TABLE OF CONTENTS

Page

| CERTAIN TERMS AND CONVENTIONS | 1 |

| CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | 2 |

| PRESENTATION OF FINANCIAL AND OTHER INFORMATION | 4 |

| SELECTED FINANCIAL DATA | 5 |

| OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 7 |

| REGULATORY RECENT DEVELOPMENTS | 23 |

| SIGNATURES | 32 |

| FINANCIAL STATEMENTS | 33 |

CERTAIN TERMS AND CONVENTIONS

All references in this Form 6-K to (i) “Itaú Unibanco Holding,” “Itaú Unibanco Group,” “we,” “us” or “our” are references to Itaú Unibanco Holding S.A. and its consolidated subsidiaries, except where otherwise specified or required by the context; (ii) the “Brazilian government” are references to the federal government of the Federative Republic of Brazil, or Brazil; (iii) “preferred shares” are references to our authorized and outstanding preferred shares with no par value; and (iv) “common shares” are references to our authorized and outstanding common shares with no par value. All references to “ADSs” are to American Depositary Shares, each representing one preferred share, without par value. The ADSs are evidenced by American Depositary Receipts, or “ADRs,” issued by The Bank of New York Mellon, or BNY Mellon. All references herein to the “real,” “reais” or “R$” are to the Brazilian real, the official currency of Brazil. All references to “US$,” “dollars” or “U.S. dollars” are to United States dollars.

Additionally, unless specified or the context indicates otherwise, the following definitions apply throughout this Form 6-K:

| · | “Itaú Unibanco” means Itaú Unibanco S.A., together with its consolidated subsidiaries; |

| · | “Itaú BBA” means Banco Itaú BBA S.A., together with its consolidated subsidiaries; |

| · | “Itaú Corpbanca” means Itaú Corpbanca, together with its consolidated subsidiaries; and |

| · | “Central Bank” means the Central Bank of Brazil. |

Additionally, acronyms used repeatedly, defined and technical terms, specific market expressions and the full names of our main subsidiaries and other entities referenced in this report on Form 6-K are explained or detailed in the glossary of terms beginning on page 200 to our annual report on Form 20-F for the year ended December 31, 2022 filed with the SEC on April 28, 2023, or our 2022 Form 20-F.

| 1 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report on Form 6-K contains statements that are or may constitute forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995, Section 27A of the United States Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the Exchange Act. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends affecting our business. These forward-looking statements are subject to risks, uncertainties and assumptions including, among other risks:

| · | Political instability in Brazil, including developments and the perception of risks in connection with the recently elected government in Brazil, as well as ongoing corruption and other investigations and increasing fractious relations and infighting within the administration of the Brazilian government, as well as policies and potential changes to address these matters or otherwise, including economic and fiscal reforms, any of which may negatively affect growth prospects in the Brazilian economy as a whole; |

| · | General economic, political, and business conditions in Brazil and variations in inflation indices, interest rates, foreign exchange rates, and the performance of financial markets in Brazil and the other markets in which we operate; |

| · | Global economic and political conditions, as well as geopolitical instability, in particular in the countries where we operate, including in relation to the United States or the Russian invasion of Ukraine; |

| · | Changes in laws or regulations, including in respect of tax matters, compulsory deposits and reserve requirements, that adversely affect our business; |

| · | Any changes in tax law, tax reforms or review of the tax treatment of our activities may adversely affect our operations and profitability; |

| · | Disruptions and volatility in the global financial markets; |

| · | Costs and availability of funding; |

| · | Failure or hacking of our security and operational infrastructure or systems; |

| · | Our ability to protect personal data; |

| · | Our level of capitalization; |

| · | Increases in defaults by borrowers and other loan delinquencies, which result in increases in loan loss allowances; |

| · | Competition in our industry; |

| · | Changes in our loan portfolio and changes in the value of our securities and derivatives; |

| · | Customer losses or losses of other sources of revenues; |

| · | Our ability to execute our strategies and capital expenditure plans and to maintain and improve our operating performance; |

| · | Our exposure to Brazilian public debt; |

| 2 |

| · | Incorrect pricing methodologies for insurance, pension plan and premium bond products and inadequate reserves; |

| · | The effectiveness of our risk management policies; |

| · | Our ability to successfully integrate acquired or merged businesses; |

| · | Adverse legal or regulatory disputes or proceedings; |

| · | Environmental damage and climate change and effects from socio-environmental issues, including new and/or more stringent regulations relating to these issues; and |

| · | Other risk factors as set forth in our 2022 Form 20-F. |

The words “believe”, “may”, “will”, “estimate”, “continue”, “anticipate”, “intend”, “expect” and similar words are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We undertake no obligation to update publicly or revise any forward-looking statements because of new information, future events or otherwise. In light of these risks and uncertainties, the forward-looking information, events and circumstances discussed in this report on Form 6-K might not occur. Our actual results and performance could differ substantially from those anticipated in such forward-looking statements.

| 3 |

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

The information found in this Form 6-K is accurate only as of the date of such information or as of the date of this Form 6-K, as applicable. Our activities, our financial position and assets, the results of operations and our prospects may have changed since that date.

Information contained in or accessible through our website or any other websites referenced herein does not form part of this Form 6-K unless we specifically state that it is incorporated by reference and forms part of this Form 6-K. All references in this Form 6-K to websites are inactive textual references and are for information only.

Effect of Rounding

Certain amounts and percentages included in this Form 6-K, including in the section of this Form 6-K entitled “Operating and Financial Review and Prospects” have been rounded for ease of presentation. Percentage figures included in this Form 6-K have not been calculated in all cases on the basis of the rounded figures but on the basis of the original amounts prior to rounding. For this reason, certain percentage amounts in this Form 6-K may vary from those obtained by performing the same calculations using the figures in our audited interim consolidated financial statements. Certain other amounts that appear in this Form 6-K may vary slightly and figures shown as totals in certain tables may not be an arithmetical aggregation of the figures preceding them.

About our Financial Information

The reference date for the quantitative information derived from our consolidated balance sheet included in this Form 6-K is as of June 30, 2023 and December 31, 2022 and the reference dates for information derived from our consolidated statement of income are the six-month periods ended June 30, 2023 and 2022, except where otherwise indicated.

Our audited interim consolidated financial statements as of June 30, 2023 and December 31, 2022 and for the six-month periods ended June 31, 2023 and 2022, included at the end of this Form 6-K, are prepared in accordance with International Financial Reporting Standards, or IFRS, issued by the International Accounting Standards Board, or IASB.

Our audited interim consolidated financial statements as of June 30, 2023 and December 31, 2022 and for the six-month periods ended June 30, 2023 and 2022 were audited in accordance with International Standards on Auditing by PricewaterhouseCoopers Auditores Independentes Ltda., or PwC, our independent auditors. Such financial statements are referred to herein as our audited interim consolidated financial statements.

Please see “Note 30 – Segment Information” to our audited interim consolidated financial statements for further details about the main differences between our management reporting systems and our audited interim consolidated financial statements prepared in accordance with IFRS issued by the IASB.

| 4 |

SELECTED FINANCIAL DATA

We present below our selected financial data derived from our audited interim consolidated financial statements included in this Form 6-K. Our audited interim consolidated financial statements are presented as of June 30, 2023 and December 31, 2022 and for the six-month periods ended June 30, 2023 and 2022 and have been prepared in accordance with IFRS issued by the IASB. Considering the adoption of IFRS 17 for insurance and reinsurance contracts held as from January 1, 2023, we adopted the modified retrospective approach with a transition date of January 1, 2022 for comparative purposes. For further details, please see “Note 2 – Significant accounting policies” to our audited interim consolidated financial statements.

Additionally, we present a summarized version of our Consolidated Statement of Income, Consolidated Balance Sheet and Consolidated Statement of Cash Flows in the section “Operating and Financial Review and Prospects.”

