UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: December 31, 2019

Commission file number: 0-21271

SANGUI BIOTECH INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

Colorado | 84-1330732 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

Neuer Wall 54, 20354 Hamburg, Germany

(Address of principal executive offices)

011-49-40-46093120

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of exchange on which registered |

None | N/A | N/A |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer [ ] | Accelerated Filer [ ] |

Non-Accelerated Filer [X] | Smaller Reporting Company [X] |

Emerging Growth Company [ ] |

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of February 13, 2020, there were 202,783,598 shares of the issuer's Common Stock, no par value, issued and 202,729,842 shares outstanding.

SANGUI BIOTECH INTERNATIONAL, INC.

Quarterly Report on Form 10-Q

For the Quarterly Period Ended December 31, 2019

INDEX

PART I – FINANCIAL INFORMATION

|

| |

Item 1 | Financial Statements .............................................................................................................................. | 1 |

Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations ................ | 13 |

Item 3. | Quantitative and Qualitative Disclosure About Market Risk ................................................................ | 16 |

Item 4. | Controls and Procedures ........................................................................................................................ | 16 |

PART II – OTHER INFORMATION

|

| |

Item 1. | Legal Proceedings................................................................................................................................. | 17 |

Item 1A. | Risk Factors........................................................................................................................................... | 17 |

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds .............................................................. | 17 |

Item 3. | Defaults Upon Senior Securities ........................................................................................................... | 17 |

Item 5. | Other Information.................................................................................................................................. | 17 |

Item 6. | Exhibits.................................................................................................................................................. | 18 |

ii

PART I - FINANCIAL INFORMATION

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q pursuant to the rules and regulations of the Securities and Exchange Commission and, therefore, do not include all information and footnotes necessary for a complete presentation of our financial position, results of operations, cash flows, and stockholders' deficit in conformity with generally accepted accounting principles in the United States of America. In the opinion of management, all adjustments considered necessary for a fair presentation of the consolidated results of operations and financial position have been included and all such adjustments are of a normal recurring nature.

Our unaudited condensed consolidated balance sheet as of December 31, 2019 and the audited balance sheet as of June 30, 2019, our unaudited condensed consolidated statements of operations and comprehensive loss for the three - and six-month period ended December 31, 2019, and 2018, our stockholders’ equity (deficit) for the three - and six-month periods ended December 31, 2019, and 2018 and our unaudited condensed consolidated statements of cash flows for the six - month period ended December 31, 2019, and 2018 are attached hereto.

1

|

|

|

|

|

|

|

|

|

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||

Condensed Consolidated Balance Sheets | ||||||||

|

|

|

|

|

|

|

|

|

ASSETS | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| December 31, |

| June 30, | ||

|

|

|

| 2019 |

| 2019 | ||

|

|

|

|

| (unaudited) |

|

|

|

CURRENT ASSETS |

|

|

|

| ||||

| Cash |

| $ | 15,395 |

| $ | 27,453 | |

| Prepaid expenses and other assets |

| 16,583 |

|

| 9,470 | ||

| Tax refunds receivable |

|

| 5,517 |

|

| 6,852 | |

| Accounts receivable, net |

|

| 14,508 |

|

| 29,525 | |

| Note receivable, related party |

|

| 985 |

|

| 5,671 | |

|

|

|

|

|

|

|

|

|

|

| Total Current Assets |

| 52,988 |

|

| 78,971 | |

|

|

|

|

|

|

|

|

|

PROPERTY AND EQUIPMENT, Net |

|

|

|

|

|

| ||

| Operating lease right-of-use asset |

| 3,002 |

|

| - | ||

|

|

|

|

|

|

|

|

|

|

| TOTAL ASSETS | $ | 55,990 |

| $ | 78,971 | |

|

|

|

|

|

|

|

|

|

LIABILITIES AND STOCKHOLDERS' DEFICIT | ||||||||

|

|

|

|

|

|

|

|

|

CURRENT LIABILITIES |

|

|

|

| ||||

|

|

|

|

|

|

|

|

|

| Accounts payable and accrued expenses | $ | 125,435 |

| $ | 164,145 | ||

| Accrued interest - related party |

| 34,783 |

|

| 28,458 | ||

| Notes payable - related party |

|

| 538,358 |

|

| 478,357 | |

| Operating lease liability |

|

| 3,002 |

|

| - | |

|

|

|

|

|

|

|

|

|

|

| Total Current Liabilities |

| 701,578 |

|

| 670,960 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STOCKHOLDERS' DEFICIT |

|

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

| Preferred stock, no par value; 10,000,000 shares |

|

|

|

|

| ||

| authorized, -0- shares issued and outstanding | $ | - |

| $ | - | ||

| Common stock, no par value; 250,000,000 shares authorized |

|

|

|

|

| ||

| 201,533,598 and 199,295,503 shares issued and |

|

|

|

|

| ||

| 201,479,842 and 199,241,747 shares outstanding respectively |

| 33,012,261 |

|

| 32,967,499 | ||

| Additional paid-in capital |

|

| 4,513,328 |

|

| 4,513,328 | |

| Treasury stock, at cost |

|

| (19,387) |

|

| (19,387) | |

| Accumulated other comprehensive income |

| 92,212 |

|

| 91,447 | ||

| Accumulated deficit |

|

| (37,600,416) |

|

| (37,503,684) | |

| Total Sangui Biotech International, Inc's stockholders' equity (defict) |

| (2,002) |

|

| 49,203 | ||

| Non-controlling interest |

|

| (643,586) |

|

| (641,192) | |

|

|

|

|

|

|

|

|

|

|

| Total Stockholders' Deficit |

| (645,588) |

|

| (591,989) | |

|

|

|

|

|

|

|

|

|

|

| TOTAL LIABILITIES AND STOCKHOLDERS' DEFICIT | $ | 55,990 |

| $ | 78,971 | |

|

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||

2

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||||||

Condensed Consolidated Statements of Operations and Comprehensive Loss | ||||||||||||

