20-F

FYGIGAMEDIA Ltd0001105101falseU0http://fasb.org/us-gaap/2023#EntertainmentMemberhttp://fasb.org/us-gaap/2023#EntertainmentMemberhttp://fasb.org/us-gaap/2023#EntertainmentMemberhttp://fasb.org/us-gaap/2023#EntertainmentMemberhttp://fasb.org/us-gaap/2023#EntertainmentMemberhttp://fasb.org/us-gaap/2023#EntertainmentMemberP1Y1http://fasb.org/us-gaap/2023#OtherNonoperatingIncomeExpensehttp://fasb.org/us-gaap/2023#OtherNonoperatingIncomeExpensehttp://fasb.org/us-gaap/2023#OtherNonoperatingIncomeExpensehttp://fasb.org/us-gaap/2023#DebtSecuritiesAvailableForSaleGainLosshttp://fasb.org/us-gaap/2023#DebtSecuritiesAvailableForSaleGainLosshttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeUnrealizedHoldingGainLossOnSecuritiesArisingDuringPeriodNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeUnrealizedHoldingGainLossOnSecuritiesArisingDuringPeriodNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossForeignCurrencyTransactionAndTranslationAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossForeignCurrencyTransactionAndTranslationAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossForeignCurrencyTransactionAndTranslationAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossForeignCurrencyTransactionAndTranslationAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OperatingLeaseRightOfUseAssethttp://fasb.org/us-gaap/2023#OperatingLeaseRightOfUseAssethttp://fasb.org/us-gaap/2023#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossPensionAndOtherPostretirementBenefitPlansAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossPensionAndOtherPostretirementBenefitPlansAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossPensionAndOtherPostretirementBenefitPlansAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossPensionAndOtherPostretirementBenefitPlansAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossPensionAndOtherPostretirementBenefitPlansAdjustmentNetOfTaxhttp://fasb.org/us-gaap/2023#OtherComprehensiveIncomeLossPensionAndOtherPostretirementBenefitPlansAdjustmentNetOfTaxJanuary 2022January 20240001105101gigm:TwoThousandSixPlanMemberus-gaap:RestrictedStockUnitsRSUMembersrt:MinimumMember2023-01-012023-12-3100011051012023-01-012023-12-310001105101srt:MaximumMembergigm:TwoThousandFourPlanMember2023-12-310001105101us-gaap:SellingAndMarketingExpenseMember2023-01-012023-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMemberus-gaap:AccumulatedTranslationAdjustmentMember2023-01-012023-12-310001105101srt:MaximumMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMembergigm:RateForEquityInvestmentMember2022-12-310001105101us-gaap:EstimateOfFairValueFairValueDisclosureMember2022-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2022-01-012022-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-12-310001105101gigm:RangeTwoMember2023-01-012023-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001105101gigm:RightOfUseAssetsAccumulatedDepreciationMember2023-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2022-12-310001105101gigm:RightOfUseAssetsCostMember2023-01-012023-12-310001105101gigm:AdvancesForPreOrderItemsMember2023-12-310001105101gigm:PcBasedOnlineSportsGamesMember2021-01-012021-12-310001105101gigm:PerformanceBondsMembergigm:RestrictedCashMember2022-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputOptionVolatilityMember2022-01-012022-12-310001105101gigm:MinistryOfFinanceTaiwanMemberMemberus-gaap:LatestTaxYearMember2023-01-012023-12-310001105101gigm:TwoThousandSevenPlanMembersrt:MinimumMember2023-01-012023-12-310001105101country:TW2023-12-310001105101gigm:AdvancesForPreOrderItemsMember2022-12-310001105101us-gaap:CarryingReportedAmountFairValueDisclosureMember2023-12-310001105101srt:MaximumMemberus-gaap:SoftwareDevelopmentMember2023-12-310001105101us-gaap:RetainedEarningsMember2022-12-310001105101srt:MaximumMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMembergigm:RateForEquityInvestmentMember2023-12-310001105101gigm:CapitalizedCostMember2022-12-310001105101srt:MaximumMembergigm:TwoThousandSevenPlanMember2023-12-310001105101gigm:ExtendedAndAmendedLicenseAgreementMemberus-gaap:LicenseMember2022-01-012022-01-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2023-01-012023-12-310001105101gigm:RightOfUseAssetsAccumulatedDepreciationMember2022-01-012022-12-310001105101country:HK2021-01-012021-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MinimumMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMembergigm:RateForEquityInvestmentMember2023-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2022-01-012022-12-310001105101us-gaap:AccumulatedTranslationAdjustmentMember2020-12-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-01-012021-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:DebtSecuritiesMemberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2022-01-012022-12-310001105101country:TWus-gaap:PensionPlansDefinedBenefitMembersrt:MinimumMember2023-01-012023-12-310001105101gigm:CapitalizedCostMember2023-01-012023-12-310001105101country:HK2023-12-310001105101gigm:OfficeFurnitureAndEquipmentMembersrt:MinimumMember2023-12-310001105101gigm:RpgsMember2021-01-012021-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2022-12-310001105101gigm:TwoThousandSevenPlanMemberus-gaap:RestrictedStockUnitsRSUMembersrt:MinimumMember2023-01-012023-12-310001105101us-gaap:InlandRevenueHongKongMember2023-01-012023-12-310001105101gigm:UnusedVirtualPointsMember2022-12-310001105101country:TW2022-01-012022-12-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2022-01-012022-12-310001105101us-gaap:PensionPlansDefinedBenefitMemberus-gaap:OperatingExpenseMember2022-01-012022-12-310001105101gigm:RpgsMember2022-01-012022-12-310001105101srt:MaximumMembergigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2022-12-310001105101srt:MinimumMembergigm:TwoThousandFourPlanMember2023-01-012023-12-310001105101gigm:MahJongAndCasinoCasualGamesMember2023-01-012023-12-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-12-310001105101srt:MinimumMember2022-12-310001105101gigm:RightOfUseAssetsAccumulatedDepreciationMember2022-12-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-01-012023-12-310001105101us-gaap:RetainedEarningsMember2023-01-012023-12-310001105101us-gaap:SeriesBPreferredStockMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2021-11-032021-11-030001105101gigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2022-07-292022-07-290001105101srt:MaximumMembergigm:TwoThousandSevenPlanMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001105101gigm:RightOfUseAssetsCostMember2022-12-310001105101us-gaap:SellingAndMarketingExpenseMember2022-01-012022-12-310001105101srt:MaximumMembergigm:TwoThousandFourPlanMember2023-01-012023-12-310001105101gigm:ConvertibleNotePurchaseAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2020-08-312020-08-310001105101us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMember2022-01-012022-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2023-01-012023-12-310001105101gigm:ConvertibleNoteAmendmentAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-08-312023-08-310001105101gigm:MinistryOfFinanceTaiwanMemberMemberus-gaap:EarliestTaxYearMember2023-01-012023-12-310001105101us-gaap:FairValueMeasurementsRecurringMember2023-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2023-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MinimumMemberus-gaap:MeasurementInputOptionVolatilityMembergigm:RateForEquityInvestmentMember2022-12-310001105101us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2020-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2022-01-012022-12-310001105101gigm:RangeOneMember2023-01-012023-12-310001105101country:HKsrt:MaximumMembergigm:MonthlyPaymentMember2023-01-012023-12-310001105101us-gaap:DomesticCountryMembergigm:UndistributedForeignEarningsMember2023-01-012023-12-310001105101gigm:RightOfUseAssetsAccumulatedDepreciationMember2023-01-012023-12-310001105101us-gaap:SellingAndMarketingExpenseMember2021-01-012021-12-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2022-01-012022-12-310001105101gigm:TwoThousandSixPlanMembersrt:MinimumMember2023-01-012023-12-310001105101us-gaap:SoftwareDevelopmentMembersrt:MinimumMember2023-12-310001105101gigm:OthersMember2021-01-012021-12-310001105101gigm:TwoThousandSixPlanMember2023-01-012023-12-310001105101gigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MinimumMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2022-12-310001105101us-gaap:LicenseMember2023-01-012023-12-3100011051012022-12-310001105101gigm:ConvertibleNotePurchaseAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2020-08-3100011051012021-12-310001105101us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001105101gigm:ConvertibleNoteAmendmentAgreementMembersrt:MinimumMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-08-310001105101gigm:CapitalizedCostMember2023-12-310001105101gigm:ForEachOfFirstFifteenYearsOfServiceMember2023-01-012023-12-310001105101gigm:OthersMember2022-01-012022-12-310001105101srt:MinimumMember2023-12-310001105101gigm:CapitalizedCostMember2022-01-012022-12-310001105101country:TW2023-01-012023-12-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2021-12-310001105101gigm:ConvertiblePromissoryNoteMemberus-gaap:SubsequentEventMembergigm:AeolusRoboticsCorporationMember2024-03-150001105101us-gaap:RetainedEarningsMember2020-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001105101gigm:MahJongAndCasinoCasualGamesMember2021-01-012021-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMemberus-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2022-01-012022-12-310001105101us-gaap:RetainedEarningsMember2021-01-012021-12-310001105101gigm:TrancheTwoMembergigm:ConvertibleNotePurchaseAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2020-08-312020-08-310001105101us-gaap:RetainedEarningsMember2022-01-012022-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMemberus-gaap:AccumulatedTranslationAdjustmentMember2022-01-012022-12-310001105101gigm:ConvertibleNoteAmendmentAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-08-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310001105101gigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMember2022-12-310001105101gigm:RangeTwoMembersrt:MinimumMember2023-12-310001105101gigm:OthersMember2023-01-012023-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMemberus-gaap:AccumulatedTranslationAdjustmentMember2023-01-012023-