chuc20221231_10k.htm

0001134765

false

0001134765

false

--12-31

2022

FY

26

2018 2019 2020 2021 2022

2019 2020 2021 2022

2

1

4

2

5

1

00011347652022-01-012022-12-31

thunderdome:item

iso4217:USD

0001134765us-gaap:SubsequentEventMember2023-03-29

0001134765us-gaap:SubsequentEventMember2023-03-28

0001134765chuc:AustinPurchaserMemberus-gaap:SubsequentEventMemberchuc:ReceivablesFinancingAgreementMember2023-01-192023-01-19

xbrli:pure

0001134765chuc:AustinPurchaserMemberus-gaap:SubsequentEventMemberchuc:ReceivablesFinancingAgreementMember2023-01-19

0001134765us-gaap:StateAndLocalJurisdictionMember2022-01-012022-12-31

0001134765us-gaap:DomesticCountryMember2022-01-012022-12-31

00011347652021-12-31

00011347652022-12-31

00011347652021-01-012021-12-31

00011347652020-12-31

0001134765us-gaap:DomesticCountryMemberus-gaap:ResearchMember2022-12-31

0001134765us-gaap:StateAndLocalJurisdictionMember2022-12-31

0001134765us-gaap:DomesticCountryMember2022-12-31

utr:Y

0001134765chuc:CorporateHeadquartersLeaseMember2022-12-31

0001134765chuc:LeaseAt5331ProductionDriveHuntingtonBeachCaMembersrt:RestatementAdjustmentMember2022-01-012022-06-30

0001134765chuc:LeaseAt5331ProductionDriveHuntingtonBeachCaMembersrt:RestatementAdjustmentMember2022-06-30

0001134765chuc:CorporateHeadquartersLeaseMember2021-01-012021-12-31

0001134765chuc:CorporateHeadquartersLeaseMember2022-01-012022-12-31

0001134765chuc:CorporateHeadquartersLeaseMember2019-11-012019-11-01

0001134765chuc:WilliamsvilleLeaseMember2022-05-012022-05-01

0001134765us-gaap:RestrictedStockMemberchuc:The2019OmnibusIncentivePlanMember2021-01-012021-12-31

0001134765us-gaap:RestrictedStockMemberchuc:The2019OmnibusIncentivePlanMember2022-01-012022-12-31

0001134765chuc:The2019OmnibusIncentivePlanMember2022-01-012022-12-31

0001134765us-gaap:RestrictedStockMemberchuc:The2019OmnibusIncentivePlanMember2022-12-31

0001134765us-gaap:RestrictedStockMemberchuc:The2019OmnibusIncentivePlanMembersrt:DirectorMember2021-11-012021-11-01

xbrli:shares

0001134765chuc:The2019OmnibusIncentivePlanMembersrt:DirectorMember2021-11-012021-11-01

0001134765us-gaap:RestrictedStockMember2021-04-012021-04-01

00011347652021-04-012021-04-01

0001134765us-gaap:CommonStockMember2018-12-312018-12-31

iso4217:USDxbrli:shares

0001134765us-gaap:RestrictedStockMember2022-12-31

0001134765us-gaap:RestrictedStockMember2022-01-012022-12-31

0001134765us-gaap:RestrictedStockMember2021-12-31

0001134765us-gaap:RestrictedStockMember2021-01-012021-12-31

0001134765us-gaap:RestrictedStockMember2020-12-31

0001134765us-gaap:CommonStockMember2021-01-012021-12-31

00011347652018-12-31

0001134765us-gaap:SeriesBPreferredStockMember2018-12-31

0001134765chuc:ConversionOfMembershipUnitsIntoSeriesBConvertiblePreferredStockMember2018-12-312018-12-31

0001134765chuc:ConversionOfMembershipUnitsIntoCommonStockMember2019-04-262019-04-26

0001134765us-gaap:EmployeeStockOptionMemberchuc:The2019OmnibusIncentivePlanMember2021-01-012021-12-31

0001134765us-gaap:EmployeeStockOptionMemberchuc:The2019OmnibusIncentivePlanMember2022-01-012022-12-31

0001134765chuc:The2019OmnibusIncentivePlanMember2022-12-31

0001134765us-gaap:EmployeeStockOptionMember2021-01-012021-12-31

0001134765us-gaap:EmployeeStockOptionMember2021-12-31

0001134765chuc:The2019OmnibusIncentivePlanMember2021-01-012021-12-31

00011347652020-01-012020-12-31

0001134765chuc:The2019OmnibusIncentivePlanMember2021-12-22

0001134765chuc:The2019OmnibusIncentivePlanMember2019-05-08

0001134765chuc:The2019OmnibusIncentivePlanMember2021-12-222021-12-22

00011347652021-03-222021-03-22

00011347652021-03-22

0001134765us-gaap:PrivatePlacementMember2021-03-222021-03-22

0001134765chuc:ConversionOfSeriesAPreferredStockToCommonStockMember2021-01-012021-12-31

0001134765chuc:ConversionOfSeriesAPreferredStockToCommonStockMember2022-01-012022-12-31

0001134765us-gaap:DividendPaidMemberus-gaap:SeriesAPreferredStockMember2021-01-012021-12-31

0001134765us-gaap:SeriesAPreferredStockMember2021-05-252021-05-25

00011347652021-05-25

00011347652021-05-252021-05-25

0001134765us-gaap:SeriesAPreferredStockMember2021-05-25

0001134765us-gaap:SeriesAPreferredStockMember2020-04-252020-04-25

0001134765us-gaap:WarrantMember2021-01-012021-12-31

0001134765us-gaap:WarrantMember2022-01-012022-12-31

0001134765us-gaap:EmployeeStockOptionMember2021-01-012021-12-31

0001134765us-gaap:EmployeeStockOptionMember2022-01-012022-12-31

00011347652021-01-012021-12-30

0001134765chuc:EIDLoanMemberchuc:DonPollyMember2020-06-24

0001134765chuc:EIDLoanMemberchuc:DonPollyMember2020-06-242020-06-24

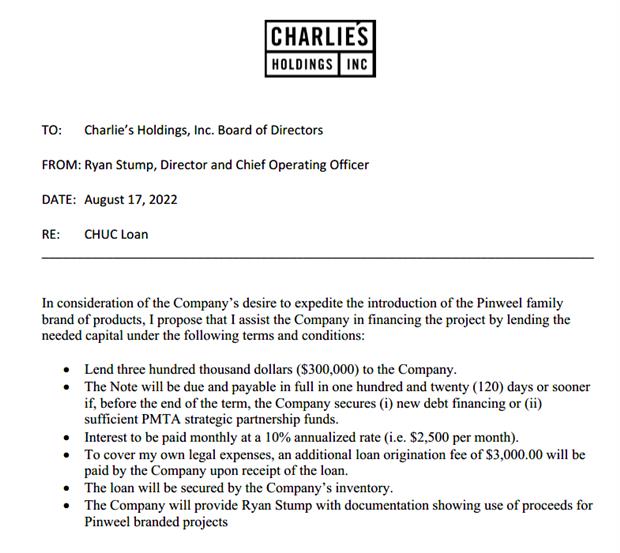

0001134765chuc:TheLoanMember2022-08-17

0001134765chuc:TheLoanMember2022-08-172022-08-17

0001134765chuc:MichaelKingMemberus-gaap:NotesPayableOtherPayablesMemberus-gaap:SubsequentEventMember2023-03-282023-03-28

0001134765chuc:MichaelKingMemberus-gaap:NotesPayableOtherPayablesMember2022-04-06

0001134765chuc:DonPollyLlcMember2022-01-012022-12-31

0001134765us-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMemberchuc:CustomerAMember2021-01-012021-12-31

0001134765chuc:CustomerAMember2021-12-31

0001134765us-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMemberchuc:CustomerBMember2022-01-012022-12-31

