As filed with the SEC on January 25, 2022

Registration No. 333-261006

U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-14/A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

/ / Pre-Effective Amendment No. 1 / / Post-Effective Amendment No. ___

TRUST FOR PROFESSIONAL MANAGERS

(Exact Name of Registrant as Specified in Charter)

615 East Michigan Street

Milwaukee, Wisconsin 53202

Milwaukee, Wisconsin 53202

(Address of Registrant’s Principal Executive Offices)

(Registrant’s Telephone Number, Including Area Code) (414) 765-4255

Jay S. Fitton

U.S. Bank Global Fund Services

615 East Michigan Street, 2nd Floor

Milwaukee, Wisconsin 53202

(Name and Address of Agent for Service)

Copies to:

Carol A. Gehl, Esq.

Godfrey & Kahn, S.C.

833 East Michigan Street. Suite 1800

Milwaukee, Wisconsin 53202

(414) 273-3500

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933, as amended.

Title of the securities being registered: Shares of beneficial interest, with no par value, of Convergence Long/Short Equity ETF.

The Registrant will hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

No filing fee is due because the Registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended.

Convergence Long/Short Equity Fund

a series of Trust for Professional Managers

January 25, 2022

Dear Valued Shareholder:

As an investor in the Convergence Long/Short Equity Fund (the “Target Fund”), a series of Trust for Professional Managers (“TPM”), we are pleased to inform you of our plan to convert the Target Fund into an exchange-traded fund (“ETF”), which will continue to be managed by Convergence Investment Partners, LLC (“Convergence”), the Target Fund’s investment adviser.

Pursuant to an Agreement and Plan of Reorganization, the Target Fund will be converted into an ETF through the reorganization of the Target Fund into the Convergence Long/Short Equity ETF (the “Acquiring Fund”), a newly-created series of TPM that has the same investment objective and substantially similar investment strategies as the converting Target Fund. The reorganization is expected to take place on or about February 18, 2022 and is intended to be structured as a tax-free reorganization under the U.S. Internal Revenue Code of 1986, as amended. In connection with the reorganization, your shares of the Target Fund will be exchanged for shares of equal value of the Acquiring Fund. Interests of shareholders will not be diluted as a result of the reorganization. Subsequent to the reorganization, the Acquiring Fund’s shares will be listed on the Cboe BZX Exchange, Inc.

We believe the reorganization will result in multiple benefits for investors. The Board of Trustees (the “Board”) of TPM, which oversees both the Target Fund and the Acquiring Fund, has approved the reorganization based on its determination that it is in the best interest of the Target Fund and its shareholders. Expected benefits include:

1)Improved Efficiency: Converting to an ETF structure can provide benefits with respect to the management of capital gains distributions allowing for potentially greater tax efficiency for shareholders.

2)Lower Overall Expenses: The management fee of 0.95% of the average daily net assets of the Acquiring Fund is lower than the current management fee of 1.00% of the average daily net assets of the Target Fund. The Acquiring Fund is also expected to experience lower overall expenses as compared to the Target Fund because the Acquiring Fund will have a unitary fee structure under which Convergence will pay all operating expenses of the Acquiring Fund subject to certain exclusions such as dividends and interest on short positions. Currently, the Target Fund pays separate fees to other service providers to cover operational expenses in addition to paying a management fee to Convergence, the investment adviser to both the Target Fund and Acquiring Fund. More details on the fee structure are provided in the enclosed Information Statement/Prospectus.

3)Tax-Free Reorganization: The Reorganization is intended to be structured such that shareholders will not recognize a taxable gain (or loss) on the conversion of mutual fund to ETF shares for U.S. federal income tax purposes. An exception, albeit small, regarding fractional mutual fund shares is explained in later sections of this document.

Shareholders of the converting Target Fund should know the options available to them with respect to the reorganization but should also consider possible tax consequences of options outside of the tax-free reorganization. Those include:

•Maintaining your current positions in the converting Target Fund and receiving ETF shares on the conversion date.

•Redeeming your shares of the converting Target Fund.

The Information Statement/Prospectus provides greater detail on the mechanics of the conversion and what to expect with your investment during and following the conversion. No shareholder vote is required or being requested to complete the conversion. Shareholders will need brokerage accounts with the ability to transact in ETF shares in connection with the reorganization. The Target Fund is currently offered only through financial intermediaries that permit shareholders to hold ETF shares so no additional action will need to be taken prior to the conversion for Target Fund shareholders to receive ETF shares.

We encourage you to carefully review the additional information provided in this document. If you have questions not answered, please contact your financial advisor. You may also contact Convergence Investment Partners, LLC at info@investcip.com.

In closing, we are excited to offer the benefits of this conversion to our funds’ shareholders. We view this event as a reflection of our continued efforts to apply innovative thinking in pursuit of better investment outcomes for our investors. Thank you for your continued trust.

Sincerely,

John P. Buckel David J. Abitz

Trust for Professional Managers Convergence Investment Partners, LLC

President President & Chief Investment Officer

QUESTIONS AND ANSWERS

We recommend that you read the complete Information Statement/Prospectus.

This section contains a brief Q&A which will help explain the Reorganization including the reasons for the Reorganization. Following this section is a more detailed discussion.

Q. What is happening to the Convergence Long/Short Equity Fund (the “Target Fund”)? Why am I receiving an Information Statement/Prospectus?

A. The Target Fund, which is currently operated as a mutual fund, will be converted into an exchange-traded fund (“ETF”) through the reorganization of the Target Fund into the Convergence Long/Short Equity ETF, a newly-created series of Trust for Professional Managers (the “Acquiring Fund”) that has the same investment objective and substantially similar investment strategies as the Target Fund (the “Reorganization”). As an ETF, the Acquiring Fund’s shares will be traded on the Cboe BZX Exchange, Inc. following the Reorganization. The Reorganization will be accomplished in accordance with the Agreement and Plan of Reorganization (the “Plan”).

Under the Plan, all of the assets and liabilities of the Target Fund will be transferred to the Acquiring Fund, in exchange for shares of the Acquiring Fund of equivalent aggregate net asset value (“NAV”). Your shares of the Target Fund will be exchanged for shares of the Acquiring Fund with an equivalent aggregate NAV of the Target Fund shares you held at the time of the Reorganization. Shares of the Acquiring Fund will be transferred to each shareholder’s brokerage account.

The IMPORTANT NOTICE ABOUT YOUR TARGET FUND ACCOUNT – QUESTIONS AND ANSWERS, below, provides important information about actions to take with respect to your account in order to ensure the seamless transition from holding shares of the Target Fund to holding ETF shares of the Acquiring Fund.

The enclosed Information Statement/Prospectus provides greater detail on the mechanics of the Reorganization and what to expect with your investment during and following the Reorganization. No shareholder vote is required or being requested to complete the Reorganization. Shareholders will need brokerage accounts with the ability to transact in ETF shares in connection with the Reorganization. The Target Fund is currently offered only through financial intermediaries that permit shareholders to hold ETF shares so no additional action will need to be taken prior to the conversion for Target Fund shareholders to receive ETF shares.

Q. Has the Board of Trustees approved the Reorganization?

A. Yes, the Board of Trustees (the “Board”) of Trust for Professional Managers (“TPM”), a Delaware statutory trust organized under the laws of the state of Delaware, which oversees the Target Fund and the Acquiring Fund, approved the Reorganization. The Board, including all of the Trustees who are not “interested persons” of the Target Fund (as defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) (the “Independent Trustees”), determined that for the Target Fund, the Reorganization is in the best interests of the Target Fund and its shareholders and that the Target Fund’s shareholders’ interests will not be diluted as a result of the Reorganization. Similarly, the Board believes that the Reorganization is in the best interests of the Acquiring Fund.