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputOptionVolatilityMember2023-01-012023-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMemberus-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2023-01-012023-12-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2023-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMembergigm:RateForEquityInvestmentMember2022-12-310001105101us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2021-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMembergigm:RateForEquityInvestmentMember2023-12-310001105101gigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-08-150001105101srt:MaximumMember2022-12-310001105101us-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001105101us-gaap:SeriesBPreferredStockMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2021-11-030001105101gigm:RightOfUseAssetsCostMember2022-01-012022-12-310001105101srt:MinimumMembergigm:OfficePremisesMember2023-12-3100011051012018-01-152018-01-150001105101us-gaap:AccumulatedTranslationAdjustmentMember2021-12-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2021-01-012021-12-310001105101us-gaap:PensionPlansDefinedBenefitMemberus-gaap:OperatingExpenseMember2023-01-012023-12-310001105101country:HK2022-01-012022-12-310001105101srt:MaximumMembergigm:InformationAndCommunicationEquipmentMember2023-12-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-12-310001105101us-gaap:FairValueInputsLevel3Member2023-01-012023-12-310001105101country:TW2021-01-012021-12-310001105101gigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-08-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2022-12-310001105101srt:MaximumMembergigm:TwoThousandSevenPlanMember2023-01-012023-12-310001105101us-gaap:EmployeeStockOptionMembersrt:MinimumMember2023-01-012023-12-310001105101gigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2023-12-310001105101gigm:PerformanceBondsMembergigm:RestrictedCashMember2023-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2020-12-310001105101gigm:PcBasedOnlineSportsGamesMember2022-01-012022-12-310001105101srt:MinimumMembergigm:PrepaidLicensingAndRoyaltyFeesMember2023-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2023-12-310001105101gigm:CapitalizedCostMember2021-12-310001105101gigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MinimumMemberus-gaap:MeasurementInputOptionVolatilityMember2022-12-310001105101us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001105101srt:MaximumMemberus-gaap:EmployeeStockOptionMember2022-01-012022-12-310001105101srt:MaximumMembergigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputOptionVolatilityMember2022-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2023-01-012023-12-310001105101gigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-09-062023-09-060001105101us-gaap:AccumulatedTranslationAdjustmentMember2022-01-012022-12-310001105101gigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMember2023-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembersrt:MinimumMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMembergigm:RateForEquityInvestmentMember2022-12-310001105101srt:MaximumMembergigm:RangeOneMember2023-12-310001105101gigm:TwoThousandSixPlanMembersrt:MaximumMember2023-01-012023-12-310001105101srt:MinimumMemberus-gaap:LicenseMember2023-01-012023-12-310001105101gigm:ConvertibleNotePurchaseAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:TrancheOneMembergigm:AeolusRoboticsCorporationMember2020-08-312020-08-310001105101gigm:RangeThreeMembersrt:MinimumMember2023-12-310001105101srt:MaximumMember2023-12-310001105101srt:MinimumMembergigm:InformationAndCommunicationEquipmentMember2023-12-310001105101us-gaap:SeriesBPreferredStockMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2022-12-310001105101gigm:RangeThreeMembersrt:MaximumMember2023-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-310001105101gigm:TwoThousandFourPlanMember2023-01-012023-12-310001105101us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001105101gigm:DeferredTaxAssetsMember2023-01-012023-12-310001105101gigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2023-08-312023-08-3100011051012020-12-310001105101gigm:PcBasedOnlineSportsGamesMember2023-01-012023-12-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2022-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-3100011051012021-01-012021-12-310001105101us-gaap:AccumulatedTranslationAdjustmentMember2022-12-310001105101gigm:RpgsMember2023-01-012023-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:DebtSecuritiesMemberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMember2023-01-012023-12-310001105101gigm:RightOfUseAssetsCostMember2021-12-310001105101gigm:MahJongAndCasinoCasualGamesMember2022-01-012022-12-310001105101gigm:TwoThousandSevenPlanMember2023-01-012023-12-310001105101us-gaap:InlandRevenueHongKongMember2023-12-310001105101us-gaap:EstimateOfFairValueFairValueDisclosureMember2023-12-3100011051012023-12-310001105101gigm:UnamortizedVirtualItemsMember2022-12-310001105101us-gaap:AccumulatedTranslationAdjustmentMember2023-01-012023-12-310001105101us-gaap:EmployeeStockOptionMember2023-01-012023-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:DebtSecuritiesMemberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMember2022-01-012022-12-310001105101srt:MaximumMemberus-gaap:LicenseMember2023-01-012023-12-310001105101us-gaap:DebtSecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2021-12-310001105101srt:MaximumMembergigm:RangeTwoMember2023-12-310001105101srt:MaximumMembergigm:OfficePremisesMember2023-12-310001105101us-gaap:BankTimeDepositsMemberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001105101us-gaap:BankTimeDepositsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMemberus-gaap:AccumulatedTranslationAdjustmentMember2022-01-012022-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2023-12-310001105101gigm:TwoThousandSixPlanMembersrt:MaximumMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2021-12-3100011051012020-01-082020-01-080001105101us-gaap:EquitySecuritiesMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMember2023-01-012023-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-012022-12-310001105101country:HK2023-01-012023-12-310001105101us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001105101gigm:RangeTwoMember2023-12-310001105101us-gaap:FairValueMeasurementsRecurringMember2022-12-310001105101country:TW2022-12-310001105101gigm:ConvertibleNotePurchaseAgreementMembergigm:ConvertiblePromissoryNoteMembergigm:AeolusRoboticsCorporationMember2020-01-012020-12-310001105101dei:BusinessContactMember2023-01-012023-12-310001105101srt:MaximumMemberus-gaap:EmployeeStockOptionMember2023-01-012023-12-310001105101gigm:OfficePremisesMember2022-12-310001105101us-gaap:AccumulatedTranslationAdjustmentMember2021-01-012021-12-310001105101srt:MaximumMembergigm:PrepaidLicensingAndRoyaltyFeesMember2023-12-310001105101country:HK2022-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:DebtSecuritiesMemberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputDiscountRateMember2023-01-012023-12-310001105101country:TWsrt:MaximumMembergigm:MonthlyPaymentMember2023-01-012023-12-310001105101gigm:MinistryOfFinanceTaiwanMemberMember2023-12-3100011051012022-01-012022-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembergigm:RateForEquityInvestmentMemberus-gaap:MeasurementInputOptionVolatilityMember2023-12-310001105101us-gaap:CarryingReportedAmountFairValueDisclosureMember2022-12-310001105101gigm:RangeOneMember2023-12-310001105101us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2022-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:DebtSecuritiesMemberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputOptionVolatilityMember2022-01-012022-12-310001105101gigm:TwoThousandSixPlanMembersrt:MaximumMember2023-12-310001105101srt:MaximumMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMembergigm:RateForEquityInvestmentMemberus-gaap:MeasurementInputOptionVolatilityMember2022-12-310001105101us-gaap:EmployeeStockOptionMember2021-01-012021-12-310001105101gigm:RightOfUseAssetsAccumulatedDepreciationMember2021-12-310001105101us-gaap:BankTimeDepositsMemberus-gaap:FairValueInputsLevel2Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001105101us-gaap:PensionPlansDefinedBenefitMemberus-gaap:OperatingExpenseMember2021-01-012021-12-310001105101us-gaap:EquitySecuritiesMemberus-gaap:AvailableforsaleSecuritiesMember2023-01-012023-12-310001105101country:TWus-gaap:PensionPlansDefinedBenefitMember2023-01-012023-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2023-01-012023-12-310001105101us-gaap:LeaseholdImprovementsMember2023-01-012023-12-310001105101us-gaap:EmployeeStockOptionMembersrt:MinimumMember2021-01-012021-12-310001105101us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-01-012021-12-310001105101us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001105101country:CN2022-12-310001105101srt:MaximumMember2023-01-012023-12-310001105101us-gaap:CommonStockIncludingAdditionalPaidInCapitalMember2023-12-310001105101gigm:OfficePremisesMember2023-12-310001105101us-gaap:FairValueInputsLevel3Memberus-gaap:DebtSecuritiesMemberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputOptionVolatilityMember2023-01-012023-12-310001105101gigm:UnusedVirtualPointsMember2023-12-310001105101us-gaap:EmployeeStockOptionMember2022-01-012022-12-310001105101us-gaap:BankTimeDepositsMemberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001105101us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2023-12-310001105101gigm:RightOfUseAssetsCostMember2023-12-310001105101us-gaap:RetainedEarningsMember2021-12-310001105101gigm:ForEachYearOfServiceThereafterMember2023-01-012023-12-310001105101srt:MaximumMembergigm:OfficeFurnitureAndEquipmentMember2023-12-310001105101us-gaap:RetainedEarningsMember2023-12-310001105101gigm:PrepaidLicensingAndRoyaltyFeesMember2020-12-310001105101us-gaap:EmployeeStockOptionMembersrt:MinimumMember2022-01-012022-12-310001105101srt:MaximumMemberus-gaap:EmployeeStockOptionMember2021-01-012021-12-310001105101gigm:RateForDebtInvestmentMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMemberus-gaap:MeasurementInputOptionVolatilityMember2023-12-310001105101us-gaap:AccumulatedTranslationAdjustmentMember2023-12-310001105101gigm:UnamortizedVirtualItemsMember2023-12-310001105101country:HK2023-01-012023-12-31xbrli:puregigm:Segmentxbrli:sharesiso4217:HKDiso4217:TWDiso4217:USDgigm:Vote

