40Use these links to rapidly review the document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the fiscal year ended December 31 , 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

Commission File Number 001-33133

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) | (Zip Code) | |||||||

(Registrant's telephone number, including area code): (617 ) 583-1700

______________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

The | ||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ý

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on the Nasdaq Capital Market on June 30, 2023 was $9,843,350 .

The number of shares outstanding of the registrant's common stock as of March 28, 2024 was 15,401,706 .

DOCUMENTS INCORPORATED BY REFERENCE

Pursuant to General Instruction G to Form 10-K, the information required by Part III, Items 10, 11, 12, 13 and 14 is incorporated herein by reference from the Company's proxy statement for the Annual Meeting of Stockholders to be held on June 20, 2024, which is expected to be filed not later than 120 days after the fiscal year end covered by this Form 10-K.

YIELD10 BIOSCIENCE, INC.

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2023

INDEX

| Page | ||||||||

3

Forward-Looking Statements

This Annual Report on Form 10-K contains "forward-looking statements" within the meaning of 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). These statements relate to our future plans, objectives, expectations and intentions and may be identified by words such as "may," "will," "should," "expects," "plans," "anticipate," "intends," "target," "projects," "contemplates," "believe," "estimates," "predicts," "potential," and "continue," or similar words.

Although we believe that our expectations are based on reasonable assumptions within the limits of our knowledge of our business and operations, the forward-looking statements contained in this document are neither promises nor guarantees. Our business is subject to significant risks and uncertainties and there can be no assurance that our actual results will not differ materially from our expectations. These forward-looking statements include, but are not limited to, statements concerning our business plans and strategies; expected future financial results and cash requirements; plans for obtaining additional funding; plans and expectations that depend on our ability to continue as a going concern; and plans for development and commercialization of our crop yield traits, technologies and intellectual property. Such forward-looking statements are subject to a number of risks and uncertainties that could cause actual results to differ materially from those anticipated including, without limitation, risks related to our limited cash resources, uncertainty about our ability to secure additional funding, risks related to the execution of our business plans and strategies, risks associated with the protection and enforcement of our intellectual property rights, as well as other risks and uncertainties set forth below under the caption "Risk Factors" in Part I, Item 1A, of this report.

The forward-looking statements and risk factors presented in this document are made only as of the date hereof and we do not intend to update any of these risk factors or to publicly announce the results of any revisions to any of our forward-looking statements other than as required under the federal securities laws.

Unless the context otherwise requires, all references in this Annual Report on Form 10-K to "Yield10 Bioscience," "Yield10," "we," "our," "us," "our company" or "the company" refer to Yield10 Bioscience, Inc., a Delaware corporation and its subsidiaries.

PART I

(With the exception of stock prices and earnings per share disclosures, all dollar amounts throughout this report are shown in thousands unless otherwise indicated.)

ITEM 1. BUSINESS

Overview

Yield10 Bioscience, Inc. ("Yield10" or the "Company") is an agricultural bioscience company focused on commercializing sustainable products using the oilseed Camelina sativa ("Camelina") as a platform crop.

We are pursuing Camelina seed oil products for two market opportunities and value chains. Each product has its own set of scale requirements, value proposition and challenges. The first product, is seed oil produced by Camelina which has been genetically engineered to enable production of high levels of the omega-3 fatty acids eicosapentanoic acid (EPA) and docosahexanoic acid (DHA). Our development is driven by the growing demand for new sources of omega-3 ingredients and the production constraints and supply volatility of the traditional raw material source fish oil. This growing omega-3 supply gap offers a market opportunity with the potential for revenue and margin growth at acreage levels operationally accessible to Yield10. When commercially available, the Company's omega-3 products will address an unmet need for a reliable, scalable supply of EPA and DHA omega-3 ingredients for aquaculture and pet/animal feed. Multiple opportunities exist for further product development to address higher value markets for omega-3 oils in nutraceuticals and pharmaceuticals. Earlier this year we received regulatory approval from USDA-APHIS for two engineered Camelina lines, the first produces our EPA Omega-3 product and the second produces our EPA+DHA Omega-3 product.

The second product is Camelina seed oil for use as a low-carbon intensity feedstock oil for biofuels, including biodiesel, renewable diesel (“RD”) and sustainable aviation fuel (“SAF”). Markets for biofuels are driven by government policies, have the potential to be very large, and will require the production of tens of millions of acres of new oilseed cover crops like Camelina that do not compete for land with food production.

4

In early 2024, we adjusted our commercial strategy for biofuels to focus on providing research and development services to third parties interested in Camelina for biofuels with the goal of generating service and licensing revenues from our advanced Camelina technology capabilities, varieties and traits. This decision reflects the current excess supply of soybean oil for the biofuels market as well as the challenges the Company faced in the current financing environment as a small cap pre-revenue company. Over the past four years, Yield10 has developed proprietary, engineered spring and winter Camelina varieties, including herbicide tolerant (“HT”) and stacked herbicide tolerant (“stacked HT”) traits which form the genetic foundation for introducing commercial-quality Camelina varieties tailored to address our target markets. Based on this biofuels strategy, we recently signed our first non-exclusive global, commercial license with Vision Bioenergy Oilseeds for certain Camelina lines and herbicide tolerance traits. Going forward, we plan to continue executing partnerships and other types of agreements for the development of Camelina technologies used in the production of biofuels. Yield10 is headquartered in Woburn, Massachusetts and has a Canadian subsidiary, Yield10 Oilseeds Inc., located in Saskatoon, Saskatchewan, Canada.

We selected Camelina, an annual oilseed plant in the mustard family, as our platform crop based on its unique attributes, including its excellent agronomic traits, such as low water and fertilizer input, drought resistance and its short growing cycle. Based on Camelina's flexible agronomic profile, we believe growers have the option of using Camelina as a winter cover crop, as a relay crop with soybean in the U.S. Midwest, and as a spring rotation crop within the U.S. and regions of Canada. Meeting the growing demand for biofuel feedstocks in North America will require tens of millions of acres of new non-food oilseed production. Given today's crop production practices, the best way to access this acreage scale is through double cropping using short season winter oilseeds as cash cover crops integrated into crop rotations in a second growing season with the major food crops corn and soybean. Winter cover crops reduce soil erosion and nutrient runoff, promote soil health and trap subsoil moisture. Camelina is in the same plant family as canola and naturally produces a relatively abundant harvest of oil-containing protein-rich seeds. Camelina has no close plant relatives in North America and as a new non-food crop it is readily segregated from commodity crops making it advantaged for producing novel seed products. This dramatically simplifies the regulatory path for engineered products in North America. Planting, harvesting, storage and transportation of Camelina does not require growers to make capital investments in new equipment. The grain can be processed in soft seed (e.g. canola) crushing facilities, using either cold press or solvent extraction and the residual protein meal can be used in certain animal feed rations in the U.S. and Canada once regulatory approval has been obtained. To unlock this potential and make Camelina an attractive option for farmers, we are developing and plan to commercialize advanced varieties with elite weed control herbicide tolerance traits, improved agronomic performance, and increased crop value.

We learned through our interactions with growers that developing elite weed control technology for Camelina to enable seamless integration into current crop rotations is a critical factor in achieving large-scale adoption of Camelina as a new crop. As a result, we prioritized the development of herbicide tolerant Camelina over the past four years. We have successfully developed commercial-quality Camelina varieties containing an HT trait for glufosinate tolerance alone or as a stacked HT trait for glufosinate tolerance in combination with tolerance to Group 2 herbicides, specifically including tolerance to both imidazolinones (“IMI”) and sulfonylureas (“SU”). The prevalence and persistence of Group 2 soil residues in some production regions limit the amount of land available for planting conventional Camelina. In November of 2023, our HT and stacked HT technologies received regulatory approval from USDA-APHIS indicating that the agency does not consider our Camelina varieties with these traits to be regulated in the United States. In early 2024, over 50 acres of our spring E3902 HT Camelina was harvested from a contra season seed scale-up conducted in Chile. This accomplishment from first field trials of HT Camelina in the spring of 2022 to regulatory approval in Q4 of 2023 and seed bulk up to tonnage scale in Q1, 2024 reflects Yield10's development strengths. We believe this outcome together with the more recent approvals for our Omega-3 Camelina reflects the favorable regulatory path for engineered Camelina in the U.S. and bodes well for the accelerated development of this crop using Yield10s advanced technology, gene traits and capabilities. We plan to continue our development work with spring E3902 stack HT Camelina and winter stack HT Camelina during early 2024, in order to continue our assessment of the efficacy of the traits in-field agronomics, seed yields and oil content. In February of 2024 we signed a non-exclusive commercial license for the HT and stacked HT traits with Vision Bioenergy Oilseeds (“Vision”) to enable Vision to begin scaling up Camelina production for the biofuel market.