Q. Why is the Reorganization occurring?

A. Convergence Investment Partners, LLC (“Convergence”), the investment adviser to the Target Fund and the Acquiring Fund, proposed that the Target Fund be reorganized into the Acquiring Fund because the ETF structure of the Acquiring Fund may provide benefits, including with respect to the management of capital gains distributions. In a mutual fund, when portfolio securities are sold, either to rebalance holdings or to raise cash for redemptions, the sale can create capital gains that impact all taxable shareholders of the mutual fund. In contrast, the mechanics of the creation and redemption process for ETFs allows ETFs to acquire securities in-kind and redeem securities in-kind generally reducing the

i

realization of capital gains by ETFs for the same processes. As a result, shareholders in an ETF are largely only subject to capital gains on their investment in the ETF after they sell their ETF shares. In addition, unlike the Target Fund, the Acquiring Fund will operate with full portfolio holding transparency. The Acquiring Fund’s portfolio holdings will be made public each day and can be found on the Acquiring Fund’s website. Some investors may find this advantageous as it may help them decide whether to invest or not; existing and potential shareholders can examine the Acquiring Fund’s portfolio holdings and decide if the specific mix of holdings meets their needs. It also means that shareholders know exactly what companies the Acquiring Fund is investing in at all times. By contrast, in a mutual fund, the fund’s portfolio holdings are only required to be disclosed quarterly. The Acquiring Fund will pursue the same investment objective and investment strategies as the Target Fund but in the ETF structure.

Q. How will the Reorganization affect me as a shareholder?

A. If the Reorganization is consummated, you will cease to be a shareholder of the Target Fund and will become a shareholder of the Acquiring Fund. Upon completion of the Reorganization, you will own shares of the Acquiring Fund offered as an ETF having an aggregate NAV equal to the aggregate NAV of the shares of the Target Fund you owned when the Reorganization happened. Shares of the Acquiring Fund will be transferred to your brokerage account. Shares of the Acquiring Fund are not issued in fractional shares. As a result, some shareholders who hold fractional shares of the Target Fund may have such fractional shares redeemed at NAV immediately prior to the Reorganization resulting in a small cash payment, which will be taxable for U.S. income tax purposes.

After the Reorganization, individual shares of the Acquiring Fund may only be purchased and sold on Cboe BZX Exchange, Inc., other national securities exchanges, electronic crossing networks and other alternative trading systems. Should you decide to purchase or sell shares in the Acquiring Fund after the Reorganization, you will need to place a trade through a broker who will execute your trade on an exchange at prevailing market prices. Because Acquiring Fund shares trade at market prices rather than at NAV, Acquiring Fund shares may trade at a price less than (discount) or greater than (premium) the Acquiring Fund’s NAV. As with all ETFs, your broker may charge a commission for purchase and sales transactions, although ETFs trade with no transaction fees (NTF) on many platforms.

Q. Am I Being Asked to Vote on the Reorganization?

A. No, a vote of the shareholders of the Target Fund is not required to approve the Reorganization. Votes of the shareholders of the Target Fund are not required to approve the Reorganization.

TPM is a Delaware statutory trust and, under applicable Delaware law and TPM’s Amended and Restated Declaration of Trust, no shareholder vote is required in connection with the Reorganization. Further, no shareholder vote is required by Rule 17a-8 under the 1940 Act because (1) there are no material differences between the investment advisory agreement for the Target Fund and the investment advisory agreement for the Acquiring Fund; (2) the Target Fund and the Acquiring Fund have the same Independent Trustees; (3) no policy of the Target Fund that could not be changed without a shareholder vote is materially different from a policy of the Acquiring Fund; and (4) neither the Target Fund nor the Acquiring Fund pay any distribution fees pursuant to a plan adopted in accordance with Rule 12b-1 under the 1940 Act.

Q. Will the Reorganization affect the way my investments are managed?

A. No. Convergence is also the investment adviser to the Acquiring Fund and the Acquiring Fund will be managed using the same investment objective and investment strategies currently used by the Target Fund.

Q. Will the fees and expenses of the Acquiring Fund be lower than the fees and expenses of the Target Fund?

A. Yes. The management fee of the Acquiring Fund will be 0.95% of the average daily net assets of the Acquiring Fund, which will be lower than the current management fee of 1.00% of the average daily net assets of the Target Fund. The Acquiring Fund is also expected to experience lower overall expenses as compared to the Target Fund because the Acquiring

ii

Fund will have a unitary fee structure under which the Acquiring Fund will pay a management fee to Convergence and Convergence will be responsible for paying operational expenses of the Fund. Currently, the Target Fund pays separate fees to Convergence for investment advisory services and to other service providers for operational expenses.

Q. Are there any differences in risks between the Target Fund and the Acquiring Fund?

A. Yes. While most of the risks of the Target Fund and the Acquiring Fund are the same, the Acquiring Fund is subject to certain risks unique to operating as an ETF. A comparison of the Target Fund risks and the Acquiring Fund risks may be found under “Additional Information About the Acquiring Fund and the Target Fund – Description of Principal Risks” in the enclosed Information Statement/Prospectus.

Q. What are some features of ETFs that differ from mutual funds?

A. The following are some unique features of ETFs as compared to mutual funds:

Transparency: The Acquiring Fund will be a transparent ETF that operate with full transparency to its portfolio holdings. Following the Reorganization, the Acquiring Fund, like other transparent ETFs, will make its portfolio holdings public each day. This holdings information, along with other information about the Acquiring Fund, will be found on the Convergence website at www.investcip.com.

Tax Efficiency: In a mutual fund, when portfolio securities are sold, either to rebalance holdings or to raise cash for redemptions, the sale can create capital gains that impact all taxable shareholders of the mutual fund. In contrast, the mechanics of the creation and redemption process for ETFs allows ETFs to acquire securities in-kind and redeem securities in-kind generally reducing the realization of capital gains by the ETFs for the same processes. As a result, shareholders in an ETF are largely only subject to capital gains on their investment in the ETF after they sell their ETF shares.

Sales on an Exchange throughout the Day: ETFs provide shareholders with the opportunity to purchase and sell shares throughout the day at market-determined prices, instead of being required to wait to make a purchase or a redemption at the next calculated NAV per share at the end of the trading day. This means that when a shareholder decides to purchase or sell shares of the ETF, the shareholder can act on that decision immediately by contacting the shareholder’s broker to execute the trade.

Sales only through a Broker at Market Price: Unlike a mutual fund’s shares, individual shares of ETFs, like the Acquiring Fund, are not purchased or sold at NAV. Individual Acquiring Fund shares may only be purchased and sold through a broker at market prices. The market price of the ETF may be higher or lower than the ETF’s NAV per share, and might not be the same as the ETF’s next calculated NAV at the close of the trading day. When buying and selling shares through a financial intermediary, a shareholder may incur brokerage or other charges determined by the financial intermediary, although ETFs trade with no transaction fees (NTF) on many platforms. In addition, a shareholder of an ETF, such as the Acquiring Fund, may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase shares (bid) and the lowest price a seller is willing to accept for shares (ask) when buying or selling shares in the secondary market (the “bid-ask spread”). Because ETF shares trade at market prices rather than at NAV, shares of an ETF, like the Acquiring Fund, may trade at a price less than (discount) or greater than (premium) the fund’s NAV. The trading prices of an ETF’s shares in the secondary market will fluctuate continuously throughout trading hours based on the supply and demand for the ETF’s shares and shares of the underlying securities held by the ETF, economic conditions and other factors, rather than an ETF’s NAV, which is calculated at the end of each business day.

Q. When is the Reorganizations expected to occur?

A. Convergence is anticipating a Reorganization date on or around February 18, 2022. This date could be delayed because some administrative conditions must be satisfied to implement the Reorganization. The Target Fund will publicly disclose updates on material developments throughout the process.

iii

Q. Will shareholders have to pay any sales load, commission or other similar fee in connection with the Reorganization?

A. No. Shareholders of the Target Fund will not pay any sales load, commission or other similar fee in connection with the receipt of Acquiring Fund shares from the Reorganization.

Q. Who will pay the costs in connection with the Reorganization?

A. Convergence will pay all expenses incurred in connection with the Reorganization.

Q. Will the Reorganization result in any U.S. federal tax liability to me?

A. The Reorganization is designed to be treated as a tax-free reorganization for U.S. federal income tax purposes. However, as part of the Reorganization, some shareholders may receive cash compensation for fractional shares of the Target Fund that they hold. The redemption of these fractional shares will likely be a taxable event, albeit a small one.

Shareholders should consult their tax advisors about possible state, local, or foreign tax considerations with respect to the Reorganization, if any, because the information about tax consequences in this document relates to certain U.S. federal income tax consequences of the Reorganization only.