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM 20-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 000-30540

GIGAMEDIA LIMITED

(Exact name of registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

REPUBLIC OF SINGAPORE

(Jurisdiction of incorporation or organization)

8 TH FLOOR, NO. 22, LANE 407, SECTION 2 TIDING BOULEVARD, TAIPEI 114-740, taiwan, R.O.C.

(Address of principal executive offices)

CHENG-MING HUANG, Chief Executive Officer

8 TH FLOOR, NO. 22, LANE 407, SECTION 2 TIDING BOULEVARD, TAIPEI 114-740, Taiwan, R.O.C.

Tel: 886-2-2656-8000; Fax: 886-2-2656-8003

Securities registered or to be registered pursuant to Section 12(b) of the Exchange Act:

|

|

|

Title of Each Class |

Trading Symbol |

Name of Each Exchange on Which Registered |

Ordinary Shares |

GIGM |

The Nasdaq Stock Market LLC |

Securities registered or to be registered pursuant to Section 12(g) of the Exchange Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

11,052,235 ordinary shares

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this annual report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S–T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.:

|

|

|

|

|

Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

Non-accelerated filer |

☒ |

|

Emerging growth company |

☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards

Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that require a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

|

|

|

|

|

|

U.S. GAAP |

☒ |

|

International Financial Reporting Standards as issued by the International Accounting Standards Board |

