EX-99.2

Exhibit 99.2

Index to the Management’s Discussion and Analysis

|

|

|

|

|

| EXECUTIVE SUMMARY |

|

|

2 |

|

|

|

| CORE BUSINESS AND STRATEGY |

|

|

4 |

|

| Core Business |

|

|

4 |

|

| Business Objective |

|

|

4 |

|

| Strategy |

|

|

5 |

|

|

|

| KEY PERFORMANCE DRIVERS AND CAPABILITIES |

|

|

11 |

|

| Key External Drivers |

|

|

11 |

|

| Key Internal Drivers |

|

|

13 |

|

|

|

| RESULTS |

|

|

20 |

|

| Overall Annual Performance |

|

|

20 |

|

| Selected Annual Information |

|

|

21 |

|

| Results Compared to 2016 Targets |

|

|

23 |

|

| Acquisitions |

|

|

24 |

|

| Discussion of Operations |

|

|

25 |

|

| Fourth Quarter Results |

|

|

40 |

|

| Quarterly Trends |

|

|

44 |

|

| Statements of Financial Position |

|

|

46 |

|

| Liquidity and Capital Resources |

|

|

48 |

|

| Other |

|

|

54 |

|

|

|

| OUTLOOK |

|

|

58 |

|

|

|

| CRITICAL ACCOUNTING ESTIMATES, DEVELOPMENTS, AND MEASURES |

|

|

63 |

|

| Critical Accounting Estimates |

|

|

63 |

|

| Accounting Developments |

|

|

64 |

|

| Materiality |

|

|

64 |

|

| Definition of Non-IFRS Measures |

|

|

65 |

|

|

|

| RISK FACTORS |

|

|

68 |

|

|

|

| CONTROLS AND PROCEDURES |

|

|

78 |

|

|

|

| CORPORATE GOVERNANCE |

|

|

78 |

|

|

|

| SUBSEQUENT EVENTS |

|

|

80 |

|

|

|

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS |

|

|

80 |

|

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-1 |

|

Stantec Inc. |

Management’s Discussion and Analysis

FEBRUARY 22, 2017

This discussion and analysis of Stantec Inc.’s (Stantec or the Company) operations, financial position, and cash flows for the year ended

December 31, 2016, dated February 22, 2017, should be read in conjunction with the Company’s 2016 audited consolidated financial statements and related notes for the year ended December 31, 2016. Our 2016 audited consolidated

financial statements and related notes are prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Unless otherwise indicated, all amounts shown in this report

are in Canadian dollars.

Additional information regarding the Company, including our Annual Information Form, is available on SEDAR at www.sedar.com and

on EDGAR at www.sec.gov. Such additional information is not incorporated by reference unless otherwise specified and should not be deemed to be made part of this Management’s Discussion and Analysis.

Executive Summary

CORE BUSINESS AND

STRATEGY

| • |

|

We collaborate across disciplines and industries to bring buildings, energy and resource, environmental, water, and infrastructure projects to life. We provide services in engineering, architecture, interior design,

landscape architecture, surveying, environmental sciences, construction services, project management, and project economics, from initial project concept and planning through to design, construction, commissioning, maintenance, decommissioning, and

remediation. Our promise is to design with community in mind. |

| • |

|

Our business objective is to be a top 10 global design firm. We plan to achieve a compound average annual growth rate of 15% through a combination of organic and acquisition growth. |

| • |

|

To achieve our business objective, we focus on the following: providing professional consulting services while maintaining our newly acquired construction management at-risk

services; using the strength of our local positioning to bring our world-class expertise to the communities in which we live and work; driving a client-focused culture through cross-selling efforts, account management strategies, and strong

local relationships; focusing on quality and creativity; positioning ourselves among the top-tier service providers in the sectors and geographic locations in which we operate; and strengthening our

capabilities and geographic reach through strategic hires and the acquisition and integration of firms to solidify our North American presence while building on our global platform. |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-2 |

|

Stantec Inc. |

KEY PERFORMANCE DRIVERS AND CAPABILITIES

| • |

|

Our performance is driven by external factors in the infrastructure and facilities industry and by internal strategic drivers and capabilities that are articulated through our value statements: we put people first,

we are better together, we do what is right, and we are driven to achieve. |

RESULTS

| • |

|

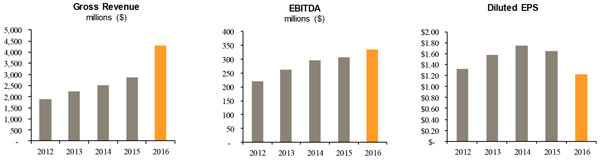

Continued profitability and growth. Our gross revenue grew 49.5% in 2016 compared to 2015. Of this gross revenue growth, 53.4% resulted from acquisitions and 1.7% was due to foreign exchange; this growth was

partly offset by a 5.6% retraction in organic revenue. We achieved a 9.8% increase in EBITDA1 and a 15.5% increase in adjusted EBITDA1. Our net

income was $130.5 million in 2016 compared to $156.4 million in 2015. Diluted earnings per share (EPS) was $1.22 in 2016 compared to $1.65 in 2015 and adjusted diluted EPS1 was $1.69 in

2016 compared to $1.84 in 2015. |

EBITDA for 2016 was impacted by a decrease in gross margin as a percentage of net revenue

and an increase in our administrative and marketing expenses—due in part to increases in acquisition-related costs in connection with the acquisition of MWH Global, Inc. (MWH), retention and merit payments to retain key employees, severance

costs in our Energy & Resources business, and professional fees. Net income was also impacted by an increase in the amortization of our intangible assets from acquisitions and software additions. As well, net interest expense increased year

over year, mainly resulting from an increase in outstanding long-term debt at the end of 2016 compared to 2015, which was primarily related to the MWH acquisition. In addition, our annual effective income tax rate increased in 2016. See pages M-21 to M-23 in this Management’s Discussion and Analysis for further EBITDA, EPS, and net income highlights.

| • |

|

Growth through acquisition. Acquisitions completed in 2016 and 2015 contributed $1.5 billion to the increase in our gross revenue in 2016 compared to 2015. We completed five acquisitions in 2016 and six in

2015, strengthening our North American presence while expanding our global reach. The MWH acquisition expanded many areas of our legacy Consulting Services business, positioned us as a global leader in the Water sector, and created a new service

offering—Construction Services. |

| • |

|

Successful public offering and new credit facilities. We financed the MWH acquisition with the net proceeds of a public offering that generated $578.1 million and with funds drawn from our new

