intend that this Agreement and the benefits provided hereunder be exempt from the requirements of Section 409A of the Code (together with any U.S. Department of Treasury regulations and other interpretive guidance issued thereunder, including without limitation any such regulations or other guidance that may be issued after the date hereof, “Section 409A”) to the maximum extent possible, whether pursuant to the short-term deferral exception described in Treasury Regulation Section 1.409A-1(b)(4) or otherwise. However, to the extent that the Performance Units (or any portion thereof) may be subject to Section 409A, the parties intend that this Agreement and such benefits comply with the deferral, payout, and other limitations and restrictions imposed under Section 409A and this Agreement shall be interpreted, operated and administered in a manner consistent with such intent. Notwithstanding any other provision of the Plan or this Agreement, the Committee shall have the right in its sole discretion (without any obligation to do so or to indemnify Grantee or any other person for failure to do so) to adopt such amendments to the Plan or this Agreement, or adopt other policies and procedures (including amendments, policies and procedures with retroactive effect), or take any other actions, as the Committee determines are necessary or appropriate either for the Performance Units to be exempt from the application of Section 409A or to comply with the requirements of Section 409A. Nothing in this Agreement or the Plan shall provide a basis for any person to take action against the Company or any Subsidiary based on matters covered by Section 409A of the Code, including the tax treatment of any amount paid or Performance Units granted under this Agreement, and neither the Company nor any of its Subsidiaries shall under any circumstances have any liability to Grantee or his or her estate or any other party for any taxes, penalties or interest due on amounts paid or payable under this Agreement, including taxes, penalties or interest imposed under Section 409A.

-4-

Exhibit 10(d)

13.Securities Law and other Legal Compliance. Notwithstanding any other provision of the Plan or this Agreement, unless there is an available exemption from any registration, qualification or other legal requirement applicable to the Common Stock, the Company shall not be required to deliver any Common Stock issuable upon settlement of the Performance Units prior to the completion of any registration or qualification of the Common Stock under any local, state, federal or foreign securities or exchange control law or under rulings or regulations of the SEC or of any other governmental regulatory body, or prior to obtaining any approval or other clearance from any local, state, federal or foreign governmental agency, which registration, qualification or approval the Company shall, in its absolute discretion, deem necessary or advisable. Grantee understands that the Company is under no obligation to register or qualify the Common Stock with the SEC or any state, provincial or foreign securities commission or to seek approval or clearance from any governmental authority for the issuance or sale of Common Stock. Further, Grantee agrees that the Company shall have unilateral authority to amend the Plan and this Agreement without Grantee’s consent to the extent necessary to comply with securities or other laws applicable to the issuance of Common Stock.

14.Grantee’s Representation. Grantee represents and warrants that he or she is acquiring the Performance Units and any Shares for investment purposes only, and not with a view to distribution thereof.

15.Confidentiality, Inventions, Non-Solicitation and Non-Competition; Stock Ownership Guidelines. In exchange for receipt of consideration in the form of the Performance Unit award pursuant to this Agreement and other good and valuable consideration, Grantee agrees that he/she shall comply with the confidentiality, inventions, non-solicitation and non-competition provisions attached hereto as Exhibit D. Grantee acknowledges its obligations, if and as applicable to Grantee’s position, described in the Company’s Stock Ownership Guidelines in effect from time to time, as summarized in Exhibit A.

16.Nature of Grant. In accepting the grant, Grantee acknowledges, understands and agrees that:

a)the Plan is established voluntarily by the Company, it is discretionary in nature and may be modified, amended, suspended or terminated by the Company at any time, to the extent permitted by the Plan;

b)the grant of Performance Units is exceptional, voluntary and occasional and does not create any contractual or other right to receive future grants of performance units, or benefits in lieu of performance units, even if performance units have been granted in the past;

c)all decisions with respect to future Performance Units or other grants, if any, will be at the sole discretion of the Company;

d)the Performance Unit grant and Grantee’s participation in the Plan shall not create a right to employment or be interpreted as forming or amending an employment or services contract with the Company and shall not interfere with the ability of the Employer to terminate Grantee’s employment or service relationship (if any);

e)Grantee is voluntarily participating in the Plan;

f)the Performance Units and the Shares subject to the Performance Units, and any related income and value, are not intended to replace any pension rights or compensation;

g)the Performance Units and the Shares subject to the Performance Units, and any related income and value, are not part of normal or expected compensation for any purposes including, but not limited to, calculating any severance, resignation, termination, payment in lieu of notice, redundancy, dismissal, end-of-service payments, holiday pay, bonuses, long-service awards, leave-related payments, pension, retirement, welfare benefits or similar payments;

-5-

Exhibit 10(d)

h)the future value of the underlying Shares is unknown, indeterminable and cannot be predicted with certainty;

i)no claim or entitlement to compensation or damages shall arise from any loss of any right or benefit, or prospective right or benefit, including the forfeiture of Performance Units resulting from the termination of Grantee’s employment or other service relationship (for any reason whatsoever whether or not later found to be invalid or in breach of applicable laws in the jurisdiction where Grantee is employed or the terms of Grantee’s employment agreement, if any) and any forfeiture of Performance Units or recoupment of Shares resulting from the application of the Recoupment Policy or any other forfeiture or recoupment pursuant to Section 11 of this Agreement;

j)unless otherwise agreed with the Company, the Performance Units and Shares subject to the Performance Units, and any related income and value, are not granted as consideration for, or in connection with, the service Grantee may provide as a director of a Subsidiary; and

k)the Company shall not be liable for any foreign exchange rate fluctuation between Grantee’s local currency and the U.S. Dollar that may affect the value of the Performance Units or of any amounts due to Grantee pursuant to the settlement of the Performance Units or the subsequent sale of any Shares acquired upon settlement.

