UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31 , 2021

OR

SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No. 001-16111

(Exact name of registrant as specified in charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||||||||

Registrant's telephone number, including area code: 770 -829-8000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company" in Rule 12b-2 of the Exchange Act.

Non-accelerated filer ☐ Smaller reporting company ☐

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter was $54,617,835,258 . The number of shares of the registrant's common stock outstanding at February 15, 2022 was 281,968,006 shares.

DOCUMENTS INCORPORATED BY REFERENCE

GLOBAL PAYMENTS INC.

2021 ANNUAL REPORT ON FORM 10-K

| Page | |||||||||||

| PART I | |||||||||||

| ITEM 1. | |||||||||||

| ITEM 1A. | |||||||||||

| ITEM 2. | |||||||||||

| ITEM 3. | |||||||||||

| PART II | |||||||||||

| ITEM 5. | |||||||||||

| ITEM 6. | |||||||||||

| ITEM 7. | |||||||||||

| ITEM 7A. | |||||||||||

| ITEM 8. | |||||||||||

| ITEM 9. | |||||||||||

| ITEM 9A. | |||||||||||

| ITEM 9B. | |||||||||||

| ITEM 9C. | |||||||||||

| PART III | |||||||||||

| ITEM 10. | |||||||||||

| ITEM 11. | |||||||||||

| ITEM 12. | |||||||||||

| ITEM 13. | |||||||||||

| ITEM 14. | |||||||||||

| PART IV | |||||||||||

| ITEM 15. | |||||||||||

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements we use in this report, and in some of the documents we incorporate by reference in this report, contain forward-looking statements concerning our business operations, economic performance and financial condition, including in particular: our business strategy and means to implement the strategy; measures of future results of operations, such as revenues, expenses, operating margins, income tax rates, and earnings per share; other operating metrics such as shares outstanding and capital expenditures; the effects of the COVID-19 pandemic on our business; our success and timing in developing and introducing new services and expanding our business; and statements about the benefits of our acquisitions, including future financial and operating results, the company’s plans, objectives, expectations and intentions, and the successful integration of our acquisitions or completion of anticipated benefits and strategic initiatives. You can sometimes identify forward-looking statements by our use of the words "believes," "anticipates," "expects," "intends," "plan," "forecast," "guidance" and similar expressions. For these statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Although we believe that the plans and expectations reflected in or suggested by our forward-looking statements are reasonable, those statements are based on a number of assumptions, estimates, projections or plans that are inherently subject to significant risks, uncertainties and contingencies, many of which are beyond our control, cannot be foreseen and reflect future business decisions that are subject to change. Accordingly, we cannot guarantee that our plans and expectations will be achieved. Our actual revenues, revenue growth rates and margins, other results of operations and shareholder values could differ materially from those anticipated in our forward-looking statements as a result of many known and unknown factors, many of which are beyond our ability to predict or control. Important factors, among others, that may otherwise cause actual events or results to differ materially from those anticipated by such forward-looking statements or historical performance include the effects of global economic, political, market, health and social events or other conditions, including the effects and duration of the COVID-19 pandemic and actions taken in response; our ability to meet our liquidity needs in light of the effects of the COVID-19 pandemic or otherwise; the outcome of any legal proceedings that may be instituted against the Company or our directors; difficulties, delays and higher than anticipated costs related to integrating the businesses of Global Payments and Total System Services, Inc., including with respect to implementing controls to prevent a material security breach of any internal systems or to successfully manage credit and fraud risks in business units; the effect of a security breach or operational failure on the Company's business; failing to comply with the applicable requirements of Visa, Mastercard or other payment networks or card schemes or changes in those requirements; the ability to maintain Visa and Mastercard registration and financial institution sponsorship; the ability to retain, develop and hire key personnel; the diversion of management’s attention from ongoing business operations; the continued availability of capital and financing; increased competition in the markets in which we operate and our ability to increase our market share in existing markets and expand into new markets; our ability to safeguard our data; risks associated with our indebtedness, foreign currency exchange and interest rate risks; our ability to meet environmental, social and governance targets, goals and commitments; the potential effects of climate change including natural disasters; the effects of new or changes in current laws, regulations, credit card association rules or other industry standards on us or our partners and customers, including privacy and cybersecurity laws and regulations; and other events beyond our control, and other factors presented in "Item 1A - Risk Factors" of this Annual Report on Form 10-K, which we advise you to review. These cautionary statements qualify all of our forward-looking statements, and you are cautioned not to place undue reliance on these forward-looking statements.

Our forward-looking statements speak only as of the date they are made and should not be relied upon as representing our plans and expectations as of any subsequent date. While we may elect to update or revise forward-looking statements at some time in the future, we specifically disclaim any obligation to publicly release the results of any revisions to our forward-looking statements, except as required by law.

3

PART I

ITEM 1- BUSINESS

Global Payments Inc. and its consolidated subsidiaries are referred to collectively as "Global Payments," the "Company," "we," "our" or "us," unless the context requires otherwise.

Introduction

We are a leading payments technology company delivering innovative software and services to approximately 4.0 million merchant locations and more than 1,350 financial institutions across more than 170 countries throughout North America, Europe, Asia-Pacific and Latin America. Our technologies, services and team member expertise allow us to provide a broad range of solutions that enable our customers to operate their businesses more efficiently across a variety of channels around the world. Headquartered in Georgia with approximately 25,000 team members worldwide, Global Payments is a Fortune 500 company and is a member of the S&P 500. Our common stock is traded on the New York Stock Exchange under the symbol "GPN."

Industry Overview

The payments technology industry provides financial institutions, businesses and consumers with payment processing services, merchant acceptance solutions and related information and other value-added services. The industry continues to grow as a result of wider merchant acceptance and increased use of credit and debit cards, advances in payment solutions and processing technology and migration to ecommerce, omnichannel and contactless payment solutions. The proliferation of credit and debit cards, as well as other digital payment solutions, has made the acceptance of digital payments a necessity for many businesses, regardless of size, in order to remain competitive. The COVID-19 pandemic has further accelerated the use of digital payments, the need for development of technologies and digital-based solutions and expansion of ecommerce, omnichannel and contactless payment solutions. This increased use of cards and the availability of more sophisticated technology services to all market segments has resulted in an increasingly competitive and specialized industry.

Strategy

We seek to leverage the adoption of, and transition to, card and digital-based payments by expanding our share in our existing markets through our distribution channels and service innovation, as well as through acquisitions to improve our offerings and scale. We also seek to enter new markets through acquisitions, alliances and joint ventures around the world. We intend to continue to invest in and leverage our technology infrastructure and our people to increase our penetration in existing markets.

The key tenets of our strategy include the following:

•Leading with technology and innovation to deepen our competitive advantages;

•Further scaling the four pillars of our strategy: software-driven focus, ecommerce & omnichannel solutions, exposure to faster growth markets and business-to-business ("B2B") payments;

•Delivering commerce enablement solutions globally to broaden our leading position as a sales-driven, product-led company;

•Providing frictionless, best-in-class customer experiences, creating longer-term relationships;

•Nurturing our culture, values and diversity, equity and inclusion initiatives to attract, retain and motivate exceptional team members; and

•Supporting our communities as a socially responsible company with purpose and understanding.

