Table of Contents

As filed with the Securities and Exchange Commission on November 16, 2012

1933 Act Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

| ¨ |

Pre-Effective Amendment No. | ¨ | Post-Effective Amendment No. |

MET INVESTORS SERIES TRUST*

(Exact Name of Registrant as Specified in Charter)

(800) 638-7732

(Area Code and Telephone Number)

5 Park Plaza – Suite 1900

Irvine, California 92614

(Address of Principal Executive Offices)

Elizabeth M. Forget

President

Met Investors Series Trust

5 Park Plaza

Suite 1900

Irvine, California 92614

(Name and Address of Agent for Service)

Copies to:

David C. Mahaffey, Esq.

Sullivan & Worcester LLP

1666 K Street, N.W.

Washington, D.C. 20006

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933, as amended.

Title of Securities Being Registered: Class A shares of beneficial interest, par value $0.001 per share, of the Registrant’s MetLife Aggressive Strategy Portfolio.

No filing fee is due because Registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended.

It is proposed that this filing will become effective on December 17, 2012 pursuant to Rule 488 under the Securities Act of 1933, as amended.

| * | On behalf of its MetLife Aggressive Strategy Portfolio |

Table of Contents

METROPOLITAN SERIES FUND

501 Boylston Street

Boston, Massachusetts 02116

December , 2012

Dear Contract Owner:

As an owner (“Contract Owner”) of a variable annuity or variable life insurance contract (the “Contract”) issued by Metropolitan Life Insurance Company or one of its affiliated insurance companies (each an “Insurance Company”), you have the right to instruct the Insurance Company how to vote certain shares of the Zenith Equity Portfolio (“MSF Portfolio”) of the Metropolitan Series Fund (“MSF”) at a Special Meeting of Shareholders to be held on February 22, 2013 (the “Meeting”). Although you are not directly a shareholder of MSF Portfolio, some or all of your Contract value is invested, as provided by your Contract, in MSF Portfolio. Accordingly, you have the right under your Contract to instruct the Insurance Company how to vote the MSF Portfolio shares that are attributable to your Contract at the Meeting. Before the Meeting, I would like your voting instructions on the important proposal described in the accompanying Prospectus/Proxy Statement.

The Prospectus/Proxy Statement describes the proposed reorganization of MSF Portfolio. All of the assets of MSF Portfolio would be acquired by MetLife Aggressive Strategy Portfolio (“MIST Portfolio”), a series of the Met Investors Series Trust, in exchange for shares of MIST Portfolio and the assumption by MIST Portfolio of the liabilities of MSF Portfolio. MIST Portfolio’s investment objective is substantially similar to that of MSF Portfolio, and MSF Portfolio’s and MIST Portfolio’s investment strategies are similar.

You will receive shares of MIST Portfolio having an aggregate net asset value equal to the aggregate net asset value of your MSF Portfolio’s shares immediately prior to the reorganization. You will receive Class A shares of MIST Portfolio in exchange for your Class A shares of MSF Portfolio. Details about MIST Portfolio’s investment objective, performance, and management team are contained in the attached Prospectus/Proxy Statement. For federal income tax purposes, the transaction is expected to be a non-taxable event for shareholders and Contract Owners.

The Board of Directors of MSF has approved the proposal for MSF Portfolio and recommends that you instruct the Insurance Company to vote FOR the proposal.

I realize that this Prospectus/Proxy Statement will take time to review, but your vote is very important. Please take the time to familiarize yourself with the proposal. If you attend the Meeting, you may give your voting instructions in person. If you do not expect to attend the Meeting, please complete, date, sign and return the enclosed voting instructions form in the enclosed postage-paid envelope. You may also transmit your voting instructions by telephone or through the Internet. Instructions on how to complete the voting instructions form or vote by telephone or through the Internet are included immediately after the Notice of Special Meeting.

If you have any questions about the voting instructions form please call MSF at 1-800-638-7732. If we do not receive your completed voting instructions form or your telephone or Internet vote within several weeks, you may be contacted by Computershare Fund Services, our proxy solicitor, who will remind you to pass on your voting instructions.

Thank you for taking this matter seriously and participating in this important process.

| Sincerely, | ||

| ||

| Elizabeth M. Forget | ||

| President | ||

| Metropolitan Series Fund | ||

Table of Contents

METROPOLITAN SERIES FUND

501 Boylston Street

Boston, Massachusetts 02116

Zenith Equity Portfolio

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To Be Held on February 22, 2013

To the Shareholders of Zenith Equity Portfolio:

NOTICE IS HEREBY GIVEN THAT a Special Meeting of the Shareholders of the Zenith Equity Portfolio of Metropolitan (“MSF”), a Delaware statutory trust, will be held at the offices of MetLife Advisers, LLC, 501 Boylston Street, Boston, Massachusetts 02116, on February 22, 2013 at 10:00 a.m. Eastern Time and any adjournments thereof (the “Meeting”) for the following purpose:

| 1. | To consider and act upon an Agreement and Plan of Reorganization (the “Plan”) providing for the acquisition of all of the assets of Zenith Equity Portfolio (“MSF Portfolio”) by MetLife Aggressive Strategy Portfolio (“MIST Portfolio”), a series of Met Investors Series Trust, in exchange for shares of MIST Portfolio and the assumption by MIST Portfolio of the liabilities of MSF Portfolio. The Plan also provides for the distribution of these shares of MIST Portfolio to shareholders of MSF Portfolio in liquidation and subsequent termination of MSF Portfolio. A vote in favor of the Plan is a vote in favor of the liquidation and dissolution of MSF Portfolio. |

The Board of Directors of MSF has fixed the close of business on November 30, 2012 as the record date for determination of shareholders entitled to notice of and to vote at the Meeting.

| By order of the Board of Trustees |

|

| Michael P. Lawlor |

| Assistant Secretary |

| Metropolitan Series Fund |

December , 2012

CONTRACT OWNERS WHO DO NOT EXPECT TO ATTEND THE MEETING ARE REQUESTED TO COMPLETE, SIGN, DATE AND RETURN THE ACCOMPANYING VOTING INSTRUCTIONS FORM IN THE ENCLOSED ENVELOPE, WHICH NEEDS NO POSTAGE IF MAILED IN THE UNITED STATES, OR FOLLOW THE INSTRUCTIONS IN THE MATERIALS RELATING TO TELEPHONE OR INTERNET VOTING. INSTRUCTIONS ON HOW TO COMPLETE THE VOTING INSTRUCTIONS FORM OR VOTE BY TELEPHONE OR OVER THE INTERNET ARE INCLUDED IMMEDIATELY FOLLOWING THIS NOTICE. IT IS IMPORTANT THAT YOU PROVIDE VOTING INSTRUCTIONS PROMPTLY.

Table of Contents

INSTRUCTIONS FOR SIGNING VOTING INSTRUCTIONS FORM

The following general rules for signing voting instructions forms may be of assistance to you and avoid the time and expense involved in validating your vote if you fail to sign your voting instructions form properly.

| 1. | INDIVIDUAL ACCOUNTS: Sign your name exactly as it appears in the registration on the voting instructions form. |

| 2. | JOINT ACCOUNTS: Either party may sign, but the name of the party signing should conform exactly to the name shown in the registration on the voting instructions form. |

| 3. | ALL OTHER ACCOUNTS: The capacity of the individual signing the voting instructions form should be indicated unless it is reflected in the form of registration. For example: |

| REGISTRATION |

VALID SIGNATURE | |

| CORPORATE ACCOUNTS |

||

| (1) ABC Corp. |

ABC Corp. | |

| (2) ABC Corp. |

John Doe, Treasurer | |

| (3) ABC Corp. |

John Doe | |

| (4) ABC Corp. Profit Sharing Plan |

John Doe, Trustee | |

| TRUST ACCOUNTS |

||

| (1) ABC Trust |

Jane B. Doe, Trustee | |

| (2) Jane B. Doe, Trustee |

Jane B. Doe | |

| CUSTODIAL OR ESTATE ACCOUNTS | ||

| (1) John B. Smith, Cust. |

John B. Smith | |

| (2) Estate of John B. Smith |

John B. Smith, Jr., Executor | |

After completing your voting instructions form, return it in the enclosed postage-paid envelope.