(unaudited) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| For the Three Months Ended |

| For the Six Months Ended | ||||||||

|

| December 31, |

| December 31, | ||||||||

|

| 2019 |

| 2018 |

| 2019 |

| 2018 | ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

REVENUES |

|

|

|

|

|

|

|

|

|

|

| |

| License revenues | $ | 11,683 |

| $ | 44,095 |

| $ | 11,965 |

| $ | 55,367 |

COST OF SALES |

| - |

|

| 26 |

|

| - |

|

| 99 | |

GROSS MARGIN |

| 11,683 |

|

| 44,069 |

|

| 11,965 |

|

| 55,268 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

OPERATING EXPENSES |

|

|

|

|

|

|

|

|

|

|

| |

| Research and development |

| 2,650 |

|

| 7,314 |

|

| 4,886 |

|

| 15,286 |

| Professional fees |

| 37,666 |

|

| 53,282 |

|

| 79,418 |

|

| 103,216 |

| General and administrative |

| 7,900 |

|

| 43,610 |

|

| 20,092 |

|

| 90,401 |

Total Operating Expenses |

| 48,216 |

|

| 104,206 |

|

| 104,396 |

|

| 208,903 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

OPERATING LOSS |

| (36,533) |

|

| (60,137) |

|

| (92,431) |

|

| (153,635) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

OTHER INCOME (EXPENSE) |

|

|

|

|

|

|

|

|

|

|

| |

| Loss on out of court settlement |

| - |

|

| - |

|

| (6,714) |

|

| - |

| Gain (loss) on foreign exchange |

| (15,111) |

|

| 5,395 |

|

| 6,709 |

|

| 6,457 |

| Interest expense |

| (3,477) |

|

| (2,525) |

|

| (6,690) |

|

| (6,216) |

Total other income (expense) |

| (18,588) |

|

| 2,870 |

|

| (6,695) |

|

| 241 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

LOSS BEFORE INCOME TAXESAND NON-CONTROLLING INTEREST |

| (55,121) |

|

| (57,267) |

|

| (99,126) |

|

| (153,394) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Provision for income taxes |

| - |

|

| 1,213 |

|

| - |

|

| 1,213 |

NET LOSS BEFORE NON-CONTROLLING INTEREST |

| (55,121) |

|

| (58,480) |

|

| (99,126) |

|

| (154,607) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| Less: Net loss attributable to non-controlling interest |

| 1,138 |

|

| 2,124 |

|

| 2,394 |

|

| 8,288 |

|

|

|

|

|

|

|

|

|

|

|

|

|

NET LOSS ATTRIBUTABLE TO COMMON STOCKHOLDERS | $ | (53,983) |

| $ | (56,356) |

| $ | (96,732) |

| $ | (146,319) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

OTHER COMPREHENSIVE LOSS |

|

|

|

|

|

|

|

|

|

|

| |

| Foreign currency translation adjustments |

| (2,255) |

|

| (1,721) |

|

| 765 |

|

| (1,336) |

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPREHENSIVE LOSS | $ | (57,376) |

| $ | (60,201) |

| $ | (98,361) |

| $ | (155,943) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| BASIC AND DILUTED LOSS PER SHARE | $ | (0.00) |

| $ | (0.00) |

| $ | (0.00) |

| $ | (0.00) |

| BASIC AND DILUTED WEIGHTED AVERAGE |

|

|

|

|

|

|

|

|

|

|

|

| NUMBER OF SHARES OUTSTANDING |

| 201,533,598 |

|

| 195,147,849 |

|

| 200,819,827 |

|

| 195,007,308 |

|

|

|

|

|

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||||||

3

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||||||||||||||||

Condensded Consolidated Statements of Stockholders' Equity (Deficit) | ||||||||||||||||||||||

(unaudited) | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Three-Month Period Ended December 31, 2018 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

| Additional |

|

|

|

| Other |

| Non- |

|

|

|

|

|

| |||

| Common Stock |

| Paid-In |

| Treasury |

| Comprehensive |

| controlling |

| Accumulated |

|

| |||||||||

| Shares |

| Amount |

| Capital |

| Stock |

| Income (Loss) |

| Interest |

| Deficit |

| Total | |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, October 1, 2018 | 192,951,503 |

| $ | 32,884,893 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 93,306 |

| $ | (628,418) |

| $ | (37,270,071) |

|

| (426,349) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common shares issued for Cash | 5,500,000 |

|

| 63,954 |

|

| - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| 63,954 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock issued for services | 844,000 |

|

| 18,652 |

|

| - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| 18,652 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Currency translation adjustment | - |

|

| - |

|

| - |

|

| - |

|

| (1,721) |

|

| - |

|

| - |

|

| (1,721) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss | - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| (2,124) |

|

| (56,356) |

|

| (58,480) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2018 | 199,295,503 |

| $ | 32,967,499 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 91,585 |

| $ | (630,542) |

| $ | (37,326,427) |

| $ | (403,944) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||||||||||||||||

Condensded Consolidated Statements of Stockholders' Equity (Deficit) | ||||||||||||||||||||||

