UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended:

or

For the transition period from ________ to ________

Commission File No.

(Exact name of registrant as specified in its charter) |

| ||

(State or other jurisdiction of |

| (I.R.S. employer |

incorporation or formation) |

| Identification No.) |

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: +

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As of the last business day of the Issuer’s most recently completed second fiscal quarter, June 30, 2024, the aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $

As of April 1, 2025, there were

DOCUMENTS INCORPORATED BY REFERENCE:

None

Table of Contents

| 2 |

| Table of Contents |

PART I

FORWARD-LOOKING STATEMENTS

Certain statements made in this Annual Report on Form 10-K are “forward-looking statements” (within the meaning of the Private Securities Litigation Reform Act of 1995) regarding the plans and objectives of management for future operations. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results, performance, or achievements of the Registrant to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The forward-looking statements included herein are based on current expectations that involve numerous risks and uncertainties. The Registrant’s plans and objectives are based, in part, on assumptions involving the continued expansion of business. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond the control of the Registrant. Although the Registrant believes its assumptions underlying the forward-looking statements are reasonable, any of the assumptions could prove inaccurate and, therefore, there can be no assurance the forward-looking statements included in this Report will prove to be accurate. In light of the significant uncertainties inherent in the forward-looking statements included herein, the inclusion of such information should not be regarded as a representation by the Registrant or any other person that the objectives and plans of the Registrant will be achieved.

The forward-looking statements are not meant to predict or guarantee actual results, performance, events, or circumstances and may not be realized because they are based upon our current projections, plans, objectives, beliefs, expectations, estimates, and assumptions and are subject to a number of risks and uncertainties and other influences, many of which we have no control over. Actual results and the timing of certain events and circumstances may differ materially from those described by the forward-looking statements as a result of these risks and uncertainties. Factors that may influence or contribute to the accuracy of the forward-looking statements or cause actual results to differ materially from expected or desired results may include, without limitation:

| ☐ | Market acceptance of our products and services; |

| ☐ | Competition from existing products or new products that may emerge; |

| ☐ | The implementation of our business model and strategic plans for our business and our products; |

| ☐ | Estimates of our future revenue, expenses, capital requirements and our need for financing; |

| ☐ | Our financial performance; |

| ☐ | Current and future government regulations regarding the sports betting industry; |

| ☐ | Developments relating to our competitors; and |

| ☐ | Other risks and uncertainties, including those listed under the section titled “Risk Factors.” |

Readers are cautioned not to place undue reliance on forward-looking statements because of the risks and uncertainties related to them and to the risk factors. We disclaim any obligation to update the forward-looking statements contained in this Report to reflect any new information or future events or circumstances or otherwise, except as required by law.

Readers should read this Report in conjunction with the discussion under the caption “Risk Factors,” our financial statements and the related notes thereto in this Report, and other documents which we may file from time to time with the SEC.

| 3 |

| Table of Contents |

USE OF DEFINED TERMS

Except where the context otherwise requires and for the purposes of this report only:

· | “we,” “us,” “our company,” “our” and “Company” refer to the combined business of Apple iSports Group, Inc., a Nevada corporation, and its consolidated subsidiaries; |

|

|

· | “AiS” or “Subsidiary” refers to Apple iSports, Inc., a Delaware corporation, and its subsidiary AiS Australia; |

|

|

· | “AiS Australia” refers to Apple iSports Australia Pty Ltd., an Australian company; |

|

|

· | “SEC” refers to the United States Securities and Exchange Commission; |

|

|

· | “AUD” refers to the Australian dollar; |

|

|

· | “U.S. dollars”, “USD,” “dollars,” and “$” refer to the United States dollar; |

|

|

· | “Securities Act” refers to the United States Securities Act of 1933, as amended; and |

|

|

· | “Exchange Act” refers to the United States Securities Exchange Act of 1934, as amended. |

Solely for the convenience of the reader, this report contains conversions of certain AUD amounts into U.S. dollars at specified rates. See “Risk Factors—Risks Related to Our Business— Fluctuations in exchange rates could adversely affect our business and the value of our securities.”

Item 1. Business.

Background

Prevention Insurance.Com (the “Company”) was incorporated under the laws of the State of Nevada in 1975 as Vita Plus Industries, Inc. In March 1999, the Company sold its remaining inventory and changed its name to Prevention Insurance.Com.

On August 31, 2023, the Company amended its Articles of Incorporation with the Nevada Secretary of State to affect the name change of the Company to Apple iSports Group, Inc.

| 4 |

| Table of Contents |

DESCRIPTION OF OUR BUSINESS

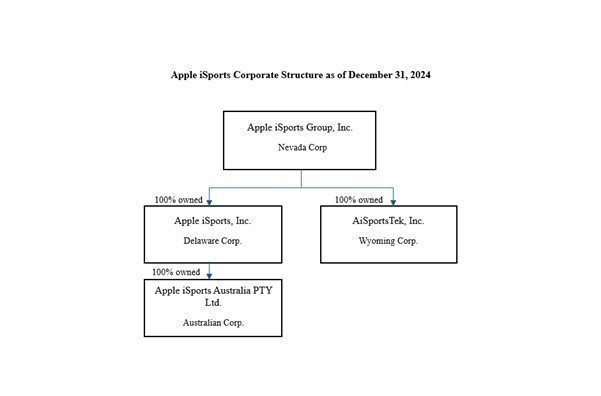

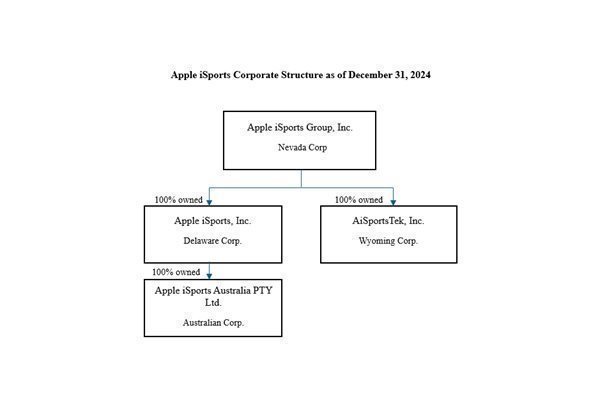

Our corporate structure is depicted below:

Industry Terms.

Pari-mutuel Betting - All the bets/money placed on an event are aggregated into a single pool of money, the “take-out” (by the totalizator operator) is subtracted, and dividends (distribution to bettors) are calculated by dividing the pool between winning bets based on their odds. The returns are subject to the calculation of dividends after the conclusion of the race. Before the market closes, approximate dividends can be displayed, but the final dividend can change after wagers are placed. Typically, pari-mutuel betting is used in thoroughbred horse racing, greyhound racing, and harness racing, among other races and other events.

Tote Derivative - Bets are paid out at a price declared by one or more pari-mutuel (totalizator) providers. Typically, this type of betting is seen in exotic bets (trifectas, quinellas, daily doubles, etc.) in racing.

Fixed Odds Betting – The oddsmakers set odds for bettors to wager on. Once bettors place their wagers, they’re locked into the odds that they’ve chosen. So, when bettors place their bets, they know their return in the event of a winning bet. This type of betting is the most common type seen in sporting events.

Advanced Deposit Wagering (ADW) – the type of account where the bettor (customer) must fund before placing a wager.

Apple iSports Business History

On May 29, 2019, Apple iSports, Inc. (“AiS”) was incorporated in Delaware. On November 9, 2021, AiS incorporated Apple iSports Australia Pty. Ltd. (“AiS Australia”) as its wholly owned subsidiary.

AiS has been engaged in developing a fixed odds and live streaming sports betting application targeting the Australian online sports betting market. Our formal licensing application with NTRWC is contingent upon board approval for funding Australian betting operations.