4

Competitive Strengths

We believe that our competitive strengths include the following:

•Global Footprint and Distribution - Our worldwide presence allows us to focus our investments on markets with promising gross domestic product fundamentals and favorable secular trends, makes us more attractive to customers with international operations and exposes us to emerging innovations that we can adopt globally, while diversifying our economic risk.

•Technology Solutions - We provide innovative technology-based solutions, including enterprise software solutions, that enable our customers to operate their business more efficiently and simplify the payments process, regardless of the channel through which the transaction occurs. We believe our robust technology solutions will continue to differentiate us in the marketplace and position us for continued growth.

•Scalable Operating Environment and Technology Infrastructure - We operate with a multi-channel, global technology infrastructure, which provides scalable and innovative service offerings and a consistent service experience to our merchants, customers, financial institutions and other partners worldwide, while also driving sustainable operating efficiencies.

•Strong, Long-lasting Partner Relationships - We have established strong, long-lasting relationships with many financial institutions, enterprise software providers, value-added resellers and other technology-based payment service providers, which enable us to deliver a set of diverse solutions to our customers.

•Disciplined Acquisition Approach - Our proven track record for selectively and successfully sourcing, completing and integrating acquired businesses in existing and new markets positions us well for future growth and as an attractive partner for potential acquisition targets.

Recent Acquisitions

On June 10, 2021, we acquired Zego, a real estate technology company that provides a comprehensive resident experience management software and digital commerce solutions to property managers, primarily in the United States, for cash consideration of approximately $933 million. This acquisition aligns with our technology-enabled, software driven strategy and expands our business into a new vertical market.

During the year ended December 31, 2021, we completed other strategic business acquisitions for an aggregate purchase price of approximately $963 million. Our acquisition of MineralTree, a leading provider of accounts payable automation and B2B payments solutions, expands our target addressable market and provides incremental avenues for growth in one of the most attractive technology markets. Our acquisitions of the Bankia merchant services business and Worldline's PayOne Austrian acquiring business deepen our presence in Europe and expand the scale of our distribution and technologies.

On September 18, 2019, we consummated our merger with Total System Services, Inc. ("TSYS") (the "Merger") for total purchase consideration of $24.5 billion, primarily funded with shares of our common stock. Prior to the Merger, TSYS was a leading global payments provider, offering seamless, secure and innovative solutions to issuers, merchants and consumers.

See "Note 2—Acquisitions" in the notes to the accompanying consolidated financial statements for further discussion of these acquisitions.

Business Segments

We operate in three reportable segments: Merchant Solutions, Issuer Solutions and Business and Consumer Solutions. See "Note 16—Segment Information" in the notes to the accompanying consolidated financial statements for additional information about our segments, including revenues, operating income and depreciation and amortization by segment as well as financial information about geographic areas in which we operate.

Our foreign operations subject us to various risks, including, without limitation, currency exchange risks and political, economic and regulatory risks. See "Item 1A - Risk Factors" for additional information about these risks.

5

Merchant Solutions Segment

Through our Merchant Solutions segment, we provide payments technology and software solutions to customers globally. Our payment technology solutions are similar around the world in that we enable our customers to accept card, check and digital-based payments. Our comprehensive offerings include, but are not limited to, authorization, settlement and funding services, customer support, chargeback resolution, terminal rental, sales and deployment, payment security services, consolidated billing and reporting.

In addition, we offer a wide array of enterprise software solutions that streamline business operations to customers in numerous vertical markets. We also provide a variety of value-added solutions and services, including specialty point-of-sale software, analytic and customer engagement, human capital management and payroll and reporting that assist our customers with driving demand and operating their businesses more efficiently.

Our value proposition is to provide distinctive high-quality, responsive and secure services to all of our customers. We distribute our Merchant Solutions services globally through multiple technology-enabled and relationship-led distribution channels and target customers in many vertical markets located throughout North America, Europe, Asia-Pacific and Latin America. The majority of our revenues is generated by services priced as a percentage of transaction value or a specified fee per transaction, depending on the payment type or the market. We also earn software subscription and licensing fees, as well as other fees based on specific value-added services that may be unrelated to the number or value of transactions.

Distribution Channels

In the Merchant Solutions segment, we actively market and provide our payment services, enterprise software solutions and other value-added services directly to our customers through a variety of technology-enabled and relationship-led distribution channels.

Technology-Enabled. Many of our payment solutions are technology-enabled in that they incorporate or are incorporated into innovative, technology-driven solutions, including enterprise software solutions, designed to enable merchants to better manage their businesses. Our technology-enabled solutions represent a substantial component of our revenues. Our technology-enabled distribution includes integrated and vertical market software solutions and ecommerce and omnichannel solutions, each as described below.

Integrated Solutions. Our integrated solutions provide advanced payments technology that is deeply embedded into business management software solutions owned by our technology partners who operate in numerous vertical markets, primarily in North America. We grow our integrated solutions business when new or existing merchants enable payments services through enterprise software solutions sold by our partners, including existing and new partners.

Vertical Markets Software Solutions. Our vertical markets software solutions provide advanced payments technology that is deeply integrated into business enterprise software solutions that we own. We distribute our vertical markets software solutions primarily through the following businesses:

•ACTIVE Network. Through ACTIVE Network, we deliver cloud-based enterprise software, including payment technology solutions, to event organizers in the communities, government services and health and fitness markets.

•AdvancedMD. Through AdvancedMD, we provide cloud-based enterprise solutions to small-to-medium sized ambulatory care physician practices in the United States.

•Education Solutions. We offer integrated payment solutions specifically designed for all levels of educational institutions. At the university level, we offer integrated commerce solutions, payment services, higher education loan services, credentialing services and open- and closed-loop payment solutions. For kindergarten through 12th grade, we provide ecommerce and in-person payments, cafeteria POS solutions and back-office management software, hardware, technical support and training.

•Gaming. We offer a comprehensive suite of solutions to the gaming market in North America. These solutions include credit and debit card cash advance, cashless advance, iGaming solutions, traditional and digital check processing and other services specific to this market.

6

•Xenial. Through Xenial, we offer leading-edge enterprise software and hardware solutions, integrated with our payment services and other adjacent business service applications, to the restaurant and hospitality vertical markets.

Ecommerce and Omnichannel. We offer ecommerce and omnichannel solutions to our customers that seamlessly blend payment gateway services, retail payment acceptance infrastructure and payment technology service capabilities through a unified commerce platform to allow merchants to accept various payment methods through any channel across our geographical footprint. We sell ecommerce and omnichannel solutions to customers of all sizes, from small businesses accepting payments in a single country to enterprise and multinational businesses that have complex payment needs and operate retail and online businesses in multiple countries.

Relationship-Led. Through our relationship-led direct sales force worldwide, as well as bank and other referral partnerships, we offer our payments technology services, software and other value-added solutions directly to customers across numerous verticals in the markets we serve. We offer high-touch services that provide our customers with reliable and secure solutions coupled with high-quality and responsive support services. Although our primary focus is on building high-quality, direct relationships with merchants, we also provide our services to merchants through independent sales organizations ("ISOs") and financial institutions.