(unaudited) | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Three-Month Period Ended December 31, 2019 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

| Additional |

|

|

|

| Other |

| Non- |

|

|

|

|

|

| |||

| Common Stock |

| Paid-In |

| Treasury |

| Comprehensive |

| controlling |

| Accumulated |

|

| |||||||||

| Shares |

| Amount |

| Capital |

| Stock |

| Income (Loss) |

| Interest |

| Deficit |

| Total | |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, October 1, 2019 | 201,533,598 |

| $ | 33,012,261 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 94,467 |

| $ | (642,448) |

| $ | (37,546,433) |

| $ | (588,212) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Currency translation adjustment | - |

|

| - |

|

| - |

|

| - |

|

| (2,255) |

|

| - |

|

| - |

|

| (2,255) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss | - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| (1,138) |

|

| (53,982) |

|

| (55,120) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2019 | 201,533,598 |

| $ | 33,012,261 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 92,212 |

| $ | (643,586) |

| $ | (37,600,415) |

|

| (645,587) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||||||||||||||||

4

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||||||||||||||||

Condensed Consolidated Statements of Stockholders' Equity (Deficit) | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Six-Month Period Ended December 31, 2018 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

| Additional |

|

|

|

| Other |

| Non- |

|

|

|

|

|

| |||

| Common Stock |

| Paid-In |

| Treasury |

| Comprehensive |

| controlling |

| Accumulated |

|

| |||||||||

| Shares |

| Amount |

| Capital |

| Stock |

| Income (Loss) |

| Interest |

| Deficit |

| Total | |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, July 1, 2018 | 191,951,503 |

| $ | 32,864,356 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 92,921 |

| $ | (622,254) |

| $ | (37,180,108) |

|

| (351,144) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common shares issued for Cash | 6,500,000 |

|

| 84,491 |

|

| - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| 84,491 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock issued for services | 844,000 |

|

| 18,652 |

|

| - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| 18,652 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Currency translation adjustment | - |

|

| - |

|

| - |

|

| - |

|

| (1,336) |

|

| - |

|

| - |

|

| (1,336) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss | - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| (8,288) |

|

| (146,319) |

|

| (154,607) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2018 | 199,295,503 |

| $ | 32,967,499 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 91,585 |

| $ | (630,542) |

| $ | (37,326,427) |

| $ | (403,944) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||||||||||||||||

Condensed Consolidated Statements of Stockholders' Equity (Deficit) | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Six-Month Period Ended December 31, 2019 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| Accumulated |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

| Additional |

|

|

|

| Other |

| Non- |

|

|

|

|

|

| |||

| Common Stock |

| Paid-In |

| Treasury |

| Comprehensive |

| controlling |

| Accumulated |

|

| |||||||||

| Shares |

| Amount |

| Capital |

| Stock |

| Income (Loss) |

| Interest |

| Deficit |

| Total | |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, July 1, 2019 | 199,295,503 |

| $ | 32,967,499 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 91,447 |

| $ | (641,192) |

| $ | (37,503,684) |

| $ | (591,989) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common stock issued for services | 2,238,095 |

|

| 44,762 |

|

| - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| 44,762 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Currency translation adjustment | - |

|

| - |

|

| - |

|

| - |

|

| 765 |

|

| - |

|

| - |

|

| 765 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net loss | - |

|

| - |

|

| - |

|

| - |

|

| - |

|

| (2,394) |

|

| (96,732) |

|

| (99,126) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance, December 31, 2019 | 201,533,598 |

| $ | 33,012,261 |

| $ | 4,513,328 |

| $ | (19,387) |

| $ | 92,212 |

| $ | (643,586) |

| $ | (37,600,416) |

|

| (645,588) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The accompanying notes are an integral part of these condensed consolidated financial statements. | ||||||||||||||||||||||

5

SANGUI BIOTECH INTERNATIONAL, INC. | ||||||||

Condensed Consolidated Statements of Cash Flows | ||||||||

(unaudited) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| For the Six Months Ended | ||||

|

|

|

| December 31, | ||||

|

|

|

| 2019 |

| 2018 | ||

|

|

|

|

|

|

|

|

|

CASH FLOWS FROM OPERATING ACTIVITIES |

|

|

|

|

| |||

| Net loss |

| $ | (99,126) |

| $ | (154,607) | |

| Adjustments to reconcile net loss to net cash |

|

|

|

|

| ||

| used by operating activities: |

|

|

|

|

| ||

|

| Common stock issued for services |

| - |

|

| 18,652 | |

|

| Common stock issued for obtaining out-of-court settlement |

| 6,714 |

|

| - | |

|

| Foreign currency exchange transactions |

| (6,709) |

|

| (6,457) | |

|

| Amortization of right to use asset |

| (3,532) |

|

| - | |

| Changes in operating assets and liabilities |

|

|

|

|

| ||

|

| Trade accounts receivable |

| 14,418 |

|

| (5,211) | |

|

| Prepaid expenses and other current assets |

| (11,781) |

|

| 747 | |

|

| Tax refunds receivable |

| 1,002 |

|

| (5,735) | |

|

| Accounts payable and accrued expenses |

| 4,386 |

|

| (2,700) | |

|

| Related party advances |

| 5,527 |

|

| 6,160 | |

|

| Related party accounts payable |

| 6,693 |

|

| 3,948 | |

|

| Operationg lease liability |

| 3,532 |

|

| - | |

|

|

| Net Cash Used in Operating Activities |

| (78,876) |

|

| (145,203) |

|

|

|

|

|

|

|

|

|

CASH FLOWS FROM FINANCING ACTIVITIES |

|

|

|

|

| |||

|

| Proceeds from related party note payable |

| 66,342 |

|

| 720,341 | |

|

| Repayment of related party note payable |

| - |

|

| (604,756) | |

|

| Proceeds from common stock issued for cash |

| - |

|

| 84,491 | |

|

| Repayment of notes payable |

| - |

|

| (37,971) | |

|

|

| Net Cash Provided by Financing Activities |

| 66,342 |

|

| 162,105 |

|

|

|

|

|

|

|

|

|

EFFECTS OF EXCHANGE RATES ON CASH |

| 476 |

|

| (1,602) | |||

|

|

|

|

|

|

|

|

|

| NET CHANGES IN CASH |

| (12,058) |

|

| 15,300 | ||

| CASH AT BEGINNING OF PERIOD |

| 27,453 |

|

| 20,943 | ||

|

|

|

|

|

|

|

|

|

| CASH AT END OF PERIOD | $ | 15,395 |

| $ | 36,243 | ||

|

|

|

|

|

|

|

|

|

| CASH FLOW INFORMATION |

|

|

|

|

| ||

| CASH PAID FOR: |

|

|

|

|

| ||

|

| Interest |

| $ | - |

| $ | 2,509 |

|

| Income Taxes | $ | - |

| $ | - | |

|

|

|

|

|

|

|

|

|

| NON - CASH INVESTING AND FINANCING ACTIVITIES |

|

|

|

|

| ||

|

| Right of use operating lease assets obtained in exchange for lease liabilities | $ | 6,504 |

| $ | - | |

|

| Stock issued in settlement of liability | $ | 44,762 |

| $ | - | |

|

|

|

|

|

|

|

|

|

| The accompanying notes are an integral part of these condensed consolidated financial statements.