☐ |

Other |

☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

|

|

|

|

|

|

Auditor Firm Id: |

1060 |

Auditor Name: |

Deloitte & Touche |

Auditor Location: |

Taipei, Taiwan |

TABLE OF CONTENTS

CERTAIN TERMS AND CONVENTIONS

In this annual report, all references to

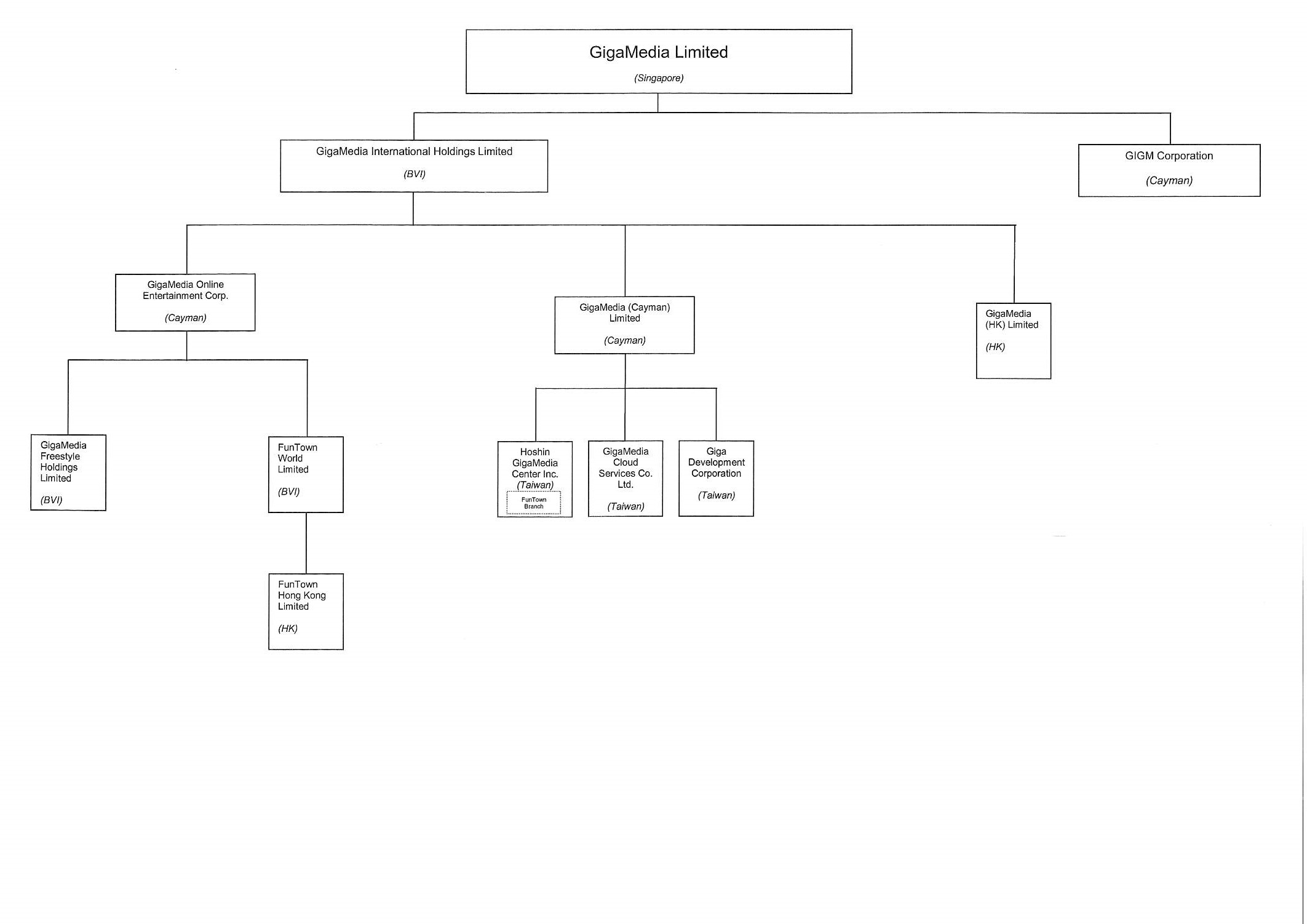

(i)“we,” “us,” “our,” “our Company” or “GigaMedia” are to GigaMedia Limited and, unless the context requires otherwise, its subsidiaries, or where the context refers to any time prior to the incorporation of any of its subsidiaries, the businesses which predecessors of the present subsidiaries were engaged in and which were subsequently assumed by such subsidiaries;

(ii)“Shares” are to ordinary shares of our Company;

(iii)“FunTown” are to our digital entertainment service business operated through our two operating subsidiaries, Hoshin GigaMedia and FunTown World Limited;

(iv)“GigaMedia Cloud” are to GigaMedia Cloud Services Co. Ltd., a wholly owned subsidiary incorporated under the laws of Taiwan, Republic of China (“Taiwan” or “R.O.C.”);

(v)“Hoshin GigaMedia” are to Hoshin GigaMedia Center Inc., a wholly owned subsidiary incorporated under the laws of Taiwan; and

(vi)“Aeolus” are to Aeolus Robotics Corporation, a private company incorporated in the Cayman Islands (“Cayman”).

For the purpose of this annual report only, geographical references to “China” and the “PRC” are to the People’s Republic of China and do not include Taiwan, the Hong Kong Special Administrative Region (“Hong Kong”) or the Macau Special Administrative Region (“Macau”). Except if the context otherwise requires, and for the purpose of this annual report only, references to “Greater China” include the PRC, Taiwan, Hong Kong and Macau. References to “Korea” or “South Korea” are to the Republic of Korea.

All references in this annual report to “U.S. dollar,” “$” or “US$” are to the legal currency of the United States; all references to “NT dollar” or “NT$” are to the legal currency of Taiwan; all references to “RMB,” “Rmb” or “Renminbi” are to the legal currency of the PRC; all references to “Hong Kong dollar” or “HK$” are to the legal currency of Hong Kong; all references to “Korean won” or “KRW” are to the legal currency of the Republic of Korea and all references to “Singapore dollar” or “S$” are to the legal currency of the Republic of Singapore.

The functional currency of each individual consolidated entity is determined based on the primary economic environment in which the entity operates. While our Company’s consolidated financial statements are presented in U.S. dollars, a large portion of our operations are conducted through subsidiaries located in Taiwan, and therefore adopt NT dollars as their functional currency. Assets and liabilities reported in our consolidated balance sheets denominated in currencies other than U.S. dollars are translated into U.S. dollars using year-end exchange rates. With respect to NT dollars, the year-end exchange rates used are 30.705, 30.71 and 27.68 to one U.S. dollar as of December 31, 2023, 2022 and 2021, respectively, which are each based on the middle rate quoted by the Bank of Taiwan. Income and expense items reported in our consolidated statements of operations denominated in currencies other than U.S. dollars are translated into U.S. dollars using average exchange rates. Certain other operating financial information denominated in currencies other than U.S. dollars, not included in our consolidated financial statements and provided in this annual report, are translated using average exchange rates.

We have approximated certain numbers in this annual report to their closest round numbers or a given number of decimal places. Due to rounding, figures shown as totals in tables may not be arithmetic aggregations of the figures preceding them.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes “forward-looking statements” within the meaning of, and intended to qualify for the safe harbor from liability established by, the United States Private Securities Litigation Reform Act of 1995. These statements, which are not statements of historical fact, may consist of or contain estimates, assumptions, projections and/or expectations regarding future events, which may or may not occur. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Some of the risks are listed under Item 3, “Key Information — D. Risk Factors” and elsewhere in this annual report. In some cases, you can identify these forward-looking statements by words such as “aim,” “anticipate,” “believe,” “consider,” “continue,” “estimate,” “expect,” “forecast,” “going forward,” “intend,” “ought to,” “plan,” “potential,” “predict,” “project,” “propose,” “seek,” “can,” “could,” “may,” “might,” “will,” “would,” “should,” “shall,” “is likely to” or similar expressions, including their negatives. These forward-looking statements include, without limitation, statements relating to:

•our business plan and strategies;

•our future business development and potential financial condition, results of operations and other projected financial information;

•our ability to manage current and potential future growth;

•expected continued acceptance of our revenue model;

•our plans for strategic partnerships, licenses and alliances;

•our acquisitions and strategic investments, and our ability to successfully integrate any acquisitions into our operations;

•our ability to protect our intellectual property rights and the security of our customers’ information;

•the launch of new digital entertainment services according to our timetable;

•expected continued acceptance of our digital entertainment services, including expected growth of the digital entertainment industry, and consumer preferences for our products and services;

•the in-house development of new digital entertainment products;

•our plans to license additional digital entertainment products from third parties, and the launch of these new products, including the timing of any such development, licenses or launches, in various geographic markets;

•our ability to maintain and strengthen our position as one of the largest online MahJong operators in Taiwan;

•changes in the competitive environment in which we operate, including the potential entry of new competitors in any of our business lines;

•the outcome of ongoing, or any future, litigation or arbitration;

•our corporate classification by various governmental entities;

•fluctuations in foreign currency rates, in particular, any material appreciation of the NT dollar against the U.S. dollar, and our ability to manage such risks;

•the political stability of our local region; and

•general local and global economic conditions and the impact of geopolitical tensions on such conditions.