INSTRUCTIONS FOR VOTING BY TELEPHONE

To vote by telephone, follow the steps below.

| 1. | Read the accompanying proxy information and voting instructions form. |

| 2. | Call [1-800-337-3503]. |

| 3. | Follow the recorded instructions. Have your voting instructions form ready. |

You do not need to return your voting instructions form if you vote by telephone.

Table of Contents

INSTRUCTIONS FOR VOTING OVER THE INTERNET

To vote over the Internet, follow the steps below.

| 1. | Read the accompanying proxy information and voting instructions form. |

| 2. | Log on to www.proxy-direct.com. |

| 3. | Follow the on-screen instructions. |

You do not need to return your voting instructions form if you vote over the Internet.

* * *

If you have any questions about how to provide voting instructions, please call MSF at 1-800-638-7732.

Table of Contents

ACQUISITION OF ASSETS AND ASSUMPTION OF LIABILITIES OF

ZENITH EQUITY PORTFOLIO

a series of

Metropolitan Series Fund

501 Boylston Street

Boston, Massachusetts 02116

(800) 638-7732

BY AND IN EXCHANGE FOR SHARES OF

METLIFE AGGRESSIVE STRATEGY PORTFOLIO

a series of

Met Investors Series Trust

5 Park Plaza

Suite 1900

Irvine, California 92614

(800) 638-7732

PROSPECTUS/PROXY STATEMENT

DATED DECEMBER , 2012

This Prospectus/Proxy Statement is being furnished in connection with the proposed Agreement and Plan of Reorganization (the “Plan”) which will be submitted to shareholders of Zenith Equity Portfolio (“MSF Portfolio”) for consideration at a Special Meeting of Shareholders to be held on February 22, 2013 at 10:00 a.m. Eastern time at the offices of MetLife Advisers, LLC (“MetLife Advisers” or the “Adviser”), 501 Boylston Street, Boston, Massachusetts 02116, and any adjournments thereof (the “Meeting”).

GENERAL

Subject to the approval of MSF Portfolio’s shareholders, the Board of Trustees of Metropolitan Series Fund (“MSF”) has approved the proposed reorganization of MSF Portfolio, which is a series of MSF, into MetLife Aggressive Strategy Portfolio (“MIST Portfolio”), a series of Met Investors Series Trust (“MIST”). MSF Portfolio and MIST Portfolio are sometimes referred to in this Prospectus/Proxy Statement individually as a “Portfolio” and collectively as the “Portfolios.”

THE SECURITIES AND EXCHANGE COMMISSION HAS NOT DETERMINED THAT THE INFORMATION IN THIS PROSPECTUS/PROXY STATEMENT IS ACCURATE OR ADEQUATE, NOR HAS IT APPROVED OR DISAPPROVED THESE SECURITIES. ANYONE WHO TELLS YOU OTHERWISE IS COMMITTING A CRIMINAL OFFENSE.

Separate accounts established by Metropolitan Life Insurance Company (“MetLife”) and other affiliated insurance companies (each an “Insurance Company” and, collectively, the “Insurance Companies”) are the record owners of MSF Portfolio’s shares and at the Meeting will vote the shares of MSF Portfolio held in their separate accounts.

As an owner of a variable life insurance or annuity contract (a “Contract”) issued by an Insurance Company, you have the right to instruct the Insurance Company how to vote the shares of MSF Portfolio at the Meeting that are attributable to your Contract. Although you are not directly a shareholder of MSF Portfolio, you have this

Table of Contents

right because some or all of your Contract value is invested, as provided by your Contract, in MSF Portfolio. For simplicity, in this Prospectus/Proxy Statement:

| • | “Record Holder” of MSF Portfolio refers to each Insurance Company which holds MSF Portfolio’s shares of record, unless indicated otherwise in this Prospectus/Proxy Statement; |

| • | “shares” refers generally to your shares of beneficial interest in MSF Portfolio; and |

| • | “shareholder” or “Contract Owner” refers to you. |

In the reorganization, all of the assets of MSF Portfolio will be acquired by MIST Portfolio in exchange for Class A shares of MIST Portfolio and the assumption by MIST Portfolio of the liabilities of MSF Portfolio (the “Reorganization”). If the Reorganization is approved, Class A shares of MIST Portfolio will be distributed to each Record Holder in liquidation of MSF Portfolio, and MSF Portfolio will be terminated as a series of MSF. Immediately after the Reorganization, you will hold that number of full and fractional shares of MIST Portfolio which have an aggregate net asset value equal to the aggregate net asset value of the shares of MSF Portfolio you held immediately before the Reorganization.

MSF Portfolio is a separate diversified series of MSF, a Delaware statutory trust, which is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). MIST Portfolio is a separate diversified series of MIST, a Delaware statutory trust, which is also registered as an open-end management investment company under the 1940 Act. The primary investment objective of MSF Portfolio is substantially similar to that of MIST Portfolio, as follows:

| Portfolio |

Investment Objective | |

| MSF Portfolio |

Long-term capital appreciation. | |

| MIST Portfolio |

Growth of capital. |

This Prospectus/Proxy Statement explains concisely the information about MIST Portfolio that you should know before voting on the Reorganization. Please read it carefully and keep it for future reference. Additional information concerning each Portfolio and the Reorganization is contained in the documents described below, all of which have been filed with the Securities and Exchange Commission (“SEC”):

| Information about MSF Portfolio: |

How to Obtain this Information: | |

| Prospectus of MSF relating to MSF Portfolio, dated April 30, 2012

Statement of Additional Information of MSF relating to MSF Portfolio, dated April 30, 2012, as amended on June 6, 2012

Annual Report of MSF relating to MSF Portfolio for the year ended December 31, 2011

Semiannual Report of MSF relating to MSF Portfolio for the six month period ended June 30, 2012

|

Copies are available upon request and without charge if you:

• Write to MSF at the address listed on the cover page of this Prospectus/Proxy Statement; or

• Call (800) 638-7732 toll-free. |

-2-

Table of Contents

| Information about MIST Portfolio: |

How to Obtain this Information: | |

| Prospectus of MIST relating to MIST Portfolio, dated April 30, 2012, which accompanies this Prospectus/Proxy Statement

Statement of Additional Information of MIST relating to MIST Portfolio, dated April 30, 2012, as amended on June 6, 2012

Annual Report of MIST relating to MIST Portfolio for the year ended December 31, 2011

Semiannual Report of MIST relating to MIST Portfolio for the six month period ended June 30, 2012 |

Copies are available upon request and without charge if you:

• Write to MIST at the address listed on the cover page of this Prospectus/Proxy Statement; or

• Call (800) 638-7732 toll-free. | |

| Information about the Reorganization: |

How to Obtain this Information: | |

| Statement of Additional Information dated December , 2012, which relates to this Prospectus/Proxy Statement and the Reorganization | A copy is available upon request and without charge if you:

• Write to MIST at the address listed on the cover page of this Prospectus/Proxy Statement; or

• Call (800) 638-7732 toll-free. | |

You can also obtain copies of any of these documents without charge on the EDGAR database on the SEC’s Internet site at http://www.sec.gov. Copies are available for a fee by electronic request at the following e-mail address: publicinfo@sec.gov, or from the Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, 100 F Street, N.E., Washington, D.C. 20549.

Information relating to MSF Portfolio contained in the Prospectus of MSF dated April 30, 2012 (SEC File No. 811-03618) is incorporated by reference into this document. Information relating to MIST Portfolio contained in the Prospectus of MIST dated April 30, 2012 (SEC File No. 811-10183) is incorporated by reference into this document. (This means that such information is legally considered to be part of this Prospectus/Proxy Statement.) The Statement of Additional Information dated December , 2012 relating to this Prospectus/Proxy Statement and the Reorganization, which includes the Annual Report of MIST relating to MIST Portfolio for the year ended December 31, 2011 (SEC File No. 811-10183), the Semiannual Report of MIST relating to the MIST Portfolio for the six month period ended June 30, 2012 (SEC File No. 811-10183), the Annual Report of MSF relating to MSF Portfolio for the year ended December 31, 2011 (SEC File No. 811-03618), the Semiannual Report of MSF relating to MSF Portfolio for the six month period ended June 30, 2012 (SEC File No. 811-03618), and pro forma financial information of MIST relating to MIST Portfolio for the twelve month period ended June 30, 2012, is incorporated by reference into this document.

