As filed with the Securities and Exchange Commission on November 16, 2015

1933 Act Registration File No. 333-207499

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

[X] Pre-Effective Amendment No. 1

[ ] Post-Effective Amendment No.

(Check appropriate box or boxes)

Pacific Funds Series Trust

(formerly named Pacific Life Funds)

(Exact Name of Registrant as Specified in Charter)

700 Newport Center Drive

P.O. Box 7500

Newport Beach, CA 92660

(Address of Principal Executives Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (949) 219-3202

Audrey L. Cheng, Esq.

Pacific Life Insurance Company

700 Newport Center Drive

Post Office Box 9000

Newport Beach, CA 92660

(Name and Address of Agent for Service)

Copy to:

Anthony H. Zacharski, Esq.

Dechert LLP

90 State House Square

Hartford, CT 06103-3702

Approximate Date of Proposed Public Offering: As soon as practicable after the Registration Statement becomes effective under the Securities Act of 1933, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until such date as the Commission, acting pursuant to said Section 8(a), may determine that the Registration Statement shall become effective.

Title of Securities Being Registered: Class A, Class C, Advisor Class, Class P, Institutional Class and Investor Class shares of Pacific Funds Small/Mid-Cap, Pacific Funds Small-Cap, Pacific Funds Small-Cap Value and Pacific Funds Small-Cap Growth, each a series of the Registrant.

No filing fee is due because the Registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an indefinite number of securities.

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Letter to Shareholders

Notice of Special Meeting

Questions and Answers

Part A - Combined Proxy Statement and Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibit

PROFESSIONALLY MANAGED PORTFOLIOS

Rothschild U.S. Small/Mid-Cap Core Fund

Rothschild U.S. Small-Cap Core Fund

Rothschild U.S. Small-Cap Value Fund

Rothschild U.S. Small-Cap Growth Fund

615 East Michigan Street

Milwaukee, WI 53202

November 20, 2015

Dear Shareholders:

The Board of Trustees (the “Board”) of Professionally Managed Portfolios (the “Trust”) has approved proposals from Rothschild Asset Management Inc. (“Rothschild”) to reorganize the Rothschild U.S. Small/Mid-Cap Core Fund, Rothschild U.S. Small-Cap Core Fund, Rothschild U.S. Small-Cap Value Fund and Rothschild U.S. Small-Cap Growth Fund (each, a “Rothschild Fund” and together, the “Rothschild Funds”), each a series of the Trust, into newly-created corresponding series (as listed below, each, a “PF Fund”) of Pacific Funds Series Trust (the “Pacific Funds Trust”), each with substantially similar investment policies and objectives as its corresponding Rothschild Fund (each a “Reorganization”, and together, the “Reorganizations”).

A joint Special Meeting of the Shareholders of each Rothschild Fund is to be held at 9:00 a.m. Pacific time, on December 16, 2015 at the offices of U.S. Bancorp Fund Services, LLC, 2020 E. Financial Way, Suite 100, Glendora, CA 91741, where you, as a shareholder of a Rothschild Fund, will be asked to vote on the proposal to merge and reorganize your Rothschild Fund with its corresponding PF Fund. The merger of each Rothschild Fund into its corresponding PF Fund will be treated as a separate Reorganization. Accordingly, shareholder approval and consummation of each Reorganization are not contingent on shareholder approval and consummation of any other Reorganization. A Combined Proxy Statement and Prospectus (the “Proxy Statement”) regarding the meeting, a proxy card for your vote at the meeting and a postage-prepaid envelope in which to return your proxy card are enclosed.

The primary purpose of the Reorganizations is to move the Rothschild Funds, along with other funds managed by Rothschild within the Trust, to the Pacific Funds Trust family of funds. The Reorganizations will result in management oversight responsibility for the Rothschild Funds becoming the responsibility of Pacific Life Fund Advisors LLC (the “Adviser”), while retaining Rothschild as the sub-adviser to the PF Funds. The Adviser is an experienced provider of investment advisory services to institutional and retail investors, with approximately $53 billion in mutual fund assets under management. Rothschild has proposed the Reorganizations because it believes that the Reorganizations have the potential to expand each Rothschild Fund’s presence in more distribution channels and increase its asset base over time.

The PF Funds’ Board of Trustees has approved the engagement of Rothschild as the sub-adviser to the PF Funds, and the portfolio managers of the Sub-Adviser who are primarily responsible for the day-to-day portfolio management of the Rothschild Funds are expected to remain substantially the same.

The advisory fees paid by the PF Funds would be the same as the advisory fees paid by the Rothschild Funds. In addition, the Adviser has contractually agreed to limit certain operating expenses incurred by the PF Funds for three years following the closing date of the Reorganizations. Accordingly, the Reorganizations will not result in any increase to the advisory fees or the overall net expense ratios (excluding extraordinary expenses) of the PF Funds for three years following the closing of the Reorganizations, as compared to the net expense ratios currently paid by the Rothschild Funds.

If approved by shareholders, each Reorganization is scheduled to take effect on or about January 11, 2016. At that time, the Rothschild Fund Investor Class shares or Institutional Class shares that you currently own would,

in effect, be exchanged on a tax-free basis for, respectively, Investor Class and Institutional Class shares of the corresponding PF Fund with the same aggregate value, as follows:

| Reorganization No. |

Rothschild Fund |

PF Fund | ||||

| (1) | Rothschild U.S. Small/Mid-Cap Core Fund | Pacific Funds Small/Mid-Cap | ||||

| Investor Class shares Institutional Class shares |

g g |

Investor Class shares Institutional Class shares | ||||

| (2) | Rothschild U.S. Small-Cap Core Fund | Pacific Funds Small-Cap | ||||

| Investor Class shares Institutional Class shares |

g g |

Investor Class shares Institutional Class shares | ||||

| (3) | Rothschild U.S. Small-Cap Value Fund | Pacific Funds Small-Cap Value | ||||

| Investor Class shares Institutional Class shares |

g g |

Investor Class shares Institutional Class shares | ||||

| (4) | Rothschild U.S. Small-Cap Growth Fund | Pacific Funds Small-Cap Growth | ||||

| Investor Class shares Institutional Class shares |

g g |

Investor Class shares Institutional Class shares | ||||

No sales loads, commissions or other transactional fees will be imposed on shareholders in connection with the tax-free exchange of their shares.

The Board of Trustees of the Trust unanimously approved the proposed Reorganizations, subject to shareholder approval.

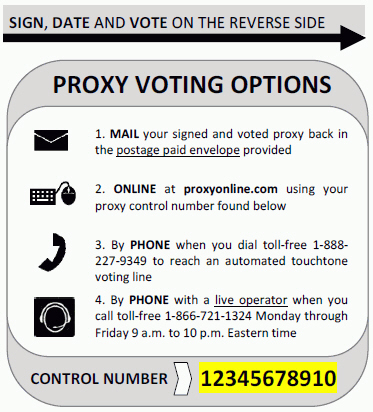

Detailed information about the proposal is contained in the enclosed materials. Whether or not you plan to attend the meeting in person, we need your vote. Once you have decided how you will vote, please promptly complete, sign, date and return the enclosed proxy card or vote by phone or via the internet by following the instructions on the enclosed proxy card. If you have any questions regarding the proposals to be voted on, please do not hesitate to call (866) 721-1324. Representatives are available to assist you Monday through Friday 9 a.m. to 10 p.m. Eastern time.

Your vote is very important to us. Thank you for your response and for participation in this important matter.

Respectfully,

| /s/ Elaine E. Richards | ||

| Elaine E. Richards, Esq. | ||

| President | ||

| Professionally Managed Portfolios | ||

PROFESSIONALLY MANAGED PORTFOLIOS

ROTHSCHILD U.S. SMALL/MID-CAP CORE FUND

ROTHSCHILD U.S. SMALL-CAP CORE FUND

ROTHSCHILD U.S. SMALL-CAP VALUE FUND

ROTHSCHILD U.S. SMALL-CAP GROWTH FUND

615 East Michigan Street

Milwaukee, WI 53202

NOTICE OF SPECIAL MEETING OF

SHAREHOLDERS TO BE HELD December 16, 2015

To the Shareholders of the Rothschild U.S. Small/Mid-Cap Core Fund, Rothschild U.S. Small-Cap Core Fund, Rothschild U.S. Small-Cap Value Fund and Rothschild U.S. Small-Cap Growth Fund (each a “Rothschild Fund”), series of the Professionally Managed Portfolios (the “Trust”):

NOTICE IS HEREBY GIVEN that a joint Special Meeting of Shareholders (the “Special Meeting”) for each Rothschild Fund will be held on December 16, 2015, at 9:00 a.m. Pacific time, at the offices of U.S. Bancorp Fund Services, LLC, 2020 E. Financial Way, Suite 100, Glendora, California 91741.