| |||||||

6

SANGUI BIOTECH INTERNATIONAL, INC.

Notes to the Condensed Consolidated Financial Statements

December 31, 2019 and June 30, 2019

(Unaudited)

NOTE 1 - BASIS OF PRESENTATION

The accompanying condensed consolidated financial statements have been prepared without audit in accordance with accounting principles generally accepted in the United States of America and rules of the Securities Exchange Commission for interim financial information. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been condensed or omitted pursuant to such rules and regulations. The unaudited condensed consolidated financial statements and notes should, therefore, be read in conjunction with the consolidated financial statements and notes thereto in the Company's Form 10-K for the year ended June 30, 2019. In the opinion of management, all adjustments (consisting of normal and recurring adjustments) considered necessary for a fair presentation, have been included. The results of operations for the three - and six-month period ended December 31, 2019 are not necessarily indicative of the results that may be expected for the full fiscal year ending June 30, 2020.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Business

Sangui Biotech International, Inc., (Sangui or the Company) was incorporated in Colorado in 1995 and conducts business through its 90% owned subsidiary, Sangui BioTech GmbH (Sangui GmbH) and its 99.8% owned subsidiary Sangui Know-how und Patentverwertungsgesellschaft mbH & Co. KG (Sangui KG). Sangui GmbH, which is headquartered in Hamburg, Germany, is engaged in the development of artificial oxygen carriers (external applications of hemoglobin, blood substitutes and blood additives) as well as in the development, marketing and sales of cosmetics and wound management products. Sangui KG is a limited partnership that holds the license rights under the various agreements that the Company enters into from time to time.

Consolidation

The consolidated financial statements include the accounts of Sangui BioTech International, Inc. and its subsidiaries. All significant intercompany accounts and transactions have been eliminated in consolidation.

Foreign Currency Translation

Assets and liabilities of the Company's foreign operations are translated into U.S. dollars at period-end exchange rates. Net exchange gains or losses resulting from such translation are excluded from net loss but are included in comprehensive loss and accumulated in a separate component of stockholders' equity (deficit). Income and expenses are translated at average exchange rates for the period.

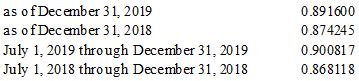

Exchanges rates used for the preparation of the consolidated balance sheet as of December 31, 2019 and June 30, 2019 and our unaudited consolidated statements of operations for the three - and six-month periods ended December 31, 2019 and 2018, were calculated as follows:

The Company accounts for the transactions denominated in foreign currencies in the Parent Company’s books as transaction gains (losses) recognized in Other income.

7

SANGUI BIOTECH INTERNATIONAL, INC.

Notes to the Condensed Consolidated Financial Statements

December 31, 2019 and June 30, 2019

(Unaudited)

Risk and Uncertainties

The Company's line of future pharmaceutical products (artificial oxygen carriers or blood substitute and additives) and medical products (wound dressings and other wound management products) being developed by Sangui GmbH, are deemed as medical devices or biologics, and as such are governed by the Federal Food and Drug and Cosmetics Act and by the regulations of state agencies and various foreign government agencies. The pharmaceuticals, under development in Germany, will be subject to more stringent regulatory requirements, because they are in vivo products for humans. The Company and its subsidiaries have no experience in obtaining regulatory clearance on these types of products. Therefore, the Company will be subject to the risks of delays in obtaining or failing to obtain regulatory clearance.

Going Concern

The accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern, which contemplates, among other things, the realization of assets and satisfaction of liabilities in the normal course of business. The Company has accumulated deficit of $37,600,416 as of December 31, 2019. The Company incurred a net loss before non-controlling interest of $99,126 for the six months ended December 31, 2019 and used cash in operating activities of $78,876 during the six months ended December 31, 2019. These conditions raise substantial doubt about the Company's ability to continue as a going concern for a period of one year from issuance of the financial statements. The Company expects to continue to incur significant capital expenses in pursuing its business plan to market its products and expand its product line, while obtaining additional financing through stock offerings or other feasible financing alternatives. In order for the Company to continue its operations at its existing levels, the Company will require significant additional funds over the next twelve months. Therefore, the Company is dependent on funds raised through equity or debt offerings. Additional financing may not be available on terms favorable to the Company, or at all. If these funds are not available, the Company may not be able to execute its business plan or take advantage of business opportunities. The ability of the Company to obtain such additional financing and to achieve its operating goals is uncertain. In the event that the Company does not obtain additional capital, is not able to collect its outstanding receivables, or is not able to increase cash flow through the increase of sales, there is a substantial doubt of its being able to continue as a going concern. The accompanying condensed consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Cash and Cash Equivalents

The Company maintains its cash in bank accounts in Germany. Cash and cash equivalents include time deposits for which the Company has no requirements for compensating balances. The Company has not experienced any losses in its uninsured bank accounts.

Research and Development

Research and development costs are charged to operations as they are incurred. Legal fees and other direct costs incurred in obtaining and protecting patents are expensed as incurred.

