UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR FISCAL YEAR ENDED: August 31, 2021

OR

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to ______________

Commission file number: 333-85072

DBMM GROUP

DIGITAL BRAND MEDIA & MARKETING GROUP, INC.

WWW.DBMMGROUP.COM

(Name of small business issuer in its charter)

|

Florida |

59-3666743 |

|

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

845 Third Avenue, 6th Floor, New York, NY 10022

(Address of principal executive offices)

(646) 722-2706

(Issuer’s telephone number)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

Common Stock, $0.001 par value |

DBMM |

OTC Markets |

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” , “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

|

|

Non-accelerated filer |

☐ |

Smaller reporting company |

☒ |

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked prices of such common equity, as of the last business day of the registrants most recently completed fourth fiscal quarter: on August 31, 2021: $1,112,660

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date:

Common Stock, par value $.001 per share: 757,718,631 Outstanding as of November 5, 2021

DOCUMENTS INCORPORATED BY REFERENCE

If the following documents are incorporated by reference, briefly describe them and identify the part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (i) any annual report to security holders; (ii) any proxy or information statement; and (iii) any prospectus filed pursuant to Rule 424(b) or (c) of the Securities Act of 1933 (the “Securities Act”). The listed documents should be clearly described for identification purposes (e.g. annual reports to security holders for fiscal year ended December 24, 1980).

None

Transitional Small Business Disclosure Format (Check one): Yes ☐ No ☒

|

FORM 10-K |

||

|

For the Fiscal Years Ended August 31, 2021, and 2020 |

||

|

Page |

||

|

PART I |

||

|

Item 1. |

4 |

|

|

Item 1A. |

4 |

|

|

Item 1B. |

5 |

|

|

Item 2. |

5 |

|

|

Item 3. |

5 |

|

|

Item 4. |

5 |

|

|

PART II |

||

|

Item 5. |

6 |

|

|

Item 6. |

6 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operation |

7 |

|

Item 8. |

21 |

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

22 |

|

Item 9A (T). |

22 |

|

|

Item 9B. |

Other Information |

|

|

PART III |

||

|

Item 10. |

23 |

|

|

Item 11. |

25 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

26 |

|

Item 13. |

26 |

|

|

Item 14. |

26 |

|

|

PART IV |

||

|

Item 15. |

27 |

|

|

28 |

||

PART I

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements. These forward-looking statements are based largely on our expectations and are subject to a number of risks and uncertainties, many of which are beyond our control. Actual results could differ materially from these forward-looking statements as a result of, among other factors, risks related to the large amount of our outstanding term loans; history of net losses and accumulated deficits; reliance on third parties to market, sell and distribute our products; future capital requirements; competition and technical advances; reliance on a small number of customers for a significant percentage of our revenues; and other risks. In light of these risks and uncertainties, there can be no assurance that the forward-looking information contained in this Annual Report will in fact occur.

ITEM 1. DESCRIPTION OF BUSINESS

ABOUT OUR BRAND DIGITAL CLARITY

Digital Clarity is the trading brand for Stylar Limited, a wholly owned subsidiary of Digital Brand Media & Marketing Group, Inc (DBMM), through its office in London, England. The Company is a multi-service digital marketing agency which specializes in creating effective strategies and campaigns for clients across a range of vertical markets, working in four key areas:

|

• |

Search Engine Marketing – for search engines like Google, Yahoo Microsoft Bing |

|

|

• |

Analytics – measuring and analyzing web traffic to optimize performance. |

|

|

• |

Strategy & Consulting – digital transformation and marketing strategy. |

|

|

• |

Social Media – planning and measuring social metrics digitally in order to diagnose strategy. |

DBMM Group can leverage its team’s experience in digital media and provide leading strategy, deployment and measurement to its core markets in many industry sectors, from creative to traditional corporate. The vertical B2B sectors encompass areas such as B2B ecommerce, SaaS, Blockchain, Fintech, Software Sales and Technology.

The Company is rolling out the services of both the technology and marketing services offerings from its operating base in the UK with a plan to increase its presence into the larger markets in the US. namely Los Angeles and New York. The intent in fiscal year 2022 will be a strategy of cash infusion to immediately correlate to increased revenues. Growth is clearly a function of available capital. Fiscal year 2021 reflected the Company's continued progress by being awarded contracts for a number of new clients, in the midst of a very challenging year because of external factors beyond the Company’s control, specifically the pandemic and the SEC Matter awaiting the Commission’s final affirmation of the dismissal. The contract model strategy results in a full digital technology and marketing consultancy from design following an analysis of the client's analytics, then executing and stewarding the evolution of the model. The Company's mantra is "ROI is our DNA," the underlying focus for business development.

EMPLOYEES

As of August 31, 2021, the Company had 7 full-time employees.

COMPETITION

There is strong competition in the digital marketing arena, though with the right level of investment and marketing, Digital Clarity has a confident outlook in using its experience to win new business in both local and international markets. DBMM has significant business relationships in place because it has a differentiating model.

Smaller reporting companies are not required to provide the information required by this item.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. DESCRIPTION OF PROPERTY

DBMM's Corporate address is 845 Third Avenue, 6th Floor, New York, NY 10022. The operating headquarters is located in the UK as Stylar Ltd., trading as Digital Clarity. is on a month-to-month lease at $1,416, as it is evaluating larger quarters.

The U.S. Securities & Exchange Commission instituted an Administrative Proceeding, File No. 3-17990, on May 16, 2017 to revoke the Company's registration statement because of delinquent filings. A hearing was held on August 9, 2017 and the Initial Decision to revoke the registration was dated November 16, 2017. The order was subsequently remanded by order of the U.S. Supreme Court in December 2017. The Company responded to the Remand with evidence of mitigating circumstances under a Protective Order and filed all its delinquent filings: a Super 10-K for 2015-2016-2017 on May 31, 2018 and 10-Q's for 2018 1Q, 2Q on June 22, 2018 and 3Q on July 15, 2018, its due date.

The Hearing for January 15, 2019 was re-scheduled because of government shutdown. Digital Brand entered a Motion to Dismiss the Proceedings on March 19, 2019 based on being current as of July 2018, and all filings to date have been filed on time for the 2019 fiscal year. The facts were presented at the hearing. The Division did not support the dismissal in a response to which Digital Brand filed two Amendments to the Consolidated 10-K for 2015- 2016-2017 and the 10-K for 2018 on April 23 and 24, 2019 respectively, and Amendments No. 2 on October 1, 2019 to supersede language in Part II, Item 9A. On November 12, 2019, Carol Fox Foelak, Administrative Law Judge, Securities & Exchange Commission ordered an Initial Decision/Dismissal of the Proceeding. The Dismissal becomes effective under Rule 360 of the Commission's Rules of Practice, 17 C.F.R., Section 201.360, following the Commission’s Order of Finality. On December 3, 2019 The Division of Enforcement Submitted a Petition for Review of Judge Carol Fox Foelak’s Initial Decision dismissing the Administrative Proceedings rendered on November 12, 2019. The Company filed a Motion for summary affirmance of the Initial Decision on December 20, 2019. The Motion for Summary Affirmance was not opposed by Enforcement.

On January 25, 2021, the Commission denied the Company’s Motion for Summary Affirmance of Judge Carol Fox-Foelak’s Dismissal of November 12, 2019 and granted the Division’s Petition for Review and set a briefing schedule beginning February 24, 2021. The Commission concluded that “briefing in the ordinary course would...assist the Commission. This appeal raises issues as to which we have an interest in articulating our views and important matters of public interest, including the proper application of the standard that governs determination of sanctions in a Section 12(j) proceeding.” Both parties have briefed and concluded April, 2021. The Company is disappointed that so much time has been lost and intends to vociferously support the original Dismissal after two years.