Q. Can I purchase or redeem shares of the Target Fund before the Reorganization takes place?

A. Yes. You can purchase Target Fund shares in a brokerage account through a broker until February 15, 2022. Shares of the Target Fund are not available for purchase directly from U.S. Bancorp Fund Services, LLC, the transfer agent to the Target Fund. You can redeem Target Fund shares until the day before the Reorganization occurs. That means your redemption order must be received by February 15, 2022. Any shares not redeemed before the date of the Reorganization, which we expect will be February 18, 2022, will be exchanged for shares of the Acquiring Fund.

Q. What do I need to do to prepare for the Reorganization?

A. Each broker that offers shares of the Target Fund will allow shareholders to hold shares of the Acquiring Fund after the Reorganization. While each broker that currently offers shares of the Target Fund will permit shareholders to hold Acquiring Fund shares in their account, certain brokers may restrict shareholders from purchasing additional Acquiring Fund shares for a period of time following the Reorganization. Please contact your broker for additional information.

Q. Whom do I contact for further information?

A. You can contact your financial advisor or other financial intermediary for further information. You also may contact Convergence at info@investcip.com.

Important additional information about the Reorganization is set forth in the accompanying Information Statement/Prospectus. Please read it carefully.

IMPORTANT NOTICE ABOUT YOUR TARGET FUND ACCOUNT

QUESTIONS AND ANSWERS

This section contains a brief Q&A which provides information for you to determine if you need to take action with respect to your shareholder account prior to the Reorganization.

iv

Q. Will my brokerage account permit me to receive Acquiring Fund shares in connection with the Reorganization?

A. Yes. The Target Fund is only offered through brokers that will allow shareholders of the Target Fund to receive Acquiring Fund shares in connection with the Reorganization. Please contact your broker or financial advisor if you have any questions about how your Target Fund shares will be treated before or after the Reorganization.

Q. Will I be able to purchase additional shares of the Acquiring Fund in my brokerage account following the Reorganization?

A. While each broker that currently offers shares of the Target Fund will permit shareholders to hold Acquiring Fund shares in their account, and most will allow shareholders to acquire additional Acquiring Fund shares following the Reorganization, certain brokers may restrict shareholders from purchasing additional Acquiring Fund shares for a period of time following the Reorganization. Please contact your broker for additional information.

Q. What if I do not want to hold ETF shares?

A. If you do not want to receive ETF shares in connection with the Reorganization, you may redeem your shares of the Target Fund prior to the Reorganization. The last day to redeem your shares of the Target Fund is February 17, 2022.

v

INFORMATION STATEMENT/PROSPECTUS

Dated January 25, 2022

Convergence Long/Short Equity Fund

a series of Trust for Professional Managers

This Information Statement/Prospectus is being furnished to shareholders of the Convergence Long/Short Equity Fund (referred to as the “Target Fund”), a series of Trust for Professional Managers (“TPM”), in connection with the reorganization of the Target Fund into the Convergence Long/Short Equity ETF (referred to as “Acquiring Fund”), a newly-created series of TPM. The Target Fund and the Acquiring Fund may each be referred to individually as a “Fund” or together as the “Funds.”

The Board of Trustees (the “Board”) of TPM approved the Agreement and Plan of Reorganization (the “Plan”) under which:

1.the Target Fund, a series of TPM, will transfer all of its assets to the Acquiring Fund, a newly-created series of TPM, in exchange solely for shares of the Acquiring Fund and the assumption by the Acquiring Fund of all of the liabilities of the Target Fund;

2.the shares of the Acquiring Fund will be distributed to the shareholders of the Target Fund according to their respective interests in such Target Fund; and

3.the Target Fund will be liquidated and dissolved (the “Reorganization”).

A copy of the Plan is provided in Exhibit A hereto.

The shares of the Acquiring Fund received by the shareholders of the Target Fund in the exchange will be equal in aggregate NAV to the aggregate NAV of their shares of the Target Fund at the closing date of the Reorganization. The Reorganization is expected to be effective on or about February 18, 2022.

The Board, including a majority of the Trustees who are not “interested persons” as defined in the Investment Company Act of 1940, as amended (the “1940 Act”) (the “Independent Trustees”), believes that the Reorganization is in the best interests of the Target Fund and that the interests of the Target Fund’s shareholders will not be diluted as a result of the Reorganization. Furthermore, the Board, including a majority of the Independent Trustees, believes that the Reorganization is in the best interests of the Acquiring Fund. For federal income tax purposes, the Reorganization is intended to be structured as a tax-free transaction for the Target Fund, the Acquiring Fund, and their shareholders. For some shareholders, there could be a small payment for the redemption of fractional shares of the Target Fund, and that would be taxable for U.S. federal income tax purposes.

THIS INFORMATION STATEMENT/PROSPECTUS IS FOR INFORMATION PURPOSES ONLY, AND NO ACTION ON YOUR PART IS REQUIRED TO EFFECT THE REORGANIZATION. WE ARE NOT ASKING YOU FOR A PROXY, AND YOU ARE NOT REQUESTED TO SEND US A PROXY.

The Target Fund is a series of TPM, a Delaware statutory trust created under the laws of the state of Delaware, which is registered with the U.S. Securities and Exchange Commission (the “Commission” or the “SEC”) as an open-end management investment company. The Acquiring Fund is also a series of TPM. The Target Fund and the Acquiring Fund have identical investment objectives and investment restrictions and substantially similar investment strategies. The principal office of TPM is located at 615 East Michigan Street, Milwaukee, Wisconsin 53202. The Target Fund and the Acquiring Fund are managed by Convergence Investment Partners, LLC (“Convergence”), located at 3801 PGA Boulevard, Suite 1001, Palm Beach Gardens, Florida 33410.

1

Shares of the Acquiring Fund will be listed for trading on Cboe BZX Exchange, Inc.

In preparation for the closing of the Reorganization, the last day to purchase shares of the Target Fund will be February 17, 2022. Redemption orders for Target Fund shares must be placed by February 17, 2022, or the Target Fund shares will be converted to Acquiring Fund shares. The Reorganization is expected to occur after the close of trading on February 18, 2022. The Acquiring Fund will be open for trading on February 22, 2022.

This Information Statement/Prospectus, which you should read carefully and retain for future reference, sets forth concisely the information that you should know before investing. A statement of additional information, dated January 25, 2022, relating to this Information Statement/Prospectus and the proposed Reorganization, is incorporated herein by reference and legally deemed to be a part of this Information Statement/Prospectus. The statement of additional information is also available upon request and without charge by calling (toll free) 877-677-9414 or writing to the Fund at: Convergence c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701.

Additional information is available in the following materials:

•Prospectus dated March 30, 2021, as amended, for the Target Fund (“Target Fund Prospectus”), which is on file with the SEC (http://sec.gov) (File Nos. 333-62298 and 811-10401) (Accession No. 0000894189-21-001746);

•Statement of Additional Information dated March 30, 2021 for the Target Fund (“Target Fund SAI”), which is on file with the SEC (http://sec.gov) (File Nos. 333-62298 and 811-10401) (Accession No. 0000894189-21-001746);

•The Target Fund’s audited financial statements and related report of the independent registered public accounting firm included in the Target Fund’s Annual Report to Shareholders for the fiscal year ended November 30, 2020 (the “Target Fund Annual Report”) which is on file with the SEC (http://sec.gov) (File No. 811-10401) (Accession No. 0000898531-21-000034).

•The Target Fund’s unaudited financial statements included in the Target Fund’s Semi-Annual Report to Shareholders for the fiscal period ended May 31, 2021 (the “Target Fund Semi-Annual Report”) which is on filed with the SEC (File No. 811-10401) (Accession No. 0000898531-21-000383).

Because the Acquiring Fund has not yet commenced operations, no annual or semi-annual report is available. The Target Fund Prospectus and Target Fund SAI are incorporated herein by reference and are legally deemed to be part of this Information Statement/Prospectus. The Statement of Additional Information to this Information Statement/Prospectus also is incorporated herein by reference and is legally deemed to be part of this Information Statement/Prospectus. The Target Fund Prospectus, Target Fund SAI, Target Fund Annual Report and Target Fund Semi-Annual Report are available at https://www.investcip.com/mutualfundstrategies.html. The Target Fund Prospectus has previously been delivered to Target Fund shareholders.