In the USA, AiS has been engaged in developing a multi-tenancy Class II, Class III and sports betting platform targeting Tribal lands - supported by provisioning broadband private LTE networks through a strategic partnership with Americrew.

In addition, we have been approved by the North Dakota Racing Commission in the State of North Dakota as an (ADW) provider, which, subject to the approval of the Thoroughbred Racing Protective Bureau (discussed below), will allow us to provide pari-mutuel betting on horse racing in North Dakota and in 20 additional U.S. states. As of the date of this filing, we do not have an online sports betting license in any state in the U.S.

| 5 |

| Table of Contents |

Our two primary markets are Australia and the U.S. (initially in North Dakota and such other states where we intend to become licensed, as well as deploying gaming solutions in Tribal Lands). We will have separate websites for both markets, namely www.appleisports.com in the U.S. and www.appleisports.com.au in Australia.

Since the inception of AiS, we have achieved the following milestones:

| · | Since the inception of AiS through December 31, 2024, we (i) established a core team with the industry skills and experience to manage the Company and (ii) received approximately $2,744,900 in private placement funding and received loans from related parties of more than $3,597,442. |

| · | From December 2021 to October 2022, we developed our Go-to Market outline and marketing strategy, including identifying preferred suppliers for each product and initiating relationships with key suppliers and consultants; |

| · | In June 2022, we submitted our application to the North Dakota Racing Commission for an (ADW) license, subject to the approval of the Thoroughbred Racing Protective Bureau. Completion of the TRPB examination is required to receive a state-issued ADW; This will be concluded subsequent to closing the capital raising. |

| · | In October 2022, we engaged a provider of white-label sportsbook platforms and began customization and integration with key components (KYC, payments, CRM, credit card verification) and data feeds.; Our platform will be implemented within 12-16 weeks of completing the capital raising.; |

| · | Effective March 23, 2023, we completed a change of control transaction pursuant to a Stock Exchange Agreement (the “Stock Exchange Agreement”) with AiS and the shareholders of AiS. The stock exchange was accounted for under the business combination under the common control of accounting. Consequently, the assets and liabilities and the historical operations that are reflected in the financial statements prior to the stock exchange are those of AiS and the Company combined. They are recorded at the historical cost basis, and the condensed consolidated financial statements after completion of the stock exchange include the combined assets and liabilities of AiS and the Company from the closing date of the stock exchange, as a result of the issuance of the shares of our common stock pursuant to the stock exchange, a change in control of the Company occurred as of the date of consummation of the transaction. |

| · | In May 2023, we began brand awareness activities by advertising around Australia on SEN Radio, the largest sports radio network in Australia. Advertising continued sporadically through August of 2024; |

Our address is 100 Spectrum Center Dr., Suite 900, Irvine, CA 92612, and our phone number is (949) 247-4210. We also maintain satellite offices at Level 1, Paspalis Centrepoint, 48-50 Smith Street Mall, Darwin NT 0800 Australia and 55 Lonsdale Street, Level 7, Melbourne, Australia 3000. In addition, as mentioned, we have two websites (which do not form a part of this filing): www.appleisports.com in the U.S. and www.appleisports.com.au in Australia.

| 6 |

| Table of Contents |

Our Apple iSports Platform

Apple iSports platform will feature the following “products”:

❖ | Fixed Odds Sport Betting |

❖ | Fixed Odds & Pari-Mutuel Odds Horse Racing |

❖ | Live Content Streaming |

These individual products are further described below:

Sports Betting. Will provide betting coverage for many major sporting leagues and events, including but not limited to the National Football League (NFL), Australian Rules Football (AFL), Major League Baseball (MLB), the National Basketball Association (NBA), as well as for other sports, such as Cricket, Golf, Ice Hockey, Soccer, and Tennis.

Sports betting, at its simplest, is placing a financial wager on the outcome of a sporting game or match, including certain events that occur within such a game or match. The product will feature functionality designed to provide a personalized customer experience. The product will be capable of taking and placing a variety of betting types and combinations.

These betting opportunities will be fixed-odds bets, which means that we will set the odds for each such event. There is a market ratio in each market offered to our customers, which is the average level of profit over every proposition in the market. We will manage our margins using smart technologies and traditional risk management methodologies.

Horse Racing. We will provide advanced racing informatics to the user. Our analysis and insights will include race and individual ratings, previous winning margins, speed maps and race analysis. We also will provide live updates for scratches, jockeys, prices, track conditions and race start time changes.

In Australia, racing wagering will include fixed odds and tote derivative betting. We derive revenues based on the management of risk. Initially, racing wagering will consist of participating in pari-mutuel pools in the United States.

Live Content Streaming. Our Live Content Sports Streaming Channel will provide great value to the Apple iSports brand. Users will be able to watch a wide range of live sporting events and sports-based shows. We believe this feature will promote more betting by users. The Live Content Sports Streaming Channel will have up to 8 minutes per hour of advertising space, and we intend to sell this space to generate revenue. Any unsold ad space will be used to promote other Apple iSports offerings where applicable and compliant with existing advertising rules governing online sports betting in Australia.

The Live Content Sports Streaming Channel will be available on the Apple iSports websites, as well as on a range of distribution platforms.

| 7 |

| Table of Contents |

Our Revenue Model.

Our revenue model is premised on several streams of operations. We expect to profit from pari-mutuel and fixed odds gaming, as well as advertising. In pari-mutuel gaming, we receive a fee on the total amount bet on an event. The type of wagering is essentially risk-free and is payable regardless of the outcome of the event since we are not on either side of a bet. Our pari-mutuel provider places bet funds from bets made through our platform in the betting pools and manages the ‘rake’ (a fixed percentage of the total amount bet on an event) and apportions our share based on the percentage of the pool contributed through all of our apps.

In fixed odds gaming, we actively manage risk through experienced risk management and smart technology, including laying off risk where necessary. We also use client profiling techniques to ensure we leverage client segmentation to enhance risk management tools.

In Australia, we expect approximately 60% of betting revenue to be from horse racing, with the rest spread across all sports). In the U.S., however, sports betting is more widely practiced than racing and we expect a much higher portion to be sports-related. Once we begin acquiring sports betting licenses in the future.

By exploring freemium pricing, microtransactions, and subscription services, Apple iSports streaming video services could expand audiences and increase engagement through diverse experiences.

We also expect to generate revenue from the deployment of technology to Tribal Casinos and gaming operators. Such revenue should include implementation fees, ongoing maintenance fees, and, in some cases, revenue share from operators.

Our Growth Strategy.

Our growth strategy is premised on market expansion and building brand positioning and reach to drive customer acquisition.

New Markets. Currently, we intend to be licensed to sell all our products throughout Australia and our racing product in North Dakota and approximately 20 other states in the United States. We are in the process of developing an iGaming platform for the tribal casino market.

Engaging Content. We believe that content delivered via our Live Content Sports Streaming Channel is essential to our success. The channel creates engagement, generates its own revenue via ad sales, and anchors users to our site, which in turn provides a range of opportunities to promote our products. The channel also delivers content, such as drag racing, beach volleyball and more, along with odds and, potentially, fantasy leagues. Odds and wagering on these events are not available through other sports betting platforms.

New Users in Existing Markets. We intend to reach new users in targeted markets using digital marketing activations such as search engine optimization, pay-per-click, and search engine marketing (SEO/PPC/SEM) by leveraging a range of marketing strategies to drive more people to our website. We will have a carefully targeted strategy that identifies traffic with high conversion rates based on industry experience and digital marketing background. We also intend to profile potential customers based on their betting history which will enable us to provide highly targeted ads and content. We will use social media to drive engagement organically.

| 8 |

| Table of Contents |

Website and Product Development.

We have entered into agreements with various software providers to develop our website, our sportsbook, and our Live Content Sports Streaming Channel.

