UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No.

(Exact name of registrant as specified in its charter) |

| ||

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

| ||

(Address of Principal Executive Offices) |

| (Zip Code) |

(

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $.0001 per share |

(Title of Class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirement for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period the registrant was required to submit such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§232.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10K. Yes ☐ No ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock held by non-affiliates computed by reference to the price at which the common stock was last sold as of June 30, 2022 was $

The number of shares of the registrant’s common stock outstanding as of March 31, 2023 was

Documents Incorporated by

Reference None

TABLE OF CONTENTS

CORRELATE INFRASTRUCTURE PARTNERS INC.

INDEX

| Page Numbers | |

|

| |

1 | ||

18 | ||

34 | ||

34 | ||

34 | ||

34 | ||

|

| |

35 | ||

| [Reserved] | 35 | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 36 | |

38 | ||

39 | ||

| F-1 | |

| F-3 | |

| F-4 | |

| Consolidated Statements of Changes in Stockholders’ Equity (Deficit) | F-5 |

| F-6 | |

| F-7 | |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 40 | |

40 | ||

41 | ||

|

|

42 | ||

48 | ||

Security Ownership and Certain Beneficial Owners and Management and Related Stockholder Matters | 49 | |

Certain Relationships and Related Transactions and Director Independence | 50 | |

50 | ||

|

| |

51 | ||

| 52 |

i |

PART I

Forward Looking Statements

This annual report on Form 10-K includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which can be identified by the use of forward-looking terminology such as “may,” “can,” “believe,” “expect,” “intend,” “plan,” “seek,” “anticipate,” “estimate,” “will,” or “continue” or the negative thereof or other variations thereon or comparable terminology. All statements other than statements of historical fact included in this annual report on Form 10-K, including without limitation, the statements under “Item 1. Business” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” and located elsewhere herein regarding the financial position and liquidity of the Company (defined below) are forward- looking statements. Although the Company believes the expectations reflected in such forward-looking statements are reasonable, it can give no assurance that such expectations will prove to have been correct. Important factors with respect to any such forward- looking statements, including certain risks and uncertainties that could cause actual results to differ materially from the Company’s expectations (“Cautionary Statements”), are disclosed in this annual report on Form 10-K, including, without limitation, in conjunction with the forward-looking statements and under the caption “Risk Factors.” In addition, important factors that could cause actual results to differ materially from those in the forward-looking statements included herein include, but are not limited to, limited working capital, limited access to capital, changes from anticipated levels of sales, future national or regional economic and competitive conditions, changes in relationships with customers, difficulties in developing and marketing new products, marketing existing products, customer acceptance of existing and new products, , technological change, dependence on key personnel, availability of key component parts, vendors, contractors, product liability, delays and disruptions in the shipment of the Company’s products, and the ability of the Company to meet its stated business goals. All subsequent written and oral forward-looking statements attributable to the Company or persons acting on its behalf are expressly qualified in their entirety by the Cautionary Statements. We do not undertake to update any forward-looking statements.

Our periodic reports, proxy statements and Reports on Form 8-K are not currently on our website, however, our reports are available on the SEC’s EDGAR system and may be viewed at http://www.sec.gov.

Item 1. Business

Our Business

Correlate Infrastructure Partners Inc., together with its subsidiaries (collectively the “Company”, “Correlate”, “we”, “us” and “our”), is a technology-enabled vertically integrated sales, development, and fulfillment platform focused on distributed clean and resilient energy solutions North America.

We focus on real estate assets that have a complex energy profile, but do not have the resources of time, expertise, or capital available to invest in technology and sustainable infrastructure upgrades that will improve the net operating income (NOI) and resiliency of those properties. Complexities can stem from building and property owners having a large portfolio of sites in different locations, or a single location that has a variety of different business processes, operations, and equipment that require a wide skillset of expertise to continually optimize (such as achieving the ISO 50001 standard).

We provide property owners and REITs access to a multitude of energy experts and solutions via a lean software-driven process, with end-to-end engineering, finance, project management, and fulfillment services for all major facility energy improvements. Through our proven processes, we manage client opportunities with the correct experts, solutions, and execution resources across their entire portfolio to help our clients achieve their sustainability mandates, ensure facility uptime, and/or improve bottom line operating margins. The Company leverages on-demand and in-house experts with leading-edge, proven technology to turn our clients drive for a competitive edge into a comprehensive energy optimization and management program. Each custom program can significantly lower our client’s energy usage, costs, and carbon footprint, thereby improving NOI and providing our clients more flexibility to focus and invest in other areas of their businesses.

The Company is also involved in the development of microgrid infrastructure opportunities in areas that cannot be properly served by centralized electrical infrastructure. These reasons include a lack of grid capacity or transmission infrastructure, lack of funding available for new buildouts, or long lead times for electricity to be delivered by the utilities. Microgrids are emerging as a flexible approach to deploying distributed energy resources that can meet the electricity needs of existing communities and new developments without necessarily being connected to the power grid.

| 1 |

| Table of Contents |

Behind this platform is a team of multi-decade industry experts in renewable energy generation, efficiency technology, software development, project finance, supply chain, and construction. The Company’s team is comprised of serial entrepreneurs and innovators that have built some of the leading companies in the clean energy space, including technology-based startups and F500 divisions. Our CEO, Todd Michaels has been in the solar industry since 2005 formerly as VP of Product Innovations at SunEdison, Senior Director – Distributed Solar at NRG Energy (NYSE: NRG), and SVP of Project Development and Marketing at Solar Power Partners (acquired by NRG Energy in 2011). Our CFO, Channing Chen has 16 years of experience and formerly held executive management roles at Solar Power Partners where he was a founding employee, SunEdison, NRG Energy (NYSE: NRG) and was the founder of Breakaway Energy Partners, LLC – a distributed energy financing and market-making platform. Jason Loyet, our Director of Commercial Solar has over 20 years in the cleantech industry and was a US Department of Energy SunShot Catalyst award winner for his work building the Solar Site Design technology platform. Our chief revenue officer Dave Bailey brings over 15 years of executive sales, supply chain management, and energy efficiency experience from Wesco’s Distributed Energy Resource division (formerly Westinghouse) and GE Supply.

We believe that building and property owners will choose our services for actionable, cashflow-positive / NOI improving energy programs. Furthermore, states are setting renewable portfolio standards and goals, in addition to the critical and significant underlying carbon reduction mandates taking effect in the US and beyond. Finally, with environmental, social, and governance (ESG) mandates increasingly becoming a priority for businesses, we believe that we are well-positioned to be one of the premier net-zero carbon, smart building platform sources in the United States.

Market Opportunity

Solar deployment in the US, relative to other energy sources, has reached a tipping point, where in 2022 solar PV accounted for over 50% of new generating capacity brought online. Yet market penetration still remains below 5%. We believe that a software-centered, asset-light development and financing business model that is focused on continuous design and process improvement will allow solar to achieve large-scale adoption.