In October of 2023, we executed our option with The Rothamsted Institute ("Rothamsted") to acquire an exclusive, global commercial license to advanced Omega-3 Camelina technology. We expect to secure this license in the second quarter of 2024. As a result of industry interest in new sources of omega-3, in October of 2023 we signed a Letter of Intent (“LOI”) with BioMar Group, an industry leader in the production of aquafeed for salmon farming, with the intent of forming a collaboration to commercially produce the oil from Omega-3 Camelina to supply this market. The omega-3 fatty acids EPA and DHA are essential for human health and wellness, and the primary dietary source of these nutrients is ocean

5

harvested fish oil. For clarity, we are using “fish oil” to include oil containing EPA and DHA omega-3 fatty acids extracted from ocean harvested fish and Krill. A third omega-3 fatty acid, alpha-linoleic acid (ALA), is also considered essential for human health and wellness. ALA is readily available from vegetable oils, including canola, soybean, flaxseed and Camelina however, plants on the other hand do not make EPA or DHA. Fish oil containing EPA and DHA purified from harvested fish, such as anchovies, is an important ingredient in the production of feed used in salmon aquafarming. Salmon is a preferred high quality protein source in the human diet and today over 85% of the salmon consumed globally is produced through aquafarming. EPA and DHA are essential feed components for farmed salmon to protect fish health during production and to provide market differentiation of the product as healthier protein source based on its omega-3 content. The growing market for farmed salmon and expanded use of omega-3 fatty acids in human nutrition, nutraceutical, pet food and other markets has placed additional pressure on harvested fish as a source of fish oil. Significant disruptions to omega-3 oil supply occurred in 2023 causing sharp increases in fish oil prices. Industry sources project a deficit in omega-3 supply to meet growing demand of over 500,000 tons per year by 2030.

Under our collaboration, Rothamsted provided us with both the two Omega-3 Camelina varieties that produce seed oil with 16-20% EPA or seed oil with 10% EPA and 10% DHA content. In 2023, the Company filed requests for Regulatory Status Review (“RSRs”) with USDA-APHIS for both Camelina varieties and both of these were approved in March 2024. In 2023, we planted EPA8 Omega-3 Camelina on 50 acres in contra season in Chile. This EPA8 Omega-3 Camelina was harvested in the first quarter of 2024. Going forward in 2024, we plan to continue executing further seed scale-up of EPA8 Omega-3 Camelina to enable production of the first commercial omega-3 product for use in aquafeed. The Company also expects to begin scaling up DHA1 Omega-3 Camelina in Chile during the fourth quarter of 2024.

We plan to bring both Omega-3 Camelina products forward in development with 2026 being the target for the first commercial-scale production of the EPA8 oil. Herbicide tolerance is critical in Camelina for on-farm performance. We are currently breeding HT traits into both current Omega-3 Camelina varieties to create second generation varieties for large acreage production. As a world leader in Camelina seed genetics and advanced trait technology development, Yield10 shares a common goal with the aquaculture industry including feed and salmon producers to establish the commercial production of thousands of tons of Camelina omega-3 oil as a new scalable, cost effective, and sustainable supplement to fish oil. We believe Camelina omega-3 oil production at scale (50,000 tons per year, based on approximately 200,000 acres) can reduce supply and price volatility in aquafeed and farmed salmon production leading to a potential increase the growth rate of the industry.

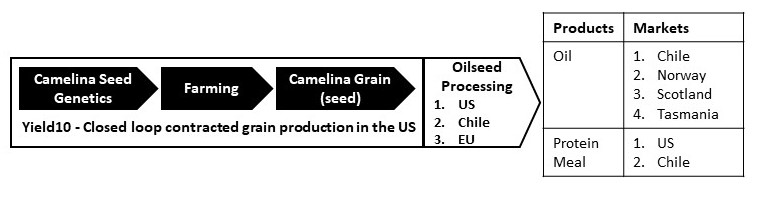

Over the course of 2022 and 2023, we gained valuable experience in establishing a closed loop value chain, the model we plan to use for the omega-3 business. We engaged growers in contracts to produce Camelina grain (for processing) and Camelina seed (for future planting) having a total acreage of approximately 1,000 acres for each of the winter and spring growing seasons. We also contracted with growers in the U.S., Canada and Chile to grow our E3902 (spring, high oil yield), WDH2 (winter, increased cold tolerance) and WDH3 (winter, early flowering) and other Camelina plant varieties to produce commercial planting seed. This activity is expected to be an essential part of our business model to produce commercial seed inventory for future grower contracts. During the second half of 2023, we took first-time deliveries of harvested Camelina grain produced under our winter and spring season grower contracts in Western Canada and the United States. Although small in scale, these initial growing seasons represented a proof-of-concept for our Camelina to be used in the commercial biofuel feedstock market.

We are building an intellectual property portfolio around our crop technologies and traits. As of December 31, 2023, Yield10 owns or holds exclusive rights to 18 patent families, including 20 issued patents and 30 pending patent applications. In October of 2023, Yield10 exercised its exclusive option to an exclusive global license to two active patent families of Rothamsted Research, including six issued patents and six pending applications which cover the production of our EPA and EPA+DHA products.

Market Opportunities

We believe the market opportunity is significant for omega-3 oil and biofuel feedstock oil produced from our elite Camelina varieties, as well as for our other proprietary seed products in development, including performance traits for use in other crops. We are targeting uses for our Camelina seed products in commercial applications such as: a) omega-3 oils for aquaculture and nutrition based on establishing a closed loop production system, and b) low-carbon feedstock oils for biofuels using an R&D services, partnering and licensing model.

6

Omega-3 (EPA, EPA+DHA) Oils: Long chain omega-3 fatty acids are essential for human nutrition, health and wellness. The three main omega-3 fatty acids are alpha-linolenic acid (“ALA”), eicosapentaenoic acid (“EPA”), and docosahexaenoic acid (“DHA”). EPA and DHA are found primarily in fish and other seafood while ALA is found primarily in plant oils such as flax. Plant oils including canola, soybean, flaxseed and Camelina naturally containing high levels of ALA but plants do not produce EPA or DHA which are found only in marine organisms. The markets and uses for omega-3 fatty acids include aquafeed used for salmon, trout and shrimp feed, pet feed, baby formula, nutraceuticals and pharmaceutical products. Omega-3 fatty acids provide many health benefits, including preventing and managing heart disease. The American Heart Association recommends that everyone eat fish at least twice a week, such as salmon that is high in omega-3 acids, and/or adding fish oils supplements to their diets. In addition, DHA is used as an essential ingredient in baby formula because of its importance in early cognitive development.

The global availability of ocean wild caught fish and krill containing omega-3 oil used in nutritional oils and aquafarming is declining due to overfishing. The primary dietary source of EPA and DHA is the consumption of oily fish or fish oil. Approximately 10% of all fish harvested from the ocean is used to produce fish meal and fish oil with the latter valued primarily as a source of omega-3. Global fish oil production has remained flat at approximately 1 million tons per annum over the last decade. In 2023, there was a significant drop in production of nearly 20% due to the cancellation of the Peru anchovy harvest. Fish oil contains different levels of the omega-3 fatty acids depending on the type of fish and location of the fish harvest. The oil extracted from recent annual anchovy harvests in Peru historically provided almost 20% of global fish oil production and had high levels of EPA (≈ 17%) and DHA (≈ 12%). The higher levels of EPA and DHA in anchovy oil make it a preferred feedstock for producing omega-3 concentrates and derivatives for direct human consumption. Northern hemisphere fish oil contains approximately 12% EPA and 10% DHA. Our vegan EPA and EPA+DHA products produced by Camelina will be attractive clean ingredients for their target markets, free of ocean pollutants including the heavy metals, lead, cadmium and mercury as well as the persistent organic pollutants increasingly prevalent in the oceans. We believe our Camelina oils will provide safety advantages to manufacturers of omega-3 pharmaceuticals and nutraceuticals and these same benefits will also accrue to farmed salmon and other species.