The Apple iSports website and products are being developed under the direction of our Chief Operating Officer and Chief Technology Officer. Strategic planning and specifications are being conducted in-house, as are key design tasks.

The sportsbook is the core of the Apple iSports backend and provides the main user database, reporting and key integration points. This includes a single sign-on/log-in to all functions. The sportsbook is being developed by a third-party vendor, Australia, with PuntersTech, securing a customized sports betting platform optimized for the Australian market.

Customization of the sportsbook, including implementation of Apple iSport’s novel bet types, reporting requirements and user interface, along with integration to core components such as payments, identity verification, specialized data feeds and geo-control, are being implemented for the Australian markets in parallel by experienced vendors, with significant collaboration with the Apple iSports team.

The Apple iSports Live Content Sports Streaming Channel is being implemented by leading sports content producers and curators in Australia, with global content and distribution reach. As our content partner, they will produce and program the content for specific markets and sports, as well as manage licensing and rights clearances. The channel will initially be integrated into the Apple iSports (Australia) website.

The sports channel developer is remunerated for the initiation and management of the channel and oversight of the technical operations of distribution and delivery. This content may be added to the primary channel programming or form the basis of a secondary linear channel or, potentially, an ad supported video on demand. After the first year of operations, a revenue share arrangement is contemplated but has not yet been agreed upon.

| 9 |

| Table of Contents |

Markets and Marketing.

Markets.

Sports betting has become one of the most important categories in entertainment because of the fanaticism of the fans. It is captivating and connects millions of people and many of the largest sectors in the global economy, from betting, online gaming, and digital platforms to live events, retail, broadcasting, sponsorship, and merchandising.

A report published by IMARC Group stated, “The global sports betting market size was valued at USD 103.08 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 224.12 Billion by 2033, exhibiting an annual growth rate of 8.56% from 2025-2033.”

In the United States, after the Supreme Court’s decision to strike down the federal ban on sports betting in the United States in May 2018, various states have legalized or introduced legislation to legalize the sports betting industry.

According to the same source, the united states holds 86.50% shares of North America. These margins have been driven by the legalization of sports betting in multiple states. This has been paired with the utilization of technological advancement such as smartphones and high-speed internet has made sports betting more convenient.

Australia is one of the most mature legal betting markets in the world, and sports betting (including racing) has been legal for over three decades in several major global markets, such as the United Kingdom, Latin America, Italy, and other parts of Europe and Asia Pacific. Much like un the United States, the Australian market is experiencing an increase in app-based sports betting that is curated to its users. It is expected that these markets will exhibit an annual growth rate of 9.45% during 2025-2033 according to IMARC Group.

Marketing.

We intend to deploy a mix of marketing strategies. These strategies include;

| · | Database and collaborative marketing with related industry partners, |

| · | Digital marketing on key industry and related sites |

| · | Marketing on various social media sites |

| · | Search engine optimization and search engine marketing, |

| · | Affiliate partnerships |

| · | Conferences and targeted corporate selling for technology offerings and |

| · | Extensive public relations to build fan awareness and support amongst financial analysts and investors |

| · | Highly selective paid advertising on media dedicated to sports and racing, such as Sports Entertainment Network in Australia |

All of our efforts are designed to bring brand awareness to potential users on these sites or venues.

| 10 |

| Table of Contents |

Our principal considerations related to attracting and retaining online users include functionality, ease of use, -of-our 24/7 sports channel, and, most importantly, best-of-breed racing and sports information and analytics combined with extremely competitive odds (where we are able to offer fixed-odds wagering).

Notwithstanding our perceived competitive advantages, we face competition from companies that are substantially larger and better financed. Our future success depends on our ability to compete effectively with them. As a result, we may have difficulty competing with these larger, established competitor companies. Generally, they have:

· | substantially greater financial, technical, and marketing resources; |

· | larger customer bases; |

· | better name recognition and |

· | potentially more expansive product or app offerings. |

These competitors are likely to command a larger market share, which may enable them to establish a stronger competitive position than we have, in part, through greater marketing opportunities. Further, our competitors may be able to respond more quickly than us to new or emerging technologies and changes in user preferences and devote greater resources than us to developing and operating networks of affinity websites. These competitors may develop products or services that are comparable or superior. If we fail to address competitive developments quickly and effectively, we may not become or be able to remain a viable entity.

We have identified external opportunities through mergers and acquisitions (M&A) to complement our organic growth initiatives, which will accelerate the achievement of our strategic objectives. This approach combines the benefits of both organic and inorganic growth strategies to drive rapid expansion and enhance our competitive position.

Intellectual Property

Trademark applications have been filed for certain Apple iSports logos and marks with the United States Patent and Trademark Office in the US and with IP Australia. The following applications have been filed:

· | Australian trademark for the Apple iSports ‘a’ icon logotype was filed on July 6, 2023 and approved on February 14, 2024 |

· | U.S. trade market for the Apple iSports ‘a’ icon logotype was filed on July 18, 2023 and remains pending as of April 1, 2025 |

· | US trademark for Apple iSports stylized name logotype was filed on July 18, 2023 and remains pending as of April 1, 2025 |

Applications in the US for the swoosh and ball logos were withdrawn in December 2023.

We have not filed for patent protection for any of our betting processes which we have developed and which we believe to be novel. Instead, we will rely on trade secrets and know-how protection. There is no assurance that others will not independently develop the same or similar technology or obtain unauthorized access to our trade secrets, know-how, and other unpatented technology. To protect our rights in these areas, we require all third parties that develop software to maintain such information as confidential. These agreements may not provide meaningful protection for our unpatented technology in the event of unauthorized use, misappropriation, or disclosure.

Government Regulation.

We are subject to various U.S. and foreign laws and regulations that affect our ability to operate in the sports betting industry. This industry is generally subject to extensive and evolving regulations that could change based on political and social norms and that could be interpreted in ways that could negatively impact its business.

| 11 |

| Table of Contents |

The sports betting industry is heavily regulated and in order to continue our operations, we must maintain licenses and pay gaming taxes or a percentage of revenue in each jurisdiction in which we operate. Our business is subject to extensive regulation under the laws, rules, and regulations of these jurisdictions. These laws, rules, and regulations generally concern the responsibility, financial stability, integrity, and character of the owners, managers, and persons with material financial interests in gaming operations, along with the integrity and security of our sports betting offerings. Violations of laws or regulations in one jurisdiction could result in disciplinary action in other jurisdictions.

These laws are generally based upon declarations of public policy designed to protect gaming consumers and the viability and integrity of the gaming industry. Gaming laws also may be designed to protect and maximize state and local tax revenues, as well as to enhance economic development and tourism. To accomplish these public policy goals, gaming laws establish stringent procedures to ensure that participants in the gaming industry meet certain standards of character and responsibility. Among other things, gaming laws require gaming industry participants to; ensure that unsuitable individuals and organizations have no role in gaming operations, establish procedures designed to prevent cheating and fraudulent practices, establish and maintain anti-money laundering practices and procedures, file periodic reports with gaming regulators, establish programs to promote responsible gaming and enforce minimum age requirements.

In addition, there are various U.S. relating to the advertising of gambling products that are not enforced by gambling regulators and are still applicable. Spam and privacy laws apply to our communications as well, such as having a link in emails or messages to allow immediate opting out.

Typically, a U.S. regulatory environment is established by statute and underlying regulations and is administered by one or more regulatory agencies (typically a gaming commission or state lottery) that regulate the affairs of owners, managers, and persons with financial interests in gaming operations. While we believe we comply in all material respects with all applicable sports betting laws, licenses and regulatory requirements in jurisdictions where we operate, we cannot assure that our activities or the activities of its users will not become the subject of any regulatory or law enforcement investigation, proceeding or other governmental action or that any such proceeding or action, as the case may be, would not have a material adverse impact on us or our business, financial condition or results of operations.