From time to time, the Company has become or may become involved in certain lawsuits and legal proceedings which arise in the ordinary course of business. The Company intends to vigorously defend its positions. However, litigation is subject to inherent uncertainties and an adverse result in those or other matters may arise from time to time that may harm its financial position, or our business and the outcome of these matters cannot be ultimately predicted.

ITEM 4. MINE SAFETY DISCLOSURES

N/A

PART II

ITEM 5. MARKET FOR COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

MARKET INFORMATION

Our common stock is currently listed for quotation on the OTC under the symbol “DBMM”.

PER SHARE MARKET PRICE DATA

The following table sets forth, for the fiscal quarters indicated, the high and low closing bid prices per share for our common stock, as reported by on PinkSheets.com. Such quotations reflect inter-dealer prices, without retail markup, markdown or commission and may not represent actual transactions.

|

Year Ended August 31, 2021: |

High |

Low |

||||||

|

First Quarter |

$ | 0.007 | $ | 0.002 | ||||

|

Second Quarter |

$ | 0.0074 | $ | 0.0014 | ||||

|

Third Quarter |

$ | 0.0074 | $ | 0.001 | ||||

|

Fourth Quarter |

$ | 0.002 | $ | 0.0001 | ||||

|

Year Ended August 31, 2020: |

High |

Low |

||||||

|

First Quarter |

$ | 0.007 | $ | 0.0002 | ||||

|

Second Quarter |

$ | 0.007 | $ | 0.0017 | ||||

|

Third Quarter |

$ | 0.0032 | $ | 0.0015 | ||||

|

Fourth Quarter |

$ | 0.0076 | $ | 0.0015 | ||||

The last reported sale price of the common stock on the OTC Electronic Bulletin Board on August 31, 2021 and 2020 were $0.0015 and $0.0076 per share, respectively. As of August 31, 2021, and 2020, there were 120 holders of record of our common stock, respectively.

DIVIDENDS

We have never declared any cash dividends with respect to our common stock. Future payment of dividends is within the discretion of our board of directors and will depend on our earnings, capital requirements, financial condition and other relevant factors. Although there are no material restrictions limiting, or that are likely to limit our ability to pay dividends on our common stock, we presently intend to retain future earnings, if any, for use in our business and have no present intention to pay cash dividends on our common stock.

ITEM 6. SELECTED FINANCIAL DATA

As a “smaller reporting company”, as defined by Rule 10(f)(1) of Regulation S-K, the Company is not required to provide this information.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Readers are cautioned that certain statements contained herein are forward-looking statements and should be read in conjunction with our disclosures under the heading "Forward-Looking Statements" above. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. This discussion also should be read in conjunction with the notes to our consolidated financial statements contained in Item 8. "Financial Statements and Supplementary Data" of this Report.

OPERATIONS OVERVIEW/OUTLOOK

The Company developed a document called the Creds Deck which provides a description to prospective clients of Digital Clarity’s value proposition http://www.dbmmgroup.com/wp-content/uploads/2020/11/Digital-Clarity-Creds-Deck_DB64F.pdf.

Coronavirus lockdown initially halted, and even now has slowed down, many business processes starting from manufacturing, supply chain to logistics, and marketing. Digital Clarity is no exception, and the negative impact for over a year and a half, is measurable.

Some businesses have permanently closed or paused their digital marketing activities temporarily, because of this uncertainty. That mindset results in drastically decreased online traffic, sales, engagement, conversation, and pushed down search ranking. There are opportunities emerging, and Digital Clarity is actively pursuing new clients in a new environment.

Digital marketing is not a quick-fix solution to gain momentum. Therefore, it does not give companies visibility overnight. Many companies using digital marketing techniques such as search engine optimization (SEO) or social media marketing, are already aware that implementations take three to four months’ time to achieve positive results. Our company mantra remains, “ROI is our DNA.”

This means that although there has been a slowdown in existing business and new business development, there is a need for reinforcement of the digital values proposition to bring or maintain a company’s brand front and center. As a consultancy, we are delivering the message.

Operationally, fiscal year 2021 has been important in continuing the direction of the Company and steering it toward a scaled growth plan which has been in neutral while the Company addressed certain external challenges beyond its control. This has also been impacted by the worldwide pandemic of Covid-19. Nevertheless, the Company continued to focus on the positive, proven operating model and used that model to maintain certain existing clients and through its digital infrastructure, is perfectly placed to expand geographic reach to new clients in 2022.

Through a turbulent 2020 to date, DBMM continues to build on its strengths. Like the rest of the world, the effect of Covid-19 and the Pandemic that still persists are a paramount concern, the Company has strong relationships within the market and will continue to extend its business focus to a wide variety of industry verticals.

No one expected that the pandemic and the SEC matter, would remain open for as long as it has.

The heart of the business is its marketing consultancy. DBMM Group’s main business Digital Clarity works in the area of Digital Marketing and company transformation. Understanding each client and developing the model to individualize the outlook has been essential, is differentiating and is its competitive advantage. This kind of close relationship with its clients resulted in Digital Clarity being considered a close professional and trusted advisor.

WHY DIGITAL EXPERTS CONTINUE TO BE IN DEMAND

The world is changing, and technology is taking the lead. Today, everything is going digital -- entertainment, health, real estate, banking and even currencies. This is, however, understandable. In North America alone, 95% of the population are online (statista).

With everything turning to digital, it means companies are also jumping online to market their businesses. And to survive the challenges of digital marketing, brands need to keep up with the latest trends. Successfully reaching one’s target audience is no longer just putting out TV and print ads. These days, social media is the new arena of digital marketers, with Statista claiming 3.7 billion people are active social media users as of October 2021.

To keep up with the ever-changing scene, digital marketing experts need to stay in step with the evolving tech trends. Social media marketing companies like ours work tirelessly to research consumers and what makes them engage with brands. We try to find the best online solutions that will cater to our clients’ end-users’ queries in the easiest and most cost-efficient way possible -- be it by developing new technology or adapting to trends.

RELENTLESS DIGITAL GROWTH POSITIONS DIGITAL CLARITY AS A LEADER

The need for seasoned expertise and insight is in huge demand. Digital Clarity’s strength, heritage and reach in the digital marketing puts the DBMM brand in an excellent position for investment and growth. Digital Clarity’s strength in Search Engine Marketing, Analytics, Social Media, Strategic Company Transformation means that the Company is ready to feed on that demand and leapfrog into a powerful revenue focused vehicle.

SHOPPERS STILL USE A MIX OF DIGITAL TOUCHPOINTS DURING COVID-19 ALONG THE BUYING JOURNEY

|

● |

In the discovery and evaluation part of the journey, search engines, social media feeds, and influencers are popular ways for shoppers to get product inspiration outside a brand’s properties. |

|

● |

In the buying part of the journey, there are new types of purchase points emerge. Mobile wallets are behind e-mail as a place to make purchases. And 63% begin making purchase through social media. |

CUSTOMERS STILL FACE SILOS ACROSS CHANNELS – THE DIGITAL LANDCAPE THROUGH THE PANDEMIC

|

● |

Customers are accessing multiple touchpoints during a purchase but there is a significant disconnect within companies. |

|

● |

75% of consumers expect consistent interactions across all departments. |

|

● |

However, 58% say that they feel like they’re communicating with separate departments and not one company. |

|

● |

And when it comes to service issues, 70% of customers expect all of the reps to have the same information about them, but 64% say that they have to re-explain issues. |

AREAS THAT DIGITAL CLARITY EXCEL ARE AREAS THAT NEED TO BE CONSIDERED TODAY

|

● |

Market from Home - Deploy campaigns quickly from home, collaborate across teams and keep marketers engaged with apps |

|

● |

Engage Customers with Empathy - Listening to customers, use real-time data to better understand their current situation and needs |

|

● |

Personalize Digital Communications - Accelerate digital channel adoptions, deliver the right message, to the right person, at the right time |

|

● |

Optimize Budget Spends – Digital Clarity unify marketing performance and make real-time decisions to minimize the negative impact |

Among, its range of services, Digital Clarity help companies ‘get found’ on search engines like Google. The Market Share chart from Statista, we can see that Google has the lion’s share of the search market worldwide. As a Google Premier Partner, Digital Clarity are well placed to advise, consult and grow companies, in 2021 and beyond.