0001134765chuc:CustomerBMember2022-12-31

0001134765us-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMemberchuc:CustomerAMember2022-01-012022-12-31

0001134765chuc:CustomerAMember2022-12-31

0001134765us-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMemberchuc:TwoCustomersMember2022-01-012022-12-31

0001134765us-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMember2022-01-012022-12-31

0001134765us-gaap:AccountsReceivableMemberus-gaap:CustomerConcentrationRiskMemberchuc:CustomerBMember2021-01-012021-12-31

0001134765chuc:FourVendorsMember2021-12-31

0001134765chuc:FourVendorsMember2022-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMemberchuc:TwoVendorsMember2021-01-012021-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMember2021-01-012021-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMemberchuc:TwoVendorsMember2022-01-012022-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMember2022-01-012022-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMemberchuc:VendorBMember2021-01-012021-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMemberchuc:VendorBMember2022-01-012022-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMemberchuc:VendorAMember2021-01-012021-12-31

0001134765chuc:InventoryPurchasesMemberus-gaap:SupplierConcentrationRiskMemberchuc:VendorAMember2022-01-012022-12-31

0001134765us-gaap:LeaseholdImprovementsMember2022-01-012022-12-31

0001134765us-gaap:LeaseholdImprovementsMember2021-12-31

0001134765us-gaap:LeaseholdImprovementsMember2022-12-31

0001134765us-gaap:OfficeEquipmentMember2022-01-012022-12-31

0001134765us-gaap:OfficeEquipmentMember2021-12-31

0001134765us-gaap:OfficeEquipmentMember2022-12-31

0001134765chuc:TradeShowBoothMember2022-01-012022-12-31

0001134765chuc:TradeShowBoothMember2021-12-31

0001134765chuc:TradeShowBoothMember2022-12-31

0001134765us-gaap:MachineryAndEquipmentMember2022-01-012022-12-31

0001134765us-gaap:MachineryAndEquipmentMember2021-12-31

0001134765us-gaap:MachineryAndEquipmentMember2022-12-31

00011347652019-04-26

0001134765chuc:PlacementAgentWarrantsMember2019-04-26

0001134765chuc:InvestorWarrantsMember2019-04-26

00011347652019-04-262019-04-26

0001134765us-gaap:MeasurementInputExpectedDividendRateMember2021-12-31

0001134765us-gaap:MeasurementInputExpectedDividendRateMember2022-12-31

0001134765us-gaap:MeasurementInputRiskFreeInterestRateMember2021-12-31

0001134765us-gaap:MeasurementInputRiskFreeInterestRateMember2022-12-31

0001134765us-gaap:MeasurementInputPriceVolatilityMember2021-12-31

0001134765us-gaap:MeasurementInputPriceVolatilityMember2022-12-31

0001134765us-gaap:MeasurementInputExpectedTermMember2021-12-31

0001134765us-gaap:MeasurementInputExpectedTermMember2022-12-31

0001134765us-gaap:MeasurementInputExercisePriceMember2021-12-31

0001134765us-gaap:MeasurementInputExercisePriceMember2022-12-31

0001134765us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-31

0001134765us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-31

0001134765us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-31

0001134765us-gaap:FairValueMeasurementsRecurringMember2021-12-31

0001134765us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-31

0001134765us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-31

0001134765us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-31

0001134765us-gaap:FairValueMeasurementsRecurringMember2022-12-31

0001134765chuc:DistributionMember2021-01-012021-12-31

0001134765chuc:DistributionMember2022-01-012022-12-31

0001134765chuc:RetailerMember2021-01-012021-12-31

0001134765chuc:RetailerMember2022-01-012022-12-31

0001134765country:US2021-01-012021-12-31

0001134765country:US2022-01-012022-12-31

0001134765us-gaap:NonUsMember2021-01-012021-12-31

0001134765us-gaap:NonUsMember2022-01-012022-12-31

0001134765chuc:CharliesChalkDustLlcAndBaziIncMember2022-12-31

0001134765chuc:ReverseStockSplitMember2021-06-162021-06-16

0001134765us-gaap:SeriesBPreferredStockMember2021-06-16

0001134765us-gaap:RetainedEarningsMember2022-12-31

0001134765us-gaap:AdditionalPaidInCapitalMember2022-12-31

0001134765us-gaap:CommonStockMember2022-12-31

0001134765us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2022-12-31

0001134765us-gaap:RetainedEarningsMember2022-01-012022-12-31

0001134765us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-31

0001134765us-gaap:CommonStockMember2022-01-012022-12-31

0001134765us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2022-01-012022-12-31

0001134765us-gaap:RetainedEarningsMember2021-12-31

0001134765us-gaap:AdditionalPaidInCapitalMember2021-12-31

0001134765us-gaap:CommonStockMember2021-12-31

0001134765us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2021-12-31

0001134765us-gaap:RetainedEarningsMember2021-01-012021-12-31

0001134765us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-31

0001134765us-gaap:CommonStockMember2021-01-012021-12-31

0001134765us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2021-01-012021-12-31

0001134765us-gaap:RetainedEarningsMember2020-12-31

0001134765us-gaap:AdditionalPaidInCapitalMember2020-12-31

0001134765us-gaap:CommonStockMember2020-12-31

0001134765us-gaap:SeriesAPreferredStockMemberus-gaap:PreferredStockMember2020-12-31

0001134765us-gaap:SeriesBPreferredStockMember2021-12-31

0001134765us-gaap:SeriesBPreferredStockMember2022-12-31

0001134765us-gaap:SeriesAPreferredStockMember2021-12-31

0001134765us-gaap:SeriesAPreferredStockMember2022-12-31

00011347652023-04-17

00011347652022-06-30

0001134765chuc:InventoryPurchasesMember2022-01-012022-12-31

0001134765us-gaap:AccountsReceivableMember2022-01-012022-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| ☒ |

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended December 31, 2022

|

|

or

|

|

☐

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission file No. 001-32420

CHARLIE’S HOLDINGS, INC.

(Exact Name of Registrant as Specified in Its Charter)

|

Nevada

|

|

84-1575085

|

|

(State or Other Jurisdiction of Incorporation or Organization)

|

|

(IRS Employer Identification No.) |

1007 Brioso Drive, Costa Mesa, CA 92627

(Address of Principal Executive Offices)

(949) 531-6855

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered under Section 12(g) of the Exchange Act:

|

Title of Each Class

|

|

Trading Symbol

|

|

Name of Each Exchange on Which Registered

|

|

Common Stock ($0.001 par value)

|

|

CHUC

|

|

OTC Markets

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

☐

|

Accelerated filer

|

☐

|

|

Non-accelerated filer

|

☒

|

Smaller reporting company

|

☒

|

| |

|

Emerging growth company

|

☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter, June 30, 2022 was approximately $8 based on a closing market price of $0.0832 per share, as reported on the OTCQB Venture Market.

There were 224,112,168 shares of the registrant’s common stock outstanding as of April 17, 2023.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2023 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K. Such Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of December 31, 2022.

CHARLIE’S HOLDINGS, INC.

ANNUAL REPORT ON FORM 10-K

YEAR ENDED DECEMBER 31, 2022

TABLE OF CONTENTS

| |

|

Page

|

|

PART I

|

|

|

|

Item 1.

|

Description of Business

|

2

|

|

Item 1A.

|

Risk Factors

|

15

|

|

Item 1B.

|

Unresolved Staff Comments

|

27

|

|

Item 2.

|

Properties

|

27

|

|

Item 3.

|

Legal Proceedings

|

27

|

|

Item 4.

|

Mine Safety Disclosures

|

27

|

| |

|

|

|

PART II

|

|

|

|

Item 5.

|

Market for Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

28

|

|

Item 6.

|

Selected Financial Data

|

28

|

|

Item 7.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

29

|

|

Item 7A.

|

Quantitative and Qualitative Disclosures About Market Risk

|

38

|

|

Item 8.

|

Financial Statements and Supplementary Data

|

38

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

|

38

|

|

Item 9A.

|

Controls and Procedures

|

38

|

|

Item 9B.

|

Other Information

|

39

|

| Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspection |

39 |

| |

|

|

|

PART III

|

|

|

|

Item 10.

|

Directors, Executive Officers and Corporate Governance

|

39

|

|

Item 11.

|

Executive Compensation

|

42

|

|

Item 12.