Revenue Recognition

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606). The new revenue recognition standard provides a five-step analysis of transactions to determine when and how revenue is recognized. The core principle is that a company should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

8

SANGUI BIOTECH INTERNATIONAL, INC.

Notes to the Condensed Consolidated Financial Statements

December 31, 2019 and June 30, 2019

(Unaudited)

The Company recognizes revenue based on the five criteria for revenue recognition established under Topic 606: 1) identify the contract, 2) identify separate performance obligations, 3) determine the transaction price, 4) allocate the transaction price among the performance obligations, and 5) recognize revenue as the performance obligations are satisfied.

Type of Revenue

The Company derives revenue primarily from licensing fees on sales of its wound spray product.

The Company recognizes revenue based on the five criteria for revenue recognition established under Topic ASC 606 set forth below.

The Company’s licenses provide a right to use and create performance obligations satisfied at a point in time. The Company recognizes revenue from the license when the performance obligation is satisfied through the transfer of the license. The Company will recognize royalty revenue a) when the licensee makes the subsequent sales or use that trigger the royalty, or (b) the performance obligation to which some or all of the sales-based or usage-based royalties has been allocated has been satisfied.

Basic and Diluted Earnings (Loss) Per Common Share

Basic earnings (loss) per common share are computed by dividing income (loss) available to common stockholders by the weighted average number of common shares outstanding during the period of computation. Diluted earnings (loss) per share give effect to all potential dilutive common shares outstanding during the period of compensation. The computation of diluted earnings (loss) per share does not assume conversion, exercise or contingent exercise of securities that would have an antidilutive effect on earnings. As of December 31, 2019, the Company had no potentially dilutive securities that would affect the loss per share if they were to be dilutive.

Comprehensive Loss

Total comprehensive loss represents the net change in stockholders' equity (deficit) during a period from sources other than transactions with stockholders and as such, includes net earnings (loss). For the Company, the components of other comprehensive loss are limited to the changes in the cumulative foreign currency translation adjustments, which is recorded as components of stockholders' equity (deficit).

Recent Accounting Pronouncements

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842), ("ASC 842"). The objective of the guidance in ASC 842 is to increase transparency and comparability among organizations by recognizing lease assets and liabilities in the balance sheet and disclosing key information. ASC 842 amends previous lease guidance to require a lessee to recognize a lease liability and a right-of-use asset on the entity’s balance sheet for all leases with terms that exceed one year. ASC 842 is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years. ASC 842 provides that lessees (for capital and operating leases) and lessors (for sales-type, direct financing, and operating leases) must apply a modified retrospective transition approach for leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements. The modified retrospective approach would not require any transition accounting for leases that expired before the earliest comparative period presented. The Company elected a policy of not recording leases on its condensed balance sheets when the leases have term of 12 months or less and the Company is not reasonably certain to elect an option to purchase the leased asset. The Company recognizes payments on these leases within selling, administrative and other expenses on a straight-line basis over the lease term. The standard did not materially impact consolidated net income or liquidity.

9

SANGUI BIOTECH INTERNATIONAL, INC.

Notes to the Condensed Consolidated Financial Statements

December 31, 2019 and June 30, 2019

(Unaudited)

Management does not believe that any recently issued, but not yet effective, accounting standards if currently adopted would have a material effect on the accompanying consolidated financial statements.

NOTE 3 - COMMITMENTS AND CONTINGENCIES

Litigation

The Company may, from time to time, be involved in various legal disputes resulting from the ordinary course of operating its business. Management is currently not able to predict the outcome of any such cases. However, management believes that the amount of ultimate liability, if any, with respect to such actions will not have a

material effect on the Company's financial position or results of operations.

At the time of reporting, no litigations are pending.

Indemnities and Guarantees

During the normal course of business, the Company has made certain indemnities and guarantees under which it may be required to make payments in relation to certain transactions. These indemnities include certain agreements with the Company's officers, under which the Company may be required to indemnify such person for liabilities arising out of their employment relationship. The duration of these indemnities and guarantees varies and, in certain cases, is indefinite. The majority of these indemnities and guarantees do not provide for any limitation of the maximum potential future payments the Company could be obligated to make. Historically, the Company has not been obligated to make significant payments for these obligations and no liabilities have been recorded for these indemnities and guarantees in the accompanying consolidated balance sheet.

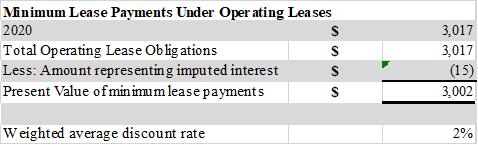

Leases

Effective from June 30, 2019 the Company has closed the site in Witten and relocated its headquarters to Hamburg. The Company leases office facilities from an unrelated third party at 685 Euros per month. The office lease contract is maintained on a month-to-month basis.

The Company also leases an automobile under an operating lease. The lease provides for a lease payment of 538 Euros per month beginning June 2018 expiring May 2020.

The following table reconciles future minimum operating lease payments to the discounted lease liability as of June 30, 2019:

License Agreement

Pursuant to the contracts dated May 2, 2018 and November 11, 2018 between Sangui GmbH respectively Sangui KG and a former contractor, Sangui KG grants that contractor a license fee on the license income received by

10

SANGUI BIOTECH INTERNATIONAL, INC.

Notes to the Condensed Consolidated Financial Statements

December 31, 2019 and June 30, 2019

(Unaudited)

Sangui for his previous services as a co-inventor. The license fee is 10% analogously to the remuneration regulation of the German Law on Employee Inventions (ArbnErfG).

NOTE 4 – DEBT

Notes Payable Related Parties

As of December 31, 2019, the Company had outstanding the following loans payable due to a Company Director:

On September 17, 209, on October 04, 2019 and on October 30, 2019 a Company Director advanced amount of 20,000 Euros ($22,432 as of December 31, 2019) each to the Company. The loans are due on demand, accrue interest annually at 2% and are unsecured. As of December 31, 2019, the notes have total interest accrued of $313.

