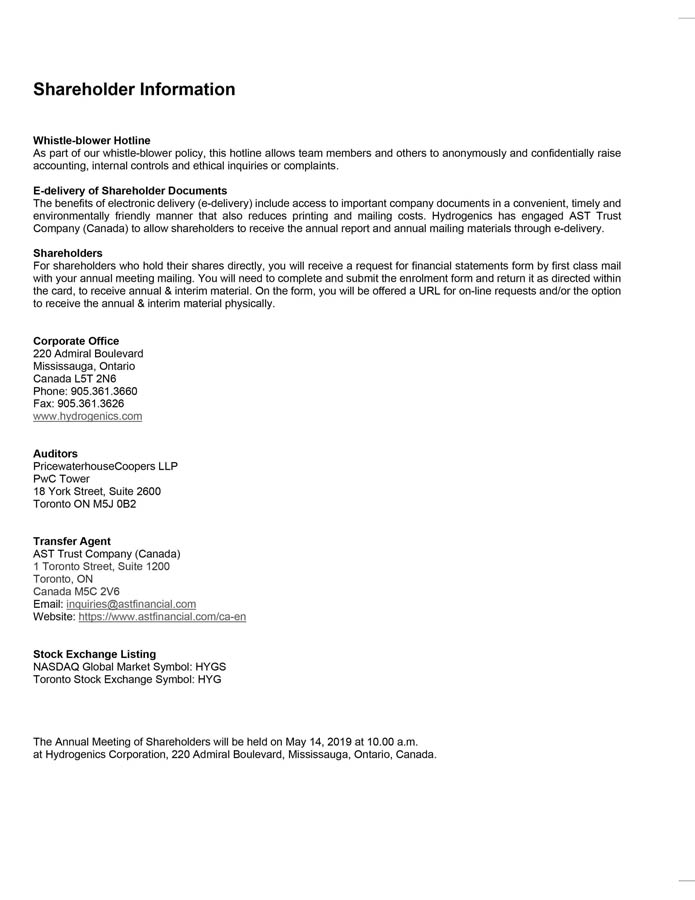

Exhibit 99.3

Hydrogenics Corporation

Table of Contents |

| Message to Shareholders |

2 |

| Management’s Responsibility for Financial Reporting |

4 |

| Management Discussion and Analysis |

|

| 1. |

|

Our Business |

5 |

| 2. |

|

Growth Strategy |

8 |

| 3. |

|

Operating Results |

9 |

| 4. |

|

Financial Condition |

15 |

| 5. |

|

Summary of Quarterly Results |

16 |

| 6. |

|

Liquidity and Capital Resources |

18 |

| 7. |

|

Outstanding Share Data |

22 |

| 8. |

|

Critical Accounting Estimates |

22 |

| 9. |

|

Changes in Accounting Policies and Recent Accounting Pronouncements |

23 |

| 10. |

|

Strategy and Outlook |

24 |

| 11. |

|

Related Party Transactions |

26 |

| 12. |

|

Disclosure Controls |

26 |

| 13. |

|

Internal Control Over Financial Reporting |

26 |

| 14. |

|

Reconciliation of Non-IFRS Measures |

27 |

| 15. |

|

Risk Factors |

28 |

| 16. |

|

Forward-looking Statements |

30 |

| Consolidated Financial Statements |

|

| |

|

Management’s Report on Internal Control over Financial Reporting |

32 |

| |

|

Independent Auditor’s Report |

33 |

| |

|

Consolidated Financial Statements |

35 |

| |

|

Notes to Consolidated Financial Statements |

39 |

| Board of Directors |

84 |

Hydrogenics Corporation

Presidents Message

Building, Connecting, Growing.

Hydrogenics is hard at work building a bridge between the old world

of energy and the new – we are stretching to span a very wide gap, as the world’s fossil fuel habit will not be broken

easily. Over one hundred years of incumbency is tough to counter, and building bridges is not easy work. There is nothing to stand

on in the middle of the gap. The tenuous working from both sides looks futile at first but, then, as the gap narrows, confidence

grows. For this effort to be successful, teamwork, partnership and trust are everything.

We have been building our team for over twenty-four years. It’s

a winning team. It’s a strong team. It’s a committed team – a team that is fully up to the job of bridging the

gap. We have the foundational technical skills to solve the challenges of optimizing electrochemistry. We have the commercial skills

to engage some of the world’s largest companies and invite them into commercial partnership to innovate together. Most importantly,

we have the ragged determination that this bridge will be built. Before any comment on the past year I just wanted to start by

acknowledging the strength of the people that make up our small but powerful team. We are all bridge builders.

Partnership has been the cornerstone for some very encouraging developments

which do, indeed, inspire confidence that the gap is closing on our mission. Large incumbent firms are now deeply engaged with

Hydrogenics to bring new solutions to reality at full scale. In September 2018, after three years of development, certification,

and testing work, Alstom’s hydrogen fuel cell trains – using our technology – came into regular public service

in Germany. Together with our partner Alstom Transport, we have brought zero emission, wireless commuter rail to reality. The cross-linking

of mature electric rail coaches with innovative fuel cell technology has shepherded in a new age in rail transportation. The acceleration

of interest due to this first important reference site has been a joy to watch. We could not have done this from our side alone

– we needed a partner. Alstom has proven to have the tenacity, fortitude and strength to face many challenges and get the

job done. By eliminating the need for costly and unsightly overhead electrical infrastructure, and with innovative energy management

approaches, we have brought the cost of electrified rail down significantly. Cleaner, cheaper, better and faster, it is all there.

We are currently active with Alstom on initiatives in Germany, France, the UK, and in North America. The scale of the opportunities

now in sight for this application are inspiring indeed.

Trust is the last critical component of bridge building, and recent

developments in our relationship with Air Liquide stand firmly in this column. For many years Air Liquide has been a partner and

customer for our industrial electrolysis products. We know each other well. In fact, our first Board Chair as a public company

was the late Norman Seagram, formerly the CEO of Air Liquide Canada. Having Air Liquide as a major shareholder was in some way

a natural evolution based on many years of connection. Underlining the trust between us was the award for the world’s largest

PEM electrolysis project at 20MW, producing 8 metric tons of Hydrogen per day. Crossing the chasm from old to new methods is a

risky step – it takes courage, conviction and boldness. At all levels in Air Liquide there is a deep conviction that scaling

up hydrogen electrolysis technology is a critical component to the decarbonation of the energy and industrial sectors. The trust

of Air Liquide was inspired by what we have already accomplished in scaling up the world’s most compact, efficient and cost-effective

electrolysis system. Evidence on the ground – the Enbridge energy storage site in Ontario – was the foundation in which

trust could be placed. We are deeply grateful that Air Liquide has chosen to be a willing partner with us as we take a giant step

towards closing the gap. This major North American hydrogen generation reference site will be the precursor for even larger projects

in the years to come.

Multiple strands of cable, multiple parallel structural supports,

and multiple points of securement are all key elements of bridge-building. Our strategy has been to keep open several pathways

and approaches rather than to narrow our aspirations prematurely. We have proven capabilities in large-scale hydrogen generation

and in a standardized, low-cost and reliable fuel cell platform. We have worked on multiple applications to learn and refine our

understanding of where value can be created. Over time we have focused and concentrated our efforts, while our offerings are being

met from the “other side” with interest and enthusiasm. However, not all the strands of engagement progress at the

same rate. Some, such as our efforts in China, go through robust cycles which are then followed by some slower progress. Nevertheless,

the goal and end game remain the same. Today the connections and relationships we have with Alstom, Air Liquide, Enbridge and many

other large firms around the globe have reduced the gap between the old energy world and the new. None of this would have happened

without such strong partnerships.

| President’s Message to Shareholders | Page 2 |

We also continue to enjoy the support of our shareholders, some

of whom have been with us for many years, and some for a lesser time. Their confidence in us has allowed us to keep building, connecting,

growing and showing that it “can be done.” I have no reason to doubt that this belief in us will be well rewarded.

We’ve also been assisted by government policies, programs, and funding here in Canada as well as many other parts of the

world. We have been supported by a patient and wise Board of Directors. We are conscious every day of the multiple stakeholders

who support us in our mission of closing the gap.