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

42

|

|

Item 13.

|

Certain Relationships, Related Transactions, and Director Independence

|

42

|

|

Item 14.

|

Principal Accountant Fees and Services

|

42

|

| |

|

|

|

PART IV

|

|

|

|

Item 15.

|

Exhibits, Financial Statement Schedules

|

43

|

|

Item 16.

|

10-K Summary

|

43

|

| |

|

|

|

Signatures

|

|

44

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains “forward-looking” statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and is subject to the safe harbor created by those sections. We intend to identify forward-looking statements in this report by using words such as “believes”, “intends”, “expects”, “may”, “will”, “should”, “plan”, “projected”, “contemplates”, “anticipates”, “estimates” “predicts”, “potential”, “continue” or similar terminology. These statements are based on our beliefs as well as assumptions we made using information currently available to us. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Because these statements reflect our current views concerning future events, these statements involve risks, uncertainties, and assumptions. Actual future results may differ significantly from the results discussed in the forward-looking statements. These risks include changes in production and demand for our products, changes in the level of operating expense, our ability to expand our network of customers, changes in general economic conditions that impact consumer behavior and spending, product supply, the availability, amount, and cost of capital to us and our use of such capital, and other risks discussed in this report. Additional risks that may affect our performance are discussed below under the section entitled “Risk Factors”.

PART I

ITEM 1. DESCRIPTION OF BUSINESS

As used in this Annual Report, unless otherwise stated or the context otherwise requires, references to the “Company”, “we”, “us”, “our” or similar references mean Charlie’s Holdings, Inc. (formerly True Drinks Holdings, Inc.), its subsidiaries and consolidated variable interest entity on a consolidated basis. References to “Charlie’s” and “CCD” refer to Charlie’s Chalk Dust, LLC, a California limited liability company and wholly-owned subsidiary of the Company, and “Don Polly” refers to Don Polly, LLC, a Nevada limited liability company that is owned by entities controlled by Brandon Stump and Ryan Stump, the Company’s former Chief Executive Officer and current Chief Operating Officer, respectively, and a consolidated variable interest for which the Company is the primary beneficiary.

On April 26, 2019, the Company (then known as True Drinks Holdings, Inc.), entered into a Securities Exchange Agreement with each of the members of Charlie’s on that date (the “Charlie’s Members”), pursuant to which the Company acquired all outstanding membership interests beneficially owned by the Charlie’s Members in exchange for certain units consisting of the Company’s securities (the “Share Exchange”). As a result, Charlie’s became a wholly owned subsidiary of the Company. Following the consummation of the Share Exchange, the primary business operations of the Company consisted of those of Charlie’s and, more recently, Don Polly.

Overview

The Company’s objective is to become a leader in three broad product categories: (i) non-combustible nicotine-related products, (ii) alternative alkaloid vapor products, and (iii) hemp-derived vapor and edible products. Through our Charlie’s subsidiary, we formulate, market, and distribute premium, nicotine-based and alternative alkaloid vapor products. Charlie’s products are produced through contract manufacturers for sale through select distributors, specialty retailers, and third-party online resellers throughout the United States, as well as in more than 80 countries worldwide. Charlie’s primary international markets include the United Kingdom, Italy, Spain, New Zealand, Australia, and Canada. Through Don Polly, we develop, market and distribute products containing compounds derived from hemp.

Our Products

Charlie’s Product Line

Our business efforts consist primarily of formulating, marketing and distributing our portfolio of premium vapor products, which we collectively refer to as the “Charlie’s Product Line” or “Charlie’s Products”.

Disposables

Disposable vapes, also referred to as (“Disposables”), are pre-filled and pre-charged vapor delivery systems. These single-use electronic vaporizers offer a draw-activated mouthpiece and are infused with e-liquid, making them ready to use immediately after purchase. Our Disposables are available in a variety of sizes (2ml, 4ml, 8ml and 12ml) and flavors, including some of our award-winning proprietary blends.

Charlie’s disposable products are produced under two brand names distinguished by their size and intended market, and offer users a variety of premium flavors containing synthetic nicotine (not derived from tobacco), tobacco derived nicotine (2ml products), or alternative alkaloids in a compact, discrete format. All disposables are shipped in flavor-specific consumer display units (“CDU”) which hold ten individually packaged disposables for quick and convenient retail sales.

| |

●

|

Pachamama 2mL Disposable. Pachamama 2mL Disposables were specifically designed with the European Union’s (“EU”) Tobacco Products Directive (“TPD”) in mind and are currently sold only in the EU. All thirteen flavors have been registered in eight EU member states.

|

| |

●

|

Pacha 4mL Disposable. Pacha 4mL Disposables were designed for the US market with the objective of providing a convenient and satisfying user experience. Currently, we have eleven flavors available in the US market.

|

| |

●

|

Pacha 8mL Disposable. Pacha 8mL Disposables offer customers a moderately higher puff count and are available in ten flavors ranging from our innovative “Clear” (flavorless) offering, to novel fruit blends and distinctive dessert flavors.

|

| |

|

|

| |

●

|

Pacha 12mL Disposable. Pacha 12mL Disposables offer customers Charlie’s highest puff count, and are available in ten fruit and “Ice” varieties.

|

E-Liquids

E-liquids used to produce vapor in vaping devices are sold separately for use in refillable tanks of open system vaporizers. Liquids are available in variable nicotine concentrations (0 mg, 3 mg, and 6 mg per milliliter) to suit user preferences. Liquids are available in a variety of our proprietary-blended flavors. The liquid solution consists of flavoring and/or nicotine dissolved in one or several hygroscopic components, which turns the water in the solution into the smoke-like vapor when heated. The most commonly used hygroscopic components are propylene glycol (“PG”), vegetable glycerin (“VG”) or polyethylene glycol 400. VG imparts sweetness and produces vapor clouds, while PG produces more “throat hit,” which simulates the feeling of smoking. Our proprietary e-liquid brands are manufactured by ISO Class 7 certified manufacturers in the United States, which helps ensure their purity and quality.

Charlie’s e-liquid products are produced under five brand names distinguished by their flavor profiles, packaging art and ingredient transparency.

| |

●

|

Pacha (domestic) and Pachamama (international markets)™. A line launched in 2016 consisting of eight eclectic mixes of natural fruit flavors such as passion fruit raspberry yuzu, blood orange banana gooseberry, and huckleberry pear acai.

|

| |

●

|

Black Label and White Label. Charlie’s original black and white product line launched in 2015. Black Label is currently available in five flavors and White Label is currently available in four flavors for sale in international markets.

|

| |

●

|

Meringue. The third brand launched in 2016, based on creative character stories, currently includes three flavors.

|

| |

●

|

Campfire™. Outdoors and Smores flavor inspired by camp nostalgia.

|

Nicotine Salt Products

Nicotine salt e-liquids (“NIC salts”) are formulated for use in lower wattage open, semi-open and closed system vaporizers and are available in higher nicotine concentrations (25mg and 50mg per milliliter) than traditional e-liquids. Nicotine salts consist of nicotine dissolved in an acid that results in a lower PH level than other e-liquids. This form of nicotine has a higher bioavailability resulting in faster blood stream absorption and more closely mimics the effects of combustible tobacco products. We broadly released Pachamama™ Salts, an extension of the Pachamama™ line, in late December 2018 to a select group of key accounts, which now includes 17 flavors domestically and 31 internationally, packaged in 10ml, 30ml, and 60ml bottles. We will continue to evaluate our product offering in this category as demand continues to evolve.