NOTE 5 – CAPITAL STOCK

Preferred Stock – The Company is authorized to issue 10,000,000 shares of preferred stock. No preferred stock has been issued to date. The authorized preferred shares are non-voting and the Board of Directors has not designated any liquidation value or dividend rates.

Common Stock – The Company is authorized to issue 250,000,000 shares of no - par value common stock. The holders of the Company's common stock are entitled to one vote for each share held of record on all matters to be voted on by those stockholders. As of December 31, 2019, and June 30, 2019, the Company had 201,533,598 shares and 199,295,503 shares of common stock issued and 201,479,842 and 199,241,747 shares outstanding, respectively.

During the six months ended December 31, 2019, the Company issued 2,238,095 shares of common stock to one individual for obtaining aa settlement in a patent matter at $44,762 ($0.0200 per share). The company recorded an accrual in the amount of $38,048 in the annual financial statements ended June 30, 2019. An additional loss of $6,714 was recorded during the six months ended December 31, 2019.

11

SANGUI BIOTECH INTERNATIONAL, INC.

Notes to the Condensed Consolidated Financial Statements

December 31, 2019 and June 30, 2019

(Unaudited)

Treasury Stock - The Company holds 53,756 of its common stock as treasury stock, which is valued at cost of $19,387 at December 31, 2019.

Stock – Based Compensation - On October 22, 2008 the Company adopted the 2008 Amended and Restated Long-Term Equity Incentive Plan, whereby the Board was authorized to issue up to 10,000,000 shares of common stock (including incentive stock options) to certain eligible employees, directors, and consultants of the Company or its subsidiaries. The term of the plan was 10 years. It expired in October 2018.

NOTE 6 – SUBSEQUENT EVENTS

Subsequent to December 31, 2019, a Company Director advanced 10,000 Euros ($11,216) to the Company. The loans are due on demand, accrues interest annually at 2% and are unsecured.

Subsequent to December 31, 2019, the Company sold 1,250,000 shares of its common stock for approximately $11,055 in cash proceeds to one individual at price of approximately $ 0.009 per share.

In accordance with ASC 855-10, the Company’s management has reviewed all material events and there are no additional material subsequent events to report.

12

Item 2 - Management's Discussion and Analysis of Financial Condition and Results of Operations

Forward-looking Statements

The following discussion of our financial condition and results of operations should be read in conjunction with the consolidated financial statements and the related notes thereto included elsewhere in this quarterly report. Some of the information in this quarterly report contains forward-looking statements, including statements related to anticipated operating results, margins, growth, financial resources, capital requirements, adequacy of the Company's financial resources, trends in spending on research and development, the development of new markets, the development, regulatory approval, manufacture, distribution, and commercial acceptance of new products, and future product development efforts. Investors are cautioned that forward-looking statements involve risks and uncertainties, which may affect our business and prospects, including but not limited to, the Company's expected need for additional funding and the uncertainty of receiving the additional funding, changes in economic and market conditions, acceptance of our products by the health care and reimbursement communities, new development of competitive products and treatments, administrative and regulatory approval and related considerations, health care legislation and regulation, and other factors discussed in our filings with the Securities and Exchange Commission.

GENERAL

Our mission is the development of novel and proprietary pharmaceutical, medical and cosmetic products. We develop our products through our German subsidiary, Sangui GmbH. Currently, we are seeking to market and sell our products through partnerships with industry partners worldwide.

Our focus has been the development of oxygen carriers capable of providing oxygen transport in humans in the event of acute and/or chronic lack of oxygen due to arterial occlusion, anemia or blood loss whether due to surgery, trauma, or other causes, as well as in the case of chronic wounds. We have thus far focused our development and commercialization efforts on such artificial oxygen carriers by reproducing and synthesizing polymers out of native hemoglobin of defined molecular sizes. In addition, we have developed external applications of oxygen transporters in the medical and cosmetic fields in the form of sprays for the healing of chronic wounds and of gels and emulsions for the regeneration of the skin. A wound dressing that shows outstanding properties in the support of wound healing, is being distributed by SastoMed GmbH (Sastomed), a former joint venture company in which we had held a share of 25%, as global licensee under the Granulox brand name. Effective as of the end of the second quarter of our fiscal year 2016 we sold this stake to SanderStrohmann GmbH.

Sangui GmbH holds distribution rights for our Chitoskin wound pads for the European Union and various other countries. Additionally, a European patent has been granted for the production and use of improved Chitoskin wound pads.

Our current key business focuses are: (a) selling our existing cosmetics and wound management products by way of licensing through distribution partners, or by way of direct sale, to end users; (b) identifying additional industrial and distribution partners for our patents, production techniques, and products; and, (c) obtaining the additional certifications on our products in development.

Artificial Oxygen Carriers

Sangui GmbH develops several products based on polymers of purified natural porcine hemoglobin with oxygen carrying abilities that are similar to native hemoglobin. These are (1) oxygen carrying blood additives and (2) oxygen carrying blood volume substitutes.

According to regulatory requirements, all drugs must complete preclinical and clinical trials before approval (e.g. Federal Drug Administration approval) and market launch. The Company’s management believes that the European and FDA approval process will take at a minimum several years to complete.

Our most promising potential product in the area of artificial oxygen carriers, the blood additive, is still in an early development stage. In the pursuit of these projects we will need to obtain substantial additional capital to continue their development. As the Company has limited financial resources, we have suspended this project temporarily in order to focus our attention on our chronic wound research and the products developed in conjunction with their treatment.