As we look forward to the coming year, two things stand out. First,

the work of delivering on major commitments and programs is ahead of us. We have been preparing for this a long time. Robust design,

careful checking, and rigorous planning – complemented by teamwork and a conscientious management system – are all

in place. We have always counted on both a strong strategy and capable execution. Second, our job in spreading the confidence we

have in these reference sites and projects is critical to accelerating the growth opportunity. The trains in Germany, our Power-to-Gas

facility with Enbridge in Canada, and our vehicles on the road all over the world are a strong testament that the bridge to a new

place is possible.

On May 24th, 1883 when the Brooklyn bridge opened, 150,000

people and 1800 vehicles crossed the bridge. However, it took John Augustus Roebling 15 years to sell the idea, and it was his

son who finished the job between construction approval in 1867 and completion 16 years later. I’m sure there were many nay-sayers,

disbelievers and skeptics over the whole journey, but on opening day there was no doubt. The river had been crossed, and the bridge

was a whole new path to travel for everyone. One hundred and thirty-six years later, it still stands and serves as a thing of beauty.

This is the kind of work that is worth committing your life to.

|

| |

| Daryl C.F. Wilson |

President & Chief Executive Officer

|

| President’s Message to Shareholders | Page 3 |

Management’s Responsibility for Financial Reporting

Management’s Discussion and Analysis of Financial Condition

and Results of Operations and the consolidated financial statements have been prepared by management and approved by the Board

of Directors of Hydrogenics Corporation (the “Company”). The consolidated financial statements were prepared in accordance

with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”)

and where appropriate, reflect management’s best estimates and judgments. Where alternative accounting methods exist, management

has chosen those methods considered most appropriate in the circumstances. Management is responsible for the accuracy, integrity

and objectivity of the consolidated financial statements within reasonable limits of materiality, and for maintaining a system

of internal controls over financial reporting as described in “Management’s Report on Internal Control Over Financial

Reporting.” Management is also responsible for the preparation and presentation of other financial information included in

the Annual Report and its consistency with the consolidated financial statements.

The Audit Committee, which is appointed annually by the Board of

Directors and comprised exclusively of independent directors, meets with management as well as with the independent auditors to

satisfy itself that management is properly discharging its financial reporting responsibilities and to review the consolidated

financial statements and the independent auditors’ report.

The Audit Committee reports its findings to the Board of Directors

for consideration in approving the consolidated financial statements for presentation to the shareholders.

The Audit Committee considers, for review by the Board of Directors

and approval by the shareholders, the engagement or reappointment of the independent auditors.

The shareholders’ auditors have full access to the Audit Committee,

with and without management being present, to discuss the consolidated financial statements and to report their findings from the

audit process. The consolidated financial statements have been audited by the shareholders’ independent auditors, PricewaterhouseCoopers

LLP, Chartered Professional Accountants, and their report is provided herein.

| |

|

|

| |

|

|

| Daryl C. F. Wilson |

|

Marc Beisheim |

| President and Chief Executive Officer |

|

Chief Financial Officer |

March 15, 2019

Mississauga, Ontario

2018 Management’s Discussion and Analysis | Page 4 |

Who We Are

Hydrogenics, together with its subsidiaries, is a globally recognized

leader in the design, development and manufacture of hydrogen generation, energy storage and fuel cell products based on water

electrolysis technology and proton exchange membrane (“PEM”), technology. Hydrogenics’ mission is to provide

safe, secure, sustainable and emission free energy as a leading global provider of clean energy solutions based on hydrogen. We

maintain operations in Belgium, Canada and Germany with a satellite office in the United States and branch offices in Russia and

Indonesia.

We believe our intellectual property provides us with a strong competitive

advantage and represents a significant barrier to entry. As part of our portfolio, we maintain a collection of innovative energy

storage patents with broad and exclusive rights concerning the use of excess electrical power to produce hydrogen from water while

simultaneously providing electric grid stabilization services. We believe these patents place Hydrogenics in the strongest possible

position to build our company over the long term and will continue to strengthen our efforts as electric grid operators look to

hydrogen as an important strategy for utility-scale energy storage.

How We Are Organized

We operate in various geographic markets and organize ourselves

in two reportable segments being Onsite Generation and Power Systems.

Our OnSite Generation business segment is primarily based in Oevel,

Belgium and develops products for industrial gas, hydrogen fueling and renewable energy storage markets. For the year ended December 31,

2018, our OnSite Generation business reported revenues of $18.3 million and, at December 31, 2018, had 81 full-time employees.

Our Power Systems business segment is primarily based in Mississauga,

Canada, with operations in Gladbeck, Germany, and a satellite facility in Carlsbad, California, USA, and develops products for

energy storage, motive power and stationary applications. For the year ended December 31, 2018 our Power Systems business

reported revenues of $15.6 million and, at December 31, 2018 had 102 full-time employees.

Where applicable, corporate and other activities are reported separately

as Corporate and Other. This is the provision of corporate services and administrative support. At December 31, 2018, our

corporate segment had four full-time employees.

OnSite Generation

Our OnSite Generation business segment, is based on water electrolysis

technology which involves the decomposition of water into oxygen and hydrogen gas by passing an electric current through a liquid

electrolyte (“alkaline”) or a solid PEM. The resultant hydrogen gas is then captured and used for industrial gas applications,

hydrogen fueling applications, and is used to store renewable and surplus energy in the form of hydrogen gas (commonly referred

to as “Power-to-Gas”).

Historically the demand for onsite generation of hydrogen gas has

been driven by relatively modest manufacturing market applications for industrial hydrogen. A typical unit for these applications

would generate 20 to 60 normal cubic meters of hydrogen and consume 100 to 300 kilowatt (kW) of electrical energy. We serve this

market with our HySTAT® and HyLYZER® branded alkaline electrolyzer products, which are based on 60 years of hydrogen experience,

meet international standards, such as ASME, CE, Rostechnadzor and UL, and are certified ISO 9001 from design to delivery. We configure

our HySTAT® products for both indoor and outdoor applications and tailor our products to accommodate various hydrogen gas requirements.

Our OnSite Generation products are sold to leading merchant gas companies, such as Air Liquide and Linde Gas and end-users requiring

high purity hydrogen produced on-site for industrial applications.

Hydrogenics is also one of the leaders in Power-to-Gas market, an

innovative energy conversion and storage solution using PEM electrolysis. Our modular PEM stack electrolyzer is the most power

dense unit in the market today and is ideally suited for large scale, multi megawatt energy storage applications. Power-to-Gas

is the three-step process of integrating renewable sources of generation by load-following, converting the surplus electricity

to hydrogen or renewable gas, and finally the gas is used for fuel, power generation or industrial purposes. An electrolyzer provides

the rapid, dynamic response to the Independent System Operator’s signals to accurately load-follow the intermittent generation

pattern of renewable sources such as wind turbines. Surplus electricity can be stored for consecutive days or even consecutive

weeks without the need to discharge; it is a seasonal storage capability. This energy storage solution bridges the power grid and

the gas grid to unlock new options. It enhances the flexibility of managing the power grid and provides the means to capitalize

on the vast potential of alternative sources of generation to produce a local source of renewable gas to de-carbonize the gas system.

Hydrogenics is working with global energy utilities such as Uniper and, most recently in a joint venture with Enbridge, to commercialize

Power-to-Gas energy storage.

2018 Management’s Discussion and Analysis | Page 5 |

In addition to Power-to-Gas market, large-scale industrial applications

are also appearing for the fueling market, which can be supported by the same PEM electrolysis technology we use for Power-to-Gas.

Fueling market opportunities are being driven by the planned deployment of heavy mobility applications for trains, buses and trucks

with fleet-based requirements. We also are promoting electrolysis in hydrogen fueling stations combined with possible Power-to-Gas

solutions at a distributed storage level. The electrolyzer can be used to generate hydrogen during periods of surplus energy levels,

thus absorbing the excess energy at lower cost to generate hydrogen. This hydrogen is then stored at site and can be used to fuel

hydrogen cars, trains, trucks and buses. If the surplus power is generated from renewable energy sources such as wind and solar,

the potential exists for a completely zero-emission “green” solution as hydrogen fuel cell vehicle emissions only produce

water vapor.

During the past year, we have identified several large-scale applications

which would consume 10 to 100 megawatts (“MW”) of power, which is 100 to 300 times larger than a typical industrial

unit to date. On February 25, 2019, we announced the first award of such a project at 20 MW for Air Liquide Canada. On December

21, 2018, we announced the signing of a Technology and Business Development Agreement (“TBDA”) with The Hydrogen Company

(“H2C”), a wholly-owned subsidiary of L’Air Liquide S.A. (“Air Liquide”). The terms of the TBDA provide

for the joint development of a large scale PEM electrolysis solution focused on lowering the total cost of ownership and collaboration

to bid this solution on large scale PEM electrolysis projects worldwide.