17.Responsibility for Taxes

a)Grantee acknowledges that, regardless of any action taken by the Company or the Employer, the ultimate liability for all income tax, social insurance, payroll tax, fringe benefits tax, payment on account or other tax-related items related to Grantee’s participation in the Plan and legally applicable to Grantee (“Tax-Related Items”), is and remains Grantee’s responsibility and may exceed the amount, if any, actually withheld by the Company or the Employer. Grantee further acknowledges that the Company and/or the Employer (1) make no representations or undertakings regarding the treatment of any Tax-Related Items in connection with any aspect of the Performance Units or the Dividend Equivalents, including, but not limited to, the grant, vesting or settlement of the Performance Units, the subsequent sale of Shares acquired pursuant to such settlement and the receipt or payment of any dividends or any Dividend Equivalents and (2) do not commit to and are under no obligation to structure the terms of the grant or any aspect of the Performance Units or the Dividend Equivalents to reduce or eliminate Grantee’s liability for Tax-Related Items or achieve any particular tax result. Further, if Grantee is subject to Tax-Related Items in more than one jurisdiction, Grantee acknowledges that the Company and/or the Employer (or former employer, as applicable) may be required to withhold or account for Tax-Related Items in more than one jurisdiction.

b)In connection with any relevant taxable or tax withholding event, as applicable, Grantee agrees to make adequate arrangements satisfactory to the Company and/or the Employer to satisfy all Tax-Related Items. In this regard, Grantee authorizes the Company and/or the Employer, or their respective agents, at their discretion, to satisfy any applicable withholding obligations, if any, with regard to all Tax-Related Items by one or a combination of the following:

(i)withholding from Grantee’s wages or other cash compensation payable to Grantee by the Company and/or the Employer; or

(ii)withholding from proceeds of the sale of Shares acquired upon vesting/settlement of the Performance Unit either through a voluntary sale or through a mandatory sale arranged by the Company (on Grantee’s behalf pursuant to this authorization);

(iii)withholding in Shares to be issued pursuant to the Performance Units; or

-6-

Exhibit 10(d)

(iv)any other method of withholding determined by the Company to comply with applicable laws and the Plan.

c)Notwithstanding Section 17(b) above or Section 17(g) below, if Grantee is subject to the reporting requirements of Section 16(a) of the Exchange Act, then any applicable withholding obligations will be satisfied by withholding in Shares to be issued pursuant to the Performance Units, unless such withholding is not feasible under applicable tax or securities law or has materially adverse accounting consequences, in which case, the Company may satisfy any withholding obligations for Tax-Related Items in accordance with Section 17(b)(i) or (ii).

d)Subject to Section 16.2 of the Plan, the Company may withhold or account for the Tax-Related Items by considering statutory withholding amounts or other applicable withholding rates in Grantee’s jurisdiction(s), including (i) maximum applicable rates, in which case Grantee may receive a refund of any over-withheld amount in cash (whether from applicable tax authorities or the Company) and will have no entitlement to the Common Stock equivalent or (ii) minimum rates or such other applicable rates, in which case Grantee may be solely responsible for paying any additional Tax-Related Items to the applicable tax authorities or the Employer.

e)If the obligation for Tax-Related Items is satisfied by withholding in Shares, for tax purposes, Grantee is deemed to have been issued the full number of Shares subject to the vested Performance Units, notwithstanding that a number of the Shares is held back solely for the purpose of paying the Tax-Related Items.

f)The Company may refuse to issue or deliver the Shares or the proceeds of the sale of Shares, if Grantee fails to comply with Grantee’s obligations in connection with the Tax-Related Items.

g)To the extent that a withholding obligation for Tax-Related Items arises prior to the Vesting Date or such other vesting event hereunder, the Company may accelerate the vesting of Performance Units to the extent necessary to satisfy such Tax-Related Items in the manner set forth in Section 17(b)(ii) or (iii). However, notwithstanding anything in this Section 17 to the contrary, to the extent that the Performance Units constitute “nonqualified deferred compensation” subject to Section 409A and Grantee is subject to U.S. federal taxation, the number of Shares withheld (or sold on Grantee’s behalf) shall not exceed the number of Shares that equals the liability for Tax-Related Items. For avoidance of doubt, any vesting and settlement of Performance Units effected to cover Tax-Related Items pursuant to this Section 17(g) shall apply only to the applicable number of Performance Units and not to any associated Dividend Equivalents thereon, which shall remain subject to vesting on the dates or events set forth in Section 5 and payable pursuant to Section 7 of this Agreement.

18.Data Privacy. Grantee hereby explicitly and unambiguously consents to the collection, use and transfer, in electronic or other form, of Grantee’s personal data as described in this Agreement and any other Performance Unit grant materials by and among, as applicable, the Company and its other Subsidiaries and Affiliates for the exclusive purpose of implementing, administering and managing Grantee’s participation in the Plan.

Grantee understands that the Company holds certain personal information about Grantee, including, but not limited to, Grantee’s name, home address, email address, telephone number, date of birth, social insurance number, passport or other identification number, salary, nationality, job title, any Shares of stock or directorships held in the Company, details of all Performance Units or any other entitlement to Shares awarded, canceled, exercised, vested, unvested or outstanding in Grantee’s favor (“Data”), for the exclusive purpose of implementing, administering and managing the Plan.

Grantee understands that Data will be transferred to Bank of America Merrill Lynch (“Merrill Lynch”), or such other stock plan service provider as may be selected by the Company in the future, which is assisting the Company with the implementation, administration and management of the Plan. Grantee understands that the recipients of the Data may be located in the U.S. or elsewhere, and that the recipients’ country (e.g., the U.S.)

-7-

Exhibit 10(d)

may have different data privacy laws and protections than Grantee’s country. Grantee understands that he or she may request a list with the names and addresses of any potential recipients of the Data by contacting his or her local human resources representative. Grantee authorizes the Company, Merrill Lynch and any other possible recipients which may assist the Company (presently or in the future) with implementing, administering and managing the Plan to receive, possess, use, retain and transfer the Data, in electronic or other form, for the sole purpose of implementing, administering and managing his or her participation in the Plan. Grantee understands that Data will be held only as long as is necessary to implement, administer and manage Grantee’s participation in the Plan. Grantee understands he or she may, at any time, view Data, request information about the storage and processing of Data, require any necessary amendments to Data or refuse or withdraw the consents herein, in any case without cost, by contacting in writing his or her local human resources representative. Further, Grantee understands that he or she is providing the consents herein on a purely voluntary basis. If Grantee does not consent, or if Grantee later seeks to revoke his or her consent, his or her employment status will not be adversely affected; the only consequence of refusing or withdrawing Grantee’s consent is that the Company would not be able to grant Performance Units or other equity awards to Grantee or administer or maintain such awards. Therefore, Grantee understands that refusing or withdrawing his or her consent may affect Grantee’s ability to participate in the Plan. For more information on the consequences of Grantee’s refusal to consent or withdrawal of consent, Grantee understands that he or she may contact his or her local human resources representative.

19.No Advice Regarding Grant. The Company is not providing any tax, legal or financial advice, nor is the Company making any recommendations regarding Grantee’s participation in the Plan, or Grantee’s acquisition or sale of the underlying Shares. Grantee should consult with his or her own personal tax, legal and financial advisors regarding his or her participation in the Plan before taking any action related to the Plan.