The Special Meeting is being held to consider the following proposals:

| 1. | Approve an Agreement and Plan of Reorganization for each Rothschild Fund, providing for the transfer of all the assets, obligations and liabilities of such Rothschild Fund to its corresponding and newly-created series (a “PF Fund”) of Pacific Funds Series Trust (the “Pacific Funds Trust”), as listed below (each, a “Reorganization” and together, the “Reorganizations”). The transfer effectively would be (a) an exchange of the Investor Class or Institutional Class shares of your Rothschild Fund for, respectively, Investor Class or Institutional Class shares of the corresponding PF Fund and (b) the distribution pro rata of such shares by the Rothschild Fund to the holders of its shares in complete liquidation of the Rothschild Fund; and |

| 2. | Transact such other business, not currently contemplated, that may properly come before the Special Meeting and any adjournment(s) thereof in the discretion of the proxies or their substitutes. |

| Reorganization No. |

Rothschild Fund |

PF Fund | ||

| (1) |

Rothschild U.S. Small/Mid-Cap Core Fund | Pacific Funds Small/Mid-Cap | ||

| (2) |

Rothschild U.S. Small-Cap Core Fund | Pacific Funds Small-Cap | ||

| (3) |

Rothschild U.S. Small-Cap Value Fund | Pacific Funds Small-Cap Value | ||

| (4) |

Rothschild U.S. Small-Cap Growth Fund | Pacific Funds Small-Cap Growth |

The merger of each Rothschild Fund into its corresponding PF Fund will be treated as a separate Reorganization. Accordingly, shareholder approval and consummation of each Reorganization are not contingent on shareholder approval and consummation of any other Reorganization.

Holders of record of the shares of beneficial interest in a Rothschild Fund as of the close of business on November 6, 2015 are entitled to vote at the Special Meeting or any adjournments or postponements thereof.

If the necessary quorum to transact business at the Special Meeting or if quorum is obtained but sufficient votes required to approve any proposal are not obtained, the persons named as proxies on the enclosed proxy card may propose one or more adjournments of the Special Meeting to permit, in accordance with applicable law, further solicitation of proxies with respect to the proposal. Any such adjournment would require the affirmative vote of the holders of a majority of the shares present in person or by proxy. The persons designated as proxies may use their discretionary authority to vote as instructed by management of the Rothschild Funds on questions of adjournment and on any other proposals raised at the Special Meeting to the extent permitted by the proxy rules of the Securities and Exchange Commission (the “SEC”), including proposals for which timely notice was not received, as set forth in the SEC’s proxy rules.

Please respond — your vote is important, regardless of the number of shares you own! Your prompt vote may save the Rothschild Funds the necessity of further solicitations to ensure a quorum at the Special Meeting.

By Order of the Board of Trustees of Professionally Managed Portfolios,

Elaine E. Richards, Esq.

President

November 20, 2015

Important Notice Regarding the Availability of Proxy Materials for the Special Meeting of Shareholders to be held on December 16, 2015, or any adjournment or postponement thereof.

This Notice and Combined Proxy Statement and Prospectus are available as follows:

By accessing proxyonline.com/does/rothschild.pdf, you will be able to obtain the Notice, the Combined Proxy Statement and Prospectus, any accompanying materials and any amendments or supplements to the foregoing material that are required to be furnished to shareholders.

We encourage you to access and review all of the important information contained in the proxy materials before voting.

| IMPORTANT — We urge you to sign and date the enclosed proxy card and return it in the enclosed addressed envelope, which requires no postage and is intended for your convenience.

You also may vote through the internet, by visiting the website address on your proxy card, or by telephone, by using the toll-free number on your proxy card.

Your prompt vote may save the Rothschild Funds the necessity of further solicitations to ensure a quorum at the Special Meeting. If you can attend the Special Meeting and wish to vote your shares in person at that time, you will be able to do so.

|

PROFESSIONALLY MANAGED PORTFOLIOS

ROTHSCHILD U.S. SMALL/MID-CAP CORE FUND

ROTHSCHILD U.S. SMALL-CAP CORE FUND

ROTHSCHILD U.S. SMALL-CAP VALUE FUND

ROTHSCHILD U.S. SMALL-CAP GROWTH FUND

(the “Rothschild Funds”)

615 East Michigan Street

Milwaukee, WI 53202

QUESTIONS AND ANSWERS

Dated: November 20, 2015

Question: What is this document and why did you send it to me?

Answer: The attached document is a proxy statement for the Rothschild U.S. Small/Mid-Cap Core Fund, Rothschild U.S. Small-Cap Core Fund, Rothschild U.S. Small-Cap Value Fund, and Rothschild U.S. Small-Cap Growth Fund, each a series of the Professionally Managed Portfolios (the “Trust”), and a prospectus for the Investor Class and Institutional Class shares for each corresponding and newly created series (each, a “PF Fund” and together, the “PF Funds”) of the Pacific Funds Series Trust (the “Pacific Funds Trust”). The purposes of this Combined Proxy Statement and Prospectus (the “Proxy Statement”) are to: (1) solicit votes from shareholders of each Rothschild Fund to approve the proposed reorganization of each Rothschild Fund into its corresponding PF Fund, as listed below (each a “Reorganization”, and together, the “Reorganizations”) and as described in the Agreement and Plan of Reorganization between the Trust and the Pacific Funds Trust (the “Plan”); and (2) provide information regarding the Investor Class and Institutional Class shares of the PF Funds.

| Reorganization No. |

Rothschild Fund |

PF Fund | ||

| (1) |

Rothschild U.S. Small/Mid-Cap Core Fund | Pacific Funds Small/Mid-Cap | ||

| (2) |

Rothschild U.S. Small-Cap Core Fund | Pacific Funds Small-Cap | ||

| (3) |

Rothschild U.S. Small-Cap Value Fund | Pacific Funds Small-Cap Value | ||

| (4) |

Rothschild U.S. Small-Cap Growth Fund | Pacific Funds Small-Cap Growth |

The Proxy Statement contains information that shareholders of each Rothschild Fund should know before voting on the Reorganization. The Proxy Statement should be retained for future reference.

Question: What is the purpose of the Reorganizations?

Answer: The primary purpose of the Reorganizations is to move the Rothschild Funds to the Pacific Funds Trust family of funds. Rothschild Asset Management Inc. (“Rothschild” or the “Sub-Adviser”), the adviser to the Rothschild Funds, recommends that the Rothschild Funds be reorganized with their corresponding PF Funds, each a newly-formed series of the Pacific Funds Trust with investment objectives and principal investment strategies that are substantially the same as those of the Rothschild Funds. Rothschild would serve as the sub-adviser to the PF Funds, and, as such, would be responsible for the day-to-day portfolio management of the PF Funds. Rothschild believes that the increased distribution channels available to the PF Funds may provide them with opportunities to increase their asset base over time that may not be available to the Rothschild Funds. Rothschild believes that an increase in the asset base has the potential to reduce the Funds’ expense ratio as fixed costs could be distributed over a larger asset base and could provide other economies of scale benefits to the Rothschild Funds’ shareholders through the Adviser’s reinvestment in the business in the form of improvements in technology and other resources and investments in personnel. Rothschild further believes that the Reorganizations will allow Rothschild to focus its resources on enhancements to its infrastructure which may promote its ability to implement its investment strategies, to the benefit of the Rothschild Funds’ shareholders and will further allow it to leverage the management, infrastructure and distribution capabilities of the Adviser and its affiliate.

Question: Has the Board of the Rothschild Funds approved the Reorganizations?

Answer: The Board of Trustees of the Trust has approved the Reorganizations and the Plan, subject to shareholder approval. The Board of Trustees believes that the proposed Reorganizations are in the best interests of the Rothschild Funds and their shareholders, and that the interest of the Rothschild Funds’ shareholders will not be diluted as a result of the Reorganizations.