The prospectuses, statements of additional information, and the most recent annual or semi-annual shareholder report listed above, have been filed with the SEC and are available, free of charge, by (i) calling Convergence (toll free) at 877-677-9414, (ii) accessing the documents at the Fund’s website at https://www.investcip.com/mutualfundstrategies.html, or (iii) writing to the Fund at: Convergence c/o U.S. Bank Global Fund Services, P.O. Box 701, Milwaukee, Wisconsin 53201-0701. In addition, these documents may be obtained from the EDGAR database on the Commission’s Internet site at http://www.sec.gov. You also may obtain this information upon payment of a duplicating fee, by e-mailing the Commission at the following address: publicinfo@sec.gov.

This Information Statement/Prospectus dated January 25, 2022, is expected to be mailed to shareholders of the Target Fund on or about January 28, 2022.

AN INVESTMENT IN THE FUND IS NOT A DEPOSIT OF ANY BANK AND IS NOT INSURED OR GUARANTEED BY THE FEDERAL DEPOSIT INSURANCE CORPORATION OR ANY OTHER

2

GOVERNMENT AGENCY. AN INVESTMENT IN THE FUND INVOLVES INVESTMENT RISK, INCLUDING THE POSSIBLE LOSS OF PRINCIPAL.

LIKE ALL FUNDS, THE COMMISSION HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES OR PASSED UPON THE ADEQUACY OF THIS INFORMATION STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

3

TABLE OF CONTENTS

| SUMMARY | |||||

| What is happening to the Target Fund? | |||||

| How will the Reorganization work? | |||||

| Why is the Reorganization happening and did the Board approve the Reorganization? | |||||

| How will the Reorganization affect me? | |||||

| Who will bear the costs associated with the Reorganization? | |||||

| What are the U.S. federal income tax consequences of the Reorganization? | |||||

| How do the Funds’ investment objectives, investment strategies, and investment policies compare? | |||||

| What are the principal risks of an investment in the Funds? | |||||

| How will the Reorganization affect my fees and expenses? | |||||

| What are the distribution arrangements for the Funds? | |||||

| What are the Funds arrangements for purchases, exchanges and redemptions? | |||||

| COMPARISON OF SOME IMPORTANT FEATURES OF THE FUNDS | |||||

| How do the performance records of the Funds compare? | |||||

| What are the fees and expenses of the Funds and what might they be after the Reorganization? | |||||

| What are the Funds’ dividend payment policies and pricing arrangements? | |||||

| Who manages the Funds? | |||||

| INFORMATION ABOUT THE REORGANIZATION | |||||

| Reasons for the Reorganization | |||||

| INFORMATION ABOUT THE PLAN | |||||

| How will the Reorganization be carried out? | |||||

| Who will pay the costs of the Reorganization? | |||||

| What are the tax consequences of the Reorganization? | |||||

| CAPITAL STRUCTURE AND SHAREHOLDER RIGHTS | |||||

| What are the capitalizations of the Funds? | |||||

| ADDITIONAL INFORMATION ABOUT THE ACQUIRING FUND AND THE TARGET FUND | |||||

| Comparison of the Funds’ Investment Objectives and Principal Investment Strategies | |||||

| Comparison of the Funds’ Principal Risks | |||||

| Description of Principal Risks | |||||

| How do the fundamental investment policies of the Funds compare? | |||||

| Where can I find more financial and performance information about the Funds? | |||||

| PRINCIPAL SHAREHOLDERS | |||||

| ADDITIONAL INFORMATION | |||||

| FINANCIAL HIGHLIGHTS | |||||

| EXHIBIT A - FORM OF AGREEMENT AND PLAN OF REORGANIZATION | A-1 | ||||

| EXHIBIT B - ADDITIONAL INFORMATION ABOUT THE ACQUIRING FUND | B-1 | ||||

4

SUMMARY

This is only a summary of certain information contained in this Information Statement/Prospectus. Shareholders should carefully read the more complete information in the rest of this Information Statement/Prospectus, including the Plan relating to the Reorganization, a form of which is attached to this Information Statement/Prospectus as Exhibit A, the section titled “Additional Information About the Acquiring Fund” which is attached to this Information Statement/Prospectus as Exhibit B. For purposes of this Information Statement/Prospectus, the terms “shareholder”, “you”, and “your” refer to shareholders of the Target Fund.

What is happening to the Target Fund?

The Target Fund, which is currently operated as a mutual fund, will be converted into an ETF through the reorganization of the Target Fund into the Acquiring Fund, a newly-created series of TPM, that has the same investment objective and substantially similar investment strategies as the Target Fund. As an ETF, the Acquiring Fund’s shares will be traded on Cboe BZX Exchange, Inc. The transaction between the Target Fund and the Acquiring Fund is referred to in this Information Statement/Prospectus as a “Reorganization.” The Reorganization will be accomplished in accordance with the Plan.

How will the Reorganization work?

Under the Plan, all of the assets of the Target Fund will be transferred to the Acquiring Fund, in exchange for shares of the Acquiring Fund with an aggregate net asset value (“NAV”) equal to the NAV of the Target Fund shares you held at the time of the Reorganization and the assumption by the Acquiring Fund of all of the liabilities of the Target Fund. Shares of the Acquiring Fund will be transferred to each shareholder’s brokerage account. After shares of the Acquiring Fund are distributed to the Target Fund’s shareholders, the Target Fund will be completely liquidated and dissolved. As a result of the Reorganization, you will cease to be a shareholder of the Target Fund and will become a shareholder of the Acquiring Fund. This exchange will occur on the closing date of the Reorganization, which is the specific date on which the Reorganization takes place. The closing date of the Reorganization is expected to occur after the close of business on or about February 18, 2022.

Why is the Reorganization happening and did the Board approve the Reorganization?

Convergence Investment Partners, LLC (“Convergence”), the investment adviser to both the Target Fund and the Acquiring Fund, proposed that the Target Fund be reorganized into the Acquiring Fund because the ETF structure of the Acquiring Fund may provide benefits, including with respect to the management of capital gains distributions. In a mutual fund, when portfolio securities are sold, either to rebalance holdings or to raise cash for redemptions, the sale can create capital gains that impact all taxable shareholders of the mutual fund. In contrast, the mechanics of the creation and redemption process for ETFs allows ETFs to acquire securities in-kind and redeem securities in-kind generally reducing the realization of capital gains by ETFs for the same processes. As a result, shareholders in an ETF are largely only subject to capital gains on their investment in the ETF after they sell their ETF shares. In addition, unlike the Target Fund, the Acquiring Fund will operate with full portfolio holdings transparency. The Acquiring Fund’s portfolio holdings will be made public each day and can be found on the Acquiring Fund’s website. Some investors may find this advantageous as it may help them decide whether to invest or not; existing and potential shareholders can examine the Acquiring Fund’s portfolio holdings and decide if the specific mix of holdings meets their needs. It also means that shareholders know exactly what companies the Acquiring Fund is investing in at all times. By contrast, in a mutual fund, the fund’s portfolio holdings are only required to be disclosed quarterly.

The Acquiring Fund will pursue the same investment objective and substantially similar investment strategies as the Target Fund but in the ETF structure. Convergence will continue to serve as the investment adviser of the Acquiring Fund after the Reorganization and no change in portfolio managers will result from the Reorganization. The management fee of the Acquiring Fund will be 0.95% of the average daily net assets of the Acquiring Fund, which will be lower than the current management fee of 1.00% of the average daily net assets of the Target Fund. The Acquiring Fund is also expected to experience lower overall expenses as compared to the Target Fund because the Acquiring Fund will have a unitary fee structure under which the Acquiring Fund will pay a management fee to Convergence and Convergence will be responsible for paying operational expenses of the Fund. Currently, the Target Fund pays separate fees to Convergence for investment advisory services and to other service providers for operational expenses. The Board recognizes that as shareholders of an ETF after the Reorganization, shareholders may bear certain costs with respect to maintaining brokerage accounts and selling Acquiring Fund shares that the shareholders did not experience as mutual fund shareholders. However, the Board believes that the benefits of the ETF structure outweigh these costs.

The Board, including all of the Independent Trustees, after careful consideration, have determined that the Reorganization is in the best interests of the Target Fund and will not dilute the interests of the existing shareholders of the Target Fund. The Board made this

5

determination based on various factors that are discussed in this Information Statement/Prospectus, under the discussion of the Reorganization in the section titled “Information About the Reorganization – Reasons for the Reorganization.” Furthermore, the Board, including all of the Independent Trustees, has approved the Reorganization with respect to the Acquiring Fund. The Board has determined that the Reorganization is in the best interests of the Acquiring Fund.