The Energy Information Administration (EIA) estimates that there are 6 million commercial buildings in the US. This sector is the largest single consumer of energy in the country – using over $2 trillion of energy each year. The EIA and DOE estimate that up to 30%, or approximately $600 billion, is wasted through inefficiencies, representing 15% of greenhouse gas emissions, according to industry experts. According to the U.S. Green Building Council, as of 2022, only 100,000 buildings in the country have a Leadership in Energy and Environmental Design (LEED) certification, a global rating system that acts as a framework to guide energy efficiency, among others. While energy upgrades have real, tangible results, this reveals that a majority of buildings still lack energy programs. According to the US Department of Energy (DOE), some of the primary barriers that prevent businesses from adopting energy measures include lack of funding, perceived insufficient return of investment, lack of the ability to investigate and implement projects, and lack of general knowledge and technical expertise to implement and maintain such projects. Despite the hesitancy of building and property owners to investigate and implement such projects, we believe that opportunities for improved energy efficiency, lower costs, and lower carbon emissions are enormous, and there are favorable market conditions that point towards market opportunities for us to significantly grow our business. For instance, rapid technological advancements and decreasing costs have driven renewable energy as the second-most widespread electricity source in the country. The US Energy Information Administration (EIA) reports that renewable energy reached a record high of 14% of total energy consumption in 2022 (latest data available). Among renewable energy sources, solar power has become the most predominant, with solar power capacity growing from just 0.34 GW in 2008 to approximately 142.3 GW in 2022, per Solar Energy Industries Association (SEIA). When it comes to commercial building retrofits, the Rocky Mountain Institute estimates that portfolio energy optimization is a $290 billion market in the US, driving deep financial savings and energy efficiency across the commercial sector.

At the same time, the US is powering itself with clean, renewable energy to strategically phase out carbon pollution by 2050. The US government has recently outlined long-term goals to cut emissions by 50% to 52% by 2030 based on 2005 levels and accomplishing a net zero economy by 2050. States and local governments are also taking action to phase out carbon pollution. There are 38 states and the District of Columbia that have renewable portfolio standards (RPS) and in 12 of those states (plus DC), the requirement is for 100% clean energy by 2050 or earlier. More than 2,000 businesses and financial institutions have partnered with the Science Based Targets initiative (SBTi) to reduce their emissions in line with climate science; meanwhile, over 400 corporations worldwide are working with RE100, a corporate initiative of businesses committed to 100% renewable energy. With massive market demand for carbon reduction and energy optimization, we believe that our scalable offerings are well- positioned to meet these goals.

| 2 |

| Table of Contents |

Our Solutions

Our management team understands the barriers that are prohibiting the scalable deployment of distributed energy solutions and has developed innovative processes and tools targeted at bulk real estate owners, educating them on the financial benefits of energy projects, allowing them to compare potential energy upgrade options, and facilitating the actual implementation of the retrofit measures via attractive turnkey offerings with no-money down, 100% funding options. We also provide custom solutions for energy contractors to more efficiently target potential clients and offer more compelling energy services – fully funded and easy to comprehend.

We use software to bring together energy project development, institutional project financing, and certified installers into a process that is standardized with strong quality, investment grade controls. This ‘market-making’ model allows us to optimize and keep fixed costs low which, in turn, leads to high scalability and improved pricing for consumers while preserving financial returns to project investors and lenders. We do not need to subsidize the marketplace as there are already large pools of installers who need more consistent, quality work.

Our Proprietary Customer Acquisition Tool

We use our proprietary customer acquisition processes and online project development platform to generate a regular flow of qualified energy project opportunities. Expensive customer acquisition is one of the major barriers to entry in the distributed energy industry which we believe our process addresses and helps to sustain profitability and standardization. We aggregate the project data entered by regional energy professionals and connect the projects to our approved centralized engineers and analysts to finalize the design and explore financing options for the site, thereby reducing customer development costs and increasing close rates. By leveraging a collaborative marketplace model, we are also able to provide clients with additional energy services and additional sources of revenue for the Company.

An Integrated Platform for Deploying Commercial Energy Solutions at Scale

Our platform was created by a team of clean energy pioneers. The innovative platform, tools, and business model were developed as a result of the team's average 20+ years of experience with energy customers and countless "voice of the customer" research engagements. The service was officially created after the results of a business model innovation project at SunEdison made it clear that any strategic energy plan requires end users to have the resources to create, implement, and manage an ongoing plan, regardless of the magnitude of the economic opportunity. These insights — combined with additional research efforts conducted by California investor-owned utilities for their energy efficiency business plans, from DNV GL, and other entities — informed the need for a platform to connect on-demand energy managers with end users of energy and develop a streamlined software workflow process based on the ISO 50001 framework for Strategic Energy Management (aka Energy Management System).

Our management team has conducted over 100 structured interviews with energy product/service providers to understand the challenges they are facing with the commercialization, deployment, and financing of their products and services. Our research was focused on gaining insights into six key areas: priority initiatives, success factors, perceived barriers, decision criteria, buying influencers, and resources that buyers trust. We have used the results of our research to create three target buyer profiles and have been designing and adjusting our go-to market, product, and pricing strategies around the target buyer’s specific needs. We believe that we have either significantly mitigated or removed risks for customers to highly prioritize and execute on their sustainability initiatives based on direct customer feedback. Contracts, pricing, and payment programs have also been created based on this feedback.

Technology Capabilities

The Company leverages a cloud-based, energy project platform designed to streamline, accelerate, and scale retrofit projects in commercial and industrial buildings. The platform uses advanced energy retrofit simulation and algorithms to manage the entire energy retrofit cycle: origination, building energy performance assessment, project development, project financing, implementation oversight, and ongoing monitoring. This technology stack typically reduces project transaction costs and execution timeline by a factor of five, and thus, is particularly well-suited for medium-sized commercial buildings.

Our central management platform is a SaaS-based Building Relationship Manager (BRM) that connects data and solution applications for up to 90% faster energy decisions. As disparate data, products, and applications make energy-related decision-making exceedingly difficult in buildings, our platform solves that problem by bringing all data points and applications into a single platform, making building energy analysis more actionable. The platform is open and standards-based, allowing us to have digital relationships with customers, partners, and utilities throughout the US.

Our services have already been deployed across more than 30 major US metropolitan areas. We have processed and completed project simulations and use cases on more than 250,000 buildings (representing over 15 billion sq ft of real estate) resulting in more than $11 billion in annual energy savings opportunities identified. We are leveraging our platform to catalyze energy retrofits in owner occupied buildings and those owned by REITs. Our bulk portfolio analysis is similar to a “Zillow for energy projects" in buildings through its ability to model properties with five basic inputs. We will increasingly adapt and simplify the user interface (UI), user experience (UX) and workflows to make them more compelling to non-energy expert stakeholders (such as SMBs), and breakdown the retrofit value proposition and business case in terms that resonate directly with the owners’ key business metrics, such as savings as a percent of profit margins, or improving bottom line net operating income (NOI).

| 3 |

| Table of Contents |

Our Process

Correlate uses its complete building energy model to rapidly create a best-fit solution bundle for each of the buildings in a given territory. The Company uses a database of building data archetypes derived from the US Department of Energy’s Commercial Reference Building Models. With this model, and a handful of building physical characteristics, the Company rapidly creates an initial assessment of current building energy performance. The data points – exact address, building use, square footage, number of floors, and year built – are enhanced by other data such as building codes, weather, energy prices, rebates, and grid programs.