As discussed in greater detail below, the proposed Reorganizations are part of a larger restructuring pursuant to which the Funds, and the other Rothschild Funds within the Trust, are proposed to be reorganized into Pacific Funds Trust family of funds. Rothschild approached the Board of Trustees with this recommendation after having determined that its existing distribution capabilities were insufficient to achieve material asset growth in the Funds and that economies of scale were therefore unlikely to be achieved in the foreseeable future. Rothschild therefore advised the Board that it had determined to seek a strategic alignment with an entity possessing existing distribution capabilities rather than expending the significant capital and resources necessary to develop its own distribution capabilities. In considering this recommendation, the Board of Trustees carefully considered a number of factors which are discussed in more detail in the enclosed proxy statement. These factors included, but were not limited to, the determination by Rothschild that it could not continue indefinitely to subsidize the Funds to support its current expense limitation, the opportunity to achieve asset growth through the Pacific Funds family of funds distribution networks, the strong similarity of the Rothschild Funds and the corresponding PF Funds’ investment objectives, policies and restrictions, the continuation of portfolio management services by Rothschild, and the terms and conditions in the Plan. The Board also took into account that Rothschild had a conflict of interest in making its recommendation in that it would receive a cash payment from the Adviser to help defray some costs associated with the creation of the new PF Funds and certain transactional expenses associated with the Reorganizations. The Board also took into account that the Adviser had a conflict of interest in that, if the Reorganizations were consummated, it would become the investment adviser, and receive advisory fees on an existing asset base from the PF Funds and that its affiliate serves as distributor and principal underwriter of the PF Funds and would be receiving distribution fees in connection therewith. In reviewing the terms of the proposed Reorganizations, the Board of Trustees considered the fact that the PF Funds advisory fees will be the same as the advisory fees paid by the Funds and that the Adviser would contractually agree to limit certain operating expenses for the first three years following the close of the transaction. The Board also considered other alternatives to the Reorganization, including the liquidation and termination of the Rothschild Fund. For further information regarding these and other factors considered by the Board of Trustees, please refer to the section below entitled “Trust Board Considerations.”

Question: How will the Reorganizations work?

Answer: To reconstitute the Rothschild Funds as series of the Pacific Funds Trust, similar funds, each referred to as the “PF Fund,” have been created as a new series of the Pacific Funds Trust. If shareholders of a Rothschild Fund approve the proposals in the Proxy Statement, such Rothschild Fund will transfer all of its assets, obligations and liabilities to its corresponding PF Fund in return for shares of that PF Fund. The Rothschild Fund will then distribute the shares it receives from the PF Fund to its shareholders. Existing shareholders of a Rothschild Fund’s Investor Class and Institutional Class shares will become shareholders of the corresponding PF Fund’s Investor Class and Institutional Class, respectively, and immediately after the Reorganization, each shareholder will hold full and fractional shares of the PF Fund with an aggregate value equal to the aggregate value of their Rothschild Fund shares immediately prior to the Reorganization. Subsequently, the Rothschild Fund will be liquidated.

The merger of each Rothschild Fund into its corresponding PF Fund will be treated as a separate Reorganization. Accordingly, shareholder approval and consummation of each Reorganization are not contingent on shareholder approval and consummation of any other Reorganization. Please refer to the Proxy Statement for a detailed explanation of the proposal and for information regarding the PF Funds. If the Plan is approved by shareholders of each of the Rothschild Funds at the joint Special Meeting of Shareholders (the “Special Meeting”), each Reorganization presently is expected to be effective on or about January 11, 2016.

Question: How will the Reorganization affect me as a shareholder?

Answer: You will become a shareholder of the PF Fund. The shares of the PF Fund that you receive will have a total net asset value equal to the total net asset value of the shares you hold in the Rothschild Fund as of the closing date of the Reorganization. The Reorganization will not affect the value of your investment at the time of the Reorganization. The Reorganizations are expected to be tax free to the Rothschild Funds and their shareholders.

The Reorganizations will transition management oversight responsibility for the Rothschild Funds from Rothschild to the Adviser. By engaging Rothschild, the adviser to the Rothschild Fund, as the sub-adviser to the PF Funds, the Adviser will provide continuity of the portfolio management team that has been responsible for the Rothschild Funds’ performance record since its inception in 2014. The portfolio managers of the Sub-Adviser who are primarily responsible for the day-to-day portfolio management of the Rothschild Funds also will serve in the same capacity for the PF Funds. The investment objective and strategies of the PF Funds will be substantially the same as those of the Rothschild Funds.

The PF Funds’ investment limitations are substantially similar to those of the Rothschild Funds; however, the investment limitations of the PF Funds are worded differently to align them with the limitations and policies of other existing funds in the Pacific Funds Trust.

The Adviser and the PF Funds operate under an exemptive order issued by the U.S. Securities and Exchange Commission (the “SEC”). Pursuant to the order, the Adviser may, subject to the approval of the Board of Trustees of the Pacific Funds Trust (the “PF Board”), hire or replace unaffiliated sub-advisers and may modify any existing or future sub-advisory agreement with an unaffiliated sub-adviser, such as Rothschild, without shareholder approval, which is known as a “manager-of-managers” structure. This is in contrast to the current arrangement with respect to the Rothschild Funds. Currently, while the Board of the Trust may terminate Rothschild as the adviser of the Rothschild Funds, shareholder approval would be required to replace Rothschild with another investment adviser. The sole initial shareholder of the PF Funds has approved the PF Funds’ participation in this manager-of-managers structure, and shareholders of the Rothschild Funds, including in their ultimate capacities as shareholders of the PF Funds, will not be asked to vote on this matter.

The Reorganizations will result in a change to certain of the Rothschild Funds’ service providers. Quasar Distributors, LLC (“Quasar”) currently serves as the distributor and principal underwriter of the Rothschild Funds’ shares. Pacific Select Distributors, LLC (“PSD”) serves as the distributor and principal underwriter for the Pacific Funds Trust, including the PF Funds, and is an affiliate of the Adviser. Pacific Life Insurance Company (“Pacific Life”), the Adviser’s parent company, serves as the administrator to the Pacific Funds Trust, and in that capacity has engaged BNY Mellon Investment Servicing (US) Inc. (“BNY Mellon”) to perform certain sub-administrative and accounting services for the PF Funds. BNY Mellon also serves as the PF Funds’ transfer agent, registrar and dividend disbursing agent. U.S. Bancorp Fund Services, LLC currently provides those services to the Rothschild Funds. U.S. Bank National Association is the current custodian to the Rothschild Funds, while The Bank of New York Mellon (“BNYM”) is the custodian to the PF Funds and Pacific Funds Trust. The Adviser also provides certain administratives services for the PF Funds.

The Reorganizations will move the assets of the Rothschild Funds from the Trust, which is a Massachusetts business trust, to the PF Funds, series of Pacific Funds Trust, which is a Delaware statutory trust. As a result of the Reorganizations, the PF Funds will operate under the supervision of the Pacific Funds Trust’s Board of Trustees. Please refer to the section in the Proxy Statement entitled “Comparison of Forms of Organization and Shareholder Rights” for more information about the differences between the Trust and the Pacific Funds Trust.

Question: Who will manage my PF Fund?

Answer: The Adviser will be responsible for overseeing the management of the PF Funds and has engaged Rothschild as the sub-adviser to the PF Funds. The portfolio managers of the Sub-Adviser who are primarily responsible for the day-to-day portfolio management of the Rothschild Funds will continue to manage the portfolios of the PF Funds.

The Adviser is an experienced provider of investment advisory services to institutional and retail investors, with over $53 billion in mutual fund assets under management. The Adviser serves as the adviser to the Pacific Funds Trust, which is currently comprised of 36 series. The Adviser is a direct subsidiary of Pacific Life Insurance Company, a company that has been offering insurance since 1868 and now offers a variety of investment products and services to individuals, businesses and pension plans.

The Sub-Adviser is a New York corporation. The Sub-Adviser was established in 1962 and had approximately $5.5 billion in assets under management as of September 30, 2015.

Question: How will the Reorganization affect the fees and expenses I pay as a shareholder of a Rothschild Fund?

Answer: The advisory fees paid by the PF Funds will be the same as the advisory fees paid by the Rothschild Funds. In addition, the Adviser agreed to limit certain operating expenses incurred by the PF Funds for three years following the closing date of the Reorganizations. As a result, the overall net expense ratios (excluding extraordinary expenses) of the PF Funds for three years following the closing of the Reorganizations will not exceed 1.35% and 1.00% for the Investor Class and Institutional Class shares, respectively, for the Pacific Funds Small/Mid-Cap, Pacific Funds Small-Cap and Pacific Funds Small-Cap Value, and 1.25% and 0.90% for the Investor Class and Institutional Class shares, respectively, of the Pacific Funds Small-Cap Growth, and which would be the same as the current overall net expense ratios of the Rothschild Funds. The PF Board intends to consider the continuation of the expense limitation in one-year increments following January 10, 2019, but there is no guarantee that such expense caps will be extended.