20.Insider Trading/Market Abuse Restrictions. Grantee may be subject to insider trading restriction and/or market abuse laws in applicable jurisdictions including, but not limited to, the U.S. and Grantee’s country of residence, which may affect Grantee’s ability to accept, acquire sell or otherwise dispose of Shares or rights to Shares (e.g., Performance Units) or rights linked to the value of Shares during such times as Grantee is considered to have “inside information” regarding the Company (as defined by the laws in the applicable jurisdictions). Any restrictions under these laws or regulations are separate from and in addition to any restrictions that may be imposed under any applicable Company insider trading policy. Grantee is responsible for ensuring Grantee’s own compliance with any applicable restrictions and is advised to speak with his or her personal legal advisor on this matter.

21.Foreign Asset / Account or Tax Reporting; Exchange Control. Grantee acknowledges that there may be certain exchange control, foreign asset/account, or tax reporting requirements which may affect Grantee’s ability to acquire or hold Shares acquired under the Plan or cash received from participating in the Plan (including from any dividends or Dividend Equivalents) in a brokerage or bank account outside Grantee’s country. Grantee may be required to report such accounts, assets or transactions to the tax or other authorities in his or her country. Grantee also may be required to repatriate sale proceeds or other funds received as a result of Grantee’s participation in the Plan to his or her country through a designated bank or broker within a certain time after receipt. Grantee acknowledges that it is Grantee’s responsibility to be compliant with such regulations, and Grantee should consult his or her personal legal advisor for any details.

22.Electronic Delivery and Participation. The Company may, in its sole discretion, decide to deliver any documents related to current or future participation in the Plan by electronic means. Grantee hereby consents to receive such documents by electronic delivery and agrees to participate in the Plan through an on-line or electronic system established and maintained by the Company or any third party designated by the Company. By Grantee’s execution of this Agreement or acceptance by electronic means and the electronic signature of the Company’s representative, Grantee and the Company agree that this Performance Units is granted under and governed by the terms and conditions of the Plan and this Agreement.

-8-

Exhibit 10(d)

23.Country-Specific Terms and Conditions. Notwithstanding any provisions in this Agreement, the Performance Unit grant shall be subject to any additional terms and conditions set forth in Exhibit C to this Agreement for Grantee’s country. Moreover, if Grantee relocates to one of the countries included in Exhibit C, the additional terms and conditions for such country will apply to Grantee, to the extent the Company determines that the application of such terms and conditions is necessary or advisable for legal or administrative reasons. Exhibit C constitutes part of this Agreement.

24.Language. Grantee acknowledges that he or she is sufficiently proficient in English, or has consulted with an advisor who is sufficiently proficient in English, so as to allow Grantee to understand the terms of this Agreement. Furthermore, if Grantee has received this Agreement or any other document related to the Plan translated into a language other than English and if the meaning of the translated version is different than the English version, the English version will control, unless otherwise required by applicable laws.

25.Imposition of Other Requirements. The Company reserves the right to impose other requirements on Grantee’s participation in the Plan, on the Performance Units and on any Shares acquired under the Plan, to the extent the Company determines it is necessary or advisable for legal or administrative reasons, and to require Grantee to sign any additional agreements or undertakings that may be necessary to accomplish the foregoing.

26.Governing Law and Venue. Except with respect to Exhibit D, the Performance Unit grant and the provisions of this Agreement and the validity, interpretation, construction and performance of same shall be governed by, and subject to, the laws of the State of Delaware, without regard to its conflict of law provisions. Any and all disputes relating to, concerning or arising from this Agreement, or relating to, concerning or arising from the relationship between the parties evidenced by the Performance Units or this Agreement, shall be brought and heard exclusively in the U.S. District Court for the District of Delaware or the Delaware Superior Court, New Castle County. Each of the parties hereby represents and agrees that such party is subject to the personal jurisdiction of said courts; hereby irrevocably consents to the jurisdiction of such courts in any legal or equitable proceedings related to, concerning or arising from such dispute, and waives, to the fullest extent permitted by law, any objection which such party may now or hereafter have that the laying of the venue of any legal or equitable proceedings related to, concerning or arising from such dispute which is brought in such courts is improper or that such proceedings have been brought in an inconvenient forum.

27.Severability. The provisions of this Agreement are severable and if any one or more provisions are determined to be illegal or otherwise unenforceable, in whole or in part, the remaining provisions shall nevertheless be binding and enforceable.

28.Waiver. Grantee acknowledges that a waiver by the Company of any provision, or breach thereof, of this Agreement on any occasion shall not operate or be construed as a waiver of such provision on any other occasion or as a waiver of any other provision of this Agreement, or of any subsequent breach by Grantee or any other Plan participant.

29.Pronouns; Including. Wherever appropriate in this Agreement, personal pronouns shall be deemed to include the other genders and the singular to include the plural. Wherever used in this Agreement, the term “including” means “including, without limitation.”

30.Successors in Interest. This Agreement shall inure to the benefit of, and be binding upon, the Company and its successors and assigns, whether by merger, consolidation, reorganization, sale of assets, or otherwise. This Agreement shall inure to the benefit of Grantee’s legal representatives. All obligations imposed upon Grantee and all rights granted to the Company under this Agreement shall be final, binding, and conclusive upon Grantee’s heirs, executors, administrators, and successors.

-9-

Exhibit 10(d)

31.Integration. This Agreement, along with any Exhibit hereto, encompasses the entire agreement of the parties related to the subject matter of this Agreement, and supersedes all previous understandings and agreements between them, whether oral or written, except as otherwise described specifically in Exhibit D. The parties hereby acknowledge and represent, that they have not relied on any representation, assertion, guarantee, warranty, collateral contract or other assurance, except those set out in this Agreement, made by or on behalf of any other party or any other person or entity whatsoever, prior to the execution of this Agreement.

32.Interpretation. The Committee shall have the sole and absolute authority to interpret, construe and apply the terms of the Plan and this Agreement and to make any and all determinations under them. Any determination or decision by the Committee shall be final, binding and conclusive upon Grantee, Grantee’s legal representative and the Company for all purposes.

***

By completing the online acceptance process, Grantee accepts the grant of Performance Units and agrees to all the terms and conditions described in this Agreement and in the Plan.

PLEASE RETAIN THIS AGREEMENT AND ALL EXHIBITS FOR YOUR RECORDS.

-10-

Exhibit 10(d)

EXHIBIT A

STOCK OWNERSHIP GUIDELINES AND RETENTION REQUIREMENT

You acknowledge that you have read the Company’s Stock Ownership Guidelines (“Guidelines”) posted on the Company’s website and you agree to comply with those Guidelines.

