UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Amendment No. 1)

(Mark One)

REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR (G) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

|

|

| For the fiscal year ended: |

|

|

OR | |

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES AND EXCHANGE ACT OF 1934 | |

|

|

OR | |

|

|

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES AND EXCHANGE ACT OF 1934 | |

|

|

| Date of event requiring this shell company report |

For the transition period from ___________ to ____________

Commission File Number:

(Exact name of Registrant as specified in its charter) |

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

Title of each class |

| Trading Symbol (s) |

| Name of each exchange on which registered |

|

| OTC |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

___________None________

Title of Class

SEC 1852 (01-12) | Persons who respond to the collection of information contained in this form are not required to respond unless the form displays a currently valid OMB control number. |

Securities registered or to be registered pursuant to Section 15(d) of the Act.

____________None________

Title of Class

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

As of September 30, 2021, there were

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☐

If the report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Security Exchange Act of 1934. YES ☐

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Security Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Security Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See the definitions of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one).

Large accelerated filer | ☐ | ☒ | |

Accelerated filer | ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

| 2 |

EXPLANATORY NOTE

This Amendment No. 1 on Form 20-F/A (the “Amendment”) is being filed by UMeWorld Limited (the “Company,” “we,” “our,” or “us”) to amend the Company’s Annual Report on Form 20-F for the fiscal year ended September 30, 2021, originally filed with the U.S. Securities Exchange Commission on February 14, 2022 (the “Original Filing”). The Company is filing this Amendment solely to furnish the Interactive Data File disclosure as Exhibit 101 in accordance with Rule 405 of Regulation S-T, which was not included in the Original Filing. Exhibit 101 includes information in eXtensible Business Reporting Language (XBRL).

This Amendment consists solely of the cover page and this explanatory note. Except as described above, this Amendment does not amend any information set forth in the Original Filing or reflect any events that occurred subsequent to the filing of the Original Filing on February 14, 2022. Accordingly, this Amendment should be read in conjunction with the Original Filing and with our filings with the U.S. Securities Exchange Commission subsequent to the Original Filing.

| 3 |

FORM 20-F

For the Years Ended September 30, 2021, 2020 and 2019

INDEX

PRELIMINARY NOTES

|

|

|

| ||

|

|

|

|

| |

|

| 7 |

| ||

|

| 7 |

| ||

|

| 7 |

| ||

|

| 23 |

| ||

|

| 34 |

| ||

|

| 34 |

| ||

|

| 41 |

| ||

|

| 46 |

| ||

|

| 47 |

| ||

|

| 48 |

| ||

|

| 49 |

| ||

|

| 52 |

| ||

|

| 52 |

| ||

|

|

|

|

|

|

|

|

|

| ||

|

|

|

| ||

|

| 53 |

| ||

Material Modifications to the Rights of Securities Holders and Use of Proceeds |

|

| 53 |

| |

|

| 53 |

| ||

|

| 55 |

| ||

|

| 55 |

| ||

|

| 55 |

| ||

|

| 55 |

| ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

|

| 55 |

| |

|

| 56 |

| ||

|

| 56 |

| ||

|

| 56 |

| ||

|

|

|

|

|

|

|

|

|

| ||

|

|

|

|

| |

|

| 57 |

| ||

|

| 57 |

| ||

|

| 57 |

| ||

| 4 |

| Table Of Contents |

INTRODUCTION

In this annual report, except where the context otherwise requires and for purposes of this annual report only:

| · | “we”, “us”, “our company”, “our” and “the Company” and similar words refer to UMeWorld Limited, a British Virgin Islands company, and its consolidated subsidiaries and affiliated entities, as appropriate, including its consolidated variable interest entity (“VIE”); |

|

|

|

| · | “China” or “PRC” refers to People’s Republic of China, and for the purpose of this annual report, excludes Taiwan, Hong Kong and Macau; |

|

|

|

| · | “shares”, or “ordinary shares” refers to our ordinary shares, par value US$0.0001 per share; |

|

|

|

| · | “RMB” or “Renminbi” refers to the legal currency of China, “HK$” refers to the legal currency of Hong Kong and “$,” “dollars,” “US$” or “U.S. dollars” refers to the legal currency of the United States; |

|

|

|

| · | “U.S. GAAP” refers to generally accepted accounting principles in the United States; |

|

|

|

| · | “VIE” refers to Guangzhou XinYiXun Network Technology Co. Ltd., a domestic PRC company in which we do not have equity interests but its financial results have been consolidated into our consolidated financial statements in accordance with U.S. GAAP; |

|

|

|

| · | “K-12” refers to the year before the first grade through the last year of high school; and |

|

|

|

| · | “PRC GAAP” refers to generally accepted accounting principles in the People’s Republic of China. |

Our financial statements are expressed in U.S. dollars, which is our reporting currency. Certain of our financial data in this annual report on Form 20-F are translated into U.S. dollars solely for the reader’s convenience. Unless otherwise noted, all foreign currency translations in this annual report on Form 20-F can be found on Note 2 of our audited consolidated financial statements on page F-10. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, at the rate stated above, or at all.

| 5 |

| Table Of Contents |

FORWARD-LOOKING INFORMAITON

This annual report contains forward-looking statements that reflect our current expectations and views of future events. These forward looking statements are made under the “safe-harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by these forward-looking statements.

You can identify some of these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to” or other similar expressions. These forward-looking statements include statements relating to:

| · | our anticipated growth strategies; |

|

|

|

| · | competition in the K-12 after-school tutoring market; |

|

|

|

| · | our future business development, results of operations and financial condition; |

|

|

|

| · | expected changes in our revenues and certain cost and expense items; |

|

|

|

| · | our ability to increase student enrollments and course fees and expand course offerings; |

|

|

|

| · | risks associated with the expansion of our geographic reach; |

|

|

|

| · | the expected increase in spending on private education in China; and |

|

|

|

| · | PRC laws, regulations and policies relating to private education and providers of after-school tutoring services. |

We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Although we believe that our expectations expressed in these forward-looking statements are reasonable, our expectations may later be found to be incorrect. You should read this annual report and the documents that we refer to in this annual report completely and with the understanding that our actual future results may be materially different from and/or worse than what we expect. We qualify all of our forward-looking statements with these cautionary statements.

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

| 6 |

| Table Of Contents |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not Applicable.

ITEM 3. KEY INFORMATION

A. | Selected Financial Data |

The following selected financial information should be read in connection with, and is qualified by reference to, our consolidated financial statements and their related notes and the section entitled “Operating and Financial Review and Prospects” included elsewhere in this annual report. The consolidated statements of operations and other comprehensive loss data for the fiscal years ended September 30, 2021, 2020 and 2019 and the consolidated balance sheets data as of September 30, 2021, 2020 and 2019 are derived from audited consolidated financial statements included elsewhere in this annual report. Our historical results for any prior period are not necessarily indicative of results to be expected in any future period.