Correlate creates solution scenarios with a business case for each and in aggregate as a bundle – efficiency, solar, storage, EV infrastructure, and other grid revenue opportunities. Appropriate financing based on the asset owners’ goals will be included to eliminate the need for upfront capital and remove performance risk.

Correlate automatically drives contract level pricing on the created building model to simulate and match each measure in its solution library to estimate the cost, energy savings, payback period, internal rate of return, carbon savings, and NOI. These measures include solar, plus upgraded HVAC systems, installation of ground or air source heat pumps, lighting upgrades, smart thermostats/controls, or real time energy management systems. The library was developed by multiple research projects and initiatives, including the DOE Building Component, the LBNL Commercial Building Energy Saver, and the Commercial Buildings Sector Agent-Based Model (CoBAM), a project of Georgia Institute of Technology and Argonne National Laboratory.

Step-by-Step Sale to Project Completion Process

The customer engagement process begins by benchmarking and prioritizing goals of our potential customer, followed by acquiring building data to analyze energy consumption to quickly identify savings (and hence, improved NOI) with intelligent machine learning. By analyzing and comparing data, numerous incentives are created through this process.

At its core, the Company uses a physics-based hourly building energy simulation model to create a “digital twin” of each building in its database. The model is used throughout the process to originate, develop, finance, and deliver retrofit projects to building owners meeting precise metrics. We provide end-to-end building energy analytics to support the development, financing, and ongoing monitoring of building energy retrofit projects. Once a lead is acquired, the following illustrates the project development workflow of our systems-based approach:

| - | Building Energy Performance Assessment – the user provides energy use information, minimum of one complete bill for each energy meter. We then adjust the calibration of the building model to benchmark and assess the overall building energy performance; |

| - | Progressive Energy Audit – the user responds to a simple online remote audit survey designed for non-energy professionals. The information is automatically reflected into our building energy model and facility database; |

| - | Retrofit Simulation – Based on information collected from the remote audit, our proposed retrofit options are recalculated, review for QA by a human expert, and presented to the opportunity lead. ESP and solutions vendors can further refine the analysis after their on-site visit to refine the scoping and make a more formal proposal to the facility owner; |

| - | Project Risk Assessment – For projects requiring third party owned financing solutions, a risk assessment provides technical due diligence capability to evaluate the uncertainty of the proposed savings measures, credit and regulatory risks; |

| - | Financing and Performance Assurance – We have developed a network of financing partners to cater to most financing needs of retrofit projects (PPA, PACE, ESA, fixed payments as a service and loans). Based on contract type, additional performance assurance plans are available from third-parties; |

| - | Measurement and Verification (M&V) – We provide M&V tools to automatically determine the baseline and run the monthly performance to forecast; |

| - | Ongoing Monitoring and Maintenance – We conduct continuous, ongoing monitoring and maintenance of all building retrofit projects. |

| 4 |

| Table of Contents |

Business Model

The majority of our revenues are generated by leveraging third party origination programs using the Company’s platform and in-house end-to-end development and fulfilment resources. Referral only organizations will be paid a commission for each transaction that we install and complete. Upon a customer’s acceptance of our recommended solution and funding package, we generate all of the required contracts through our system, where clients sign digitally, and any deposit or milestone payment can be collected online or via wire. We generate revenue through the following models:

Revenue Stream | Pricing |

Project Development and Sale | 15-45% Gross Margin |

Project Energy Services (Own/Operate) | Recurring Contracted cash flows |

Future Revenue (e.g. Grid Services) | TBD |

| 5 |

| Table of Contents |

Acquisition and Growth Strategy

The Company actively seeks to acquire private companies that can complement its business model, grow pipeline, bring critical execution capabilities, and contribute to EBITDA. Potential acquisition targets will include specialized software companies that help further scale aspects of project development, financing, supply chain management, and unique regional fulfillment needs.

Value Proposition to the Building Owner

We offer a multi-value proposition to building owners, as set forth below:

| 6 |

| Table of Contents |

Industry Performance and Outlook

Renewable energy has become the second-most prevalent electricity source in the US. Rapid technology advancements and decreasing costs of renewable energy resources, along with the increased competitiveness of battery storage, have made renewables one of the most competitive energy sources.

The industry has moved past the supply chain constraints, increased shipping costs, and rising commodity prices experienced during the Covid-19 pandemic (2020-2021). Furthermore, in 2022 the Inflation Reduction Act of 2022 was signed into Law, providing increased federal tax incentives for renewable energy projects.

Many cities, states, and utilities in the US are setting ambitious clean energy goals, increasing renewable portfolio standards, and enacting energy storage procurement mandates. Furthermore, more than 4,500 businesses and financial institutions worldwide are working with the Science Based Targets initiative (SBTi) to reduce their emissions in line with climate science.

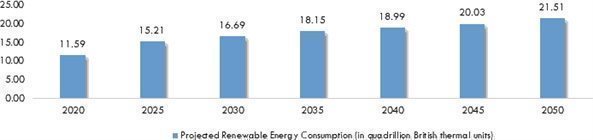

Renewable Energy Consumption in the US 2020-2050 (US Energy Information Administration)

Renewable energy growth is poised to accelerate in 2023 and beyond, as concern for climate change and support for environmental, sustainability, and governance (ESG) considerations grow, along with accelerated demand for cleaner energy sources from most market segments. At the same time, federal and state mandates are helping spur activity in the renewable sector that will likely drive further growth. By 2025, the EIA projects that approximately 15.21 quadrillion Btu of renewable energy are expected to be consumed in the US. And by 2050, this could reach 21.51 quadrillion Btu, almost doubling the estimated renewable energy consumed in 2020.

Solar is the Fastest Growing Generation Resource

Solar power is more affordable, accessible, and prevalent in the US than ever before. From just 0.34 gigawatts (GW) in 2008, solar power capacity has grown to an estimated 142.3 (GW) today, as per the SEIA. This is enough to power the equivalent of 25 million average American homes. To add, over 3.4% of US electricity comes from solar energy in the form of solar photovoltaics (PV) and concentrating solar-thermal power (CSP). Since 2014, the average cost of solar PV panels has dropped nearly 70% and markets for solar energy are maturing rapidly around the US since solar electricity is now economically competitive with conventional energy sources in most states.

It is estimated that solar PV panels on just 22,000 square miles of the nation’s total land area – about the size of Lake Michigan – could supply enough electricity to power the entire country. Solar panels can also be installed on rooftops with essentially no land use impacts, and it is projected that more than 1 in 7 homes will have a rooftop solar PV system by 2030. The EIA, in a December 2021 report, said it projects the US will add about 78 GW of new electricity generation capacity in 2022 through year-end 2023. The agency said 62% of that total, or about 49 GW, will come from large-scale solar power and energy storage projects. This means 2023 could well see the industry growing solar-plus-storage buildouts, exploring floating solar PV modules, and expanding community solar projects to new markets. Pairing storage with solar offers cost synergies, operational efficiencies, and the opportunity to reduce storage capital costs with the solar investment tax credit.