$1.25 billion syndicated senior secured credit facilities. The proceeds from these new credit facilities were also used to repay all outstanding indebtedness under our existing $350 million revolving credit facility, redeem all our senior

secured notes, and repay the outstanding indebtedness of MWH under its existing revolving credit facility. As at December 31, 2016, $329.1 million of additional borrowing was available under our revolving credit facility for future

acquisitions, working capital needs, and general corporate purposes. |

OUTLOOK

| • |

|

We anticipate continued economic improvement in the United States, increased infrastructure spending in both Canada and the United States, increased spending in the water and wastewater sector, strong spending growth in

the US transportation sector, a modest improvement in the energy and resource sectors compared to 2016, continued support for alternative project delivery (APD) methods—including public-private partnerships (P3s)—in Canada with increasing

opportunities for APD in the United States, and modest global economic growth, offset by a moderate slowdown in the Canadian housing market. |

|

| 1 EBITDA, adjusted EBITDA, and adjusted diluted EPS are defined in the Definition of Non-IFRS Measures

in the Critical Accounting Estimates, Developments, and Measures section (the “Definitions section”) of this report. |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-3 |

|

Stantec Inc. |

RISKS

| • |

|

Various risk factors could cause our actual results to differ materially from those projected in the Outlook section and forward-looking statements of this report. The material known risks are described in the

Risk Factors section of this report. We believe there will be increased activity from the improving US economy and recent government infrastructure spending announcements in both Canada and the United States. Economic pressures and

uncertainties, volatility in foreign exchange rates, volatility in energy and commodity prices, changes in private industry spending, and changes in public infrastructure funding may adversely impact our current outlook for 2017. In addition, our

current outlook for 2017 could be unfavorably impacted if we are unable to successfully manage our integration program—particularly for larger acquisitions such as the MWH acquisition—or respond to the complexity of managing and running a

global business. |

Core Business and Strategy

The following discussion includes forward-looking statements. For an outline of the material risks and assumptions associated with these statements, refer to

the Cautionary Note Regarding Forward-Looking Statements at the end of this report.

CORE BUSINESS

We collaborate across disciplines and industries to bring buildings, energy and resource, environmental, water, and infrastructure projects to life. Our

work—engineering, architecture, interior design, landscape architecture, surveying, environmental sciences, construction services, project management, and project economics, from initial project concept and planning through to design,

construction, commissioning, maintenance, decommissioning, and remediation—begins at the intersection of community, creativity, and client relationships.

Our local strength, knowledge, and relationships, coupled with our world-class expertise, have allowed us to go anywhere to meet our clients’ needs in

more creative and personalized ways. With a long-term commitment to the people and places we serve, Stantec has the unique ability to connect to projects on a personal level and advance the quality of life in communities across the globe.

BUSINESS OBJECTIVE

Our business objective is to be a top 10 global

design firm. Based on our annual gross revenue, we are currently within the top 5 design firms in North America and top 15 design firms globally. We continue to work diligently to be the top-tier service

provider in the sectors and geographic regions we serve. While revenue and size are one way of measuring our position as top tier, our position in the industry is also measured qualitatively for information that tells us about our position in a

sector, our local presence, and our global expertise.

We believe that our continued growth will increase shareholder value and give our employees the

opportunity to bring their talent and expertise to top clients that have complex projects spanning multiple disciplines around the world. We plan to achieve a compound average annual growth rate of 15% through a combination of organic and

acquisition growth.

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-4 |

|

Stantec Inc. |

STRATEGY

To establish

a clear plan for achieving our business objective—to be a top 10 global design firm—we employ a three-year strategic planning process: three execution years where the third year is also a comprehensive strategic review year. During that

year, we develop our long-range (five-year) strategy, performing a more in-depth review of the market environment and industry and challenging the direction of past

strategic plans. In the interim execution years, we focus on implementing and executing that long-range strategy. In 2015, we completed a comprehensive strategic review, determining that the key elements of our strategy will not materially change

over the next three years. This remains true following the 2016 acquisition of MWH, the largest acquisition in our Company’s history; however, we have evolved our 2017 strategic plan to leverage this achievement.

On May 6, 2016, we acquired MWH, a Broomfield, Colorado-based global engineering, consulting, and construction management firm providing program

management and management consulting, construction management, and engineering and technical services, particularly in the water, renewable energy, and sustainability sectors. Worldwide, MWH had 187 offices operating in 26 countries with

approximately 6,800 employees. This acquisition expanded our presence in water resources infrastructure while earning us a greater presence in key targeted geographic regions, including the United States, the United Kingdom,

Australia, New Zealand, South and Central America, Europe, and the Middle East.

A key component of implementing our strategic plan is the full

integration of acquired companies. Therefore, in 2017, one of our focuses will be successfully integrating MWH’s people, systems, and best practices into legacy Stantec, thereby creating a successful combined company poised for growth. Our

business objectives for integrating MWH include achieving costs synergies, creating a combined North American organization structure that supports future growth, executing a strategy that positions global operations for investments in markets with

strong growth potential, and incorporating best-in-class systems, tools, and processes from each organization.

Historically, our acquisition strategy has focused on acquisitions in North America to develop a mature presence across our business portfolio. In our

comprehensive planning year, we identified the constraints of this North American-focused acquisition strategy, namely, the availability of suitable firms. As part of our 2016 Strategic Plan, we expanded our acquisition strategy by including

firms with a global presence. That resulted in the MWH acquisition, which greatly expanded our global presence. For 2017, we plan to augment our disciplined North American acquisition strategy, integrate our new operations, and explore opportunities

to further expand our global footprint.

Purpose, Promise, and Values

Our Company’s purpose, promise, and values form the foundation of our strategy and have not changed from 2015. Our purpose is to create communities, and

our promise is to design with community in mind. Our values follow:

| • |

|

We are driven to achieve |

Our values provide the principles that govern our employees and how we behave and

make decisions. For each action-oriented value, we identify annual initiatives for talent management, learning and growth, client relationships, business processes, and operational and financial performance. (Our value statements, the results of our

2016 key initiatives, and our 2017 initiatives are further described in the Key Performance Drivers and Capabilities section of this report.)

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-5 |

|

Stantec Inc. |

Strategic Elements

The elements of our strategy have not materially changed; however, we have enhanced some elements given our Company’s significant growth in 2016.

Corporate strategic pillars

| • |

|

Design. We focus on professional consulting while maintaining our newly acquired construction management at-risk services. |

| • |

|

Top tier. We position ourselves among the top-tier service providers in the sectors and geographic regions we serve. |

| • |

|

Diversification. We continue to diversify our projects, clients, and geographies, thereby mitigating risk. |

| • |

|

Community presence. We use the strength of our local position to bring world-class expertise to the communities where we live and work. |

| • |

|

Strengthening our reach. We continue to solidify our North American presence while building on our new global platform, particularly in the United Kingdom, Australia, and New Zealand. |

| • |

|

Business conduct. We embrace safety and ethical business practices as the foundation for everything we do. |

Business strategic pillars

| • |

|

Single brand and platform. Our guiding principle is to use a common brand and common systems, as well as to follow common operational policies, practices, and programs. We customize this approach to

accommodate the unique needs of our various business operating units. |

| • |

|

Local and global client focus. We drive a client-focused culture through cross-selling efforts and account management strategies. |

| • |

|

Leadership model. We organize and manage our business through a collaborative, consensus-based approach. Our leadership model evolves to meet the needs of our business and geographic regions we serve.

|

| • |

|

Technical excellence. We focus on quality to provide value-added services through integrated quality management systems. |

| • |

|

Creative solutions. We focus on creativity to provide value-added services. |

| • |

|

People. We attract talent, develop our people, and provide a diverse and inclusive work environment, ensuring we have the right people in the right roles. |

Reportable Segments

In the first quarter of 2016, our Company had

one reportable segment, Consulting Services, an aggregate of our previous operating segments. These operating segments were based on regional geographic areas. Our chief operating decision maker (chief executive officer) assesses our Company’s

performance based on financial information available from our operating segments.