Selected Consolidated Statements of Operations and Other Comprehensive Loss Data:

|

| For the Years Ended September 30, |

| |||||||||

|

| 2021 |

|

| 2020 |

|

| 2019 |

| |||

Revenues |

|

| 2,832 |

|

|

| 4 |

|

|

| 113 |

|

Gross loss |

|

| (16,809 | ) |

|

| 4 |

|

|

| (477 | ) |

Operating expenses |

|

| (86,848 | ) |

|

| (134,953 | ) |

|

| (117,177 | ) |

Loss from operations |

|

| (103,657 | ) |

|

| (134,949 | ) |

|

| (117,654 | ) |

Other (expenses) income, net |

|

| (3,779 | ) |

|

| (14,015 | ) |

|

| 14 |

|

Net loss |

|

| (107,436 | ) |

|

| (148,964 | ) |

|

| (117,640 | ) |

Selected Consolidated Balance Sheets Data:

|

| As of September 30, |

| |||||||||

|

| 2021 |

|

| 2020 |

|

| 2019 |

| |||

Current assets |

|

| 36,963 |

|

|

| 16,890 |

|

|

| 14,579 |

|

Total assets |

|

| 56,203 |

|

|

| 16,890 |

|

|

| 14,579 |

|

Current liabilities |

|

| 262,969 |

|

|

| 363,316 |

|

|

| 381,517 |

|

Total liabilities |

|

| 262,969 |

|

|

| 363,316 |

|

|

| 381,517 |

|

Total shareholders’ deficit |

|

| (206,766 | ) |

|

| (346,426 | ) |

|

| (366,938 | ) |

| 7 |

| Table Of Contents |

Selected Consolidated Statements of Cash Flows Data:

|

| For the Years Ended September 30, |

| |||||||||

|

| 2021 |

|

| 2020 |

|

| 2019 |

| |||

Net cash used in operating activities |

|

| (120,144 | ) |

|

| (65,681 | ) |

|

| (5,861 | ) |

Net cash used in investing activities |

|

| (20,687 | ) |

|

| - |

|

|

| - |

|

Net cash provided by financing activities |

|

| 120,634 |

|

|

| 66,604 |

|

|

| - |

|

Effect of exchange rate changes on cash and cash equivalents |

|

| 11,127 |

|

|

| 15,422 |

|

|

| (20 | ) |

Net (decrease) increase in cash |

|

| (9,070 | ) |

|

| 16,345 |

|

|

| (5,881 | ) |

Cash and cash equivalents, beginning of the year |

|

| 16,890 |

|

|

| 545 |

|

|

| 6,426 |

|

Cash and cash equivalents, end of the year |

|

| 7,820 |

|

|

| 16,890 |

|

|

| 545 |

|

B. | Capitalization and Indebtedness |

|

|

| Not applicable. |

|

|

C. | Reasons for the Offer and Use of Proceeds |

|

|

| Not applicable. |

D. | Risk Factors |

Investment in our ordinary shares involves a high degree of risk. You should carefully consider, among other matters, the following risk factors in addition to the other information in this annual report on Form 20-F when evaluating our business because these risk factors may have a significant impact on our business, financial condition, operating results or cash flow. If any of the material risks described below or in subsequent reports we file with the Securities and Exchange Commission (“SEC”) actually occur, they may materially harm our business, financial condition, operating results or cash flow. Additional risks and uncertainties that we have not yet identified or that we presently consider to be immaterial may also materially harm our business, financial condition, operating results or cash flow.

Risks Related to Our Business and Industry

We are exposed to the risks of an economic recession, credit and capital markets volatility and economic and financial crisis (including as a result of the COVID-19 virus pandemic), which could adversely affect the demand for our products and adversely affect the market price of our ordinary shares.

The COVID-19 pandemic has created unique global and industry-wide challenges, including challenges to our business. In early 2020, the COVID-19 pandemic resulted in the temporary closure of many corporate offices and schools across China. Given the strict quarantine measures put in place during this period, normal economic activity throughout China was sharply curtailed and normal in-school education was temporarily suspended. All of our revenues and our workforce are concentrated in China. Consequently, to the extent that COVID-19 exerts long-term negative impact on the Chinese economy, our results of operations and financial performance may be adversely affected

| 8 |

| Table Of Contents |

The COVID-19 virus pandemic has resulted in significant financial market volatility and uncertainty in recent months. The extent to which the COVID-19 impacts our results will depend on future developments, which are highly uncertain and will include emerging information concerning the severity of the COVID-19, the vaccine roll-out and actions taken by governments and private businesses to attempt to contain the coronavirus, A continuation or worsening of the levels of market disruption and volatility seen in the recent past could have an adverse effect on us.

Additionally, the pandemic may also affect our overall ability to react timely to mitigate the impact of this event and may hamper our efforts to provide our investors with timely information and comply with our filing obligations with the SEC, especially in the event of office closures, stay-in-place orders and a ban on travel or quarantines.

Significant uncertainties exist in relation to the interpretation and implementation of, or proposed changes to, the PRC laws, regulations and policies regarding the private education industry. In particular, our compliance with the Opinions on Further Alleviating the Burden of Homework and After-School Tutoring for Students in Compulsory Education and the implementation measures issued thereunder by the relevant PRC government authorities has materially and adversely affected and will materially and adversely affect our business prospect.