Credit and Debit Card Transaction Processing

Credit and debit card transaction processing includes the processing of the world's major international card brands, including American Express, Discover Card ("Discover"), JCB, Mastercard, UnionPay International and Visa, as well as certain domestic debit networks, such as Interac in Canada. Credit and debit networks establish uniform regulations that govern much of the payment card industry. During a typical payment transaction, the merchant and the card issuer do not interface directly with each other, but instead rely on payments technology companies, such as Global Payments, to facilitate transaction processing services, including authorization, electronic draft capture, file transfers to facilitate funds settlement and certain exception-based, back office support services such as chargeback resolution.

We process funds settlement under two models: a sponsorship model and a direct membership model. Under the sponsorship model, member clearing financial institutions ("Members") sponsor us and require our adherence to the standards of the networks. In these markets, we have sponsorship or depository and clearing agreements with financial institution sponsors. These agreements allow us to route transactions under the Members' control and identification numbers to clear card transactions through Mastercard and Visa. In this model, the standards of the card networks restrict us from performing funds settlement or accessing merchant settlement funds, and, instead, require that these funds be in the possession of the Member until the merchant has been funded.

Under the direct membership model, we are direct members in various payment networks, allowing us to process and fund transactions without third-party sponsorship. Under this model, we route and clear transactions directly through the card brand’s network and are not restricted from performing funds settlement. Otherwise, we process these transactions similarly to how we process transactions in the sponsorship model. We are required to adhere to the standards of the various networks in which we are direct members. We maintain relationships with financial institutions, which may also serve as our Member sponsors for other card brands or in other markets, to assist with funds settlement.

How a Card Transaction Works

A typical payment transaction begins when a cardholder presents a card for payment at a merchant location where the card information is captured by a point-of-sale ("POS") terminal card reader or mobile device card reader, which may be sold or leased to the merchant and serviced by us. Alternatively, card and transaction information may be captured and transmitted to our network through a POS device or ecommerce portal by one of a number of services that we offer directly or through a value-added reseller. The card reader electronically records sales draft information, such as the card identification number, transaction date and transaction amount.

After the card and transaction information is captured, the POS device automatically connects to our network through the internet or other communication channel in order to receive authorization of the transaction. For a credit card transaction, authorization services generally refer to the process in which the card issuer indicates whether a particular credit card is authentic and whether the impending transaction amount will cause the cardholder to exceed defined credit limits. In a debit card transaction, we obtain authorization for the transaction from the card issuer through the payment network verifying that the cardholder has access to sufficient funds for the transaction amount.

7

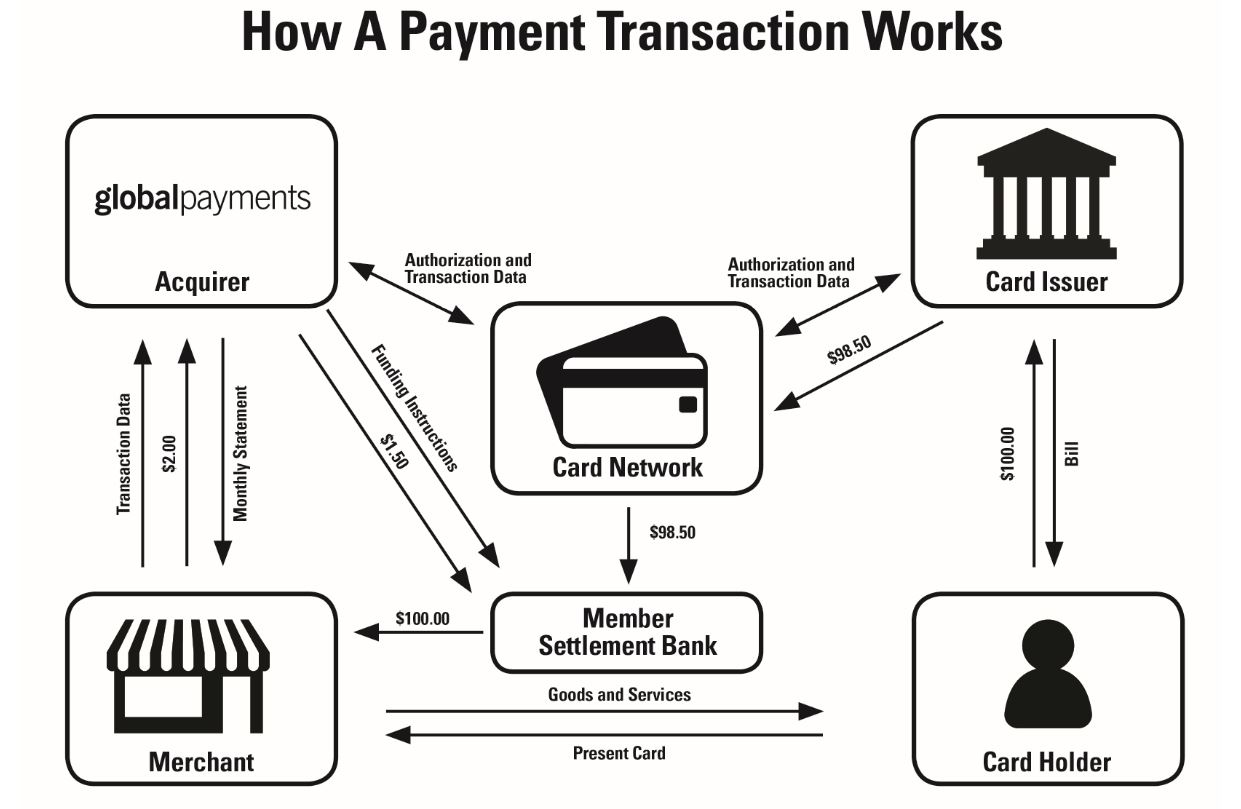

As an illustration, shown below in the sponsorship model, on a $100.00 card transaction, the card issuer may fund the Member, our sponsor, (indirectly through the card network) $98.50 after retaining approximately $1.50 referred to as an interchange fee. The card issuer seeks reimbursement of $100.00 from the cardholder in the cardholder's monthly credit card statement. The Member would, in turn, pay the merchant $100.00. The net settlement after this transaction would require us to advance the Member $1.50. After the end of the month, we would bill the merchant a percentage of the transaction amount, or merchant discount, to cover the full amount of the interchange fee and our fee from the transaction. If our discount rate for the merchant in the above example was 2.00%, we would bill the merchant $2.00 after the end of the month for the transaction, reimburse ourselves for $1.50 in interchange fees and retain $0.50 as our fees for the transaction. Under some arrangements, we remit the net amount of $98.00 to the merchant, rather than funding the full $100.00 and subsequently billing the merchant at the end of the month. Discount rates vary based on negotiations with merchants and the economic characteristics of transactions. Interchange rates also vary based on the economic characteristics of individual transactions. Accordingly, our fee per transaction varies across our merchant base and is subject to change based on changes in discount rates and interchange rates. Our profit on the transaction reflects the fee received less payment network fees and operating expenses, including systems cost to process the transaction and commissions paid to our sales force or ISO. Payment network fees are charged by the card brands, in part, based on the value of transactions processed through their networks.