These forward-looking statements are based on our own information and on information from other sources we believe to be reliable. Our actual results may differ materially from those expressed or implied by these forward-looking statements as a result of risk factors and other factors noted throughout this annual report, including those described under Item 3, “Key Information — D. Risk Factors” and those detailed from time to time in other filings with the United States Securities and Exchange Commission (the “SEC”). We do not guarantee that the transactions and events described in this annual report will happen as described or that they will happen at all. We undertake no obligation to update or revise any forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events. Whether actual results will conform to our expectations and predictions is subject to a number of risks and uncertainties, many of which are beyond our control, and reflect future business decisions that are subject to change. Given this level of uncertainty, you are advised not to place undue reliance on such forward-looking statements.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Related to Our Business and Industry

We may not be successful in operating and improving our existing digital entertainment services to satisfy the changing demands and preferences of consumers.

The level of demand and market acceptance of our existing digital entertainment services is subject to a high degree of uncertainty. Our future operating results will depend on numerous factors, many of which are beyond our control. These factors include:

•the popularity of existing and new digital entertainment services operated by us;

•the introduction of new digital entertainment services by us or third parties, competing with or replacing our existing services;

•general economic conditions, particularly economic conditions adversely affecting discretionary consumer spending;

•changes in our customer demands and preferences;

•regulatory and other risks associated with our operations in Taiwan and Hong Kong;

•the availability of other forms of amusement and entertainment; and

•critical reviews and public tastes and preferences, all of which change rapidly and cannot be predicted.

Our ability to plan for product development and distribution and promotional activities will be significantly affected by how well we anticipate and adapt to relatively rapid changes in consumer tastes and preferences. Currently, a substantial portion of our digital entertainment services revenue is derived from revenues from PC-based online games including MahJong games and other casual games offered in Taiwan and Hong Kong by FunTown and the licensed online games such as Tales Runner, a multi-player sports game, and Yume100, a single player role-playing game. In recent years, revenues from our PC-based games have been largely flat or declining, reflecting the overall shift in player preferences, and the lack of growth momentum in PC-based games. This decline in the popularity of PC-based online games, and declines in the popularity of online games in general, is likely to adversely affect our business, financial condition and results of operations. To maintain competitiveness of our digital entertainment services, we must regularly invest in enhancing, improving, expanding or upgrading our services. If we fail to do so, revenues generated from our existing services will likely decline.

As our services are currently accessed primarily through PC and, increasingly, mobile devices, successful development of services for such devices will be imperative if we are to maintain or increase our revenues, and our inability to do so may result in lower growth of or a decline in revenues.

Devices other than personal computers, such as mobile phones and tablets, are used increasingly to access the Internet. We believe that, for our business to be successful, we will need to develop versions of our existing digital entertainment offerings, our pipeline offerings and any future offerings that work well with such devices. Manufacturers of such devices may establish restrictive conditions for developers of applications to be used on such devices, and as a result our offerings may not work well, or at all, on such devices. As new devices are released or updated, we may encounter problems in developing versions of our offerings for use on such devices and we may need to devote significant resources to the creation, support, and maintenance of games for such devices. If we are unable to successfully expand the types of devices on which our existing and future offerings are available, or if the versions of our offerings that we create for such devices do not function well or are not attractive to consumers, our revenues may fail to grow and may decline.

The digital entertainment industry is characterized by rapid technological change, and failure to respond quickly and effectively to new Internet technologies or standards may have a material adverse effect on our business.

The digital entertainment industry is evolving rapidly. Any new technologies or new standards may require increases in expenditures for development and operations. In addition, we use internally developed software systems that support nearly all aspects of our billing and payment transactions in our digital entertainment service business. All of our businesses may be adversely affected if we are unable to upgrade our systems effectively to accommodate future traffic levels, to avoid obsolescence or to successfully integrate any newly developed or acquired technology with our existing systems. Capacity constraints could cause unanticipated system disruptions and slower responses, which could adversely affect data transmission and service experience. These factors could, among other things, cause us to lose existing or potential users and existing or potential service development partners.

In operating our digital entertainment service business, we may fail to launch new products according to our timetable, and our new products may not be commercially successful.

In order for our digital entertainment service business strategy to succeed over time, we will need to license, acquire or develop new digital entertainment products that can generate additional revenue and further diversify our revenue sources. A number of factors, including technical difficulties, government approvals and licenses of intellectual property rights required for launching new products, lack of sufficient development personnel and other resources, and adverse developments in our relationship with the licensors of our new licensed products could result in delay in launching our new products. Therefore, we cannot assure you that we will be able to meet our timetable for new launches.

There are many factors that may adversely affect the popularity of our new products. For example, we may fail to anticipate and adapt to future technical trends and new business models, fail to satisfy consumer preferences and requirements, fail to effectively plan and organize marketing and promotion activities, fail to effectively detect and prevent programming errors or defects in the products, and fail to operate our new products at acceptable costs. We cannot assure you that our new products will gain market acceptance and become commercially successful. If we are not able to license, develop or acquire additional digital entertainment products that are commercially successful, our future revenues and profitability may decline.

Our digital entertainment service business faces intense competition, which may adversely affect our revenues, profitability and planned business expansion.

The digital entertainment market is highly competitive. Online game operators in Taiwan and Hong Kong are currently our primary competitors. Our major competitors in Taiwan and Hong Kong include Soft-World International Corporation (“Soft-World”), International Games System, Co., Ltd. (“IGS”), UserJoy Technology Co., Ltd. (“UserJoy”) and GodGame Inc. (“GodGame”). In addition, we compete for users against various offline amusement and entertainment, such as console games, arcade games and handheld games, as well as various other forms of traditional or online entertainment.

We expect more digital entertainment service providers to enter the markets where we operate, and a wider range of digital entertainment products to be introduced to these markets, given the relatively low entry barriers to the digital entertainment industry and the increasing popularity of Internet-based businesses. Our competitors vary in size and include private and public companies, many of which have greater financial, marketing and technical resources as well as name brand recognition than us. We intend to continue to enhance our market position through providing competitive products and quality services that meet market trends and users’ preferences, as well as strengthening sales effectiveness. As a result of the above, significant competition may reduce the number of our users or the growth rate of our user base, reduce the average hours spent on our services, or cause us to reduce usage fees. All of these competitive factors could have a material adverse effect on our business, financial condition and results of operations.

