UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the quarterly period ended October 31, 2021

OR

| Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

Commission File Number: 001-32224

(Exact name of Registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | ||||

(Address of principal executive offices)

Telephone Number (415 ) 901-7000

(Registrant’s telephone number, including area code)

| Securities registered pursuant to Section 12(b) of the Act | ||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 (the “Exchange Act”) during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

As of November 30, 2021, there were approximately 985 million shares of the Registrant’s Common Stock outstanding.

1

INDEX

| Page No. | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

PART I.

ITEM 1. FINANCIAL STATEMENTS

salesforce.com, inc.

Condensed Consolidated Balance Sheets

(in millions)

| October 31, 2021 | January 31, 2021 | ||||||||||

| Assets | (unaudited) | ||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Marketable securities | |||||||||||

| Accounts receivable, net | |||||||||||

| Costs capitalized to obtain revenue contracts, net | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Property and equipment, net | |||||||||||

| Operating lease right-of-use assets, net | |||||||||||

| Noncurrent costs capitalized to obtain revenue contracts, net | |||||||||||

| Strategic investments | |||||||||||

| Goodwill | |||||||||||

| Intangible assets acquired through business combinations, net | |||||||||||

| Deferred tax assets and other assets, net | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders’ equity | |||||||||||

| Current liabilities: | |||||||||||

Accounts payable, accrued expenses and other liabilities | $ | $ | |||||||||

Operating lease liabilities, current | |||||||||||

Unearned revenue | |||||||||||

| Total current liabilities | |||||||||||

| Noncurrent debt | |||||||||||

| Noncurrent operating lease liabilities | |||||||||||

| Other noncurrent liabilities | |||||||||||

| Total liabilities | |||||||||||

| Stockholders’ equity: | |||||||||||

| Common stock | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

| Retained earnings | |||||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See accompanying Notes.

3

salesforce.com, inc.

Condensed Consolidated Statements of Operations

(in millions, except per share data)

(unaudited)

| 3 | Three Months Ended October 31, | Nine Months Ended October 31, | |||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Revenues: | |||||||||||||||||||||||

| Subscription and support | $ | $ | $ | $ | |||||||||||||||||||

| Professional services and other | |||||||||||||||||||||||

| Total revenues | |||||||||||||||||||||||

| Cost of revenues (1)(2): | |||||||||||||||||||||||

| Subscription and support | |||||||||||||||||||||||

| Professional services and other | |||||||||||||||||||||||

| Total cost of revenues | |||||||||||||||||||||||

| Gross profit | |||||||||||||||||||||||

| Operating expenses (1)(2): | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Marketing and sales | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||

| Income from operations | |||||||||||||||||||||||

| Gains on strategic investments, net | |||||||||||||||||||||||

| Other expense | ( | ( | ( | ( | |||||||||||||||||||

| Income before benefit from (provision for) income taxes | |||||||||||||||||||||||

| Benefit from (provision for) income taxes (3) | ( | ( | |||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Basic net income per share | $ | $ | $ | $ | |||||||||||||||||||

| Diluted net income per share | $ | $ | $ | $ | |||||||||||||||||||

| Shares used in computing basic net income per share | |||||||||||||||||||||||

| Shares used in computing diluted net income per share | |||||||||||||||||||||||

(1) Amounts include amortization of intangible assets acquired through business combinations, as follows:

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Cost of revenues | $ | $ | $ | $ | |||||||||||||||||||

| Marketing and sales | |||||||||||||||||||||||

(2) Amounts include stock-based expense, as follows:

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Cost of revenues | $ | $ | $ | $ | |||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Marketing and sales | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

(3) During the second quarter of fiscal 2021, the Company recorded approximately $2.0 billion of a one-time benefit from a discrete tax item related to the recognition of deferred tax assets resulting from an intra-entity transfer of intangible property.

See accompanying Notes.

4

salesforce.com, inc.

Condensed Consolidated Statements of Comprehensive Income

(in millions)

(unaudited)

| 3 | Three Months Ended October 31, | Nine Months Ended October 31, | |||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Other comprehensive income (loss), net of reclassification adjustments: | |||||||||||||||||||||||

| Foreign currency translation and other losses | ( | ( | ( | ( | |||||||||||||||||||

| Unrealized gains (losses) on marketable securities and privately held debt securities | ( | ( | ( | ||||||||||||||||||||

| Other comprehensive income (loss), before tax | ( | ( | ( | ||||||||||||||||||||

| Tax effect | ( | ||||||||||||||||||||||

| Other comprehensive income (loss), net | ( | ( | ( | ||||||||||||||||||||

| Comprehensive income | $ | $ | $ | $ | |||||||||||||||||||

See accompanying Notes.

5

salesforce.com, inc.

Condensed Consolidated Statements of Stockholders’ Equity

(in millions)

(unaudited)

| Three and Nine months ended October 31, 2021 | |||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-in Capital | Accumulated Other Comprehensive Loss | Retained Earnings | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||

| Balance at January 31, 2021 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Common stock issued | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Stock-based expense | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | 0 | 0 | 0 | ( | 0 | ( | |||||||||||||||||||||||||||||

| Net income | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Balance at April 30, 2021 | ( | ||||||||||||||||||||||||||||||||||

| Common stock issued | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Shares issued related to the acquisition of Slack | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Stock-based expense | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | 0 | 0 | 0 | ( | 0 | ( | |||||||||||||||||||||||||||||

| Net income | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Balance at July 31, 2021 | ( | ||||||||||||||||||||||||||||||||||

| Common stock issued | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Stock-based expense | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | 0 | 0 | 0 | ( | 0 | ( | |||||||||||||||||||||||||||||

| Net income | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Balance at October 31, 2021 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Three and Nine months ended October 31, 2020 | |||||||||||||||||||||||||||||||||||

| Common Stock | Additional Paid-in Capital | Accumulated Other Comprehensive Loss | Retained Earnings | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||

| Balance at January 31, 2020 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Common stock issued | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Stock-based expense | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | 0 | 0 | 0 | ( | 0 | ( | |||||||||||||||||||||||||||||

| Net income | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Balance at April 30, 2020 | ( | ||||||||||||||||||||||||||||||||||

| Common stock issued | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Stock-based expense | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Other comprehensive income, net of tax | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Net income | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Balance at July 31, 2020 | ( | ||||||||||||||||||||||||||||||||||

| Common stock issued | 0 | 0 | 0 | ||||||||||||||||||||||||||||||||

| Stock-based expenses | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Other comprehensive loss, net of tax | 0 | 0 | 0 | ( | 0 | ( | |||||||||||||||||||||||||||||

| Net income | 0 | 0 | 0 | 0 | |||||||||||||||||||||||||||||||

| Balance at October 31, 2020 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

See accompanying Notes.

6

salesforce.com, inc.