Government Licensing.

In order to operate in certain jurisdictions, we must obtain either a temporary or permanent license or a determination of suitability from the responsible authorities. We will ensure that we obtain all necessary licenses to develop and put forth its offerings in the jurisdictions in which we operate and where our users are located. In this regard, we have received a provisional Advance Deposit Wagering license from the North Dakota Racing Commission (subject to terms as outlined above). As a result of this license, we are able to offer pari-mutuel wagering on racing in that state and a number of other U.S. states that do not currently have specific racing regulations.

Gaming laws require us, and often each of our holding and intermediary companies as well as subsidiaries, certain of its directors, officers, and employees, and in some cases, certain of our controlling shareholders, to obtain licenses from, or found suitable by, gaming authorities. Licenses and suitability findings require a determination that the applicant is qualified. Where not mandated by statute, rule or regulation, gaming authorities typically have broad discretion in determining who must apply for a license or finding of suitability and whether an applicant qualifies for licensing or should be deemed suitable to conduct operations within a given jurisdiction. When determining to grant a license to an applicant, gaming authorities generally consider: (i) the financial stability, integrity, responsibility and suitability of the applicant and its applicable affiliated entities and individuals (including verification of the applicant’s sources of funding); (ii) the quality and security of the applicant’s online real-money gaming platform, hardware and related software, including the platform’s ability to operate in compliance with local regulation, as applicable; (iii) the applicant’s history; (iv) the applicant’s ability to operate its gaming business in a socially responsible manner; and (v) in certain circumstances, the effect on competition.

| 12 |

| Table of Contents |

Gaming authorities may, subject to certain administrative procedural requirements, (i) deny an application, or limit, condition, revoke or suspend any license issued, or suitability finding made, by them; (ii) impose fines, either on a mandatory basis or as a consensual settlement of regulatory action; (iii) demand that named individuals or shareholders be disassociated from a gaming business; and (iv) in serious cases, liaise with local prosecutors to pursue legal action, which may result in civil or criminal penalties.

Events that may trigger the revocation of a gaming license or another form of sanction vary by jurisdiction. However, typical events include, among others: (i) conviction in any jurisdiction of certain persons with an interest in, or key personnel of, the licensee of an offense that is punishable by imprisonment or may otherwise cast doubt on such person’s integrity (provided that, generally, an individual with a conviction will not result in revocation of the company’s license, rather, if required by the regulator, that person must be removed from involvement with the company); (ii) failure to comply with any material term or condition of the gaming license; (iii) declaration of, or otherwise engaging in, certain bankruptcy, insolvency, winding-up or discontinuance activities, or an order or application with respect to the same; (iv) obtaining the gaming license by a materially false or misleading representation or in some other improper way; (v) violation of applicable anti-money laundering and/or counter terrorist financing laws or regulations; (vi) failure to meet commitments to users, including social responsibility commitments; (vii) failure to pay in a timely manner all gaming or betting taxes or fees due; or (viii) determination by the gaming authority that there is another material and sufficient reason to revoke or impose another form of sanction upon the licensee.

Employees.

As of the date of this filing, we have 6 full time employees, including senior management.

Item 1A. Risk Factors

Our plan of operation is to obtain debt or equity finance to meet our ongoing operating expenses and attempt to merge with another entity with experienced management and opportunities for growth in return for shares of our common stock to create value for our shareholders. There can be no assurance that any of the events can be successfully completed, that any such business will be identified or that any stockholder will realize any return on their shares after such a transaction has been completed. In particular, there is no assurance that any such business will be located or that any stockholder will realize any return on their shares after such a transaction. Any merger or acquisition completed by us can be expected to have a significant dilutive effect on the percentage of shares held by our current stockholders. We believe we are an insignificant participant among the firms that engage in the acquisition of business opportunities. There are many established venture capital and financial concerns that have significantly greater financial and personnel resources and technical expertise than we have. Given our limited financial resources and limited management availability, we will continue to be at a significant competitive disadvantage compared to our competitors.

You should be aware that there are various risks associated with our business, including the risks discussed below. You should carefully consider these risk factors, as well as the other information contained herein, in evaluating our business and us.

Risks Related to Our Company

OUR CASH REQUIREMENTS ARE SIGNIFICANT. THE FAILURE TO RAISE ADDITIONAL CAPITAL WILL HAVE A SIGNIFICANT ADVERSE EFFECT ON OUR FINANCIAL CONDITION AND OUR OPERATIONS. Our business plan of developing, introducing and marketing our gaming platform will require a significant cash infusion. As stated elsewhere herein, we estimated that the costs to complete our business plan are approximately $5,500,000. In addition, our ongoing annual expenses are approximately $2 to $3 million, excluding marketing. Therefore, we likely will need significant, additional capital until we achieve positive cash flow. As of December 31, 2024, the Company reported net losses of $2,821,336. In addition, as of December 31, 2024, the Company had a working capital deficit of approximately $6,539,584 (of $4,210,127 is due to related parties) with cash on hand of approximately $42,167 Our auditor’s report for the December 31, 2024, year-end period includes an explanatory paragraph to their audit opinion stating that our recurring losses from operations and working capital deficiency raise substantial doubt about our ability to continue as a going concern. Currently, we do not have sufficient financial resources to fund our business plan. Therefore, we need additional financing to continue these operations and as mentioned, we may need significant additional capital to achieve positive cash flow.

| 13 |

| Table of Contents |

We believe that our existing capital resources are inadequate to enable it to execute its business plan. As of the date of this filing, we have closed our private placement at $0.25 and we raised a total of $2,744,900. We expect to continue to raise funds through the private placement of our capital stock. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. We estimate we will require additional cash resources during fiscal 2025 and beyond based on our current operating plan and condition. If we fail to generate positive cash flow or obtain additional financing, when required, we may have to modify, delay, or abandon some or all of our business plans.

OUR NEED FOR CAPITAL WILL CREATE ADDITIONAL RISKS AND CREATE POTENTIAL SUBSTANTIAL DILUTION TO EXISTING SHAREHOLDERS. As mentioned above, we will need to raise additional, perhaps significant, capital in the future. These capital expenditures are intended to be funded from third-party sources and from affiliates if available, including the incurring of debt (which may be converted into common stock) and/or the sale of additional equity securities. As of the date of this filing, the Company is indebted to certain affiliates in the amount of approximately $4,210,127 . This debt is due on demand, and the Company cannot repay its existing debt. To the extent that this debt is converted to common stock, the conversion of this debt will cause additional dilution to existing shareholders, which may be substantial. In addition, the sale of additional equity securities or the sale and conversion of other debt will likewise be dilutive to the interests of current equity holders, and such dilution may be substantial. In addition, there can be no assurance that such additional financing, whether debt or equity, will be available to the Company or that it will be available on acceptable commercial terms. Any inability to secure such additional financing on appropriate terms could have a materially adverse impact on the business, financial condition, and operating results of the Company.

WE HAVE INCURRED NET LOSS IN THE PAST AND WE MAY CONTINUE TO EXPERIENCE LOSSES IN THE FUTURE. As stated above, we incurred a net loss of approximately $2,821,336 for the annual period ended December 31, 2024. We cannot assure you that we will be able to generate net profits or positive cash flow from operating activities in the future. Our ability to achieve and maintain profitability will depend in large part on our ability to, among other things, continue to develop our gaming and sports betting platform in a cost-effective manner, sequentially increase the number of users during a short period of time, and optimize our cost structure. We may not be able to achieve any of the above. We intend to continue to invest heavily in our fulfillment infrastructure and technology platform in the foreseeable future to support an even more carefully curated selection of products and offer additional value-added services. As a result of the foregoing, we believe that we may incur net losses in the future.