An investment in MIST Portfolio through a Contract:

| • | is not a deposit of, or guaranteed by, any bank |

| • | is not insured by the FDIC, the Federal Reserve Board or any other government agency |

| • | is not endorsed by any bank or government agency |

| • | involves investment risk, including possible loss of the purchase payment of your original investment |

-3-

Table of Contents

| Page | ||||

| 5 | ||||

| 5 | ||||

| 5 | ||||

| After the Reorganization, what shares of MIST Portfolio will I own? |

5 | |||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| Who will be the investment adviser of my Portfolio after the Reorganization? |

7 | |||

| How do the Portfolios’ investment objectives and principal investment strategies compare? |

7 | |||

| 7 | ||||

| 7 | ||||

| What will be the primary federal tax consequences of the Reorganization? |

9 | |||

| 10 | ||||

| What are the principal risks of investing in each Portfolio? |

10 | |||

| 17 | ||||

| How do the Portfolios’ investment objectives, principal investment strategies and risks compare? |

17 | |||

| 19 | ||||

| 20 | ||||

| 21 | ||||

| 24 | ||||

| 24 | ||||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

| 29 | ||||

| 29 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 31 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| A-1 | ||||

-4-

Table of Contents

THIS SECTION SUMMARIZES THE PRIMARY FEATURES AND CONSEQUENCES OF THE REORGANIZATION. IT MAY NOT CONTAIN ALL OF THE INFORMATION THAT IS IMPORTANT TO YOU. TO UNDERSTAND THE REORGANIZATION, YOU SHOULD READ THIS ENTIRE PROSPECTUS/PROXY STATEMENT AND THE EXHIBIT.

This summary is qualified in its entirety by reference to the additional information contained elsewhere in this Prospectus/Proxy Statement, the Prospectuses and Statements of Additional Information relating to the Portfolios and the form of the Agreement and Plan of Reorganization (the “Plan”), which is attached to this Prospectus/Proxy Statement as Exhibit A.

Why is the Reorganization being proposed?

The Reorganization is part of a restructuring designed to eliminate the offering of overlapping funds in the MetLife families of funds with similar investment objectives and similar principal investment strategies and that serve as funding vehicles for insurance contracts that are offered by affiliates of MetLife. The Adviser determined the Portfolios were similar, but MIST Portfolio offered greater diversification for its shareholders because it has greater flexibility to allocate its assets among a more diverse universe of Underlying Portfolios than in which MSF Portfolio invests, and may periodically adjust its allocations as appropriate. In addition to the Reorganization, the Adviser separately recommended that one of the three Underlying Portfolios (as defined below) in which MSF Portfolio invests its assets be merged into another portfolio. Moreover, the Portfolios’ Adviser has agreed to pay all of the costs of the Meeting and any adjourned session, all of the costs associated with this proxy solicitation and all of the expenses incurred in connection with the preparation of this Prospectus/Proxy Statement and any of its enclosures. Accordingly, the Trustees of MSF believe that the Reorganization is in the best interests of MSF Portfolio’s shareholders.

What are the key features of the Reorganization?

The Plan sets forth the key features of the Reorganization. For a complete description of the Reorganization, see Exhibit A. The Plan generally provides for the following:

| • | the in-kind transfer of all of the assets of MSF Portfolio to MIST Portfolio in exchange for Class A shares of MIST Portfolio; |

| • | the assumption by MIST Portfolio of all of the liabilities of MSF Portfolio; |

| • | the liquidation of MSF Portfolio by distribution of Class A shares of MIST Portfolio to MSF Portfolio’s Class A shareholders; and |

| • | the structuring of the Reorganization as a tax-free reorganization for federal income tax purposes. |

Subject to the required shareholder approval, the Reorganization is expected to be completed on or about April 29, 2013.

After the Reorganization, what shares of MIST Portfolio will I own?

If you own Class A shares of MSF Portfolio, you will own Class A shares of MIST Portfolio. The new shares you receive will have the same total value as your shares of MSF Portfolio as of the close of business on the day immediately prior to the Reorganization.

-5-

Table of Contents

How will the Reorganization affect me?

Total portfolio operating expenses for the twelve months ended June 30, 2012 for Class A shares of MSF Portfolio are 0.69%, while total portfolio operating expenses for the twelve months ended June 30, 2012 for the Class A shares of MIST Portfolio are 0.85%. However, as a result of the Reorganization, MIST Portfolio’s expenses are expected to be reduced to 0.81% for the Class A shares on a pro forma basis, which is higher than for the MFS Portfolio.

The Reorganization will not affect your Contract rights. The value of your Contract will remain the same immediately following the Reorganization. MIST Portfolio will sell its shares on a continuous basis at net asset value only to Insurance Companies. Each Insurance Company will keep the same separate account. Your Contract values will be allocated to the same separate account and that separate account will invest in MIST Portfolio after the Reorganization. After the Reorganization, your Contract values will depend on the performance of MIST Portfolio rather than on that of MSF Portfolio. Neither MIST Portfolio, MSF Portfolio nor their respective shareholders will bear any costs of the Meeting or any adjourned session, any of the costs associated with this proxy solicitation or any of the expenses incurred in connection with the preparation of this Prospectus/Proxy Statement or any of its enclosures. All of these costs and expenses will be paid by MetLife Advisers, the investment adviser to the Portfolios.

Although MSF Portfolio and MIST Portfolio have substantially similar investment objectives and similar investment strategies, all or a substantial portion of the shares of Underlying Portfolios held by MSF Portfolio may be sold in order to comply with the investment practices of MIST Portfolio in connection with the Reorganization. However, because each Portfolio operates as a fund of funds, the Portfolios do not pay transaction costs when buying or selling shares of Underlying Portfolios, so such costs will not be borne by the Portfolios’ shareholders.

Like MSF Portfolio, MIST Portfolio will declare and pay dividends from net investment income and will distribute net realized capital gains, if any, to the Insurance Company separate accounts (not to you) once a year. These dividends and distributions will continue to be reinvested by your Insurance Company in additional Class A shares of MIST Portfolio.

Will I be able to purchase and redeem shares, change my investment options, annuitize and receive distributions the same way?

The Reorganization will not affect your right to purchase and redeem shares, to change among the Insurance Company’s separate account options, to annuitize, or to receive distributions as permitted by your Contract. After the Reorganization, you will be able under your current Contract to purchase additional Class A shares of MIST Portfolio. For more information, see “Purchase and Redemption Procedures,” “Exchange Privileges” and “Dividend Policy” below.

How do the Trustees recommend that I vote?

The Board of Trustees of MSF, including the Trustees who are not “interested persons” of MSF (the “Independent Trustees”), as such term is defined in the 1940 Act, has concluded that the Reorganization would be in the best interests of MSF Portfolio and that the interests of the shareholders of MSF Portfolio would not be diluted as a result of the Reorganization. Accordingly, the Trustees have submitted the Plan for the approval of the shareholders of MSF Portfolio.

-6-

Table of Contents

THE TRUSTEES RECOMMEND THAT YOU VOTE FOR THE PROPOSED REORGANIZATION

The Board of Trustees of MIST has also approved the Plan on behalf of MIST Portfolio.

Who will be the investment adviser of my Portfolio after the Reorganization?

MetLife Advisers, LLC serves as the investment adviser to both Portfolios, and will continue to serve as the investment adviser to MIST Portfolio after the Reorganization. For more information, see “Comparison of the Portfolios—Who will be the adviser and portfolio manager of my Portfolio after the Reorganization? What will the management fee be after the Reorganization?”

How do the Portfolios’ investment objectives and principal investment strategies compare?

The investment objective of MSF Portfolio is substantially similar to that of MIST Portfolio, and the principal investment strategies of the Portfolios are similar. The investment objective of each Portfolio is non-fundamental, which means that it may be changed by vote of the Trustees and without shareholder approval.