Condensed Consolidated Statements of Cash Flows

(in millions)

(unaudited)

| 3 | Three Months Ended October 31, | Nine Months Ended October 31, | |||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Operating activities: | |||||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||||||||||||||

| Depreciation and amortization | |||||||||||||||||||||||

| Amortization of costs capitalized to obtain revenue contracts, net | |||||||||||||||||||||||

| Stock-based expense | |||||||||||||||||||||||

| Gains on strategic investments, net | ( | ( | ( | ( | |||||||||||||||||||

| Tax benefit from intra-entity transfer of intangible property | ( | ||||||||||||||||||||||

| Changes in assets and liabilities, net of business combinations: | |||||||||||||||||||||||

| Accounts receivable, net | |||||||||||||||||||||||

| Costs capitalized to obtain revenue contracts, net | ( | ( | ( | ( | |||||||||||||||||||

| Prepaid expenses and other current assets and other assets | ( | ( | |||||||||||||||||||||

| Accounts payable and accrued expenses and other liabilities | ( | ( | |||||||||||||||||||||

| Operating lease liabilities | ( | ( | ( | ( | |||||||||||||||||||

| Unearned revenue | ( | ( | ( | ( | |||||||||||||||||||

| Net cash provided by operating activities | |||||||||||||||||||||||

| Investing activities: | |||||||||||||||||||||||

| Business combinations, net of cash acquired | ( | ( | ( | ( | |||||||||||||||||||

| Purchases of strategic investments | ( | ( | ( | ( | |||||||||||||||||||

| Sales of strategic investments | |||||||||||||||||||||||

| Purchases of marketable securities | ( | ( | ( | ( | |||||||||||||||||||

| Sales of marketable securities | |||||||||||||||||||||||

| Maturities of marketable securities | |||||||||||||||||||||||

| Capital expenditures | ( | ( | ( | ( | |||||||||||||||||||

| Net cash used in investing activities | ( | ( | ( | ( | |||||||||||||||||||

| Financing activities: | |||||||||||||||||||||||

| Proceeds from issuance of debt, net of issuance costs | ( | ||||||||||||||||||||||

| Repayments of Slack Convertible Notes, net of capped call proceeds (Note 8) | ( | ( | |||||||||||||||||||||

| Proceeds from employee stock plans | |||||||||||||||||||||||

| Principal payments on financing obligations | ( | ( | ( | ( | |||||||||||||||||||

| Repayments of debt | ( | ( | ( | ( | |||||||||||||||||||

| Net cash provided by (used in) financing activities | ( | ||||||||||||||||||||||

| Effect of exchange rate changes | ( | ( | ( | ||||||||||||||||||||

| Net decrease in cash and cash equivalents | ( | ( | ( | ( | |||||||||||||||||||

| Cash and cash equivalents, beginning of period | |||||||||||||||||||||||

| Cash and cash equivalents, end of period | $ | $ | $ | $ | |||||||||||||||||||

See accompanying Notes.

7

salesforce.com, inc.

Condensed Consolidated Statements of Cash Flows

Supplemental Cash Flow Disclosure

(in millions)

(unaudited)

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Supplemental cash flow disclosure: | |||||||||||||||||||||||

| Cash paid during the period for: | |||||||||||||||||||||||

| Interest | $ | $ | $ | $ | |||||||||||||||||||

| Income taxes, net of tax refunds | $ | $ | $ | $ | |||||||||||||||||||

| Non-cash investing and financing activities: | |||||||||||||||||||||||

| Fair value of equity awards assumed | $ | $ | $ | $ | |||||||||||||||||||

| Fair value of common stock issued as consideration for the acquisition of Slack | $ | $ | $ | $ | |||||||||||||||||||

See accompanying Notes.

8

salesforce.com, inc.

Notes to Condensed Consolidated Financial Statements

1. Summary of Business and Significant Accounting Policies

Description of Business

Salesforce (the “Company”) is a global leader in customer relationship management ("CRM") technology that brings companies and customers together. With the Customer 360 platform, the Company delivers a single source of truth, connecting customer data across systems, apps and devices to help companies sell, service, market and conduct commerce from anywhere. Since its founding in 1999, Salesforce has pioneered innovations in cloud, mobile, social, analytics and artificial intelligence (“AI”), enabling companies of every size and industry to transform their businesses in the all-digital, work-from-anywhere era.

On July 21, 2021, the Company acquired Slack Technologies, Inc. (“Slack”). Slack is a channel-based messaging platform (see Note 6, “Business Combinations”).

Fiscal Year

The Company’s fiscal year ends on January 31. References to fiscal 2022, for example, refer to the fiscal year ending January 31, 2022.

Basis of Presentation

The accompanying condensed consolidated balance sheet as of October 31, 2021 and the condensed consolidated statements of operations, condensed consolidated statements of comprehensive income, condensed consolidated statements of stockholders' equity and condensed consolidated statements of cash flows for the three and nine months ended October 31, 2021 and 2020 are unaudited.

These financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) for interim financial information. Accordingly, they do not include all of the financial information and footnotes required by U.S. GAAP for complete financial statements. In the opinion of the Company’s management, the unaudited condensed consolidated financial statements include all adjustments necessary for the fair presentation of the Company’s balance sheet as of October 31, 2021, and its results of operations, including its comprehensive income, stockholders' equity and its cash flows for the three and nine months ended October 31, 2021 and 2020. All adjustments are of a normal recurring nature. The results for the three and nine months ended October 31, 2021 are not necessarily indicative of the results to be expected for any subsequent quarter or for the fiscal year ending January 31, 2022.

These unaudited interim condensed consolidated financial statements should be read in conjunction with the consolidated financial statements and related notes included in the Company's Annual Report on Form 10-K for the fiscal year ended January 31, 2021, filed with the Securities and Exchange Commission (the “SEC”) on March 17, 2021.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions in the Company’s condensed consolidated financial statements and notes thereto.

Significant estimates and assumptions made by management include the determination of:

•the fair value of assets acquired and liabilities assumed for business combinations;

•the standalone selling price (“SSP”) of performance obligations for revenue contracts with multiple performance obligations;

•the valuation of privately-held strategic investments, including impairments;

•the recognition, measurement and valuation of current and deferred income taxes and uncertain tax positions;

•the average period of benefit associated with costs capitalized to obtain revenue contracts;

•the useful lives of intangible assets; and

•the fair value of certain stock awards issued.

9

Principles of Consolidation

The condensed consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

Concentrations of Credit Risk, Significant Customers and Investments

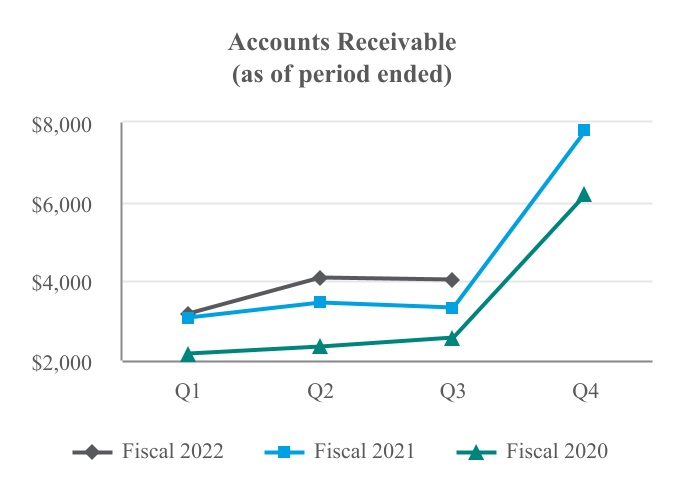

The Company’s financial instruments that are exposed to concentrations of credit risk consist primarily of cash and cash equivalents, marketable securities and accounts receivable. The Company’s investment portfolio consists primarily of investment-grade securities, and per the Company’s policy, limits the amount of credit exposure to any one issuer. The Company monitors and manages the overall exposure of its cash balances to individual financial institutions on an ongoing basis. The Company does not require collateral for accounts receivable. The Company maintains an allowance for its doubtful accounts receivable due to estimated credit losses. This allowance is based upon historical loss patterns, the number of days that billings are past due, an evaluation of the potential risk of loss associated with delinquent accounts and current market conditions and reasonable and supportable forecasts of future economic conditions to inform adjustments to historical loss patterns. The Company records the allowance against bad debt expense through the condensed consolidated statements of operations, included in general and administrative expense, up to the amount of revenues recognized to date. Any incremental allowance is recorded as an offset to unearned revenue on the condensed consolidated balance sheets. Receivables are written off and charged against the recorded allowance when the Company has exhausted collection efforts without success.