Moreover, the solar market is a proven incubator for job growth throughout the nation. Further data from DOE shows that solar jobs in the US have increased 167% over the past decade, which is 5 times faster than the overall job growth rate in the US economy. There are more than 255,000 solar workers in the US in fields spanning manufacturing, installation, project development, trade, distribution, and more.

| 7 |

| Table of Contents |

Clean Energy Goals Boost Commercial Solar Demand

EIA’s Commercial Buildings Energy Consumption Survey estimated that there were 6 million commercial buildings in the US in 2018, and this sector accounts for about 76% of electricity use and 40% of all US primary energy use and associated greenhouse gas (GHG) emissions. In 2019, only 69,066 buildings had a Leadership in Energy and Environmental Design (LEED) certification – one of the most commonly used green building rating systems in the world. Developed by the US Green Building Council, this system acts as a framework to guide buildings when it comes to energy efficiency, among other cost-saving standards.

Further data from EIA shows that while large buildings (greater than 100,000 square feet, such as high-rise office buildings) represent just 2% of US commercial buildings, they represent nearly 35% of the US commercial building stock floor area, and they are more likely to have smart building technology components such as distributed energy resources. Small and medium buildings (100,000 square feet or smaller) represent nearly 98% of US commercial buildings and typically lack smart building technologies. This shows that a majority of commercial buildings still lack energy projects, and therefore represent a large market opportunity for the Company. Particularly, the portfolio energy optimization market, according to Rocky Mountain Institute, is a $290 billion opportunity in the US.

Buildings Sector: A Snapshot

Expected Growth in Corporate Investments

Environmental, social, and governance (ESG) has emerged as a major influence on corporate policies and practices as businesses and investors are increasingly called upon to address topics such as sustainability and environmental equity, among others. As a result, many large companies are pledging to utilize renewable energy. Climate change is having a major effect on the ways businesses plan, assess risk, and deploy resources, and investors are now asking how businesses are reducing their carbon footprint. These initiatives are fueling the dramatic growth of renewable energy, especially investment in solar power. As a result, total corporate spending for solar projects, including venture capital funding and debt financing, reached $24.1 billion in 2022 according to Mercom Capital.

Furthermore, a 2022 survey completed by Net Zero Tracker found that more than a third of publicly-traded companies have net zero targets, up from only one-fifth in 2020. This trend is only expected to grow, as net-zero initiatives become more critical to an organization’s longevity. Energy cost savings, increasing energy security, and customer attraction / retention are the biggest drivers of investment.

Reasons for Investment in Smart Building Technologies (Johnson Controls Energy Efficiency Indicator Survey, 2020)

Rated as ‘extremely or very significant’ by organizations

Energy cost savings |

|

| 85 | % |

Increasing energy security |

|

| 75 | % |

Customer attraction / retention |

|

| 73 | % |

Enhanced brand or reputation |

|

| 72 | % |

Improving operational efficiency |

|

| 70 | % |

Government / utility incentives / rebates |

|

| 69 | % |

Increasing building resilience |

|

| 69 | % |

Greenhouse gas footprint reduction |

|

| 68 | % |

| 8 |

| Table of Contents |

Clean Energy Commitments and Initiatives

In 2022, more than 4,500 businesses and financial institutions (including American Express, Owens Corning, Molson Coors, BNSF Railway, etc.) are working with the Science Based Targets initiative (SBTi) to reduce their emissions in line with climate science. Additionally, 60% of Fortune 500 companies (2020) have set a climate or energy-related commitment. This represents a 12% increase from 2017. While renewable generation is an essential strategy for these companies to meet their climate and sustainability promises, energy efficiency solutions are expected to be the single largest strategy to reduce their emissions and carbon footprint, as per EIA.

Also, as of March 2022, approximately 400 corporations worldwide have joined RE100 and have made a commitment to go 100% renewable. According to RE100, if the current roster of RE100 members were a country, they would be the 21st largest electricity consumer in the world – bigger than South Africa. In December of 2021, President Biden signed an Executive Order that directed the Federal Government to use its scale and procurement power to achieve 100% carbon pollution-free electricity by 2023 with half to be locally supplied clean energy, 100% zero-emission vehicle acquisitions by 2035, net-zero emissions from Federal procurement, net-zero emissions building portfolio by 2045, and net-zero emissions from overall Federal operations by 2050 including a 65% emissions reduction by 2030.

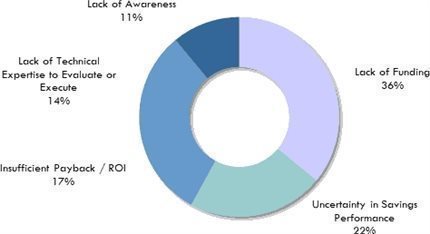

Barriers to Renewable Energy Technologies

Renewable energy has overcome numerous barriers to become competitive with coal, natural gas, and nuclear power. Nonetheless, renewables still face major obstacles when it comes to adoption. Data from Johnson Controls shows the leading deterrents to successful smart building carbon reduction programs. In order to solve these issues, the Company’s solutions involve no money upfront (100% financing), deployment of energy managers and resources, performing detailed analytics, and continuous performance monitoring, among others. By providing a solution to these deterrents, we believe that our solutions unlock significant opportunities that exist in renewable energy.

Lack of Funding / Uncertainty in Savings Performance

The most obvious and widely publicized barrier to renewable energy is capital costs, or the upfront expense of building and installing solar farms. According to McKinsey, a holistic US Energy efficiency program would yield gross energy savings worth more than $1.2 trillion, well above the $520 billion needed for upfront investment in efficiency measures. Such a program is estimated to reduce end use energy consumption by 9.1 quadrillion Btus, roughly 23% of projected demand, abating up to 1.1 gigatons of greenhouse gases annually. Like most renewables, solar is exceedingly cheap to operate – its “fuel” is free, and maintenance is minimal – so the bulk of the expense comes from building the technology.

According to the Solar Energy Industries Association (SEIA), commercial solar panel systems cost an average of $1.45 per watt as of Q3 2022. For example, a factory with a system size of 350 kW would cost around $507,500. Limited access to commercial financing has long been recognized by experts to be one of the major barriers to implementing energy efficiency projects. Competing for financing with other core business investment projects, energy efficiency projects often rank low on the priority lists of high-level private sector managers or investors. Higher construction costs also make financial institutions more likely to perceive renewables as risky, lending money at higher rates, and making it harder for utilities or developers to justify the investment. Funding can be difficult to secure and as a result can deter building owners, however, the Company has the ability to provide financing options for 100% of the project costs with no out-of-pocket cost to building owners leveraging experience from the solar industry where power purchase agreements (PPAs) have helped drive the rapid adoption of commercial solar since 2005.

| 9 |

| Table of Contents |

Reasons Smart Building Carbon Reduction Programs Fail (Johnson Controls Energy Efficiency Indicator Survey, 2020)

Perceived Insufficient Payback / ROI

A common barrier in the utility sector is the perception that energy efficiency actions will reduce a company’s revenue. Businesses also face uncertainty about how long it will take to pay back their energy investments. While true in some cases, energy efficiency programs can help electricity companies better manage peak demand and also defer the need for investing in new power infrastructure, and thus can be very profitable for electricity companies. The Company’s solutions also provide recommendations such as short, medium, and long-term pay back with ROI scenarios to make it extremely transparent and easy for our clients to understand and analyze the benefits of our product offerings and programs.

