UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

[X] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM OCTOBER 1, 2015 TO DECEMBER 31, 2016

Commission file number:000-31355

| FTE NETWORKS, INC. |

| (Exact name of registrant as specified in its charter) |

| Nevada | 81-0438093 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

| 999 Vanderbilt Beach Rd., Suite 601, Naples, Florida 34108 |

| (Address of principal executive offices) |

Registrant’s telephone number, including area code:1-877-878-8136

Securities registered pursuant to Section 12(b) of the Act: Not Applicable

Securities registered pursuant of section 12(g) of the Act: Common Stock, par value $0.001 per share

Indicate by check mark if the registrant is well-known seasoned issuer, as defined in Rule-405 of the Securities Act. [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Note-Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§ 235.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [X] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant of Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definite proxy of information statements incorporated by reference in Part III of the Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “larger accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| None-accelerated filer [ ] | (Do not check if a smaller reporting company) | Smaller Reporting Company [X] |

Emerging growth company [ ] |

||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [ ] No

As of June 30, 2016, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $2,632,421.

As of May 11, 2017, there were 126,247,694 shares of common stock outstanding.

FTE NETWORKS, INC.

FORM 10-K

TABLE OF CONTENTS

TRANSITION PERIOD ENDED DECEMBER 31, 2015 AND DECEMBER 31, 2016

Some of the statements in this Annual Report on Form 10-K may be “forward-looking statements.” Forward-looking statements are not historical facts but include, but are not limited to, statements that express our intentions, beliefs, expectations, strategies, predictions or any other statements relating to our future activities or other future events or conditions. These statements are based on current expectations, estimates and projections about our business based, in part, on assumptions made by management. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that are difficult to predict.

Forward-looking statements can be identified by the use of terminology such as “estimates,” “projects,” “plans,” “believes,” “expects,” “anticipates,” “intends,” or the negative or other variations, or by discussions of strategy that involve risks and uncertainties. We urge you to be cautious of the forward-looking statements which are contained in this Annual Report on Form 10-K because they reflect our current beliefs with respect to future events and involve known and unknown risks, uncertainties and other factors affecting our operations, market growth, services, products and licenses. No assurances can be given regarding the achievement of future results, as actual results may differ materially as a result of the risks we face, and actual events may differ from the assumptions underlying the statements that have been made regarding anticipated events. Factors that may cause actual results, our performance or achievements, or industry results, to differ materially from those contemplated by such forward-looking statements include, without limitation:

| ● | Our ability to maintain sufficient liquidity; | |

| ● | Our ability to attract and retain key personnel and temporary workers; | |

| ● | Our ability to collect account receivables; | |

| ● | Our ability to manage the growth of our operations and effectively integrate acquisitions; | |

| ● | Our ability to retain our key customers and market share; | |

| ● | Our ability to compete for suitable merger prospects; | |

| ● | Our ability to successfully integrate future acquisitions; | |

| ● | Our ability to satisfy our service level agreements; | |

| ● | Our ability to effectively manage our backlog; | |

| ● | The impact of legislative actions and significant regulations on our business; | |

| ● | Our ability to adapt to swift changes in the telecommunications industry; | |

| ● | The effectiveness of our physical infrastructure and services; | |

| ● | Fluctuations in general conditions; | |

| ● | Our ability to comply with regulations; | |

| ● | The effects of any employment related to other claims against our business; | |

| ● | Our ability to maintain workers’ compensation insurance coverage at commercially reasonable terms; and | |

| ● | Our ability to raise capital when needed and on acceptable terms and conditions. |

All written and oral forward-looking statements made in connection with this Annual Report on Form 10-K that are attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. Any forward-looking statements speak only as of the date on which they are made, and we do not undertake any obligation to update any forward-looking statement to reflect events or circumstances after the date of this Annual Report on Form 10-K. Given the uncertainties that surround such statements, you are cautioned not to place undue reliance on such forward-looking statements.

| 1 |

FTE Networks, Inc. (FTNW), and its wholly owned subsidiaries, is a leading international networking infrastructure service solutions company. The Company designs, build, and support telecommunications and technology systems and infrastructure services for Fortune 500 companies operating four (4) telecommunications markets; Data Center Infrastructure, Fiber Optics, Wireless Integration, and Surveillance & Security. FTE Networks is headquartered in Naples, Florida, with offices throughout the United States and Europe.

● Jus-Com, Inc., (dba FTE Network Services) specializes in the design, engineering, installation, and maintenance of all forms of telecommunications infrastructure. Services include engineering consulting, design, installation, maintenance, and emergency response in various categories including cabling, equipment installation and configuration, rack and stack, wiring build-outs, infrastructure build-outs, DC power installation, OSP/ISP fiber placement, fiber cable splicing and testing.

● FTE Wireless, LLC, offers wireless solutions to major wireless carriers including equipment installation, fiber backhaul, antennae installation and testing, small cell solutions, fiber-to-site and other turnkey solutions as needed by such clients.

● Focus Venture Partners, Inc. (dba FVP Worx) is a multifaceted employment firm offering full service staffing solutions, specializing in the telecommunications, technology and construction services industries.

FTE Network Services and FTE Wireless Service, LLC are reported in the Company’s telecommunications segment. FVP Worx represents the Company’s staffing segment.

CORPORATE HISTORY

Prior to Beacon Merger

Beacon Enterprise Solutions Group

Beacon Enterprise Solutions Group, Inc. (“Beacon”) was incorporated in the state of Nevada on December 30, 2007. On September 5, 2012 Beacon sold its operating assets and Beacon ceased its business operations, in order to meet its financial obligations and avoid bankruptcy, but maintained its public company “shell” status.

Focus Venture Partners, Inc.

Focus Venture Partners, Inc. (“Focus”) was incorporated in the state of Nevada on March 26, 2012 as a holding company operating in the telecommunications industry managing and developing its wholly owned subsidiaries, which were focused on the development of telecommunications networks, acting as a service and support provider, as well as providing temporary and part-time staffing solutions.

Through Optos Capital Partners, LLC, a Delaware limited liability company (“Optos”), its wholly owned subsidiary, Focus operated the following wholly owned entities:

| ● | Focus Fiber Solutions, LLC, a Delaware limited liability company (“Focus Fiber”), which specialized in the design, engineering, installation, and maintenance of a telecommunications infrastructure network. |

| ● | JusCom, Inc., an Indiana corporation (“JusCom”), which was a telecommunication service provider providing various services including engineering consulting, design, installation and emergency response in various categories including cable rack/wiring buildouts, infrastructure buildouts, DC power installation, fiber cable splicing and security camera installation. JusCom also operated as a temporary and permanent staffing agency specializing in the telecommunications market. Prior to the Beacon Merger, Focus reorganized such that Jus-Com became a subsidiary of Focus, and was no longer a subsidiary of Optos. |

| 2 |

Beacon Merger

On May 10, 2013, Beacon and Beacon Acquisition Sub, Inc. a Nevada corporation and a wholly owned subsidiary of Beacon (the “Merger Sub”) entered into a merger agreement with Focus (the “Merger Agreement”). Pursuant to the Merger Agreement, the Merger Sub merged with and into Focus, with Focus continuing as the surviving corporation, with the result that Focus became a subsidiary of Beacon (the “Beacon Merger”). The closing of the merger took place on June 19, 2013.

For accounting purposes, the Beacon Merger has been treated as an acquisition of Beacon, and a recapitalization of Focus Venture Partners. The historical consolidated financial statements prior to June 19, 2013 are those of Focus Venture Partners. In connection with the Beacon Merger, Focus Venture Partners has restated its statements of stockholders’ deficiency on a recapitalization basis so that all equity accounts are presented as if the recapitalization had occurred as of the beginning of the earliest period presented.