No single customer accounted for more than five percent of accounts receivable at October 31, 2021 and January 31, 2021. No single customer accounted for five percent or more of total revenue during the nine months ended October 31, 2021 and 2020. As of October 31, 2021 and January 31, 2021, assets located outside the Americas were 11 percent and 15 percent of total assets, respectively. As of October 31, 2021 and January 31, 2021, assets located in the United States were 88 percent and 82 percent of total assets, respectively.

As of October 31, 2021, the Company held one privately held investment with a carrying value that was individually greater than 15 percent of its total strategic investments. As of January 31, 2021, the Company held three investments that were individually greater than five percent of its strategic investment portfolio, of which two were publicly traded and one was privately held.

Revenue Recognition

The Company derives its revenues from two sources: subscription and support revenues, and professional services and other revenues. Subscription and support revenues include subscription fees from customers accessing the Company’s enterprise cloud computing services (collectively, “Cloud Services”), software license revenues from the sales of term and perpetual licenses, and support revenue from the sales of support and updates beyond the basic subscription fees or related to the sales of software licenses. Professional services and other revenues include professional and advisory services for process mapping, project management and implementation services, and training services.

Revenue is recognized upon transfer of control of promised products and services to customers in an amount that reflects the consideration the Company expects to receive in exchange for those products or services. If the consideration promised in a contract includes a variable amount, for example, overage fees, contingent fees or service level penalties, the Company includes

10

an estimate of the amount it expects to receive for the total transaction price if it is probable that a significant reversal of cumulative revenue recognized will not occur.

The Company determines the amount of revenue to be recognized through the application of the following steps:

•identification of the contract, or contracts, with a customer;

•identification of the performance obligations in the contract;

•determination of the transaction price;

•allocation of the transaction price to the performance obligations in the contract; and

•recognition of revenue when or as the Company satisfies the performance obligations.

Subscription and Support Revenues

Subscription and support revenues are comprised of fees that provide customers with access to Cloud Services, software licenses and related support and updates during the term of the arrangement.

Cloud Services allow customers to use the Company's multi-tenant software without taking possession of the software. Revenue is generally recognized ratably over the contract term. Substantially all of the Company’s subscription service arrangements are non-cancelable and do not contain refund-type provisions.

Subscription and support revenues also include revenues associated with term and perpetual software licenses that provide the customer with a right to use the software as it exists when made available. Revenues from term and perpetual software licenses are generally recognized at the point in time when the software is made available to the customer. Revenue from software support and updates is recognized as the support and updates are provided, which is generally ratably over the contract term.

The Company typically invoices its customers annually and its payment terms provide that customers pay within 30 days of invoice. Amounts that have been invoiced are recorded in accounts receivable and in unearned revenue or revenue, depending on whether transfer of control to customers has occurred.

Professional Services and Other Revenues

The Company’s professional services contracts are either on a time and materials, fixed fee or subscription basis. These revenues are recognized as the services are rendered for time and materials contracts, on a proportional performance basis for fixed price contracts or ratably over the contract term for subscription professional services contracts. Other revenues consist primarily of training revenues recognized as such services are performed.

Significant Judgments - Contracts with Multiple Performance Obligations

The Company enters into contracts with its customers that may include promises to transfer multiple performance obligations such as Cloud Services, software licenses, support and updates, and professional services. A performance obligation is a promise in a contract with a customer to transfer products or services that are concluded to be distinct. Determining whether products and services are distinct performance obligations that should be accounted for separately or combined as one unit of accounting may require significant judgment.

Cloud Services, software licenses, and support and updates services are generally concluded to be distinct because such offerings are often sold separately. In determining whether professional services are distinct, the Company considers the following factors for each professional services agreement: availability of the services from other vendors, the nature of the professional services, the timing of when the professional services contract was signed in comparison to the subscription start date and the contractual dependence of the service on the customer’s satisfaction with the professional services work. To date, the Company has concluded that professional services included in contracts with multiple performance obligations are distinct.

The Company allocates the transaction price to each performance obligation on a relative SSP basis. The SSP is the price at which the Company would sell a promised product or service separately to a customer. Judgment is required to determine the SSP for each distinct performance obligation.

The Company determines SSP by considering its overall pricing objectives and market conditions. Significant pricing practices taken into consideration include the Company’s discounting practices, the size and volume of the Company’s transactions, the customer demographic, the geographic area where services are sold, price lists, the Company's go-to-market strategy, historical and current sales and contract prices. In instances where the Company does not sell or price a product or service separately, the Company determines SSP using information that may include market conditions or other observable inputs. As the Company’s go-to-market strategies evolve, the Company may modify its pricing practices in the future, which could result in changes to SSP.

11

In certain cases, the Company is able to establish SSP based on observable prices of products or services sold or priced separately in comparable circumstances to similar customers. The Company uses a single amount to estimate SSP when indicated by the distribution of its observable prices.

Alternatively, the Company uses a range of amounts to estimate SSP when the pricing practices or distribution of the observable prices is highly variable. The Company typically has more than one SSP for individual products and services due to the stratification of those products and services by customer size and geography.

Costs Capitalized to Obtain Revenue Contracts

The Company capitalizes incremental costs of obtaining non-cancelable Cloud Services subscription, ongoing Cloud Services support and license support and updates revenue contracts. For contracts with on-premises software licenses where revenue is recognized upfront when the software is made available to the customer, costs allocable to those licenses are expensed as they are incurred. Capitalized amounts consist primarily of sales commissions paid to the Company’s direct sales force. Capitalized amounts also include (1) amounts paid to employees other than the direct sales force who earn incentive payouts under annual compensation plans that are tied to the value of contracts acquired, (2) commissions paid to employees upon renewals of subscription and support contracts, (3) the associated payroll taxes and fringe benefit costs associated with the payments to the Company’s employees, and (4) to a lesser extent, success fees paid to partners in emerging markets where the Company has a limited presence.

Costs capitalized related to new revenue contracts are amortized on a straight-line basis over four years , which is longer than the typical initial contract period, but reflects the estimated average period of benefit, including expected contract renewals. In arriving at this average period of benefit, the Company evaluated both qualitative and quantitative factors which included the estimated life cycles of its offerings and its customer attrition. Additionally, the Company amortizes capitalized costs for renewals and success fees paid to partners over two years .

The capitalized amounts are recoverable through future revenue streams under all non-cancelable customer contracts. The Company periodically evaluates whether there have been any changes in its business, the market conditions in which it operates or other events which would indicate that its amortization period should be changed or if there are potential indicators of impairment.

Amortization of capitalized costs to obtain revenue contracts is included in marketing and sales expense in the accompanying condensed consolidated statements of operations.

During the nine months ended October 31, 2021, the Company capitalized $1.2 billion of costs to obtain revenue contracts and amortized $992 million to marketing and sales expense. During the nine months ended October 31, 2020, the Company capitalized $973 million of costs to obtain revenue contracts and amortized $768 million to marketing and sales expense. Costs capitalized to obtain a revenue contract, net, on the Company's condensed consolidated balance sheets totaled $3.1 billion as of October 31, 2021 and $2.9 billion as of January 31, 2021. There were no

Cash and Cash Equivalents

The Company considers all highly liquid investments purchased with an original maturity of three months or less to be cash equivalents. Cash and cash equivalents are stated at fair value.

Marketable Securities

The Company considers all of its marketable debt securities as available for use in current operations, including those with maturity dates beyond one year, and therefore classifies these securities within current assets on the condensed consolidated balance sheets. Securities are classified as available for sale and are carried at fair value, with the change in unrealized gains and losses, net of tax, reported as a separate component on the condensed consolidated statements of comprehensive income until realized. Fair value is determined based on quoted market rates when observable or utilizing data points that are observable, such as quoted prices, interest rates and yield curves. Securities with an amortized cost basis in excess of estimated fair value are assessed to determine what amount of the excess, if any, is caused by expected credit losses. Expected credit losses on securities are recognized in other expense, net on the condensed consolidated statements of operations, and any remaining unrealized losses, net of taxes, are included in accumulated other comprehensive loss in stockholders' equity. For the purposes of computing realized and unrealized gains and losses, the cost of securities sold is based on the specific-identification method. Interest on securities classified as available for sale is included as a component of investment income within other expense.