Issuer Solutions Segment

Through our Issuer Solutions segment, we provide solutions that enable financial institutions and other financial service providers to manage their card portfolios, reduce technical complexity and overhead and offer a seamless experience for cardholders on a single platform. In addition, we provide flexible commercial payments and ePayables solutions that support B2B payment processes for businesses and governments. We also offer complementary services, including account management and servicing, fraud solution services, analytics and business intelligence, cards, statements and correspondence, customer contact solutions and risk management solutions.

Issuer Solutions segment revenues are derived from long-term processing contracts with financial institutions and other financial services providers. Payment processing services revenues are generated primarily from charges based on the number of accounts on file, transactions and authorizations processed, statements generated and/or mailed, managed services, cards embossed and mailed, and other processing services for cardholder accounts on file. Most of these contracts

8

have prescribed annual minimums, penalties for early termination, and service level agreements that may affect contractual fees if specific service levels are not achieved. Issuer Solutions segment revenues also include loyalty redemption services and professional services.

Business and Consumer Solutions Segment

Our Business and Consumer Solutions segment provides general purpose reloadable ("GPR") prepaid debit and payroll cards, demand deposit accounts and other financial service solutions to the underbanked and other consumers and businesses in the United States and parts of Europe through our Netspend® and other brands. Through our Business and Consumer Solutions segment, we provide customers with access to depository accounts insured by the Federal Deposit Insurance Corporation ("FDIC") with a menu of features specifically tailored to their needs. The Business and Consumer Solutions segment has an extensive distribution and reload network comprised of financial service centers and other retail locations throughout the United States, and is a program manager for FDIC-insured depository institutions that provide the services that the Business and Consumer Solutions segment develops, promotes and distributes. Business and Consumer Solutions currently has active agreements with four card issuing banks. Additionally, our Business and Consumer Solutions segment provides B2B payment services and software-as-a-service (“SaaS”) offerings that automate key procurement processes, including invoice capture, coding and approval, and enable virtual cards and integrated payments options across a variety of key vertical markets.

The Business and Consumer Solutions segment markets its services through multiple distribution channels, including alternative financial service providers, traditional retailers, direct-to-consumer and online marketing programs and contractual relationships with corporate employers. Business and Consumer Solutions segment revenues principally consist of fees collected from cardholders and fees generated by cardholder activity in connection with the programs that we manage. Customers are typically charged a fee for each purchase transaction made using their cards, unless the customer is on a monthly or annual service plan, in which case the customer is instead charged a monthly or annual subscription fee, as applicable. Customers are also charged a monthly maintenance fee after a specified period of inactivity. We also charge fees associated with additional services offered in connection with programs we manage, including the use of overdraft features, a variety of bill payment options, card replacement, foreign exchange and card-to-card transfers of funds initiated through our call centers. Revenues are recognized net of fees charged by the payment networks for services they provide in processing transactions routed through them. We have recently commenced a strategic evaluation of the consumer portion of this segment with the intent to focus on our growing B2B portfolio.

Competition

Our Merchant Solutions segment competes with financial institutions, merchant acquirers and other financial technology companies who provide businesses with merchant acquiring services and related services. As of December 31, 2021, we believe that we were one of the largest merchant acquirers in the small and medium-sized business segment (merchants who have less than $5 million in annual bankcard sales volume) in the United States. In the United States, we compete primarily with Fiserv, Inc. (and its alliances) ("Fiserv"), Fidelity National Information Services, Inc. ("FIS"), Chase Paymentech Solutions, LLC, Elavon, Inc., a subsidiary of U.S. Bancorp, Wells Fargo Bank, N.A and Block Inc. (formerly known as Square, Inc.). While these are our primary competitors, our vertically focused business in the United States competes with other organizations. Advances in technology are also enabling new entrants, some of which depart from traditional payment models.

Internationally, financial institutions remain the primary providers of payment technology services to merchants, although the outsourcing of these services to third-party service providers is becoming more prevalent. In addition to financial institutions, competitors in Europe include Ayden N.V. and FIS. We expect competition to continue to increase as new companies enter our markets and existing competitors expand or consolidate their product lines and services.

Our Issuer Solutions segment encounters competition from other third-party payment card processors, the card brands, core banking platform providers, independent software vendors and various other firms that provide products and services to payment card issuers in the markets we serve. The United States market for third-party issuer processing is primarily serviced by three vendors, including TSYS. As of December 31, 2021, we believe that we were the largest third-party processor for credit card issuers in North America and one of the largest in Europe based on net revenue from solutions provided to credit card issuers.

Our Business and Consumer Solutions segment primarily competes with other demand deposit account and prepaid debit account program managers to provide financial service solutions to the underbanked and other consumers and businesses. Our primary competitors in this space include Green Dot Corporation, InComm, Fiserv and Chime. As of

9

December 31, 2021, we believe that we were one of the two largest prepaid program managers in the United States based on gross dollar volume (total spending on the accounts we manage) processed.

Safeguarding Our Business

In order to provide our services, we process and store sensitive business information and personal information, which may include credit and debit card numbers, bank account numbers, social security numbers, driver’s license numbers, names and addresses, and other types of personal information or sensitive business information. Some of this information is also processed and stored by financial institutions, merchants and other entities, as well as third-party service providers to whom we outsource certain functions and other agents, which we refer to collectively as our associated third parties. We may have responsibility to the card networks, financial institutions, and in some instances, our merchants, ISOs and/or individuals, for our failure or the failure of our associated third parties (as applicable) to protect this information.

We are subject to cyber security and information theft risks in our operations, which we seek to manage through cyber and information security programs, training and insurance coverage. To strengthen our security and cyber defenses, we continue to deploy multiple methods at different layers to defend our systems against misuse, intrusions and cyberattacks and to protect the data we collect. Further, we work with information security and forensics firms and employ advanced technologies to help prevent, investigate and address issues relating to processing system security and availability. We also collaborate with third parties, regulators and law enforcement, when appropriate, to resolve security incidents and assist in efforts to prevent unauthorized access to our processing systems.

Intellectual Property

Our intellectual property is an important part of our strategy to be a leading provider of payment technology and software solutions. We use a combination of internal policies, intellectual property laws and contractual provisions to protect our proprietary technologies and brands. In addition, to protect our various brands, we seek and maintain registration of U.S. and international patents, trademarks, service marks and domain names that align with our brand strategy. We also enforce our trademarks against potential sources of misunderstanding that could harm our brand and ability to compete. In addition to using our intellectual property in our own operations, we grant licenses to certain of our customers to use our intellectual property.

Human Capital Management

Team Member Population

We currently do business in over 170 countries around the world, with team members living and working in 32 of them. As of December 31, 2021, our approximately 25,000 team member workforce represented approximately 80 nationalities and 18 natively spoken languages, with approximately 64% residing in the Americas, 16% residing in Europe and 20% residing in Asia Pacific. Many of our team members are highly skilled in technical areas specific to payment technology and software solutions.