For the purposes of the expense limitation agreements between the Adviser and each PF Fund, “operating expenses” that are subject to the expense limitation consist of the ordinary operating expenses incurred by a PF Fund in any fiscal year, including the administration fees and organizational expenses. Expenses excluded from such limitation agreements consist of the investment advisory fee, distribution and/or service fees, dividends on securities sold short, acquired fund fees and expenses, foreign taxes on dividends, interest or gains, interest (including commitment fees), taxes, brokerage commissions and other transactional expenses. Other expenses excluded from the limitation agreement include “extraordinary expenses” which are expenses not incurred in the ordinary course of a PF Fund’s business (such as expenses associated with a Private Letter Ruling from the Internal Revenue Service) or litigation costs.

Accordingly, the Reorganizations will not result in any increase to the advisory fees or the overall net expense ratios (excluding extraordinary expenses) of the PF Funds for three years following the closing of the Reorganizations, as compared to the net expense ratios currently paid by the Rothschild Funds.

Question: Will the Reorganizations result in any taxes?

Answer: We expect that neither the Rothschild Funds nor its shareholders will recognize any gain or loss for federal income tax purposes as a direct result of the Reorganizations, and the Trust and the Pacific Funds Trust expect to receive a tax opinion confirming this position. Shareholders should consult with their tax adviser about possible state and local tax consequences of a Reorganization, if any, because the information about tax consequences in this document relates to the federal income tax consequences of the Reorganization only.

Question: Will I be charged a sales charge as a result of the Reorganizations?

Answer: No sales loads, commissions or other transactional fees will be imposed on shareholders in connection with the Reorganizations.

Question: Why do I need to vote?

Answer: Your vote is needed to ensure that a quorum and sufficient votes are present at the Special Meeting so that the proposal can be acted upon. Your immediate response on the enclosed Proxy Card will help prevent the need for any further solicitations for a shareholder vote, which will result in additional expenses. Your vote is very important to us regardless of the number of shares you own.

Question: How does the Trust’s Board of Trustees recommend that I vote?

Answer: After careful consideration and upon recommendation of Rothschild, the Board of Trustees of the Trust unanimously recommends that shareholders of each Rothschild Fund vote “FOR” the Plan.

Question: Who is paying for expenses related to the Special Meeting and the Reorganizations?

Answer: The Adviser and Rothschild will pay all direct costs relating to the Reorganizations, including the costs relating to the Special Meeting and the Proxy Statement. The Rothschild Funds will not incur any expenses in connection with the Reorganizations.

Question: What will happen if the Plan is not approved by shareholders of each Rothschild Fund?

Answer: If shareholders of a Rothschild Fund do not approve the Plan, that Rothschild Fund will not be reorganized into its corresponding PF Fund and the Board of Trustees of the Trust will consider other alternatives. The failure of a Rothschild Fund to obtain shareholder approval of the Plan will not have any impact on the Reorganization of any other Rothschild Fund into its corresponding PF Fund.

As of the date of this Proxy Statement, Rothschild, its employees and affiliates of Rothschild (“Rothschild Affiliates”) hold a sufficient number of shares to cause the Plan for each Rothschild Fund to be approved. It is expected that the Rothschild Affiliates will vote FOR the Plan at the Special Meeting.

Question: How do I vote my shares?

Answer: You can vote your shares by mail, or by telephone following the instructions on the enclosed proxy card.

Question: Who do I call if I have questions?

Answer: If you have any questions about the proposal or the proxy card, please do not hesitate to call (866) 721-1324.

COMBINED PROXY STATEMENT AND PROSPECTUS

November 20, 2015

FOR THE REORGANIZATION OF

ROTHSCHILD U.S. SMALL/MID-CAP CORE FUND

ROTHSCHILD U.S. SMALL-CAP CORE FUND

ROTHSCHILD U.S. SMALL-CAP VALUE FUND

ROTHSCHILD U.S. SMALL-CAP GROWTH FUND,

Each a series of Professionally Managed Portfolios

c/o U.S. Bancorp Fund Services, LLC,

615 East Michigan St., Milwaukee, WI 53202

INTO

Pacific FundsSM Small/Mid-Cap

Pacific FundsSM Small-Cap

Pacific FundsSM Small-Cap Value

Pacific FundsSM Small-Cap Growth

(each, a “PF Fund” and together, the “PF Funds”),

series of Pacific Funds Series Trust

700 Newport Center Drive, Newport Beach, CA 92660

INTRODUCTION

This combined proxy statement and prospectus (the “Proxy Statement”) is being sent to you in connection with the solicitation of proxies by the Board of Trustees (the “Board”) of the Professionally Managed Portfolios (the “Trust”) in connection with the joint Special Meeting of Shareholders (the “Special Meeting”) of the Rothschild U.S. Small/Mid-Cap Core Fund, Rothschild U.S. Small-Cap Core Fund, Rothschild U.S. Small-Cap Value Fund and Rothschild U.S. Small-Cap Growth Fund (each, a “Rothschild Fund” and together, the “Rothschild Funds”), each a series of the Trust, managed by Rothschild Asset Management Inc. (“Rothschild” or the “Sub-Adviser”), at 9:00 a.m. Pacific time on December 16, 2015, at the offices of U.S. Bancorp Fund Services, LLC, 2020 E. Financial Way, Suite 100, Glendora, California 91741.

At the Special Meeting, the shareholders of each Rothschild Fund will be asked to consider the following proposals (the “Proposals”):

| 1. | Approve an Agreement and Plan of Reorganization for each Rothschild Fund, providing for the transfer of all the assets, obligations and liabilities of such Rothschild Fund to its corresponding and newly-created series (a “PF Fund”) of Pacific Funds Series Trust (the “Pacific Funds Trust”), as listed below (each, a “Reorganization” and together, the “Reorganizations”). The transfer effectively would be (a) an exchange of the Investor Class or Institutional Class shares of your Rothschild Fund for, respectively, Investor Class or Institutional Class shares of the corresponding PF Fund and (b) the distribution pro rata of such shares by the Rothschild Fund to the holders of its shares in complete liquidation of the Rothschild Fund; and |

| 2. | Transact such other business, not currently contemplated, that may properly come before the Special Meeting and any adjournment(s) thereof in the discretion of the proxies or their substitutes. |

| Reorganization No. |

Rothschild Fund |

PF Fund | ||

| (1) |

Rothschild U.S. Small/Mid-Cap Core Fund | Pacific Funds Small/Mid-Cap | ||

| (2) |

Rothschild U.S. Small-Cap Core Fund | Pacific Funds Small-Cap | ||

| (3) |

Rothschild U.S. Small-Cap Value Fund | Pacific Funds Small-Cap Value | ||

| (4) |

Rothschild U.S. Small-Cap Growth Fund | Pacific Funds Small-Cap Growth |

Under the Agreement and Plan of Reorganization (the “Plan”), and as a result of the Reorganization, the shares of your Rothschild Fund will be exchanged for full and fractional shares of the corresponding PF Fund with an aggregate value equal to the aggregate value of your Rothschild Fund shares immediately prior to the Reorganization, and the Rothschild Fund would then be completely liquidated. The closing date of the Reorganizations is currently scheduled for January 11, 2016, or such other date as the parties may agree (“Closing Date”).

The Rothschild Funds are series of the Trust, an open-end management investment company registered with the SEC and organized as a Massachusetts business trust. The PF Funds are newly created series of the Pacific Funds Trust, an open-end management investment company registered with the SEC and organized as a Delaware statutory trust.

Because you, as a shareholder of one or more Rothschild Funds, are being asked to approve the Proposals with respect to the Rothschild Fund or Funds in which you hold shares, including the Reorganization for your Rothschild Fund(s), which would make you a shareholder of one or more PF Funds, this document also serves as a Prospectus for the PF Funds.

This Proxy Statement sets forth the basic information you should know before voting on the Proposals. You should read it and keep it for future reference. Additional information relating to the PF Funds and the Proxy Statement is set forth in the Statement of Additional Information to this Proxy Statement dated November 20, 2015, which is incorporated by reference into the Proxy Statement.