Strategic Investments

The Company holds strategic investments in privately held debt and equity securities and publicly held equity securities in which the Company does not have a controlling interest.

12

Privately held equity securities where the Company does not have a controlling financial interest in but does exercise significant influence over the investee are accounted for under the equity method. Privately held equity securities not accounted for under the equity method are recorded at cost and adjusted for observable transactions for same or similar investments of the same issuer (referred to as the measurement alternative) or impairment. All gains and losses on privately held equity securities, realized and unrealized, are recorded through gains on strategic investments, net on the condensed consolidated statements of operations. Privately held debt securities are recorded at fair value with changes in fair value recorded through accumulated other comprehensive loss on the condensed consolidated balance sheet.

Valuations of privately held securities are inherently complex and require judgment due to the lack of readily available market data. The carrying value is not adjusted for the Company's privately held equity securities if there are no observable price changes in a same or similar security from the same issuer or if there are no identified events or changes in circumstances that may indicate impairment, as discussed below. In determining the estimated fair value of its strategic investments in privately held companies, the Company utilizes the most recent data available to the Company. The Company assesses its privately held debt and equity securities in its strategic investment portfolio at least quarterly for impairment. The Company’s impairment analysis encompasses an assessment of both qualitative and quantitative factors, including the investee's financial metrics, market acceptance of the investee's product or technology and the rate at which the investee is using its cash. If the investment is considered impaired, the Company recognizes an impairment through the condensed consolidated statements of operations and establishes a new carrying value for the investment.

Publicly held equity securities are measured at fair value with changes recorded through gains on strategic investments, net on the condensed consolidated statements of operations.

Derivative Financial Instruments

The Company enters into foreign currency derivative contracts with financial institutions to reduce foreign exchange risk associated primarily with intercompany receivables and payables. The Company uses forward currency derivative contracts, which are not designated as hedging instruments, to minimize the Company’s exposure to balances primarily denominated in the Euro, British Pound Sterling, Canadian Dollar, Australian Dollar, Brazilian Real, and Japanese Yen. The Company’s derivative financial instruments program is not designated for trading or speculative purposes. The Company generally enters into master netting arrangements with the financial institutions with which it contracts for such derivatives, which permit net settlement of transactions with the same counterparty, thereby reducing risk of credit-related losses from a financial institutions' nonperformance. While the contract or notional amount is often used to express the volume of foreign currency derivative contracts, the amounts potentially subject to credit risk are generally limited to the amounts, if any, by which the counterparties’ obligations under the agreements exceed the obligations of the Company to the counterparties. The notional amount of foreign currency derivative contracts as of October 31, 2021 and January 31, 2021 was $5.2 billion and $5.3 billion, respectively.

Outstanding foreign currency derivative contracts are recorded at fair value on the condensed consolidated balance sheets. Unrealized gains or losses due to changes in the fair value of these derivative contracts, as well as realized gains or losses from their net settlement, are recognized as other expense consistent with the offsetting gains or losses resulting from the remeasurement or settlement of the underlying foreign currency denominated receivables and payables.

Property and Equipment

| Computers, equipment and software | |||||

| Furniture and fixtures | |||||

| Leasehold improvements | Shorter of the estimated lease term or | ||||

| Buildings and building improvements | |||||

When assets are retired or otherwise disposed of, the cost and accumulated depreciation and amortization are removed from their respective accounts and any loss on such retirement is reflected in operating expenses.

13

Leases

The Company determines if an arrangement is a lease at inception and classifies its leases at commencement. Operating leases are included in operating lease right-of-use (“ROU”) assets and current and noncurrent operating lease liabilities on the Company’s condensed consolidated balance sheets. Assets recognized from finance leases (also referred to as ROU assets) are included in property and equipment, accrued expenses and other liabilities and other noncurrent liabilities, respectively, on the Company’s condensed consolidated balance sheets. ROU assets represent the Company's right to use an underlying asset for the lease term. The corresponding lease liabilities represent its obligation to make lease payments arising from the lease. The Company does not recognize ROU assets or lease liabilities for leases with a term of 12 months or less for any asset classes.

Lease liabilities are recognized based on the present value of the future minimum lease payments over the lease term at commencement, net of any future tenant incentives. The Company has lease agreements which contain both lease and non-lease components, which it has elected to combine for all asset classes. As such, minimum lease payments include fixed payments for non-lease components within a lease agreement, but exclude variable lease payments not dependent on an index or rate, such as common area maintenance, operating expenses, utilities, or other costs that are subject to fluctuation from period to period. The Company’s lease terms may include options to extend or terminate the lease. Periods beyond the noncancellable term of the lease are included in the measurement of the lease liability when it is reasonably certain that the Company will exercise the associated extension option or waive the termination option. The Company reassesses the lease term if and when a significant event or change in circumstances occurs within the control of the Company. As most of the Company’s leases do not provide an implicit rate, the net present value of future minimum lease payments is determined using the Company’s incremental borrowing rate. The Company's incremental borrowing rate is an estimate of the interest rate the Company would have to pay to borrow on a collateralized basis with similar terms and payments, in the economic environment where the leased asset is located.

The lease ROU asset is recognized based on the lease liability, adjusted for any rent payments or initial direct costs incurred or tenant incentives received prior to commencement.

Lease expenses for minimum lease payments for operating leases are recognized on a straight-line basis over the lease term. Amortization expense of finance lease ROU assets is recognized on a straight-line basis over the lease term, and interest expense for finance lease liabilities is recognized based on the incremental borrowing rate. Expense for variable lease payments are recognized as incurred.

On the lease commencement date, the Company also establishes assets and liabilities for the present value of estimated future costs to retire long-lived assets at the termination or expiration of a lease. Such assets are included in property and equipment, net and are amortized over the lease term to operating expense.

The Company has entered into subleases or has made decisions and taken actions to exit and sublease certain unoccupied leased office space. Similar to other long-lived assets discussed below, management tests ROU assets for impairment whenever events or changes in circumstances indicate that the carrying amount of such assets may not be recoverable. For leased assets, such circumstances would include the decision to leave a leased facility prior to the end of the minimum lease term or subleases for which estimated cash flow do not fully cover the costs of the associated lease.

Intangible Assets Acquired through Business Combinations

Intangible assets are amortized over their estimated useful lives. Each period, the Company evaluates the estimated remaining useful life of its intangible assets and whether events or changes in circumstances warrant a revision to the remaining period of amortization. Management tests for impairment whenever events or changes in circumstances occur that could impact the recoverability of these assets.

Impairment Assessment

The Company evaluates intangible assets and long-lived assets for possible impairment whenever events or changes in circumstances indicate that the carrying amount of such assets may not be recoverable. This includes but is not limited to significant adverse changes in business climate, market conditions or other events that indicate an asset's carrying amount may not be recoverable. Recoverability of these assets is measured by comparing the carrying amount of each asset to the future undiscounted cash flows the asset is expected to generate. If the undiscounted cash flows used in the test for recoverability are less than the carrying amount of these assets, the carrying amount of such assets is reduced to fair value.