Our results of operations are subject to significant fluctuations. We have incurred operating and net losses in past years, and we may experience losses in the future.

Our revenues, expenses and results of operations have varied in the past and may fluctuate significantly in the future due to a variety of factors, many of which are beyond our control. In 2023, 2022 and 2021, we incurred consolidated operating losses of US$3.2 million, US$3.0 million and US$4.0 million as well as net losses of US$3.4 million, US$2.8 million and US$3.4 million, respectively. Our future profitability will depend to a great extent upon the performance of our digital entertainment service business, as well as certain non-operating aspects. The key factors affecting our businesses or profitability include:

•our ability to retain existing users;

•attracting new users and maintaining user satisfaction;

•the pace of rolling out new offerings or updating existing ones by us or our competitors;

•the amount and timing of operating costs and capital expenditures relating to our business operations and expansion;

•seasonal trends in Internet use;

•price competition in the industry;

•regulatory and other risks associated from our operations in Taiwan and Hong Kong;

•interest rate regarding our time deposits; and

•operational and financial prospects of our investees, specifically Aeolus.

In addition, our operating expenses are based on our expectations of the future demand for our services and are relatively fixed in the short term. We may be unable to adjust spending quickly enough to offset any unexpected demand shortfall. A decrease in revenues in relation to our expenses could have a material and adverse effect on our business, results of operations and financial condition. You should not place undue reliance on year-to-year or quarter-to-quarter comparisons of our results of operations as indicators of our future performance and we cannot assure you that we will not experience operating or net losses in future periods.

Our business strategy, which contemplates growth through acquisitions and strategic investments, exposes us to significant risks.

We have pursued and may continue to pursue growth through acquisitions and strategic investments. Any acquisition or investment is subject to a number of risks. Such risks include the diversion of management time and resources, disruption of our ongoing business, lack of familiarity with new markets, difficulties in supporting the acquired business, and dilution to existing stockholders if our common stock is issued in consideration for an acquisition or investment, incurring or assuming indebtedness or other liabilities in connection with an acquisition. For any business expansion into an industry that is very different from the one in which we currently operate, we may face financial challenges and difficulties arising from a very different cost structure and business model; we may also be exposed to a very different set of labor relations, technological, environmental, regulatory and other non-market risks associated with any new industry we seek to enter.

We entered into multiple strategic alliances in the past and later recognized related impairment losses on investments and goodwill. We may incur debts in the future upon an acquisition or suffer losses related to impairment of these investments. We will continue to examine the merits, risks and feasibility of potential transactions, and expect to explore additional acquisition opportunities in the future. Such examination and exploration efforts, and any related discussions with third parties, may or may not lead to future acquisitions and investments. We may not be able to complete acquiring or investing transactions that we initiate. Our ability to grow through such acquisitions and investments will depend on many factors, including the availability of suitable acquisition candidates at an acceptable cost, our ability to reach agreement with acquisition candidates or investee companies on commercially reasonable terms, the availability of financing to complete transactions and our ability to obtain any required governmental approvals.

We also face challenges in integrating any acquired business. These challenges include eliminating redundant operations, facilities and systems, coordinating management and personnel, retaining key employees, managing different corporate cultures, maintaining the relationship with the suppliers, vendors and/or distributors of acquired businesses, and achieving cost reductions and cross-selling opportunities. There can be no assurance that we will be able to successfully integrate all aspects of acquired businesses. The process of integrating the acquired business may disrupt our business and divert our resources, including the resources of our management. In addition, the benefits of an acquisition or investment transaction may take considerable time to be fully realized and we cannot assure you that any particular acquisition or investment and the subsequent integration will produce the intended benefits.

Further, our business could be adversely impacted by the performance of our investments in other entities. Our investments may generate significant losses arising from factors that may be out of our control, such as economic downturns, geopolitical tensions and macroeconomic volatility. We may incur impairment charges in respect of our equity investees and investments in debt securities, which may affect our results of operations. With respect to equity method investees, if any, we may be required to share a portion of such investees’ losses in accordance with U.S. GAAP. In each case, our results of operations may be adversely impacted if our investments do not perform.

Our business could suffer if we do not successfully achieve and manage current growth and potential future growth.

We are pursuing a number of growth strategies. Some of these strategies relate to services, products or markets in which we lack experience and expertise. Anticipated expansion of our operations will place a significant strain on our management, operation systems and resources. In addition to training and managing our workforce, we will need to continue to develop and improve our financial and management controls and our reporting systems and procedures, including those of acquired businesses. We cannot assure you that we will be able to effectively manage the growth of our operations, and any failure to do so may limit our future growth and materially and adversely affect our business, financial condition and results of operations.

Undetected programming errors or defects in our software, services and games and the proliferation of cheating programs could materially and adversely affect our digital entertainment service business, financial condition and results of operations.

Our digital entertainment services may contain undetected programming errors or other defects. These errors or other defects could damage our reputation and subject us to liability. As to online games, parties unrelated to us may develop cheating programs that enable users to acquire superior features for their game characters that they would not have otherwise. Furthermore, certain cheating programs could cause the loss of a character’s superior features acquired by a user. The occurrence of undetected errors or defects in our digital entertainment services, and our failure to discover and disable cheating programs affecting the fairness of our service environment, could disrupt our operations, damage our reputation and ruin our users’ experiences. As a result, such errors, defects and cheating programs could materially and adversely affect our business, financial condition and results of operations. If such errors, defects and cheating programs occur in software, services and games we operate, our business operations and, in turn, our business and financial condition, could be materially and adversely affected.

Increased energy costs, power outages, and limited availability of electrical resources may adversely affect our operating results.

Our data centers are susceptible to increased costs of power and to electrical power outages. Our customer contracts do not contain provisions that would allow us to pass on any increased costs of energy to our customers, which could affect our operating margins. Any increases in the price of our services to recoup these costs could not be implemented until the end of a customer contract term. Further, power requirements at our data centers are increasing as a result of the increasing power demands of today’s servers. Increases in our power costs could impact our operating results and financial condition. Since we rely on third parties to provide our data centers with power sufficient to meet our needs, our data centers could have a limited or inadequate amount of electrical resources necessary to meet our customer requirements. We attempt to limit exposure to system downtime due to power outages by using backup generators and power supplies. However, these protections may not limit our exposure to power shortages or outages entirely. Any system downtime resulting from insufficient power resources or power outages could damage our reputation and lead us to lose current and potential customers, which would harm our operating results and financial condition.

We may need additional capital in the future, and it may not be available on acceptable terms.

The development of our business may require significant additional capital in the future to:

•enhance and expand the range of products and services we offer; and

•respond to competitive pressures and perceived opportunities, such as investment, acquisition and international expansion activities.

We cannot assure you that additional financing will be available on terms favorable to us, if at all. If adequate funds are not available on acceptable terms, we may be forced to curtail or cease our operations. Moreover, even if we are able to continue our operations, any failure to obtain additional financing could have a material and adverse effect on our business, financial condition and results of operations, and we may need to delay the deployment of our services. See Item 5, “Operating and Financial Review and Prospects — B. Liquidity and Capital Resources.”