The following selected financial data should be read together with “Presentation of Financial and Other Information” and “Operating and Financial Review and Prospects.”

| 5 |

| Income Information | For the six-month period ended June 30, |

Variation | |

| 2023 | 2022 | ||

| (In millions of R$, except percentages and basis points) | % | ||

| Operating Revenues | 76,173 | 70,011 | 8.8 |

| Net interest income(1) | 47,732 | 43,332 | 10.2 |

| Non-interest income(2) | 28,441 | 26,679 | 6.6 |

| Expected Loss from Financial Assets | (16,029) | (13,235) | 21.1 |

| Other operating income (expenses) | (41,000) | (37,722) | 8.7 |

| Net income attributable to owners of the parent company | 15,974 | 13,966 | 14.4 |

| Recurring Return on Average Equity - Annualized - Consolidated (3) | 18.6% | 18.6% | - |

| Return on Average Equity – Annualized - Consolidated(4) | 18.5% | 18.1% | 40 bps |

| (1) Includes: (i) interest and similar income; (ii) interest and similar expenses; (iii) income of financial assets and liabilities at fair value through profit or loss; and (iv) foreign exchange results and exchange variations in foreign transactions. (2) Includes commissions and banking fees, income from insurance contracts and private pension and other income. | |||

| (3) The Recurring Return on Average Equity is obtained by dividing the Recurring Result (R$16,081 million and R$14,348 million in the six-month periods ended June 30, 2023 and 2022, respectively) by the Average Stockholders’ Equity adjusted by the dividends proposed (R$172,707 million and R$154,342 million in the six-month periods ended June 30, 2023 and 2022, respectively). The resulting amount is multiplied by the number of periods in the year to derive the annualized rate. The calculation bases of returns were adjusted by the dividends proposed after the balance sheet closing dates, which have not yet been approved at annual Stockholders' or Board meetings. | |||

| (4) The Return on Average Equity is calculated by dividing the Net Income (R$15,974 million and R$13,966 million in the six-month periods ended June 30, 2023 and 2022, respectively) by the Average Stockholders’ Equity adjusted by the dividends proposed (R$172,707 million and R$154,342 million in the six-month periods ended June 30, 2023 and 2022, respectively). This average considers the Stockholders’ Equity from the four previous quarters. The quotient of this division was multiplied by the number of periods in the year to arrive at the annual ratio. The calculation bases of returns were adjusted by the proposed dividend amounts after the balance sheet dates not yet approved at the annual shareholders 'meeting or at the Board of Directors' meetings. | |||

| Balance Sheet Information | As of June 30, | As of December 31, | Variation |

| 2023 | 2022 | ||

| (In millions of R$, except percentages and basis points) | % | ||

| Total assets | 2,434,208 | 2,321,066 | 4.9 |

| Total loans and finance lease operations | 901,185 | 909,422 | (0.9) |

| (-) Provision for expected loss(1) | (54,046) | (52,324) | 3.3 |

| Common Equity Tier I Ratio - in % | 12.2% | 11.9% | 30 bps |

| Tier I Ratio - in % | 13.6% | 13.5% | 10 bps |

| Total Capital Ratio - in % | 15.1% | 15.0% | 10 bps |

| (1) Comprises Expected Credit Loss for Financial Guarantees Pledged R$ (778) at 06/30/2023 (R$ (810) at 12/31/2022) and Loan Commitments R$ (3,094) at 06/30/2023 (R$ (2,874) at 12/31/2022). Please see “Note 10 — Loan and Lease operations” to our audited interim consolidated financial statements for further details. | |||

| Other Information | For the six-month period ended June 30, |

Variation | |

| 2023 | 2022 | % | |

| Net income per share – R$ (1) | 1.63 | 1.43 | 14.0 |

| Weighted average number of outstanding shares - basic | 9,795,857,635 | 9,797,123,736 | (0.0) |

| Total Number of Employees | 99,864 | 99,913 | (0.0) |

| Brazil | 88,078 | 87,703 | 0.4 |

| Abroad | 11,786 | 12,210 | (3.5) |

| Total Branches and CSBs – Client Service Branches | 4,081 | 4,192 | (2.6) |

| ATM – Automated Teller Machines (2) | 42,400 | 43,747 | (3.1) |

| (1) Calculated based on the weighted average number of outstanding shares for the period. | |||

| (2) Includes ESBs (electronic service branches) and service points at third-party locations and Banco24Horas ATMs. | |||

| 6 |

OPERATING AND FINANCIAL REVIEW AND PROSPECTS

The following discussion should be read in conjunction with our audited interim consolidated financial statements and accompanying notes and other financial information included elsewhere in this Form 6-K and the description of our business in “Item 4. Information on the Company” in our 2022 Form 20-F. The following discussion contains forward-looking statements that involve risks and uncertainties. Our actual results may differ materially from those discussed in forward-looking statements as a result of various factors, including those set forth in “Forward-Looking Statements” herein and in our 2022 Form 20-F.

Results of Operations

The table below presents our summarized consolidated statement of income for the six-month periods ended June 30, 2023 and 2022. The interest rates presented are expressed in Brazilian reais and include the effect of the variation of the real against foreign currencies. For more information on the products and services we offer, see “Item 4. Information on the Company” in our 2022 Form 20-F.

Please see our audited interim consolidated financial statements for the six-month period ended June 30, 2023 and 2022 for further details about our Consolidated Statement of Income.

| Summarized Consolidated Statement of Income | For the six month period ended June 30, |

Variation | ||

| 2023 | 2022 | R$ million | % | |

| (In millions of R$) | ||||

| Operating revenues | 76,173 | 70,011 | 6,162 | 8.8 |

| Net interest income(1) | 47,732 | 43,332 | 4,400 | 10.2 |

| Non-interest income(2) | 28,441 | 26,679 | 1,762 | 6.6 |

| Expected loss from financial assets | (16,029) | (13,235) | (2,794) | 21.1 |

| Other operating income (expenses) | (41,000) | (37,722) | (3,278) | 8.7 |

| Net income before income tax and social contribution | 19,144 | 19,054 | 90 | 0.5 |

| Current and deferred income and social contribution taxes | (2,681) | (4,492) | 1,811 | (40.3) |

| Net income | 16,463 | 14,562 | 1,901 | 13.1 |

| Net income attributable to owners of the parent company | 15,974 | 13,966 | 2,008 | 14.4 |

| (1) Includes: | ||||

| (i) interest and similar income (R$111,549 million and R$84,127 million in the six-month periods ended June 30, 2023 and 2022, respectively); (ii) interest and similar expenses (R$(81,576) million and R$(46,025) million in the six-month periods ended June 30, 2023 and 2022, respectively); (iii) income of financial assets and liabilities at fair value through profit or loss (R$11,917 million and R$4,879) million in the six-month periods ended June 30, 2023 and 2022, respectively); and (iv) foreign exchange results and exchange variations in foreign transactions (R$5,842 million and R$351 million in the six-month periods ended June 30, 2023 and 2022, respectively). | ||||

| (2) Includes commissions and banking fees, Income from insurance contracts and private pension and other income. | ||||

Six-month period ended June 30, 2023, compared to six-month period ended June 30, 2022.

Net income attributable to owners of the parent company increased by 14.4% to R$15,974 million for the six-month period ended June 30, 2023, from R$13,966 million for the same period of 2022. This is mainly due to an 8.8%, or R$6,162 million, increase in operating revenues, and 40.3%, or R$1,811 million, decrease in current and deferred income and social contribution taxes, offset by an 8.7%, or R$3,278 million, increase in other operating income (expenses), and 21.1%, or R$2,794 million, increase in expected loss from financial assets. These line items are further described below:

Net interest income increased by R$4,400 million, or 10.2%, for the six-month period ended June 30, 2023, compared to the same period of 2022, mainly due to increases in the following line items (i) R$27,422 million in interest and similar income, mainly due to increases of R$10,803 million in income from securities purchased under agreements to resell, R$10,323 million in loan operations income, and R$3,524 million in financial assets at fair value through other comprehensive income; (ii) R$7,038 million in income of financial assets and liabilities at fair value through profit or loss; and (iii) R$5,491 million in foreign exchange results and exchange variations in foreign transactions. These increases were offset by an increase of R$35,551 million in interest and similar expenses.

| 7 |

| o | Interest and similar income increased by 32.6% for the six-month period ended June 30, 2023, compared to the same period of 2022, due to higher income from securities purchased under agreements to resell and the positive effect of the growth of our loan portfolio, associated with the gradual change in the composition of credit risk assets between periods, or the Mix of Credit Products, in addition to the positive impact of the increase in the Brazilian base interest rate, or SELIC Rate. As of June 30, 2023, the SELIC Rate was 13.75% per annum compared to 13.25% per annum as of June 30, 2022. |

| o | Interest and similar expenses increased by 77.2% for the six-month period ended June 30, 2023 compared to the same period of 2022, due to increases in the following line items: (i) R$15,510 million in expenses from deposits, especially in time deposits; and (ii) R$11,781 million in expenses from securities sold under repurchase agreements. The increases mentioned above are a result of the increase in the volume of our operations and the slight increase in interest rates. |

Please see “Note 21 – Interest and similar income and expenses and income of financial assets and liabilities at fair value through profit or loss” to our audited interim consolidated financial statements for further details on interest and similar expenses.