Figure 1. Camelina Omega-3 Oil Production Value Chain

Source: Yield10 Bioscience

The Omega-3 Deficit: Based on a recent analyst report on Nuseed from UBS and our discussions with prospective customers and partners interested in new sources of EPA and DHA, there is a growing disconnect between the constrained supply from ocean harvested fish and krill with demand growing steadily at around 3% per year for aquafeed and 7-8% for other applications mainly human nutrition. This omega-3 deficit is estimated to increase to around 300,000 -600,000 tons of fish oil equivalent per year.

Fish oil for aquafeed is used primarily to supply three main markets, Chile, Norway and Scotland, as shown in Figure 1. The aquaculture product sector will play a major role in meeting the growing global demand for fish, an important high value protein source in human diets. Sustainable land-based sources of key feed ingredients will need to be developed and adopted to support this demand. This includes high value specialty ingredients, and in particular, new sources of EPA and DHA to replace oil from stagnating supplies of ocean-harvested fish used in feed production. Fish oil supplied from ocean-harvested fish is particularly important for farmed salmon. The Atlantic Salmon aquaculture sector is expected to grow at 4% CAGR through 2026, reaching an annual harvest of over 3 million tonnes. The growth of the salmon farming sector along with increasing additional demand from new nutraceutical product markets for direct human consumption are expected to exceed the world's sustainable supply. In 2021, 4.7 million metric tonnes of fish feed was used globally for salmon aquafarming. Although it can vary, fish oil represented up to 10% of fish feed by weight and is the most expensive ingredient. We estimate that there is approximately 500,000 tons of fish oil consumed annually in salmon feed production.

7

Global fish oil production has been relatively flat over the last 10 years and some industry experts predict the demand for omega-3 will increase by more than 7% per year over the next 5 years. The demand from salmon farming alone is expected to grow by approximately 4% per year, according to the 2022 Salmon Farming Industry Handbook. The entire aquaculture industry rests on a shaky sustainability platform as wild caught fish are ground to produce for feed, including omega-3 and fish meal protein. We believe our Camelina omega-3 oils will enable this entire industry to attain a truly sustainable foundation.

Fish oil is also a key raw material source for producing refined and concentrated omega-3 oils and purified omega-3 fatty acid derivative compounds for use in the growing human nutrition, nutraceutical and pharmaceutical markets. One such derivative is ethyl-EPA. There are currently about 20 commercial producers of ethyl-EPA. Currently produced from fish oil, we estimate that ethyl-EPA production is in the range of 10,000 – 14,000 tons per year with a reported market value of approximately $1.6 billion which is predicted to grow to $3.4 billion by 2030. We believe that the EPA oil from our first and second generation EPA8 Omega-3 Camelina may be an advantaged feedstock for this market given the high EPA content and the absence of DHA in those oils.

High Protein Meal: There is a growing global demand for additional protein sources for animal feed and food applications. Camelina seed can be processed using existing oilseed processing facilities to extract the oil, and the residual meal that remains is a high-quality protein. On a dry basis, the meal contains approximately 42% protein with a good amino acid profile for animal feed applications. Camelina meal has been approved for use in some animal feed applications, and we expect that with accelerated breeding using genome editing, the meal quality can be further enhanced to improve its feed value and expand this application.

Incentives to Reduce Carbon Emissions: The global macro driver to reduce greenhouse gas emissions encompasses not only liquid transportation fuels but includes reducing CO2 production from agricultural and aquaculture farming practices. In the case of liquid transportation fuels this has resulted in targeted government policies.

When renewable diesel or sustainable aviation fuel produced primarily from used cooking oil and vegetable oil is used instead of traditional petroleum diesel, it helps reduce carbon emissions. Camelina oil has a particular advantage because of its low carbon footprint. Currently, there are existing regulatory incentives from regional greenhouse gas reduction mandates established for fuel producers. This includes California's Low Carbon Fuel Standards market, which measures the specific carbon index, or CI, of every type of fuel, assigns a credit/deficit for every gallon of fuel produced based on its CI, and requires all fuel producers selling into California to purchase enough credits to keep their portfolio CI score below an established baseline. Biofuel manufacturers are highly motivated to utilize compatible feedstocks with a low-carbon footprint in order to meet the regulatory standards to lower carbon emissions. As a benchmark, petroleum diesel has a reported CI of 100, soybean oil has a CI of 56, and in the case of Camelina oil, Sustainable Oils, a subsidiary of Global Clean Energy Holdings, Inc., has reported a CI of 23.

Similarly, large food companies are working to reduce their greenhouse gas footprint and promoting regenerative agricultural practices to improve their carbon footprint and overall ESG scores, in part to create marketing advantages with consumers. Vegetable oils produced using winter Camelina cover cropping to produce low CI vegetable oils for human consumption may be an attractive option. Similarly, the salmon farming sector is looking specifically to reduce its carbon footprint and transition to more sustainable practices including reducing the use of ocean harvested fish as sources of protein and omega-3 fatty acids for aquafeed.

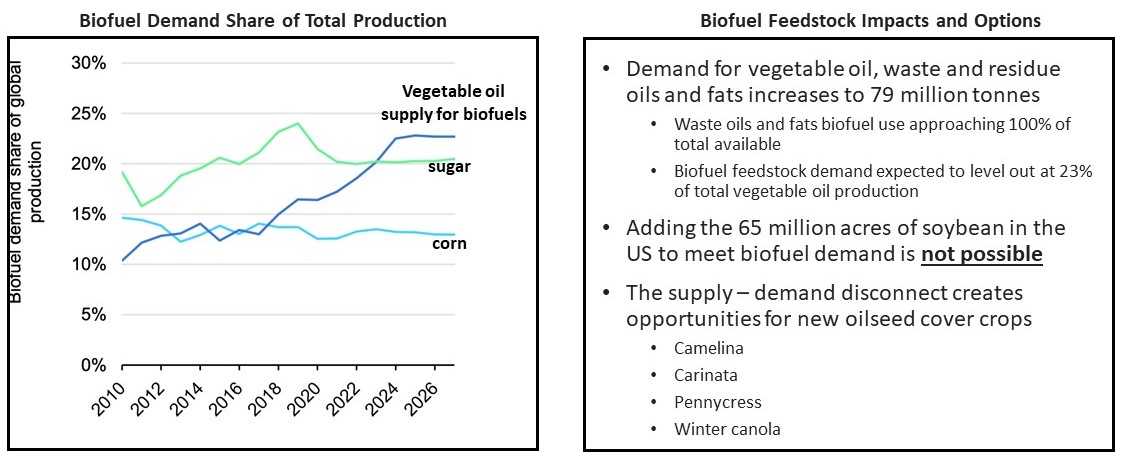

Feedstock Oil for Biofuels: As part of the energy transition, a substantial increase in renewable diesel capacity in the United States and Canada is currently underway, with proposed and funded renewable diesel facilities having a total capacity of over 6 billion gallons of biofuels per year. Initiatives are also underway in the U.S, targeting 35 billion gallons of annual production as well as in the EU and Japan where incentives are being considered to encourage the use of sustainable aviation fuel (SAF), all of which will further increase the demand for vegetable oil feedstocks. Renewable diesel expansion has surged due to its low carbon footprint, federal and local subsidies, and its ability to be used as a drop-in replacement for petroleum diesel. Renewable diesel feedstock is supplied primarily from used cooking oil, animal fats (e.g., tallow), and vegetable oil, with the former two feedstock sources in short supply due to limited production availability. Numerous studies and regulatory approvals have shown Camelina oil’s usefulness as a low-carbon feedstock oil for renewable diesel and sustainable aviation fuel. Camelina’s low-carbon footprint, and ability to be grown as a cover crop on otherwise fallow land, makes it an attractive choice to fill the biofuel feedstock supply gap. Based on the assumption of 60-100 gallons of Camelina oil per acre, 1 billion gallons of feedstock oil would require 10 to 15 million acres of Camelina production. For comparison purposes, canola is currently grown on approximately 21 million acres per year in Canada.