Don Polly

Don Polly is a company under common ownership with the Company, and was established in April 2019 for the specific purpose of developing, marketing, and distributing proprietary and innovative hemp-derived, non-THC, products which we refer to the “Don Polly Products” and “Don Polly Product Line”. In June 2019, we introduced, through Don Polly, full-spectrum hemp extract and CBD isolate wellness products across a variety of formats and with different strengths. The Company’s current portfolio also includes products containing compounds that are derived from hemp, including Delta-8-Tetrahydrocannabinol (“Delta-8-THC”) and other novel cannabinoids , all of which are offered by way of a licensing agreement between Don Polly and Charlie’s, entered on April 25, 2019 (the “Licensing Agreement”). In the near term, we expect to continue expanding the hemp-derived products line to include products based on other innovative cannabinoids, currently in development.

Don Polly is owned by two limited liabilities companies, of which one is wholly-owned by Brandon Stump, the Company’s former Chief Executive Officer, and the other is wholly-owned by Ryan Stump, the Company’s Chief Operating Officer. Pursuant to the Licensing Agreement, Charlie’s granted Don Polly a limited right and license to use certain of Charlie’s trademarks, copyrights, and original artwork, in connection with Don Polly’s branded hemp products, as well as a Services Agreement pursuant to which Charlie’s provides certain services to Don Polly related to the sales, marketing, and brand development of Don Polly products.

Full Spectrum CBD Products

Our full spectrum hemp extract comes from whole plant extraction which retains the plant’s natural compounds. This extraction method ensures each product preserves the holistic benefits of the plant including minimal amounts of THC (0.3% or less), which allows for optimal absorption of the plant’s nutrients. While CBD alone is a beneficial cannabinoid, full spectrum products provide the body access to all the plant’s cannabinoids, allowing the end user to achieve a wide range of benefits. The full spectrum products are formulated with single-source and single strain hemp extracts. Don Polly believes this sourcing practice yields various compounds that work synergistically to heighten the effects of the products, making them superior to single-compound CBD isolates. In June 2019, we introduced the Pachamama™ tincture and topical full spectrum products. Currently, the tincture offering includes two flavors Black Pepper Turmeric and Kava Kava Valerian, which are available in 30ml bottle sizes and both 750mg and 1750mg strengths.

Broad Spectrum CBD Products

In addition to isolate and full spectrum CBD products, we believe broad spectrum hemp-derived CBD products can be developed to provide the same benefits of full spectrum CBD products. Through additional processing of hemp-derived extracts, we can eliminate the presence of THC. This category of THC-free, broad spectrum products will provide consumers with the same level of quality and the same nutrients we value in our full spectrum products, without the concern of consuming minimal amounts of THC. In Q4 of 2019, we released three very dynamic broad spectrum topicals; our Pain Cream 850mg, Icy Muscle Gel 500mg and Body Lotion 300mg. The Pain Cream, offered in a 100ml bottle, offers a combination of broad-spectrum CBD, menthol, MSM, arnica and capsaicin to provide quick, effective relief. The Icy Muscle Gel roll-on has a blend of ancient Chinese herbs along with cooling menthol and camphor to temporarily relieve nagging pains, and provide anti-inflammatory treatment to muscles and joints. Don Polly’s Body Lotion rounds out the initial broad spectrum topical portfolio offerings with 300mg of CBD and an ultra-nourishing blend of botanical oils for soft, radiant, and balanced skin. The Body Lotion is not currently offered. In March 2021 we launched Sleep Well Gummies, specifically formulated with a unique blend of cannabinol (“CBN”), CBD, melatonin, and Elderberry extract to support the immune system and to encourage better sleep. Sleep Well Gummies have grown to become the Company’s best-selling product in the broad-spectrum category.

Other Cannabinoids

Offered to adult consumers under the PINWEEL™ brand name, our Other Cannabinoid products are formulated from proprietary live resin blends of hemp-derived cannabinoids. Since our PINWEEL product line contains only cannabinoids made from 100% hemp extract, we are able to legally manufacture, distribute and sell to consumers in the United States. As a result of the Agriculture Improvement Act (the “Farm Bill”), ratified and signed into law in December 2018, cannabis containing less than 0.3% Delta 9-THC is legally classified as hemp and is thus legal under federal law. All Other Cannabinoid products are shipped in flavor specific CDUs which hold ten individually packaged disposables for quick and convenient retail sales.

| |

●

|

PINWEEL Disposable is a vaping device that is designed to be used until empty; then its is discarded. The device comes pre-charged, pre-filled, and provides the ultimate convenience, giving the user an effortless vaping experience that requires no knowledge of vapor products. It is as simple as taking a puff and enjoying the proprietary blend of hemp-derived cannabinoids with which the device is filled. While most disposable vaping devices come filled with vape juice, PINWEEL Disposables are filled with hemp-derived cannabinoids with an infusion of terpenes. The distillate blend provides the many benefits and effects the cannabinoid is known for, while the variety of terpenes act as diluents and also provide unique, award-winning flavor profiles.

|

| |

●

|

PINWEEL Carts are similar to disposables in the sense that they are designed to be used until they are empty and then discarded. PINWEEL carts work just like standard vape carts, which means the user can attach the cartridge to a standard 510-threaded battery and then use the device. A cart is made up of a cylindrical container that houses the distillate blend, a wick, an atomizer, and a mouthpiece. When the user attaches the cart to the battery, the battery delivers power to the atomizer to heat up the extract until it vaporizes for inhalation. PINWEEL carts are designed for the more advanced, regular user of hemp-derived cannabinoids who do not require a ready-to-use product right out of the box. By having the end user supply the battery for the cart we are able to market and sell PINWEEL Carts at a relatively low price point.

|

| |

●

|

PINWEEL Edibles are products that are infused with hemp derived cannabinoids and intended to be ingested by adult consumers. Edibles are a popular alternative to the traditional form of smoking or vaping a hemp product. PINWEEL Edibles are made with a proprietary blend of hemp-derived cannabinoids, natural and artificial flavoring, and terpenes.

|

Manufacturing and Distribution

Manufacturing

Charlie’s Product Line. We work closely with contract manufacturing partners in the United States, Ireland, Scotland and China to manufacture our products. Our e-liquid and NIC salts products are manufactured to meet our proprietary formula specifications in facilities that are ISO Class 7 certified, which helps ensure their purity and quality. In 2020, we added an additional supplier and sourced over 90% of our e-liquid finished goods from three manufacturers in the United States. During 2021, we launched our Pacha line of synthetic nicotine disposable vapor products, which required expansion of our vendor network. We have developed a strong relationship with our vendor in China to design and produce products to our strict specifications. While we have developed long-standing relationships with our manufacturing sources and take great care to ensure that they share our commitment to quality, we do not have any long-term term contracts with these parties for the production of our product lines. We maintain redundancies in our supply chain and are aware of several alternative sources for our products.

Don Polly Product Line. Our hemp-derived, Don Polly Products are manufactured with contract manufacturers to meet our formula specifications. While we do not have any long-term contracts with these parties, we are strengthening our supplier partnerships as well as identifying additional supplier and contract manufacturing opportunities.

Distribution

Charlie’s Product Line. Once manufactured, Charlie’s Products are directly distributed throughout the United States and in more than 80 countries, primarily the United Kingdom, Italy, Spain, New Zealand, Australia, and Canada. Our products are carried by more than 3,000 specialty retailers that are serviced through direct sales and through distributors and wholesalers both in the United States and internationally. While growing our base of specialty retailers, we have also increased distribution of our products in convenience stores, liquor stores, and gas stations. With respect to products that we sell through third-party distributors and wholesalers, we typically sell our products to these customers for their re-sale. In select markets we maintain exclusive arrangements with distributors and, when warranted, will memorialize these agreements contractually.