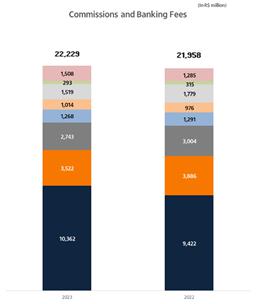

Non-interest income increased by 6.6%, or R$1,762 million for the six-month period ended June 30, 2023 compared to the same period of 2022. This increase was mainly due to (i) a 39.6%, or R$973 million, increase in income from insurance contracts and private pension, due to higher insurance sales mainly related to group life products, credit life and mortgage insurance products, and the increase in our financial result of the period; and (ii) a 1.2%, or R$271 million, increase in commissions and banking fees, due to the higher transaction volume from credit and debit cards, both in the issuance and acquiring businesses.

The following chart shows the main components of our banking service fees for the six-month period ended June 30, 2023, and 2022:

|

|

Please see “Note 22 – Commissions and Banking Fees” to our audited interim consolidated financial statements for further details on banking service fees.

| 8 |

Expected Loss from Financial Assets

Our expected loss from financial assets increased by R$2,794 million, or 21.1%, for the six-month period ended June 30, 2023, compared to the same period of 2022, mainly due to an increase in expected loss with loan and lease operations of R$2,570 million for the six-month period ended June 30, 2023, compared to the same period of 2022. This increase was mainly due to an increase in our credit portfolio and higher provisions in the Retail Business in Brazil, a result of the increase in origination of unsecured consumer credit products.

Please see “Note 10 — Loan and Lease operations” to our audited interim consolidated financial statements for further details on our loan and lease operations portfolio.

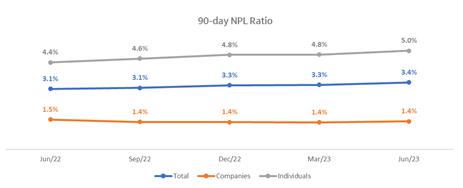

| o | Non-performing loans: We calculate our 90-day non-performing loan, or NPL ratio, as the value of our 90-days non-performing loans to our loan portfolio. |

As of June 30, 2023, our 90-day NPL ratio was 3.4%, an increase of 30 basis points compared to June 30, 2022. This increase was due to the increase of 60 basis points in the 90-day NPL ratio in respect of our individuals loan portfolio, which experienced higher delinquency rates. This was partially offset by a decrease of 10 basis points in the NPL ratio of our companies loan portfolio. In the second quarter of 2023, we recorded sales of active portfolios with no risk retention to unaffiliated companies. From these sales, R$185 million refer to active loans that were more than 90 days overdue, of which R$139 million would still be an active loan portfolio at the end of the period if not sold. Additionally, we sold R$99 million which refer to active portfolios non-overdue or with short delinquency from our Latin American operations. These sales did not have a material impact on delinquency ratios.

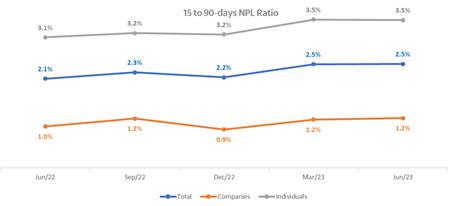

We calculate our 15 to 90 days non-performing loan ratio as the value of our 15 to 90 days NPL to our loan portfolio. The 15 to 90 days NPL ratio is an indicator of early delinquency.

As of June 30, 2023, our 15 to 90 days NPL ratio was 2.5%, an increase of 40 basis points when compared to June 30, 2022. During this period our 15 to 90-day NPL ratio increased by 40 basis points in the 15 to 90-day NPL ratio of our individuals loan portfolio, which is returning to its pre-pandemic levels, mainly due to higher delinquency rates, and increased by 20 basis points in respect of our companies loan portfolio, as of June 30, 2023 compared to June 30, 2022.

The chart below shows a comparison of both NPL ratios for each quarter as of June 30, 2022, through June 30, 2023:

| 9 |

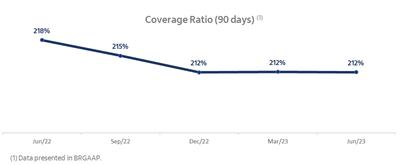

Coverage ratio (90 days): We calculate our coverage ratio as provisions for expected losses to 90-day non-performing loans. As of June 30, 2023, our coverage ratio in accordance with accounting practices adopted in Brazil applicable to institutions authorized to operate by the Central Bank, or BRGAAP, was 212% compared to a ratio of 218% as of June 30, 2022. This decrease was mainly due to an increase in 90-day NPL, concentrated in the individuals segment in Brazil and driven by the growth of our loan portfolio, especially in the Retail Business segment.

The chart below shows a comparison in the coverage ratios for each quarter as of June 30, 2022, through June 30, 2023:

Other Operating Income (Expenses) increased by 8.7% to an expense of R$41,000 million for the six-month period ended June 30, 2023, from an expense of R$37,722 million for the same period of 2022. This increase was mainly due to the R$3,069 million, or 9.2%, increase in our general and administrative expenses for the six-month period ended June 30, 2023. This increase was due to: (i) the effects of our annual collective wage agreement; (ii) the increase in profit sharing expenses; (iii) higher expenses with data processing and telecommunications; and (iv) higher expenses with depreciation and amortization.

Please see “Note 23 – General and Administrative Expenses” to our audited interim consolidated financial statements for further details.

Current and deferred income and social contribution taxes amounted to an expense of R$2,681 million for the six-month period ended June 30, 2023, from an expense of R$4,492 million in the six-month period ended June 30, 2022, mainly driven by the increase in the average annualized long-term interest rate, or TJLP, from 6.45% in the six-month period ended June 30, 2022 to 7.325% in the same period of 2023.

Please see “Note 24 – Taxes” to our audited interim consolidated financial statements for further details.

Basis for Presentation of Segment Information

| 10 |

We maintain segment information based on reports used by senior management to assess the financial performance of our businesses and to make decisions regarding the allocation of funds for investment and other purposes.

Segment information is not prepared in accordance with IFRS issued by the IASB but based on BRGAAP. It also includes the following adjustments: (i) the recognition of the impact of capital allocation using a proprietary model; (ii) the use of funding and cost of capital at market prices, using certain managerial criteria; (iii) the exclusion or inclusion of extraordinary items from our results; and (iv) managerial adjustments and reclassifications applied to allow us to review our business analyses from the management point of view.

Extraordinary items correspond to relevant events (with a positive or negative accounting effect) identified in our results of operations for each relevant period. We apply a historically consistent methodology (approved by our governance procedures) pursuant to which relevant events are either not related to our core operations or are related to previous fiscal years. The provisions for restructuring are extraordinary items and, as such, do not impact the results and analysis regarding our segment information below.

For more information on our segments, see “Item 4. Information on the Company” in our 2022 Form 20-F and “Note 30 – Segment Information” to our audited interim consolidated financial statements.

The table below sets forth the summarized results from our operating segments for the six-month period ended June 30, 2023:

| Summarized Consolidated Statement of Income from January 1, 2023 to June 30, 2023(1) |

Retail Business (a) |

Wholesale Business (b) |

Activities with the Market + Corporation (c) |

Total (a)+(b)+(c) |

Adjustments | IFRS consolidated(2) |

| (In millions of R$) | ||||||

| Operating revenues | 47,644 | 26,466 | 2,167 | 76,277 | (104) | 76,173 |

| Cost of Credit | (16,462) | (2,067) | - | (18,529) | 2,500 | (16,029) |

| Claims | (761) | (7) | - | (768) | 768 | - |

| Other operating income (expenses) | (22,102) | (9,983) | (779) | (32,864) | (8,136) | (41,000) |

| Income tax and social contribution | (2,004) | (4,247) | (306) | (6,557) | 3,876 | (2,681) |

| Non-controlling interest in subsidiaries | (19) | (370) | 7 | (382) | (107) | (489) |

| Net income | 6,296 | 9,792 | 1,089 | 17,177 | (1,203) | 15,974 |

| (1) The first three columns are our business segments. Additional information about each of our business segments can be found below under the headings "(a) Retail Business", "(b) Wholesale Business" and "(c) Activities with the Market + Corporation". The adjustments column includes the following pro forma adjustments: (i) the recognition of the impact of capital allocation using a proprietary model; (ii) the use of funding and cost of capital at market prices, using certain managerial criteria; (iii) the exclusion of non-recurring events from our results; and (iv) the reclassification of the tax effects from hedging transactions we enter into for our investments abroad. The IFRS consolidated column is the total result of our three segments plus adjustments. (2) The IFRS Consolidated figures do not represent the sum of the parties because there are intercompany transactions that were eliminated only in the consolidated statements. Segments are assessed by top management, net of income and expenses between related parties. | ||||||

The following discussion should be read in conjunction with our audited interim consolidated financial statements, especially “Note 30 – Segment Information.” The adjustments column shown in this note shows the effects of the differences between the segmented results (substantially in accordance with BRGAAP) and those calculated according to the principles adopted in our audited interim consolidated financial statements in IFRS as issued by the IASB.