There were no

14

Business Combinations

The Company uses its best estimates and assumptions to assign fair value to the tangible and intangible assets acquired and liabilities assumed at the acquisition date. The Company’s estimates are inherently uncertain and subject to refinement. During the measurement period, which may be up to one year from the acquisition date, the Company may record adjustments to the fair value of these tangible and intangible assets acquired and liabilities assumed, with the corresponding offset to goodwill. In addition, uncertain tax positions, tax-related valuation allowances and pre-acquisition contingencies are initially recorded in connection with a business combination as of the acquisition date. The Company continues to collect information and reevaluates these estimates and assumptions quarterly and records any adjustments to the Company’s preliminary estimates to goodwill provided that the Company is within the measurement period. Upon the conclusion of the measurement period or final determination of the fair value of assets acquired or liabilities assumed, whichever comes first, any subsequent adjustments are recorded to the Company’s condensed consolidated statements of operations.

In the event the Company acquires an entity with which the Company has a preexisting relationship, the Company will generally recognize a gain or loss to settle that relationship as of the acquisition date within operating income on the condensed consolidated statements of operations. In the event that the Company acquires an entity in which the Company previously held a strategic investment, the difference between the fair value of the shares as of the date of the acquisition and the carrying value of the strategic investment is recorded as a gain or loss and recorded within net gains or (losses) on strategic investments in the condensed consolidated statements of operations.

Stock-Based Expense

Stock-based expense is measured based on grant date at fair value using the Black-Scholes option pricing model for stock options and the grant date closing stock price for restricted stock awards. The Company recognizes stock-based expense related to stock options and restricted stock awards on a straight-line basis, net of estimated forfeitures, over the requisite service period of the awards, which is generally the vesting term of four years . The estimated forfeiture rate applied is based on historical forfeiture rates.

Stock-based expense related to the Company’s Amended and Restated 2004 Employee Stock Purchase Plan (“ESPP” or “2004 Employee Stock Purchase Plan”) is measured based on grant date at fair value using the Black-Scholes option pricing model. The Company recognizes stock-based expense related to shares issued pursuant to the 2004 Employee Stock Purchase Plan on a straight-line basis over the offering period, which is 12 months. The ESPP allows employees to purchase shares of the Company's common stock at a 15 percent discount from the lower of the Company’s stock price on (i) the first day of the offering period or on (ii) the last day of the purchase period and also allows employees to reduce their percentage election once during a six-month purchase period (December 15 and June 15 of each fiscal year), but not increase that election until the next one-year offering period. The ESPP also includes a reset provision for the purchase price if the stock price on the purchase date is less than the stock price on the offering date.

Stock-based expense related to performance share grants, which are awarded to executive officers and other members of senior management and vest, if at all, based on the Company’s performance over a three-year period relative to the Nasdaq 100. Performance share grants are measured based on grant date at fair value using a Monte Carlo simulation model and expensed on a straight-line basis, net of estimated forfeitures, over the service period of the awards, which is generally the vesting term of three years .

Income Taxes

The Company uses the asset and liability method of accounting for income taxes. Under this method, deferred tax assets and liabilities are determined based on temporary differences between the financial statement and tax basis of assets and liabilities using enacted tax rates in effect for the year in which the differences are expected to reverse. The effect on deferred tax assets and liabilities of a change in tax laws is recognized in the condensed consolidated statements of operations in the period that includes the enactment date.

The Company’s tax positions are subject to income tax audits by multiple tax jurisdictions throughout the world. The Company recognizes the tax benefit of an uncertain tax position only if it is more likely than not that the position is sustainable upon examination by the taxing authority, solely based on its technical merits. The tax benefit recognized is measured as the largest amount of benefit which is greater than 50 percent likely to be realized upon settlement with the taxing authority. The Company recognizes interest accrued and penalties related to unrecognized tax benefits in the income tax provision.

15

Warranties and Indemnification

The Company’s enterprise cloud computing services are typically warranted to perform in a manner consistent with general industry standards that are reasonably applicable and materially in accordance with the Company’s online help documentation under normal use and circumstances.

The Company’s arrangements generally include certain provisions for indemnifying customers against liabilities if its products or services infringe a third party’s intellectual property rights. To date, the Company has not incurred any material costs as a result of such obligations and has not accrued any material liabilities related to such obligations in the accompanying condensed consolidated financial statements.

The Company has also agreed to indemnify its directors and executive officers for costs associated with any fees, expenses, judgments, fines and settlement amounts incurred by any of these persons in any action or proceeding to which any of those persons is, or is threatened to be, made a party by reason of the person’s service as a director or officer, including any action by the Company, arising out of that person’s services as the Company’s director or officer or that person’s services provided to any other company or enterprise at the Company’s request. The Company maintains director and officer insurance coverage that would generally enable the Company to recover a portion of any future amounts paid. The Company may also be subject to indemnification obligations by law with respect to the actions of its employees under certain circumstances and in certain jurisdictions.

New Accounting Pronouncement Adopted in Fiscal 2022

In December 2019, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update No. 2019-12, “Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes,” which modifies and eliminates certain exceptions to the general principles of ASC 740, Income Taxes. ASU 2019-12 was adopted in the first quarter of fiscal 2022. The prospective adoption of ASU 2019-12 was not material.

New Accounting Pronouncements Pending Adoption

In October 2021, the FASB issued Accounting Standards Update No. 2021-08, “Business Combinations (Topic 805): Accounting for Contract Assets and Contract Liabilities from Contracts with Customers” (“ASU 2021-08”), which requires contract assets and contract liabilities (i.e., unearned revenue) acquired in a business combination to be recognized and measured in accordance with ASC 606, Revenue from Contracts with Customers. Currently, the Company recognizes contract assets and contract liabilities at the acquisition date based on fair value estimates, which historically has resulted in a reduction to unearned revenue on the balance sheet, and therefore, a reduction to revenues that would have otherwise been recorded as an independent entity. ASU 2021-08 is effective for interim and annual periods beginning after December 15, 2022 on a prospective basis, with early adoption permitted. The Company expects to adopt ASU 2021-08 in the first quarter of fiscal 2023. The Company is currently evaluating the potential impact of ASU 2021-08 to its consolidated financial statements.

Reclassifications

Certain reclassifications to fiscal 2021 amounts were made to conform to the current period presentation in the Disaggregation of Revenue disclosure included in Note 2 “Revenues”. Disaggregation of revenues now includes Data, a new

16

2. Revenues

Disaggregation of Revenue

Subscription and Support Revenue by the Company's Service Offerings

Subscription and support revenues consisted of the following (in millions):

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Sales | $ | $ | $ | $ | |||||||||||||||||||

| Service | |||||||||||||||||||||||

| Platform and Other (1) | |||||||||||||||||||||||

| Marketing and Commerce | |||||||||||||||||||||||

| Data | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

(1) Slack revenues are included in Platform and Other

Total Revenue by Geographic Locations

Revenues by geographical region consisted of the following (in millions):

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Americas | $ | $ | $ | $ | |||||||||||||||||||

| Europe | |||||||||||||||||||||||

| Asia Pacific | |||||||||||||||||||||||

| $ | $ | $ | $ | ||||||||||||||||||||

Revenues by geography are determined based on the region of the Company's contracting entity, which may be different than the region of the customer. Americas revenue attributed to the United States was approximately 94 96

Contract Balances

Contract Assets

The Company records a contract asset when revenue recognized on a contract exceeds the billings. Contract assets were $744 million as of October 31, 2021 as compared to $477 million as of January 31, 2021, and are included in prepaid expenses and other current assets and deferred tax assets and other assets, net on the condensed consolidated balance sheets. Impairments of contract assets were immaterial during the three and nine months ended October 31, 2021 and 2020.