Talent Management and Retention

We place an emphasis on attracting and retaining premier and diverse team members. To that end, we have implemented programs and initiatives focused on enriching new hire experiences, developing team members through extensive training and professional development opportunities, including mentorship programs, promoting team members’ wellness and safety, particularly during challenging times such as the COVID-19 pandemic, providing flexible work arrangements and offering comprehensive and competitive benefits packages, including paid parental leave, team member assistance and savings and retirement programs. Further, we honor and recognize the efforts of all of our team members and celebrate our team members through a combination of programs, including team appreciation activities to celebrate all team members and annual awards programs to honor top performers and notable contributors. We also regularly survey our team members to help us understand their perspectives related to workplace culture, engagement, well-being and to inform our diversity and inclusion strategies and initiatives. The results from these surveys are leveraged to further develop our talent management initiatives.

10

Well-being and Safety

The success of our business is connected to the well-being of our team members. Accordingly, we are committed to the health, safety and wellness of our team members worldwide, and we provide team members with various health and wellness programs and benefits.

In response to the COVID-19 pandemic, we implemented significant changes that we determined were in the best interest of our team members as well as the communities in which we operate. This included enabling the vast majority of our worldwide team members to seamlessly shift to remote work. Over the past several years, we have made significant investments in modernizing our operating environments and technologies that support day-to-day execution. The largely cloud-based systems and collaboration tools we use globally facilitated this smooth transition of operations to business continuity mode. For those team members who continued to work in our offices, and as team members have returned in certain regions in accordance with local guidelines and mandates, we have implemented health and safety protocols to help keep our team members safe, such as:

•Increasing cleaning protocols across all our locations;

•Initiating regular communication regarding effects of the COVID-19 pandemic on our operations, including health and safety protocols and procedures;

•Expanding resources and benefits available to team members, including hosting team member vaccination clinics, free at-home COVID-19 testing and expanded mental health and well-being initiatives;

•Adjusting attendance policies to encourage those who are sick to stay home; and

•Implementing protocols to address actual and suspected COVID-19 cases and potential exposure.

Growth and Development

Our strategy to develop and retain the best talent includes an emphasis on team member development and training. We provide a variety of training and development opportunities to team members globally, including our online training platform that contains a vast array of tools and application resources for all team members to build learning experiences and skills. In order to help our team members strengthen the skills and behaviors needed for career advancement, our new performance management program enables team members to drive their development with a focus on growth, performance, and well-being through regular meetings with their leader.

Inclusion and Diversity

Our inclusion and diversity program focuses on workforce (our team members), workplace (culture, tools and programs) and community. We believe that our business is strengthened by a diverse workforce that reflects the communities in which we operate. We believe all of our team members should be treated with respect and equality, regardless of gender, ethnicity, sexual orientation, gender identity, religious beliefs, or other characteristics; to further this goal, we formally launched an inclusion and diversity initiative in 2018. In 2020, we undertook a series of initiatives to further enhance our existing diversity and inclusion programs. We have also broadened our focus on inclusion and diversity by including social and racial equity in our conversations and equipping and empowering our Employee Resource Group ("ERG") leaders with the right tools and training to lead their networks. Through this plan, our aspirational goals are to:

•Improve diversity at all levels across the company, including increasing the representation of women and minorities in leadership positions;

•Increase team member engagement and awareness through education and participation in diversity and inclusion programs, such as our Conversations of Understanding series we have launched to discuss racial inequality in our communities, and the Inclusion and Diversity Advisory Counsel, consisting of team members worldwide who provide insight and input on the progress of our inclusion and diversity initiatives; and

•Enhance the strategy and initiatives for our ERGs to expand their reach and effectiveness in educating and supporting our team members.

11

Environmental, Social and Governance ("ESG")

As part of our annual ESG reporting, we provide additional information about our approach to ESG matters in our Global Responsibility Report (which is not incorporated herein), available in the investor relations section of our website at www.globalpaymentsinc.com.

Regulation

Various aspects of our business are subject to regulation and supervision under federal, state and local laws in the United States, and foreign laws, regulations and rules, as well as local escheat laws and privacy and information security regulations. In addition, we are subject to rules promulgated by the various payment networks, including American Express, Discover, Interac, Mastercard and Visa. Set forth below is a brief summary of some of the significant laws and regulations that apply to us. These descriptions are not exhaustive, and these laws, regulations and rules frequently change and are increasing in number.

We are currently in compliance with existing legal and regulatory requirements and do not expect that maintaining compliance with these regulations will have a material adverse effect on our capital expenditures, earnings or competitive and financial positions. See "Item 1A - Risk Factors" for additional discussion of the potential risks associated with future changes in laws or regulations.

Dodd-Frank Act

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the "Dodd-Frank Act") restricts the amounts of debit card fees that certain institutions can charge merchants. Pursuant to regulations promulgated by the Federal Reserve Board, debit interchange rates for card issuers with assets of $10 billion or more are capped at $0.21 per transaction and an ad valorem component of 5 basis points to reflect a portion of the issuer's fraud losses plus, for qualifying issuers, an additional $0.01 per transaction in debit interchange for fraud prevention costs.

In addition, the Dodd-Frank Act limits the ability of payment card networks to impose certain restrictions because it allows merchants to: (i) set minimum dollar amounts (not to exceed $10) for the acceptance of a credit card (and allows federal governmental entities and institutions of higher education to set maximum amounts for the acceptance of credit cards) and (ii) provide discounts or incentives to encourage consumers to pay with cash, checks, debit cards or credit cards.

The rules also contain prohibitions on network exclusivity and merchant routing restrictions that require a card issuer to enable at least two unaffiliated networks on each debit card, prohibit card networks from entering into exclusivity arrangements and restrict the ability of issuers or networks to mandate transaction routing requirements. The prohibition on network exclusivity has not significantly affected our ability to pass on network fees and other costs to our customers, nor do we expect it to in the future.

The Dodd-Frank Act also created the Consumer Financial Protection Bureau ("CFPB"), which has assumed responsibility for enforcing federal consumer protection laws, and the Financial Stability Oversight Council, which has the authority to determine whether any nonbank financial company, such as us, should be supervised by the Board of Governors of the Federal Reserve System (the "Federal Reserve") on the ground that it is "systemically important" to the U.S. financial system. Accordingly, we may be subject to additional systemic risk-related oversight.

Money Transmission, Sale of Checks and Payment Instrument Laws and Regulations

Our Business and Consumer Solutions segment is subject to money transfer and payment instrument licensing regulations. We have obtained licenses to operate as a money transmitter, seller of checks and/or provider of payment instruments in 49 states and the District of Columbia.