8

Figure 2. Outlook for Biofuel Demand

Source: IEA.Org

Cover Crops: To meet growing demand for oils and protein, and to mitigate the negative environmental impacts of current farming practices, particularly in the corn belt region, the development of cash cover crops or relay crops is another means to increase land productivity and address growing demand without impacting food production. Cover or relay crops are planted between harvest and sowing of major commodities, such as soybean, in effect increasing the number of harvests per growing season. Yield10 believes that Camelina, with its winter hardiness and short growing season, has considerable potential to be used as a cover crop to reduce soil erosion, improve soil quality, control diseases and pests and nutrient run-off from land that is used for row crop production. Camelina can also be used in crop rotation with other crops such as wheat, cereals, corn, and soybean. Third party estimates indicate that Camelina has up to 30 million acres of potential as a cover crop in the U.S. Midwest. By developing technologies to enable winter cover cropping of Camelina to be seamlessly integrated into major row crop rotations, we are in effect “creating” an additional 30 million acres of productive crop land. We plan to evaluate the CI of Camelina oil from cover cropping for both biofuel feedstock and omega-3 oil production where we anticipate there may be further CI improvements.

Business Strategy

In addition to our Camelina products addressing key sustainability drivers, we believe they should also reward farmers and increase profitability across the value chain with any sustainability benefits providing a marketing advantage for our future customers along with potential upside from any available government credits.

Our business strategy for our omega-3 products is to produce omega-3 oil in a closed loop production system based on the capabilities we established and demonstrated in 2022/2023. We will contract with growers to produce omega-3 Camelina solely for sale to Yield10 and contract crushing to produce the oil. Yield10 plans to sell the EPA or EPA+DHA oil focused initially on the aquafeed market through offtake agreements. Our plan is to generate sales for the first 50,000 tons of omega-3 oil in Chile to serve the demand in that market. We plan to file for regulatory approval for the use of our omega- oils in aquafeed formulations in Chile this year.

In early 2024, we revised our business strategy for biofuels to focus on providing research and development services to third parties better resourced and interested in scaling Camelina production for biofuels with the goal of generating R&D service and licensing revenues. By becoming an R&D partner and/or licensing our technologies on a non-exclusive basis to third parties we hope to enable them to accelerate grower adoption and supporting robust value chains to supply the oil. Provided this strategy is successful, we believe Yield10 will be able to build a royalty revenue stream from trait licensing for Camelina which can grow as the number of acres of Camelina planted increases year over year.

We plan to launch a business focused on the production of EPA and EPA+DHA oils based on the Omega-3 Camelina traits developed over the last 10 years by Rothamsted in the U.K. Yield10 signed an Exclusive Collaboration and Option Agreement for this technology with Rothamsted in November 2020 and this Agreement was extended until December

9

31, 2023. In October of 2023 Yield10 executed its exclusive option and expects to finalize the Exclusive Commercial License in the second quarter of 2024. The Omega-3 Camelina business model is to establish closed loop production of the oil for sale into the different omega-3 markets. For the largest volume opportunity, aquafeed, we are looking to form a partnership with one of the world's major aquafeed producers to facilitate and accelerate our entry into that market. For these reasons we plan to continue developing our grower network by shifting to a traditional seed sales model for some of our Camelina varieties. We have a considerable number of growers interested in the buildup of agronomic experience and the development of other applications for Camelina as a crop. Once we complete the regulatory work for the HT and stacked HT Camelina varieties, we expect to make them available to growers as well. The grower network built up for these activities will form the foundation for the future contracted production of the Omega-3 Camelina that is currently in early commercial development.

Yield10 will continue its focus on developing elite Camelina varieties with herbicide tolerance, disease resistance, higher yield and oil content, with the intent to breed Rothamsted's omega-3 product trait into this germplasm in the future. In the meantime, Yield10 plans to use the existing EPA8 and DHA1 Omega-3 Camelina varieties to begin scaling up omega-3 oils production in the near term.

Target Crop: The Oilseed Camelina

Camelina was grown extensively in Europe, Russia and Central Asia since medieval times for oil and protein but was replaced by cultivation of rapeseed during the 1940s. Camelina has the potential to replicate the development path of modern canola from rapeseed on an accelerated timeline based on modern biotechnologies. Starting in the 1960s, the breeding of canola from rapeseed to the first generation was not completed until 1982 and was based on time consuming traditional breeding through mutagenesis and selection to improve the oil fatty acid profile for human consumption (low erucic acid content) and improving the protein meal (low glucosinolates) for use in animal feed. This was followed by incorporating herbicide tolerance and hybrid technologies in the 1990s. Today, canola is grown on 21 million acres in Canada and is reported by the Canola Council of Canada to generate an estimated $30 billion for the Canadian economy.

Camelina has not been subject to intensive plant breeding efforts or crop production improvements, therefore, the full potential of this crop has not yet been achieved. Initial interest in using Camelina oil in biofuels resulted in additional investment in the development of the crop in North America. This work demonstrated that Camelina has several beneficial attributes; it is amenable to production practices used for canola, grows on marginal lands, has enhanced drought and cold tolerance, demonstrated early maturation and requires fewer inputs than other oilseed crops. Camelina is also naturally resistant to diseases that impact canola and its fast-growing cycle makes this crop suitable for spring and winter planting in the Northwest U.S. and into Western Canada as an alternative rotation crop where the relatively overall short growing season would make double cropping very challenging. Further south, the longer overall growing season in the upper mid-west together with Camelina’s short growing season makes it an attractive winter oilseed for relay or cover cropping in corn and soybean rotations. Although the double cropping scenario is where we see the greatest long-term potential for Camelina, our current varieties and capabilities are better positioned for initial commercial activities in the Northwest U.S. and Western Canada. Camelina is an attractive choice of crop for the following reasons:

•Camelina, as an underdeveloped crop, has high technology upside potential to improve agronomics (including herbicide tolerance), seed yield, and seed value.

•There is a growing demand for crops that diversify the crop landscape, have a lower environmental footprint and have the potential to produce high value secondary products, opening new opportunities for farmers.

•Although it can be planted, harvested, stored and processed using existing farm equipment and infrastructure, Camelina has a small seed size and is readily segregated from other grains.

•Camelina, like soybean and corn is non-native to North America and does not outcross to weedy relatives to form viable plants and is readily engineered using advanced genetic tools, making it an ideal platform for accelerated development and the production of novel seed products using advanced gene technologies.

◦Yield10 has engineered Camelina to incorporate well-proven elite herbicide tolerance trait technologies that are not considered regulated by USDA-APHIS in the U.S. under the SECURE rule.

◦Camelina has been engineered to produce seed oil containing high levels of omega-3 (EPA and DHA+EPA) fatty acids as a drop-in replacement oil for fish oil in aquafeed markets as well as for use in nutraceutical and pharmaceutical applications.