In connection with the Beacon Merger, the Board of Directors authorized the designation of a new series of preferred stock, the Beacon Series D Shares, out of its available “blank check preferred stock” and authorized the issuance of up to 2,000,000 Beacon Series D Shares. We filed a Certificate of Designation with the Secretary of State of the State of Nevada on June 17, 2013. Under the Certificate of Designation, each Beacon Series D Share has various rights, privileges and preferences, including: (i) a stated value of $4.00 per share; (ii) mandatory conversion into 20 shares of Common Stock (subject to adjustments) upon the filing of the amendment to our Articles of Incorporation after incorporating the 1 for 20 reverse stock split of the outstanding shares of common stock required by the Merger Agreement (and an effective increase in the Company’s authorized common stock); and (iii) a liquidation preference in the amount of the stated value.

In connection with the Beacon Merger the Board of Directors authorized the designation of a new series of preferred stock, the Beacon Series E Shares, out of its available “blank check preferred stock” and authorized the issuance of up to 1,000,000 Beacon Series E Shares. We filed a Certificate of Designation with the Secretary of State of the State of Nevada on June 17, 2013. Under the Certificate of Designation, each Beacon Series E Share has various rights, privileges and preferences, including (i) a liquidation value of $1.00 per share (subject to adjustments); (ii) mandatory redemption of 10,000 shares per month at the liquidation value; and (iii) conversion at the option of the Company of all outstanding Beacon Series E Shares at a price equal to half the liquidation value after 48 mandatory redemption payments have been made.

Pursuant to the terms of the Merger Agreement: (i) shares of Series B Preferred Stock of Focus, par value $0.0001 per share (the “Focus Preferred B Shares”) and common stock of Focus, par value $0.0001 per share (the “Focus Common Stock”) were converted into the right to receive an aggregate of 1,250,011 shares of Beacon Series D Preferred Shares, par value $0.01 per share); (ii) all shares of Series A Preferred Stock of Focus, par value $0.0001 per share, were converted into the right to receive an aggregate number of 1,000,000 shares of Beacon Series E shares, par value $0.01 per share, (iii) all shares of capital stock of Merger Sub were converted into one share of Focus Common Stock. Each Beacon Series D and Beacon Series E share is entitled to vote alongside the common stockholders and has 20 and 1 vote(s) each, respectively. The Beacon Series E shares were subject to redemption and were recorded as a liability, but the shares were returned to the Company and derecognized on September 30, 2013. The Beacon Merger represented a change of control of Beacon and Focus management became responsible for the consolidated entity.

The consideration issued in the Merger was determined as a result of arm’s length negotiations between the parties.

| 3 |

Changes Resulting from the Merger

Our mission is to expand the operations of Jus-Com Inc. dba FTE Network Services as our primary line of business. Jus-Com is headquartered in Naples, Florida specializing in the design, engineering, installation, construction and maintenance of telecommunications and technology networks and infrastructure.

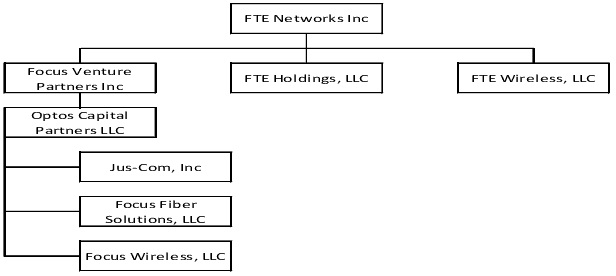

Following the Beacon Merger, on March 13, 2014, Beacon changed its name to “FTE Networks, Inc.” (“FTE” or the “Company”). JusCom began doing business as FTE Network Services (“FTE Network Services”) - a turn-key infrastructure services company. Focus Venture Partners began doing business as FVP Worx, Inc., offering full service staffing solutions. Optos Capital Partners remains for the purpose of future diversification opportunities. The following graphic depicts our organization following the Beacon Merger and the organizational changes described above, and represents the current organization of the Company:

| 4 |

RECENT DEVELOPMENTS

The Registration and Trading of Our Securities

Prior to September 12, 2014 (the “Revocation Date”), our Common Stock was registered under Section 12(g) of the Exchange Act of 1934, as amended (the “Exchange Act”). Pursuant to such registration, the Company was subject to the requirements of Regulation 13(a) of the Exchange Act which required us to file with the SEC, in part, annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and to comply with all other obligations of the Exchange Act applicable to issuers filing registration statements pursuant to Section 12(g) of the Exchange Act.

After we ceased our business operations and became a public company “shell” on September 5, 2012, we fell behind on the compilation of our books and records, due to challenges related to staffing, access to historical data and insufficient funding. Consequently, we failed to comply with the reporting requirements of Regulation 13(a) of the Exchange Act. Further, the Company underestimated the time that it would take for the registrant to access and analyze the historical data to enable it to become current in its financial reporting. As a result, on August 20, 2014, the U.S. Securities and Exchange Commission (the “SEC”), via Release No. 72872, ordered the commencement of an Administrative Proceeding (File No. 3-16024) with respect to the Company. The SEC observed and asserted that the Company had failed to comply with its obligations under Exchange Act Section 13(a) and Rules 13a-1 and 13a-13 thereunder because the Company had not filed any periodic reports with the SEC since the period ended June 30, 2012. Also on August 20, 2014, in connection with the foregoing, the SEC announced the temporary suspension of trading in the securities of the Company.

Subsequently, on September 8, 2014, the Company entered into an Offer of Settlement with the SEC regarding the Administrative Proceeding (File No. 3-16024) whereby, in part, the Company consented to the entry of an Order by the SEC containing the findings that: (1) the Company was a Nevada corporation located in Naples, Florida with a class of securities registered with the Commission under Exchange Act Section 12(g) and as of August 18, 2014, the common stock of the Company (symbol FTNW) was quoted on OTC Link (formerly “Pink Sheets”) operated by OTC Markets Inc., had ten market makers, and was eligible for the “piggyback” exception of Exchange Act Rule15c2-11(f)(3); (2) the Company had failed to comply with Exchange Act Section 13(a) and Rules 13a-1 and 13a-13 thereunder because it had not filed any periodic reports with the SEC since the period ended June 30, 2012; and that on the basis of the foregoing (3) pursuant to Section 12(j) of the Exchange Act, registration of each class of the Company’s securities registered pursuant to Exchange Act Section 12 be revoked.

As such, on the Revocation Date, via Release No. 73085, the SEC ordered that, effective immediately pursuant to Section 12(j) of the Exchange Act, the registration of each class of the Company’s securities registered pursuant to Exchange Act Section 12 be revoked.

Following the above described revocation of registration, on March 17, 2015 we filed a registration statement on Form 10, to once again register our Common Stock pursuant to Section 12(g) of the Exchange Act. On May 16, 2015, the registration statement became effective, and we are again subject to the requirements of Regulation 13(a) of the Exchange Act, which requires us to file, in part, annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and we are required to comply with all other obligations of the Exchange Act applicable to issuers filing registration statements pursuant to Section 12(g) of the Exchange Act.

On December 10, 2015, our common stock resumed trading on the OTC Pink marketplace. As of December 31, 2016, our common stock is trading on the OTCQX marketplace.

| 5 |

Authorization of Series F Preferred Stock

The Board of Directors of the Company authorized the designation of a new series of preferred stock, the Series F Stock (“Series F Stock”), out of its available “blank check preferred stock” and authorized the issuance of up to 1,980,000 shares of the Series F Stock. A Certificate of Designation was filed with the Secretary of State of the State of Nevada on November 2, 2015. The Series F Stock has various rights, privileges and preferences, including: (i) a stated value of $4.00 per share; (ii) conversion into 20 shares of Common Stock (subject to adjustments) upon the filing of an amendment to the Company’s Articles of Incorporation incorporating a reverse stock split; and (iii) a liquidation preference in the amount of the stated value.