Both Portfolios operate as funds of funds and invest their assets in other investment companies (the “Underlying Portfolios”) that are part of the MetLife families of funds. Although both Portfolios invest in Underlying Portfolios, there are some differences between the Portfolios. MSF Portfolio invests its assets on an equal basis among Pioneer Fund Portfolio, a separate portfolio of MIST, and Jennison Growth Portfolio and FI Value Leaders Portfolio, each of which is a separate portfolio of MSF. In contrast, MIST Portfolio invests substantially all its assets in shares of a wider range of Underlying Portfolios, which may be portfolios of MIST or MSF and it may periodically adjust those allocations as appropriate. In addition, MIST Portfolio has target allocations to equity and fixed income securities. For more information, see “Comparison of the Portfolios— How do the Portfolios’ investment objectives, principal investment strategies and risks compare?”

Are the risk factors for the Portfolios similar?

Yes. The risk factors are similar due to the substantially similar investment objectives and similar principal investment strategies of MSF Portfolio and MIST Portfolio. For more information, see “Comparison of the Portfolios—What are the principal risks of investing in each Portfolio?” and “Comparison of the Portfolios—Are there any other risks of investing in each Portfolio?”

How do the Portfolios’ fees and expenses compare?

MSF Portfolio offers one class of shares (Class A), while MIST Portfolio offers two classes of shares (Class A and Class B). Class B shares of MIST Portfolio are not involved in the Reorganization. You will not pay any initial or deferred sales charge in connection with the Reorganization.

The following tables allow you to compare the various fees and expenses, including the costs of investing in Underlying Portfolios, that you may pay for buying and holding Class A shares of each of the Portfolios. The information provided for “MIST Portfolio (Pro Forma)” shows you what fees and expenses, including the costs of investing in Underlying Portfolios, are estimated to be assuming the Reorganization takes place.

The amounts for the Class A shares of MSF Portfolio and MIST Portfolio set forth in the following table and in the example are based on the expenses for each Portfolio’s Class A shares for the twelve month period ended June 30, 2012. The amounts for Class A shares of MIST Portfolio (Pro Forma) set forth in the following table and example are based on what expenses of MIST Portfolio would have been for the period ended June 30, 2012, had the Reorganization taken place as of July 1, 2011.

-7-

Table of Contents

THESE TABLES DO NOT REFLECT THE CHARGES AND FEES ASSESSED BY THE INSURANCE COMPANY UNDER YOUR CONTRACT. IF THOSE FEES AND EXPENSES HAD BEEN INCLUDED, YOUR COSTS WOULD BE HIGHER.

Shareholder Fees (fees paid directly from your investment)—None

Annual Portfolio Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| MSF Portfolio | MIST Portfolio | MIST Portfolio (Pro Forma) |

||||||||||

| Class A | Class A | Class A | ||||||||||

| Management Fees |

0.00 | % | 0.09 | % | 0.07 | % | ||||||

| Distribution and/or Service (12b-1) Fees |

None | None | None | |||||||||

| Other Expenses |

0.02 | % | 0.01 | % | 0.03 | % | ||||||

| Acquired Fund (Underlying Portfolio) Fees and Expenses |

0.67 | % | 0.75 | % | 0.71 | % | ||||||

| Total Annual Gross Portfolio Operating Expenses and Acquired Fund (Underlying Portfolio) Fees and Expenses |

0.69 | % | 0.85 | % | 0.81 | % | ||||||

As an investor in an Underlying Portfolio, each Portfolio bears its pro-rata portion of the operating expenses of that Underlying Portfolio, including such Underlying Portfolio’s management fee. The percentage shown for Acquired Fund (Underlying Portfolio) Fees and Expenses shows the fees and expenses that each Portfolio incurred indirectly as a result of its investments in shares of the relevant Underlying Portfolios during the twelve month period ended June 30, 2012.

The tables below show examples of the total expenses you would pay on a $10,000 investment over one-, three-, five- and ten-year periods. The examples are intended to help you compare the cost of investing, including the cost of investing in the Underlying Portfolios, in MSF Portfolio versus MIST Portfolio and MIST Portfolio (Pro Forma), which assumes the Reorganization takes place. The examples assume a 5% average annual return, that you redeem all of your shares at the end of each time period and that you reinvest all of your dividends. The following tables also assume that total annual operating expenses remain the same. The examples are for illustration only, and your actual costs may be higher or lower.

THE EXAMPLES DO NOT REFLECT THE FEES, EXPENSES OR WITHDRAWAL CHARGES IMPOSED BY THE CONTRACTS FOR WHICH THE PORTFOLIOS SERVE AS INVESTMENT VEHICLES. IF THOSE FEES AND EXPENSES HAD BEEN INCLUDED, YOUR COSTS WOULD BE HIGHER.

Examples of Portfolio Expenses

| One Year | Three Years | Five Years | Ten Years | |||||||||||||

| MSF Portfolio |

||||||||||||||||

| Class A |

$ | 70 | $ | 221 | $ | 384 | $ | 859 | ||||||||

| MIST Portfolio |

||||||||||||||||

| Class A |

$ | 87 | $ | 271 | $ | 471 | $ | 1,049 | ||||||||

| MIST Portfolio (Pro Forma) |

||||||||||||||||

| Class A |

$ | 83 | $ | 259 | $ | 450 | $ | 1,002 | ||||||||

-8-

Table of Contents

What will be the primary federal tax consequences of the Reorganization?

Prior to and as a condition to the closing of the Reorganization, MSF Portfolio and MIST Portfolio will have received an opinion from the law firm of Sullivan & Worcester LLP that, while the matter is not entirely free from doubt: (1) no gain or loss will be recognized by MSF Portfolio or the separate accounts through which each Insurance Company owns its shares (“Record Holders”) for federal income tax purposes as a result of receiving shares of MIST Portfolio in connection with the Reorganization; (2) the holding period and aggregate tax basis of the shares of MIST Portfolio that are received by the Record Holders of MSF Portfolio will be the same as the holding period and aggregate tax basis of the shares of MSF Portfolio previously held by such Record Holders, provided that such shares of MSF Portfolio are held as capital assets; (3) the holding period and tax basis of the assets of MSF Portfolio in the hands of MIST Portfolio as a result of the Reorganization will be the same as the holding period and tax basis of such assets in the hands of MSF Portfolio immediately prior to the Reorganization; and (4) no gain or loss will be recognized by MIST Portfolio upon the receipt of the assets of MSF Portfolio in exchange for shares of MIST Portfolio and the assumption by MIST Portfolio of MSF Portfolio’s liabilities.

-9-

Table of Contents

What are the principal risks of investing in each Portfolio?

An investment in each Portfolio is subject to certain risks. There is no assurance that the investment performance of either Portfolio will be positive or that the Portfolios will meet their investment objectives. There are direct and indirect risks of investing in the Portfolios. The following disclosure highlights the principal risks associated with investment in each of the Portfolios.

Direct Risk of Investing in each of the Portfolios:

Performance Risk

The investment performance of a Portfolio that invests all or substantially all of its assets in Underlying Portfolios is directly related to the performance of the Underlying Portfolios. The ability of a Portfolio to meet its investment objective depends upon the allocation of the Portfolio’s assets among Underlying Portfolios and the ability of the Underlying Portfolios to meet their investment objectives. A Portfolio may not meet its investment objective, which could adversely affect its performance, if an Underlying Portfolio fails to execute its investment strategy effectively or the Portfolio allocates a significant portion of its assets to an Underlying Portfolio that performs poorly, including relative to other Underlying Portfolios. There can be no assurance that the investment objective of the Portfolio or any Underlying Portfolio will be achieved.

Direct Risk of Investing in MIST Portfolio only:

Asset Allocation Risk

The Portfolio’s ability to achieve its investment objective depends upon MetLife Advisers’ analysis of such factors as macroeconomic trends, outlooks for various industries and asset class valuations and MetLife Advisers’ ability to select the appropriate mix of asset classes based on its analysis of such factors. MetLife Advisers’ analysis, including any evaluations and assumptions regarding such trends, outlooks and valuations, may prove incorrect. The Portfolio may experience losses or poor relative performance if MetLife Advisers allocates a significant portion of the Portfolio’s assets to an asset class or subset of an asset class that does not perform as MetLife Advisers anticipated, including relative to other asset classes or other subsets of asset classes. The Portfolio may underperform funds that allocate their assets differently than the Portfolio, due to differences in the relative performance of asset classes and subsets of asset classes.