OUR OPERATING LOSSES, WORKING CAPITAL, AND ACCUMULATED DEFICIT DEFICIENCY RAISE SUBSTANTIAL DOUBT ABOUT OUR ABILITY TO CONTINUE AS A GOING CONCERN. IF WE DO NOT CONTINUE AS A GOING CONCERN, INVESTORS COULD LOSE THEIR ENTIRE INVESTMENT. Our operating losses, working capital deficiency, and accumulated deficit raise substantial doubt about our ability to continue as a going concern. If we do not generate revenues, do not achieve profitability, and do not have other sources of financing for our business, we may have to curtail or cease our development plans and operations, which could cause investors to lose the entire amount of their investment.

THE ADMINISTRATIVE COSTS OF PUBLIC COMPANY REGULATORY COMPLIANCE COULD BECOME BURDENSOME AND CONSUME A SIGNIFICANT AMOUNT OF OUR CASH RESOURCES WHICH COULD MATERIALLY AND ADVERSELY AFFECT OUR BUSINESS. We will incur significant costs and expenses in connection with assuring compliance with all laws, rules, and regulations applicable to us as a public company. We anticipate that our ongoing costs and expenses of complying with our public reporting company obligations will be approximately $300,000 to $500,000 annually. Our reporting and compliance costs and expenses may increase substantially if we are able to deploy our business model on an international basis, which will add significant cross-border jurisdictional complexity to our regulatory compliance and our accounting controls and procedures. Our compliance costs and expenses could also increase substantially if we apply to trade our securities on a national stock exchange, which may have listing requirements that engender additional administration and compliance costs. We have assigned a high priority to establishing and maintaining controls, procedures, corporate compliance, and public company reporting; however, there can be no assurance that we will have sufficient cash resources to satisfy our public company reporting and compliance obligations. If we cover the cost of proper administration of our public company compliance and reporting obligations, we could become subject to sanctions, fines, and penalties, our stock could be barred from trading in public capital markets, and we may have to cease doing business

| 14 |

| Table of Contents |

INABILITY TO MAINTAIN OPERATIONAL INFRASTRUCTURE AND SYSTEMS. We understand that there are several challenges related to our infrastructure that we are going to face in future. The main challenges are computing platforms, data acquisition, compute provisioning and management, data storage architectures, data analytics, and networks and communication. Some challenges that we may face in the future such as:

❖ | Lack of Powerful Computing Platforms |

The major challenge in growing processing power of computers has been the lack of energy and space to power supercomputers. IT managers have always been on the lookout for better and faster systems which will help in the faster processing of the large amounts of data available today.

❖ | Data Acquisition Problems |

Firewalls that protect emails, applications, and web browsing, which can cause important packet losses in TCP/IP networks. This can result in important data loss and reduce network speeds considerably, making online collaboration impossible. Similar losses can occur due to switches and routers that do not have the required high-speed memory.

❖ | The dearth of Ways to Improve Data Analytics |

Currently, there are not many methods in place that an app company can use to separate quality data from the humongous data sets. It is important to identify patterns in the data, correctly analyze it, and use it to make business decisions in infrastructure management.

❖ | Improper Networks and Connectivity |

For any app company to work smoothly, a good and reliable network must be in place. Without a reliable network connection, it is difficult to maintain service quality. New software-based methods and network architecture design are required for data optimization.

WE HAVE LIMITED OPERATING HISTORY MAKES IT DIFFICULT TO EVALUATE OUR BUSINESS AND PROSPECTS. We commenced operations in late 2021 and have a limited operating history. However, our historical performance may not indicate of our future growth or financial results. Our growth may slow down or become negative, and revenues may decline for several possible reasons, some of which are beyond our control, including decreasing consumer spending, increasing competition, declining growth of our overall market or industry, the emergence of alternative business models, changes in rules, regulations, government policies or general economic conditions. It is difficult to evaluate our prospects, as we may not have sufficient experience in addressing the risks to which companies operating in rapidly evolving markets may be exposed. You should consider our prospects in light of the risks and uncertainties that companies with a limited operating history may encounter.

INTELLECTUAL PROPERTY INFRINGEMENT RESULTING IN COSTLY LITIGATION. Our success depends in part upon our proprietary technology. We rely primarily on trademark, copyright, service mark and trade secret laws, confidentiality procedures, license agreements and contractual provisions to establish and protect our proprietary rights. Despite these precautions, third parties could copy or otherwise obtain and use our technology without authorization or develop similar technology independently. We also pursue the registration of our domain names, trademarks, and service marks in the United States. We cannot assure you that the protection of our proprietary rights will be adequate or that our competitors will not independently develop similar technology, duplicate our products and services or design around any intellectual property rights we hold.

We cannot assure you that third parties will not claim our current or future products infringe on their intellectual property rights. Any such claims, with or without merit, could cause costly litigation that could consume significant management time. Such claims also might require us to enter into royalty or license agreements. If required, we may not be able to obtain such royalty or license agreements or obtain them on terms acceptable to us.

| 15 |

| Table of Contents |

WE MAY BE NEGATIVELY AFFECTED BY ADVERSE GENERAL ECONOMIC CONDITIONS. Current conditions in domestic and global economies are extremely uncertain. Adverse changes may occur due to softening global economies, wavering consumer confidence caused by the threat of terrorism and war, and other factors capable of affecting economic conditions. Such changes could have a material adverse effect on our business, financial condition, and results of operations.

BECAUSE OUR PRINCIPAL SHAREHOLDER CONTROLS OUR ACTIVITIES, HE MAY CAUSE US TO ACT IN A MANNER THAT IS MOST BENEFICIAL TO HIMSELF AND NOT TO OTHER SHAREHOLDERS, WHICH COULD CAUSE US NOT TO TAKE ACTIONS THAT OUTSIDE INVESTORS MIGHT VIEW FAVORABLY. Our principal shareholder, through his affiliates, owns approximately 42% of our outstanding common stock. As a result, he effectively controls all matters requiring stockholder approval, including the election of directors, and the approval of significant corporate transactions, such as mergers and related party transactions. These insiders may have the ability to delay or perhaps even block, by their ownership of our stock, an unsolicited tender offer. This concentration of ownership could have the effect of delaying, deterring or preventing a change in control of our company that you might view favorably.

OUR OFFICERS AND DIRECTORS MAY HAVE CONFLICTS OF INTEREST WHICH MAY NOT BE RESOLVED FAVORABLY TO US. Certain conflicts of interest may exist between our officers and directors and us. Our officers and directors have other business interests to which they also must devote their time, resources, and attention. Thus, a conflict of interest may arise in the future that may cause our business to fail, including conflicts of interest in allocating their resources, time and attention to our Company and their other business interests.

Risks Related To the Gaming/Sports Betting Industry

WE MAY EXPERIENCE FLUCTUATIONS IN OUR OPERATING RESULTS, WHICH MAKE OUR FUTURE RESULTS DIFFICULT TO PREDICT AND MAY CAUSE ITS OPERATING RESULTS TO FALL BELOW EXPECTATIONS. We expect our financial results to fluctuate in the future. These fluctuations may be due to various factors, some of which are outside of our control and may not fully reflect the underlying performance of its business.

Our financial results in any given period may be influenced by numerous factors, many of which we cannot predict or are outside of its control, including the impact of seasonality, customer betting results, and the other risks and uncertainties set forth herein. Consumer engagement in our gaming and online sports betting services may decline or fluctuate as a result of several factors, including the user’s level of satisfaction with its platforms, its ability to improve and innovate, its ability to adapt its platform, outages and disruptions of online services, the services offered by its competitors, its marketing and advertising efforts or declines in consumer activity generally as a result of economic downturns, among others. Any decline or fluctuation in the recurring portion of our business may negatively impact on our business, financial condition, results of operations or prospects.