From Google’s parent Alphabet’s latest results, In the third quarter of 2020, Google's revenue amounted to 46.02 billion U.S. dollars, up from 37.99 billion U.S. dollars in the preceding quarter. Google's main revenue source is advertising through Google sites and its network.

HOW MACHINE LEARNING IS ENHANCING DIGITAL MARKETING STRATEGY

Digital Clarity applies strategy to algorithmic based machine learning tools. The launch of Google’s new machine learning tool, RankBrain which contributes to search engine results, left many people wondering what impact machine learning would have in the realm of Search Engine Optimization (SEO).

With the tech industry going crazy for all things Artificial Intelligence (AI), Natural Language Processing (NLP), machine learning, and chatbots – companies like Digital Clarity help brands make sense of this ever-changing landscape.

MACHINE LEARNING AND DIGITAL MARKETING

Because machine learning is being used to solve a huge set of diverse problems with the help of data, channels, content, and context, as marketers, Digital Clarity stands to benefit from this information and phenomenon as a whole. But, as the information we gather grows, digital marketing as we know it is set to change. Digital Clarity will be at the forefront of this change.

PAY PER CLICK (PPC) CAMPAIGNS

With Google launching new “smart” features such as Google Smart Bidding, Smart Display Campaigns, and In-Market Audience to help businesses maximize conversions, it is clear that the future of PPC lies in machine learning.

To become more strategic and take PPC campaigns to the next level for its clients, Digital Clarity:

|

● |

Get to grips with the metrics that are most valuable to your business |

|

● |

Understand obstacles that could get in the way of meeting your goals |

|

● |

Know the underlying performance drivers to make more strategic decisions |

SEARCH - OVERALL

Search makes up half (52%) of advertising spend, increasing on par at 15% to £3.3bn, next is non-video display at £1.33bn (+9%), then video display £967m (40%). Classifieds remains at £726m and other remained at £41m.

DIGITAL CLARITY EMBRACE GOOGLE’S MACHINE LEARNING MARKETING SUITE

Machine learning and AI have grown at a rapid pace and are an integral part of day to day search advertising management and planning. Though machine learning has been an integral part of the ad world, what has been more significant has been the addition of Artificial Intelligence or AI. According to a recent report in The Harvard Business Review by Deloitte, AI in Digital Marketing is not just getting bigger, it’s getting far more persuasive

MIT researchers recently unveiled a chip that can perform inference using neural network computations three to seven times faster than previous chips, and with up to 95 percent less power consumption. Dozens of companies working on new generations of AI chips—for use both in and outside of data centers—are attracting significant investment. These companies raised more than $1.5 billion in funding last year, nearly twice the amount they raised the year before.

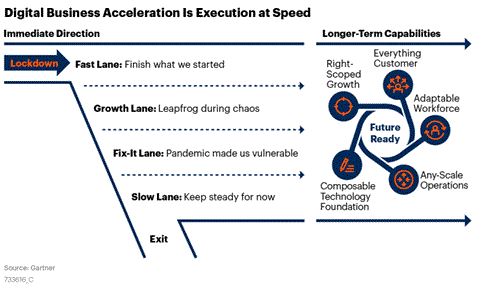

DIGITAL CLARITY PERFECTLY POSITIONED FOR THE FUTURE

According to Gartner's Digital Business Acceleration report: Where to Focus Now, Enterprises have the intention of becoming more digital due to COVID-19.

CONTENT MARKETING

Although still extremely important, the internet has become inundated with too much content. There is consensus among companies that in order to succeed, brands need to be creating content that is valuable to readers. To do this, you need to understand consumer trends, data and engagement. Machine learning tools alongside Digital Clarity’s strategic approach allows its clients to reduce the amount of time spent tracking data, as well as better decipher that data to create actionable tasks that will lead to success.

DIGITAL MARKETING SERVICES

There is no denying that 2020/21 has proved challenging for Digital Marketing Services. When the pandemic hit in March 2020, many companies’ long-term plans and strategies were thrown out the window, as everyone from the frontlines to the C-suite shifted into fire-fighting mode. Many worked around the clock by leveraging remote technology.

Most businesses, except for those engaged in essentials, have been at a standstill and enterprises are cutting back on costs. The axe falls on marketing. The virus has brought most scheduled digital marketing plans to a grinding halt or slowed them down. The impact is felt in digital marketing, with predicted patterns now appearing skewed.

During the main part of the lock-down., Google announced $800 million in funding and grants for businesses advertisers. It has on offer $ 340 million in credits for active advertisers. The clear opportunity is at the foundation of the Company, namely the need to expedite and continue to encourage development in the digital marketing services sector. The marketing services product is labour intensive and thus the Company must jumpstart the growth by significant capital to grow simultaneously in multiple geographies.

The Company’s outlook remains robust for 2022 and the foreseeable future, particularly as businesses adjust and redirect their retail business to online digital marketing in the COVID / Post COVID world.

KEY MILESTONES

During the fiscal 2021, revenues decreased due to external circumstances out of the company’s control which placed enormous pressure on the operating business.

Despite these circumstances, the client base is expanding in base number and the size of client serviced. At any point in time, our clients represent a variety of industries. Many of these clients choose to operate under an NDA as our clients see DBMM as a competitive advantage. Under that disclaimer, we cannot share all clients’ names, but here are a few key clients representing diverse verticals, as follows:

|

|

1. |

Leading project management software and solution provider to the construction industry Kahua Inc, announced it was ramping up growth using the power of digital marketing in partnership with digital consultancy, Digital Clarity. |

|

2. |

Digital Clarity shortlisted for prestigious UK Search Awards in the hotly contested ‘Best Use of Search’ along with client Bentley SYNCHRO, a global construction project management software company that supports the professional needs of those responsible for creating and managing the world’s infrastructure. |

|

3. |

Synergy SKY, a Norwegian based company that develops and markets software platforms to manage all meetings and video conferences, announce online marketing partnership with Digital Clarity. |

|

4. |

Digital Clarity release SEO Guides for business during Covid-19 Pandemic. The company has a long history with Google search both paid and organic, with these guides specifically focusing on three core areas: |

|

● |

The Importance of a Strong Internal Linking Strategy |

|

● |

How to Get to the Top of Google |

|

● |

How Much Does SEO Cost? |

|

5. |

The Luxury Property Show partners with Digital Clarity. The Luxury Property Show at Olympia London and is the only event in Europe dedicated to luxury and high-value property aimed at High-net-Worth Individuals. |

Other examples are representative of the diversity of client base. DBMM's approach using a client's analytics and executing an individualized model to increase ROI as the prime objective, spans a wide range of industries.

Digital Clarity’s services are in demand and the company is pursuing opportunities in Formula 1, Aviation and high-end marketing for Luxury Brands.

Core industry verticals for Digital Clarity include: FinTech, Unified Communication Companies and discretionary advice for professional service providers.

SEARCH ENGINE OPTIMIZATION EVOLUTION

From an SEO point of view, keywords could become less important. Search engines receive more revenue for ads when they provide users with higher quality content. As a result, the algorithm they use needs to be more focused on providing each user with content that will serve a specific purpose, rather than be packed with the right keyword density. Therefore, the need to start thinking about the quality of your content as a ranking factor on search engines. This is where Digital Clarity comes in to help shape content ‘in the right way’ to direct potential buyers to the client’s website.