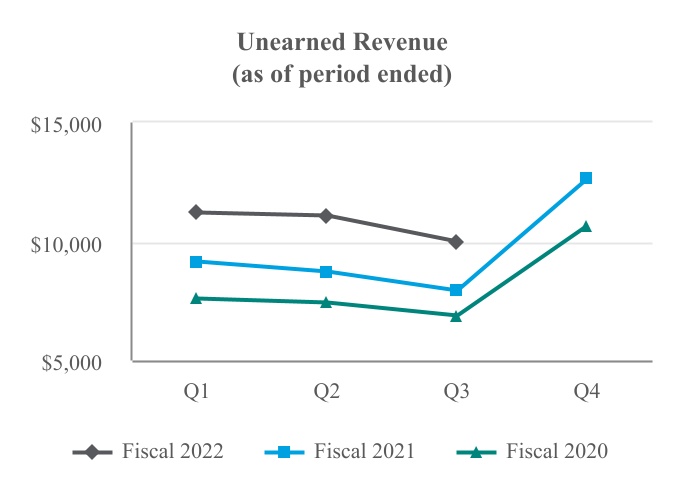

Unearned Revenue

Unearned revenue represents amounts that have been invoiced in advance of revenue recognition and is recognized as revenue when transfer of control to customers has occurred or services have been provided. The unearned revenue balance does not represent the total contract value of annual or multi-year, non-cancelable subscription agreements. The unearned revenue balance is influenced by several factors, including seasonality, the compounding effects of renewals, invoice duration, invoice timing, dollar size and new business linearity within the quarter.

17

The change in unearned revenue was as follows (in millions):

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Unearned revenue, beginning of period | $ | $ | $ | $ | |||||||||||||||||||

| Billings and other (1) | |||||||||||||||||||||||

| Contribution from contract asset | |||||||||||||||||||||||

| Revenue recognized over time | ( | ( | ( | ( | |||||||||||||||||||

| Revenue recognized at a point in time | ( | ( | ( | ( | |||||||||||||||||||

| Unearned revenue from business combinations | |||||||||||||||||||||||

| Unearned revenue, end of period | $ | $ | $ | $ | |||||||||||||||||||

(1) Other includes, for example, the impact of foreign currency translation.

The majority of revenue recognized for these services is from the beginning of period unearned revenue balance.

Revenue recognized over time primarily includes Cloud Services revenue which is generally recognized over time, professional services revenue which is generally recognized ratably or as delivered, training revenue that is primarily recognized as delivered and software support and updates revenue which is generally recognized ratably.

Revenue recognized at a point in time substantially consists of on-premises software licenses.

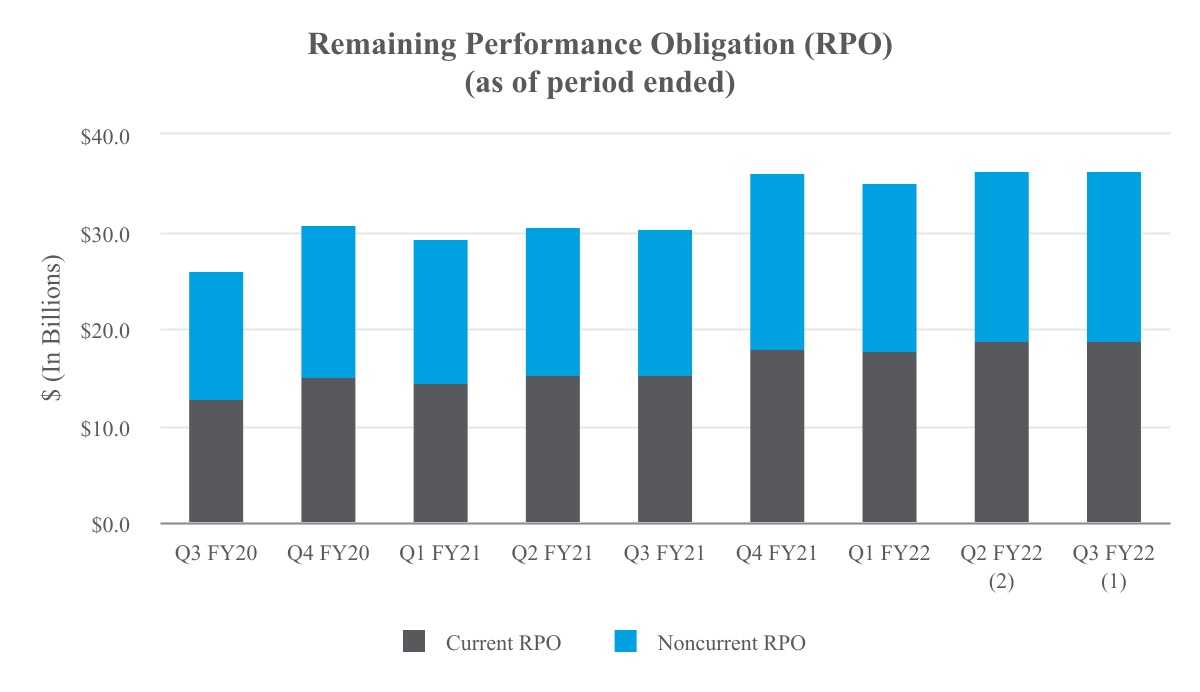

Remaining Performance Obligation

Remaining performance obligation represents contracted revenue that has not yet been recognized and includes unearned revenue and unbilled amounts that will be recognized as revenue in future periods. Transaction price allocated to the remaining performance obligation is based on SSP. Remaining performance obligation is influenced by several factors, including seasonality, the timing of renewals, the timing of software license deliveries, average contract terms and foreign currency exchange rates. Remaining performance obligation is also impacted by acquisitions. Unbilled portions of the remaining performance obligation denominated in foreign currencies are revalued each period based on the period end exchange rates. Unbilled portions of the remaining performance obligation are subject to future economic risks, including bankruptcies, regulatory changes and other market factors.

The Company excludes amounts related to performance obligations from professional services contracts that are billed and recognized on a time-and-materials basis.

The majority of the Company's noncurrent remaining performance obligation is expected to be recognized in the next 13 to 36 months.

Remaining performance obligation consisted of the following (in billions):

| Current | Noncurrent | Total | |||||||||||||||

| As of October 31, 2021 (1) | $ | $ | $ | ||||||||||||||

| As of January 31, 2021 | $ | $ | $ | ||||||||||||||

(1) Includes approximately $900 million of remaining performance obligation related to the Slack acquisition.

18

3. Investments

Marketable Securities

At October 31, 2021, marketable securities consisted of the following (in millions):

| Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | ||||||||||||||||||||

| Corporate notes and obligations | $ | $ | $ | ( | $ | ||||||||||||||||||

| U.S. treasury securities | ( | ||||||||||||||||||||||

| Mortgage-backed obligations | ( | ||||||||||||||||||||||

| Asset-backed securities | ( | ||||||||||||||||||||||

| Municipal securities | |||||||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||

| Covered bonds | ( | ||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Total marketable securities | $ | $ | $ | ( | $ | ||||||||||||||||||