Don Polly Product Line. Don Polly Products are currently distributed to more than 1,000 distributor and retail accounts in the United States and United Kingdom. Like the Charlie’s Product Line, we sell Don Polly Products directly to retailers, as well as through distributors, third-party wholesalers, and independent brokers. We currently sell certain Don Polly Products through multiple internally managed e-commerce platforms.

Online Sales

Charlie’s Product Line and Don Polly Product Line. We do not currently sell our Charlie’s Products on an e-commerce platform. However, we market Charlie’s Products and sell branded merchandise through our website, charlieschalkdust.com and pacha.co. A portion of the Don Polly Product Line is offered for sale directly to consumers under our Pachamama brand through our in-house, e-commerce platforms on our websites, pachamamacbd.com, and donpolly.com.

Sales and Marketing

Charlie’s and Don Polly Product Lines. We have an experienced, twelve-person sales team, based in the United States, that promotes our Charlie’s and Don Polly Products globally. Salespeople seek to form long-term “360 degree” collaborative relationships with their clients, partnering with them on sell-through efforts, providing access to our marketing and creative teams, and advising and educating them on not only the Charlie’s and Don Polly Product Lines but also on industry-related issues. In 2021, we expanded our sales and marketing strategy to include use of “Brand Advocates” who are responsible for canvassing for potential new customers, while raising general awareness of both the Charlie’s and Don Polly product lines. Currently, we advertise our products primarily through customer engagement through social media channels, print media, directed internet marketing, industry tradeshows and, collaborative events with retail partners. Participation at industry-specific tradeshows has traditionally played a large role in our marketing and distribution strategy. In addition, we have allocated resources to collaborative events; our marketing team is now focusing its efforts on fostering relationships with key distributors and retailers by launching customer-specific marketing campaigns, in-person visits to new customer accounts, and other forms of direct customer engagement. In 2022, approximately 16% of our sales were made to customers outside of the United States.

Source and Availability of Raw Materials

Charlie’s Product Line. Our manufacturing partners source the ingredients for our proprietary vapor products from a variety of sources, in accordance with our formulations and quality specifications. We source our proprietary e-liquids from multiple ISO Class 7 certified manufacturers in the United States, which helps ensure their purity and quality. Our disposable vapor products are designed in collaboration with our Chinese manufacturer; however, the manufacturer is responsible for procurement of all raw materials necessary to complete our purchase orders. In an effort to maintain consistency across our supply chain, we purchase directly certain product packaging and are responsible for managing various third-party supplier relationships.

Don Polly Product Line. For our hemp-derived, alternative cannabis and CBD products, we currently source the individual components and oils from several suppliers. Each is delivered to our primary manufacturer for storage prior to manufacturing. We source hardware components from China for certain of our other hemp-derived products, which are then combined with ingredients sourced domestically to create finished goods.

Although we own the formulas for the Charlie’s Products and the Don Polly Products, we obtain certain components, such as packaging, flavors and certain raw materials, from third party suppliers. None of the third-party suppliers are considered to be material to the business on a standalone basis and the components are readily available from other suppliers on the market. However, given the rapid growth of the vaping, e-cigarette and hemp-derived products industries, there may be fluctuations in the availability of certain of the materials we obtain from third-parties due to high demand from our competitors. If any given supplier or distributor is lost or unavailable in a specific region, and we are unable to contract with alternative suppliers or distributors to provide the requisite service(s) and product(s), we may be unable to fulfill customer orders and our business could be materially harmed.

Competition

The industries in which we operate are highly competitive.

Charlie’s Product Line. Our Charlie’s Product Line competes in a highly-fragmented and rapidly evolving industry. Some identifiable competitors of Charlie’s include Naked100, Savage, Elf Bar, Puff Bar, Flum, and Hyde. Other brands such as Juul, Vuse, Group Mark Ten, Green Smoke, Blu, Vaporfi, Njoy, and Logic all participate in a different but related segment of the electronic cigarette market which focuses heavily on distribution in national and regional chain stores (primarily convenience, gas, and grocery stores) .

In the vapor products space, due to low barriers to entry, and despite FDA regulations for many products, new brands and products emerge frequently. The market is highly fragmented and the barriers to entry are relatively low. Recently, the rapid emergence of disposable vapor products from companies such as Elf Bar have become popular in the market. Some brands compete by offering a wide variety of choices and/or low-priced “value” products, while other companies, like Charlie’s Chalk Dust, carve out their identity with branding and more nuanced flavor combinations.

Part of our business strategy focuses on the establishment of relationships with distributors and prominent branding focused on performance and quality. We are aware that e-cigarette competitors in the industry are also seeking to enter into such relationships to try and create brand loyalty. In many cases, competitors for such relationships may have greater management, human, and financial resources than we do for attracting and maintaining distributor accounts. Furthermore, certain of our electronic cigarette competitors may have better control of their supply and distribution, are more established, larger and better financed than our Company.

We compete primarily on the basis of product quality, brand recognition, brand loyalty, service, marketing, and the development of intellectual property. We are subject to highly competitive conditions in all aspects of our business. The competitive environment and our competitive position can be significantly influenced by weak economic conditions, erosion of consumer confidence, competitors’ introduction of low-priced products or innovative products, cigarette excise taxes, higher absolute costs, larger gaps between price categories, and product regulation that diminishes a company’s ability to differentiate its products.

We also compete against “Big Tobacco” – U.S. cigarette manufacturers of both conventional tobacco cigarettes and electronic cigarettes like Altria Group, Inc., Lorillard, Inc. and Reynolds American, Inc. We compete with Big Tobacco companies that offer not only conventional tobacco cigarettes and electronic cigarettes but also smokeless tobacco products such as “snus” (a form of moist ground smokeless tobacco that is usually sold in sachet form that resembles small tea bags), chewing tobacco and snuff. Big tobacco has virtually limitless resources, existing global distribution networks, and a customer base that is fiercely loyal to their brands. Furthermore, we believe that Big Tobacco will devote more attention and resources to developing and offering electronic cigarettes as the market for electronic cigarettes continues to grow. Because of their well-established sales and distribution channels, marketing expertise, and significant resources, Big Tobacco companies may be better positioned than small competitors like Charlie’s to capture a larger share of the electronic cigarette market.

Don Polly Product Line. The market for hemp-based products is growing rapidly, highly competitive, and continually evolving. The competition consists of publicly traded and privately-owned companies, which tend to be highly fragmented in terms of both geographic market coverage and products offered. With the Company’s leading brand status, innovation capabilities, existing sales and marketing platform, established distribution channels, and high-quality manufacturing, Management believes the Company is well-positioned to capitalize on favorable long-term trends in the hemp-based products segment.

Intellectual Property

Patents and Trademarks

Charlie’s Product Line and Don Polly Product Line. We are the registered owner of a several federal trademarks for our Charlie’s and Don Polly product lines. We also maintain registrations in several international markets and will work with our international distributors to manage intellectual property and trademark registrations when necessary.

We plan to continue to expand our brand names and our proprietary trademarks and designs worldwide as our business grows and plan to seek patent and/or trademark protection as we deem appropriate.

Licensing Agreements

Charlie’s Product Line. The Company occasionally evaluates and enters into licensing opportunities to expand its footprint in the global nicotine-based products marketplace.