THE NEXT-GENERATION SEARCH ENGINE MARKET SET TO GROW 25.5% DURING 2021-2026

Over the last few years, the number of voice searches witnessed an exponential growth rate. Also, it is becoming less of a novelty and more like a new standard. Therefore, the next-generation search engines are more oriented toward voice-based search engines.

Next-generation search engines are also increasing because of deep neural networks, machine learning, and other advancements in AI technologies. Virtual assistants, such as smart speakers, are used for various applications across several end-user industries, such as retail, BFSI, and healthcare. One major consumer-facing application is as a personal assistant. It helps consumers accomplish various tasks. For instance, Apple's Siri offers an intuitive interface for connected homes or cars.

These assistants' capabilities can be personalized based on the end-user, thereby improving customer experience in various industries. Thus, although the personal segment holds a significant position, the commercial segment holds a massive opportunity to expand over the forecast period, owing to the growing industrial applications. For instance, virtual assistants can help customers find a doctor's office in the healthcare sector, fill and refill a prescription, and receive payment reminders.

Moreover, the voice search mobility trend is growing at a high pace with the advancements in speech recognition technology or voice search technology. Google has a 95% accuracy rate when spoken correctly in English. Moreover, Google voice search on smartphones is available in over 60 languages.

Personalized responses are one of the famous use cases of voice search, which Google has attained to a large extent, as Google can know and guess the next question the users will be most likely to ask. On the other hand, Alexa cannot understand the context to the same extent as Google. Alexa relies on custom-built skills and protocols, whereas the Google Assistant can understand specific user requests and further personalize the response.

THE GROWTH OF DIGITAL MARKETING & CONSULTANCY SERVICES

The skill set historically owned by agencies offering disciplines such as UX, design, creativity, customer-centric data analytics and customer engagement is now being immersed with large consultancy businesses whose traditional bread and butter was Digital Transformation.

Accenture, Deloitte, IBM, KPMG, McKinsey and PricewaterhouseCoopers rank among the most aggressive players in acquiring and partnering with agencies such as Digital Clarity. They present not only an opportunity for Digital Clarity but also a prospective exit and investment opportunity.

Digital Clarity have continued to develop their Digital Consulting and Strategy Planning offering. The forward looking program is to be a recognized leader in this field and fulfill companies seeking Digital Transformation for their originations.

THE NEED FOR PROFESSIONAL CONSULTANCY AND OPPORTUNITY FOR MASSIVE GROWTH

Four consultancies lead Ad Age's ranking of the 10 largest agency companies in the world. With combined revenue of $13.2 billion, the marketing services units of Accenture, PwC, IBM and Deloitte sit just below WPP, Omnicom, Publicis Groupe, Interpublic and Dentsu. Last year, only two consultancies—Accenture Interactive and IBM iX—made the top 10. IBM iX was the first to break into the top 10.

Given the experience of the team, Digital Clarity’s advisory and consultancy is in demand. With the recent growth in these business areas, and the rise of consultancies, it is confirmation that Digital Clarity is headed in the right direction for growth.

THE GROWTH OF DIGITAL TRANSFORMATION WORLDWIDE

The Global Digital Transformation Market size is expected to reach $1,302.9 billion by 2027, rising at a market growth of 20.8% CAGR during the forecast period. Digital transformation is considered as the utilization of digital technology. Digitally transformed enterprises can be flexible to the changing technological landscape and can address abrupt shifts in the industry, particularly the one presently created by the COVID-19 pandemic; studies show that the efficiency and rate of adaptation of digitally transformed companies to a post-pandemic era are relatively larger than conventional businesses. Source

Digital Clarity can help various businesses that have been considerably affected by the global outbreak of the COVID-19 pandemic. One of the significant challenges for the global economy in 2020 was to facilitate business continuity in the midst of social distancing guidelines, lockdowns norms, work-from-home culture, and other operational challenges. The lack of availability of digital strategies, infrastructure, or tools worsens the challenges for various companies that were needed to abruptly shift operations online or allow workers to work from their homes.

The situation, on the other hand, resulted in a considerable surge in awareness regarding the urgent requirement for digital transformation across a majority of the industries and created some lucrative opportunities for the global market. Companies are getting more aware of the advantages of digital transformation, particularly in the work-from-home culture that needs a business to allow the employees to easily learn, collaborate and perform organizational functions across remote locations.

DIGITAL CONTINUES TO DRIVE GROWTH IN CONSULTING

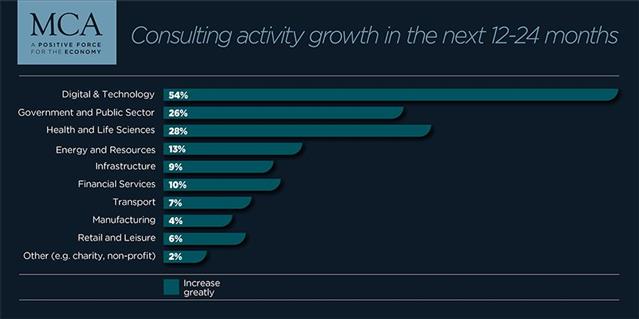

Such is the dominance of US consulting, that its status as the world’s largest consulting market barely bears mentioning anymore. The global consulting market grew by about 8% to $160 billion in 2020, but accounting for 44% of that, the US saw another year of meteoric growth last year according to Source Global Research. While it is still undeniably America first when it comes to consulting, however, the battle to be the second largest consulting market is much more tightly contested.

Despite slowed growth in the UK, the management consulting market in the UK has remained the globe’s second largest. Nearest rival Germany accounts for 0.3% less of the global consulting market than Britain.

THE IMPORTANCE OF STRATEGIC CONSULTANCY IN 2021 AND BEYOND

Across industries, organizations are accelerating digital transformation processes for long-term growth and profitability. Yet: “53% of the organizations surveyed remain untested in the face of digital challenge and their digital transformation readiness therefore uncertain.” This report from Gartner highlights the need embrace change.

Businesses had no choice but to respond quickly to challenging conditions. Although not formally classed as ‘agile’, the twists and turns of the pandemic have required executives to innovate on the fly and collaborate to get things done. This has been compounded by working from home, which has cut out distractions and created more time for ‘deep thinking’.. Regardless of headcount, a return to more stable trading conditions shouldn’t mean running back to the standard practices and silos that previously slowed marketers down.

Adobe says that, Business-to-business (B2B) commerce will continue to undergo a major transformation in 2021 as companies adopt the latest technologies to find new customers, improve their supply-chain efficiencies, and provide a more personalized user experience to their clientele.

Digital Clarity has created a unique Diagnosis Workshop that helps brands identify needs as well as assess the opportunity available. The core focus is to help reduce wastage and increase results.

Areas of focus include:

|

● |

Cost analysis |

|

● |

Audit current channels |

|

● |

Digital strategy planning |

|

● |

ROI projection planning |

|

● |

Digital consulting and training |

GLOBAL AD SPEND CONTINUES

|

● |

Global advertising spend is expected to grow by 10.4.% or US$60bn to US$634bn |

|

● |

Spend will rise past pre-pandemic levels, a year sooner than previously predicted |

|

● |

All regions forecast to return to growth in 2021 with Canada, the US and Australia expected to be fastest growing markets in 2021 |

|

● |

Digital continues to drive recovery, returning to double digit growth. It will represent 50.0% share of global spend this year |

Advertising investment is forecast to grow by 10.4% globally in 2021, according to the latest dentsu Ad Spend Report.

COMPETITIVE LANDSCAPE

Digital advertising is the fastest-growing segment of the global market for advertising spending. The increasing use of smartphones and the availability of cheap internet services are the two major factors propelling the growth prospects for this market. More than 30% of the companies are planning to spend around 75% of their advertising expenditures on digital marketing within the next five years.