Entry into a Credit Facility and Repayment of Senior Secured Notes

On November 3, 2015, the Company entered into a credit agreement (the “Agreement”) pursuant to which the Company received $8 million in term loans from Lateral Investment Management (“Lateral”). A portion of the proceeds was used to extinguish an aggregate principal amount of approximately $3.4 million of Senior Secured Promissory Notes, pursuant to a tender offer. The noteholders who tendered their notes received the tender offer consideration of $0.50 per $1 principal amount of the Notes from the proceeds from the term loan, and all interest payable on the notes was forgiven. The Company recognized approximately a $3.4 million gain related to the extinguishment of the Senior Secured Promissory Notes.

In connection with the agreement, the Company issued 555,344 shares of preferred stock to Lateral, 163,441 designated as Series D preferred stock and 391,903 designated as Series F preferred stock. Upon the approval of the reverse split of common stock on or about May 26, 2016, these preferred shares mandatorily converted to 11,106,880 shares of common stock, based upon their 1 for 20 conversion rate. The Company and Lateral also entered into a registration rights agreement (“Registration Rights Agreement”) in connection with the issuance of these shares, pursuant to which the Company must file a registration statement with the SEC, with respect to the shares. Lateral may request redemption of some or all of its shares any time after October 28, 2017, subject to the Company (a) meeting certain minimum capitalization and EBITDA requirements; and (b) being able to continue as a going concern on a post-redemption basis. The redemption price per share is variable and equals 10 (ten) times the last twelve months EBITDA, multiplied by the Lateral fully-diluted ownership percentage and then divided by the Lateral shares outstanding. In addition, Lateral was granted anti-dilution rights which permit it to receive additional equity securities to maintain its fully-diluted ownership interest to the extent that the Company issues equity securities to third parties, up to a maximum of $5,000,000. On April 5, 2016, the Company entered into an amendment agreement to its existing credit facility with Lateral, amending the original credit agreement signed October 28, 2015. The agreement amends select provisions of the original credit agreement, including equity raises and changes to certain financial and operational covenants. On September 30, 2016, the Company entered into a second amendment agreement to its existing credit facility, maturing October 28, 2017, amending the original credit agreement signed October 28, 2015. The agreement was amended solely to consolidate a series of short term bridge loans granted to the company from time to time during the second and third quarter of 2016 into a 2.5 million loan, which matures on April 30, 2017. The second amendment also amended the covenants related to consolidated EBITDA, consolidated leverage, consolidated debt service, selling, general, and administrative expenses, and compensation expense. On April 20, 2017, in conjunction with the acquisition of Benchmark Builders Inc, Lateral amended the original credit agreement to provide for approximately $10.1 million towards the cash purchase price of the Benchmark acquisition, refinancing this new advance with the existing debt, extending the maturity date of the facility to March 31, 2019.

Reverse Split of Common Stock

On December 23, 2015, the Board unanimously authorized and approved an amendment to our Articles of Incorporation to effect a reverse stock split of our Common Stock at a 1-for-20 ratio (the “Reverse Split”). On December 30, 2015, stockholders holding a majority of our voting power approved by written consent the amendment to our Articles of Incorporation, which would affect the Reverse Split. The Reverse Split will reduce the number of outstanding shares of our Common Stock by reclassifying and converting all outstanding shares of our Common Stock into a proportionately fewer number of shares of Common Stock. On March 9, 2016, the Company filed a Form Pre-14C with the SEC concerning the 1 for 20 reverse stock split and the increase of the authorized shares of common stock from 70,000,000 to 200,000,000. On April 18, 2016, the Company filed its Definitive Form 14-C with the SEC. On May 25, 2016 “FINRA” approved the Reverse Split, which was effectuated on May 26, 2016. All share and share information in this transitional report have been retroactively restated for the reverse split.

Officer/Strategic Board Appointments

On July 28, 2016, the Board of Directors of FTE Networks, Inc. (the “Company”) approved the appointment of Michael Bonewitz as the Company’s Chief Technology Officer commencing on August 24, 2016 and has replaced Carlie Ancor who will transition into a new role supporting the Company’s major account sales strategy. Mr. Bonewitz has over 20 years of senior management experience in communications network engineering and information technology industries developing cutting edge capabilities via advanced IT automation and data analytics driving operational and financial performance. Prior to FTE, he was VP of Strategy and Product Development for Cloud services, Fiber engineering and construction at Nexius where he developed and launched the company’s first fiber deployment program supporting multiple Tier 1 service providers in the US. He also led the company strategy and participation into Open Compute Project (OCP) as a Platinum member and as an original member of Facebook’s Telcom Infra Project (TIP). He has held previous technology and engineering leadership positions with Ericsson, Zayo and Level 3.

On September 27, 2016, the Board of Directors appointed Mr. Lynn Martin as Chief Operating Officer. As COO, Mr. Martin will be responsible for the prioritization and alignment of company initiatives overseeing, developing, and setting the strategic direction for the day-to-day operations of FTE Networks and ensuring operational excellence across the company. Prior to joining FTE, Mr Martin was head of the communications, software, and technology division of Nexius where he was responsible for growing the business by delivering end-to-end network solutions for emerging technologies, such as Open Source/NFV/SDN and infrastructure services that provided relevant value to customers and helped them to optimize their businesses. In addition to leading the software and technology teams, he created several new business offerings in Engineering, Fiber and Open Source development where he joined efforts with Open Compute Project and Telecom Infra Project communities both founded by Facebook to provide new network architectures and solutions with greater simplicity and efficiency. Before Nexius, Mr. Martin served as Executive Director of Telcordia Technologies, where he ran the company’s next generation software product line, was a senior strategist in Accenture’s Network Practice, and spent over a decade at Level 3 Communications as VP of Operational Integration and Process Management.

| 6 |

On December 7, 2016, a Strategic Advisory Board was created to provide senior counsel to the company on opportunities to evolve and advance the deployment of its disruptive multi-edge computing services. External members of FTE Networks’ Multi-Edge Computing Strategic Advisory Board are:

John Morgan. Mr. Morgan is currently working with operators to improve network coverage and capacity to make the world more open and connected. Morgan has over twenty-five years in the Communications and IT Industries and is currently supporting operators with the adoption of open source hardware and software in their networks through the Open Compute Project (OCP) and Telecom Infrastructure Project (TIP) initiatives. Prior to his current work, Morgan was global technical lead for legacy network migrations at Accenture where he worked with operators on product rationalization and simplification, copper to fiber migration platform implementations, and decommissioning strategies for copper and central office equipment. Prior to Accenture, he held executive positions with several software start-up firms in the communications industry, as well as with leading operators, such as Verizon, Level 3 Communications, and Genuity. His background includes work in network planning and engineering, product management, OSS/BSS development, finance, and operations. He completed his undergraduate work in Accounting at the College of William and Mary and received his MS in Information and Telecommunications Systems from the Johns Hopkins University.

David Kalinske. Mr. Kalinske is the Chief of Staff for A3 by Airbus Group and former Aide to two U.S. Presidents, President George W. Bush and President Barack Obama. In his previous role, he was the recipient of the Defense Superior Service Medal for superior meritorious service in the position of significant national responsibility as Aide to the President of the United States. He also served as a research engineering leader with Lockheed Martin Aeronautics supporting Advanced Development programs, also known as The Skunk Works, and founded Global Hybrid Company, an airborne logistics provider utilizing the revolutionary Hybrid Airship. A TOPGUN graduate and a Marine Corps fighter squadron Commanding Officer (CO), he was selected via scholarship into the Harvard University, Kennedy School of Government, National Security Fellow program with a focus in the study of cybersecurity policy.