Engagement with other lead customers, such as Uniper and Enbridge,

continues to suggest substantial long-term opportunity for Power-to-Gas, an application for energy conversion and storage. The

ongoing commercialization of these applications will coincide with changes to legal and regulatory frameworks in countries that

recognize the commercial importance of energy storage as a key factor in energy management and reducing a carbon footprint for

electricity generation. A notable development in 2018 was the adoption of the Renewable Energy Directive, Part ii in June by the

European union, which formally sanctioned hydrogen as a zero-emission solution across both motive and Power-to-Gas applications.

The business objectives for our OnSite Generation group are to:

(i) continue to pursue opportunities for customers to convert otherwise wasted renewable energy, such as wind, solar or excess

baseload energy, into hydrogen; (ii) further expand into global markets, such as Eastern Europe (including Russia), Asia, Australia,

North America and the Middle East; (iii) grow our fueling station business; (iv) further increase the gross margins of existing

product lines by improving our procurement and manufacturing processes; (v) reduce the total cost of ownership of our products

through design and technology improvement; and (vi) further increase the reliability and durability of our products to exceed the

expectations of our customers and improve the performance of our applications.

Power Systems

Our Power Systems business segment is based on PEM fuel cell technology,

which transforms chemical energy liberated during the electrochemical reaction of hydrogen and oxygen into electrical energy. Our

HyPM® branded fuel cell products are based on our extensive track record of on-bench testing and real-time deployments across

a wide range of stationary and motive power profiles. We configure our HyPM® products into multiple electrical power outputs

ranging from three kW to one MW with ease of integration, high reliability and operating efficiency, delivered from a highly compact

fuel cell and balance of stack design.

Our target markets include motive power applications, such as trains,

buses, trucks and heavy-duty utility vehicles and stationary power applications (including primary and back-up power). Our target

future addressable markets (stationary power and mobility markets) are estimated to be in excess of $2 billion specifically related

to power systems now largely served by diesel power generation and other liquid fuels.

Our Power Systems products are sold to leading Original Equipment

Manufacturers (“OEMs”) and drive systems integrators for motive power. Additionally, our products are sold for prototype

field tests intended to be direct replacements for traditional lead-acid battery packs for motive applications. We also sell our

power systems in stationary power applications such as those employed for telecom applications. Finally, we also sell our Power

Systems products to aerospace, military and other early adopters of emerging technologies.

2018 Management’s Discussion and Analysis | Page 6 |

The business objectives for our Power Systems group are to: (i)

offer a standard fuel cell platform configurable for many markets, thereby enabling manufacturing efficiencies and reduced development

spending; (ii) achieve further market penetration in the stationary power and motive power markets by tailoring our HyPM® fuel

cell products to meet market specific requirements, including price, performance and features; (iii) reduce product cost while

improving durability and reliability; (iv) invest in sales and market development activities in the backup power and motive power

markets; (v) continue to target early adopters of emerging technologies as a bridge to future commercial markets; and (vi) secure

the requisite people and processes to align our anticipated growth plans with our resources and capabilities.

Our Power Systems business competes with several well-established

battery and internal combustion engine companies in addition to several other fuel cell companies. We compete on relative price

to performance, design innovation and ease of integration. In the backup power market, we believe our HyPM® systems have an

advantage over batteries and internal combustion engines for customers seeking extended run requirements, by offering more reliable

and economical performance. In motive power markets, we believe our HyPM® products are well positioned against diesel generation

and lead-acid batteries by offering increased productivity, lower operational costs and extended range.

There are four types of fuel cells other than PEM fuel cells that

are generally considered to have possible commercial applications, including phosphoric acid fuel cells, molten carbonate fuel

cells, solid oxide fuel cells and alkaline fuel cells. Each of these fuel cell technologies differs in their component materials

and operating characteristics. While all fuel cell types may have potential environmental and efficiency advantages over traditional

power sources, we believe PEM fuel cells can be manufactured less expensively and are more efficient and more practical in compact-scale

stationary and motive power applications. Furthermore, most automotive companies have selected PEM technology for fuel cell powered

automobiles. We expect this will help establish concentration around PEM technology and may result in a lower cost in the supply

chain, as compared to the other fuel cell technologies.

How We Sell Our Products

Our products are sold worldwide to OEMs, systems integrators and

end-users through a direct sales force and a network of distributors. Our sales method varies depending on the product offering,

market and stage of technology adoption. As discussed above, the terms of the TBDA with Air Liquide provide for a joint collaboration

to bid on large scale PEM electrolysis projects.

Intellectual Property

We protect our intellectual property by means of a combination of

patents, copyrights, trademarks, trade secrets, licenses, non-disclosure agreements and contractual provisions. We generally enter

into non-disclosure and confidentiality agreements with each of our employees, consultants and third parties that have access to

our proprietary technology. We currently hold 175 patents in a variety of jurisdictions and have 45 patent applications pending.

Additionally, we enter into commercial licenses and cross-licenses to access third party intellectual property.

We believe our intellectual property provides us with a strong competitive

advantage and represents a significant barrier to entry into our industry for potential competitors. As part of our patent

portfolio, we maintain a collection of innovative energy storage patents with broad and exclusive rights concerning the use of

excess electrical power to produce hydrogen from water while simultaneously providing electric grid stabilization services.

We believe these patents place Hydrogenics in the strongest possible position to build our Company over the long-term and will

continue to strengthen our efforts across the target markets and applications described above.

We typically retain sole ownership of intellectual property developed

by us. In certain situations, we provide for shared intellectual property rights. We have these rights in perpetuity, including

subsequent improvements to the licensed technology.

Given the relative early stages of our industry, our intellectual

property is and will continue to be important in providing differentiated products to customers.

2018 Management’s Discussion and Analysis | Page 7 |

Government Regulation

We are not subject to regulatory commissions governing traditional

electric utilities and other regulated entities in any of the jurisdictions that we operate in. Our products are subject to oversight

and regulation by governmental bodies in regards to building codes, fire codes, public safety, electrical and gas pipeline connections

and hydrogen siting, among others.

Our strategy is to develop electrolyzer and fuel cell products for

sale to OEMs, integrators, electric utilities, gas utilities, merchant gas companies, municipalities and other owners of mass transit

applications (such as buses and trains) and end-users requiring highly reliable products offered at competitive prices. We believe

our success will be substantially predicated on the following factors:

Increasing Market Penetration

At December 31, 2018, we had 17 full-time staff employed in

sales functions. Five of our senior management team are also actively involved in sales initiatives, including maintaining close

contact with our more significant customers. Our focus remains to strengthen the sales function by continually assessing responsibilities

to permit dedicated sales leadership, obtaining detailed assessments of markets, and leveraging our strategic relationships with

companies such as Enbridge, Air Liquide and Alstom. Notable in 2018 was the signing of the TBDA with Air Liquide noted in

Section 1 above.

During 2018, we continued the focus prior years on developing several

key markets and geographies. After a strong start in the Chinese market in 2017 for Power Systems, progress slowed in 2018. The

integration and deployment of the earlier shipped volumes consumed the available execution capability to deploy more. We anticipate

ongoing growth in demand in China and we continue our discussions with multiple existing and new partners to realize further sales

and deliver on current backlog. Also on the mobility front, work continued on our 10 year contract to develop and supply hydrogen

fuel cell propulsion systems for Alstom Transport for passenger rail in Europe. Notable in 2018 was the certification and subsequent

commissioning into service of the Coradia iLint platform. This has provided Alstom with a significant catalyst in their sales efforts

for the platform as it is now in service and production orders under our contract are expected in 2019. We are also actively investigating

extending hydrogen rail opportunities into other markets; notably, in North America, Europe and Asia.

Additionally, we have developed or maintained relationships with

third parties we believe are well positioned in our relevant markets to identify new opportunities for our products. In the industrial

gas market, these third parties include leading merchant gas companies, such as Air Liquide. In the energy storage market, we are

leveraging our strategic relationship with Enbridge. During 2018, the energy storage facility project was commissioned and accepted

by the Independent Energy Service Operator (“IESO”). The facility began in-service operations under an IESO Regulation

Services contract effective May 2018.