“U. S. Marketers are expected to spend $110.1 billion on digital ads this year, or 51% of the $214.6 billion total U.S. advertising spending forecast, excluding political ads. Newspapers, radio, magazines, and local television now account for just 21% of the U.S. ad market.” From The Wall Street Journal

DIGITAL CLARITY HAS A COMPETITIVE ADVANTAGE

Digital Clarity operate in a highly commoditized market but have over the years build a stellar reputation that makes it different from its competitors. Some of these areas include:

|

1. |

Our DNA is Strategically Driven |

We believe the path to successful customer acquisition lies in understanding a client’s business – not just running a campaign. We seek to help clients understand that success has to be objective and measurable.

|

2. |

We are Business Led |

Digital marketing is not a cost but an asset. Not a line in a spreadsheet but an emotive force that if done right, will bring real business change and growth.

|

3. |

We are Digital Thinkers |

Marketing has to be at the heart of the business. Delivering real innovation in digital marketing requires not just knowledge but authority and bravery. We think digital. We drive results.

|

4. |

Our goal is to deliver Digital Performance |

We help our clients to understand their goals and objectives, using digital marketing to drive new business opportunities and retain their current customers.

In April 2020, HIS Markit, research firm, reported: “Each dollar that companies spent on advertising in the United States last year, led to $9 in sales.

THE GROWTH OF B2B SOCIAL MEDIA

2020 will go down as the year that marketing was pulled into the boardroom. 80% of senior executives said the role of marketing in setting strategy has expanded since the pandemic. Traditional consumers have moved online, making the digital environment even more important right now.

This priority has raised the profile of marketing as companies scramble to understand the digital-first consumer. The battleground for 2021 will be about speed and agility. Now that many companies have treasure troves of data, the difference is how fast they can personalise the experience and respond to consumer behaviour. Expect to see more investment and innovation in technology infrastructure alongside marketing.

|

● |

40% of B2B content marketers increased their investment in social media and online communities in response to COVID-19. |

|

● |

76% of B2B organizations use social media analytics to measure content performance. |

|

● |

By 2025, 80% of B2B sales interactions will occur on digital channels. |

|

● |

U.S. B2B business will spend an estimated $1.64 billion on LinkedIn ads in 2021, $1.99 billion in 2022, and $2.33 billion in 2023. |

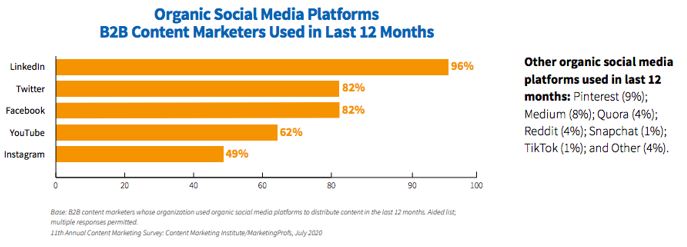

Almost all B2B content marketers (96%) use LinkedIn. They also rated it as the top-performing organic platform.

GROWTH IN LINKEDIN ADVERTISING SET TO SOAR TILL 2023

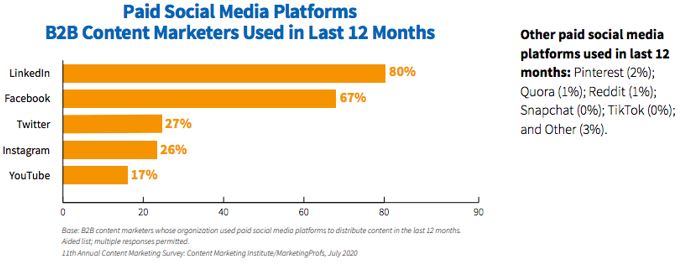

For paid social posts, the picture is similar but not identical.

LinkedIn again comes out on top (80%).

But Facebook outranks Twitter and Instagram outranks YouTube.

GLOBAL B2B ECOMMERCE SALES IN 2021

In the US alone, B2B eCommerce sales will hit $1.184 trillion by the end of 2021.

The predominance of B2B ecommerce means that B2B businesses must improve and simplify their shopping journey, channeling the B2C ordering experience. The B2B shopping experience is a lot more complicated than that of a B2C buyer.

Because of the nature of the transaction, B2B buyers usually need to go through various steps, including sales representative interaction, negotiations, and approvals before they can make a successful purchase. In short, B2B eCommerce businesses must adapt to a more seamless transaction building advanced functionality quote management, price negotiation, easy ordering, order and inventory management for the B2B market.

According to Forbes Magazine in 2021 the largest ecommerce markets are:

|

1 |

China: |

$636 billion |

|

2 |

United States: |

$504 billion |

|

3 |

Japan: |

$104 billion |

|

4 |

United Kingdom: |

$86 billion |

|

5 |

Germany: |

$70 billion |

|

6 |

France: |

$43 billion |

|

7 |

South Korea: |

$37 billion |

|

8 |

Canada: |

$30 billion |

|

9 |

Russia |

$20 billion |

|

10 |

Brazil |

$19 billion |

US B2B DIGITAL AD MARKET SET FOR POST PANDEMIC GROWTH

According to eMarketer's July 2021 forecast, 2023 will be a pivotal year for the US B2B digital ad market as spending approaches $15 billion. By then, the seismic transformation spurred by the pandemic will be permanent.

Last year, US B2B pivoted from in-person channels to digital ads to reach audiences. In 2021, the growth in digital ad spending will be even greater than was originally estimated by eMarketer, indicating the shift to digital isn’t slowing down.

Digital ads will also remain a more prevalent part of the B2B media mix in the coming years.

US B2BS SPEND ON LINKEDIN DISPLAY

LinkedIn makes up the largest share of US B2B display in 2021 with 32.2% of the $5.09 billion that will be spent on B2B display this year. We estimate US B2B LinkedIn display ad revenues will be $1.64 billion in the US, growing 27.1% from 2020 when $1.29 billion was spent on LinkedIn B2B display.

US B2BS SPEND ON SEARCH TO INCREASE

In 2021, US B2Bs will spend $5.36 billion on search ads, more than what will be allocated to display.

But search’s growth rate isn’t as strong: It will increase by 19.5% from 2020.

THE NEW NORMAL WILL BE DIGITAL

In just one-year, digital adoption has happened at five to ten times the projected rate.

Lockdown periods, economic uncertainty and loss of predictability have forced customers and businesses online in previously unseen numbers. This migration has upset the power balance, with customers now more in control of the relationship and less loyal to brands and products. On top of that, 60% of companies have seen new buying behaviours such as changes to average basket size and product interests.

Pandemic disruption is also causing many businesses to demand a similar level of convenience to consumers. When we return to normal, there’s no question that the new normal will be digital.

GROWTH IN INVESTOR AWARENESS AND OUTREACH.

During 2022, Digital Brand Media & Marketing Group, Inc. will initiate a significant effort to raise positive awareness of DBMM's growth potential on a global basis. The Company had to continue to defer its 2020/21 plans until certain SEC Matters regarding the delinquent filings brought current in July 2018, remain open. The global pandemic made it impossible to initiate any Investor Awareness Program.

Hopefully in 2022 the strategic outreach will be directed at investors around the world who understand the digital marketplace and its expanding influence on consumer decisions. DBMM will target new investors through a global digital and traditional integrated investor outreach campaign which will be run by Digital Clarity, with third parties, as required, for distribution. In all areas, the Company will act in the interests of all stakeholders.