Our Business and Consumer Solutions segment is subject to direct supervision and regulation by the relevant state banking departments or similar agencies charged with enforcement of the relevant statutes and we must comply with various requirements, such as those related to the maintenance of a certain level of net worth, surety bonding, selection and oversight of our authorized agents, maintaining permissible investments in an amount equal to or in excess of our outstanding payment obligations, recordkeeping and reporting and disclosures to consumers. Our Business and Consumer Solutions segment is also subject to periodic examinations by the relevant licensing authorities, which may include reviews of our compliance practices, policies and procedures, financial position and related records, various agreements that we have with our issuing

12

banks, distributors and other third parties, privacy and data security policies and procedures and other matters related to our business.

Banking Laws and Regulations

Because we provide digital payment processing services to banks and other financial institutions, we are subject to examination by the Federal Financial Institutions Examination Council (the "FFIEC"), an interagency body comprised primarily of federal banking regulators, and also subject to examination by the various state financial regulatory agencies that supervise and regulate the financial institutions for which we provide digital payment processing and other payment related services. The FFIEC examines large data processors in order to identify and mitigate risks associated with systemically significant service providers, including specifically the risks they may pose to the banking industry.

Privacy, Information Security and Other Business Practices Regulation

Aspects of our business are subject, directly or indirectly, to privacy and data protection regulations in the United States, the United Kingdom, the European Union and elsewhere. In most of the countries in which we operate, these laws impose requirements on the manner in which personal information can be collected, processed, stored and shared. They also impose requirements, which vary materially by jurisdiction, in the event of a personal data breach.

Compliance with the data protection regulations could potentially require substantive technology infrastructure and process changes across many of the Company’s businesses. Noncompliance with the General Data Protection Regulation ("GDPR"), the California Consumer Privacy Act, or similar laws and regulations could lead to substantial regulatory fines and penalties, or damages from private causes of action.

We also face security and operational risks relating to third parties upon whom we rely to facilitate or enable our business activities or upon whom our customers rely. Such third parties include vendors and other partners.

New regulations (including new state laws in the United States or a possible federal privacy law) and new interpretations of existing regulations like the GDPR could create new privacy rights for individuals and new obligations for companies handling personal information. Such additional laws and regulations could limit our ability to use and share personal or other data, increase costs related to compliance, or adversely affect our ability to move data across borders. The effect of the regulations could harm our business and financial condition.

The U.S. Health Insurance Portability and Accountability Act of 1996 (“HIPAA”), together with the HIPAA Privacy Rule, governs the use and disclosure of protected health information in healthcare treatment, payment and operations by covered entities. In addition, multiple states, Congress and regulators outside the United States are considering similar laws or regulations which could create new individual privacy rights and impose increased obligations on companies handling personal data. See "Item 1A - Risk Factors" for additional discussion of the potential risks associated with future changes in laws or regulations.

Anti-Money Laundering, Anti-Bribery and Sanctions Regulations

In many countries, we are legally or contractually required to comply with the anti-money laundering laws and regulations, such as, in the United States, the Bank Secrecy Act, as amended by the USA PATRIOT Act (collectively, the "Bank Secrecy Act"), and similar laws of other countries, which require that customer identifying information be obtained and verified. In some countries, we are directly subject to these requirements; in other countries, we have contractually agreed to assist our sponsor financial institutions with their obligation to comply with anti-money laundering requirements that apply to them. In addition, we and our sponsor financial institutions are subject to the laws and regulations enforced by the Office of Foreign Assets Control ("OFAC"), which prohibit U.S. persons from engaging in transactions with certain prohibited persons or entities. Similar requirements apply in other countries. We have developed procedures and controls that are designed to monitor and address legal and regulatory requirements and developments and that allow our customers to protect against having direct business dealings with such prohibited countries, individuals or entities.

The Financial Crimes Enforcement Network of the U.S. Department of the Treasury ("FinCEN") has issued a rule regarding the applicability of the Bank Secrecy Act's anti-money laundering provisions to "prepaid access programs." This rulemaking clarifies the anti-money laundering obligations for entities, such as our Business and Consumer Solutions business and its distributors, engaged in the provision and sale of prepaid access devices like our GPR prepaid cards. Certain of our operating subsidiaries have registered with FinCEN as a money services business. This registration results in our having direct responsibility to maintain and implement an anti-money laundering compliance program for such subsidiaries.

13

We are subject to anti-corruption laws and regulations, including the U.S. Foreign Corrupt Practices Act (“FCPA”) and similar laws outside of the U.S. such as the U.K. Bribery Act, that prohibit the making or offering of improper payments to foreign government officials and political figures. The FCPA has a broad reach and requires maintenance of appropriate records and adequate internal controls to prevent and detect possible FCPA violations.

State Wage Payment Laws and Regulations

The use of payroll card programs as a means for an employer to remit wages or other compensation to its employees or independent contractors is governed by state labor laws related to wage payments, which laws are subject to change. The paycard portion of our Business and Consumer Solutions segment includes payroll cards and convenience checks and is designed to allow employers to comply with applicable state wage and hour laws. Most states permit the use of payroll cards as a method of paying wages to employees, either through statutory provisions allowing such use or, in the absence of specific statutory guidance, the adoption by state labor departments of formal or informal policies allowing for their use. Nearly every state allowing payroll cards places certain requirements and/or restrictions on their use as a wage payment method, the most common of which involve obtaining the prior written consent of the employee, limitations on fees and disclosure requirements.

Escheat Laws

We are subject to unclaimed or abandoned property state laws in the United States and in certain foreign countries that require us to transfer to certain government authorities the unclaimed property of others that we hold when that property has been unclaimed for a certain period of time. Moreover, we are subject to audit by state and foreign regulatory authorities with regard to our escheatment practices.

Debt Collection and Credit Reporting Laws

Portions of our business may be subject to the Fair Debt Collection Practices Act ("FDCPA"), the Fair Credit Reporting Act ("FCRA") and similar state laws. These debt collection laws are designed to eliminate abusive, deceptive and unfair debt collection practices and may require licensing at the state level. The FCRA regulates the use and reporting of consumer credit information and also imposes disclosure requirements on entities that take adverse action based on information obtained from credit reporting agencies.

Telephone Consumer Protection Act

We are subject to the Telephone Consumer Protection Act ("TCPA") and various state laws to the extent we place telephone calls and short message service ("SMS") messages to customers and consumers. The TCPA regulates certain telephone calls and SMS messages placed using automatic telephone dialing systems or artificial or prerecorded voices.

ESG and Sustainability

Certain governments around the world are adopting laws and regulations pertaining to ESG performance, transparency and reporting. Regulations may include mandated corporate reporting on ESG overall or in individual areas such as mandated reporting on climate-related financial disclosures.

Other

In addition, there are other laws, rules and or regulations, including the Telemarketing Sales Act, that may directly affect us or the activities of our merchant customers and in some cases may subject us to investigations, fees, fines and disgorgement of funds in the event we are deemed to have aided and abetted or otherwise provided the means and instrumentalities to facilitate the illegal activities of the merchant through our payment processing services.