Please also refer to Section 1 Our Business under Power Systems

and OnSite Generation for further discussion related to increasing our market penetration.

Future Markets

There are several drivers which will accelerate growth in our markets

in the coming year. Electrification of transport, elimination of diesel fuel and ongoing concern about air quality are major themes.

Increasingly around the world, governments are supporting these themes with policy and funding initiatives. Hydrogen is a versatile

energy carrier which enables the “coupling” of sectors which depend on energy. Renewable power generation, efficient

grid operations, industrial demand and transport can all be served in an integrated way with hydrogen. Accordingly, our combined

competence in electrolysis (the fuel side) and fuel cells (the engine side) supports attractive future market optionality for the

company.

Advancing Our Product Designs

Within our OnSite Generation business segment, we remain focused

on two key areas. First, reducing the cost of our HySTAT® alkaline electrolyzer and improving its efficiency. Innovation in

the design, elimination of non-value adding components, improved component sourcing and fundamental electrochemical improvements

have all contributed to ongoing cost reduction initiatives in 2018 and beyond. We also recognize the opportunity for larger scale

energy storage installations and are continuing to develop significantly scale-up products to better meet this market opportunity.

Second, we are looking at continuing the rollout of PEM electrolysis, particularly in the area of Power-to-Gas where PEM technology

provides a more scalable solution than alkaline electrolysis at higher power levels. The terms of the TBDA announced with Air Liquide

noted in Section 1 aligns with this focus area as it provides for the joint development of a large-scale PEM electrolysis solution

focused on lowering the total cost of ownership.

2018 Management’s Discussion and Analysis | Page 8 |

Within our Power Systems business segment, we spent much of 2018

focusing on further reducing the cost of a fully integrated fuel cell system inclusive of its components and expanding our core

product range to 50kW. We continue to leverage our integration capability in taking a standard fuel cell stack and finding multiple

cost-effective applications. The result is a common building block such as our (HD30 30kW fuel cell) being used in multiple applications

such as buses, stationary power and grid stabilization. We have achieved significant cost reduction milestones but will continue

to further improve the financial viability of the product in the marketplace by looking at both scale (increased volume ordering

from suppliers) as well as bringing components of the supply chain in-house to further reduce production cost.

Selected Financial information

(in thousands of US dollars, except per share amounts)

| | |

| | |

| | |

| | |

| | |

| |

| | |

Year ended December 31, | | |

Favourable

(Unfavourable) | |

| | |

2018 | | |

2017 | | |

2016 | | |

2018 vs 2017 | | |

2017 vs 2016 | |

| OnSite Generation | |

$ | 18,308 | | |

$ | 25,268 | | |

$ | 17,510 | | |

| (28 | )% | |

| 44 | % |

| Power Systems | |

| 15,588 | | |

| 22,847 | | |

| 11,480 | | |

| (32 | )% | |

| 99 | % |

| Total revenue | |

| 33,896 | | |

| 48,115 | | |

| 28,990 | | |

| (30 | )% | |

| 66 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Gross profit | |

| 8,725 | | |

| 11,678 | | |

| 5,995 | | |

| (25 | )% | |

| 95 | % |

| Gross Margin % | |

| 26 | % | |

| 24 | % | |

| 21 | % | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Selling, general and administrative expenses | |

| 11,613 | | |

| 13,626 | | |

| 10,825 | | |

| 15 | % | |

| (26 | )% |

| Research and product development expenses, net | |

| 7,486 | | |

| 6,376 | | |

| 3,576 | | |

| (17 | )% | |

| (78 | )% |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loss from operations | |

| (10,374 | ) | |

| (8,324 | ) | |

| (8,406 | ) | |

| (25 | )% | |

| 1 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Loss from joint ventures | |

| (1,637 | ) | |

| (334 | ) | |

| (156 | ) | |

| (390 | )% | |

| (114 | )% |

| Finance loss, net | |

| (1,028 | ) | |

| (2,108 | ) | |

| (1,295 | ) | |

| 51 | % | |

| (63 | )% |

| Income tax expense | |

| (300 | ) | |

| – | | |

| – | | |

| n/a | | |

| n/a | |

| Net loss | |

$ | (13,339 | ) | |

$ | (10,766 | ) | |

$ | (9,857 | ) | |

| (24 | )% | |

| (9 | )% |

| Net loss per share | |

$ | (0.86 | ) | |

$ | (0.77 | ) | |

$ | (0.79 | ) | |

| (12 | )% | |

| 2 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Cash operating costs1 | |

$ | 18,309 | | |

$ | 17,725 | | |

$ | 13,894 | | |

| (3 | )% | |

| (28 | )% |

| Adjusted EBITDA1 | |

| (9,387 | ) | |

| (5,960 | ) | |

| (7,555 | ) | |

| (57 | )% | |

| 21 | % |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| Cash used in operating activities | |

| (8,381 | ) | |

| (4,782 | ) | |

| (13,213 | ) | |

| (75 | )% | |

| 64 | % |

| Cash and cash equivalents (including restricted cash) | |

| 8,737 | | |

| 22,414 | | |

| 11,278 | | |

| (61 | )% | |

| 99 | % |

| Total assets | |

| 49,924 | | |

| 66,215 | | |

| 49,273 | | |

| (25 | )% | |

| 34 | % |

| Total non-current liabilities (excluding contract liabilities and deferred funding) | |

$ | 6,521 | | |

$ | 9,492 | | |

$ | 10,103 | | |

| 31 | % | |

| 6 | % |

| 1 | Cash operating costs and Adjusted EBITDA are Non-IFRS measures. Refer to section 14 – Reconciliation of Non-IFRS

Measures. |

2018 Management’s Discussion and Analysis | Page 9 |

Highlights for the year ended December 31, 2018 compared to the

year ended December 31, 2017

| • | Revenues decreased by $14.2 million, or 30% to $33.9 million for the year ended

December 31, 2018 compared to $48.1 million in the prior year. Power Systems business segment revenues declined by 32% primarily

attributable to delayed customer orders against our backlog for the Chinese market due to the capacity of our existing integration

partners to deploy and support more units beyond the large number of units they ordered in 2017. OnSite Generation business segment

revenues declined by 28% due to reduced demand for our onsite industrial hydrogen solution. |

| | | |

| | • | We received $32.9 million in new orders for the year ended December 31, 2018 (2017

– $75.9 million) consisting of $19.4 million (2017 – $21.7 million) for the OnSite Generation business

and $13.5 million (2017 – $54.2 million) for the Power Systems business. The OnSite Generation business achieved

a net positive order intake of $1.1 million, whereas orders delivered exceeded orders received by $2.1 million in Power Systems.

As discussed in our Q2-2018 MD&A, we commenced discussions with Kolon Water and Energy Co. Ltd. with respect to dissolving

our joint arrangement. Accordingly, $7.5 million of backlog with the joint venture arrangement for Power Systems was cancelled

at that time. Accumulated backlog otherwise remains strong and our sales pipeline remains very active across both lines of business. |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| | |

December 31, 2017

backlog | | |

IFRS 15

Adj. | | |

Orders

Received | | |

FX | | |

Orders

Delivered/

Revenue

Recognized | | |

Orders cancelled | | |

December 31, 2018

backlog | |

| OnSite Generation | |

$ | 19.9 | | |

$ | (0.8 | ) | |

$ | 19.4 | | |

$ | 0.4 | | |

$ | 18.3 | | |

$ | – | | |

$ | 20.6 | |

| Power Systems | |

| 124.7 | | |

| (0.3 | ) | |

| 13.5 | | |

| (2.7 | ) | |

| 15.6 | | |

| 7.5 | | |

| 112.1 | |

| Total | |

$ | 144.6 | | |

$ | (1.1 | ) | |

$ | 32.9 | | |

$ | (2.3 | ) | |

$ | 33.9 | | |

$ | 7.5 | | |

$ | 132.7 | |

| • | Of the above backlog of $132.7 million, we expect to recognize approximately $49.0

million as revenue in the following 12 months. |

| | | |

| | • | Gross margin increased from 24% to 26% of revenue primarily due to product mix within

the Power Systems segment, which saw an increase in gross margin from 35% to 39%. The OnSite Generation segment gross margin of