Eric Salzman. Mr. Salzman has 20 years of experience working with communications and software companies with a focus on driving operational and financial excellence. He is currently a Senior Managing Director at Monarch Capital Group, LLC, a boutique investment bank and money management firm and serves as an independent director on several public and private technology company boards including 8x8, Inc., ASG Technologies, Sorenson Communications and FragranceNet.com. Prior to 2011, Mr. Salzman spent eight years at Lehman Brothers as a Managing Director in the Private Equity and Principal Investing Group, as well as a Managing Director in the Global Trading Strategies Division, including three years managing the operational and financial restructuring of dozens of companies within the Lehman Bankruptcy. Prior to Lehman Brothers, Mr. Salzman was a senior investment professional focused on the technology and communications industry at a multi-strategy hedge fund and at two growth-oriented private equity funds. Mr. Salzman began his career in the M&A Group at CS First Boston. Mr. Salzman graduated with a B.A. Honors from the University of Michigan and received his MBA from Harvard University.

TELECOMMUNICATIONS INFRASTRUCTURE SERVICES INDUSTRY

FTE Network Services provides comprehensive telecommunications solutions to Fortune 500 and other customers in the wireline and wireless telecommunications industry. Services performed by FTE include the design, engineering, installation, repair and maintenance of fiber optic, copper and coaxial cable networks used for video, data and voice transmission. In the wireless space, FTE provides engineering, design, installation and upgrade of wireless communications networks, including infrastructure, antennas, switching systems, and backhaul links from wireless systems to voice, data and video networks. FTE also provides emergency restoration services, including the repair of telecommunications infrastructure damaged by inclement weather. We also provide premise wiring where we install, repair, and maintain the telecommunications structure within improved structures.

FTE Network Services’ success in these technology spaces is the result of experienced management and leadership, purchasing relationships and logistics, project planning, project management disciplines, training, quality control and top down commitment to customer satisfaction.

We believe that certain provisions of the American Recovery and Reinvestment Act of 2009 (“ARRA”) will continue to create additional demand for our services. Specifically, the ARRA includes federal stimulus funding for the deployment of broadband services to underserved areas that lack sufficient bandwidth to adequately support economic development. We also expect many customers who received stimulus funds to continue to expand their networks even though stimulus funding may no longer be available.

The combination of a growing North American wireless subscriber base, greater use of wireless data for consumer and enterprise applications and services, and the development of innovative consumer wireless data products has led to a significant increase in the amount of wireless data traffic on wireless networks. As a result, the traditional backhaul infrastructure that has historically linked wireless cell sites to broader voice, data and video networks is reaching capacity. To handle current and future wireless data traffic demands and to improve wireless network quality and reliability, wireless carriers are implementing plans to replace their legacy backhaul networks based on T-1 lines and circuit switching applications with fiber optic networks, typically referred to as “fiber to the cell site” initiatives. We believe these initiatives will continue several more years before the backhaul system upgrade is completed, resulting in additional opportunities to assist our wireless customers in their fiber to the cell site initiatives.

| 7 |

We anticipate increased long-term opportunities arising from plans by a number of wireless companies to deploy and implement 4G and LTE (Long Term Evolution) and XLTE (Extended Long Term Evolution) technology and networks throughout North America. These technologies are being deployed in the United States using a new spectrum, which effectively requires an entirely new network to be built. As a result, we expect significant capital expenditures will be made over a relatively long period of time as wireless carriers build out their 4G and LTE networks and then augment and optimize their networks for reliability and network quality. We believe wireless carriers are in the very early stages of their 4G and LTE network deployment plans.

Fiber to the X (“FTTx”) comprises the many variants of fiber optic access infrastructure. These include fiber to the home (“FTTH”), fiber to the premise (“FTTP”), fiber to the building (“FTTB”), fiber to the node (“FTTN”), and fiber to the curb or cabinet (“FTTC”). GIA announces the release of a comprehensive global report on Fiber Optic Components market. Global market for Fiber Optic Components is projected to reach US$42 billion by the year 2017. Growth will be driven by the continuously growing demand for bandwidth and the ensuing need for fiber-based broadband, robust growth in mobile internet, and stronger FTTx related deployments.

Outside Plant Operations

Outside Plant Operations (OSP) includes all forms and methods of connecting the nation’s telecommunications infrastructure. Historically this work has been with copper and then coax. Today, it is predominately aerial and buried fiber. FTE builds outside plant for large corporate customers, government entities and private investors.

FTE Network Services has scaled to approximately 200+ concurrent crews in multiple geographies representing multiple customers and multiple projects. FTE Network Services’ success is based on several factors:

| ● | Staff construction experience in these markets over many years in the past provides an understanding of the challenges in most every market with respect to local regulations to diverse soil types and rock formations. | |

| ● | FTE has a network of seasoned Project Managers and Construction Managers that it leverages in all markets on all projects. | |

| ● | FTE uses a blend of self-perform and sub-contract that maintains internal quality standards and allows the company to expand operation rapidly and likewise downsize at completion preserving company profitability. | |

| ● | FTE creates a local presence for all projects with local office and warehouse space to run and manage the project and handle materials logistics respectively. | |

| ● | FTE has relationships with major national suppliers for everything from heavy equipment to custom order fiber optic cable. | |

| ● | All contract outside plant operations are fulfilled with a combination of our fleet of aerial trucks, underground plows, directional drills, fiber placement crews, and fiber splicers. | |

| ● | All equipment used on OSP projects is mobile, with dedicated logistics to service these projects as demands change. FTE Network Services can meet any scheduling requirement and accommodate changing demands by calling on its extensive network of strategic partners. | |

| ● | Finally, FTE itself has a broad base of experienced operators and installers dedicated to each project, and we are committed to providing the necessary personnel and equipment to meet the demands of every engagement. |

Inside Plant Operations

Inside Plant Operations (ISP) are services provided to major telecommunications services providers in their switching and processing facilities. The scope of services includes the following:

| ● | Cable rack / wiring build-outs | |

| ● | Infrastructure build-outs | |

| ● | DC power installation | |

| ● | Battery installation / maintenance | |

| ● | Uninterrupted power source (“UPS”) installation | |

| ● | Power distribution unit (“PDU”) installation | |

| ● | Fiber cable splicing | |

| ● | Structured cable installation | |

| ● | All low-voltage cable installation | |

| ● | Provisioning, test, turn-up of FTTP, FTTN, FTTH, FTTx. | |

| ● | Security camera installation | |

| ● | AC circuits & conduit builds |

Each major telecommunications client has their own build and quality standards. FTE trains its technicians in each specific protocol and has quality standards that it maintains on each and every project. FTE has the capability to engineer, build, turn up, test and manage every component in a client’s facility. The facilities that we work in performing ISP work are secure, highly available and mission critical to the countries telecommunications infrastructure. The client facilities that FTE works inside of touches everything from Wall Street trading floors to the video, telephone and data services used every day by the typical family and individual. This critical infrastructure connects corporate land based services, mobile data services, on-demand video, TV and cable broadcast, internet, public networks, private networks and telephone. The quality of the work product from engineering to construction in this work is critical.

| 8 |

Our clients engage us with confidence as is shown by our solid, standing relationships and repeat business opportunities that have been tested and forged over time.