Indirect Risks (Direct Risks of Investing in the Underlying Portfolios) of Investing in each of the Portfolios:

Market Risk

An Underlying Portfolio’s share price can fall because of, among other things, weakness in the broad market, a particular industry or specific holding, or changes in general economic conditions, such as prevailing interest rates and investor sentiment. The market as a whole can decline for many reasons, including disappointing corporate earnings, adverse political or economic developments here or abroad, changes in investor psychology, or heavy institutional selling. The value of a particular investment may fall as a result of factors directly relating to the company that issued the investment, such as decisions made by its management or lower demand for the company’s products or services. A security’s value may also fall because of factors affecting not just the company but also companies in the same industry or in a number of different industries such as increases in production costs. In addition, an assessment by an Underlying Portfolio’s adviser of particular companies may prove incorrect, resulting in losses or poor performance by those holdings, even in a rising market. An Underlying Portfolio could also miss attractive investment opportunities if its adviser underweights markets or

-10-

Table of Contents

industries where there are significant returns, and could lose value if the adviser overweights markets or industries where there are significant declines. Stocks and other equity securities are generally considered to be more volatile than fixed income securities.

Markets tend to move in cycles with periods of rising prices and periods of falling prices. Like the stock market generally, the investment performance of an Underlying Portfolio will fluctuate within a wide range, so an investor may lose money over short or even long periods.

Significant disruptions to the financial markets could adversely affect the liquidity and volatility of securities. During periods of extreme market volatility, prices of securities may be negatively impacted due to imbalances between market participants seeking to sell particular securities or similar securities and market participants willing or able to buy such securities. As a result, the market price of a security held by an Underlying Portfolio could decline at times without regard to the financial condition of or specific events impacting the issuer of the security.

Stocks purchased in initial public offerings (“IPOs”) have a tendency to fluctuate in value significantly shortly after the IPO relative to the price at which they were purchased. These fluctuations could impact the net asset value and return earned on an Underlying Portfolio’s shares.

Foreign Investment Risk

Investments in foreign securities, including depositary receipts, tend to be more volatile and less liquid than investments in U.S. securities because, among other things, they involve risks not associated with investing in U.S. securities. These additional risks may adversely affect an Underlying Portfolio’s performance.

Investments in foreign securities, whether denominated in U.S. dollars or foreign currencies, are subject to political, social and economic developments in the countries and regions where the issuers operate or are domiciled or where the securities are traded.

Less information may be publicly available about foreign companies than about U.S. companies. Foreign companies are generally not subject to the same accounting, auditing and financial reporting standards and practices as are U.S. companies. In addition, an Underlying Portfolio’s investments in foreign securities may be subject to the risk of nationalization or expropriation of assets, imposition of currency exchange controls or restrictions on the repatriation of foreign currency and confiscatory taxation. Moreover, an Underlying Portfolio may have more limited recourse against an issuer than it would in the United States.

The costs of buying, selling and holding foreign securities, including brokerage, tax and custody costs, may be higher than those involved in domestic transactions. Foreign settlement and clearance procedures and trade regulations may involve certain risks (such as delays in payment for or delivery of securities) not typically associated with the settlement of U.S. investments.

To the extent an Underlying Portfolio owns foreign securities denominated in foreign currencies, directly holds foreign currencies or purchases and sells foreign currencies, changes in currency exchange rates may affect the Underlying Portfolio’s net asset value, as well as the value of dividends and interest earned, and gains and losses realized on the sale of foreign securities. An increase in the strength of the U.S. dollar relative to these other currencies may cause the value of an Underlying Portfolio to decline. Certain foreign currencies may be particularly volatile, and foreign governments may intervene in the currency markets, causing a decline in value or liquidity of an Underlying Portfolio’s foreign currency or securities holdings. Although an Underlying Portfolio may employ certain techniques, such as forward contracts and futures contracts, in an effort to reduce the risk of unfavorable changes in currency exchange rates, there is no assurance that those techniques will be effective. If such techniques are employed and are effective, they will generally reduce or eliminate the benefit of any changes in currency exchange rates that otherwise would have been favorable to the Underlying Portfolio.

-11-

Table of Contents

All of the risks of investing in foreign securities are typically increased by investing in emerging market countries. Generally, economic structures in these countries are less diverse and mature than those in developed countries, and their political systems are less stable. Investments in emerging market countries may be affected by national policies that restrict foreign investment in certain issuers or industries or that prevent foreign investors from withdrawing their money at will. Small securities markets and low trading volumes in emerging market countries can make investments illiquid and more volatile than investments in developed countries, and such securities may be subject to abrupt and severe price declines.

Market Capitalization Risk

Stocks fall into three broad market capitalization categories—large, medium and small. An Underlying Portfolio that invests primarily in one of these categories carries the risk that due to current market conditions that category may be out of favor with investors.

If valuations of large capitalization companies appear to be greatly out of proportion to the valuations of small or medium capitalization companies, investors may migrate to the stocks of small and medium-sized companies. Larger, more established companies may also be unable to respond quickly to new competitive challenges such as changes in technology and consumer tastes. Many larger companies also may not be able to attain the high growth rate of successful smaller companies, especially during extended periods of economic expansion.

Investing in medium and small capitalization companies may be subject to special risks associated with narrower product lines, more limited financial resources, fewer experienced managers, dependence on a few key employees, and a more limited trading market for their stocks, as compared with larger companies. In addition, securities of these companies are subject to the risk that, during certain periods, the liquidity of particular issuers or industries will shrink or disappear with little forewarning as a result of adverse economic or market conditions, or adverse investor perceptions, whether or not accurate. Securities of medium and smaller capitalization issuers may therefore be subject to greater price volatility and may decline more significantly in market downturns than securities of larger companies. Smaller and medium capitalization issuers may also require substantial additional capital to support their operations, to finance expansion or to maintain their competitive position; and may have substantial borrowings or may otherwise have a weak financial condition, and may be susceptible to bankruptcy. Transaction costs for these investments are often higher than those of larger capitalization companies. There is typically less publicly available information about small capitalization companies.

Some small and medium capitalization companies also may be relatively new issuers, which carries risks in addition to the risks of other medium and small capitalization companies. New issuers may be more speculative because such companies are relatively unseasoned. These companies will often be involved in the development or marketing of a new product with no established market, which could lead to significant losses.

Investment Style Risk

Different investment styles tend to shift in and out of favor depending upon market and economic conditions, as well as investor sentiment. An Underlying Portfolio may outperform or underperform other funds that employ a different investment style. An Underlying Portfolio may also employ a combination of styles that impact its risk characteristics. Examples of different investment styles include growth and value.

Growth stocks may be more volatile than other stocks because they are more sensitive to investor perceptions of the issuing company’s growth of earnings potential. Also, because growth companies usually invest a high portion of earnings in their business, growth stocks may lack the dividends of some value stocks that can cushion stock prices in a falling market. Growth oriented funds will typically underperform when value investing is in favor.

-12-

Table of Contents

Value stocks are those which are undervalued in comparison to their peers due to adverse business developments or other factors. Value investing carries the risk that the market will not recognize a security’s inherent value for a long time, or that a stock judged to be undervalued by an Underlying Portfolio’s Subadviser may actually be appropriately priced or overvalued. Value oriented funds will typically underperform when growth investing is in favor.

Portfolio Turnover Risk

The investment techniques and strategies utilized by the Underlying Portfolios might result in a high degree of portfolio turnover. In addition, the Underlying Portfolios’ turnover rates may vary significantly from time to time depending on economic and market conditions. Variations in portfolio turnover rates may also be due to a fluctuating volume of subscriptions and redemptions or due to a change in an Underlying Portfolio’s subadviser. High portfolio turnover rates will increase the Underlying Portfolios’ transaction costs, which can adversely affect the returns on the Portfolio’s investments in those Underlying Portfolios.