14% was the same as last year. |

| | | |

| | • | Selling, general and administrative (“SG&A”) expenses for 2018 of

$11.6 million were lower by $2.0 million, or 15%, compared to $13.6 million for the year ended December 31, 2017. The decrease

is attributable to non-cash gains realized on the revaluation of Deferred Share Units (“DSUs”) in 2018 due to changes

in our stock price, a reconciliation of which is provided in Section 14 under Cash Operating Costs. Net of these non-cash gains,

SG&A for the year decreased by $0.4 million, or 3.3% as compared to last year. |

| | | |

| | • | Net research and product development (“R&D”) expenses were $7.5

million for the year ended December 31, 2018 compared to $6.4 million in 2017, an increase of $1.1 million, or 17%. Of the $7.5

million spent on net R&D, $1.3 million relates to construction of a hydrogen fueling station we will own and operate in the

Greater Toronto Area, $0.6 million relates to commissioning costs for the 2.5MW Power-to-Gas joint venture with Enbridge, $1.8

million relates to our Fuel Cell Power Module (“FCPM”) manufacturing expansion and process improvement initiatives,

$2.2 million relates to expanding our FCPMs to new mobility use cases and furthering development on the next generation of our

fuel cell stack platform, and $1.6 million relates to product development within our OnSite Generation business. |

| | | |

| | • | Loss from operations increased by $2.1 million for the year ended December 31, 2018

to $10.4 million as compared to $8.3 million in 2017. The increase is attributable to lower revenue and reduced gross profit, higher

net R&D expenses partially offset by lower SG&A for the year, as noted above. |

| | | |

| | • | Loss from joint ventures increased by $1.3 million for the year ended December 31,

2018 attributable to the loss of $1.6 million recorded in the second quarter of 2018 to adjust the carrying value of our investment

in our joint venture arrangement with Kolon Water and Energy Co. Ltd. |

| | | |

| | • | Net finance loss decreased by $1.1 million for the year ended December 31, 2018

due primarily to the non-cash gains on the change in fair value of outstanding warrants due to a lower share price. |

2018 Management’s Discussion and Analysis | Page 10 |

| | • | Net loss for the year ended December 31, 2018 was $13.3 million, or $0.86 per share,

compared to a net loss of $10.8 million, or $0.77 per share, for the prior year. The increase in net loss in the current year is

a result of lower revenue and gross profit, the increase in loss from joint ventures and higher net R&D partially offset by

the decreases in SG&A expenses and net finance loss, as discussed above. |

| | | |

| | • | Cash operating costs increased by $0.6 million for the year ended December 31, 2018

compared to last year attributable to an increase in net R&D of $1.1 million, partially offset by a $0.4 million decrease in

SG&A expenses. |

| | | |

| | • | Adjusted EBITDA loss increased by $3.4 million to $9.4 million for the year ended

December 31, 2018 from $6.0 million for the prior year. The increase is primarily attributable to lower gross profit of $3.0 million

and higher cash operating costs of $0.6 million. |

Highlights for the previous year ended December 31, 2017 compared

to the year ended December 31, 2016

| | • | Revenues increased by $19.1 million, or 66%, to $48.1 million for the year ended

December 31, 2017 compared to $29.0 million in the prior year due primarily to increases in shipments in both of our segments.

Specifically: i) an $8.7 million increase in Power Systems revenue principally related to the delivery of fuel cell mobility orders

to the Chinese mobility market; and ii) $11.1 million in energy storage orders related to Power-to-Gas applications for EGAT Thailand,

Doosan Babcock in Aberdeen, Scotland, and Brunsbuttel, Germany. |

| | | |

| | • | The Company received new orders for $21.7 million (2016 - $21.2 million) for the

OnSite Generation business and $54.2 million (2016 - $22.8 million) for the Power Systems business. |

| | |

| | |

| | |

| | |

| | |

| |

| | |

December 31, 2016

backlog | | |

Orders

Received | | |

FX | | |

Orders

Delivered/

Revenue

Recognized | | |

December 31, 2017

backlog | |

| OnSite Generation | |

$ | 20.8 | | |

$ | 21.7 | | |

$ | 2.4 | | |

$ | 25.0 | | |

$ | 19.9 | |

| Power Systems | |

| 85.8 | | |

| 54.2 | | |

| 7.8 | | |

| 23.1 | | |

| 124.7 | |

| Total | |

$ | 106.6 | | |

$ | 75.9 | | |

$ | 10.2 | | |

$ | 48.1 | | |

$ | 144.6 | |

| | • | Gross margin increased from 21% to 24% of revenue primarily due to product mix within

the Power Systems segment, which saw an increase in gross margin from 22% to 35%. This was partially offset by several key first-of-a-kind

projects having a lower margin profile within the OnSite Generation segment. |

| | | |

| | • | SG&A expenses for 2017 of $13.6 million were

greater by $2.8 million, or 26%, compared to $10.8 million for the year ended December 31, 2016. Excluding the impact of

the reversal of an indemnification liability of $0.5 million associated with an acquisition in 2004 included within the year ended

2016 as well as the reversal of previously charged compensation expense for PSUs of $0.2 million also included within the year

ended 2016, SG&A expenses increased $2.1 million. This increase was due to: i) mark-to-market expenses totaling $1.2 million

as a result of the increase in our share price for the year ended December 31, 2017 as compared to the year ended December 31,

2016 (to C$14.00 from C$5.75); ii) an increase of $0.5 million in allowance for doubtful accounts related to the collectability

of a receivable related to a energy storage project; and iii) an increase of $0.4 million relating to increased business activity,

such as compensation costs tied to the achievement of targets, legal fees and insurance costs. |

| | | |

| | • | R&D expenses were $6.4 million for the year

ended December 31, 2017 compared to $3.6 million in 2016, an increase of $2.8 million, or 78%. In the Power Systems segment, the

increase represents increased spending on R&D, primarily for multi-megawatt energy storage projects specifically for

our Power-to-Gas facility with our Enbridge joint venture in Toronto, Canada, and mobility applications such as ongoing development

on the next generation of our fuel cell stack platform for mobility applications such as rail, trucks and buses. While net R&D

expenses also increased in the OnSite Generation segment, this increase was principally due to a decline in funded R&D as there

was a significant Power-to-Gas demonstration project ongoing in Denmark in 2016. Overall gross R&D spending levels at OnSite

Generation declined year-over-year. |

| | | |

| | • | Adjusted EBITDA loss decreased to $6.0 million for the year ended December 31, 2017

from $7.6 million for the prior year, for the reasons noted above. |

2018 Management’s Discussion and Analysis | Page 11 |

| | • | Net loss for the year ended December 31, 2017 was

$10.8 million, or $0.79 per share, compared to a net loss of $9.9 million, or $0.79 per share, for the prior year. While gross

profit increased over $5.7 million, the increase in SG&A expenses and R&D expenses, as discussed above, resulted in a consistent

loss from operations when compared to the year ended December 31, 2016. The increase in net loss in the current period reflects

an increase in other finance losses of $1.0 million. There was a $0.7 million loss on fair value adjustments relating to

outstanding and exercised warrants in the year ended December 31, 2017, whereas the year ended December 31, 2016 included a $0.8

million fair value gain related to outstanding warrants. This was offset by an increase in net foreign currency gains (losses)

from a loss of $0.3 million for the year ended December 31, 2016 to a gain of $0.6 million in the current year. |

| | | |

| | • | Cash operating costs increased 28% to $17.8 million for the year ended December

31, 2017, compared to $13.9 million for the year ended December 31, 2016, primarily reflecting the increase in SG&A and net

R&D expenses above. |

Business Segment Review

We report our results in two business segments: OnSite Generation

and Power Systems. Our reporting structure reflects the way we manage our business and how we classify our operations for planning

and measuring performance. The corporate office and administrative support is reported under Corporate and Other. Refer to Section

10 Strategy and Outlook for a more extensive discussion regarding our products, markets and our business segment strategy.