The PRC private education industry, especially the after-school tutoring sector, has experienced intense scrutiny and has been subject to significant regulatory changes recently. In particular, the Opinions on Further Alleviating the Burden of Homework and After-School Tutoring for Students in Compulsory Education jointly promulgated by the General Office of State Council and the General Office of Central Committee of the Communist Party of China on July 24, 2021, or the Alleviating Burden Opinion, sets out a series of operating requirements on after-school tutoring institutions, including, among other things, (i) local government authorities shall no longer approve any new after-school tutoring institutions providing tutoring services on academic subjects for students in compulsory education, or the Academic AST Institutions, and all the existing Academic AST Institutions shall be registered as non-profit, and local government authorities shall no longer approve any new after-school tutoring institutions providing tutoring services on academic subjects for pre-school-age children and students in grade ten to twelve; (ii) online Academic AST Institutions that have filed with the local education administration authorities will be subject to review and re-approval procedures by competent government authorities, and any failure to obtain such approval will result in the cancellation of its previous filing and ICP license; (iii) Academic AST Institutions are prohibited from raising funds by listing on stock markets or conducting any capitalization activities and listed companies are prohibited from investing in Academic AST Institutions through capital markets fund raising activities, or acquiring assets of Academic AST Institutions by paying cash or issuing securities; (iv) foreign capital is prohibited from controlling or participating in any Academic AST Institutions through mergers and acquisitions, entrusted operation, joining franchise or variable interest entities; (v) after-school tutoring institutions shall not provide tutoring services on academic subjects during national holidays, weekends and school breaks; (vi) no advertisements for after-school tutoring shall be published or broadcasted in the network platforms and billboards displayed in the mainstream media, new media, public place and residential areas; (vii) fees charged for academic subjects tutoring in compulsory education will need to follow the guidelines from the government to prevent any excessive charging or excessive profit-seeking activity; (viii) government authorities will implement risk management and control for the pre-collection of fees by after-school tutoring institutions with requirements such as setting up third-party custodians and risk reserves, and strengthen supervision over loans regarding tutoring services; and (ix) online tutoring for preschool-age children is prohibited, and offline academic subjects (including foreign language) tutoring services for preschool-age children is also strictly prohibited. The Alleviating Burden Opinion further provides that administration and supervision over academic subjects tutoring institutions for students on grade ten to twelve shall be implemented by reference to the relevant provisions of the Alleviating Burden Opinion. It remains uncertain as to how and to what extent the administration over academic subjects tutoring institutions for students in grade ten to twelve will be implemented by reference of the Alleviating Burden Opinion. Furthermore, on August 18, 2021, the Beijing Municipality Government and the Beijing Municipal Committee of the Communist Party of China jointly published the full text of the Beijing Municipality’s Measures to Further Reduce the Burden of Homework and After-School Tutoring on Students in Compulsory Education in Beijing, or the Beijing Measures, to implement the Alleviating Burden Opinion.

To implement the Alleviating Burden Opinion, on September 7, 2021, the Chinese Ministry of Education, or the MOE, published on its official website that the MOE, together with two other government authorities, issued a circular requiring all Academic AST Institutions to complete registration as non-profit by the end of 2021, and all Academic AST Institutions shall, before completing such registration, suspend enrollment of students and charging fees.

Our business prospect have been and will be materially and adversely affected by the actions we have taken to date and consider taking to be in compliance with the Alleviating Burden Opinion and its implementation measures. We are closely monitoring the evolving regulatory environment and are making efforts to seek guidance from and cooperate with the government authorities to comply with the Alleviating Burden Opinion and its implementation measures.

If we are unable to maintain a good relationship with China Mobile, our business will suffer.

China Mobile is the primary distribution, marketing, promotion and payment platform for UMFun. We generate substantially all of our users through the China Mobile “AND” Education Platform and expect to continue to do so for the foreseeable future. Any deterioration in our relationship with China Mobile would harm our business and adversely affect the value of our ordinary shares.

We are subject to China Mobile’s terms and conditions for application developers, which govern the promotion, distribution and operation of educational applications on the “AND” Education Platform. We have entered into a Product Co-operation Agreement with China Mobile, which governs the promotion, distribution and operation of educational applications on the “AND” Education Platform. This Agreement expired on October 31, 2021. There can be no assurance that China Mobile will renew this Agreement.

Our business would be harmed if:

| · | China Mobile discontinues or limits access to its platform by us; |

|

|

|

| · | China Mobile terminates or does not renew our Product Co-operation Agreement; |

|

|

|

| · | China Mobile modifies its terms of service or other policies, including fees charged to, or other restrictions on, us or other application developers, or China Mobile changes how the personal information of its users is made available to application developers on the “AND” Education Platform or shared by users; |

|

|

|

| · | China Mobile establishes more favorable relationships with one or more of our competitors; or |

|

|

|

| · | China Mobile develops its own competitive offerings. |

We have benefited from China Mobile’s strong brand recognition and large user base. If China Mobile loses its market position or otherwise falls out of favor with Internet users, we would need to identify alternative channels for marketing, promoting and distributing our products, which would consume substantial resources and may not be effective. In addition, China Mobile has broad discretion to change its terms of service and other policies with respect to us and other developers, and those changes may be unfavorable to us. China Mobile may also change its fee structure, add fees associated with access to and use of the “AND” Education Platform. Any such changes may harm our business.

Changes in the policies, guidelines or practice of mobile network operators or the PRC government with respect to mobile applications and other content may negatively affect our business operations for mobile applications.

| 9 |

| Table Of Contents |

We rely on PRC mobile network operators, directly and indirectly, to distribute our products to our users. The mobile telecommunication business in China is highly concentrated and major mobile network operators, such as China Mobile, may from time to time issue new policies or change their business practices, requesting or stating their preferences for certain actions to be taken by all mobile service providers using their networks. In addition, the PRC government may also implement new policies or change existing policies regulating the mobile telecommunication business. Such new policies or changes may negatively affect our business operations for mobile applications.

A significant portion of our revenues will be dependent on market acceptance of our online learning and assessment platform and other cloud-based testing technologies, and if we are unable to anticipate and meet our clients’ technological needs and challenges from new technologies and industry standards, our products and services may lose market acceptance or become obsolete, and our margins and results of operations may be adversely affected.

Our advanced technologies for the creation and delivery of online assessment, including our UMFun platform, are a key factor in growing and maintaining our relationships with educational institution clients and educational program content providers. Our future success depends on our ability to upgrade our systems, develop new technologies and anticipate and meet the technical needs of our clients on a regular basis. The emergence in the market of new test creation and delivery technologies or substitute products and services could reduce the competitiveness or result in the obsolescence of our current technologies and services. Moreover, if other companies develop similar technologies offering functionality comparable to that of our technologies, pricing pressure may increase, and our margins and results of operations may be adversely affected. Additionally, industry standards such as standard interfaces and data exchange protocols may be developed for testing technologies, and if these industry standards are incompatible with our technologies, demand for our technologies, products and services may decline significantly. To the extent we are unable to maintain our market position in key testing technologies or anticipate and respond to technological developments and changes in industry standards in a timely and cost-effective manner, our products and services may lose market acceptance or become obsolete.

Technical errors or failures in relation to cloud-based tests delivered through our delivery platform could result in negative publicity, loss of clients, liability claims and costly and disruptive litigation.

Due to the complexity of the technologies, we have developed and use to create and deliver cloud-based learning and assessment services for our clients, there is a risk that technical errors or failures may occur in relation to these services. These may include errors, failures or bugs in our self-developed software applications and test security technologies, breakdowns or failures of our servers and computer networks, and connectivity failures between our networks. While we have not experienced major problems to date due to errors, breakdowns, failures, bugs or defects, we cannot assure you that we will not experience such problems in the future. If such a problem were to occur, it could disrupt or compromise the integrity of the test-taking process or of test content and results, which could lead to negative publicity and loss of clients and may subject us to liability claims. Although we have established a formal crisis management system to respond to technical problems, it has never been tested in a real crisis situation. Any litigation or negative publicity resulting from an error or failure, with or without merit, could result in substantial costs and divert management’s attention and resources from our business and operations.