Indirect Risks of Investing in MSF Portfolio only:

Interest Rate Risk

The values of debt securities are subject to change when prevailing interest rates change. When interest rates go up, the value of existing debt securities and certain dividend paying stocks tends to fall. For an Underlying Portfolio that invests its assets in debt securities or stocks purchased primarily for dividend income, when interest rates rise, the value of your investment may decline. Alternatively, when interest rates go down, the value of debt securities and certain dividend paying stocks may rise. The interest earned on an Underlying Portfolio’s investments in fixed income securities may decline when prevailing interest rates decline.

Interest rate risk will affect the price of a fixed income security more if the security has a longer duration. Fixed income securities with longer durations will therefore generally be more volatile than similar fixed income securities with shorter durations. The average maturity and duration of an Underlying Portfolio’s fixed income investments will affect the volatility of the Underlying Portfolio’s share price.

Some debt securities grant the issuer the right to call or repay the debt before it is due and involve the risk that an issuer will repay the principal or repurchase the security before it matures. An Underlying Portfolio may buy another security with the proceeds, but that other security might pay a lower interest rate. Also, if an Underlying Portfolio paid a premium when it bought the security, it may receive less from the issuer than it paid for the security.

Credit and Counterparty Risk

The value of a debt security is directly affected by an issuer’s ability to pay principal and interest on time. Although securities issued or guaranteed by the U.S. Government are generally considered to be subject to a relatively low amount of credit risk, most securities issued by agencies and instrumentalities of the U.S. Government are not backed by the full faith and credit of the U.S. Government and are supported only by the credit of the issuing agency or instrumentality. If an Underlying Portfolio invests in debt securities, the value of your investment may be adversely affected if a security’s credit rating is downgraded, an issuer of an investment held by the Underlying Portfolio fails to pay an obligation on a timely basis, otherwise defaults, or is perceived by other investors to be less creditworthy.

An Underlying Portfolio may also be subject to the credit risk presented by another party (counterparty credit risk) to the extent it engages in transactions, such as securities loans, repurchase agreements or certain derivatives, which involve a promise by the counterparty to honor an obligation to the Underlying Portfolio. If an Underlying Portfolio engages in transactions with a counterparty, the value of your investment may be adversely affected if the counterparty files for bankruptcy, becomes insolvent, or otherwise becomes unable or unwilling to honor its obligation to the Portfolio.

-13-

Table of Contents

High Yield Debt Security Risk

High yield debt securities, or “junk bonds”, are securities which are rated below “investment grade” or are not rated but are of equivalent quality. An Underlying Portfolio with high yield debt securities generally will be exposed to greater market risk and credit and counterparty risk than an Underlying Portfolio that invests only in investment grade debt securities because issuers of high yield debt securities are less secure financially, are more likely to default on their obligations, and their securities are more sensitive to interest rate changes and downturns in the economy. In addition, the secondary market for lower-rated debt securities may not be as liquid as that for more highly rated debt securities. As a result, the Underlying Portfolio’s adviser may find it more difficult to value lower-rated debt securities or sell them and may have to sell them at prices significantly lower than the values assigned to them by the Underlying Portfolio.

An Underlying Portfolio that invests in high yield debt securities generally seeks to receive a correspondingly higher rate of interest to compensate it for the additional credit risk and market risk it has assumed. High yield debt securities range from those for which the prospect for repayment of principal and interest is predominantly speculative to those which are currently in default on principal or interest payments or whose issuers are in bankruptcy. High yield debt securities are not generally meant for short-term investing.

An Underlying Portfolio that invests in securities that are the subject of bankruptcy proceedings or otherwise in default or at risk of being in default as to the repayment of principal and/or interest at the time of acquisition by the Underlying Portfolio or that are rated in the lower rating categories by one or more nationally recognized statistical rating organizations (for example, Ca or lower by Moody’s and CC or lower by S&P or Fitch) or, if unrated, are judged by the Underlying Portfolio’s adviser to be of comparable quality high yield debt securities that are rated C or below, or (“distressed securities,”) will incur significant risk in addition to the risks generally associated with investments in high yield debt securities. Distressed securities frequently do not produce income while they are outstanding. An Underlying Portfolio may be required to bear certain extraordinary expenses in order to protect and recover its investment in distressed securities. An Underlying Portfolio investing in distressed securities will be subject to significant uncertainty as to when and in what manner and for what value the obligations evidenced by the distressed securities will eventually be satisfied.

Mortgage-backed and Asset-backed Securities Risk

Mortgage-backed securities generally represent a participation in, or are secured by, mortgage loans. Asset-backed securities are structured similarly to mortgage-backed securities, but instead of mortgage loans or interests in mortgage loans, the underlying assets may include such items as installment loan contracts, leases or various types of real and personal property and receivables from credit card agreements. Payment of interest on these securities and repayment of principal largely depend on the cash flows generated by the underlying assets backing the securities. The value of investments in mortgage-backed and asset-backed securities is subject to interest rate risk and credit risk. Like other debt securities, changes in interest rates generally affect the value of a mortgage-backed security or an asset-backed security. Additionally, some mortgage-backed securities may be structured so that they may be particularly sensitive to interest rates.

Mortgage-backed and asset-backed securities are subject to varying degrees of credit risk. Mortgage-backed securities that are issued or guaranteed by the U.S. Government, its agencies or instrumentalities are subject to a lower degree of credit risk than mortgage-backed securities that are not guaranteed by the U.S. Government, its agencies or instrumentalities and mortgage-backed and assetbacked securities that are issued by private issuers. Payment of principal and interest on mortgage-backed securities that are not guaranteed by the U.S. Government, its agencies or instrumentalities and mortgage-backed and asset-backed securities that are issued by private issuers may depend primarily or solely on the cash flows generated by the underlying assets backing those securities. In the event of failure of these securities to pay interest or repay principal, the assets backing these securities may be insufficient to support the payments on the securities.

-14-

Table of Contents

Mortgage-backed and asset-backed securities are also subject to prepayment risk, which is the risk that the principal amount owed may be prepaid voluntarily or as a result of refinancing or foreclosure of the underlying asset. Securities subject to prepayment risk generally offer less potential for gains when prevailing interest rates decline, and have greater potential for loss when interest rates rise, depending upon the coupon of the underlying securities. The impact of prepayments on the price of a security may be difficult to predict and may increase the volatility of the price. In addition, early repayment of principal amounts may expose an Underlying Portfolio to a lower rate of return if it reinvests the repaid principal in less attractive investments. Further, an Underlying Portfolio may buy mortgage-backed or asset-backed securities at a premium. Accelerated prepayments on these securities could cause an Underlying Portfolio to lose a portion of its principal investment represented by the premium the Underlying Portfolio paid.

Mortgage-backed and asset-backed securities are also subject to extension risk. When interest rates rise, repayments of mortgage-backed and asset-backed securities may occur more slowly than anticipated, extending the effective duration of these securities and locking in below market interest rates. This may cause an Underlying Portfolio’s share price to be more volatile as the value of the mortgage-backed and asset-backed securities becomes more sensitive to changes in interest rates.

The amount of market risk associated with mortgage-backed and asset-backed securities depends on many factors, including the deal structure, the quality of the underlying assets, the level of credit support, if any, provided for the securities, and the credit quality of the credit support provider, if any.

If an Underlying Portfolio purchases mortgage-backed or asset-backed securities that are subordinated to other interests in the same mortgage or asset pool, the Underlying Portfolio may only receive payments after the pool’s obligations to other investors have been satisfied. Defaults on the assets held by the pool may limit substantially the pool’s ability to make payments of principal or interest to an Underlying Portfolio as a holder of such subordinated interest, reducing the values of those securities and potentially rendering them worthless. The risk of defaults is generally higher in the case of pools that are backed by lower rated securities such as subprime obligations. An unexpectedly high or low rate of prepayments on a pool’s underlying assets may have a similar effect on subordinated securities. A mortgage or asset pool may issue securities subject to various levels of subordination; the risk of non-payment affects securities at each level, although the risk is greater in the case of more highly subordinated securities.