OnSite Generation

Selected Financial Information

| | |

| | |

| | |

| |

| | |

Years ended December 31, | | |

Favourable

(Unfavourable) | |

| | |

2018 | | |

2017 | | |

2018 vs 2017 | |

| Revenues | |

$ | 18,308 | | |

$ | 25,268 | | |

| (28 | )% |

| Gross profit | |

| 2,648 | | |

| 3,663 | | |

| (28 | )% |

| Gross margin % | |

| 14 | % | |

| 14 | % | |

| - | |

| Selling, general and administrative expenses | |

| 2,959 | | |

| 3,381 | | |

| 12 | % |

| Research and product development expenses, net | |

| 2,927 | | |

| 1,275 | | |

| (130 | )% |

| Segment loss | |

$ | (3,238 | ) | |

$ | (993 | ) | |

| (226 | )% |

Revenues decreased by 28% for the year ended December

31, 2018 as compared to last year due to reduced demand for industrial hydrogen equipment. New orders awarded for the year ended

December 31, 2018 amounted $19.4 million (2017 – $21.7 million), resulting in a net increase of $0.7 million in

our backlog during the year. Backlog at December 31, 2018 of $20.6 million (2017 - $19.9 million) is expected to be recognized

as revenue in the next twelve months.

Gross margin remained consistent with last year despite

the lower level of revenue available to absorb fixed production overheads.

SG&A expenses decreased by 12% in 2018 versus

2017 attributable to the write-off in 2017 of $0.4 million for bad debts. Otherwise expenses were comparable year over year.

Net R&D expenses increased in 2018 versus 2017,

primarily attributable to the construction of a hydrogen fueling station in the Greater Toronto Area that the Company will own

and operate. These expenses amounted to $1.3 million for the year ended December 31, 2018 with a further $1.6 million spent related

to product development activities.

Segment loss increased by $2.2 million for the year

ended December 31, 2018, as compared to the same period last year, reflecting lower gross profit of $1.0 million and the increase

in net R&D expenses of $1.7 million, partially offset by the decrease in SG&A of $0.4 million.

2018 Management’s Discussion and Analysis | Page 12 |

Power Systems

Selected Financial Information

| | |

| | |

| | |

| |

| | |

Years ended December 31, | | |

Favourable

(Unfavourable) | |

| | |

2018 | | |

2017 | | |

2018 vs 2017 | |

| Revenues | |

$ | 15,588 | | |

$ | 22,847 | | |

| (32 | )% |

| Gross Profit | |

| 6,077 | | |

| 8,015 | | |

| (24 | )% |

| Gross margin % | |

| 39 | % | |

| 35 | % | |

| 11 | % |

| Selling, general and administrative expenses | |

| 4,276 | | |

| 4,321 | | |

| 1 | % |

| Research and product development expenses, net | |

| 4,495 | | |

| 4,996 | | |

| 10 | % |

| Segment loss | |

$ | (2,694 | ) | |

$ | (1,302 | ) | |

| (107 | )% |

Revenues decreased $7.3 million for the year ended

December 31, 2018 as compared to the same period in 2017. The decrease in revenue is attributable to delayed customer orders against

our existing backlog for the Chinese market due to the capacity of our existing integration partners to deploy and support more

units beyond the larger number of units they ordered in 2017.

Orders awarded through 2018 amounted to $13.5 million (2017–

$54.2 million) versus revenue of $15.6 million over the same period, resulting in a $2.1 million net decrease in backlog.

As discussed in Section 3 Overall Performance and in our Q2-2018 MD&A, we commenced discussions in June 2018 with Kolon Water

and Energy Co. Ltd. with respect to dissolving our joint venture arrangement. Accordingly, $7.5 million of backlog with the joint

venture was cancelled in the second quarter 2018. The balance of backlog reduction year over year relates to foreign exchange movements.

Backlog otherwise remained strong and our sales pipeline remains very active. Specifically, at December 31, 2018, backlog

was $112.1 million (2017 – $124.7 million) with approximately $28.4 million of this backlog expected to be recognized

as revenue in the next twelve months.

Gross margin of 39% was achieved in 2018, compared

to 35% in 2017. The lower margin in 2017 was due in part to the initial production run of the Alstom commuter rail power modules.

However, the improved margin in 2018 also reflects year-over-year progress towards product standardization, production process

efficiencies and improved supply chain management.

SG&A expenses in 2018 were comparable with the

prior year.

Net R&D expenses were down $0.5 million for

the year ended December 31, 2018 versus the comparative period in 2017 attributable to Canadian government funding received in

2018 towards manufacturing and product development initiatives. Year-to-date 2018 expenses of $4.5 million reflect spending of

$0.6 million on the development of the multi-megawatt energy storage project using PEM fuel cell technology, $1.7 million on government

funded FCPM manufacturing expansion and process improvement initiatives, and $2.2 million related to expanding our FCPMs to new

mobility use cases, such as heavy duty commercial vehicles, and ongoing development on the next generation of our fuel cell stack

platform. The Canadian government funding noted above was awarded in March 2018 and subsequently cancelled effective September

28, 2018, coinciding with a change in government and policy direction.

Segment loss increased $1.4 million for the year ended

December 31, 2018 compared to same period in 2017 due to lower revenue and lower gross profit of $1.9 million offset by the decrease

in R&D expenses of $0.5 million.

2018 Management’s Discussion and Analysis | Page 13 |

Corporate and Other

Selected Financial Information

| | |

| | |

| | |

| |

| | |

Years ended December 31, | | |

Favourable

(Unfavourable) | |

| | |

2018 | | |

2017 | | |

2018 vs 2017 | |

| Selling, general and administrative expenses | |

$ | 4,378 | | |

$ | 5,924 | | |

| 26 | % |

| Research and product development expenses, net | |

| 64 | | |

| 105 | | |

| 39 | % |

| Loss from joint ventures | |

| 1,637 | | |

| 334 | | |

| (390 | )% |

| Interest expense, net | |

| 1,469 | | |

| 1,812 | | |

| 19 | % |

| Foreign currency gains, net | |

| (144 | ) | |

| (635 | ) | |

| (77 | )% |

| Other finance (gains) losses, net | |

| (297 | ) | |

| 931 | | |

| n/a | |

| Segment loss | |

$ | 7,107 | | |

$ | 8,471 | | |

| 16 | % |

SG&A expenses decreased $1.5 million for the year ended

December 31, 2018 versus the comparative period in 2017. The decrease is a result of a net $1.6 million positive change in the

non-cash fair value adjustments of DSUs (as reflected in the reconciliation of Cash Operating Costs in Section 14 Reconciliation

of Non-IFRS measures). SG&A expenses for the year ended December 31, 2018 were otherwise comparable to same period in 2017.

Loss from joint ventures increased $1.3 million for

the year ended December 31, 2018 as compared to the prior year. The increase relates primarily to the loss of $1.6 million recorded

in the second quarter of 2018 to reflect a reduction of the carrying value of the assets of Kolon Hydrogenics to their estimated

net recoverable amount based upon an assessment of fair values less costs of disposal. This write-down coincided with discussions

commenced in June 2018 with Kolon Water and Energy Co. Ltd. with respect to dissolving our joint venture arrangement expected in

2019.

Net interest expense decreased $0.3 million for the

year ended December 31, 2018 as compared to last year due to lower debt outstanding year over year due to principal repayments.

Net foreign currency gains decreased as a result of

principal repayments of Canadian dollar denominated loans during the year.

Other net finance gains (losses) improved $1.2 million

for the year ended December 31, 2018 compared to last year attributable to non-cash fair value adjustments for outstanding warrants.

The improvement was driven by a lower share price as well as the effect of fewer warrants outstanding relative to the prior year.

2018 Management’s Discussion and Analysis | Page 14 |

| | |

| | |

| | |

| | |

| |

| | |

December 31, | | |

December 31, | | |

Increase (decrease) | |

| | |

2018 | | |

2017 | | |

$ | | |

% | |

| Cash, cash equivalents and restricted cash | |

$ | 8,737 | | |

$ | 22,414 | | |

$ | (13,677 | ) | |

| (61 | )% |

| Trade and other receivables | |

| 6,728 | | |

| 8,736 | | |

| (2,008 | ) | |

| (23 | )% |

| Contract assets – (current and non-current) | |

| 6,223 | | |

| 7,223 | | |

| (1,000 | ) | |

| (14 | )% |

| Inventories | |

| 17,174 | | |

| 15,048 | | |

| 2,126 | | |

| 14 | % |

| Prepaid expenses | |

| 1,960 | | |

| 1,374 | | |

| 586 | | |

| 43 | % |

| Operating borrowings | |

| – | | |

| 1,200 | | |

| (1,200 | ) | |

| 100 | % |

| Trade and other payables | |

| 9,068 | | |

| 9,736 | | |

| (668 | ) | |

| (7 | )% |

| Contract liabilities – (current and non-current) | |

| 16,001 | | |

| 14,044 | | |

| 1,957 | | |

| 14 | % |

| Financial liabilities | |

| 3,359 | | |

| 4,913 | | |

| (1,554 | ) | |

| (32 | )% |

| Provisions – (current and non-current) | |

| 2,851 | | |

| 2,720 | | |

| 131 | | |

| 5 | % |

| Deferred funding – (current and non-current) | |

| 1,973 | | |

| 913 | | |

| 1,060 | | |

| 116 | % |

| Other non-current liabilities | |

| 5,711 | | |

| 8,516 | | |

$ | (2,805 | ) | |

| (33 | )% |

Cash, cash equivalents and restricted cash decreased

$13.7 million or 61% in 2018. $5.8 million was used to pay principal and interest on long term debt and repay operating borrowings

and $8.4 million was used for operating activities. This was offset by net $0.5 million of cash provided by investing activities

attributable to government funding and proceeds on the disposal of equipment. Refer to Section 6 – Liquidity and Capital

Resources for a more detailed discussion of the change in cash, cash equivalents and restricted cash.