13

Nano Formulations for the Regeneration of the Skin

Healthy skin is supplied with oxygen both from the inside as well as through diffusion from the outside. A lack of oxygen will cause degenerative alterations, ranging from premature aging, to surface damage, and even as extensive as causing open wounds. The cause for the lack of oxygen may be a part of the normal aging process, but it may also be caused by burns, radiation, trauma, or a medical condition. Impairment of the blood flow, for example caused by diabetes mellitus or by chronic venous insufficiency, can also lead to insufficient oxygen supply and the resulting skin damage.

In response, we developed nano-emulsion based cosmetic preparations that in their design are able to help support regeneration of the skin by improving its oxygen supply. Our line of cosmetic products was thoroughly tested by an independent research institute and received top marks for skin moisturizing, and enhanced skin elasticity, respectively. However, sales of this series have remained at a low level and during the first quarter of the 2016 financial year we decided to decrease our operations in this particular segment and to abandon the patent protection for this range of products.

Chitoskin Wound Pads

Usually, normal (“primary”) wounds tend to heal over a couple of days without leaving scars following a certain sequence of phases. Burns and certain diseases impede the normal wound healing process, resulting in large, hardly healing (“secondary”) wounds which only close by growing new tissue from the bottom. Wound dressings serve to safeguard the wound with its highly sensitive new granulation tissue from mechanical damage as well as from infection. Using the natural polymer chitosan, Sangui’s Chitoskin wound dressings show outstanding properties in supporting wound healing. Sangui GmbH holds various distribution rights for our Chitoskin wound pads, and it is the strategy of the company to find industry partners ready to acquire or license this product range as a whole.

Hemospray Wound Spray

Sangui GmbH has developed a novel medical technology supporting the healing of chronic wounds. Lack of oxygen supply to the cells in the wound ground is the main reason why those wounds lose their genuine healing power. Based on its concept of artificial oxygen carriers, the wound spray product we developed bridges the watery wound surface and permits an enhanced afflux of oxygen to the wound ground.

Sangui GmbH has granted SastoMed global distribution rights to this product. Distribution of the wound spray began in the European Union in April 2012 under the brand name “Granulox.”

In December 2012, product distribution was initiated in Mexico by Sastomed and their local distribution partner Bio-Mac Pharma. International distribution has been expanded since then through cooperation agreements with local distribution partners in the Benelux countries and South Eastern Europe.

Since December 2013, international distribution outside Germany in collaboration with local partners has occurred in more than 40 countries in Europe and Latin American.

On November 13, 2017, the Company announced that Infirst Healthcare Ltd has announced that the United States (US) Food and Drug Administration had granted Fast Track designation to Granulox for the treatment of diabetic foot ulcers. It is the first and only hemoglobin spray to receive the Fast Track designation - a process designed to facilitate the development, and expedite the review of, new therapies to treat serious conditions and fill an unmet medical need.

Despite the positive reviews of our product, Granulox sales have become more volatile. We remain confident, however, that SastoMed will be able to considerably increase its sales along with more international markets entering actual distribution of the product.

In December 2010, Sangui GmbH established a joint venture company with SanderStrothmann GmbH of Georgsmarienhuette, Germany, under the name of SastoMed GmbH. This enterprise was in charge of obtaining the

14

CE mark certification authorizing the distribution of one of SGBI’s products in the member states of the European Union. Effective December 31, 2015, Sangui GmbH sold its stake in Sastomed GmbH to SanderStrohmann GmbH.

On or about June 18, 2018, Sangui GmbH together with Sastomed GmbH founded Sangui Know-How- und Patentverwertungsgesellschaft mbH & Co. KG (“Sangui KG”). Sangui KG is a limited partnership. On June 22, 2018, Sangui KG acquired all the rights in the license agreement made on December 17, 2010, between Sastomed GmbH and Sangui GmbH.

Pursuant to the contracts dated May 2, 2018 and November 11, 2018 between Sangui GmbH respectively Sangui KG and a former contractor Sangui KG grants that contractor a license fee on the license income received by Sangui for his previous services as a co-inventor. The license fee is 10% analogously to the remuneration regulation of the German Law on Employee Inventions (ArbnErfG).

Given the Company’s business strength is primarily in research and product development, we have decided to partner with established distribution entities who license our marketable products, or those products that are close to market entry, for sale to end users. In pursuit of this strategy we have licensed the most promising product, a hemoglobin based wound spray technology to Sastomed GmbH, a former joint venture of SGBI, for distribution in several European, Latin American and Asian countries. In addition, we are entering the preclinical testing of hemoglobin based artificial oxygen carriers aiming at the remediation of ischemic conditions in human patients.

FINANCIAL POSITION

During the six months ended December 31, 2019, our total assets decreased $22,981 from $78,971 at June 30, 2019 to $55,990 at December 31, 2019. A decrease of accounts receivables and a decrease of cash from June 30, 2019 to December 31, 2019, of $15,017 and $12,058 respectively were primarily responsible for the decrease in the total assets.

We funded our operations primarily through our existing cash reserves and cash received from the issuance of shares of common stock and notes payables from related parties. Our stockholders’ equity (deficit) increased by $53,599 from ($591,989) at June 30, 2019 to ($645,588) at December 31, 2019. The primary factor behind this was net loss attributable to common stockholders of $96,732 offset by the issuance of stock, valued at $44,762 in connection to the out-of-court settlement.

RESULTS OF OPERATIONS

For the three-month and six-month period December 31, 2019 and 2018:

REVENUES – Revenues reported were $11,683and $44,095 for the three months ended December 31, 2019 and 2018 respectively. For the six months ended December 31, 2019 and 2018 revenues were $11,965 and $55,367. Revenues decreased by $32,412 for the three months ended December 31, 2019 and 2018 and decreased by $43,402 for the six months ended December 31, 2019 and 2018. The decrease of $32,412 and $43,402 respectively can be traced back to a decrease in royalties from the licensing agreement with SastoMed. Cost of sales were $0 and $99 for the six months ended December 31, 2019 and 2018 respectively.