As a result of the MWH acquisition and effective the second quarter of

2016, our reportable segments (in accordance with IFRS) are based on our two primary service offerings—Consulting Services and Construction Services—and our regional geographic areas. The Company now has four operating and reportable

segments:

| • |

|

Consulting Services – Canada |

| • |

|

Consulting Services – United States |

| • |

|

Consulting Services – Global |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-6 |

|

Stantec Inc. |

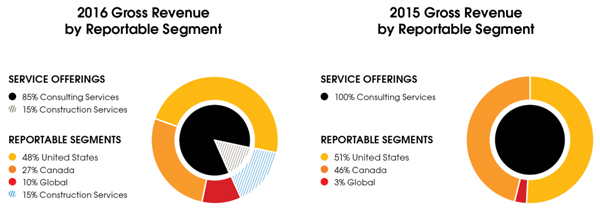

In 2016, we earned 27% of our gross revenue in Consulting Services – Canada, 48% in Consulting Services

– United States, 10% in Consulting Services – Global, and 15% in Construction Services.

Consulting Services

In Consulting Services, we provide knowledge-based solutions through value-added professional consulting services in engineering, architecture, interior

design, landscape architecture, surveying, environmental sciences, project management, and project economics in the area of infrastructure and facilities, principally under

fee-for-service agreements with clients. Our business operating unit leaders provide strategic direction, mentoring, and technical support to operations across our

geographic regions.

Construction Services

In

Construction Services, we provide construction management and project delivery at-risk services, primarily on water-related projects to key long-term clients in the United States and United Kingdom. We offer start-to-finish construction capabilities to municipal, utility, federal, and industrial clients, including commissioning and start-up

services. Separate from project delivery, we also provide construction management and professional supervision services. Construction Services revenue is derived primarily from cost-reimbursable, guaranteed-maximum price contracts and fixed-price

contracts. Compared to our other reportable segments, Construction Services uses more subcontractors and subconsultants and has lower gross margins.

The

main contract types in this segment fall generally into four functional areas:

| • |

|

Construction management at-risk |

| • |

|

Design-build and progressive design-build |

| • |

|

Construction management in support of design completed by Consulting Services |

| • |

|

Hard-bid construction with self-performance |

We separate the

construction business from the consulting businesses in our operational structure. This is key to leveraging our construction capabilities when they are advantageous to the client. This separation allows both streams of expertise to operate

effectively and allows synergies to develop that complement but do not distract from the strategy of each business. In addition, the two businesses can be bundled when beneficial for the client.

We expect that the expertise available in our newly acquired Construction Services business will augment and improve our Consulting Services business.

Consulting Services can then better prepare for and execute design-build projects with construction partners outside of Stantec in water markets and other sectors that we participate in.

Business Model

Our business model, a key element of our strategy,

is based on providing services across diverse geographic regions, business operating unit specialization, and all phases of the infrastructure and facilities project life cycle—planning, design, construction, commissioning, maintenance,

decommissioning, and remediation.

Because of our diverse model, we can generally adapt to changes in market conditions by offsetting a decreased demand

for services in one business operating unit or geographic location with an increased demand in another. We believe this strategy helps us mitigate risk while we continue to increase our revenue and earnings. Also, we work on tens of thousands of

projects for thousands of clients in hundreds of locations. This ensures we do not rely on a few large projects for our revenue.

The following

information outlines the three main components of our business model: geographic diversification, business operating units, and life-cycle solutions.

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-7 |

|

Stantec Inc. |

Geographic Diversification

The first element of our business model is geographic diversification. Traditionally, we operated in three regional operating units—Canada, the United

States, and International. Before acquiring MWH, we had international offices in the Middle East, the United Kingdom, and the Caribbean. The MWH acquisition has increased our geographic diversification as follows:

| • |

|

Expanded our geographic footprint. MWH is strongly positioned and experienced in global markets through its platform in the United Kingdom, Australia, New Zealand, South and Central America, Europe, and the

Middle East. The MWH acquisition provided us with immediate geographic breadth, creating a platform for expansion and diversification. We believe that the combination of MWH’s and Stantec’s complementary capabilities, market presence, and

cultures creates opportunities to service more clients and offer a broader range of services worldwide. |

| • |

|

Created additional growth opportunities. We believe that the engineering and construction sector will continue to consolidate and that both scale and global capabilities will be important competitive

differentiators, particularly on large and complex projects. MWH has been in business for approximately 200 years, so it has a wealth of experience operating in global markets. Augmented by our strong statement of financial position, history of

operational effectiveness, and experience in successfully completing and integrating acquisitions, we expect to be well positioned to grow both organically and by acquisition. MWH’s platform in the United Kingdom and Asia Pacific regions gives

us the opportunity to expand our current North American acquisition strategy into new global markets, which we believe widens the platform for our acquisition program. |

Geographic Opportunities

Since the MWH

acquisition, our Consulting Services business has continued to operate as three regional operating units—Canada, the United States, and Global (formerly International). Our Construction Services business is a new reportable segment.

Over the next two years, we will continue our growth in North America through both organic and acquisition growth; we expect to augment this growth with

acquisitions and organic growth in the United Kingdom, Australia, and New Zealand. During this time, we will gradually increase our geographic reach in other markets that are suited for and receptive to our services.

Canada. At December 31, 2016, we had approximately 7,500 employees in Canada. We benefit from a mature position within each region and view

our strategic opportunities as follows:

| • |

|

Pursuing business expansion opportunities within our Water and Transportation sectors |

| • |

|

Continuing to strengthen our infrastructure presence in the Greater Toronto Area, other parts of Ontario, and the Atlantic, Alberta, and British Columbia regions |

| • |

|

Continuing to capitalize on opportunities in LNG facilities; pipelines; ports and marine terminals; tidal water markets; and health, education, commercial, and civic markets |

| • |

|

Capitalizing on alternative energy projects, specifically in the expanding wind, hydro, co-generation, and carbon-capture markets |

| • |

|

Securing additional projects serving First Nations communities because of our strong Aboriginal partnerships and connection to local communities, as well as the federal government’s plans for infrastructure

spending |

| • |

|

Continuing to capitalize on opportunities in P3 markets |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-8 |

|

Stantec Inc. |

United States. At December 31, 2016, we had approximately 9,700 employees in the United States

(including 750 in Construction Services), where the economy is expanding. Due to acquisitions completed over the past number of years we are achieving critical mass and diversity in many sectors and geographies.