How will the Reorganization affect me?

If the Reorganization is consummated, you will cease to be a shareholder of the Target Fund and will become a shareholder of the Acquiring Fund. Upon completion of the Reorganization, you will own shares of the Acquiring Fund offered as an ETF having an aggregate NAV equal to the aggregate NAV of the shares of the Target Fund you owned when the Reorganization happened. Shares of the Acquiring Fund will be transferred to your brokerage account. Shares of the Acquiring Fund are not issued in fractional shares, so for some shareholders, fractional shares of the Target Fund may be redeemed at NAV immediately prior to the Reorganization resulting in a small cash payment, which will be taxable.

After the Reorganization, individual shares of the Acquiring Fund may only be purchased and sold on Cboe BZX Exchange, Inc., other national securities exchanges, electronic crossing networks and other alternative trading systems through a broker-dealer at market prices. A shareholder may pay brokerage or other charges determined by the shareholder’s financial intermediary, although ETFs do trade with no transaction fees (NTF) on many platforms, and incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase shares (bid) and the lowest price a seller is willing to accept for shares (ask) when buying or selling shares in the secondary market (the “bid-ask spread”). Because Acquiring Fund shares trade at market prices rather than at NAV, Acquiring Fund shares may trade at a price less than (discount) or greater than (premium) the Acquiring Fund’s NAV.

Who will bear the costs associated with the Reorganization?

Convergence will bear all costs incurred in connection with the Reorganization.

What are the U.S. federal income tax consequences of the Reorganization?

As a condition to the closing of the Reorganization, the Target Fund and the Acquiring Fund must receive an opinion of Godfrey & Kahn, S.C. (“Godfrey & Kahn”), legal counsel to TPM, to the effect that the Reorganization will constitute a “reorganization” within the meaning of Section 368 of the Internal Revenue Code of 1986, as amended (the “Code”). Accordingly, it is expected that neither you nor, in general, the Target Fund or the Acquiring Fund will recognize gain or loss as a direct result of the Reorganization of the Target Fund (except with respect to cash received by a shareholder in lieu of fractional shares, if any), and the holding period and aggregate tax basis for the Acquiring Fund shares that you receive will be the same as the holding period and aggregate tax basis of the Target Fund shares that you surrender in the Reorganization. Prior to the consummation of the Reorganization, you may redeem your Target Fund shares, generally resulting in the recognition of gain or loss for U.S. federal income tax purposes.

You should consult your tax advisor regarding the effect, if any, of the Reorganization, in light of your individual circumstances. You should also consult your tax advisor about state, local or foreign tax consequences. For more information about the tax consequences of the Reorganization, please see the section “Information About the Plan—What are the tax consequences of the Reorganization?”.

How do the Funds’ investment objectives, investment strategies, and investment policies compare?

The Target Fund and the Acquiring Fund have identical investment objectives. Each Fund’s investment objective is non-fundamental and may be changed by the sole action of the Board, without shareholder approval. Although the Target Fund and the Acquiring Fund describe their principal investment strategies somewhat differently, each Fund employs substantially similar principal investment strategies in seeking to achieve their respective investment objectives.

Investment Objectives and Investment Strategies

The investment objective of the Target Fund and the Acquiring Fund is to seek long-term capital growth. Each of the Target Fund and Acquiring Fund pursue their investment objective by investing, under normal market conditions, at least 80% of its net assets (plus any borrowings for investment purposes) in long and short positions in equity securities of domestic companies. Each Fund focuses primarily on companies with medium and large market capitalizations, although each Fund may establish long and short positions in companies of any market capitalization.

6

In making investment decisions for each Fund, Convergence utilizes a proprietary stock ranking process. For each Fund, Convergence systematically measures both current factor exposures for company stocks and the market’s factor preferences and tilts the portfolio towards stocks that are ranked highly from a fundamental perspective. The factors which Convergence employs for each Fund include valuation, growth, momentum and quality. The principal investment strategies for the Acquiring Fund provide additional disclosure on how Convergence evaluates valuation, growth, momentum and quality for the Acquiring Fund. For further information, please see “Exhibit B – Additional Information About the Acquiring Fund – Investment Strategies, Related Risks and Disclosure of Portfolio Holdings.”

Investment Policies and Restrictions

The Target Fund and the Acquiring Fund have adopted identical fundamental investment restrictions, which may not be changed without prior shareholder approval. The Target Fund’s fundamental investment restrictions are listed in the Target Fund’s SAI dated March 30, 2021, which is incorporated by reference into the statement of additional information relating to this Information Statement/Prospectus, and is available upon request. For further information please see “Additional Information About the Acquiring Fund and the Target Fund - How do the fundamental investment policies of the Funds compare?”.

What are the principal risks of an investment in the Funds?

An investment in the Target Fund or the Acquiring Fund involves risks common to most open-end funds. There is no guarantee against losses resulting from investments in the Funds, nor that the Funds will achieve their investment objectives. You may lose money if you invest in the Funds. The risks associated with an investment in the Target Fund and the Acquiring Fund are identical, except that the Acquiring Fund is subject to certain risks unique to operating as an ETF. The Acquiring Fund is subject to the following risks for an ETF:

ETF Risks. The Acquiring Fund is an ETF, and, as a result of an ETF’s structure it is exposed to the following risks:

*Authorized Participants, Market Makers, and Liquidity Providers Concentration Risk. The Fund has a limited number of financial institutions that may act as Authorized Participants (“APs”). In addition, there may be a limited number of market makers and/or liquidity providers in the marketplace. To the extent either of the following events occur, shares of the Fund (“Shares”) may trade at a material discount to NAV and possibly face delisting: (i) APs exit the business or otherwise become unable to process creation and/or redemption orders and no other APs step forward to perform these services, or (ii) market makers and/or liquidity providers exit the business or significantly reduce their business activities and no other entities step forward to perform their functions.

*Cash Redemption Risk. The Fund’s investment strategy may require it to redeem Shares for cash or to otherwise include cash as part of its redemption proceeds. The Fund may be required to sell or unwind portfolio investments to obtain the cash needed to distribute redemption proceeds. This may cause the Fund to realize a capital gain that it might not have realized if it had made a redemption in-kind. As a result, the Fund may pay out higher annual capital gain distributions than if the in-kind redemption process was used. To the extent that the transaction fees charged for redemptions of creation units is insufficient to cover the Fund’s transaction costs of selling portfolio securities, the Fund’s performance could be negatively impacted.

*Costs of Buying or Selling Shares. Due to the costs of buying or selling Shares, including brokerage commissions imposed by brokers and bid/ask spreads, frequent trading of Shares may significantly reduce investment results and an investment in Shares may not be advisable for investors who anticipate regularly making small investments.

*Shares May Trade at Prices Other Than NAV. As with all ETFs, Shares may be bought and sold in the secondary market at market prices. As a result, investors in the Fund may pay significantly more or receive significantly less for Shares than the Fund’s NAV. Although it is expected that the market price of Shares will approximate the Fund’s NAV, there may be times when the market price of Shares is more than the NAV intra-day (premium) or less than the NAV intra-day (discount) due to supply and demand of Shares or during periods of market volatility. This risk is heightened in times of market volatility, periods of steep market declines, and periods when there is limited trading activity for Shares in the secondary market, in which case such premiums or discounts may be significant. Such conditions may also cause the bid/ask spreads for an ETF to widen.

*Trading. Although Shares are listed for trading on the Exchange and may be traded on U.S. exchanges other than the Exchange, there can be no assurance that Shares will trade with any volume, or at all, on any stock exchange. In stressed market conditions, the liquidity of Shares may begin to mirror the liquidity of the Fund’s underlying portfolio holdings, which can be significantly less liquid than Shares. This could lead to an increase in the bid/ask spread for the Shares or the Shares trading at a price that is higher or lower than the Fund’s NAV.

7

For further information about the risks of investments in the Funds, see “Additional Information About the Acquiring Fund and the Target Fund - Comparison of the Funds’ Principal Risks” below.

How will the Reorganization affect my fees and expenses?