Six-month period ended June 30, 2023, compared to the six-month period ended June 30, 2022:

| (a) | Retail Business |

This segment consists of business with retail customers, account holders and non-account holders, individuals and legal entities, high income clients (Itaú Uniclass and Personnalité) and the companies’ segment (microenterprises and small companies). It includes financing and credit assignments made outside the branch network, in addition to credit cards and payroll loans.

| 11 |

The following table sets forth our summarized consolidated statement of income with respect to our Retail Business segment for the six-month periods ended June 30, 2023, and 2022:

| Summarized Consolidated Statement of Income - Retail Business | For the six-month period ended June 30, | Variation | ||

| 2023 | 2022 | R$ million | % | |

| (In millions of R$) | ||||

| Operating revenues | 47,644 | 43,550 | 4,094 | 9.4 |

| Interest margin | 29,315 | 26,184 | 3,131 | 12.0 |

| Non-interest income (1) | 18,329 | 17,366 | 963 | 5.5 |

| Cost of credit and claims | (17,223) | (14,644) | (2,579) | 17.6 |

| Other operating income (expenses) | (22,102) | (21,060) | (1,042) | 4.9 |

| Income tax and social contribution | (2,004) | (2,416) | 412 | (17.0) |

| Non-controlling interest in subsidiaries | (19) | (31) | 12 | (38.7) |

| Net income | 6,296 | 5,399 | 897 | 16.6 |

| (1) Non-interest income include: commissions and banking fees; income from insurance and private pension operations before claim and selling expenses and other revenues. | ||||

Net income from our Retail Business segment increased by 16.6%, to R$6,296 million for the six-month period ended June 30, 2023, from R$5,399 million for the same period of 2022. These results are explained as follows:

Operating revenues: increased by R$4,094 million for the six-month period ended June 30, 2023, compared to the same period of 2022, due to an increase of 12.0% in interest margin, as a result of the increase in the Mix of Credit Products. Moreover, non-interest income increased by 5.5% in the six-month period ended June 30, 2023, compared to the same period of 2022, driven by the increase in commissions and fees, as a result of the increase in acquiring revenues, due to the higher transaction volume from credit cards and higher gains from “flex” products offered as part of our merchant services (advance payment of card receivables by the acquirer), and of the increase in card-issuing activities due to higher gains from interchange fees, driven by the increase in the transaction volume related to credit cards. Revenues from insurance also increased, driven by the increase in earned premiums.

Cost of credit and claims increased by R$2,579 million for the six-month period ended June 30, 2023, compared to the same period of 2022, due to an increase in provisions for loan losses, driven by the increased origination in consumer credit and unsecured credit products, the portfolio growth, and the increased in volume of renegotiations.

Other operating income (expenses) increased by R$1,042 million for the six-month period ended June 30, 2023, compared to the same period of 2022, mainly due to (i) higher personnel expenses, as a result of our annual collective wage agreement and the higher profit sharing expenses; and (ii) higher administrative expenses, due to the increase in expenses with data processing and telecommunications, and depreciation and amortization.

Income tax and social contribution for the Retail Business segment, as well as for the Wholesale Business segment and Activities with the Market + Corporation segment, is calculated by adopting the full income tax rate, net of the tax effect of any payment of interest on capital. The difference between the income tax amount determined for each business segment and the effective income tax amount, as stated in our audited interim consolidated financial statements, is recorded under the Activities with the Market + Corporation segment. As discussed above under “Net income attributable to owners of the parent company - Current and deferred income and social contribution taxes,” our current and deferred income and social contribution taxes decreased mainly as a result of a decrease in income before tax and social contribution.

| 12 |

(b) Wholesale Business

This business segment consists of products and services offered to middle-market companies, high net worth clients (Private Banking), and the operation of Latin American units and Itaú BBA, which is the unit responsible for business with large companies and investment banking operations.

The following table sets forth our summarized consolidated statement of income with respect to our Wholesale Business segment for the six-month periods ended June 30, 2023, and 2022:

| Summarized Consolidated Statement of Income - Wholesale Business | For the six-month period ended June 30, |

Variation | ||

| 2023 | 2022 | R$ million | % | |

| (In millions of R$) | ||||

| Operating revenues | 26,466 | 23,072 | 3,394 | 14.7 |

| Interest margin | 19,418 | 15,756 | 3,662 | 23.2 |

| Non-interest income (1) | 7,048 | 7,316 | (268) | (3.7) |

| Cost of credit and claims | (2,074) | (584) | (1,489) | 254.8 |

| Other operating income (expenses) | (9,983) | (9,192) | (791) | 8.6 |

| Income tax and social contribution | (4,247) | (4,398) | 152 | (3.5) |

| Non-controlling interest in subsidiaries | (370) | (502) | 133 | (26.5) |

| Net income | 9,792 | 8,396 | 1,396 | 16.6 |

| (1) Non-interest income include: commissions and banking fees; income from insurance and private pension operations before claim and selling expenses and other revenues. | ||||

Net income from the Wholesale Business segment increased by 16.6%, to R$9,792 million for the six-month period ended June 30, 2023 from R$8,396 million for the same period of 2022. These results are explained as follows:

Operating revenues: increased by R$3,394 million, or 14.7%, for the six-month period ended June 30, 2023 compared to the same period of 2022, due to an increase of 23.2% in the interest margin, driven by the higher margin of liabilities recorded during the period and the higher result from structured operations. The 3.7% decrease in non-interest income was driven by lower volumes of economic advisory and brokerage services. As of June 30, 2023, we participated in 89 local operations, which included debentures and promissory notes issuance, as well as securitization transactions, totaling R$22.1 billion, ranking first in volume and in number of operations pursuant to a ranking published by the Brazilian Financial and Capital Markets Association (Associação Brasileira das Entidades dos Mercados Financeiro e de Capitais, or ANBIMA). In the equity markets, we ranked first in number of operations, participating in seventeen operations (including Block Trades), and second in volume with R$4.7 billion, both in Dealogic´s ranking, as of June 30, 2023. We also provided financial advisory services for fifteen M&A transactions in Brazil, totaling R$14.8 billion. As of June 30, 2023, we were ranked second place in number of M&A deals and fourth place in volume in Dealogic’s ranking.

Cost of credit and claims increased by R$1,489 million for the six-month period ended June 30, 2023 compared to the same period of 2022, due to the normalization in the provision for loan losses in the Wholesale Business segment in Brazil.

| 13 |

Other operating income (expenses) decreased by R$791 million for the six-month period ended June 30, 2023, compared to the same period of 2022, mainly due to the higher personnel expenses as a result of the effects of the annual collective wage agreement, and the increase in administrative expenses due to higher expenses with data processing and telecommunications, and depreciation and amortization.

Income tax and social contribution for this business segment, as well as for the Retail Business and Activities with the Market + Corporation segments, is calculated by adopting the full income tax rate, net of the tax effect of any payment of interest on capital. The difference between the income tax amount determined for each segment and the effective income tax amount, as stated in our audited interim consolidated financial statements, is recorded under the Activities with the Market + Corporation segment. As discussed above, our current and deferred income and social contribution taxes increased mainly due to an increase in income before tax and social contribution.

(c) Activities with the Market + Corporation

This segment consists of results from capital surplus, subordinated debt surplus and the net balance of tax credits and debits. It also includes the financial margin on market trading, treasury operating costs, and equity in earnings of companies not included in either of the other segments.