If we fail to maintain a strong brand identity, our business may not grow, and our financial results may be adversely impacted.

We believe that maintaining and enhancing the value of the “UMFun” brand is important to attracting clients. Our success in maintaining brand awareness will depend on our ability to consistently provide high quality, value-adding, user-friendly and secure products and services. To establish a significant recognition of our “UMFun” brand among schools, teachers, students and parents, we may need to spend significant resources on advertising. As we have limited experience with advertising and other activities required to establish a widely recognized brand, we cannot assure you that we will effectively allocate our resources for these activities or succeed in maintaining and broadening our brand recognition and appeal. If we fail to maintain a strong brand identity, our business may not grow and our financial results may be adversely impacted.

| 10 |

| Table Of Contents |

We have significant historical losses and may continue to incur losses in the future.

We have incurred annual operating losses since our inception. Consequently, as of September 30, 2021, we had an accumulated deficit of $30,992,977. Our revenues for the years ended September 30, 2021, 2020, and 2019 were $2,832, $4, and $113, respectively. Our revenues have not been sufficient to sustain our operations. In order to achieve profitability our revenue streams will have to increase and there is no assurance that revenues can increase to such a level. We may never be profitable. Our ability to achieve profitability is affected by various factors, including:

| - | growth of the online education market; |

| - | the continued growth and maintenance of our user base; |

| - | our efforts to sell and market our products through licensees, distributors and other partners; |

| - | our ability to establish partnerships and licensing arrangements; |

| - | the time and costs involved in obtaining regulatory approvals; |

| - | our ability to control our costs and expenses; and |

| - | the continued ability to source investments from our investors. |

| 11 |

| Table Of Contents |

Many of these factors are beyond our control. We may continue to incur net losses in the future due to our continued investments in content, bandwidth and technology. If we cannot successfully offset our increased costs with an increase in net revenues, our gross margin, financial condition and results of operations could be materially and adversely affected. We may also continue to incur net losses in the future due to changes in the macroeconomic and regulatory environment, competitive dynamics and our inability to respond to these changes in a timely and effective manner.

The Company has limited cash resources and a history of operating losses. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. We believe we have developed a viable plan to continue as a going concern. However, the plan relies upon our ability to obtain additional sources of capital and financing. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, we may be required to cease operations.

We face significant competition, and if we fail to compete effectively, we may lose our market share or fail to gain additional market share, and our profitability may be adversely affected.

We operate in a highly competitive market subject to rapid technological changes, and increasing competition could lead to pricing pressures, reduced operating margins, loss of market share and increased capital expenditures. The markets for our products and services are highly competitive, and we expect increased competition in the future that could adversely affect our revenue and market share. Our current competitors include but are not limited to:

| · | providers of online and offline supplemental instructional materials for the core subject areas of English language, mathematics and Chinese studies for K-12 institutions; |

|

|

|

| · | companies that provide K-12-oriented software and web-based educational assessment and remediation products and services to students, educators, parents and educational institutions; |

|

|

|

| · | providers of online and offline test preparation materials; |

|

|

|

| · | traditional print textbook and workbook companies that publish K-12 core subject educational materials, standardized test preparation materials or paper and pencil assessment tools; |

|

|

|

| · | summative assessment companies, which traditionally assess student learning at the end of a class period, that have expanded their line to include products that provide periodic assessment in the classroom to gauge student learning and inform instruction, also known as formative assessment; and |

|

|

|

| · | non-profit and membership educational organizations and government agencies that offer online and offline products and services, including in some cases at no cost, to assist individuals in standards mastery and test preparation. |

Some of our competitors may have more resources than we do, and several of the largest K-12 educational publishers may have more experience, larger customer bases and greater brand recognition in the markets we serve. Further, larger established companies with high brand recognition and extensive experience providing various educational products to the K-12 market may develop online products and services that are competitive with our core products and services. These competitors may be able to devote greater resources than us to the development, promotion and sale of their products and services and respond more quickly than we can to new technologies or changes in customer requirements or preferences. We may not be able to compete effectively with current or future competitors, especially those with significantly greater resources or more established customer bases, which may materially adversely affect our sales and our business.

| 12 |

| Table Of Contents |

Our failure to protect our intellectual property rights may undermine our competitive position, and litigation to protect our intellectual property rights or defend against third party allegations of infringement may be costly and ineffective.

We believe that our copyrights, trademarks and other intellectual property are essential to our success. We depend to a large extent on our ability to develop and maintain the intellectual property rights relating to our technology and products. We have devoted considerable time and energy to the development and improvement of our websites, our online platform and educational materials.

We rely primarily on copyrights, trademarks, trade secrets and other contractual restrictions for the protection of the intellectual property used in our business. Nevertheless, these provide only limited protection and the actions we take to protect our intellectual property rights may not be adequate. Our trade secrets may become known or be independently discovered by our competitors. Third parties have, in the past, pirated our courses, books and other course materials and may in the future infringe upon or misappropriate our other intellectual property. Infringement upon, or misappropriation of, our proprietary technologies or other intellectual property could have a material adverse effect on our business, financial condition or operating results. Policing the unauthorized use of proprietary technology can be difficult and expensive. Also, litigation may be necessary to enforce our intellectual property rights, protect our trade secrets or determine the validity and scope of the proprietary rights of others. The outcome of such potential litigation may not be in our favor and any success in litigation may not be able to adequately protect our rights. Such litigation may be costly and divert management’s attention away from our business. An adverse determination in any such litigation would impair our intellectual property rights and may harm our business, prospects and reputation. Enforcement of judgments in China is uncertain, and even if we are successful in litigation, it may not provide us with an effective remedy. In addition, we have no insurance coverage against litigation costs and would have to bear all costs arising from such litigation to the extent we are unable to recover them from other parties. The occurrence of any of the foregoing could have a material adverse effect on our business, financial condition and results of operations.

We have not registered copyrights for all of our products, which may limit our ability to enforce them.

We have not registered our copyrights in all of our software, written materials, website information, designs or other copyrightable works. Preventing others from copying our products, written materials and other copyrightable works is important to our overall success in the marketplace. In the event we decide to enforce any of our copyrights against infringers, we will first be required to register the relevant copyrights, and we cannot be sure that all of the material for which we seek copyright registration would be registrable in whole or in part, or that once registered, we would be successful in bringing a copyright claim against any such infringers.