Derivatives Risk

An Underlying Portfolio may invest in derivatives to obtain investment exposure, enhance return or “hedge” or protect its assets from an unfavorable shift in the value or rate of a reference instrument. Derivatives can significantly increase an Underlying Portfolio’s exposure to market risk and credit and counterparty risk. Derivatives also involve special risks and costs. For example, derivatives may be illiquid and difficult to value.

When a derivative or other instrument is used as a hedge against an offsetting position that an Underlying Portfolio also holds, any loss generated by that derivative or other instrument will be substantially offset by the gains on the hedged security, and vice versa. To the extent an Underlying Portfolio uses a derivative security or other instrument for purposes other than as a hedge, or if an Underlying Portfolio hedges imperfectly, the Underlying Portfolio will be directly exposed to the risks of that derivative or other instrument and any loss generated by that derivative or other instrument will not be offset by a gain.

Due to their complexity, derivatives may not perform as intended. As a result, an Underlying Portfolio may not realize the anticipated benefits from a derivative it holds or it may realize losses. An Underlying Portfolio may not be able to terminate or sell a derivative under some market conditions, which could result in substantial losses.

-15-

Table of Contents

Derivative transactions may involve leveraging risk, which means adverse changes in the value or level of the underlying asset, reference rate or index can result in a loss substantially greater than the amount invested in the derivative itself. Certain derivatives have the potential for unlimited loss, regardless of the size of the initial investment. When an Underlying Portfolio uses derivatives for leverage, investments in the Underlying Portfolio will tend to be more volatile, resulting in larger gains or losses in response to market changes.

Each Portfolio currently claims an exclusion from the definition of the term “commodity pool operator” under the Commodity Exchange Act (the “CEA”), which means that it is not subject to registration or regulation as a commodity pool operator under the CEA. On February 9, 2012, the Commodity Futures Trading Commission (“CFTC”) adopted amendments to its rules that, upon effectiveness, may affect the Portfolio’s ability to continue to claim this exclusion. Under the amended CFTC rules, a Portfolio claiming the exclusion would be limited in its ability to use certain derivatives, such as futures, certain options, and swaps, after the effectiveness of the amended rules. If a Portfolio’s and/or an Underlying Portfolio’s use of derivatives would prevent the Portfolio from claiming the exclusion, then MetLife Advisers would be subject to registration and regulation in its capacity as the Portfolio’s commodity pool operator, and the Portfolio would be subject to regulation under the CEA. A Portfolio may incur additional expense as a result of the CFTC’s registration and regulation obligations and its and/or the Underlying Portfolios’ use of certain derivatives and other instruments may be limited or restricted.

Real Estate Investment Risk

Real estate investments are subject to market risk, interest rate risk and credit risk. The performance of an Underlying Portfolio that invests a substantial portion of its assets in the real estate industry or in securities related to the real estate industry may be adversely affected when the real estate market declines. When an Underlying Portfolio focuses its investments in particular sub-sectors of the real estate industry (e.g., apartments, retail, hotels, offices, industrial, health care) or particular geographic regions, the Underlying Portfolio’s performance would be especially sensitive to developments that significantly affected those particular sub-sectors or geographic regions. The shares of an Underlying Portfolio that concentrates its investments in the real estate industry may be more volatile compared to the value of shares of a portfolio with investments in a mix of different industries.

Investments in real estate investment trusts (“REITs”) may be particularly sensitive to falling property values and increasing defaults on real estate mortgages. Due to their dependence on the management skills of their managers, REITs may underperform if their managers are incorrect in their assessment of particular real estate investments. REITs are subject to heavy cash flow dependency, defaults by borrowers, self-liquidation and the possibility of failing to qualify for tax-free pass through of income under the Internal Revenue Code of 1986 or failing to maintain exemption from the Investment Company Act of 1940, as amended. An adverse development in any of these areas could cause the value of a REIT to fall and the performance of the Portfolio to decline. In the event an issuer of debt securities collateralized by real estate defaults, it is conceivable that a REIT could end up holding the underlying real estate. The disposition of such real estate could cause a REIT to incur unforeseen expenses that could reduce the value of the REIT.

Convertible Securities Risk

Investments in convertible securities may be subject to market risk, credit and counterparty risk, interest rate risk and other risks associated with investments in equity and fixed income securities, depending on the price of the underlying security and the conversion price. The value of a convertible security will tend to be more susceptible to fixed income security related risks (e.g., interest rate risk and credit risk) when the price of the underlying security is less than the price at which the convertible security may be converted into an equity security. Conversely, the value of a convertible security will tend to be more susceptible to equity security related risks (e.g., market risk) when the price of the underlying security is greater than the price at which the convertible

-16-

Table of Contents

security may be converted into an equity security. An issuer of convertible securities may have the right to buy back the securities at a time and a price that is disadvantageous to an Underlying Portfolio.

Investment Company and Exchange Traded Fund Risk

Investments in open-end and closed-end investment companies and exchange traded funds, or ETFs, involve substantially the same risks as investing directly in the instruments held by these entities. However, the total return from such investments will be reduced by the operating expenses and fees of the investment company or ETF. An investment company or ETF may not achieve its investment objective or execute its investment strategy effectively, which may adversely affect the Portfolio’s performance. The Portfolio must pay its pro rata portion of an investment company’s or ETF’s fees and expenses. Shares of a closed-end investment company or ETF may trade at a premium or discount to the net asset value of its portfolio securities depending on a variety of factors, including market supply and demand.

Are there any other risks of investing in each Portfolio?

Although not principal risks, each Portfolio also may be subject to the indirect risks described below.

Leveraging Risk

Derivatives and other transactions in which an Underlying Portfolio engages may give rise to a form of leverage. Transactions that may give rise to leverage include, among others, swap agreements, futures contracts, short sales, reverse repurchase agreements, loans of portfolio securities, and the use of when-issued, delayed delivery or forward commitment transactions. Leveraging may cause an Underlying Portfolio’s performance to be more volatile than if the Underlying Portfolio had not been leveraged. Leveraging may expose an Underlying Portfolio to losses in excess of the amounts invested or borrowed. An Underlying Portfolio will segregate or “earmark” liquid assets on its books in an amount sufficient to cover its obligations under the transaction that gives rise to leveraging risk. The use of leverage may cause an Underlying Portfolio to liquidate portfolio securities when it may not be advantageous to do so to satisfy its obligations or to meet segregation requirements.

How do the Portfolios’ investment objectives, principal investment strategies and risks compare?

The following table summarizes a comparison of MSF Portfolio and MIST Portfolio with respect to their investment objectives and principal investment strategies, as set forth more fully in the Prospectuses and Statement of Additional Information relating to the Portfolios.

| MSF Portfolio |

MIST Portfolio | |||

| Investment Objective | Long-term capital appreciation. | Growth of capital. |

-17-

Table of Contents

| MSF Portfolio |

MIST Portfolio | |||

| Principal Investment Strategies | The Portfolio seeks to achieve its investment objective by investing its assets equally among the Class A shares of the Underlying Portfolios, which are the Pioneer Fund Portfolio of MIST and the Jennison Growth Portfolio and FI Value Leaders Portfolio of the MSF, rather than in a portfolio of securities. The Portfolio’s actual allocations to the Underlying Portfolios could vary substantially from this equal division because of, for example, changes to the Underlying Portfolios’ asset values. MetLife Advisers, the adviser to the Portfolio, will rebalance the Portfolio’s holdings each fiscal quarter to maintain the Portfolio’s equal division of assets among the Underlying Portfolios. The Portfolio will invest at least 80% of its assets in equity securities. Each Underlying Portfolio has a different subadviser that will use a separate set of investment strategies, exposing each Underlying Portfolio to its own investment risks. | The Portfolio seeks to achieve its objective by investing substantially all of its assets in Class A shares of the Underlying Portfolios, which are portfolios of MIST and MSF. The Portfolio has a target allocation between the two broad asset classes (equity and fixed income). MetLife Advisers, the adviser to the Portfolio, establishes specific target investment percentages for the asset classes and the various components of each asset category. MetLife Advisers determines these target allocations based on a variety of factors, including its long-term outlook for the return and risk characteristics of the various asset classes and the relationship between those assets classes. MetLife Advisers then selects the Underlying Portfolios in which the Portfolio invests, based on, among other factors, the Underlying Portfolios’ investment objectives, policies, investment processes and portfolio analytical and management personnel.