THE SUCCESS, INCLUDING WIN OR HOLD RATES, OF EXISTING OR FUTURE IGAMING AND SPORTS BETTING PRODUCTS DEPENDS ON A VARIETY OF FACTORS AND IS NOT ENTIRELY IN OURCONTROL. The gaming and sports betting industries are characterized by an element of chance. Accordingly, we employ theoretical win rates to estimate what a certain type of gaming or sports bet, on average, will win or lose after a significant number of iterations. The net win is impacted by variations in the hold percentage (the ratio of a net win to the total amount wagered), or actual outcome, on the gaming and sports betting products that we offer to our users. We use the hold percentage as an indicator of a gaming’s or sports bet’s performance against its expected outcome. Although each gaming or sports bet generally performs within a defined statistical range of outcomes, actual outcomes may vary in accordance with statistical probability. In addition to the element of chance, win rates (hold percentages) may also (depending on the game involved) be affected by the spread of limits and factors that are beyond our control, such as a user’s skill, experience and behavior, the mix of games played, the financial resources of users, the volume of bets placed, and the amount of time spent gambling. As a result of the variability in these factors, the actual win rates for our gaming offerings and sports betting wagers may differ materially from the theoretical win rates we have estimated and could result in the winnings exceeding its expectations based on statistical law. The variability of win rates (hold rates) also has the potential to negatively impact our financial condition, cash flow and overall business operations. In addition, we do not have an insurance policy to cover any excessive losses.

| 16 |

| Table of Contents |

WE WILL REQUIRE ADDITIONAL CAPITAL TO SUPPORT ITS GROWTH INITIATIVES, AND SUCH CAPITAL MAY NOT BE AVAILABLE ON ECONOMICALLY FAVORABLE TERMS, IF AT ALL. THIS COULD HAMPER OUR GROWTH AND ADVERSELY AFFECT OUR BUSINESS. To fully develop our business plan and otherwise support our growth in the sports and gaming industries, we will need to raise additional capital to address these needs. These funds may be in the form of additional equity or debt financings. Our ability to obtain additional capital when required will depend on our business plans, investor demand, operating performance, capital markets conditions, and other variables, some of which are uncertain. If we raise additional funds by issuing equity, equity-linked, or debt securities, those securities may have rights, preferences, or privileges senior to the rights of its currently issued and outstanding equity, and its existing stockholders may experience dilution. If we are unable to obtain additional capital when required, or on satisfactory terms, our ability to continue to support our business growth or to respond to business opportunities, challenges, or unforeseen circumstances will be adversely affected, and our business will be severely harmed.

LACK OF INSURANCE FOR FIXED ODDS BETTING. The Company intends to manage its fixed odds betting through smart technology. There are no assurances that the Company will successfully manage its fixed odds betting. In addition, the Company does not maintain, nor does it intend to maintain, insurance to cover these types of bets. A significant loss in the fixed odds segment of its business will adversely impact on the Company and its operations.

INTENSE COMPETITION. We will face intense competition in the gaming/sports betting industry. Substantially some of our competitors have greater managerial, financial, and technical resources than our company, as well as greater name and brand recognition than us. This type of environment is extremely challenging for a start-up company like us and, as a result, we may find it difficult for us to overcome and become a successful company.

Risks Related To Our Information Technology

WE RELY ON INFORMATION TECHNOLOGY AND OTHER SYSTEMS AND PLATFORMS, AND ANY FAILURES, ERRORS, DEFECTS OR DISRUPTIONS IN SUCH SYSTEMS OR PLATFORMS COULD DIMINISH OUR BRAND AND REPUTATION, SUBJECT US TO LIABILITY, DISRUPT ITS BUSINESS, AFFECT ITS ABILITY TO SCALE ITS TECHNICAL INFRASTRUCTURE AND ADVERSELY AFFECT ITS OPERATING RESULTS AND GROWTH PROSPECTS. OUR ONLINE GAMING OFFERINGS, SOFTWARE APPLICATIONS AND SYSTEMS, AND THE THIRD-PARTY PLATFORMS UPON WHICH THEY ARE MADE AVAILABLE COULD CONTAIN UNDETECTED ERRORS. Our technology infrastructure is provided by third party providers critical to the performance of our platform and offerings. For example, our back-end platform and all of our apps, which are critical to the Company’s performance, are provided by independent third-party providers. Third party providers’ systems may not be adequately designed with the necessary reliability and redundancy to avoid performance delays or outages that could be detrimental to our business.

The third parties upon which we rely provide resources for network and data security to protect our systems and data. We cannot assure with certainty that the measures we and such third parties take to prevent or reduce the likelihood of cyber-attacks, protect their systems, data, and user information, prevent outages, prevent data or information loss and fraud, and to prevent or detect security breaches, will provide absolute security. We may experience future website disruptions, outages and other performance problems resulting from various factors, including internet and application connection issues, infrastructure failure and changes, human or software errors and capacity constraints. Such disruptions from unauthorized access to, fraudulent manipulation of, or tampering with our computer systems and technological infrastructure, or those of third parties, could result in a wide range of negative outcomes, each of which could materially adversely affect our business, financial condition, results of operations and business prospects.

| 17 |

| Table of Contents |

Some of our third-party platforms and systems are not fully redundant, and disaster recovery planning may not be sufficient for all eventualities. Our third-party service provider’s disaster recovery systems do not offer full offsite failover recovery, which could result in our operations and offerings being offline for a period of time to sufficiently recover any impacted third-party infrastructure and recover the latest available data, as well as any time required to receive the required regulatory approvals.

Additionally, our offerings may contain errors, bugs, flaws or corrupted data, and these defects may only become apparent after their launch. If a particular offering is unavailable when users attempt to access it, or navigation through our platforms is slower than they expect, users may be unable to place their gaming or sports betting wagers in time and may be less likely to return to our platform as frequently, if at all. Furthermore, programming errors, defects and data corruption could disrupt our operations, adversely affect the experience of our users, harm our brand perception, cause our users to stop utilizing its platforms, divert our resources and delay market acceptance of its offerings, any of which could result in legal liability to us or harm its business, financial condition, results of operations and business prospects.

WE RELY ON AGREEMENTS WITH ALL OF OUR SOFTWARE PROVIDERS. All of our software provider agreements for the development of our platform and apps grant us a license to use the platform and apps during the term of the respective agreement. These agreements call for a payment to the provider either a fixed monthly fee or a royalty type payment based on our revenues. In addition, the agreements can be terminated by either party with written notice after a period of time, usually a year. If for any reason, an agreement is terminated, including a monetary default, we may be unable to provide a substitute software provider in a timely manner to replace the outgoing platform or app. In addition, if we are required to enter into a new agreement with a replacement vendor, we may be required to invest a significant amount of additional capital to fully develop that application. These events could have a material adverse impact on our business and operations.