At January 31, 2021, marketable securities consisted of the following (in millions):

| Amortized Cost | Unrealized Gains | Unrealized Losses | Fair Value | ||||||||||||||||||||

| Corporate notes and obligations | $ | $ | $ | $ | |||||||||||||||||||

| U.S. treasury securities | |||||||||||||||||||||||

| Mortgage-backed obligations | |||||||||||||||||||||||

| Asset-backed securities | ( | ||||||||||||||||||||||

| Municipal securities | |||||||||||||||||||||||

| Covered bonds | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Total marketable securities | $ | $ | $ | ( | $ | ||||||||||||||||||

| As of | |||||||||||

| October 31, 2021 | January 31, 2021 | ||||||||||

| Due within 1 year | $ | $ | |||||||||

| Due in 1 year through 5 years | |||||||||||

| Due in 5 years through 10 years | |||||||||||

| $ | $ | ||||||||||

Strategic Investments

| Measurement Category | |||||||||||||||||||||||

| Fair Value | Measurement Alternative | Other | Total | ||||||||||||||||||||

| Equity securities | $ | $ | $ | $ | |||||||||||||||||||

| Debt securities and other investments | |||||||||||||||||||||||

Balance as of October 31, 2021 | $ | $ | $ | $ | |||||||||||||||||||

19

| Measurement Category | |||||||||||||||||||||||

| Fair Value | Measurement Alternative | Other | Total | ||||||||||||||||||||

| Equity securities | $ | $ | $ | $ | |||||||||||||||||||

| Debt securities and other investments | |||||||||||||||||||||||

Balance as of January 31, 2021 | $ | $ | $ | $ | |||||||||||||||||||

Measurement Alternative Adjustments

The Company recognized $28 million and $6 million of impairments and downward adjustments and $131 million and $31 million of upward adjustments during the three months ended October 31, 2021 and 2020, respectively. The Company recognized $55 million and $82 million of impairments and downward adjustments and $933 million and $86 million of upward adjustments during the nine months ended October 31, 2021 and 2020. Approximately $369 million of the upward adjustments during the nine months ended October 31, 2021 was related to the mark-up of one of the Company’s privately held investments.

Since February 1, 2018, cumulative impairments and downward adjustments were $181 million and cumulative upward adjustments were $1.2 billion through October 31, 2021 for measurement alternative investments still held as of October 31, 2021.

Gains on Strategic Investments, Net

| 3 | Three Months Ended October 31, | Nine Months Ended October 31, | |||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Unrealized gains (losses) recognized on publicly traded equity securities, net | $ | $ | $ | ( | $ | ||||||||||||||||||

| Unrealized gains recognized on privately held equity securities, net | |||||||||||||||||||||||

| Realized gains on sales of securities, net | |||||||||||||||||||||||

| Impairments on privately held equity and debt securities | ( | ( | ( | ( | |||||||||||||||||||

| Gains on strategic investments, net | $ | $ | $ | $ | |||||||||||||||||||

Realized gains on sales of securities, net reflects the difference between the sale proceeds and the carrying value of the security at the beginning of the period or the purchase date, if later. The realized gains for the three months ended October 31, 2021 were primarily driven by the sale of one of the Company’s publicly traded investments resulting in a realized gain of $112 million. The realized gains for the nine months ended October 31, 2021 were also driven by the acquisition of one of the Company’s privately held equity investments in a stock and cash transaction by a publicly traded company of $155 million. The cumulative net gains, measured as the sale price less the initial purchase price, for equity securities exited during the three and nine months ended October 31, 2021 were $498 million and $1.6 billion, respectively. Cumulative net realized gains in the three and nine months ended October 31, 2021 include gains related to partial sales of two of the Company’s publicly traded investments, which resulted in cumulative net gains of $505 million and $1.5 billion, respectively.

In the three months ended October 31, 2021 and 2020, for strategic investments still held as of those respective period ends, the Company recognized net unrealized gains of $249 million and $1.0 billion, respectively. These include approximately $11 million and $8 million of impairments on privately held equity and debt securities in the three months ended October 31, 2021 and 2020, respectively.

4. Fair Value Measurement

The Company uses a three-tier fair value hierarchy, which prioritizes the inputs used in the valuation methodologies in measuring fair value:

Level 1. Quoted prices (unadjusted) in active markets for identical assets or liabilities.

Level 2. Significant other inputs that are directly or indirectly observable in the marketplace.

Level 3. Significant unobservable inputs which are supported by little or no market activity.

20

All of the Company’s cash equivalents, marketable securities and foreign currency derivative contracts are classified within Level 1 or Level 2 because the Company’s cash equivalents, marketable securities and foreign currency derivative contracts are valued using quoted market prices or alternative pricing sources and models utilizing observable market inputs.

The following table presents information about the Company’s assets and liabilities that were measured at fair value as of October 31, 2021 and indicates the fair value hierarchy of the valuation (in millions):

| Description | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Balance as of October 31, 2021 | |||||||||||||||||||

| Cash equivalents (1): | |||||||||||||||||||||||

| Time deposits | $ | $ | $ | $ | |||||||||||||||||||

| Money market mutual funds | |||||||||||||||||||||||

| Cash equivalent securities | |||||||||||||||||||||||

| Marketable securities: | |||||||||||||||||||||||

| Corporate notes and obligations | |||||||||||||||||||||||

| U.S. treasury securities | |||||||||||||||||||||||

| Mortgage-backed obligations | |||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||

| Municipal securities | |||||||||||||||||||||||

| Commercial paper | |||||||||||||||||||||||

| Covered bonds | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Strategic investments: | |||||||||||||||||||||||

| Publicly held equity securities | |||||||||||||||||||||||

| Total assets | $ | $ | $ | $ | |||||||||||||||||||

(1) Included in “cash and cash equivalents” in the accompanying condensed consolidated balance sheets in addition to $2.7 billion of cash, as of October 31, 2021.

The following table presents information about the Company’s assets and liabilities that were measured at fair value as of January 31, 2021 and indicates the fair value hierarchy of the valuation (in millions):

| Description | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Balance as of January 31, 2021 | |||||||||||||||||||

| Cash equivalents (1): | |||||||||||||||||||||||

| Time deposits | $ | $ | $ | $ | |||||||||||||||||||

| Money market mutual funds | |||||||||||||||||||||||

| Cash equivalent securities | |||||||||||||||||||||||

| Marketable securities: | |||||||||||||||||||||||

| Corporate notes and obligations | |||||||||||||||||||||||

| U.S. treasury securities | |||||||||||||||||||||||

| Mortgage-backed obligations | |||||||||||||||||||||||

| Asset-backed securities | |||||||||||||||||||||||

| Municipal securities | |||||||||||||||||||||||

| Covered bonds | |||||||||||||||||||||||

| Other | |||||||||||||||||||||||

| Strategic investments: | |||||||||||||||||||||||

| Publicly held equity securities | |||||||||||||||||||||||

| Total assets | $ | $ | $ | $ | |||||||||||||||||||

(1) Included in “cash and cash equivalents” in the accompanying condensed consolidated balance sheets in addition to $2.8 billion of cash, as of January 31, 2021.

21

Strategic Investments Measured and Recorded at Fair Value on a Non-Recurring Basis

The Company's privately held debt and equity securities and equity method investments are recorded at fair value on a non-recurring basis. The estimation of fair value for these investments requires the use of significant unobservable inputs, and as a result, the Company deems these assets as Level 3 within the fair value measurement framework. For investments without a readily determinable fair value, the Company applies valuation methods based on information available, including the market approach and option pricing models (“OPM”). Observable transactions, such as the issuance of new equity by an investee, are indicators of investee enterprise value and are used to estimate the fair value of the Company’s investments. An OPM may be utilized to allocate value to the various classes of securities of the investee, including classes owned by the Company. Such information available to the Company from investee companies is supplemented with estimates such as volatility, expected time to liquidity and the rights and obligations of the securities the Company holds. The Company's privately held debt and equity securities and other investments amounted to $3.4 billion and $1.8 billion as of October 31, 2021 and January 31, 2021, respectively.

5. Leases and Other Commitments

Leases

The Company has operating leases for corporate offices, data centers and equipment under non-cancelable operating leases with various expiration dates. The leases have remaining terms of 1 to 18 years, some of which include options to terminate within one year .

Total operating lease costs were $294 million and $278 million for the three months ended October 31, 2021 and 2020, respectively, and $818 million and $815 million for the nine months ended October 31, 2021 and 2020, respectively.