Your minimum stock ownership level and retention requirements, based on the Grantee Level stated on the first page of this Agreement, are set forth below. In the event of a conflict between this Exhibit A and the Guidelines, the Guidelines will prevail.

| Grantee Level | Title | Ownership Multiple of Annual Base Salary | Retention Requirement Percentage | ||||||||

| 0 | Chief Executive Officer | 6 | 50% | ||||||||

| 1 | Executive Officers (other than the Chief Executive Officer) | 3 | 50% | ||||||||

| 2 | Executive Vice Presidents and Senior Vice Presidents (other than Executive Officers) | 2 | 50% | ||||||||

| 3 | All Other Associates/Participants | 0 | 0% | ||||||||

-11-

Exhibit 10(d)

EXHIBIT B

PERFORMANCE GOAL FOR

rTSR PERFORMANCE UNIT AWARD

| Grant ID: | /$GrantID$/ | ||||

| Grant Date: | /$GrantDate$/ | ||||

| Target Share Units: | /$AwardsGranted$/ | ||||

| Performance Period: | Three-Year Period Comprised of Fiscal Years 2025, 2026 and 2027 (September 1, 2024 through August 31, 2027) | ||||

| Measurement Date: | August 31, 2027 (end of third fiscal year) | ||||

| Vesting Date: | The later of the date on which the Committee certifies the achievement level of the Performance Goal after the Measurement Date, or the third anniversary of the Grant Date, October 24, 2027 | ||||

| Benchmark Group: | S&P 400 Capital Goods Index (see below for list of companies in this Index) | ||||

Performance Goal:

The achievement of a level of the relative Total Shareholder Return Performance Measure (as defined below) between the Threshold and Maximum as shown in the table below (the “Achievement Level”). Final performance will be measured against the payout curve as of the Measurement Date. The number of shares you will receive will be calculated by multiplying your Target Share Units by the Payout % between 0% and 200%. The exact Payout % will be determined by linear interpolation of the Achievement Level of the Performance Measure between the bend points illustrated below. If the Performance Measure is at or below Threshold, no payout will be received.

The following table shows the Achievement Levels.

| Threshold Payout | Target Payout | Maximum Payout | |||||||||

| Performance Measure | 25th Percentile Rank and Below 25th Percentile Rank compared to Benchmark Group | 50th Percentile Rank of Company compared to Benchmark Group | 75th and above Percentile Rank of Company compared to Benchmark Group | ||||||||

| Achievement Level | 0% | 100% | 200% | ||||||||

Definition:

Total Shareholder Return (“TSR”) means the stock price appreciation from the beginning to end of the Performance Period, plus dividends and distributions made or declared during the Performance Period (it shall be assumed that such dividends or distributions are reinvested as of the ex-dividend date), expressed as a percentage return. Relative total shareholder return (“rTSR”) is the percentile rank of the Company’s TSR over the

-12-

Exhibit 10(d)

Performance Period as compared to the TSR of each company in the Benchmark Group (the “Performance Measure”).

Calculation of Relative Total Shareholder Return (rTSR):

TSR for Acuity and each peer company will be calculated using the equation shown below:

| TSR = | (Ending Stock Price - Beginning Stock Price) | X 100 | ||||||

| Beginning Stock Price | ||||||||

The Beginning Stock Price equals the average closing stock price during the 20-trading day period preceding the start of the Performance Period. The Ending Stock Price will equal the average closing price over the 20-trading day period ending on the last day of the Performance Period, assuming dividends distributed during the Performance Period are reinvested on the ex-dividend date for additional shares of the issuing company’s stock.

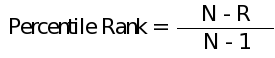

At the end of the Performance Period the TSR of each company in the peer group (excluding Acuity) will be ranked from highest to lowest, with the company with the highest TSR being assigned a rank of 1. Acuity’s percentile rank within the Peer Group will be calculated using the formula below, where N is the total companies in the Peer Group excluding Acuity and R is Acuity’s ranking within the Peer Group. N equals 45 as of the Valuation Date.

The percentile rank of Acuity’s TSR within the peer group will be calculated using the equation below, where PRAcuity and TSRAcuity equal Acuity’s percentile rank and TSR, PRabove and TSRabove equal the percentile rank and TSR of the peer company performing just above Acuity, and PRbelow and TSRbelow equal the percentile rank and TSR of the peer company performing just below Acuity.

PRAcuity = PRabove + (PRbelow − PRabove) X | (TSRabove − TSRAcuity) | ||||

(TSRabove − TSRbelow) | |||||

If Acuity’s TSR is greater than the highest TSR of the peer companies, its TSR will be positioned at the 100th percentile. Similarly, if Acuity’s TSR is less than the lowest TSR of the peer companies, its TSR will be positioned at the 0th percentile.

-13-

Exhibit 10(d)

Payout Example:

A payout example assuming an award of 100 Target Share Units would be as follows:

Determine Acuity TSR. The Beginning Stock Price for Acuity was $25.01 per share and the Ending Stock Price was $41.45 per share, then the TSR for Acuity would be 65.73%. The calculation is as follows:

| Acuity TSR = | ($41.45 - $25.01) | X 100 | 0.6573 | ||||||||

| $25.01 | |||||||||||

Determine Benchmark Group rank and percentile rank.

| Company | TSR | Rank | Percentile | |||||||||||

| Company A | 95.54% | 1 | 100.00% | |||||||||||

| Company B | 92.53% | 2 | 92.30% | |||||||||||

| Company C | 91.19% | 3 | 84.61% | |||||||||||

| Company D | 71.00% | 4 | 76.92% | |||||||||||

| Company E | 65.87% | 5 | 69.23% | |||||||||||

| Company F | 62.56% | 6 | 61.53% | |||||||||||

| Company G | 46.59% | 7 | 53.84% | |||||||||||

| Company H | 46.29% | 8 | 46.15% | |||||||||||

| Company I | 45.02% | 9 | 38.46% | |||||||||||

| Company J | 37.92% | 10 | 30.76% | |||||||||||

| Company K | 24.70% | 11 | 23.07% | |||||||||||

| Company L | 9.62% | 12 | 15.38% | |||||||||||

| Company M | 7.46% | 13 | 7.69% | |||||||||||

| Company N | 0.95% | 14 | 0.00% | |||||||||||

| Acuity Inc. 65.73% | ||||||||||||||

Determine the relative percentile rank of Acuity’s TSR within the Benchmark Group.