The following table sets forth our summarized consolidated statement of income with respect to our Activities with the Market + Corporation segment for the six-month periods ended June 30, 2023, and 2022:

| Summarized Consolidated Statement of Income - Activities with the Market + Corporation | For the six-month period ended June 30, | Variation | ||

| 2023 | 2022 | R$ million | % | |

| (In millions of R$) | ||||

| Operating revenues | 2,167 | 1,662 | 505 | 30.4 |

| Interest margin | 1,957 | 1,745 | 213 | 12.2 |

| Non-interest income (1) | 210 | (83) | 294 | (353.1) |

| Other operating income (expenses) | (779) | (103) | (676) | 655.6 |

| Income tax and social contribution | (306) | (175) | (131) | 74.8 |

| Non-controlling interest in subsidiaries | 7 | (140) | 147 | (105.1) |

| Net income | 1,089 | 1,244 | (155) | (12.5) |

| (1) Non-interest income include: commissions and banking fees; income from insurance and private pension operations before claim and selling expenses and other revenues. | ||||

Net income from the Activities with the Market + Corporation segment decreased by R$155 million, or 12.5%, for the six-month period ended June 30, 2023, compared to the same period of 2022. We recorded an increase of R$676 million in other operating income (expenses), due to the tax benefit received in the six-month period ended June 30, 2022. This effect offsets the increase of R$505 million in operating revenues.

Income tax and social contribution for this segment, as well as for the Retail Business and Wholesale Business segments, is calculated by adopting the full income tax rate, net of the tax effect of any payment of interest on capital. The difference between the income tax amount determined for each segment and the effective income tax amount, as stated in our audited interim consolidated financial statements, is recorded under the Activities with the Market + Corporation segment. As discussed above, our current and deferred income and social contribution taxes decreased mainly due to a decrease in income before tax and social contribution.

| 14 |

Balance Sheet

The table below sets forth our summarized balance sheet as of June 30, 2023 and December 31, 2022. Please see our audited interim consolidated financial statements for further details about our Consolidated Balance Sheet.

| Summarized Balance Sheet - Assets | As of | Variation | ||||

| June 30, 2023 | December 31, 2022 | R$ million | % | |||

| (In millions of R$) | ||||||

| Cash | 30,636 | 35,381 | (4,745) | (13.4) | ||

| Financial assets at amortized cost | 1,606,250 | 1,578,789 | 27,461 | 1.7 | ||

| Compulsory deposits in the Central Bank of Brazil | 136,749 | 115,748 | 21,001 | 18.1 | ||

| Interbank deposits, securities purchased under agreements to resell and securities at amortized cost | 506,296 | 494,397 | 11,899 | 2.4 | ||

| Loan and lease operations portfolio | 901,185 | 909,422 | (8,237) | (0.9) | ||

| Other financial assets | 113,957 | 109,909 | 4,048 | 3.7 | ||

| (-) Provision for Expected Loss | (51,937) | (50,687) | (1,250) | 2.5 | ||

| Financial assets at fair value through other comprehensive income | 134,347 | 126,748 | 7,599 | 6.0 | ||

| Financial assets at fair value through profit or loss | 541,074 | 464,682 | 76,392 | 16.4 | ||

| Insurance contracts, Investments in associates and join ventures, Fixed assets, Goodwill and Intangible assets and other assets | 59,544 | 55,821 | 3,723 | 6.7 | ||

| Tax assets | 62,357 | 59,645 | 2,712 | 4.5 | ||

| Total assets | 2,434,208 | 2,321,066 | 113,142 | 4.9 | ||

June 30, 2023, compared to December 31, 2022.

Total assets increased by R$113,142 million, as of June 30, 2023, compared to December 31, 2022, mainly due to an increase in financial assets at fair value through profit or loss and in financial assets at amortized cost. This result is further described below:

Financial assets at amortized cost increased by R$27,461 million, or 1.7%, as of June 30, 2023, compared to December 31, 2022, mainly due to an increase in compulsory deposits in the Central Bank of Brazil, interbank deposits, securities purchased under agreements to resell and securities at amortized cost, and other financial assets.

Interbank deposits, securities purchased under agreements to resell, securities at amortized cost increased by R$11,899 million, or 2.4%, as of June 30, 2023 compared to December 31, 2022, mainly due to an increase of R$22,985 million in securities, mainly in corporate securities, especially in rural product notes (Cédula do Produtor Rural) and debentures, partially offset by decreases of: (i) R$8,237 in loan and lease operations, mainly in foreign loans due to the exchange variation; and (ii) R$4,820 in securities purchased under agreements to resell.

Please see “Note 4 - Interbank Deposits and Securities Purchased Under Agreements to Resell”, “Note 9 - Financial assets at amortized cost – Securities”, and “Note 10 – Loan and lease operations” to our audited interim consolidated financial statements for further details.

Loan and lease operations portfolio decreased by R$8,237 million, or 0.9%, as of June 30, 2023, compared to December 31, 2022, mainly due to the decreases of R$6,467 million in foreign loans – Latin America, due to the impact of exchange variation; and R$5,251 million in our corporate portfolio. The increase of R$6,845 million in our individuals loan portfolio, was due to increases of R$5,657 million in mortgage loans; and R$5,236 million in personal loans; which were partially offset by the seasonal decrease of R$6,452 million in credit cards as holders tend to use their cards less in the first quarter.

| 15 |

| Loan and Lease Operations, by asset type | As of | Variation | ||

| June 30, 2023 | December 31, 2022 | R$ million | % | |

| (In millions of R$) | ||||

| Individuals | 406,948 | 400,103 | 6,845 | 1.7 |

| Credit card | 129,403 | 135,855 | (6,452) | (4.7) |

| Personal loan | 59,181 | 53,945 | 5,236 | 9.7 |

| Payroll loans | 75,203 | 73,633 | 1,570 | 2.1 |

| Vehicles | 32,440 | 31,606 | 834 | 2.6 |

| Mortgage loans | 110,721 | 105,064 | 5,657 | 5.4 |

| Corporate | 134,017 | 139,268 | (5,251) | (3.8) |

| Micro/Small and Medium Businesses | 161,532 | 164,896 | (3,364) | (2.0) |

| Foreign Loans Latin America | 198,688 | 205,155 | (6,467) | (3.2) |

| Total Loan operations and lease operations portfolio | 901,185 | 909,422 | (8,237) | (0.9) |

Please see “Note 10 – Loan and Lease Operations” to our audited interim consolidated financial statements for further details.

The table below sets forth our summarized balance sheet – liabilities and stockholders’ equity as of June 30, 2023 and December 31, 2022. Please see our audited interim consolidated financial statements for further details about our Consolidated Balance Sheet.

| Summarized Balance Sheet - Liabilities and Stockholders' Equity | As of | Variation | ||||

| June 30, 2023 | December 31, 2022 | R$ million | % | |||

| (In millions of R$) | ||||||

| Financial Liabilities | 1,912,522 | 1,836,690 | 75,832 | 4.1 | ||

| At Amortized Cost | 1,840,419 | 1,755,498 | 84,921 | 4.8 | ||

| Deposits | 923,281 | 871,438 | 51,843 | 5.9 | ||

| Securities sold under repurchase agreements | 319,099 | 293,440 | 25,659 | 8.7 | ||

| Interbank market funds, Institutional market funds and other financial liabilities | 598,039 | 590,620 | 7,419 | 1.3 | ||

| At Fair Value Through Profit or Loss | 68,231 | 77,508 | (9,277) | (12.0) | ||

| Provision for Expected Loss | 3,872 | 3,684 | 188 | 5.1 | ||

| Insurance contracts and private pension | 249,769 | 233,126 | 16,643 | 7.1 | ||

| Provisions | 20,140 | 19,475 | 665 | 3.4 | ||

| Tax liabilities | 7,360 | 6,773 | 587 | 8.7 | ||

| Other liabilities | 55,476 | 47,895 | 7,581 | 15.8 | ||

| Total liabilities | 2,245,267 | 2,143,959 | 101,308 | 4.7 | ||

| Total stockholders’ equity attributed to the owners of the parent company | 178,853 | 167,717 | 11,136 | 6.6 | ||

| Non-controlling interests | 10,088 | 9,390 | 698 | 7.4 | ||

| Total stockholders’ equity | 188,941 | 177,107 | 11,834 | 6.7 | ||

| Total liabilities and stockholders' equity | 2,434,208 | 2,321,066 | 113,142 | 4.9 | ||

Total liabilities and stockholders’ equity increased by R$113,142 million, as of June 30, 2023, compared to December 31, 2022, mainly due to an increase in financial liabilities at amortized cost. These results are detailed as follows:

Deposits increased by R$51,843 million, or 5.9%, as of June 30, 2023, compared to December 31, 2022, mainly due to an increase of R$56,008 million in time deposits, due to the commercial strategy to focus on this product in the Retail Business segment and higher demand for fixed income products.

| 16 |

Please see “Note 15 – Deposits” to our audited interim consolidated financial statements for further details.

Securities sold under repurchase agreements increased by R$25,659 million, or 8.7%, as of June 30, 2023 compared to December 31, 2022, mainly due to an increase of R$49,063 million in government securities, partially offset by a decrease of R$22,622 million in assets received as collateral.