In the full industry context of dramatic expansion of digital footprints, there has been no direct correlation between DBMM's revenues and its share price. Economic and industry analysts have opined that the industry multiple continues to grow to, in some cases, 25-30 times revenues. DBMM will expand its client and geographic scale, thus increasing revenues. There were matters outside of DBMM's control which caused growth to be in neutral, and in 2020/21 the pandemic threw all planning into disarray. With capital infusion, 2022 will follow the model of a growing client base and geographic reach until it achieves a TBD level of profitability. We anticipate the benchmark will replicate successful industry models in digital technology, marketing and company transformation.

FINANCIAL OVERVIEW/OUTLOOK

DBMM has been honing its commercial model since the acquisition of Digital Clarity (“DC”) in 2011 which has been cash-flow positive as an operating company since its acquisition. External events outside of DBMM's control has precluded the growth expected to this point, however, its margins will continue to be strong on an annual basis, and once the business reaches appropriate scale with assumed profitability and cross-over point, DBMM trajectory suggests a resultant very successful business for all of its stakeholders.

The growth trajectory anticipated is expected during 2022, following capital infusion and return to normal trading. Once that occurs, the clients benefit immediately due to a wider range of resources; the shareholders will benefit as the market cap grows. The media market multiple far exceeds the “old” manufacturing multiples, as digital technology and marketing has become one of the fastest growing industries in the world today.

DBMM's place in the sector is strong. The industry environment continues to grow exponentially and the future of digital marketing as an essential strategy for any consumer-facing business has been proven over-and-over as certain retail businesses are forced to close their doors for lack of or an ineffective digital presence. DBMM's brand, Digital Clarity, increases its valuation with client case studies and industry awards resulting in its being considered a leader in the sector for its size. DBMM's increasing client base, coupled with decreasing certain kind of debt and expenses, positions the Company to attract mezzanine financing, something sought after by many and achieved by few.

Coincidently, 2020/21 results have slowed down temporarily due to Brexit unease in the UK and clients concern about trade issues with or without the European Union. So in the midst of the uncertainty caused by the Brexit slowdown, the COVID -19 global outbreak has caused further slowdown as clients paused and business development much different during an initial lockdown , then lifted only to be reinstated on November 5, 2020. That only made the uncertainty further exacerbated, while clients need to extend or double down on their digital footprint as the industry has become essential during the pandemic. Nevertheless, Digital Clarity is revising its model to adjust to changing circumstances, when client revenues are paused or delayed.

The Company received a commitment for future working capital in order to grow the Company in key markets, with the intent to move to DBMM profitability following a return to normal trading. At that point, DBMM would not require future financing until it was ready to acquire 1-2 additional companies to complement and further develop the digital marketing business. Growth capital will increase as the client base re-balanced and expands in size and scope.

Going forward, there will be an emphasis on investor awareness as soon as the SEC dismissal has been affirmed by the full commission. DBMM has been current in its filings since July 2018 and is encouraged by the outlook after normal trading has recommenced. DBMM intends to make significant strides in aggressively widening its brand exposure using a variety of digital and social channels. There are investors around the globe who understand the digital marketplace and its increasing influence on consumer decisions. DBMM will be targeting these new investors in the public market through a global digital and traditional, integrated campaign which will be run by Digital Clarity, with third parties, as required for distribution.

The expectations for fiscal year 2022 remain to return to normal trading following affirmance of the dismissal by the full commission. The Company intends to move ahead thereafter to the scaled, growth plan in multiple geographies to benefit all stakeholders, being mindful of the impact of the global pandemic.

During fiscal 2021, and to a lesser extent, in fiscal 2020, we successfully reached agreements with certain lenders resulting in gain on extinguishment for loans payable which amounted to the difference between the carrying value and the revised amount of the obligations. The gain on extinguishment of principal and accrued interest amounted to $169,837 and $57,802 and during fiscal 2021 and 2020, respectively.

We also successfully reached an agreement with a holder of convertible debentures aggregating $249,800 to modify its terms. Such debentures are no longer convertible, are now non-interest bearing, and have been reclassified to loans payable. It also resulted in a decrease in derivative liabilities and an increase in additional paid-in capital of approximately $260,000 during fiscal 2021.

We have not issued convertible debentures since 2015.

Fiscal Year 2021

We had approximately $10,000 in cash and our working capital deficiency amounted to approximately $5.5 million at August 31, 2021.

During fiscal 2021, we used cash in our operating activities amounting to approximately $437,000. Our cash used in operating activities was comprised of our net loss of approximately $701,000 adjusted primarily for the following:

Accounts payable, accrued expenses, accrued interest, and accrued compensation, of approximately $273,000, resulting from a short fall in liquidity and capital resources, which is net of gain on extinguishment of debt of approximately $170,000.

During fiscal 2021, we generated cash from financing activities of approximately $410,000 which primarily consists of the proceeds from demand notes payable of approximately $398,000, offset by an increase in officer loans of approximately $ 12,000.

Fiscal Year 2020

We had approximately $34,000 in cash and our working capital deficiency amounted to approximately $5.1 million at August 31, 2020.

During fiscal 2020, we used cash in our operating activities amounting to approximately $276,000. Our cash used in operating activities was comprised of our net loss of approximately $656,000 adjusted primarily for the following:

Accounts payable, accrued expenses, accrued interest, and accrued compensation, of approximately $332,000, resulting from a short fall in liquidity and capital resources, which is net of gain on extinguishment of debt of approximately $58,000.

During fiscal 2020, we generated cash from financing activities of approximately $281,000 which primarily consists of the proceeds from demand notes payable of approximately $348,000, offset by repayments and officer loans of $ 67,000.

Going Concern

The accompanying consolidated financial statements have been prepared on a going concern basis. The financial statements do not reflect any adjustments that might result if The Company is unable to continue as a going concern.

The Company has outstanding loans and convertible notes payable aggregating $2.2 million at August 31, 2021 and doesn’t have sufficient cash on hand to satisfy such obligations. The preceding raise substantial doubt about the ability of the Company to continue as a going concern. However, the Company generated proceeds of approximately $410,000 from financing activities during fiscal 2021. The Company also has a non-binding Commitment Letter from an investor of $250,000 which also includes a right of first refusal on additional capital raise up to $3 million which will contribute to satisfying such obligations and fund any potential cash flow deficiencies from operations for the foreseeable future.

Accordingly, the accompanying consolidated financial statements have been prepared in conformity with U.S. GAAP, which contemplates continuation of the Company as a going concern and the realization of assets and satisfaction of liabilities in the normal course of business. The carrying amounts of assets and liabilities presented in the financial statements do not necessarily purport to represent realizable or settlement values. The financial statements do not include any adjustment that might result from the outcome of this uncertainty.

RESULTS OF OPERATIONS

Comparison of Results for fiscal 2021 and 2020

|

Consolidated Operating Results |

||||||||||||||||

|

For the Years Ended August 31, |

||||||||||||||||

|

Increase/ |

Increase/ |

|||||||||||||||

|

(Decrease) |

(Decrease) |

|||||||||||||||

|

2021 |

2020 |

$ 2021 vs 2020 |

% 2021 vs 2020 |

|||||||||||||

|

SALES |

$ | 171,712 | $ | 268,957 | $ | (97,245 |

) |

(36 |

)% |

|||||||

|

COST OF SALES |

167,669 | 241,665 | (73,996 |

) |

(31 |

)% |

||||||||||

|

GROSS PROFIT |

4,043 | 27,292 | (23,249 |

) |

(85 |

)% |

||||||||||

|

COSTS AND EXPENSES |

||||||||||||||||

|

Sales, general and administrative |

557,427 | 434,164 | (123,263 |

) |

28 |

% |

||||||||||

|

TOTAL OPERATING EXPENSES |

557,427 | 434,164 | (123,263 |

) |

28 |

% |

||||||||||

|

OPERATING LOSS |

(553,384 |

) |

(406,872 |

) |

146,512 | 36 |

% |

|||||||||

|

OTHER (INCOME) EXPENSE |

||||||||||||||||

|

Interest expense |

327,271 | 318,500 | 8,771 | 3 |

% |

|||||||||||

|

Other income |

- | (12,728 |

) |

(12,728 |

) |

NM | ||||||||||

|

Gain on extinguishment of debt |

(169,837 |

) |

(57,802 |

) |

112,035 | NM | ||||||||||

|

Change in fair value of derivative liability |

(9,170 |

) |

944 | (10,114 |

) |

NM | ||||||||||

|

TOTAL OTHER EXPENSE |

148,264 | 248,914 | (100,650 |

) |

(40 |

)% |

||||||||||

|

NET LOSS |

$ | (701,650 |

) |

$ | (655,786 |

) |

$ | 45,864 | 7 |

% |

||||||

NM: not meaningful

We currently generate revenue through our Pay-Per-Click Advertising, Search Engine Marketing, Search Engine Optimization Services, Web Design, Social Media, Digital analytics and Advisory Services.