PRAcuity = 69.23% + (61.53% − 69.23%) X | (65.87% − 65.73%) | ||||

(65.87% − 62.56%) | |||||

PRAcuity = 68.90%

A 68.90% percentile rank results in an achievement level of between Target (50th percentile) and Maximum (75th percentile and above). The payout percentage would be interpolated between 100% and 200% to be 176%. The number of shares earned as a result are as follows:

100 Target Shares x 176% payout percentage = 176 shares earned

-14-

Exhibit 10(d)

S&P 400 Capital Goods Index - 45 Companies

The S&P 400 Capital Goods Index (the “Benchmark Group”) will be considered “closed” as of September 1, 2022, with no new companies being added subsequent to the establishment of the Benchmark Group.

| AECOM | MasTec, Inc. | ||||

| AGCO Corporation | MDU Resources Group, Inc. | ||||

| Axon Enterprise, Inc. | Mercury Systems, Inc. | ||||

| Builders FirstSource, Inc. | MSC Industrial Direct Co., Inc. | ||||

| Carlisle Companies Incorporated | nVent Electric plc | ||||

| Chart Industries, Inc. | Oshkosh Corporation | ||||

| Crane Holdings Incorporated | Owens Corning | ||||

| Curtiss-Wright Corporation | Regal Rexnord Corporation | ||||

| Donaldson Company, Inc. | Simpson Manufacturing Co., Inc. | ||||

| Dycom Industries, Inc. | SunPower Corporation | ||||

| EMCOR Group, Inc. | Sunrun Inc. | ||||

| EnerSys | Terex Corporation | ||||

| ESAB Corporation | The Middleby Corporation | ||||

| Flowserve Corporation | The Timken Company | ||||

| Fluor Corporation | The Toro Company | ||||

| GATX Corporation | Trex Company, Inc. | ||||

| Graco Inc. | Univar Solutions Inc. | ||||

| Hexcel Corporation | Valmont Industries, Inc. | ||||

| Hubbell Incorporated | Vicor Corporation | ||||

| ITT Inc. | Watsco, Inc. | ||||

| Kennametal Inc. | Watts Water Technologies, Inc. | ||||

| Lennox International Inc. | Woodward, Inc. | ||||

| Lincoln Electric Holdings, Inc. | |||||

-15-

Exhibit 10(d)

EXHIBIT C

ADDITIONAL TERMS AND CONDITIONS FOR GRANTEES OUTSIDE THE U.S.

[Omitted]

-16-

Exhibit 10(d)

EXHIBIT D

CONFIDENTIALITY, INVENTIONS, NON-SOLICITATION AND NON-COMPETITION PROVISIONS

1.Definitions.

A.“Confidential Information” “Confidential Information” means the following:

i.data and information relating to the Company’s Business (as defined herein); which is disclosed to Grantee or of which Grantee became aware of as a consequence of Grantee’s relationship with the Company; has value to the Company; is not generally known to the competitors of the Company; and which includes trade secrets, methods of operation, names of customers, price lists, financial information and projections, personnel data, and similar information. For purposes of the Confidentiality, Inventions, Non-Solicitation and Non-Competition Provisions (the “Confidentiality Provisions”), subject to the foregoing, and according to terminology commonly used by the Company, the Company’s Confidential Information shall include, but not be limited to, information pertaining to: (1) business opportunities; (2) data and compilations of data relating to the Company’s Business; (3) compilations of information about, and communications and agreements with, customers and potential customers of the Company; (4) computer software, hardware, network and internet technology utilized, modified or enhanced by the Company or by Grantee in furtherance of Grantee’s duties with the Company; (5) compilations of data concerning Company products, services, customers, and end users including but not limited to compilations concerning projected sales, new project timelines, inventory reports, sales, and cost and expense reports; (6) compilations of information about the Company’s employees and independent contracting consultants; (7) the Company’s financial information, including, without limitation, amounts charged to customers and amounts charged to the Company by its vendors, suppliers, and service providers; (8) proposals submitted to the Company’s customers, potential customers, wholesalers, distributors, vendors, suppliers and service providers; (9) the Company’s marketing strategies and compilations of marketing data; (10) compilations of data or information concerning, and communications and agreements with, vendors, suppliers and licensors to the Company and other sources of technology, products, services or components used in the Company’s Business; (11) any information concerning services requested and services performed on behalf of customers of the Company, including planned products or services; and (12) the Company’s research and development records and data. Confidential Information also includes any summary, extract or analysis of such information together with information that has been received or disclosed to the Company by any third party as to which the Company has an obligation to treat as confidential.

ii.Confidential Information shall not include:

a)Information generally available to the public other than as a result of improper disclosure by Grantee;

b)Information that becomes available to Grantee from a source other than the Company (provided Grantee has no knowledge that such information was obtained from a source in breach of a duty to the Company);

c)Information disclosed pursuant to law, regulations or pursuant to a subpoena, court order or legal process; and/or

d)Information obtained in filings with the Securities and Exchange Commission.

B.“Trade Secrets” has the meaning set forth under Georgia law, O.C.G.A. §§ 10-1-760, et seq.

-17-

Exhibit 10(d)

C.“Customers” means those entities and/or individuals which, within the two-year period preceding the Date of Termination (as that term is defined in the Performance Unit Award Agreement): (i) Grantee had material contact on behalf of the Company; (ii) about whom Grantee acquired, directly or indirectly, Confidential Information or Trade Secrets as a result of his/her employment with the Company; and/or (iii) Grantee exercised oversight or responsibility of subordinates who engaged in Material Contact on behalf of the Company. Additionally, “Customers” references only those entities and/or individuals with whom the Company currently has a business relationship, or with whom it expended resources to have or resume the same during the two-year period referenced herein.

D.“Company” means Acuity Inc. (previously known as Acuity Brands, Inc.), along with its Subsidiaries or other Affiliates.

E.“Company’s Business” means the design, manufacture, installation, servicing, and/or sale of one or more of the following and any related products and/or services: lighting fixtures and systems; lighting control components and systems (including but not limited to dimmers, switches, relays, programmable lighting controllers, sensors, timers, and range extenders for lighting and energy management and other purposes); building management and/or control systems; commercial building lighting controls; intelligent building automation and energy management products, software and solutions; motorized shading and blind controls; building security and access control and monitoring for fire and life safety; emergency lighting fixtures and systems (including but not limited to exit signs, emergency light units, inverters, back-up power battery packs, and combinations thereof); battery powered and/or photovoltaic lighting fixtures; electric lighting track units; hardware for mounting and hanging electrical lighting fixtures; aluminum, steel and fiberglass fixture poles for electric lighting; light fixture lenses; sound and electromagnetic wave receivers and transmitters; flexible and modular wiring systems and components (namely, flexible branch circuits, attachment plugs, receptacles, connectors and fittings); LED drivers and other power supplies; daylighting systems including but not limited to prismatic skylighting and related controls; organic LED products and technology; medical and patient care lighting devices and systems; indoor positioning products and technology; software and hardware solutions that collect data about building and business operations and occupant activities via sensors and use that data to provide software services or data analytics; sensor based information networks; and any wired or wireless communications and monitoring hardware or software related to any of the above. This shall not include any product or service of the Company if the Company is no longer in the business of providing such product or service to its customers at the relevant time of enforcement.