Please see “Note 17 – Securities Sold Under Repurchase Agreements and Interbank and Institutional Market Funds” to our audited interim consolidated financial statements for further details.

Interbank market funds, institutional market funds and other financial liabilities increased by R$7,419 million, or 1.3%, as of June 30, 2023 compared to December 31, 2022, mainly due to an increase of R$23,795 million in interbank market funds, offset by decreases of R$10,693 million in institutional market funds and R$5,683 million in other financial liabilities.

Please see “Note 17 – Securities Sold Under Repurchase Agreements and Interbank and Institutional Market Funds” and “Note 18 – Other assets and liabilities” to our audited interim consolidated financial statements for further details.

Insurance contracts and private pension increased by R$16,643 million, or 7.1%, as of June 30, 2023 compared to December 31, 2022, mainly due to the update of standard private pension contracts known as PGBL and VGBL.

Capital Management

Capital Adequacy

Through our Internal Capital Adequacy Assessment Process, or ICAAP, we assess the adequacy of our capital to face the risks to which we are subject. For ICAAP, capital is composed of regulatory capital for credit, market and operational risks, and by the necessary capital to cover other risks.

In order to ensure our capital soundness and availability to support business growth, we maintain capital levels above the minimum requirements, according to the Common Equity Tier I, Additional Tier I Capital, and Tier II minimum ratios.

Our Total Capital, Tier I Capital and Common Equity Tier I Capital ratios are calculated on a consolidated basis, applied to institutions included in our Prudential Conglomerate which comprises not only financial institutions but also consortium administrators (administradoras de consórcio), payment institutions, factoring companies or companies that directly or indirectly assume credit risk, and investment funds in which our Itaú Unibanco Group retains substantially all risks and rewards.

| 17 |

| As of June 30, | As of December 31, | |

| 2023 | 2022 | |

| (In R$ million, except percentages) | ||

| Available capital (amounts) | ||

| Common Equity Tier I (CET I) | 155,372 | 147,781 |

| Tier I | 173,670 | 166,868 |

| Total capital | 192,828 | 185,415 |

| Risk-weighted assets (amounts) | ||

| Total risk-weighted assets (RWA) | 1,274,840 | 1,238,582 |

| Risk-based capital ratios as a percentage of RWA | ||

| Common Equity Tier I ratio (%) | 12.20% | 11.90% |

| Tier I ratio (%) | 13.60% | 13.50% |

| Total capital ratio (%) | 15.10% | 15.00% |

| Additional CET I buffer requirements as a percentage of RWA | ||

| Capital conservation buffer requirement (%) | 2.50% | 2.50% |

| Countercyclical buffer requirement (%) (1) | 0.00% | 0.00% |

| Bank G-SIB and/or D-SIB additional requirements (%) | 1.00% | 1.00% |

| Total of bank CET I specific buffer requirements (%) | 3.50% | 3.50% |

| (1) The countercyclical capital buffer is fixed by the Financial Stability Committee and currently is set to zero. | ||

As of June 30, 2023, our Total Capital reached R$192,828 million, an increase of R$7,413 million compared to December 31, 2022. Our Basel Ratio (calculated as the ratio between our Total Capital and the total amount of Risk Weighted Assets, or RWA) reached 15.1%, an increase of 10 basis points due to the result of the period and prudential and equity adjustments, partially offset by the increase of Risk-Weighted Assets.

Additionally, the Fixed Asset Ratio (Índice de Imobilização) indicates the level of total capital committed to adjusted permanent assets. Itaú Unibanco Holding is within the maximum limit of 50% of total adjusted capital, as established by the Central Bank. On June 30, 2023, our Fixed Asset Ratio reached 20%, which represents a buffer of R$57,779 million.

| Three-month period ended, | ||

| Liquidity Coverage Ratio | June 30, 2023 | December 31,2022 |

| Total Weighted Value (average) | ||

| (In millions of R$) | ||

| Total High Liquidity Assets (HQLA)1 | 355,222 | 325,269 |

| Cash Outflows2 | 368,049 | 361,902 |

| Cash Inflows3 | 170,357 | 164,104 |

| Total Net Cash Outflows | 197,692 | 197,798 |

| LCR% | 179.7% | 164.4% |

| (1) High Quality Liquidity Assets correspond to inventories, in some cases weighted by a discount factor, of assets that remain liquid in the market even in periods of stress, that can easily be converted into cash and that are classified as low risk. | ||

| (2) Outflows — total potential cash outflows for a 30-day horizon, calculated for a standard stress scenario as defined by BACEN Circular 3,749. | ||

| (3) Inflows — total potential cash inflows for a 30-day horizon, calculated for a standard stress scenario as defined by BACEN Circular 3,749. | ||

Our Tier I ratio reached 13.6%, as of June 30, 2023, an increase of 10 basis points compared to March 31, 2023, due to the result of the period, partially offset by the increase in Risk-Weighted Assets. Considering the regulatory changes, the Tier I Capital ratio Pro Forma would have reached 14.7%.

Please see “Note 32 – Risk and Capital Management” of our audited interim consolidated financial statements for further details about regulatory capital.

Liquidity Ratios

The Basel III Framework introduced global liquidity standards, providing for minimum liquidity requirements and aims to ensure that banks can rely on their own sources of liquidity, leaving central banks as a lender of last resort. Basel III provides for two liquidity ratios to ensure that financial institutions have sufficient liquidity to meet their short-term and long-term obligations: (i) the liquidity coverage ratio, or LCR, and (ii) the net stable funding ratio, or NSFR.

| 18 |

We believe that the LCR and NSFR provide more relevant information than an analysis of summarized cash flows.

We present below a discussion of our LCR for the average of the three-month period ended on June 30, 2023, and NSFR as of June 30, 2023.

Liquidity Coverage Ratio

The LCR measures the short-term resistance of a bank’s liquidity risk profile. It is the ratio of the stock of high-quality liquid assets to expected net cash outflows over the next 30 days, assuming a scenario of idiosyncratic or systemic liquidity stress.

We calculate our LCR according to the methodology established in Central Bank Circular No. 3,749/2015. We measure our total high liquidity assets for the end of each period to cash outflows and inflows as the daily average value for each period. Pursuant to Central Bank regulations, effective as of January 1, 2019, the minimum LCR is 100%.

| Three-month period ended, | ||

| Liquidity Coverage Ratio | June 30, 2023 | December 31,2022 |

| Total Weighted Value (average) | ||

| (In millions of R$) | ||

| Total High Liquidity Assets (HQLA)1 | 355,222 | 325,269 |

| Cash Outflows2 | 368,049 | 361,902 |

| Cash Inflows3 | 170,357 | 164,104 |

| Total Net Cash Outflows | 197,692 | 197,798 |

| LCR% | 179.7% | 164.4% |

| (1) High Quality Liquidity Assets correspond to inventories, in some cases weighted by a discount factor, of assets that remain liquid in the market even in periods of stress, that can easily be converted into cash and that are classified as low risk. | ||

| (2) Outflows — total potential cash outflows for a 30-day horizon, calculated for a standard stress scenario as defined by BACEN Circular 3,749. | ||

| (3) Inflows — total potential cash inflows for a 30-day horizon, calculated for a standard stress scenario as defined by BACEN Circular 3,749. | ||

Our average LCR as of June 30, 2023 was 179.7% and, accordingly, above Central Bank requirements.

Net Stable Funding Ratio

The NSFR measures long-term liquidity risk. It is the ratio of available stable funding to required stable funding over a one-year time period, assuming a stressed scenario.

We calculate our NSFR according to the methodology established in Central Bank Circular No. 3,869/2017. The NSFR corresponds to the ratio of our available stable funds for the end of each period (recursos estáveis disponíveis, or ASF) to our required stable funds for the end of each period (recursos estáveis requeridos, or RSF).

Pursuant to Central Bank regulations, effective as of October 1, 2018, the minimum NSFR is 100%.

| 19 |

| As of June 30, | As of December 31, | |

| Net Stable Funding Ratio | 2023 | 2022 |

| Total Ajusted Value | ||

| (In millions of R$) | ||

| Total Available Stable Funding (ASF)¹ | 1,216,666 | 1,151,750 |

| Total Required Stable Funding (RSF)² | 951,168 | 922,395 |

| NSFR (%) | 127.9% | 124.9% |

| (1) ASF – Available Stable Funding – refers to liabilities and equity weighted by a discount factor according to their stability, pursuant to Central Bank Circular 3,869/2017. | ||

| (2) RSF – Required Stable Funding – refers to assets and off-balance exposures weighted by a discount factor to their necessity, pursuant to Central Bank Circular 3,869/2017. | ||

As of June 30, 2023, our ASF totaled R$1,216.7 billion, mainly due to capital and Retail Business and Wholesale Business funding, and our RSF totaled R$951.2 billion, particularly due to loans and financings with Wholesale Business and Retail Business customers, central governments and transactions with central banks.