Lack of Technical Expertise to Evaluate or Execute

Since renewable energy technology is comparatively new and not optimally developed, there is a lack of knowledge about operation and maintenance. Efficiency cannot be achieved if a system is not optimally operated and if maintenance is not carried out regularly. We quickly identify and analyze energy savings potential, helping building owners determine current building performance, benchmarking, and retrofit plans.

Lack of Awareness

Approximately 11% of respondents to the Johnson Controls survey pointed to a general lack of awareness of the importance, benefits, and potential of renewable energy both among the general public and major stakeholders, thus constraining rapid adoption. There is often a lack of awareness of the cost of solar systems in particular, and many operators assume they are cost prohibitive without understanding ROI benefits.

Expanding Government Energy Policies

A combination of federal incentives, state policies, and market conditions have accelerated increases in renewable electricity generation, and is expected to drive demand for the Company’s services. For example, the US has recently set long-term goals to reach net zero emissions by 2050. As part of this initiative, the US will not only move to 100% clean energy, but will also prioritize clean fuels like hydrogen and biofuels where needed, cut energy waste, reduce methane and non-carbon emissions, and scale up carbon removal. Additionally, the current administration plans to cut emissions from 50% to 52% by 2030 based on 2005 levels, achieving total carbon free power by 2035 and achieving a net zero economy by 2050.

Building Energy Codes Program

Some commercial and/or residential construction codes mandate certain energy performance requirements for the design, materials, and equipment used in new construction and renovation. The DOE’s Building Energy Codes Program, for instance, aims to improve building energy efficiency, and to help states achieve maximum savings. This program assesses the savings impacts of model energy codes, calculating energy, cost, and carbon savings, and coordinates with key stakeholders to improve model energy codes, including architects, engineers, builders, code officials, and a variety of other energy professionals.

| 10 |

| Table of Contents |

According to the US Government, energy codes for residential and commercial buildings are projected to save $138 billion in energy costs, 900 MMT of avoided Co2 emissions, and 13.5 Btus of primary energy (cumulative 2010-2040). These savings equate to the annual emissions of 195 million passenger vehicles, 227 coal power plants, and 108 million homes.

States’ Renewable Portfolio Standards and Goals

As of the end of 2021, 31 states and the District of Columbia had established renewable portfolio standards (RPS) or renewable goals, and in 12 of those states (and the District of Columbia), the requirement is for 100% clean electricity by 2050 or earlier. Designed to increase the use of renewable energy sources for electricity generations, state RPS programs vary widely in terms of program structure, enforcement mechanisms, size, and application. According to EIA, states have generally met their interim RPS targets in recent years, with only a few exceptions reflecting unique, state-specific policy designs. Roughly half of all growth in US renewable electricity generation and capacity since 2000 is associated with state RPS requirements. Nationally, the role of RPS policies represented about 23% of all US renewable electricity capacity additions in 2019. Within particular regions – especially the Northeast – RPS policies continue to serve a central role in motivating growth in renewable electricity generation.

California’s RPS Milestones – In California, the state’s ambitious RPS was established in 2002 and requires that by 2020, at least 33% of all electricity flowing into households and commercial buildings should be sourced from renewable energy. According to the Natural Resources Defense Council (NRDC), billion-dollar renewable energy investments in the state has created more than 100,000 jobs as early as 2015. In 2021, Los Angeles Times reported that the state hit nearly 95% of its renewable energy goals – supplying power to over 6.4 million homes and reducing harmful carbon emissions by over 21 million metric tons annually. The program is growing so fast in part because of the measurable economic benefits. Through the end of 2020, participants collectively saved nearly

$1.2 billion. These efforts are widely supported by Californians. 83% of California residents support setting a target for the state to generate 50% of its electricity from renewable resources.

A number of factors helped create an environment favorable for RPS compliance, including RPS-qualified generation projects that take advantage of federal incentives; reductions in the cost of renewable technologies; complementary state and local policies that either reduce costs or increase revenue streams associated with RPS-eligible technologies. States have adopted a number of other policies to support greater investment in the adoption of renewable energy, including Public Benefits Funds for Renewable Energy, Output–Based Environmental Regulations, Interconnection Standards, Net Metering, Feed-In Tariffs, and programs by the US EPA.

The Future is Renewable

The Solar Market Insight Report ranks the top states across the country based on the total amount of solar electric capacity installed and in operation as of the end of the first quarter of 2021. To put into context, SEIA figures also include the equivalent number of homes that can be powered by that solar capacity in the individual state. Here are the current leaders for solar power in the US:

Top Solar Energy States (Solar Market Insight Report, 2021)

State | Cumulative Solar Capacity (Megawatts) | Equivalent Number of Homes Supplied |

California | 31,873 | 8,548,370 |

Texas | 9,311 | 1,082,407 |

North Carolina | 7,132 | 859,707 |

Florida | 7,074 | 842,897 |

Arizona | 5,247 | 810,751 |

Nevada | 3,904 | 672,707 |

New Jersey | 3,653 | 586,709 |

Massachusetts | 3,263 | 545,258 |

Georgia | 3,069 | 359,160 |

New York | 2,840 | 474,848 |

While California has dominated the US solar market, other markets are continuing to expand rapidly and are emerging solar hotbeds. For instance, some smaller Northeastern states, like Massachusetts and New Jersey, are emerging solar states. The above leaderboard shows that it is not just about land space and the natural sunshine; the policies and economics driving these installations are just as impactful.

We believe that as the price of solar continues to fall, new state entrants will grab an increasingly larger share of the national market. In order to illustrate this opportunity, the table below shows the states that have adopted official zero-GHG or 100% renewable energy goals for their power sector or whole economy.

| 11 |

| Table of Contents |

100% Clean Energy States

| Power Sector | Whole Economy | |||||

State | 100% Renewable Energy | Zero GHG | Zero GHG | ||||

| Executive Order | Legislation | Board Decision | Executive Order | Legislation | Executive Order | Legislation |

California |

|

|

|

| 2045 | 2045 | |

Colorado |

|

|

|

| 2050 |

| |

Connecticut |

|

|

| 2040 |

|

| |

Washington, DC |

| 2032 |

|

|

|

| |

Hawaii |

| 2045 |

|

|

|

| |

Illinois |

|

|

|

| 2050 |

| |

Louisiana |

|

|

|

|

| 2050 | |

Maine |

| 2050 |

|

|

|

| |

Massachusetts |

|

|

|

|

|

| 2050 |

Michigan |

|

|

|

|

| 2050 |

|

Nebraska |

|

|

| 2050 |

|

|

|

Nevada |

|

|

|

| 2045 |

|

|

New Jersey |

|

|

|

| 2040 |

|

|

New Mexico |

|

|

|

| 2050 |

|

|

New York |

|

|

|

| 2040 |

|

|

North Carolina |

|

|

|

|

|

|

|

Oregon |

|

|

|

|

|

|

|

Rhode Island | 2030 |

|

|

|

|

|

|

Virginia |

|

|

|

| 2050 |

|

|

Washington |

|

|

|

| 2045 |

|

|

Wisconsin |

|

|

| 2050 |

|

|

|

Target Market Demographics

We operate on a nationwide basis, with an emphasis on the Northeast region, California, and Hawaii. States in the Northeast have a long history of climate leadership from strengthening renewable energy standards, to reducing power sector emissions and modernizing transportation systems. In fact, all 9 states in the region have an RPS and are part of the Regional Greenhouse Gas Initiative (RGGI), which serves to reduce global warming pollution from power plants through implementation of a carbon cap-and-trade system.