We will remain focused on strengthening our service capabilities and reaching maturity in the markets we serve. We view our strategic opportunities as

follows:

| • |

|

Continuing to leverage our recognized expertise in community development and infrastructure to capitalize on opportunities related to the strong US housing market |

| • |

|

Continuing to pursue infrastructure opportunities in the US West region and Sunbelt states |

| • |

|

Expanding our Federal Services group and our disaster management and resilience efforts |

| • |

|

Growing our Environmental Services business across the United States |

| • |

|

Continuing to expand our US Buildings business, particularly in the US West, and diversifying from healthcare |

| • |

|

Continuing to pursue acquisition opportunities in our Energy & Resources business operating unit |

Global. At December 31, 2016, we had approximately 4,800 employees in our Global operations (including 1,000 in Construction Services, all located

in the United Kingdom). The MWH acquisition provided immediate geographic breadth, creating a platform for expanding and diversifying. Our focus in 2017 will be to develop a leadership and organizational structure that brings together Stantec’s

legacy International operations with MWH’s global operations and supports further growth in key markets and regions. We view our strategic opportunities as follows:

| • |

|

Continuing to solidify our existing Stantec presence in the United Kingdom and the United Arab Emirates |

| • |

|

Leveraging MWH’s top-tier brand in the United Kingdom so we can continue working on projects through the United Kingdom’s Asset Management Program |

| • |

|

Enhancing and growing our strategic technical consulting business in the United Kingdom and expanding MWH’s UK service offerings beyond water through a focused acquisition strategy |

| • |

|

Cross-selling services in continental Europe |

| • |

|

Expanding service offerings in the United Kingdom, Australia, and New Zealand by capitalizing on Stantec synergies |

Business Operating Unit Specialization

Business operating unit

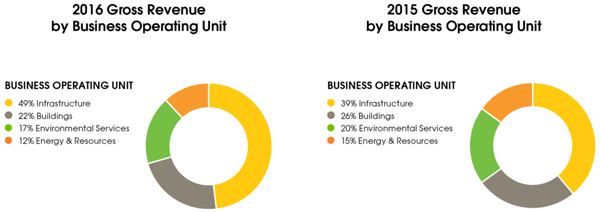

specialization is the second element of our business model. In Consulting Services during 2016, we had four specialized business operating units: Buildings, Energy & Resources, Environmental Services, and Infrastructure. In 2016, we earned

22% of our Consulting Services gross revenue in Buildings, 12% in Energy & Resources, 17% in Environmental Services, and 49% in Infrastructure.

Within these four Consulting Services business operating units, we focus on the top 14 sectors that our clients operate in. By better understanding our

clients’ goals, the market influences, and our business drivers, we can offer multidisciplinary solutions to meet their needs.

Buildings

We generate most revenue in our Buildings business operating unit by providing pre-design, design, and

construction administration services in planning, architecture, buildings engineering, and interior design services for vertical infrastructure. We earn most of our revenue from private sector and institutional clients; the remaining revenue is

from public sector clients. We provide services in the following sectors:

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-9 |

|

Stantec Inc. |

Energy & Resources

We generate most of our revenue in our Energy & Resources business operating unit from industrial engineering, project management, and construction

management services primarily for private sector clients. Services are provided in the following sectors:

Environmental Services

We generate most of our revenue in our Environmental Services business operating unit by providing front-end

environmental services for private sector clients and remediation activities for private and public sector clients. Environmental Services provides services across all Company sectors, though more than 45% of its revenue is generated from our

Energy & Resources business operating unit.

Infrastructure

We generate most of our revenue in our Infrastructure business operating unit by providing front-end design and

engineering services, with a small portion from project and construction management services. We provide services in the following sectors:

| • |

|

Transportation (Bridges, Roadways, and Transit & Rail) |

Our Community Development sector mainly serves private sector clients. Our Transportation and Water

sectors mainly serve public sector clients, but a growth area is delivering these services using alternative project delivery methods.

MWH’s

cross-selling capabilities to various end markets

MWH adds global capabilities in water-related design services to our key hydropower, oil and

gas, mining, and industrial clients. MWH’s global client portfolio is expected to generate opportunities for our Energy & Resources business operating unit to cross-sell its engineering services. We believe that further opportunities

exist to cross-sell services provided by our Buildings and Environmental Services business operating units to MWH’s clients.

Evolution of our

business operating unit specialization

We continually evolve our organizational structure so that it adapts to changes in the marketplace, meets

our business needs, and positions us for long-term success. The MWH acquisition added a world-class design presence to our Water sector and a truly global platform from which we can enhance our Consulting Services offerings. For these reasons, we

are realigning our Consulting Services organizational structure. Bringing our

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-10 |

|

Stantec Inc. |

total number of business operating units to five, at the beginning of 2017, we added Water as a separate business operating unit by segregating the legacy Stantec Water sector from our

Infrastructure business operating unit and combining it with MWH’s capabilities in water.

Considering this realignment, our restated 2016 gross

revenue earned in Consulting Services is 22% in Buildings, 12% in Energy & Resources, 17% in Environmental Services, 28% in Infrastructure, and 21% in Water. (Refer to the Results section of this report for additional details about the

restated 2016 figures.)

Life-Cycle Solutions

We provide

professional services in all phases of the project life cycle: planning, design, construction, commissioning, maintenance, decommissioning, and remediation. This inclusive approach enables us to deliver services during periods of strong new capital

project activity (design and construction) and of redevelopment and operational spending activity (maintenance, integrity management, and remediation). We believe this strategy enables us to maintain long-term client relationships throughout the

life of a project or an infrastructure asset.

Beginning with the planning and design stages, we provide conceptual and detailed design services, conduct

feasibility studies, and prepare plans and specifications. During the construction phase, we generally act as the owner’s representative, providing project management, construction management, surveying, and resident engineering services. In

our Consulting Services business, we focus principally on fee-for-service work and rarely act as the contractor or take on construction risk. In our Construction

Services business, we provide construction management at-risk services. During the maintenance phase that follows project completion, we provide ongoing professional services for integrity management, as well

as for maintenance and rehabilitation projects such as facilities and infrastructure management, facilities operations, and performance engineering. In the final decommissioning phase, we provide solutions, recommendations, and remediation

strategies for taking facilities out of active service. The MWH acquisition provided a broader enhanced service offering throughout the complete project life cycle and expanded our service offerings in the construction phase.

Key Performance Drivers and Capabilities

Our key performance drivers are defined by external forces and by internal initiatives that are articulated through our value statements: we put people first,

we are better together, we do what is right, and we are driven to achieve.

The following discussion includes forward-looking statements. For an outline

of the material risks and assumptions associated with these statements, refer to the Cautionary Note Regarding Forward-Looking Statements at the end of this report.

KEY EXTERNAL DRIVERS

Consulting Services

Our Consulting Services business is driven by external industry factors that affect the demand for our services.

Buildings

Our Buildings business operating unit

consists of seven market sector groups. This diversity means that Buildings is driven by a combination of factors such as economic outlook, technology advancements, aging infrastructure, resiliency trends, regulatory changes, project complexity,

population growth, urbanization, and demographic changes. Drivers specific to our key market sectors include the following: passenger and air freight traffic (Airports & Aviation), US healthcare reform (Healthcare), the incorporation of

full automation in warehousing and the supply chain (Industrial), Internet commerce (Commercial), municipal government funding (Civic), and a focus on science, technology, engineering, and mathematics education (Education and Science &

Technology).