F.“Employee Services” shall mean the duties and services of the type conducted, authorized, offered, or provided by Grantee in his/her capacity as an Employee on behalf of the Company within twelve (12) months prior to the Date of Termination.

G.“Territory” means the country in which Grantee is employed by the Company (the “Country”). Grantee acknowledges that the Company is licensed to do business in the Country and in fact does business in all states, territories, provinces and other parts of the Country. Grantee further acknowledges that the services she/he has performed on behalf of the Company are at a senior level and are not limited in their territorial scope to any particular city, state, or region, but instead affect the Company’s activity within the Country. Specifically, Grantee provides Employee Services on the Company’s behalf throughout the Country, meets with Company agents and distributors, develops products and/or contacts throughout the Country, and otherwise engages in his/her work on behalf of the Company on a national level. Accordingly, Grantee agrees that these restrictions are reasonable and necessary to protect the Confidential Information, trade secrets, business relationships, and goodwill of the Company.

H.“Material Contact” shall have the meaning set forth in O.C.G.A. § 13-8-51(10), which includes contact between an employee and each Customer or potential Customer: with whom or which Grantee dealt on behalf of the Company; whose dealings with the Company were coordinated or supervised by Grantee;

-18-

Exhibit 10(d)

about whom Grantee obtained confidential information in the ordinary course of business as a result of such employee’s association with the Company; and/or who receives products or services authorized by the Company, the sale or provision of which results or resulted in compensation, commissions, or earnings for Grantee within two years prior to the Date of Termination.

I.“Termination for Cause” or “Terminated for Cause” shall mean the involuntary termination of Grantee by the Company for the following reasons:

i.If termination shall have been the result of an act or acts by Grantee which constitute an indictable offense, a felony or any crime involving dishonesty, theft, fraud or moral turpitude;

ii.If termination shall have been the result of an act or acts by Grantee which are determined, in the good faith judgment of the Company, to be in violation of written policies of the Company;

iii.If termination shall have been the result of an act or acts of dishonesty by Grantee resulting or intended to result directly or indirectly in gain or personal enrichment to Grantee at the expense of the Company;

iv.Upon the willful and continued failure by Grantee to substantially perform the duties assigned to Grantee (other than any such failure resulting from incapacity due to mental or physical illness constituting a Disability), after a demand in writing for substantial performance of such duties is delivered by the Company, which demand specifically identifies the manner in which the Company believes that Grantee has not substantially performed his or her duties; or

v.If termination shall have been the result of the unauthorized disclosure by Grantee of the Company’s Confidential Information or violation of any other provision of the Confidentiality Provisions.

J.“Inventions” and “Works For Hire.” The term “Invention” means contributions, discoveries, improvements and ideas and works of authorship, whether or not patentable or copyrightable, and: (i) which relate directly to the Company’s Business, or (ii) which result from any work performed by Grantee or by Grantee’s fellow employees for the Company, or (iii) for which equipment, supplies, facilities, Confidential Information or Trade Secrets of the Company are used, or (iv) which is developed on the Company’s time. The term “Works For Hire” (“Works”) means all documents, programs, software, creative works and other expressions and information in any tangible medium created, in whole or in part, by Grantee during the period of and relating to his/her employment with the Company, whether copyrightable or otherwise protectable, other than Inventions.

2.Confidentiality, Inventions, Non-Solicitation and Non-Competition.

A.Purpose and Reasonableness of Provisions. Grantee acknowledges that, during the term of his/her employment with the Company and after the Date of Termination, the Company has furnished and may continue to furnish to Grantee Trade Secrets and Confidential Information, which, if used by Grantee on behalf of, or disclosed to, a competitor of the Company or other person, could cause substantial detriment to the Company. Moreover, the parties recognize that Grantee, during the term of his/her employment with the Company, has developed important relationships with customers, agents, and others having valuable business relationships with the Company, and that these relationships may continue to develop after the Date of Termination. In view of the foregoing, Grantee acknowledges and agrees that the restrictive covenants contained in this Section 2 are reasonably necessary to protect the Company’s legitimate business interests, Confidential Information, and good will.

B.Trade Secrets and Confidential Information. Grantee agrees that he/she shall protect the Company’s Trade Secrets (as defined in Section 1(b) above) and Confidential Information (as defined in Section 1(a)

-19-

Exhibit 10(d)

above) and shall not disclose to any person or entity, or otherwise use or disseminate, except in connection with the performance of his/her duties for the Company, any Trade Secrets or Confidential Information. However, Grantee may make disclosures required by a valid order or subpoena issued by a court or administrative agency of competent jurisdiction, in which event Grantee will promptly notify the Company of such order or subpoena to provide it an opportunity to protect its interests. Grantee’s obligations under this Section 2(b) have applied throughout his/her active employment, shall continue after the Date of Termination, and shall survive any expiration or termination of the Confidentiality Provisions, so long as the information or material remains Confidential Information or a Trade Secret, as applicable.

Grantee further confirms that during his/her employment with the Company, including after the Date of Termination, he/she has not and will not offer, disclose or use on Grantee’s own behalf or on behalf of the Company, any information Grantee received prior to employment by the Company which was supplied to Grantee confidentially or which Grantee should reasonably know to be confidential.

Nothing in this section prohibits Grantee from reporting possible violations of law or regulation to any governmental agency or entity, or making other disclosures that are protected under the whistleblower provisions of law or regulation. Grantee does not need the prior authorization of the Company to make any such reports or disclosures, and Grantee is not required to notify the Company that Grantee has made such reports or disclosures.

C.Return of Property. On or before the Date of Termination, Grantee agrees to deliver promptly to the Company all files, customer lists, management reports, memoranda, research, Company forms, financial data and reports and other documents (including all such data and documents in electronic form) of the Company, supplied to or created by him/her in connection with his/her employment hereunder (including all copies of the foregoing) in his/her possession or control, and all of the Company’s equipment and other materials in his/her possession or control. Grantee further agrees and covenants not to retain any such property and to permanently delete such information residing in electronic format to the best of his/her ability and not to attempt to retrieve it. Grantee’s obligations under this Section 2(c) shall survive any expiration or termination of the Confidentiality Provisions.