10

Yield10 Technology Advantage and Traits in Development

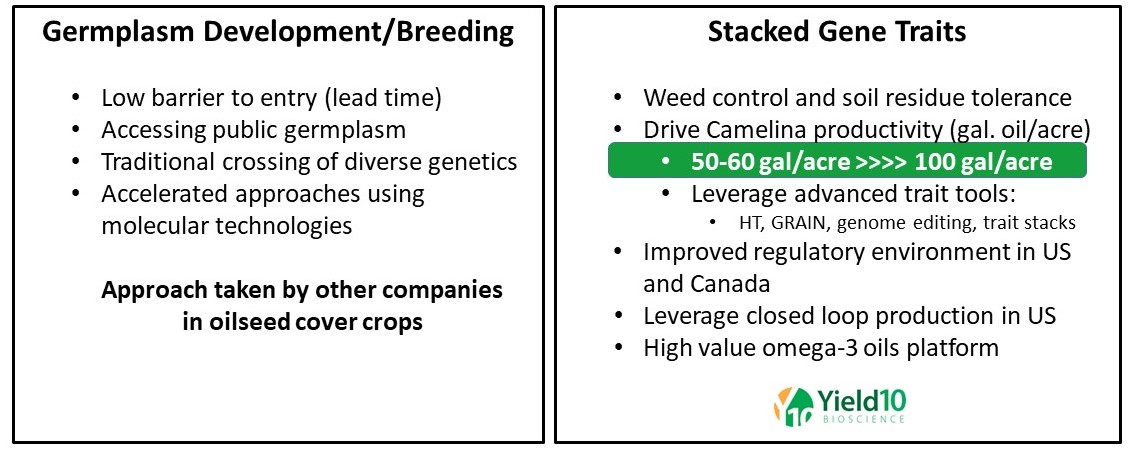

As our predecessor company, Metabolix, we carried out an in-depth review of the scale potential and positive and negative attributes of several “non-food” alternative oilseed crops, including Crambe, pennycress, and Brassica carinata (a rapeseed relative). As a result, we selected Camelina as offering the best option for developing a new platform crop for accelerated development and producing new seed products. Based on our background in advanced synthetic biology, commitment to deploying GMO traits and over 14 years of R&D investment, we believe we are the world leader in discovering and developing advanced gene technologies for Camelina. In addition to our ongoing spring and winter Camelina breeding programs to select new lines with higher yield, early maturity and fungal disease resistance, Yield10 has established a strong pipeline of gene traits for Camelina including input traits such as herbicide tolerance, performance traits including seed and oil yield and new product traits including EPA and EPA plus DHA omega- 3 oils. Yield10 has also demonstrated the production of PHA bioplastic in Camelina seed, and although this project is on hold due to resource constraints, we view this as potentially an exciting future product.

Figure 3. Approaches to Oilseed Cover Crop Development

Figure 4. Pipeline of Genetic Traits for Camelina

11

INPUT TRAITS

Herbicide Tolerance

We recognized early on the need to develop Camelina lines optimized for seamless integration into both crop and chemical rotations in our target geographies. For the Northwest U.S. and Western Canada, the herbicide tolerance traits selected for accelerated development were chosen to address critical farmer issues in that geography. The first requirement is for broadleaf and grassy weed control. The second requirement is to impart into Camelina tolerance to soil residues of herbicides used in crop rotations. An ideal herbicide trait package in Camelina would combine herbicide tolerance traits to manage grassy weeds, broadleaf weeds, and soil residual herbicides. With respect to managing grassy weeds, Camelina is naturally tolerant to the grass herbicide Clethodim, so there is no need to develop new traits in Camelina to provide tolerance to this chemical.

Our glufosinate herbicide tolerance (“GLU”) trait offers farmers an important tool for fighting broadleaf weeds that, if left uncontrolled, can reduce crop yields significantly and increase weed pressure on that land for subsequent crop plantings. We have field tested spring and winter Camelina engineered with GLU with encouraging results over the past two years.

Camelina is very sensitive to Group 2 herbicide residues which can prevent seed emergence and severely impair seed yields. Group 2 weed control chemistries persist longer in the soil which results in plant back restrictions for the next crop in the rotation and in some cases, this can be up to two years. Development is on track with our stacked HT trait which includes tolerance to GLU in combination with both types of Group 2 herbicides, SU and IMI which are commonly used in the target production region for Camelina. Based on discussions with farmers we believe that the stacked HT trait package will be an important enabler for large acre adoption and particularly for winter Camelina varieties which will be planted in the fall following the harvest of spring crops. These HT and stacked HT traits and the availability of Clethodim for grassy weed control provides Yield10 with an ideal herbicide package for the commercial launch of these varieties in the target regions of North America. Yield10 is executing a plan to complete the development of GLU tolerant Camelina including steps to de-regulate meal for use in animal feed.

Complementing our work in engineering new traits into Camelina we have also established a Camelina breeding program. A key goal of this program is to develop a wide range of traits to improve the agronomic performance of Camelina including developing traits for tolerance to the fungal pathogen downy mildew ("DMR") and other fungal diseases, which can negatively impact Camelina seed yields. In 2021, we acquired the rights to a Camelina line with DMR. We also have two backup Camelina lines demonstrating partial resistance and a funded breeding program ongoing for producing additional DMR lines. As these traits are identified we plan to breed them into our advanced HT Camelina lines.

PRODUCT TRAITS

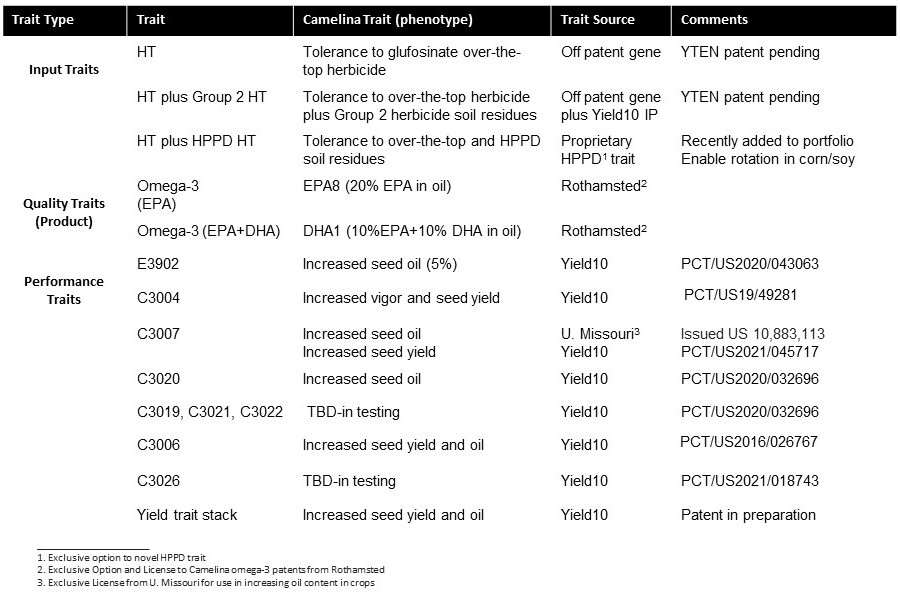

Omega-3 (EPA, DHA+EPA) oil traits

In October of 2023, we executed our option to a global exclusive License to the Omega-3 Camelina technology from Rothamsted and expect to finalize the Commercial License Agreement in the second quarter of 2024. The EPA8 omega-3 trait enables the accumulation of EPA at up to 20% of the fatty acid composition in the Omega-3 Camelina seed oil. The DHA1 omega-3 trait enables the accumulation of EPA at up to 10% of the fatty acid composition plus DHA at up to 10% of the fatty acid composition in the DHA1 Omega-3 Camelina seed oil. We plan to bring both omega-3 varieties forward in development with 2026 being the target for the first commercial-scale production for EPA8 Omega-3 Camelina. Herbicide tolerance is critical in Camelina for on-farm performance and we are breeding HT traits into the omega-3 Camelina varieties to create second generation varieties for large acreage production.

PERFORMANCE TRAITS

Examples of Seed Oil Enhancing Traits: C3007, C3008, C3009, C3010, C3012 and C3020

Yield10 is progressing a series of novel performance traits targeted at increasing the seed oil content in Camelina. We began the technical work in Camelina during 2016 with our C3008a, C3008b and C3009 traits, which regulate the

12

production and degradation of oils in oilseed crops. The best line containing these modifications is designated as our triple-edited, or C3008a, C3008b and C3009 trait in the spring Camelina line E3902 line which consistently shows an approximately 4.7 percent increase in seed oil content as a percentage of overall seed weight. In 2018, we received confirmation from the U.S. Department of Agriculture - Animal and Plant Health Inspection Service's ("USDA-APHIS") Biotechnology Regulatory Services ("BRS") that Camelina line E3902 is not considered to be regulated articles under 7 CFR part 340. We have also gained additional clearances that allow growth of Camelina line E3902 in Argentina, Chile and Canada.