Trade and other receivables decreased $2.0 million

consistent with lower revenue in current year versus last year.

Contract assets (current and non-current) decreased

$1.0 million due to the change in value of amounts recognized on performance obligations satisfied over time for a long-term Power

Systems contract as well as revenue recognized for start-up and commissioning of equipment consistent with the application of IFRS

15, described in Section 9 Changes in Accounting Policies and Recent Accounting Pronouncements.

Inventories increased $2.1 million attributable to

work in progress and finished goods inventory build-up required to support the schedule of expected deliveries against our backlog

for Power Systems and OnSite Generation products into Q1-2019.

Prepaid expenses increased $0.6 million reflecting

prepayment of purchasing commitments and transaction costs incurred for the subscription agreement with Air Liquide.

Trade and other payables decreased $0.7 million as

we reduced purchases for long lead items only given the availability of current inventory levels to support scheduled deliveries

over the next quarter.

Contract liabilities (current and non-current) increased

$2.0 million primarily attributable to the net receipt of deposits on new contracts versus deposits applied to invoiced contracts

as compared to the prior year.

Financial liabilities decreased $1.6 million reflecting

the revaluation to fair value of outstanding warrants and DSU liabilities compared to December 31, 2017 attributable to drop in

our share price year over year.

Provisions include warranty and start-up and commissioning.

Warranty provisions increased $0.2 million mainly attributable to additional work required on projects delivered in the prior year

offset by a $0.1 million decrease in start-up and commissioning provisions mainly due to strengthening of U.S. dollar against Euro

during the year.

Deferred funding increased $1.1 million reflecting

the receipt of funding for new energy storage projects in Europe.

Other non-current liabilities decreased $2.8 million

due to principal repayments made in the year on our long-term debt with Export Development Canada and the Province of Ontario.

2018 Management’s Discussion and Analysis | Page 15 |

| 5 | Summary of Quarterly Results |

The following table highlights selected financial information for the eight consecutive

quarters ended December 31, 2018.

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| | |

2018 | | |

2018 | | |

2018 | | |

2018 | | |

2017 | | |

2017 | | |

2017 | | |

2017 | |

| | |

Q4 | | |

Q3 | | |

Q2 | | |

Q1 | | |

Q4 | | |

Q3 | | |

Q2 | | |

Q1 | |

| Revenues | |

$ | 10,475 | | |

$ | 7,665 | | |

$ | 7,609 | | |

$ | 8,147 | | |

$ | 19,745 | | |

$ | 12,079 | | |

$ | 7,556 | | |

$ | 8,735 | |

| Gross profit | |

| 1,915 | | |

| 1,471 | | |

| 2,101 | | |

| 3,238 | | |

| 5,668 | | |

| 2,897 | | |

| 440 | | |

| 2,673 | |

| Gross margin % | |

| 18.3 | % | |

| 19 | % | |

| 28 | % | |

| 40 | % | |

| 29 | % | |

| 24 | % | |

| 6 | % | |

| 31 | % |

| Adjusted EBITDA | |

| (2,805 | ) | |

| (2,529 | ) | |

| (2,447 | ) | |

| (1,606 | ) | |

| 175 | | |

| (1,947 | ) | |

| (3,446 | ) | |

| (742 | ) |

| Net loss | |

| (3,141 | ) | |

| (3,443 | ) | |

| (4,801 | ) | |

| (1,954 | ) | |

| (975 | ) | |

| (2,032 | ) | |

| (5,462 | ) | |

| (2,297 | ) |

| Net loss per share - basic and fully diluted | |

$ | (0.20 | ) | |

$ | (0.22 | ) | |

$ | (0.31 | ) | |

$ | (0.13 | ) | |

$ | (0.06 | ) | |

$ | (0.13 | ) | |

$ | (0.43 | ) | |

$ | (0.18 | ) |

| Weighted average common shares outstanding | |

| 15,441,947 | | |

| 15,442,416 | | |

| 15,440,888 | | |

| 15,436,879 | | |

| 15,133,194 | | |

| 15,232,905 | | |

| 12,677,167 | | |

| 12,545,076 | |

When comparing the fourth quarter of 2018 to the fourth quarter

of 2017, our net loss increased by $2.2 million to $3.1 million ($0.20 per common share) compared to a net loss of $1.0 million

($0.06 per common share). This increase was driven by lower revenue of $9.3 million and a decrease in gross profit of $3.8 million.

Adjusted EBITDA decreased by $3.0 million to a loss of $2.8 million from a profit of $0.2 million reflecting the decrease in gross

profit of $3.8 million, offset by a decrease in cash operating costs of $0.6 million. The decrease in cash operating costs is attributable

to lower SG&A expenses of $1.0 million offset by higher net R&D expenses of $0.4 million attributable to FCPM manufacturing

expansion and process improvement initiatives in the current quarter. The focus of our R&D activities in Q4-2018 also included

expanding our FCPMs to new mobility use cases, such as heavy duty commercial vehicles, and furthering development on the next generation

of our fuel cell stack platform and electrolyzer products.

When comparing the third quarter of 2018 to the third quarter of

2017, our net loss increased by $1.4 million (70%) to $3.4 million ($0.22 per common share) compared to a net loss of $2.0 million

($0.13 per common share). This increase was driven by lower revenue of $4.4 million and a decrease in gross profit of $1.4 million.

Adjusted EBITDA decreased by $0.6 million to a loss of $2.5 million from a loss of $1.9 million reflecting the decrease in gross

profit of $1.4 million offset by an improvement in cash operating costs of $0.9 million. The improvement in cash operating costs

is attributable to reduced net R&D expenses; notably, an increase in government funded FCPM manufacturing expansion and process

improvement initiatives in the current quarter. The focus of our R&D activities in Q3-2018 also included expanding our FCPMs

to new mobility use cases, such as heavy duty commercial vehicles, and furthering development on the next generation of our fuel

cell stack platform and electrolyzer products.

When comparing the second quarter of 2018 to the second quarter

of 2017, our net loss decreased by $0.7 million (12%) to $4.8 million ($0.31 per common share) compared to a net loss of $5.4 million

($0.43 per common share). This improvement was driven by the increase in gross profit of $1.7 million reflecting a gross margin

improvement to 28% from 6%, offset by an increase in losses from our joint venture with Kolon. Adjusted EBITDA improved by $1.0

million to a loss of $2.4 million from a loss of $3.4 million. The improvement reflects additional gross profit of $1.7 million

offset by an increase of $0.7 million in cash operating costs year-over-year. The increase in cash operating costs reflects $0.3

million and $0.4 million respectively of additional expenditures for SG&A and net R&D. The increase in SG&A is attributable

to increased business development and marketing activities. The focus of our R&D activities in the quarter included commissioning

the 2.5MW Power-to-Gas facility with Enbridge, government funded FCPM manufacturing expansion and process improvement initiatives,

expanding our FCPMs to new mobility use cases, such as heavy duty commercial vehicles, and furthering development on the next generation

of our fuel cell stack platform and electrolyzer products.