D.Inventions. Grantee does hereby assign to the Company the entire right, title and interest in any Invention which is or was made or conceived, either solely or jointly with others, during his/her employment with the Company, including after the Date of Termination. Grantee attests that he/she has disclosed (or promptly will disclose, if after the Date of Termination) to the Company all such Inventions. Grantee will, if requested, promptly execute and deliver to the Company a specific assignment of title for any such Invention and will at the expense of the Company, take all reasonably required action by the Company to patent, copyright or otherwise protect the Invention.

E.Non-Competition. In the event that Grantee,

i.voluntarily resigns from the Company,

ii.is Terminated for Cause (as defined above), or

iii.declines to sign a Confidential Severance Agreement and Release offered by the Company in the event of a termination for any reason other than a Termination for Cause (including, for example, as a result of a position elimination).

Grantee acknowledges and agrees that during his/her employment, and for twelve (12) months after the Date of Termination, he/she has not and will not, directly or indirectly, engage in, provide, or perform any Employee Services on behalf of any person or entity (or, if organized into divisions or units, any distinct

-20-

Exhibit 10(d)

division or operating unit) in the Territory that derives revenue from providing goods or services substantially similar to those which comprise the Company’s Business. Notwithstanding the foregoing, if the Company terminates Grantee’s employment for any reason other than a Termination for Cause (including, for example, as a result of a position elimination), and Grantee signs a Confidential Severance Agreement and Release offered by the Company, the period covered by this non-competition covenant will be reduced to either: (i) the time within which severance payments are scheduled to be paid to Grantee under such agreement, or (ii) if severance is paid to Grantee in a lump sum, the number of weeks of Grantee’s then-current regular salary that are used to calculate such lump sum payment; provided, however, that the restrictive period calculated hereunder shall not, in any event, exceed twelve (12) months following the Date of Termination.

F.Non-Solicitation of Customers. Grantee acknowledges and agrees that during his/her employment, and for twenty-four (24) months after the Date of Termination, Grantee has not and will not directly or indirectly solicit Customers (as defined in Section 1(c) above) with whom he/she had Material Contact (as defined in 1(g) above) for the purpose of providing goods and/or services competitive with the Company’s Business.

G.Non-Solicitation of Employees and Agents. Grantee acknowledges and agrees that during his/her employment, and for a period of twenty-four (24) months after the Date of Termination, Grantee has not and will not, directly or indirectly, whether on behalf of Grantee or others, solicit, lure or attempt to hire away any of the Company’s employees or agents.

H.Non-Solicitation of Sales Agents. Grantee acknowledges and agrees that during his/her employment, and for a period of twenty-four (24) months after the Date of Termination, Grantee has not and will not, directly or indirectly, whether on behalf of Grantee or others, solicit any of the Company’s Sales Agents for the purpose of disrupting their relationship with the Company and/or selling and/or facilitating the sale of products competitive with the Company’s Business. For purposes of this Section 2, a “Sales Agent” is any third-party agency, and/or its representatives, with which or whom the Company has contracted for the purpose of facilitating the sale of the Company’s products during the last twenty-four (24) months of Grantee’s employment with the Company.

I.Injunctive Relief. Grantee acknowledges that if he/she breaches or threatens to breach any of the provisions of this Section 2, his/her actions may cause irreparable harm and damage to the Company which could not be compensated in damages. Accordingly, if Grantee breaches or threatens to breach any of the provisions of this Section 2, the Company shall be entitled to seek injunctive relief, in addition to any other rights or remedies the Company may have. The existence of any claim or cause of action by Grantee against the Company, whether predicated on the Confidentiality Provisions or otherwise, shall not constitute a defense to the enforcement by the Company of Grantee’s agreements under this Section 2.

3.Non-Assignable by Grantee. The parties acknowledge that the Confidentiality Provisions have been entered into due to, among other things, the special skills and knowledge of Grantee, and agree that the Confidentiality Provisions may not be assigned or transferred by Grantee.

4.Notices. All notices, requests, demands and other communications required or permitted hereunder shall be in writing and shall be deemed to have been duly given when delivered or seven days after mailing if mailed first class, certified mail, postage prepaid, addressed as follows:

If to the Company: Acuity Inc.

Attention: Corporate Secretary

1170 Peachtree Street, NE, Suite 1200

Atlanta, Georgia 30309-7676

-21-

Exhibit 10(d)

If to Grantee: To his or her last known address on file with the Company.

Any party may change the address to which notices, requests, demands and other communications shall be delivered or mailed by giving notice thereof to the other party in the same manner provided herein.

5.Provisions Severable. If any provision or covenant, or any part thereof, contained in the Confidentiality Provisions is held by any court, agency, arbitrator or other competent authority to be invalid, illegal, or unenforceable, either in whole or in part, such invalidity, illegality or unenforceability shall not affect the validity, legality or enforceability of the remaining provisions or covenants, or any part thereof, in the Confidentiality Provisions, all of which shall remain in full force and effect. Each and every provision, paragraph and subparagraph of Section 2 above is severable from the other provisions, paragraphs and subparagraphs and constitutes a separate and distinct covenant. To the extent a court, agency, arbitrator or other competent authority finds that a provision is unenforceable because it is overbroad, the court may modify or reform the provision to the minimum extent necessary for the provision to remain in force and effect for the maximum duration, subject matter scope and geographic area as to which it may be enforceable.

The restrictive covenants set forth in Section 2 of the Confidentiality Provisions represent the entire agreement of the parties with respect to the subject matter thereof and supersede any prior agreement with respect thereto; provided, however, that the restrictive covenants described in this Exhibit D shall not supersede those set forth in either: (a) any Executive Severance Agreement applicable to Grantee, if any, (b) any Confidentiality, Inventions and Non-Solicitation Agreement to which Grantee is a party, if any, or (c) any restrictive covenants to which Grantee is a party under any employment agreement or offer letter, if any. To the extent that any agreement applicable to Grantee include restrictive covenant provisions that conflict with the provisions contained in these Confidentiality Provisions, the provisions that are more restrictive on Grantee will control.

6.Waiver. Failure of either party to insist, in one or more instances, on performance by the other in strict accordance with the terms and conditions of the Confidentiality Provisions shall not be deemed a waiver or relinquishment of any right granted in the Confidentiality Provisions or the future performance of any such term or condition or of any other term or condition of the Confidentiality Provisions, unless such waiver is contained in a writing signed by the party making the waiver.