Risks Relating to Compliance with Gaming and Other Regulations

OUR BUSINESS IS SUBJECT TO A VARIETY OF U.S. LAWS, MANY OF WHICH ARE UNSETTLED AND STILL DEVELOPING, AND WHICH COULD SUBJECT IT TO CLAIMS OR OTHERWISE HARM ITS BUSINESS. ANY CHANGE IN EXISTING REGULATIONS OR THEIR INTERPRETATION, OR THE REGULATORY CLIMATE APPLICABLE TO OUR PRODUCTS AND SERVICES, OR CHANGES IN TAX RULES AND REGULATIONS OR INTERPRETATION THEREOF RELATED TO ITS PRODUCTS AND SERVICES, COULD ADVERSELY IMPACT ITS ABILITY TO OPERATE ITS BUSINESS AS CURRENTLY CONDUCTED OR AS IT SEEKS TO OPERATE IN THE FUTURE, WHICH COULD HAVE A MATERIAL ADVERSE EFFECT ON ITS FINANCIAL CONDITION AND RESULTS OF OPERATIONS. We are generally subject to laws and regulations relating to gaming and online sports betting in the jurisdictions in which we conduct our business, as well as the general laws and regulations that apply to all e-commerce businesses, such as those related to privacy and personal information, tax, and consumer protection. These laws and regulations vary by jurisdiction and future legislative and regulatory action, court decisions or other governmental action, which may be affected by, among other things, political pressures, attitudes, and climates, as well as personal biases, may have a material impact on our operations and financial results. Some jurisdictions have introduced regulations attempting to restrict or prohibit online gaming, while others have taken the position that online gaming should be licensed and regulated and have adopted or are in the process of considering legislation and regulations to enable that to happen. The regulatory environment in any jurisdiction may change in the future and any such change could have a material adverse effect on our results of operations. For example, in 2018, the U.S. Department of Justice (“DOJ”), reversed its previously issued opinion published in 2011, which stated that interstate transmissions of wire communications that do not relate to a “sporting event or contest” fall outside the purview of the Wire Act of 1961 (“Wire Act”). The DOJ’s updated opinion concluded instead that the Wire Act was not uniformly limited to gaming relating to sporting events or contests and that certain of its provisions apply to non-sports-related wagering activity. In June 2019, a federal district court in New Hampshire ruled that the DOJ’s new interpretation of the Wire Act was erroneous and vacated the DOJ’s new opinion. The DOJ appealed the decision of the district court to the U.S. Court of Appeals for the First Circuit, which reaffirmed the district court’s decision on January 20, 2021. If such a ruling were to be appealed to the U.S. Supreme Court, an adverse ruling or other disposition of the case by the U.S. Supreme Court could impact our ability to engage in online internet gaming in the future.

| 18 |

| Table of Contents |

Future legislative and regulatory action, and court decisions, or other governmental action may have a material impact on our operations and financial results. Governmental authorities could view us as having violated local laws and us as violating local laws despite our efforts to obtain all applicable licenses or approvals. There is also the risk that civil and criminal proceedings, including class actions brought by or on behalf of prosecutors public entities or incumbent monopoly providers, or private individuals, could be initiated against

OUR GROWTH PROSPECTS DEPEND ON THE LEGAL STATUS OF REAL-MONEY GAMING IN VARIOUS JURISDICTIONS, AND LEGALIZATION MAY NOT OCCUR IN AS MANY STATES AS WE EXPECT OR MAY OCCUR AT A SLOWER PACE THAN WE ANTICIPATE. ADDITIONALLY, EVEN IF JURISDICTIONS LEGALIZE REAL MONEY GAMING, THIS MAY BE ACCOMPANIED BY LEGISLATIVE OR REGULATORY RESTRICTIONS AND/OR TAXES THAT MAKE IT IMPRACTICABLE OR LESS ATTRACTIVE TO OPERATE IN THOSE JURISDICTIONS OR THE PROCESS OF IMPLEMENTING REGULATIONS OR SECURING THE NECESSARY LICENSES TO OPERATE IN A PARTICULAR JURISDICTION MAY TAKE LONGER THAN WE ANTICIPATES, WHICH COULD ADVERSELY AFFECT ITS FUTURE RESULTS OF OPERATIONS AND MAKE IT MORE DIFFICULT TO MEET ITS EXPECTATIONS FOR FINANCIAL PERFORMANCE. Several states have legalized or are currently evaluating the legalization of real money gaming, and our business, financial condition, results of operations, and business prospects are significantly dependent upon the legalization status in these states. Our business plan is partially based upon the legalization of real money gaming in additional states and the legalization may not occur as anticipated. Additionally, if a large number of additional states or the federal government enact real money gaming legislation and we are unable to obtain, or are otherwise delayed in obtaining, the necessary licenses to operate online sports betting in U.S. jurisdictions where such games are legalized, our future growth in online sports betting could be materially impaired.

As we enter new jurisdictions, states or the federal government may legalize real money gaming in an unfavorable manner. As a result, we may encounter legal, regulatory, and political challenges that are difficult or impossible to foresee and could result in an unforeseen adverse impact on planned revenues or costs associated with the new opportunity. For example, certain states require us to have a relationship with a land-based, licensed casino for online sports betting access, which tends to increase our costs. States that have established state-run monopolies may limit opportunities for private sector participants like us. States also impose substantial tax rates on online sports betting revenue, in addition to a federal excise tax of 25 basis points on the amount of each sports wager. Tax rates, whether federal- or state-based, that are higher than we expect will make it more costly and less desirable for us to launch in a given jurisdiction, while tax increases in any of its existing jurisdictions may adversely impact our profitability.

Therefore, even in cases in which a jurisdiction purports to license and regulate sports betting, the licensing and regulatory regimes can vary considerably in terms of their business-friendliness and, at times, may be intended to provide incumbent operators with advantages over new licensees. Therefore, some “liberalized” regulatory regimes are considerably more economically viable than others.

FAILURE TO COMPLY WITH REGULATORY REQUIREMENTS IN A PARTICULAR JURISDICTION, OR THE FAILURE TO SUCCESSFULLY OBTAIN A LICENSE OR PERMIT APPLIED FOR IN A PARTICULAR JURISDICTION, COULD IMPACT OUR ABILITY TO COMPLY WITH LICENSING AND REGULATORY REQUIREMENTS IN OTHER JURISDICTIONS, OR COULD CAUSE THE REJECTION OF LICENSE APPLICATIONS OR CANCELATION OF EXISTING LICENSES IN OTHER JURISDICTIONS, OR COULD CAUSE FINANCIAL INSTITUTIONS, ONLINE AND MOBILE PLATFORMS, AND DISTRIBUTORS TO STOP PROVIDING SERVICES TO US, WHICH WE RELY UPON TO RECEIVE PAYMENTS FROM, OR DISTRIBUTE AMOUNTS TO, ITS USERS, OR OTHERWISE TO DELIVER AND PROMOTE ITS SERVICES. Compliance with the various regulations applicable to real-money gaming is costly and time-consuming. Regulatory authorities at the U.S. federal, state and local levels have broad powers with respect to the regulation of real money gaming operations and may revoke, suspend, condition, or limit our real money gaming licenses, impose substantial fines, or take other actions, any one of which may have a material adverse effect on our business, financial condition, results of operations and business prospects. These laws and regulations are dynamic and subject to potentially differing interpretations, and various legislative and regulatory bodies may expand current laws or regulations or enact new laws and regulations regarding these matters. We will strive to comply with all applicable laws and regulations relating to our business. It is possible, however, that these requirements may be interpreted and applied in a manner inconsistent from one jurisdiction to another and may conflict with other rules. Non-compliance with any such law or regulations could expose us to claims, proceedings, litigation and investigations by private parties and regulatory authorities, as well as substantial fines and negative publicity, each of which may materially and adversely affect our business.

| 19 |

| Table of Contents |

Any real money gaming license could be revoked, suspended or conditioned at any time. The loss of a license in one jurisdiction could trigger the loss of a license or affect our eligibility for such a license in another jurisdiction, and any of such losses, or potential for such loss, could cause us to cease offering some or all of its offerings in the impacted jurisdictions. We may be unable to obtain or maintain all necessary registrations, licenses, permits, or approvals, and we could incur fines or experience delays related to the licensing process, which could adversely affect its operations. Our delay or failure to obtain or maintain licenses in any jurisdiction may prevent it from distributing its offerings, increasing its customer base and/or generating revenues. We cannot guarantee that it will be able to obtain and maintain the licenses and related approvals necessary to conduct its iGaming and online sports betting operations. Any failure to maintain or renew Our existing licenses, registrations, permits or approvals could have a material adverse effect on its business, financial condition, results of operations and business prospects.