Additional information about the PF Funds has been filed with the SEC and is available upon request and without charge by writing to the Pacific Funds Trust or by calling (800) 722-2333 select Option 2. The Rothschild Funds expects that the Proxy Statement will be mailed to shareholders on or about November 20, 2015.

The following documents have been filed with the SEC and are incorporated by reference into this Proxy Statement, which means that these documents are considered legally to be part of the Proxy Statement:

| • | Statement of Additional Information to this Proxy Statement, dated November 20, 2015 (on file with the SEC (http://www.sec.gov) (File No. 333-207499)); |

| • | Prospectus and Statement of Additional Information of the Rothschild Fund, each dated December 22, 2014 (on file with the SEC (http://www.sec.gov) (File Nos. 811-05037; 33-12213) (Accession No. 0000894189-14-006083)), as supplemented January 23, 2015 (on file with the SEC (http://www.sec.gov) (File No. 033-12213) (Accession No. 0000894189-15-000274)) and November 13, 2015 (on file with the SEC (http://www.sec.gov) (File No. 033-12213) (Accession No. 0000894189-15-005848); and |

| • | Statement of Additional Information of the Rothschild Fund dated December 22, 2014 (http://www.sec.gov) (File Nos. 811-05037; 33-12213) (Accession No. 0000894189-14-006083); and |

| • | Semi-Annual Report to Shareholders of the Rothschild Funds for the six-month period ended May 31, 2015 (on file with the SEC (http://www.sec.gov) (File No. 811-05037) (Accession No. 0000894189-15-003812)). |

The Rothschild Funds’ Summary Prospectuses dated December 22, 2014 and Semi-Annual Report to Shareholders for the six-month period ended May 31, 2015, containing unaudited financial statements, have been

2

previously mailed to shareholders. Copies of these documents are available upon request and without charge by writing to the Rothschild Funds, through the internet at www.rothschild.com/raminc/usfunds, or by calling (844) 726-3863.

Because each PF Fund has not yet commenced operations as of the date of this Proxy Statement, no annual or semi-annual report are available for the PF Funds at this time. Pro forma financial information has not been prepared for the Reorganizations because the PF Funds are newly organized series of the Pacific Funds Trust with no assets and liabilities that will commence operations upon consummation of the Reorganizations.

The Rothschild Funds and the PF Funds are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended, and file reports, proxy materials and other information with the SEC. You can copy and review information about the Rothschild Funds and the Trust and the PF Funds and the Pacific Funds Trust, including the prospectus, statement of additional information, annual and semi-annual reports, proxy materials and other information at the SEC’s Public Reference Room, 100 F Street N.E., Room 1580, Washington, D.C. 20549-1520. You may obtain information from the Public Reference Room by calling the SEC at 1-202-551-8090. Such materials are also available in the EDGAR Database on the SEC’s website at http://www.sec.gov. You may obtain copies of this information, after paying a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, Office of Consumer Affairs and Information, Securities and Exchange Commission, Washington, D.C. 20549-1520.

THE SEC HAS NOT APPROVED OR DISAPPROVED THESE SECURITIES, NOR HAS IT PASSED ON THE ACCURACY OR ADEQUACY OF THIS PROXY STATEMENT AND PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

3

| INTRODUCTION | ||||||||||||||

| I. |

PROPOSAL — TO APPROVE THE AGREEMENT AND PLAN OF REORGANIZATION |

6 | ||||||||||||

| A. |

6 | |||||||||||||

| B. |

6 | |||||||||||||

| C. |

7 | |||||||||||||

| D. |

|

COMPARISON OF INVESTMENT OBJECTIVES, PRINCIPAL INVESTMENT STRATEGIES AND |

10 | |||||||||||

| E. |

17 | |||||||||||||

| F. |

19 | |||||||||||||

| G. |

26 | |||||||||||||

| H. |

35 | |||||||||||||

| I. |

|

COMPARISON OF DISTRIBUTION AND PURCHASE, REDEMPTION AND EXCHANGE |

35 | |||||||||||

| J. |

37 | |||||||||||||

| 1. | 37 | |||||||||||||

| 2. |

39 | |||||||||||||

| 3. |

39 | |||||||||||||

| 4. |

40 | |||||||||||||

| 5. |

41 | |||||||||||||

| K. |

42 | |||||||||||||

| 1. |

42 | |||||||||||||

| 2. |

43 | |||||||||||||

| 3. |

43 | |||||||||||||

| 4. |

PAYMENTS TO BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES |

43 | ||||||||||||

| II. |

43 | |||||||||||||

| A. |

43 | |||||||||||||

| B. |

44 | |||||||||||||

| C. |

44 | |||||||||||||

| D. |

45 | |||||||||||||

| E. |

45 | |||||||||||||

| F. |

45 | |||||||||||||

| III. |

45 | |||||||||||||

| A. |

45 | |||||||||||||

| B. |

46 | |||||||||||||

| C. |

46 | |||||||||||||

| D. |

46 | |||||||||||||

| A-1 | ||||||||||||||

| B-1 |

||||||||||||||

| C-1 |

||||||||||||||

4

INTRODUCTION

You should read this entire Proxy Statement carefully, including the Appendices, and review the Plan, which is attached as Appendix A.

The proposed Reorganization:

At the meeting held on August 17-18, 2015, the Board of Trustees of the Trust (the “Board”) approved the Plan for each Rothschild Fund. Subject to shareholder approval, the Plan provides for:

| • | the transfer of all of the assets, obligations and liabilities of each Rothschild Fund to the corresponding PF Fund in exchange for shares of such PF Fund; |

| • | the distribution of shares of each PF Fund to the shareholders of the corresponding Rothschild Fund so that each shareholder will receive a number of full and fractional shares of the PF Fund with an aggregate value equal to the aggregate value of the number of full and fractional shares of the Rothschild Fund held by such shareholder; and |

| • | the complete liquidation of each Rothschild Fund. |

The Reorganizations are expected to be effective as of the close of business on January 11, 2016, or such other date as the parties may agree (the “Closing Date”).

In considering whether to approve the Reorganizations, please note:

| • | The Funds have the same investment goals. |

| • | The Funds have substantially the same investment strategies and risks. |

| • | The Funds will have the same advisory fees and the Reorganization will not result in any increase to the overall net expense ratios (excluding extraordinary expenses) of the PF Funds for three years following the closing of the Reorganization, as compared to the net expense ratios currently paid by the Rothschild Funds. |

| • | The Funds will have the same day-to-day investment management by Rothschild, the current adviser to the Rothschild Funds, which will act as sub-adviser to the PF Funds. |

| • | The PF Funds will have a different investment adviser, Pacific Life Fund Advisors LLC. The Adviser will oversee Rothschild as the sub-adviser to the PF Funds. The PF Funds also have different service providers than the Rothschild Funds and are supervised by a different board of trustees. See Comparison of Investment Objectives, Principal Investment Strategies and Management of the Funds section below for information on the Funds’ strategies, characteristics and holdings. |

5

I. PROPOSAL — TO APPROVE THE AGREEMENT AND PLAN OF REORGANIZATION

| A. | OVERVIEW |

The Board, which is comprised entirely of Trustees who are not “interested persons,” as that term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”), of the Trust, has approved the recommendation of Rothschild that each Rothschild Fund reorganize into its corresponding PF Fund and that each Rothschild Fund shareholder become a shareholder of the PF Fund, pursuant to the Plan, the form of which is attached to this Proxy Statement as Appendix A. The Board considered the Reorganizations at its regularly scheduled meeting held on August 17-18, 2015.