Risks Related to Our Reliance on Third Parties

Dependence on network suppliers may adversely affect our operating results.

Our success depends in part upon the capacity, reliability, and performance of our network infrastructure, including the capacity leased from our Internet bandwidth suppliers. We depend on these companies to provide uninterrupted and error-free service through their telecommunications networks. We exercise little control over these providers, which increases our vulnerability to problems with the services they provide. We have experienced and expect to continue to experience interruptions or delays in network service. Any failure on our part or the part of our third-party suppliers to achieve or maintain high data transmission capacity, reliability or performance could significantly reduce customer demand for our services and damage our business. As our customer base grows and their usage of telecommunications capacity increases, we will be required to make additional investments in our capacity to maintain adequate data transmission speeds, the availability of which may be limited or the cost of which may be on terms unacceptable to us. If adequate capacity is not available to us as our customers’ usage increases, our network may be unable to achieve or maintain sufficiently high data transmission capacity, reliability or performance. In addition, our business would suffer if our network suppliers increased the prices for their services and we were unable to pass along the increased costs to our customers.

We rely on Google Cloud for certain of our mobile-based digital entertainment services. Any disruption of or interference with our use of the Google Cloud operation would negatively affect our operations and seriously harm our business.

Google provides a distributed computing infrastructure platform for business operations, or what is commonly referred to as a “cloud” computing service, and we currently rely on Google Cloud for certain of our mobile-based digital entertainment services. Any significant disruption of or interference with our use of Google Cloud would negatively impact our operations and our business would be seriously harmed. If our users are not able to access our products through Google Cloud or encounter difficulties in doing so, we may lose users. The level of service provided by Google Cloud may also impact the usage of and our users’ satisfaction with our products and could seriously harm our business and reputation. If Google Cloud experiences interruptions in service regularly or for a prolonged basis, or other similar issues, our business would be seriously harmed. Hosting costs will also increase as our user base and user engagement grows and may seriously harm our business if we are unable to grow our revenues faster than the cost of utilizing the services of Google or similar providers.

In addition, Google may take actions beyond our control that could seriously harm our business, including:

•discontinuing or limiting our access to its Google Cloud platform;

•increasing pricing terms;

•terminating or seeking to terminate our contractual relationship altogether;

•establishing more favorable relationships with one or more of our competitors; or

•modifying or interpreting its terms of service or other policies in a manner that impacts our ability to run our business and operations.

Google has broad discretion to change and interpret its terms of service and other policies with respect to us, and those actions may be unfavorable to us. Google may also alter how we are able to process data on the Google Cloud platform. If Google makes changes or interpretations that are unfavorable to us, our business would be seriously harmed.

Any failure to maintain a stable and efficient distribution and payment network could have a material and adverse impact on our digital entertainment service business, financial condition and results of operations.

Our digital entertainment service business operation relies heavily on a multi-layer distribution and payment network composed of third-party distributors for our sales to, and collection of payment from, our users. As we do not enter into long-term agreements with any of our distributors, we cannot assure you that we will continue to maintain favorable relationships with them. If we fail to maintain a stable and efficient distribution and payment network, our business, financial condition and results of operations could be materially and adversely affected.

In addition, our ability to process electronic commerce transactions depends on bank processing and credit card systems. In order to prepare for certain types of system problems, we have a formal disaster recovery plan. Nevertheless, any system failure, including network, software or hardware failure, which causes a delay or interruption in our e-commerce services could have a material adverse effect on our business, revenues, results of operations and financial condition.

Risks Related to Intellectual Property

We may be subject to claims of intellectual property right infringement by third parties, which could subject us to significant liabilities and other costs.

Our success depends largely on our ability to use and develop our technology and know-how without infringing upon the intellectual property rights of third parties. There has been substantial litigation in the various segments of the technology, PC application and mobile application markets, including with respect to the online content, electronics, and related industries regarding intellectual property rights. From time to time, third parties may claim infringement by us of their intellectual property rights. Our broad range of application of current technology and technology under development increases the likelihood that third parties may claim infringement by us of their intellectual property rights. The validity and scope of claims relating to the intellectual property may involve complex scientific, legal and factual questions and analysis, and tend to be uncertain. If third parties assert copyright or patent infringement or violation of other intellectual property rights against us, we will have to defend ourselves in legal or administrative proceedings, which can be costly and time consuming and may significantly divert the efforts and resources of our technical and management personnel. An adverse determination in any such proceedings to which we may become a party could subject us to significant liability to third parties, require us to seek licenses from third parties, or prevent us from selling our products and services. The imposition of liabilities that are not covered by insurance, in excess of insurance coverage or for which we are not indemnified by a content provider, could have a material adverse effect on our business, results of operations and financial condition.

Certain technologies necessary for us to provide our services may, in fact, be patented by other parties either now or in the future. If such technology were held under patent by another person, we would have to negotiate a license for the use of that certain technology. We may not be able to negotiate such a license at a price that is acceptable. The existence of such patents, or our inability to negotiate a license for any such technology on acceptable terms, could force us to cease using such technology and offering products and services incorporating such technology. If we were found to be infringing on the intellectual property rights of any third party in lawsuits or other claims and proceedings that may be asserted against us in the future, we could be subject to liabilities for such infringement, which could be material. We could also be required to refrain from using, manufacturing or selling certain products or using certain processes, either of which could have a material adverse effect on our business and operating results. From time to time, we may receive in the future, notices of claims of infringement, misappropriation or misuse of other parties’ proprietary rights. We cannot assure you that we will always prevail in these discussions and actions or that other actions alleging infringement by us of third-party patents will not be asserted or prosecuted against us. Furthermore, lawsuits like these may require significant time and expense to defend, may divert management’s attention away from other aspects of our operations and, upon resolution, may have an adverse effect on our business, results of operations, financial condition and cash flows.

We may need to incur significant expenses to protect our intellectual property rights, and if we are unable to adequately protect our intellectual property rights, our competitive position could be harmed.

We regard our copyrights, service marks, trademarks, trade secrets, patents and other intellectual property as critical to our success. We rely on a combination of copyright and trademark laws, trade secret protection, confidentiality and non-disclosure agreements, and other contractual provisions to protect our proprietary software, trade secrets and similar intellectual property. We have patents, copyrights and trademarks in certain jurisdictions and may apply for further trademark and copyright registrations and additional patents, which may provide such protection in relevant jurisdictions. However, we cannot assure you that our efforts will prove to be sufficient or that third parties will not infringe upon or misappropriate our proprietary rights. Unauthorized use of the intellectual property, whether owned by or licensed to us, could adversely affect our business and reputation.

The validity, enforceability and scope of protection of intellectual property in Internet-related industries are evolving, and therefore, uncertain. In particular, the laws and enforcement procedures of Taiwan and Hong Kong are uncertain or do not protect intellectual property rights to the same extent as the laws and enforcement procedures of the United States do. We may have to engage in litigation or other legal proceedings to enforce and protect our intellectual property rights, which could result in substantial costs and diversion of our resources, and have a material adverse effect on our business, financial condition and results of operations.

Our future results of operations or the growth of our business may suffer if the licensors of our digital entertainment services fall short of providing us sufficient and continual support for the operation of licensed games.