When comparing the first quarter of 2018 to the first quarter of

2017, our net loss decreased 15% to $2.0 million ($0.13 per common share) from $2.3 million ($0.18 per common share). An increase

in gross profit of $0.6 million was principally due to improved direct margins due to product mix. Finance loss improved from a

loss of $0.9 million to income of $0.1 million primarily as a result of adjustments to the fair value of outstanding warrants related

to the net decrease in the Company’s share price in the current quarter as compared to a net increase in share price for

the comparative quarter of March 31, 2017. SG&A expenses decreased $0.2 million in the first quarter of 2018. Excluding mark

to market expenses relating to our DSUs as a result of the increase in our share price for the three months ended March 31, 2018

as compared to the three months ended March 31, 2017, SG&A expenses increased $0.4 million. The increase is the result of increased

advertising and marketing costs, facility costs, and information technology costs within the Company. These improvements were offset

by an increase in net R&D expenses of $1.1 million primarily due to increased spending on the 2.5MW energy storage project,

and mobility applications such as the demonstration of the technical viability of our Celerity PlusTM product in heavy

duty commercial vehicle applications, as well as furthering development on the next generation of our fuel cell stack platform.

2018 Management’s Discussion and Analysis | Page 16 |

In the fourth quarter of 2017, our net loss improved by $1.5 million

to a net loss of $1.0 million ($0.06 per common share) from a net loss of $2.5 million ($0.20 per common share) in the fourth quarter

of 2016. An increase in gross profit of $3.7 million was principally due to increased revenues and improved direct margins due

to product mix through increased production and delivery of standardized fuel cells for the mobility market, as well as economies

of scale, particularly within the Power Systems business segment. This was partially offset by an increase in net R&D spending

during the quarter of $1.0 million and an increase of $1.4 million relating to SG&A expenses as compared to the fourth quarter

of 2016. Excluding the impact of an increase in DSU expense of $0.6 million for the three months ended December 31, 2017 as a result

of the increase in the share price in the current quarter, SG&A expenses increased $0.8 million. The improvement in gross profit

was also partially offset by an increase in fair value adjustments (loss) relating to outstanding warrants ($0.1 million) in the

three months ended December 31, 2017 as a result of the increase in the share price in the current quarter, whereas the three months

ended December 31, 2016 had a gain of $0.2 million. This was offset by the movement in net foreign currency gains (losses), from

a loss of $0.2 million for the three months ended December 31, 2016 to a gain of $0.1 million in the current year.

In the third quarter of 2017, our net loss was consistent at $2.0 million

($0.13 per common share from $0.15 per common share), compared to the third quarter of 2016. An increase in gross profit of $1.8 million

was principally due to increased revenues and improved direct margins due to product mix. This was partially offset by an increase

in net R&D spending during the quarter of $1.9 million, and fair value adjustments (loss) relating to outstanding warrants

($0.6 million) in the three months ended September 30, 2017, whereas the three months ended September 30, 2016 had

a loss of $0.1 million.

In the second quarter of 2017, our net loss increased to $5.7 million

from $3.1 million ($0.45 per common share) compared to the second quarter of 2016 ($0.25 per common share). A decrease in gross

profit of $1.5 million was principally due to decreased revenues and reduced direct margins due to product mix. Also contributing

to the decrease in gross margin was lower absorption of indirect overhead costs as a result of the decrease in revenue. There was

also an increase in other finance losses of $1.1 million in the three months ended June 30, 2017 compared to the same period of

2016 due to the fair value adjustments relating to outstanding warrants (a loss of $0.8 million) in the three months ended June

30, 2017, whereas the three months ended June 30, 2016 included a gain of $0.3 million.

In the first quarter of 2017, our net loss remained consistent at

$2.3 million ($0.18 per common share) compared to the first quarter of 2016. An increase in gross profit of $1.5 million was principally

due to increased revenue and improved direct margins due to product mix. This was offset by: i) an increase in SG&A expenses

related to the increased mark-to-market expenses due to the increase in our share price; ii) the absence of a reversal in SG&A

expenses of $0.5 million related to the indemnification liability in the first quarter of 2016; iii) an increase in other finance

losses of $0.7 million in the three months ended March 31, 2017 compared to the same period of 2016 due to the fair value adjustments

relating to outstanding warrants in the three months ended March 31, 2017 compared to the three months ended March 31, 2016; and

iv) a fair market value adjustment gain of $0.1 million on unsettled foreign exchange contracts included in the 2016 quarter.

2018 Management’s Discussion and Analysis | Page 17 |

| 6 | Liquidity and Capital Resources |

Cash Used in Operating Activities

| | |

| | |

| | |

| | |

| |

| | |

Years ended | | |

| | |

| |

| | |

December 31, | | |

| | |

| |

| (Thousands of US dollars) | |

2018 | | |

2017 | | |

$ Change | | |

% Change | |

| Net loss | |

$ | (13,339 | ) | |

$ | (10,766 | ) | |

$ | (2,573 | ) | |

| (24 | )% |

| (Increase) decrease in restricted cash | |

| (304 | ) | |

| 134 | | |

| (438 | ) | |

| n/a | |

| Net change in non-cash operating assets | |

| 1,750 | | |

| (223 | ) | |

| 1,973 | | |

| n/a | |

| Other items not affecting cash | |

| 3,512 | | |

| 6,073 | | |

| (2,561 | ) | |

| (42 | )% |

| Cash used in operating activities | |

$ | (8,381 | ) | |

$ | (4,782 | ) | |

$ | (3,599 | ) | |

| (75 | )% |

Cash used in operating activities increased by $3.6 million in 2018

compared to 2017 due primarily to lower gross profit of $3.0 million and an increase in cash operating costs of $0.7 million.

Cash Provided by Investing Activities

| | |

| | |

| | |

| | |

| |

| | |

Years ended | | |

| | |

| |

| | |

December 31, | | |

| | |

| |

| (Thousands of US dollars) | |

2018 | | |

2017 | | |

$ Change | | |

% Change | |

| Investment in joint venture | |

$ | – | | |

$ | (93 | ) | |

$ | 93 | | |

| n/a | |

| Purchases of property, plant and equipment | |

| (1,001 | ) | |

| (3,920 | ) | |

| 2,919 | | |

| 74 | % |

| Receipt of government funding | |

| 974 | | |

| 1,792 | | |

| (818 | ) | |

| (46 | )% |

| Proceeds from disposals of property, plant and equipment | |

| 700 | | |

| 1,035 | | |

| (335 | ) | |

| (32 | )% |

| Purchase of intangible assets | |

| (125 | ) | |

| (25 | ) | |

| (100 | ) | |

| 406 | % |

| Cash provided by (used in) investing activities | |

$ | 548 | | |

$ | (1,211 | ) | |

$ | 1,759 | | |

| n/a | |

Cash provided by investing activities improved by $1.8 million in

2018 over 2017 due primarily to reduced capital expenditures net of government funding.

Cash Used in Financing Activities

| | |

| | |

| | |

| | |

| |

| | |

Years ended | | |

| | |

| |

| | |

December 31, | | |

| | |

| |

| (Thousands of US dollars) | |

2018 | | |

2017 | | |

$ Change | | |

% Change | |

| Proceeds from common shares issued and stock options exercised, net of issuance costs | |

$ | 40 | | |

$ | 19,745 | | |

$ | (19,705 | ) | |

| n/a | |

| Principal repayment of long-term debt | |

| (3,120 | ) | |

| (1,639 | ) | |

| (1,481 | ) | |

| (90 | )% |

| Exercise of warrants | |

| – | | |

| 1,374 | | |

| (1,374 | ) | |

| n/a | |

| Interest payment | |

| (1,498 | ) | |

| (1,274 | ) | |

| (224 | ) | |

| (18 | )% |

| Repayment of operating borrowings | |

| (1,193 | ) | |

| (873 | ) | |

| (320 | ) | |

| (37 | )% |

| Repayment of repayable government contributions | |

| – | | |

| (171 | ) | |

| 171 | | |

| n/a | |

| Cash provided by (used in) financing activities | |

$ | (5,771 | ) | |

$ | 17,162 | | |

$ | (22,933 | ) | |

| n/a | |

Cash used in financing activities for 2018 amounted to $5.8 million

and related entirely to debt service and repayment of operating borrowings.

2018 Management’s Discussion and Analysis | Page 18 |

Credit and Loan Facilities

At December 31, 2018, the Company’s subsidiary in Belgium

(the “Borrower”) had a joint credit and operating line facility of €7,000, which renews annually in April upon

review. Under this facility, the Borrower may borrow up to a maximum of 75% of the value of awarded sales contracts, approved by

the Belgian financial institution, to a maximum of €500; and may also borrow up to €1,500 for general business purposes,