In order to reorganize the Rothschild Funds into a series of the Pacific Funds Trust, substantially similar funds — Pacific Funds Small/Mid-Cap, Pacific Funds Small-Cap, Pacific Funds Small-Cap Value and Pacific Funds Small-Cap Growth (and each referred to as the “PF Fund” and collectively, the “PF Funds”) have been created as new series of the Pacific Funds Trust. If the shareholders of a Rothschild Fund approve the Plan, the Reorganization of that Rothschild Fund into its corresponding PF Fund will have three primary steps:

| • | First, the Rothschild Fund will transfer all of its assets to the corresponding PF Fund in exchange solely for Institutional Class shares and Investor Class shares of the PF Fund and the PF Fund’s assumption of the Rothschild Fund’s obligations and liabilities; |

| • | Second, each holder of that Rothschild Fund will receive a pro rata distribution of the PF Fund’s Institutional Class and Investor Class shares, as the case may be; and |

| • | Third, the Rothschild Fund will be liquidated. |

The Plan provides for multiple reorganizations. Each such reorganization, including the proposed Reorganizations as listed below, shall be treated as if it had been the subject of a separate Plan. Accordingly, shareholder approval and consummation of each Reorganization are not contingent on shareholder approval and consummation of any other Reorganization.

| Reorganization No. |

Rothschild Fund |

PF Fund | ||

| (1) |

Rothschild U.S. Small/Mid-Cap Core Fund | Pacific Funds Small/Mid-Cap | ||

| (2) |

Rothschild U.S. Small-Cap Core Fund | Pacific Funds Small-Cap | ||

| (3) |

Rothschild U.S. Small-Cap Value Fund | Pacific Funds Small-Cap Value | ||

| (4) |

Rothschild U.S. Small-Cap Growth Fund | Pacific Funds Small-Cap Growth |

Approval of the Plan for each Rothschild Fund will constitute approval of the transfer of the Rothschild Fund’s assets, the assumption of its obligations and liabilities, the distribution of the corresponding PF Fund’s Institutional Class and Investor Class shares, and liquidation of the Rothschild Fund. The Institutional Class and Investor Class shares of the PF Funds issued in connection with the Reorganizations will have an aggregate net asset value equal to the net asset value of the assets that the Rothschild Funds transferred to the PF Funds. The value of a shareholder’s account with the PF Funds immediately after the Reorganizations will be the same as the value of such shareholder’s account with the Rothschild Funds immediately prior to the Reorganizations. No sales charge or fee of any kind will be charged to the Rothschild Funds’ shareholders in connection with the Reorganizations.

The Trust believes that the Reorganizations will constitute a tax-free transaction for federal income tax purposes. The Trust and the Pacific Funds Trust will receive an opinion from tax counsel to the Pacific Funds Trust confirming such tax treatment and effect. Therefore, shareholders should not recognize any gain or loss on their Rothschild Fund shares for federal income tax purposes as a direct result of the Reorganization.

| B. | REASONS FOR THE REORGANIZATIONS |

The primary purpose of the Reorganizations is to move the investment portfolio and shareholders presently associated with the Rothschild Funds to the Pacific Funds family of funds. Rothschild has recommended the

6

Reorganizations to the Trust as it believes that reconstituting the Rothschild Funds as a series of the Pacific Funds Trust has the potential to expand the distribution network and increase each of the Rothschild Funds’ assets, as the Pacific Funds Trust has access to greater resources and distribution channels than do the Rothschild Funds. Rothschild further believes that the Reorganizations will allow Rothschild to focus its resources on enhancements to its infrastructure and will allow it to leverage the management, infrastructure and distribution capabilities of the Adviser and its affiliate.

The Reorganizations will shift management oversight responsibility for the Rothschild Funds from Rothschild to the Adviser. However, by engaging Rothschild as the sub-adviser, the Adviser will provide continuity of the portfolio management team that has been responsible for the Rothschild Funds’ performance record since their inception in 2014. The portfolio managers of the Sub-Adviser who are primarily responsible for the day-to-day portfolio management of the Rothschild Funds will remain the same, although the Adviser may terminate the Sub-Advisory Agreement with Rothschild at any time without shareholder approval, upon the approval of the PF Fund’s Board of Trustees. The investment objective and strategies of the PF Funds will be substantially the same to those of the Rothschild Funds. The PF Funds’ investment limitations are very similar to those of the Rothschild Funds; however, those limitations are worded to align with current limitations of the other series of the Pacific Funds Trust.

The Reorganizations will result in a change to certain of the Rothschild Funds’ service providers. Quasar Distributors, LLC (“Quasar”) currently serves as the distributor and principal underwriter of the Rothschild Funds’ shares. Pacific Select Distributors, LLC (“PSD”) serves as the distributor and principal underwriter for the Pacific Funds Trust, including the PF Funds, and is an affiliate of the Adviser. Pacific Life Insurance Company (“Pacific Life”), the Adviser’s parent company, serves as the administrator to the Pacific Funds Trust, and in that capacity has engaged BNY Mellon Investment Servicing (US) Inc. (“BNY Mellon”) to perform certain sub-administrative and accounting services for the PF Funds. BNY Mellon also serves as the PF Funds’ transfer agent, registrar and dividend disbursing agent. U.S. Bancorp Fund Services, LLC currently provides those services to the Rothschild Funds. U.S. Bank National Association is the current custodian to the Rothschild Funds, while The Bank of New York Mellon (“BNYM”) is the custodian to the PF Funds and Pacific Funds Trust. The Adviser also provides certain administrative services for the PF Funds. The PF Funds are also overseen by a different board of trustees than the Board of Trustees for the Trust.

The Rothschild Funds assess no front-end sales charge, contingent deferred sales charge, redemption fees or exchange fees, and no such fees will be assessed by the Investor Class or Institutional Class shares of the PF Funds. The Reorganizations will not result in any increase in the advisory fees or the overall net expense ratios (excluding extraordinary expenses) of the PF Funds for three years following the closing of the Reorganizations, as compared to the net expense ratios currently paid by the Rothschild Funds.

| C. | TRUST BOARD CONSIDERATIONS |

Rothschild and the Adviser proposed, and the Board considered, the Reorganization of each Rothschild Fund at an in-person meeting of the Board held on August 17-18, 2015. Based upon the recommendation of Rothschild, its evaluation of the relevant information presented to it at these meetings, and in light of its fiduciary duties under federal and state law, the Board, comprised entirely of trustees who are not “interested persons” of the Trust under the 1940 Act, determined that each Reorganization is in the best interests of each Rothschild Fund and its shareholders.

In approving the proposed Reorganizations, the Board carefully considered the following matters, among other things:

The Size of the Funds and the Strategic Decision Made by Rothschild with Respect to the Future Growth Plans for the Funds. The Board considered that the Rothschild Funds have not yet reached their first

7

full year of operations and that their assets have not achieved economies of scale in the short time since their inception on December 31, 2014, despite relatively good performance. The Board further considered that Rothschild had made a decision to seek a strategic alignment with an entity possessing existing distribution capabilities rather than to expend the significant capital and resources necessary to develop its own distribution capabilities. As a result, the Board considered that the Funds would likely not achieve significant asset growth on its own and that Rothschild would be required to subsidize the Funds’ expenses over the long term in order for the Funds to maintain a competitive expense ratio.

The Terms and Conditions of the Reorganizations. The Board considered the terms of the Plan, and, in particular, the requirement that the transfer of the assets of the Rothschild Funds’ Institutional Class shares and Investor Class shares be in exchange for Institutional Class shares and Investor Class shares of the PF Funds and the PF Funds’ assumption of all obligations and liabilities of the Rothschild Funds. The Board also took note of the fact that no sales charges would be imposed in connection with the Reorganizations. The Board noted that Rothschild Funds shareholders would receive the same dollar value in Institutional Class or Investor Class shares of the PF Funds as their Rothschild Funds shares immediately prior to the Reorganizations and would not result in the dilution of such shareholders’ interests. The Board further noted that the Reorganization would be submitted to the each Rothschild Fund’s shareholders for approval.

Strong Similarity of Investment Objectives, Policies and Restrictions and Continuity of Portfolio Management. The Board considered that the PF Funds were designed to be substantially similar to the Rothschild Funds with substantially the same investment objectives and strategies. The investment restrictions of the PF Funds are substantially similar to those of the Rothschild Funds, although they are worded to conform with the current restrictions of the other series of the Pacific Funds Trust. As a result, and when coupled with the continuation of the Rothschild Funds’ portfolio management teams through the engagement of Rothschild as sub-adviser, there would be a continuity in the investment management process for shareholders.

Expenses Relating to Reorganization. The Board noted that the Adviser and Rothschild will bear the direct costs associated with the Reorganizations, Special Meeting, and solicitation of proxies, including the expenses associated with preparing and filing the registration statement that includes this Proxy Statement and the cost of copying, printing and mailing proxy materials.

Advisory Fees Relative Expense Ratios and Cap on Expenses. The Board considered that the advisory fees paid by the PF Funds will be the same as the advisory fees paid by the Rothschild Funds. The Board also considered that the Adviser would contractually agree to limit certain operating expenses of each PF Fund, through at least January 10, 2019, such that the total annual operating expense ratios (excluding extraordinary expenses) of Institutional Class shares and Investor Class shares of the PF Funds would not, for the first three years following the close of the transaction, exceed the current overall operating expense ratios of the Rothschild Funds. The Board understands that the PF Board intends to consider the continuation of the expense cap in one-year increments following January 10, 2019, but that there is no guarantee that such expense caps will be extended.