7.Amendments and Modifications. The Confidentiality Provisions and any Exhibit hereto may be amended or modified only by a writing signed by both parties hereto, which makes specific reference to the Confidentiality Provisions. However, this Section does not affect a court of competent jurisdiction or arbitrator`s ability to modify the Confidentiality Provisions, pursuant to O.C.G.A. §§ 13-8-51(11); 53(d); or 54 in the event that either party initiates legal proceedings that relate in any way to this Confidentiality Provisions, including any action brought by either party seeking to enforce any provision set forth herein.

8.Governing Law and Venue. The validity and effect of the Confidentiality Provisions shall be governed by and construed and enforced in accordance with the laws of the State of Georgia, United States of America, without regard to its conflict of law provisions. Any and all disputes relating to, concerning or arising from the Confidentiality Provisions, or relating to, concerning or arising from the relationship between the parties evidenced by the Confidentiality Provisions, shall be brought and heard exclusively in the U.S. District Court for the District of Delaware or the Delaware Superior Court, New Castle County. Each of the parties hereby represents and agrees that such party is subject to the personal jurisdiction of said courts; hereby irrevocably consents to the jurisdiction of such courts in any legal or equitable proceedings related to, concerning or arising from such dispute, and waives, to the fullest extent permitted by law, any objection which such party may now or hereafter have that the laying of the venue of any legal or equitable proceedings related to, concerning or arising from such dispute which is brought in such courts is improper or that such proceedings have been brought in an inconvenient forum.

-22-

Exhibit 10(d)

9.Legal Fees. Each party shall pay its own legal fees and other expenses associated with any dispute under the Confidentiality Provisions or any Exhibit hereto.

10.Tender Back Provision. If, in the context of a lawsuit involving Grantee or any other person or entity arguing on Grantee’s behalf, any court determines that any provisions of Section 2 are void, invalid, illegal, or otherwise unenforceable, Grantee shall be required to immediately return to the Company 70% of all monies paid out under the Performance Unit Award Agreement, or to return 70% of any unsold shares Grantee still owns of such Performance Units awarded under the Performance Unit Award Agreement. For purposes of this section, the amount to be paid back shall be determined by ascertaining the value and amount the share(s) sold at the time that Grantee actually sold such share(s). You acknowledge and agree that this covenant does not constitute a penalty clause.

11.Tolling Period. If Grantee is found by a court to have violated any restriction in Section 2 of the Confidentiality Provisions, he/she agrees that the time period for such restriction shall be extended by one day for each day that he/she is found to have violated the restriction, up to a maximum of 18 months.

12.Language. The parties acknowledge that they have requested and are satisfied that the Confidentiality Provisions and all related documents be in the English language.

-23-

Exhibit 10(d)

SPECIAL TERMS AND CONDITIONS EXHIBIT TO THE CONFIDENTIALITY, INVENTIONS, NON-SOLICITATION AND NON-COMPETITION PROVISIONS FOR GRANTEES OUTSIDE THE U.S.

[Omitted]

-24-

Exhibit 10(d)

SPECIAL TERMS AND CONDITIONS EXHIBIT TO THE CONFIDENTIALITY, INVENTIONS, NON-SOLICITATION AND NON-COMPETITION PROVISIONS FOR GRANTEES IN THE U.S.

This Appendix includes additional state-specific terms and conditions that apply to Grantees in states listed below with respect to the Confidentiality, Inventions, Non-Solicitation and Non-Competition Provisions (the “Confidentiality Provisions”). This Appendix is part of the Confidentiality Provisions and contains terms and conditions material to Grantee’s rights and obligations under the Confidentiality Provisions. Unless otherwise provided below, capitalized terms used but not defined herein shall have the same meanings assigned to them in the Plan and the Confidentiality Provisions.

FOR ALL GRANTEES IN THE US

With respect to Grantees who are not supervisors for the purposes of the National Labor Relations Act, nothing contained in the Confidentiality Provisions, in any way, restricts or impedes Grantee from exercising Grantee’s rights under Section 7 of the National Labor Relations Act (such protected rights include assisting coworkers or former coworkers with workplace issues concerning their employer, communicating with others including a union and the NLRB, about their employment, or discussing the terms and conditions of employment, including, but not limited to, wages or salary, benefits, severance, the terms of this Agreement, job responsibilities and vacation, with coworkers or union representatives).

Nothing in this Agreement limits any Grantee from testifying truthfully in any legal proceeding, including, but not limited to responding to any inquiries made by the EEOC or any government agency; from discussing or disclosing information about unlawful acts in the workplace, such as harassment or discrimination or any other conduct that Grantee has reason to believe is unlawful; or from disclosing factual information related to an administrative claim or civil action concerning sexual assault, sexual harassment, workplace harassment or discrimination, failure to prevent an act of workplace harassment or discrimination, or an act of retaliation against a person for reporting or opposing harassment or discrimination. Grantee may respond accurately and fully to any question or request for information when required to do so by law.

Further, nothing in this Agreement limits any Grantee’s rights to: (i) file a charge (including a challenge to the validity of this Agreement) with, communicate with, or participate in an investigation or proceeding conducted by the U.S. Equal Employment Opportunity Commission (“EEOC”), the National Labor Relations Board (“NLRB”), or any other similar federal, state, or local government office, official, or agency; (ii) testify in an administrative, legislative, or judicial proceeding concerning alleged criminal conduct or alleged sexual harassment on the part of any other party, or on the part of the agents or employees of another party, when the person testifying has been required or requested to attend the proceeding pursuant to a court order, subpoena, or written request from an administrative agency or legislature; or (iii) provide information to the U.S. Securities and Exchange Commission, EEOC, or any other regulatory or enforcement agency or collect rewards under a whistleblower program.

Further, to the extent that any Grantee does not meet the compensation threshold required for a post-termination covenant to be enforceable under applicable state law, either at the time the Agreement is entered into or at the time of enforcement, then, to the extent required by applicable state law, Section 2(E)(Non-Competition), Section 2(F)(Non-Solicitation of Customers), Section 2(G) Non-Solicitation of Employees and Agents, or Section 2(H)(Non-Solicitation of Sales Agents) of the Confidentiality Provisions shall not apply to any such Grantee.

Grantee is advised to consult with an attorney of Grantee’s own choosing and at Grantee’s own cost before signing this Agreement.

CALIFORNIA

-25-

Exhibit 10(d)