14

Where to Find More Information

We file annual and quarterly reports, proxy statements and other information with the U.S. Securities and Exchange Commission ("SEC"). You may read and print materials that we have filed with the SEC from its website at www.sec.gov. In addition, certain of our SEC filings, including our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and amendments to them can be viewed and printed, free of charge, from the investor relations section of our website at www.globalpaymentsinc.com as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. Certain materials relating to our corporate governance, including our codes of ethics applicable to our directors, senior financial officers and other employees, and our Global Responsibility Report (which is not incorporated herein) are also available in the investor relations section of our website. Copies of our filings, specified exhibits and corporate governance materials are also available, free of charge, by writing us using the address on the cover of this Annual Report on Form 10-K. You may also telephone our investor relations office directly at (770) 829-8478. We are not including the information on our website as a part of, or incorporating it by reference into, this Annual Report on Form 10-K.

15

ITEM 1A - RISK FACTORS

An investment in our common stock involves a high degree of risk. You should consider carefully the following risks and other information contained in this Annual Report on Form 10-K and other SEC filings before you decide whether to buy our common stock. The risks identified below are not all encompassing but should be considered in establishing an opinion of our future operations. If any of the events contemplated by the following discussion of risks should occur, our business, financial condition, results of operations and cash flows could suffer significantly. As a result, the market price of our common stock could decline and you may lose all or part of your investment in our common stock.

Risks Related to Our Business Model and Operations Including the Use of Technology

Our ability to protect our systems and data from continually evolving cybersecurity risks or other technological risks could affect our reputation among our customers and cardholders, adversely affect our continued card network registration or membership and financial institution sponsorship, and expose us to penalties, fines, liabilities and legal claims.

In order to provide our services, we process and store sensitive business and personal information, which may include credit and debit card numbers, bank account numbers, social security numbers, driver’s license numbers, names and addresses, and other types of personal information or sensitive business information. Some of this information is also processed and stored by financial institutions, merchants and other entities, as well as third-party service providers to whom we outsource certain functions and other agents, which we refer to collectively as our associated third parties. We may have responsibility to the card networks, financial institutions, and in some instances, our merchants, ISOs and/or individuals, for our failure or the failure of our associated third parties (as applicable) to protect this information.

We are a regular target of malicious third-party attempts to identify and exploit system vulnerabilities, and/or penetrate or bypass our security measures, in order to gain unauthorized access to our networks and systems or those of our associated third parties. Such access could lead to the compromise of sensitive, business, personal or confidential information. As a result, we follow a defense-in-depth model for cybersecurity, meaning we proactively seek to employ multiple methods at different layers to defend our systems against intrusion and attack and to protect the data we collect. However, we cannot be certain that these measures will be successful or will be sufficient to counter all current and emerging technology threats.

Our computer systems and/or our associated third parties’ computer systems could be subject to penetration, and our data protection measures may not prevent unauthorized access. The techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and are often difficult to detect and continually evolve and become more sophisticated. Threats to our systems and our associated third parties’ systems can derive from human error, fraud or malice on the part of employees or third parties, including state-sponsored organizations with significant financial and technological resources. Computer viruses and other malware can be distributed and could infiltrate our systems or those of our associated third parties. In addition, denial of service, ransomware or other attacks could be launched against us for a variety of purposes, including to interfere with our services or create a diversion for other malicious activities. Our defensive measures may not prevent downtime, unauthorized access or use of sensitive data. While we maintain first- and third-party insurance coverage that may cover certain aspects of cyber risks, such insurance coverage may be insufficient to cover all losses. Companies we acquire may require post-closing implementation of additional cyber defense methods to align with our standards and, as a result, there may be a period of increased risk between the closing of an acquisition and the completion of such implementation. Further, certain of our third-party relationships are subject to our vendor management program and governed by written contracts; however, we do not control the actions of our associated third parties, and any problems experienced by these third parties, including those resulting from breakdowns or other disruptions in the services provided by such parties or cyberattacks and security breaches, could adversely affect our ability to service our customers or otherwise conduct our business.

In addition, we cannot provide assurance that the contractual requirements related to use, security and privacy that we impose on our associated third parties who have access to this data will be followed or will be adequate to prevent the misuse of this data. Any misuse or compromise of personal information or failure to adequately enforce these contractual requirements could result in liability, protracted and costly litigation and, with respect to misuse of personal information of our customers, lost revenue and reputational harm.

Any type of security breach, attack or misuse of data described above or otherwise, whether experienced by us or an associated third party, could harm our reputation and deter existing and prospective customers from using our services or from making digital payments generally, increase our operating expenses in order to contain and remediate the incident, expose us to unanticipated or uninsured liability, disrupt our operations (including potential service interruptions), distract our management, increase our risk of litigation or regulatory scrutiny, result in the imposition of penalties and fines under state, federal and foreign laws or by the card networks, and adversely affect our continued card network registration or membership and financial

16

institution sponsorship. Our removal from networks' lists of Payment Card Industry Data Security Standard compliant service providers could mean that existing customers, sales partners or other third parties may cease using or referring our services. Also, prospective merchant customers, financial institutions, sales partners or other third parties may choose to terminate negotiations with us, or delay or choose not to consider us for their processing needs. In addition, the card networks could refuse to allow us to process through their networks.

We may experience software defects, undetected errors, and development delays, which could damage customer relations, decrease our potential profitability and expose us to liability.

Our services are based on software and computing systems that often encounter development delays, and the underlying software may contain undetected errors, viruses or defects. Defects in our software services and errors or delays in our processing of digital transactions could result in additional development costs, diversion of technical and other resources from our other development efforts, loss of credibility with current or potential customers, harm to our reputation and exposure to liability claims. In addition, we rely on technologies and software supplied by third parties that may also contain undetected errors, viruses or defects that could have a material adverse effect on our business, financial condition, results of operations and cash flows.

Our systems or our third-party providers' systems may fail, which could interrupt our service, cause us to lose business, increase our costs and expose us to liability.

We depend on the efficient and uninterrupted operation of our computer systems, software, data centers and telecommunications networks, as well as the systems and services of third parties. A system outage or data loss could have a material adverse effect on our business, financial condition, results of operations and cash flows. Not only could we suffer damage to our reputation in the event of a system outage or data loss, but we may also be liable to third parties. Many of our contractual agreements with financial institutions and certain other customers require the payment of penalties if we do not meet certain operating standards. Our systems and operations or those of our third-party providers could be exposed to damage or interruption from, among other things, fire, climate-related events, including extreme weather events, natural disasters, pandemics, power loss, telecommunications failure, terrorist acts, war, unauthorized entry, human error, and computer viruses or other defects. Defects in our systems or those of third parties, errors or delays in the processing of payment transactions, telecommunications failures, or other difficulties (including those related to system relocation) could result in loss of revenues, loss of customers, loss of merchant and cardholder data, harm to our business or reputation, exposure to fraud losses or other liabilities, negative publicity, additional operating and development costs, fines and other sanctions imposed by card networks, and/or diversion of technical and other resources. There is also a risk that third-party suppliers of hardware and infrastructure required to support our employee productivity or our vendors could be affected by supply chain disruptions, such as manufacturing and shipping delays. An extended supply chain disruption could also affect the delivery of our services.

The payments technology industry is highly competitive and highly innovative, and some of our competitors have greater financial and operational resources than we do, which may give them an advantage with respect to the pricing of services offered to customers and the ability to develop new and disruptive technologies.