RESEARCH AND DEVELOPMENT – Research and development expenses decreased by $4,664 to $2,650 from $7,314 for the three-month periods ending December 31, 2019 and 2018. Research and development expenses decreased $10,400 to $4,886 in the first half-year of our 2020 financial year from $15,286 in the comparable period of the previous year. This decrease is mainly attributed to lower fees for patents.

GENERAL AND ADMINISTRATIVE and PROFESSIONAL FEES –The combined accumulated general and administrative expenses and professional fees decreased $51,326 to $ 45,567 in the three months ended December 31, 2019, from $96,892 in the respective period of the previous year. Accumulated general and administrative expenses and professional fees decreased $94,107 to $99,510 in the half-year ended December 31,

15

2019, from $193,617 in the respective period of the previous year mainly due to lower personnel costs, lower rental expenses and lower professional fees.

INTEREST EXPENSE - interest expenses for the three-month period ended December 31, 2019 and 2018 were $3,477 and $2,525, an increase of $952. For the six months ended December 31, 2019 and 2018, interest expense increased by $474 to $6,690 from $6,216. The increase relates to the increase of interest - bearing debt financing.

NET LOSS - As a result of the above factors, the net loss attributed to common shareholders decreased to $53,983 compared to a loss of $56,356 for the three months ended December 31, 2019 and 2018 respectively and a loss of $96,732 compared to a loss of $146,319 for the six month ended December 31, 2019 and 2018 respectively. The loss per share for both periods was $(0.00).

Our consolidated net loss before non-controlling interest was $55,121, or $(0.00) per common share, for the three months ended December 31, 2019, compared to $58,480 or $(0.00) per common share, during the comparable period in our 2019 financial year. Our consolidated net loss before non-controlling interest was $99,126 or $(0.00) per common share, for the six months ended December 31, 2019, compared to $154,607 or $(0.00) per common share, during the comparable period in our 2019 financial year.

LIQUIDITY AND CAPITAL RESOURCES

For the six months ended December 31, 2019, net cash used in operating activities decreases $66,327 to $(78,876), compared to $(145,203) in the corresponding period of the previous year. This is mainly due to a decrease of the operating loss of approximately $55,481 from a loss of $(154,607) in 2018 to a loss of $(99,126) in 2019.

The Company funded its business in the first six months ended December 31, 2019 by issuing note payables totaling 60,000Euros ($ 66,606).

We had a working capital deficit of approximately $648,590 at December 31, 2019, an increase of approximately $56,601from June 30, 2018.

At December 31, 2019 compared to June 30, 2018, we had cash of $15,395 compared to $27,453, prepaid expenses of $16,583 compared to $9,470 and accounts receivable of $14,508 compared $29,525. We will need substantial additional funding to fulfill our business plan and we intend to explore financing sources for our future development activities. No assurance can be given that these efforts will be successful.

Item 3 - Quantitative and Qualitative Disclosures about Market Risk

We are a smaller reporting company as defined by §229.10(f)(1) and are not required to provide the information under this item.

Item 4 - Controls and Procedures

Disclosure Controls and Procedures

As of the date of the end of the period covered by this report, our Chief Executive Officer and Chief Financial Officer conducted an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures, as required by Exchange Act Rule 13a-15. Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were not effective as of the end of the period covered by this report to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified by the SEC’s rules and forms.

Disclosure controls and procedures are controls and other procedures that are designed to ensure that

16

information required to be disclosed in our reports filed or submitted under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed in our reports filed under the Exchange Act is accumulated and communicated to management, including our Chief Executive Officer and our Chief Financial Officer, to allow timely decisions regarding required disclosure.

Changes in Internal Control Over Financial Reporting

There has been no change in our internal control over financial reporting that occurred during our last fiscal quarter that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

The term “internal control over financial reporting” is defined as a process designed by, or under the supervision of, the registrant’s principal executive and principal financial officers, or persons performing similar functions, and effected by the registrant’s board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles and includes those policies and procedures that:

(a)Pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of the registrant;

(b)Provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the registrant are being made only in accordance with authorizations of management and directors of the registrant; and

(c)Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the registrant’s assets that could have a material effect on the financial statements.

PART II - OTHER INFORMATION

The Company is not aware of pending claims or assessments, which may have a material adverse impact on the Company’s financial position or results of operations.

Item 1a - Risk Factors

We are a smaller reporting company as defined by §229,10(f)(1) and are not required to provide the information under this item.

Item 2 - Unregistered Sales of Equity Securities and Use Of Proceeds

None

Item 3 - Defaults Upon Senior Securities

None.

None.

17

1. Financial Statements. The unaudited condensed consolidated Balance Sheet of Sangui Biotech International, Inc. as of December 31, 2019 and the audited balance sheet as of June 30, 2019, the unaudited condensed consolidated Statements of Operations for the three and six - month periods ended December 31, 2019 and 2018, the condensed unaudited Statements of Stockholder’s Equity (Deficit) as of December 31. 2019 and 2018, and the unaudited condensed consolidated Statements of Cash Flows for the six-month period ended December 31, 2019 and 2018, together with the notes thereto, are included in this Quarterly Report on Form 10-Q.

2. Exhibits. The following exhibits are either filed as a part hereof or are incorporated by reference. Exhibit numbers correspond to the numbering system in Item 601 of Regulation S-K.

Exhibit

Number Description of Exhibit

31.01 | Certification of CEO Pursuant to Rule 13a-14(a) and 15d-14(a), filed herewith |

31.02 | Certification of principal financial officer Pursuant to Rule 13a-14(a) and 15d-14(a), filed herewith |

32.01 | Certification Pursuant to Section 1350 of Title 18 of the United States Code, filed herewith |

|

|

Pursuant to the requirements of the Securities Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

SANGUI BIOTECH INTERNATIONAL, INC.

Dated: February 13, 2020/s/ Thomas Striepe

By: Thomas Striepe

Chief Executive Officer

18