As of June 30, 2023, our NSFR was 127.9% and, accordingly, above Central Bank requirements.

Liquidity and Capital Resources

We define our consolidated group operational liquidity reserve as the total amount of assets that can be rapidly turned into cash, based on local market practices and legal restrictions. The operational liquidity reserve generally includes: (i) cash and deposits on demand, (ii) funded positions of securities purchased under agreements to resell and (iii) unencumbered government securities.

The following table presents our operational liquidity reserve as of June 30, 2023 and 2022:

| Operational Liquidity Reserve | As of June 30, | 2023 Average Balance(1) | |

| 2023 | 2022 | ||

| (In millions of R$) | |||

| Cash | 30,636 | 33,839 | 33,653 |

| Securities purchased under agreements to resell – Funded position (2) | 58,798 | 57,892 | 55,148 |

| Unencumbered government securities (3) | 199,180 | 157,054 | 182,816 |

| Operational reserve | 288,614 | 248,785 | 271,617 |

| (1) Average calculated based on audited interim financial statements. | |||

| (2) Net of R$ 7.915 (R$ 4.768 at 06/30/2022), which securities are restricted to guarantee transactions at B3 S.A.—Brasil, Bolsa Balcão (B3) and the Central Bank. | |||

| (3) Present values are included as a result of the change in the reporting of future flows of assets that are now reported as future value as of September 2016. | |||

Our main sources of funding are interest-bearing deposits, deposits received under repurchase agreements, on lending from government financial institutions, lines of credit with foreign banks and the issuance of securities abroad.

Please see “Note 15 – Deposits” to our audited interim consolidated financial statements for further details about funding.

Capital Expenditures

In accordance with our practice in the last few years, our capital expenditures in the six-month period ended June 30, 2023, were funded with internal resources. We cannot provide assurance that we will make capital expenditures in the future and, if made, that the amounts will correspond to the current estimates. The table below presents our capital expenditures for the six-month period ended June 30, 2023, and for the year ended December 31, 2022:

| 20 |

| Six-month period ended | For the year ended | |

| Capital Expenditures | June 30, 2023 | December 31, 2022 |

| (In millions of R$, except percentages) | ||

| Fixed Assets | 973 | 2,727 |

| Fixed assets under construction | 457 | 905 |

| Land and buildings | 0 | 8 |

| Improvements | 39 | 56 |

| Installations, furniture and data processing equipment | 454 | 1,710 |

| Other | 23 | 48 |

| Intangible Assets | 2,999 | 5,768 |

| Goodwill | 603 | 0 |

| Software acquired or internally developed | 2,124 | 4,727 |

| Other intangibles | 272 | 1,041 |

| Total | 3,972 | 8,495 |

Please see “Note 13 – Fixed Assets” and “Note 14 – Goodwill and Intangible Assets” to our audited interim consolidated financial statements for details about our capital expenditures.

Capitalization

The table below presents our capitalization as of June 30, 2023. The information described is derived from our audited interim consolidated financial statements as of and for the six-month period ended June 30, 2023. As of the date of this Form 6-K, there has been no material change in our capitalization since June 30, 2023.

| 21 |

| Capitalization | For the six-month period ended June 30, 2023 | |

| R$ | US$ (1) | |

| (In millions, except percentages) | ||

| Current liabilities | ||

| Deposits | 430,808 | 89,398 |

| Securities sold under repurchase agreements | 268,430 | 55,702 |

| Structured notes | - | - |

| Derivatives | 34,728 | 7,206 |

| Interbank market funds | 155,437 | 32,255 |

| Institutional market funds | 9,829 | 2,040 |

| Other financial liabilities | 157,367 | 32,656 |

| lnsurance contracts and private pension | 462 | 96 |

| Provisions | 6,531 | 1,355 |

| Tax liabilities | 2,826 | 586 |

| Other Non-financial liabilities | 50,843 | 10,550 |

| Total | 1,117,261 | 231,845 |

| Long-term liabilities | ||

| Deposits | 492,473 | 102,194 |

| Securities sold under repurchase agreements | 50,669 | 10,514 |

| Structured notes | 86 | 18 |

| Derivatives | 32,598 | 6,764 |

| Interbank market funds | 162,945 | 33,813 |

| Institutional market funds | 108,860 | 22,590 |

| Other financial liabilities | 4,420 | 917 |

| lnsurance contracts and private pension | 249,307 | 51,734 |

| Provision for Expected Loss | 3,872 | 803 |

| Provisions | 13,609 | 2,824 |

| Tax liabilities | 4,040 | 838 |

| Other Non-financial liabilities | 4,634 | 962 |

| Total | 1,127,512 | 233,972 |

| Income tax and social contribution - deferred | 494 | 103 |

| Non-controlling interests | 10,088 | 2,093 |

| Stockholders’ equity attributed to the owners of the parent company (2) | 178,853 | 37,114 |

| Total capitalization (3) | 2,434,208 | 505,127 |

| BIS ratio (4) | 15.1% | |

| (1) Convenience translation at 4.819 reais per U.S. dollar, the exchange rate in effect on June 30, 2023. | ||

| (2) Itaú Unibanco Holding’s authorized and outstanding share capital consists of 4,958,290,359 common shares and 4,841,653,914 preferred shares, all of which are fully paid. For more information regarding our share capital see Note 19 to our audited consolidated financial statements as of and for the period ended June 30, 2023. | ||

| (3) Total capitalization corresponds to the sum of total current liabilities, long-term liabilities, deferred income, minority interest in subsidiaries and stockholders’ equity. | ||

| (4) Calculated by dividing total regulatory capital by risk weight assets. | ||

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements, other than the guarantees, financial guarantees, commitments to be released, letters of credit to be released and contractual commitments that are described in “Note 13 – Fixed assets,” “Note 14 – Goodwill and Intangible assets,” “Note 32 – Risk and Capital Management, I.I – Collateral and policies for mitigating credit risk” and “Note 32 – Risk and Capital Management – I.IV – Maximum Exposure of Financial Assets to Credit Risk” to our audited interim consolidated financial statements.

| 22 |

REGULATORY RECENT DEVELOPMENTS

We are subject to the regulation and supervision of various regulatory entities in the segments we operate. The supervision of these entities is essential to the structure of our business and directly impacts our growth strategies. Our 2022 Form 20-F contains disclosure of the regulations and supervision of various regulatory entities to which we are subject in “Item 4B. Business Overview - Supervision and Regulation.”

We describe below the material regulatory developments applicable to us that took place during the six-month period ended June 30, 2023 and through the date of this Form 6-K.

| 23 |

Central Bank regulates partnerships and outsourcing services established within PIX

On February 17, 2023, the Central Bank published Resolution No. 293, which establishes additional rules for partnerships and outsourcing arrangements established within PIX (Central Bank’s instant payments system) by market participants, which were previously defined in Central Bank Resolution No. 269, issued on December 1, 2022. Both rules amended Central Bank Resolution No. 1, which establishes the regulations for the PIX payment scheme.

Central Bank Resolution No. 269, among other amendments, introduced the definition of “partnerships” within the PIX scheme as a commercial relationship between two or more institutions directly participating in the PIX scheme and “outsourcing” as a relationship between a participating institution and a non-participating private agent. Central Bank Resolution No. 269 also explicitly prohibits PIX related outsourcing arrangements in two cases: (i) when the third party offers transactional accounts (i.e., current or payment accounts, among other types as defined by Central Bank Resolution No. 1, of 2020, which establishes the PIX regulations); and (ii) when the third party does not hold a transactional account but initiates payment transactions through an account provided by a participating institution.

The first type of outsourcing is expressly forbidden because the agent that holds a transactional account and wishes to offer PIX to its customers must necessarily be a PIX participant, going through the adhesion process, which includes the performance of software homologation tests and the evaluation of the requirements for user experience, rather than relying on another direct PIX participant to offer PIX transactions to its client-base.

Through Resolution No. 293, the Central Bank defined a transition regime for institutions that implemented the first type of restricted outsourcing arrangement, applicable to institutions with agreements in effect as of December 1, 2022, provided they submit a request to join the PIX scheme as a direct participant by May 31, 2023. With the transition regime, such agents may, exceptionally, maintain the PIX offering to their clients through an outsourcing arrangement executed with a PIX participant for the duration of the adhesion process.