We operate in the payments technology industry, which is highly competitive and highly innovative. In this industry, our primary competitors include other independent payment processors, credit card processing firms, third-party card processing software institutions, as well as financial institutions, ISOs, prepaid programs managers and, potentially, card networks. Some of our current and potential competitors may be larger than we are and have greater financial and operational resources or brand recognition than we have. Our competitors that are financial institutions or subsidiaries of financial institutions do not incur the costs associated with being sponsored by a direct member for participation in the card networks, as we do in certain jurisdictions, and may be able to settle transactions more quickly for merchants than we can. These financial institutions may also provide payment processing services to merchants at a loss in order to generate banking fees from the merchants. It is also possible that larger financial institutions, including some who are customers of ours, could decide to perform in-house some or all of the services that we currently provide or could provide. These attributes may provide them with a competitive advantage in the market.

Furthermore, we are facing increasing competition from nontraditional competitors, including new entrant technology companies, who offer certain innovations in payment methods. Some of these competitors utilize proprietary software and service solutions. Some of these nontraditional competitors have significant financial resources and robust networks and are highly regarded by consumers. In addition, some nontraditional competitors, such as private companies or startup companies, may be less risk averse than we are and, therefore, may be able to respond more quickly to market demands. These competitors may compete in ways that minimize or remove the role of traditional card networks, acquirers, issuers and processors in the digital payments process. If these nontraditional competitors gain a greater share of total digital payments transactions, it could have a material adverse effect on our business, financial condition, results of operations and cash flows.

17

Additionally, the market for prepaid cards, demand deposit accounts and alternative financial services is similarly highly competitive, and competition is increasing as more companies endeavor to address the needs of underbanked consumers. We anticipate increased competition from alternative financial services providers who are often well positioned to service the underbanked and who may wish to develop their own prepaid card or demand deposit account programs. We also face strong price competition. To stay competitive, we may have to increase the incentives that we offer to our distributors and reduce the prices of our services, which could adversely affect our financial position, operating results and cash flows.

In order to remain competitive and to continue to increase our revenues and earnings, we must continually and quickly update our services, a process that could result in higher costs and the loss of revenues, earnings and customers if the new services do not perform as intended or are not accepted in the marketplace.

The payments technology industry in which we compete is characterized by rapid technological change, new product introductions, evolving industry standards and changing customer needs. In order to remain competitive, we are continually involved in a number of projects, including the development of new platforms, mobile payment applications, ecommerce services and other new offerings emerging in the payments technology industry. These projects carry the risks associated with any development effort, including cost overruns, delays in delivery and performance problems. In the payments technology markets, these risks are even more acute. Any delay in the delivery of new services or the failure to differentiate our services could render our services less desirable to customers, or possibly even obsolete. Furthermore, as the market for alternative payment processing services evolves, it may develop too rapidly or not rapidly enough for us to recover the costs we have incurred in developing new services targeted at this market.

In addition, certain of the services we deliver to the payments technology market are designed to process very complex transactions and deliver reports and other information on those transactions, all at very high volumes and processing speeds. Any failure to deliver an effective and secure product or any performance issue that arises with a new product or service could result in significant processing or reporting errors or other losses. We rely in part on third parties, including some of our competitors and potential competitors, for the development of and access to new technologies. As a result of these factors, our development efforts could result in higher costs that could reduce our earnings in addition to a loss of revenues and earnings if promised new services are not delivered timely to our customers or do not perform as anticipated.

Our revenues from the sale of services to merchants that accept Visa and Mastercard are dependent upon our continued Visa and Mastercard registrations, financial institution sponsorship and, in some cases, continued membership in certain card networks.

In order to provide our Visa and Mastercard transaction processing services, we must be either a direct member or be registered as a merchant processor or service provider of Visa and Mastercard, respectively. Registration as a merchant processor or service provider is dependent upon our being sponsored by Members of each organization in certain jurisdictions. If our sponsor financial institution in any market should stop providing sponsorship for us, we would need to find another financial institution to provide those services or we would need to attain direct membership with the card networks, either of which could prove to be difficult and expensive. If we are unable to find a replacement financial institution to provide sponsorship or attain direct membership, we may no longer be able to provide processing services to affected customers and potential customers in that market, which would negatively affect our revenues, earnings and cash flows. Furthermore, some agreements with our financial institution sponsors give them substantial discretion in approving certain aspects of our business practices, including our solicitation, application and qualification procedures for merchants and the terms of our agreements with merchants. Our sponsors' discretionary actions under these agreements could have a material adverse effect on our business, financial condition, results of operations and cash flows. In connection with direct membership, the rules and regulations of various card associations and networks prescribe certain capital requirements. Any increase in the capital level required would limit our use of capital for other purposes.

The termination of our registration, or any changes in the Visa or Mastercard rules that would impair our registration, could require us to stop providing Visa and Mastercard payment processing services, which would make it impossible for us to conduct our business on its current scale. The rules of the card networks may be influenced by card issuers, and some of those issuers also provide acquiring services and are our competitors or our customers in both the Merchant Solutions and Issuer Solutions segments. If we fail to comply with the applicable requirements of the card networks, the card networks could seek to fine us, suspend us or terminate our registrations or membership. The termination of our registrations or our membership or our status as a service provider or a merchant processor, or any changes in card association or other network rules or standards, including interpretation and implementation of the rules or standards, that increase the cost of doing business or limit our ability to provide transaction processing services to our customers, could have a material adverse effect on our business, financial condition, results of operations and cash flows. If a merchant or an ISO customer fails to comply with the applicable

18

requirements of the card associations and networks, we or the merchant or ISO could be subject to a variety of fines or penalties that may be levied by the card associations or networks. If we cannot collect or pursue collection of such amounts from the applicable merchant or ISO, we may have to bear the cost of such fines or penalties, resulting in lower earnings for us.

Our Business and Consumer Solutions segment relies on certain relationships with issuing banks, distributors, marketers and brand partners. The loss of such relationships, or if we are unable to maintain such relationships on terms that are favorable to us, may materially adversely affect our business, financial position, operating results and cash flows.

Our Business and Consumer Solutions segment relies on arrangements that we have with issuing banks to provide us with critical products and services, including the FDIC-insured depository accounts tied to the cards and accounts we manage, access to the ATM networks, membership in the card associations and network organizations and other banking services. The majority of our active Business and Consumer Solutions cards and accounts are issued or opened through Meta Payment Systems ("MetaBank"). If any material adverse event were to affect MetaBank's or another of our critical issuing banks, or we were to lose MetaBank or another critical bank, or MetaBank or another critical bank grew to a size such that it was no longer able to avail itself of certain regulatory exemptions for small banks, we may be forced to find an alternative provider for these critical banking services. It may not be possible to find a replacement bank on terms that are acceptable to us or at all. Any change in the issuing banks could disrupt the business or result in arrangements with new banks that are less favorable to us than those we have with our existing issuing banks, either of which could have a material adverse effect on our business, financial position, operating results and cash flows.