In 2018, we signed an exclusive global license agreement with the University of Missouri for advanced oilseed technology, including the C3007 trait. We have produced several CRISPR genome edited versions of C3007 in both Camelina and canola. Through a series of submissions to USDA-APHIS, we have developed several lines of Camelina and canola edited in combinations of the C3007 genes that USDA-APHIS BRS does not consider to be regulated under 7 CFR part 340. In addition, in 2021 the Ministry of Agriculture, Livestock and Fisheries in Argentina indicated that two C3007 Camelina lines would not be subject to regulation in that country.

Yield10 researchers achieved proof of concept showing that four novel gene targets identified using our proprietary GRAIN trait gene discovery platform impact seed development and/or oil content. In greenhouse testing in 2020, one of the three targets, C3020, produced a 10% increase in seed oil content when engineered with increased activity in Camelina. Data obtained from increasing activity of the other three targets, C3019, C3021, and C3022 indicates these may represent suitable targets for CRISPR genome-editing.

Regulatory Requirements

Ever since the first successful commercialization of a biotechnology-derived agricultural crop in the 1990s, many new crop varieties have been developed and made available to farmers in the U.S. and worldwide. Farmers in the U.S., Canada, and areas of South America have rapidly adopted many of these new biotechnology-derived varieties. According to the USDA, in 2020 over 90 percent of U.S. corn, upland cotton and soybeans planted in the U.S. were varieties produced through traditional forms of genetic engineering. We have established certain core regulatory capabilities and in key geographies, we believe we are benefiting from a science-driven approach to regulations pertaining to genetically engineered (“GE”) crops based on a 30-year history of biotechnology-derived agricultural crops.

Biotechnology-derived or genetically engineered crops are subject to a significant amount of regulation in the U.S. and worldwide. Field tests and field trials of such crops need to ensure that traits in development do not escape or mix with native plants, and crops that may be used in the human and animal food chains must meet certain safety standards. Government regulations, regulatory systems and the political environment that influence them vary significantly among jurisdictions.

For purposes of this discussion, the term “GE” includes both biotechnology-derived or genetically engineered plants that are modified by the insertion of recombinant DNA (“Traditional Genome Modification”) or genetically engineered plants modified through the application of more modern techniques of genome editing. We have seed traits that fall within each of these two generalized categories of GE plants, as summarized above under the subheading “Traits in Development.”

United States Regulation

The U.S. government agencies primarily responsible for overseeing the products of modern agricultural biotechnology are the USDA, the FDA and the EPA. Depending on its characteristics, a product may be subject to the jurisdiction of one or more of these agencies under the federal government’s 1986 Coordinated Framework for the Regulation of Biotechnology, as updated. Other environmental laws or regulations also apply, depending on the specific product and its potential applications or intended uses.

Our seed traits and any future products that are successfully developed containing our seed traits are subject to USDA, FDA and EPA regulatory requirements. Those requirements will vary depending on the particular seed trait and the type and intended use of any product that will be commercialized. Future products that we plan to produce and sell, for

13

example deployment of herbicide tolerant traits, are likely to have EPA regulatory requirements, and the regulations relating to manufacturing and consumer protection will also need to be addressed.

Within USDA, APHIS administers the regulations in 7 CFR part 340, ‘‘Introduction of organisms and products altered or produced through genetic engineering which are plant pests for which there is reason to believe are plant pests.’’ These regulations govern the introduction (importation, interstate movement, or release into the environment) of certain GE organisms. Along with the EPA and the FDA, APHIS is responsible for the oversight and review of GE organisms.

On May 18, 2020, the USDA updated the biotechnology regulations in the Plant Protection Act (7 C.F.R. Part 340) and set up a new paradigm called the Sustainable, Ecological, Consistent, Uniform, Responsible, Efficient (“SECURE”) rule. This Act establishes updated regulations for importation, interstate movement, and environmental release of GE organisms and products. It provides exemptions for plants if the genetic modification is solely a deletion of any size, or the genetic modification is a single base pair substitution or if the genetic modification is solely introducing nucleic acid sequences from within the plant’s natural gene pool. Exemptions also apply if the modification is from editing nucleic acid sequences in a plant to correspond to a sequence known to occur in that plant’s natural gene pool or if the plant is an offspring of a GE plant and does not retain the genetic modification in the GE plant parent. In addition to the above, § 340.1(c) states that modified plants would not be subject to the regulations if they have plant-trait mechanism of action (“MOA”) combinations that are the same as those of modified plants for which APHIS has conducted a regulatory status review and found not to be subject to the regulations under part 340. The focus rests on the organism itself rather than the methods and technologies used to generate it, which is important given improvements in delivery and genome editing modalities over the past 33 years.

In 2020, the regulatory exemptions and confirmation process under the SECURE rule took effect, representing the first comprehensive revision of APHIS’ biotechnology regulations since 1987. The revisions enable APHIS to regulate organisms developed using genetic engineering for plant pest risk with greater precision and reduces the regulatory burden for developers of organisms that are unlikely to pose plant pest risks. Since the new process was enacted, certain of our CRISPR edited Camelina C3007 lines have been confirmed by APHIS as being exempt from regulation by USDA-APHIS under 7 CFR part 340. In addition, in the fourth quarter of 2023 we received confirmation from USDA that both the HT and Stacked HT Camelina are not considered regulated by USDA-APHIS.

For herbicide-tolerant crops the USDA-APHIS regulates the crops while the EPA regulates the herbicide. The EPA establishes tolerances for the allowable amount of herbicide residues that may remain on the crop. Tolerances, as defined by the EPA, are “the maximum amount of a pesticide allowed to remain in or on a food” as part of the process of regulating pesticides. Yield10 cooperated with one of the major producers of glufosinate herbicides to request EPA approval to add Camelina to the producer's herbicide label for use with our GLU HT Camelina. A response from EPA is pending.

Separate from approval for genetic modifications from USDA-APHIS regulations under 7 CFR part 340, a GE plant also will be regulated by the FDA if it is intended to be used as human food or animal feed. Since 1992, the FDA has had in place a voluntary consultation process for developers of bioengineered food (“Biotechnology Consultations”). Final agency decisions and other information from these Biotechnology Consultations are made publicly available by the FDA. Biotechnology Consultations are data-intensive and examine the new food product’s safety and nutritional profile, among other issues. Generally, the FDA has found that such food products do not pose unique health risks to humans or animals, but if a novel allergen or other distinction from the conventional food is present in the new plant variety, the agency may require specific label statements on the product to ensure that consumers are made aware of material differences between GE and conventional versions.

In October 2018, FDA leadership issued a document entitled the “Plant and Animal Biotechnology Innovation Action Plan” (the “Action Plan”) that identified three key priorities for the agency in this area: 1) advancing human and animal health by promoting product innovation and applying modern, efficient and risk-based regulatory pathways; 2) strengthening public outreach and communication regarding the FDA’s approach to innovative plant and animal biotechnology; and 3) increasing engagement with domestic and international partners on biotechnology issues. The Action Plan also stated that the FDA has reviewed the comments and other information it received in response to the January 2017 request for comments, and that it intends to develop guidance for the industry explaining how the FDA’s existing regulatory policy for foods derived from new plant varieties applies to foods produced using genome editing. The FDA also stated in the Action Plan that it intends to begin updating the existing procedures for voluntary Biotechnology Consultations to reflect the agency’s 25 years of experience with foods derived from biotechnology plants and to incorporate any additional issues

14

related to genome editing of food crops. Such procedural updates are expected to be developed and implemented over the next two years.

For herbicide tolerant and Omega-3 Camelina, field trials and analytical work must be conducted to evaluate the composition of the meal and/or oil to ensure their composition is similar to conventional Camelina and that they are free of potential allergens and toxins. Yield10 is developing regulatory plans to support commercialization of products produced in HT, stacked HT and omega-3 Camelina.