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-11 |

|

Stantec Inc. |

Energy & Resources

Our Energy & Resources business operating unit is driven primarily by supply and demand for commodities both globally and locally. Our Oil &

Gas and Mining sectors are impacted by economics, commodity prices, cost reduction and efficiencies, technological advancement, and political and regulatory drivers (including carbon emission reductions). Other considerations include alternative

fuels, aging infrastructure, and energy efficiency trends. These sectors are highly cyclical and can experience rapid and dramatic fluctuations in price and supply and demand.

Our Power sector is more of an infrastructure business, but economic activity also affects power demand and therefore impacts this market. Regulations,

infrastructure age, the location of supply and demand for transmission and distribution, and renewable subsidization also influence activity in our Power sector.

Significant drivers for the Waterpower & Dams sector include climate change and the associated demand for hydroelectric power, both as a renewable

generation source and for its ability to integrate other renewables (wind and solar). Aging infrastructure results in the need to rehabilitate, modernize, and upgrade existing dam and hydroelectric projects.

Environmental Services

Our Environmental Services

business operating unit performs services in some capacity across all Company sectors, though most significantly in our Energy & Resources business operating unit and our Transportation and Commercial sectors. Therefore, the drivers

for Environmental Services overlap with those affecting other business operating units. Following are the most significant drivers affecting Environmental Services: economic and political conditions, construction growth, environmental regulations,

emphasis on environmentally sustainable behaviors, demand for emergency site remediation planning and cleanups, Aboriginal involvement in resource-based projects, and increasing spending on infrastructure improvements in Canada and the United

States.

Infrastructure

Our Infrastructure

business operating unit is driven by a combination of economic, demographic, urbanization and housing, technology, public funding, and regulatory factors. Additional drivers include employment rates, interest rates, water conservation efforts,

public and active transport usage, technological advancements, aging infrastructure, resiliency trends, and regulatory changes. Drivers specific to key market sectors include the housing-affordability crisis (Community Development), connected and

autonomous vehicles, and Smart Cities and design-build (Transportation). Overall, this business operating unit relies heavily on local and regional clients and benefits from Stantec’s strong community presence.

Water

We will report Water as a distinct

Consulting Services business operating unit effective January 1, 2017. The Water business operating unit performs services in the following sectors:

| • |

|

Client Enterprise Systems |

| • |

|

Urban Stormwater & Wet Weather Flow |

| • |

|

Water Resources Planning & Management |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-12 |

|

Stantec Inc. |

Our Water business operating unit is driven primarily by regulatory and public funding factors as well as aging

infrastructure, resiliency strategies, demographic shifts, water scarcity, climate change, globalization and geopolitics, technology, and economic cycles.

Construction Services

Key performance drivers for Construction

Services are similar to the drivers for our legacy Stantec Water sector; these Water sector drivers were carried over to our newly defined Water business operating unit. Specifically, trends that are expected to impact water infrastructure

requirements and drive growth in the sector include demographic shifts, water scarcity, climate change, globalization and geopolitics, technology, and economic cycles.

KEY INTERNAL DRIVERS

We believe our actionable value statements

best reflect what unites Stantec and compels our people to come to work and to do their best every day. Our performance depends on our ability to achieve excellence by putting people first, developing strong, long-lasting relationships with each

other and our clients, doing what is right, and being driven to achieve at every level. Our value system provides a framework for the strategic initiatives that we implement to drive our performance and help obtain our overall business objective of

being a top 10 global design firm.

We Put People First

We

continue to evolve by attracting talent and developing our people. This entails assessing and guiding current employees, engaging and developing leadership, and ensuring we create an experience and a work environment that retains talent. The total

number of employees at our Company was approximately 15,200 at the end of 2015 and approximately 22,000 at the end of 2016.

Employees

Our people remain at the core of what we do. We strive to attract and retain the best employees in the field and to further develop their talents.

We are committed to supporting, fostering, and investing in each employee’s success through a culture of opportunity, equity, development, diversity, and

innovation. Specific career streams provide employees with career development direction and growth opportunities based on their primary area of interest. We also have a formalized succession planning process and offer a number of leadership

programs. In 2016, we initiated the pilot phase of a Talent Management System so we can collect and integrate all talent data across Stantec. In 2017, we will start a phased-in implementation process.

Our Diversity and Inclusion committees foster a workplace that supports the unique differences of our clients and employees. In 2016, we continued to deliver

initiatives supporting diversity and inclusion, including rolling out unconscious-bias training to leadership, and in 2017, it will be available Company-wide. We will also expand our mandate for employee resource groups to bring together communities

of employees with shared backgrounds and values. We will also call on the expertise of the Canadian Centre for Diversity and Inclusion to support our ongoing development of a comprehensive diversity and inclusion plan.

We measure the success of our various initiatives through retention rates, employee surveys, 360-degree feedback, and

exit interviews. The results help us develop future programs and initiatives.

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-13 |

|

Stantec Inc. |

Senior leadership

Our Executive Vice President Team (EVPT) is made up of our senior leaders: the chief executive officer (CEO), chief financial officer (CFO), chief operating

officer (COO), chief business officer (CBO), and executive vice presidents (EVPs). The EVPT oversees the Company’s overall performance, including developing and monitoring our business plan, monitoring financial performance and risks, approving

policies and procedures, and overseeing acquisitions and divestitures. EVPs are specifically responsible for the performance of our reportable segments and business operating units.

In 2016, we worked toward building fully developed processes to assess, grow, reward, and promote our leaders to achieve success today and prepare for future

talent and business needs. In 2017, we will compare core leadership needs and gaps to our business plan and acquisition needs. We will assess current succession planning processes, tools, and outcomes for employees, including those joining Stantec

through acquisition. We will identify mission-critical roles and run succession-planning pilots in certain areas of our Company.

Compensation

Our ability to align the activities of our senior leadership and other key employees with our short- and long-term financial and strategic goals

is a key driver of our success. In addition to their fixed salaries, we provide short- and long-term compensation on a discretionary basis for their individual and corporate contributions to meeting our objectives.

For our senior leadership, senior managers, and other key employees, we provide a short-term incentive program (STIP) that is paid annually in cash. The total

amount available in the STIP for any given year is calculated as a percentage of our annual pretax, pre-STIP net income, which encourages our senior managers to achieve profitable business results. To

determine the STIP awards for the year, we evaluate each eligible employee’s personal performance and achievement of Company-wide and business unit objectives. In our view, this compensation program creates a sense of shared responsibility for

achieving outstanding business results and meeting our clients’ needs.

Our compensation program for our senior leadership team provides a long-term

incentive plan (LTIP) using both share options and performance share units (PSUs), in addition to base salary and STIP participation. The mix of fixed salary, STIP compensation, and LTIP compensation varies, depending on the seniority of the

executive within the organization. Our CEO, CFO, COO, CBO, and EVP targeted total compensation is more heavily weighted to long-term incentives. This motivates our most senior executives to make decisions that are in the long-term interest of the

shareholders.