Don Polly Product Line. On April 25, 2019, the Company and Charlie’s entered into a Licensing Agreement with Don Polly. Don Polly is classified as a variable interest entity for which the Company is the primary beneficiary, and is owned by entities controlled by Ryan Stump, the Company’s Chief Operating Officer, and Brandon Stump, the Company’s former Chief Executive Officer. Pursuant to the Licensing Agreement, Charlie’s provides Don Polly with a limited right and license to use certain of Charlie’s intellectual property rights, including certain trademarks, copyrights and original artwork, in connection with certain of Don Polly’s branded CBD products. In exchange for such license, Don Polly (i) pays Charlie’s monthly royalties amounting to 75% of its net profits, (ii) uses its best efforts to market, promote and advertise its products, (iii) provides Charlie’s with most favored nations pricing in the event that Charlie’s wishes to sell products sold by Don Polly, (iv) provide Charlie’s with the exclusive right of first refusal to purchase Don Polly, including all of its assets and liabilities, for a purchase price of $111,618 on or before December 31, 2025, and (v) will not license any intellectual property from any other source other than Charlie’s in connection with its design, manufacture, advertisement, promotion distribution, and sale of CBD infused products within the agreed upon territory. The Licensing Agreement will continue in perpetuity unless terminated in accordance with its terms.

Concurrently with the execution of the Licensing Agreement, Charlie’s and Don Polly also entered into a Services Agreement (the “Services Agreement”), pursuant to which Charlie’s provides certain services to Don Polly, including, without limitation, (i) the development and creation of Don Polly’s sales, marketing, brand development, and customer service strategies and (ii) performing sales, branding, marketing, and other business functions at the request of Don Polly. Charlie’s will perform such services in the capacity of a contractor, and all materials and work product created by Charlie’s in its capacity as such will be the property of Don Polly. As consideration for the Services provided by Charlie’s, Don Polly (i) pays Charlie’s 25% of its net profits on a quarterly basis, and (ii) reimburse Charlie’s for all out-of-pocket business expenses that are preapproved in writing by Don Polly. The Services Agreement will continue in perpetuity unless terminated in accordance with its terms.

Government Regulations

Nicotine Products

The U.S. tobacco industry faces a number of business and legal challenges that have materially adversely affected and may continue to materially adversely affect our business and results of operations, including:

| |

●

|

restrictions and requirements imposed by the Family Smoking Prevention and Tobacco Control Act (“FSPTCA”), and restrictions and requirements (and related enforcement actions) that have been, and in the future will be, imposed by the FDA;

|

| |

●

|

actual and proposed excise tax increases;

|

| |

●

|

bans and restrictions on tobacco use imposed by governmental entities and private establishments and employers;

|

| |

●

|

other federal, state and local government actions, including:

|

| |

o

|

restrictions on the sale of certain tobacco products, the sale of tobacco products by certain retail establishments, the sale of tobacco products with characterizing flavors and the sale of tobacco products in certain package sizes;

|

| |

o

|

additional restrictions on the advertising and promotion of tobacco products;

|

| |

o

|

other actual and proposed tobacco-related legislation and regulation;

|

| |

o

|

reductions in consumption levels of nicotine products;

|

| |

●

|

increased efforts by tobacco control advocates and other private sector entities (including retail establishments) to further restrict the availability and use of tobacco products and

|

| |

●

|

additional regulation over synthetic nicotine products.

|

FSPTCA and FDA Regulation

The FSPTCA, its implementing regulations and its 2016 deeming regulations establish broad FDA regulatory authority over all tobacco products and, among other provisions:

| |

o

|

impose restrictions on the advertising, promotion, sale and distribution of tobacco products (see Final Tobacco Marketing Rule below);

|

| |

o

|

establish pre-market review pathways for new and modified tobacco products;

|

| |

o

|

prohibit any express or implied claims that a tobacco product is or may be less harmful than other tobacco products without FDA authorization;

|

| |

o

|

authorize the FDA to impose tobacco product standards that are appropriate for the protection of the public health; and

|

| |

o

|

equip the FDA with a variety of investigatory and enforcement tools, including the authority to inspect product manufacturing and other facilities.

|

The FSPTCA also bans descriptors such as “light,” “low” or “mild” when used as descriptors of modified risk, unless expressly authorized by the FDA.

In March 2022, the U.S. Congress expanded the statutory definition of tobacco products to include products containing nicotine derived from any source, including synthetic nicotine. The amendment became effective in April 2022.

Final Tobacco Marketing Rule: As required by the FSPTCA, in March 2010, the FDA promulgated a wide range of advertising and promotion restrictions for cigarettes and smokeless tobacco products (the “Final Tobacco Marketing Rule”). The May 2016 deeming regulations amended the Final Tobacco Marketing Rule to expand specific provisions to all tobacco products, including cigars, pipe tobacco and e-vapor and oral nicotine products containing tobacco-derived nicotine or other tobacco derivatives.

The Final Tobacco Marketing Rule, as amended, among other things:

| |

o

|

restricts the use of non-tobacco trade and brand names on cigarettes and smokeless tobacco products;

|

| |

o

|

prohibits sampling of all tobacco products except that sampling of smokeless tobacco products is permitted in qualified adult-only facilities;

|

| |

o

|

prohibits the sale or distribution of items such as hats and tee shirts with cigarette or smokeless tobacco brands or logos;

|

| |

o

|

prohibits cigarettes and smokeless tobacco brand name sponsorship of any athletic, musical, artistic or other social or cultural event, or any entry or team in any event; and

|

| |

o

|

requires the development by the FDA of graphic warnings for cigarettes, establishes warning requirements for other tobacco products, and gives the FDA the authority to require new warnings for any type of tobacco product.

|

Subject to certain limitations arising from legal challenges, the Final Tobacco Marketing Rule took effect in June 2010 for cigarettes and smokeless tobacco products, in August 2016 for all other tobacco products, including e-vapor and oral nicotine pouch products containing tobacco-derived nicotine, and in April 2022 for tobacco products, including e-vapor and oral nicotine pouch products, that contain synthetic nicotine.

Rulemaking and Guidance: From time to time, the FDA issues proposed regulations and guidance, which may be issued in draft or final form, generally involve public comment, and may include scientific review. The FDA’s implementation of the FSPTCA and related regulations and guidance also may have an impact on enforcement efforts by states, territories and localities of their laws and regulations. Such enforcement efforts may adversely affect our operating companies’ ability to market and sell regulated tobacco products in those states, territories and localities.

FDA’s Comprehensive Plan for Tobacco and Nicotine Regulation: In July 2017, the FDA announced a “Comprehensive Plan for Tobacco and Nicotine Regulation” (“Comprehensive Plan”) designed to strike a balance between regulation and encouraging the development of innovative tobacco products that may be less risky than cigarettes. Since then, the FDA has issued additional information about its Comprehensive Plan in response to concerns associated with the rise in the use of e-vapor products by youth and the potential youth appeal of flavored tobacco.

Pre-Market Review Pathways for Tobacco Products and Market Authorization Enforcement: The FSPTCA permits the sale of tobacco products on the market as of February 15, 2007 and not subsequently modified (“Pre-existing Tobacco Products”) and new or modified products authorized through the pre-market tobacco application (“PMTA”), Substantial Equivalence (“SE”) or SE Exemption pathways. Subsequent FDA rules also provide a Supplemental PMTA pathway designed to increase the efficiency of submission and review for modified versions of previously authorized products. Through these processes, a manufacturer could receive (i) a “not substantially equivalent” determination, (ii) a denial of a PMTA or (iii) a marketing order withdrawal by the FDA on one or more products, which would require the removal of the product or products from the market.

Since there were virtually no e-liquid, e-cigarettes or other vaping products on the market as of February 15, 2007, there is no way to utilize the less onerous substantial equivalence or substantial equivalence exemption pathways that traditional tobacco corporations can utilize. In order to obtain premarket approval, practically all e-liquid, e-cigarettes or other vaping products would have to follow the PMTA pathway which would cost hundreds of thousands of dollars per application. Upon submission of a PMTA, such products would be permitted to be sold pending the FDA’s review of the submitted PMTAs.