Our primary sources of revenue are Per-Click Advertising, Web Design, and Advisory Services, which amounted to 38%, 33% and 21% of our revenues during fiscal 2021.

Revenue is recognized upon transfer of control of promised or services to customers in an amount that reflects the consideration the Company expect to receive in exchange for those services. The Company enter into contracts that can include various combinations of services, which are generally capable of being distinct and accounted for as separate performance obligations. Revenue is recognized net of any taxes collected from customers, which are subsequently remitted to governmental authorities.

The decrease in our revenues during fiscal 2021, when compared to the prior year, is due to Brexit unease in the UK and clients concern about trade issues with or without the European Union, and the uncertainty associated with COVID-19 and its impact on Digital Clarity’s clients.

Cost of sales during fiscal 2021 decreased primarily from a reduction a correlated decrease in revenues.

The increase in general and administrative costs during fiscal 2021, when compared to the prior year, is primarily as a result of lower than usual professional fees and travel expenses due to COVID-19 in fiscal 2020 and lower UK tax credits.

The increase in interest expense, which include interest accrued on certain notes and loans, is primarily lower rate payable under certain unsecured loans payable in fiscal 2021 when compared to the prior year. Additionally, the Company’s gain on extinguishment of debt increased in fiscal 2021 primarily as a result of successful modification of terms on larger notes. The remaining other income and expenses did not significantly change between fiscal 2021 and 2020.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK.

As a “smaller reporting company”, as defined by Rule 10(f)(1) of Regulation S-K, the Company is not required to provide this information.

ITEM 8. CONSOLIDATED FINANCIAL STATEMENTS

|

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS |

|

|

Page |

|

|

F-1 |

|

|

F-2 |

|

|

F-3 |

|

|

F-4 |

|

|

Consolidated Statements of Cash Flows for the years ended August 31, 2021 and 2020 |

F-5 |

|

F-6 |

|

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of Digital Brand Media & Marketing Group, Inc.

Opinion on the Financial Statements

We have audited the accompanying balance sheets of Digital Brand Media & Marketing Group, Inc. (the Company) as of August 31, 2021 and 2020, and the related consolidated statements of operations and comprehensive loss, changes in stockholders’ deficit, and cash flows for each of the years in the two-year period ended August 31, 2021, and the related notes (collectively referred to as the financial statements). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of August 31, 2021 and 2020, and the results of its operations and its cash flows for each of the years in the two-year period ended August 31, 2021, in conformity with accounting principles generally accepted in the United States of America.

Going Concern

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the financial statements, the Company has suffered net losses from operations and has a net capital deficiency, which raises substantial doubt about its ability to continue as a going concern. Management’s plans regarding those matters are discussed in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB .

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and the significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe our audits provide a reasonable basis for our opinion.

Critical Audit Matters

The critical audit matter communicated below is a matter arising from the current period audit of the financial statements that were communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the financial statements, taken as a whole, and we are not, by communicating the critical audit matters below, providing separate opinion on the critical audit matters or on the accounts or disclosures to which they relate.

As discussed in Note 7 to the financial statements, the company has a derivative liability due to a tainted equity environment.

To evaluate the appropriateness of the fair value determined by management, we examined and evaluated the inputs management used in calculating the fair value of the stock-based compensation. To evaluate the appropriateness of the estimates used by the derivative specialist, we examined and evaluated the inputs the specialist used in calculating the value of the derivatives.

/s/ M&K CPAS, PLLC

M&K CPAS, PLLC

We have served as the Company’s auditor since 2020

Houston, TX

|

November 5, 2021 |

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

|

August 31, |

August 31, |

|||||||

|

2021 |

2020 |

|||||||

|

ASSETS |

||||||||

|

CURRENT ASSETS |

||||||||

|

Cash |

$ | 9,787 | $ | 34,461 | ||||

|

Accounts receivable, net |

16,251 | 15,333 | ||||||

|

Prepaid expenses and other current assets |

470 | 470 | ||||||

|

Total current assets |

26,508 | 50,264 | ||||||

|

Property and equipment - net |

1,420 | 1,978 | ||||||

|

TOTAL ASSETS |

$ | 27,928 | $ | 52,242 | ||||

|

LIABILITIES AND STOCKHOLDERS' DEFICIT |

||||||||

|

CURRENT LIABILITIES |

||||||||

|

Accounts payable and accrued expenses |

$ | 657,275 | $ | 438,246 | ||||

|

Accrued interest |

643,331 | 587,397 | ||||||

|

Accrued compensation |

1,439,886 | 1,436,686 | ||||||

|

Derivative liability |

506,360 | 773,676 | ||||||

|

Loans payable, net |

1,648,248 | 980,109 | ||||||

|

Officers loans payable |

89,709 | 77,044 | ||||||

|

Convertible debentures, net |

590,991 | 840,791 | ||||||

| 5,575,800 | 5,133,949 | |||||||

|

Loan payable, net of short-term portion |

46,192 | 49,656 | ||||||

|

TOTAL LIABILITIES |

5,621,992 | 5,183,605 | ||||||

|

STOCKHOLDERS' DEFICIT |

||||||||

|

Preferred stock, Series 1, par value .001; authorized 2,000,000 shares; 1,995,185, and 1,995,185 shares issued and outstanding |

1,995 | 1,995 | ||||||

|

Preferred stock, Series 2, par value .001; authorized 2,000,000 shares; 0 and 0 shares issued and outstanding |

- | - | ||||||

|

Common stock, par value .001; authorized 2,000,000,000 shares; 757,718,631, and 757,718,631, shares issued and outstanding |