We may be exposed to infringement claims by third parties or held liable for defamation or negligence to third parties for information displayed on, retrieved from or linked by our websites, for the content of the books and reference materials or marketing materials that we or our lecturers publish or distribute or for information delivered or shared through our services, which could disrupt our business and cause us to incur substantial legal costs, or damage our reputation.

We cannot assure you that our services and products do not or will not infringe any intellectual property rights held by third parties. We cannot assure you that in the future we will not receive claims of infringement of third parties’ proprietary rights or claims for indemnification resulting from infringement arising from our services or products. We may also become subject to claims that content on our websites or in the books and reference materials or marketing materials that we or our lecturers publish or distribute is protected by third parties’ copyrights or trademark.

In addition, as a provider of Internet content and other value-added telecommunications services, we may face liability for defamation, negligence and other claims based on the nature and content of the materials displayed on our websites or delivered or shared through our services. We could also be subject to claims based on content accessible on our websites or through our networks, such as content and materials posted by visitors on message boards, online communities, or emails. By providing hypertext links to third-party websites, we may be held liable for copyright or trademark violations by those third-party websites. Third parties could assert claims against us for losses incurred in reliance on any erroneous information distributed by us.

| 13 |

| Table Of Contents |

Royalty or licensing agreements, if required, may not be available on acceptable terms, if at all. A successful claim of infringement against us and our failure or inability to obtain a license to use the infringed or similar technology or content on commercially acceptable terms, or at all, could prevent us from producing and offering our services or products or cause us to incur great expense and delay in developing non-infringing services or products. Any of the above events could in turn have a material and adverse impact on our financial condition and results of operations. Any defamation or negligence claims against us, even if they do not result in liability to us, could cause us to incur significant costs in investigating and defending against these claims. We do not have general liability insurance to cover all potential claims to which we are exposed, and our insurance coverage may not be adequate to indemnify us from all liability that may be imposed.

Concerns about the security of our transaction systems and confidentiality of information on the Internet may reduce use of our services and impede our growth.

Public concerns over the security and privacy of electronic settlement, online transmittal and communications have to some extent constrained the rapid development and expansion of online transactions. If these concerns are not adequately addressed, they will restrict the growth of value-added telecommunications services generally and in particular the use of the Internet as a means of conducting commercial transactions. If a well-publicized breach of security were to occur, general usage of value-added telecommunications services could decline, which could reduce our visitor traffic and the number of course participants, and impede our growth. We are continuously vigilant about protecting and improving our cyber security and have not experienced any material cyberattacks on our information technology systems. We cannot assure you, however, that our current security measures will be adequate or sufficient to prevent any theft or misuse of personal data of our course participants. Further, security breaches could expose us to litigation and possible liability for failing to secure confidential customer information, and could harm our reputation and ability to attract or retain course participants. In addition, we do not have any cyber security insurance coverage for our operations, and any material cyberattack on our information technology systems and our online education websites could expose us to substantial costs and losses.

We are subject to currency fluctuations, which may affect our results.

The majority of our expenses and some of our debts are in Chinese Renminbi, Canadian dollars and U.S. dollars, while our revenues are primarily in Chinese Renminbi. We also incur expenses in Hong Kong dollars related to our Hong Kong subsidiary. The fluctuation of the Canadian dollar, Hong Kong dollar and U.S. dollar vis-a-vis the Chinese Renminbi could materially impact our operating results and financial position.

We will require additional financing to sustain our operations, and our ability to secure additional financing is uncertain.

We may be unable to raise on acceptable terms, if at all, the substantial capital resources necessary to conduct our operations. If we are unable to raise the required capital, we may be forced to curtail business development activities and, ultimately, cease operations. As at September 30, 2021, we had working capital deficiency of $226,006 as compared to working capital deficiency of $346,426 as at September 30, 2020. The independent auditor’s report for the year ended September 30, 2021 includes an explanatory paragraph stating that our recurring losses from operations and working capital levels raise substantial doubt about our ability to continue as a going concern.

| 14 |

| Table Of Contents |

We may be unable to retain key employees or recruit additional qualified personnel.

Because of the specialized educational nature of our business, we are highly dependent upon qualified educational, technical, and managerial and marketing personnel. There is competition for qualified personnel in our business. Therefore, we may not be able to attract and retain the qualified personnel necessary for the development of our business. The loss of the services of existing personnel, as well as the failure to recruit additional key educational, technical, and managerial personnel in a timely manner would harm our research and development programs and our business.

Risks Relating to Our Corporate Structure and Restrictions on Our Industry

We do not have direct ownership of our VIEs in China and rely on VIE Agreements with our VIEs for our business operations, which may not be as effective in providing operational control or enabling us to derive economic benefits as through ownership of controlling equity interests.

We do not have direct ownership of our VIEs in China and rely on and expect to continue to rely on the VIE Agreements with our VIEs in China and their respective shareholders to operate business. VIE Agreements may not be as effective as an ownership of controlling equity interests would be in providing us with control over the VIEs, or in enabling us to derive economic benefits from the operations of, the affiliated consolidated entities. Under the current VIE Agreements, as a legal matter, if any of the affiliated consolidated entities or any of their shareholders fails to perform its, his or her respective obligations under the VIE Agreements, we may have to incur substantial costs and resources to enforce such arrangements, and rely on legal remedies available under PRC laws, including seeking specific performance or injunctive relief, and claiming damages, which we cannot assure you will be effective. For example, if shareholders of a variable interest entity were to refuse to transfer their equity interests in such variable interest entity to us or our designated persons when we exercise the purchase option pursuant to these contractual arrangements, we may have to take a legal action to compel them to fulfill their contractual obligations.

If (i) the applicable PRC authorities invalidate these contractual arrangements for violation of PRC laws, rules and regulations, (ii) any variable interest entity or its shareholders terminate the contractual arrangements or (iii) any variable interest entity or its shareholders fail to perform their obligations under these contractual arrangements, our business operations in China would be materially and adversely affected, and the value of your stock would substantially decrease. Further, if we fail to renew these contractual arrangements upon their expiration, we would not be able to continue our business operations unless the then current PRC law allows us to directly operate businesses in China.

In addition, if any VIE or all or part of its assets become subject to liens or rights of third-party creditors, we may be unable to continue some or all of our business activities, which could materially and adversely affect our business, financial condition and results of operations. If any of the VIE undergoes a voluntary or involuntary liquidation proceeding, its shareholders or unrelated third-party creditors may claim rights to some or all of these assets, thereby hindering our ability to operate our business, which could materially and adversely affect our business and our ability to generate revenues.