The management fee of the Acquiring Fund will be 0.95% of the average daily net assets of the Fund, which is lower than the current management fee of 1.00% of the average daily net assets of the Target Fund. In addition, the Acquiring Fund is expected to experience lower overall expenses as compared to the Target Fund because the Acquiring Fund will have a unitary fee structure under which the Acquiring Fund will pay a management fee to Convergence and Convergence will be responsible for paying all expenses of the Acquiring Fund except interest charges on any borrowings, dividends and other expenses on securities sold short, taxes, brokerage commissions and other expenses incurred in placing orders for the purchase and sale of securities, acquired fund fees and expenses, accrued deferred tax liability, extraordinary expenses, distribution fees and expenses paid by the Fund under any distribution plan adopted pursuant to Rule 12b-1 under the 1940 Act, and the unitary management fee payable to Convergence. Currently, the Target Fund pays separate fees to Convergence for investment advisory services and to other service providers for operational expenses. A comparison of the fees and expenses of the Target Fund and Acquiring Fund is provided below under the heading, “Comparison of Some Important Features of the Funds - What are the fees and expenses of the Funds and what might they be after the Reorganization?”.

What are the distribution arrangements for the Funds?

The principal underwriter to the Target Fund is Quasar Distributors, LLC (“Quasar”), located at 111 East Kilbourn Avenue, Suite 2200, Milwaukee, Wisconsin 53202. Foreside Fund Services, LLC (“Foreside”), located at Three Canal Plaza, Suite 100, Portland, Maine 04101, will serve as the principal underwriter to the Acquiring Fund. Quasar and Foreside are both controlled by Foreside Financial Group, LLC.

What are the Funds’ arrangements for purchases, exchanges and redemptions?

The Target Fund and the Acquiring Fund have different procedures for purchasing and redeeming shares. You may refer to Exhibit B of this Information Statement/Prospectus, under the section titled “How to Buy & Sell Shares” for the procedures applicable to purchases and sales of the shares of the Acquiring Fund, which are also summarized below. The Target Fund Prospectus provides information under the sections titled “Shareholder Information - How to Purchase Shares” and “Shareholder Information - How to Redeem Shares” with respect to the procedures applicable to purchases and sales of the shares of the Target Fund, which are also summarized below.

Shares of the Target Fund are available for purchase in a brokerage account through a broker. Shares of the Target Fund are not available for purchase directly from U.S. Bancorp Fund Services, LLC, the transfer agent to the Target Fund. Shareholders of the Target Fund may purchase or sell (redeem) shares of the Target Fund on each day that the New York Stock Exchange (“NYSE”) is scheduled to be open for business by contacting their financial intermediary regarding purchase and redemption procedures.

The purchase price of a share of the Target Fund is its NAV per share. The NAV per share of the Target Fund is calculated after the close of the NYSE (normally, 4:00 p.m. Eastern Time) on each day the NYSE is open. Shares of the Target Fund will be priced at the public offering price, which is the NAV of the shares next determined after receipt of the investor’s order. The Target Fund reserves the right to reject any initial or subsequent investment request.

Unlike the Target Fund, individual shares of the Acquiring Fund are not purchased or sold at NAV. The Acquiring Fund will issue (or redeem) shares at NAV only to certain financial institutions that have entered into agreements with the Acquiring Fund’s distributor, Foreside, in large aggregated blocks known as “Creation Units.” The Acquiring Fund generally issues and redeems Creation Units in exchange for a portfolio of securities closely approximating the holdings of the Acquiring Fund (the “Deposit Securities”) and/or a designated amount of U.S. cash.

Shares of the Acquiring Fund are listed on the Cboe BZX Exchange, Inc., and individual Shares may only be purchased and sold in the secondary market through a broker or dealer at market prices, rather than NAV. Because Shares trade at market prices rather than NAV, Shares may trade at a price greater than NAV (premium) or less than NAV (discount). Shares of the Acquiring Fund can be bought and sold during the day like shares of other publicly traded companies When buying or selling shares of the Acquiring Fund through a broker, you will incur customary brokerage commissions and charges, and you may pay some or all of the spread between the bid and the offer price in the secondary market on each leg of a round trip (purchase and sale) transaction. The commission is frequently a fixed amount and may be a significant proportional cost for investors seeking to buy or sell small amounts of shares. The spread with respect to shares of the Acquiring Fund varies over time based on the Fund’s trading volume and market liquidity and is generally lower if the

8

Acquiring Fund has a lot of trading volume and market liquidity and higher if the Acquiring Fund has little trading volume and market liquidity.

Neither the Target Fund nor the Acquiring Fund permits exchanges of shares of the Fund for shares of another fund.

9

COMPARISON OF SOME IMPORTANT FEATURES OF THE FUNDS

How do the performance records of the Funds compare?

The Acquiring Fund is a newly-formed “shell” fund that has not yet commenced operations, and therefore, has no performance history predating the Reorganization. The Acquiring Fund has been organized solely in connection with the Reorganization to acquire all of the assets and liabilities of the Target Fund and continue the business of the Target Fund. Therefore, after the Reorganization, the Target Fund will remain the “accounting survivor.” This means that the Acquiring Fund will continue to show the historical investment performance and returns of the Target Fund (even after the Target Fund’s liquidation).

The historical performance of the Target Fund, as it is to be adopted by the Acquiring Fund, is shown below and will be included in the Acquiring Fund’s Prospectus. The performance information below demonstrates the risks of investing in the Target Fund by showing changes in the Target Fund’s performance from year to year and by showing how the Target Fund’s average annual returns for the one-year, five-year and ten-year periods compare with those of a broad measure of market performance. Remember, the Target Fund’s past performance, before and after taxes, is not necessarily an indication of how the Target Fund or Acquired Fund will perform in the future.

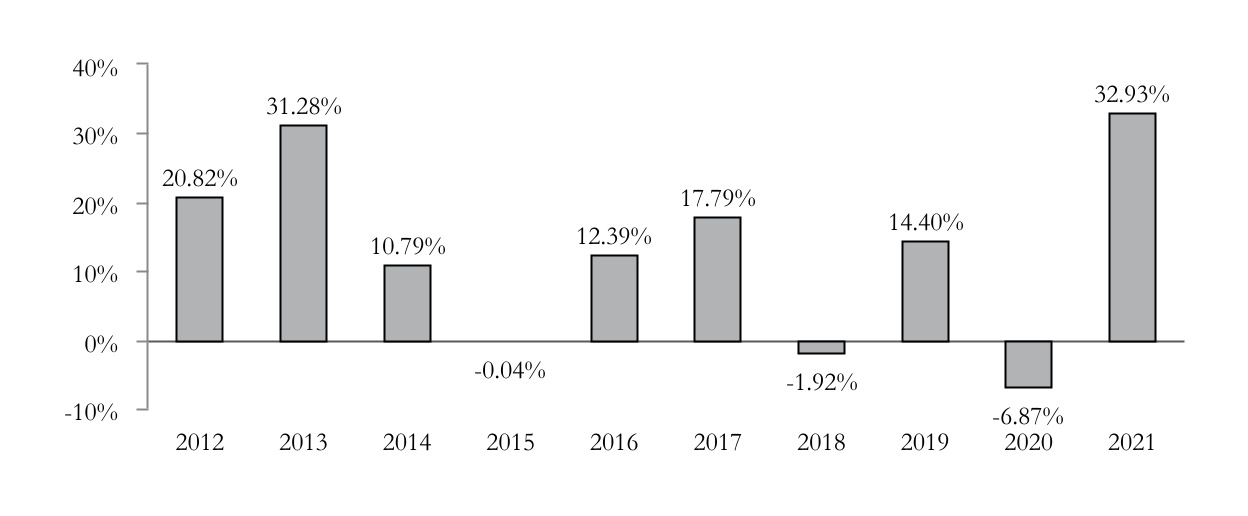

Calendar Year Returns as of December 31

During the period shown in the bar chart, the best performance for a quarter was 15.83% (for the quarter ended March 31, 2012). The worst performance was -18.08% (for the quarter ended March 31, 2020).

Average Annual Total Returns (Periods Ended December 31, 2021) | |||||||||||

| One Year | Five Years | Ten Years | |||||||||

| Return Before Taxes | 32.93% | 10.35% | 12.44% | ||||||||

| Return After Taxes on Distributions | 26.74% | 6.60% | 9.82% | ||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | 21.63% | 7.05% | 9.45% | ||||||||

Russell 3000® Total Return Index (reflects no deduction for fees, expenses or taxes) | 25.66% | 17.97% | 16.30% | ||||||||

Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are calculated using the historical highest individual federal marginal income tax rates in effect and do not reflect the effect of state and local taxes. The after-tax returns shown are not relevant to investors who hold their shares through tax-deferred or other tax-advantaged arrangements such as 401(k) plans or individual retirement accounts (“IRA”).