Project Estimating and Feasibility Studies

Our subsidiaries share an estimating department that provides all cost needs, both internal and external, as a value-added service to telecommunications clients. For extremely difficult builds, we use a “boots on the ground” approach, ready with someone to look at the project up close, typically within 24 hours. For the bid process, the following steps are followed:

| ● | A request for a proposal, or a request for information is received from a prospective customer: typically a data file is provided with a general route, cell tower locations, laterals, rings, etc. | |

| ● | Using Google Earth, we provide a solution based on aerial and underground construction options, utilizing the U.S. geological studies for ground conditions and “street view” programs to analyze the conditions. Additional services are often used, including: MS Streets & Trips, MapInfo, Bing Maps, Delorme, and a national database of GIS maps. At the same time, we reach out to vendors and suppliers to start assessing rough costs for materials and labor. | |

| ● | We specialize in complex projects with a large geographical footprint and multiple customer drop points. This goal is met by importing the customer drop points (i.e., latitude and longitude) into whichever software program the customer has specified as the deliverable. Then, using the aforementioned methods, we identify the best installation path and verify whether the most cost-effective method of installation will be aerial, underground, or existing conduit paths. This conclusion is portrayed on the deliverable software, and the different methods of construction are clearly defined by specific colors on the reports. | |

| ● | The project is broken into segments with independent budgets for each segment, allowing the customer to identify the fiber size based upon end-use requirements. This all flows into a master project budget, giving the customer a snapshot that will allow them to make changes to the individual segments at their discretion based upon the budgetary information provided. | |

| ● | The nationwide network of project managers is utilized to analyze the geography of each part of the project and provide feedback on critical portions of the proposed build. | |

| ● | This all culminates into finished proposals - ones that we believe accurately represent the ideal and most cost-effective approach to the build process. Due to the process, we have solidified in our estimating department, bringing in and training additional support staff typically takes less than 2 weeks. |

Customer Relationships

Our current customers include, in part, multiple Fortune 500 telecommunications and technology providers and integrators. We also provide telecommunications engineering, construction, installation and maintenance services to a number of cable television multiple system operators. Premise wiring services are provided to various corporations and state and local governments.

Our customer base is concentrated. Due to the fact that the majority of our revenues are non-recurring, project-based revenues, it is not unusual for there to be significant period-to-period shifts in customer concentrations. Revenue may significantly decline if the Company were to lose one or more of its significant customers, or if the Company were not able to obtain new customers upon the completion of significant contract. The Company’s strategy for the future includes customer and service diversification reducing the customer revenue concentration to less than 15% for any single customer.

For the year ended September 30, 2015, the Company’s largest customers included a telecommunications company providing fiber optic based network solutions, (Customer C), and a corporate staffing customer within the Company’s staffing segment, (Customer D). During the transitional three months ended December 31, 2015, the Company’s largest customers included a multinational provider of communications technology and services, (Customer I) and a corporate staffing customer within the Company’s staffing segment, (Customer D). For the year ended December 31, 2016, the Company’s largest customers included multinational telecommunications conglomerate (Customer M) and leader service provider in network managed and professional services, (Customer J).

| 9 |

The following tables set forth our revenues and accounts receivable balances for the periods indicated:

| For the Year Ended | For

the Transitional Three Months Ended |

For the Year Ended | ||||||||||||||||||||||

| December 31, 2016 | December 31, 2015 | September 30, 2015 | ||||||||||||||||||||||

| Revenues | $ | % | $ | % | $ | % | ||||||||||||||||||

| Customer C | 164,987 | 1 | % | 41,664 | 1 | % | 5,196,380 | 36 | % | |||||||||||||||

| Customer D | - | - | % | 1,592,193 | 52 | % | 5,324,866 | 37 | % | |||||||||||||||

| Customer I | 91,000 | 1 | % | 316,931 | 11 | % | 106,850 | 1 | % | |||||||||||||||

| Customer J | 1,804,760 | 14 | % | - | - | - | - | |||||||||||||||||

| Customer M | 6,332,966 | 52 | % | 130,771 | 4 | % | 552,054 | 4 | % | |||||||||||||||

| All other customers | 3,875,366 | 32 | % | 989,246 | 32 | % | 3,208,532 | 22 | % | |||||||||||||||

| Total Revenues, net of discounts | $ | 12,269,079 | 100 | % | $ | 3,070,805 | 100 | % | $ | 14,388,682 | 100 | % | ||||||||||||

| For the Year Ended | For

the Transitional Three Months Ended |

For the Year Ended | ||||||||||||||||||||||

| December 31, 2016 | December 31, 2015 | September 30, 2015 | ||||||||||||||||||||||

| Accounts Receivable | $ | % | $ | % | $ | % | ||||||||||||||||||

| Customer B | 85,112 | 1 | % | 152,475 | 10 | % | 152,475 | 12 | % | |||||||||||||||

| Customer E | 603,663 | 9 | % | 718,035 | 47 |

% | 617,825 | 47 | % | |||||||||||||||

| Customer H | 102,796 | 2 | % | 215,609 | 14 | % | 50,767 | 4 | % | |||||||||||||||

| Customer M | 4,624,600 | 66 | % | 62,233 | 4 | % | 66,832 | 5 | % | |||||||||||||||

| All other customers | 1,722,354 |

22 | % | 387,128 | 25 | % | 416,546 | 32 | % | |||||||||||||||

| Total Receivables | 7,138,525 |

100 | % | $ | 1,535,480 | 100 | % | $ | 1,304,445 | 100 | % | |||||||||||||

| Less Allowance for doubtful accounts | (118,949 |

) | $ | (89,000 | ) | $ | (89,000 | ) | ||||||||||||||||

| Accounts Receivable, net of allowance | 7,019,576 |

$ | 1,446,480 | $ | 1,215,445 | |||||||||||||||||||

Competition

The markets in which we operate are highly competitive. We compete with other contractors in most of the geographic markets in which we operate, and several of our competitors are large companies that have significant financial, technical and marketing resources. In addition, there are relatively few barriers to entry into some of the industries in which we operate and, as a result, any organization that has adequate financial resources and access to technical expertise may become a competitor. A significant portion of our revenues is currently derived from unit price or fixed price agreements, and price is often an important factor in the award of such agreements. Accordingly, we could be underbid by our competitors in an effort by them to procure such business. Economic conditions have increased the impacts of competitive pricing in certain of the markets that we serve. We believe that customers consider other factors in choosing a service provider, including technical expertise and experience, financial and operational resources, nationwide presence, industry reputation and dependability, which we expect to benefit larger contractors such as us. In addition, competition may lessen as industry resources, such as labor supplies, approach capacity. There can be no assurance, however, that our competitors will not develop the expertise, experience and resources to provide services that are superior in both price and quality to our services, or that we will be able to maintain or enhance our competitive position. We also face competition from the in-house service organizations of our existing or prospective customers, including telecommunications and engineering companies, which employ personnel who perform some of the same types of services as those provided by us. Although a significant portion of these services is currently outsourced by many of our customers, there can be no assurance that our existing or prospective customers will continue to outsource services in the future.

Regulation

Our operations are subject to various federal, state, local and international laws and regulations including:

| ● | licensing, permitting and inspection requirements applicable to contractors, electricians and engineers; | |

| ● | regulations relating to worker safety and environmental protection; | |

| ● | permitting and inspection requirements applicable to construction projects; | |

| ● | wage and hour regulations; | |

| ● | regulations relating to transportation of equipment and materials, including licensing and permitting requirements; and | |

| ● | building and electrical codes. |

| 10 |

We believe that we have all the licenses required to conduct our operations and that we are in substantial compliance with applicable regulatory requirements. Our failure to comply with applicable regulations could result in substantial fines or revocation of our operating licenses, as well as give rise to termination or cancellation rights under our contracts or disqualify us from future bidding opportunities.