Companies and investors in the region want to see smart policy solutions that will help them meet their climate goals, improve public health, create jobs, and cut costs for businesses and communities alike.

The Northeast leads the nation in electricity consumption and in the adoption of renewables; however, there is still room for growth in these states. With over 2.1 million businesses across the region, we believe that we are properly positioned to capitalize on and address this market.

Northeast Region Demographics

State | % Renewable Electricity | Compliance Year | Total Households | Total Businesses |

Maine | 40% | 2017 | 587,633 | 55,990 |

New Hampshire | 25% | 2025 | 557,262 | 67,388 |

Rhode Island | 16% | 2019 | 422,324 | 38,757 |

Massachusetts | 15% | 2020 | 2,699,633 | 279,800 |

Vermont | 20% | 2017 | 265,838 | 31,695 |

Connecticut | 27% | 2020 | 1,388,735 | 166,088 |

New Jersey | 22.5% | 2021 | 3,321,271 | 315,982 |

Pennsylvania | 18% | 2021 | 5,163,155 | 457,737 |

New York | 29% | 2015 | 7,482,516 | 708,406 |

| 12 |

| Table of Contents |

Regional Opportunities

To meet 2030 emissions targets, at least 35% of the Northeast region’s power generation needs to come from renewable sources such as solar and wind. Including hydroelectricity, 57% of the Northeast's energy must be renewable by 2030. In a report, the Pace Energy and Climate Center has identified two key opportunities for growth in the region.

| · | The Northeast United States buys a large volume of voluntary green power, but does not supply much of it. This suggests an opportunity to capture private investment dollars and emissions reductions that are currently leaving the region. The disparity between sales and supply in the region highlights the low impact of voluntary demand on renewable energy development in the Northeast. However, renewable energy generators in the Northeast can participate in both RPS and voluntary markets for renewable energy, and there are many examples of facilities that currently supply both. Renewable energy generators can move between markets, which allows them to maximize prices and manage volatility. |

|

|

|

| · | Corporate procurement of renewable energy is a major potential driver for renewable energy development in the Northeast region, as it is across the country. Many large companies have the interest and ability to develop projects themselves, directly finance or invest in construction of new renewable capacity, or enter into long-term PPAs with new suppliers. These companies are motivated by corporate social responsibility commitments, the demands of their customers, and, increasingly, energy cost savings. In the Northeast, these companies can take advantage of currently high renewable energy credit (REC) prices by “arbitraging” the RECs from the projects – that is, selling the RECs from the Northeast project into local compliance markets and then purchasing cheaper RECs from outside the region. Depending on the price differential between the sold and replacement RECs, this can substantially lower the cost of renewable energy for these companies, while producing primary- tier local supply in the Northeast. |

Competitive Strengths

Our competitive strengths include the following:

| - | Low-Cost Origination with Ongoing Upsell: We have an extensive referral partner network that brings us qualified leads keeping our cost of customer acquisition low. Our referral partner network includes original equipment manufacturers (OEMs), industry consultants, facility management providers, and industry peers. Additionally, since we stay with the customer’s facility over a multi-year contract, subsequent sales are very low cost and can be coordinated on a timely basis based on market and facility conditions we actively monitor. Our programs facilitate rapid engagements and get facilities to take action to manage their energy. Our tools are also used by our third-party Energy Service/Product providers to unlock their regional markets and historic client base. We believe that this provides an aggregation that further reduces our costs and increases the velocity of our growth for our ecosystem model. |

|

|

|

| - | Simple, Transparent, Turnkey Customer Experience (Efficiency, Generation, EVs): When a client opts-in to our program services you gain access to a multitude of products, services, and installation capacity via a lean software driven process. Facility surveys, analytics, engineering, finance, project management and fulfillment services are all provided from one source for all major energy improvements. We address heating, cooling and lighting solutions, with clean onsite generation, that allows us to reach for Net Zero goals, while supporting new electric vehicle infrastructure growth. Industry standard is separating providers by solution, forcing clients to manage multiple relationships, sort through complex proposals, and manage challenging contractors through completion. Our proactive management and monitoring systems address these issues allowing facility owners to focus on their core business as we provide a transparent turnkey experience for them. |

|

|

|

| - | Competition Across All Supply Chains: We are not tied to any particular product, equipment type, technology or project finance fund, allowing us to seek the best partner and supplier for each project to our advantage. A majority of facility owners and our clients put a premium on the disaggregation of our products and services for pricing transparency, but seek integrated solutions with a single, simple interface that we provide. Our ability to drive competition across the full supply chain from materials and labor, to project capital given our scale and diverse project portfolio provides a consistent margin advantage. Our best-in-class procurement software further drives competition, decisions, insights, and speed to completion of client projects over time. |

|

|

|

| - | Highly Scalable National Development to Regional/Local Installation: Our team is comprised of multi-decade industry experts in sales, technology, project finance, supply chain, and construction. Our team includes serial entrepreneurs and innovators that have built and scaled leading companies in the clean energy space. We believe that we have achieved the optimal the balance between sophisticated, shared, centralized, remote development resources that then leverage local fulfilment teams across the diverse national US markets. We optimize for margin, risk, and customer satisfaction for each opportunity by market. |

|

|

|

| - | Consistent Ongoing Customer Management via Software Driven Process: We provide unique tools and simple reports online for clients that make clear the benefits, timelines, actions, and approvals required upfront and overtime. Our software and solutions allow us to streamline our processes and services without the need for a large-scale customer support staff to manage hundreds of new locations per year. Our internal staff uses customized, best in class customer engagement methods and support software to quickly and accurately respond to current and potential clients. |

| 13 |

| Table of Contents |

Commitment to Environmental, Social and Governance Leadership

We believe that leadership in environment, social and governance (“ESG”) issues is central to our mission of creating a clean electrification ecosystem and driving the clean energy transition of our customers across the United States. We have taken and plan to continue to take steps to address the environmental and social risks and opportunities of our operations, services and products. As our ESG efforts progress, we plan to report how we oversee and manage ESG factors and evaluate our ESG objectives by using industry- specific frameworks such as the Sustainability Accounting Standards Board (“SASB”) and elements of the United Nations Sustainable Development Goals (“UN SDGs”). We plan to organize our ESG initiatives into three pillars, which, in turn, will contain focus areas for our attention and action:

| · | Our Environmental Pillar is focused on providing clean, affordable energy to our customers; maintaining a robust environmental management program that ensures we protect the environment, including in the communities where we operate; and helping to make our energy infrastructure more sustainable and resilient; |

|

|

|

| · | Our Social Pillar is expected to focus on attracting and retaining the best talent and offering opportunities to progress their careers; ensuring a safety-first workplace for our employees through proper training, policies and protocols; and supporting ethical supply chains through our Supplier Code of Conduct; and |

|

|

|

| · | Our Governance Pillar is expected to focus on ensuring Board oversight and committee ownership of our enterprise risk management and sustaining a commitment to ethical business conduct, transparency, honesty and integrity. |

All of our actions and each of our ESG pillars are, or are expected to be, underpinned by our vision to put clean energy in every business, every home and every electric vehicle.