All of VIE Agreements are governed by PRC law and provide for the resolution of disputes through arbitration in the PRC. The legal environment in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. In the event we are unable to enforce these contractual arrangements, we may not be able to exert effective control over our operating entities and we may be precluded from operating our business, which would have a material adverse effect on our financial condition and results of operations.

If the PRC government determines that the agreements that establish the structure for operating our business in China are not in compliance with applicable PRC laws and regulations, we could be subject to severe penalties.

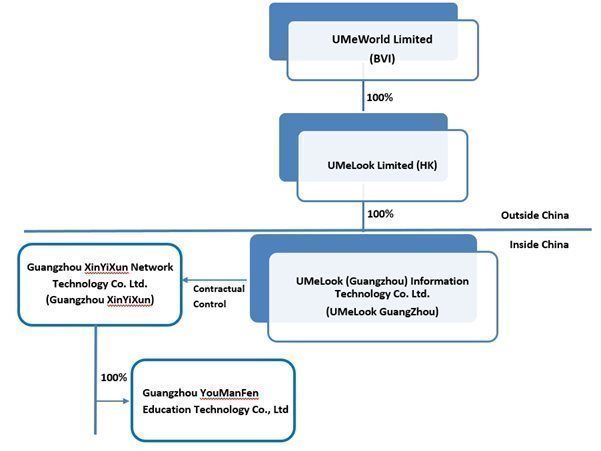

PRC laws and regulations currently require any foreign entity that invests in the education business in China to be an educational institution with relevant experience in providing education services outside China. None of our offshore holding companies is an educational institution or provides education services. To comply with PRC laws and regulations, we have entered into (i) a series of contractual arrangements among UMeLook (Guangzhou) Information Technology Co. Ltd. (“UMeLook Guangzhou”), Guangzhou XinYiXun Network Technology Co. Ltd. (“Guangzhou XinYiXun”) and their respective shareholders. Accordingly, Guangzhou XinYiXun is our VIE, and we rely on the contractual arrangements with our VIE and their respective shareholders, or the VIE Contractual Arrangements, to conduct most of our services in China.

We have been and are expected to continue to be dependent on our VIE in China to operate our education business until we qualify for direct ownership of educational businesses in China. Pursuant to the VIE Contractual Arrangements, we, through our wholly owned subsidiaries in China, exclusively provide comprehensive intellectual property licensing, technical and business support services to UMeLook Guangzhou and Guangzhou XinYiXun, our Consolidated Affiliated Entities in exchange for payments from them. In addition, the VIE Contractual Arrangements provide us with the ability to effectively control our VIE and its respective existing and future subsidiaries and schools, as applicable.

It is uncertain whether any new PRC laws, rules or regulations relating to variable interest entity structures will be adopted or if adopted, what they would provide. In August 2018, the Ministry of Justice published a draft Implementation Rules for Private Education Law, or the draft Implementation Rules, for review. The draft Implementation Rules, among other things, provide that entities implementing group-based education shall not control non-profit schools by merger, acquisition, franchise or contractual arrangements. The draft Implementation Rules also provide that transactions among private schools and their affiliates shall be fair and open to public. For those agreements entered into by non-profit schools and their affiliates which is long-term or involving important interests or repeated performance, the educational authorities shall audit the necessity, legitimacy and legal compliance of such agreements. Such requirements, if remained in the final version and signed into law, may challenge the validity and enforceability of our VIE Contractual Arrangements.

If the corporate structure and contractual arrangements through which we conduct our business in China are found to be in violation of any existing or future PRC laws or regulations, or such arrangements are determined as illegal and invalid by PRC courts, arbitration tribunals or regulatory authorities, or if we fail to obtain or maintain any of the required permits or approvals, we would be subject to potential actions by the relevant PRC regulatory authorities with broad discretion, which actions could include:

| 15 |

| Table Of Contents |

| · | revoke our business and operating licenses; |

|

|

|

| · | require us to discontinue or restrict our operations; |

|

|

|

| · | limit our business expansion in China by way of entering into contractual arrangements; |

|

|

|

| · | restrict our right to collect revenues or impose fines; |

|

|

|

| · | block our websites; |

|

|

|

| · | require us to restructure our operations in such a way as to compel us to establish a new enterprise, re-apply for the necessary licenses or relocate our businesses, staff and assets; |

|

|

|

| · | impose additional conditions or requirements with which we may not be able to comply; or |

|

|

|

| · | take other regulatory or enforcement actions against us that could be harmful to our business. |

Any of these actions could cause significant disruption to our business operations and severely damage our reputation, which would in turn materially and adversely affect our business, financial condition and results of operations. If any of these actions results in our inability to direct the activities of our Consolidated Affiliated Entities that most significantly impact their economic performance, and/or our failure to receive the economic benefits from our Consolidated Affiliated Entities, we may not be able to consolidate these entities in our consolidated financial statements in accordance with U.S. GAAP. However, we do not believe that such actions would result in the liquidation or dissolution of our company, our wholly owned subsidiaries in China or our VIE.

Our contractual arrangements may be subject to national security review under PRC laws and regulations and, thus, be challenged by relevant regulatory authorities.

On February 3, 2011, the General Office of the State Council issued the Circular of the General Office of the State Council on the Establishment of Security Review System for Foreign Investors’ Merger and Acquisition of Domestic Enterprises (the “Circular on the Establishment of Security Review”), which became effective on March 4, 2011. Among other things, the Circular on the Establishment of Security Review stipulates that the scope of the security review lies in foreign investors’ acquisition of domestic military enterprises, military-related enterprises, enterprises involving sensitive military facilities and other enterprises that impact national defense security; foreign investors’ acquisition of domestic enterprises which may provide foreign investors with de facto control over industries relating to national security, such as important agricultural products, energy and natural resources, infrastructures, transportation services, technologies and major equipment manufacturing. On August 25, 2011, the Ministry of Commerce issued the Circular of the Ministry of Commerce on the Implementation of Security Review System for Foreign Investors’ Merger and Acquisition of Domestic Enterprises (the “Circular on the Implementation of Security Review”), which became effective on September 1, 2011. Among other things, the Circular on the Implementation of Security Review further specifies that whether a foreign investors’ acquisition of domestic enterprises falls within the scope of the security review depends on the said transaction’s substantive content and practical influence. Foreign investors shall not circumvent the security review through any arrangements or schemes, including but not limited to trust, lease and/or contractual arrangements.