Safety and Risk Management

We are committed to ensuring that our employees perform their work safely and we regularly communicate with our employees to reinforce that commitment and instill safe work habits. We review accidents and claims for our operations, examine trends and implement changes in procedures to address safety issues. Claims arising in our business generally include workers’ compensation claims, various general liability and damage claims, and claims related to vehicle accidents, including personal injury and property damage. We insure against the risk of loss arising from our operations up to certain deductible limits in substantially all of the states in which we operate. In addition, we retain risk of loss, up to certain limits, under our employee group health plan.

We carefully monitor claims and actively participate with our insurers in determining claims estimates and adjustments. The estimated costs of claims are accrued as liabilities, including estimates for claims incurred but not reported. Due to fluctuations in our loss experience from year to year, insurance accruals have varied and can affect the consistency of operating margins. If we experience insurance claims in excess of our umbrella coverage limit, our business could be materially and adversely affected.

Seasonality

Our revenues are affected by seasonality as a significant portion of the work we perform is outdoors. Consequently, our operations are impacted by extended periods of inclement weather. Generally, inclement weather is more likely to occur during the winter season, which falls during our first and fourth fiscal quarters. Also, a disproportionate percentage of total paid holidays fall within our fourth quarter, which decreases the number of available workdays. Additionally, our customer premise equipment installation activities for cable providers historically decrease around calendar year-end holidays as their customers generally require less activity during this period. As a result, we may experience reduced revenue in the first or fourth quarters of our fiscal years.

Environmental Matters

A significant portion of our work is performed underground. As a result, we are potentially subject to material liabilities related to encountering underground objects which may cause the release of hazardous materials or substances. Additionally, the environmental laws and regulations which relate to our business include those regarding the removal and remediation of hazardous substances and waste. These laws and regulations can impose significant fines and criminal sanctions for violations. Costs associated with the discharge of hazardous materials or substances may include clean-up costs and related damages or liabilities. These costs could be significant and could adversely affect our results of operations and cash flows.

STAFFING INDUSTRY

Effective May 8, 2014, we began operations for a temporary and permanent staffing agency providing full service human capital solutions specializing in telecommunications, construction, engineering and technology through our wholly owned subsidiary, FVP Worx. On December 31, 2016, a strategic decision was made to continue operating the staffing segment but at a reduced scale of operations in order to fully deploy our management’s focus and working capital to our higher margin business in the OSP and ISP segments.

Segment Reporting

We operate in the telecommunications infrastructure services industry and, effective May 8, 2014, entered the staffing industry. For the year ended December 31, 2016, our staffing business generated $108,057 in revenues and $126,087 in expenses. For reporting purposes, the Company will continue to report the staff business as a separate segment from the telecommunications services business. We reported segment results pursuant to ASC 280-10 “Segment Reporting” for the year ended December 31, 2016, transitional three months ended December 31, 2015, and the year ended September 30, 2015.

EMPLOYEES

As of May 1, 2017, we, together with our subsidiaries, employ 136 full-time employees and 1 part-time employee. None of our employees are represented by local collective bargaining units. The number of our employees varies according to the level of our work in progress. We maintain a nucleus of technical and managerial personnel to supervise all projects and add employees as needed to complete specific projects.

ACQUISITION STRATEGY

With respect to our acquisition strategy, FTE intends to pursue a clearly defined telecommunications niche, but may, in its discretion, pursue acquisitions outside of this niche, although this will not be our focus. We selectively pursue acquisitions when we believe doing so is operationally and financially beneficial to our existing operations, although we do not rely solely on acquisitions for growth. In particular, we may pursue those acquisitions that we believe will provide us with incremental revenue and geographic diversification while complementing our existing operations. We generally target companies for acquisition that have defensible leadership positions in their market niches, are EBITDA positive, which meet or exceed industry averages, and have proven operating histories, sound management, and certain clearly identifiable cost synergies. On October 28, 2016, the Company signed a non-binding letter of intent (the “LOI”) with Benchmark Builders, Inc. (“Benchmark”) which summarized the principal terms of a possible acquisition of Benchmark, a privately held corporation. On March 9, 2017, the Company, entered into a Stock Purchase Agreement (the “Purchase Agreement”) with (i) Benchmark, and (ii) each of Benchmark’s stockholders. On April 20, 2017, the Company closed on the Purchase Agreement, acquiring 100% of the outstanding shares of Benchmark stock. On April 20, 2017, in conjunction with the acquisition of Benchmark Builders Inc, Lateral amended the original credit agreement to provide for approximately $10.1 million towards the cash purchase price of the Benchmark acquisition, refinancing this new advance with the existing debt, extending the maturity date of the facility to March 31, 2019. See Item 8.

| 11 |

As a “smaller reporting company” as defined by Item 10 of Regulation S-K, we are not required to provide information required by this Item

ITEM 1B. Unresolved Staff Comments.

None.

| 12 |

On December 1, 2015, our executive offices were relocated to 999 Vanderbilt Beach Road, Suite 601, Naples, Florida, 34108 and our telephone number is (877) 878-8136. The old Naples, FL office lease expired on October 31, 2015. Our current lease expires November 30, 2022 and the square footage increase from 3,310 square feet to 5,377 square feet. Our subsidiaries lease five additional office/warehouse facilities throughout the United States, which is summarized below.

| Location: | Usage | Square Footage | Lease Start Date | Lease End Date | Monthly Obligation | |||||||||||

| Naples, FL | Office | 5,377 | 11/01/2015 | 11/30/2022 | $ | 19,034 | ||||||||||

| Indianapolis, IN | Office | 4,000 | 01/01/2016 | 12/31/2018 | $ | 2,700 | ||||||||||

| Dallas, TX | Office | 3,000 | 12/01/2016 | 11/30/2019 | $ | 4,000 | ||||||||||

| Des Moines, IA | Office | 5,000 | 03/01/2016 | 02/28/2018 | $ | 2.000 | ||||||||||

| Naples, FL | Warehouse | 4,500 | 11/01/2015 | 10/31/2018 | $ | 4,770 | ||||||||||

| Dallas, TX | Office | 8,640 | 5/1/2016 | 4/30/2019 | $ | 4,500 | ||||||||||

We are involved in litigation claims arising in the ordinary course of business from time to time, and as of December 31, 2016 we have no material litigation matters. See Footnote 10 Commitment and Contingencies, Accrued Litigation Expense.

ITEM 4. Mine Safety Disclosures.

None.

| 13 |

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our shares were quoted on the OTC Pink Sheets, under the symbol “BEAC” through March 17, 2014 and under the symbol “FTNW” thereafter, until August 20, 2014, when the U.S. Securities and Exchange Commission (the “SEC”) suspended trading of our securities, because we failed to comply with certain reporting requirements outlined in the Securities Exchange Act of 1934. Subsequently, the SEC issued an Order that the registration of each class of the Company’s securities registered pursuant to Exchange Act Section 12 be revoked pursuant to Section 12(j) of the Exchange Act, effective September 12, 2014. Subsequent to the foregoing, our common stock was not listed, traded or quoted on any national stock exchange or on the OTC Markets.

On May 16, 2015, our registration statement on Form 10 became effective and on December 10, 2015, our common stock resumed trading on the OTC Pink marketplace. On March 1, 2016, we uplisted to the OTCQB marketplace, and on June 29, 2016, we uplisted to the OTCQX marketplace.