757,718 | 757,718 | ||||||

|

Additional paid in capital |

9,528,590 | 9,270,444 | ||||||

|

Other comprehensive loss |

(35,984 | ) | (16,787 | ) | ||||

|

Accumulated deficit |

(15,846,383 | ) | (15,144,733 | ) | ||||

|

TOTAL STOCKHOLDERS' DEFICIT |

$ | (5,594,064 | ) | $ | (5,131,363 | ) | ||

|

TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT |

$ | 27,928 | $ | 52,242 | ||||

See Notes to Consolidated Financial Statements

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

|

For the year ended |

||||||||

|

August 31, 2021 |

August 31, 2020 |

|||||||

|

SALES |

$ | 171,712 | $ | 268,957 | ||||

|

COST OF SALES |

167,669 | 241,665 | ||||||

|

GROSS PROFIT |

4,043 | 27,292 | ||||||

|

COSTS AND EXPENSES |

||||||||

|

Sales, general and administrative |

557,429 | 434,164 | ||||||

|

TOTAL OPERATING EXPENSES |

557,429 | 434,164 | ||||||

|

OPERATING LOSS |

(553,386 | ) | (406,872 | ) | ||||

|

OTHER (INCOME) EXPENSE |

||||||||

|

Interest expense |

327,271 | 318,500 | ||||||

|

Other income |

- | (12,728 | ) | |||||

|

Gain on extinguishment of debt |

(169,837 | ) | (57,802 | ) | ||||

|

Change in fair value of derivative liability |

(9,170 | ) | 944 | |||||

|

TOTAL OTHER EXPENSES, NET |

148,264 | 248,914 | ||||||

|

NET LOSS |

$ | (701,650 | ) | $ | (655,786 | ) | ||

|

OTHER COMPREHENSIVE LOSS |

||||||||

|

Foreign exchange translation |

(19,197 | ) | (26,003 | ) | ||||

|

COMPREHENSIVE LOSS |

(720,847 | ) | (681,789 | ) | ||||

|

NET LOSS PER SHARE |

||||||||

|

Basic and diluted |

$ | (0.00 | ) | $ | (0.00 | ) | ||

|

WEIGHTED AVERAGE NUMBER OF SHARES |

||||||||

|

Basic and diluted |

757,718,631 | 757,718,631 | ||||||

See Notes to Consolidated Financial Statements

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' DEFICIT

|

For the Year Ended August 31, |

||||||||

|

2021 |

2020 |

|||||||

|

Series 1 |

||||||||

|

Preferred Stock |

||||||||

|

Shares, beginning and end of year |

1,995,185 | 1,995,185 | ||||||

|

Preferred Stock |

||||||||

|

Balance, beginning and end of year |

$ | 1,995 | $ | 1,995 | ||||

|

Series 2 |

||||||||

|

Preferred Stock |

||||||||

|

Shares, beginning and end of year |

- | - | ||||||

|

Preferred Stock |

||||||||

|

Balance, beginning and end of year |

$ | - | $ | - | ||||

|

Common Stock |

||||||||

|

Shares, beginning and end of year |

757,718,631 | 757,718,631 | ||||||

|

Balance, beginning and end of year |

$ | 757,718 | $ | 757,718 | ||||

|

Additional paid-in capital |

||||||||

|

Balance, beginning of year |

$ | 9,270,444 | $ | 9,270,444 | ||||

|

Reclassification of liability contracts |

||||||||

|

From liability to equity contracts |

258,146 | - | ||||||

|

Balance, end of year |

$ | 9,528,590 | $ | 9,270,444 | ||||

|

Other Comprehensive Income (Loss) |

||||||||

|

Balance, beginning of year |

$ | (16,787 | ) | $ | 9,216 | |||

|

Other comprehensive income (loss) |

(19,197 | ) | (26,003 | ) | ||||

|

Balance, end of year |

$ | (35,984 | ) | $ | (16,787 | ) | ||

|

Accumulated Deficit |

||||||||

|

Balance, beginning of year |

$ | (15,144,733 | ) | $ | (14,488,947 | ) | ||

|

Net loss |

(701,650 | ) | (655,786 | ) | ||||

|

Balance, end of period |

$ | (15,846,383 | ) | $ | (15,144,733 | ) | ||

|

Total Stockholders' Deficit |

$ | (5,594,064 | ) | $ | (5,131,363 | ) | ||

See Notes to Consolidated Financial Statements

DIGITAL BRAND MEDIA & MARKETING GROUP, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

|

For the Year Ended |

||||||||

|

August 31, |

August 31, |

|||||||

|

2021 |

2020 |

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES |

||||||||

|

Net loss |

$ | (701,650 | ) | $ | (655,786 | ) | ||

|

Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

|

Depreciation |

558 | 45 | ||||||

|

Change in fair value of derivative liability |

(9,170 | ) | 944 | |||||

|

Bad debt expense |

- | (1,465 | ) | |||||

|

Gain on extinguishment of debt |

(169,837 | ) | (57,802 | ) | ||||

|

Changes in operating assets and liabilities: |

||||||||

|

Accounts receivable |

(386 | ) | 48,176 | |||||

|

Accounts payable and accrued expenses |

214,790 | 39,388 | ||||||

|

Accrued interest |

225,773 | 182,500 | ||||||

|

Accrued compensation |

3,200 | 168,397 | ||||||

|

NET CASH USED IN OPERATING ACTIVITIES |

(436,722 | ) | (275,603 | ) | ||||

|

CASH FLOWS FROM INVESTING ACTIVITIES |

||||||||

|

Purchase of equipment |

- | (521 | ) | |||||

|

NET CASH USED IN INVESTING ACTIVITIES |

- | (521 | ) | |||||

|

CASH FLOWS FROM FINANCING ACTIVITIES |

||||||||

|

Proceeds from loan payable |

398,497 | 347,728 | ||||||

|

Officer loans payable |

12,240 | (67,090 | ) | |||||

|

NET CASH PROVIDED BY FINANCING ACTIVITIES |

410,737 | 280,638 | ||||||

|

EFFECT OF VARIATION OF EXCHANGE RATE OF CASH |

||||||||

|

HELD IN FOREIGN CURRENCY |

1,311 | 12,384 | ||||||

|

NET INCREASE/(DECREASE) IN CASH |

(24,674 | ) | 16,898 | |||||

|

CASH - BEGINNING OF YEAR |

34,461 | 17,563 | ||||||

|

CASH - END OF YEAR |

9,787 | 34,461 | ||||||

|

Supplemental disclosures of cash flow information: |

||||||||

|

Cash paid for interest |

$ | - | $ | - | ||||

|

Cash paid for taxes |

$ | - | $ | - | ||||

|

Noncash financing and investing activities: |

||||||||

|

Reclassification of liability contracts |

$ | 258,146 | $ | - | ||||

See Notes to Consolidated Financial Statements

DIGITAL BRAND MEDIA & MARKETING GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 – ORGANIZATION, BASIS OF PRESENTATION AND GOING CONCERN

Nature of Business and History of the Company

Digital Brand Media & Marketing Group, Inc. (“The Company”) is an OTC:PK listed company. The Company was organized under the laws of the State of Florida on September 29, 1998.

The Company strategically focuses on developing the business of its wholly owned and revenue generating online marketing services company, Digital Clarity. With deep DNA in its operating market, blending the services of an experienced professional workforce leveraging a technology offering positions the Company in a strong, forward looking structure. Digital Clarity operates in the growing area of digital marketing that helps companies make the most of the digital economy focusing on areas such as Search Engine Marketing (Google, Yahoo! & Bing), Social Media (Twitter, Facebook & LinkedIn) and Internet Strategy Planning including Design, Analytics and Mobile Marketing.

Following the acquisition of Digital Clarity in 2011 the Company has been honing its business model to be the differentiating service provider in digital marketing space to its clients and prospective business as DBMM grows into one of the leaders in the industry going forward.

Today, DBMM Group crafts, designs and executes digital marketing strategies across multiple ad platforms and social media networks for a broad array of clients to help each of them establish a uniform brand identity across the digital universe. The product offering is a unique value proposition of intelligent analytics provided by an experienced digital marketing and technology team. Therefore, DBMM Group is a blend of data, strategy and creative execution.

Going Concern

The accompanying consolidated financial statements have been prepared on a going concern basis. The financial statements do not reflect any adjustments that might result if the Company is unable to continue as a going concern.

The Company has outstanding loans and convertible notes payable aggregating $2.2 million at August 31, 2021 and doesn’t have sufficient cash on hand to satisfy such obligations. The preceding raise substantial doubt about the ability of the Company to continue as a going concern. However, the Company generated proceeds of approximately $400,000 from financing activities during fiscal 2021. The Company also has a non-binding Commitment Letter from an investor of $250,000 which also includes a right of first refusal on additional capital raise up to $3 million which will contribute to satisfying such obligations and fund any potential cash flow deficiencies from operations for the foreseeable future.