During the quarter ended September 30, 2020, the FDA's Center for Tobacco Products informed us that our PMTA received a valid submission tracking number, passed the FDA’s filing review phase, and recently entered the substantive review phase. To date, the Company has invested more than $5.1 million for our PMTA submissions. We engaged a team of more than 200 professionals, including doctors, scientists, biostatisticians, data analysts, and numerous contract research organizations to create our comprehensive PMTA submission. During the quarter ended September 30, 2021, the FDA began issuing Marketing Denial Orders (“MDOs”) for electronic nicotine delivery system (“ENDS”) products that lack evidence to demonstrate that permitting the marketing of such products would be appropriate for the protection of the public health.

On March 15, 2022, a new rider to the Federal Food, Drug and Cosmetic Act was passed granting the FDA authority over synthetic nicotine. These regulations make synthetic nicotine products subject to the same FDA rules as tobacco-derived nicotine products. As such, the Company was required to file a PMTA for its existing synthetic nicotine products marketed under the Pacha brands by May 14, 2022 or be subject to FDA enforcement. The Company filed new PMTAs for its synthetic Pacha products, on May 13, 2022, prior to the May 14, 2022, deadline. On November 3, 2022, FDA accepted for scientific review certain of our PMTAs for synthetic nicotine products and, on November 4, 2022, FDA refused to accept certain other PMTAs for these products, rendering the latter products subject to FDA enforcement. The Company submitted an administrative appeal with FDA regarding its refusal to accept certain of the PMTAs, and has resubmitted PMTAs for, and continues to sell, the affected synthetic nicotine products while the administrative appeal process is pending.

As December 31, 2022, Charlie’s 2020 PMTA remains among the select minority of applications submitted to the FDA for a tobacco-derived nicotine ENDS product that has not received an MDO or Refuse-to-File designation.

FDA Regulatory Actions

| |

o

|

Graphic Warnings: In March 2020, the FDA issued a final rule requiring 11 textual warnings accompanied by color graphics depicting certain negative health consequences of smoking on cigarette packaging and advertising. The final rule was set to become effective on October 6, 2023. In December 2022, the U.S. District Court for the Eastern District of Texas found in favor of cigarette manufacturers in one such suit and blocked the rule, finding it unconstitutional on the basis that it compelled speech in violation of the First Amendment. The FDA has appealed the decision.

|

| |

o

|

Underage Access and Use of Certain Tobacco Products: The FDA announced regulatory actions in September 2018 to address underage access and use of e-vapor products. Additionally, the FDA issued final guidance in April 2020, stating that it intends to prioritize enforcement action against certain product categories, including cartridge-based, flavored e-vapor products and products targeted to minors.

|

| |

o

|

Potential Product Standards

|

| |

o

|

Nicotine in Cigarettes and Other Combustible Tobacco Products: In March 2018, the FDA issued an ANPRM seeking comments on the potential public health benefits and any possible adverse effects of lowering nicotine in combustible cigarettes to non-addictive or minimally addictive levels. In January 2023, the Biden Administration published its Fall 2022 Unified Regulatory Agenda, which includes the FDA’s plans to propose, by October 2023, a product standard that would establish a maximum nicotine level in cigarettes and other combustible tobacco products.

|

| |

o

|

Flavors in Tobacco Products: In April 2022, the FDA issued two proposed product standards: (i) banning menthol in cigarettes and (ii) banning all characterizing flavors (including menthol) in cigars. The Biden Administration’s Fall 2022 Unified Regulatory Agenda includes the FDA’s plans to complete rulemaking with respect to these proposed product standards by the end of 2023.

|

Excise Taxes

Tobacco products are subject to substantial excise taxes in the United States. Significant increases in tobacco-related taxes or fees have been proposed or enacted (including with respect to e-vapor products) and are likely to continue to be proposed or enacted at the federal, state and local levels within the United States. The frequency and magnitude of excise tax increases can be influenced by various factors, including the composition of executive and legislative bodies.

International Treaty on Tobacco Control

The World Health Organization’s Framework Convention on Tobacco Control (the “FCTC”) entered into force in February 2005. The FCTC is the first international public health treaty and its objective is to establish a global agenda for tobacco regulation with the purpose of reducing initiation of tobacco use and encouraging cessation. The treaty recommends (and in certain instances, requires) signatory nations to enact legislation that would address various tobacco-related issues. There are a number of proposals currently under consideration by the governing body of the FCTC, some of which call for substantial restrictions on the manufacture, marketing, distribution and sale of tobacco products.

Other International, Federal, State and Local Regulation

Various states and localities have enacted or proposed legislation that imposes restrictions on tobacco products (including cigarettes, smokeless tobacco, cigars, e-vapor products and oral nicotine pouches), such as legislation that (i) prohibits the sale of all tobacco products or certain tobacco categories, such as e-vapor, (ii) prohibits the sale of tobacco products with characterizing flavors, such as menthol cigarettes and flavored e-vapor products, (iii) requires the disclosure of health information separate from or in addition to federally mandated health warnings and (iv) restricts commercial speech or imposes additional restrictions on the marketing or sale of tobacco products. The legislation varies in terms of the type of tobacco products, the conditions under which such products are or would be restricted or prohibited, and exceptions to the restrictions or prohibitions. For example, a number of proposals involving characterizing flavors would prohibit smokeless tobacco products with characterizing flavors. As of February 23, 2023, multiple states and localities are considering legislation to ban flavors in one or more tobacco products, and six states (California, Massachusetts, New Jersey, Utah, New York and Illinois) and the District of Columbia have passed such legislation. The legislation in California, which became effective in December 2022, bans the sale of most tobacco products with characterizing flavors. Massachusetts passed legislation capping the amount of nicotine in e-vapor products. Similar legislation is pending in other states.

It is not possible to predict what, if any, additional legislation, regulation, or other governmental action will be enacted or implemented (and, if challenged, upheld) relating to the manufacturing, design, packaging, marketing, advertising, sale or use of tobacco products, or the tobacco industry generally. Any such legislation, regulation or other governmental action could have a material adverse impact on our business, results of operations, cash flows or financial position.

Company’s efforts to mitigate risks associated with new and evolving regulation

The Company is consistent in its efforts to remain in compliance with all existing and reasonably expected future regulations. The Company, through its internal compliance team, market consultants, technicians, and testing labs plans to stay in accordance with all standards whether set forth in the New Tobacco Products Directive or the Deeming Regulations. Making sure that all vapor products meet and exceed the standards set forth by each market’s regulatory body is of the highest concern for the Company. Staying in compliance with all marketing and packaging directives is imperative to maintaining access to the markets. Although these processes are costly and time consuming, it is imperative for the Company’s success that these steps are taken and kept up to date. These regulations may limit our ability to enter certain markets outside the U.S. Similar to the costs of regulatory compliance in the U.S., foreign regulations require significant financial and operational resources to ensure compliance, and we cannot assure that we will always be in compliance despite our best efforts to do so. Failure to comply in a timely fashion to any particular directive or regulation could have material adverse effects on the results of business operations.

Don Polly Product Line

Don Polly’s CBD products are subject to various state and federal laws regarding the production and sales of hemp-based products. Section 12619 of the Agriculture Improvement Act of 2018 (“2018 Farm Bill”) removed “hemp”, as defined in the Agricultural Marketing Act of 1946 (the “1946 Agricultural Act”), from the classification of “marijuana,” which is generally prohibited as a Schedule I drug under the Controlled Substances Act of 1970 (“CSA”). Under the 1946 Agricultural Act (as amended by the 2018 Farm Bill), the term “hemp” means “the plant Cannabis sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis”. As a result of the passage of the 2018 Farm Bill, and since the Company believes the Don Polly Products contain parts of the cannabis plant with a THC concentration of not more than 0.3 percent on a dry weight basis, the Company believes that Don Polly Products are not governed by the CSA and, ergo, would not be subject to prosecution thereunder because the Company believes Don Polly Products contain “hemp” within the meaning of the 1946 Agricultural Act (as amended by the 2018 Farm Bill) and do not contain any “marijuana” as prohibited under the CSA (as amended by the 2018 Farm Bill); provided, however, there is a lack of legal protection for hemp-based products that contain more than 0.3 percent THC and there is a risk that the Company would be subject to prosecution under the CSA in the event that its CBD products are found to contain more than 0.3 percent THC.