According to our PRC counsel, as our contractual arrangements were established in 2013, the new security review system may apply to our contractual arrangements. We cannot guarantee, however, that the Ministry of Commerce will not promulgate additional implementing rules or new rules that will bring our contractual arrangements under the scope of the security review system. Moreover, according to a press conference held by the Ministry of Commerce on September 20, 2011, there are no specific laws or regulations governing contractual arrangements like the ones that we employ, but the Ministry of Commerce together with other authorities would study how to regulate them in the future. Hence, we cannot assure you that our contractual arrangements will not be subject to new regulations that will be issued by relevant regulatory authorities and that such new regulations will not have a material adverse effect on our existing structure.

| 16 |

| Table Of Contents |

We rely on the VIE Contractual Arrangements for our PRC operations, which may not be as effective in providing operational control as direct ownership.

We have relied and expect to continue to rely on the VIE Contractual Arrangements to operate our education business in China. See “Item 4.C. - Information on the Company - Organizational Structure - VIE Contractual Arrangements.” The VIE Contractual Arrangements may not be as effective in providing us with control over our Consolidated Affiliated Entities as direct ownership. If we had direct ownership of the Consolidated Affiliated Entities, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of these entities, which in turn could effect changes, subject to any applicable fiduciary obligations, at the management level. However, under the VIE Contractual Arrangements, we rely on the performance by our Consolidated Affiliated Entities and their respective shareholders of their obligations under the contracts to exercise control over and receive economic benefits from our Consolidated Affiliated Entities.

Any changes in the PRC foreign investment legal regime may materially and adversely affect our operations and the contractual arrangements.

In January 2015, the Ministry of Commerce, or MOC, published a discussion draft of the proposed Foreign Investment Law for public review and comments, and on March 15, 2019, the Foreign Investment Law was promulgated and implemented on January 1, 2020. The draft Foreign Investment Law expanded the definition of foreign investment and introduced the principle of “actual control” in determining whether a company is considered a foreign-invested enterprise, or an FIE. Under the draft Foreign Investment Law, variable interest entities would also be deemed as FIEs, if they are ultimately “controlled” by foreign investors, and be subject to restrictions on foreign investments. However, the draft law did not take a position on what actions will be taken with respect to the existing companies with the “variable interest entity” structure, whether or not these companies are controlled by Chinese parties. The final Foreign Investment Law does not include the contractual control concept from the 2015 draft and so the government’s view on variable interest entities continues to be unclear. The Foreign Investment Law also retains a comprehensive oversight over all “foreign investors who invest in China through laws, administrative regulations or other methods prescribed by the State Council”. Foreign investment refers to any investment activity directly or indirectly carried out by foreign natural persons, enterprises, or other organizations, including investment in new construction project, establishment of foreign funded enterprise or increase of investment, merger and acquisition, and investment in any other way stipulated under laws, administrative regulations, or provisions of the State Council. Accordingly, it cannot be ruled out that the National People’s Congress or relevant departments may introduce a series of related supporting policies in the future to resolve any ambiguity on the application of the Foreign Investment Law.

If the ownership structure, contractual arrangements and business of our company or any of our Consolidated Affiliated Entities are found to be in violation of any existing or future PRC laws or regulations, or we fail to obtain or maintain any of the required permits or approvals, the relevant governmental authorities would have broad discretion in dealing with such violation, including levying fines, confiscating our income or the income of our Chinese subsidiaries and VIE, revoking the business licenses or operating licenses of our Chinese subsidiaries or VIE, discontinuing or placing restrictions or onerous conditions on our operations, requiring us to undergo a costly and disruptive restructuring, restricting or prohibiting our use of proceeds from our offerings to finance our business and operations in China, and taking other regulatory or enforcement actions that could be harmful to our business. Any of these actions could cause significant disruption to our business operations and severely damage our reputation, which would in turn materially and adversely affect our business, financial condition and results of operations. If any of these occurrences results in our inability to direct the activities of our VIE, and/or our failure to receive economic benefits from our VIE, we may not be able to consolidate their results into our consolidated financial statements in accordance with U.S. GAAP.

| 17 |

| Table Of Contents |

We may rely on dividends and other distributions on equity paid by our PRC subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our PRC subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business.

We are a holding company, and we may rely on dividends and other distributions on equity paid by our PRC subsidiaries for our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders and service any debt we may incur. If our PRC subsidiaries incur debt on their own behalf in the future, the instruments governing the debt may restrict their ability to pay dividends or make other distributions to us. In addition, the PRC tax authorities may require UMeLook Guangzhou to adjust its taxable income under the contractual arrangements it currently has in place with our PRC consolidated VIE in a manner that would materially and adversely affect its ability to pay dividends and other distributions to us.

Under PRC laws and regulations, our PRC subsidiaries, which are wholly foreign-owned enterprises may pay dividends only out of their respective accumulated profits as determined in accordance with PRC accounting standards and regulations. In addition, a wholly foreign-owned enterprise is required to set aside at least 10% of its accumulated after-tax profits each year, if any, to fund a certain statutory reserve fund, until the aggregate amount of such fund reaches 50% of its registered capital. At its discretion, a wholly foreign-owned enterprise may allocate a portion of its after-tax profits based on PRC accounting standards to an enterprise expansion fund, or a staff welfare and bonus fund. The statutory reserve funds, enterprise expansion funds and staff welfare and bonus funds are not distributable as cash dividends.

Any limitation on the ability of our PRC subsidiaries to pay dividends or make other distributions to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends, or otherwise fund and conduct our business.

Our contractual arrangements may be subject to scrutiny by the PRC tax authorities, and a finding that we owe additional taxes could substantially reduce our consolidated net income and the value of your investment.

Under PRC laws and regulations, arrangements and transactions among related parties may be subject to audit or challenge by the PRC tax authorities. We could face material and adverse tax consequences if the PRC tax authorities determine that the contractual arrangements among our PRC subsidiary and our PRC consolidated VIE do not represent an arm's-length price and adjust our PRC consolidated VIE's income in the form of a transfer pricing adjustment. A transfer pricing adjustment could, among other things, result in a reduction, for PRC tax purposes, of expense deductions recorded by our PRC consolidated VIE, which could in turn increase their tax liabilities. In addition, the PRC tax authorities may impose late payment fees and other penalties to our PRC consolidated VIE for under-paid taxes. Our consolidated net income may be materially and adversely affected if our tax liabilities increase or if we are found to be subject to late payment fees or other penalties.

The Chinese government exerts substantial influence over the manner in which we must conduct our business activities. We are currently not required to obtain approval from Chinese authorities to list on U.S exchanges nor the execution of VIE Agreements, however, if our VIE or the holding company were required to obtain approval in the future and were denied permission from Chinese authorities to list on U.S. exchanges, we will not be able to continue listing on U.S. exchange, continue to offer securities to investors, or materially affect the interest of the investors and cause significantly depreciation of our price of Ordinary Shares.