For the three months ended October 31, 2021 and 2020, cash payments for operating leases were $210 million and $222 million, respectively, and $664 million and $672 million for the nine months ended October 31, 2021 and 2020, respectively. Operating lease commencements and modifications resulted in increases to ROU assets and corresponding operating lease liabilities of $37 million and $196 million during the three months ended October 31, 2021 and 2020, respectively, and $174 million and $562 million during the nine months ended October 31, 2021 and 2020, respectively. The July 2021 acquisition of Slack resulted in an increase in ROU assets and operating lease liabilities of $208 million and $283 million, respectively.

| Operating Leases | Finance Leases | ||||||||||

| Fiscal Period: | |||||||||||

| Remaining three months of fiscal 2022 | $ | $ | |||||||||

| Fiscal 2023 | |||||||||||

| Fiscal 2024 | |||||||||||

| Fiscal 2025 | |||||||||||

| Fiscal 2026 | |||||||||||

| Thereafter | |||||||||||

| Total minimum lease payments | |||||||||||

| Less: Imputed interest | ( | ( | |||||||||

| Total | $ | $ | |||||||||

Operating lease amounts above do not include sublease income. The Company has entered into various sublease agreements with third parties. Under these agreements, the Company expects to receive sublease income of approximately $189 million in the next five years and $29 million thereafter.

As of October 31, 2021, the Company has additional operating leases that have not yet commenced totaling $1.4 billion and therefore not reflected on the condensed consolidated balance sheets and tables above. These operating leases include agreements for office facilities to be constructed. These operating leases will commence between fiscal year 2022 and fiscal year 2025 with lease terms of 3 to 18 years.

Letters of Credit

22

6. Business Combinations

Slack Technologies, Inc.

On July 21, 2021, the Company acquired all outstanding stock of Slack, a leading channel-based messaging platform. The Company has included the financial results of Slack in the condensed consolidated financial statements from the date of acquisition. The transaction costs associated with the acquisition were approximately $54 million and were recorded in general and administrative expense during the nine months ended October 31, 2021. The preliminary acquisition date fair value of the consideration transferred for Slack was approximately $27.1 billion, which consisted of the following (in millions):

| Fair Value | |||||

| Cash | $ | ||||

| Common stock issued | |||||

| Fair value of stock options, restricted stock units and restricted stock awards assumed | |||||

| Total | $ | ||||

The fair value of the stock options assumed by the Company was determined using the Black-Scholes option pricing model. A share conversion ratio of 0.1885 and 0.1804 was applied to convert Slack's outstanding (i) stock options and restricted stock units and (ii) restricted stock awards, respectively, into equity awards for shares of the Company’s common stock.

| Fair Value | |||||

| Cash and cash equivalents | $ | ||||

| Accounts receivable | |||||

| Acquired customer contract asset | |||||

| Operating lease right-of-use assets | |||||

| Other assets | |||||

| Goodwill | |||||

| Intangible assets | |||||

| Accounts payable, accrued expenses and other liabilities | ( | ||||

| Unearned revenue | ( | ||||

| Slack Convertible Notes (see Note 8) | ( | ||||

| Operating lease liabilities | ( | ||||

| Deferred tax liability | ( | ||||

| Net assets acquired | $ | ||||

The excess of purchase consideration over the fair value of other assets acquired and liabilities assumed was recorded as goodwill. The resulting goodwill is primarily attributed to the assembled workforce and expanded market opportunities, including integrating the Slack product offering with existing Company service offerings in a digital-first, work anywhere world. The goodwill has no basis for U.S. income tax purposes. The fair values assigned to tangible assets acquired and liabilities assumed are preliminary based on management’s estimates and assumptions and may be subject to change as additional information is received and certain tax matters are finalized. Certain adjustments were made during the three months ended October 31, 2021 to the preliminary fair values resulting in a net increase to goodwill of $233 million primarily related to the customer relationships intangible asset and the corresponding deferred tax liability. The primary areas that remain preliminary relate to the fair values of intangible assets acquired, certain tangible assets and liabilities acquired, legal and other contingencies as of the acquisition date, income and non-income-based taxes and residual goodwill. The Company expects to finalize the valuation as soon as practicable, but not later than one year from the acquisition date.

23

| Fair Value | Useful Life | ||||||||||

| Developed technology | $ | ||||||||||

| Customer relationships | |||||||||||

| Other purchased intangible assets | |||||||||||

| Total intangible assets subject to amortization | $ | ||||||||||

Developed technology represents the preliminary estimated fair value of Slack's data analysis technologies. Customer relationships represent the preliminary estimated fair values of the underlying relationships with Slack customers.

The Company assumed unvested stock options, restricted stock units and restricted stock awards with a preliminary estimated fair value of $1.7 billion. Of the total consideration, $205 million was preliminarily allocated to the purchase consideration and $1.5 billion was preliminarily allocated to future services and will be expensed over the remaining service periods on a straight-line basis.

| Total revenues | $ | ||||

| Pretax loss | ( | ||||

The following pro forma financial information summarizes the combined results of operations for the Company and Slack, as though the companies were combined as of the beginning of the Company’s fiscal 2021. The pro forma financial information was as follows (in millions):

| Three Months Ended October 31, | Nine Months Ended October 31, | ||||||||||||||||||||||

| 2021 | 2020 | 2021 | 2020 | ||||||||||||||||||||

| Total revenues | $ | $ | $ | $ | |||||||||||||||||||

| Pretax income | |||||||||||||||||||||||

| Net income | |||||||||||||||||||||||

The pro forma financial information for all periods presented above has been calculated after adjusting the results of Slack to reflect the business combination accounting effects resulting from this acquisition, including the fair value adjustment to revenue contracts, the amortization expense from acquired intangible assets and the stock-based compensation expense for unvested stock options, restricted stock units and restricted stock awards assumed as though the acquisition occurred as of the beginning of the Company’s fiscal year 2021. The historical consolidated financial statements have been adjusted in the pro forma combined financial statements to give effect to pro forma events that are directly attributable to the business combination and factually supportable. The pro forma financial information is for informational purposes only and is not indicative of the results of operations that would have been achieved if the acquisition had taken place at the beginning of the Company’s fiscal 2021.

Acumen Solutions, Inc.

In February 2021, the Company acquired all outstanding stock of Acumen Solutions, Inc. (“Acumen”), a professional services firm that provides innovative and critical solutions to clients using the Company’s service offerings and other advanced cloud technologies. The acquisition date fair value of the consideration transferred for Acumen was approximately $433 million, in cash. The Company recorded approximately $99 million for customer relationships with estimated useful lives of eight years . The Company recorded approximately $337 million of goodwill which is primarily attributed to the assembled workforce. For the goodwill balance there is no basis for U.S. income tax purposes. The fair values assigned to tangible assets acquired and liabilities assumed are based on management’s estimates and assumptions and may be subject to change as additional information is received and certain tax returns are finalized. The primary areas that remain preliminary relate to the fair values of intangible assets acquired, certain tangible assets and liabilities acquired, legal and other contingencies as of the acquisition date, income and non-income-based taxes and residual goodwill. The Company expects to finalize the valuation as soon as practicable, but not later than one year from the acquisition date.

The Company has included the financial results of Acumen in its condensed consolidated financial statements from the date of acquisition, which were not material. The transaction costs associated with the acquisition were not material.

24

7. Intangible Assets Acquired Through Business Combinations and Goodwill

Intangible Assets Acquired Through Business Combinations

Intangible assets acquired through business combinations were as follows (in millions):

| Intangible Assets, Gross | Accumulated Amortization | Intangible Assets, Net | Weighted Average Remaining Useful Life (Years) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| January 31, 2021 | Additions and retirements, net | October 31, 2021 | January 31, 2021 | Expense and retirements, net | October 31, 2021 | January 31, 2021 | October 31, 2021 | October 31, 2021 | |||||||||||||||||||||||||||||||||||||||||||||

| Acquired developed technology | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||||