OUR GROWTH PROSPECTS AND MARKET POTENTIAL WILL DEPEND ON ITS ABILITY TO OBTAIN LICENSES TO OPERATE IN JURISDICTIONS, AND IF WE FAIL TO OBTAIN SUCH LICENSES, ITS BUSINESS, FINANCIAL CONDITION, RESULTS OF OPERATIONS, AND BUSINESS PROSPECTS COULD BE IMPAIRED. Our ability to grow its business will depend on its ability to obtain and maintain licenses to offer its product offerings in many jurisdictions or heavily populated jurisdictions. If we fail to obtain and maintain licenses in large jurisdictions or a greater number of mid-market jurisdictions, this may prevent us from expanding the footprint of its product offerings, increasing its user base and/or generating revenues. We cannot be certain that it will be able to obtain and maintain licenses and related approvals necessary to conduct its online sports betting operations. Any failure to obtain and maintain licenses, registrations, permits or approvals could have a material adverse effect on its business, financial condition, results of operations and business prospects.

IN SOME JURISDICTIONS, OUR KEY EXECUTIVES, CERTAIN EMPLOYEES, OR OTHER INDIVIDUALS RELATED TO THE BUSINESS ARE SUBJECT TO LICENSING OR COMPLIANCE REQUIREMENTS. FAILURE BY SUCH INDIVIDUALS TO OBTAIN THE NECESSARY LICENSES OR COMPLY WITH INDIVIDUAL REGULATORY OBLIGATIONS COULD CAUSE THE BUSINESS TO BE NON-COMPLIANT WITH ITS OBLIGATIONS OR IMPERIL ITS ABILITY TO OBTAIN OR MAINTAIN LICENSES NECESSARY FOR THE CONDUCT OF THE BUSINESS. IN SOME CASES, THE REMEDY TO SUCH SITUATION MAY REQUIRE THE REMOVAL OF A KEY EXECUTIVE OR EMPLOYEE AND THE MANDATORY REDEMPTION OR TRANSFER OF SUCH PERSON’S EQUITY SECURITIES. As part of obtaining real money gaming licenses, the responsible Gaming Authority will generally determine the suitability of certain directors, officers, and employees and, in some instances, significant stockholders. The criteria used by Gaming Authorities to determine who requires a finding of suitability or the suitability of an applicant to conduct gaming operations varies among jurisdictions but generally requires extensive and detailed application disclosures followed by a thorough investigation. Gaming Authorities typically have broad discretion in determining whether an applicant should be found suitable to conduct operations within a given jurisdiction. If any Gaming Authority with jurisdiction over our business were to find an applicable officer, director, employee, or significant stockholder is deemed by competent authorities to be unsuitable for licensing or unsuitable to continue having a relationship with us, we would be required to sever its relationship with that person. Furthermore, such Gaming Authorities may require us to terminate the employment of any person who refuses to file required applications. Either result could have a material adverse effect on our business, operations, and prospects.

| 20 |

| Table of Contents |

Risks Related To Our Securities

WE WILL NEED TO RAISE ADDITIONAL CAPITAL. IF WE ARE UNABLE TO RAISE ADDITIONAL CAPITAL, OUR BUSINESS MAY FAIL. As stated elsewhere herein, we will need to raise additional capital to fund our ongoing operations. We have limited cash on hand and working capital. To secure additional financing, we may need to borrow money or sell more securities. Under the current circumstances, we may be unable to secure additional financing on favorable terms, if available at all.

OUR NEED FOR CAPITAL WILL CREATE ADDITIONAL RISKS AND CREATE POTENTIAL SUBSTANTIAL DILUTION TO EXISTING SHAREHOLDERS. Our capital expenditures are intended to be funded from third-party sources and affiliates if available, including the incurrence of debt (which may be converted into common stock) and/or the sale of additional equity securities. As of December 31, 2024, the Company is indebted to certain affiliates in the amount of $4,210,127. This debt is due on demand and the Company has no means to repay its existing debt. To the extent that this debt is converted to common stock, the conversion of this debt will cause additional dilution to existing shareholders, which may be substantial. In addition, the sale of additional equity securities or the sale and conversion of other debt will likewise be dilutive to the interests of current equity holders, and such dilution may be substantial. In addition, there can be no assurance that such additional financing, whether debt or equity, will be available to the Company or that it will be available on acceptable commercial terms. Any inability to secure such additional financing on appropriate terms could have a materially adverse impact on the business, financial condition, and operating results of the Company.

THE REGULATION OF PENNY STOCKS BY THE SEC AND FINRA MAY HAVE AN EFFECT ON THE TRADABILITY OF OUR SECURITIES. Our shares are subject to a Securities and Exchange Commission rule that imposes special sales practice requirements upon broker-dealers who sell such securities to persons other than established customers or accredited investors. For purposes of the rule, the phrase “accredited investors” means, in general terms, institutions with assets in excess of $5,000,000, or individuals having a net worth in excess of $1,000,000 or having an annual income that exceeds $200,000 (or that, when combined with a spouse’s income, exceeds $300,000).

For transactions covered by the rule, the broker-dealer must make a special suitability determination for the purchaser and receive the purchaser’s written agreement to the transaction before the sale. Consequently, the rule may affect the ability of broker-dealers to sell our securities and also may affect the ability of purchasers in this offering to sell their securities in any market that might, therefore, develop.

In addition, the Securities and Exchange Commission has adopted a number of rules to regulate “penny stocks.” Such rules include Rules 3a51-1, 15g-1, 15g-2, 15g-3, 15g-4, 15g-5, 15g-6, 15g-7, and 15g-9 under the Securities Exchange Act of 1934, as amended. Because our securities constitute “penny stocks” within the meaning of the rules, the rules would apply to us and to our securities. The rules may further affect the ability of owners of Shares to sell our securities in any market that might develop for them.

Shareholders should be aware that, according to the Securities and Exchange Commission, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include (i) control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer; (ii) manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; (iii) “boiler room” practices involving high-pressure sales tactics and unrealistic price projections by inexperienced sales persons; (iv) excessive and undisclosed bid-ask differentials and markups by selling broker-dealers; and (v) the wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired consequent investor losses. Our management is aware of the abuses historically in the penny stock market. Although we do not expect to be able to dictate the behavior of the market or of broker-dealers who participate in the market, management will strive within the confines of practical limitations to prevent the described patterns from being established with respect to our securities.

The shares of our common stock may be thinly traded on OTC-Pink, meaning that the number of persons interested in purchasing our shares of common stock at or near ask prices at any given time may be relatively small or non-existent. This situation is attributable to a number of factors, including the fact that we are a small company which is relatively unknown to stock analysts, stock brokers, institutional investors and others in the investment community that generate or influence sales volume, and that even if we came to the attention of such persons, they tend to be risk-averse and would be reluctant to follow an unproven, early stage company such as ours or purchase or recommend the purchase of our shares of common stock until such time as we became more seasoned and viable. As a consequence, there may be periods of several days or more when trading activity in our shares of common stock is minimal or non-existent, as compared to a seasoned issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on Securities price.

| 21 |

| Table of Contents |

OUR STOCK WILL, IN ALL LIKELIHOOD, BE THINLY TRADED, AND AS A RESULT, YOU MAY BE UNABLE TO SELL AT OR NEAR ASK PRICES OR AT ALL IF YOU NEED TO LIQUIDATE YOUR SHARES. To date, the public market for our Common Stock has been limited. We cannot predict that a broader or more active public trading market for our shares of Common Stock will develop or be sustained or that any trading levels will be sustained. Due to these conditions, we; cannot assure investors that they will be able to sell their shares of Common Stock at or near ask prices or at all.