Regarding the second type, the rule simply reiterates the regulatory impediment that payment initiation service providers, or PISPs, carry out their activities without the required authorization to operate from the Central Bank and mandatory participation in Open Finance.

The changes introduced by Central Bank Resolution No. 269 mentioned herein, as well as the entirety of Central Bank Resolution No. 293, entered into effect on March 1, 2023.

Central Bank improves implementation requirements to the Open Finance process

On February 27, 2023, the Central Bank published Resolution No. 294, which amended Central Bank Resolution No. 32, of October 29, 2020, and established technical requirements and operational procedures for the Open Finance implementation in Brazil. The main change introduced by the new rule is related to the scope of the monitoring function assigned to the governance structure responsible for implementing Open Finance.

The rule also improves definitions regarding the directory of Open Finance participants and the responsibility for managing their information, formally establishing the need for prior consent from the Central Bank in case of exclusion of a participating institution from the ecosystem or exclusion of a participation modality.

On the same date, the Central Bank also published Resolution No. 295, which exempts from mandatory participation in the Open Finance ecosystem institutions that (i) do not hold accounts that can be freely used by their clients through electronic channels; (ii) do not have individuals, microentrepreneurs and small companies as clients, as defined in Supplementary Law No. 123, of December 13, 2006; (iii) offer unblocked accounts (contas de livre movimentação) only to a specific and limited set of individual clients, such as their own employees, and other cases in which their participation is not able to bring customers significant benefits in the light of the objectives and principles of Open Finance; or (iv) provide their clients with access to electronic channels to operate their accounts only in contingency situations.

| 24 |

Unlike the previous criteria of exemption, which was automatic, the Open Finance participation waivers introduced by Resolution No. 295 will require prior approval by the Central Bank.

Resolutions Nos. 294 and 295 entered into effect on April 1, 2023.

Central Bank establishes guidelines for acceptance of Bank Credit Certificates as collateral for the issuance of Financial Liquidity Lines

On March 3, 2023, the Central Bank defined basic guidelines, through Central Bank Vote No. 40/2023, for the acceptance of Bank Credit Certificates (Cédulas de Crédito Bancário, or CCBs) as eligible collateral in the context of the issuance of Financial Liquidity Lines (Linhas Financeiras de Liquidez, or LFL) by the Central Bank.

The LFL were established by the Central Bank in 2021, as a structural measure to improve its operational framework for the purposes of supplying liquidity to the National Financial System, whether in response to market-wide dysfunctions or specific problems in some institutions. Currently, the only assets eligible to be offered as collateral are debentures and commercial certificates.

The definition of guidelines, approved by Central Bank Vote No. 40/2023, aims to direct and coordinate the market for the developments necessary for effective operation as of the first quarter of 2024. In summary, book-entry and notarial CCBs deposited in Central Depositaries of financial assets will be eligible as collateral for LFLs. The admissibility rules will be similar to those of the Special Temporary Liquidity Line for the Acquisition of Financial Bills Guaranteed by Financial Assets (Linha Temporária Especial de Liquidez para Aquisição de Letra Financeira com Garantia em Ativos Financeiros, or LTEL-LFG), whose criteria will be determined based on the information provided by the Credit Information System (Sistema de Informações de Crédito, or SCR). The Central Bank will also define the eligible modalities of credit and the phasing in of the production of these modalities.

The incorporation of CCBs as eligible collateral assets in the LFL is a structural measure in the LFL evolution agenda. With the evolution, the Central Bank will seek to deepen the use of the LFL to allow the structural reduction of compulsory deposits. These changes are expected to be implemented in the first quarter of 2024.

Central Bank announces guidelines for the pilot project of its digital currency, the “Real Digital,” or DREX

On March 6, 2023, the Central Bank reviewed the guidelines applicable to its proposed digital currency, the Real Digital, through Vote No. 31/2023.

Some relevant guidelines applicable to the project include (i) that tokenized assets will follow their respective regulatory regimes, so as not to generate asymmetry between the current and tokenized forms of these assets; (ii) the emphasis on the design of a distributed ledger technology, or DLT, that enables the registration of assets of various natures and the incorporation of technologies with smart contracts and programmable currency; and (iii) total adherence to the regulations concerning secrecy, data protection, and anti-money laundering.

In line with the updated guidelines, the pilot project began in March 2023, with the first tests of a platform for operations with the “Real Digital”, a collaborative environment for testing and developing of the solution.

Additionally, on April 27, 2023, the Central Bank issued Resolution No. 315, which establishes formal rules applicable to the pilot project of the “Real Digital” and institutes the Executive Management Committee of the “Real Digital” platform.

Pursuant to Resolution No. 315, the number of participants in the pilot project is limited to up to 10 institutions subject to Central Bank supervision, such as us, selected according to criteria and procedures set forth in the regulation. The Executive Committee received proposals from entities interested in participating in the pilot project. The rule also provides that the Executive Committee of the pilot project could expand the list of selected participants to up to 20 candidates, if necessary. Institutions authorized to operate by the Central Bank that necessarily have the capacity to test, based on their corresponding business model, transactions involving the issuance, redemption or transfer of financial assets, as well as executing the simulation of financial flows resulting from trading events, when applicable to financial assets subject to the test, were allowed to participate in the pilot project. On May 24, 2023, the regulator disclosed a list of 14 selected participants, which included us. Adhesion will be formalized through the execution of a Term of Participation and the submission of a proposal to the Central Bank. The Central Bank will begin incorporating participants into the Real Digital Pilot platform by mid-June 2023.

| 25 |

Resolution No. 315 also establishes that, during the conduction of the pilot project, a forum will be created for the exchange of information and adequate orientation of the expectations in relation to the development of the “Real Digital” platform and the proposed tests.

Central Bank Resolution No. 315 entered into effect on April 28, 2023.

Additionally, on August 7, 2023, the Central Bank announced “DREX” as the official name of its digital currency.

Central Bank approves changes in the local rules applicable internal ratings-based approach for credit risks established in Basel III

On March 16, 2023, the Central Bank issued Resolution No. 303, which provides for changes in the calculation of the capital requirement related to credit risk exposures calculated through the internal ratings-based, or IRB, approach (RWACIRB). This new rule is in accordance with the best practice recommendations of the Basel Committee on Banking Supervision, or BCBS, inserted in the set of recommendations known as "Basel III" and will replace Central Bank Circular No. 3,648, issued on March 4, 2013.

The Central Bank expects that the new framework of IRB approaches will be more robust and limit the variability of the capital requirement among the institutions that eventually adopt them. To this end, Resolution No. 303 introduces limits for some parameters, reduces the set of portfolios eligible to the IRB approaches and introduces several improvements to the applicable prudential regulation, including flexibility in the application process for the use of the IRB approaches, which now allows partial adoption by the institution, for specific portfolios.

The rule is applicable to financial institutions classified in segments S1, such as us, and S2, according to classifications issued by the Central Bank for the purposes of the proportional application of prudential regulation according to systemic risk. Currently, none of the institutions included in these segments, including us, uses IRB approaches, whose adoption is optional and subject to prior approval by the Central Bank.

Resolution No. 303 entered into effect on July 1, 2023.

Central Bank introduces changes to the Pillar 3 Report

On March 23, 2023, the Central Bank issued Resolution No. 306, in order to alter several prudential rules to include in their scope of application regulatory conglomerates (conglomerados prudenciais) led by payment institutions.

Among such adjustments, this rule also updated Central Bank Resolution No. 54, issued on December 16, 2020, which establishes the disclosure of Pillar 3 report and is applicable to regulatory conglomerates led by financial institutions, such as ours.

Among other changes, two new topic sections were included in the Pillar 3 report. The first deals with the comparison between the RWA, amounts calculated through the standard approach and through the IRB approaches, and the second with the disclosure of information related to assets subject to any impediment or restriction of negotiation due to a legal, regulatory, statutory or contractual aspect.

Resolution No. 306 entered into effect on July 1, 2023.

Central Bank issues regulations on the registration and centralized deposit of real estate receivables

On March 28, 2023, the Central Bank issued Resolution No. 308, which regulates the activities of registration and centralized deposit of real estate receivables associated with real estate projects.

| 26 |

The intention is to enable, at the discretion of the market participants, the use of the services provided by the registering entities and central depositaries and the structure of the systems managed by these institutions improve the management process of real estate receivables and the broader and more transparent access to the receivables agendas by potential financiers, which could contribute to the access to better credit conditions for developers and subdivision owners.