Certain key employees who are not members of the senior leadership team are also granted options through an LTIP approved by shareholders

in 2014, further aligning their interests with our shareholders’ interests, as well as encouraging them to remain with us over the long term.

The

CEO’s STIP is evaluated by the board annually and is based on achieving corporate and individual performance metrics, and he is awarded annual long-term incentive grants of share options and PSUs. His total compensation is 25% fixed base

salary, 25% short-term cash incentive opportunity, and 50% equity-based long-term incentives. The long-term incentives granted are one-third share options and two-thirds

PSUs.

We require our CEO, CFO, COO, CBO, and EVPs to own a minimum number of shares in the Company. These executives must own a multiple of their base

salary in shares. We believe that our long-term programs and the minimum ownership requirement provide the appropriate incentives for our EVPT to achieve growth in our share price, thereby aligning their compensation with the interests of

shareholders.

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-14 |

|

Stantec Inc. |

We also have an executive compensation claw-back policy which shows our commitment to the principle that

compensation paid to our executives—based on financial information that has since been restated—should be returned.

We Are Better Together

Strong, long-lasting relationships are at the center of everything we do, and each employee brings individual strengths to our Company, whether that

is technical expertise, particular sector experience, or exceptional client relationships. When we combine those strengths, we believe we reach our full potential to build lasting relationships with our clients. Building and developing a

consistently positive client-centered experience is essential for the continued growth and success of our organization.

Organizational evolution

In 2016, we continued the process of realigning our internal structure to better serve our clients. The acquisition of MWH added a world-class

design presence in the water sector, including a top-tier presence in the United States and United Kingdom, and a world-class presence in waterpower and dams. To best leverage this expertise and offer a higher

degree of leadership and increased visibility for clients and employees, effective January 1, 2017, we are combining legacy Stantec’s Water sector (from the Infrastructure business operating unit) and MWH’s Water businesses into a

separate business operating unit—Water.

Account management and client development

We continue to pursue a client strategy that focuses on growing global accounts while augmenting the strength of our local client base and differentiating

ourselves from our peers in the marketplace. The purpose of our account management program is to position Stantec for sustainable organic growth. In 2017, we will focus on strengthening our ability to establish key accounts, align capable account

managers, develop new business with those accounts, and measure our success.

In 2016, we developed a client-centric, cross-functional Client Services

team to improve the growth of our key accounts and the services we provide to our clients. As well, account managers were asked to develop account development plans for each national and global top client identified for 2017. We plan to extend this

program to local and regional accounts in 2017. We also plan to leverage MWH’s sales and client development capabilities.

Alternative project

delivery

Although our business has historically followed a

fee-for-service model, we do have processes for evaluating, pursuing, and executing projects using alternative project delivery (APD) methods, such as various forms of

design-build and P3s, and bundling engineering, procurement, and construction management (EPCM) services. In 2016, we proposed that—over a period of a few years and for select projects, clients, and sectors—we will continue exploring our

service delivery approach and risk appetite to better meet our clients’ needs. We will continue this approach in 2017.

MWH’s Construction

Services will continue to focus on its existing business, but we will consider how we can incorporate their construction knowledge and identify ways they might support our overall strategy for EPCM projects.

Creativity and Innovation Program

We continue to

support and promote creative and innovative thinking. In 2016, we formalized a program that recognizes and celebrates, internally and externally, the efforts of our employees to develop and apply ideas that benefit us, our clients, and our

communities. The program includes an annual fund to support research, development, and innovative ideas initiated by our employees, as well as financial rewards for staff who publish

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-15 |

|

Stantec Inc. |

articles or speak at conferences. The program also includes a venture fund intended to support innovative ventures into markets we are not yet in or services we do not currently offer. In 2017,

we will work to integrate MWH best practices into our existing program with the goal of having a fully integrated approach for 2017.

Practice

technology framework and cybersecurity

Our Company embraces digital technologies that assist us in delivering professional services and help us

improve services to our clients. We also recognize the importance of cybersecurity and therefore have a comprehensive IT security program designed to predict, prevent, detect, and respond to cybersecurity threats. (Cybersecurity is further described

in the Risk section of this report.) In 2016, we completed an assessment of practice technology needs across the business. We are now focused on developing strategic priorities and critical business needs to improve practice technology support,

governance, and resources.

Balanced leadership model

Because our Company has evolved, we continue to strengthen and customize our balanced leadership model to enable the unique needs of our business. The balanced

leadership model—consisting of both geographic and business leadership—offers our clients a local presence and diverse services and facilitates the cross-selling of services to new clients and in new geographies. Our structure will

continue evolving to meet our clients’ needs.

Brand positioning

In 2016, we began resurveying our clients and industry decision makers to measure the progress we made in our brand positioning since 2013. We also surveyed

MWH clients to better understand MWH’s position in its markets and the key attributes that matter most to its clients. The research findings will help us make recommendations for effectively integrating MWH’s brand into Stantec’s

brand and identify ways to develop Stantec’s existing strategic brand platform. The intent is to leverage the strengths of both brands in the global marketplace in 2017 and beyond. Following these recommendations, we will develop comprehensive

internal and external brand campaigns to communicate our combined brand to employees and the marketplace.

We Do What Is Right

Doing what is right means paying attention to the impact that every decision has on the way we do business and holding ourselves to a high standard of ethics

and integrity in everything we do. It also means committing to professional excellence in a manner that fosters an innovative, forward-looking culture of safety and sustainability.

Ethics and integrity

Our reputation remains a

significant asset; therefore, our focus continues to be on aligning our actions and decisions with our ethics and integrity policies. One way we ensure this is by conducting annual mandatory ethics, integrity, and anti-corruption compliance training

for all employees. We articulate our high standard of business practices through our Project Management Framework, Code of Ethics, and policies and practices. We also engage an outside agency to monitor, review, and report any issues identified

through our Integrity Hotline. In 2017, we will deploy an updated ethics and integrity compliance training program to focus on issues routinely faced by design and construction firms and build on MWH’s strong global compliance program.

Health, safety, security, and environment

We are

committed to ensuring the health and safety of all employees and stakeholders involved in our professional work. We continue to promote a culture of safety across our organization by implementing numerous formal and informal initiatives. In 2016, we

reorganized our former Health, Safety, and Environment group. The Health, Safety, Security, and Environment (HSSE) group is now focused on three main areas: occupational health and safety, security, and the environment.

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-16 |

|

Stantec Inc. |

We will continue developing a mature health and safety culture that is focused on leading indicators and that

decreases our total recordable injury rate. In 2017, HSSE will focus on refining our environmental management system and tools and establishing security processes which address both staff mobility and facilities assessment to enhance leadership

engagement and reduce employee injuries. To achieve this, we will enhance our employees’ understanding of how Stantec employees are “Safer Together” by highlighting the employees’ personal connection and commitment and senior

leadership’s accountability. In addition, we will focus on combining the best of the systems and processes acquired through the MWH transaction.