Under normal circumstances, the Portfolio invests substantially all of its assets in Underlying Portfolios that may hold large cap, small cap, mid cap or foreign equity securities in accordance with target allocations of 100% to equity securities.

The foreign equity allocation may be invested in foreign equity securities of any capitalization or country but primarily will be invested in larger capitalization companies of developed countries.

The Portfolio seeks to achieve capital growth primarily through its investments in Underlying Portfolios that invest in equity securities. These investments may include Underlying Portfolios that invest mainly in stock of large established U.S. companies, as well, to a lesser extent, in stocks of foreign companies and small U.S. companies with above-average growth potential. |

-18-

Table of Contents

| MSF Portfolio |

MIST Portfolio | |||

| Periodically, MetLife Advisers will evaluate the Portfolio’s allocation between equity and fixed income, inclusive of the exposure to various investment styles and asset sectors, relative to the Portfolio’s risk profile. It is anticipated that changes between these broad asset classes will be within a range of plus or minus 10%. Concurrently, MetLife Advisers will consider whether to make changes to the Portfolio’s investments in any of the Underlying Portfolios. |

Although each Portfolio operates as a fund of funds that invests in Underlying Portfolios, there are some differences between the Portfolios. MSF Portfolio invests its assets on an equal basis among three Underlying Portfolios, while MIST Portfolio invests substantially all its assets in shares of a wider range of Underlying Portfolios of MIST and MSF and it may periodically adjust the allocations to these Underlying Portfolios as appropriate. The following chart describes the target allocations of MIST Portfolio, as of April 30, 2012, to equity securities.

| Asset Class |

Target Allocation | |||

| Equity |

85 | % | ||

| U.S. Large Cap |

38 | % | ||

| U.S. Mid Cap |

23 | % | ||

| U.S. Small Cap |

9 | % | ||

| Foreign Equity |

30 | % | ||

Although MIST Portfolio’s investments in the Underlying Portfolios will be made in an attempt to achieve these target allocations, the actual allocations to equity and fixed income securities may vary from its target allocations. Deviations from the asset class target allocations will affect the asset class subset target allocations. In addition, MIST Portfolio’s actual allocations could vary substantially from the target allocations because of, for example, changes to the Underlying Portfolios’ asset values due to market movements. MetLife Advisers may manage cash flows into or out of MIST Portfolio’s Underlying Portfolios in a way to bring actual allocations more closely in line with the target allocations. In addition, MetLife Advisers may, from time to time, rebalance allocations among the Underlying Portfolios to correspond to the target allocations.

Although MSF Portfolio and MIST Portfolio have substantially similar investment objectives and similar investment strategies, all or a substantial portion of the securities of Underlying Portfolios held by MSF Portfolio may be sold in order to comply with the investment practices of MIST Portfolio in connection with the Reorganization. However, because each Portfolio operates as a fund of funds, the Portfolios do not pay transaction costs when buying or selling shares of Underlying Portfolios, so such costs will not be borne by the Portfolios’ shareholders.

How do the Portfolios’ portfolio turnover rates compare?

Each Portfolio operates as a fund of funds, and does not pay transaction costs when it buys and sells shares of Underlying Portfolios (or “turns over” its portfolio). An Underlying Portfolio pays transaction costs, such as commissions, when it turns over its portfolio, and a higher portfolio turnover rate may indicate higher transaction costs. These costs, which are not reflected in annual portfolio operating expenses or in the Example, affect the performance of both the Underlying Portfolios and the Portfolio. During the most recent fiscal year, MSF Portfolio’s and MIST Portfolio’s portfolio turnover rates were 2% and 22.6%, respectively, of the average value of their portfolios. Some of the Underlying Portfolios, however, may have portfolio turnover rates as high as 200% or more.

-19-

Table of Contents

How do the Portfolios’ performance records compare?

The following charts show how the Class A shares of each Portfolio have performed in the past. Past performance is not an indication of future results.

PAST PERFORMANCE DOES NOT REFLECT THE FEES, EXPENSES OR WITHDRAWAL CHARGES IMPOSED BY THE CONTRACTS FOR WHICH THE PORTFOLIOS SERVE AS INVESTMENT VEHICLES. IF THOSE FEES AND EXPENSES HAD BEEN INCLUDED, PERFORMANCE WOULD BE LOWER.

The bar charts below show the performance of each Portfolio’s Class A shares for the last ten full calendar years or since inception, as applicable, and indicates how each Portfolio has varied from year to year. The performance of MIST Portfolio’s Class A shares for the period prior to inception reflects the performance of Class B shares, adjusted for the difference in applicable fees. These charts include the effects of Portfolio expenses. MSF Portfolio and MIST Portfolio can also experience short-term performance swings as indicated in the high and low quarter information at the bottom of each chart.

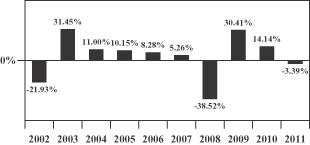

Year-by-Year Total Return as of December 31 of Each Year

MSF Portfolio Class A Shares

Highest Quarter: 2nd – 2003 16.17%

Lowest Quarter: 4th – 2008 -21.90%

MIST Portfolio Class A Shares

Highest Quarter: 2nd – 2009 20.35%

Lowest Quarter: 4th – 2008 -24.36%

-20-

Table of Contents

The next set of tables lists the average annual total return of the Class A shares of MSF Portfolio for the one-, five- and ten-year periods (ended December 31, 2011) and Class A shares of MIST Portfolio for the one- and five-year periods and since inception (ended December 31, 2011). These tables include the effects of portfolio expenses and compare each Portfolio’s average annual compounded total returns for each class with index returns. A description of the relevant index can be found following the table. It is not possible to invest directly in an index.

Average Annual Total Return as of December 31, 2011

| MSF Portfolio |

1 Year | 5 Years | 10 Years | |||||||||

| Class A shares |

-3.39 | % | -1.43 | % | 2.37 | % | ||||||

| S&P 500 Index (reflects no deduction for mutual fund fees or expenses) |

2.11 | % | -0.25 | % | 2.92 | % | ||||||

| MIST Portfolio |

1 Year | 5 Years | Since Inception |

Inception Date |

||||||||||||

| Class A Shares |

-5.57 | % | -2.12 | % | 2.51 | % | 5-2-05 | |||||||||

| Dow Jones Aggressive Index (reflects no deduction for mutual fund fees or expenses) |

-5.14 | % | 0.29 | % | 5.48 | %* | ||||||||||

| * | Index performance is from 11-4-04. |

The S&P 500 Index is a widely recognized unmanaged index that measures the stock performance of 500 large- and medium-sized companies and is often used to indicate the performance of the overall stock market.

The Dow Jones Aggressive Index is a total returns index designed to provide asset allocation strategists with a target risk benchmark. The index consists of both domestic and foreign stocks from Dow Jones and will always have a 100% allocation to stocks.

For a detailed discussion of the manner of calculating total return, please see the Statement of Additional Information for MIST Portfolio. Generally, the calculations of total return assume the reinvestment of all dividends and capital gain distributions on the reinvestment date and the deduction of all recurring expenses that were charged to shareholders’ accounts.

Important information about MIST Portfolio is also contained in management’s discussion of MIST Portfolio performance which appears in the most recent Annual Report of MIST relating to MIST Portfolio.

Who will be the adviser and portfolio managers of my Portfolio after the Reorganization? What will the management fee be after the Reorganization?

Management of the Portfolios

The overall management of MSF Portfolio and of MIST Portfolio is the responsibility of, and is supervised by, the Board of Trustees of MSF and the Board of Trustees of MIST, respectively.

Adviser

MetLife Advisers, LLC is the investment manager for MSF Portfolio and MIST Portfolio. MetLife Advisers is responsible for the general management and administration of the Portfolios, and for determining the asset allocation range for each Portfolio. MetLife Advisers will rebalance MSF Portfolio’s holdings as deemed necessary to bring the asset allocation of the Portfolio back into alignment with its fixed percentage allocations. MetLife Advisers is also responsible for establishing specific percentage targets for each asset class and each

-21-

Table of Contents