Sales and Marketing

The Company’s goal is to position itself as the most reliable and capable tech-enabled clean energy optimization provider nationwide. The Company will utilize a cohesive client acquisition strategy, involving the use of direct and online marketing channels and tactics to position itself appropriately to its target market. A large portion of this strategy will be driven by direct business development initiatives and strategic partnerships. Each of the Company’s marketing initiatives will be tailored over time to best attract the most ROI, while positioning itself as a major force in the renewable energy space, as well as in the commercial buildings sector, in the US and beyond. We intend to achieve these goals by utilizing the following marketing channels and tactics.

Marketing Strategies

| 14 |

| Table of Contents |

Business Development

The Company’s business development strategies involve creating a brand that will drive potential clients in need of the Company’s services to reduce their energy consumption patterns. Specifically, this process includes attracting prospective commercial property owners, building engagement, then converting these opportunities into clients. Once clients have been on-boarded onto the platform, the process begins to devise measures to help them optimize their energy consumption sustainably, and, where applicable, recommend clean energy generation opportunities.

| · | Medium-sized business facility owners will be invited to enter their address (if in the database, the basic information about their property will populate; if not, they will be prompted to enter size in square feet, number of floors, year built, property use), and submit energy bills for at least one month (to allow calculation of energy use intensity for their specific property). |

|

|

|

| · | For larger businesses, Correlate will offer the option of a paid turnkey project development, orchestration, and delivery service at a low cost to the owner (“concierge service” for solution discovery and transaction execution). |

Strategic Partnerships

The Company promotes its brand to potential partners such as energy service/product providers for indirect channel, local and national energy service/product providers, utilities, non-profit efficiency organizations, and local governments. For example, Correlate is partnered with the Alaska Center for Energy and Power and the Alaska Energy Authority; they have used the Company’s subscription service to efficiently gain engagement from business energy consumers. As with any marketing intensive business, the Company will benefit from participating in a number of corporate collaboration or networking opportunities that have the potential to yield new clients as well as further develop existing ones.

Word-of-Mouth and Referrals

Correlate will also leverage word-of-mouth marketing and referrals in order to build trust and reliability amongst potential partners and clients. Satisfied clients are drawn to discuss their experience with using the Company’s services among their peers, family, business partners, and other acquaintances. We believe that this will result in new client acquisition for Correlate.

Website

Correlate has a dedicated website located at www.correlateinfra.com featuring cohesive information about the Company’s solutions, technology, portfolio, testimonials, and more. The Company will continue to engage in digital marketing initiatives to ensure its website shows up anytime a user searches for any relevant keywords on search engines.

SEO & PPC

Correlate will implement an aggressive search engine optimization (SEO) strategy, whereby the Company will optimize its content using keywords related to its energy optimization solutions. By creating website content related to its target keywords, the Company will organically aggregate higher on Google, Bing, and Yahoo search engines when users search for such keywords, thus increasing website traffic.

The Company will potentially pursue a pay-per-click (PPC) advertising campaign in which it can pay additional funds for visible ads on search engines like Google and Bing. These campaigns target high search volume terms relevant to the business that will drive traffic to the website.

Social Media

A solid online social media presence represents an inexpensive promotional and informational marketing strategy. In turn, the Company will operate and post via its various social media platforms, with a focus on the LinkedIn community. Social media posts, while less official, are a great venue for more creative presentations of the Correlate brand. Real-time updates on these sites seek to keep clients informed of company updates, special promotions, partnership activity, and more.

Supply Chain

We along with our partners purchase equipment, including solar panels, inverters and batteries from a variety of manufacturers and suppliers. If one or more of the suppliers and manufacturers that we rely upon to meet anticipated demand reduces or ceases production, it may be difficult to quickly identify and qualify alternatives on acceptable terms. In addition, equipment prices may increase in the coming years, or not decrease at the rates we historically have experienced, due to tariffs or other factors. For further information, please see the section entitled “Risk Factors” elsewhere in this prospectus.

| 15 |

| Table of Contents |

Intellectual Property

While the success of our business depends more on such factors as our employees’ technical expertise and innovative skills, the success of our business also relies on our ability to protect our proprietary technology. Accordingly, we seek to protect our intellectual property rights in a variety of ways. Although we do not currently have any patented technologies that we use in our business, we seek to protect our proprietary technology and other proprietary rights by requiring our employees and contractors to execute confidentiality and invention assignment agreements. We also rely on employee and third-party nondisclosure agreements and other intellectual property protection methods, including proprietary know-how, to protect our confidential information and our other intellectual property.

We have registered each of Correlate and the Correlate logo as service marks with the US Patent and Trademark Office.

Regulatory

Although we are not regulated as a public utility in the United States under applicable national, state or other local regulatory regimes where we conduct business, we compete primarily with regulated utilities. As a result, we are committed to maintaining key relationships with policy experts that keep us informed key regulatory and legislative issues impacting the entire industry. We believe these efforts help us better navigate local markets through relationships with key stakeholders and facilitate a deep understanding of the national and regional policy environment.

To operate our systems, we obtain interconnection permission from the applicable local primary electric utility. Depending on the size of the solar energy system and local law requirements, interconnection permission is provided by the local utility directly to us and/or our customers. In almost all cases, interconnection permissions are issued on the basis of a standard process that has been pre- approved by the local public utility commission or other regulatory body with jurisdiction over net metering policies. As such, no additional regulatory approvals are required once interconnection permission is given.

Our operations are subject to stringent and complex federal, state and local laws, including regulations governing the occupational health and safety of our employees and wage regulations. For example, we are subject to the requirements of the federal Occupational Safety and Health Act, as amended (“OSHA”), and comparable state laws that protect and regulate employee health and safety. We endeavor to maintain compliance with applicable OSHA and other comparable government regulations.

Government Incentives

Federal, state and local government bodies provide incentives to owners, distributors, system integrators and manufacturers of solar energy systems to promote solar energy in the form of rebates, tax credits, payments for RECs associated with renewable energy generation and exclusion of solar energy systems from property tax assessments. These incentives enable us to lower the price we charge customers for energy from, and to lease, our solar energy systems, helping to catalyze customer acceptance of solar energy as an alternative to utility-provided power. In addition, for some investors, the acceleration of depreciation creates a valuable tax benefit that reduces the overall cost of the solar energy system and increases the return on investment.