Canadian Regulation

In Canada, GE crops, and the food products into which they are incorporated, are regulated by multiple government agencies under a federal framework for the regulation of biotechnology products that is similar to the U.S. system. First, the CFIA is the lead agency for ensuring that a new agricultural biotechnology crop will not pose new risks to Canadian plants, animals, and other agricultural commodities. The Plant Biosafety Office ("PBO") is responsible for conducting environmental assessments of biotechnology-derived plants, referred to as "plants with novel traits" ("PNT"). Authority for the PBO includes both approving confined field trials with the PNT through permits and authorizing their “unconfined release” as a first step towards commercialization. PNTs are defined in the Canadian Seeds Regulations (i) as plants into which a trait or traits have been intentionally introduced, and (ii) where the trait is new in Canada and has the potential to impact the environment. The CFIA also has in place a remutation policy, whereby plants containing the same mutation as a previously authorized plant of the same species are included in the authorization of the original PNT and are therefore subject to the same conditions.

In 2023, the CFIA adopted new regulation and guidelines on determining whether a plant is regulated under Part V of the Seeds Regulations and specifically indicating that genome editing technologies as utilized in crops do not present any unique or specifically identifiable environmental or human health safety concerns as compared to other technologies of plant development. In early 2024, the PBO of the CFIA reviewed information on the Company’s E3902 Camelina and determined that E3902 is not a PNT and is not subject to a pre-market notification under Part V of the Seeds Regulations.

Under the Food and Drugs Act and related regulations, Health Canada is responsible for reviewing a pre-market safety assessment that must be submitted by the manufacturer or importer of a “novel food,” a term of art that includes any PNT or other biotechnology-derived foods. The safety assessment should provide assurances that the novel food is safe when prepared or consumed according to its intended use before it enters the Canadian market and food system. A multi-disciplinary team of experts from Health Canada evaluates the data and information about the novel food and make a determination regarding whether it is safe and nutritious before it can be sold in Canada, as well as whether any restrictions are warranted under applicable law or the product’s safety profile. Health Canada’s final decision documents regarding the safety of these novel foods are made available to the public by the government. As in the U.S., approval of a PNT or a novel food product does not take into account the method with which such product was produced. Rather, Health Canada employs a product-based (as opposed to a process-based) approach to its regulatory oversight of such emerging foods and food ingredients.

As the lead agency for public health and safety, Health Canada also works in conjunction with the CFIA on food labeling oversight when it identifies a potential health or safety issue with a food that could be mitigated through labeling or other disclosures. For example, if the biotechnology-derived food contains a new allergen that is otherwise not present in the conventional version of the food, then specific label statements are required to alert consumers to that important health information. However, the CFIA has primary oversight over non-health issues related to food labeling, packaging, and advertising. Accordingly, the CFIA is the lead agency for ensuring that food labeling and advertising meet the legal requirements of the Food and Drugs Act, and that labeling representations do not create a potential risk of fraud or consumer confusion and are compliant with Canada’s voluntary disclosure standard for GE food ingredients.

Environment Canada is also available to serve as a regulatory “safety net” if a novel product does not naturally fall within the jurisdiction of the CFIA, Health Canada, or the Pest Management Regulatory Agency that oversees pesticide products.

Our work involving the development, greenhouse testing, and field testing of novel yield trait genes in crop plants requires certain government and municipal permits, and we must ensure compliance with all applicable regulations, including regulations relating to GE crops. With laboratories and greenhouses in both the U.S. and Canada, we are also subject to regulations governing the shipment of seeds and other plant material (including GE seeds and GE plant material) between our

15

facilities in the U.S. and Canada, including USDA-APHIS and CFIA permits for the import and phytosanitary certificates for the export of plant materials that could pose a risk to domestic agriculture.

Having deployed our own research and development operations in Saskatoon, Canada in 2010, we have been conducting field studies of various yield traits in that country since 2016 under PNT permits issued by Canadian regulators.

Regulation in Other Jurisdictions

Other jurisdictions and governmental authorities, including in South America and Asia, are increasingly taking an interest in regulating agricultural products of biotechnology. Regulatory approaches vary by jurisdiction, including the existing public health framework and phytosanitary laws in the country, and other less tangible factors such as cultural and religious norms that may have an impact on individual country risk assessments and decision-making. We cannot predict future changes in the global regulatory landscape regarding GE plants subjected to Traditional Genome Modification or GE plants subjected to genome editing. Further, although U.S. and Canadian regulatory authorities have taken similar approaches to overseeing both traditional biotechnology-derived plants and genome edited plants under their national plant health and biosafety laws, regulation of all GE plants in the EU is significantly more stringent than in North America. U.S. and Canadian regulators have also determined that genome edited GE plants pose fewer risks that those subjected to Traditional Genome Modification. A July 2018, Court of Justice of the European Union legal ruling indicates that the existing European regulations for GE plants modified by the insertion of recombinant DNA should be strictly applied to genome edited plants as well. There is thus a sharp distinction between how European and North American regulatory agencies oversee novel seed traits, including those that are generated using the more modern techniques of genome editing. Although we are not currently targeting European markets for the development or commercialization of our products, the EU approach to regulating GE plants without regard to the scientific distinctions between Traditional Genome Modification and directed genome editing could be adopted by emerging oversight regimes for GE products in other jurisdictions. However, an increasing number of countries that dominate GE crop production such as Argentina, Brazil and China are adopting a more favorable regulatory approach towards genome edited plants that do not contain foreign DNA by equating the crops to conventionally bred varieties. This approach first implemented by Argentina, followed by many other countries, demonstrates the evolving landscape for GE crops informed by over 25 years of regulation and GE crop production.

In 2020, Japan published final guidelines for genome edited plants and food that state that these can be sold to the public, without the need for pre-market authorization provided they meet the criteria of being similar to products of traditional breeding.

In 2022, the Chinese Ministry of Agriculture and Rural Affairs published new guidelines for the review and approval of genome edited crops and products paving the way for faster commercialization in that country.

In-License Agreements

Exclusive Collaboration Agreement with Rothamsted Research

On November 12, 2020, Yield10 signed an exclusive collaboration agreement with Rothamsted to support Rothamsted’s Flagship Program to develop omega-3 oils in Camelina. As part of the agreement, Yield10 received an exclusive two-year option to sign a global, exclusive or non-exclusive license agreement to the technology. In November 2022, Yield10 and Rothamsted agreed to extend the collaboration agreement, including the license option, without additional funding support, through December 31, 2023. In October of 2023 Yield10 exercised its exclusive option and expects to execute the global Exclusive License Agreement for this technology with Rothamsted in the second quarter of 2024.

License Agreement with the University of Missouri

Pursuant to a license agreement with the University of Missouri (“UM”) dated as of May 17, 2018, we have an exclusive, worldwide license to novel gene technologies including the C3007 trait to boost oil content in crops. We are obligated to pay UM a license execution payment, milestone payments relating to any regulatory filings and approvals covered by the license agreement, royalties on any sales of licensed products following regulatory approval, as well as a percentage of any sublicense royalties related to the licensed products.

16

We may terminate the license agreement at any time upon 90 days’ prior written notice to UM. Either party may terminate the license agreement upon written notice for a breach that is not cured within 30 days after receiving written notice of the breach. In addition, UM may terminate the license agreement with respect to certain patent rights immediately upon written notice in the event we contest the validity or enforceability of such patent rights.

Competitive Landscape for our Business

Camelina Oilseed and Alternative Cover Crops: Camelina, because it is not currently a major food crop, has been of recent interest in North America for large-scale production of feedstock oil for biofuels, both renewable diesel and sustainable aviation fuel. We believe that there is a growing interest among oilseed crushers and energy companies in sourcing non-food, low CI feedstock oil for supplying the biofuel market. Camelina is attractive, not only as a spring rotation crop, but also as a winter cover crop, enabling a second oil harvest annually for each acre planted. The general interest in cover crops has been steadily increasing over the last several years. The companies focusing on Camelina include Sustainable Oils, S&W Seed, and Smart Earth. There have also been recent investments in oilseed cover crop alternatives to Camelina including the development of carinata by Nuseed and the efforts by CoverCress Inc. over the last several years to develop pennycress as a cover crop for the mid-west corn and soybean belt. In 2023, Chevron/Bunge acquired Chacraservicios S.r.l., based in Argentina from the Italian-based Adamant Group. This latest investment in novel seeds adds a new oil source in Bunge and Chevron’s global supply chains and will help both companies meet the growing demand for lower carbon renewable feedstocks. In 2023 Vision Bioenergy Oilseeds was formed as a joint venture owned by Shell and S&W Seed to develop and commercialize novel plant genetics for oil seed cover crops for biofuel production. Earlier this year, we signed a non-exclusive License Agreement with Vision for the use of our HT and stacked HT Camelina technologies.