Economies of Scale. The Board considered the potential of the PF Funds to experience economies of scale as a result of its being a series of the Pacific Funds Trust because certain fixed costs, such as accounting, shareholder services and trustee expenses, would be spread over a larger fund complex. The Board concluded that, given the strategic decision by Rothschild not to further develop its own mutual fund distribution capabilities, the proposed structure had the potential benefit to grow the assets in the Funds and benefit shareholders as the PF Funds grows.

Distribution and Service Fees. The Board considered the fund distribution capabilities of the Adviser and its affiliates and the commitment to distribute shares of the PF Funds. The Board further considered that the Rothschild Funds charges no fees for distribution and/or shareholder services pursuant to Rule 12b-1 under the 1940 Act (“Rule 12b-1”) for its Institutional Class shares, and that no Rule 12b-1 distribution or service fees will be charged for the Institutional Class shares of the PF Funds. The Board noted that Investor Class shares of the Rothschild Funds and Investor Class shares of the PF Funds both charge the same amount, 0.25%, for distribution services pursuant to

8

Rule 12b-1. Unlike the Investor Class shares of the Rothschild Funds, however, Investor Class shares of the PF Funds will not charge a shareholder servicing fee of 0.10%.

The Experience and Expertise of the Adviser and Sub-Adviser. The Board took into account the Adviser’s reputation, financial strength and resources. The Board noted that the Adviser is an experienced provider of investment advisory services to institutional and retail investors, with over $53 billion in mutual fund assets under management. The Board considered the Adviser’s authority to function as a “manager of managers” pursuant to an exemptive order (the “Order”) from the SEC.

The Board noted that the Order permits the Adviser, on behalf of the series of the Pacific Funds Trust including the PF Funds, and subject to the approval of the PF Trust’s Board of Trustees, including a majority of the PF Board members who are not “interested persons” (as the term is defined in the 1940 Act) of Pacific Funds Trust, to hire or replace unaffiliated sub-advisers and to modify any existing or future sub-advisory agreement with an unaffiliated sub-adviser without shareholder approval. The Order grants the Adviser and the Pacific Funds Trust an exemption from the provisions of Section 15(a) of the 1940 Act and Rule 18f-2 thereunder to the extent necessary to permit the Adviser and the Pacific Funds Trust, on behalf of the PF Fund, and without the approval of shareholders, to: (a) engage new or additional unaffiliated sub-advisers; (b) enter into and modify existing sub-advisory agreements with unaffiliated sub-advisers; or (c) replace sub-advisers with unaffiliated sub-advisers.

The Board noted that use of the Order provides the Adviser and the Board of the Pacific Funds Trust with increased flexibility to recommend, supervise, evaluate, and change sub-advisers without incurring the significant delay and expense associated with obtaining prior shareholder approval. This permits the PF Funds to operate more efficiently and cost-effectively. Without the Order, Pacific Funds Trust would be required to call and hold a shareholder meeting for the PF Funds before it appoints a new sub-adviser or materially amends a sub-advisory agreement. Each time a shareholder meeting is called, Pacific Funds Trust would be required to create and distribute proxy materials to and solicit proxy votes from the PF Funds’ shareholders. This process is time-consuming and costly and such costs would generally be borne by the PF Funds, thereby reducing shareholders’ investment returns.

The Adviser currently monitors the performance of all sub-advisers and will monitor the performance and provision of investment advisory services provided by Rothschild, as the sub-adviser to the PF Funds. The Adviser is responsible for recommending to the PF Board whether a sub-advisory agreement should be entered into or terminated. In determining whether to make such recommendations, the Adviser considers several factors, including the sub-adviser’s performance record. When a shareholder invests in the PF Funds, the shareholder effectively hires the Adviser to manage the assets of the fund, either directly or via a sub-adviser under the Adviser’s supervision. The Pacific Funds Trust prospectus informs shareholders that the Adviser and the Pacific Funds Board will take responsibility for overseeing any sub-advisers, including Rothschild, engaged for the PF Funds and for recommending whether a particular sub-adviser should be hired, terminated, or replaced. The initial sole shareholder of the PF Funds has approved this manager-of-managers arrangement.

The Board also considered that at the closing of the Reorganizations, the Pacific Funds family of funds is expected to have 18 retail mutual funds, including the six Rothschild U.S. equity funds, the six Adviser managed fixed income funds (managed through its Pacific Asset Management business division), and six asset allocation funds that will be available as direct investment options to Rothschild Fund shareholders. This broader range of investment options will permit investors in the Pacific Funds Trust family of funds to diversify their investments and to participate in a range of investment styles currently prevalent in the market. Shareholders can, with a few exceptions, make purchases of or exchanges for certain classes of other series of the Pacific Funds family of funds. Thus, if the Reorganizations are approved and completed, Rothschild Funds shareholders will have more investment options and greater flexibility to change investments through exchanges. Any such exchanges generally will be taxable for U.S. federal income tax purposes.

9

The Board considered that the current adviser to the Rothschild Funds would provide sub-advisory services to the PF Funds. The Board noted that the Sub-Adviser’s team members have significant investment experience related to the investment management of the Rothschild Funds and have been responsible for its performance record since its inception.

Conflicts of Interest. The Board considered that Rothschild and the Adviser are subject to a conflict of interest in making their recommendation to the Board. In this regard, the Board received information regarding the terms of a “Fund Adoption Agreement” entered into between the Adviser and Rothschild pursuant to which Rothschild will receive a cash payment from the Adviser to help defray certain costs associated with the establishment of the Rothschild Funds and certain transactional expenses resulting from the Reorganizations. The Board also considered that the Adviser had a conflict of interest in that if the Reorganizations were consummated, it would become the investment adviser, and would be paid advisory fees, on an existing asset base from the PF Funds and that its affiliate serves as the distributor and principal underwriter of the PF Funds and would be receiving distribution fees in connection there with.

Tax Consequences. The Board considered that the Reorganizations are expected to be free from adverse federal income tax consequences.

Other Alternatives. The Board considered several alternatives to the Reorganizations, including the potential liquidation of the Funds. After considering the merits and viability of these other alternatives, the Board concluded that the possible alternatives were less desirable than the Reorganizations as the Reorganizations would provide shareholders with the options of (i) transferring their investment to a similar fund on a tax-free basis in the Reorganization or (ii) redeeming their investment in the Rothschild Funds, which may have tax consequences for them. The Board noted that liquidating and terminating the Rothschild Funds would provide shareholders with only one option that may have adverse tax consequences for them. The Board further considered that Rothschild did not feel that it was economically prudent for it to continue to subsidize the Funds’ expenses over the long term given the fact that it had determined not to expend the significant resources necessary to further develop its mutual fund distribution capabilities.

Based on the foregoing and additional information presented at the Board meetings discussed above, the Board determined that the Reorganization is the best alternative for each Rothschild Fund at this time and is in the best interests of each Rothschild Fund and its shareholders. The Board approved the Reorganizations, subject to approval by shareholders of the applicable Rothschild Fund and the solicitation of the shareholders of each Rothschild Fund to vote “FOR” the approval of the Reorganization for such Rothschild Fund, including the Plan, the form of which is attached to this Proxy Statement in Appendix A.

D. COMPARISON OF INVESTMENT OBJECTIVES, PRINCIPAL INVESTMENT STRATEGIES AND MANAGEMENT OF THE FUNDS

The Rothschild Funds and the PF Funds have substantially similar investment objectives and strategies, which are presented in the table below.

The PF Funds have been created as a shell series of the Pacific Funds Trust solely for the purpose of acquiring the corresponding Rothschild Funds’ assets and continuing that Fund’s investment strategy, and will not conduct any investment operations until after the closing of the Reorganizations. The Adviser has reviewed each Rothschild Fund’s current portfolio holdings and determined that those holdings are compatible with the PF Fund’s investment objectives and policies. As a result, the Adviser believes that, if each Reorganizations is

10

approved, all or substantially all of each Rothschild Fund’s assets will be transferred to and held by the corresponding PF Fund.

Rothschild U.S. Small/Mid-Cap Core Fund and Pacific Funds Small/Mid-Cap:

| Rothschild Fund

|

PF Fund

| |||

| Investment Objective |

The Rothschild Fund’s objective is to seek long-term capital appreciation.

|

Same. | ||

| The Rothschild Fund’s investment objective is a non-fundamental policy which may be changed by the Board without shareholder approval upon 60 days’ written notice to shareholders.

|

Same. | |||

| Principal Investment Strategies |

In normal market conditions, the Rothschild Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in common stocks and other equity securities of small and medium capitalization U.S. companies.