In certain cases, the figure representing “Return After Taxes on Distributions and Sale of Fund Shares” may be higher than the other return figures for the same period. A higher after-tax return results when a capital loss occurs upon redemption and provides an assumed tax benefit to the investor.

10

What are the fees and expenses of the Funds and what might they be after the Reorganization?

Shareholders of the Funds pay various fees and expenses, either directly or indirectly. The tables below show the fees and expenses that you would pay if you were to buy, hold or sell shares of each Fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below. The fees and expenses in the tables appearing below are based on the expenses of the Target Fund for the fiscal year ended November 30, 2020 and the anticipated expenses of the Acquiring Fund during its first year of operation. The tables also show the pro forma expenses of the Acquiring Fund after giving effect to the Reorganization, based on pro forma net assets as of December 31, 2021. Pro forma numbers are estimated in good faith and are hypothetical. Actual expenses may vary significantly. You will not pay any sales load, contingent deferred sales charge, brokerage commission, redemption fee, or other transaction fee in connection with the receipt of Acquiring Fund shares from the Reorganization.

Target Fund | Acquiring Fund | Pro Forma—Acquiring Fund after Reorganization | |||||||||

Shareholder Fees (fees paid directly from your investment): | None | None | None | ||||||||

Annual Fund Operating Expenses for the Target Fund and the Acquiring Fund (expenses deducted from Fund assets)

Target Fund (Convergence Long/Short Equity Fund) | Acquiring Fund (Convergence Long/Short Equity ETF) | Pro Forma—Acquiring Fund after Reorganization | |||||||||

| Management Fee | 1.00% | 0.95%* | 0.95%* | ||||||||

| Other Expenses | |||||||||||

| Dividends and Interest on Short Positions** | 0.89% | 0.89% | 0.89% | ||||||||

| Remainder of Other Expenses | 0.69% | 0.00% | 0.00% | ||||||||

| Total Annual Fund Operating Expenses | 2.58% | 1.84% | 1.84% | ||||||||

| Fees Waived / Expenses Reimbursed | (0.19)%*** | 0.00% | 0.00% | ||||||||

| Total Annual Fund Operating Expenses After Fee Waiver | 2.39% | 1.84% | 1.84% | ||||||||

* The Acquiring Fund will have a unitary fee structure under which both operating expenses and management fees will be paid.

** “Dividends and Interest on Short Positions” reflect interest expense and dividends paid on borrowed securities. Interest expenses result from a Fund’s use of prime brokerage arrangements to execute short sales. Dividends paid on borrowed securities are an expense of short sales. These expenses are required to be treated as a Fund expense for accounting purposes and are not payable to Convergence. Any interest expense amount or dividends paid on securities sold short will vary based on a Fund’s use of those investments as an investment strategy best suited to seek the investment objective of the Fund.

*** Pursuant to an operating expense limitation agreement between Convergence and TPM, on behalf of the Target Fund, Convergence has agreed to waive its management fees and/or reimburse expenses of the Target Fund to ensure that Total Annual Fund Operating Expenses (excluding any front-end or contingent deferred loads, Rule 12b-1 plan fees, shareholder servicing plan fees, taxes, leverage expenses (i.e., any expenses incurred in connection with borrowings made by the Target Fund), interest (including interest incurred in connection with bank and custody overdrafts), brokerage commissions and other transactional expenses, acquired fund fees and expenses, dividends or interest expenses on short positions, expenses incurred in connection with any merger or reorganization, or extraordinary expenses such as litigation, (collectively, “Excluded Expenses”)) do not exceed 1.50% of the Target Fund’s average daily net assets, through at least March 30, 2022, and subject thereafter to annual re-approval of the agreement by the Board. To the extent the Target Fund incurs Excluded Expenses, Total Annual Operating Expenses After Fee Waiver and/or Expense Reimbursement is greater than 1.50%.

11

Target Fund liabilities to be assumed by the Acquiring Fund shall not include any liabilities, costs or charges relating to fee waiver and expense reimbursement arrangements between TPM, on behalf of the Target Fund and Convergence (including any potential recoupment by Convergence of any fees or expenses of the Target Fund previously waived or reimbursed.

Expense Examples

This Example is meant to help you compare the cost of investing in the Acquiring Fund with the cost of investing in the Target Fund.

The Example assumes that you invest $10,000 in the Funds for the time periods indicated. The Example also assumes that your investment has a 5% return each year and that a Fund’s operating expenses remain the same (taking into account the Target Fund’s contractual expense limitation agreement in place for one year). Although your actual costs may be higher or lower, based on these assumptions, your costs whether you redeem or hold your shares would be:

| 1 Year | 3 Years | 5 Years | 1 0 Years | |||||||||||

Target Fund - Convergence Long/Short Equity Fund | $242 | $784 | $1,353 | $2,901 | ||||||||||

Acquiring Fund - Convergence Long/Short Equity ETF | $187 | $579 | $995 | $2,159 | ||||||||||

| Pro Forma—Acquiring Fund after Reorganization | $187 | $579 | $995 | $2,159 | ||||||||||

What are the Funds’ dividend payment policies and pricing arrangements?

Each Fund intends to make distributions of net investment income and net capital gain, if any, at least annually, typically during the month of December. Each Fund will declare and pay income and capital gain distributions in cash.

The way that dividends are received differs between the Target Fund and Acquiring Fund. Shareholders of the Target Fund automatically receive all income dividends and capital gains distributions in additional shares of the Target Fund at NAV, unless a shareholder chooses to either (1) receive distributions of net capital gain in cash, while reinvesting net investment income distributions in additional Fund shares; (2) receive all distributions in cash; or (3) reinvest net capital gain distributions in additional Fund shares, while receiving distributions of net investment income in cash. Shareholders of the Acquiring Fund will receive all income dividends and capital gains distributions in cash, unless a shareholder’s broker provides an option for the reinvestment of dividends.

The Target Fund and Acquiring Fund have substantially the same procedures for calculating their share prices. The Funds determine their NAV per share after the close of the NYSE (normally, 4:00 p.m., Eastern Time). The Funds will not be priced on days that the NYSE is closed for trading. The Board has adopted identical policies and procedures for valuing the Funds’ portfolio assets. The Funds’ investments are valued at their current market value or, if market quotations are not readily available, at their fair value as determined in accordance with procedures adopted by the Board.

For more information about the Acquiring Fund pricing procedures, you may refer to “Exhibit B - Additional Information About the Acquiring Fund” in this Information Statement/Prospectus, under the section titled “Determination of Net Asset Value.”

Who manages the Funds?

The Investment Adviser

Convergence Investment Partners, LLC, a Delaware limited liability company located at 3801 PGA Boulevard, Suite 1001, Palm Beach Gardens, Florida 33410 has entered into an advisory agreement with both the Target Fund and the Acquiring Fund. Convergence is a registered investment adviser founded in November 2004 as QIS Advisors, LLC (“QIS Advisors”). On December 16, 2008, the firms’s name was changed to Mariner Quantitative Solutions, LLC. On January 27, 2011, the firm’s name was changed to Convergence Investment Partners, LLC. Since February 2005, Convergence has managed separate accounts and other pooled investment vehicles using a long/short investment strategy similar to the strategy implemented with the Funds. As of October 31, 2021, Convergence had approximately $224 million in assets under management. Convergence is majority-owned by Nile Capital Group, LLC, a Delaware limited liability company.

Subject to the overall supervision of the Board, Convergence manages the overall investment operations of the Funds in accordance with the Funds’ investment objective and policies and formulates a continuing investment strategy for each Fund pursuant to the terms of an

12

investment advisory agreement between TPM and Convergence (the “Advisory Agreement”). Other than the unitary fee structure, there are no material differences between the Advisory Agreement of the Target Fund and the Acquiring Fund.

The Portfolio Managers

The Target Fund and the Acquiring Fund have the same portfolio managers. Mr. David J. Abitz and Mr. Justin Neuberg are each a portfolio manager of the Funds and are jointly and primarily responsible for the day-to-day management of the Fund’s investment portfolio.