Furthermore, the 1946 Agricultural Act (as amended by the 2018 Farm Bill) provides additional regulations regarding the production of hemp-based products and there is the risk that Don Polly Products may be found to be in violation of these regulations. Specifically, the 1946 Agricultural Act (as amended by the 2018 Farm Bill) contains provisions relating to the shared state-federal jurisdiction over hemp cultivation and production, whereby states and Indian tribes have been delegated the broad authority to regulate and limit the production and sale of hemp and hemp products within their borders. Under the 1946 Agricultural Act (as amended by the 2018 Farm Bill), a plan under which a State or Indian tribe monitors and regulates the production of hemp shall only be required to include “(i) a practice to maintain relevant information regarding land on which hemp is produced in the State or territory of the Indian tribe, including a legal description of the land, for a period of not less than three calendar years; (ii) a procedure for testing, using post-decarboxylation or other similarly reliable methods, delta-9 tetrahydrocannabinol concentration levels of hemp produced in the State or territory of the Indian tribe; (iii) a procedure for the effective disposal of—(I) plants, whether growing or not, that are produced in violation of this subtitle; and (II) products derived from those plants; (iv) a procedure to comply with enforcement procedures; (v) a procedure for conducting annual inspections of, at a minimum, a random sample of hemp producers to verify that hemp is not produced in violation of this subtitle; (vi) a procedure for submitting the information, as applicable, to the Secretary of Agriculture (the “Secretary”) not more than 30 days after the date on which the information is received; and (vii) a certification that the State or Indian tribe has the resources and personnel to carry out the practices and procedures described in clauses (i) through (vi)”. Further, a hemp producer in a State or the territory of an Indian tribe for which a State or Tribal plan is approved shall be determined to have negligently violated the State or Tribal plan, including by negligently— “(i) failing to provide a legal description of land on which the producer produces hemp; (ii) failing to obtain a license or other required authorization from the State department of agriculture or Tribal government, as applicable; or (iii) producing Cannabis sativa L. with a delta-9 THC concentration of more than 0.3 percent on a dry weight basis.” A hemp producer that negligently violates a State or Tribal plan 3 times in a 5-year period shall be ineligible to produce hemp for a period of 5 years beginning on the date of the third violation. If the State department of agriculture or Tribal government in a State or the territory of an Indian tribe for which a State or Tribal plan, as applicable, determines that a hemp producer in the State or territory has violated the State or Tribal plan with a culpable mental state greater than negligence— “(i) the State department of agriculture or Tribal government, as applicable, shall immediately report the hemp producer to —(I) the Attorney General; and (II) the chief law enforcement officer of the State or Indian tribe, as applicable.” In the case of a State or Indian tribe for which a State or Tribal plan is not approved, the production of hemp in that State or the territory of that Indian tribe shall be subject to a plan established by the Secretary to monitor and regulate that production. A plan established by the Secretary under shall include— “(A) a practice to maintain relevant information regarding land on which hemp is produced in the State or territory of the Indian tribe, including a legal description of the land, for a period of not less than 3 calendar years; (B) a procedure for testing, using post-decarboxylation or other similarly reliable methods, delta-9 tetrahydrocannabinol concentration levels of hemp produced in the State or territory of the Indian tribe; (C) a procedure for the effective disposal of—(i) plants, whether growing or not, that are produced in violation of this subtitle; and (ii) products derived from those plants; (D) a procedure to comply with the enforcement procedures; and (E) a procedure for conducting annual inspections of, at a minimum, a random sample of hemp producers to verify that hemp is not produced in violation of this subtitle; and (F) such other practices or procedures as the Secretary considers to be appropriate. The Secretary shall also establish a procedure to issue licenses to hemp producers. In the case of a State or Indian tribe for which a State or Tribal plan is not approved under applicable law, it shall be unlawful to produce hemp in that State or the territory of that Indian tribe without a license issued by the Secretary. A violation of a plan established by the Secretary shall be subject to enforcement and the Secretary shall report the production of hemp without a license issued by the Secretary to the Attorney General.” In the event that the Company’s hemp-derived products are found to be in violation of these regulations, the Company may become subject to enforcement action as provided for in the 1946 Agricultural Act (as amended by the 2018 Farm Bill) and may become subject to prosecution thereunder.

Research and Development

Our research and development activities consist of development and testing of new flavors, formulations, formats, and delivery methods for our existing products, as well as development of new products for the Charlie’s Product Line and the Don Polly Product Line. Costs related to the completion and submission of PMTAs to the FDA also constitute research and development activities. For the years ended December 31, 2022, and 2021, respectively, research and development costs primarily consisted of product development and testing fees.

For the years ended December 31, 2022 and 2021, Charlie’s recorded research and development expense of $804,000 and $24,000, respectively.

Employees

We had 35 full-time employees across Charlie’s Holdings Inc., Charlie’s Chalk Dust LLC and Don Polly LLC as of April 17, 2023. We believe that we maintain a good working relationship with our employees, and we have not experienced any labor disputes. None of our employees are represented by labor unions.

Cost of Compliance with Environmental Laws

We have not incurred any costs associated with compliance with environmental regulations, nor do we anticipate any future costs associated with environmental compliance; however, no assurances can be given that we will not incur such costs in the future.

Available Information

As a public company, we are required to file our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements on Schedule 14A and other information (including any amendments) with the SEC. You can also find the Company’s SEC filings at the SEC’s website at www.sec.gov.

We are a Nevada corporation originally incorporated in 2001. Our principal executive offices are located at 1007 Brioso Drive, Costa Mesa, CA 92627 and our phone number is (949) 531-6855. Our Internet address is www.charliesholdings.com. Information contained on our website is not part of this Annual Report on Form 10-K. Our SEC filings (including any amendments) will be made available free of charge on www.charliesholdings.com, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC.

ITEM 1A. RISK FACTORS

We are subject to various risks that could have a negative effect on the Company and its financial condition. These risks could cause actual operating results to differ from those expressed in certain “forward looking statements” contained in this Annual Report on Form 10-K as well as in other communications.

Risks Related to the Company

Our ability to achieve and maintain positive cash flow is uncertain.

Although Charlie’s generated net revenue of approximately $26.4 million during the year ended December 31, 2022 and $21.5 million for the year ended December 31, 2021, there can be no guarantee that the Company will continue to grow revenue or achieve positive cash flow in the future. Cash used in operating activities was approximately $1.7 million and $1.3 million during the years ended December 31, 2022 and 2021, respectively. Generating positive cash flows in the future will depend on our ability to successfully create, sell and market nicotine, nicotine alternative and hemp-derived products. There is no guarantee that we will be able to achieve or sustain positive cash flows and profitability in the future. Our inability to successfully achieve positive cash flows and profitability will decrease our long-term viability and prospects.

We have limited cash resources and may require additional financing.

As of December 31, 2022, we had working capital of approximately $1.1 million, which consisted of current assets of approximately $5.9 million and current liabilities of approximately $4.8 million. If needed, our ability to obtain additional financing will be subject to many factors, including limitations on incurring debt in with respect to our Series A convertible preferred stock (“Series A Preferred”), market conditions, our operating performance and investor sentiment. If we are unable to raise additional capital when required or on acceptable terms, we may have to significantly restrict our operations or obtain funds by entering into agreements on unattractive terms, which would likely have a material adverse effect on our business, stock price and our relationships with third parties with whom we have business relationships, at least until additional funding is obtained. If we do not have sufficient funds to continue operations, we could be required to seek bankruptcy protection or other alternatives that would likely result in our stockholders losing some or all of their investment in us.

Our auditors have issued a going concern opinion on our financial statements as of December 31, 2022.