The following table sets for the range of high and low bid information for our common stock for the periods indicated. Such over-the-counter market quotations reflect inter-dealer prices without retail mark-up, mark-down or commissions and may not necessarily represent actual transactions. Note that our common stock did not trade during fiscal 2015.

| Price Range | ||||||||

| Low | High | |||||||

| Year ended September 30, 2015 | ||||||||

| First quarter (October 1, 2014 to December 31, 2014) | $ | N.A | $ | N.A | ||||

| Second quarter (January 1, 2015, to March 31, 2015) | $ | N.A | $ | N.A | ||||

| Third quarter (April 1, 2015 to June 30, 2015) | $ | N.A | $ | N.A | ||||

| Fourth quarter (July 1, 2015 to September 30, 2015) | $ | N.A | $ | N.A | ||||

| For the transitional three months Ended December 31, 2015 | ||||||||

| Fourth Quarter (October 1, 2015 to December 31, 2015) | $ | 0.20 | 1 | $ | 2.00 | 1 | ||

| Year ended December 31, 2016 | ||||||||

| First quarter (January 1 to March 31, 2016) | $ | 0.40 | 1 | $ | 1.59 | 1 | ||

| Second quarter (April 1 to June 30, 2016) | $ | 0.62 | 1 | $ | 0.88 | |||

| Third quarter (July 1 to September 30, 2016) | $ | 0.40 | $ | 0.84 | ||||

| Fourth quarter (October 1 to December 31, 2016) | $ | 0.32 | $ | 0.58 | ||||

1 Price adjust to reflect 1:20 reverse split of common shares effective May 26, 2016.

Stockholders

There were 440 holders of record of our common stock as of May 11, 2017.

Dividends

We have not declared or paid any dividends on our common stock and do not anticipate paying cash dividends in the foreseeable future. We plan to retain any future earnings for use in our business operations. Any decisions as to future payments of cash dividends will depend on our earnings and financial position and such other factors as the Board deems relevant.

| 14 |

Recent Sales of Unregistered Securities

During the transitional three month period ended December 31, 2015, the Company issued the following:

On October 2, 2015, the Company received $145,000 from its investor from the stock subscription receivable.

On November 2, 2015, the Company issued 163,441 shares of its Series D preferred stock with a grant date value of $126,840, under the terms of the Company’s new senior credit facility.

On November 2, 2015, the Company issued 391,903 shares of its Series F preferred stock with a grant date value of $310,540, under the terms of the Company’s new senior credit facility.

On November 5, 2015, the Company issued 26,996 shares of its common stock with a grant date value of $139,701 as a settlement with one of the Company’s vendors.

On December 4, 2015, the Company issued 25,641 shares of its common stock with a grant date value of $5,120 as part of a legal settlement agreement.

On December 18, 2015, the Company issued 6,250 shares of its Series F preferred stock with a grant date value of $25,000 in settlement for investor relations services.

On December 21, 2015, the Company issued 519,309 shares of its Series F preferred stock with a grant date value of $342,743 to various employees under the terms of their employment agreements.

During the fiscal year ended December 31, 2016 the Company issued the following:

During the fiscal year ended December 31, 2016, the Company issued 285,664 shares of its Preferred Series F stock with a grant date value of $35,186 to one of its investors as an incentive to continue raising equity proceeds.

During the fiscal year ended December 31, 2016, the Company issued 231,041 shares of its Preferred Series F stock to its independent directors and two officers with a grant date value of $152,487 for compensation.

During the fiscal year ended December 31, 2016 the Company issued 5,029,000 shares of its common stock with a grant date value of $2,569,800 to several employees under the terms of their employment agreements, of which $2,305,040 remains unvested.

During the fiscal year ended December 31, 2016, the Company issued 3,809,389 shares of its common stock to settle debt with a grant date value of $1,798,438.

During the fiscal year ended December 31, 2016, the Company issued 841,500 shares of its common stock with a grant date value of $445,800 to consultants for services performed for the Company.

During the fiscal year ended December 31, 2016, the Company issued 7,594,999 shares of its common stock to individual investors for an equity raise totaling $2,628,000.

The Series D and Series F preferred shares issued as described above were not registered under the Securities Act of 1933, as amended (the “Securities Act”) in reliance upon the exemption from registration provided by Section 4(2) of that Act and Regulation D promulgated thereunder, which exempts transactions by an issuer not involving any public offering. These securities may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements. Certificates representing these securities contain a legend stating the same.

Issuer Purchases of Equity Securities

During the year ended December 31, 2016, there were no purchases of our equity by us or any “affiliated purchaser”.

ITEM 6. Selected Financial Data.

FTE Networks, Inc. is a “smaller reporting company” as defined by Regulation S-K and as such, is not required to provide the information contained in this item pursuant to Regulation S-K.

| 15 |

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Overview

FTE Networks, Inc. (FTNW), and its wholly owned subsidiaries, is a leading international networking infrastructure service solutions company. The Company designs, build, and support telecommunications and technology systems and infrastructure services for Fortune 500 companies operating telecommunications services in Data Center Infrastructure, Fiber Optics, Wireless Integration, and Surveillance & Security. FTE Networks is headquartered in Naples, Florida, with offices throughout the United States and Europe.

● Jus-Com, Inc., (dba FTE Network Services) specializes in the design, engineering, installation, and maintenance of all forms of telecommunications infrastructure. Services include engineering consulting, design, installation, maintenance, and emergency response in various categories including cabling, equipment installation and configuration, rack and stack, wiring build-outs, infrastructure build-outs, DC power installation, OSP/ISP fiber placement, fiber cable splicing and testing.

● FTE Wireless, LLC, offers wireless solutions to major wireless carriers including equipment installation, fiber backhaul, antennae installation and testing, small cell solutions, fiber-to-site and other turnkey solutions as needed by such clients.

● Focus Venture Partners, Inc. (dba FVP Worx) is a multifaceted employment firm offering full service staffing solutions, specializing in the telecommunications, technology and construction services industries.

FTE Network Services and FTE Wireless Service, LLC are reported in the Company’s telecommunications segment. FVP Worx represents the Company’s staffing segment.

Recent Business Developments

On November 3, 2015, the Company entered into a credit agreement, dated October 28, 2015 (the “Agreement”), pursuant to which the Company received $8 million in term loans from Lateral Investment Management (“Lateral”). A portion of the proceeds was used to extinguish an aggregate principal amount of approximately $3.4 million of Senior Secured Promissory Notes, pursuant to a tender offer. The noteholders who tendered their notes received the tender offer consideration of $0.50 per $1 principal amount of the Notes from the proceeds from the term loan, and all interest payable on the notes was forgiven. The Company expects to recognize approximately a $3.4 million gain related to the extinguishment of the Senior Secured Promissory Notes. In connection with the agreement, the Company issued 555,344 shares of preferred stock to Lateral, 163,441 designated as Series D preferred stock and 391,903 designated as Series F preferred stock. Upon the approval of the reverse split of common stock May 26, 2016, these preferred shares mandatorily converted to 11,106,880 shares of common stock, based upon their 1 for 20 conversion rate. The Company and Lateral also entered into a Registration Rights agreement in connection with the issuance of these shares, pursuant to which the Company must file a registration statement with the SEC, with respect to the shares. Lateral may request redemption of some or all of its shares any time after October 28, 2017, subject to the Company (a) meeting certain minimum capitalization and EBITDA requirements; and (b) being able to continue as a going concern on a post-redemption basis. The redemption price per share is variable and equals 10 (ten) times the last twelve months EBITDA, multiplied by the Lateral fully-diluted ownership percentage and then divided by the Lateral shares outstanding. In addition, Lateral was granted anti-dilution rights which permit it to receive additional equity securities to maintain its fully-diluted ownership interest to the extent that the Company issues equity securities to third parties, up to a maximum of $5,000,000. On April 5, 2016, the Company entered into an amendment agreement to its existing credit facility with Lateral, amending the original credit agreement signed October 28, 2015. The agreement amends select provisions of the original credit agreement, including equity raises and changes to certain financial and operational covenants. On September 30, 2016, the Company entered into a second amendment agreement to its existing credit facility, maturing October 28, 2017, amending the original credit agreement signed October 28, 2015. The agreement was amended solely to consolidate a series of short term bridge loans granted to the company from time to time during the second and third quarter of 2016 into a $2.5 million loan, which matures on April 30, 2017. The second amendment also amended the covenants related to consolidated EBITDA, consolidated leverage, consolidated debt service, selling, general, and administrative expenses, and compensation expense. On April 20, 2017, in conjunction with the acquisition of Benchmark Builders Inc, Lateral amended the original credit agreement to provide for approximately $10.1 million towards the cash purchase price of the Benchmark acquisition, refinancing this new advance with the existing debt, extending the maturity date of the facility to March 31, 2019.