David J. Abitz, CFA, founded QIS Advisors, the predecessor firm to Convergence, in 2004. Mr. Abitz has more than two decades of investment experience and is the President and Chief Investment Officer of Convergence. Prior to founding Convergence, Mr. Abitz was Chief Investment Officer of the Custom Quantitative Solutions Group at M&I Investment Management Corporation from 2000 to 2004, where he managed the Marshall Equity Income Fund, Tax Efficient Portfolios, M&I High Dividend Income Portfolios and the M&I Long/Short Fund. Mr. Abitz began his career at M&I Investment Management Corporation as a fundamental equity research analyst and an equity trader. Mr. Abitz is a Chartered Financial Analyst with a BBA in Finance from the University of Wisconsin – Oshkosh and an MBA from the University of Wisconsin – Madison. He is a member of the Society of Quantitative Analysts, the Chicago Quantitative Alliance group, and the Chartered Financial Analyst (“CFA”) Society of South Florida.

Justin Neuberg, CFA, Portfolio Manager, joined Convergence in 2014. Mr. Neuberg has worked in the financial services industry since 2002 and has an extensive background in investment analytics. Prior to joining the firm, Mr. Neuberg was an analyst and portfolio strategist at Mariner Wealth Advisors from 2009 to 2013, where he was a member of the Mariner Assets Allocation Committee. Mr. Neuberg has a bachelor’s degree in physics from the University of Virginia and a Master of Business Administration degree with a concentration in finance from Georgetown University. Mr. Neuberg is a Chartered Financial Analyst with a professional certificate in finance from the University of California at San Diego. Mr. Neuberg is a member of the CFA Society of South Florida.

CFA® and Chartered Financial Analyst® are registered trademarks owned by the CFA Institute.

Target Fund Operating Expense Limitation Agreement

Under the terms of an operating expense limitation agreement entered into by TPM, on behalf of the Target Fund, and Convergence, Convergence has contractually agreed to waive its management fees and/or reimburse expenses of the Target Fund to ensure that Total Annual Fund Operating Expenses (excluding any Excluded Expenses) do not exceed 1.50% of the Target Fund’s average daily net assets, through at least March 30, 2022, and subject thereafter to annual re-approval of the agreement by the Board. To the extent the Target Fund incurs Excluded Expenses, Total Annual Operating Expenses After Fee Waiver and/or Expense Reimbursement is greater than 1.50%. The operating expense limitation agreement may be terminated only by, or with the consent of, the Board.

The liabilities of the Target Fund to be assumed by the Acquiring Fund shall not include any liabilities, costs or charges relating to fee waiver and expense reimbursement arrangements between TPM, on behalf of the Target Fund, and Convergence (including any potential recoupment by Convergence of any fees or expenses of the Target Fund previously waived or reimbursed). Due to the unitary fee structure of the Acquiring Fund, Convergence has not entered into an operating expense limitation agreement with TPM, on behalf of the Acquiring Fund.

INFORMATION ABOUT THE REORGANIZATIONS

Reasons for the Reorganization

Convergence proposed that the Target Fund be reorganized into the Acquiring Fund because the ETF structure of the Acquiring Fund may provide benefits with respect to the management of capital gains distributions. In a mutual fund, such as the Target Fund, when portfolio securities are sold, either to rebalance holdings or to raise cash for redemptions, the sale can create capital gains that impact all taxable shareholders of the mutual fund. In contrast, the mechanics of the creation and the redemption process for ETFs allows ETFs to acquire securities in-kind and redeem securities in-kind generally reducing the realization of capital gains by the ETFs for the same processes. As a result, shareholders in an ETF are largely only subject to capital gains on their investment in the ETF after they sell their ETF shares.

The Acquiring Fund will pursue the same investment objective and substantially similar investment strategies as the Target Fund but have the risks and benefits of operating in the ETF structure. Convergence will continue as the investment adviser of the Acquiring Fund after the Reorganization and no change in portfolio managers will result from the Reorganization. In addition, the Acquiring Fund will have a lower management fee than the Target Fund. The Acquiring Fund is also expected to experience lower overall expenses as compared to the Target Fund under its unitary fee structure.

13

The Board considered the Reorganization and approved the Plan with respect to the Target Fund. In considering the Plan, the Board requested and received detailed information from Convergence regarding the Reorganization, including: (1) the specific terms of the Plan; (2) the investment objectives, investment strategies, and investment policies of the Target Fund and the Acquiring Fund; (3) comparative data analyzing the fees and expenses of the Funds; (4) the proposed plans for ongoing management, distribution, and operation of the Acquiring Fund; (5) the management, financial position, and business of Convergence and its affiliates; and (6) the impact of the Reorganization on the Target Fund and its shareholders.

With respect to the information listed above, the Board considered that, among other information: (1) the Reorganization was designed to be a tax-free reorganization and the shares of the Acquiring Fund that would be received by the shareholders of the Target Fund in the exchange will be equal in aggregate NAV to the aggregate NAV of their shares of the Target Fund as of the closing date of the Reorganization; (2) the investment objectives and policies of the Target Fund and the Acquiring Fund are identical and the investment strategies are substantially similar; (3) the management fee of the Acquiring Fund is lower than the management fee of the Target Fund, and the Acquiring Fund is expected to experience lower overall expenses as compared to the Target Fund under its unitary fee structure; (4) the plans for the ongoing management, distribution, and operation of the Acquiring Fund as an ETF will benefit tax conscious shareholders; and (5) Convergence is the adviser of both the Target Fund and Acquiring Fund and the terms of the investment advisory agreements are materially the same other than with respect to the investment advisory fees. The Board also considered that the Reorganization met the conditions under Rule 17a-8 under the 1940 Act to be consummated without the vote of shareholders of the Target Fund or Acquiring Fund.

In approving the Reorganization with respect to the Target Fund, the Board, including all of the Independent Trustees, determined that (i) participation in the Reorganization is in the best interest of the Target Fund’s shareholders, and (ii) the interests of the Target Fund’s shareholders will not be diluted as a result of the Reorganization.

In making these determinations, the Board, including all of the Independent Trustees, considered a number of factors, including the potential benefits and costs of the Reorganization to the shareholders of the Target Fund. These considerations included the following:

•The same investment adviser and portfolio managers that currently manage the Target Fund are expected to manage the Acquiring Fund following the closing of the Reorganization;

•The management fee of the Acquiring Fund is lower than the management fee of the Target Fund, and the Acquiring Fund is expected to experience lower overall expenses as compared to the Target Fund under its unitary fee structure;

•Other than with respect to the management fee, there are no material differences in the contractual terms of the Target Fund’s investment advisory agreement with Convergence as compared to the Acquiring Fund’s investment advisory agreement, and Convergence does not anticipate that the Reorganization will result in any decline in the level of services from the level of services that historically have been provided to the Target Fund;

•The investment objectives and investment policies of the Target Fund and the Acquiring Fund are identical and the investment strategies are substantially similar;

•Convergence will bear all costs incurred in connection with the Reorganization;

•The ETF structure of the Acquiring Fund may provide benefits with respect to the management of capital gains distributions;

•All shareholders of the Target Fund hold their shares in a brokerage account that is permitted to hold Acquiring Fund shares;

•A vote of shareholders of the Target Fund is not required under TPM’s governing documents or the 1940 Act;

•Except with respect to any cash payment received in lieu of fractional shares, the Reorganization is intended to be tax-free for U.S. federal income tax purposes for shareholders of the Target Fund;

14

•The Acquiring Fund does not issue fractional shares so for some shareholders, fractional shares of the Target Fund will be redeemed at NAV immediately prior to the Reorganization and result in a small cash payment, which will be taxable for U.S. federal income tax purposes; and

•Shareholders of the Target Fund may redeem their shares of the Target Fund prior to the Reorganization if the shareholders do not wish to hold shares of an ETF.

Based upon their evaluation of the relevant information presented to it, and in light of its fiduciary duties under federal and state law, the Board, including all of the Independent Trustees, concluded that completing the Reorganization is in the best interests of the shareholders of the Target Fund and that no dilution of value would result to the shareholders of the Target Fund from the Reorganization.

INFORMATION ABOUT THE PLAN

This is only a summary of the Plan. You should read the form of the Plan, which is attached as Exhibit A to this Information Statement/Prospectus, for complete information about the Reorganization.

How will the Reorganization be carried out?