Quality management

We use various methods to

ensure high-quality project execution, including the following:

| • |

|

Project Management Framework. We are committed to efficient and high-quality project execution within a framework that incorporates ethics, safety, sustainability, innovation, and profitability. In legacy Stantec

operations, our Project Management (PM) Framework helps us improve project planning, remain committed to quality assurance, and fulfill independent review requirements, and these principles are consistently applied to all projects. For MWH

operations, we use a proprietary handbook of PM practices that will be integrated with the legacy Stantec PM Framework in 2017 and adopted by all our Consulting Services operations. MWH Construction Services uses a Project Management Administration

Plan to tailor its project management practices to each project and integrate quality, risk, health and safety, information technology (IT), and change management procedures. |

We always strive to enhance our project execution and forecasting ability and to facilitate more efficient resource management. Currently, we

use a diverse range of tools, including our Enterprise Management System, to execute projects effectively, and we will continue to invest in these tools in 2017.

| • |

|

Internal practice audits. We conduct internal practice audits to identify opportunities for practice improvement across regions, disciplines, and sectors. |

| • |

|

Integrated Management System. In legacy Stantec operations, our Integrated Management System (IMS) clarifies expectations for project delivery and client service excellence and conveys the steps employees must

take to achieve more consistent and successful project outcomes. In 2016, we redefined our internal practice audit program and expanded the number of internal practice audits and client surveys conducted annually. We are also in the process of

consolidating our audit, client survey, incident notification, and improvement plans on a Company-wide Governance Risk Control application. |

| • |

|

Programs and Business Solutions. Effective project management depends not only on tools but also on people. Project Management is a career stream at Stantec. In 2016, we merged our legacy Stantec Project Delivery

Office with MWH’s Business Solutions group to create the Programs and Business Solutions (PBS) group. PBS houses a group of senior project managers and project management specialists who can be deployed when needed to any project throughout

Stantec. PBS addresses the project and commercial needs of major projects, including APD and P3 projects. It also provides a systematic way to manage and mitigate the risk profiles on major projects. |

| • |

|

Regulatory compliance. We operate in diverse regulatory environments and are committed to complying with regulatory requirements. For instance, we comply with employment practices and financial reporting

standards and controls. We also demonstrate our commitment to excellence through our documented policies and practices. |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-17 |

|

Stantec Inc. |

Sustainability

We believe that every service that Stantec provides—from external services to our clients that ensure we continue to design in a sustainable way to our

own internal impact on the environment while we deliver our services—contributes to a sustainable environment.

We are committed to finding ways to

further enhance our services. In addition, we continue to invest in LEED-accredited and Envision professionals through training and mentorship to ensure we are well positioned as leaders in the field of sustainable and integrated infrastructure

solutions. Envision is a planning framework and evaluation system developed by the Institute for Sustainable Infrastructure and the Harvard Graduate School of Design. It provides a holistic framework for planning, designing, evaluating, and rating

the community, environmental, and economic benefits of infrastructure projects and systems.

In our internal operations, we are committed to reducing our

negative impact on the environment by progressing toward least-impact approaches to energy consumption, paper consumption, and waste disposal. We track and report our progress in our annual Sustainability Report and in the Carbon Disclosure Project

(CDP). In 2017, we will remain focused on meeting established targets to reduce our environmental impact.

Community engagement

Our purpose is to create communities. At Stantec, we are active members in our communities, making lasting connections with the people that we live with and

work with. To help support their growth and development, we regularly partner with a number of charitable and community organizations to work on social projects, environmental projects, and charitable initiatives.

In 2016, our Company contributed approximately $3 million to community engagement activities in arts, education, environment, and health and wellness. In

addition to these funds, we continued to give back to our communities by volunteering, fundraising, and being a partner. For example, as part of our fourth annual Company-wide Stantec in the Community Day, more than 8,000 employees volunteered

approximately 16,000 hours in communities around the world.

In every region, we make decisions with local input. We recognize that local employees

best understand how to match our resources and capabilities to our communities’ priorities and how to provide support to the organizations that make a difference. Corporately, we provide the framework that guides decision making,

ensuring our community investments align with our organizational objectives and resonate with our employees and business leaders in the communities we serve.

We target donating up to 1% of our annual pretax profits through direct cash contributions or services in kind to charitable and not-for-profit endeavors in the arts and in education, environment, and health and wellness.

We Are Driven to Achieve

Achievement at every level begins and

ends with a firm commitment to being the best that we can be. To do this, we will continue to balance growth, execution, and risk appetite while we focus on long-term sustainability.

We will continue to pursue top-tier positioning in the markets we serve and maintain the balance of our diversified

business model over the long term. We will do so through our organic growth strategies and continue to strategically execute our small- and mid-sized North American acquisitions and augment that strategy to

include small to midsized acquisitions in the United Kingdom, Australia, and New Zealand.

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-18 |

|

Stantec Inc. |

Growth opportunities

Our aim is to achieve consistent growth and profitability. We will do this by sustaining a culture of excellence and remaining committed to our clients, our

people, our communities, and our shareholders. We commit to maintaining our diversification strategy, ensuring an appropriate balance within our sector mix.

Achieving a high level of market presence in communities we serve is a key driver to our success. Our approach to regional growth is to effectively service

our existing regional and local clients, develop new client relationships, and grow our reputation and business where opportunities exist. Our target is to be among the top-tier service providers in each

region and sector. With this level of market presence, we are less likely to be affected by downturns in regional economies.

Organic growth has been and

continues to be an element of our strategy. To achieve growth, we leverage client relationships by cross-selling, following a sector-based approach, and delivering our account management programs. We refine internal strategies that promote a culture

of revenue generation in all areas of our Company.

Acquisitions are key to our strategy, and increasing the depth of our capabilities and broadening our

geographic coverage enables us to better service our clients and achieve growth. Historically, we have focused our acquisition strategy on growth in design-related services in North America. As part of our 2016 strategic plan development, we

recognized the need to start modifying our strategy to maintain our historical growth rates. MWH presented an opportunity to acquire a North American firm that aligns with our Company’s culture and strategy and that expands our services and

growth opportunities into a larger global marketplace.

For 2017, we intend to continue executing a disciplined North American acquisition approach:

targeting firms that enhance our service capabilities, deepening our geographic positioning, aligning our culture and strategy, and acting as a catalyst for enhanced organic growth. As we focus on integrating our global operations, we plan to

explore opportunities to further expand our new global footprint.

Financing

Our continued ability to finance our growth plan supports our success. Adequate financing gives us the flexibility to acquire firms that are appropriate for

our vision and complement our business model.

Since the public trading of our shares began on the Toronto Stock Exchange (TSX) in 1994, we have increased

our gross revenue at a compound annual rate of 19.3%. To fund acquisition growth, we require cash generated from both internal and external sources. Historically, we have completed acquisitions almost entirely using cash generated from operations,

credit facilities, and vendor notes. However, under certain favorable market conditions, we do consider issuing common shares to facilitate acquisition growth or to reduce borrowings under our credit facilities. This was the case for the MWH

acquisition: we financed the acquisition through the net proceeds of both a public offering of common shares and funds drawn from our credit facilities (further described in the Capital Management and Shareholders’ Equity sections of this

report).