Omega-3 Oil: The growing demand for alternative sustainable sources of EPA and DHA omega-3 fatty acids for human nutrition including food/beverage, pharmaceutical, and aquafeed and animal feed applications has made this an attractive area for investment by several companies. Alternative sources include algal fermentation processes commercialized by Veramaris (the joint venture between Evonic and DSM, with a production facility in Blair, Nebraska), Corbion and by Archer Daniels Midland Co. (with a production facility in Clinton, Iowa). We believe that crop based production systems for producing omega-3 oils will always be lower cost to produce and scale than algal fermentations and for this reason we have focused on competing crop based solutions. On the crop-based production side, two different genetically engineered varieties of the oilseed canola have been developed and approved by USDA-APHIS to address this growing demand. Following their acquisition of Bayer’s canola seed business, BASF stopped commercial development of their EPA producing canola. The BASF canola variety produced mostly EPA. Nuseed, a subsidiary of NuFarm is making good progress with the commercial production of its DHA canola oil which has around 10% DHA and a small amount of EPA and recently received regulatory approval for this oil in Norway. This is a major positive development for the use of GMO ingredients in aquaculture feed in the world’s largest farmed salmon production region. We believe the Camelina technology, which enables production of omega-3 EPA, and EPA+DHA oils, have high potential as a drop-in replacement for fish oil in aquafeed. Feed producers in general will blend ingredients from different suppliers to meet their own final product specifications and manage costs. Our Camelina EPA oil has potential use in feed in combinations with other sources of DHA such as algae or the Nuseed DHA oil product.

Intellectual Property

Our continued success depends in large part on our proprietary technology. As of December 31, 2023, Yield10 owns or holds exclusive rights to 18 patent families, including 20 issued patents and 30 pending patent applications. In October of 2023 Yield10 exercised its exclusive option to an exclusive global license to two active patent families of Rothamsted Research, RR213 and RR305, including six issued patents and six pending applications which cover the production of EPA and EPA plus DHA oils in Camelina. We expect to finalize the Commercial License Agreement in the second quarter of 2024.

We continue to seek, develop and evaluate new technologies and related intellectual property that might enhance our business strategy, industry position or deployment options.

Human Capital Resources

As of December 31, 2023, we had 29 full-time employees. Of those employees, 24 were in research and development. Among our staff, 13 hold Ph.D.’s and 13 hold masters’ or bachelors’ degrees in their respective disciplines. Our technical staff has expertise in the following areas: plant genetics, plant biology, plant breeding, microbial genetics,

17

bioinformatics, metabolic engineering and systems biology. Our headquarters is located in Massachusetts, and our wholly-owned subsidiary, Yield10 Oilseeds Inc. ("YOI"), maintains a research and development facility, including greenhouse facilities, in Saskatoon, Canada. None of our employees are subject to a collective bargaining agreement and we consider our relationship with our employees to be good.

Talent Acquisition and Retention

We recognize that our employees largely contribute to our success. To this end, we support business growth by seeking to attract and retain best-in-class talent. We use internal and external resources to recruit highly skilled candidates for open positions. We believe that we are able to attract and retain superior talent as measured by our minimal turnover rate and high employee service tenure.

Total Rewards

Our total rewards philosophy has been to create investment in our workforce by offering a competitive compensation and benefits package for the two geographies in which we have offices. We provide employees with compensation packages that include base salary, annual incentive bonuses, and long-term equity incentive awards. We also offer comprehensive employee benefits, such as life, disability, and health insurance as well as flexible spending accounts, paid time off, and a 401(k) plan. It is our expressed intent to be an employer of choice in our industry by providing a market-competitive compensation and benefits package.

Health, Safety, and Wellness

The health, safety, and wellness of our employees is a priority in which we have always invested and will continue to do so. We provide our employees with access to a variety of innovative, flexible, and convenient health and wellness programs. Program benefits are intended to provide protection and security, so employees can have peace of mind concerning events that may require time away from work or that may impact their financial well-being.

Diversity, Equity, and Inclusion

We believe a diverse workforce is critical to our success. Our mission is to value differences in races, ethnicities, religions, nationalities, genders, ages, and sexual orientations, as well as education, skill sets and experience. We are focused on inclusive hiring practices, fair and equitable treatment, organizational flexibility, and training and resources.

Corporate History and Investor Information

In 1992, our Company was incorporated in Massachusetts under the name Metabolix, Inc. In September 1998, we reincorporated in Delaware and in January 2017, we changed our name to Yield10 Bioscience, Inc. to reflect our change in mission around innovations in agricultural biotechnology focused on developing disruptive technologies for step-change improvements in crop yield. Financial and other information about our Company is available on our website at www.yield10bio.com.

We make available on our website, free of charge, copies of our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after filing such material electronically or otherwise furnishing it to the Securities and Exchange Commission (the "SEC"). In addition, the SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. Our filings with the SEC may be accessed through the SEC's website at http://www.sec.gov.

ITEM 1A. RISK FACTORS

Risk Factor Summary

Our business is subject to numerous risks. We encourage you to carefully review the full risk factors contained in this Annual Report on Form 10-K. Some of the principal risk factors are summarized below:

•We have a history of net losses and our future profitability is uncertain.

18

•We will need to secure additional funding to finance our operations and may not be able to do so when necessary, and/or the terms of any financings may not be advantageous to us.

•Our seed products and crop science technologies are at an early stage of development. We may never commercialize a technology or product that will generate meaningful, or any, revenues.

•There can be no assurance that we will be able to comply with the continued listing standards of The Nasdaq Capital Market.

•The impact of global geopolitical conflicts, including the Russian invasion of Ukraine and the Israel-Hamas war may adversely affect our business, financial condition or results of operations.

•The crop science product development cycle is lengthy and uncertain, and our progress will depend on our ability to attract third-party investment in research under license agreements and on our ability to establish collaborative partnerships to develop and commercialize our innovations.

•Any potential collaborative partnerships that we may enter into in the future may not be successful, which could adversely affect our ability to develop and commercialize our innovations.

•Our crop science program may not be successful in developing commercial products or if our future collaborators are successful in developing commercial products that incorporate our traits, such products may not achieve commercial success.

•Our estimates of market opportunity and forecasts of market growth may prove to be inaccurate, and even if the markets in which we may compete in the future achieve growth, our business could fail to achieve the same growth rates as others in the industry.

•If ongoing or future field trials conducted by us or our future collaborators are unsuccessful, we may be unable to complete the regulatory process for, or commercialize, our products in development on a timely basis.

•Adverse weather conditions, natural disasters, crop disease, pests and other natural conditions can impose significant costs and losses on our business.

•Competition in the market for traits and seeds is intense and requires continuous technological development, and, if we are unable to compete effectively, our financial results will suffer.

•Our business is subject to various government regulations in the United States and Canada; the regulatory requirements for our future products in development are evolving and are subject to change, and if there are adverse changes to the current regulatory framework, our or our future collaborators’ ability to market our traits could be delayed, prevented or limited.

•If we or our future collaborators are unable to comply with and timely complete the regulatory process in the United States and Canada for our future products in development, our or our future collaborators’ ability to market our traits could be delayed, prevented or limited.

•The regulatory environment for genetically engineered crops in jurisdictions outside the United States and Canada varies greatly, and some jurisdictions have more restrictive regulations that could delay, prevent or limit our or our future collaborators’ ability to market our traits.

•Consumer resistance to genetically engineered crops may negatively affect the ability to commercialize future crops containing our traits, as well as our public image, and may reduce any future sales of seeds containing our yield traits.

•Government policies and regulations, particularly those affecting the agricultural sector and related industries, could adversely affect our operations and our ability to generate future revenues and to achieve profitability.

•The products of third parties, or the environment itself, may be negatively affected by the unintended appearance of our trait genes, novel seed compositions and novel seed products.