On December 23, 2015, the Board unanimously authorized and approved an amendment to our Articles of Incorporation to effect a reverse stock split of our Common Stock at a 1-for-20 ratio (the “Reverse Split”). On December 30, 2015, stockholders holding a majority of our voting power approved by written consent the amendment to our Articles of Incorporation, which would affect the Reverse Split. The Reverse Split will reduce the number of outstanding shares of our Common Stock by reclassifying and converting all outstanding shares of our Common Stock into a proportionately fewer number of shares of Common Stock. On March 9, 2016, the Company filed a Form Pre-14C with the SEC concerning the 1 for 20 reverse stock split and the increase of the authorized shares of common stock from 70,000,000 to 200,000,000. On April 18, 2016, the Company filed its Definitive Form 14-C with the SEC. On May 25, 2016 “FINRA” approved the Reverse Split, which was effectuated on May 26, 2016. All share and share information in this transitional report has been retroactively restated for the reverse split.

Effective January 27, 2016, the Company changed its fiscal year end from September 30 to December 31 and filed an unaudited transitional report on Form 10-QT to cover the period from October 1, 2015 to December 31, 2015 with the Securities and Exchange Commission on April 11, 2016. This current annual report as of December 31, 2016 includes the audited three month transitional period ended December 31, 2015.

| 16 |

On October 28, 2016, the Company signed a non-binding letter of intent (the “LOI”) with Benchmark Builders, Inc. (“Benchmark”) which summarized the principal terms of a possible acquisition of Benchmark, a privately held corporation. On March 9, 2017, the Company, entered into a Stock Purchase Agreement (the “Purchase Agreement”) with (i) Benchmark, and (ii) each of Benchmark’s stockholders. On April 20, 2017 (the “Closing Date”), FTE Networks, Inc. (“FTE Networks”) acquired all of the issued and outstanding shares of common stock (the “Benchmark Shares”) of Benchmark Builders, Inc., a privately held New York corporation (“Benchmark”) from each of its stockholders (collectively, the “Sellers”), pursuant to the Stock Purchase Agreement, dated as of March 9, 2017, by and among FTE Networks, Benchmark, and the Sellers (the “Purchase Agreement”), as amended by Amendment No. 1 to Stock Purchase Agreement, dated as of the Closing Date (the “Purchase Agreement Amendment” and together with the Purchase Agreement, the “Amended Purchase Agreement”). FTE Networks, Benchmark, and the Sellers, entered into the Purchase Agreement Amendment in order to address certain changes in the purchase price as set forth in the Purchase Agreement. As described in FTE Networks’ Current Report on Form 8-K filed with filed with the Securities and Exchange Commission (the “SEC”) on March 9, 2017, the Purchase Agreement provided that the consideration to the Sellers for the Benchmark Shares would consist of (i) $55,000,000 in cash consideration, (ii) an aggregate of 17,825,350 shares of the Company’s common stock, and (iii) promissory notes in the aggregate amount of $10,000,000 to the Sellers. The Purchase Agreement Amendment has, inter alia, modified the purchase price set forth in the Purchase Agreement to consist of (i) cash consideration of approximately $17,250,000, subject to certain prospective working capital adjustments (the “Cash Consideration”), approximately $10 million cash provided by Lateral and $7 million provided by certain of the sellers, (ii) 26,738,445 shares of FTE Networks’ common stock (the “FTE Shares”), (iii) convertible promissory notes in the aggregate principal amount of $12,500,000 to certain stockholders of Benchmark (the “Series A Notes”, which mature on April 20, 2019), (iv) promissory notes in the aggregate principal amount of $30,000,000 to certain stockholders of Benchmark (the “Series B Notes”, which mature on April 20, 2020) and (v) promissory notes in the aggregate principal amount of $7,500,000 to certain stockholders of Benchmark (the “Series C Notes”, which mature on October 20, 2018, and together with the Series A Notes and the Series B Notes, the “Notes”) in the Amended Purchase Agreement. Additionally, Lateral amended its existing credit facility to provide for the approximate $10 million cash and to restructure the existing debt, which now has a maturity date of March 30, 2019. The $75 million acquisition will enable FTE to deliver integrated network services, cutting-edge technology, and construction management services on the largest and most complex projects, from conception to completion. Benchmark intends to immediately begin to aggressively roll-out FTE’s “compute to the edge” technology in New York City and the surrounding region. This leading edge technology, called CrossLayer, allows building owners to provide exceptional broadband access at significant savings to both landlords and tenants, while creating revenue generating opportunities for landlords and recurring revenue platforms for FTE. The transaction will allow FTE and Benchmark to begin offering services to each other’s clients and expanding their offerings nationally.

| 17 |

Critical Accounting Policies

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires us to make estimates and judgments that affect the reported amounts of assets and liabilities, revenues and expenses, and related disclosures of contingent assets and liabilities. These estimates and judgments are based on historical information, information that is currently available to us and on various other assumptions that we believe to be reasonable under the circumstances. Actual results could differ from those estimates. Our most significant estimates relate to our allowances for receivables and deferred tax assets, plus the valuation of equity issuances.

Revenue and Cost of Goods Sold Recognition

Generally, including the staffing business, revenue is recognized when all of the following criteria are met: (1) persuasive evidence of an arrangement exists, (2) delivery has occurred or services have been rendered, (3) the price to the buyer is fixed or determinable, and (4) collectability is reasonably assured.

Due to the short-term nature of our construction contracts, revenue is recognized once 100% of a contract segment is completed. A contract may have many segments, of which, once a segment is completed; the revenue for the segment is recognized and no further obligation exists. The Network’s construction contracts or segments of contracts typically can range from several days to two to four months. Contract costs may be billed as incurred. Contract costs include all direct material and labor costs and those indirect costs related to contract performance, such as indirect labor, supplies, tools and repairs. Selling, general and administrative costs are charged to expense as incurred. We begin recognizing revenue on a project as project costs are incurred and revenue recognition criteria are met.

Provisions for losses on uncompleted contracts are made in the period such losses are known. Changes in job performance, job conditions and estimated profitability, including those arising from contract penalty provisions, changes in raw materials costs, and final contract settlements may result in revisions to revenue, costs and income and are recognized in the period in which the revisions are determined.

Valuation of Long-lived Assets

We evaluate our long-lived assets for impairment in accordance with related accounting standards. Assets to be held and used (including projects under development as well as property and equipment), are reviewed for impairment whenever indicators of impairment exist. If an indicator of impairment exists, we first group our assets with other assets and liabilities at the lowest level for which identifiable cash flows are largely independent of the cash flows of other assets and liabilities (the “asset group”). Secondly, we estimate the undiscounted future cash flows that are directly associated with and expected to arise from the completion, use and eventual disposition of such asset group. We estimate the undiscounted cash flows over the remaining useful life of the primary asset within the asset group. If the undiscounted cash flows exceed the carrying value, no impairment is indicated. If the undiscounted cash flows do not exceed the carrying value, then an impairment is measured based on fair value compared to carrying value, with fair value typically based on a discounted cash flow model. If an asset is still under development, future cash flows include remaining construction costs. There were no impairments during the periods presented.

Income Taxes