The Chinese government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulation and state ownership. Our ability to operate in China may be harmed by changes in its laws and regulations, including those relating to taxation, environmental regulations, land use rights, property and other matters. The central or local governments of these jurisdictions may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations. Accordingly, government actions in the future, including any decision not to continue to support recent economic reforms and to return to a more centrally planned economy or regional or local variations in the implementation of economic policies, could have a significant effect on economic conditions in China or particular regions thereof, and could require us to divest ourselves of any interest we then hold in Chinese properties.

For example, the Chinese cybersecurity regulator announced on July 2, 2021, that it had begun an investigation of Didi Global Inc. (NYSE: DIDI) and two days later ordered that the company’s app be removed from smartphone app stores. As such, the Company’s business segments may be subject to various government and regulatory interference in the provinces in which they operate. The Company could be subject to regulation by various political and regulatory entities, including various local and municipal agencies and government sub-divisions. The Company may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply.

Furthermore, it is uncertain when and whether the Company will be required to obtain permission from the PRC government to list on U.S. exchanges or enter into VIE Agreements in the future, and even when such permission is obtained, whether it will be denied or rescinded. Although the Company is currently not required to obtain permission from any of the PRC federal or local government to obtain such permission and has not received any denial to list on the U.S. exchange and or enter into VIE Agreements, our operations could be adversely affected, directly or indirectly, by existing or future laws and regulations relating to our business or industry.

Risks Related to Our Ordinary Shares

The market price of our ordinary shares is volatile.

The market price of our ordinary shares has been, and we expect it to continue to be, highly unstable. Factors, including our announcement of technological improvements or announcements by other companies, regulatory matters, research and development activities, new or existing products or procedures, signing or termination of licensing agreements, concerns about our financial condition, operating results, litigation, government regulation, developments or disputes relating to agreements, patents or proprietary rights, and public concern over the safety of activities or products have had a significant impact on the market price of our stock. We expect such factors to continue to impact our market price for the foreseeable future.

| 18 |

| Table Of Contents |

Our ordinary shares are classified as "penny stock" under SEC rules that may make it more difficult for our shareholders to resell our ordinary shares.

Our ordinary shares are traded on the OTC Market. As a result, the holders of our ordinary shares may find it more difficult to obtain accurate quotations concerning the market value of the ordinary shares. Shareholders also may experience greater difficulties in attempting to sell the shares than if there were listed on or quoted on a national stock exchange. Because our ordinary shares are not traded on a national stock exchange , and the market price of our ordinary shares is less than $5.00 per share, our ordinary shares are classified as "penny stock." Rule 15g-9 of the Securities Exchange Act of 1934 imposes additional sales practice requirements on broker-dealers that recommend the purchase or sale of penny stocks to persons other than those who qualify as an "established customer" or an "accredited investor." This includes the requirement that a broker-dealer must make a determination that investments in penny stocks are suitable for the customer and must make special disclosures to the customer concerning the risks of penny stocks. Application of the penny stock rules to our ordinary shares could adversely affect the market liquidity of the shares, which in turn may affect the ability of holders of our ordinary shareholders to resell the shares. We have a significant number of options and warrants outstanding that could be exercised in the future. Subsequent resales of these and other shares could cause our share price to decline. This could also make it more difficult to raise funds at acceptable levels, via future securities offerings.

We have identified material weaknesses in our internal control over financial reporting. If we fail to develop and maintain an effective system of internal control over financial reporting, we may be unable to accurately report our financial results or prevent fraud, and investor confidence and the market price of our ordinary shares may be materially and adversely affected.

We have identified “material weaknesses” and other control deficiencies including significant deficiencies in our internal control over financial reporting. As defined in the standards established by the Public Company Accounting Oversight Board of the United States, or PCAOB, a “material weakness” is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the annual or interim financial statements will not be prevented or detected on a timely basis.

One material weakness that has been identified related to our lack of sufficient financial reporting and accounting personnel with appropriate knowledge of U.S. GAAP and SEC reporting requirements to properly address complex U.S. GAAP accounting issues and to prepare and review our consolidated financial statements and related disclosures to fulfill U.S. GAAP and SEC financial reporting requirements. As our operations continue to expand, we plan to hire additional accounting and finance staff to increase segregation of duties and also invest in technology infrastructure to support our financial reporting function. Despite all these remedial measures, we might efficiently address the weaknesses we have identified.

We are subject to the Sarbanes-Oxley Act of 2002. Section 404 of the Sarbanes-Oxley Act, or Section 404, requires that we include a report from management on the effectiveness of our internal control over financial reporting in our annual report on Form 20-F beginning with this report. In addition, once we cease to be an “emerging growth company” as such term is defined in the JOBS Act, our independent registered public accounting firm must attest to and report on the effectiveness of our internal control over financial reporting. Our management may conclude that our internal control over financial reporting is not effective. Moreover, even if our management concludes that our internal control over financial reporting is effective, our independent registered public accounting firm, after conducting its own independent testing, may issue a report that is qualified if it is not satisfied with our internal controls or the level at which our controls are documented, designed, operated or reviewed, or if it interprets the relevant requirements differently from us. In addition, after we become a public company, our reporting obligations may place a significant strain on our management, operational and financial resources and systems for the foreseeable future. We may be unable to timely complete our evaluation testing and any required remediation.

| 19 |

| Table Of Contents |

During the course of documenting and testing our internal control procedures, in order to satisfy the requirements of Section 404, we may identify other weaknesses and deficiencies in our internal control over financial reporting. In addition, if we fail to maintain the adequacy of our internal control over financial reporting, as these standards are modified, supplemented or amended from time to time, we may not be able to conclude on an ongoing basis that we have effective internal control over financial reporting in accordance with Section 404. If we fail to achieve and maintain an effective internal control environment, we could suffer material misstatements in our financial statements and fail to meet our reporting obligations, which would likely cause investors to lose confidence in our reported financial information. This could in turn limit our access to capital markets, harm our results of operations, and lead to a decline in the trading price of our ordinary shares. Additionally, ineffective internal control over financial reporting could expose us to increased risk of fraud or misuse of corporate assets and subject us to potential delisting from the stock exchange on which we list, regulatory investigations and civil or criminal sanctions. We may also be required to restate our financial statements from prior periods.

Lack of independent directors

We cannot guarantee that our Board of Directors will have a majority of independent directors in the future. In the absence of a majority of independent directors, our executive officers, who are also shareholders and directors, could establish policies and enter into transactions without independent review and approval thereof. This could present the potential for a conflict of interest between us and our shareholders generally and the controlling officers, stockholders or directors.

Ownership of our ordinary shares by current officers and directors.