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-19 |

|

Stantec Inc. |

Results

OVERALL ANNUAL PERFORMANCE

In 2016, we continued to grow by consistently executing our strategy. Our results and performance reflect the five

strategic acquisitions completed in the year, a common share offering, and the renegotiation of our long-term debt in the second quarter of 2016. In particular, the MWH acquisition, the largest in our history, significantly added to our

operating results.

The following highlights other major financial achievements and strategic activities in 2016 that contributed to our financial

performance and overall financial condition:

| • |

|

Continuous profitability. We ended 2016 with 49.5% growth in gross revenue. EBITDA increased 9.8% and adjusted EBITDA increased 15.5% in 2016 compared to 2015. Our net income was $130.5 million in 2016

compared to $156.4 million in 2015. Diluted earnings per share (EPS) was $1.22 in 2016 compared to $1.65 in 2015; adjusted diluted EPS was $1.69 in 2016 compared to $1.84 in 2015. See pages M-21 to M-23 in this report for further EBITDA and net income highlights. (EBITDA, adjusted EBITDA, and adjusted diluted EPS are defined in the Definition of Non-IFRS Measures in

the Critical Accounting Estimates, Developments, and Measures section the “Definitions section” of this report.) |

| • |

|

Growth through acquisition. By successfully executing our acquisition and integration strategy, acquisitions completed in 2016 and 2015 contributed $1.5 billion to our growth in gross revenue year over year,

mainly from our MWH acquisition. In particular, MWH expanded many areas of our Consulting Services business, positioned us as a global leader in the Water sector, and created a new service offering—Construction Services. |

| • |

|

Effective and diversified business model. By consistently executing our business strategy and by capitalizing on opportunities to increase project activity in our Infrastructure business operating unit, we were

able to partly offset the organic revenue retraction in our Buildings, Energy & Resources, and Environmental Services business operating units. Overall, in 2016, organic gross revenue retracted 5.6%. |

| • |

|

Growth in backlog. Our contract backlog grew 77.3%—from $2.2 billion at December 31, 2015, to $3.9 billion at December 31, 2016. (Backlog, a

non-IFRS measure, is further discussed in the Definitions section of this report.) |

| • |

|

Successful public offering. We financed the MWH acquisition through the net proceeds of (a) a public

offering of 19,964,000 shares for $30.25 each and (b) funds drawn from New Credit Facilities described |

|

|

|

|

|

| Management’s Discussion and Analysis

December 31, 2016 |

|

M-20 |

|

Stantec Inc. |

| |

below. The $603.9 million public offering of shares was completed through an agreement with CIBC World Markets Inc. and RBC Dominion Securities Inc. on behalf of a syndicate of underwriters.

After share issuance costs and underwriters’ fees, our net proceeds from the public offering were $578.1 million. |

| • |

|

New credit facilities. Concurrent with the acquisition of MWH, we entered into an agreement for new $1.25 billion senior secured credit facilities (New Credit Facilities) consisting of a senior

secured revolving credit facility of a maximum of $800 million and a $450 million senior secured term loan in three tranches. The proceeds from the New Credit Facilities were used to repay all outstanding indebtedness under our

existing $350 million revolving credit facility and redeem all senior secured notes. We also used the proceeds from the New Credit Facilities to repay the outstanding indebtedness of MWH under its existing revolving credit facility with Bank of

America Merrill Lynch. (See the Capital Management section of this report for additional information.) |

SELECTED ANNUAL INFORMATION

The following table highlights trending of certain annual information:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (In millions of Canadian dollars,

except per share amounts and %) |

|

2016 |

|

|

2016 vs.

2015

(%) |

|

|

2015 |

|

|

2015 vs.

2014

(%) |

|

|

2014 |

|

|

|

|

|

|

|

| Gross revenue |

|

|

4,300.1 |

|

|

|

49.5% |

|

|

|

2,877.2 |

|

|

|

13.7% |

|

|

|

2,529.9 |

|

| Net revenue |

|

|

3,098.4 |

|

|

|

30.5% |

|

|

|

2,373.7 |

|

|

|

14.4% |

|

|

|

2,075.3 |

|

| EBITDA (note 1) |

|

|

336.3 |

|

|

|

9.8% |

|

|

|

306.3 |

|

|

|

3.9% |

|

|

|

294.7 |

|

| Adjusted EBITDA (note 1) |

|

|

352.3 |

|

|

|

15.5% |

|

|

|

305.1 |

|

|

|

3.2% |

|

|

|

295.6 |

|

| Net income |

|

|

130.5 |

|

|

|

(16.6%) |

|

|

|

156.4 |

|

|

|

(4.9%) |

|

|

|

164.5 |

|

| EPS – basic |

|

|

1.22 |

|

|

|

(26.5%) |

|

|

|

1.66 |

|

|

|

(5.7%) |

|

|

|

1.76 |

|

| EPS – diluted |

|

|

1.22 |

|

|

|

(26.1%) |

|

|

|

1.65 |

|

|

|

(5.2%) |

|

|

|

1.74 |

|

| Adjusted EPS – basic (note 1) |

|

|

1.69 |

|

|

|

(8.6%) |

|

|

|

1.85 |

|

|

|

(1.1%) |

|

|

|

1.87 |

|

| Adjusted EPS – diluted (note 1) |

|

|

1.69 |

|

|

|

(8.2%) |

|

|

|

1.84 |

|

|

|

(0.5%) |

|

|

|

1.85 |

|

| Cash dividends declared per common share |

|

|

0.45 |

|

|

|

7.1% |

|

|

|

0.42 |

|

|

|

13.5% |

|

|

|

0.37 |

|

|

|

|

|

|

|

| Total assets |

|

|

4,284.7 |

|

|

|

83.0% |

|

|

|

2,341.9 |

|

|

|

19.5% |

|

|

|

1,959.6 |

|

| Total long-term debt |

|

|

1,020.5 |

|

|

|

179.3% |

|

|

|

365.4 |

|

|

|

18.1% |

|

|

|

309.3 |

|

|

|

|

|

|

|

| Cash flows |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| From operating activities |

|

|

285.7 |

|

|

|

|

|

|

|

205.5 |

|

|

|

|

|

|

|

207.2 |

|

| Used in investing activities |

|

|

(1,136.6) |

|

|

|

|

|

|

|

(252.4) |

|

|

|

|

|

|

|

(174.3) |

|

| From (Used) in financing activities |

|

|

995.1 |

|

|

|

|

|

|

|

(44.3) |

|

|

|

|

|

|

|

(24.7) |

|

|

|

|

|

|

|

| Outstanding common shares as at |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| December 31 |

|

|

114,081,229 |

|

|

|

|

|

|

|

94,435,898 |

|

|

|

|

|

|

|

93,836,258 |

|

| February 22, 2017 |

|

|

114,128,589 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Outstanding share options as at |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| December 31 |

|

|

3,655,020 |

|

|

|

|

|

|

|

2,980,601 |

|

|

|

|

|

|

|

2,676,568 |

|

| February 22, 2017 |

|

|

3,600,660 |

|

|

|

|

|

|

|

|