The Rothschild Fund defines small and medium capitalization companies as companies whose market capitalizations falls within the range of the Russell 2500™ Index at the time of purchase. As of June 30, 2014, the market capitalization range of the Russell 2500™ Index was $143 million to $9.9 billion.

The Rothschild Fund invests in securities which the portfolio management team believes are attractively valued with the potential to exceed investor expectations. The Rothschild Fund’s investment team analyzes a variety of quantitative and fundamental inputs in making stock decisions, and the team seeks to build portfolios which are well diversified by stock and by economic sector. The Rothschild Fund may sell securities which no longer meet the investment criteria of the portfolio management team. |

Same. | ||

| Temporary Defensive Position |

The Rothschild Fund may temporarily depart from its principal investment strategy and make short-term investments in cash, cash equivalents, short-term debt securities, exchange-traded funds and money market instruments in response to adverse market, economic or political | The PF Fund may take temporary defensive positions that are inconsistent with its investment strategies if the Manager believes adverse market, economic, political or other conditions make it appropriate to try to protect the PF Fund from potential loss, for | ||

11

| Rothschild Fund

|

PF Fund

| |||

| conditions. To the extent the Rothschild Fund makes such “defensive investments,” it may not achieve its investment objective. | redemptions, at start-up of the PF Fund, or other reasons. In such cases, the PF Fund may temporarily invest (partially or extensively) in U.S. government securities, high quality corporate debt securities/debt obligations, mortgage-related and asset-backed securities or money market instruments (short-term high quality instruments) and/or cash equivalents (overnight investments). In addition, the PF Fund may invest cash balances in such instruments at any time. These investments may alter the risk/return characteristics of the PF Fund and cause the PF Fund to miss investment opportunities and not to achieve its investment goal. Defensive positions could detract from investment performance in a period of rising market prices, but may reduce the severity of losses in a period of falling market prices and provide liquidity for making additional investments or for meeting redemptions. | |||

| Investment Adviser

|

Rothschild Asset Management Inc. | Pacific Life Fund Advisors LLC. | ||

| Sub-Adviser

|

None. | Rothschild Asset Management Inc. | ||

| Portfolio Managers |

R. Daniel Oshinskie, CFA, Chief Investment Officer, Lead Portfolio Manager of the Rothschild Fund since inception, 2014.

Joseph Bellantoni, CFA, Managing Director, Portfolio Manager of the Rothschild Fund since inception, 2014.

Tina Jones, CFA, Managing Director, Portfolio Manager of the Rothschild Fund since inception, 2014.

Douglas J. Levine, CFA, Managing Director, Portfolio Manager of the Rothschild Fund since inception, 2014. |

Same. |

12

Rothschild U.S. Small-Cap Core Fund and Pacific Funds Small-Cap:

| Rothschild Fund

|

PF Fund

| |||

| Investment Objective |

The Rothschild Fund’s objective is to seek long-term capital appreciation.

|

Same. | ||

| The Rothschild Fund’s investment objective is a non-fundamental policy which may be changed by the Board without shareholder approval upon 60 days’ written notice to shareholders.

|

Same. | |||

| Principal Investment Strategies |

In normal market conditions, the Rothschild Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in common stocks and other equity securities of small capitalization U.S. companies.

For purposes of the Rothschild Fund’s investments, small capitalization companies are defined as those whose market capitalizations falls within the range of the Russell 2000® Index at the time of purchase. The market capitalization range for the Russell 2000® Index was $143 million to $4.5 billion as of June 30, 2014.

The Rothschild Fund invests in securities which the portfolio management team believes are attractively valued with the potential to exceed investor expectations. The Rothschild Fund’s investment team analyzes a variety of quantitative and fundamental inputs in making stock decisions, and the team seeks to build portfolios which are well diversified by stock and by economic sector. The Rothschild Fund may sell securities which no longer meet the investment criterial of the portfolio management team. |

Same. | ||

| Temporary Defensive Position |

In response to adverse market, economic or political conditions, the Rothschild Fund may temporarily depart from its principal investment strategies and may make short-term investments in cash, cash equivalents, short-term debt securities, exchange-traded funds and money market instruments. To the extent the Rothschild Fund makes such | The PF Fund may take temporary defensive positions that are inconsistent with its investment strategies if the sub-adviser believes adverse market, economic, political or other conditions make it appropriate to try to protect the PF Fund from potential loss. In such cases, the PF Fund may temporarily invest in U.S. government securities, | ||

13

| Rothschild Fund

|

PF Fund

| |||

| “defensive investments,” it may not achieve its investment objective. | high quality corporate debt securities/debt obligations, mortgage related and asset-backed securities or money market instruments and/or cash equivalents. These investments may result in the PF Fund not achieving its investment goal. | |||

| Investment Adviser

|

Rothschild Asset Management Inc. | Pacific Life Fund Advisors LLC. | ||

| Investment Sub-Adviser

|

None. | Rothschild Asset Management Inc. | ||

| Portfolio Managers |

Joseph Bellantoni, CFA, Managing Director, Lead Portfolio Manager of the Rothschild Fund since inception, 2014.

Tina Jones, CFA, Managing Director, Portfolio Manager of the Rothschild Fund since inception, 2014.

Douglas J. Levine, CFA, Managing Director, Portfolio Manager of the Rothschild Fund since inception, 2014.

R. Daniel Oshinskie, CFA, Chief Investment Officer, Portfolio Manager of the Rothschild Fund since inception, 2014. |

Same. |

Rothschild U.S. Small-Cap Value Fund and Pacific Funds Small-Cap Value:

| Rothschild Fund

|

PF Fund

| |||

| Investment Objective |

The Rothschild Fund’s objective is to seek long-term capital appreciation.

The Rothschild Fund’s investment objective is a non-fundamental policy which may be changed by the Board without shareholder approval upon 60 days’ written notice to shareholders.

|

Same.

Same. | ||

| Principal Investment Strategies |

In normal market conditions, the Rothschild Fund will invest at least 80% of its net assets (plus any borrowings for investment purposes) in common stocks and other equity securities of small capitalization U.S. companies.

For purposes of the Rothschild Fund’s investments, a small capitalization company is defined as one whose market capitalization falls within the range of the Russell 2000® Value Index at the time of |

Same. |

14

| Rothschild Fund

|

PF Fund

| |||

| purchase. The Rothschild Fund defines value companies as companies in or similar to companies in the Russell 2000® Value Index. The market capitalization range for the Russell 2000 Value Index was $156 million to $4.4 billion as of June 30, 2014.

The Rothschild Fund invests in securities which the portfolio management team believes are attractively valued with the potential to exceed investor expectations. The Rothschild Fund’s investment team analyzes a variety of quantitative and fundamental inputs in making stock decisions, and the team seeks to build portfolios which are well diversified by stock and by economic sector. The Rothschild Fund may sell securities which no longer meet the investment criterial of the portfolio management team.

|

||||

| Temporary Defensive Position |

In response to adverse market, economic or political conditions, the Rothschild Fund may temporarily depart from its principal investment strategies and may make short-term investments in cash, cash equivalents, short-term debt securities, exchange-traded funds and money market instruments. To the extent the Rothschild Fund makes such “defensive investments,” it may not achieve its investment objective. | The PF Fund may take temporary defensive positions that are inconsistent with its investment strategies if the sub-adviser believes adverse market, economic, political or other conditions make it appropriate to try to protect the PF Fund from potential loss. In such cases, the PF Fund may temporarily invest in U.S. government securities, high quality corporate debt securities/debt obligations, mortgage related and asset-backed securities or money market instruments and/or cash equivalents. These investments may result in the PF Fund not achieving its investment goal. | ||

| Investment Adviser

|

Rothschild Asset Management Inc. | Pacific Life Fund Advisors LLC. | ||

| Investment Sub-Adviser

|

None. | Rothschild Asset Management Inc. | ||

| Portfolio Managers |

Tina Jones, CFA, Managing Director, Lead Portfolio Manager of the Rothschild Fund since inception, 2014.

Joseph Bellantoni, CFA, Managing Director, Portfolio Manager of the Rothschild Fund since inception, 2014. |

Same. |

15

| Rothschild Fund

|

PF Fund

| |||