While we are focused on strengthening our ability to develop our own casual games, we have historically sourced, and may in the future source, casual games, advanced casual games and other forms of digital entertainment services through licensing from developers in various regions where digital entertainment development is relatively established. We depend on our licensors to provide the necessary technical support for the operation of the licensed games as well as expansion packs and upgrades that sustain continuing interest in the games. The licensors’ ability and willingness to continually provide us sufficient support is very critical. Therefore, apart from the ability of our licensors’ continual development of the licensed games, we also need to maintain stable and satisfactory working relationships with our licensors in order to ensure the steady operation of our licensed games and our continued access to upgrades and new content of the games. Our ability to maintain satisfactory working relationships with our licensors may also influence our access to license new products developed by the same or other licensors. If our licensors fall short of providing us sufficient and continual support for the operation of licensed games, or if we are unable to maintain satisfactory relationships with our licensors, our financial condition, results of operations, future profitability and growth prospects may be materially and adversely affected.

Risks Related to Cybersecurity and Technology Infrastructure

Our digital entertainment service business depends on the reliability of the network infrastructure and related services provided by ourselves and third parties, which is subject to physical, technological, security and other risks. We could suffer a loss of revenue and increased costs, exposure to significant liability, reputational harm and other serious negative consequences if we sustain damages, cyber-attacks or other data security breaches that disrupt our operations or result in the dissemination of proprietary or confidential information about us or our customers or other third parties.

The development and operation of our online networks are subject to physical, technological, security and other risks which may result in interruption in service or reduced capacity. These risks include physical damage, power loss, telecommunications failure, capacity limitation, hardware or software failures or defects and breaches of physical and cybersecurity by computer viruses, system break-ins or otherwise. An increase in the volume of usage of online services could strain the capacity of the software and hardware employed to prevent and identify such failures, breaches and attacks, which could result in slower response time or system failures. In particular, our industry has witnessed an increase in the number, intensity and sophistication of cybersecurity incidents caused by hackers and other malicious actors such as foreign governments, criminals, hacktivists, terrorists and insider threats. Hackers and other malicious actors may be able to penetrate our network security and misappropriate or compromise our confidential, sensitive, personal or proprietary information, or that of third parties, and engage in the unauthorized use or dissemination of such information. They may be able to create system disruptions, or cause shutdowns. Hackers and other malicious actors may be able to develop and deploy viruses, worms, ransomware and other malicious software programs that attack our products or otherwise exploit any security vulnerabilities of our systems. In addition, sophisticated hardware and operating system software and applications that we procure from third parties may contain defects in design or manufacture, including “bugs,” cybersecurity vulnerabilities and other problems that could unexpectedly interfere with the operation or security of our systems.

We have a variety of backup servers at our primary site to deal with possible system failures. However, we do not have redundant facilities in the event of an emergency. The occurrence of any of these events could result in interruptions, delays or cessation in service to users of our online services, which could have a material adverse effect on our business and results of operations. We may be required to expend significant capital or other resources to protect against the threat of security breaches and attacks or to alleviate problems caused by such actions, including the following:

•expenses to rectify the consequences of the damage, security breach or cyber attack;

•liability for stolen assets or leaked information;

•costs of repairing damage to our systems;

•lost revenue and income resulting from any system downtime caused by such breach or attack;

•loss of competitive advantage if our proprietary information is obtained by competitors as a result of such breach or attack;

•increased costs of cyber security protection;

•costs of incentives we may be required to offer to our customers or business partners to retain their business; and

•damage to our reputation.

In addition, any compromise of security from a security breach or cyber attack could deter customers or business partners from entering into transactions that involve providing confidential information to us. As a result, any compromise to the security of our systems could have a material adverse effect on our business, reputation, financial condition, and operating results.

Our network may be vulnerable to unauthorized access, computer viruses, denial of service and other disruptive problems. For example, in recent years, we have detected and mitigated incidents of denial-of-service attacks against network providers that affected latency of connections to our games. Such incidents, however, did not result in significant financial impact on our operations and financial results. We have experienced in the past, and may experience in the future, security breaches or attacks. There can be no assurance that any measures implemented will not be circumvented in the future.

The audit committee of the board of directors oversees our cyber risk management and periodically reviews summaries of recent cybersecurity incidents, if any, and updates on the execution of our risk management program, as prepared by our management team. If a material cybersecurity incident were to occur, our board of directors would be responsible for making a prompt assessment of our countermeasures and mitigation actions. See Item 16K, “Cybersecurity” in this annual report.

Our business is also vulnerable to delays or interruptions due to our reliance on infrastructure and related services provided by third parties. End-users of our offerings depend on Internet Service Providers (“ISPs”) and our system infrastructure for access to the Internet games and services we offer. Some of these services have experienced service outages in the past and could experience service outages, delays and other difficulties due to system failures, stability or interruption. For example, prior earthquakes in Taiwan, Indonesia and Japan have caused damage to undersea fiber optic cables linking Malaysia, Singapore, Australia, Japan, South Korea, China, the United States and Europe, causing disruptions in Internet traffic worldwide. We may lose customers as a result of delays or interruption in service, including delays or interruptions relating to high volumes of traffic or technological problems, which may prevent communication over the Internet and could materially adversely affect our business, revenues, results of operations and financial condition.

We could be liable for breaches of security on our web site, fraudulent activities of our users, or the failure of third-party vendors to deliver credit card transaction processing services.

A fundamental requirement for operating our Internet-based, international communications service and electronic billing of our customers is the secure transmission of confidential information and media (such as customers’ credit card numbers and expiration dates, personal information and billing addresses) over public networks. Although we have developed systems and processes that are designed to protect consumer information and prevent fraudulent credit card transactions and other security breaches and are not aware of any breaches of security on our websites having occurred, failure to mitigate such fraud or breaches may expose us to litigation and possible liability for failing to secure confidential customer information and could harm our reputation and ability to attract and retain customers, consequently adversely affect our operating results. The laws relating to the liability of providers of online payment services are currently unsettled and certain jurisdictions may enact their own rules with which we may not comply. We rely on third-party providers to process and guarantee payments made by our subscribers up to certain limits, and we may be unable to prevent our customers from fraudulently receiving goods and services. Our risk of liability will increase if a larger portion of our transactions involve fraudulent or disputed credit card transactions. Any costs we incur as a result of fraudulent or disputed transactions could harm our business. In addition, the functionality of our current billing system relies on certain third-party vendors delivering services. If these vendors are unable or unwilling to provide services, we will not be able to charge for our services in a timely or scalable fashion, which could significantly decrease our revenue and have a material adverse effect on our business, financial condition and operating results.

We may experience losses due to subscriber fraud and theft of service.

Subscribers may obtain access to our service without paying for service by unlawfully using our authorization codes or by submitting fraudulent credit card information. To date, no material losses from unauthorized credit card transactions and theft of service have occurred. We have implemented anti-fraud procedures in order to control losses relating to these practices, but these procedures may not be adequate to effectively limit all of our exposure in the future from fraud. If our procedures are not effective, consumer fraud and theft of service could significantly decrease our revenue and have a material adverse effect on our business, financial condition and operating results.

Risks Related to Legal and Regulatory Compliance

We may face litigation risks and regulatory disputes in the course of our business.