The federal government currently offers an investment tax credit (“Commercial ITC”) under Section 48(a) of the Code, for the installation of certain solar power facilities owned for business purposes. If construction on the facility began before January 1, 2020, the amount of the Commercial ITC available is 30%, if construction began during 2020, 2021, or 2022 the amount of the Commercial ITC available is 26%, and if construction begins during 2023 the amount of the Commercial ITC available is 22%. The Commercial ITC steps down to 10% if construction of the facility begins after December 31, 2023 or if the facility is not placed in service before January 1, 2026. The depreciable basis of a solar facility is also reduced by 50% of the amount of any Commercial ITC claimed. The Internal Revenue Service (the “IRS”) provided taxpayers guidance in Notice 2018-59 for determining when construction has begun on a solar facility. This guidance is relevant for any facilities which we seek to deploy in future years but take advantage of a higher tax credit rate available for an earlier year. For example, we have sought to avail ourselves of the methods set forth in the guidance to retain the 30% Commercial ITC that was available prior to January 1, 2020 by incurring certain costs and taking title to equipment in 2019 or early 2020 and/or by performing physical work on components that will be installed in solar facilities. From and after 2023, we may seek to avail ourselves of the 26% credit rate by using these methods to establish the beginning of construction in 2020, 2021, or 2022 and we may plan to similarly further utilize the program in future years if the Commercial ITC step down continues.

More than half of the states, and many local jurisdictions, have established property tax incentives for renewable energy systems that include exemptions, exclusions, abatements and credits. Approximately thirty states and the District of Columbia have adopted a renewable portfolio standard (and approximately eight other states have some voluntary goal) that requires regulated utilities to procure a specified percentage of total electricity delivered in the state from eligible renewable energy sources, such as solar energy systems, by a specified date. To prove compliance with such mandates, utilities must surrender solar renewable energy credits (“SRECs”) to the applicable authority. Solar energy system owners such as our investment funds often are able to sell SRECs to utilities directly or in SREC markets.

| 16 |

| Table of Contents |

While there are numerous federal, state and local government incentives that benefit our business, some adverse interpretations or determinations of new and existing laws can have a negative impact on our business.

Facilities

Our corporate headquarters are located in Shreveport, Louisiana, where we lease office space on a month-to-month basis.

Corporate Information

We were originally formed as a Texas corporation in 1995 under the name TBX Resources, Inc. In December 2011 we changed our name to Frontier Oilfield Services Inc. In January 2020, we merged with and into Triccar Inc., a Nevada corporation and Triccar Inc. was the surviving entity. In December 2021, we acquired one hundred percent of the equity interests of each of Correlate Inc. and Loyal Enterprises LLC. In February 2022, a majority of our stockholders approved an amendment to our articles of incorporation and the change of our corporate name from Triccar Inc. to Correlate Infrastructure Partners Inc., to better reflect our future growth and focus. On April 5, 2022, we filed an amendment to our articles of incorporation with the State of Nevada to change our corporate name from Triccar Inc. to Correlate Infrastructure Partners Inc. Our principal executive offices are located at 220 Travis Street, Suite 501, Shreveport, Louisiana 71101, and our telephone number is (855) 264-4060.

Human Capital Resources

As of December 31, 2022, we had nine employees, all of whom were full-time employees. As of December 31, 2022, none of our employees are represented by a labor union or are subject to a collective bargaining agreement. We believe that our employee relations are good. We also rely on independent contractors for ongoing project work and job specific tasks. At December 31, 2022, we had two full time equivalent independent contractors engaged with us on various projects.

In shaping our culture, we aim to combine a high standard of excellence, technological innovation and agility and operational and financial discipline. We believe that our flat and transparent structure and our collaborative and collegial approach enable our employees to grow, develop and maximize their impact on our organization. To attract and retain top talent in our highly competitive industry, we have designed our compensation and benefits programs to promote the retention and growth of our employees along with their health, well-being and financial security. Our short- and long-term incentive programs are aligned with key business objectives and are intended to motivate strong performance. As an equal opportunity employer, all qualified applicants receive consideration without regard to race, national origin, gender, gender identity, sexual orientation, protected veteran status, disability, age or any other legally protected status.

We seek to create an inclusive, equitable, culturally competent, and supportive environment where our management and employees model behavior that enriches our workplace.

Legal Proceedings

There are no material legal proceedings currently pending or, to our knowledge, threatened against us.

| 17 |

| Table of Contents |

Item 1A. Risk Factors

RISK FACTORS

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below as well as the other information included in this prospectus, including “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus, before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risk Factors Relating to Our Operations and Business

We have incurred operating losses before income taxes and may be unable to achieve or sustain profitability in the future.

We have incurred losses from operations during each of the last two years, which as of December 31, 2022, accumulated to $5,792,407, including an operating loss of $5,717,158 and $75,249 for the years ended December 31, 2022 and 2021, respectively. We may continue to incur operating losses as we increase our spending to finance the expansion of our operations, expand our installation, engineering, administrative, sales and marketing staffs, increase spending on our brand awareness and other sales and marketing initiatives, make significant investments to drive future growth in our business and implement internal systems and infrastructure to support our growth. We do not know whether our revenue will grow rapidly enough to absorb these costs and our limited operating history makes it difficult to assess the extent of these expenses or their impact on our results of operations. Our ability to sustain profitability depends on a number of factors, including but not limited to:

| · | growing our customer base; |

| · | raising additional capital in the form of equity, debt or a combination thereof; |

| · | reducing the cost of components for our solar service offerings; |

| · | growing and maintaining our third-party sales channel; |

| · | maintaining high levels of product quality, performance, and customer satisfaction; |

| · | successfully integrating acquired businesses; and |

| · | reducing our operating costs by lowering our customer acquisition costs and optimizing our design and installation processes. |

|

|

|

We may be unable to achieve positive cash flows from operations in the future.

Our growth strategy depends on the widespread adoption of solar power and renewable energy technology.

The market for solar power products is emerging and rapidly evolving, and our future success is uncertain. If solar power technology proves unsuitable for widespread commercial deployment or if demand for solar power products fails to develop sufficiently, it is likely that we would be unable to generate enough revenues to achieve and sustain profitability and positive cash flow. The factors influencing the widespread adoption of solar power technology include but are not limited to:

| · | cost-effectiveness of solar power technologies as compared with conventional and non-solar alternative energy technologies; |

| · | performance and reliability of solar power products as compared with conventional and non-solar alternative energy products; |

| · | continued deregulation of the electric power industry and broader energy industry; |

| 18 |

| Table of Contents |

| · | fluctuations in economic and market conditions which impact the viability of conventional and non-solar alternative energy sources, such as increases or decreases in the prices of oil and other fossil fuels; and |

| · | availability of governmental subsidies and incentives. |

|

|

|

If we cannot compete successfully against other companies that provide services that compete with ours, we may not be successful in developing our operations and our business may suffer.

The solar and energy industries are characterized by intense competition and rapid technological advances, both in the U.S. and internationally. We compete with other technology-enabled clean energy optimization companies with business models that are similar to ours. In addition, we compete with solar companies in the downstream value chain of solar energy. We face competition from purely sales and finance driven organizations that acquire customers and then subcontract out the installation of solar energy systems, from installation businesses that seek financing from external parties, from large construction companies and utilities, and increasingly from sophisticated electrical and roofing companies. Further, some competitors are integrating vertically in order to ensure supply and to control costs. Many of our competitors also have significant brand name recognition and have extensive knowledge of our target markets, as well as significantly greater personnel and financial resources that us. If we are unable to compete in the market, there will be an adverse effect on our business, financial condition, and results of operations.